2015.10.06 employee benefits

TRANSCRIPT

Employee Benefits

Panel, October 6, 2015

PROFESSION – INNOVATION – DIVERSITY

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

Moderator and Speakers

Sabrina Hartusch: Global Head of Insurance, Triumph,

Switzerland; president of SIRM

Paolo Marini: Global Head Customer Management, Corporate Life

& Pensions, Zurich, Switzerland

Janine Heijckers: Aon Global Benefits Practice Director EMEA,

The Netherlands

Holger Kraus: Insurance Risk Financing and Strategy, Siemens,

Germany

2

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

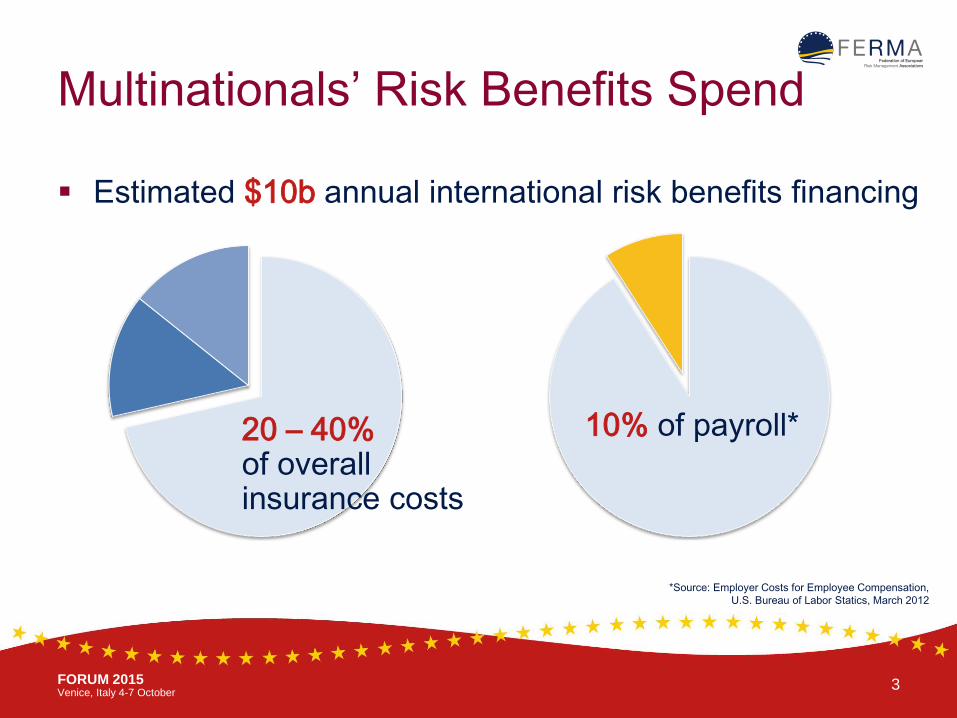

Multinationals’ Risk Benefits Spend

Estimated $10b annual international risk benefits financing

*Source: Employer Costs for Employee Compensation,

U.S. Bureau of Labor Statics, March 2012

3

20 – 40% of overall insurance costs

10% of payroll*

Paolo Marini

PROFESSION – INNOVATION – DIVERSITY

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

Today vs Tomorrow

Increasing Complexity

Fewer HR Resources

More Centralized Financing

Rise of the CRO

Protection Gap

Simplify Administration

Reduce Global Costs

Access Accurate Data Easily

Ensure Compliance Certainty

Duty of Care

5 FORUM 2015 Venice, Italy 4-7 October

Janine Heijckers

PROFESSION – INNOVATION – DIVERSITY

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

7

1. The trend of centralisation is ahead of operational reality

2. “Centres of excellence” more like “centres of mediocrity”

Benefit administration is a major drain on strategic resources 3.

4. Lack of benefits plan data is a barrier to strategic priorities

5. Financing of benefits is moving beyond multinational pooling

Aon Global Benefits Study 2015 Key Conclusions

6. Clear opportunities for improved eficiencies and to drive savings

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

Financing strategies

Localised Insurance contracts

Captive reinsurance

Multinational Pooling

Partnership Arrangement

Global Risk Policies

Life Disability Medical Accident

Some None Most

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

Benefit Strategy Development

9

PHASE 1 Inventory

Broad global benefits philosophy

Corporate policy metrics as context

Data and information collection

PHASE 2 Assessment

Design risks & opportunities

Financial risks & opportunities

Operational risks & opportunities

PHASE 3 Strategy

Current opportunities

and risks

Ongoing opportunities

and risks

PHASE 4 Governance

Prioritization and timeframe for

corrective actions

Global benefits policies to improve

alignment and avoid future risks

Corporate committee

and responsibility

Regional committees & COE and responsibility

Local mgmt. and HR/Fin responsibility

PHASE 5 Optimisation

Maximise value of benefit

programmes

Finance benefits efficiently

and minimise financial risks

Consistent employee experience &

operational efficiency

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

•About Aon

•Aon plc (NYSE:AON) is a leading global provider of risk management, insurance and reinsurance brokerage, and human resources solutions and outsourcing services. Through its more than 66,000 colleagues worldwide, Aon unites to empower results for clients in over 120 countries via innovative and effective risk and people solutions and through industry-leading global resources and technical expertise. Aon has been named repeatedly as the world’s best broker, best insurance intermediary, reinsurance intermediary, captives manager and best employee benefits consulting firm by multiple industry sources. Visit www.aon.com for more information on Aon and www.aon.com/manchesterunited to learn about Aon’s global partnership and shirt sponsorship with Manchester United.

•© Aon plc 2015. All rights reserved.

•The information contained herein and the statements expressed are of a general nature and are not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information and use sources we consider reliable, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

•www.aon.com

•Risk. Reinsurance. Human Resources

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

Financing Strategies - Continuum

Local self-

insurance

Local insured policies

International policies

Multinational pooling

Enhanced pooling

strategies

Captive re-insurance of employee

benefits

Global partnership

arrangement

Global risk policies

Local profit sharing

Premium cost reduction

Pooling international

dividend

Advanced international

dividend

Global negotiated

local premium reduction

Global premium payment

Captive influences

local premium rates

Some None Most

Life Disability Medical / Healthcare Accident

Holger Kraus

PROFESSION – INNOVATION – DIVERSITY

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

Global Management of EB

13

Why:

Significant expense position

Limited transparency

Untapped financial efficiencies

What:

Fronted EB Captive Program

Use of existing reinsurance captive company

How:

HR: benefit design

Insurance Risk Management: benefit financing

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

Challenges

14

Complex Issue with a number of internal and external stakeholders

Integration / management of different stakeholder perspectives is key – don´t underestimate cultural aspects and implications of changes in roles

Finance

Insurance

HR

Procurement

Insurers

Brokers

Consultants

...

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

Critical Success Factors

15

Integration of perspectives and trustbuilding

Communication is key

Approach (mandatory / freedom to join) needs to fit

corporate culture)

Acceptance, that best of both worlds (optimal solution

from local as well as central perspective is not

achievable)

Thank you!

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

APPENDIX

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

Employee Benefits Today

COORDINATED

3,000 Pools for

approximately 1,200

Multinationals

70 global benefits captive

programs

$2.5b risk premium annually

18

UNCOORDINATED

5,000 Multinationals don’t

coordinate global benefits

provision and costs

$7.5b yearly risk premium

outside any coordinated

programs

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

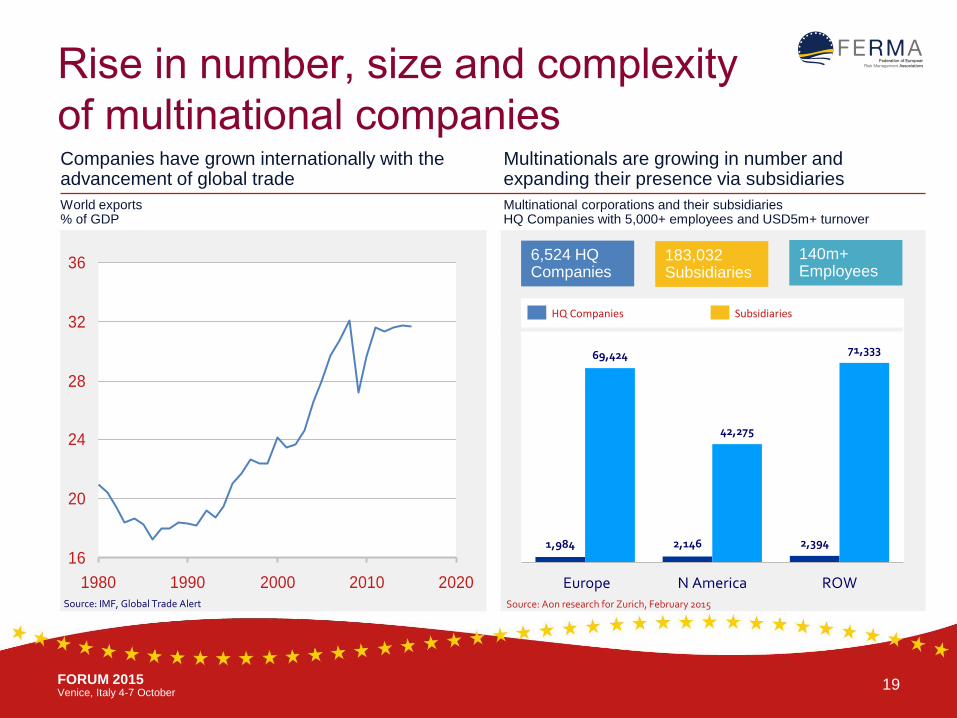

Rise in number, size and complexity

of multinational companies

19

16

20

24

28

32

36

1980 1990 2000 2010 2020

HQ Companies Subsidiaries

1,984 2,146 2,394

69,424

42,275

71,333

Europe N America ROW

6,524 HQ Companies

140m+ Employees

183,032 Subsidiaries

Source: IMF, Global Trade Alert Source: Aon research for Zurich, February 2015

Companies have grown internationally with the advancement of global trade

World exports % of GDP

Multinationals are growing in number and expanding their presence via subsidiaries

Multinational corporations and their subsidiaries HQ Companies with 5,000+ employees and USD5m+ turnover

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

From Domestic Policies to ASO

20

Financial Improvement Scale

Modest Significant High

1 3 4 5 2 6

No multinational pools

Traditional multinational pools

Managed pools (negotiated improvements)

Pools reinsured to captive

Premiums held by captive

Reserves held by captive

Administrative Services Only no local reserves

Head Office Involvement Scale

None Modest Significant High

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

Employee Benefits Captives in 2014*

21

Estimated Number of Employee Benefit Captives in 2014

Estimated Premiums Paid to Employee Benefit Captives in 2014 ($ billions)

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

Value proposition for financing benefits

through captives

22

Cost Savings

Cash Flow

Coverage Capacity

Control

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

Captive considerations

23

Financing Fronting fees / Risk charges

Administration fees

Operational fees

• Securitization • Reinsurance

trust • Letters of credit

• Exposure • Risks retained by

fronting carrier • Amount of

additional protection required (beyond expected costs)

• Cost to “rent paper”

• Risk charges for retained risks

• Stop loss • Other expenses

• Same services and costs as traditional funding arrangements

• Premium taxes • Captive

management fees

• Feasibility study • Legal fees • Independent

fiduciary fees

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

Solvency II — for EU based captives

24

Insurance risk

Market risk

Credit risk

Liquidity risk

Operational risk

SOLVENCY II

Embedding Solvency II in your business

Pillar 1 Quantitative requirements

Reserving

Regulations on minimum capital requirements

Investment

Pillar 2 Supervisor Review

Quantitative requirements

Regulations on financial services supervision

(Capabilities and powers of regulators, areas of activity)

Pillar 3 Market discipline

Transparency

Disclosure requirements

Competition related elements

Implementation Control Disclosure

Capital Requirements Governance & Risk Management

Disclosure & Transparency

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

Reinsuring US Employee Benefits

25

Internal Revenue Service (IRS) Department of labor (ERISA)

• Parent company can take a tax deduction equal to all the premium paid to the…

• …captive if at least 30% is generated from unrelated business

• EB plan are considered unrelated to the partner company

• EB plans are prohibited from being reinsured b a captive (unless certain requirements are met)

• DOL concerned with solvency and potential for self-dealing

• Prohibited Transaction Exemption required

• Benefit improvement must be implemented

• Captive must be US domiciled

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

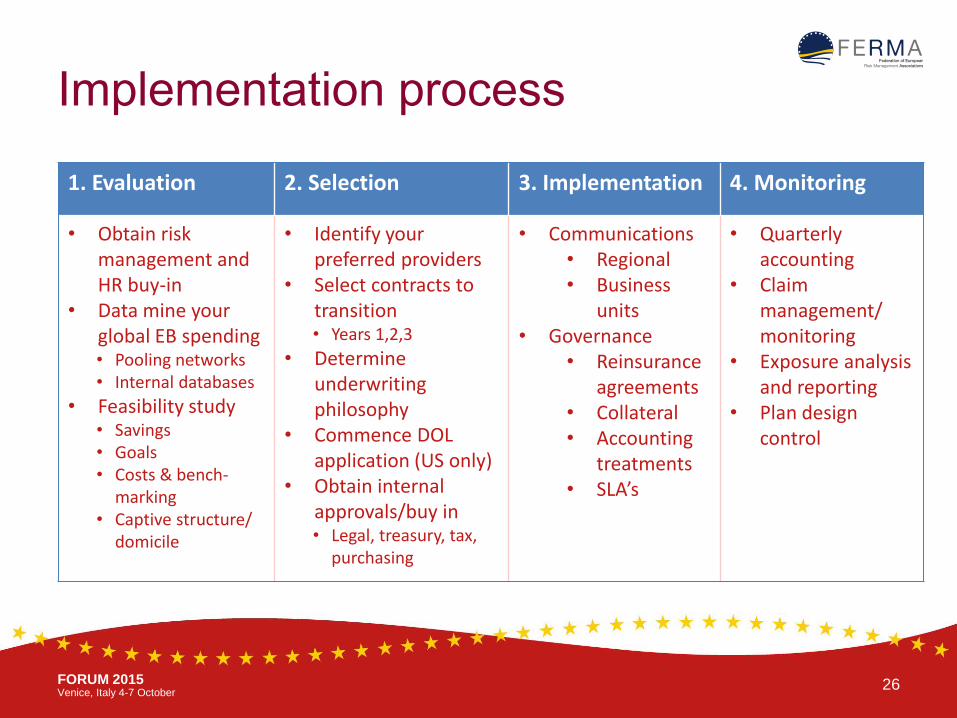

Implementation process

26

1. Evaluation 2. Selection 3. Implementation 4. Monitoring

• Obtain risk management and HR buy-in

• Data mine your global EB spending • Pooling networks • Internal databases

• Feasibility study • Savings • Goals • Costs & bench-

marking • Captive structure/

domicile

• Identify your preferred providers

• Select contracts to transition • Years 1,2,3

• Determine underwriting philosophy

• Commence DOL application (US only)

• Obtain internal approvals/buy in • Legal, treasury, tax,

purchasing

• Communications • Regional • Business

units • Governance

• Reinsurance agreements

• Collateral • Accounting

treatments • SLA’s

• Quarterly accounting

• Claim management/ monitoring

• Exposure analysis and reporting

• Plan design control

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

2016 Captive Implementation Timing

27

2016 onwards

Q3 2015 Q2 2015 Q1 2015 Q4 2015 WORKSTREAM

Data collection

Implement captive strategy if appropriate (e.g. setup, licensing)

1. Evaluation & captive feasibility

Feasibility analysis

2. Network selection/ negotiation

Agree/sign agreements and treaties

Negotiate with networks

Governance framework created/adjusted and agreed to reflect strategy and responsibilities

3. Governance framework

Communications drafted and rolled out internally and through broking network

4. Communication

Implement in line with strategy (timing depends on local renewals)

5. Local Implementation

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

Zurich International Programs for

Employees

28

Reducing the complexity and effort of negotiating and implementing policies one-by-one in each country

Fulfilling the duty of care to employees globally

Ensuring that the right cover is in place

Attracting and retaining the best talent globally

Accessing reliable data on existing employee benefit programs

Gaining and maintaining understanding, transparency and control of employee risk programs and their costs

Consolidating relationships with insurers

Standardizing and increasing the efficiency of employee risk programs

Ensuring that insurance is aligned with local regulatory requirements

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

Income Protection Gap

As important as retirement / longevity gap, and linked to it

Compounded by effects of financial crisis

Survey of major markets worldwide

Risks generally underestimated

Shift in reasons for loss of income

Diverging perceptions of public sector’s role

Uneven trust in ability of State to honor commitments

Engagement of employers and invidudals required

29

BRUSSELS, 20-21 October www.ferma.eu

FORUM 2015 Venice, Italy 4-7 October

Benefit Exchanges

Recently implemented in US

At “concept stage” elsewhere

Potential alternative to managed global risk financing

Will the concept gain traction beyond healthcare?

Will it be exported?

Is the UK the most likely follower?

30