2014 straumann 9-month and third-quarter · pdf file2014 straumann 9-month and third-quarter...

TRANSCRIPT

1

2014 Straumann 9-month and third-quarter results

Basel, 23 October 2014

2

This presentation contains certain forward-looking statements that reflect the current views of management. Such statements are subject to known and unknown risks, uncertainties and other factors that may cause actual results, performance or achievements of the Straumann Group to differ materially from those expressed or implied in this presentation. Straumann is providing the information in this presentation as of this date and does not undertake any obligation to update any statements contained in it as a result of new information, future events or otherwise.

The availability and indications/claims of the products illustrated and mentioned in this presentation may vary according to country.

Disclaimer

HighlightsMarco Gadola, CEO

4

After successful restructuring, Straumann is entering a new phase with cultural change and further adaptation to new market realities

A new phase in Straumann’s development

■ Dr Sandro Matter, EVP Instradent Management & Strategic Alliances, leaves Straumann after 12 years in various leadership roles

■ CFO Thomas Dressendörfer is leaving in June 2015 having had a key role in resizing and restoring profitability

■ Dr Peter Hackel, former CFO of Oerlikon Drive Systems, rejoins Straumann as new CFO

Further expansion

5

9M REVENUE GROWTH REGIONS KEY DRIVERS

+5% Growth in all regions Roxolid SLActive

9M: +5% (organic1) +3% (CHF)Q3: +7% (organic) +6% (CHF)

Double-digit growth in APAC throughout and in N. America in Q3; Europe solid. Best performers: US, China and Japan

Customers convert from titaniumimplants to Roxolid SLActive, drivingvolumes and revenues

FULL SOLUTIONS PENETRATING VALUE OUTLOOK

Portfolio expands Instradent advances Guidance lifted

New prosthetics range, new-generation tapered implant, full regenerative range; innovation leadership

Subsidiary in Italy plans to launch Neodent and Medentika in 2015

Full-year guidance raised to mid-single-digit revenue growth in l.c., with operating profit margin >20%

1 The term ‘organic’ used throughout these documents means ‘excluding the effects of currency fluctuations and M&A.

Business and regional reviewThomas Dressendörfer, CFO

* Straumann, Nobel Biocare, Zimmer Dental, Biomet 3i, Dentsply Implants - based on company and SEC reports as well as management comments.

7

Pace quickens

1Straumann, Nobel Biocare, Zimmer Dental, Biomet 3i, Dentsply Implants, based on company and SEC reports, as well as management comments. 7

-15%

-10%

-5%

0%

5%

10%

Market for tooth replacement & restoration (leading implant companies)Straumann l.c. growth

1

7.3%1.7% 13.8% 13.1%

Change in l.c.

8

All regions contribute to growth

(2.8%)

5.4% in l.c.

In CHF million, rounded

2.6% in CHF

2013 2014

510.0

(13.4)

496.6

4.7

9.5

9.53.1

523.4

Revenue 9M2013

FX Effect Revenue 9M2013 @ FX

2014

Europe North America APAC ROW Revenue 9M2014

Strong performance in N. America; Europe solid

56%

Europe returns to growth; solid Q3 (+3%) despite challenging market environment

Scandinavia and the UK continue to post good results

Germany posts growth; Swiss market declines

2.7%

(1.5%)

4.1%

(1.4%)(3.4%)

0.2%

Q3 2014Q2 2014Q1 2014Q4 2013Q3 2013Q2 2013

Euro

peN

orth

Am

eric

a Double-digit growth returns in Q3, driven by strong demand for implants

Market share gains

Roxolid and SLActive help to win competitor accounts and increase share-of-wallet with existing customers

Revenue change (organic)

27%

9

11.4%

5.4% 5.2%

11.0% 9.1% 10.6%

Q3 2014Q2 2014Q1 2014Q4 2013Q3 2013Q2 2013

53%

Boost from emerging markets and Japan

56%

Dynamic growth driven by China and Japan

General market recovery continues in Japan

Bone level SLActive launched in Japan in Q3

17.0%15.3%

8.3%

16.3%

7.9%

0.9%

Q3 2014Q2 2014Q1 2014Q4 2013Q3 2013Q2 2013

Asi

aPa

cific

Res

t ofW

orld

3.0%9.0%

28.6%

1.8%

35.1%

4.1%

Q3 2014Q2 2014Q1 2014Q4 2013Q3 2013Q2 2013

Modest Q3 reflects high baseline due to exceptional distributor ordersin prior year

Good performances in Brazil and Mexico

Neodent posts low double-digit growth in first nine months

15%

5%

10

Revenue change (organic)

Implants

Strong demand for implants and regenerative products offsets softness in prosthetics

Restorative Regeneratives

1111

Q3 highlights – products & solutions update Marco Gadola, CEO

13

■ Full regenerative portfolio launched

■ Controlled release of Bone Level Tapered Implant

■ Reduced-diameter (3.3mm) PURE ceramic implant launched

Key events used to launch new products and solutions

EAO: 3500 participants

Bone&TissueDays: 800 participants

13

1 US only

Straumann: a full solution provider with a comprehensive regenerative range

Straumann botiss GeistlichBone allografts 1 Bone xenografts Synthetic bone grafts Bone blocks Custom bone blocks Bone rings Collagen cones Fleeces & sponges Membranes 1 Soft-tissue grafts ()Emdogain

14

15

botiss goes Straumann

16

Two new products sold under licence to fill portfolio gaps

Straumann® Membrane Plus™

■ Collagen membrane with convenient handlingand predictable resorption over 6 months

■ Ideal for larger defects requiring longer healing

Straumann® XenoGraft

■ Excellent biocompatibility; optimal calcium-phosphate balance; characteristics comparable to human bone

■ Low crystallinity offers favorable surface for new bone; high porosity supports osteoconduction

■ Gradual resorption - extended volume maintenance

New membrane and xenograft in North America

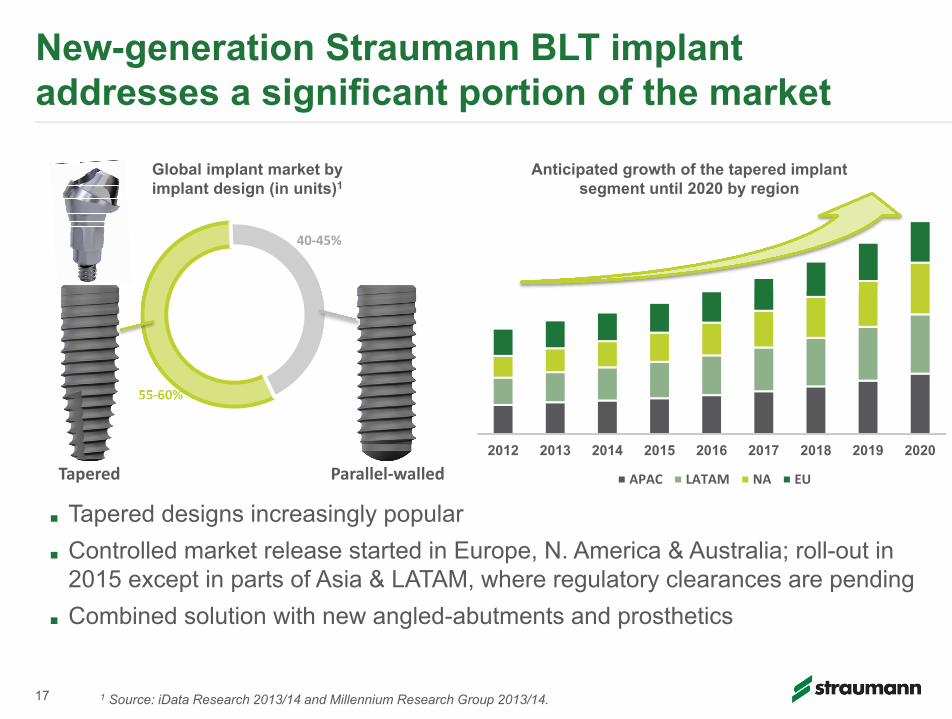

55‐60%

40‐45%

17

New-generation Straumann BLT implant addresses a significant portion of the market

1 Source: iData Research 2013/14 and Millennium Research Group 2013/14.

2012 2013 2014 2015 2016 2017 2018 2019 2020

APAC LATAM NA EU

■ Tapered designs increasingly popular■ Controlled market release started in Europe, N. America & Australia; roll-out in

2015 except in parts of Asia & LATAM, where regulatory clearances are pending ■ Combined solution with new angled-abutments and prosthetics

Parallel‐walledTapered

Global implant market by implant design (in units)1

Anticipated growth of the tapered implant segment until 2020 by region

18

Straumann® Pro Arch™ addresses market needs for immediate fixed edentulous solutions

Protocol developed by Dr. P. Malo in mid 90s

19

■ Createch high-end CADCAM bars and prosthetics are now included in Straumann solutions

Createch prosthetics available to Straumann customers in Europe

Botiss and Createch – partners in Straumann’s common platform for technology & production

20

Broad spectrum of regeneratives to complement implant therapy

High-precision prosthetics to complement CADCAM-based restorations

21

■ ClearChoice Clinical Advisory Board chooses Straumann’s broad range of proven products and cutting-edge technologies

■ Unique Roxolid® SLActive® BLT implant and new prosthetics range important in decision

■ ClearChoice affiliated doctors will also have access to other attractive and effective implant solutions through Straumann’sInstradent platform

■ ClearChoice performs more implant procedures than any other facility or network in the United States

■ Straumann and Instradent ramp up capacity to begin supply in 2015

Straumann to supply ClearChoice

22

■ Designed for metal-free treatments in narrow spaces (e.g. esthetic zone at front of mouth)

■ Complements 4.1mm PURE ceramic implant launched in Q1

■ Innovative manufacturing process; 100% tested in 360°strength test, setting benchmark in reliability

■ 97.6% clinical success & survival rates reported with 4.1mm version1

Small-diameter PURE ceramic implant

1 Gahlert M et al, EAO 2013, Poster 252, Clin. Oral Impl. Res. 24 (Suppl. s9), 2013, p. 123

23

■ Instradent/Neodent operations combined in Iberia■ Instradent subsidiary established in Italy

■ Planned launch of Neodent and Medentika brands early 2015■ Italy = world’s 4th largest market for dental implants (by volume)

■ Instradent USA (formerly Neodent USA) established with a view to including Medentika prosthetics in range early in 2015

Instradent distribution platform expands

24

Instradent goes online

25

Instradent e-shop launched in US

Outlook

27

■ Straumann expects the global implant market to develop positively in 2014.

■ The Group will continue to invest in growth markets and its non-premium offering.

■ Based on its year-to-date performance, it expects full-year revenue to grow in the mid-single-digit range (l.c.).

■ Despite investments, and thanks to its ongoing cost controls, Straumann expects to deliver its operating-profit-margin target of more than 20% already in 2014.

Outlook 2014Barring unforeseen circumstances

27

28

Questions & Answers

Calendar of upcoming events

201423 October Third‐quarter results Webcast

20 November Credit Suisse Swiss Midcap conference Zurich

03 December Berenberg European conference Bagshot/London

04 December Investor meetings London

2015 27 February Full‐year 2014 results Basel HQ

10 April Annual General Meeting Congress Center Basel

2929 Results publication and corporate events. More information on straumann.com → Events

30

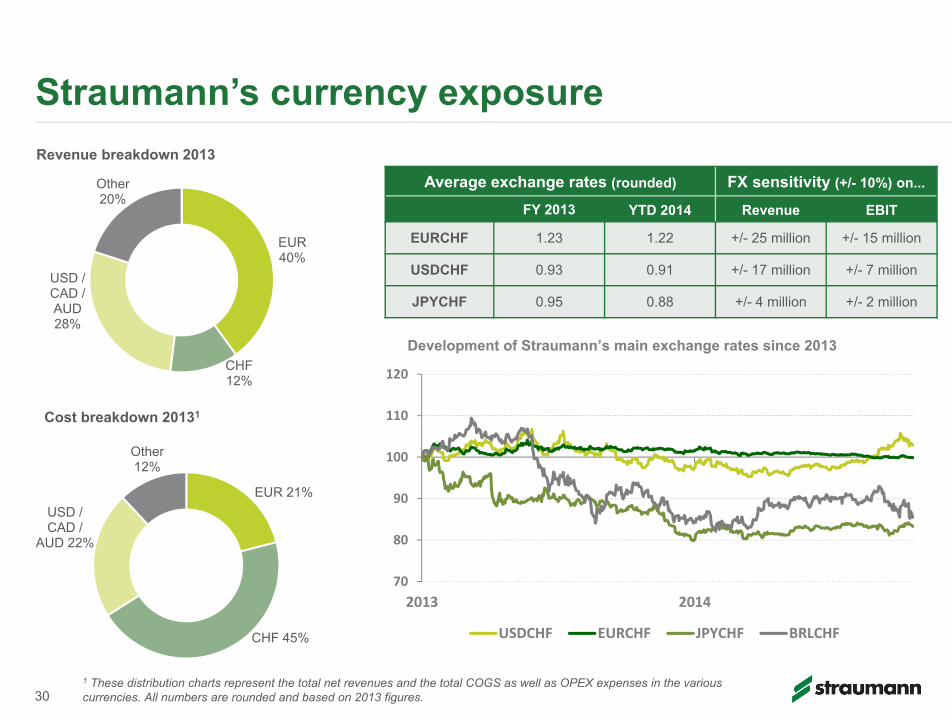

Straumann’s currency exposure

Cost breakdown 20131

Revenue breakdown 2013

1 These distribution charts represent the total net revenues and the total COGS as well as OPEX expenses in the various currencies. All numbers are rounded and based on 2013 figures.

Average exchange rates (rounded) FX sensitivity (+/- 10%) on...

FY 2013 YTD 2014 Revenue EBIT

EURCHF 1.23 1.22 +/- 25 million +/- 15 million

USDCHF 0.93 0.91 +/- 17 million +/- 7 million

JPYCHF 0.95 0.88 +/- 4 million +/- 2 million

30

EUR 40%

CHF 12%

USD / CAD / AUD 28%

Other 20%

EUR 21%

CHF 45%

USD / CAD /

AUD 22%

Other 12%

70

80

90

100

110

120

2013 2014

Development of Straumann’s main exchange rates since 2013

USDCHF EURCHF JPYCHF BRLCHF

Your contacts

Fabian HildbrandCorporate Investor RelationsTel. +41 (0)61 965 13 27Email [email protected]

Mark Hill Thomas KonradCorporate CommunicationsTel. +41 (0)61 965 13 21 Tel. +41 (0)61 965 15 46Email [email protected] Email [email protected]

31

International Headquarters

Institut Straumann AGPeter Merian-Weg 12CH-4002 Basel, SwitzerlandPhone +41(0)61 965 11 11Fax +41(0)61 965 10 01www.straumann.com