2012 - pma · 4-7 government debt structure, 2008-2012 28 4-8 government debt as a percent of gdp,...

TRANSCRIPT

Financial Stability Assessment

2012FINANCIAL STABILITY REPORT

Research and Monetary Policy Department

September, 2013

Financial Stability Assessment

Financial Stability Assessment

© September, 2013All Rights Reserved.

In the case of quotation, please refer to this publication as follows:Palestine Monetary Authority (PMA), 2013. Finanical Stabilty Report 2012: September Ramallah – Palestine

All Correspondence shall be directed to:Palestine Monetary Authority (PMA)P. O. Box 452, Ramallah, Palestine

Tel.: (+ 970) 2-2409920Fax: (+ 970) 2-2409922E-mail: [email protected] Page : www.pma.ps

III

ForewordFinancial stability alongside monetary stability has acquired increased attention after becoming the primary target of a number of central banks. The great emphasis central banks and international financial institutions have given to financial stability reflects the state of the financial sector and its ability to cope with risks, and carry out its functions of supporting economic growth and realizing sustainable development efficiently and effectively.

Given that the banking sector is the backbone of the Palestinian financial system, it is the most vulnerable to risks, especially since other non-banking financial institutions are still in the developmental and founding stages. However, some of these institutions have witnessed significant progress, particularly in the stock market and the field of insurance.

The Palestine Monetary Authority (PMA) views financial stability as the state which allows smooth flowing of funds between households, firms, and the government and between residents and the rest of the world. This requires the operation of sound financial intermediaries and well-functioning financial markets on the one hand. On the other hand, financial stability requires that financial corporation’s be resilient to adverse macroeconomic shocks, to credit risk, to liquidity shocks and to contagion risk. It also requires sufficient liquidity, and a good measure of confidence in the operation of the financial markets.

As such, financial instability can manifest itself through bank failures, excessive leverage and credit growth either in the aggregate or in some sectors or debtor categories , poor quality of debt and loans, asset price bubbles, drying up of liquidity, and fading confidence in the financial system.

The PMA’s mission is to ensure the maintenance of price stability and to contribute to financial stability both in the interest of balanced and sustainable economic growth. The PMA’s analysis of financial stability and the publication of a Financial Stability Report (FSR) is directly connected to its mandate as the sole institution that is authorized to oversee the payment service providers and the safety and efficacy of the payment systems to ensure financial stability.

The FSR describes the PMA’s assessment of the risks and potential threats to the financial intermediaries and to the financial system and evaluates the system’s resilience in the face of these risks and threats. By publishing this report, the PMA wishes to communicate the results of its assessments and stimulate debate on the pertinent issues. In these reports and on the basis of its assessments, the PMA makes recommendations to enhance financial stability and, whenever necessary, to avoid and overcome potential risks and threats.

GovernorDr. Jihad Khalil Alwazir

IV

Contents

Chapter one: Financial Stability Assessment

1Overview

11- Underlying risks in the Palestinian financial system

22- Risks facing the banking sector

43- risks linked with non-banking financial institutions

44- Infrastructure development of the financial system

Chapter Two: Global and Local Economic Developments

5Overview

51- Global economy

62- Israeli economy

73- Jordanian economy

74- Local economy

Chapter Three: Infrastructure and Development Indicators in The Financial System

13Overview

131- Legal and regulatory framework

142- Developments and updates of the banking system

163- Development indicators in the financial system

Chapter Four: Credit Risks in The Banking Sector

21Overview

211- Risks associated with credits granted to public and private sectors

222- Risks associated with credits granted to households and corporate sector

233- Risks associated with credits granted according to residency

244- Risks associated with credits granted to mortgage and housing

255- Risks associated with NPLs

266- Risks associated with public finance

Contents

V

Contents

Chapter Five: Financial Soundness Indicators of The Banking Sector

31Overview

311- Capital indicators

332- Asset quality indicators

343- Profitability indicators

354- Liquidity Indicators

Chapter Six: Development In Non-Banking Financial Institutions

37Overview

371- Money changers

382- Specialized lending Institutions

383- Securities sector

394- Insurance sector

415- Mortgage sector

426- Financial leasing sector

Chapter Seven: Financial Pressure “Stress Testing”: A Future Outlook

43Overview

431- Macroeconomic stress testing

452- Interbanking stress testing

Tables17Financial services developments, 2008-20123-1

18Number of accounts and values in banks operating in Palestine, 2008-20123-2

22Sectoral distribution of credit according to banks nationality, 2008-2012 4-1

22Credit distribution according to bank nationality, 2008-20124-2

23Credit distribution according to residency and bank nationality, 2008-20124-3

24Housing and mortgage credit portfolio according to bank nationality, 2008-20124-4

36Soundness indicators of banks operating in Palestine, 2008-2012 5-1

37Money changers in Palestine, 2010-20116-1

39Financial operational indicators of insurance companies, 20126-2

41Performing indicators for mortgage sector, 2008-20126-3

44 Change in provisions forecasts according to different scenarios7-1

45Capital adequacy ratio for banks operating in Palestine after the shock, 20127-2

VI

Contents

Figures

6Bank of Israel interest rate (monthly), 20122-1

8Real GDP growth rate in Palestine comparing with other regions, 2008-20122-2

8USD exchange rate fluctuations against NIS (annual, period average), 2008-20122-3

8USD/NIS exchange margins (period average), 2008-20122-4

9Total deposits at banks operating in Palestine by currency, 2008-20122-5

9Credit portfolio by currency, 2008-20122-6

9Deposit and lending rates in Palestine by currency, 2008-20122-7

16Branches of banks operation in Palestine, 2008-20123-1

16Herfindahl index, 2008-20123-2

19Credits as a percent of GDP in Palestine and some neighboring countries, 2008-20123-3

19Private sector credits as a percent of total credits in Palestine and some neighboring countries, 2008-2012

3-4

19Private sector deposits as a percent of customer deposits in Palestine and some neighboring countries, 2008-2012

3-5

20Credit to deposit ratio in Palestine and some neighboring countries, 2008-20123-6

20PEX market capitalization as a percent of GDP in Palestine and some neighboring countries,2008-2012

3-7

21Distribution of credit portfolio between private and public sector, 2008-20124-1

25NPLs structure in local banks, 2008-20124-2

26NPLs structure in foreign banks, 2008-20124-3

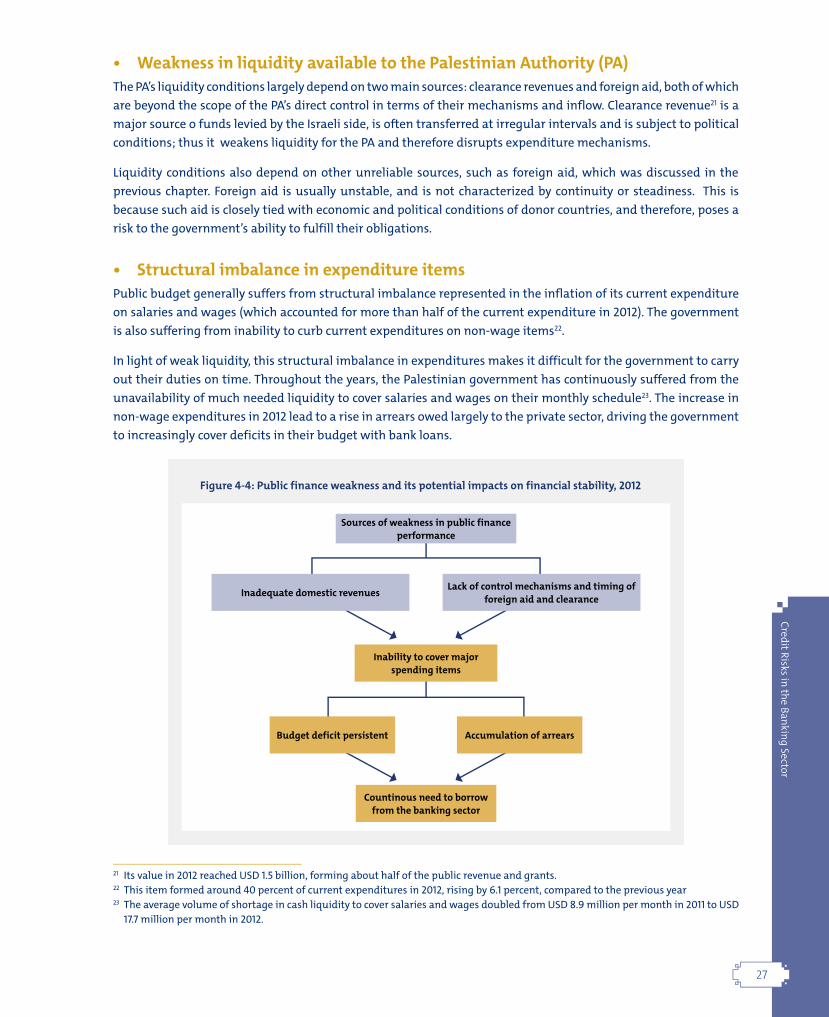

27Public finance weakness and its potential impacts on financial stability, 20124-4

28Government revenue structure, 2008-20124-5

28Government revenue as a percent of current expenditures, 2008-20124-6

28Government debt structure, 2008-20124-7

29Government debt as a percent of GDP, 2008-20124-8

32Capital adequacy ratio, 2008-20125-1

32(NPLs-provisions) as a percent of core capital, 2008-20125-2

VII

Contents

33Core capital as a percent of total assets, 2008-20125-3

33Large-expousures as a percent of core capital, 2008-20125-4

34NPLs as a percent of total credits, 2008-20125-5

34Total credits as a percent of total assets, 2008-20125-6

35Return on average assets (ROAA), 2008-20125-7

35Return on average core capital, 2008-20125-8

35Liquid assets as a percent of total assets, 2008-20125-9

36Liquid assets as a percent of short-term liabilities, 2008-20125-10

40Linkages between insurance and banking sector, 2008-20126-1

42Housing and mortgage loans, 20126-2

42NPLs according to subsectors, 2011-20126-3

45Capital adequacy ratio for banks operating in Palestine before and after the shock, 20127-2

10Arab safety net and the shortage of liquidity in Palestine1

15Foreign account tax compliance act (FATCA)2

Boxes

1

Financial Stability Assessment1. Underlying risks to the Palestinian Financial System

The analysis of risks to which the Palestinian financial system may be vulnerable requires first the identification of the institutions in this system. It also calls for the analysis of relations and channels of impact transmission between institutions (banking and non-banking) in order to determine the substantial risk pits, and potential financial contagion between the institutions embraced by the Palestinian financial system. This would ensure clarity of vision for those in charge of managing and controlling the system, and would assist them in making policy, and in taking suitable measures to face risks and their possible consequences. Analysis shows the conditions of financial stability in Palestine to be sensitive to three main sources of risks.

Chapter One Financial Stability Assessment

Overview

The risks which the Palestinian financial system with all its banking and non-banking institutions faces emanate from several sources. Perhaps the most prominent and dangerous of these are found in the continued Israeli occupation, and the dependency of the Palestinian economy on the Israeli counterpart, the internal political schism, and the consequent adverse repercussions felt in all other areas. Other underlying risks to the financial system reflect the financial difficulties that the government faces, and the risks arising from structural problems caused by the failure to complete the legislative framework and governance measures for non-banking financial institutions. Legal challenges associated with compliance with the American tax law “The Foreign Account Tax Compliance Act-FATCA”, are also a source of concern. In addition, there are dangers which may be transmitted to the Palestinian financial system from neighboring countries, especially those which suffer from a lack of political and economic stability, and other risks that may pose a threat to financial stability.

In spite of these risks, financial soundness indicators for 2012 reflected the ability of banking system to withstand risks, supported by the continued development in infrastructure, which include laws, regulations and procedures governing the operations of these entities.

2

Financial Stability Assessment

First: the continued Israeli occupation and control of crossings, hampering communication between Palestinian cities and their isolation, and the Palestinian economy’s forced reliance on the Israeli economy. Palestine is therefore greatly affected by the dependency on, and the effects of Israeli economic and monetary policies. This is especially so considering the country’s monetary dependency and the use of the Israeli Shekel (NIS) as the most widely circulated currency within Palestine. Although essentially external, this risk needs to be dealt with as an inevitable reality; this requires specially adaptive policy in order to withstand possible consequences. These consequences are not limited to the Palestinian financial system, but in fact extend to all aspects of Palestinian life whether economic, social, political or security-related.

Second: the Palestinian government’s increasing dependency on the banking system to finance budget deficits due to the lack of other alternatives and financial instruments available to the government, such as bonds and bills. This increase coincides with the vast decline in the amount of foreign aid and occasional delays in clearance revenue transfers from Israeli authorities. Obviously, the funds derived from both sources are not subject to the direct control of the Palestinian government, but rather to political and economic developments, adding a sense of irregularity and vulnerability to government revenues. These sources (foreign aid and clearance revenues) are considered as the main channels of risks which the Palestinian banking system may be exposed to.

Third: the continued internal political schism and the subsequent multiplicity and in some cases conflicts of policies, laws and decisions, especially those related to the economy. This may cause significant distortions and abnormalities in the structure of the economy in general, and the financial system in particular. The situation is aggravated by the fact that some banks in Gaza were licensed and opened without the supervision of the PMA, the only legal body authorized to license and supervise banks, foreign exchange companies and specialized lending institutions. In addition, some financial companies and institutions in the field of insurance were opened without obtaining the required licenses from the Palestine Capital Market Authority (PCMA). This unhealthy work environment helped the informal sector to prosper, and consequently undermined the safety of the Palestinian economy in general and the financial sector in particular. The essential step to face these risks is only the quick completion of the reconciliation process. If there are any delays in this process, it will only deepen the problems from which the Palestinian economy already suffers.

2. Risks facing the Banking SystemAnalysis of the risks and developments which the banking sector witnessed in 2012 reveal that the substantial risk which this system faces is not in its systems and internal management as much as in its exposure to the financial crisis of the government. There are three implications of this risk:

i. The first is the substantial increase in government’s recourse to borrowing from banks, most notably as a result of the decrease in foreign aid, and the continous deficit in the overall budget’s balance, especially in recent years. The outstanding debt owed to banks by the Palestinian government reached around US Dollars (USD) 1.4 billion (around 55.8 percent of the government’s public debt) at the end of 2012, in comparison to the USD 0.5 billion in 2008.

ii. Second is the mounting credit facilities granted to public sector employees and the risk of default. This may be manifested in either the inability of the government to pay the wages or irregularity in these payments.

iii. Third are the facilities extended by banks to private sector institutions that deal with the government and the occasional inability of government to repay their dues to these institutions, which leads to the default of these institutions to repay their debts to the banks.

The potential risks and fears in public finance stem from the inveterate dependency on foreign aid, which formed around 29.5 percent of revenues and grants in the year 2012. It is a known fact that this aid is linked with

3

Financial Stability Assessment

economic and political conditions that prevail in donor countries or in Palestine. As a consequence, such source is not characterized by continuity and consistency, but rather fluctuates greatly, creating a source of risk to the government’s ability to meet its obligations. This is in addition to the fact that foreign aid received by the Palestine Authority (PA) is in currencies other than the main currency of expenditure (NIS), subjecting proceeds to further fluctuations due to changes in exchange rates. Such conditions prompted the Palestinian government to depend increasingly on banks operating in Palestine in order to finance public spending.

The continued recourse of the government to borrowing from the banking sector has led to a state of uncertainty in fiscal sustainability on the one hand, and crowding out the private sector from obtaining financing, on the other. This situation may lead to the incapacity of the private sector to support growth as a result of insufficient funding or a rise in costs. It is worth mentioning that the ratio of credit extended to the government has increased from about 29.1 percent in 2008 to 33.5 percent of total credit granted in 2012.

As for the performance of the banking system, the financial soundness indicators reflected a good measure of stability, and the capacity to endure risks. The capital adequacy ratio for all banks operating in Palestine reached 20.3 percent at the end of 2012, in comparison to 21.1 percent in the previous year. Likewise, non-performing loans (NPLs) minus provisions relative to capital increased from 3.8 percent in the year 2011, to 4.9 percent in 2012. This may have affected capital’s ability to face the most prominent banking risks i.e., credit default. Even though NPLs increased to 3.1 percent of total loans, in comparison to 2.8 percent in 2011, this ratio remains generally low in comparison to those in other countries, and it does not pose a serious threat to financial stability.

With regard to profitability indicators, the Return on Average Assets (ROAA) remained almost stable in 2012 at 1.8 percent in comparison to 1.9 percent in the previous year. Furthermore, the Return on Core Capital fell to 16.3 percent in 2012, compared to 17 percent in 2011. As for liquidity, the liquid assets to short-terms liabilities was 49.3 percent in 2012 as opposed to 49 percent in the previous year.

Financial depth indicators have also improved as credit facilities increased to 40.2 percent of GDP in 2012, while it was 35 percent in the previous year. However, this ratio seems low compared to neighboring countries, reflecting a relative weakness in the strength of interaction between the banking system and real economic sectors. It is noteworthy that the PMA aims to increase domestic credit and strengthen relations between the banking sector and the real economy by reducing the level of banks’ placements abroad .

The previous indicators mirror the extent of progress and improvement made in the financial intermediation process in Palestine, whereby the ratio of loans to customer deposits increased from 50.9 percent in 2011 to 56.1 percent in 2012. This ratio is moderate compared to neighboring countries, where it was 71.4 percent in Jordan, 49.5 percent in Egypt and 54 percent in Lebanon in 2012.

On another side, and in the framework of enhancing and deepening the analysis of risks which banks operating in Palestine may be exposed to, the PMA conducted financial stress tests under specific scenarios. Two tests were completed: the first measures the flexibility of banks operating in the Palestinian economy to withstand adverse shocks on the macroeconomic level. Loan provisions were used as a measure of financial default. A number of variables were chosen on the macro-economic level in order to measure its effects on these provisions, such as: growth rate, inflation rate, interest rate on loans and deposits on currencies circulated in the Palestinian economy, and the exchange rates of the U.S dollar and the JD against the IsraeliNIS.

The tests were carried out according to two scenarios: the baseline scenario and the pessimistic scenario. The results showed that according to the baseline scenario, the net loan provisions will increase by about USD 1.7 million in 2013. On the contrary, according to the pessimistic scenario, these will plunge by USD 9.2 million in the same time frame. The second test examines the resilience of banks to the collapse of any one of the banks operating in Palestine. The results illustrated bank immunity in terms of capital adequacy and the limited contagion effects on the rest of the

4

Financial Stability Assessment

banks in the hypothetical event of one of them failing.

3. Risks linked with Non-banking Financial InstitutionsRisk analysis results in regard to other non-banking financial institutions, specially the specialized lending institutions, revealed that these institutions do not pose a substantial risk to the stability of the Palestinian financial system due to the small size of their operations compared to banks. Loans granted by specialized lending institutions did not exceed 2.5 percent of the loans offered by the banks, and did not exceed 1 percent of GDP. Accordingly, the limited relationship of these institutions with banks reduces the possibility of risk transmission. In spite of this, there are some risks inherent in these institutions which are found in weak governance practices-a result of multiplicity in the legal form of these institutions, the nature of their work, the financial and administrative systems inherited from many years and the subjugation to more than one regulatory and supervision authority. It should be noted that the PMA has begun to address the causes of weak governance in these institutions and have also begun developing their systems and consolidating their conditions especially since the licensing and supervision of specialized lending institutions system was issued in 2011.

With regards to Palestine Exchange (PEX), and with the aim to increase efficiency of the financial market, toughen governance and transparency, and increase PEX’s investment attractiveness both domestically and internationally, the listing system in the stock exchange was adjusted and divided into two markets. Based on certain conditions, large companies were listed in the first market and relatively small companies were listed in the second market. In the same context, a joint cooperation agreement was signed between the PMA and the Palestine Securities Exchange (PEX) to implement cash settlement procedures for trade transactions in the stock market, using the PMA’s BURAQ system. This agreement may reduce risks in the settlement of trade transactions.

With regards to the insurance sector, the analysis results of the channels transmission of effect between the insurance sector and the banking sector shows that the degree of risk that the banking sector poses to the insurance sector is clearly larger than the banking sector’s exposure to risks arising in the insurance sector. Deposits of insurance companies in banks formed about 14.5 percent of total assets of these companies and 27 percent of their total investments at the end of 2012, while these deposits accounted for only 0.6 percent of total deposits in the banking sector. This is to be expected, especially since the banking sector still carries the largest weight in the financial system in comparison to other financial institutions, which are still in a developing stage.

4. Infrastructure Development of the Financial SystemThe previous risk analyses show the importance of strengthening the financial system’s infrastructure (including legal and supervisory systems and frameworks) as it is the main requisite to achieve financial stability. In this regard, both the PCMA and the PMA persevered to achieve a number of accomplishments in 2012. The PMA issued the “National Payments System”, which demonstrates the importance of using electronic payment systems. The PMA also obtained membership in the International Association of Deposit Insurers (IADA) for its efforts to establish a deposit insurance corporation, which is an essential component of the financial safety net in Palestine. The PCMA Board of Directors also approved the mortgage draft law, in order to facilitate its approval and ratification by the Council of Ministers.

It is noteworthy that the emergence of legal and supervisory challenges facing banks in Palestine could mean the emergence of new risks that may affect the degree of financial stability. One challenge is posed by the new U.S tax bill, FATCA, under which the disclosure of financial account details of individuals possessing U.S citizenships and their subsequent submission to the Internal Revenue Service (IRS), are incumbent upon all financial institutions operating out of the USA (including banks operating in Palestine). Sanctions will be applied to non-cooperating banks by a 30 percent discount from the offending bank accounts in U.S banks. This means that non-cooperative banks will be exposed to both operational and reputational risks. Work is still underway to determine which options are most suitable to comply with this law; consultations as well as internal and regional communications with Arab financial institutions, such as the Union of Arab Banks and the Arab Monetary Fund, are being conducted.

55

Local and International Economic D

evelopments

Chapter Two Local and International Economic Developments

Overview

A range of financial and economic conditions in neighboring countries, in addition to some international financial and economic developments, play a crucial role in influencing the degree of stability in the Palestinian financial sector. Palestine’s forced economic reliance upon the Israeli economy, for example, poses a number of risks that include mainly the Israeli control of clearance revenue which is one of the main pillars of the Palestinian budget, along with the impact generated by fluctuations versus other currencies in the exchange rate of the NIS, the main currency circulating in the Palestinian economy.

Risks from the international environment are associated mainly with foreign aid, which is the other major pillar of the Palestinian economy in general, and the government’s budget in particular. The fluctuations in the value and regularity of such aid constitute one source of instability in the Palestinian financial sector. In addition, the Palestinian external sector (balance of payments) suffers from a structural imbalance due to structural imbalances in the economy, reflecting mainly high imports and a weak export base, exacerbating the current account deficit.

1. Global Economy In 2012, global economic developments indicate a relative improvement on the previous year. This improvement was visible in the mitigation of the financial crises in the euro-area as a direct result of pledges made by countries in the region, and reduced uncertainty due to financial safety nets1. This is to be added to aid contribution by some international institutions such as the International Monetary Fund (IMF), to countries such as Greece, suffering from deep financial problems.

In the U.S, the economic and capital market complications led to the adoption of conflicting policies in some instances. On the one hand, there was an increase in taxes and on the other, a decrease in public expenditure, all in order to reduce budget deficits. However, the Federal Reserve (Fed) continued to inject more money into the economy so as to stimulate growth and activities against the backdrop of still high but declining unemployment rates, and a limited capacity to create sufficient new jobs.

1 Represented by the European Financial Stability Facility (EFSF), the European Financial Stabilization Mechanism (EFSM) and the European Stability Mechanism (ESM).

66

Local and International Economic D

evelopments

The economies of developed countries are extremely vital as they are a key source of aid and support for developing countries. However, the economic and financial problems in the former countries made the flow of aid to the latter countries vulnerable to the risk of rationing or cancellation as a result of priority changes in donor countries. According to the UN’s Annual Economic Stability Report, there has been a decrease in aid to developing countries from developed countries over the past few years, especially those following the global financial crisis, and that this aid remained below commitments by the more affluent countries.

Foreign aid is considered to be one of the most important sources of funding for the Palestinian economy and a key pillar for its sustainability, especially by way of supporting the Palestinian government budget and covering some of its various expenditures. There is no doubt that through this channel the economic and financial risks which developed countries may be vulnerable to will directly impact the Palestinian economy. Furthermore, the U.S dollar is one of the most widely used currency in the Palestinian market; and since a number of assets are valued in the dollar, any changes in the value of the dollar against other currencies will have a direct effect on the value of these assets.

At the regional level, the reliance of the Palestinian economy on the Israeli economy as well as the close link with Jordan, particularly in the banking sector, make developments in these two economies especially important for the Palestinian economy.

2. Israeli EconomyThe Israeli economy demonstrated a slowdown in its performance in 2012, whereby GDP grew by about 3.3 percent in comparison to 4.4 percent in the previous year. With regard to monetary policy, Bank of Israel reduced the interest rate to settle at 2 percent at the end of 2012 as opposed to a 2.75 percent at the beginning of the year. It should be noted that Bank of Israel seeks to maintain price stability and to keep inflation within 1-3 percent band. In order to achieve this goal, monetary policies are monitored and adjusted.

As mentioned above, the Palestinian economy is heavily dependent upon its Israeli counterpart. Thus in addition to the large volume of trade between the two economies and the wide use of theNIS in the Palestinian market, there is also substantial clearance activity between the two economies resulting from the Israeli control of Palestinian external outlets. Finally, there is the significant Palestinian employment in Israel.

These linkages between the two parties make developments in the Israeli economy of huge importance to the Palestinian economy, but not vice versa. This is due to the smallness of the Palestinian economy in all aspects compared to the Israeli economy.

Figure 2-1: Bank of Israel interest rate (monthly), 2012

Perc

ent

Month

77

Local and International Economic D

evelopments

3. Jordanian EconomyThe Jordanian economy recorded a growth of 2.7 percent in 2012, which is very close to the rate of 2011. The inflation rate, however, rose to almost 4.8 percent, reflecting the persistent rise in prices overall, which increased pressures on the jordanian dinar (JD). At the same time, the Central Bank of Jordan’s (CBJ) balances of foreign currencies continued to fall, reaching approximately USD 6.6 billion at the end of 2012, with a recorded decrease of 37 percent compared with the previous year. Likewise, fiscal deficit recorded around 8.2 percent of GDP as opposed to 6.8 percent in the previous year.

Bank interaction between Palestine and Jordan is considered a key determinant of the economic relationship between the two countries. This interaction is manifested in the existence of several Jordanian banks holding a large market share in the banking activities of Palestine, whether in terms of deposits or facilities. This is in addition to the use of the JD, alongside the NIS and the U.S dollar.

There is no doubt that the developments in the Jordanian economy increase pressures on the Jordanian currency, and so, any additional risks that this currency may be exposed to will directly affect the Palestinian economy. Likewise, Jordanian banks’ branches and offices operating in Palestine are another channel of transmission of risk from the Jordanian financial sector to its Palestinian counterpart.

4. Local Economy Palestinian real GDP recorded a growth of 5.9 percent in 2012, compared with 12.2 percent in the previous year, while the global economy has grown by 3.2 percent in 2012, compared to 4 percent in 2011. Likewise, the group of developing countries achieved a growth of 5.1 percent in 2012, versus 6.4 percent in the previous year.

Although the Palestinian economy’s performance is not immune to the direct or indirect impact of global economic performance and the like, it is still governed by a set of exceptional factors, such as the continued Israeli occupation and control of crossings, and the internal political schism, etc. All these directly affect the Palestinian Economy in general and the financial sector in particular. It is possible to consider the latter factors as the main channels of transmission of potential risk to the Palestinian financial system.

• Exchange RatesThe Palestinian multi-currency economy has become exposed to the risk of exchange fluctuations in the aforementioned three currencies. Historical exchange rate data of currencies used in the Palestinian market, specifically the U.S dollar and the IsraeliNIS indicate instability in the exchange rate between these two currencies.

The exchange rate fluctuations in these two currencies are reflected almost entirely in the exchange rate between theNIS and the dinar as a result of the fixed exchange rate between the dollar and the dinar. Figure 2-3 shows clearly the fluctuations in the exchange rates between the dollar and theNIS. Although the source of these fluctuations is external, they still affect the Palestinian economy in terms of prices, the value of assets and other vital economic

Figure 2-2: Real GDP growth rate in Palestine comparing with other regions, 2008-2012

Perc

ent

Plestine WorldEmerging countries

88

Local and International Economic D

evelopments

and financial indicators. In contrast, it is unlikely for the Palestinian economy to have any effects on the two currencies, as it is a small economy compared to that of Israel.

On the other side, figure 2-4 demonstrates that the exchange market in Palestine was not exposed to any disturbances as a result of instability in exchange rates between the two currencies.

The margin between the buying and selling rates remained stable at 0.1 NIS per dollar on average between the years 2008-2012. This reflects the lack of speculation in the currency exchange market and the invulnerability to panic which usually arises from speculations and exaggerated expectations.

The changes in exchange rates produced fundamental changes in the pattern of deposits over time as the shares of the dollar and the dinar declined in favor of the NIS (figure 2-5). Between 2008-2012, the dollar and the dinar shares fell by 13.1 percent, and 16.3 percent respectively, as opposed to the increase in the share of the NIS by 53 percent in the same period. This transformation in deposit behavior reflects the extent of change in customer sentiment towards the stability of various exchange rates. Specifically the tendency of the public to deposit the NIS over other currencies consist with changes in the respective exchange rates.

Direct credit facilities granted in NIS also witnessed a rise in share by 5.5 percent between 2008 and 2012. Also, there was an increase in the share of the dinar facility by 5.3 percent, compared with a decrease in the dollar share by about 10.7 percent in the same period (figure 2-6). However, it is difficult to link these changes with exchange rates alone as interest rates on various currencies may be a main determinant of facilities’ portfolio fluctuations. Nevertheless, the relative stability of interest rates compared to exchange rate fluctuations makes the connection of facilities portfolio with exchange rates the most accurate.

• Interest RatesAnnual interest rates on deposits and lending of different currencies used by banks operating in Palestine indicate some changes in 2012 compared

NIS

per

USD

BidAsk

Figure 2-4: USD/NIS exchange margins (period average), 2008-2012

Figure 2-5: Total deposits at banks operating in Palestine by currency, 2008-2012

Perc

ent

USD JD NIS Others

Figure 2-3: USD exchange rate fluctuations against NIS (period average), 2008-2012

Perc

ent

99

Local and International Economic D

evelopments

to 2011. The interest rate on the dinar increased by about 52 basis points (bps) for deposits, and 48 bps for lending, bringing the interest rate of dinar facilities to 8.11 percent, and of dinar deposits to 1.70 percent.

In comparison, interest rate on dollar facilities increased by about 18 bps, while dollar deposits rate increased by 13 bps, making the interest rate 6.97 percent for facilities, and 0.46 percent for deposits.

In contrast, interest on NIS facilities decreased by 43 bps in 2012, as opposed to arise in interest rate on NIS deposits by around 21 bps. This reduced the interest rate of NIS facilities to 11.26 percent while interest on deposits rose to 1.22 percent.

The widening margin between the deposit and lending rates on these currencies can be linked to several reasons, including the margin in the interset in country of origin, where interest on the NIS, for example is considered high in Israel in comparison to the dollar and the dinar. Likewise, security and political conditions make the Palestinian economy a highly risky environment compared to other countries, which affects interest rates level and tendency to rise.

• Palestinian External SectorThe importance of Palestine’s external position from a financial stability perspective emanates from its being a channel of potential risks to the stability of vital sectors in the local economy in general and the banking and financial sector in particular. This is largely through exchange rates, interest rates and foreign aid. Palestinian balance of payments (BoP) data at end 2012 indicate continued deterioration in current account deficit which amounted to USD 2,814.7 million, a rise by 28.4 percent over the previous year. This increased the deficit to GDP ratio to 27.4 percent, a rise by 5 percentage points compared to the year before.

Israel remains of prevailing dominance in trade relations with Palestine considering that 84 percent of exports and 70 percent of imports are made with it, evidently demonstrating the importance of the NIS as the main currency in Palestinian-Israeli trade relations. As a consequence, any developments in the NIS value will be reflected in the Palestinian economy through prices of goods, and both the volume and value of imports and exports. Theoretically, however, this may also apply to the JD, but with a much less importance, since the value of trade between Palestine and Jordan remains low, amounting to just 6 percent and 2 percent of imports and exports respectively.

Figure 2-7: Deposit and lending rates in Palestine by currency, 2008-2012

Deposit USD Deposit JD Deposit NIS

Lending USD Lending JD Lending NIS

Figure 2-6: Credit portfolio by currency, 2008-2012

Perc

ent

USD JD NIS Others

1010

Local and International Economic D

evelopments

Box (1): Arab safety net and the shortage of liquidity in PalestineThe Palestinian government suffered from severe financial difficulties, especially during the past two years, which led to its failure to cover main public expenditure items (such as wages and salaries) on a regular basis, hence, pushing it to constantly resort to borrowing from banks in order to carry out its functions. With the purpose of limiting the negative impact of these difficulties, the Arab fraternity expressed their readiness, at the 2012 Arab Summit held in Baghdad, to provide a financial safety net with a value of USD 100 million per month to the Palestinian government. This aid would assist in facing the difficulties that may arise from Israeli threats following Palestine’s initiative to go to the UN in the same year. The fraternity also committed to continue support of the Al Aqsa and the Al Quds Intifada funds*. This is in addition to providing urgent support, as of 1/4/2012 according to the 2002 Beirut summit**,apart from the financial safety net. These funds are non-refundable and contributions are mandatory upon all member states calculated according to their shares in the Arab League secretariat’s general budget.

Arab donations for Palestinian budget support, 2009-2012(USD million)

2012201120102009Country

26.652.726.326.0Algeria

3.31.78.1--Egypt

99.5221.7128.540.7Saudi Arabia

85.00.015.2230.7United Arab Emirates

30.110.252.7164.3Qatar

25.2------Iraq

269.7286.2230.8461.7Total

34.735.420.334.3As a percent of total budget support (%)Source: Palestinian Ministry of Finance, monthly reports.

Wages and non-wages arrears, 2009-2012

Non-wagesWages & SalariesYear

Percent (%)Value (USD million)Percent (%)Value (USD million)

20288.6453.52009

670.6349.62010

18258.76106.52011

19272.112213.02012Source: Palestinian Ministry of Finance, monthly reports.

* These two funds have been established in accordance with the decisions of the Cairo Summit 2000. The first fund was named “Al Quds Intifada Fund” in order to support the martyrs and wounded families with a capital of USD 200 million, and the second was named the Al Aqsa Fund, to aid the Palestinian economy with a capital of USD 800 million.

** Urgent support of USD 55 million for 6 months, subject to automatic renewal for a further 6 months as long as the Palestinian government is in need of this support.

Despite aid transfers by the Arab fraternity to support the budget, such aid remains insufficient to finance the deficit. In fact, the disbursements were much less than the commitments pledged by the Arab countries for both the financial safety net, approved at the 2012 Baghdad summit (a

1111

Local and International Economic D

evelopments

total of USD 1,395 million), and the urgent support pledged at the 2002 Beirut summit. Overall, the percentage disbursed reached only 19.3 percent of the commitments in 2012.

There is no doubt that if the Arab support had pledges materialized in full, they would have reduced the overall budget deficits to a minimum, alleviated the difficulties of liquidity, and toughened Palestine’s political position in coping with Israeli pressures with respect to clearance transfers. This in turn would not only have led to closing the financing gap without the need of borrowing from banks, but would also have reduced government debt. This would requires the activation of the decisions made at the Arab summits in this regards.

• Foreign AidThe Palestinian government largely relies on foreign aid2, which is hugely interlinked with the political and economic conditions prevailing in the donor countries and as well as in Palestine, making the flow of aid inconsistent and greatly prone to fluctuations. This constitutes a source of risk to the government, making it unable to fulfill its obligations. An additional related risk is the fact that the aid receipts are denominated in a different currency than the main currency of expenditure (NIS), making them vulnerable to exchange rate fluctuations.

In order to alleviate Israeli pressures exerted upon the Palestinian government in terms of blocking customs tax revenue, it was agreed that the Arab countries will provide Palestine with a financial safety net valued at USD 100 million per month in order to face the difficulties arising from Israel’s withholding of clearance revenues.

2 Despite the government’s efforts over the past few years to reduce their dependency on foreign aid, it still accounts for a high proportion of total revenues (volumes reaching USD 0.9 billion in 2012, or 29.5 percent of revenues and grants compared to 31 percent in 2011).

1212

13

Infrastructure and Developm

ent Indicators in the Financial Sector

Chapter Three Infrastructure and Development Indicators in the Financial Sector

Overview

The infrastructure of the financial sector, with all its legal and supervisory frameworks and systems, is considered to be a key factor in achieving financial stability. Starting with the PMA’s responsibility of maintaining financial stability and ensuring that bank management is in compliance with the highest international standards and practices, the development of this infrastructure has continued, enhancing its efficiency in various aspects and related frameworks. A number of crucial accomplishments were achieved in 2012, whether in legislations, instructions and supervisory systems or in completing several major projects and updating supervisory systems. Moreover, financial and banking inclusion were enhanced, in addition to remarkable progress in the implementation of the recommendations of the Basel Committee on banking supervision. This all served to gradually fulfill the requirements of transforming into a modern, full-fledged central bank.

1. Legal and Regulatory FrameworkThe National Payments System Law was passed on 23/11/2012, under the resolution of law No. (17) of 2012. This law represents an integral step towards the implementation of electronic payment methods. Likewise, it also facilitates electronic and final settlement for bank accounts and the financial transactions resulting thereof. Furthermore, It also allows the installation of electronic clearing systems between banks via the scanning feature.

It is also expected that the establishment of the Palestine Deposit Insurance Corporation (PDIC) will strengthen the financial safety net, protect depositors, and maintain financial stability. It will ensure customers’ deposits in the Palestinian banking system, covering approximately 93 percent of bank depositors in the West Bank and Gaza. The establishment of the PDIC is expected to result in increased deposits, thus enhancing the vital role played by banks in promoting economic and financial development in Palestine. In the same context, the PMA has obtained membership in the IADI as an associate member. This membership came prior to the issuance of the Deposit Insurance Corporation Law3 to allow taking advantage of the practical experiences of members in the IADI, which includes 132 deposit insurance corporations worldwide.

3 At a post report date, the Palestine Deposit Insurance Corporation’s Law has been issued as a Resolution Act on 29/05/2013.

14

Infrastructure and Developm

ent Indicators in the Financial Sector

In light of the Banking Law No (9) of 2010, the PMA embarked in 2012 upon a comprehensive review of all previously issued supervisory instructions to achieve more consistency with the amendments and additions made to this law. Moreover, the PMA issued new supervisory instructions which regulate and control banking activities in view of the national and international legal and supervisory developments. In this respect, the PMA issued instructions covering a number of areas: rules for granting bonuses and incentives, the required reserve base, and the “primary bank account” for each citizen. These instructions come under the PMA’s policy of increasing banking sector participation in promoting financial inclusion in all segments of society, thus enabling participants to take advantage of the banking services available. The PMA furthermore issued several instructions which address the following: ATM services, regulating the work of the external auditors, managing money changer accounts, updating the BURAQ system, requirements of opening accounts for cooperatives and charitable institutions and civil society bodies, launching of the reporting system for lost and suspended checks, and finally, appointments, transfers, disciplinary actions and resignations, and counterfeit currency.

Additionally, the PMA issued several circulars governing routine procedures and updates in the banking business. For example, circular No. (7/2012) prohibits foreign banks from granting credit to an applicant if it makes the exposure exceed 10 percent of the core capital of foreign bank branches, without a prior approval from the PMA. This is also the case with circular No. (103/2012),which requires banks to modify their systems and customer account numbers in accordance with the International Bank Account Number-IBAN code given to Palestine.

It is expected that with the start of the year 2014, the legal and regulatory challenges facing banks operating in Palestine would be new, and as such, they may directly and indirectly impact financial stability. These challenges emanate mainly from the FATCA law, under which all the financial institutions outside the U.S, including those operating in Palestine, are obligated to disclose the financial account details of individuals possessing U.S citizenships; these would have to be submitted to the IRS for tax collections and combating tax evasion. Various consultations and internal and regional communications with Arab financial institutions, especially the Arab Bank Union and the Arab Monetary Fund, have been conducted regarding this issue. It is important to note that work is still underway via the aforementioned channels to determine the appropriate option to comply with this law.

2. Developments and Updates of Baking System The PMA relentlessly pressed forward to develop modern banking systems in accordance with the highest international standards and practices, all within the framework of building a robust and comprehensive banking infrastructure. This infrastructure reduces risks that threaten the banking system in particular and the financial system in general. As such, in 2012 the PMA completed further developmental procedures in some of the banking system that have been initiated in previous years. It also began the implementation of new projects expected to be completed in the next two years.

Some of the projects which were completed (or are underway) are the following: implementing Standards II &III of the Basel Committee, the IBAN, establishing an electronic national switch for electronic payment instruments, settlement of net transactions in the financial market via BURAQ system4, creating a supervisory position for key payment systems, the Mobile Banking Project and launch of the Lost and Suspended Checks System5. These are in addition to preparing for the launch of the Unified Query System which aims to provide disclosure and allow public access to information regarding the ratings of clients listed on the Bounced Checks System, Updates on the Credit Scoring System, and the PMA’s Business Continuity Project. These are intended to ensure sustainability by delivering different banking services in times of crises and emergency.

4 Though this project was listed in the 2012 plan, it was only completed in February 2013 due to delays in the adoption of the Palestinian Payment Law until end of 2012.

5 This system was launched under instruction number (10/2012) on 19/09/2012.

15

Infrastructure and Developm

ent Indicators in the Financial Sector

Box (2): Foreign Account Tax Compliance Act (FATCA)Banks worldwide are preparing to examine their U.S citizen customer account statements in compliance with FATCA, which the American congress passed on 18th March 2012. This act was enforced in order to fill the legislative vacuum in the field of taxation and to combat tax evasion by U.S citizens who own properties and deposits abroad.

Based on this act, the U.S government, as of mid-2014, will request all foreign financial institutions to submit names and statement details of customers subject to the U.S levy. According to U.S legislations, citizens as well as their alien residents are subject to this levy. Under this act, all the financial institutions, including Arab banks, are obligated to identify the concerned parties holding U.S citizenship or to disclose their identity should their assets exceed USD 50,000.

In line with the regulations of FATCA, there are two possible options that foreign banks can adhere to: the first requires the local government- and not the banks- to apply the law themselves, and furthermore, to sign agreements cooperating with the U.S government. Conversely, the second will be applied in the event that the government fails to sign the designated agreements directly with the U.S. Consequently, the banks will be required to intercede in direct agreements with the U.S tax administration within the deadlines of the law.

Based on this, dealing with this law presents two alternatives: The first is that it is incumbent upon designated institutions to enter into agreement, named “Conveyance of reporting and income tax information agreement”, with the U.S internal tax services office/ Internal Revenue Service (IRS). These institutions will be labeled thereof “cooperating banks”. As for the second, in the event if non-cooperation, the law allows the IRS to deduct 30 percent from the offending accounts at U.S banks. This means that non-cooperating banks will be exposed to operational risks (deduction of 30 percent tax) and reputational risks (U.S banks may stop dealing with non-cooperating banks).

Obviously, compliance with this law may entail many operational costs arising from the amendment procedures: opening new accounts and their follow-ups, monitoring and auditing. Moreover, there are also costs related to finding systems for processing transactions, identification procedures of clients who use foreign banks, efforts to raise awareness and establishing a special union for those complying with this law and employing qualified personnel. These are to be added to the reputational risk which was previously mentioned.

It should be noted that the U.S has reached FATCA agreements with more than 80 countries and judicial authorities. These include Germany, Spain, Norway, Switzerland, Iceland, Mexico, Denmark and Great Britain. Similar agreement negotiations are currently underway with a dozen other countries. On the other hand, the group of 8 nations (G8) agreed to the automatic exchange of data, which means exchanging customer account information among these countries.

16

Infrastructure and Developm

ent Indicators in the Financial Sector

3. Development Indicators in the Banking System

• Branching Policy and ConcentrationAt the end of 2012, bank mergers and restructuring operations resulted in a decrease in the number of banks operating in Palestine to 17 banks, 7 of which are domestic and 10 are foreign (8 Jordanian Banks,1 Egyptian, and 1 foreign bank). This came following the successful merger between the National Bank6 and the Arab Palestinian Investment Bank on 1/1/2012.

These banks operate through a network of branches and offices spread over various areas in Palestine. They number 232 branches and offices; 121 are domestic, and 111 are foreign. In 2012, 6 new branches and offices were opened: a branch and an office for Bank of Palestine, a branch for Al-Quds Bank, a branch for the National Bank, two branches for the Arab Bank, and a branch for Bank of Jordan.

By licensing new branches and offices, the PMA aims at delivering banking services to all Palestinian cities and villages, prioritizing rural communities and remote regions in order to facilitate the commercial and economic activities of citizens, as well as different financial transactions. This trend was reinforced in the PMA’s branching policy adopted in 2007. Through this policy, the PMA seeks to reduce the ratio of persons per branch in order to raise the efficiency of services provided, as well as to remain consistent with internationally recognized rates (10,000 persons per branch). With this increase in branches, the ratio of persons per branch has decreased to about 16,800 persons per branch by the end of 2012, suggesting in theory, room for more bank branching opportunities.

In 2012, an improvement was recorded in market concentration in the banking sector, as measured by the Herfindahl index7, whether in terms of deposits or facilities compared to the previous year.

Herfindahl index of banks’ market shares in private sector deposits dropped to 1,738 points in 2012, in comparison to 1,796 points in 2011, which is below the internationally recognized critical limit (which is 1800 points). A decrease was also registered in 2012 under concentration indicators in banks’ market shares of total direct credit facilities, reaching 1,716 points, against 1,735 points in the previous year, also below the critical limit of concentration.

Accordingly, it is possible to say that the banking sector entered into competition on both sides of the financial intermediation process (attracting savings and granting facilities). It is well known that the increase in market concentration will reduce the possible benefits that can be achieved by a competitive market, not to mention,

6 Al-Rafah Microfinance Bank underwent name change to become the National Bank. This was based on the decision of the board of directors and the approval of the general assembly. The name change was completed by the Companies Controller registering the company in Nov. 2012, and then in Dec. 2012, the bank completed the acquisition of the Arab Palestinian Investment Bank.

7 The formula for the Herfindahl Index is: =(MS1)2H=

ni , where (H) is the value of the Herfindahl index, (MS1) is the bank share (i) of the

total desired variable to calculate the concentration accordingly, such as total bank assets or total deposits and so on. The inverse Herfindahl index indicates the number of banks dominating the banking market to any specific value for this index, calculated as follows: N= 1

H, where N is the number of equal-sized-banks that the banking market can contain to any specific value (H). The index can range between 0-10,000 points (if its value is 10,000, it implies complete monopoly). The relationship between the index value and the degree of competition is inversed. This means that the higher the index value, the lower the degree of bank concentration and the higher the degree of inequality between banks and weakness in competitiveness and vice versa. Concentration is considered high if the index value is greater than 1,800 points (this limit is approved by the U.S).

No.

of b

ranc

hes

Popu

lati

on p

er b

ranc

h

No. of branches (lift) Population per branche (right)

Figure 3-1: Branches of banks operating in Palestine, 2008-2012

17

Infrastructure and Developm

ent Indicators in the Financial Sector

that banking instability increases risks, thus directly impinging on financial stability at large.

The previous developments in the banking sector (whether legal and supervisory or in the field of developmental systems and legislations and branching policy) contributed vastly to boosting the volume and quality of financial services offered to the public. As a result, the number of ATMs increased by 16.2 percent annually between the years 2008-2012, corresponding with the increase in the number of cards and transactions executed through this device. It is worth noting that the instructions which the PMA issued in 2012, assigning ATMS services and the development of electronic banking products, includes the minimum requirements for ATM operations, the conditions necessary to provide them, the foundations of security and protection, as well as the feeding and maintenance of these devices.

Similarly, electronic Points of Sale (POS) were also developed in the same time period. Their average increased by 34.5 percent per annum, numbering 3,952 POS in 2012, alongside an increase in the number of electronic cards (debit and credit cards). This consequently raised the value of transactions executed through them up by an average of 22.3 percent for debit cards and 53.2 percent for credit cards annually.

This clearly indicates the increasing tendency towards the use of electronic payments systems, which contributes to increasing the velocity of cash circulation and to stimulation of growth in the economy.

Table (3-1): Financial services developments, 2008-2012(values in USD million)

Average growth rate (%)20122011201020092008Financial Services

ATMs

16.2435378335305240 Number of machines

19.3122,379101,72871,68468,18562,180 Number of cards

28.44,879,2125,554,97011,318,4164,613,0433,515,116 Number of transactions

3.9946.41264.41256.6866.9909.8 Values

34.53,9253,658231417451248 Number of PoS

Debit Crards

15.2410,536354,352308,962285,228233,795 Number of cards

28.43,374,4973,016,5012,519,0032,133,3361,302,489 Number of transactions

22.3749.6721.3610.1544.4351.5 Values

Credit cards

34.256,83547,04637,37429,08218,017 Number of cards

76.51,162,135858,263641,474244,101140,295 Number of transactions

53.2117.198.210239.928.2 Values

Figure 3-2: Herfindahl index, 2008-2012

Poin

t

Private sector desposits Credit facilities

18

Infrastructure and Developm

ent Indicators in the Financial Sector

• Development of Bank Accounts (Deposits and Borrowing)The previous developments in the banking sector, mainly in enhancing the use of electronic banking services, have positively affected indicators of financial intermediation and success of the latter in performing its assigned role. The number of bank accounts increased on average by 8.8 percent during 2008-2012, reaching around 2.7 million accounts or 63.3 accounts per 100 people in Palestine. Similarly, depositors numbered 1.5 million (representing 34 percent of population) and an average of 6.6 percent growth in the year 2012. Meanwhile, the number of borrowers increased, reaching almost a quarter of a million (253,441 borrowers), an average of 18.8 percent growth, and the number of loans which they obtained amounted to approximately 343,466 loans in 2012.

Despite the tangible progress in the indicators of intermediation, a relative weakness continues to exist regarding small and medium enterprises’ shares in banking services (as opposed to clear concentration on part of individuals). The number of deposit accounts for these companies did not exceed 1.2 percent of the total depositors, and the value of their deposits was approximately 2.5 percent of total customer deposits in 2012. The case is similar with respect to borrowers, where the ratio of small and medium enterprises borrowing from the banking sector reached 1.7 percent of total borrowers, and the value of their loans were around 6.2 percent of gross credit in 2012.

Table (3-2): Number of Accounts and values in banks operating in Palestine, 2008-2012 (values in USD million)

Average growth rate (%)20122011201020092008Financial Services

8.82,715,3542,543,3472,185,7792,011,2421,947,265Number of banking accounts

6.61,463,9781,416,4901,414,2381,216,398-Number of depositors

27.016,96013,91412,0328,383- Of which: SMEs

6.21,406,0261,385,1621,382,9701,182,928- Individuals

6.47484.26972.56802.46296.85846.9Value of customer deposits

-3.3186.6239.1286.1222.5- Of which: SMEs

4.55457.65308.14990.14782.3- Individuals

12.2343,466332,297246,460234,947222,216Number of loans

18.8253,441226,245180,339151,750-Number of creditors

26.14,3032,9932,0312,328- Of which: SMEs

16.9233,328213,156172,951146,667- Individuals

23.24199.13550.72885.92234.21828.2Total Credits

24.0259.6210.8181.0136.6- Of which: SMEs

30.71628.61315.11023.2733.0- Individuals

• Financial Depth IndicatorsGenerally, the indicators of financial depth strengthened as credit (facilities) to nominal GDP ratio increased to 40.2 percent in 2012, as opposed to 35 percent in the previous year. However, this ratio seems low compared to neighboring countries where the ratio was 80.1 percent in both Egypt and Jordan and 166.8 percent in Lebanon. It is important to note that PMA is aiming to increase local credit through the reduction of bank placements abroad

19

Infrastructure and Developm

ent Indicators in the Financial Sector

in order to deepen the relationship between the banking sector and various economic sectors.

Despite the importance of the development in the credit ratio to GDP, limiting fluctuations in this ratio is still necessary. Empirical evidence has shown that this fluctuation should not exceed 20 percent, as its increase was one of the common denominators of the financial crises which struck the banking sector in many countries8. Note that this ratio (the fluctuation in the ratio of credit facilities to GDP) ranged between 3.3 percent and 8 percent in the period between 2008-2012- a moderate rate, well below the 20 percent mark.

Other ratios of financial dpth, such as the ratio of credit extended to the private sector out of total credit, fell to 66.5 percent in 2012 compared to 69 percent in the previous year (this ratio formed an average of 70.7 percent between 2008-2012). Note that this ratio was 91.1 percent in Jordan, 85.4 percent in Egypt and 54.9 percent in Lebanon in 2012.

Among the ratios of financial depth which measure the propensity of the public towards savings, is the ratio of customer deposits to GDP, which slightly escalated from 71.3 percent in 2011 to 73.0 percent in 2012. This is a moderate ratio in comparison to neighboring countries where it hits 112.3 percent in Jordan during the same time period.

This is not so different from the private sector’s propensity for savings, where the ratio of the private sector deposits out of total customer deposits reached 91.7 percent in Palestine in 2012, as opposed to 93.2 percent in Jordan, 85.5 percent in Egypt and 97.9 percent in Lebanon during the same year.

In general, the role of financial intermediation in Palestine improved and developed over time, where the loans to customer deposits ratio increased from 50.9 percent in 2011 to 56.1 percent in 2012. It seems that this ratio is moderate when compared with some neighboring countries, where it was 71.4 percent in Jordan, 49.5 percent in Egypt, and 54 percent in Lebanon.

8 The session of economic and financial stability policies, which was convened by the Arab Monetary Fund between the 10th and 21st of June 2012.

Perc

ent

Palestine Jordan Egypt Lebanon

Figure 3-3: Credits as a percent of GDP in Palestine and some neighboring countries, 2008-2012

Perc

ent

Figure 3-4: Private sector credits as a percent of total credits in Palestine and some neighboring countries, 2008-2012

Palestine Jordan Egypt Lebanon

Figure 3-5: Private sector deposits as a percent of customer deposits in Palestine and some neighboring

countries, 2008-2012

Perc

ent

Palestine Jordan Egypt Lebanon

20

Infrastructure and Developm

ent Indicators in the Financial Sector

Perc

ent

Palestine Jordan Egypt Lebanon

Figure 3-6: Credit to deposits ratio in Palestine and some neighboring countries, 2008-2012

Perc

ent

Palestine Jordan Egypt Lebanon

Figure 3-7: PEX market capitalization as a percent of GDP in Palestine and neighboring countries, 2008-2012

On the other hand, and despite the decline in the market value of the traded shares in PEX as a percent of GDP from 28.5 percent in 2011 to 27.9 percent in 2012, this ratio remains moderate compared to neighboring countries, where it was 86.1 percent in Jordan, 24 percent in Egypt and 27.4 percent in Lebanon.

21

Credit Risks in the Banking Sector

Chapter Four Credit Risks in the Banking Sector

Overview

Credit risks are considered to be some of the systemic financial risks and the most prominent type of risk which exposes banks to potential losses, and hence, affects its capital and profits. Against this background, this chapter deals with the analysis of credit portfolio for both foreign and local banks, and granted to both the public and private sectors. Furthermore, it analyzes risks associated with public finance, especially in light of the continued financial difficulties which the Palestinian government suffers from, in addition to an examination of mortgage and housing lending portfolios. This comes in the framework of the volume of risk which financial stability may be vulnerable to in Palestine and the various trends of these risks. This chapter also addresses the most vital measures and control instructions which guarantee that the extent of these risks is as low as possible, including maintaining the sustainability of financial stability in general.

Figure 4-1: Distribution of credit portfolio between private and public sectors, 2008-2012

Public sector Private sector

Perc

ent

1. Risks associated with credits granted to Public and Private SectorFigure 1-4 demonstrates an increase in the public sector’s share of total credit granted by banks operating in Palestine over time. Particularly in 2012, we see this ratio rising to 33.5 percent, in comparison to 31 percent in the previous year, mainly due to the severity of the financial difficulties that the government faces. This indicates an increase in the risks that banks are exposed to, as the credit granted to the government has exceeded the ownership equity of all banks. As a precautionary measure to limit these risks, the PMA called upon banks to proceed with extreme caution when dealing with credit offered to the government.

22

Credit Risks in the Banking Sector

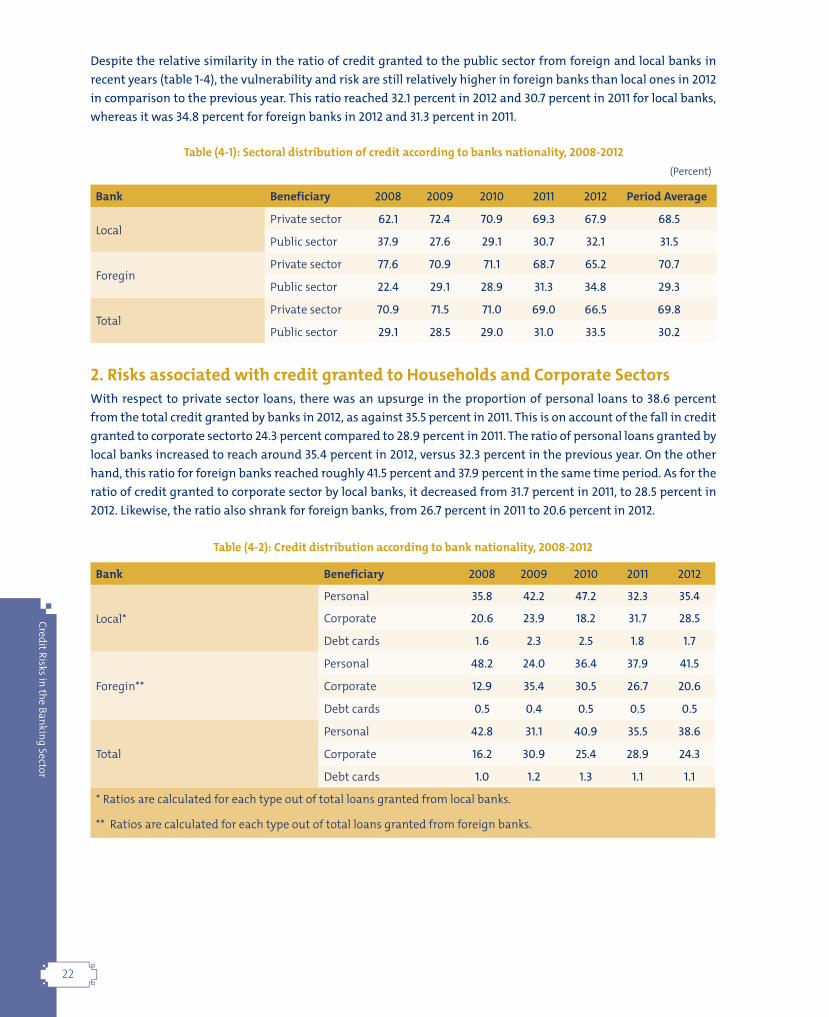

Despite the relative similarity in the ratio of credit granted to the public sector from foreign and local banks in recent years (table 1-4), the vulnerability and risk are still relatively higher in foreign banks than local ones in 2012 in comparison to the previous year. This ratio reached 32.1 percent in 2012 and 30.7 percent in 2011 for local banks, whereas it was 34.8 percent for foreign banks in 2012 and 31.3 percent in 2011.

Table (4-1): Sectoral distribution of credit according to banks nationality, 2008-2012(Percent)

Bank Beneficiary 2008 2009 2010 2011 2012 Period Average

LocalPrivate sector 62.1 72.4 70.9 69.3 67.9 68.5

Public sector 37.9 27.6 29.1 30.7 32.1 31.5

ForeginPrivate sector 77.6 70.9 71.1 68.7 65.2 70.7

Public sector 22.4 29.1 28.9 31.3 34.8 29.3

TotalPrivate sector 70.9 71.5 71.0 69.0 66.5 69.8

Public sector 29.1 28.5 29.0 31.0 33.5 30.2

2. Risks associated with credit granted to Households and Corporate SectorsWith respect to private sector loans, there was an upsurge in the proportion of personal loans to 38.6 percent from the total credit granted by banks in 2012, as against 35.5 percent in 2011. This is on account of the fall in credit granted to corporate sectorto 24.3 percent compared to 28.9 percent in 2011. The ratio of personal loans granted by local banks increased to reach around 35.4 percent in 2012, versus 32.3 percent in the previous year. On the other hand, this ratio for foreign banks reached roughly 41.5 percent and 37.9 percent in the same time period. As for the ratio of credit granted to corporate sector by local banks, it decreased from 31.7 percent in 2011, to 28.5 percent in 2012. Likewise, the ratio also shrank for foreign banks, from 26.7 percent in 2011 to 20.6 percent in 2012.

Table (4-2): Credit distribution according to bank nationality, 2008-2012

Bank Beneficiary 2008 2009 2010 2011 2012

Local*

Personal 35.8 42.2 47.2 32.3 35.4

Corporate 20.6 23.9 18.2 31.7 28.5

Debt cards 1.6 2.3 2.5 1.8 1.7

Foregin**

Personal 48.2 24.0 36.4 37.9 41.5

Corporate 12.9 35.4 30.5 26.7 20.6

Debt cards 0.5 0.4 0.5 0.5 0.5

Total

Personal 42.8 31.1 40.9 35.5 38.6

Corporate 16.2 30.9 25.4 28.9 24.3

Debt cards 1.0 1.2 1.3 1.1 1.1

* Ratios are calculated for each type out of total loans granted from local banks.

** Ratios are calculated for each type out of total loans granted from foreign banks.

23

Credit Risks in the Banking Sector

Personal loans include loans guaranteed by mortgages, car loans, educational loans and other consumption loans. These loans are granted against multiple collaterals that reduce potential risks. Meanwhile, credit extended to the corporate sector include investment loans and short-term loans (overdrafts), with the latter constituting around 20.1 percent of gross credit extended to corporations in local banks, and 22 percent in foreign banks. It should be noted that overdrafts are riddled with relatively higher risks than loan risks. Because of this, the PMA took certain control measures for overdraft facilities so that their balance does not exceed 30 percent of the total credit of banks9.

Credit cards, especially those granted to individuals or corporations, account for a limited ratio, which amounted to 1.1 percent of the total credit granted to banks in both 2011 and 2012. In terms of nationality, the ratio of credit extended to credit cards was higher in local banks (1.7 percent in 2012 and 1.8 percent in 2011) compared to foreign banks, where the ratio of total credit granted remained stable at 0.5 percent. Based on this, it is clear that credit granted by the banking sector in the form of credit cards is limited and consequently the risks associated with it do not pose a large threat to financial stability.

3. Risks associated with credit granted according to residencyIt is noticed from table (4-3) that the majority of credit extended by banks is to residents, with a ratio of 96.4 percent of gross credit during the period 2008-2012. This is in contrast to the credit granted to non-residents, which did not exceed 3.6 percent during the same time period. Likewise, in 2012, it is also noticed that there were equal ratios granted to non-residents by local and foreign banks at about 1.1 percent. The value of credit granted to non-residents by local banks amounted to USD 21.1 million in 2012, versus USD 24 million by foreign banks.

Accordingly, the risk associated with credits to non-residents is limited and inconsequential. It does not pose a source of great worry to financial stability in Palestine, especially since there are control measures governing the mechanism of granting credits to non-residents.

Table (4-3): Credit distribution according to residency and bank nationality, 2008-2012(Percent)

Bank Beneficiary 2008 2009 2010 2011 2012 Period average (%)

LocalResident 97.8 97.5 98.4 98.7 98.9 98.9

Non-resident 2.2 2.5 1.6 1.3 1.1 1.7

ForeginResident 89.2 90.7 97.7 98.2 98.9 94.9

Non-resident 10.8 9.3 2.3 1.8 1.1 5.1

TotalResident 92.9 93.4 98.0 98.4 98.9 96.4

Non-resident 7.13 6.6 2.0 1.1 1.1 3.6

Based on instruction number (5/2008), the most distinctive of these controls are: (i) limiting the exploitation of these credits to Palestine exclusively, (ii) consisting with a plan to encourage investment, and (ii) enjoying sufficient and provisioned collaterals “if in a cash form” or registered under the name of the bank “if in the form of physical collaterals”. Apart from these conditions, it is mandatory to obtain written pre-approval from the PMA.

9 Overdrafts granted to the government and public sector institutions are excluded from the overdraft value for the purpose of calculating this ratio. Likewise, it also excludes those granted as cash guarantee.

24

Credit Risks in the Banking Sector

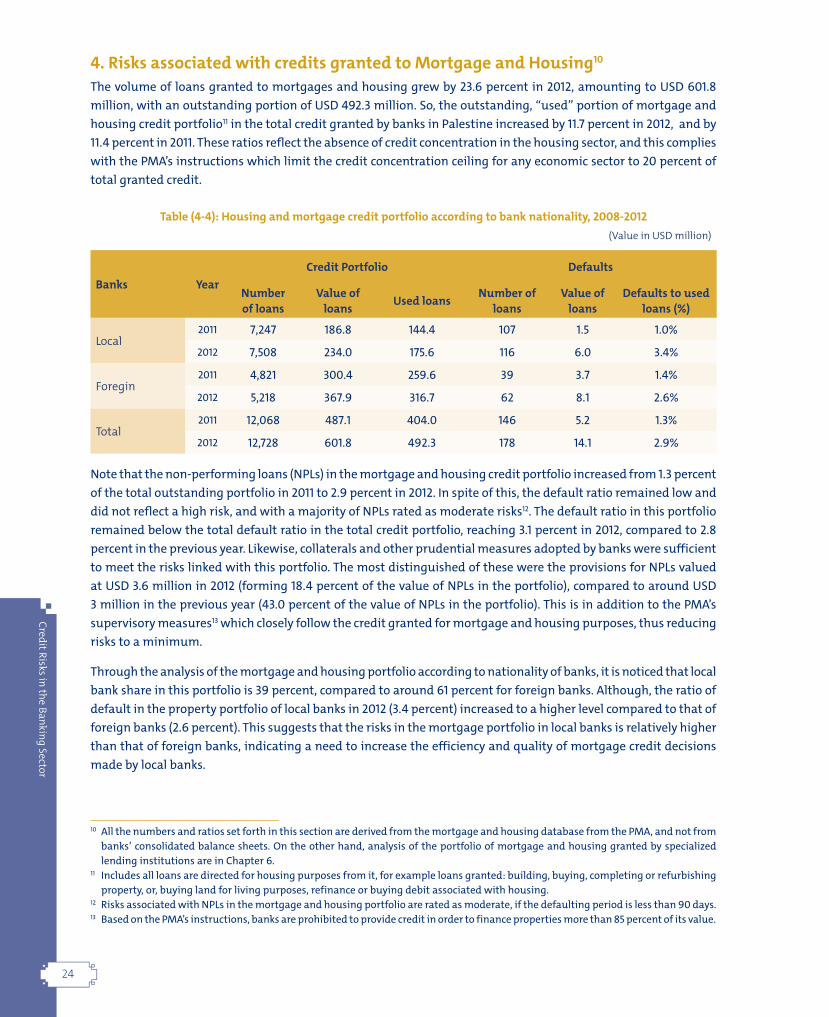

4. Risks associated with credits granted to Mortgage and Housing10

The volume of loans granted to mortgages and housing grew by 23.6 percent in 2012, amounting to USD 601.8 million, with an outstanding portion of USD 492.3 million. So, the outstanding, “used” portion of mortgage and housing credit portfolio11 in the total credit granted by banks in Palestine increased by 11.7 percent in 2012, and by 11.4 percent in 2011. These ratios reflect the absence of credit concentration in the housing sector, and this complies with the PMA’s instructions which limit the credit concentration ceiling for any economic sector to 20 percent of total granted credit.

Table (4-4): Housing and mortgage credit portfolio according to bank nationality, 2008-2012(Value in USD million)

Banks YearCredit Portfolio Defaults

Number of loans

Value of loans Used loans Number of

loansValue of

loansDefaults to used

loans (%)

Local2011 7,247 186.8 144.4 107 1.5 1.0%

2012 7,508 234.0 175.6 116 6.0 3.4%

Foregin2011 4,821 300.4 259.6 39 3.7 1.4%

2012 5,218 367.9 316.7 62 8.1 2.6%

Total2011 12,068 487.1 404.0 146 5.2 1.3%

2012 12,728 601.8 492.3 178 14.1 2.9%

Note that the non-performing loans (NPLs) in the mortgage and housing credit portfolio increased from 1.3 percent of the total outstanding portfolio in 2011 to 2.9 percent in 2012. In spite of this, the default ratio remained low and did not reflect a high risk, and with a majority of NPLs rated as moderate risks12. The default ratio in this portfolio remained below the total default ratio in the total credit portfolio, reaching 3.1 percent in 2012, compared to 2.8 percent in the previous year. Likewise, collaterals and other prudential measures adopted by banks were sufficient to meet the risks linked with this portfolio. The most distinguished of these were the provisions for NPLs valued at USD 3.6 million in 2012 (forming 18.4 percent of the value of NPLs in the portfolio), compared to around USD 3 million in the previous year (43.0 percent of the value of NPLs in the portfolio). This is in addition to the PMA’s supervisory measures13 which closely follow the credit granted for mortgage and housing purposes, thus reducing risks to a minimum.

Through the analysis of the mortgage and housing portfolio according to nationality of banks, it is noticed that local bank share in this portfolio is 39 percent, compared to around 61 percent for foreign banks. Although, the ratio of default in the property portfolio of local banks in 2012 (3.4 percent) increased to a higher level compared to that of foreign banks (2.6 percent). This suggests that the risks in the mortgage portfolio in local banks is relatively higher than that of foreign banks, indicating a need to increase the efficiency and quality of mortgage credit decisions made by local banks.