2013 annual report - bank of commerce holdings

TRANSCRIPT

2013 Annual Report

April 10, 2014

Dear Fellow Shareholders, Customers and Friends:

As your new CEO, this is my first opportunity to write the shareholder letter for Bank of Commerce

Holdings, an organization that I have been passionate about since joining our Company in 2001.

I am pleased to report that 2013 was another successful year, and I can think of no better way to

start this letter than by expressing my profound and continued appreciation for the employees and

customers who make it possible for us to build shareholder value and serve our communities.

Financial Highlights for 2013:

• Net income of $7.9 million, a 7% increase over 2012

• Non-maturing core deposits grew by 11%

• Diluted earnings per share of $0.52 were 27% higher than the prior year

• Share price increased 24% over the prior year

The best way to enhance value is to build a great Company with outstanding people, high quality

products and services, excellent systems, quality accounting and reporting, and effective controls.

We strongly believe we are building a great Company for all of our highly valued shareholders.

Your Management Team and Board of Directors are committed to growing your Company and executing

on the opportunities before us. We have rebranded Roseville Bank of Commerce to Sacramento Bank

of Commerce, added a full service Small Business Administration Lending Division staffed by a group

of seasoned and highly talented bankers, and have entered the San Francisco Bay Area Homeowner

Association Deposit Market. As we venture into new products and markets, the foundation of our

Company continues to be Redding Bank of Commerce and the customers and community that are

served by our dedicated and loyal employees.

On behalf of all of us at Bank of Commerce Holdings, we thank you for your continued support. As

always I encourage your feedback and I invite you to contact me at any time.

Sincerely,

Randall S. EslickPresident & CEO

PRESIDENT’S WELCOME

Interest Income Net Interest IncomeProvision for Loan LossesNoninterest IncomeNoninterest ExpenseTotal Revenues Net Income Attributable to Bank of Commerce Holdings

$41,46528,950

9,4754,758

16,13846,223

$6,005

$42,478 33,08112,850

5,98618,68948,464

$6,220

$41,63134,155

8,9913,891

19,92745,522

$7,255

$40,33735,108

9,4006,593

21,63246,930

$7,416

$37,26133,783

2,7503,542

22,24140,803

$7,935

Total Assets Total Gross Portfolio Loans Allowance for Loan and Lease Losses Total Deposits Total Stockholders’ Equity

0.75%9.01%8.28%

12.06%13.31%

3.90%91.42%

1.92%1.14%1.86%

113.50%47.88%

0.69%6.50%

10.55%13.74%15.00%

4.03%93.41%

2.43%1.84%2.14%

159.73%47.83%

0.79%6.71%

11.76%15.28%16.53%

4.02%95.99%

2.68%1.85%1.82%

202.53%52.38%

0.78%6.66%

11.69%14.52%15.77%

3.99%95.39%

4.25%1.48%1.67%

347.40%51.87%

Average Common Shares Outstanding – basic Average Common Shares Outstanding – diluted Book Value Per Common Share Basic earnings per share attributable to continuing operations Basic earnings (loss) per share attributable to discontinued operations Diluted earnings per share attributable to continuing operations Diluted earnings (loss) per share attributable to discontinued operations Cash Dividends Per Common Share

8,7118,711$5.72$0.55$0.03$0.55$0.03$0.24

14,95114,951

$4.97$0.30$0.05$0.30$0.05$0.18

16,991 16,991

$5.33$0.34$0.03$0.34$0.03$0.12

16,34416,344

$5.66$0.41

$(0.01)$0.41

$(0.01)$0.12

14,94014,964

$5.86$0.52$0.00$0.52$0.00$0.14

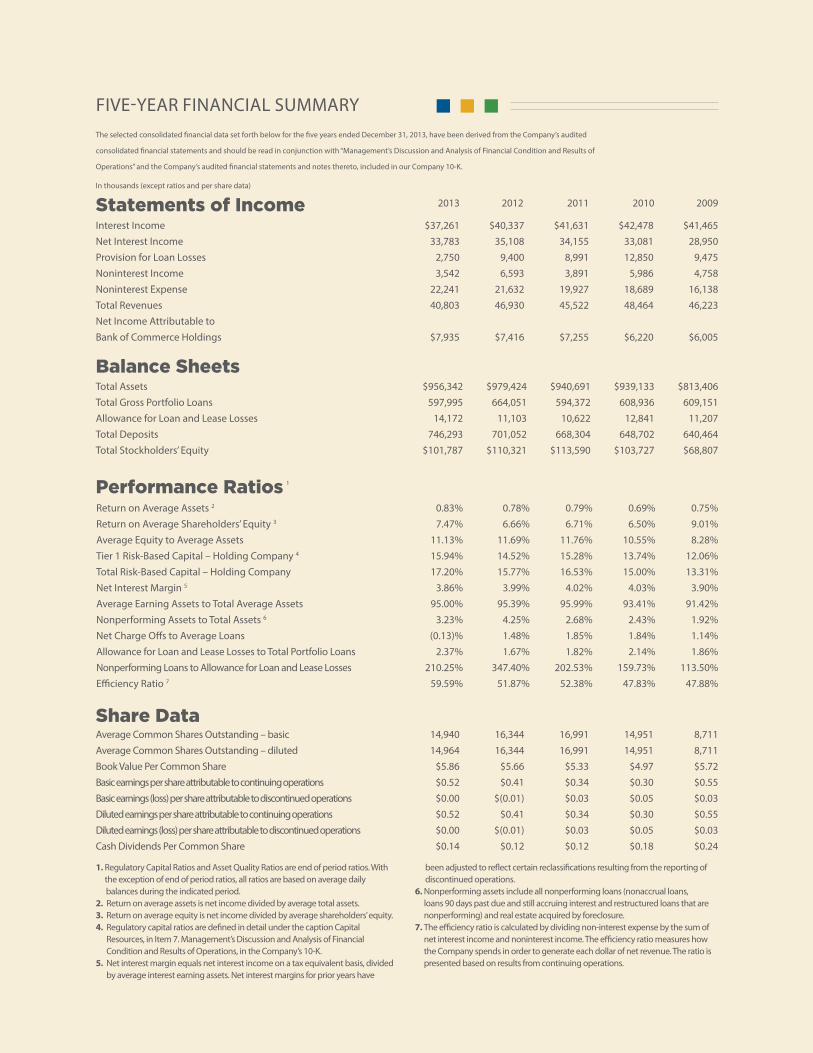

FIVE-YEAR FINANCIAL SUMMARY

Statements of Income

Balance Sheets

Performance Ratios

Share Data

The selected consolidated financial data set forth below for the five years ended December 31, 2013, have been derived from the Company’s audited

consolidated financial statements and should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of

Operations” and the Company’s audited financial statements and notes thereto, included in our Company 10-K.

1. Regulatory Capital Ratios and Asset Quality Ratios are end of period ratios. With the exception of end of period ratios, all ratios are based on average daily

balances during the indicated period.2. Return on average assets is net income divided by average total assets.3. Return on average equity is net income divided by average shareholders’ equity.4. Regulatory capital ratios are defined in detail under the caption Capital

Resources, in Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations, in the Company’s 10-K.

5. Net interest margin equals net interest income on a tax equivalent basis, divided by average interest earning assets. Net interest margins for prior years have

been adjusted to reflect certain reclassifications resulting from the reporting of discontinued operations.6. Nonperforming assets include all nonperforming loans (nonaccrual loans,

loans 90 days past due and still accruing interest and restructured loans that are nonperforming) and real estate acquired by foreclosure.

7. The efficiency ratio is calculated by dividing non-interest expense by the sum of net interest income and noninterest income. The efficiency ratio measures how the Company spends in order to generate each dollar of net revenue. The ratio is presented based on results from continuing operations.

$813,406609,151

11,207640,464$68,807

$939,133608,936

12,841648,702

$103,727

$940,691594,372

10,622668,304

$113,590

$979,424664,051

11,103701,052

$110,321

$956,342597,995

14,172746,293

$101,787

0.83% 7.47%

11.13% 15.94% 17.20%

3.86% 95.00% 3.23%

(0.13)% 2.37%

210.25% 59.59%

Return on Average Assets 2

Return on Average Shareholders’ Equity 3

Average Equity to Average Assets Tier 1 Risk-Based Capital – Holding Company 4

Total Risk-Based Capital – Holding CompanyNet Interest Margin 5

Average Earning Assets to Total Average Assets Nonperforming Assets to Total Assets 6

Net Charge Offs to Average LoansAllowance for Loan and Lease Losses to Total Portfolio Loans Nonperforming Loans to Allowance for Loan and Lease Losses Efficiency Ratio 7

2013 2012 2011 2010 2009

In thousands (except ratios and per share data)

1

Five Year Total Core Deposits(in thousands)

2009 2010 2011 2012 2013

$300,836$339,808

$374,948$415,589

$460,819

Five Year Net Income Available to Common Shareholders

(in thousands)

2009 2010 2011 2012 2013

$5,063 $5,280$6,312

$6,536$7,735

Five Year Allowance for Loan & Lease Losses Funding

(in thousands)

2009 2010 2011 2012 2013

$9,475

$12,850

$8,991$9,400

$2,750

FINANCIALS AT A GLANCE

Five Year Return on Average Shareholders’ Equity

2009 2010 2011 2012 2013

9.01%

6.50% 6.71% 6.66%7.47%

Five Year History Stock Price

2009 2010 2011 2012 2013

$5.28

$4.25

$3.35

$4.60

$5.71

Five Year Return on Average Assets

2009 2010 2011 2012 2013

0.75%0.69%

0.79% 0.78% 0.83%

Joeseph Q. Gibson Director / Chairman of CRA Committee

BOARD OF DIRECTORS

Jon W. Halfhide Vice-Chairman of the Board / Chairman of ALCO Committee and Executive Compensation Committee

Gary R. Burks Director / Chairman of Nominating and Corporate Governance Committee

Orin N. BennettDirector / Chairman of Loan Committee

Lyle L. TullisChairman of the Board/ Chairman of Executive Committee and Long Range Planning Committee

Terence J. StreetDirector

Linda J. MilesBank Director

Randall S. EslickPresident and Chief Executive Officer, Director

David H. ScottDirector / Chairman of Audit and Qualified Legal Compliance Committee

CUSTOMER PROFILE

Thirty years ago, we were in need of a local bank that would take a more personal

interest in our growing business. Through the years, Redding Bank of Commerce has

supported our growth and has become a trusted and loyal partner.”

“

Nicole Rayl, Frozen Gourmet, Inc.

Below: Bill Kohn, President; Daphne Kohn, CFO; Nikki Rayl, VP Administration; Rob Kohn, VP Operations

Amber YoungSBA Loan Specialist

Ken FerreiraSVP/SBA Lending Division Manager

We have put together a team of experienced

SBA lending professionals with over 100 years

of combined industry experience who are

highly committed to excellence. Our objective

is to become a premier provider of small

business financing using the U.S. Small Business

Administration’s 7(a) and 504 loan programs

by recognizing the specific needs of the small

businesses we serve and providing best in class

service to our customers.”

Roseville Bank of Commerce has been my business

bank for Discovery Door Inc. for 10 years now.

Over that time they have worked with us through

good and bad economic years, never losing sight

that we were a client as well as an intricate part of

their success. Recently we have engaged with their

new SBA division in refinancing our building and

financing a new construction project. The SBA staff

has certainly added a new dimension to what is

already an outstanding financial institution.”

SBA LENDING

In 2013 Redding Bank of Commerce expanded its commercial lending platform to include a dedicated

SBA Lending Department. While Redding Bank of Commerce has participated as a Preferred Lender with

the U.S. Small Business Administration since 1993, the formation of a dedicated SBA lending department

enhances the Bank’s ability to increase its lending opportunities to small businesses. This department will

offer a full range of U.S. Small Business Administration program loans focusing on the origination of 7(a),

Express and 504 loans.

Ken Ferreira, Senior Vice PresidentSBA Lending Division Manager

Kevin Wilsey, Discovery Door, Inc. and Highland Ranch, LLC

Penny JohnsonVP/SBA Operations Manager

Mike McGraneVP/SBA Business Development

Rich StefaniVP/SBA Business Development

Bob PuccinelliVP/SBA Business Development

Elaine PowellSBA Loan Specialist

Sue GlassVP/SBA Business Development

Jeff GreensteinVP/SBA Business Development

“ “

COMMUNITY REINVESTMENT

IN 2013, WE DONATED A TOTAL OF $91,885

• $5,000 of which were in scholarships given to high school students.

• Approximately $69,000 benefited the Redding area.

• Approximately $23,000 benefited the Sacramento area.

1,838 HOURS OF COMMUNITY DEVELOPMENT VOLUNTEER ASSISTANCE WERE PROVIDED BY OUR BOARD OF DIRECTORS, EXECUTIVE TEAM AND OUR STAFF TO 55 DIFFERENT ORGANIZATIONS.

• 1,378 hours benefited the Redding area.

• 460 hours benefited the Sacramento area.

This year Redding Bank of Commerce and Shasta

Head Start have joined forces to educate and

empower families to receive the maximum allowable

tax refund through Earned Income Tax Credit (EITC).

Together we conducted a simple survey that identified

178 families who were unaware of EITC, and who could

potentially receive thousands of dollars each based on

earned income and family size.

As a result, Redding Bank of Commerce with the

assistance of Diane M. Moore, EA, and Shasta

Head Start launched an education effort to

support families in utilizing the tax filing software

in order to receive the full tax benefit obtainable.

Redding Bank of Commerce provided training

to approximately 50 Shasta Head Start staff

in budgeting, credit repair and identity theft.

Subsequently Shasta Head Start is offering these

trainings free of charge to enrolled families in

Shasta, Siskiyou and Trinity Counties.

Together we can make a difference.

Head Start Partnership

Education and Testing Enrichment

Program for Anderson Middle School

Mrs. Ruth Copeland formulated a project that uses

computer tablets to help teach the nationwide

Common Core Standards to her fifth grade class. The

program will cover a wide array of subjects such as

mastery of math facts, financial literacy, and access

to online text books. It will also bring more fun to

learning in the classroom. Redding Bank of Commerce

is pleased to have provided a grant to purchase tablets

for her students to share as the project gets underway

this year.

GIVING BACK

Carla Clark, Executive Director; Jacquie Arends, Vice President Redding Bank of Commerce; Linda Cole, Deputy Director; Randi Brickey, Family Services Manager

Education and Testing Enrichment

Program for Anderson Middle School

Senior Vice PresidentsMario CallegariCasey FreelandDavid GonzalesRobert MatrangaDonna MooreDale OrchardBobby Ranger

Vice PresidentsJacqueline Arends Tammi ArrowsmithKatherine BreadonAllen FelsenthalLynnann FosterSteven HampDeni JauchJudy Johnson

Vice Presidents (continued)

Sherry MarshallLeona McCoachTammy ParkerKaren Perry Jason PetersonJosh SandersonPhilip Saska Andrea Schneck Candace SpangleDerek TaffDaniel TaylorBrenda TruettRobert TurnerBlake WernerAllan WesternCheryl WhitmerLynn Vasquez

Assistant Vice PresidentsGregory BambinoTania GunariBecky LooperJason Luther Kendra Nelson Farm Saechin Alec SkellyJaime Taylor Robin Williams

OfficersChristy Davis

Randall S. Eslick – President and Chief Executive OfficerSamuel D. Jimenez – Executive Vice President Chief Operating Officer and Chief Financial OfficerRobert H. Muttera – Executive Vice President Chief Credit OfficerPatrick J. Moty – Executive Vice President Regional President, Redding MarketRobert J. O’Neil - Senior Vice President Regional President, Sacramento MarketDebra A. Sylvester – Senior Vice President Chief Administrative OfficerBlake W. Pelletier – Senior Vice President Chief Information Officer

OFFICERS

Senior Vice PresidentsAllan Bernhard Richard ChackelKenneth FerreiraPamela HalperinScott HolthausAlan Koski

Vice PresidentsSusan GlassJeffrey GreensteinWilliam Hoover Penny JohnsonMichael McGraneRobert PuccinelliCathy Smallhouse Richard Stefani

Assistant Vice PresidentsCarleen AciaLoretta Alves Diane EbbittSandra GutierrezRobert LimDeborah MortimeyerBetina Schessow

Redding Bank of Commerce

Sacramento Bank of Commerce

Executive and Senior Management Team

Raymond James Financial

John T. Cavender555 Market StreetSan Francisco, CA 94105(800) 346-5544

Sandler O’Neill + Partners, LP.

Brian Sullivan1251 Avenue of the Americas, 6th FloorNew York, NY 10022(212) 466-8022

McAdams Wright Ragen, Inc.

Joey Warmenhoven1211 SW Fifth Avenue, Suite 1400Portland, OR 97204(866) 662-0351

Stifel Nicolaus

Perry Wright1255 East Street, Suite 100Redding, CA 96001(530) 244-7199

FIG Partners

Mike Hedrei1175 Peachtree Street NE #100Colony Square, Suite 2250Atlanta, GA 30361(212) 899-5217

For questions regarding your registered shareholder account, contact:Registrar and Transfer CompanyAttn: Investor Relations10 Commerce DriveCranford, NJ 07016(800) [email protected]

Bank of Commerce Holdings1901 Churn Creek RoadRedding, California 96002(800) 421-2575bankofcommerceholdings.com

Sacramento Bank of Commerce1504 Eureka Road, Suite 100Roseville, California 95661(916) 772-0131sacramentobankofcommerce.com

Redding Bank of Commerce1177 Placer StreetRedding, California 96001(530) 241-2265reddingbankofcommerce.com

1951 Churn Creek RoadRedding, California 96002(530) 224-3333reddingbankofcommerce.com

3455 Placer StreetRedding, California 96001(530) 243-6100reddingbankofcommerce.com

PURCHASES & SALES

CONTACT

Bank of Commerce Holdings(NASDAQ Symbol: BOCH)