2015 budget seminar...(i) investment allowance – energy efficiency schemes(ia-ee) current 1. ia-ee...

TRANSCRIPT

2015 Budget SeminarSolving tomorrow’s problems today

Florence LohPartner, Corporate Tax

www.pwc.com/sg

PwC

Agenda

1. Extended help on rising business costs– Transition Support Package

2. Innovation and internationalisation – Mergers & Acquisitions

– International Growth Scheme

– Double Tax Deduction for Internationalisation

3. Rationalisation and review

2

Extended help on rising business costs

3

PwC

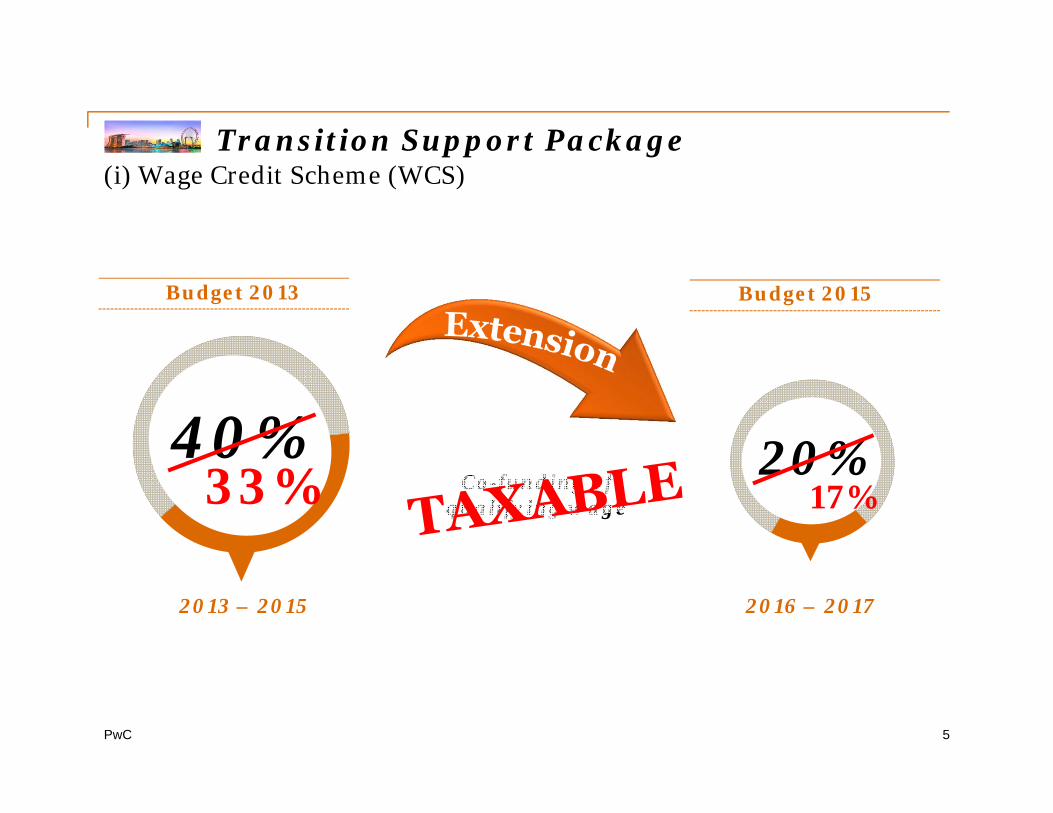

Transition Support Package(i) Wage Credit Scheme (WCS)

4

Budget 2013

2013 – 2015

40% 20%

2016 – 2017

Co-funding of qualifying wage

Budget 2015

PwC

Transition Support Package(i) Wage Credit Scheme (WCS)

5

Budget 2013

2013 – 2015

40% 20%

2016 – 2017

Co-funding of qualifying wage

Budget 2015

33% 17%

PwC

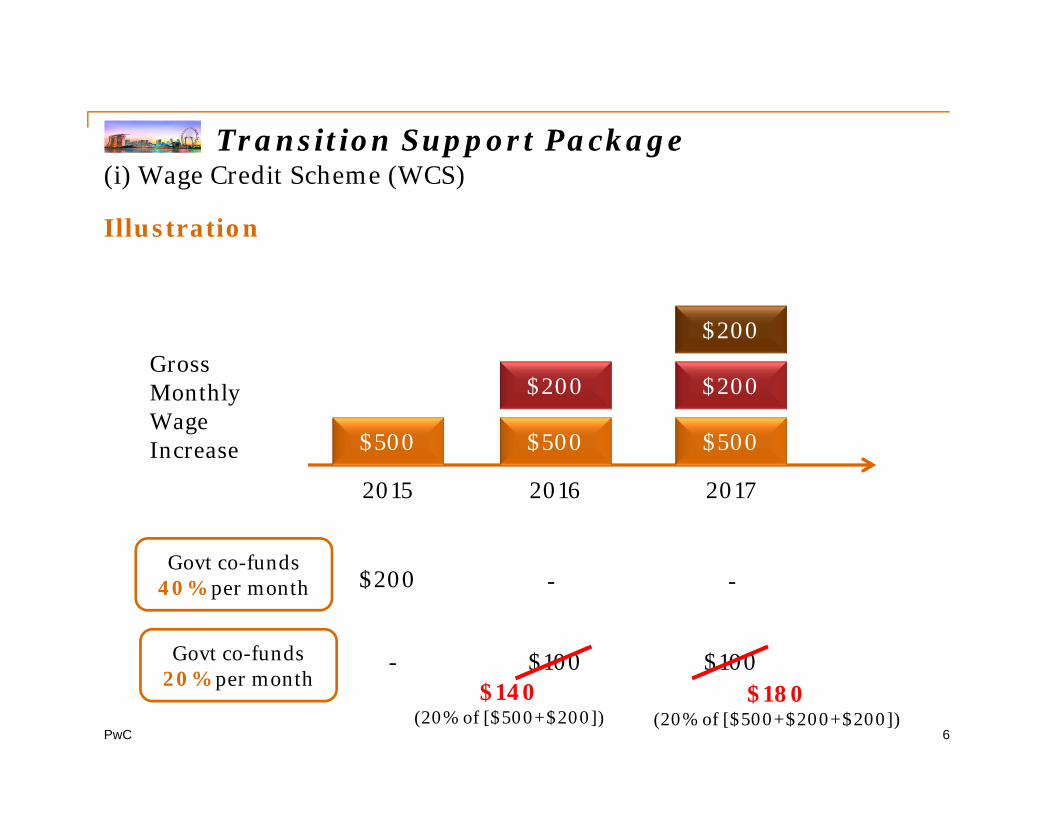

Transition Support Package(i) Wage Credit Scheme (WCS)

6

Illustration

Gross Monthly Wage Increase $500 $500

$200

$500

$200

$200

2015 2016 2017

Govt co-funds 40% per month $200

$140(20% of [$500+$200])

$180(20% of [$500+$200+$200])

Govt co-funds 20% per month

- -

- $100 $100

PwC

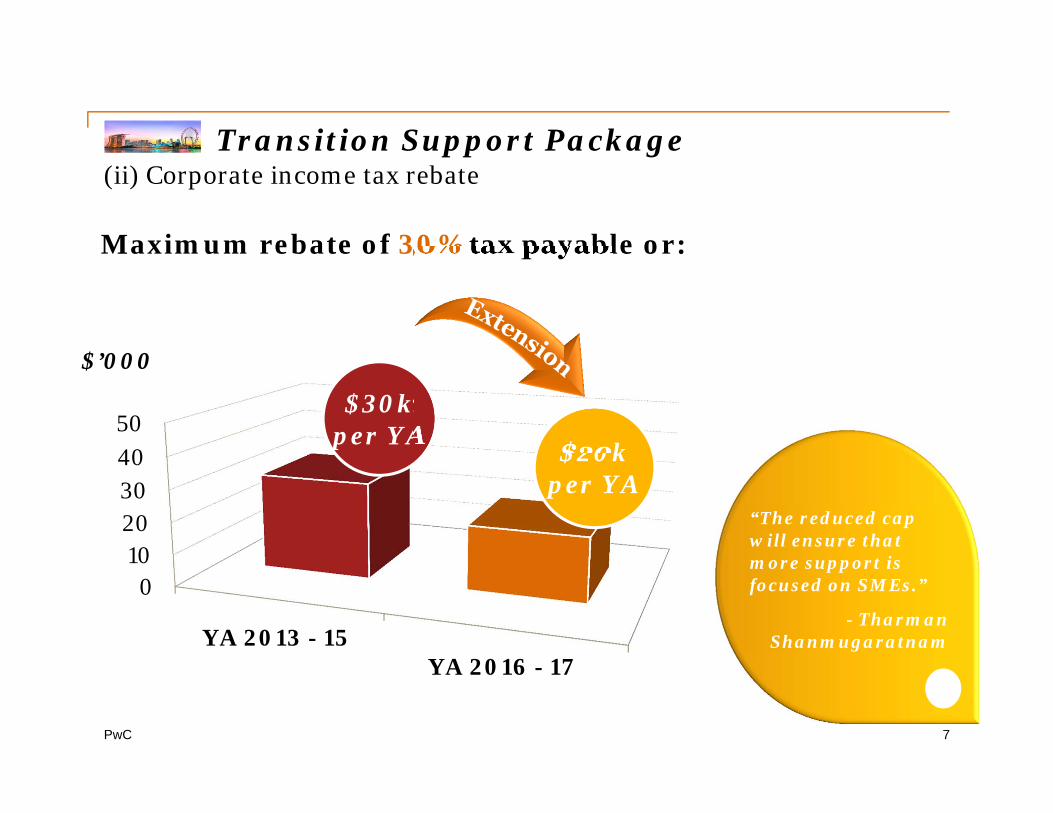

Transition Support Package(ii) Corporate income tax rebate

7

01020304050

YA 2013 - 15YA 2016 - 17

Maximum rebate of 30% tax payable or:

$30kper YA $20k

per YA

$’000

“The reduced cap will ensure that more support is focused on SMEs.”

- TharmanShanmugaratnam

PwC

Transition Support Package(iii) Productivity and innovation credit (PIC) bonus

8

• Dollar-for-dollar matching cash bonus for YAs 2013 to 2015

• Overall combined cap of $15,000 for 3 YAs

PIC Bonus

PwC

Transition Support Package(iii) Productivity and innovation credit (PIC) bonus

9

• Dollar-for-dollar matching cash bonus for YAs 2013 to 2015

• Overall combined cap of $15,000 for 3 YAs

PwC

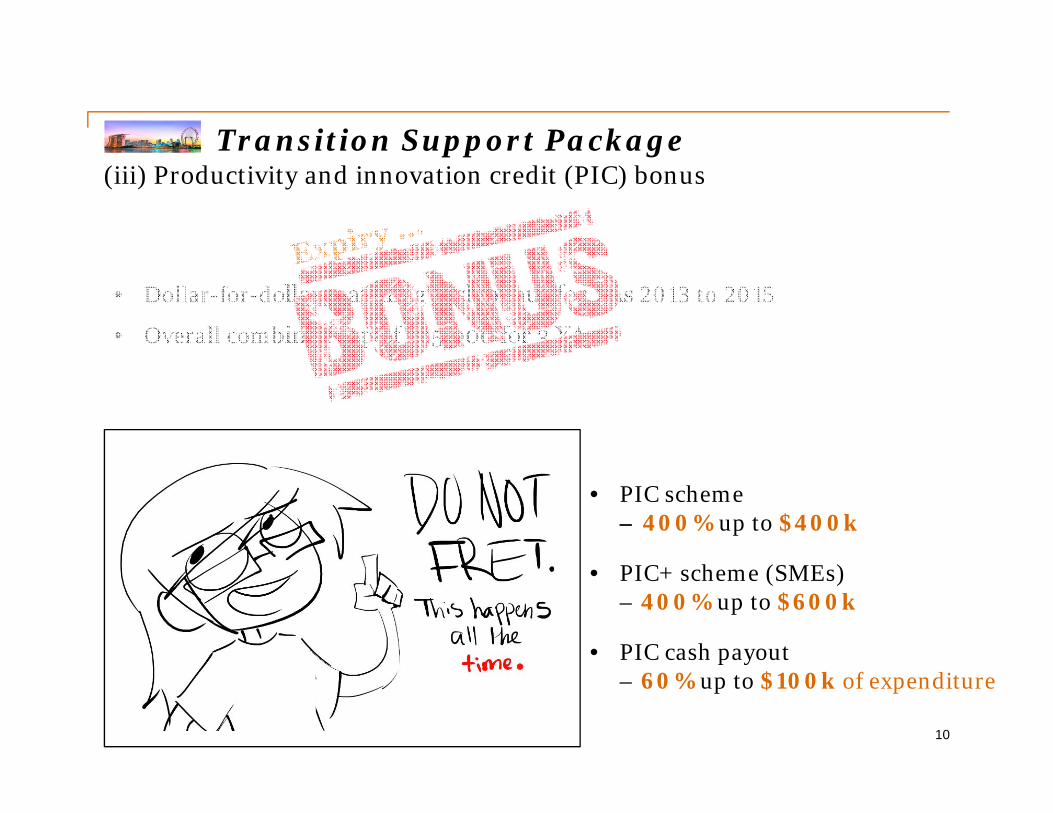

Transition Support Package(iii) Productivity and innovation credit (PIC) bonus

10

• Dollar-for-dollar matching cash bonus for YAs 2013 to 2015

• Overall combined cap of $15,000 for 3 YAs

• PIC scheme – 400% up to $400k

• PIC+ scheme (SMEs) – 400% up to $600k

• PIC cash payout– 60% up to $100k of expenditure

PwC

Transition Support Package(iii) Productivity and innovation credit (PIC) bonus

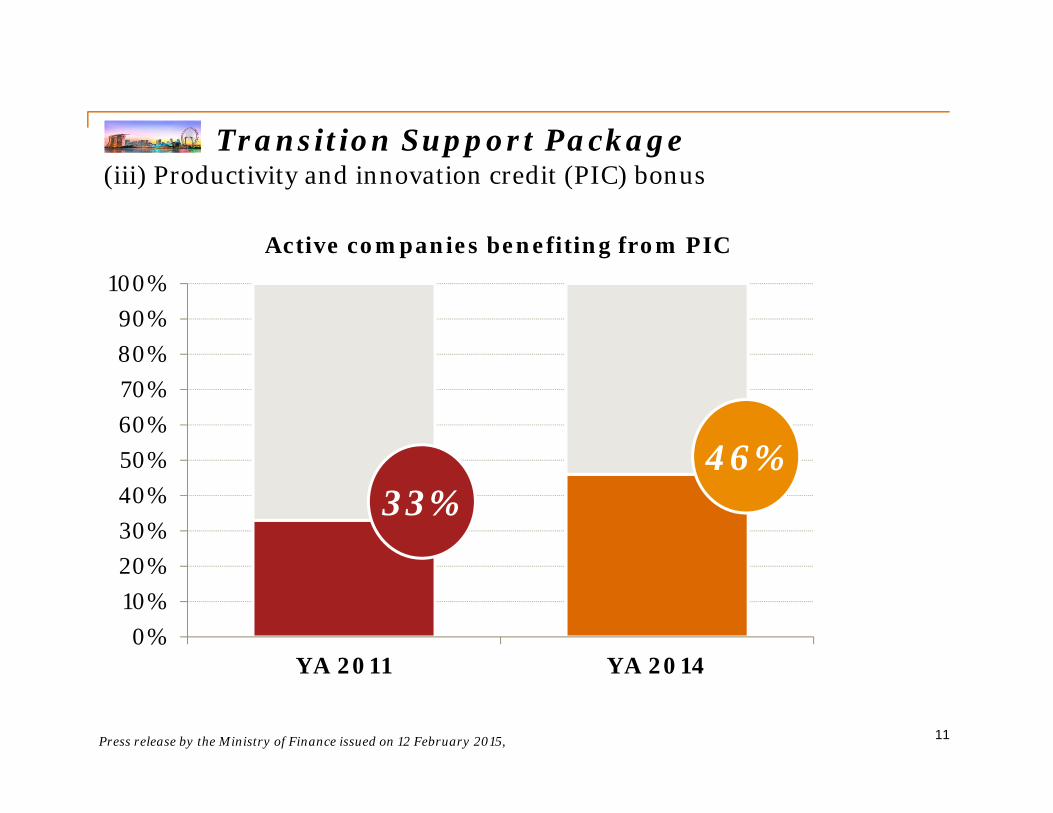

11

0%10%20%30%40%50%60%70%80%90%

100%

YA 2011 YA 2014

33%46%

Active companies benefiting from PIC

Press release by the Ministry of Finance issued on 12 February 2015,

Innovation & Internationalisation

12

PwC

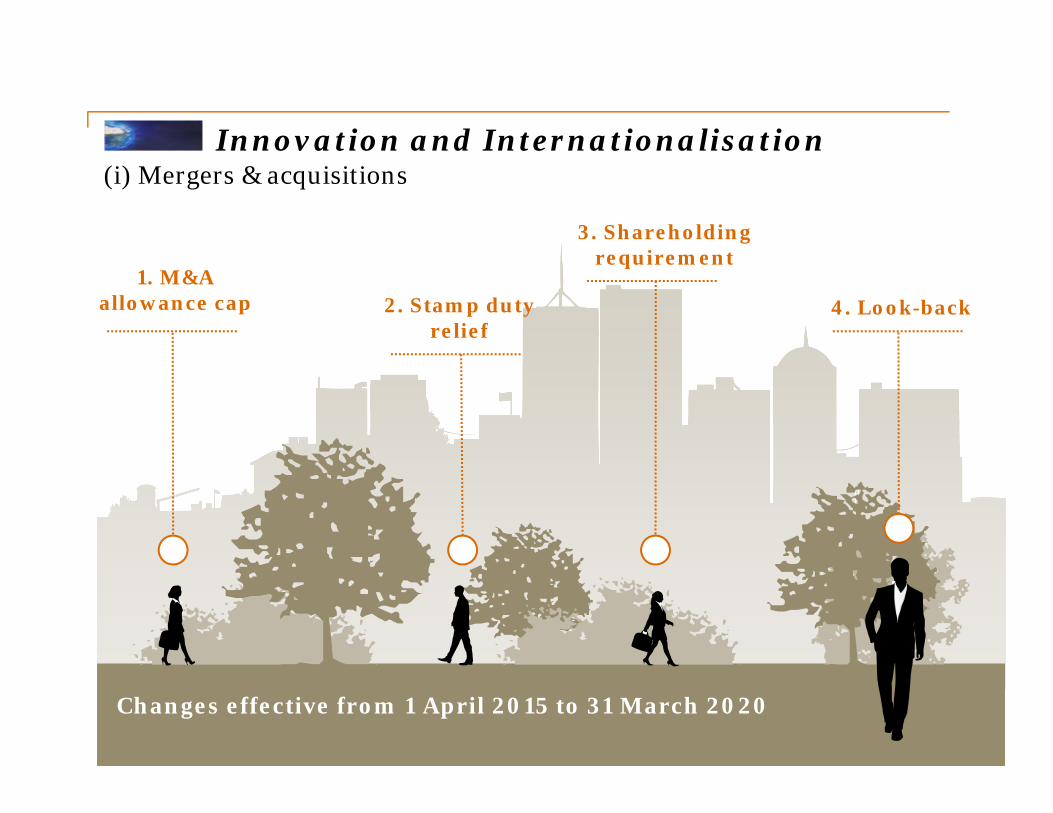

Innovation and Internationalisation(i) Mergers & acquisitions

13

“Singapore M&A deals see 35% increase in value…

hitting US$50.7bn.” Channel NewsAsia

11 Dec 2014

PwC

Innovation and Internationalisation(i) Mergers & acquisitions

14

1. M&A allowance cap 2. Stamp duty

relief

3. Shareholding requirement

4. Look-back

Changes effective from 1 April 2015 to 31 March 2020

PwC

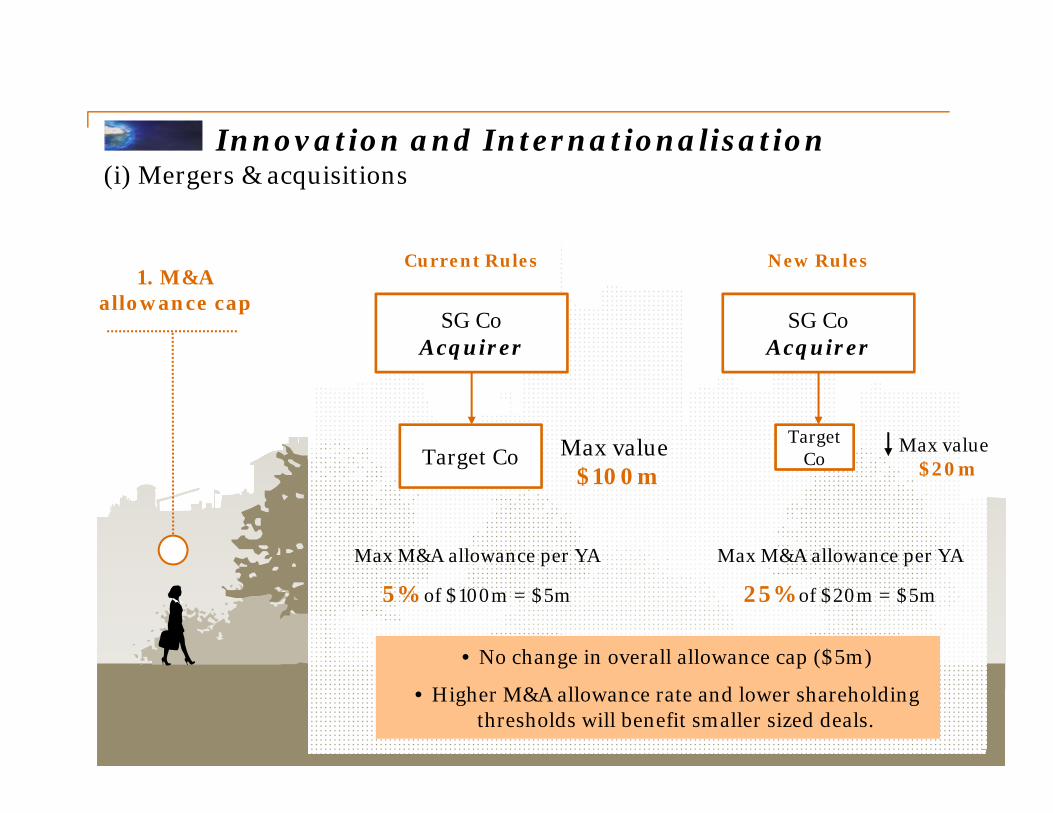

Innovation and Internationalisation(i) Mergers & acquisitions

15

1. M&A allowance cap

SG CoAcquirer

Target Co Max value $100m

Current Rules

Max M&A allowance per YA

5% of $100m = $5m

SG CoAcquirer

Target Co

New Rules

Max M&A allowance per YA

25% of $20m = $5m

• No change in overall allowance cap ($5m)

• Higher M&A allowance rate and lower shareholding thresholds will benefit smaller sized deals.

Max value $20m

PwC

Innovation and Internationalisation(i) Mergers & acquisitions

16

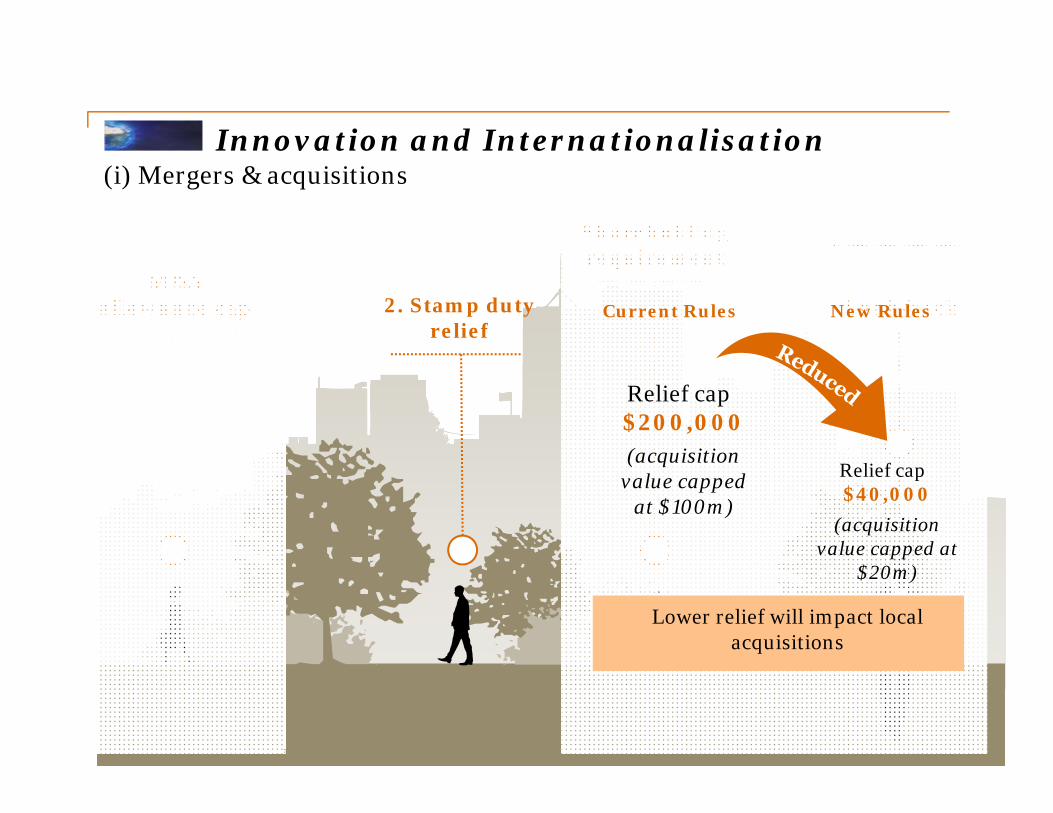

M&A allowance cap 2. Stamp duty

relief

Shareholding requirement

Look-back

Lower relief will impact local acquisitions

Current Rules New Rules

Relief cap $200,000(acquisition

value capped at $100m)

Relief cap $40,000

(acquisition value capped at

$20m)

PwC

Innovation and Internationalisation(i) Mergers & acquisitions

17

M&A allowance cap

Stamp duty relief

3. Shareholding requirement

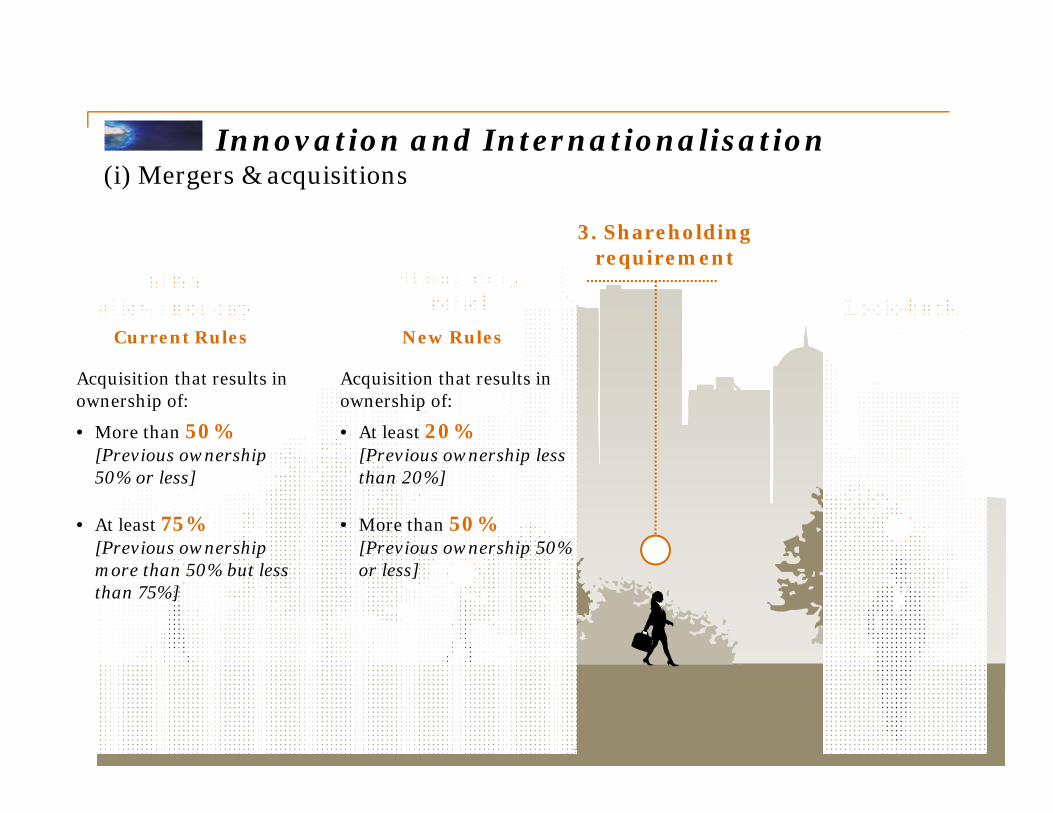

Look-backCurrent Rules New Rules

Acquisition that results in ownership of:

• At least 20%[Previous ownership less than 20%]

• More than 50%[Previous ownership 50% or less]

Acquisition that results in ownership of:

• More than 50% [Previous ownership 50% or less]

• At least 75%[Previous ownership more than 50% but less than 75%]

PwC

Innovation and Internationalisation(i) Mergers & acquisitions

18

M&A allowance cap

Stamp duty relief

3. Shareholding requirement

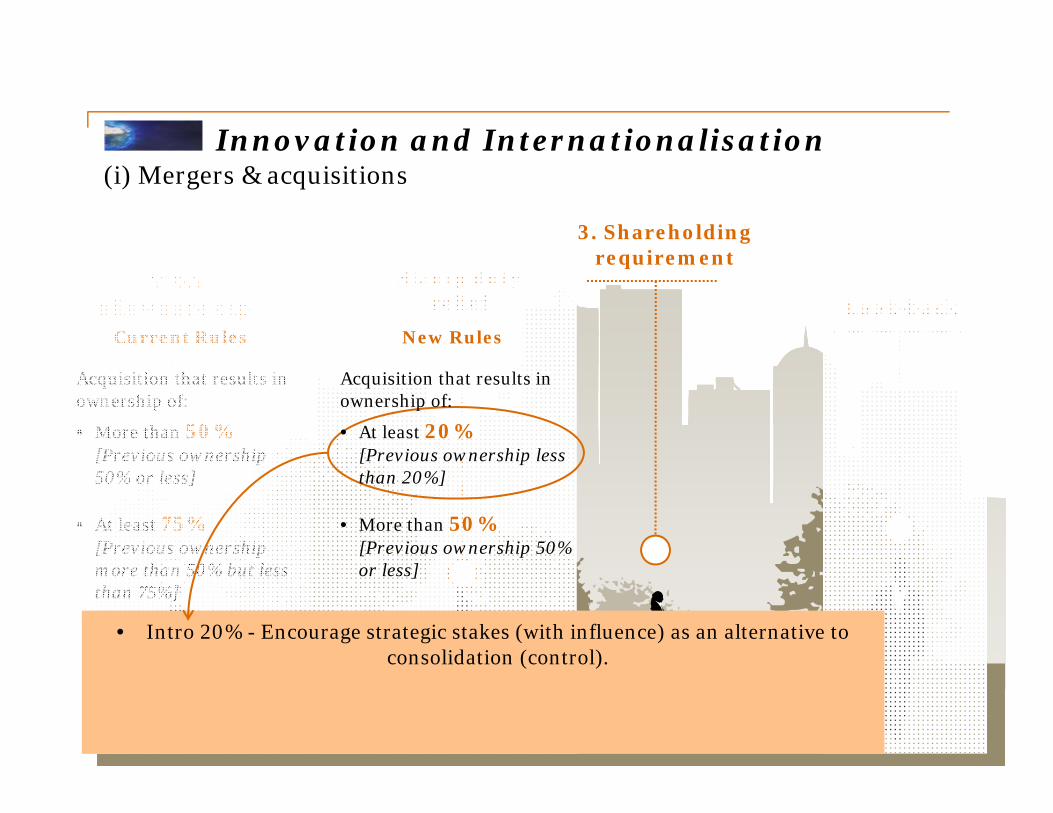

Look-backCurrent Rules New Rules

Acquisition that results in ownership of:

• At least 20%[Previous ownership less than 20%]

• More than 50%[Previous ownership 50% or less]

Acquisition that results in ownership of:

• More than 50% [Previous ownership 50% or less]

• At least 75%[Previous ownership more than 50% but less than 75%]

IRAS – additional conditions:

The acquiring company must have:

(i) At least 1 directorrepresented on the Board of Directors of the target company; and

(ii) Acquired a shareholding of at least 20% in the target company and that company is considered an associate of the acquiring company under Singapore FRS rules.

PwC

Innovation and Internationalisation(i) Mergers & acquisitions

19

M&A allowance cap

Stamp duty relief

3. Shareholding requirement

Look-back

• Intro 20% - Encourage strategic stakes (with influence) as an alternative to consolidation (control).

Current Rules New Rules

Acquisition that results in ownership of:

• At least 20%[Previous ownership less than 20%]

• More than 50%[Previous ownership 50% or less]

Acquisition that results in ownership of:

• More than 50% [Previous ownership 50% or less]

• At least 75%[Previous ownership more than 50% but less than 75%]

PwC

Innovation and Internationalisation(i) Mergers & acquisitions

20

M&A allowance cap

Stamp duty relief

3. Shareholding requirement

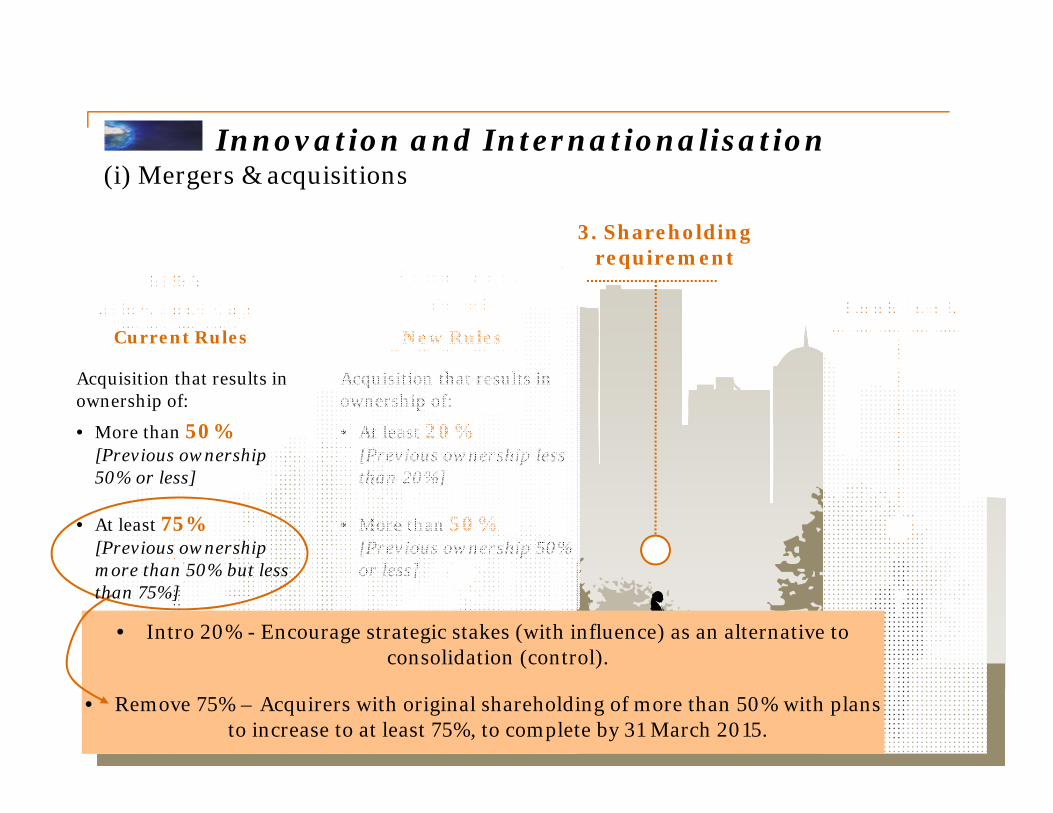

Look-back

• Intro 20% - Encourage strategic stakes (with influence) as an alternative to consolidation (control).

• Remove 75% – Acquirers with original shareholding of more than 50% with plans to increase to at least 75%, to complete by 31 March 2015.

Current Rules New Rules

Acquisition that results in ownership of:

• At least 20%[Previous ownership less than 20%]

• More than 50%[Previous ownership 50% or less]

Acquisition that results in ownership of:

• More than 50% [Previous ownership 50% or less]

• At least 75%[Previous ownership more than 50% but less than 75%]

PwC

Innovation and Internationalisation(i) Mergers & acquisitions

21

M&A allowance cap Stamp duty

relief

Shareholding requirement

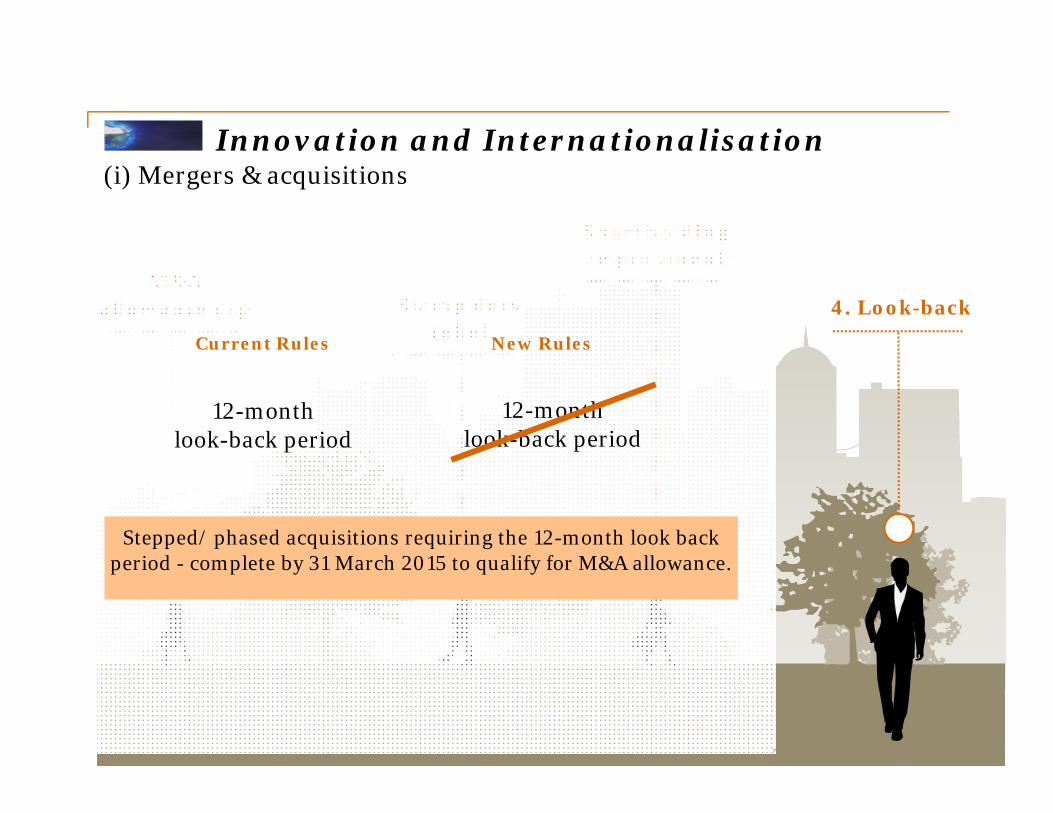

4. Look-back

Stepped/ phased acquisitions requiring the 12-month look back period - complete by 31 March 2015 to qualify for M&A allowance.

Current Rules New Rules

12-monthlook-back period

12-monthlook-back period

PwC

Innovation and Internationalisation(ii) Double tax deduction for internationalisation (DTD)

22

Current scheme

• 200% tax deduction for qualifying expenses for qualifyingmarket expansion & investment development activities.

• Approval from IE Singapore.

• Automatic deduction up to $100,000 per YA for certain qualifying activities

PwC

Innovation and Internationalisation(ii) Double tax deduction for internationalisation (DTD)

23

airfare hotel

meals roadshows

freight consultants

ExamplesCurrent scheme

• 200% tax deduction for qualifying expenses for qualifyingmarket expansion & investment development activities.

• Approval from IE Singapore.

• Automatic deduction up to $100,000 per YA for certain qualifying activities

Budget 2012 enhancement

(i) Overseas trips/ missions for• business development• investment study• trade fairs

(ii) Local trade fairs approved by IE Singapore or STB

PwC

Innovation and Internationalisation(ii) Double tax deduction for internationalisation (DTD)

24

Enhancement

• Qualifying manpower expenses (1 July 2015 to 31 March 2020) for Singaporeans posted to new overseas entities

• Capped at $1 million per approved entity per year

• Approval from IE Singapore

Clarity by May 2015 ?

• “Overseas entities” – representative offices, branches, companies, partnerships, joint ventures ?

• “Qualifying manpower expenses”- where costs are borne by the overseas entities?- where costs are recharged by the overseas entities?- where partial costs are absorbed by Singapore entity?

PwC

Innovation and Internationalisation(iii) International Growth Scheme

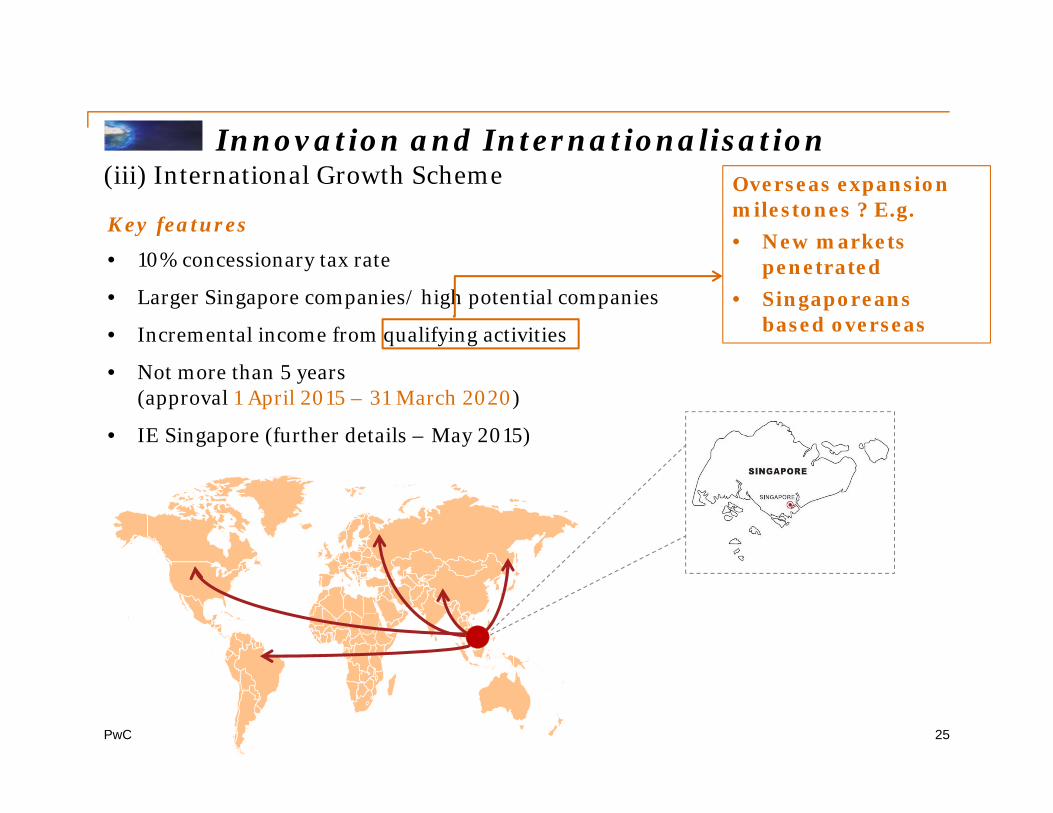

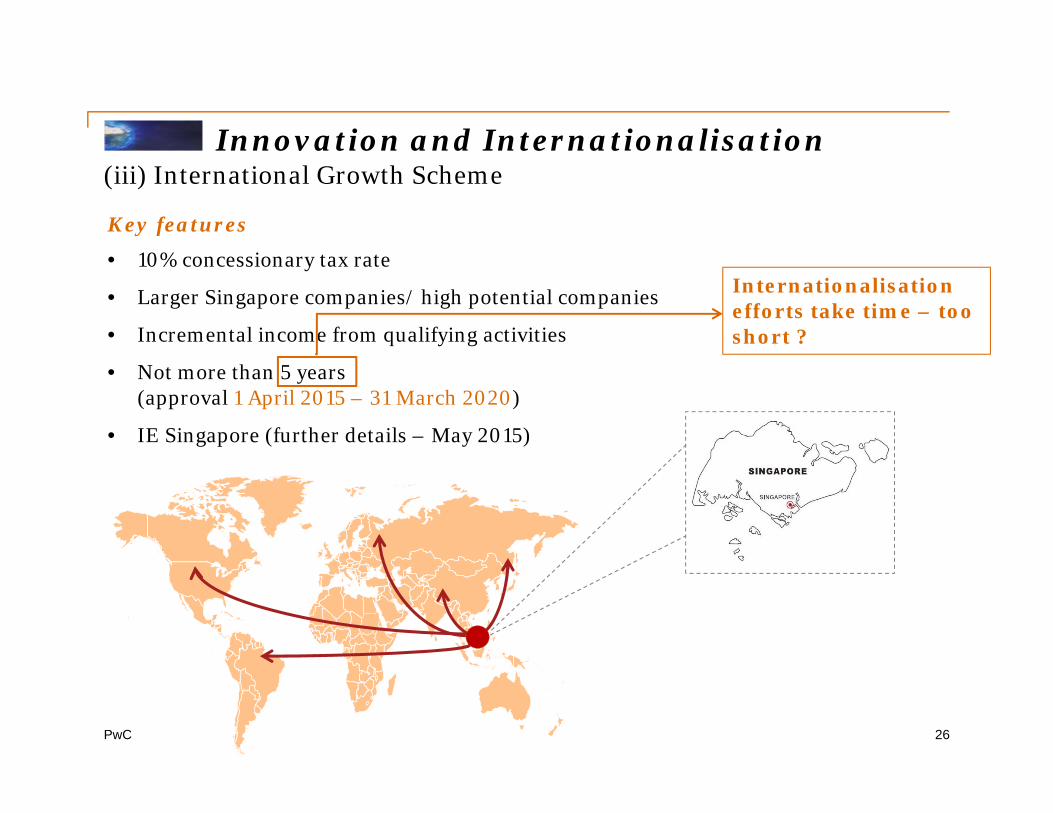

Key features

• 10% concessionary tax rate

• Larger Singapore companies/ high potential companies

• Incremental income from qualifying activities

• Not more than 5 years (approval 1 April 2015 – 31 March 2020)

• IE Singapore (further details – May 2015)

25

Overseas expansion milestones ? E.g. • New markets

penetrated• Singaporeans

based overseas

PwC

Innovation and Internationalisation(iii) International Growth Scheme

Key features

• 10% concessionary tax rate

• Larger Singapore companies/ high potential companies

• Incremental income from qualifying activities

• Not more than 5 years (approval 1 April 2015 – 31 March 2020)

• IE Singapore (further details – May 2015)

26

Internationalisationefforts take time – too short ?

Rationalisation and Review

27

PwC

Rationalisation and Review(i) Investment allowance – energy efficiency schemes(IA-EE)

Current

1. IA-EE Scheme –

2. IA-EE for Green Data Centres Scheme –

Both scheduled to lapse after 31 March 2015

28

New

• From 1 March 2015 – The two schemes will be combined into one scheme, “IA-EE scheme”.

• Extended to 31 March 2021

•

PwC

Rationalisation and Review(ii) International telecommunications submarine cable system

Current

• Section 19D

• Writing down allowances for capital expenditure incurred on the acquisition of an IRU of any international telecommunications submarine cable system

29

New

• Review date – 31 December 2020

PwC

Rationalisation and Review(iii)Approved Foreign Loan (AFL) and Approved Royalties Incentive (ARI)

Current

• ARI – tax exemption or concessionary rateApproved royalties, technical assistance fees or contributions to R&D costs made to non-tax residents for providing cutting-edge technology and know-how

• AFL incentive – tax exemption or concessionary rateInterest payments made to non-tax residents for loans to purchase productive equipment. Minimum loan quantum $200,000.

30

New

• The minimum loan quantum under the AFL incentive will be $20 million from 24 February 2015. Other loan quantums may be approved by the Minister for Trade and Industry

• Review date – 31 December 2023

PwC

Rationalisation and Review(iii) Phasing out

Offshore leasing – withdrawn from 1 January 2016

• 10% concessionary tax rate on income derived by a leasing company in respect of offshore leasing of machinery and plant

31

Operational headquarters – withdrawn from 1 October 2015

• Scheme was introduced to encourage companies to use Singapore as a base to conduct headquarter management activities by providing tax exemption or a concessionary tax rate of 10% on income from qualifying HQ services

• HQ companies may still qualify for DEI, subject to conditions

Royalties – withdrawn from YA 2017

• Section 10(16) of the ITA provides a tax concession on royalties and other payments from approved intellectual property or innovation

PwC

Concluding …

32

PwC

What colour is this dress?

33

White & Gold Blue & Black

PwC

What colour is Budget 2015?

34

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers Services LLP, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2015 PricewaterhouseCoopers Services LLP. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers Services LLP which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.

Your PwC Contacts

Florence Loh

Partner Corporate [email protected]+65 6236 3368

Florence Loh

Partner Corporate [email protected]+65 6236 3368

Florence Loh

Partner Corporate [email protected]+65 6236 3368