2016 benefit guide esc region 20 - cigna version 1

DESCRIPTION

ÂTRANSCRIPT

ESC REGION 20 BENEFITS COOPERATIVE

EFFECTIVE:

09/01/2016 - 8/31/2017

BENEFIT GUIDE

www.esc20bc.net

1

Benefit Contact Information 3 How to Enroll 4-5 Annual Benefit Enrollment 6-11 1. Benefit Updates 6 2. Section 125 Cafeteria Plan Guidelines 7 3. Annual Enrollment 8 4. Eligibility Requirements 9 5. Helpful Definitions 10 6. Health Savings Account (HSA) vs. Flexible

Spending Account (FSA) 11

MDLIVE Telehealth 12-13 APL MEDlink® Medical Supplement 14-17 APL Accident 18-21 Cigna Dental 22-27 Superior Vision 28-29 Cigna Short Term Disability 30-33 Cigna Long Term Disability 34-37 APL Cancer 38-41 Texas Life Individual Life 42-45 Cigna Life and AD&D 46-51 HSA Bank Health Savings Account (HSA) 52-55 NBS Flexible Spending Account (FSA) 56-59 ID Watchdog Identity Theft 60-61

Table of Contents

HOW TO ENROLL

PG. 4

BENEFIT UPDATE—WHAT’S NEW

PG. 6

YOUR BENEFITS PACKAGE

PG. 12

FLIP TO...

2

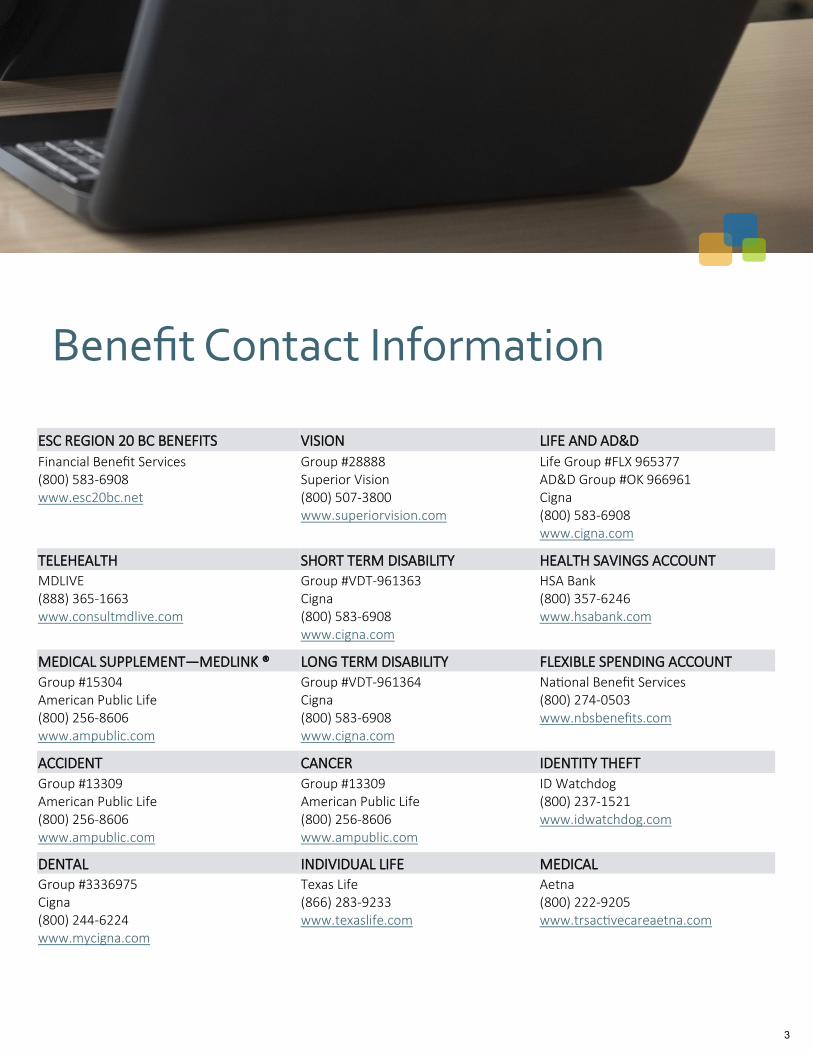

Benefit Contact Information

ESC REGION 20 BC BENEFITS VISION LIFE AND AD&D

Financial Benefit Services (800) 583-6908 www.esc20bc.net

Group #28888 Superior Vision (800) 507-3800 www.superiorvision.com

Life Group #FLX 965377 AD&D Group #OK 966961 Cigna (800) 583-6908 www.cigna.com

TELEHEALTH SHORT TERM DISABILITY HEALTH SAVINGS ACCOUNT MDLIVE (888) 365-1663 www.consultmdlive.com

Group #VDT-961363 Cigna (800) 583-6908 www.cigna.com

HSA Bank (800) 357-6246 www.hsabank.com

MEDICAL SUPPLEMENT—MEDLINK ® LONG TERM DISABILITY FLEXIBLE SPENDING ACCOUNT Group #15304 American Public Life (800) 256-8606 www.ampublic.com

Group #VDT-961364 Cigna (800) 583-6908 www.cigna.com

National Benefit Services (800) 274-0503 www.nbsbenefits.com

ACCIDENT CANCER IDENTITY THEFT

Group #13309 American Public Life (800) 256-8606 www.ampublic.com

Group #13309 American Public Life (800) 256-8606 www.ampublic.com

ID Watchdog (800) 237-1521 www.idwatchdog.com

DENTAL INDIVIDUAL LIFE MEDICAL Group #3336975 Cigna (800) 244-6224 www.mycigna.com

Texas Life (866) 283-9233 www.texaslife.com

Aetna (800) 222-9205 www.trsactivecareaetna.com

Benefit Contact Information

3

!

How to Enroll

On Your Computer Access the ESC Region 20 BC

benefits website from your

computer, tablet or smartphone!

Our online benefit enrollment

platform provides a simple and

easy to navigate process. Enroll

at your own pace, whether at

home or at work.

www.esc20bc.net delivers

important benefit information

with 24/7 access, as well as

detailed plan information, rates

and product videos.

On Your Device

Enrollment has just become

easier!

Avoid typing long URLs and scan

directly to your benefits websites,

videos, and benefit guides.

Try it yourself! Scan the following

code in the picture.

SCAN:

4

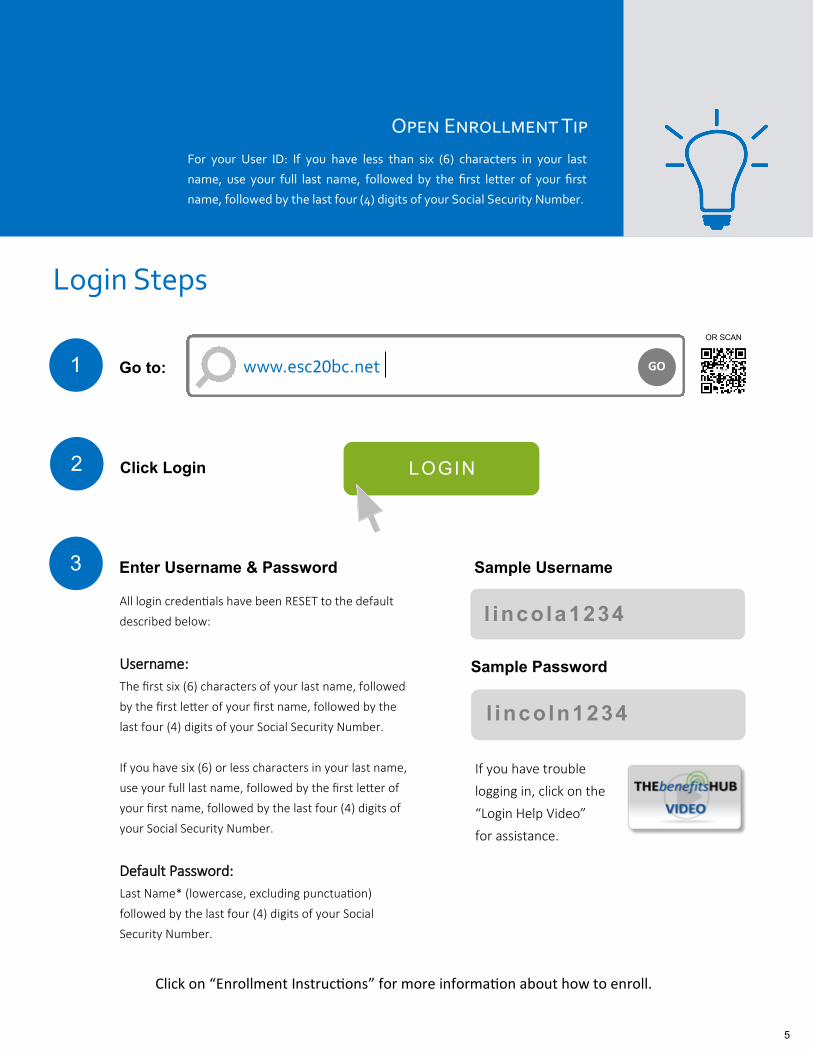

GO www.esc20bc.net 1

2

Login Steps

3

Go to:

Click Login

Enter Username & Password

OR SCAN

All login credentials have been RESET to the default

described below:

Username:

The first six (6) characters of your last name, followed

by the first letter of your first name, followed by the

last four (4) digits of your Social Security Number.

If you have six (6) or less characters in your last name,

use your full last name, followed by the first letter of

your first name, followed by the last four (4) digits of

your Social Security Number.

Default Password:

Last Name* (lowercase, excluding punctuation)

followed by the last four (4) digits of your Social

Security Number.

Sample Password

l incola1234

l incoln1234

If you have trouble

logging in, click on the

“Login Help Video”

for assistance.

Click on “Enrollment Instructions” for more information about how to enroll.

Sample Username

LOGIN

Open Enrollment Tip

For your User ID: If you have less than six (6) characters in your last

name, use your full last name, followed by the first letter of your first

name, followed by the last four (4) digits of your Social Security Number.

5

Login and complete your benefit enrollment from 07/18/2016 - 08/22/2016

Enrollment assistance is available by calling Financial Benefit Services at (866) 914-5202

to speak to a representative Monday—Friday between 8am – 5pm CST

Update your profile information: home address, phone numbers, email, beneficiaries

Update dependent social security numbers and student status for college aged children

Benefit Updates - What’s New:

Don’t Forget!

Benefit elections will become effective 9/1/2016. Elections requiring evidence of insurability, such as Life Insurance, may have a later effective date, if approved. After annual enrollment, benefit changes can only be made if you experience a qualifying event. Changes must be made within 30 days of event.

If you currently participate in a Healthcare or

Dependent Care Flexible Spending Account, you MUST re-elect a new contribution amount in the summer enrollment to continue to participate.

Your current monthly HSA contribution will rollover to

next plan year unless you make a change to your election during the summer enrollment window.

IMPORTANT: Reminder, the LOW PPO Dental Plan pays

differently when you go to an out-of-network dentist. If

you choose to go out-of-network, CIGNA will only reimburse what your dentist charges up to the negotiated in-network level fee. What this could mean to you: high out-of-pocket costs since you will be balance-billed the difference between what your dentist charges and what CIGNA pays. If you use an out-of-network dentist, you may want to consider changing to the High PPO Dental plan (gives you flexibility to use an out-of-network dentist). If you want to stay on the Low PPO dental plan, go to an in-network dentist. The Low PPO dental plan provides lower premiums and cost-savings due to utilizing in-network dentists since CIGNA negotiates lower fees with in-network providers, making your benefits go further.

Effective 9/1/2016, MDLIVE Telehealth premium will

Increase.

Annual Benefit Enrollment

SUMMARY PAGES

6

CHANGES IN STATUS (CIS):

QUALIFYING EVENTS

Marital Status A change in marital status includes marriage, death of a spouse, divorce or annulment (legal separation is not recognized in all states).

Change in Number of Tax Dependents

A change in number of dependents includes the following: birth, adoption and placement for adoption. You can add existing dependents not previously enrolled whenever a dependent gains eligibility as a result of a valid change in status event.

Change in Status of Employment Affecting

Coverage Eligibility

Change in employment status of the employee, or a spouse or dependent of the employee, that affects the individual's eligibility under an employer's plan includes commencement or termination of employment.

Gain/Loss of Dependents' Eligibility Status

An event that causes an employee's dependent to satisfy or cease to satisfy coverage requirements under an employer's plan may include change in age, student, marital, employment or tax dependent status.

Judgment/Decree/Order

If a judgment, decree, or order from a divorce, annulment or change in legal custody requires that you provide accident or health coverage for your dependent child (including a foster child who is your dependent), you may change your election to provide coverage for the dependent child. If the order requires that another individual (including your spouse and former spouse) covers the dependent child and provides coverage under that individual's plan, you may change your election to revoke coverage only for that dependent child and only if the other individual actually provides the coverage.

Eligibility for Government Programs

Gain or loss of Medicare/Medicaid coverage may trigger a permitted election change.

A Cafeteria plan enables you to save money by using pre-tax dollars to pay for eligible group insurance premiums sponsored and offered by your employer. Enrollment is automatic unless you decline this benefit. Elections made during annual enrollment will become effective on the plan effective date and will remain in effect during the entire plan year.

Changes in benefit elections can occur only if you experience a qualifying event. You must present proof of a qualifying event to your Benefit Office within 30 days of your qualifying event and meet with your Benefit/HR Office to complete and sign the necessary paperwork in order to make a benefit election change. Benefit changes must be consistent with the qualifying event.

Section 125 Cafeteria Plan Guidelines

SUMMARY PAGES

7

Annual Enrollment

During your annual enrollment period, you have the opportunity

to review, change or continue benefit elections each year.

Changes are not permitted during the plan year (outside of

annual enrollment) unless a Section 125 qualifying event occurs.

Changes, additions or drops may be made only during the

annual enrollment period without a qualifying event.

Employees must review their personal information and verify

that dependents they wish to provide coverage for are

included in the dependent profile. Additionally, you must

notify your employer of any discrepancy in personal and/or

benefit information.

Employees must confirm on each benefit screen (medical,

dental, vision, etc.) that each dependent to be covered is

selected in order to be included in the coverage for that

particular benefit.

New Hire Enrollment

All new hire enrollment elections must be completed in the

online enrollment system within the first 31 days of benefit

eligibility employment. Failure to complete elections during this

timeframe will result in the forfeiture of coverage.

Q&A

Who do I contact with Questions?

For supplemental benefit questions, you can contact your

Benefits/HR department or you can call Financial Benefit Services

at 866-914-5202 for assistance.

Where can I find forms?

For benefit summaries and claim forms, go to the ESC Region

20 BC benefit website: www.esc20bc.net. Click on your school

district, then click on the benefit plan you need information

on (i.e., Dental) and you can find the forms you need under

the Benefits and Forms section.

How can I find a Network Provider?

For benefit summaries and claim forms, go to the ESC Region

20 BC benefit website: www.esc20bc.net. Click on your school

district, then click on the benefit plan you need information

on (i.e., Dental) and you can find provider search links under

the Quick Links section.

When will I receive ID cards?

If the insurance carrier provides ID cards, you can expect to

receive those 3-4 weeks after your effective date. For most

dental and vision plans, you can login to the carrier website

and print a temporary ID card or simply give your provider the

insurance company’s phone number and they can call and

verify your coverage if you do not have an ID card at that

time. If you do not receive your ID card, you can call the

carrier’s customer service number to request another card.

If the insurance carrier provides ID cards, but there are no

changes to the plan, you typically will not receive a new ID

card each year.

SUMMARY PAGES

8

PLAN CARRIER MAXIMUM AGE

Accident American Public Life Through 25

Cancer American Public Life Through 25

Dental Cigna Through 25

Dependent Flex

National Benefit Services

12 or younger or qualified individual unable to care for themselves & claimed

as a dependent on your taxes

Healthcare FSA National Benefit Services Through 25 or IRS Tax Dependent

Health Savings Account HSA Bank IRS Tax Dependent

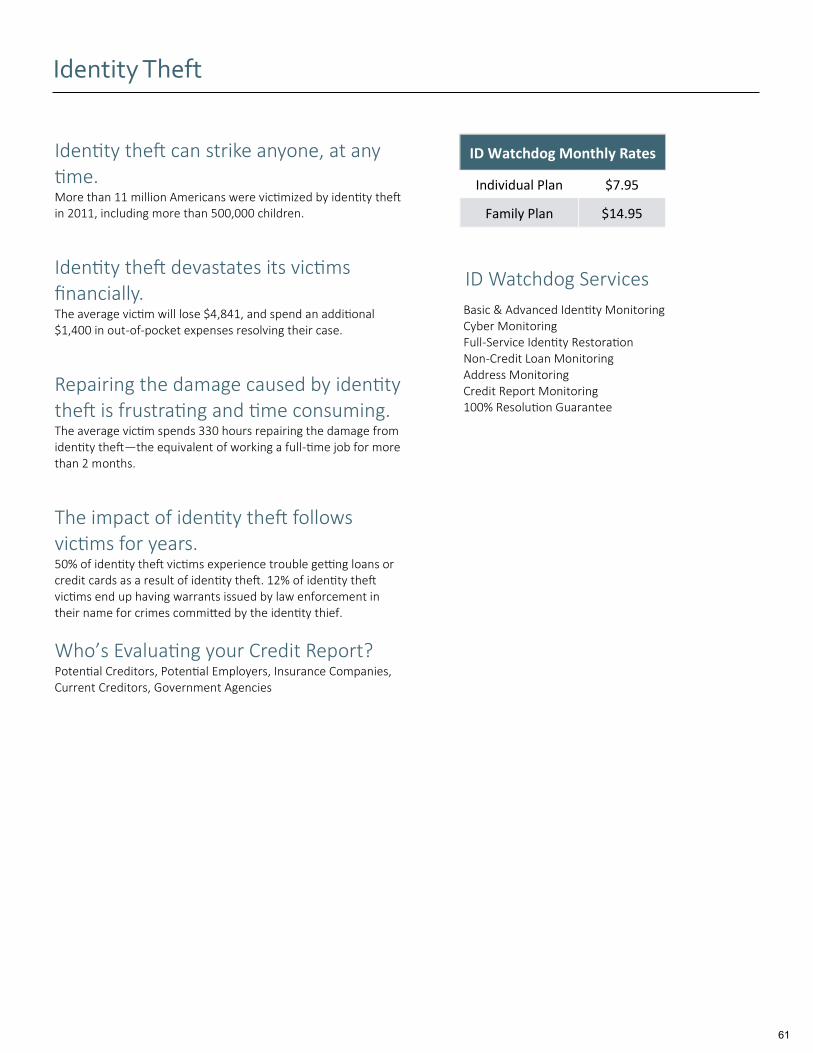

Identity Theft ID Watchdog Through 25

Medical Supplement Plan American Public Life Through 25

Permanent Life Texas Life Through 21

Telehealth MDLIVE Through 25

Vision Superior Vision Through 25

Voluntary Life Cigna Through 25

Employee Eligibility Requirements

Supplemental Benefits: Eligible employees must work 20 or more

regularly scheduled hours each work week.

Eligible employees must be actively at work on the plan effective

date for new benefits to be effective, meaning you are physically

capable of performing the functions of your job on the first day of

work concurrent with the plan effective date. For example, if

your 2016 benefits become effective on September 1, 2016, you

must be actively-at-work on September 1, 2016 to be eligible for

your new benefits.

Dependent Eligibility Requirements

Dependent Eligibility: You can cover eligible dependent

children under a benefit that offers dependent coverage,

provided you participate in the same benefit, through the

maximum age listed below. Dependents cannot be double

covered by married spouses within ESC Region 20 BC or as

both employees and dependents.

If your dependent is disabled, coverage may be able to continue past the maximum age under certain plans. If you have a disabled dependent who is reaching an ineligible age, you must provide a physician’s statement confirming your dependent’s disability. Contact your HR/Benefit Administrator to request a continuation of coverage.

SUMMARY PAGES

9

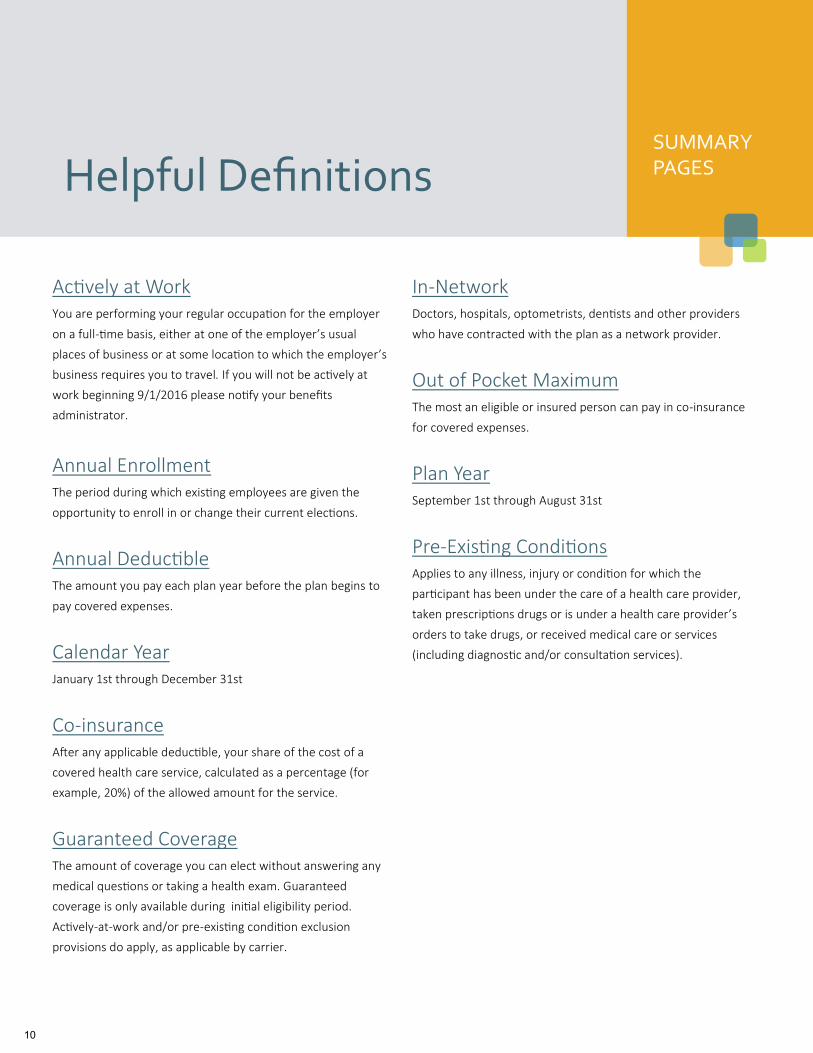

Actively at Work You are performing your regular occupation for the employer

on a full-time basis, either at one of the employer’s usual

places of business or at some location to which the employer’s

business requires you to travel. If you will not be actively at

work beginning 9/1/2016 please notify your benefits

administrator.

Annual Enrollment The period during which existing employees are given the

opportunity to enroll in or change their current elections.

Annual Deductible The amount you pay each plan year before the plan begins to

pay covered expenses.

Calendar Year January 1st through December 31st

Co-insurance After any applicable deductible, your share of the cost of a

covered health care service, calculated as a percentage (for

example, 20%) of the allowed amount for the service.

Guaranteed Coverage The amount of coverage you can elect without answering any

medical questions or taking a health exam. Guaranteed

coverage is only available during initial eligibility period.

Actively-at-work and/or pre-existing condition exclusion

provisions do apply, as applicable by carrier.

In-Network Doctors, hospitals, optometrists, dentists and other providers

who have contracted with the plan as a network provider.

Out of Pocket Maximum The most an eligible or insured person can pay in co-insurance

for covered expenses.

Plan Year September 1st through August 31st

Pre-Existing Conditions Applies to any illness, injury or condition for which the

participant has been under the care of a health care provider,

taken prescriptions drugs or is under a health care provider’s

orders to take drugs, or received medical care or services

(including diagnostic and/or consultation services).

Helpful Definitions SUMMARY PAGES

10

Health Savings Account (HSA) (IRC Sec. 223)

Flexible Spending Account (FSA) (IRC Sec. 125)

Description

Approved by Congress in 2003, HSAs are actual bank accounts in employee’s names that allow employees to save and pay for unreimbursed qualified medical expenses tax-free.

Allows employees to pay out-of-pocket expenses for copays, deductibles and certain services not covered by medical plan, tax-free. This also allows employees to pay for qualifying dependent care tax-free.

Employer Eligibility A qualified high deductible health plan. All employers

Contribution Source Employee and/or employer Employee and/or employer

Account Owner Individual Employer

Underlying Insurance Requirement

High deductible health plan None

Minimum Deductible $1,300 single (2016) $2,600 family (2016) N/A

Maximum Contribution $3,350 single (2016) $6,750 family (2016)

Varies per employer

Permissible Use Of Funds

Employees may use funds any way they wish. If used for non-qualified medical expenses, subject to current tax rate plus 20% penalty.

Reimbursement for qualified medical expenses (as defined in Sec. 213(d) of IRC).

Cash-Outs of Unused Amounts (if no medical expenses)

Permitted, but subject to current tax rate plus 20% penalty (penalty waived after age 65).

Not permitted

Year-to-year rollover of account balance?

Yes, will roll over to use for subsequent year’s health coverage.

No. Access to some funds can may be extended if your employer’s plan contains a 2 1/2 –month grace period or $500 rollover provision.

Does the account earn interest?

Yes No

Portable? Yes, portable year-to-year and between jobs.

No

FOR HSA INFORMATION

FLIP TO… PG. 52

FOR FSA INFORMATION

FLIP TO… PG. 56

HSA vs. FSA SUMMARY PAGES

11

Telehealth provides 24/7/365 access to board-certified doctors via telephone consultations that can diagnose, recommend treatment and prescribe medication. Whether you are at home, traveling or at work, Telehealth makes care more convenient and accessible for non-emergency care when your primary care physician is not available.

About this Benefit

Telehealth

DID YOU KNOW?

75%

of all doctor, urgent care, and ER visits could be handled safely and effectively via

telehealth.

MDLIVE YOUR BENEFITS PACKAGE

This is a general overview of your plan benefits. If the terms of this outline differ from your policy, the policy will govern. Additional plan details on covered expenses, limitations and exclusions are included in the summary plan description located on the

ESC Region 20 BC Benefits Website: www.esc20bc.net 12

Telehealth

When should I use MDLIVE? If you’re considering the ER or urgent care for a non-

emergency medical issue

Your primary care physician is not available

At home, traveling, or at work

24/7/365, even holidays!

What can be treated? Allergies

Asthma

Bronchitis

Cold and Flu

Ear Infections

Joint Aches and Pain

Respiratory Infection

Sinus Problems

And More!

Pediatric Care related to: Cold & Flu

Constipation

Ear Infection

Fever

Nausea & Vomiting

Pink Eye

And More!

Who are our doctors? MDLIVE has the nation’s largest network of telehealth doctors. On average, our doctors have 15 years of experience practicing medicine and are licensed in the state where patients are located. Their specialties include primary care, pediatrics, emergency medicine and family medicine. Our doctors are committed to providing convenient, quality care and are always ready to take your call.

Are children eligible? Yes. MDLIVE has local pediatricians on-call 24/7/365. Please note, a parent or guardian must be present during any interactions involving minors. We ask parents to establish a child record under their account. Parents must be present on each call for children 18 or younger.

How much does it cost? $8 for Employee Only. $16 for Family.

Download the App Doctor visits are easier and more convenient with the MDLIVE App. Be prepared. Download today. www.mdlive.com/getapp

Access to a doctor anywhere: at home, at work, or on the go

Choose doctors from one of the nation's largest telehealth networks

Available 24/7 by video or phone

Private, secure and confidential visits

Connect instantly with MDLIVE Assist

Disclaimers: MDLIVE does not replace the primary care physician. MDLIVE operates subject to state regulation and may not be available in certain states. MDLIVE does not guarantee that a prescription will be written. MDLIVE does not prescribe DEA controlled substances, non-therapeutic drugs and certain other drugs which may be harmful because of their potential for abuse. MDLIVE physicians reserve the right to deny care for potential misuse of services. For complete terms of use visit www.mdlive.com/pages/terms.html 010113

Call us at (888) 365-1663 or visit us at www.consultmdlive.com

Scan with your smartphone to get the app.

13

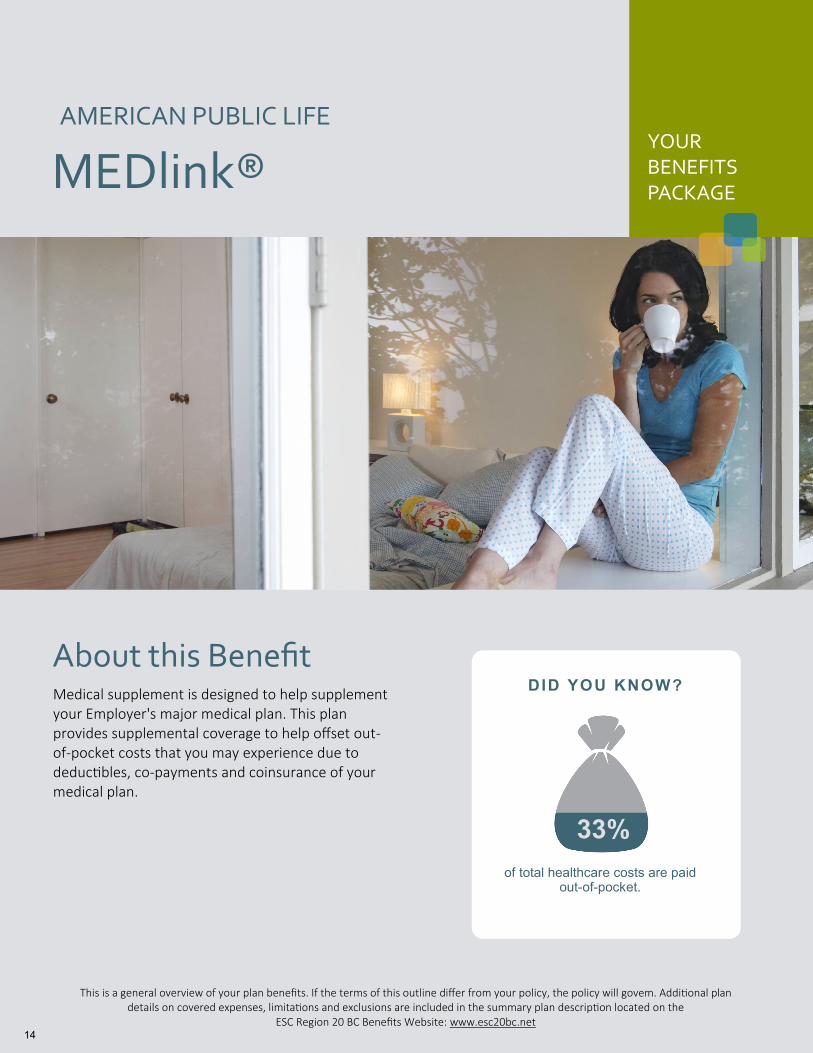

Medical supplement is designed to help supplement your Employer's major medical plan. This plan provides supplemental coverage to help offset out-of-pocket costs that you may experience due to deductibles, co-payments and coinsurance of your medical plan.

About this Benefit

MEDlink®

DID YOU KNOW?

33%

of total healthcare costs are paid out-of-pocket.

AMERICAN PUBLIC LIFE YOUR BENEFITS PACKAGE

This is a general overview of your plan benefits. If the terms of this outline differ from your policy, the policy will govern. Additional plan details on covered expenses, limitations and exclusions are included in the summary plan description located on the

ESC Region 20 BC Benefits Website: www.esc20bc.net 14

SUMMARY OF BENEFITS

Base Policy Option 1 Option 2

In-Hospital Benefit - Maximum In-Hospital Benefit $1,500 per confinement $2,500 per confinement

Outpatient Benefit up to $200 per treatment up to $200 per treatment

Physician Outpatient Treatment Benefit $25 per treatment; $125 max per family per Calendar Year

$25 per treatment; $125 max per family per Calendar Year

Option 1 Total Monthly Premiums by Plan*

Issue Ages 17-54 Issue Ages 55-59 Issue Ages 60-69

Employee Only $21.50 $32.00 $49.00

Employee + Spouse $39.50 $59.00 $88.00

Employee + Child(ren) $36.50 $47.00 $64.00

Family Coverage $54.50 $74.00 $103.00

Option 2 Total Monthly Premiums by Plan*

Issue Ages 17-54 Issue Ages 55-59 Issue Ages 60-69

Employee Only $28.00 $44.50 $68.50

Employee + Spouse $51.50 $81.50 $122.50

Employee + Child(ren) $45.50 $62.00 $86.00

Family Coverage $69.00 $99.00 $140.00

Plans available to employees age 70 and over if You work for an employer employing 20 or more employees on a typical workday in the preceding

Calendar Year.

*Total premium includes the Plan selected and any applicable rider premium. Premiums are subject to increase with notice.

Limitations Eligibility This policy will be issued to those persons who meet American Public Life Insurance Company’s insurability requirements. Evidence of insurability acceptable to us may be required. If our underwriting rules are met, you are on active service, you are covered under your Employer’s Medical Plan and premium has been paid, your insurance will take effect on the requested Effective Date or the Effective Date assigned by us upon approval of your written application, whichever is later.

Covered Charges mean those charges that are incurred by a Covered Person because of an Accident or Sickness; are for necessary treatment, services and medical supplies and recommended by a Physician; are not more than any dollar limit set forth in the Schedule; are incurred while insured under the Policy, subject to any Extension of Benefits; and are not excluded under the Policy.

A Hospital is not any institution used as a place for rehabilitation; a place for rest, or for the aged; a nursing or convalescent home; a long term nursing unit or geriatrics ward; or an extended care facility for the care of convalescent, rehabilitative or ambulatory patients.

In-Hospital Benefit Benefits payable are limited to any out-of-pocket deductible amount; any out-of-pocket co-payment or coinsurance amounts the Covered Person actually incurs after the Employer’s Medical Plan has paid; any out-of-pocket amount the Covered Person actually incurs for surgery performed by a Physician after the Employer’s Medical Plan has paid; and the Maximum In-Hospital Benefit shown in the Policy Schedule. The Covered Person must be an Inpatient and covered by your Employer’s Medical Plan when the Covered Charges are incurred.

Outpatient Benefits Treatment is for the same or related conditions, unless separated by a period of 90 consecutive days. After 90 consecutive days, a new Outpatient Benefit will be payable. The Covered Person must be covered by your Employer’s Medical Plan when the Covered Charges are incurred.

Physician Outpatient Treatment Benefit Benefit maximum of $125 per family per Calendar Year. The Covered Person must be covered by your Employer’s Medical Plan when the Covered Charges are incurred. The Covered Person must not be an Inpatient when the Covered Charges are incurred.

APSB-22330(TX)-0116 MGM/FBS ESC Region 20 Benefits Co-op

MEDlink® Limited Benefit Medical Expense Supplemental Insurance

THE POLICY UNDER WHICH THIS CERTIFICATE IS ISSUED IS NOT A POLICY OF WORKERS’ COMPENSATION INSURANCE. THE EMPLOYER DOES NOT BECOME A

SUBSCRIBER TO THE WORKERS’ COMPENSATION SYSTEM BY PURCHASING THE POLICY AND IF THE EMPLOYER IS A NON-SUBSCRIBER, THE EMPLOYEE LOSES

THOSE BENEFITS WHICH WOULD OTHERWISE ACCRUE UNDER THE WORKERS’ COMPENSATION LAWS. THE EMPLOYER MUST COMPLY WITH THE WORKERS’

COMPENSATION LAW AS IT PERTAINS TO NON-SUBSCRIBERS AND THE REQUIRED NOTIFICATIONS THAT MUST BE FILED AND POSTED.

ESC Region 20 Benefits Co-op

15

Premiums The premium rates may be changed by Us. If the rates are changed, We will give You at least 31 days advance written notice. If a change in benefits increases Our liability, premium rates may be changed on the date Our liability is increased. This plan may be continued in accordance with the Consolidated Omnibus Reconciliation Act of 1986.

Exclusions We will pay no benefits for any expenses incurred during any period the Covered Person does not have coverage under your Employer’s Medical Plan, except as provided in the Absence of your Employer’s Medical Plan provision or which result from: (a) suicide or any attempt, thereof, while sane or insane; (b) any intentionally self-inflicted injury or Sickness; (c) rest care or rehabilitative care and treatment; (d) outpatient routine newborn care; (e) voluntary abortion except, with respect to You or Your covered

Dependent spouse: (1) where Your or Your Dependent spouse’s life would be endangered if the fetus were carried to term; or (2) where medical complications have arisen from abortion; (f) pregnancy of a Dependent child; (g) participation in a riot, civil commotion, civil disobedience, or unlawful assembly. This does not include a loss which occurs while acting in a lawful manner within the scope of authority; (h) commission of a felony; (i) participation in a contest of speed in power driven vehicles, parachuting, or hang gliding; (j) air travel, except: (1) as a fare-paying passenger on a commercial airline on a regularly scheduled route; or (2) as a passenger for transportation only and not as a pilot or crew member; (k) intoxication; (Whether or not a person is intoxicated is determined

and defined by the laws and jurisdiction of the geographical area in which the loss occurred.)

(l) alcoholism or drug use, unless such drugs were taken on the advice of a Physician and taken as prescribed; (m) sex changes; (n) experimental treatment, drugs, or surgery; (o) an act of war, whether declared or undeclared, or while

performing police duty as a member of any military or naval organization; (This exclusion includes Accident sustained or Sickness contracted while in the service of any military, naval, or air force of any country engaged in war. We will refund the pro rata unearned premium for any such period the Covered Person is not covered.)

(p) Accident or Sickness arising out of and in the course of any occupation for compensation, wage or profit; (This does not apply to those sole proprietors or partners not covered by Workers’ Compensation.)

(q) mental illness or functional or organic nervous disorders, regardless of the cause; (r) dental or vision services, including treatment, surgery, extractions,

or x-rays, unless: (1) resulting from an Accident occurring while the Covered Person’s coverage is in force and if performed within 12 months of the date of such Accident; or (2) due to congenital disease or anomaly of a covered newborn child. (s) routine examinations, such as health exams, periodic check-ups, or routine physicals, except when part of Inpatient routine newborn care; (t) any expense for which benefits are not payable under the Covered Person’s Employer’s Medical Plan; or (u) air or ground ambulance.

Termination of Coverage Your Insurance coverage will end on the earliest of these dates: the date You no longer qualify as an Insured; the end of the last period for which premium has been paid; the date the Policy is discontinued; the date You retire; if You work for an employer employing less than 20 employees on a typical work day in the preceding Calendar Year, the date You attain age 70; the date You cease to be on Active Service; the date Your coverage under Another Medical Plan ends; or the date You cease employment with the employer through whom You originally became insured under the Policy. Insurance coverage on a Dependent will end on the earliest of these dates: the date Your coverage terminates; the end of the last period for which premium has been paid; the date the Dependent no longer meets the definition of Dependent; the date the Dependent’s coverage under Another Medical Plan ends; or the date the Policy is modified so as to exclude Dependent coverage. We may end the coverage of any Covered Person who submits a fraudulent claim. We may end the coverage of a Subscribing Unit if fewer persons are insured than the Policyholder’s application requires.

MEDlink® Limited Benefit Medical Expense Supplemental Insurance

Underwritten by American Public Life Insurance Company. This is a brief description of the coverage. For complete benefits, limitations, exclusions and other provisions, please refer to the policy and riders. This coverage does not replace Workers’ Compensation Insurance. This product is inappropriate for people who are eligible for Medicaid coverage. | This policy is considered an employee welfare benefit plan established and/or maintained by an association or employer intended to be covered by ERISA, and will be administered and enforced under ERISA. Group policies issued to governmental entities and municipalities may be exempt from ERISA guidelines. | Policy Form MEDlink® Series | Texas | Limited Benefit Medical Expense Supplemental Insurance | (10/14) | ESC Region 20 Benefits Co-op

APSB-22330(TX)-0116 MGM/FBS ESC Region 20 Benefits Co-op

2305 Lakeland Drive | Flowood, MS 39232

ampublic.com | 800.256.8606

16

MEDlink® Limited Benefit Medical Expense Supplemental Insurance

17

Accident insurance is designed to supplement your medical insurance coverage by covering indirect costs that can arise with a serious, or a not-so-serious, injury. Accident coverage is low cost protection available to you and your family without evidence of insurability.

About this Benefit

Accident

of disabling injuries suffered by American workers are not work related.

DID YOU KNOW?

36% of American workers report they always or usually live paycheck to paycheck.

2/3

AMERICAN PUBLIC LIFE YOUR BENEFITS PACKAGE

This is a general overview of your plan benefits. If the terms of this outline differ from your policy, the policy will govern. Additional plan details on covered expenses, limitations and exclusions are included in the summary plan description located on the

ESC Region 20 BC Benefits Website: www.esc20bc.net 18

Accident insurance is designed to supplement your medical insurance coverage by covering indirect costs that can arise with a serious, or a not-so-serious,injury. Accident coverage is low cost protectionavailable to you and your family without evidence of insurability.

About this Benefit

AccidentYOUR

BENEFITS

A-3 Supplemental Limited Benefit Accident Expense Insurance

THE POLICY UNDER WHICH THIS CERTIFICATE IS ISSUED IS NOT A POLICY OF WORKERS’ COMPENSATION INSURANCE. THE EMPLOYER DOES NOT BECOME A

SUBSCRIBER TO THE WORKERS’ COMPENSATION SYSTEM BY PURCHASING THE POLICY AND IF THE EMPLOYER IS A NON-SUBSCRIBER, THE EMPLOYEE LOSES

THOSE BENEFITS WHICH WOULD OTHERWISE ACCRUE UNDER THE WORKERS’ COMPENSATION LAWS. THE EMPLOYER MUST COMPLY WITH THE WORKERS’

COMPENSATION LAW AS IT PERTAINS TO NON-SUBSCRIBERS AND THE REQUIRED NOTIFICATIONS THAT MUST BE FILED AND POSTED.

Summary of Benefits*

Benefit Description Level 1 - 1 Unit

Accidental Death - per unit $5,000

Medical Expense Accidental Injury Benefit - per unit actual charges up to $500

Daily Hospital Confinement Benefit $75 per day

Air and Ground Ambulance Benefit actual charges up to $1,250

Accidental Dismemberment BenefitSingle finger or toe Multiple fingers or toes Single hand, arm, foot or leg Multiple hands, arms, feet or legs

$500 $500

$2,500 $5,000

Accidental Loss of Sight Benefit - per unit Loss of Sight in one eye

Loss of Sight in both eyes $2,500 $5,000

Individual Individual & Spouse

1 Parent Family

2 Parent Family

Level 1 - 1 Unit $10.80 $19.40 $21.20 $29.80

*The premium and amount of benefits vary dependent upon the Plan selected at time of application. Premiums are subject to

increase with notice.

of disabling injuries

suffered by American

workers are not work

related.

DID YOU KNOW?

36% of American workers

report they always or

usually live paycheck

to paycheck.

2/3

This is a general overview of your plan benefits. If the terms of this outline differ from your policy, the policy will govern. Additional plan details on covered expenses, limitations and exclusions are included in the summary plan description located on the

ESC Region 20 benefits Co-op Benefits Website: www.mybenefitshub.com/region20

AMERICAN PUBLIC LIFE

APSB-22329(TX)-MGM/FBS ESC Region 20 Benefits Co-op

ESC Region 20 Benefits Co-op

19

A-3 Supplemental Limited Benefit Accident Expense Insurance A-3 Supplemental Limited Benefit Accident Expense Insurance

Underwritten by American Life Insurance Company. This is a brief description of the coverage. For actual benefits, limitations, exclusions and other provisions, please refer to the policy and riders. This coverage does not replace Workers’ Compensation Insurance. | This product is inappropriate for people who are eligible for Medicaid coverage. | Policy Form A3 Series | Texas | Supplemental Limited Benefit Accident Expense Insurance Policy | (10/14) | ESC Region 20 Benefits Co-op

Limitations and Exclusions Eligibility This policy will be issued to only those persons who meet American Public Life Insurance Company’s insurability requirements. Persons not meeting APL’s insurability requirements will be excluded from coverage by an endorsement attached to the policy.

Base Policy No benefits are payable for a pre-existing condition. Pre-existing condition means an Injury that pertains solely to an Accidental Bodily Injury which resulted from an accident sustained before the Effective Date of coverage. Pre-Existing Conditions specifically named or described as permanently excluded in any part of this contract are never covered. A Hospital is not an institution which is primarily a place for alcoholics or drug addicts; the aged; a nursing, rest or convalescent nursing home; a mental institution or sanitarium; a facility contracted for or operated by the United States Government for treatment of members or ex-members of the armed forces (unless You are legally required to pay for services rendered in the absence of insurance); or, a long-term nursing unit or geriatrics ward.

Medical Expense Accidental Injury Benefit Expenses must commence within 60 days of the covered accident. The maximum benefit amount payable for any one accident for the Insured Person shall not exceed the Medical Expense Benefit.

Air and Ground Ambulance Benefit Emergency transportation must occur within 21 calendar days of the accident causing such Injury.

Daily Hospital Confinement Benefit The maximum benefit period for this benefit is 30 days per covered accident.

Accidental Death Accidental Death must result within 90 days of the covered accident causing the injury.

Accidental Dismemberment Benefit The total amount payable for all Losses resulting from the same accident will not exceed the Maximum Dismemberment Benefit of $5,000 cumulative per unit, per Accident. Loss must be within 90 days of the accident causing such Injury.

Exclusions Benefits otherwise provided by this Policy will not be payable for services or expenses or any such Loss resulting from or in connection with:

(1) sickness, illness or bodily infirmity; (2) suicide, attempted suicide or intentional self-inflicted Injury, whether sane or insane; (3) dental care or treatment unless due to accidental Injury to natural teeth; (4) war or any act of war (whether declared or undeclared) or participating in a riot or felony; (5) alcoholism or drug addiction; (6) travel or flight in or descent from any aircraft or device which can fly above the earth’s surface in any capacity other than as a fare paying passenger on a regularly scheduled airline; (7) Injury originating prior to the effective date of the Policy; (8) Injury occurring while intoxicated (Intoxication means that which is determined and defined by the laws and jurisdiction of the geographical area in which the loss or cause of loss is incurred.); (9) Voluntary inhalation of gas or fumes or taking of poison or asphyxiation; (10) Voluntary ingestion or injection of any drug, narcotic or sedative, unless administered on the advice and taken in such doses as prescribed by a Physician; (11) Injury sustained or sickness which first manifests itself while on full-time duty in the armed forces; (Upon notice, We will refund the proportion of unearned premium while in such forces.) (12) Injury incurred while engaging in an illegal occupation; (13) Injury incurred while attempting to commit a felony or an assault; (14) Injury to a covered person while practicing for or being a part of organized or competitive rodeo, sky diving, hang gliding, parachuting or scuba diving;

(15) driving in any race or speed test or while testing an automobile or any vehicle on any racetrack or speedway;

(16) hernia, carpal tunnel syndrome or any complication therefrom;

If You are entitled to benefits under this Policy as a result of sprained or lame back, or any intervertebral disk conditions, such benefits shall be payable for a maximum period of time, not exceeding in the aggregate three (3) months for any Injury.

Guaranteed Renewable You have the right to renew this Policy until the first premium due date on or after Your 69th birthday, if you pay the correct premium when due or within the Grace Period. When an Insured’s coverage terminates at age 70, coverage for other Insured Persons, if any, shall continue under this Policy. We have the right to change premium rates by class.

APSB-22329(TX)-MGM/FBS ESC Region 20 Benefits Co-op APSB-22329(TX)-MGM/FBS ESC Region 20 Benefits Co-op

2305 Lakeland Drive | Flowood, MS 39232

ampublic.com | 800.256.8606

20

A-3 Supplemental Limited Benefit Accident Expense Insurance A-3 Supplemental Limited Benefit Accident Expense Insurance

Underwritten by American Life Insurance Company. This is a brief description of the coverage. For actual benefits, limitations, exclusions and other provisions, please refer to the policy and riders. This coverage does not replace Workers’ Compensation Insurance. | This product is inappropriate for people who are eligible for Medicaid coverage. | Policy Form A3 Series | Texas | Supplemental Limited Benefit Accident Expense Insurance Policy | (10/14) | ESC Region 20 Benefits Co-op

Limitations and Exclusions Eligibility This policy will be issued to only those persons who meet American Public Life Insurance Company’s insurability requirements. Persons not meeting APL’s insurability requirements will be excluded from coverage by an endorsement attached to the policy.

Base Policy No benefits are payable for a pre-existing condition. Pre-existing condition means an Injury that pertains solely to an Accidental Bodily Injury which resulted from an accident sustained before the Effective Date of coverage. Pre-Existing Conditions specifically named or described as permanently excluded in any part of this contract are never covered. A Hospital is not an institution which is primarily a place for alcoholics or drug addicts; the aged; a nursing, rest or convalescent nursing home; a mental institution or sanitarium; a facility contracted for or operated by the United States Government for treatment of members or ex-members of the armed forces (unless You are legally required to pay for services rendered in the absence of insurance); or, a long-term nursing unit or geriatrics ward.

Medical Expense Accidental Injury Benefit Expenses must commence within 60 days of the covered accident. The maximum benefit amount payable for any one accident for the Insured Person shall not exceed the Medical Expense Benefit.

Air and Ground Ambulance Benefit Emergency transportation must occur within 21 calendar days of the accident causing such Injury.

Daily Hospital Confinement Benefit The maximum benefit period for this benefit is 30 days per covered accident.

Accidental Death Accidental Death must result within 90 days of the covered accident causing the injury.

Accidental Dismemberment Benefit The total amount payable for all Losses resulting from the same accident will not exceed the Maximum Dismemberment Benefit of $5,000 cumulative per unit, per Accident. Loss must be within 90 days of the accident causing such Injury.

Exclusions Benefits otherwise provided by this Policy will not be payable for services or expenses or any such Loss resulting from or in connection with:

(1) sickness, illness or bodily infirmity; (2) suicide, attempted suicide or intentional self-inflicted Injury, whether sane or insane; (3) dental care or treatment unless due to accidental Injury to natural teeth; (4) war or any act of war (whether declared or undeclared) or participating in a riot or felony; (5) alcoholism or drug addiction; (6) travel or flight in or descent from any aircraft or device which can fly above the earth’s surface in any capacity other than as a fare paying passenger on a regularly scheduled airline; (7) Injury originating prior to the effective date of the Policy; (8) Injury occurring while intoxicated (Intoxication means that which is determined and defined by the laws and jurisdiction of the geographical area in which the loss or cause of loss is incurred.); (9) Voluntary inhalation of gas or fumes or taking of poison or asphyxiation; (10) Voluntary ingestion or injection of any drug, narcotic or sedative, unless administered on the advice and taken in such doses as prescribed by a Physician; (11) Injury sustained or sickness which first manifests itself while on full-time duty in the armed forces; (Upon notice, We will refund the proportion of unearned premium while in such forces.) (12) Injury incurred while engaging in an illegal occupation; (13) Injury incurred while attempting to commit a felony or an assault; (14) Injury to a covered person while practicing for or being a part of organized or competitive rodeo, sky diving, hang gliding, parachuting or scuba diving;

(15) driving in any race or speed test or while testing an automobile or any vehicle on any racetrack or speedway;

(16) hernia, carpal tunnel syndrome or any complication therefrom;

If You are entitled to benefits under this Policy as a result of sprained or lame back, or any intervertebral disk conditions, such benefits shall be payable for a maximum period of time, not exceeding in the aggregate three (3) months for any Injury.

Guaranteed Renewable You have the right to renew this Policy until the first premium due date on or after Your 69th birthday, if you pay the correct premium when due or within the Grace Period. When an Insured’s coverage terminates at age 70, coverage for other Insured Persons, if any, shall continue under this Policy. We have the right to change premium rates by class.

APSB-22329(TX)-MGM/FBS ESC Region 20 Benefits Co-op APSB-22329(TX)-MGM/FBS ESC Region 20 Benefits Co-op

2305 Lakeland Drive | Flowood, MS 39232

ampublic.com | 800.256.8606

21

Dental insurance is a coverage that helps defray the costs of dental care. It insures against the expense of routine care, treatment and dental disease.

About this Benefit

Dental

Good dental care may improve your overall health.

Also Women with gum disease may be at greater risk of giving birth to a preterm or low birth weight baby.

DID YOU KNOW?

CIGNA YOUR BENEFITS PACKAGE

This is a general overview of your plan benefits. If the terms of this outline differ from your policy, the policy will govern. Additional plan details on covered expenses, limitations and exclusions are included in the summary plan description located on the

ESC Region 20 BC Benefits Website: www.esc20bc.net 22

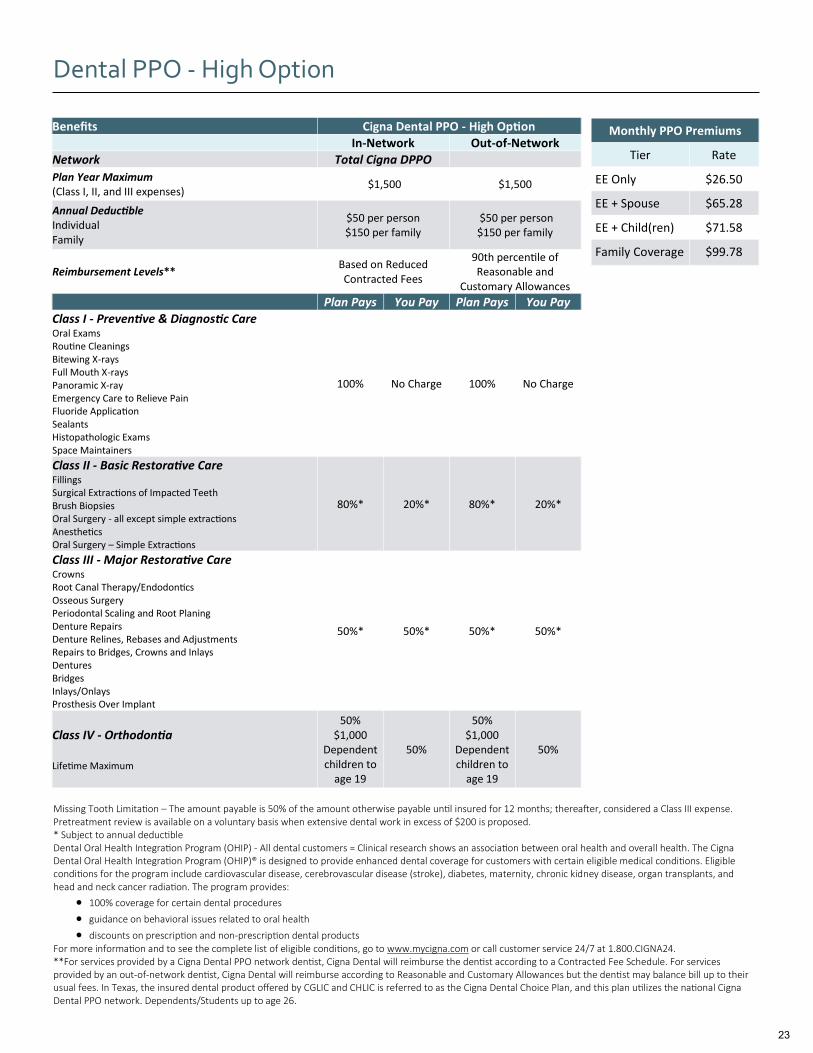

Dental PPO - High Option

Benefits Cigna Dental PPO - High Option

In-Network Out-of-Network

Network Total Cigna DPPO

Plan Year Maximum (Class I, II, and III expenses)

$1,500 $1,500

Annual Deductible Individual Family

$50 per person $150 per family

$50 per person $150 per family

Reimbursement Levels** Based on Reduced Contracted Fees

90th percentile of Reasonable and

Customary Allowances

Plan Pays You Pay Plan Pays You Pay

Class I - Preventive & Diagnostic Care Oral Exams Routine Cleanings Bitewing X-rays Full Mouth X-rays Panoramic X-ray Emergency Care to Relieve Pain Fluoride Application Sealants Histopathologic Exams Space Maintainers

100% No Charge 100% No Charge

Class II - Basic Restorative Care Fillings Surgical Extractions of Impacted Teeth Brush Biopsies Oral Surgery - all except simple extractions Anesthetics Oral Surgery – Simple Extractions

80%* 20%* 80%* 20%*

Class III - Major Restorative Care Crowns Root Canal Therapy/Endodontics Osseous Surgery Periodontal Scaling and Root Planing Denture Repairs Denture Relines, Rebases and Adjustments Repairs to Bridges, Crowns and Inlays Dentures Bridges Inlays/Onlays Prosthesis Over Implant

50%* 50%* 50%* 50%*

Class IV - Orthodontia Lifetime Maximum

50% $1,000

Dependent children to

age 19

50%

50% $1,000

Dependent children to

age 19

50%

Monthly PPO Premiums

Tier Rate

EE Only $26.50

EE + Spouse $65.28

EE + Child(ren) $71.58

Family Coverage $99.78

Missing Tooth Limitation – The amount payable is 50% of the amount otherwise payable until insured for 12 months; thereafter, considered a Class III expense. Pretreatment review is available on a voluntary basis when extensive dental work in excess of $200 is proposed. * Subject to annual deductible Dental Oral Health Integration Program (OHIP) - All dental customers = Clinical research shows an association between oral health and overall health. The Cigna Dental Oral Health Integration Program (OHIP)® is designed to provide enhanced dental coverage for customers with certain eligible medical conditions. Eligible conditions for the program include cardiovascular disease, cerebrovascular disease (stroke), diabetes, maternity, chronic kidney disease, organ transplants, and head and neck cancer radiation. The program provides:

100% coverage for certain dental procedures

guidance on behavioral issues related to oral health

discounts on prescription and non-prescription dental products For more information and to see the complete list of eligible conditions, go to www.mycigna.com or call customer service 24/7 at 1.800.CIGNA24. **For services provided by a Cigna Dental PPO network dentist, Cigna Dental will reimburse the dentist according to a Contracted Fee Schedule. For services provided by an out-of-network dentist, Cigna Dental will reimburse according to Reasonable and Customary Allowances but the dentist may balance bill up to their usual fees. In Texas, the insured dental product offered by CGLIC and CHLIC is referred to as the Cigna Dental Choice Plan, and this plan utilizes the national Cigna Dental PPO network. Dependents/Students up to age 26.

23

Dental PPO - Low Option

Benefits Cigna Dental PPO - Low Option

In-Network Out-of-Network

Network Total Cigna DPPO Plan Year Maximum (Class I, II, and III expenses)

$750 $750

Annual Deductible Individual Family

$50 per person $150 per family

$50 per person $150 per family

Reimbursement Levels** Based on Reduced Contracted Fees

Based on Maximum Allowable Charge (In-

network fee level)

Plan Pays You Pay Plan Pays You Pay

Class I - Preventive & Diagnostic Care Oral Exams Routine Cleanings Bitewing X-rays Full Mouth X-rays Panoramic X-ray Emergency Care to Relieve Pain Fluoride Application Sealants Histopathologic Exams Space Maintainers

100% No Charge 100% No Charge

Class II - Basic Restorative Care Fillings Brush Biopsies Oral Surgery – Simple Extractions

60%* 40%* 60%* 40%*

Class III - Major Restorative Care Crowns Root Canal Therapy/Endodontics Osseous Surgery Periodontal Scaling and Root Planing Surgical Extractions of Impacted Teeth Oral Surgery - all except simple extractions Anesthetics Denture Repairs Denture Relines, Rebases and Adjustments Repairs to Bridges, Crowns and Inlays Dentures Bridges Inlays/Onlays Prosthesis Over Implant

40%* 60%* 40%* 60%*

Class IV - Orthodontia Not covered 100% of your

dentist’s usual fees

Not covered 100% of your

dentist’s usual fees

Monthly PPO Premiums

Tier Rate

EE Only $13.28

EE + Spouse $26.98

EE + Child(ren) $31.02

Family Coverage $47.36

Missing Tooth Limitation – The amount payable is 50% of the amount otherwise payable until insured for 12 months; thereafter, considered a Class III expense. Pretreatment review is available on a voluntary basis when extensive dental work in excess of $200 is proposed. * Subject to annual deductible Dental Oral Health Integration Program (OHIP) - All dental customers = Clinical research shows an association between oral health and overall health. The Cigna Dental Oral Health Integration Program (OHIP)® is designed to provide enhanced dental coverage for customers with certain eligible medical conditions. Eligible conditions for the program include cardiovascular disease, cerebrovascular disease (stroke), diabetes, maternity, chronic kidney disease, organ transplants, and head and neck cancer radiation. The program provides:

100% coverage for certain dental procedures

guidance on behavioral issues related to oral health

discounts on prescription and non-prescription dental products For more information and to see the complete list of eligible conditions, go to www.mycigna.com or call customer service 24/7 at 1.800.CIGNA24. **For services provided by a Cigna Dental PPO network dentist, Cigna Dental will reimburse the dentist according to a Contracted Fee Schedule. For services provided by an out-of-network dentist, Cigna Dental will reimburse according to Reasonable and Customary Allowances but the dentist may balance bill up to their usual fees. In Texas, the insured dental product offered by CGLIC and CHLIC is referred to as the Cigna Dental Choice Plan, and this plan utilizes the national Cigna Dental PPO network. Dependents/Students up to age 26.

24

Dental PPO - High and Low Options

Procedure Exclusions and Limitations Late Entrants Limit None Exams Two per Plan year Prophylaxis (Cleanings) Two per Plan year Fluoride 1 per Plan year for people under 19 Histopathologic Exams Various limits per Plan year depending on specific test X-Rays (routine) Bitewings: 2 per Plan year X-Rays (non-routine) Full mouth: 1 every 36 consecutive months, Panorex: 1 every 36 consecutive months Model Payable only when in conjunction with Ortho workup Minor Perio (non-surgical) Various limitations depending on the service Perio Surgery Various limitations depending on the service Crowns and Inlays Replacement every 5 years Bridges Replacement every 5 years Dentures and Partials Replacement every 5 years Relines, Rebases Covered if more than 6 months after installation Adjustments Covered if more than 6 months after installation Repairs - Bridges Reviewed if more than once Repairs - Dentures Reviewed if more than once Sealants Limited to posterior tooth. One treatment per tooth every three years up to age 14 Space Maintainers Limited to non-Orthodontic treatment Prosthesis Over Implant 1 per 60 consecutive months if unserviceable and cannot be repaired. Benefits are based on the amount payable for nonprecious metals. No porcelain or white/tooth colored material on molar crowns or bridges Alternate Benefit When more than one covered Dental Service could provide suitable treatment based on common dental standards, Cigna HealthCare will determine the covered Dental Service on which payment will be based and the expenses that will be included as Covered Expenses

Benefit Exclusions Services performed primarily for cosmetic reasons Replacement of a lost or stolen appliance Replacement of a bridge or denture within five years following the date of its original installation Replacement of a bridge or denture which can be made useable according to accepted dental standards Procedures, appliances or restorations, other than full dentures, whose main purpose is to change vertical dimension, diagnose or treat

conditions of TMJ, stabilize periodontally involved teeth, or restore occlusion Veneers of porcelain or acrylic materials on crowns or pontics on or replacing the upper and lower first, second and third molars Bite registrations; precision or semi-precision attachments; splinting A surgical implant of any type Instruction for plaque control, oral hygiene and diet Dental services that do not meet common dental standards Services that are deemed to be medical services Services and supplies received from a hospital Charges which the person is not legally required to pay Charges made by a hospital which performs services for the U.S. Government if the charges are directly related to a condition

connected to a military service Experimental or investigational procedures and treatments Any injury resulting from, or in the course of, any employment for wage or profit Any sickness covered under any workers’ compensation or similar law Charges in excess of the reasonable and customary allowances To the extent that payment is unlawful where the person resides when the expenses are incurred; Procedures performed by a Dentist who is a member of the covered person’s family (covered person’s family is limited to a spouse,

siblings, parents, children, grandparents, and the spouse’s siblings and parents); For charges which would not have been made if the person had no insurance; For charges for unnecessary care, treatment or surgery; To the extent that you or any of your Dependents is in any way paid or entitled to payment for those expenses by or through a public

program, other than Medicaid; To the extent that benefits are paid or payable for those expenses under the mandatory part of any auto insurance policy written to

comply with a “no-fault” insurance law or an uninsured motorist insurance law. Cigna HealthCare will take into account any adjustment option chosen under such part by you or any one of your Dependents.

In addition, these benefits will be reduced so that the total payment will not be more than 100% of the charge made for the Dental Service if benefits are provided for that service under this plan and any medical expense plan or prepaid treatment program sponsored or made available by your Employer.

This benefit summary highlights some of the benefits available under the proposed plan. A complete description regarding the terms of coverage, exclusions and limitations, including legislated benefits, will be provided in your insurance certificate or plan description. Benefits are insured and/or administered by Connecticut General Life Insurance Company. "Cigna HealthCare" refers to various operating subsidiaries of Cigna Corporation. Products and services are provided by these subsidiaries and not by Cigna Corporation. These subsidiaries include Connecticut General Life Insurance Company, Cigna Health and Life Insurance Company, and HMO or service company subsidiaries of Cigna Health Corporation and Cigna Dental Health, Inc. DPPO insurance coverage is set forth on the following policy form numbers: AR: HP-POL77; CA: HP-POL57; CO: HP-POL78; CT: HP-POL58; DE: HP-POL79; FL: HP-POL60; ID: HPPOL82; IL: HP-POL62; KS: HP-POL84; LA: HP-POL86: MA: HP-POL 63; MI: HP-POL88; MO: HP- POL65; MS: HP-POL90; NC: HP-POL96; NE: HP-POL92; NH: HP-POL94; NM: HP-POL95; NV: HP-POL93; NY: HP-POL67; OH: HP-POL98; OK: HP-POL99; OR: HP-POL68; PA: HP-POL100; RI: HP-POL101; SC: HP-POL102; SD: HP-POL103; TN: HP-POL69; TX: HP-POL70; UT: HP-POL104; VA: HP-POL72; VT: HP-POL71; WA: POL-07/08; WI: HP-POL107; WV: HP-POL106; and WY: HP-POL108. “Cigna,” the “Tree of Life” logo and “Cigna Dental Care” are registered service marks of Cigna Intellectual Property, Inc., licensed for use by Cigna Corporation and its operating subsidiaries. All products and services are provided by or through such operating subsidiaries and not by Cigna Corporation. Such operating subsidiaries include Connecticut General Life Insurance Company (CGLIC), Cigna Health and Life Insurance Company (CHLIC), Cigna HealthCare of Connecticut, Inc., and Cigna Dental Health, Inc. and its subsidiaries. Cigna Dental PPO plans are underwritten or administered by CGLIC or CHLIC, with network management services provided by Cigna Dental Health, Inc. and certain of its subsidiaries. In Arizona and Louisiana, the insured Dental PPO plan offered by CGLIC is known as the “CG Dental PPO”. In Texas, the insured dental product offered by CGLIC and CHLIC is referred to as the Cigna Dental Choice Plan, and this plan utilizes the national Cigna Dental PPO network. Cigna Dental Care (DHMO) plans are underwritten or administered by Cigna Dental Health Plan of Arizona, Inc., Cigna Dental Health of California, Inc., Cigna Dental Health of Colorado, Inc., Cigna Dental Health of Delaware, Inc., Cigna Dental Health of Florida, Inc., a Prepaid Limited Health Services Organization licensed under Chapter 636, Florida Statutes, Cigna Dental Health of Kansas, Inc. (Kansas and Nebraska), Cigna Dental Health of Kentucky, Inc. (Kentucky and Illinois), Cigna Dental Health of Maryland, Inc., Cigna Dental Health of Missouri, Inc., Cigna Dental Health of New Jersey, Inc., Cigna Dental Health of North Carolina, Inc., Cigna Dental Health of Ohio, Inc., Cigna Dental Health of Pennsylvania, Inc., Cigna Dental Health of Texas, Inc., and Cigna Dental Health of Virginia, Inc. In other states, Cigna Dental Care plans are underwritten by CGLIC, CHLIC, or Cigna HealthCare of Connecticut, Inc. and administered by Cigna Dental Health, Inc. BSD46380 © 2015 Cigna

25

Dental DHMO

Monthly DHMO Premiums

Tier Rate

EE Only $8.99

EE + Spouse $16.99

EE + Child(ren) $19.15

Family Coverage $29.66

What You’ll Pay

Sampling of covered procedures Cost with Cigna Dental Care

Estimated cost without dental coverage

Adult cleaning (two per calendar year each at $0) (additional cleanings available at $45 each)

$0 $70–$136 each

Child cleaning (two per calendar year each at $0) (additional cleanings available at $30 each)

$0 $53–$102 each

Periodic oral evaluation $0 $40–$76

Comprehensive oral evaluation $0 $62–$118

Topical fluoride (two per calendar year each at $0) (additional topical fluoride available at $15 each)

$0 $28–$53

X–rays – (bitewings) 2 films $0 $33–$63

X–rays – panoramic film $0 $84–$161

Sealant – per tooth $17 $42–$80

Amalgam filling (silver colored) – 2 surfaces $28 $118–$226

Composite filling (tooth–colored) – 1 surface, Anterior $33 $120–$231

Molar root canal (excluding final restoration) $595 $852–$1,640

Comprehensive orthodontics – child (up to 19th birthday) – Banding

$515 $1,042–$2,005

Periodontal (gum) scaling & root planing – 1 quadrant $135 $179–$344

Periodontal (gum) maintenance $93 $109–$209

Removal/extraction of erupted tooth $64 $120–$231

Removal/extraction of impacted tooth $300 $370–$712

Crown – porcelain fused to high noble metal $480 $849–$1,634

Implant supported retainer for porcelain fused to metal fixed partial denture

$780 $1,097–$2,112

Occlusal appliance, by report (for treatment of TMJ) $575 $640–$1,233

Procedure Limit

Exams Two per calendar year

X-rays (routine) Bitewings: 2 per calendar year

X-rays (non-routine) Full mouth: 1 every 3 calendar years. Panorex: 1 every 3 calendar years

Crowns and inlays Replacement every 5 years

Bridges Replacement every 5 years

Dentures and partials Replacement every 5 years

Relines, rebases One every 36 months

Adjustments Four within the first 6 months after installation

Prosthesis over implant Replacement every 5 years if unserviceable and can-not be repaired

Temporomandibular

Joint (TMJ) treatment One occlusal orthotic device per 24 months

Athletic mouth guard One athletic mouth guard per 12 months when listed on your PCS

Finding a network dentist is easy. There are several ways to chooseyour network general dentist: Find a dentist at Cigna.com. Our

online dental directory is updated weekly.

Call 1.800.Cigna24 (1.800.244.6224) to speak with a customer service representative.Our representatives can send youa customized dental directorylisting via email.

26

Dental DHMO

Under your plan, you have coverage for hundreds of dental procedures. This overview shows you a small sampling of covered services and what you will pay compared to your estimated cost without coverage. See savings below! Review your plan materials to understand how your plan works. For questions on the plan before enrollment, call 1.800.Cigna24 (1.800.244.6224) and select the “Enrollment Information” prompt. Key plan features

There is a $5 office visit fee associated with your plan.

No deductibles – you don’t have to reach a certain level of out-of-pocket expenses before your insurance kicks in.

No dollar maximums – you don’t have to worry about your coverage running out after your covered expenses reach a certain dollar amount.

Easy to understand plan – the fees you pay your dentist are clearly listed on your Patient Charge Schedule (PCS).

There are no claim forms to fill and no waiting periods for coverage.

The network general dentist you choose will manage your overall dental care.

Covered family members can choose their own network general dentists – near home, work or school.

You don’t need a referral for children under seven to visit a network pediatric dentist. And you don’t need a referral to see a network orthodontist.

There’s no age limit on sealants, which help prevent tooth decay.

Your plan covers certain procedures to help detect oral cancer in its early stages.

24/7 access to the Dental Information Line—this line is staffed by trained professionals who can help you if you have questions about dental treatment and clinical symptoms.

Referrals are required for specialty care services. Specialty treatment plans require payment authorization for services to be covered under your plan, except for Pediatrics, Orthodontics and Endodontics. You should verify with your Network Specialty Dentist that your treatment plan has been authorized for payment by Cigna before treatment begins. Listed below are the services or expenses which are NOT covered under your Dental Plan and which are your responsibility at the dentist’s usual fees. There is no coverage for: Or in connection with an injury arising out of, or in the course of,

any employment for wage or profit Charges which would not have been made in any facility, other

than a hospital or a correctional institution owned or operated by the United States government or by a state or municipal government if the person had no insurance

To the extent that payment is unlawful where the person resides when the expenses are incurred or the services are received

The charges which the person is not legally required to pay Charges which would not have been made if the person had

no insurance Due to injuries which are intentionally self-inflicted Services not listed on the PCS Services provided by a non-network dentist without Cigna

Dental’s prior approval (except emergencies, as described in your plan documents)

Services related to an injury or illness paid under workers’ compensation, occupational disease or similar laws

Services provided or paid by or through a federal or state governmental agency or authority, political subdivision or a public program, other than Medicaid

Services required while serving in the armed forces of any country or international authority or relating to a declared or undeclared war or acts of war

Services performed primarily for cosmetic reasons unless specifically listed on your PCS

General anesthesia, sedation and nitrous oxide, unless specifically listed on your PCS

Prescription medications Replacement of filled and/or removable appliances (including

filled and removable orthodontic appliances) that have been lost, stolen, or damaged due to patient abuse, misuse or neglect

Surgical implant of any type unless specifically listed on your PCS

Services considered to be unnecessary or experimental in nature or do not meet commonly accepted dental standards

Procedures or appliances for minor tooth guidance or to control harmful habits

Services and supplies received from a hospital The completion of crowns, bridges, dentures, or root canal

treatment already in progress on the effective date of your Cigna Dental coverage

The completion of implant supported prosthesis (including crowns, bridges and dentures) already in progress on the effective date of your Cigna Dental coverage, unless specifically listed on your PCS4

Consultations and/or evaluations associated with services that are not covered

Endodontic treatment and/or periodontal (gum tissue and supporting bone) surgery of teeth exhibiting a poor or hopeless periodontal prognosis

Bone grafting and/or guided tissue regeneration when performed at the site of a tooth extraction unless specifically listed on your PCS

Bone grafting and/or guided tissue regeneration when performed in conjunction with an apicoectomy or periradicular surgery

Intentional root canal treatment in the absence of injury or disease to solely facilitate a restorative procedure

Services performed by a prosthodontist Localized delivery of antimicrobial agents when performed

alone or in the absence of traditional periodontal therapy Any localized delivery of antimicrobial agent procedures when

more than eight (8) of these procedures are reported on the same date of service.

Infection control and/or sterilization The recementation of any inlay, onlay, crown, post and core

or filled bridge within 180 days of initial placement The recementation of any implant supported prosthesis

(including crowns, bridges and dentures) within 180 days of initial placement

Services to correct congenital malformations, including the replacement of congenitally missing teeth

The replacement of an occlusal guard (night guard) beyond one per any 24 consecutive month period, when this limitation is noted on the PCS

Crowns, bridges and/or implant supported prosthesis used solely for splinting

Resin bonded retainers and associated pontics

27

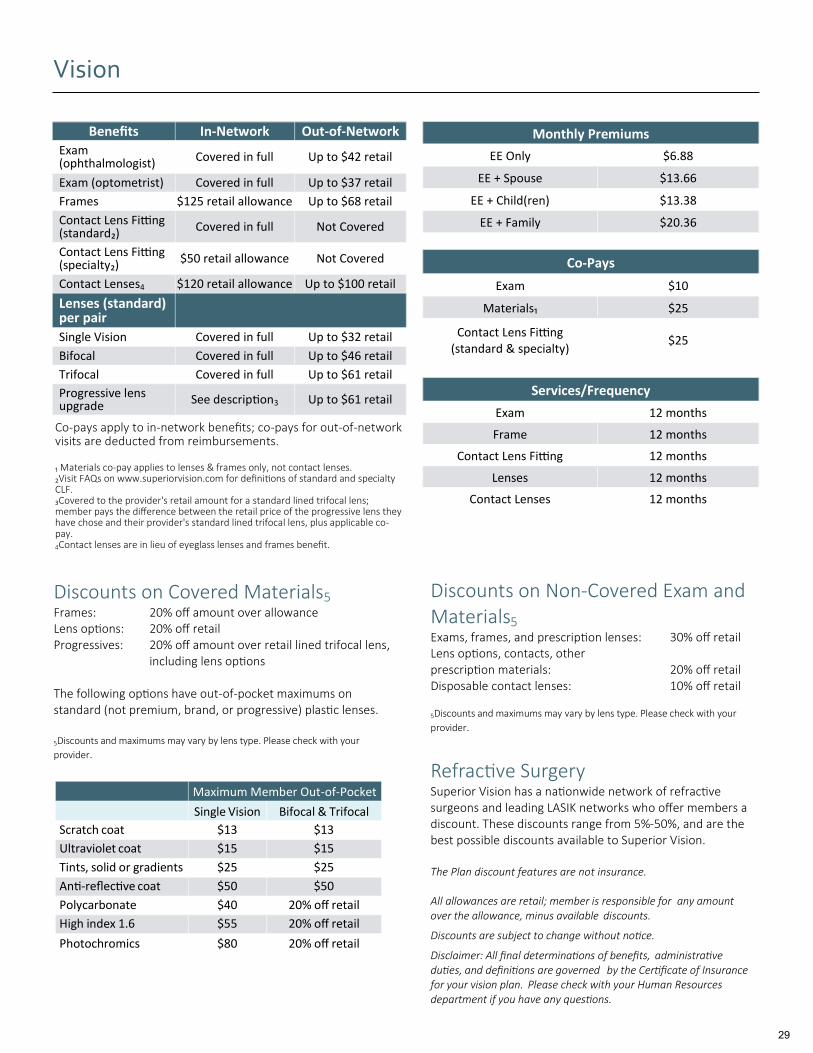

Vision insurance provides coverage for routine eye examinations and may cover all or part of the costs associated with contact lenses, eyeglasses and vision correction, depending on the plan.

About this Benefit

Vision

75%

DID YOU KNOW?

of U.S. residents between age 25 and 64 require some sort of vision

correction.

SUPERIOR VISION YOUR BENEFITS PACKAGE

This is a general overview of your plan benefits. If the terms of this outline differ from your policy, the policy will govern. Additional plan details on covered expenses, limitations and exclusions are included in the summary plan description located on the

ESC Region 20 BC Benefits Website: www.esc20bc.net 28

Co-Pays

Exam $10

Materials₁ $25

Contact Lens Fitting (standard & specialty)

$25

Services/Frequency

Exam 12 months

Frame 12 months

Contact Lens Fitting 12 months

Lenses 12 months

Contact Lenses 12 months

Benefits In-Network Out-of-Network

Exam (ophthalmologist) Covered in full Up to $42 retail

Exam (optometrist) Covered in full Up to $37 retail

Frames $125 retail allowance Up to $68 retail

Contact Lens Fitting (standard₂) Covered in full Not Covered

Contact Lens Fitting (specialty₂) $50 retail allowance Not Covered

Contact Lenses4 $120 retail allowance Up to $100 retail

Lenses (standard) per pair

Single Vision Covered in full Up to $32 retail

Bifocal Covered in full Up to $46 retail

Trifocal Covered in full Up to $61 retail

Progressive lens upgrade See description3 Up to $61 retail

Co-pays apply to in-network benefits; co-pays for out-of-network visits are deducted from reimbursements. ₁ Materials co-pay applies to lenses & frames only, not contact lenses. ₂Visit FAQs on www.superiorvision.com for definitions of standard and specialty CLF. ₃Covered to the provider's retail amount for a standard lined trifocal lens; member pays the difference between the retail price of the progressive lens they have chose and their provider's standard lined trifocal lens, plus applicable co-pay. 4Contact lenses are in lieu of eyeglass lenses and frames benefit.

Vision

Discounts on Covered Materials5

Frames: 20% off amount over allowance Lens options: 20% off retail Progressives: 20% off amount over retail lined trifocal lens, including lens options The following options have out-of-pocket maximums on standard (not premium, brand, or progressive) plastic lenses. 5Discounts and maximums may vary by lens type. Please check with your

provider.

Maximum Member Out-of-Pocket

Single Vision Bifocal & Trifocal

Scratch coat $13 $13

Ultraviolet coat $15 $15

Tints, solid or gradients $25 $25

Anti-reflective coat $50 $50

Polycarbonate $40 20% off retail

High index 1.6 $55 20% off retail

Photochromics $80 20% off retail

Discounts on Non-Covered Exam and Materials5 Exams, frames, and prescription lenses: 30% off retail Lens options, contacts, other prescription materials: 20% off retail Disposable contact lenses: 10% off retail

5Discounts and maximums may vary by lens type. Please check with your

provider.

Refractive Surgery Superior Vision has a nationwide network of refractive surgeons and leading LASIK networks who offer members a discount. These discounts range from 5%-50%, and are the best possible discounts available to Superior Vision. The Plan discount features are not insurance. All allowances are retail; member is responsible for any amount over the allowance, minus available discounts.

Discounts are subject to change without notice.

Disclaimer: All final determinations of benefits, administrative duties, and definitions are governed by the Certificate of Insurance for your vision plan. Please check with your Human Resources department if you have any questions.

Monthly Premiums

EE Only $6.88

EE + Spouse $13.66

EE + Child(ren) $13.38

EE + Family $20.36

29

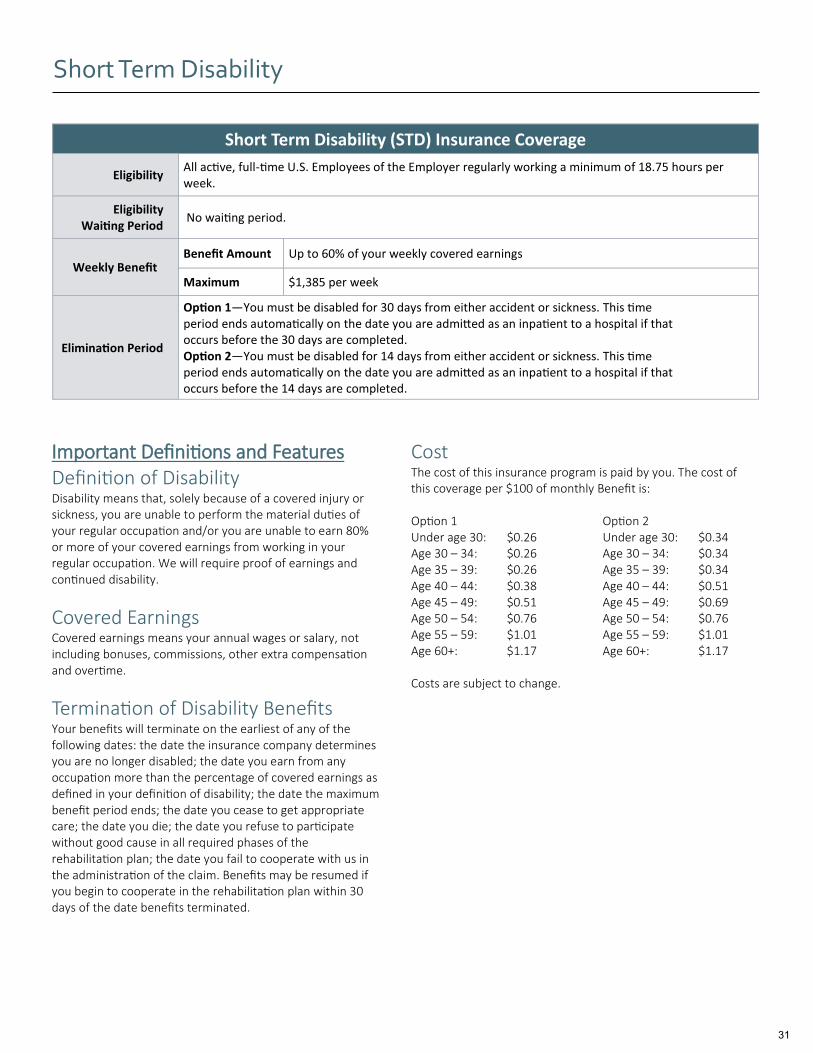

Disability insurance protects one of your most valuable assets, your ability to earn a living. This insurance will replace a portion of your income in the event that you become physically unable to work. Short term disability coverage provides benefits when you are unable to work for a short period of time due to a covered sickness or injury.

About this Benefit

Short Term Disability CIGNA

DID YOU KNOW?

60% of Americans do not have a “rainy day” fund to cover three

months of unanticipated financial emergencies.

YOUR BENEFITS PACKAGE

This is a general overview of your plan benefits. If the terms of this outline differ from your policy, the policy will govern. Additional plan details on covered expenses, limitations and exclusions are included in the summary plan description located on the

ESC Region 20 BC Benefits Website: www.esc20bc.net 30

Short Term Disability

Important Definitions and Features Definition of Disability Disability means that, solely because of a covered injury or sickness, you are unable to perform the material duties of your regular occupation and/or you are unable to earn 80% or more of your covered earnings from working in your regular occupation. We will require proof of earnings and continued disability.

Covered Earnings Covered earnings means your annual wages or salary, not including bonuses, commissions, other extra compensation and overtime.

Termination of Disability Benefits Your benefits will terminate on the earliest of any of the following dates: the date the insurance company determines you are no longer disabled; the date you earn from any occupation more than the percentage of covered earnings as defined in your definition of disability; the date the maximum benefit period ends; the date you cease to get appropriate care; the date you die; the date you refuse to participate without good cause in all required phases of the rehabilitation plan; the date you fail to cooperate with us in the administration of the claim. Benefits may be resumed if you begin to cooperate in the rehabilitation plan within 30 days of the date benefits terminated.

Cost The cost of this insurance program is paid by you. The cost of this coverage per $100 of monthly Benefit is: Option 1 Option 2 Under age 30: $0.26 Under age 30: $0.34 Age 30 – 34: $0.26 Age 30 – 34: $0.34 Age 35 – 39: $0.26 Age 35 – 39: $0.34 Age 40 – 44: $0.38 Age 40 – 44: $0.51 Age 45 – 49: $0.51 Age 45 – 49: $0.69 Age 50 – 54: $0.76 Age 50 – 54: $0.76 Age 55 – 59: $1.01 Age 55 – 59: $1.01 Age 60+: $1.17 Age 60+: $1.17 Costs are subject to change.

Short Term Disability (STD) Insurance Coverage

Eligibility All active, full-time U.S. Employees of the Employer regularly working a minimum of 18.75 hours per week.

Eligibility Waiting Period

No waiting period.

Weekly Benefit Benefit Amount Up to 60% of your weekly covered earnings

Maximum $1,385 per week

Elimination Period

Option 1—You must be disabled for 30 days from either accident or sickness. This time period ends automatically on the date you are admitted as an inpatient to a hospital if that occurs before the 30 days are completed. Option 2—You must be disabled for 14 days from either accident or sickness. This time period ends automatically on the date you are admitted as an inpatient to a hospital if that occurs before the 14 days are completed.

31

Short Term Disability

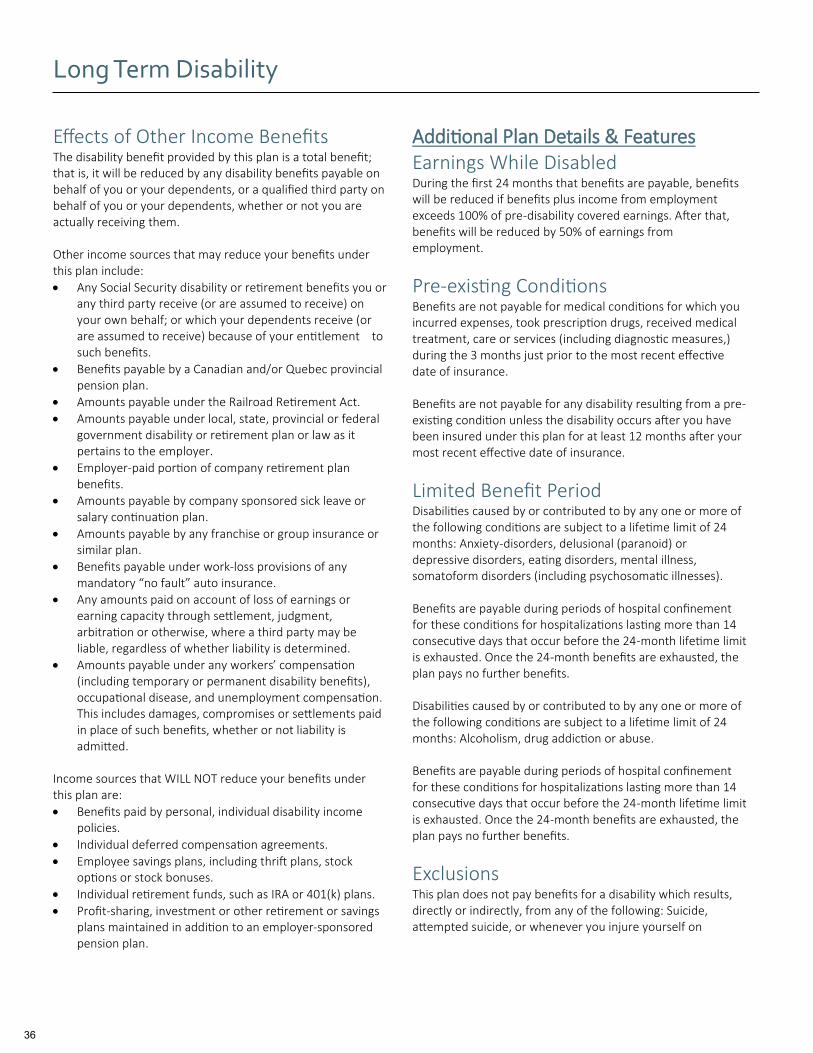

Effects of Other Income Benefits The disability benefit provided by this plan is a total benefit; that is, it will be reduced by any disability benefits payable on behalf of you or your dependents, or a qualified third party on behalf of you or your dependents, whether or not you are actually receiving them. Your disability benefits will not be reduced by any Social Security disability benefits you are not receiving as long as you cooperate fully in efforts to obtain them and agree to repay any overpayment when and if you do receive them. Other income sources that may reduce your benefits under this plan include:

Any Social Security disability or retirement benefits you or any third party receive (or are assumed to receive) on your own behalf; or which your dependents receive (or are assumed to receive) because of your entitlement to such benefits.

Benefits payable by a Canadian and/or Quebec provincial pension plan.

Amounts payable under the Railroad Retirement Act.

Amounts payable under any local, state, provincial or federal government disability or retirement plan or law as it pertains to the employer.

Employer-paid portion of company retirement plan benefits.

Amounts payable by company sponsored sick leave or salary continuation plan.

Amounts payable by any franchise or group insurance or similar plan.

Benefits payable under work-loss provisions of any mandatory “no fault” auto insurance.

Any amounts paid on account of loss of earnings or earning capacity through settlement, judgment, arbitration or otherwise, where a third party may be liable, regardless of whether liability is determined.

Income sources that WILL NOT reduce your benefits under this plan are:

Benefits paid by personal, individual disability income policies.

Individual deferred compensation agreements.

Employee savings plans, including thrift plans, stock options or stock bonuses.

Individual retirement funds, such as IRA or 401(k) plans.

Profit-sharing, investment or other retirement or savings plans maintained in addition to an employer-sponsored pension plan.

Additional Plan Details & Features