2014.11 - apresentação institucional...

TRANSCRIPT

Investor Presentation

November, 2014

1

Gerdau Investment Highlights

Strategy

Agenda

Financial and Operational Highlights

Outlook

Gerdau Investment Highlights

► Global player with dominant regional presence and operations in 14 countries

– Largest long steel producer in the Americas and 2ª globally

► Vertically integrated operations with flexible production processes

A leading low cost producer

► Over 110 years of profitable operations in the steel market

– Not a single yearly loss during its history

Investor Presentation

– A leading low cost producer

► Relevant market share and diversified product offering via downstream and service centers

► Strong balance sheet and cash generation track record

3

► With more than 120,000 shareholders and ADTV of over US$ 80 MM, Gerdau shares are listed on the São Paulo, New York and Madrid stock exchanges

Tata Corus

Evrazholding

Long Steel Producers - Ranking by company (million tonnes)*

Global Player with Dominant Regional Presence

USA. & Canada

Mexico

Dominican Republic

India

SpainArcelor Mittal

Nucor Group

Gerdau

11.0

11.9

18.1

25.5

54.4

Nippon Steel

Source: Steel on the Net*Last information available: 2014

► Largest long steel producer in the Americas and 2nd globally

► Operations in 14 countries with relevant market share

Steel Units

Associated Companies

Joint ventures

Colombia

Peru

Chile

Uruguai

Argentina

Brazil

VenezuelaGuatemala

4Investor Presentation

JFE Steel Group

Hebei Steel

Riva Group

Celsa Group 8.7

8.7

9.1

10.4

10.9

11.0

Gerdau Investment Highlights

Strategy

Agenda

Financial and Operational Highlights

Outlook

Vertically Integrated Operations

Billets

Reheating furnaceFinishing

unitLaying headWire rodDrawing unit

Iron ore Converter

Blast furnace

Continuous casting

LadleScrap

Pig iron

Electric arc furnace

Ladle furnace

Integrated mill

Mini - mill

Rolling mill

Billets

Reheating furnaceFinishing

unitLaying headWire rodDrawing unit

Iron ore Converter

Blast furnace

Continuous casting

LadleScrap

Pig iron

Electric arc furnace

Ladle furnace

Integrated mill

Mini - mill

Rolling mill

► Relevant level of direct purchase and captive scrap (50%)

► 6.3 billion tonnes of iron ore resources

– Self-sufficiency at Ouro Branco mill

► Coke unit and coking coal mine in Colombia

► Partial level of energy self generation

Upstream

Cooling bed

Galvanizing unit

Drawn wire

Nail machine

Welding manufacturing

processes

Cooling bed

Galvanizing unit

Drawn wire

Nail machine

Welding manufacturing

processes

► Focus of Gerdau’s operations

► Low cost structure

► Mini-mills and integrated mills key to low cost strategy

► Latest generation technology

Steel

► Reinforcing steel fabrication facilities (Fab Shops)

► Drawn products

► Multi-product distribution network

► Tailor-made added-value approach (~40% of sales to civil construction)

Downstream

Combination of vertical business model with mini-mills positions Gerdau competitively along the cost curve

6

Products

Brazil North America Special Steel

Ready-to-use products

► Housing► Infrastructure ► Automotive

Billets, blooms& slabs

Merchant bars

Rebars

Fabricated steel

Heavystructural shapes

Wire-rodWires

NailsSBQ

Latin America

► Housing

Consumer Markets

HRC

Iron Ore

► Raw material for

Iron Ore

► Infrastructure

► Industry and commercial buildings

► Agricultural

► Exports of slabs, blooms and billets

► Infrastructure

► Non-residential

► Industrial

► Automotive

► Shipbuilding

► Energy

7

► Housing

► Infrastructure

► Industry and commercial buildings

33% of Net Sales

52% of EBITDA

31% of Net Sales

16% of EBITDA

13% of Net Sales

9% of EBITDA

20% of Net Sales

17% of EBITDA

Note: Net Sales and EBITDA LTM until September.

3% of Net Sales

6% of EBITDA

► Raw material for

the steel industry

Gerdau Investment Highlights

Strategy

Agenda

Financial and Operational Highlights

Outlook

Geographic diversification reduces volatility in results

Consolidated EBITDA & EBITDA Margin

EBITDA LTM: R$ 4,960 million

1,413 1,3701,196 1,170 1,224

13.5% 13.3%11.3% 11.2% 11.4%

3Q13 4Q13 1Q14 2Q14 3Q14

EBITDA and EBITDA margin per BO

9

EBITDA (R$ million) EBITDA Margin (%) Participation of EBITDA per BO (last 12 months)

131 109 109

9,2% 8,4%7,6%

3Q13 2Q14 3Q14

Latin America BO

Brazil BO North America BO

933

598 587

23,5%

17,4%16,5%

3Q13 2Q14 3Q14

129

281 337

3,7%

7,8%9,1%

3Q13 2Q14 3Q14

273 230 231

13,3%

10,5% 11,0%

3Q13 2Q14 3Q14

49 53 10

38,6%

24,5%

4,8%

3Q13 2Q14 3Q14

EBITDA and EBITDA margin per BO

Special Steel BO

Iron OreBO

15.516.3 16.4 16.4

18.1

2.8x2.5x 2.5x 2.4x

2.7x

Debt Maturity Schedule

R$ billionR$ billion

Debt and Leverage Ratio

Debt impacted by exchange variation

3.0

11.2

3.5 4.2 3.5 4.0 4.7

sep.13 dec.13 mar.14 jun.14 sep.14

Gross Debt Principal (R$ billion) Cash (R$ billion) Net Debt/EBITDA¹

(1) EBITDA LTM.

10

Average Debt Term: 7.2 yearsAverage Debt Cost: 6.5%

Average debt term of over 7 years

0.3 1.4 0.8 0.7 0.7

4Q14 2015 2016 2017 2018 2019 2020 and after

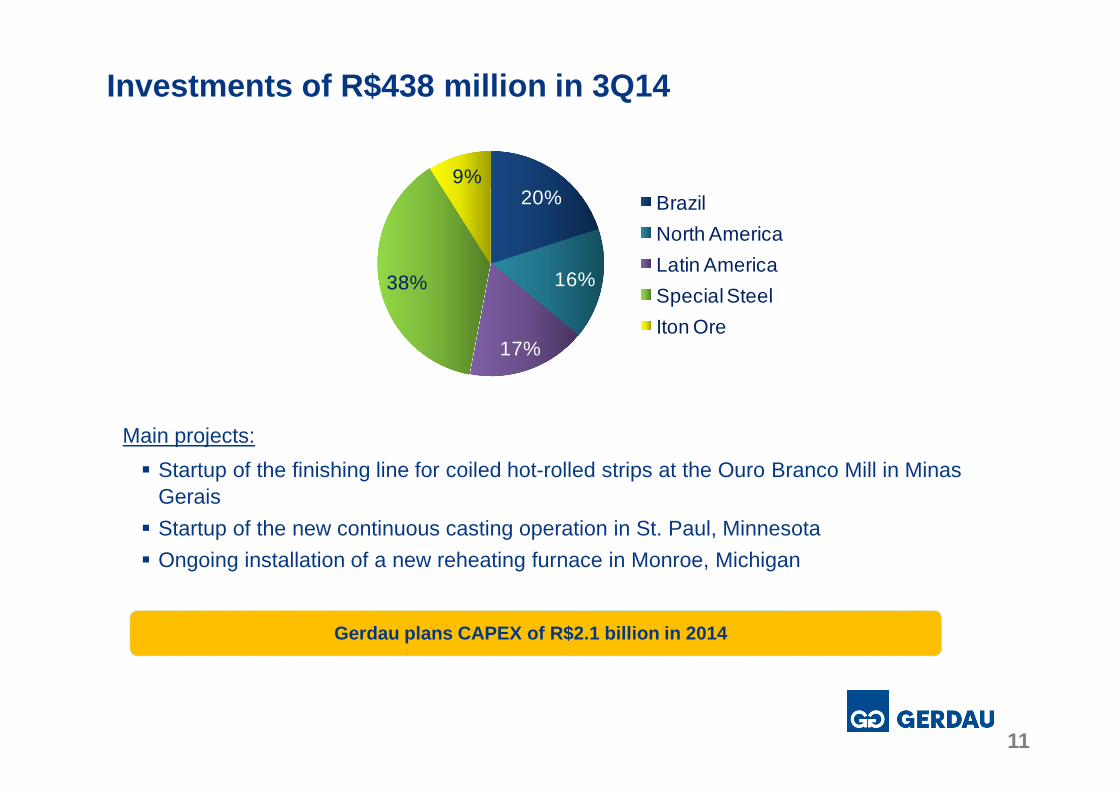

Investments of R$438 million in 3Q14

20%

16%

17%

38%

9%Brazil

North America

Latin America

Special Steel

Iton Ore

Main projects:

� Startup of the finishing line for coiled hot-rolled strips at the Ouro Branco Mill in Minas Gerais

� Startup of the new continuous casting operation in St. Paul, Minnesota

� Ongoing installation of a new reheating furnace in Monroe, Michigan

11

Gerdau plans CAPEX of R$2.1 billion in 2014

Gerdau Investment Highlights

Strategy

Agenda

Financial and Operational Highlights

Outlook

R$ 45 BnR$ 91 Bn (R$ 56 Bn in

5 years and R$ 35 Bn in 25 years)–10,000 Km

R$ 5.5 Bn (PAC 2)*+ concessions

R$ 55 Bn (until 2020)

R$ 42 Bn (R$ 24 Bn in 5 years and R$ 19 Bn in

R$40 Bn (R$ 25 Bn already invested and

Brazil Business Operation

Key Investments in Infrastructure

PORTS

AIRPORTS

RAILROADS

HPP’s

HPP’s: outlook for demand in the sector (tonnes)

98.033 97.11198,033 99,488 97,111

1.5% -2.4%

years and R$ 19 Bn in20 years)–7,5 thousand Km

already invested and R$15 Bn until 2020)

13

► Concession of Guarulhos, Viracopos, Galeãoand Confins airports

► Privatization and construction of roads, railways, ports and airports aiming to upgrade the country’s infrastructure

► High investments in energy generation to supply increasing consumption demand

ROADS WIND FARMS

*Programa de Aceleração do Crescimento II (Brazil Federal Government package of infrastructure investments)

Main projects in progress

2013 2014 2015

ENTERPRISE ST VOLUME PERIOD

UHE TELES PIRES MT 45,000 2011 - 2015

UHE BELO MONTE RO 68,000 2012 -2018

North America Business Operation

Manufacturing and Non Manufacturing IndexesInstitute of Supply Management (ISM): jan.03 through sep.14Home Prices and Foreclosures

► US GDP forecasted growth for 2015: +3.1%

Source: FMI, S&P Case-Shiller (prices), RealtyTrac (foreclosures) and ISM.

14

Latin America Business Operation

► Latin America GDP forecasted growth for 2015: +2.2%

Apparent finished steel use (Mt)

+2.6% +4.6%

► 2 plants► Access to the U.S.

market► New structural profile

rolling mill (2014)

Mexico

Colombia5.8 5.96.0

42.6 43.745.7

Others

15

Source: FMI and worldsteel (SRO oct.14).

► Coal resources and coke production

Colombia

► Excellent logistics► Strong growth

Peru

► Mature market► Good distribution network

Chile5.1 4.7 4.82.7 2.6 2.63.5 3.9 4.02.9 3.0 3.12.8 2.7 3.4

19.7 21.0 21.8

5.8 5.9

2013 2014 (f) 2015 (f)

Mexico

Venezuela

Peru

Colombia

Chile

Argentina

Special Steel Business Operation

► Global Coverage ► Second largest producer worldwide

1,500 kgNAFTA: Total Light Vehicle Production

16

150 kg

NAFTA: Automotive Production

Source: Wards Automotive .

Units (thousand) Growth

Units (thousand) Growth

NAFTA 4,135 6.2% 16,692 5.1%

US 2,814 8.6% 11,304 6.9%

Canada 528 -6.8% 2,314 -2.3%

Mexico 792 7.8% 3,073 4.4%

Total Autos and Light Trucks

3 months through september 12months through september

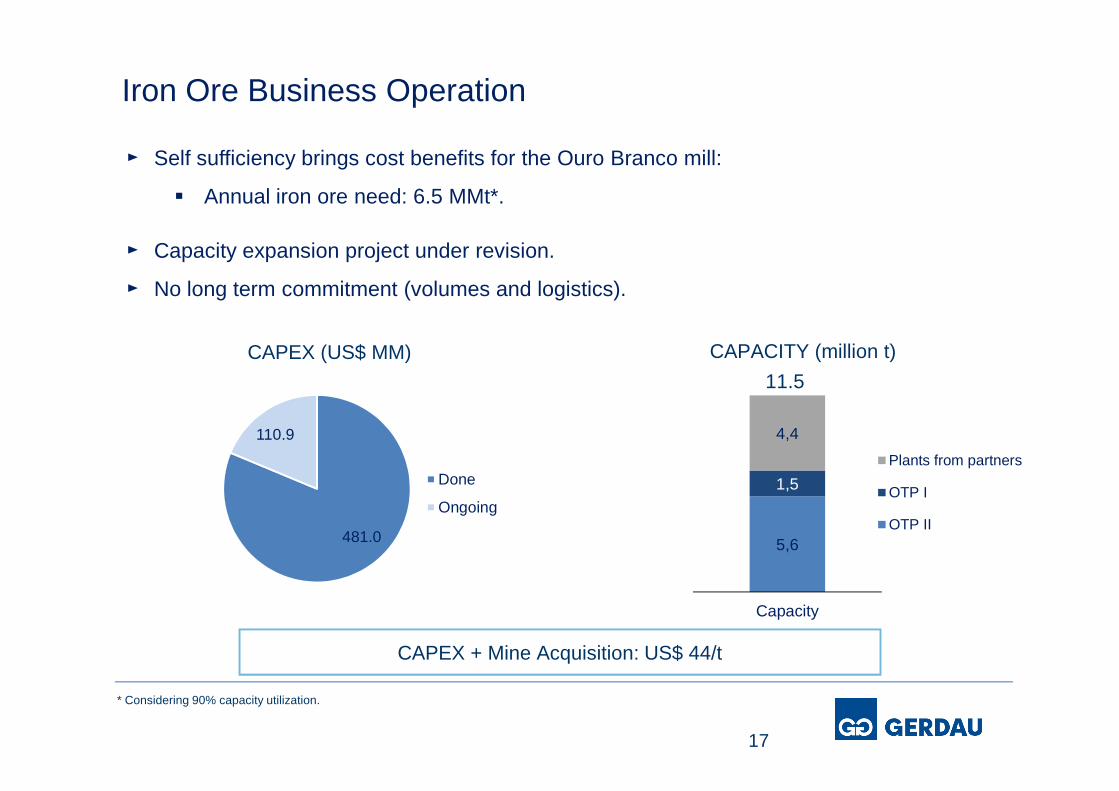

Iron Ore Business Operation

CAPEX (US$ MM) CAPACITY (million t)

11.5

► Self sufficiency brings cost benefits for the Ouro Branco mill:

� Annual iron ore need: 6.5 MMt*.

► Capacity expansion project under revision.

► No long term commitment (volumes and logistics).

5,6

1,5

4,4

Capacity

Plants from partners

OTP I

OTP II

17

CAPEX + Mine Acquisition: US$ 44/t

481.0

110.9

Done

Ongoing

* Considering 90% capacity utilization.

This presentation may contain forward-looking statements. These forward-looking

statements rely upon estimates, information or methods that may be incorrect or

inaccurate and may not actually occur. These estimates are also subject to risks,

uncertainties and assumptions, including, among others: general economic, political

and commercial conditions in Brazil and in the markets where we operate and existing

and future government regulations. Potential investors are hereby informed that these

estimates do not constitute a guarantee of future performance as they involve risks and

Statement

18

estimates do not constitute a guarantee of future performance as they involve risks and

uncertainties. The Company does not undertake, and specifically denies, any obligation

to update any estimate, which only speak as of the date they are made.

Investor Presentation