2013 annual convention critical tax and valuation issues...

TRANSCRIPT

2013 Annual Convention

Critical Tax and Valuation Issues in Mergers and Acquisitions

Transactions

Corporate Counsel Section

2.5 CLE Hours

May 8-10, 2013 ♦ Cleveland

CONTRIBUTORS

Bruce D. Bernard, JD, CPA/ABV (Inactive) Attorney at Law Worthington, Ohio Mr. Bernard received his BA from Capital University and his JD from Capital University Law School. His professional memberships include the American Institute of Certified Public Accountants, Ohio Society of Certified Public Accountants, Columbus Bar Association, Ohio State Bar Association, Worthington Estate Planning Council, Columbus Bar Foundation (Fellow), and Worthington Chamber of Commerce. Mr. Bernard has been a licensed attorney since 1985. He is the principal of his firm, which he established after he retired from a nearly 30-year-long career as a CPA. Mr. Bernard concentrates his practice in the area of tax reduction planning. He counsels clients in the areas of buying and selling companies, business valuation, tax planning for businesses and individuals, estate planning, and entity structure. Mr. Bernard is a certified public accountant (inactive status). He is a highly sought-after, well-respected, and knowledgeable speaker on the subjects of tax and estate planning, business valuations, mergers and acquisitions, charitable giving, and business planning. Mr. Bernard has had over 50 articles published in national and local periodicals and has authored two books, Selecting the Right Form of Business: The Comprehensive Decision-Making Guide for the Business Advisor (Irwin Publishing 1996) and Selecting the Form of Business Entity, Analyzing LLCs and Other Entity Choices (Ohio State Bar Association, 1999, 2001, 2003). For additional information, please visit www.bbernardlaw.com.

Sandra J. Dickinson, PhD Sandra J. Dickinson, LLC Columbus, Ohio Dr. Dickinson received her JD from The Ohio State University Michael E. Moritz College of Law and her PhD from The Ohio State University. She is a member of the Ohio State Bar Association (Corporate Counsel Section (Section Council)). Dr. Dickinson has over 15 years of business law experience from startup through windup stages of the business life cycle. She has provided counsel and transactional services to both for-profit and nonprofit clients, doing business across the country regarding a broad range of matters, including formation, governance, business planning and feasibility analysis, corporate compliance, contract management, policies and procedures, risk management and insurance, documentation and information systems, qualified employee retirement plans, shareholder relations, and merger and acquisition. Dr. Dickinson has served as executive director of a nonprofit entrepreneurial education organization and taught numerous education law and business law courses for colleges and universities in central Ohio. As former in-house general counsel for an architecture firm, she has in-depth experience in dispute resolution in the construction law arena. Currently in solo practice, Dr. Dickinson provides outside corporate counsel services to businesses threatened by the “zone of insolvency.”

Timothy T. McDaniel, CPA/ABV, ASA, CBA Rea & Associates Dublin, Ohio Mr. McDaniel earned his BSBA from Bowling Green State University. He is the director of business valuations at his firm and specializes in business valuation and succession planning. Mr. McDaniel is a recognized leader in the business valuation field, having been involved in over 1800 valuation engagements and numerous merger and acquisition transactions. He also consults with family businesses on integrating family and business issues surrounding succession planning. Mr. McDaniel prides himself on using plain English to teach business owners the value of their most prized asset and how to increase that value. He is a certified public accountant and the author of the recently released book, Know and Grow the Value of Your Business: An Owner’s Guide to Retiring Rich. For additional information, please visit www.reacpa.com.

Critical Tax and Valuation Issues in Mergers

and Acquisitions Session # 501

Critical Tax and Valuation Issues in M&A Transactions: How to Get 10 to 100 Times Earnings on the Sale of Your Company and Pay No More Taxes Than Romney Bruce D. Bernard, JD, CPA/ABV (Inactive), Timothy T. McDaniel, CPA/ABV, ASA, CBA, and Sandra J. Dickinson, PhD I. Valuation Theory ............................................................................................................................... 1 II. Definition of Earnings—from the Most Narrow to the Expanded Definition .............................. 2 III. Rates of Return—Private Versus Public Companies .................................................................... 4 IV. Business Valuation Basics .............................................................................................................. 5 V. Maximizing Value ............................................................................................................................. 6 VI. Tax Strategies ................................................................................................................................. 7 VII. Timing ............................................................................................................................................ 8 Supplemental Material ....................................................................................................................... 13

Meyer Manufacturing, Inc. Case Study Facts/Assumptions ...................................................... 15 Form 1120: U.S. Corporation Income tax Return ....................................................................... 17 Form 1125-A: Cost of Goods Sold ................................................................................................ 23 Form 1125-E: Compensation of Officers ..................................................................................... 27 Schedule G (Form 1120): Information on Certain Persons Owning the

Corporation’s Voting Stock .................................................................................................... 29 Asset Purchase Agreement Proposed Terms .............................................................................. 31

Critical Tax and Valuation Issues in M&A Transactions • 1

Critical Tax and Valuation Issues in M&A Transactions: How to Get 10 to 100 Times Earnings on the Sale of Your Company and Pay No More Taxes Than Romney

Bruce D. Bernard, JD, CPA/ABV (inactive) Attorney at law

Worthington, Ohio

Timothy T. McDaniel, CPA/ABV, ASA, CBA Rea & Associates

Dublin, Ohio

Sandra J. Dickinson, PhD Sandra J. Dickinson, LLC

Columbus, Ohio

I. VALUATION THEORY

Establishing a benchmark.

A. What causes stocks to increase or decrease in public markets

1. External market factors.

2. Future expectations of the individual company.

B. Standard of value to use in the engagement.

1. Fair Market Value.

2. Synergistic or Investment Value.

2 • Critical Tax and Valuation Issues

C. What is being valued?

1. The value of the stock.

2. Certain assets, including intangibles.

D. It’s not always the best price that wins.

1. After tax proceeds.

2. How much seller’s financing.

3. Earn-out.

4. Nonfinancial issues.

E. Nonfinancial issues that may influence price paid for business.

1. Supply and demand of buyers.

2. The reason for selling the business.

3. Financing issues credit availability and interest rates.

II. DEFINITION OF EARNINGS—FROM THE MOST NARROW TO THE EXPANDED DEFINITION

A. Book income.

1. GAAP—generally accepted accounting principles.

2. GAAP—departures.

B. EBT—Earnings Before Taxes.

C. Taxable income.

1. Can be smaller or larger than EBT.

2. Tax deferral means tax deductions are greater than book deductions, but these eventually reverse.

3. Without temporary and timing differences, taxable income will generally be greater than EBT because of permanent differences of deductions not allowed for tax purposes.

4. Financial statements can be prepared on a tax bases, which is a GAAP departure.

Critical Tax and Valuation Issues in M&A Transactions • 3

5. Otherwise, taxable income normally does not show anywhere in the financial statements.

6. Schedule M1 on page 4 of the tax return (1120,1120S, or 1065) shows a

reconciliation of book income to taxable income.

D. EBIT—Earnings Before Interest and Taxes.

1. Interest is added back, but not finance charges.

2. This is the one that makes fun of the definition of earnings how the company

has financed the balance sheet.

E. EBITDA—Earnings Before Interest Depreciation and Taxes, or after

Enron, Earnings Before I Tricked a Dumb Auditor.

1. The noncash deductions of depreciation and amortization are eliminated from

the definition of earnings.

2. However, the companies cost to capital is not being considered in EBITDA and

sometimes EBITDA is and should be adjusted or CAPX.

3. The most common definition of earnings for middle market merger and

acquisition transactions.

4. There is normally little difference between EBT and EBITDA for service

companies, but the difference could be large for capital intense businesses.

Therefore, while the most popular definition, EBITDA can misleading to

determine value for capital intensive businesses if EBITDA is not adjusted for

capital expenditures.

5. Adjustments are normally not necessary for amortization because the

expenditures that generate amortizable assets are generally not repeated.

F. SDE—Seller Discretionary Earnings.

1. Compensation and fringe benefits to owners are added back.

2. Fair market value of rent paid for real estate owned by the owners should not

be added back.

3. Often used in smaller company deals.

4. Proprietorships are already adjusted for compensation of the owner since

salary can be paid to a proprietor; however, fringe benefits still need to be added

back.

4 • Critical Tax and Valuation Issues

G. Adjusted earnings.

1. Earnings are almost always adjusted in a transaction to put them in a better light for a perspective buyer—higher earnings means more value in a higher price.

2. Normalizing adjustments will be made to the true economic income of the company—see the discussion below.

3. Additional adjustments to reflect the synergy to a buyer or a field of buyers.

III. RATES OF RETURN—PRIVATE VERSUS PUBLIC COMPANIES

A. Large cap stocks have returned approximately 12-13 percent based on most studies.

1. This averages out to about 8 to 10 times earnings.

2. But, we see P/E ratios anywhere from say 4 to 100 times earnings, and companies that have never had positive earnings yet have a price quoted on the exchange.

3. P/E ratios are measured by the current price divided by the trailing 12 months earnings.

4. But, the market looks at the anticipated, including growth to set the price. So, if P/E ratios were expressed as the price divided by some type of future earnings number, we would see multiples more in the range of an average of 8-10 percent lower for higher risk large cap companies and higher for lower risk large cap companies.

B. Small cap publicly traded stocks.

1. Investment returns on average are about 2-5 percent higher for small cap publicly traded stocks as compared to large cap.

2. This converts to an average range of about a 14-18 percent return and P/E ratios of 6-7 times earnings.

C. Private.

1. Rate returns for privately owned companies will average in a range of 17-25 percent, which converts to 4 to 6 times earnings.

2. This assumes earnings are defined the same as they are for large and small cap publicly traded stocks, that is a trailing 12 months after tax book (GAAP) earnings.

Critical Tax and Valuation Issues in M&A Transactions • 5

D. Summary.

1. As you can see, the price expresses multiple of earnings will vary greatly depending on the definition of earnings- pretax, EBIT, EBITDA, SDE, and where the earnings are adjusted for normalization items and/or the synergy of the fire.

2. So, you can easily get 100 times earnings depending on how you define earnings—see example.

3. However, this seminar is not about manipulating earnings to get the multiple you want, but is about maximizing the value of your clients businesses and the price they received on an ultimate sale.

IV. BUSINESS VALUATION BASICS

A. Income approach to value.

1. Types of income approaches to value.

a. Capitalization of earnings or cash flows.

i. Used when future cash flows are relatively stable.

ii. Easiest to use and understand.

a. Discounted earnings or cash flow.

i. Requires a forecast of future years.

ii. Used when future cash flows or income in not stable.

2. Operating value is determined by dividing the proper benefit stream (cash flow or income) by a Discount or Capitalization Rate. The value of any purchased non-operating assets must be added to determine total value.

B. Asset approach to value.

1. What is book value?

a. May not represent true value of assets and liabilities.

b. Adjustments to fair market value from book value must be made.

2. Determine the value of the assets and liabilities on a fair market basis for the assets you are buying and if any of the assets being bought are non-operating assets.

3. If the income approach and market approach to value is lower than the asset approach, then consider performing a liquidation value.

6 • Critical Tax and Valuation Issues

C. Market approach to value.

1. Comparison to publicly traded securities.

a. Company should have significant sales.

b. Usually does not apply to mom and pop businesses.

2. Actual transactions of comparable companies.

a. Must be comparable in size and type of business operations.

b. Must determine the right earnings or cash flow stream.

c. Must account for differences in companies balance sheets.

d. Determine if comparable company transactions are synergistic verses financial transactions.

3. Market data sources.

a. Bizcomps Online.

b. Done Deals Data Base.

c. Pratt’s Stats.

d. Institute of Business Appraisers database.

e. Mergers & Acquisitions Magazine.

f. 10k’s (Edgar—Compact disclosure).

g. Trade publications.

V. MAXIMIZING VALUE

A. What benefit stream?

1. Historical earnings.

a. Can be used to project future earnings—“guide to the future.”

b. Adds “realism” to what would otherwise be a best guess.

c. No “logic” behind looking at past earnings.

d. Problems: random and non-recurring items, owner compensation, non-operating assets, report all income, etc.

Critical Tax and Valuation Issues in M&A Transactions • 7

2. Future earnings under present ownership.

a. Provides an indication of the current value of a firm based on the operating policies and strategies of management.

b. Less than complete information

3. Future earnings under future ownership.

a. Same as “future earnings under current ownership” with calculation based on new assumptions.

b. Is not “fair market value” but rather “investment value.”

B. Selling your company.

1. Maximum price is to a strategic buyer.

2. Usually public traded companies pay more.

3. Determine their rate of return.

4. Market data information.

5. Should start up to five years in advance.

6. Understand SWOT.

7. Clean, clear financial statements.

VI. TAX STRATEGIES

A. Major goals?

1. Take advantage of deferral and exclusion opportunities.

2. Maximize after-tax sales proceeds.

3. Maximizing deductions to buyer, to help you get what you want.

4. Maximizing capital gain as opposed to ordinary income.

5. Minimizing payroll and self-employment tax.

6. Avoiding double tax.

B. Keeping the company in a “saleable tax position.”

1. Choice of entity decisions.

8 • Critical Tax and Valuation Issues

2. Documenting under compensation.

3. Deferred compensation in non-qualified stock options.

4. Watch employment and non-competition agreements between the company and owners and determine what assets should be held inside versus outside the company.

5. Watch the tax impact of non-operating assets

C. Preliminary issues.

1. What is being sold?

2. Asset versus ownership interest/stock sale.

3. How long have you been an S corporation if you were once a C corporation?

4. Keep your options open and do not commit too early to a particular form of transaction or tax planning idea.

5. Can be used as a negotiating tool to get parties closer together on price.

6. Look for win-win opportunities in situations where the net benefit to one party is greater than the net cost to the other party.

D. Specific planning ideas.

See supplemental material.

VII. TIMING

The timing.

A. Timing is the single most important factor in selling or transferring your business, but how do you time the sale or transfer to your advantage? Many factors contribute to maximizing optimal timing such as economic conditions, industry trends, buyer activity, as well as your company’s performance and overall organization.

B. Examples of great timing.

1. Auto dealerships.

2. Dot coms.

3. IT consulting firms.

Critical Tax and Valuation Issues in M&A Transactions • 9

C. Examples of poor timing.

1. Auto dealerships.

2. Dot coms.

3. IT consulting firms.

D. Controllable factors.

Remember that a buyer of any business is really buying a stream of cash flows. The maximum price to them is when the future stream of cash flows will be at their highest and the risk levels associated with the Company are at the lowest levels.

The owner of the business can have some influence over many items. Setting a definitive strategy early assist the business owner to take advantage of the optimal timing for either selling or transferring their business.

1. Financial position of the company.

2. Management depth.

3. Facility conditions.

4. Effective systems in place.

5. Impeccable financial records.

6. Strengths and weaknesses of the company.

7. Customer concentrations.

8. Owners’ involvement.

9. Before owner is burned-out.

10. Planned retirement is best reason for selling.

E. External factors.

Are all beyond the control of the individual business owner. However properly recognizing the influence these factors will have on a sale or transfer will enable the business owner to either maximize the proceeds from a sale or minimize the costs of transferring the business.

1. Economic conditions.

2. Interest rates.

10 • Critical Tax and Valuation Issues

3. Tax implications.

4. Credit availability.

5. Stock market.

6. Industry changes and legislation.

7. Labor activity.

8. Buyer activity, including rollups.

F. Team member issues.

1. Do you have an organizational structure?

2. How do you rate your team members?

3. What frustrations do your team members have with their jobs?

4. How does the team rate your commitment to customer care?

5. What training do you do for your team?

6. What frustrations do you have with your team members?

G. Products and services.

1. Do you have any exclusive products?

2. How much of your sales revenue is derived from servicing your clients?

3. Have you done a product analysis?

4. Do you know your ROI by product line?

5. Do you track changes in your sales mix?

6. How do you cost your products?

7. What are the differentiating features of your products?

8. Does your pricing policy reflect the quality of your product and service compared to your competition?

9. Do you have a coherent marketing strategy?

H. Customer issues.

1. How often do your customers deal with you?

Critical Tax and Valuation Issues in M&A Transactions • 11

2. What proportion deal exclusively with you for the products and services you offer?

3. How important are your products to your customers?

4. Do you have a database of customers?

5. Do you have regular contact with your customers?

6. Does one large customer dominate your sales?

7. Have you done an analysis on your customers?

8. Have you calculated the lifetime value of a customer?

9. Why do customers deal with you?

10. What are your customers’ key frustrations with your business?

11. What is different about your product?

12. How many active customers do you serve?

13. How many of your customers were acquired in the last 12 months?

14. How effective is your advertising?

15. How effective is your team at converting leads to sales?

16. Which noncompetitive businesses serve your market place?

17. Do you do anything with non-converted leads?

I. Competitor issues.

1. How many local firms offer the same products or services as you?

2. How many do it in the same way as you?

3. Do bigger firms in your industry have any specific competitive advantages?

4. How much does it cost to set up a business in your industry?

J. Supplier issues.

1. What proportion of your purchases comes from your top three suppliers?

2. Do they also supply other firms in your area?

3. What proportion of their total output do you think you receive?

12 • Critical Tax and Valuation Issues

4. How important is your performance to your suppliers?

5. What are the positives and negatives of dealing with your key suppliers?

6. How easy would it be to change suppliers?

K. Environmental trends.

1. How has the competitive environment changed since you started the business?

2. What has caused this?

3. Will the changes continue, and what will be the effect on your business?

4. What opportunities and threats are there?

Critical Tax and Valuation Issues in M&A Transactions • 13

Supplemental Material

14 • Critical Tax and Valuation Issues

Critical Tax and Valuation Issues in M&A Transactions • 15

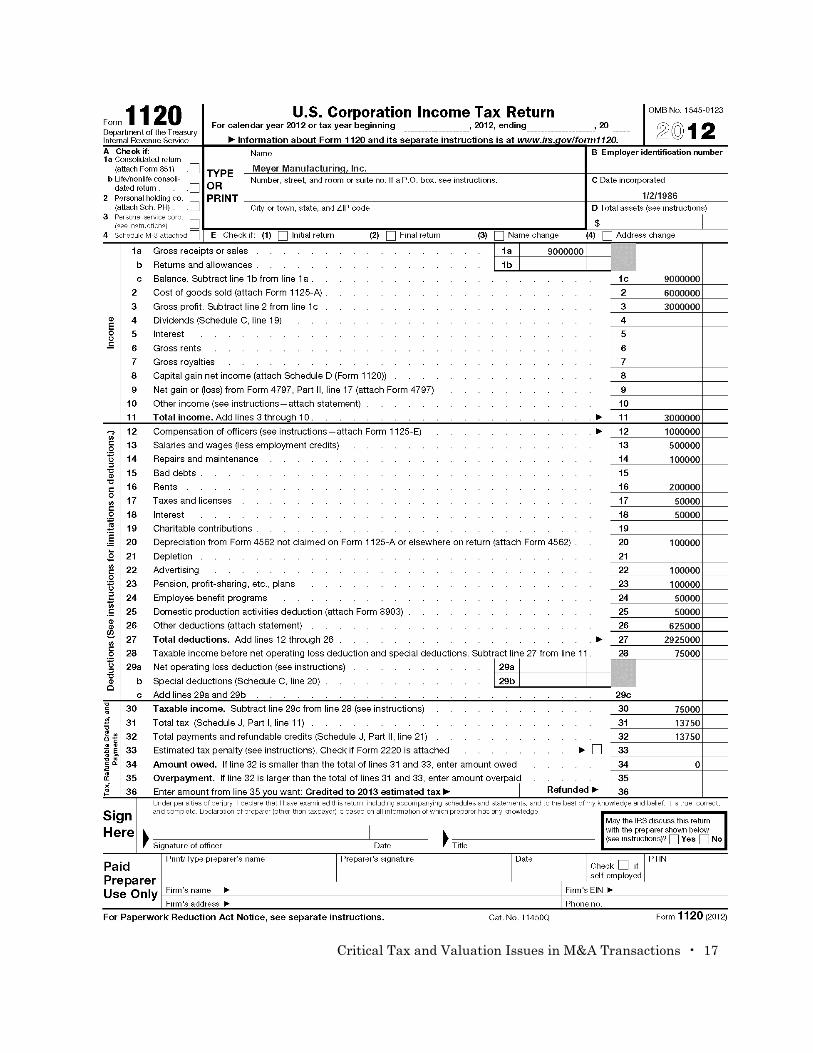

MEYER MANUFACTURING, INC. CASE STUDY FACTS/ASSUMPTIONS:

1. The company manufactures footballs (players too!)

2. Buyer distributes football equipment, some of which is manufactured by the buyer

3. Buyer and sellers have discussed a transaction for the last few years; although no one can remember who brought-up the idea first, so they have decided to for each party to draft a terms sheet and then meet to discuss

4. For the last couple years the owners have done little (real) work in the business, but still have significant contacts with customers and suppliers and are in the office and plant frequently

5. The Mortgages, notes, bonds payable in less than 1 year on the balance sheet is a line of credit which is at zero several times during the year

6. The tax returns for the last few years have been consistent with the 2012 1120—i.e., the company has taxable income of about $75,000, with the after tax amount of $61,250 retained in the company, sales increasing steadily, capital equipment of about $200,000 added yearly, steady working capital needs. . . .

16 • Critical Tax and Valuation Issues

Critical Tax and Valuation Issues in M&A Transactions • 17

18 • Critical Tax and Valuation Issues

Critical Tax and Valuation Issues in M&A Transactions • 19

20 • Critical Tax and Valuation Issues

Critical Tax and Valuation Issues in M&A Transactions • 21

22 • Critical Tax and Valuation Issues

Critical Tax and Valuation Issues in M&A Transactions • 23

24 • Critical Tax and Valuation Issues

Critical Tax and Valuation Issues in M&A Transactions • 25

26 • Critical Tax and Valuation Issues

Critical Tax and Valuation Issues in M&A Transactions • 27

28 • Critical Tax and Valuation Issues

Critical Tax and Valuation Issues in M&A Transactions • 29

30 • Critical Tax and Valuation Issues

Critical Tax and Valuation Issues in M&A Transactions • 31

ASSET PURCHASE AGREEMENT PROPOSED TERMS

Parties Seller: Meyer Manufacturing, Inc.

Buyer: BYZ Distributing

Assets Purchased All assets that are exclusive to the business (except those

specifically excluded), including: (e.g., (a) real property

lease, (b) tangible personal property, (c) inventory,

(d) work in progress, (e) accounts receivable, (f) goodwill,

(?)).

Excluded Assets Certain assets of Seller will not be transferred, including:

(e.g., cash, investments (?))

Assumed Liabilities Buyer will assume certain mutually agreed

liabilities/obligations of the Seller related to the business,

including: (e.g., Line of Credit, accounts payable (?))

Excluded Liabilities Other than the assumed liabilities, Seller will remain

responsible for other liabilities of the Seller.

Cash Purchase Price An amount of cash to be paid to the Seller at the Closing

will be equal to $_______________

- Earn Out ?

- Adjustments?

Financial Statement If different from the date of Closing, the effective date of

Effective Date financial statements forming the basis of the purchase

price will be ______.