2012 annual mortgage fraud risk report

TRANSCRIPT

1Mortgage Fraud Risk Report 2012 Annual

© Interthinx, Inc. 2013. All rights reserved. Interthinx and FraudGUARD are

registered trademarks of Interthinx, Inc.. No part of this publication may be

reproduced, stored in a retrieval system or transmitted, in any form or by any

means, electronic, mechanical, photocopying, recording or otherwise, without

prior written permission. The information contained within should not be

construed as a recommendation by Interthinx, Inc. or Verisk Analytics for any

course of action regarding financial, legal or accounting matters.

2012

Annual Mortgage Fraud Risk Report In-depth analysis of nationwide

risk as indicated by the

Interthinx® Fraud Risk Indices

22012 Annual

a SMARTER Approach To Risk

©2013. All rights reserved. FraudGUARD is a registered trademark of Interthinx, Inc., Interthinx is a registered trademark of Interthinx, Inc..

Executive Summary

This report highlights some of the most significant mortgage fraud risk trends based on analysis of loan applications processed in 2012 by the Interthinx FraudGUARD® system.

• The2012AnnualMortgageFraudRiskIndexvalueis150(n = 100), a 3 percent increase from2011’svalueof145.Thiscontinuesthegraduallyrisingtrendinfraudriskobservedover the past two years as markets begin to stabilize, inventories begin to shrink, and prices begin to increase.

• Therewasamarkedshiftinfraudriskfromwesttoeast,withsevenofthetop10stateslocatedintheeasternhalfoftheUS.Manyofthesestateswerehithardbymortgagefraudand foreclosures early in the boom years, and most are judicial foreclosure states where real estate sales activity was depressed before the “robo-signing” foreclosure abuse lawsuit was settled. The rise in fraud risk is an indicator that these markets may have hit a true bottom, since rising markets are more attractive to fraudsters seeking profits, and fraud is easier to commit when property values are increasing than when they are decreasing.

• DespitethedecreaseinfraudriskinthewesternUnitedStates,NevadaandArizona–perennialentrantsinthetopfive–arerankedasthe1stand3rdriskiest,respectively.Californiadroppedto6thplace–itsfirsttimefinishingoutofthetopfivesincetheinceptionoftheAnnualreportin2010–eventhoughitcontainseightoftheriskiestMetropolitanStatisticalAreas(MSAs)forEmployment/IncomeFraudRisk,sixofthe riskiestMSAsoverall,andfiveofthe25riskiestZIPcodes.

• Employment/IncomeFraudRiskisup7percentnationallyfrom2011andisparticularlyconcentrated in northern California, while Occupancy Fraud Risk declined 11 percent from one year ago, likely reflecting investors’ ability to use cash for purchases. Despite the decline in Occupancy Fraud Risk, investor loans remained significantly more risky than owner-occupied and second home loans.

• Purchaseloanapplicationswithloan-to-valueratios(LTVs)ofexactly20percentareextremelyriskywithaMortgageFraudRiskIndexof637.Itislikelythattheseloansareassociatedwithpiggy-backtypeloanswheretheborroweroriginatesaloanwithanLTV of 20 percent for simultaneous use as the down-payment for a loan with a second lender for 80 percent of the property value.

3Mortgage Fraud Risk Report 2012 Annualinterthinx.com 800.333.4510 [email protected]

Section 1: 2012 Mortgage Fraud Risk Hot Spots

Figure1showsthatthenationalMortgageFraudRiskIndexvaluefor2012is150,representinga 3.4 percent increase from the 2011 value of 146, and a 4 percent increase from the 2010 value of 144.

Figure 1 also shows the fraud risk index for each state, with risk decreasing from left to right. Illustrating the persistence of fraud risk over time within specific geographies, six of the top 10 riskiest states for overall mortgage fraud risk have been in the top 10 since 2010. Nevada, withaMortgageFraudRiskIndexvalueof233,remainsinthenumberonespotforthethirdconsecutive year, while Florida and Arizona return to round out the top three. Florida jumped from 3rd in 2011 to 2nd for 2012 with an index value of 219, while Arizona drops from 2nd to 3rdwithanindexvalueof205.AlsoreturningtothelistareConnecticut(in5thplace,upfrom9thlastyear),California(at6th,downfrom4thlastyear),Georgia(at7th,upfrom8thlastyear),andMichigan(at8th,downfrom6thlastyear).NewJersey(4th),Ohio(9th)andNewYork(10th)roundoutthetop10.

Nineofthe10stateswiththelowestMortgageFraudRiskIndexvalue–Kentucky,Montana,Iowa,NorthDakota,Mississippi,Maine,WestVirginia,Kansas,andSouthDakota–alsoreturnfromlastyear.Wyomingroundsoutthebottom10,replacingAlaska.Nineofthebottom10experiencedadoubledigitpercentagedecreaseinMortgageFraudRiskIndexvalues.Kentucky,up 10 percent from 2011, is the only state in the lowest risk category to have experienced an increase in risk.

Figure 1: 2012 Mortgage Fraud Risk Index by State

Mortgage Fraud Risk Index for the United States is 150

Mort

gag

e F

raud

Ris

k Index

2012

0

50

100

150

200

250

Nev

ada

Flo

rid

aA

rizo

naN

ew J

erse

yC

onn

ectic

utC

alifo

rnia

Geo

rgia

Mic

hig

anO

hio

New

Yo

rkIll

ino

isT

enne

ssee

Min

neso

taC

olo

rad

oP

enns

ylva

nia

So

uth

Car

olin

aO

reg

on

Haw

aii

Was

hing

ton

Mar

ylan

dD

elaw

are

Rho

de

Isla

ndW

isco

nsin

New

Ham

psh

ire

Ver

mo

ntLo

uisi

ana

Mas

sach

uset

tsT

exas

No

rth

Car

olin

aA

lab

ama

Uta

hO

klah

om

aN

ew M

exic

oV

irg

inia

Mis

sour

iIn

dia

naN

ebra

ska

Ala

ska

Ark

ansa

sId

aho

Ken

tuck

yW

yom

ing

Mo

ntan

aIo

wa

No

rth

Dak

ota

Mis

siss

ipp

iM

aine

Wes

t V

irg

inia

Kan

sas

So

uth

Dak

ota

42012 Annual

a SMARTER Approach To Risk

©2013. All rights reserved. FraudGUARD is a registered trademark of Interthinx, Inc., Interthinx is a registered trademark of Interthinx, Inc..

Table1liststhe10MSAswiththehighestfraudriskin2012,alongwiththeircorresponding2012 rank, 2011 rank, 2012 index values and percentage change in index value from 2011 to2012.ElCentro*CaliforniaistheriskiestMSAwithariskindexvalueof291,a16percentincrease from last year.

Onlythreestates–California,ColoradoandFlorida–arerepresentedinthislist.CaliforniacontainsthethreeriskiestMSAs–ElCentro,MercedandYubaCity–aswellasMadera-Chowchilla,ModestoandStocktonin6th,7thand8thplaces,respectively.Colorado,whichisonlythe14thriskieststate,hastwoMSAsrepresentedinthetop10:GrandJunctionin4thplace,andPuebloin9th.Thetop10isroundedoutbytheFloridametrosofMiamiandSebastian-Vero Beach.

2012 Rank 2011 Rank MSA 2012 Mortgage Fraud Risk Index

Percentage Change from

2011

1 8 ElCentro,CAMetro 291 15.7%

2 1 Merced,CAMetro 282 -13.5%

3 10 YubaCity,CAMetro 263 6.0%

4 26 GrandJunction,COMetro 252 23.7%

5 9 Miami-FortLauderdale-PompanoBeach,FLMetro 251 1.0%

6 23 Madera-Chowchilla,CAMetro 251 20.1%

7 3 Modesto,CAMetro 250 -10.6%

8 2 Stockton,CAMetro 247 -12.6%

9 27 Pueblo,COMetro 244 20.4%

10 54 Sebastian-VeroBeach,FLMetro 243 42.2%

United States 150 2.5%

*TheMSAtablesinthequarterlyandannualInterthinxMortgageFraudRiskReportsincludeonlythoseMSAswith sufficient loan applications for statistical significance. As a result, metros which do not have sufficient loan applicationstobelistedinthequarterlyreportscanexceedtherequiredthresholdwhendatafromallfourquartersarecombined,andhencecanbeincludedintheannualreport.ThemostnotableexampleisElCentro,whichistheriskiestMSAinthisreportdespitenothavingappearedinanyofthequarterlyreportsduring2012.

Sixofthe10riskiestMSAsforoverallmortgagefraudriskwerealsorankedinthetop10listin2011.TheseincludefiveofthesixCaliforniaMSAs–theexceptionbeingMadera-Chowchilla–andMiami,whichhashadastrongshowinginmostofthetop10tablesin2012’squarterlyreports.ThepersistenceoftheseMSAsinthetop10listdemonstrates the difficulty in reducing mortgage fraud risk once it has been established.

Table1:Top10RiskiestMSAsforMortgageFraudRiskin2012

5Mortgage Fraud Risk Report 2012 Annualinterthinx.com 800.333.4510 [email protected]

-21.5

-16.5

-21.9

-12.9

-11.8

-18.3

-31.3

-12.3

-21.3

-10.3

-13.3

-20.0

-13.2

-15.1

-30.1

26.532.9

55.8

22.9

26.9

12.9

18.7

30.7

34.6

17.6

18.0

48.4

20.4

30.2

13.2

21.1

-8.8

-4.7

-0.3

-5.6

-6.7

-5.0

-8.4

-8.1 3.5

7.8

1.3

4.7

7.0

0.4

1.2

-13.1

15.0

10 States with the largest Mortgage Fraud Risk Index increase between 2011 and 2012

10 States with the largest Mortgage Fraud Risk Index decrease between 2011 and 2012

Other

Section 2: Eastward Fraud Migration

In the previous section we observed the persistence of fraud risk hot spots, with seven of the10riskieststatesandsixofthetop10riskiestMSAsreturningfrom2011.Despitethis,underlying changes in risk are occurring as fraudsters adapt to changing market opportunities and conditions. One distinct trend is the eastward migration of fraud risk.

Figure2showsthestatelevelchangeintheMortgageFraudRiskIndexfromoneyearago and clearly illustrates the migration of fraud risk from west to east. The 10 states with the largest increase in fraud risk index values are shown in red; the 10 states with the largest decrease are shown in green. All of the states whose risk increased significantly are in the easternhalfoftheUnitedStates,ledbyNewJersey,NewYorkandLouisianawithincreases of56,48and35points,respectively.Mostofthestateswithlargeriskdecreasesareinthewest(theexceptionsareMississippiandArkansas),andthestateswiththelargestdecreasesareArizona(-31points),Utah(-30points)andNevada(-22points).Whilethedropinfraudriskin the west is certainly encouraging, close attention should be paid to the emerging risk regions in the eastern United States.

Figure 2: Change in Fraud Risk Index between 2011 and 2012, by State

62012 Annual

a SMARTER Approach To Risk

©2013. All rights reserved. FraudGUARD is a registered trademark of Interthinx, Inc., Interthinx is a registered trademark of Interthinx, Inc..

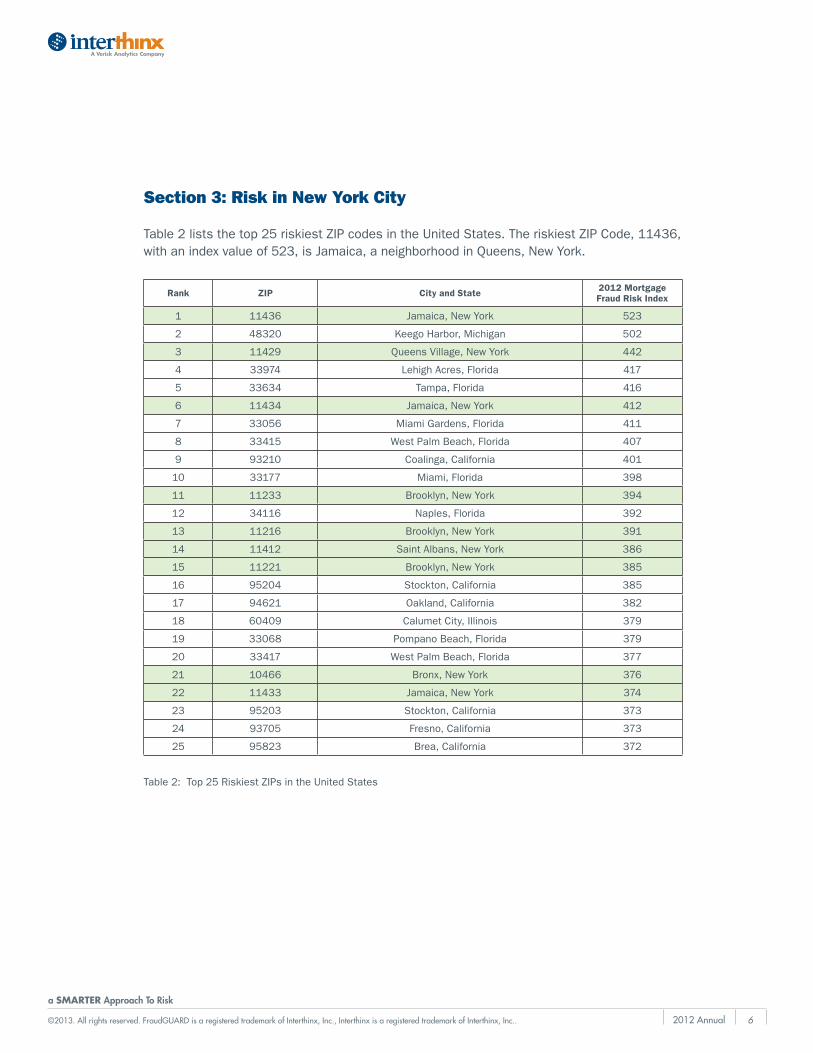

Section 3: Risk in New York City

Table2liststhetop25riskiestZIPcodesintheUnitedStates.TheriskiestZIPCode,11436,withanindexvalueof523,isJamaica,aneighborhoodinQueens,NewYork.

Rank ZIP City and State 2012 Mortgage Fraud Risk Index

1 11436 Jamaica,NewYork 523

2 48320 KeegoHarbor,Michigan 502

3 11429 QueensVillage,NewYork 442

4 33974 LehighAcres,Florida 417

5 33634 Tampa, Florida 416

6 11434 Jamaica,NewYork 412

7 33056 MiamiGardens,Florida 411

8 33415 WestPalmBeach,Florida 407

9 93210 Coalinga, California 401

10 33177 Miami,Florida 398

11 11233 Brooklyn,NewYork 394

12 34116 Naples, Florida 392

13 11216 Brooklyn,NewYork 391

14 11412 SaintAlbans,NewYork 386

15 11221 Brooklyn,NewYork 385

16 95204 Stockton, California 385

17 94621 Oakland, California 382

18 60409 Calumet City, Illinois 379

19 33068 PompanoBeach,Florida 379

20 33417 WestPalmBeach,Florida 377

21 10466 Bronx,NewYork 376

22 11433 Jamaica,NewYork 374

23 95203 Stockton, California 373

24 93705 Fresno, California 373

25 95823 Brea, California 372

Table2:Top25RiskiestZIPsintheUnitedStates

7Mortgage Fraud Risk Report 2012 Annualinterthinx.com 800.333.4510 [email protected]

Onlythreestatesaccountfor22ofthe25riskiestZIPcodes.TheseareNewYork,FloridaandCalifornia,whichaccountfornine,eightandsixZIPs,respectively.NewYork,withnineZIPs,isparticularlynoteworthy.AllnineareinNewYorkCityboroughs,withfiveinQueens,threeinBrooklynandoneintheBronx.ThispreponderanceofextremelyriskyNewYorkCityZIPcodesisparticularlysurprisingsinceNewYorkStateisonlythe10thriskieststate,andtheNewYorkMSAisonlythe47thriskiestmetrointhecountry.Thisfindingillustratesthatfraudriskisnotevenly distributed across large geographies, and lenders should be alert to emerging fraud risk at very granular levels.

Figure3illustratestheincreaseinoverallmortgagefraudriskinsouthernNewYorkStatefrom2011 to 2012. Although there are pockets of high risk in the northern portion, many of the areaswhereriskincreasedarelocatedonLongIsland,particularlyinandaroundQueens,andinareasthatexperiencedsignificantdamagefromHurricaneSandy.

Figure3:FraudRiskinNewYorkZIPsin2011and2012

0-100 101-200 201-300 301+

Mortgage Fraud Risk Index

2011 2012

82012 Annual

a SMARTER Approach To Risk

©2013. All rights reserved. FraudGUARD is a registered trademark of Interthinx, Inc., Interthinx is a registered trademark of Interthinx, Inc..

Section 4: Concentration of Employment/Income Fraud Risk in California

Figure 4 shows the percent change in the type-specific indices at the national level. The largestchangesareintheOccupancyFraudRiskIndex–down11percent–andintheEmployment/IncomeFraudRiskIndex,whichincreased7percent.Thesechangesarelikelydue to changes in the macroeconomic environment as investors shift from the buy-and-flip strategy of the boom years to a buy-to-hold for rental strategy, and as their purchases reduce available inventory, spur price increases and reduce affordability.

Figure 4: Changes in Fraud Risk Indices between 2011 and 2012

-15%

-10%

-5%

0%

5%

10%

Ove

rall

Pro

per

ty V

alua

tion

Iden

tity

Occ

upan

cy

Em

plo

ymen

t/In

com

e

Ch

an

ge f

rom

2011 t

o 2

012

Fraud Risk Index

9Mortgage Fraud Risk Report 2012 Annualinterthinx.com 800.333.4510 [email protected]

AsignificanttrendunderlyingtheincreaseinthenationalEmployment/IncomeFraudRiskbetween2011and2012istheconcentrationofEmployment/IncomeFraudRiskinCalifornia.AsillustratedinFigure5,riskwasgeographicallydispersedin2011,with10statesrepresentedinthetop10listforriskiestMSAsforEmployment/IncomeFraudRisk.Incontrast,California,witheightMSAs,dominatesthetop10in2012.Thisislikelydueto intense investor interest and purchase activity in distressed California markets, which is reducing available inventory, raising prices, and causing bidding wars that make homes less affordable, especially for first time buyers.

Figure 5: Number of the 10 Riskiest MSAs for Employment/Income Fraud Risk in each state, 2011 and 2012

0

1

2

3

4

5

6

7

8

9

10

AZ

CA HI

MO

NC NJ

SD TX

VA VT

Num

ber

of

MS

As

in T

op 1

0

State

2011

2012

102012 Annual

a SMARTER Approach To Risk

©2013. All rights reserved. FraudGUARD is a registered trademark of Interthinx, Inc., Interthinx is a registered trademark of Interthinx, Inc..

The10riskiestMSAsforEmployment/IncomeFraudRiskarelistedinTable3.Thetwonon-CaliforniaMSAsinthetop10–Burlington-SouthBurlingtonVermontandOceanCityNewJersey–showadecreaseintheirindexvalues.Despitea15percentdecrease,Burlington-SouthBurlington,at202,maintainsitsstatusastheriskiestMSAforEmployment/IncomeFraudRisk.OceanCityNewJersey,in5thplace,sawa5percentdecreaseinitsindexvalue.Incontrasttothesedecreases,alleightCaliforniaMSAsinthetable–Oxnard-ThousandOaks-Ventura,Napa,SanDiego-Carlsbad-SanMarcos,LosAngeles-LongBeach-SantaAna,SanJose-Sunnyvale-SantaClara,SanFrancisco-Oakland-Fremont,StocktonandRedding–experienced large gains, with most increases in excess of 10 percent from one year ago.

2012 Rank 2011 Rank MSA – Employment/Income Fraud Risk 2012 Index Percentage Change from 2011

1 1 Burlington-SouthBurlington,VTMetro 202 -15.3%

2 31 Oxnard-ThousandOaks-Ventura,CAMetro 189 31.3%

3 72 Napa,CAMetro 188 56.0%

4 15 SanDiego-Carlsbad-SanMarcos,CAMetro 188 21.2%

5 3 OceanCity,NJMetro 187 -5.2%

6 13 LosAngeles-LongBeach-SantaAna,CAMetro 184 16.9%

7 11 SanJose-Sunnyvale-SantaClara,CAMetro 174 5.8%

8 18 SanFrancisco-Oakland-Fremont,CAMetro 171 12.0%

9 17 Stockton, California 171 11.0%

10 43 Redding,CAMetro 170 26.9%

United States 117 7.4%

Table3:Top10RiskiestMSAsforEmployment/IncomeFraudRiskin2012

11Mortgage Fraud Risk Report 2012 Annualinterthinx.com 800.333.4510 [email protected]

The concentration of fraud risk in California is further illustrated in Figure 6, which shows theEmployment/IncomeFraudRiskforMSAsnationwide.Themajorityofthosewithveryhighrisk(definedasanEmployment/IncomeFraudRiskIndexvaluegreaterthan150)arelocated in California, where investor demand for rental properties has reduced available inventory and created double-digit year-over-year median price increases in many markets.

Figure6:Employment/IncomeFraudRiskin2012byMSA

150+Less than 100 100 - < 125Employment/Income Fraud Risk Index

125 - < 150

122012 Annual

a SMARTER Approach To Risk

©2013. All rights reserved. FraudGUARD is a registered trademark of Interthinx, Inc., Interthinx is a registered trademark of Interthinx, Inc..

0

50

100

150

200

250

300

$1K

- $

2K

$2 -

$3K

$3K

- $

4K

$4K

- $

5K

$5K

- $

6K

$6 -

$7K

$7K

- $

8K

$8K

- $

9K

$9K

- $

10K

> $

10K

Fra

ud

Ris

k In

dex

Borrower Monthly Income

Overall Risk

Employment/Income Risk

Section 5: Non-Geographic Indicators of Mortgage Fraud Risk

In addition to the geographic factors that have been the focus of previous sections, there are a number of non-geographic factors associated with loan applications that can provideactionableintelligence,includingloancharacteristics(e.g.,loanpurpose,loanamount),propertycharacteristics(e.g.,appraisedvalue,propertytype),andborrowercharacteristics(e.g.,occupancytype,income,creditscore).

In this section we examine the non-geographic indicators of mortgage fraud risk that have contributed to the rise in overall risk observed in 2012.

Figure7showsmortgagefraudrisktrendsassociatedwithborrowerincome.Bothoverallfraudrisk(blue)andEmployment/IncomeFraudRisk(red)increaseastheborrowerincomerepresentedontheloanapplicationincreases,withEmployment/IncomeFraudRiskexhibitingthestrongerincreasingtrend.Thisislikelyduetoborrowerincomebeingmisstated–eitherbytheborrowertogetqualified,orbyprofessionalsassociatedwiththetransactioninordertogettheborrowerqualifiedandtoearncommissionsontheclosedsales.

Figure 7: Overall and Employment/Income Fraud Risk vs. Borrower Monthly Income

132012 Annual

a SMARTER Approach To Risk

©2013. All rights reserved. FraudGUARD is a registered trademark of Interthinx, Inc., Interthinx is a registered trademark of Interthinx, Inc..

0

50

100

150

200

250

300

350

400

0 -

100K

$100

K -

$20

0K

$200

K -

$30

0K

$300

K -

$41

7K

$417

K -

$72

9.75

K

> $

729.

75K

Fra

ud

Ris

k In

dex

Loan Amount

Overall Risk

Property Valuation Index

Figure 8 illustrates the fraud risk as it relates to a borrower’s loan amount. The graph highlightstheoverallrisk(blue)andPropertyValuationFraudRisk(red)trends.Bothindices increase as the loan amount increases, which suggests that as the loan amount increases,mortgagefraudriskislikelytoincreaseaswell.BothoverallandPropertyValuation Fraud Risk almost double when comparing the lowest loan amount buckets to the highest buckets.

Figure 8: Overall and Property Valuation Fraud Risk vs. Loan Amount

142012 Annual

a SMARTER Approach To Risk

©2013. All rights reserved. FraudGUARD is a registered trademark of Interthinx, Inc., Interthinx is a registered trademark of Interthinx, Inc..

0

50

100

150

200

250

Inve

sto

r

Ow

ner

Occ

upie

d

Sec

ond

Ho

me

Mort

gage F

rau

d R

isk In

dex

Occupancy Type

WhiletheMortgageFraudRiskIndexvalueforinvestorloanshasdeclinedfrom310in2011to202in2012,asinvestorsusecashtoacquireproperties,thetrendofinvestorloanscarryinghigherrisklevels,firstnotedinthe2011InterthinxMortgageFraudRiskReport, continues. As shown in Figure 9, investor loan applications are significantly riskier, withaMortgageFraudRiskIndexvalueofaround200,comparedwithowner-occupiedandsecondhomeapplications,bothofwhichhaveaFraudRiskIndexvalueofaround150.

Figure 9: Mortgage Fraud Risk Index by Occupancy Type

152012 Annual

a SMARTER Approach To Risk

©2013. All rights reserved. FraudGUARD is a registered trademark of Interthinx, Inc., Interthinx is a registered trademark of Interthinx, Inc..

0

50

100

150

200

250

300

350

400

0 to

1%

5% t

o 6

%

10%

to

11%

15%

to

16%

20%

to

21%

25%

to

26%

30%

to

31%

35%

to

36%

40%

to

41%

45%

to

46%

50%

to

51%

55%

to

56%

60%

to

61%

65%

to

66%

70%

to

71%

75%

to

76%

80%

to

81%

85%

to

86%

90%

to

91%

95%

to

96%

> 1

00%

Mort

gage F

rau

d R

isk Index

LTV

Segmentationbyloan-to-value(LTV),thatis,theratiooftheloanamounttotheappraisedvalue of the property, reveals interesting new insights. Figure 10 shows that, in general, fraudriskincreasesasLTVincreases,fromanindexvalueofaround100forloanswithanLTVlessthan10percent,tojustover150forloanswithLTVsgreaterthan90percent.

However,thereisapronouncedspikeinfraudriskatLTVsofexactly 20 percent, where thefraudriskindexisalmost350.Infact,furthersegmentationbyloanpurposeshowsthattheextremelyhighriskisconcentratedinpurchaseloanapplicationswithanLTVof20percent,whichhaveanindexvalueof637.ItislikelythattheseloanswithLTVof20are associated with piggy-back type loans where the borrower originates a loan with an LTVof20andusesthatasthedown-paymentforaloanfor80percentofthevaluewitha second lender.

Figure 10: Mortgage Fraud Risk Index by LTV.

162012 Annual

a SMARTER Approach To Risk

©2013. All rights reserved. FraudGUARD is a registered trademark of Interthinx, Inc., Interthinx is a registered trademark of Interthinx, Inc..

Extended Forecast

The changes in geographic and type-specific fraud risks observed in this report reflect changes in the residential housing market. As economic conditions change, fraud schemes are adjusted to take advantage of current conditions. Although mortgage fraud riskremainshighinthewesternUnitedStates,riskineasternstates–particularlythosethatarebeginningtorecoverfromtherealestatebust–isrisingandlendersshould be alert to emerging fraud trends in these geographies in order to prevent fraud inapplicationsfromtranslatingintodelinquenciesanddefaultsinclosedloans.Lenderswould also be well advised to proactively consider how regulatory changes, such as the“qualifiedmortgage”rulewithitsemphasisonverificationofborrowerincomeandassets, will influence fraud schemes in the future.

17Mortgage Fraud Risk Report 2012 Annualinterthinx.com 800.333.4510 [email protected]

About the Interthinx Fraud Risk Indices

TheFraudRiskIndicesarecalculatedbasedonthefrequencywithwhichindicators of fraudulent activity are detected in mortgage applications processed by the Interthinx FraudGUARD®system, a leading loan-level fraud detection tool available to lenders and investors.

TheInterthinxFraudRiskIndicesconsistoftheMortgageFraudRiskIndex,whichmeasurestheoverallriskofmortgagefraud,andthePropertyValuation,Identity,OccupancyandEmployment/IncomeIndices,whichmeasuretheriskofthesespecifictypes of fraudulent activity.

TheMortgageFraudRiskIndexconsiders40+indicatorsoffraudulentactivityincludingpropertymis-valuation;identity,occupancyandemployment/incomemisrepresentation;non arms-length transactions; property flipping; straw-buyers; “silent seconds”; and concurrent closing schemes. The four type-specific indices are based on the subset of indicators that are relevant to each type of fraudulent activity.

EachIndexiscalibratedsothatavalueof100representsanominalleveloffraudrisk,avaluecalculatedfromtheoccurrenceoffraudulentindicatorsbetween2003and2007instates with low foreclosure levels. For all five indices, a high value indicates an elevated risk of mortgage fraud and each Index is linear to simplify comparison across time and location.

The Interthinx Indices are leading indicators based predominantly on the analysis of current loanoriginations.FBIandFinCENreportsarelaggingindicatorsbecausetheyarederivedprimarilyfromSuspiciousActivityReports(SARs),themajorityofwhicharefiledaftertheloans have closed. The time lag between origination and the SAR report can be several years. For this reason, the Interthinx Fraud Risk Indices’ top geographies and type-specific findingsmaydifferfromFBIandFinCENfraudreports.

182012 Annual

a SMARTER Approach To Risk

©2013. All rights reserved. FraudGUARD is a registered trademark of Interthinx, Inc., Interthinx is a registered trademark of Interthinx, Inc..

About the Interthinx Mortgage Fraud Risk Report

The Interthinx Fraud Risk Report represents an in-depth analysis of residential mortgage fraud risk throughout the United States as indicated by the Interthinx Fraud Risk Indices. Publishedquarterly,aspartoftheFraudRiskReport,InterthinxwillreportonthegeographicregionswiththehighestMortgageFraudRiskIndexaswellasthosewiththehighestPropertyValuation,Identity,Occupancy,andEmployment/IncomeFraudRiskIndices.TheInterthinxFraudRiskIndicestracktheserisksinallStates,Metropolitanareas,Countiesandcountyequivalents,throughouttheUnitedStates.

About Interthinx

Interthinx,aVeriskAnalytics(Nasdaq:VRSK)subsidiary,providesessentialproductsand services to mitigate risk in the mortgage and retail lending marketplace. Interthinx offerssolutionsinmortgagefraudandverification,propertyvaluation,compliance,qualitycontrol, loss mitigation, retail loan loss forecasting, and capital planning that are used by the nation’s top financial institutions. Interthinx helps its clients minimize risk, increase operational efficiencies, satisfy regulator demands, manage data verification, and remain compliant.Formoreinformation,visitwww.interthinx.comorcall1-800-333-4510.

MEDIACONTACT: DepthPublicRelationsTelephone:301-337-8477Email:[email protected]