2015 january investor presentation

TRANSCRIPT

Investor Presentation

January 2015

Non-GAAP Financial Measures

SemGroup

Adjusted EBITDA is presented in this presentation for certain periods. Adjusted EBITDA is not a U.S. generally accepted accounting principles (“GAAP”) measure

and is not intended to be used in lieu of a GAAP presentation of net income (loss). Adjusted EBITDA is presented in this presentation because SemGroup believes

it provides additional information with respect to its performance. Adjusted EBITDA represents earnings before interest, taxes, depreciation and amortization,

adjusted for selected items that SemGroup believes impact the comparability of financial results between reporting periods. Although SemGroup presents selected

items that it considers in evaluating its performance, you should also be aware that the items presented do not represent all items that affect comparability between

the periods presented. Variations in SemGroup’s operating results are also caused by changes in volumes, prices, exchange rates, mechanical interruptions and

numerous other factors. These types of variances are not separately identified in this presentation. Because all companies do not use identical calculations,

SemGroup’s presentation of Adjusted EBITDA may be different from similarly titled measures of other companies, thereby diminishing its utility. Reconciliations of

net income (loss) to Adjusted EBITDA for the periods presented are included on our website.

Rose Rock Midstream

This presentation includes the non-GAAP financial measures of Adjusted gross margin, Adjusted EBITDA and distributable cash flow, which may be used

periodically by management when discussing our financial results with investors and analysts. Our website provides reconciliations of these non-GAAP financial

measures to their most directly comparable financial measures calculated and presented in accordance with GAAP. Adjusted gross margin, Adjusted EBITDA and

distributable cash flow are presented as management believes they provide additional information and metrics relative to the performance of our business.

Operating income (loss) is the GAAP measure most directly comparable to Adjusted gross margin, net income (loss) and cash provided by (used in) operating

activities are the GAAP measures most directly comparable to Adjusted EBITDA, and net income (loss) is the GAAP measure most directly comparable to

distributable cash flow. Our non-GAAP financial measures should not be considered as alternatives to the most directly comparable GAAP financial measures.

These non-GAAP financial measures have important limitations as analytical tools because they exclude some, but not all, items that affect the most directly

comparable GAAP financial measures. You should not consider Adjusted gross margin, Adjusted EBITDA or distributable cash flow in isolation or as substitutes for

analysis of our results as reported under GAAP. Because Adjusted gross margin, Adjusted EBITDA and distributable cash flow may be defined differently by other

companies in our industry, our definitions of these non-GAAP financial measures may not be comparable to similarly titled measures of other companies, thereby

diminishing their utility.

Management compensates for the limitation of Adjusted gross margin, Adjusted EBITDA and distributable cash flow as analytical tools by reviewing the comparable

GAAP measures, understanding the differences between Adjusted gross margin, Adjusted EBITDA and distributable cash flow, on the one hand, and operating

income (loss), net income (loss) and net cash provided by (used in) operating activities, on the other hand, and incorporating this knowledge into its decision-

making processes. We believe that investors benefit from having access to the same financial measures that our management uses in evaluating our operating

results.

2

Forward-looking Information

Certain matters contained in this presentation include "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended,

and Section 21E of the Securities Exchange Act of 1934, as amended. We make these forward-looking statements in reliance on the safe harbor protections

provided under the Private Securities Litigation Reform Act of 1995.

All statements, other than statements of historical fact, included in this presentation including the prospects of our industry, our anticipated financial performance,

our anticipated annual dividend growth rate, NGL Energy Partners LP (NYSE: NGL) anticipated financial performance, management's plans and objectives for

future operations, business prospects, outcome of regulatory proceedings, market conditions and other matters, may constitute forward-looking statements.

Although we believe that the expectations reflected in these forward-looking statements are reasonable, we cannot assure you that these expectations will prove

to be correct. These forward-looking statements are subject to certain known and unknown risks and uncertainties, as well as assumptions that could cause actual

results to differ materially from those reflected in these forward-looking statements. Factors that might cause actual results to differ include, but are not limited to,

the factors discussed above; our ability to comply with the covenants contained in the instruments governing our indebtedness and to maintain certain financial

ratios required by our credit facilities; NGL's operations, which we do not control; the ability of our subsidiary, Rose Rock Midstream L.P. (NYSE: RRMS), to make

minimum quarterly distributions; the possibility that our hedging activities may result in losses or may have a negative impact on our financial results; any

sustained reduction in demand for the petroleum products we gather, transport, process and store; our ability to obtain new sources of supply of petroleum

products; our failure to comply with new or existing environmental laws or regulations or cross border laws or regulations; the possibility that the construction or

acquisition of new assets may not result in the corresponding anticipated revenue increases; changes in currency exchange rates; and the risks and uncertainties

of doing business outside of the U.S., including political and economic instability and changes in local governmental laws, regulations and policies, as well as other

risk factors discussed from time to time in each of our documents and reports filed with the SEC.

Readers are cautioned not to place undue reliance on any forward-looking statements contained in this presentation which reflect management's opinions only as

of the date hereof. Except as required by law, we undertake no obligation to revise or publicly release the results of any revision to any forward-looking statements.

SemGroup and Rose Rock Midstream use their Investor Relations website and social media outlets as channels of distribution of material company information.

Such information is routinely posted and accessible on our Investor Relations websites at ir.semgroupcorp.com and ir.rrmidstream.com.

Both companies are present on Twitter and LinkedIn, follow us at the links below:

SemGroup Twitter and LinkedIn Rose Rock Midstream Twitter and LinkedIn

3

Two Public Companies

Note: Enterprise Value, Market Cap, Unit/Share Price and Yield as of December 31, 2014. Balance sheet data

as of September 30, 2014

C-Corp – assets in US, Canada, Mexico & UK

General Partner of RRMS

Publicly Traded – November 2010

Shares: 43.5 million

Enterprise Value: $3.8 billion

Market Cap: $3.0 billion

Share Price: $68.39

Yield: 1.8%

Current Annualized Dividend: $1.20

Total Assets: $2.7 billion

PP&E: $1.2 billion

Master Limited Partnership (MLP)

IPO – December 2011

Units: 29.0 million

Enterprise Value: $1.8 billion

Market Cap: $1.3 billion

Unit Price: $45.45

Yield: 5.1%

Current Annualized Distribution: $2.30

Total Assets: $1.1 billion

PP&E: $333 million

SemGroup Corporation Rose Rock Midstream

4

SemGroup Ownership Structure

5

Note: NGL Common Units are as of January 2, 2015

Business Strategy

Risk Management

Mitigate commodity price exposure

Maintain financial flexibility and utilize

leverage prudently

Quality Cash Flows

Generate consistent earnings and

cash flows

Focus on fee-based activities

Focused Growth

Capitalize on organic growth

opportunities with existing and

new assets

Grow our business through strategic

and accretive asset acquisitions

6

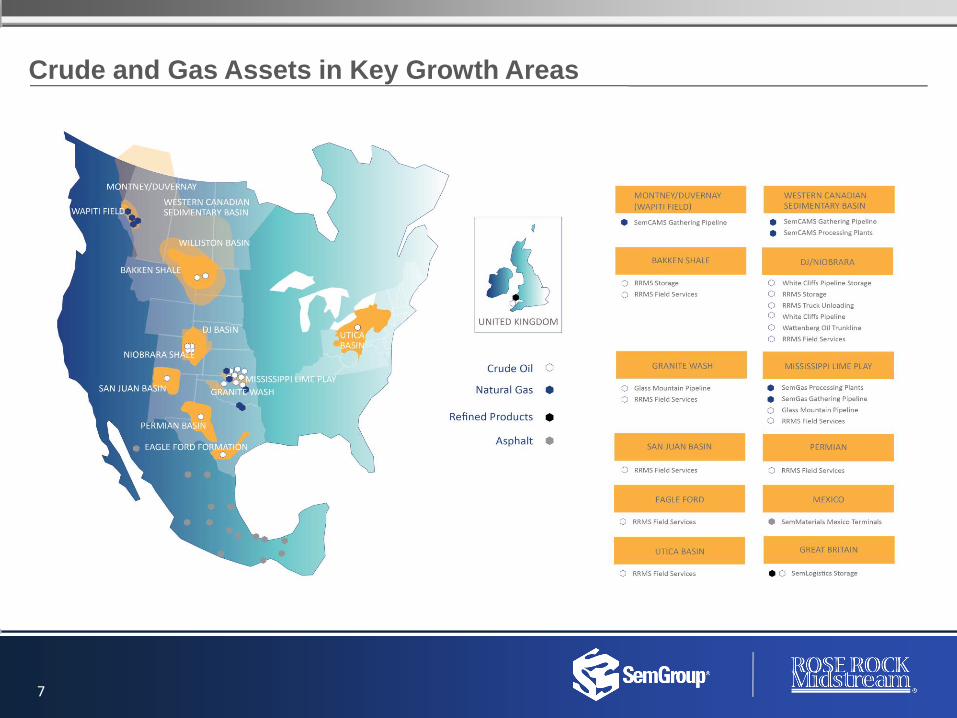

Crude and Gas Assets in Key Growth Areas

7

Crude Business Overview

Glass Mountain Pipeline – In service February 2014

210-mile pipeline

Two laterals – Granite Wash and Mississippi

Lime Play join and terminate in Cushing

140,000 bpd current capacity

Wattenberg Oil Trunkline – In service November 2013

37-mile, 12-inch pipeline and storage in DJ Basin

Transports Noble Energy production to White Cliffs

38-mile pipeline extension backed by long-term agreement with

Noble Energy – Expected 4Q 2014

SemGroup Corporation

8

Crude Business Overview

Cushing

7.6 million barrels of storage

86% under long-term fixed fee contracts with first expiration

2016

2014 average storage rate of $0.37 per month

Connectivity to all major inbound/outbound pipelines

White Cliffs Pipeline

51% ownership

DJ Basin to Cushing, OK

Two 527-mile, 12-inch pipelines

150,000 bpd current capacity

Expanding capacity to approximately 215,000 bpd

– Expected completion 3Q 2015

Field Services

Fleet of more than 250 crude oil trucks

Servicing the Bakken, DJ/Niobrara, Eagle Ford, Granite Wash,

Mississippi Lime, Permian, San Juan and Utica plays

Tampa Pipeline

12-mile, 12-inch pipeline from Platteville to Tampa, CO rail

facility

Constructed a new 5-mile lateral pipeline segment

Rose Rock Midstream

Kansas/Oklahoma System

Approximately 600-mile gathering and

transportation pipeline system

Currently operating at full capacity

Connects to third-party pipelines, Kansas and

Oklahoma refineries and Cushing terminal

620,000 barrels of storage capacity

Platteville

16-lane truck unloading facility

Origin of White Cliffs Pipeline

230,000 barrels of storage capacity

4 new truck unloading bays and 100,000 barrels of

additional storage – Expected completion 2Q 2015

Bakken Shale 17 gathering trucks

Transport via truck, third-party pipeline or rail

61,800 barrels of storage capacity

9

24.1 22.1 25.6

48.7 49.6 39.3

51.5

0

15

30

45

60

1Q 2Q 3Q 4Q 1Q 2Q 3Q

29.7 30.9 42.7 46.1

75.0

0

20

40

60

80

3Q 4Q 1Q 2Q 3Q

2013

2014

2013

2014

2013

2014

Crude Key Performance Metrics

(1) Pipeline volumes include KS/OK system, ND transportation and Tampa pipeline

(2) White Cliffs Pipeline is currently owned 51% by RRMS; includes Platteville and Healy volumes; 100% throughput

(3) Glass Mountain Pipeline is owned 50% by SEMG; average volumes Q1 2014 reflects two months operational; 100% throughput

(4) Field Services average volumes for Q3 2013 reflects one month operational

Crude Transportation Volumes

(Thousand Barrels per Day)

n Contracted(1) n Operational / Marketing n Uncontracted

Crude Cushing Storage 7.6 million Barrels Capacity

10

n Pipeline Volumes(1) n White Cliffs PL(2)

n Wattenberg Oil Trunkline n Glass Mountain PL(3)

Crude Marketing Volumes (Thousand Barrels per Day)

Field Services Transportation Volumes(4)

(Thousand Barrels per Day)

6.50 6.50 6.00

4.40

2.90

1.10 1.10 1.10

1.10

1.10

0.50

2.10

3.60

0

2

4

6

8

2014 2015 2016 2017 2018

55.7 57.3 54.6 57.1 67.3 64.9 65.2

66.8 66.8 67.3 77.4 72.7 74.1 98.5

11.0 26.6 28.5 31.2 43.7 61.7 61.1

0

50

100

150

200

250

300

1Q 2Q 3Q 4Q 1Q 2Q 3Q

97% 98% 100% 95% 92% 91% 90%

3% 2%

5% 8% 9% 10%

0%

20%

40%

60%

80%

100%

1Q 2Q 3Q 4Q 1Q 2Q 3Q

Owner Non-Owner

11

White Cliffs Pipeline Customer Mix

2013

2014

White Cliffs Pipeline volumes are primarily driven by owner throughput

White Cliffs Customer Throughput %

60.0 67.1 66.7 71.0 70.5 96.6

143.4 156.9 167.7

251.4

315.9

0

50

100

150

200

250

300

350

400

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q

Processing Volumes Capacity

2012

2013

2014

SemGas Areas of Operation Northern Oklahoma Average Processed Volume (mmcf/d)

12

Located in liquids rich oil plays

Four processing facilities - 388 mmcf/d of current capacity

1,300 miles of gathering lines

Significant growth in Mississippi Lime Play

– Rose Valley II – 200 mmcf/d capacity – Expected completion mid-2015

SemGas Natural Gas Business

213.9 250.3

283.9 272.6 285.8

148.2

274.2

162.6 128.5

159.6 146.9

152.6

186.1

138.3

0

100

200

300

400

500

1Q 2Q 3Q 4Q 1Q 2Q 3Q 2013

2014

SemCAMS Natural Gas Business

SemCAMS Areas of Operation Average Throughput Volume (mmcf/d)

13

Located in:

– Western Canadian Sedimentary Basin – sour gas

– Montney – liquids rich sour gas

– Duvernay – liquids rich sweet gas

Current operational capacity aproximately 700 mmcf/d

600 miles of transport and gathering lines

n K3 Plant n KA Plant

376.5 378.8

443.5

419.5 438.4

334.3

412.5

“Montney continues to gain steam (currently ~3Bcf/d) as operators look to accelerate in a $3-4/mcf price world. Scale (450Tcf recoverable) and

economics ($0-2.50/mcf break-even) conjure images of a thicker Marcellus. Changes in completion design are another arrow in quiver to improve

economics. And just like the leading US gas basin, takeaway is crucial, leading many E&Ps to own midstream and hoard FT. While bottlenecks could

emerge with high tariffs, we believe economics will justify increased drilling in basin and drive NA gas supply growth.”

– TPH 12/4/2014

SemGroup Capitalization & Liquidity

Conservative leverage ratio

provides financial flexibility

Perspective consolidated Net

Debt / Adjusted EBITDA

target of 3.5x or better

Available liquidity to fund

future growth opportunities

(in millions) September 30, 2014

December 31,

2013

Total Consolidated Debt $ 793 $ 615

Owner's Equity 1,171 1,214

Total Book Capitalization $ 1,964 $ 1,829

Consolidated Credit Metrics

Net Debt $ 726 $ 536

Total Debt/Capitalization 40% 34%

Net Debt/Adjusted EBITDA LTM 2.8x 2.8x

Committed Liquidity

Cash and Cash Equivalents $ 67 $ 79

Revolver Availability(1)

SemGroup 476 426

Rose Rock Midstream 426 306

Total Liquidity $ 969 $ 811

14

(1) Availability reduced by outstanding letters of credit

SemGroup Corporation 2014 Capital Expenditure Guidance

2014 Capital Expenditures – $475 million(1)(2)

Nearly 90% of capital expenditures are

focused on growth capital

Mid-teens or higher returns on organic

growth projects in key asset plays

Maintenance and Regulatory capital

focused on pipeline integrity

n Natural Gas

n Crude

n Other Growth Projects

n Maintenance and Regulatory

$185

48%

39%

2%

11%

$227

$11

$52

(1) Includes Rose Rock Midstream and excludes potential acquisitions

(2) Guidance updated June 23, 2014

15

SemGroup Corporation 2014 Capital Expenditure Guidance

(1) Guidance updated June 23, 2014

(2) Investments in affiliate; reflects our ownership in joint ventures

(3) Includes amounts paid to acquire additional ownership

Delivering organic growth with mid-teen or higher returns

16

(in millions)

Segment Description

Estimated

Completion Date

Project Spend

Through

12/31/2013 2014 Capex(1) 2015 Capex

Total

CapEx

Crude-RRMS White Cliffs Pipeline expansion(2) August 2014 32 30 — 62

Crude-RRMS Tampa Pipeline lateral July 2014 5 — 5

Crude-RRMS Chesapeake trucking acquisition June 2014 — 46 — 46

Crude-RRMS Platteville expansion 2Q 2015 — 7 4 11

Crude-SEMG Glass Mountain Pipeline and truck unloading facilities(2)(3) February 2014 128 8 — 136

Crude-SEMG Wattenberg Oil Trunkline extension 4Q 2014 — 34 16 50

Crude-SEMG White Cliffs Pipeline expansion(2) August 2014 66 23 — 89

SemGas Northern Oklahoma gas gathering and processing expansion varies 157 135

SemGas Cryo Plant redeployment 4Q 2014 — 6 2 8

SemCAMS Montney and Duvernay Pipeline growth varies 24 9 — 33

SemCAMS K3 Plant projects varies 4 14 — 18

SemCAMS Wapiti Pipeline Expansion varies 14 27 41

Other/undesignated growth projects varies 70 116-166

Maintenance, refurbishment & regulatory 52

Total $254 $475 $300 - $350

17

Adjusted EBITDA(1)

3Q 2014 2Q 2014 1Q 2014 2014 Guidance(2)

SemGroup $79.4 million $57.5 million $67.3 million $260 - $275 million

Rose Rock Midstream $31.0 million $20.6 million $27.8 million $115 - $120 million

Third Quarter Results

(1) Non-GAAP Financial Data Reconciliations can be found on the company’s

website, SemGroup includes fully consolidated Rose Rock Midstream

(2) Guidance updated June 23, 2014

(3) CAGR is based on the midpoint of 2014 Adjusted EBITDA Guidance

SemGroup Segment Results

(1) Non-GAAP Financial Data Reconciliations can be found on the company’s website

(2) Crude segment includes fully consolidated Rose Rock Midstream

Key Highlights (3Q 2014 vs 2Q 2014)

Crude increased $10.3 million – $4.6 million increase driven by increased White Cliffs Pipeline transportation volumes

– $2.3 million increase related to higher transportation volumes, excluding White Cliffs Pipeline

– $1.7 million decrease in G&A expenses primarily due to rating agency fees and drop down costs incurred during 2Q

SemCAMS increased $8.8 million – $3.6 million increase related to higher capital fee recoveries

– $3.4 million increase a result of higher volumes which were primarily impacted by the planned outage at the K3 Plant

– $1.8 million increase related to operating expense recoveries

Segment Adjusted EBITDA(1) (in millions, unaudited) 3Q 2014 2Q 2014 1Q 2014

Crude(2) $ 40.6 $ 30.3 $ 35.1

SemGas 17.1 14.6 12.8

SemCAMS 16.8 8.0 11.7

SemLogistics (2.3) 0.4 1.1

SemMaterials Mexico 4.5 3.0 5.1

SemStream 6.4 5.7 5.2

Corporate and Other (3.7) (4.5) (3.7)

Total Adjusted EBITDA(1) $ 79.4 $ 57.5 $ 67.3

18

SemGroup’s Fee-based Business Model

(1) LTM September 30, 2014

(2) SemGas 3Q 2014 margin contribution 59% fixed fee, 41% variable fee

(3) Rose Rock Midstream includes White Cliffs cash distributions resulting from 17% ownership for 3

months, 34% ownership for 6 months and 51% ownership for 3 months

Fixed Fee Variable Fee Marketing

SemGas(2) 53% 47%

SemCAMS 100%

SemLogistics 100%

SemMaterials Mexico 100%

White Cliffs Pipeline 100%

Rose Rock Midstream(3) 83% 17%

Margin Contribution(1)

n Fixed Fee n Variable Fee n Marketing

86 %

5 %

9 %

Fixed Fee

– Storage fees

– Transportation fees

– Unloading fees

– Gathering and processing fees

Variable Fee

– Gas processing – percent of proceeds

Marketing

– Back-to-back marketing transactions

Margin Descriptions

19

2013

2014

$0.1900 $0.2000

$0.2100 $0.2200

$0.2400

$0.2700

$0.3000

$0.1500

$0.2500

$0.3500

1Q 2Q 3Q 4Q 1Q 2Q 3Q

20

SemGroup Corporation Dividend Growth

58% cumulative increase in dividends since initiation in 1Q 2013

Our current dividend policy is to pass

through the after-tax cash distributions

received from our MLP investments

Targeting dividend growth of 40-45%

year over year

2012

2013

2014

$0.4025

$0.4300 $0.4400

$0.4500 $0.4650

$0.4950

$0.5350

$0.5750

$0.2000

$0.3000

$0.4000

$0.5000

$0.6000

4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q

21

2014 Target Annual Coverage Ratio 1.1x-1.2x

2014 Target Distribution Growth 25% year-over-year(1)

Rose Rock Midstream Distribution Per LP Unit

59% cumulative increase in distributions since IPO

(1) Assumes no further drop downs or acquisitions

• Four natural gas processing facilities

• Total processing capacity of 388 mmcf/d

• ~1,300 miles of gathering lines

• 8.7 million barrels of owned multi-product storage

• Two deep water jetties

• 100% fixed-fee gross margin

Glass Mountain Pipeline • Joint venture with NGL Energy Partners – 50% ownership

• 210-mile, 140,000 barrel per day crude oil pipeline and storage

• Two laterals – Granite Wash and Mississippi Lime Play join and terminate in Cushing, OK

Wattenberg Oil Trunkline • 37-mile, 12-inch pipeline and storage in DJ Basin

• Transports Noble Energy production to White Cliffs Pipeline

SemLogistics

Future Growth in Drop Downs

Glass Mountain Pipeline • Joint venture with Gavilon – 50% ownership

• 210-mile, 140,000 barrel per day crude oil pipeline and storage

• Operational January 2014

White Cliffs Pipeline

(51% ownership)

• 527-mile crude oil pipeline - 76,000 bpd capacity

• Incremental 80,000 bpd expansion – 2Q 2014 completion

• 100,000 barrels of crude oil storage

Glass Mountain Pipeline • Joint venture with Gavilon – 50% ownership

• 210-mile, 140,000 barrel per day crude oil pipeline and storage

• Operational January 2014

SemCAMS • Two sour and two sweet natural gas processing plants

• Total capacity of approximately 700 mmcf/d

• ~600 miles of transport and gathering lines

White Cliffs Pipeline

(51% ownership)

• 527-mile crude oil pipeline - 76,000 bpd capacity

• Incremental 80,000 bpd expansion – 2Q 2014 completion

• 100,000 barrels of crude oil storage

Glass Mountain Pipeline • Joint venture with Gavilon – 50% ownership

• 210-mile, 140,000 barrel per day crude oil pipeline and storage

• Operational January 2014

Rose Rock Midstream’s relationship with SemGroup allows for potential future drop downs

SemGas

Wattenberg Oil Trunkline

Extension

• 38-mile, 12-inch pipeline extension and storage in DJ Basin to move crude oil from Noble

Energy production to White Cliffs Pipeline

• 4Q 2014 completion

22

Glass Mountain Pipeline, Wattenberg Oil Trunkline and Wattenberg Oil Trunkline Extension are

expected to be dropped down 1Q 2015