2014 jp morgan-taylor fry general insurance barometer · see page 185 for analyst certification and...

TRANSCRIPT

www.morganmarkets.com

Australia Equity Research 13 January 2015

2014 J.P. Morgan Taylor Fry General Insurance Barometer

Direct Underwriters, Reinsurers and Brokers

Insurance

Siddharth Parameswaran AC

(61-2) 9003-8629

Alvin Liu

(61-2) 9003-8622

J.P. Morgan Securities Australia Limited

See page 185 for analyst certification and important disclosures, including non-US analyst disclosures. J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

This is the result of a joint research effort between J.P. Morgan and Taylor Fry.

Deloitte

Taylor Fry

Kevin Gomes

(61-2) 9249-2918

Sharanjit Paddam

(61-2) 9249-2914

Joshua Jaroudy

(61-2) 9249-2934

____________________________________

2

Australia Equity Research 13 January 2015

Table of Contents

Survey Description ...................................................................3

Executive Summary .................................................................4

Macro backdrop for Australian insurers ................................6

What history / the survey say about growth ........................ 17

The Impact of Technology on Insurance .............................. 30

The Political Impact of Climate Change on Insurers ........... 36

Alternative Capital .................................................................. 40

Survey Participants ................................................................ 43

3

Australia Equity Research 13 January 2015

Survey Description

This is the third edition of The Barometer, a joint effort between J.P. Morgan and

Taylor Fry. The publication continues from 19 editions of the J.P. Morgan Deloitte

General Insurance Survey, the last of which was published in 2012, for the year to

2011, with the first edition of the Barometer published the following year.

The 2014 J.P. Morgan Taylor Fry General Insurance Barometer provides a detailed

overview of the current state of the Australian general insurance industry and the

industry’s expectations. The report conveys analyses on the key elements of the

industry from the perspective of direct underwriters, reinsurers and brokers,

including:

detailed product information for the current period and industry expectations for

the next two years, covering issues such as premium rate trends, capacity

changes, claims trends, loss and expense ratios

perceptions of product profitability

distribution trends

practitioner views on key issues affecting the industry and particular classes

brokers’ perceptions of underwriters.

As has been our longstanding custom, we have also provided editorial comments

from J.P. Morgan and Taylor Fry on key industry issues which serve as a

commentary on industry developments to complement the survey results and

respondent feedback.

Sources of Information

All information in this report is sourced from a survey of the major underwriters,

reinsurers and brokers in the Australian general insurance industry, along with

certain APRA data. A complete list of participating companies is contained at the end

of this report.

The survey is the 22nd

consecutive data collection and accordingly there is now a

substantial body of trend data available, and many of the comments and observations

in the report have been drawn from this information.

Acknowledgments

This report has been produced with the support of the Australian insurance industry.

The insurance industry’s support has been generous and is greatly appreciated.

The J.P. Morgan and Taylor Fry teams hope you find this a valuable reference.

4

Australia Equity Research 13 January 2015

Executive Summary

The key themes to emerge from the 2014 survey and our analysis are outlined below.

Another great set of combined ratios…but as good as it gets

The 2014 year saw very strong combined ratios for the insurance industry, primarily

due to the impact of previous rate increases, a soft period for natural peril claims and

a continuation of reserve releases, though at reduced levels. Survey respondents

reported overall combined ratios of 87% in 2014 – same as in 2013. This was

matched by a Direct Insurer APRA RoE of 18%, flat on the 2013 level. For the

straight domestic lines that we cover in the survey, the combined ratio improved to

86% from 89% in 2013. This is supported by very strong results in householders,

offset by some deterioration (though still good results) in motor, and tough trends

again in NSW CTP. In the commercial classes, the combined ratio was 91%, a slight

deterioration from 2013 (90%). Reserve release continued in both commercial and

personal lines, although at a reduced rate compared to 2013. The COR trends in 2014

were better than the industry expected in the 2013 survey (92%).

Premium rate pressures are strong, with outlook quite weak

Participants said that domestic class rates slowed to 2% (nominal), below claims

inflation of 3%. Domestic class rates were expected to slow further in 2015.

Householders in particular slowed from 5 years of double digit rises from 2009 to

4% in 2014, with more softness expected going forward. This class had by far been

the biggest driver of growth in premium in the last few years, so its slowdown should

leave a hole in GWP growth. In commercial lines, rate trends were much weaker as

well (-6% reduction overall on weighted average basis, on largely an inflation

adjusted basis) – significantly less than the flat result expected in the 2013 survey.

We note that underwriters recorded better rate results than brokers – which may

reflect brokers focusing on 30 June, top end results. Fire/ISR showed very soft trends

for both underwriters and brokers - averaging -12%. The industry is expecting

negative commercial rate trends for both 2015 and 2016.

Claims trends – claim size inflation continuing at moderate levels, frequency

favourable again

For both domestic lines and commercial lines, inflation in 2014 was at similar levels

overall to 2013 (3% and 4%, respectively). The only class showing some claim size

inflation was workers compensation (both WA and in TAS/ ACT / NT). The outlook

is reasonably similar. Frequency trends in most classes were favourable in 2014 (0%

in domestic lines, -3.2% in commercial lines), although both NSW CTP and D&O

showed some increases. Whilst inflation / frequency trends are subdued, some

insurers expressed concern around the ability to maintain margins in an environment

of premium pressures, and low yields on investment income.

Top concerns for the insurance industry

69% of underwriters in the survey identified competition /rates / capacity as a key

concern (up from 2nd spot last year where it was behind regulation). This was

followed by 50% identifying technology as a key concern (double the figure in

2013). Regulation and staff development tied for 3rd place with 38%.

75% of insurance brokers worried about an excessively competitive rates

environment, up from 43% last year. 63% indicated concerns regarding staff

retention, also up on last year.

Reinsurers flagged regulatory issues as their key concern, followed by excess capital

and competition in the market.

5

Australia Equity Research 13 January 2015

Pa

rt 1

: E

dito

ria

l C

om

me

nts

6

Australia Equity Research 13 January 2015

Australia’s economic

environment had been a relative

‘safe haven’ compared to global

peers – but that may be set to

change

The J.P. Morgan economist’s

base case for Australia is for

below trend growth – but still

positive for the 24th year in a row.

We note history suggests that the

end of mining booms are often

associated with recessions

Macro backdrop for Australian insurers

Siddharth Parameswaran, Alvin Liu, J.P. Morgan

The economic environment since the ‘global financial crisis’ (GFC) of 2008/2009

proved to be one of low global growth prospects, but without the extreme downside

economic outcomes feared. Australia had been a relative outperformer when

compared against other “developed” economies although the prospects going

forward may be different with the US and UK rebounding and Australia facing the

prospects of falling commodity prices, and considerably reduced business

investment.

From a global perspective, 2014 saw modest rates of economic growth in developed

economies such as the US and UK but weak growth in Europe. Europe continues to

show uncertainty with the initial recovery seen from Mar13 to Mar14 appearing to

have plateaued between Mar14 to Sep14. With weak growth in Europe our

J.P.Morgan economists expect the ECB to announce a €500m sovereign QE program

at its next meeting on 22 January 2015, which may be able to stimulate growth going

for CY151. Unemployment rate for Europe remains high at 9.6%, although below its

peak of ~10% for the Jun13 quarter. The U.S. appears to be recovering, showing real

GDP growth of 2.2% for CY14, which is in line with their long term average and

unemployment has improved significantly from ~10% in Dec-09 to ~6% in Jun-14.

Similar positive trends have also been observed for UK. Figure 20 - Figure 21.

Australia arguably faced fewer concerns than some of its developed world peers

during 2014, but arguably it was sub long term trend levels. The J.P. Morgan

Economist and Strategists suggest there may similar pressures for Australia in 2015

being sub-par growth and increasing unemployment2. This may have implications for

the Australian economy, and ultimately for our insurance sector.

We focus in this section of the report on the macro drivers affecting the outlook for

the general insurance industry.

Economic indicators in Australia

The outlook based on recent research by the J.P. Morgan Economist is that

Australia could grow close to trend in 2015 (CY15) at 2.9%, which is above the

2.7% expected for 2014. He does, warn that the composition of the growth will

be driven largely by exports stemming from previous capital expenditure in

mining (as the resources are extracted and sold overseas, thereby boosting net

exports), rather than consumption or investment led growth. As such he suggests

that much of the growth will not be apparent to other parts of the economy.

The unemployment rate in Australia was 6.3% in November 2014 according to

statistics from the ABS and has been rising slowly from 5.8% a year earlier. This

is above the generally accepted target for NAIRU (non-accelerating inflation rate

of unemployment) of 5%; however, we note in recent times the NAIRU may be

considered to have increased slightly above this level3. The J.P. Morgan Australia

1 We reference research by J.P. Morgan Economist on 9 January 2015 “Global Data Watch”.

2 We reference research by J.P. Morgan Economist on 9 January 2015 “Outlook for Australia

in 2015: is there an echo in here?”. 3 We reference research by J.P. Morgan Economist on 19 November 2010 “Australia: lack of

slack to change inflation tack” & on 20 January 2012 “Does the RBA care about the

distribution of growth?” to form our view on the NAIRU.

7

Australia Equity Research 13 January 2015

Economist predicts an increase in the unemployment rate to peak at 6.5% in the

second half of 2015 as a result of continued forecasted sub-trend GDP growth.4

RBA currently has a record low cash rate of 2.5% which gives RBA less room for

further monetary policy expansion should it be needed (having already used this

tool – see Figure 7). According to the J.P. Morgan Australia Economist, RBA

may jettison their "period of stability" comment the RBA made last February and

our economist forecasts that there will be a rate hike in late 2015.

Housing sales volumes and prices were strong in 2014 and the J.P. Morgan

Australian economist expects this to continue to be the case in 2015 although at a

slower pace than in 2014. Our economist expects an increase in home

construction will follow solid house price growth (forecasted at a single digit

pace) for 2015.5

The Australian dollar touched a five year low of US$0.81 this month following

comments by RBA that they preferred a lower AUD as the method to deliver

easier monetary conditions. A depreciating Australian dollar can pose some cost

push inflation risk for insurers.

4 We reference research by J.P. Morgan Economist on 9 January 2015 “Outlook for Australia

in 2015: is there an echo in here?” 5 We reference research by J.P. Morgan Economist on 9 January 2015 “Outlook for Australia

in 2015: is there an echo in here?”

8

Australia Equity Research 13 January 2015

Figure 1: Unemployment rate Australia

Source: Bloomberg (12/1/20115)

Figure 2: Real GDP growth in Australia

Figure 3: Government fiscal rectification a drag to GDP growth

Source: JPM

Figure 4: Investments as % of GDP – mining /non-mining

Source: JPM

Figure 5: Price in US$ of commodities falling (Iron ore, Oil)

Source: Bloomberg

Figure 6: A big risk is a highly leveraged consumer

Source: JPM

9

Australia Equity Research 13 January 2015

Figure 7: Inflation rate indices vs. bond yields – Australia

Source: Bloomberg

Figure 8: A$ weakened but arguably still too strong for RBA’s liking

Source: Bloomberg

Claims: some inflation risks worsened by any economic deterioration

Consumer price inflation metrics are within the RBA’s long-term target range of

2-3%, with the inflation rate for the year to September 2014 being 2.4%. The

generally soft economic environment, and falls in petrol prices may offset some

of the cost-push inflation that may be expected from a depreciating exchange

rate. If CPI remains at reasonable levels, this is positive for the insurance industry

– particularly short tail insurers (to the extent that CPI can be used as a proxy

indicator of claims inflation).

Average Weekly Earnings rose 2.4% in the year to May 2014 (ABS), which is at

the lower end of recent historical levels. This is unsurprising given the softening

economic climate. This may be a slight negative for some classes such as

workers’ compensation whose premiums are levied as a % of wage roll (whereas

certain claim costs such as medical and legal may move independently of wage

inflation). However, for other classes, there are likely to have a positive effect to

the extent that the wage components of repair costs could increase at a slower rate

in short tail lines, and costs of compensation in court awards (where the award

takes into account salary levels) could be subdued in long tail lines.

Another key area highlighted in terms of claims inflation is the legal

environment, with respondents referring to a slow and effective erosion of tort

reforms over time. This particularly affects the liability and CTP classes,

however, we believe the impact is still quite limited, and the reforms have by and

large held up quite favourably.

10

Australia Equity Research 13 January 2015

Catastrophe experience

2014 catastrophe losses were below-trend for the global insurance industry,

according to our estimates. A similar benign CAT environment was observed in

Australia, where catastrophe claims were significantly below the 10 year trailing

average.

Figure 9: Australian catastrophe loss experience favourable in 2014, but has had increasing trends over the past 5 years

Source: J.P. Morgan estimates, ICA. Note: the 2014 figure includes the latest ICA estimate

(11/12/2014) of the Queensland hailstorm of ~$804m. The figures are inflation and exposure

adjusted

Figure 10: US industry catastrophe trends ($bn)– inflation adjusted, but not exposure adjusted

Source: J.P. Morgan estimates, Insurance Institute Information

Figure 11: Lloyds CAT claims (£m) in 1H14 was extremely benign

Source: J.P. Morgan estimates, Lloyds. Note: All figures are indexed to 2013, except 1H2014,

which is indexed to 1H14. These trends are inflation but not exposure adjusted.

Figure 12: 1H14 a relatively light period for catastrophe losses worldwide

Source: Swiss Re, Munich Re.. Inflation but not exposure adjusted.

Catastrophe costs globally have

been benign in 2014.

11

Australia Equity Research 13 January 2015

In Australia, weather changes can be a significant driver of catastrophe costs.

Adverse trends can impact loss ratios in short tail classes (fire/ISR &

householders in particular). The current 2014/15 summer has neutral conditions

forecast for the Southern Oscillation Index (which seems to be a major driver of

catastrophe costs) according to the Bureau of Meteorology. This continues a shift

away from the La Nina episode of 2011 and prior, which saw higher rainfall and

cyclone activity particularly on the east coast of Australia.

The charts below show a forecast for a below average cyclone season in 2014/15

and a relatively dry period for the 3 months to February 2015.

Figure 13: Normal season for parts of eastern Australia - Forecast for 3 months to February 2015

Source: Bureau of Meteorology

Figure 14: Average to below-average cyclone season most likely for Australia

Source: Bureau of Meteorology

The shift from La Nina to more neutral conditions, according to the Bureau of

Meteorology, could benefit insurers in terms of catastrophe costs. On average

since 1967, neutral years have had an average catastrophe cost (excluding

earthquakes) of $902m, which is significantly below the $3,043m during La Nina

years. Compared to the overall average annual catastrophe cost of $1,098m since

1967, a neutral year would represent on average a ~$200m benefit to the general

insurance industry.

12

Australia Equity Research 13 January 2015

Figure 15: Catastrophe losses, excluding earthquake (A$m in 2011 normalised costs) – against the Southern Oscillation Index (indicator of El Nino, Neutral and La Nina Years )

Source: BOM, ICA, J.P. Morgan estimates. Note: the latest ICA estimate (11/12/2014) of the

Queensland hailstorm of ~$804m is included for 2014.

Figure 16: Average catastrophe losses (excl. earthquake) for El Nino, Neutral and La Nina years using ICA data for catastrophes (excluding earthquake losses).

Source: ICA, BOM, J.P. Morgan estimates. Note: the latest ICA estimate (11/12/2014) of the

Queensland hailstorm of ~$804m is included for 2014.

Investment markets – falling investment yields hurting outlook for all classes.

Yields on fixed interest investments (typically held by insurance companies in

Australia to back their liabilities), have been falling as the RBA continues to work to

boost the economy through monetary stimulus in light of global and domestic

weakness. Falling yields have been further exacerbated by credit spreads contracting

in line with a hunt for yield by investors. As seen below, current yields on fixed

income assets of 3-year duration in Australia (of all credit grades) are even lower

than the levels seen during the GFC. We note that yields post the ‘as at date’ for the

survey had not moved substantially.

Figure 17: Yields on fixed income assets of 3 year duration in Australia

Source: Bloomberg

Equity markets were volatile in 2014, but the ASX200 Accumulation index

ultimately finished up 6% including dividends.

Yields on fixed income assets

appear to continue to fall, albeit

at a slower rate than previously

observed between 2010- 2012.

This is a concern for long tail

lines in particular.

The extent of reductions is large

enough to even affect short tail

RoEs.

13

Australia Equity Research 13 January 2015

Figure 18: ASX 200 Accumulation Index

Source: Bloomberg

Figure 19: ZCB bonds rates has flattened considerably – signaling uncertainty and weak outlook for the economy

Source: Bloomberg

14

Australia Equity Research 13 January 2015

Macro factors overseas impacting global insurance markets

Macro trends in the U.S. and U.K. improving but still uncertain for Europe

The charts below show that in the US and UK, economic growth data is now at

levels matching Australia. In Europe also, growth has recovered (still below other

markets). Unemployment levels there still remain challenging. Our global

economics team6 is forecasting an improvement in developed market growth

driven in part by lower oil prices and continued central bank stimulus in Europe

and Japan. Top-line (i.e. premium) growth may return in such an environment.

Historically there has often been a correlation between weak economic activity

and a rise in claims. Given that we didn’t see that pressure in any region when

economic growth was weak this cycle, we think that it is unlikely we will see an

improvement in claims trends in line with expected economic growth trends.

Figure 20: Real GDP Growth – Selected Developed Markets

Source: Bloomberg (15/12/2014)

Figure 21: Unemployment Levels – U.S. and U.K.

Source: Bloomberg (15/12/2014)

Inflation continues to remain while real yields remain weak

The threat of high inflation in conjunction with negative real yields is a very

detrimental combination for insurers. Yields in the US fixed income markets have

been improving although are still at historically low levels. As a result the

continuing low yielding environment continues to be a threat to the insurance

industry as the inflation drivers of claims (now and in the future) were arguably

remaining constant, while the expected investment earnings on the assets backing

claims liabilities remain poor.

Figure 22: Implied inflation and real yields in U.S. bond market

Source: Bloomberg (15/12/2014)

6 “Deus ex Machina: 2015 Global Outlook”, Bruce Kasman

Growth in UK in particular has

improved over the past 2 years

but latest trends for Europe

continue weak, having initially

shown positive trends in FY14.

Claims trends are potentially a

concern with inflation remaining

and low yields as seen in

previous years

15

Australia Equity Research 13 January 2015

With the view in the market that tapering of the U.S. Federal Reserves’ asset

purchase programme is likely, long-term interest rates have been starting to rise,

which is a boost for investment income available for insurers on government

bonds. Upward pressure on interest rates, which should be a benefit for the

insurance industry, although we note that in the US due to accounting standards

that do not require insurers to mark assets to market, disclosed running yields we

think are still likely to increase.

Premium rates increases tending to zero but capital levels are strengthening

The outlook on global premium rates has weakened since the peak in 1Q13 and

there has been negative to minimal premium rate growth observed in 2Q14 and

3Q14 across the small, middle and large corporate market. Capital levels however

are still quite strong in the U.S. and appear to be trending positively (see Figure

24).

Figure 23: Premium rate movements in U.S. commercial markets

Source: CIAB

Figure 24: U.S. surplus capital - from amalgamated accounts

Source: Insurance Information Institute

Reserve releases are expected to decline going forward in the U.S. (see Figure 25,

based on information from the Insurance Information Institute) although there

still appears to be the ability to support reported profits to some extent through

reserve releases. Inflation data overall remains relatively subdued.

Figure 25: U.S. P/C surpluses – JPM estimate of surpluses in the market reducing (JPM Australia estimate of the US market).

Source: JPM analysis on reserve surplus position of the US market at Dec 2013

0%

2%

4%

6%

8%

10%

12%

14%

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

2007 2008 2009 2010 2011 2012 2013

US$000s

US Industry Reserve Surplus / (Deficiency) - Direct business excluding latest accy (LHS)

Current Surplus for all accident years / Latest Annual NEP (RHS)

Commercial rates trends have

continued to slow - trending to

zero.

16

Australia Equity Research 13 January 2015

Figure 26: U.S. Towers Watson – inflation indices

Source: CIAB

Figure 27: U.S. Towers Watson – inflation indices (superimposed)

Source: Insurance Information Institute

Global reinsurance rates have been trending downwards as expected, as a result

of a benign CAT environment as well as the excess capital in the market. In the

US, there has also been a significant growth in collateralised reinsurance over the

past 4 years.

Figure 28: Global rate-on-line index by region, 1990 - 2014

Source: As of Jan 1 2014. Guy Carpenter

Figure 29: US Reinsurance Trends – sharp rise in collateralised reinsurance over the past 4 year

Source: Insurance Information Institute

Implications for the outlook for Australian Insurers

The 2015 outlook for the Australian economy appears relatively weak with similar

sub-par growth trends observed in 2014, likely to be seen in 2015. For Australian

insurers this should mean weaker growth prospects and increasing competitive and

claims pressures.

Low investment yields continue to be a concern. For long tail lines in particular, this

can make a substantial difference to returns in the absence of adequate premium rate

increases.

Globally, economic trends are strengthening in the US and UK, which should boost

premium volumes in those markets. Growth remains challenging in Europe, with

some reinsurers entering into deals with brokers to increase capacity in the market, in

what is a low growth environment. In the U.S. rate increases are trending towards

zero. Australian insurance companies in this environment are likely to receive no

favours from the economic cycle for the growth or profit prospects.

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013*

Auto, subtotal Workers compensation Other, bodily injuryOther, property damage Fire Commercial multiple perilCPI, all items

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013*

Auto Workers' Other Bodily injuryOther, property damage Fire Commercial multiple peril

17

Australia Equity Research 13 January 2015

What history / the survey say about growth

Siddharth Parameswaran, Alvin Liu; J.P. Morgan

Sharanjit Paddam, Kevin Gomes; Taylor Fry

In this article, we provide thoughts on the outlook for growth in the general

insurance industry in Australia. We examine historical statistics on growth in

premiums around the world, outline views from participants in the survey on growth

prospects and overlay that with our thoughts on forward looking challenges the

industry faces.

Historical GWP Growth statistics

Australian Experience

We have analysed growth and profitability data from the last 20 years of data in the

Australian industry. Whilst that is a very long history, we caution about using this

alone as a guide to future growth prospects due to the following: (1) 20 years of data

is a little limited and can be influenced by the number of phases of different

insurance cycles that are included (if more up-swings in the cycle than down-swings

are included, it can limit the extent to which one can draw meaningful conclusions

(2) the data is impacted by collection problems – as there are significant periods

where APRA / ISC did not collect data, which led to us interpolate some premium

figures; We also note that APRA has not been consistent over time in its definition of

profits and premium - which can distort the trends seen (3) there have been changes

in government involvement in underwriting some workers' compensation schemes

that has influenced growth seen (and this may not continue in the future) (4) history

does not always repeat.

Long Term Average Growth ~ matches GDP: The charts below show that

nominal growth in GWP has matched nominal GDP. The 20 years to 2013

showed average GWP of 6.61% p.a., whilst nominal GDP averaged 6.33% p.a.

We think this trend was artificially boosted in part by the very high initial figure

in 1994, driven by a very sharp hard market (poor profitability) and some

exceptionally strong growth in workers' compensation. Excluding 1994 - GWP

grew about 0.4% p.a. lower than nominal GDP.

Figure 30: Australia GWP growth vs. Nominal GDP growth Time Series – APRA/ ISC statistics

Source: ISC, JPM interpolation, APRA, Bloomberg. APRA has been inconsistent in its definition of premium (it was prospective

contracts at one stage, in between matching the accounting definition of GWP). They also did not collect data between 2002 and 2004

(we have interpolated figures).

In Australia, Premium growth

averaged close to GDP in the

last 20 years- but this may have

been influenced by 3 hard cycles

and only 2 prolonged soft cycles

Home has been the class

showing the strongest growth,

along with professional

indemnity.

Motor and Workers’

Compensation have been the

weakest classes for growth.

Growth is currently slowing in

Australia – as (a) the economy is

slowing (b) there is a soft market

market in commercial lines – and

no signs of superimposed

inflation (c) competition in

personal lines

18

Australia Equity Research 13 January 2015

Figure 31: Australia GWP growth Time Series vs. Normalised RoEs– APRA/ ISC statistics. JPM

Source: ISC, JPM interpolation, APRA, Bloomberg. APRA has been inconsistent in its definition of premium (it was prospective

contracts at one stage, in between matching the accounting definition of GWP). They also did not collect data between 2002 and 2004

(we have interpolated figures). JPM Estimates of RoEs. using consistent calculation of Capital

Home and professional indemnity have shown strongest growth: The

charts below show the growth by class of business. It appears that

professional indemnity and home have been the fastest growing classes.

Workers' compensation and motor appear to be quite weak. Within home –

the last 4 years have boosted that average growth figure by 1.3% p.a.,

reflecting the extent of rates increases we have seen in the class in recent

times. In fact – in the last 4 years it has only been home and Fire/ ISR that

have been driving the growth at an overall level above long run averages

(all other classes have been at or below long run averages). The long tail

classes have been influenced by 3 factors in our view: (1) superimposed

inflation that can take a while for insurers to recognise – but is then

followed by extremely high rate increases (2) tort reforms – that often

follow the rate increases - which then lead to gradual reductions in rates (3)

changing investment yields - which if large can influence the premium rates

environment. In the early and late 1990s we saw elevated levels of inflation

that lead to reforms, and that then resulted in prolonged soft markets.

Figure 32: Australia GWP growth % p.a. Time Series by class of business– APRA/ ISC statistics

Source: ISC, JPM interpolation, APRA, Bloomberg. APRA has been inconsistent in its definition of premium (it was prospective

contracts at one stage, in between matching the accounting definition of GWP). They also did not collect data between 2002 and 2004

(we have interpolated figures).

19

Australia Equity Research 13 January 2015

Figure 33: Australia Average GWP growth by class – 1993 to 2013 Class Average Growth %

Fire and ISR 6.69 Houseowners/householders 8.12 CTP Motor vehicle 7.00 Commercial Motor Vehicle 5.59 Domestic Motor Vehicle 5.91 Professional Indemnity 8.47 Public and Product Liability 6.31 Employers' Liability 5.09 Other 6.14

Commercial Direct 6.00 Personal Direct 7.08

Total ex Re 6.61 Nominal GDP 6.33

Source: ISC, JPM interpolation, APRA, Bloomberg. APRA has been inconsistent in its definition of premium (it was prospective

contracts at one stage, in between matching the accounting definition of GWP). They also did not collect data between 2002 and 2004

(we have interpolated figures).

Figure 34: Growth in GWP in Fire and ISR – Australia 1993 - 2013

Source: APRA, ISC

Figure 35: Growth in GWP in Home – Australia 1993 - 2013

Source: APRA, ISC

Figure 36: Growth in GWP in CTP – Australia 1993 - 2013

Source: APRA, ISC

Figure 37: Growth in GWP in Commercial Motor – Australia 1993 - 2013

Source: APRA, ISC

20

Australia Equity Research 13 January 2015

Figure 38: Growth in GWP in Domestic Motor – Australia 1993 - 2013

Source: APRA, ISC

Figure 39: Growth in GWP in Prof Indemnity – Australia 1993 - 2013

Source: APRA, ISC

Figure 40: Growth in GWP in Public and Product Liab – Australia 1993 - 2013

Source: APRA, ISC

Figure 41: Growth in GWP in Employers' Liability – Australia 1993 - 2013

Source: APRA, ISC

Figure 42: Growth in GWP in Commercial Direct – Australia 1993 - 2013

Source: APRA, ISC

Figure 43: Growth in GWP in Personal Direct – Australia 1993 - 2013

Source: APRA, ISC

21

Australia Equity Research 13 January 2015

US Experience

We have 43 years of data on growth in premium and return statistics from the US.

Given the long time periods included, and the very limited involvement of

government as an underwriter, growth statistics are likely to be less impacted by the

phases of different insurance cycles or significant changes in government

involvement in underwriting.

Long Term Average Growth slightly below GDP: The charts below show that

nominal growth in Net Written Premium in the US P&C industry has averaged

6.21% p.a. since 1971. This is slightly below nominal GDP growth (6.72%p.a.

since 1971). This suggests that historically the growth of the sector has been

averaged 0.51 p.a. slower than GDP. For investors – assuming constant margins,

we think that all else being the same – we think this implies a PE that should have

been ~0.5x lower than the broader market assuming a 15% RoE for both.

Figure 44: US P&C Nominal Net Premium Growth Time Series

Source: III, AM Best

Figure 45: US P&C Nominal Net Premium vs. Nominal GDP growth

Source: III, AM Best,. Bloomberg

Insurance premiums in the US

grew slightly slower than

nominal GDP. Within this, most

years were sub nominal GDP –

whilst there were a few very

large peaks that made up for

this.

If history is a guide - soft cycles

remain soft for quite long

periods of time.

22

Australia Equity Research 13 January 2015

Figure 46: Difference between P&C NWP and GDP growth

Source: III, AM Best

Likelihood that a weak growth period will continue for some time: What is

clear is that most periods show NWP growth being lower than GDP (i.e. the

mode [most commonly occurring outcome] is for NWP growth to be less than

GDP). This is however offset by a few periods (hard cycles) where the growth in

NWP is well above GDP. If history follows that pattern, it suggests that when

growth in premium starts slowing, it will remain weak for some time. The last 2

hard periods (mid 1980s and 2001) were triggered by several preceding years of

falling profitability (see below) in part driven by competition causing premium

growth to be well below inflation, and also the response of insurers to

acknowledging some superimposed inflation.

Figure 47: US P&C Net Premium Growth against US P&C RoEs

Source: III, AM Best

US recently showing some growth: The current environment in the US has

shown a return in the last 3 years to growth in Net Premium in line with GDP

(largely premium rate driven - although this is petering out).

Other experience

We show in the table below inflation adjusted (i.e. “real”) growth in regions

according to Swiss Re.

23

Australia Equity Research 13 January 2015

What it shows is that there has been reasonably strong growth in “South and

East” Asia and to some extent Africa. Growth in most other regions has been

rather weak. It seems that growth in premium is stronger than GDP in countries

where per capita income, and capital stock values are low but where both are

growing quickly.

Figure 48: Growth in “inflation adjusted” P&C Premium by Region

Source: Swiss Re, JPM compilation of figure

Our explanation of drivers of growth

We think the drivers of growth in GWP include the following:

1. Nominal Economic growth (see Figure 30 – which shows a strong link between

the two). As the economy grows, more material goods and potential future

production can be insured.

2. Catastrophe Events: A collection of these (or lack of) can lead to changes in

estimates on long term claims costs / as well as some retrospective pricing. This

usually has a lagged impact on GWP growth (it takes a year or more to feed

changed perceptions on risk into achieved increases in rates). The increases in

Fire / ISR and home post 2009 were arguably driven by such events.

Figure 49: Catastrophe against short tail cat exposed premium growth (LHS = growth; RHS = $m gross catastrophe costs I n 2011 dollars)

Source: JP Morgan, ICA, APRA / ISC

Growth in premium is stronger

than GDP in countries where per

capita income, and capital stock

values are low but where both

are growing quickly.

We think GWP growth rates are

influenced by:

- Nominal economic growth

- Perceptions/ experience

on catastrophe costs

- superimposed inflation /

tort reforms

- yields

- capital / returns

- rate of improvement in risk

management

- extent to which new

products of insurance

arrive

24

Australia Equity Research 13 January 2015

3. Superimposed inflation / tort reforms: As we have explained earlier, in ~1994

and ~2000 we saw some very hard markets in long tail classes stemming in part

from re-estimates of inflation. Post 2002 in particular, there were very significant

tort reforms across Australia that curbed court awards in liability and professional

indemnity and to some extent CTP classes. In 1999 there were reforms affecting

NSW CTP / Workers Compensation. All of these lead to a significant soft period

in long tail lines. See Figure 36, Figure 39, Figure 40, Figure 41. As a general

rule most insurers believe that there is underlying superimposed inflation (in

terms of average claim size) evident in most classes over time – perhaps as

society believes that it can compensate more generously for loss as it gets richer

over time.

4. Changing investment yields: In 2009 in response to large falls in yields, there

were large increases in rates on long tail lines to compensate for reduced

investment income.

5. Capital levels: Increased capital levels usually are caused by the factors

described above (e.g. a lack of catastrophe can boost retained earnings).

Nevertheless – it is often mechanistically quoted as a factor leading to reduced

rates (we think it is at best only part causation, part correlation). We think high

levels of profits attract incremental capital into the market. The chart below

shows that profitability is now very high by historical standards –suggesting that

there could be some incremental.

Figure 50: Historical Notional Industry ROE* (smoothed investment return, hypothetical capital based on current APRA standards - if capital levels were set for a large diversified insurer)

Source: JPM calculations, J.P. Morgan Taylor Fry Barometer

6. Improvements in risk mitigation / management: We think some classes such

as motor and workers compensation have seen ever reducing costs of risks on a

per unit basis, which means that GWP growth has tended through the cycle to be

less than for many other classes. We show this in the charts below. In motor for

example, fatality rates have been falling for a very long time (we estimate that

between 1970 and 2010 the rate of improvement was 3.3% p.a.). We can also see

that whilst vehicles have been growing faster than population (suggesting motor

should be a growth class), the statistics show that GWP growth has been weaker

than nominal GDP (and actually one of the weakest classes) and that despite the

weak GWP trends profitability has not been affected. This all suggests that

underlying frequency of risk must be getting much better (i.e. cars are getting

safer etc). We argue that the only reason that motor insurance has not been a class

that declined quicker is that average claim size has risen as the components in

cars have become more expensive to replace. Similar improving statistics are

25

Australia Equity Research 13 January 2015

evident in workers compensation (see below) where we estimate that between

2001 and 2013 the serious injury frequency rate improved by 3.1% p.a.

Figure 51: Frequency of Road Deaths – Australia. Improved dramatically

Source: ABS, DITRD

Figure 52: Growth in Motor Vehicles vs. Population Growth - Australia

Source: ABS

Figure 53: Growth in GWP in Domestic Motor – Australia 1993 - 2013

Source: APRA, ISC

Figure 54: Combined Ratios and premium rate increases in Australia – Domestic and Commercial Motor Combined

Source: JP Morgan Taylor Fry Barometer, APRA

Figure 55: Workers' Compensation Serious Injury Frequency Statistics (per 1000 employees) - Australia

Age Group 2000-01 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13p

Change from 2001

to 2013 <20 years 9.7 8.5 7.7 6.8 7.2 6.9 6.4 -34% 20-24 years 13.3 10.6 10.0 9.2 9.3 9.3 9.2 -31% 25-29 years 14.7 11.1 10.5 9.7 9.5 9.5 9.1 -38% 30-34 years 16.7 12.3 11.6 11.2 10.8 10.3 9.4 -44% 35-39 years 18.2 13.8 13.4 13.0 12.4 11.8 10.8 -41% 40-44 years 18.1 15.1 14.5 14.4 14.0 13.5 12.2 -32% 45-49 years 18.1 15.9 15.1 15.2 15.4 15.0 13.4 -26% 50-54 years 19.3 16.5 16.0 16.0 16.0 15.6 14.2 -26% 55-59 years 18.0 15.9 15.8 15.6 15.3 15.3 14.0 -22% 60-64 years 19.2 15.6 14.3 15.0 14.9 15.4 14.2 -26% Total claims 16.3 13.3 12.8 12.4 12.3 12.0 11.1 -32%

Source: http://www.safeworkaustralia.gov.au/sites/swa/about/publications/pages/australian-workers-compensation-statistics-2012-13

7. New classes / heads of damage: Given our comments above that we think that

frequency in most classes are likely to be improving, we think that insurance

companies have to keep innovating to find new risks to insure. As an example,

we note that the insurance industry has recently started providing much greater

coverage for flood on home insurance policies. This would have increased some

26

Australia Equity Research 13 January 2015

of the costs of the events. Other examples of growth into new areas include

growth in cyber insurance and pet insurance. It is notable that both of these are

being pioneered by overseas insurers operating here either through their Lloyds

or domestic license. As such – the large domestic insurers are largely not

partaking in that new growth at the moment.

Thoughts on growth from survey participants

As part of this survey, we specifically included questions on the issue of growth

prospects for the industry. We outline below a summary of the survey participant's

responses:

Survey Participants expectations on growth: In the section of the survey “Issues

Confronting the Underwriters” we summarise answers from respondents where we

asked participants questions about growth. These included (a) whether they saw the

general insurance industry as a growth industry, (b) whether the industry was

expanding its product range and (c) whether alternatives e.g. alternative capital,

mitigation of risks were reducing demand for traditional insurance. We also

separately asked about the cycle. We outline below the findings:

Most think the general insurance industry is a GDP or sub GDP growth business.

In the short run - many made comments about the cycle in particular and

competition in personal lines being a near term headwind. The more bullish

participants said that in the medium term improved risk management would be

offset by higher weather related claims from climate change, new products and

privatization of government insurance schemes. Nevertheless, in the long run –

most participants thought growth would be GDP or sub GDP.

Table 1: Responses in Survey from Participants on whether General Insurance is a growth industry in the near term and medium term (number of respondents)

Near Term

~Medium Term

Sub GDP ~GDP More than GDP Sub GDP GDP More than GDP 4 1 3 3 1

Source: JPM Taylor Fry Barometer 2014. There were 16 respondents but some left responses blank or did not provide enough information to decide exactly where they stood on this issue

We also asked 3 questions about (a) the cycle (b) which class respondents saw the

greatest change in capacity and whether it was positive or negative (c) which

class respondents saw the greatest risks to profits.

Figure 56: Questions asked of respondents on competition in personal lines and commercial lines

Source: JPM Taylor Fry Barometer

Please indicate the level of competition in the personal and commercial lines markets, on the following scale:

1 2 3 4 5

Personal lines

Commercial lines

1 2 3 4 5

Personal lines

Commercial lines

Not rational,

unprofitable

Target ROEs

being met

Excessively competitive,

lapse rates rising, rates

falling significantly

Rates and

lapse rates

holding

Not competiitve,

rates falling,

premium rates

rising

Please indicate how rational you believe the pricing in the personal and commerical lines markets to be, on the

following scale:

Very profitable, above

target profit levels

Most survey participants

thought that in the near term the

industry would be a sub GDP

growth business.

In the medium term it was more

mixed – but most seemed to

think that the industry was either

a GDP or sub GDP growth

business

27

Australia Equity Research 13 January 2015

Table 2: Answers to competition question

1 2 3 4 5 Average

Personal lines competition 0 0 2 8 0 3.80 Commercial lines competition 1 0 2 6 4 3.92 Personal lines rationality 1 0 10 1 0 2.92 Commercial lines rationality 0 7 6 0 0 2.46

Source JPM Taylor Fry Barometer

Table 3: Answers to capacity question and profit risks.

Greatest change in capacity Profit Risk

Votes Positive Negative Votes

Domestic Motor Vehicle 4 3 1 4 Householders 2 1 1* 1 CTP(NSW & QLD) 0 0 0 1 Underwritten Workers' Comp (WA) 0 0 0 0 Underwritten Workers' Comp (TAS ACT & NT) 0 0 0 1 Fire / ISR 6 3 3* 2 Commercial Motor Vehicle 0 0 0 0 Public & Product Liability 1 1 0 2 Professional Indemnity 1 1 0 2 Directors' & Officers' 1 0 1* 2

Source: JPM Taylor Fry Barometer. * we think these respondents said the class faced a negative change in capacity when they intended to say they had a positive change in capacity.

What is clear is that there is considerable pressure on premium rates in

commercial and personal lines according to the industry, with participants saying

both classes had scores near 4 (“lapse rates rising, premium rates falling”). In

commercial lines – there was a bit more concern about the pressure leading to

irrational rates. In terms of change - participants signaled large increases in

capacity in domestic motor, householders and Fire / ISR. In terms of changes in

profitability - it seemed that participants were most concerned about growth in

capacity in Fire / ISR, motor and householders.

JPM Views on Outlook for growth

In the near term – we are very cautious about the outlook for growth in the industry,

due to the following:

Growth now slowest rate in the last 20 years: A confluence of factors has led

to the GWP growth trends in the 2 quarters to September 2014 being the lowest

they have been in the last 20 years (see charts below). We don’t think there is any

respite likely in the quarters ahead.

We are very cautious on growth

prospects:

- current growth rates are

lowest ever

- competition is very strong in

personal and commercial lines

due to all time high RoEs

- economic growth could be a lot

slower

- frequency has been falling at

3% p.a. + in key classes

- there are no offsetting claims

size inflation driven drivers

boosting growth

- domestic insurers not

expanding into new classes

28

Australia Equity Research 13 January 2015

Figure 57: Long Term trends on GWP Growth – Australia

Source: APRA, ISC, JPM estimates

Figure 58: Latest trends on GWP growth - current levels of Growth are the lowest in 20 years - Australia

Source: APRA

Cycle: We believe that premium rates in both personal lines and commercial

lines are under pressures.

RoEs are as high on an underlying basis as we have ever seen them – which is

inviting competition in from overseas (e.g. Lloyds) as well as domestically e.g.

from banks in personal lines.

Superimposed Trends: There have been no signs of superimposed inflation for

some time – which means growth in premium in response to this is unlikely.

There are also likely to be fewer incremental boosts to profitability to come from

weakening claims trends in long tail lines in our view (insurers are getting much

closer to setting assumptions assuming minimal inflation).

Lack of expansion into new classes: There are no new classes that domestic

Australian insurers seem to be pushing in a big way to make up for some of the

pressures we have seen. Most of the expansion into cyber insurance / pet

insurance has been made by foreign insurers. There could be some respite from

privatization of South Australian compensation schemes.

Frequency continuing to fall – but maybe even claim size: Classes such as

motor could see accelerated reductions in frequency from new technologies.

There is even a risk that average claim sizes could start falling in classes such as

motor due to the new technology, and the cost of that technology coming down.

This is something we have not seen for a while.

29

Australia Equity Research 13 January 2015

Table 4: Summary of JPM Views on Growth Outlook

Driver Outlook - in terms of impact on premium rates Comment

Growth -ve This is expected to be weak Catastrophe - Arguably 2014 may be slightly above average

Superimposed inflation flat to –ve This has not been evident for some time. Insurers are talking about reducing assumptions on these.

Changing investment yields +ve Interest rates could fall - thereby forcing insurers and regulators to consider increases in long tail rates

Capital -ve There is still inflow of capital into commercial markets, returns are at all-time highs in the sector.

Risk Mitigation / Management -ve

The outlook for motor in particular in the long run (driverless cars, technology assisting in avoiding collisions) should be weak in the medium to longer term. This may be offset partially by some increases in property classes from climate change related risk

New classes Flat At this stage - the domestic industry has been slow to embrace new classes such as cyber insurance etc.

Source: JPM

30

Australia Equity Research 13 January 2015

The Impact of Technology on Insurance

Kevin Gomes, Sharanjit Paddam, Catherine Weston; Taylor Fry

Siddharth Parameswaran, Alvin Liu; J.P. Morgan

The current strongly competitive market is driving demand for innovation in insurance. Technology is supplying innovation, and is impacting all aspects of insurance – from products, through rating, distribution, and claims management. In this article, we discuss the different opportunities and challenges to insurers from recent and future

technological advances.

Products

The major impact of technology on insurance has been the potential for new

insurance policies to cover new and emerging risks, including cyber insurance,

transport networking companies, home sharing, and drones. However, each of these

new products presents new challenges for insurers.

Cyber insurance

Technology has transformed businesses over the last twenty years as companies have

gone online in order to access customers, and to store their information in the

“cloud”. However, this has also exposed them to the risk of a cyber attack.

Traditional commercial insurance products often did not respond to these risks, as

they generally only provided cover for tangible property.

Cyber insurance has been offered for many years now, and covers loss due to a

cyber-attack, data protection laws, and the mismanagement of personal data. Policies

are usually written on a claims made basis, with the main cover being liability, and

additional coverage provided for legal, investigation, fines and other expenses.

Damages from a cyber-attack can be large. Publically known examples of cyber

attacks include the recent hacking of the Sony corporate network, including the

demand for the movie The Interview not to be released. However, many cyber

attacks, particularly those affecting small and medium companies, will go

unreported.

Given the lack of historical data, Cyber insurance can be difficult for insurers to

price. There are, however, at least two risk modelling companies in the process of

cyber risk modelling.7

Transportation Network Companies (TNCs)

The smartphone app taxi service, Uber, has risen in popularity since expanding its

services in 2012 to UberX with non-luxury cars and non-commercial drivers. Other

relatively new companies in the US based on a similar ride share model are Lyft and

Sidecar. Low costs are possible not only due to the nature of drivers owning their

own vehicle, but also because TNCs typically take out “contingent” insurance

(details varying depending on the country) - effectively a ‘Plan B’ to the driver’s

personal insurance policy.

7 http://www.theage.com.au/it-pro/security-it/insurance-risk-modelers-look-to-clarify-cyber-risk-

costs-20141222-12c2tw.html

31

Australia Equity Research 13 January 2015

The insurance implications for Uber users are particularly concerning in Australia, as

The Insurance Council of Australia (ICA) is not aware of insurance products in

Australia that cover ride sharing8. A car ride share warning was released by the ICA

in June 2014 stating “any motorist considering providing a ride sharing service

should first discuss this with their insurer to check the impact this might have on

their motor vehicle insurance policies, in particular third party property or

comprehensive car insurance”9. If an insurance company proves a driver’s actions to

be illegal (for example, a non-commercial driver in a non-commercial vehicle

receiving a fee for service), a claim against the insurance policy can be declined.

In Australia, Uber requires drivers to have a full license, CTP coverage and third

party property damage insurance, however it is likely that a personal insurance claim

will be denied. Uber therefore provides “contingent coverage” (in the event that a

driver’s personal insurance does not apply) in the amount of US$5 million for bodily

injury and property damage to third parties. This would still leave the driver’s vehicle

uncovered in the case of a personal comprehensive claim being declined.10

TNCs provide unique challenges for insurers, including if any such service is in fact

legal. A Roads and Maritime Services spokeswoman stated that “while Uber is not

breaching the Passenger Transport Act 1990 by offering the service, motorists

transporting passengers for a fare are”. NSW Roads and Maritime Services has

issued five $2,500 fines, threatening legal action against UberX drivers. The

Victorian Government issued more than $50,000 worth of $1,700 fines to drivers

around May 201411

.

Airbnb

The home hosting website, Airbnb, has faced similar insurance issues to TNCs,

providing secondary liability coverage which push the insurance onus onto ‘primary’

insurance - the host’s home insurance policy, which will often not cover commercial

activity. This was put to the test as described in December 2014 by The New York

Times, reporting that one host: “talked to an agent about her rental activity, it quickly

became clear that it could not offer her any kind of liability rider and no longer

wanted her as a customer”12

. Another insurance company in the US sets a cap on

rental income, which appears to be a good interim measure until sufficient Home

hosting data can be analysed to better determine appropriate insurance cover and

pricing.

It appears that in the US, where Airbnb has 177,539 listings (and over 1 million

worldwide)13

, the insurance industry is not well prepared. CNBC reported in

December 2014 that "If Airbnb succeeds in sharing risk with personal insurance

companies, then everyone's premiums have to rise to cover it. ... Insurance

companies could solve this by asking all policyholders about their hosting habits, but

none of the 10 … contacted said that they had made any changes to their policies as

home-renting has grown."14

8 http://www.smh.com.au/digital-life/smartphone-apps/nsw-cracks-down-on-uber-ridesharing-

20140617-zsabx.html 9

http://www.insurancecouncil.com.au/assets/media_release/2014/030614%20FINAL%20Car%20ride%20share%20warning.pdf 10

http://blog.uber.com/OzRidesharing 11

http://www.smh.com.au/digital-life/smartphone-apps/nsw-cracks-down-on-uber-ridesharing-20140617-zsabx.html 12

http://www.nytimes.com/2014/12/20/your-money/the-insurance-market-mystifies-an-airbnb-host.html?_r=0 13

as at 22 December 2014 14

http://www.cnbc.com/id/102245404

32

Australia Equity Research 13 January 2015

Drones

Drones have been used for military purposes for many years, however drones have

also been tested for the delivery of books and food (including pizza, taco’s and

Indian food). The first regulatory hurdle in Australia for the use of Remotely Piloted

Aircraft (RPA) is obtaining an Unmanned Operators Certificate (UOC), which is

approved by the Civil Aviation Safety Authority (CASA). CASA also “recommends

that you contact your insurance provider to obtain information surrounding public

liability insurance. Insurance costs can be significant and could influence your

decision to apply”15

. The UOC requirement and the insurance issues could be factors

in drones being slow to ‘take off’ in Australia.

Rating

The pricing of insurance products is improving with more accurate rating factor data

and the introduction of additional rating factors available due to advances in

technology. An example of this is using mapping technology to assess fire and flood

danger zones to price property insurance. Information such as the landscape on the

property, the proximity to bush-land or rivers and the construction of the building

itself can be valuable in assessing the risk of bushfire or flood. Another example of

advances in rating factors is telematics, used for motor vehicle insurance.

Telematics

The data collection for pay as you drive (PAYD) is designed to capture usage based

driving and driver behaviour. The question: ‘are you willing to put a black box in

your car?’ is a rating factor in itself. Customers who drive less often, less often in

peak hour, and less often in dangerous areas have a lower claim risk due to the nature

of their usage. Steering, braking and acceleration are assumed to be factors in motor

vehicle claims risk and are used for telematics. The less erratic a driver is, the lower

risk of a claim and therefore the lower the premium. There may be a critical point in

time whereby insurers not offering telematics may be left with the worst drivers.

Telematics is also assisting insurers in the faster management of claims as well as

being used as a launch pad for other services such as traffic alerts, collision warning

systems, anti-theft, fuel consumption analysis and post-accident services.

Another insurance line that has plans to utilise monitoring/tracking technology in

2015 is pet insurance. In the UK, an insurer is offering a 20% discount on a pet

insurance policy if the pet wears a micro chipped GPS collar16

. The collar will not

only be used for lost pets, but its primary purpose will be to track the exercise routine

of the pet due to increasing costs in pet insurance which are assumed to be largely

due to higher obesity levels. Lower premiums and other rewards will be given to

owners who follow the applicable exercise guidelines.

To date, telematics has not seen widespread take-up in Australia. One factor has been

the large expense associated with installing a black box in a policyholder’s car.

Recently however, smartphones with inbuilt GPS chips have provided an alternative,

and much cheaper means of tracking individual drivers, although such data is more

difficult to verify – e.g. was the policyholder a driver or a passenger when the data

was collected?

15

http://www.casa.gov.au/scripts/nc.dll?WCMS:STANDARD::pc=PC_101985 16

http://www.telegraph.co.uk/health/petshealth/11206443/Track-your-dog-with-a-GPS-collar-to-save-20pc-on-insurance.html

33

Australia Equity Research 13 January 2015

Distribution

Technology has changed the way insurance is sold and has also allowed insurers to

segment their markets and target specific groups of customers. Arguably many new

entrants to the Australian motor and home markets have been successful in cherry

picking profitable segments of the incumbents’ market through the use of

sophisticated data analytics.

Insurers have also started to make use of additional sources of data on their

customers, such as credit card purchase history, loyalty programs, social media,

general smart phone and tablet use, as well as equipment such as GPS – all of which

are now part of everyday life.

Internet giants may also prove to be an insurance industry game changer, as Google

makes further inroads into the insurance industry. In 2012, Google launched ‘Google

Compare’, providing quotes in the UK for banking products, motor vehicle and travel

insurance. Google’s plans for 2015 are to expand its insurance interests and sell

motor vehicle insurance online in the US.17

Claims management

After the Brisbane storms of November 2014, a record proportion of claims were

lodged online rather than over the phone. There are several possible reasons for this,

including: the possibility that people are less likely to require human advice for

hailstorm claims; smartphone use becoming mainstream; as well as customers

preferring the convenience of the online channel compared to being kept on hold on

the phone.

Automated claims management software is also being used to identify high risk

claims in much shorter time frames than previous manual processes.

Once a claim has been accepted, advances in technology can be used to reduce

claims cost. One example is the robotic spraying of cars which reduces repair

expenses.

Claims costs are experiencing a long term reduction in frequency, both through

reduced numbers of accidents and a reduction in fraudulent claims. Cameras have

been used for many years in reducing fraudulent claims. Telematics can be used to

encourage better driver behaviour. Driverless cars have the potential to significantly

reduce accidents by removing the component of human error.

Driverless cars

Driverless cars are not the fictitious idea they once were, having been approved to be

tested in several states in the US, albeit with a hefty insurance bond requirement -

California’s requirement being USD 5 million18

. Germany and the UK have also

been making inroads. Germany has tested driverless cars on the Autobahn, and the

UK recently announced a government project to test the suitability of driverless cars.

The UK testing aims to investigate driver behaviour, and will also include examining

issues such as risk, liability and insurance as well as the practicalities of integrating

driverless cars with traffic and pedestrians. Kenny Leitch, the Global Telematics

Director of the firm that won the contract, RSA, said: "Driverless cars are a fantastic

innovation which will fundamentally change the world of motoring and car

insurance. There are many unanswered questions around how these cars will be

17

http://www.insurancejournal.com/news/national/2015/01/09/353593.htm 18

http://www.businessinsider.com.au/audi-jumps-to-the-front-of-the-line-for-self-driving-cars-in-california-2014-9

34

Australia Equity Research 13 January 2015

insured and through our involvement in this project we will be one of the first

insurers to gain first-hand knowledge of the technology. As a result, we’ll be strongly

positioned to educate drivers and also offer the most appropriate insurance for these

cars.”19

Testing driverless cars has expanded, with plans to test the car on multi-level

highways in Shanghai and Beijing.20

Driverless cars are a game changer and insurers will have to make considerable

adjustments in order to adapt to a world with driverless cars. We expect the

following changes to occur:

Fewer accidents as ‘human error’ is removed as a potential cause of

accident, provided the technology used is sound and durable

New challenges to materialise for lawmakers regarding licensing,

responsibility for vehicle operation and liability

Fewer cars on the road if this technology is employed successfully

Insurers will need to be able to respond to these social and technological changes,

and the following represent real challenges insurers will need to address.

Who is liable?

If an accident occurs where an autonomous car is at fault, who is deemed liable?

Would liability fall on the car manufacturer, the technical systems manufacturer, the

network supplying GPS information, or will the occupant still be deemed as having

ultimate responsibility for the vehicle’s operation? If manufacturers are considered

liable, we could expect an increase in the number of product liability claims — and

an increase in premiums.

Any alterations to the concept of liability which stems from system failure that result

in accidents will carry across to CTP insurance. If manufacturers are deemed liable,

the concept of driver fault may come under pressure and some of the Australian CTP

schemes may need to change.

Determining premiums

How will premiums for autonomous vehicles be determined? Removing driver

judgment and ability from the equation means a 21 year old male may have the same

expected claims cost as a 40 year old female. The usual rating variables of age,

gender, license tenure and claims history will no longer be good predictors of claim

frequency and severity.

We might expect an increase in repair costs for autonomous vehicles damaged in

road accidents relative to conventional vehicles. These automobiles are likely to

require the services of specialised repairers when system repairs are needed. This

would impact the premiums paid by the owners of both the driverless and regular

cars, the latter incurring higher expected repair costs upon colliding with a driverless

car.

Insurers will have to establish premiums in the absence of a claims history and

judicial precedents. Provided the technology employed is reliable and durable we

19

http://www.actuarialpost.co.uk/article/rsa-chosen-as-insurance-partner-for-driverless-cars-project-6996.htm 20

http://www.techtimes.com/articles/16791/20141001/bmw-partners-with-baidu-to-test-self-driving-cars-in-china.htm

35

Australia Equity Research 13 January 2015

could expect the reduction in claim frequency to be sizeable. While we acknowledge

that other factors will need to be considered in the setting of premiums, when looking

at the effects on premiums from this angle alone, we may expect comprehensive

motor premiums to reduce for autonomous cars compared to their driver operated

counterparts.

Premium setting for shared vehicles

Given that autonomous cars have the potential to be easily shared between owners,

how will premiums be set? Should a large scale car sharing scheme be introduced

there will be fewer cars on the road, less cars manufactured and a reduction in the

number of cars that require insurance. If cars are able to drive to their owners, car

sharing becomes easier and the demand for taxis will reduce. Insurers will need to

consider that such cars will be on the road more often and factors including where

located and if garaged will have less relevance where there are multiple owners.

Whilst the propensity to cause an accident may be lower in the case of driverless

cars, the frequency of ‘not at fault collision’, storm and windshield claims may

increase due to increased time vehicles are on the road. Will insurance premiums

change on a trip by trip basis, depending on whether the driver will be in control or

not, or even depending on the weather forecast and time of day?

Additional challenges in a driverless car society

The proliferation of autonomous cars must be accompanied by stable and secure

infrastructure. In other words, there can be no network crashes and back-up systems

must be installed in vehicles to seamlessly take over if components fail. In addition,

this increased reliance on technology means the risk of system hacking needs to be

minimised and consideration should be given to what type of personal information is

collected and stored.

In highly automated commercial aircraft, pilot error is still reported as the leading

cause of aviation accidents21

. Despite simulator emergency training and currency

requirements, there have been several major accidents where the pilots have failed to

undertake the most basic of recovery procedures, such as recovering from a stall.

Would ‘drivers’ of driverless cars lose their skills, becoming reliant on automation?

Society will need to consider these issues and respond if driverless cars become part

of everyday life.

Conclusion

Advances in technology have the potential to transform and challenge the insurance

industry. Improvements in rating and fraud detection are already being seen on the

international insurance scene. These are clearly benefits to the insurance industry,

and those not keeping up with technology could suffer. For example, a strong

increase in the number of insurers offering competitive telematics car insurance

could leave the cautious insurers with the worst drivers. Challenges to the insurance

industry are the emergence of companies such as ride-sharing and home hosting,

where insurance companies would benefit from reconsidering their insurance

provisions. A little further away is the driverless car society, which is likely to reduce

claims from driver error, however introduce complexities such as liability and

technology malfunctions and/or hacking. Will advances in technology increase the

demand for Cyber insurance, or would breach notification legislation be the driver

for Cyber insurance demand?

21 http://www.newyorker.com/science/maria-konnikova/hazards-automation

36

Australia Equity Research 13 January 2015

The Political Impact of Climate Change on Insurers

Sharanjit Paddam, Taylor Fry

Climate change is likely to exacerbate affordability issues for Australian

homeowners, as noted in a recent research paper: Can actuaries really afford to

ignore climate change? by actuaries Jon Harwood, Sharanjit Paddam, and Jessica

Egan, and Andy Pittman, Professor of climate science at UNSW.22

These affordability issues will pose significant challenges for insurers, who already

face widespread negative publicity for increases in insurance premiums for properties

located in areas exposed to natural perils, such as bushfires, cyclones and flood. In

turn, these will generate political issues, as consumers perceive higher premiums as

being unfair.

A number of potential changes in climate systems could also have a significant and

relatively sudden impact on claims costs. As home insurance policies usually only

offer cover on an annual basis, this could leave communities exposed very abruptly if

there is significant increases in premium, or the removal of cover, or the exit of

insurers from unprofitable markets.

Location, location, location

Figure 59: Buildings insurance premium as a proportion of annual income under various climate change scenarios

Source: Harwood et al.

The box-chart above shows the variation in ratio of buildings insurance premiums to

average annual income for different geographic locations across Australia. It is

based on the current premium rating structure of a major Australian insurer (Base

22

Available at

http://www.actuaries.asn.au/Library/Events/GIS/2014/GIS2014EganEtAlClimateChangePres.

37

Australia Equity Research 13 January 2015

Scenario), and also shows the same information under different future climate change

impacts on Bushfire, Cyclone and Flood perils. The base scenario already shows

substantial variability in the affordability of buildings insurance. To some extent this

affordability is underestimated in the chart, as properties that are currently uninsured

have been excluded from the sample set.

The chart shows that Climate change impacts are likely to be minimal for the median

household as most Australian homes do not have any significant material bushfire,

flood or cyclone risk at the current time. However, the worst affected homes could

see buildings premiums of about 38% of annual income under certain scenarios by

2100. This is a significant affordability problem that impacts homes in high risk

areas. As the real estate saying goes, it’s all about location, location, location.

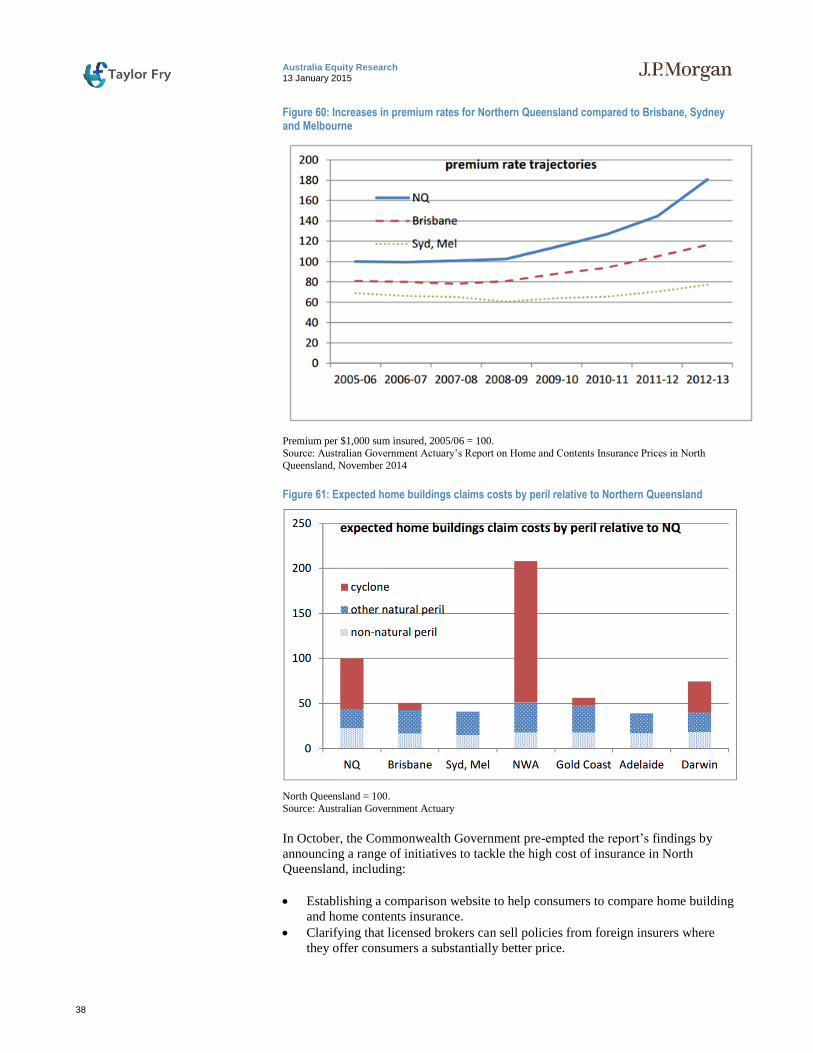

In terms of increases in buildings premiums under the modelled scenarios, over

300,000 households could see a buildings increase of up to 48% by 2100. 60,000-

80,000 households could see increases of up to 104% by 2100. These changes will

exacerbate existing affordability issues.

Political impact of risk pricing vs risk pooling

As increasing amounts of data on natural perils becomes available – in particular