2012 mtf savage.ppt - berrydunn initiatives shawn savage.pdf · shawn savage irs stakeholder...

TRANSCRIPT

IRS Initiatives

Date: November 8, 2012

Shawn Savage IRS Stakeholder Liaison

Tax Year 2012Tax Law Update

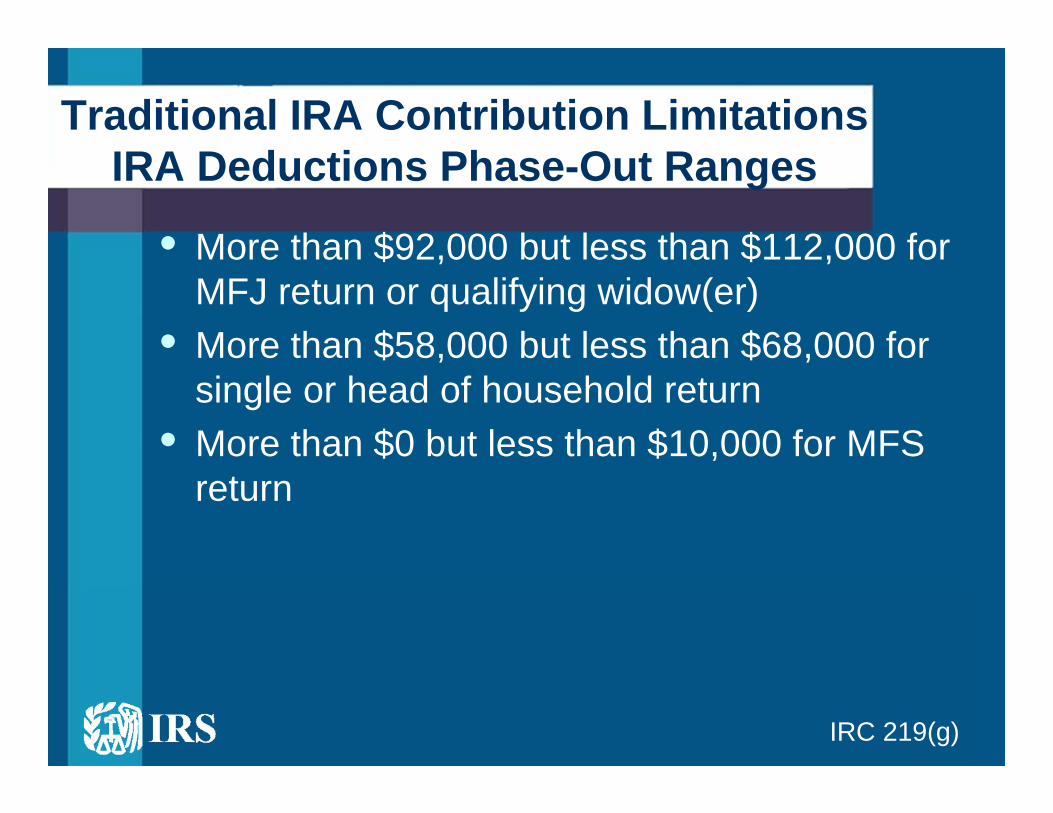

Traditional IRA Contribution LimitationsIRA Deductions Phase-Out Ranges

• More than $92,000 but less than $112,000 for MFJ return or qualifying widow(er)

• More than $58,000 but less than $68,000 for single or head of household return

• More than $0 but less than $10,000 for MFS return

IRC 219(g)

AMT Exemption Amount

$48,450

$33,705

$74,450

$45,000

$37,225

$22,500

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Exemption Amount

Single or Head ofHousehold

Married Filing Jointly orSurviving Spouse

Married FilingSeparately

Filing Status

20112012

Non-Refundable Credits & the AMT

• Credit for child and dependent care expenses• Credit for elderly or disabled• Mortgage interest credit• Education

IRC 26(a)(2)

Expired Tax Provisions

• Deduction for mortgage insurance premiums• Deduction for state & local sales taxes instead

of state & local income taxes• Tuition and fees deduction • Tax-free distribution from retirement accounts

for charitable purposes• 0% capital gains rate for DC Zone assets

Expired Tax Provisions

• Adoption credit • Credit for non-business energy property• Plug-in electric vehicle credit• Plug-in conversion credit• Alternative fuel vehicle refueling property credit• Indian employment credit

Expired Tax Provisions

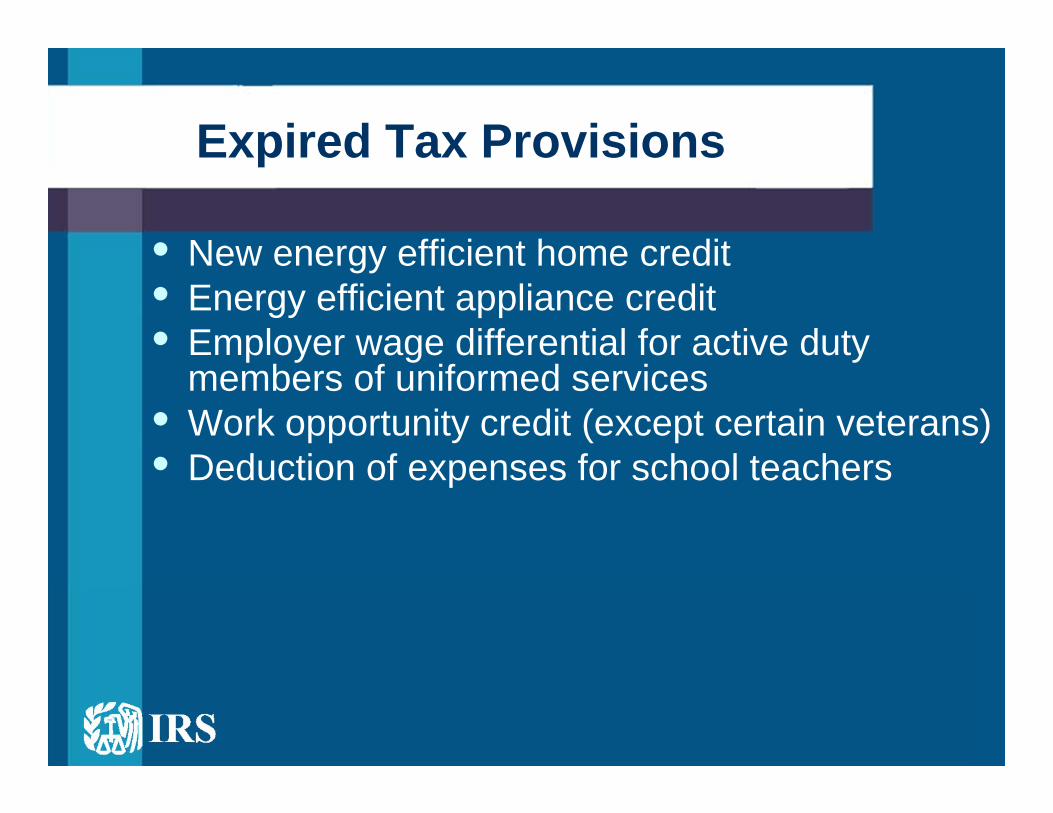

• New energy efficient home credit• Energy efficient appliance credit• Employer wage differential for active duty

members of uniformed services• Work opportunity credit (except certain veterans)• Deduction of expenses for school teachers

Reminders

• First-Time Homebuyer Credit, repayment continues this year

• Report ½ of 2010 Roth IRA conversions or rollovers on 2012 Form 1040

Update on New Rules for Federal

Tax Return Preparers

Phases of New Rules for Preparers

Phase 1PTIN Registration

Phase 2Competency Test

Phase 3Continuing EdRequirements

Phase 4Compliance &Enforcement

Must register annually

Must renew PTIN

PTIN valid calendar year

Since 01/01/11, must use PTIN on return; not SSN.

IRS urging preparers to test now (RTRP or EA)

Schedule using PTIN Account

Topics: tax law and Form 1040 prep

New starting 2012 for RTRPs and RTRP candidates

15-hours for RTRP candidates annually

CE hours from authorized providers only

Tax Compliance Check for all

Compliance letters and visits

Identifying those not in compliance

2014: Only certain authorized preparers can do 1040 prep.

1 2 3 4

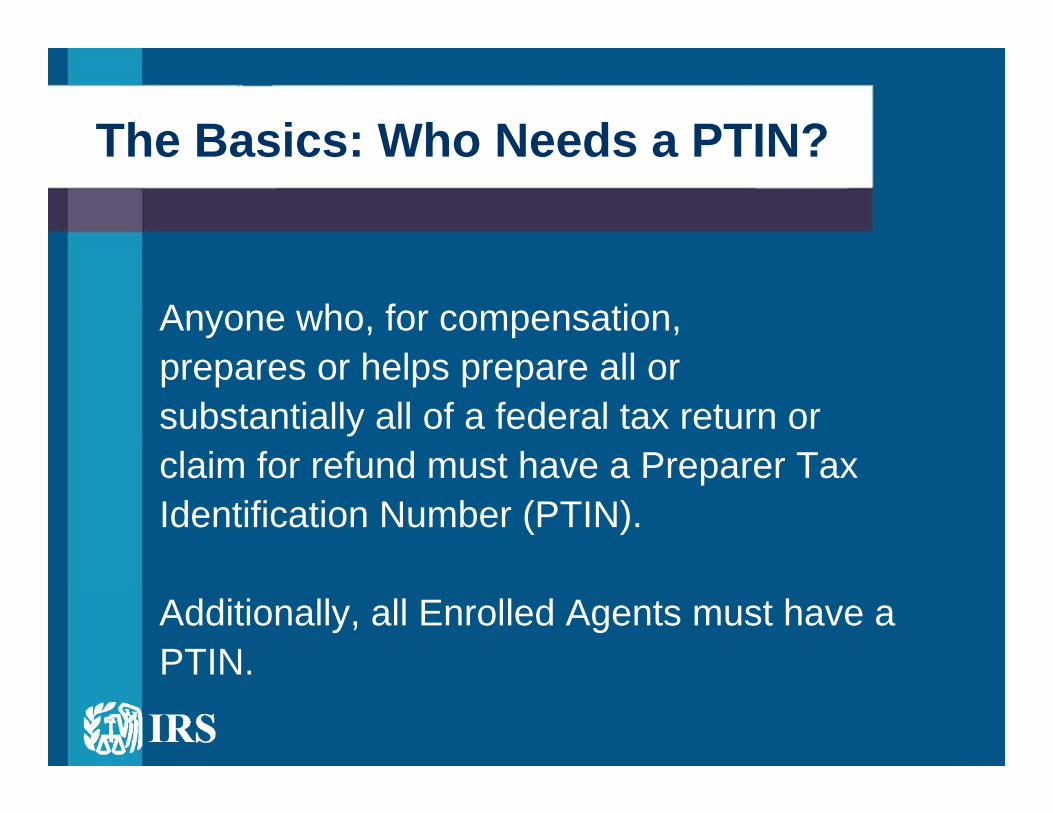

Anyone who, for compensation,prepares or helps prepare all orsubstantially all of a federal tax return orclaim for refund must have a Preparer TaxIdentification Number (PTIN).

Additionally, all Enrolled Agents must have aPTIN.

The Basics: Who Needs a PTIN?

The Basics: The PTIN

• All PTINs expire on December 31 and must be renewed annually

• Renewal period opens mid-October• First-time fee: $64.25; Renewal fee: $63• Go to www.irs.gov/ptin to register and renew• TIP: Do NOT wait until Dec. 31!

The Basics: The PTIN

TIP: You will always need your user ID and password to access your online PTIN Account.

• Forgot your log-in info? Click on the appropriate link on the log-in page for assistance:–Forgot User ID?–Forgot password?–Forgot or Cannot Access Email?

Identity TheftDon’t Be a Victim

How IRS and Tax Professionals CanPrevent Identity Theft and Assist

Taxpayers Who Are Victims

• Maintaining close security of IRS systems and proper protection of taxpayer information is a top priority for the IRS

• Protecting privacy and preventing identity theft helps to instil confidence and public trust in tax administration

IRS and Privacy

ID Theft Continued Major Problem

• Number one consumer complaint reported to FTC for past 12 years

• An average victim now spends 12 hours and $354 out of pocket to resolve crime

• Incidents related to government benefits–most common–more complex–more time and money to detect and resolve

Recognizing ID Theft

• Taxpayers may have awareness that they are• victims of ID theft in several ways:

–E-file return rejects because SSN used on another return

–IRS contacts taxpayer about reported income taxpayer did not earn

–Taxpayer begins receiving bills or notices for unauthorized purchases or actions

ID Theft Affect on Clients’ Taxes

• Scenario 1: Refund-related crime, Identity thief uses stolen SSN to file forged tax return and obtain refund early in the filing season

• Scenario 2: Employment-related crime, Identity thief uses stolen SSN to obtain employment

Combating Tax-Related ID Theft

• Goal: IRS strives to prevent identity theft and detect refund fraud before it occurs and assist taxpayers who are victims.

• IRS has developed a comprehensive identity protection program that uses a three-pronged approach–Prevention and detection–Protection–Victim assistance

IRS Prevention and Detection Efforts

• Using business filters and rules to analyze returns filed on ID theft victim accounts to ensure legitimate returns are accepted and false returns rejected

• Placing identity theft indicators on taxpayer accounts to track and manage identity theft incidents

• Identifying and investigating refund fraud

Business Filters

• Identify possible identity theft• Ensure only legitimate returns are processed• Flag questionable returns for manual review

to validate legitimacy• Reject fraudulent returns

ID Theft Indicators

• Prevent victims from facing the same problems every year

• Distinguish legitimate tax returns from fraudulent returns

• Identify and track tax-related identity theft problems

• Measure the problem, monitor victims’ accounts, and develop processes to resolve

ID Theft Indicators

• They reflect different types and risks of identity theft–Refund-related identity theft–Employment-related identity theft–Accounts with no filing requirement–Increased risk due to a lost item such as a

wallet

New Business Rules to Deter False Returns

• Suspension of fraudulent return detection, ID verification letter sent to filer –If unable to establish identity, return

archived without processing–If able (and no compliance issues found),

refund released

IRS Victim Protection Efforts

• Notifying taxpayers when identity theft has affected their tax accounts

• Sending a notification letter to a victim when an identity theft indicator is placed on the victim’s account

• Issuing victims Identity Protection PINs

ID Protection PIN

• IP PIN is a six-digit number assigned to taxpayers who:–Were identified as identity theft victims–Submitted required documentation–Had their account issues resolved

Key IP PIN Information

• The IP PIN is specific to the tax year• A new IP PIN is issued every year• The IP PIN should not be confused with the

electronic signature ‘self-select’ PIN• Allows legitimate return to bypass identity

theft filters• Prevents processing of fraudulent returns• Allows taxpayers to avoid delays in their

federal tax return processing

IRS Victim Assistance Efforts

• Develop specialized units quickly and efficiently resolve identity theft cases

• Provide more training for employees who assist ID theft victims

• Step up outreach and education so taxpayers can prevent and resolve tax-related ID theft issues quickly

Identity Protection Specialized Unit

• Central point of contact for taxpayers who are reporting their identities as stolen

• Toll-free: 800-908-4490• Monday - Friday, 7 a.m. - 7 p.m. local time• Taxpayers may self-report they are victims

before tax accounts are affected

Tax Pro Responsibilities

• Educate clients to safeguard personal information

• Advise to regularly check credit reports and other financial records

• Remind them the IRS does not initiate contact with taxpayers by email to request personal or financial information–Any type of electronic communication–text messages –social media channels

• Contact the IPSU• Contact financial institutions• Contact credit bureaus to place a fraud alert

and obtain free copies of credit reports• File police report with local law enforcement• Contact Federal Trade Commission, visit

www.consumer.gov/idtheft/index.html

Actions for ID Theft Victims

Online ID Theft

• Phishing via the phishing Web form• Malware by downloading malicious

executable code• Email via email (or money order)• Vishing via the faxback form• Stock via email (or wire transfer)

Receipt of Suspicious IRS-Related Communications

• Report all unsolicited email claiming to be from the IRS to [email protected]

• Go to IRS.gov, click on ‘Report Phishing’ on the bottom of web page

Issue Management Resolution System

What is IMRS?

• Provides mechanism for raising concerns–IRS policies, practices and procedures–Systemic problems

• Facilitates issue identification, resolution and feedback

Issue Submission

• Gather all information• Contact local stakeholder liaison staff

–Visit IRS.gov–Search keyword “stakeholder liaison”

Elevating an Issue

• Is it an IRS issue?• Is clarification needed?• Are policy or procedural changes needed?• How widespread is the issue?

Response and Resolution

• Direct response from Stakeholder Liaison• Changes to policy and practices • Expanded education and outreach• Monthly IMRS reports on IRS.gov

Search “IMRS” on IRS.gov

• Hot issues• IMRS monthly overviews• Industry issues quarterly report• Prior year issues sorted by subject• Stakeholder Liaison local contacts

Name: Shawn Savage, IRS Sr Stakeholder Liaison

Phone Number: 207-491-1888E-Mail Address: [email protected]

Contact information