2016 · frm® exam review 2016 frm ® part i covers all topics in part i formula sheets

TRANSCRIPT

FRM® EXAM REVIEW2016

FRM PART I®

COVERS ALL TOPICS

IN PART I

FORMULA SHEETS

Cover image: Loewy Design Cover design: Loewy Design

Copyright © 2016 by John Wiley & Sons, Inc. All rights reserved.

Published by John Wiley & Sons, Inc., Hoboken, New Jersey.

Published simultaneously in Canada.

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, scanning, or otherwise, except as permitted under Section 107 or 108 of the 1976 United States Copyright Act, without either the prior written permission of the Publisher, or authorization through payment of the appropriate per-copy fee to the Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers, MA 01923, (978) 750-8400, fax (978) 646-8600, or on the Web at www.copyright.com. Requests to the Publisher for permission should be addressed to the Permissions Department, John Wiley & Sons, Inc., 111 River Street, Hoboken, NJ 07030, (201) 748-6011, fax (201) 748-6008, or online at http://www.wiley.com/go/permissions.

Limit of Liability/Disclaimer of Warranty: While the publisher and author have used their best efforts in preparing this book, they make no representations or warranties with respect to the accuracy or completeness of the contents of this book and specifically disclaim any implied warranties of merchantability or fitness for a particular purpose. No warranty may be created or extended by sales representatives or written sales materials. The advice and strategies contained herein may not be suitable for your situation. You should consult with a professional where appropriate. Neither the publisher nor author shall be liable for any loss of profit or any other commercial damages, including but not limited to special, incidental, consequential, or other damages.

For general information on our other products and services or for technical support, please contact our Customer Care Department within the United States at (800) 762-2974, outside the United States at (317) 572-3993 or fax (317) 572-4002.

Wiley publishes in a variety of print and electronic formats and by print-on-demand. Some material included with standard print versions of this book may not be included in e-books or in print-on-demand. If this book refers to media such as a CD or DVD that is not included in the version you purchased, you may download this material at http://booksupport.wiley.com. For more information about Wiley products, visit www.wiley.com.

ISBN 978-1-119-34823-8 (ebk)

Printed in the United States of America

10 9 8 7 6 5 4 3 2 1

Foundations of Risk Management (FRM)

Elton, ChaptEr 13

© 2016 Wiley 2

Elton, Chapter 13

E R RE R R

f fm f

mX( )

( )= +

−σ

σ

E R R E R Ri F i M F( ) ( ( ) )= + −β

Where:

E R i

Rp

F

( ) ==

expected return of asset (of portfolio)

risk-freee rate of returnexpected rate of return of the markE RM( ) = eet portfolioCov

Var1β =( , )

( )

R R

Ri M

M

Equation of CML:

E R RE R R

pp fm f

m

( ) = + ( )

σσ

−×

βσ

ρ σ σσ

ρ σσi

i m

m

i m i m

m

i m i

m

R R= = =

Cov ,

2

,( , ) ,2

© 2016 Wiley 3

amEnC, ChaptEr 4

Amenc, Chapter 4

Sharpe ratio = R Rp f

p

−σ

Treynor ratio = R Rp f

p

−β

α βp p f p m fR R R R= − + −[ ( )]

TrackingError = σ (ActiveReturn − BenchmarkReturn)

IR( )

=−−

R R

s R RP B

P B

SR T

DR= −

BodiE, ChaptEr 10

© 2016 Wiley 4

Bodie, Chapter 10

E R Rp F p k p K( ) ..., ,= + +λ β λ β1 1

Required return = Risk-free rate + (Risk premium)1 + (Risk premium)2 + . . . + (Risk premium)k

Risk premiumi = Factor sensitivityi × Factor risk premiumi

Quantitative Analysis (QA)

millEr, ChaptEr 2

© 2016 Wiley 6

Miller, Chapter 2

P A or B) P(A) P(B) P(AB)

P A and B) P(A) P(B)

(

(

= + −= ×

© 2016 Wiley 7

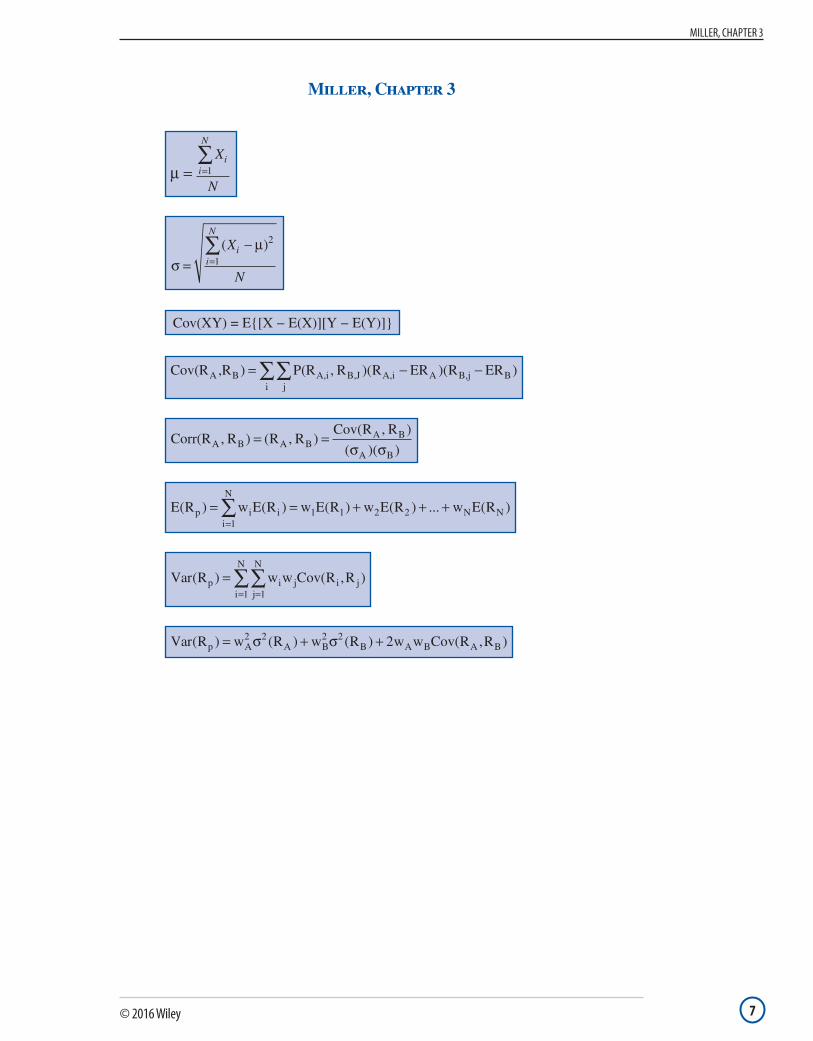

millEr, ChaptEr 3

Miller, Chapter 3

μ = X

N

ii

N

=∑

1

σµ

=−

=∑( )X

N

ii

N2

1

Cov(XY) = E{[X − E(X)][Y − E(Y)]}

Cov(R ,R ) P(R R R ER R ERA B A,i B,J A,i A B,j Bji

= − −∑∑ , )( )( )

Corr(R , R ) R RCov R , R

A B A BA B

A B

= =( , )( )

( )( )σ σ

E R w E R w E R w E R w E Rp i ii

N

N N( ) ( ) ( ) ( ) ... ( )= = + + +=∑

11 1 2 2

Var R w w Cov R Rp i j i jj

N

i

N

( ) ( , )===∑∑

11

Var R w R w R w w Cov R Rp A A B B A B A B( ) ( ) ( ) ( , )= + +2 2 2 2 2σ σ

millEr, ChaptEr 4

© 2016 Wiley 8

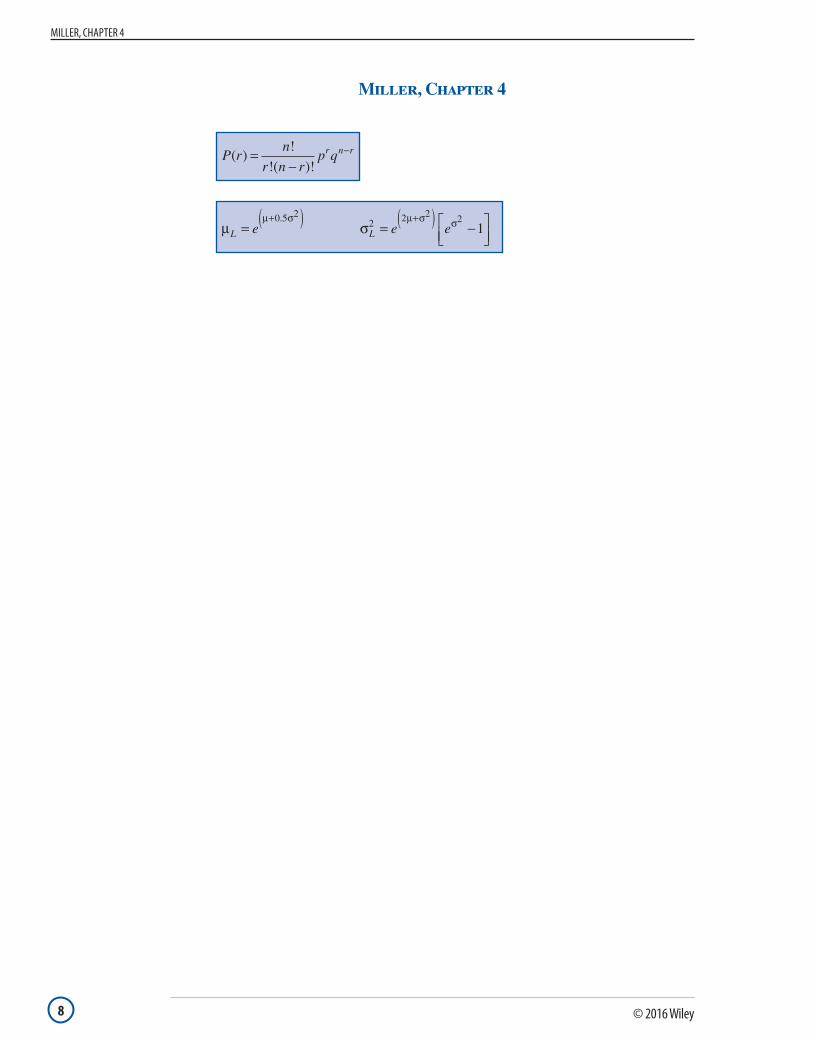

Miller, Chapter 4

P rn

r n rp qr n r( )

!

!( )!=

−−

µ σµ σ µ σ σ

L Le e e= = −

+( ) +( )0 5 22 2 2 2

1.

© 2016 Wiley 9

millEr, ChaptEr 6

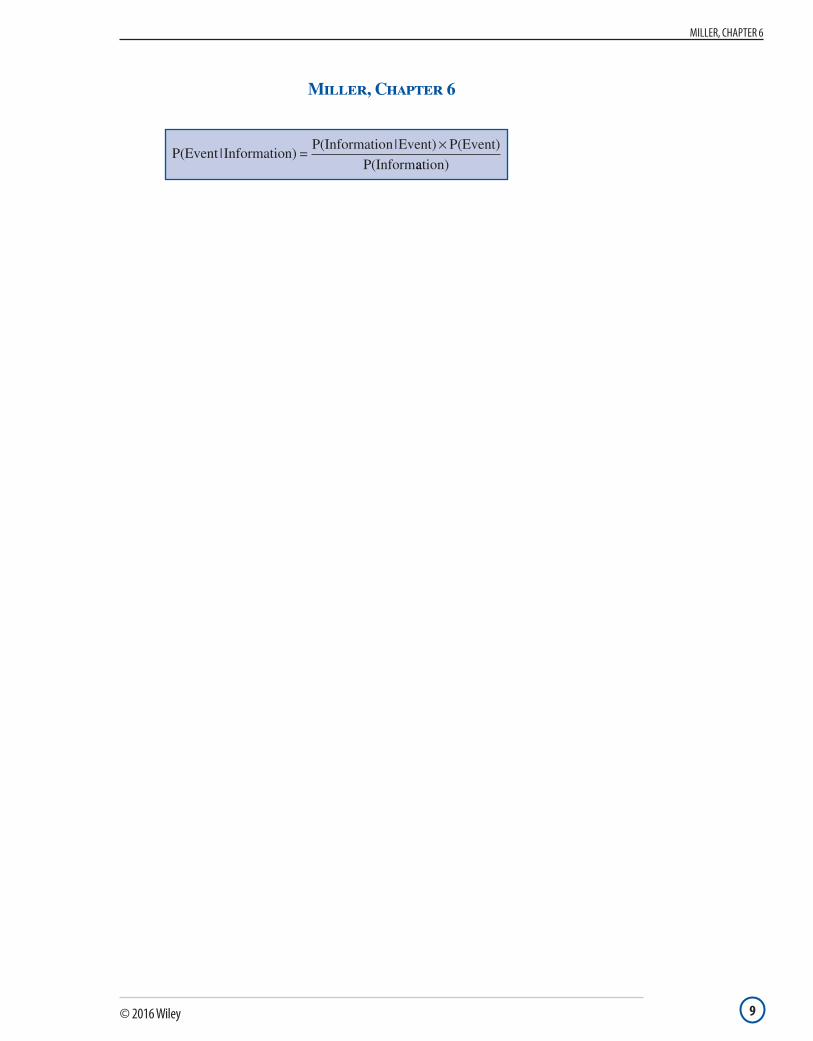

Miller, Chapter 6

P(Event |Information) =P(Information|Event) P(Event)

P(Inform

×aation)

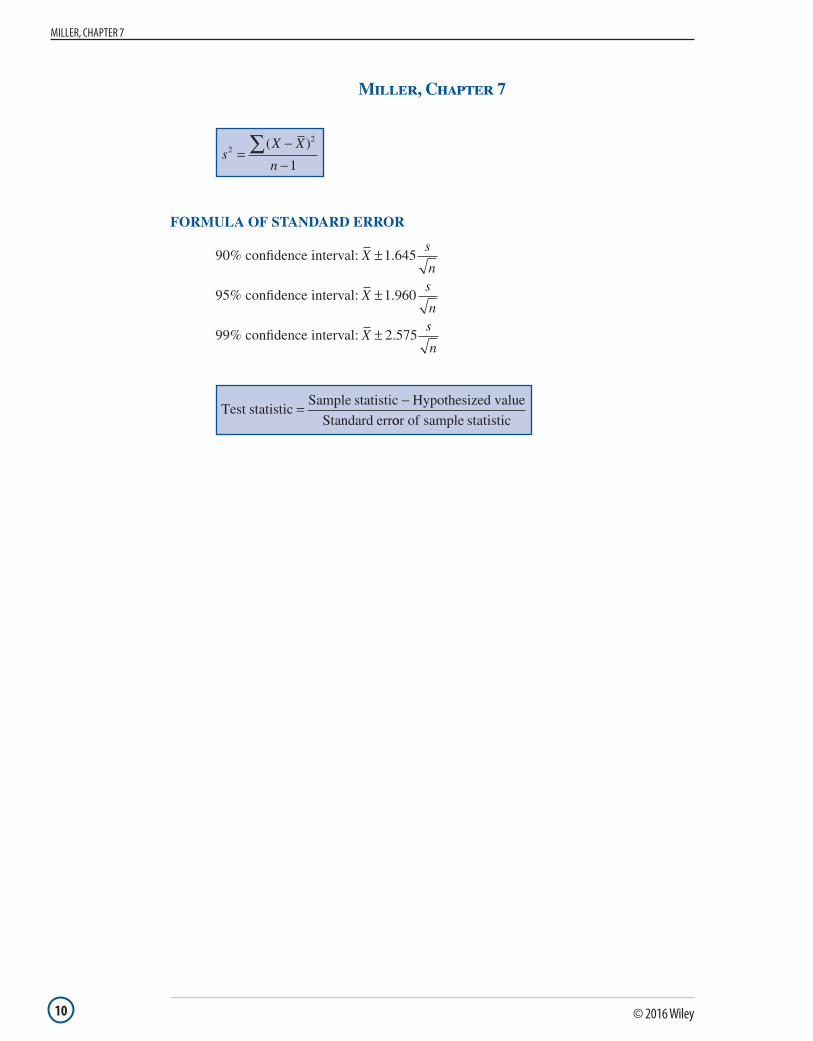

millEr, ChaptEr 7

© 2016 Wiley 10

Miller, Chapter 7

sX X

n2

2

=−

−∑( )

1

FoRMulA oF StAndARd ERRoR

90% confidence interval: Xs

n±1 645.

95% confidence interval: Xs

n±1 960.

99% confidence interval: Xs

n± 2 575.

Test statisticSample statistic Hypothesized value

Standard err= −

oor of sample statistic

© 2016 Wiley 11

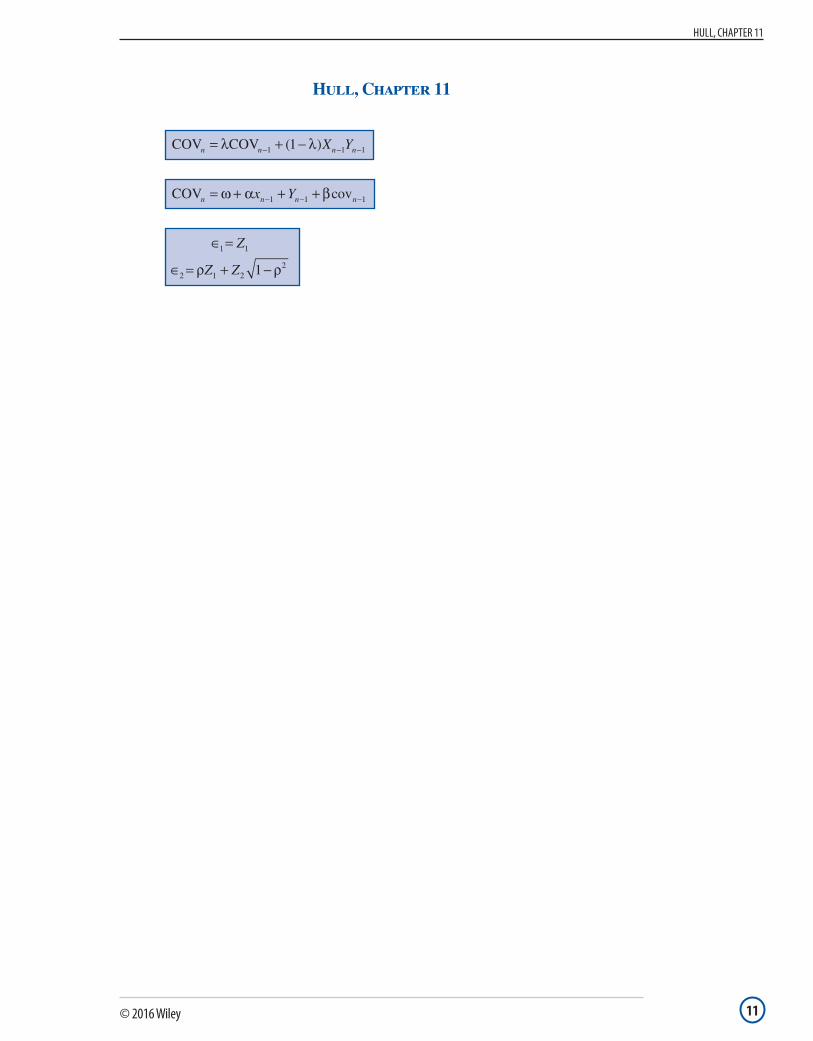

hull, ChaptEr 11

Hull, Chapter 11

COV COV 1n n n nX Y= + −− − −λ λ( )1 1 1

COV 1n n n nx Y= + + +− − −ω α β1 1cov

∈ =

∈ = + −1 1

2 1 221

Z

Z Zρ ρ

StoCk, ChaptEr 4

© 2016 Wiley 12

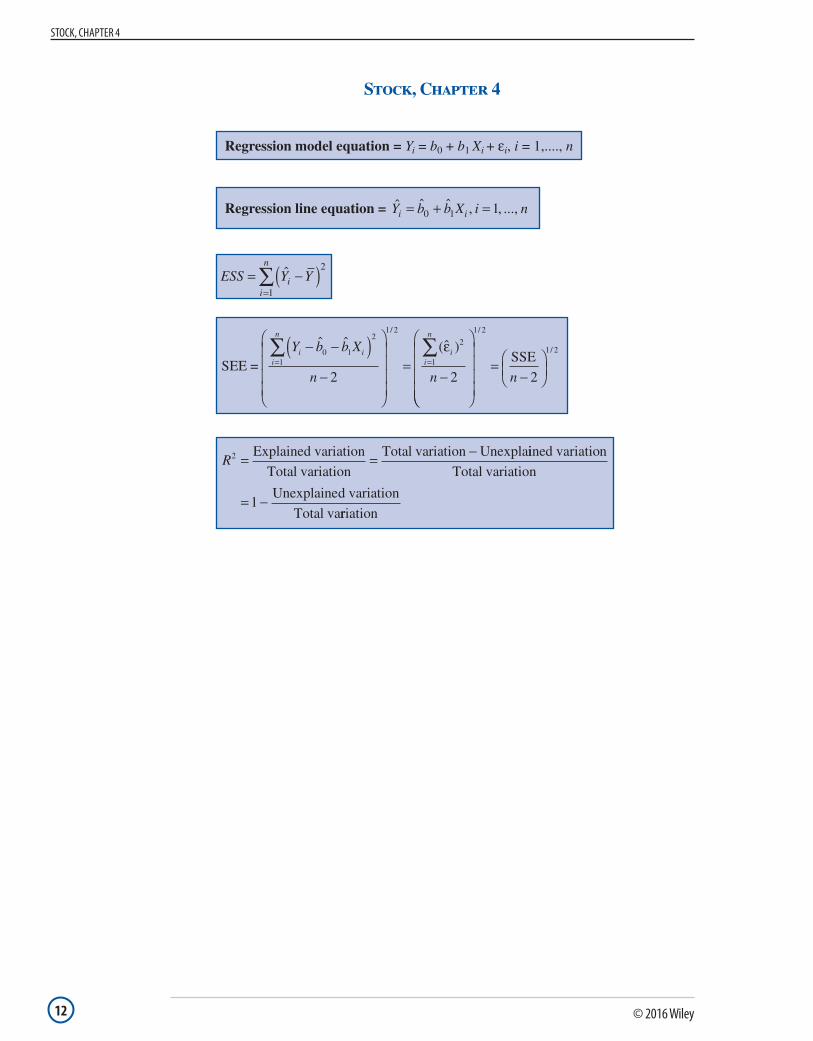

Stock, Chapter 4

Regression model equation = Yi = b0 + b1 Xi + εi, i = 1,...., n

Regression line equation = ˆ ˆ ˆ , , ...,Y b b X i ni i= + =0 1 1

ESS Y Yii

n

= −( )=∑ ˆ 2

1

SEE =Y b b X

n n

i ii

n

ii

n

− −( )−

=−

= =∑ ∑ˆ ˆ (ˆ )

/

0 1

2

1

1 2

2

1

2 2

ε

=−

1 2

1 2

2

/

/SSE

n

R2 = = −Explained variation

Total variation

Total variation Unexplaiined variation

Total variation

Unexplained variation

Total va= −1

rriation

© 2016 Wiley 13

StoCk, ChaptEr 5

Stock, Chapter 5

ˆ ( )

(

ˆb t s

t

j c bj± ×

±estimated regression coefficient critical -valuue)(coefficient standard error)

StoCk, ChaptEr 6

© 2016 Wiley 14

Stock, Chapter 6

Var Slopex x

( )( )

=−∑

σ2

2

Fk

n k +-

MSR

MSE

SS/

SSE [ ( 1)]stat

R

/= =

−

© 2016 Wiley 15

StoCk, ChaptEr 7

Stock, Chapter 7

Adjusted 2R R R= = − −− −

−2 211

11

n

n k( )

diEBold, ChaptEr 5

© 2016 Wiley 16

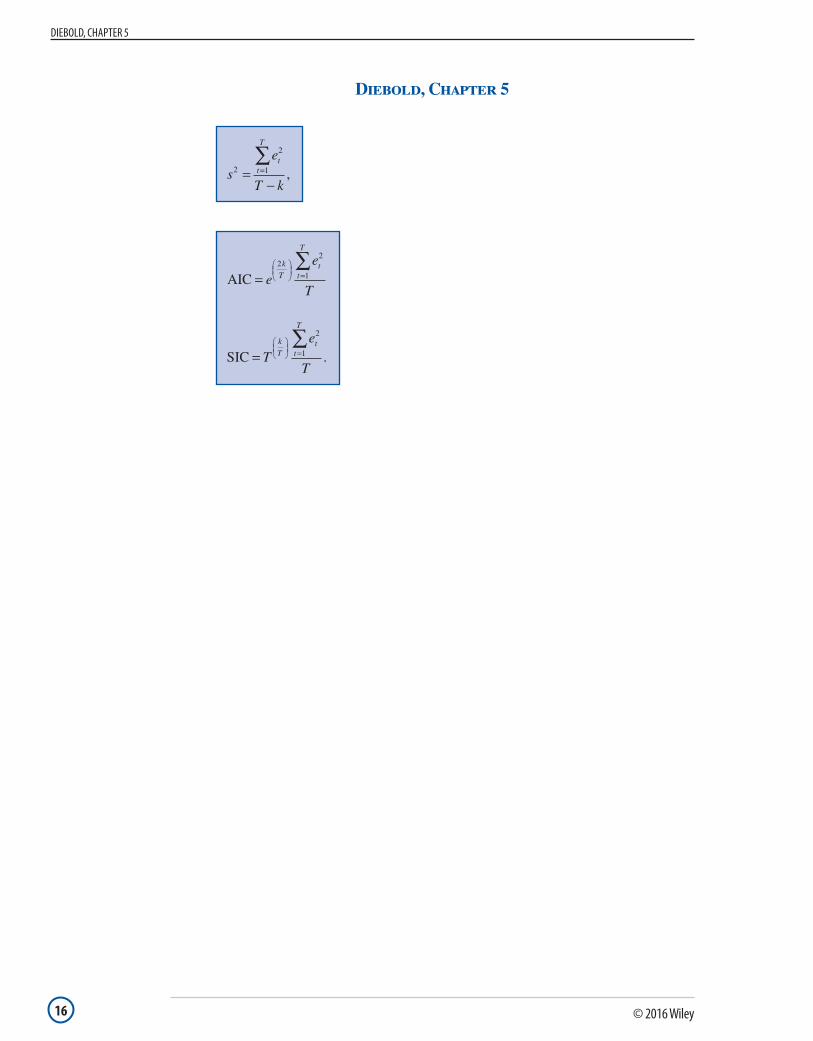

diebold, Chapter 5

se

T k

tt

T

2

2

1=−

=∑

,

AIC =

=∑

ee

T

k

Tt

t

T

22

1

SIC =

=∑

Te

T

k

Tt

t

T2

1 .

© 2016 Wiley 17

hull, ChaptEr 23

Hull, Chapter 23

σ γ α βσn L n nU21

21

2= + +− −V

σ ω α βσn n nU21

21

2= + +− −

xb

bt =−

0

11

Financial Markets and Products (FMP)

© 2016 Wiley 19

Hull, CHapter 1

Hull, Chapter 1

V T S F TT T( , ) ( , )0 0= −

F 0 T = S 1+ r0T( , ) ( )

V 0 T = St F 0 T / 1+rtT t( , ) [ ( , ) ( ) ]− −

Hull, CHapter 3

© 2016 Wiley 20

Hull, Chapter 3

MinimumVarianceHedgeRa o s

r

ti = ρσσ

# of Futures =−

×MD MD

MD

MV

MVTarget Portfolio

Futures

Portfolio

Futurres ContractYield× β

# of Futures =−

×β β

βTarget Portfolio

Futures

Portfolio

Futures

MV

MV CContract

© 2016 Wiley 21

Hull, CHapter 4

Hull, Chapter 4

PV =PMT

1 + Z

PMT

1 + Z

PMT + FV

1 + Z11

2 NN( ) ( )

...( )

+ + +2

relationship between multiperiod spot rates and forward rates:

1 1 11 1 2

2+( ) +( ) = +( )s f s0 1 0

1 1 12

2

1 3

3+( ) +( ) = +( )s f s0 2 0

∆ ∆ ∆B

BD y C y= − + 1

22( )

Convexity adjustment = Convexity estimate r 1002× ×( )∆

Hull, CHapter 5

© 2016 Wiley 22

Hull, Chapter 5

F Si

iFC/DC FC/DCFC

DC

= ×+( )+( )

1

1

F Si

iFC/BC FC/BCFC

BC

= ×+( )+( )

1

1

F S Si i Actual

i ActualFC/DC FC/DC FC/DC

FC DC

DC

− =−( ) ×

+ ×( )

360

1 360

− =−( ) ×

+ ×F S S

i i Actual

i ActuFC/BC FC/BC FC/BC

FC BC

BC

360

1 aal360( )

F S eContinuously compounded risk-free rate

0rT=

=0

r

F S e r+U T0 0= ( )

F S e r+U Y T0 0= −( )

© 2016 Wiley 23

Hull, CHapter 6

Hull, Chapter 6

( )days between dates/days in period * during the perinterest earned iiod

f TB T + Y r T FV CI 0 T

CF T

CF T Conversion

0C T

0

01( ) =

( ) + ( ) − ( )( )

( ) =

, ,

ffactor on CTD bond

Forward Rate Futures Rate T T= − 1

22

1 2σ

AI = the boxed formula

Hull, CHapter 7

© 2016 Wiley 24

Hull, Chapter 7

Swap fixed rate =1 B N

B B B B N0

− ( )( ) + ( ) + + + ( )

×0

0 0 01 2 31

( ) ...000

© 2016 Wiley 25

Hull, CHapter 11

Hull, Chapter 11

c S≤

C S≤

p K≤

p K≤

c S Ke rT− ≥ − −max 0 0( , )

C S KT= −max( , )0

p Ke rT S≥ − −max( , )0 0

C X/ 1+r S Pt0+ = +( )

C c0 0≥

P p0 0≥

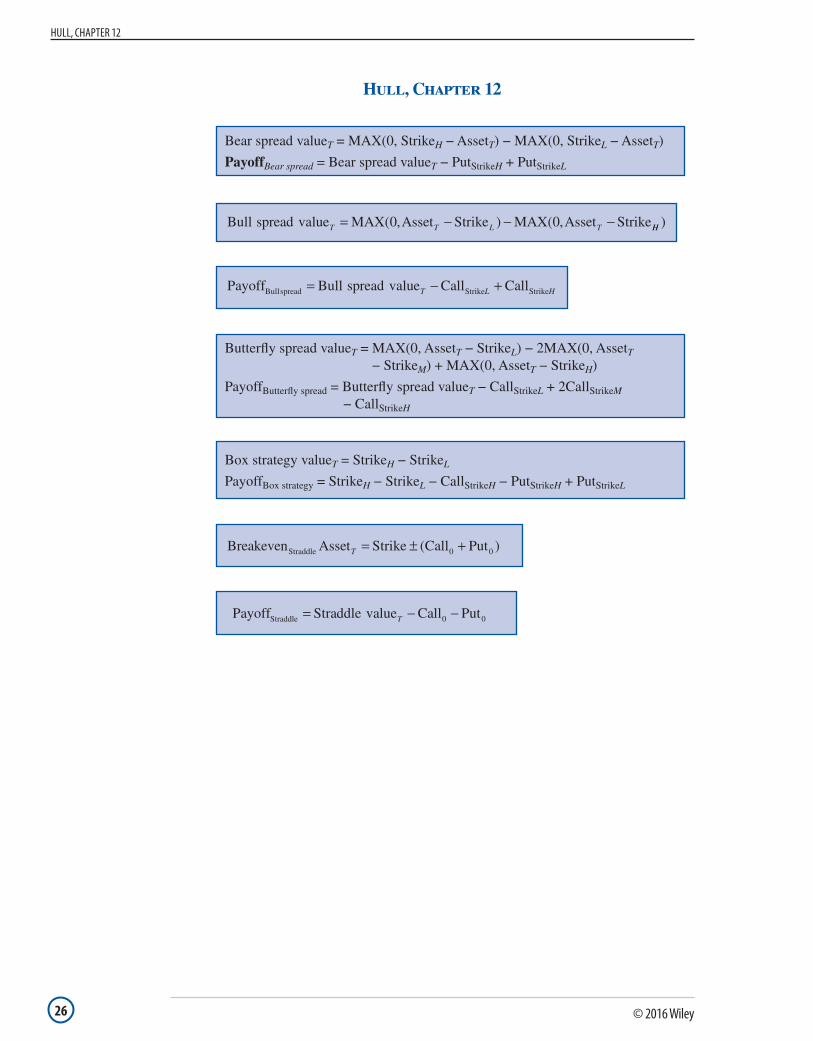

Hull, CHapter 12

© 2016 Wiley 26

Hull, Chapter 12

Bear spread valueT = MAX(0, StrikeH − AssetT) − MAX(0, StrikeL − AssetT)

PayoffBear spread = Bear spread valueT − PutStrikeH + PutStrikeL

Bull spread value MAX 0 Asset Strike MAX 0 Asset StrikeT T L T= − − −( , ) ( , HH )

Payoff Bull spread value Call CallBullspread StrikeStrike= − +T L H

Butterfly spread valueT = MAX(0, AssetT − StrikeL) − 2MAX(0, AssetT − StrikeM) + MAX(0, AssetT − StrikeH)

PayoffButterfly spread = Butterfly spread valueT − CallStrikeL + 2CallStrikeM − CallStrikeH

Box strategy valueT = StrikeH − StrikeL

PayoffBox strategy = StrikeH − StrikeL − CallStrikeH − PutStrikeH + PutStrikeL

Breakeven Asset Strike ( )Straddle 0 0T = ± +Call Put

Payoff Straddle value Call PutStraddle 0 0= − −T

© 2016 Wiley 27

MCDonalD, CHapter 6

McDonald, Chapter 6

F S eo Tr T

,( )= −

0δ

F S e r U T0 0= +( )

SaunDerS, CHapter 13

© 2016 Wiley 28

Saunders, Chapter 13

( ) ( )

(

Forward rate Spot rate

Spot rate 1

− =−

+IR IR

IRDomestic Foreign

FForeign

Domestic

Foreign

and

IR

IR

)

( )

( )

Forward

Spot

1

1=

++

Real exchange rate = S P PDC/FC DC/FC FC DC× ( )/

© 2016 Wiley 29

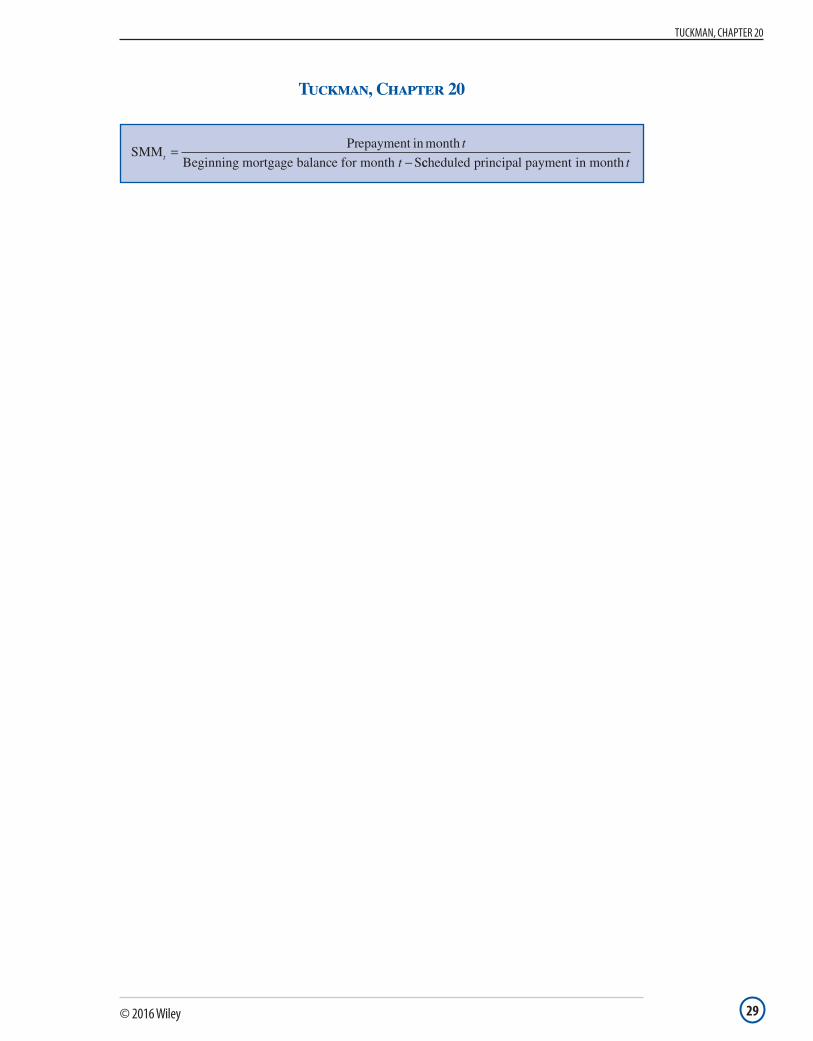

tuCkMan, CHapter 20

Tuckman, Chapter 20

SMMepayment in month

Beginning mortgage balance for month St

t

t=

−Pr

ccheduled principal payment in month t

Valuation and Risk Models (VRM)

© 2016 Wiley 31

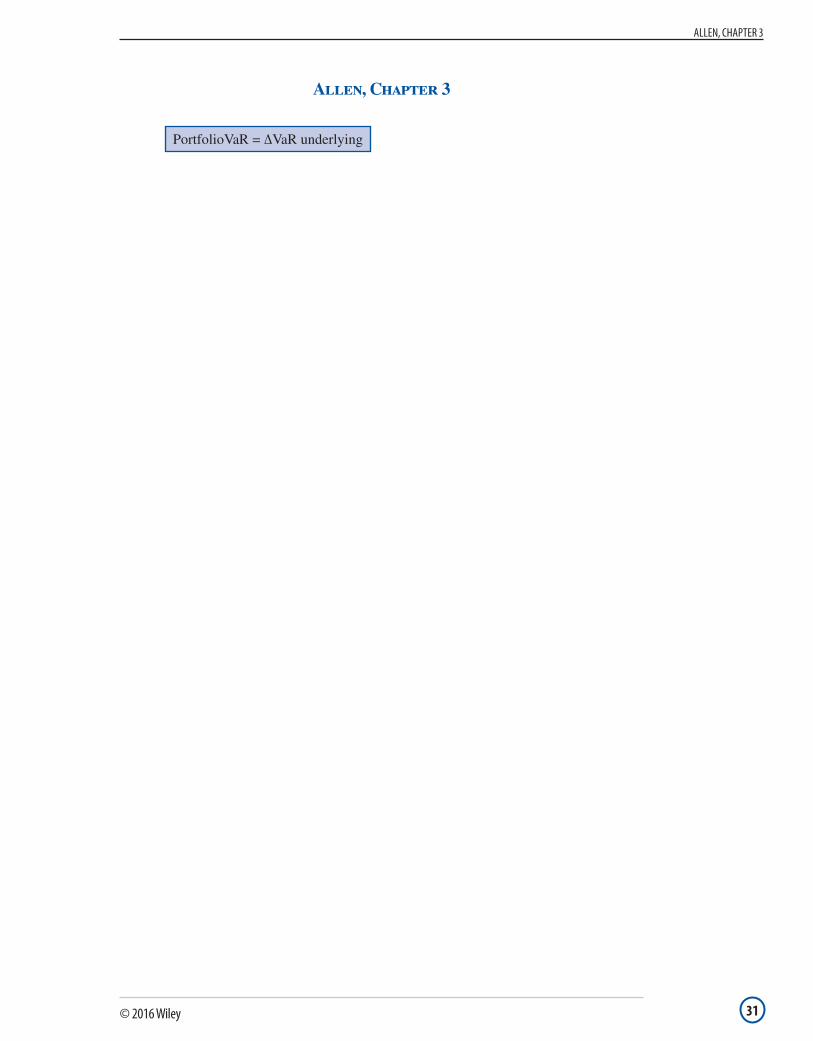

allen, CHapter 3

Allen, Chapter 3

PortfolioVaR = ΔVaR underlying

DoWD, CHapter 2

© 2016 Wiley 32

Dowd, Chapter 2

ES =− ∑1

1 α( ) * ( )greatest loss pr loss

© 2016 Wiley 33

Hull, CHapter 13

Hull, Chapter 13

n = −−

+ −

+ −c c

S S

cc c

r= + −

+

+ −π π( )

( )

1

1

π = + −−

( )

( )

1 r d

u d

Hull, CHapter 15

© 2016 Wiley 34

Hull, Chapter 15

RP P

PNi

i i 1

i 1

= , i = 1 to− −

−

R R Nic

i i to= + =ln( ),1 1

σ2

2

1

1=

−

−=∑( )R R

N

ic

ic

i

N

σ σ= 2

c = S0N(d1) − Ke−rT N(d2)

and

p = Ke−rT N(−d2) − S0N(−d1)

where

dS K r T

T

dS K r T

Td T

10

2

20

2

1

2

2

=+ +

=+ −

= −

ln( / ) ( / )

ln( / ) ( / )

σσ

σσ

σ

© 2016 Wiley 35

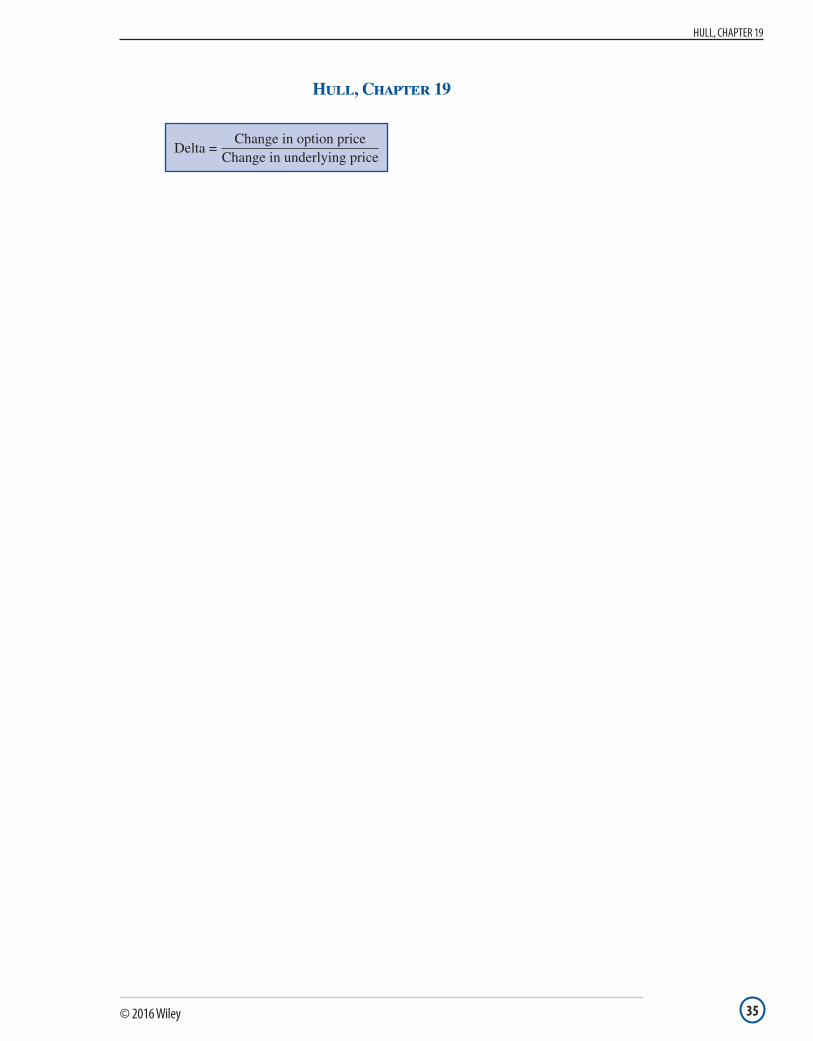

Hull, CHapter 19

Hull, Chapter 19

Delta =Change in option price

Change in underlying price

tuCkMan, CHapter 1

© 2016 Wiley 36

Tuckman, Chapter 1

PV FVDays

YearDR= × − ×

1

DRYear

Days

FV PV

FV=

× −

PVFull = PVFull + AI

AI = t / T × PMT

© 2016 Wiley 37

tuCkMan, CHapter 2

Tuckman, Chapter 2

d tr t t

( )(

( ))

=+

1

12

2

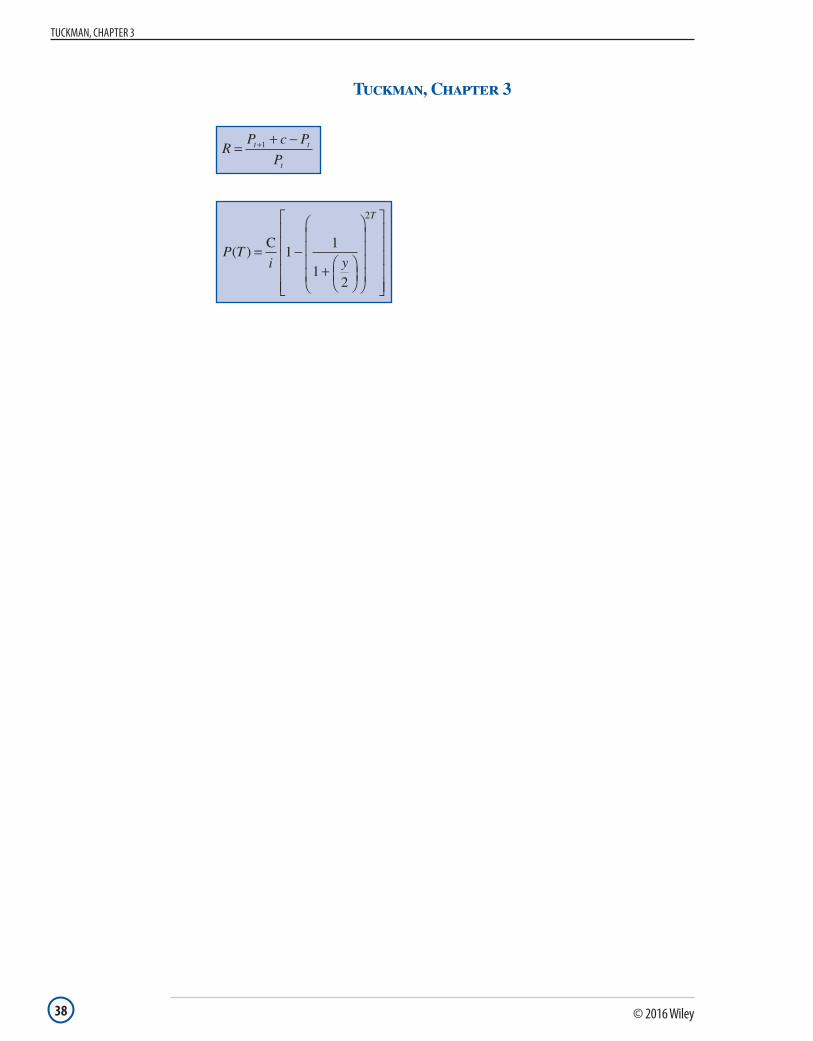

tuCkMan, CHapter 3

© 2016 Wiley 38

Tuckman, Chapter 3

RP c P

Pt t

t

=+ −+1

P Ti y

T

( ) = −+

C1

1

12

2

© 2016 Wiley 39

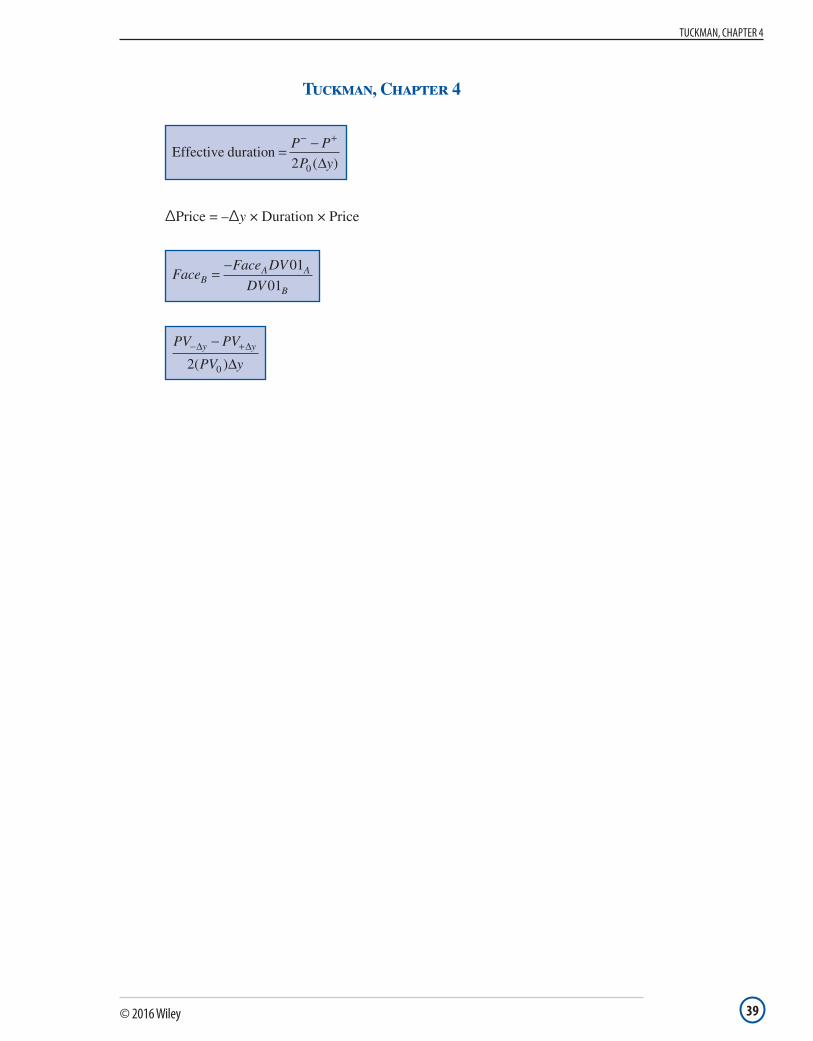

tuCkMan, CHapter 4

Tuckman, Chapter 4

Effective duration = −− +P P

P y2 0 ( )∆

ΔPrice = –Δy × Duration × Price

FaceFace DV

DVBA A

B

=− 01

01

PV PV

PV yy y− +−∆ ∆

∆2 0( )

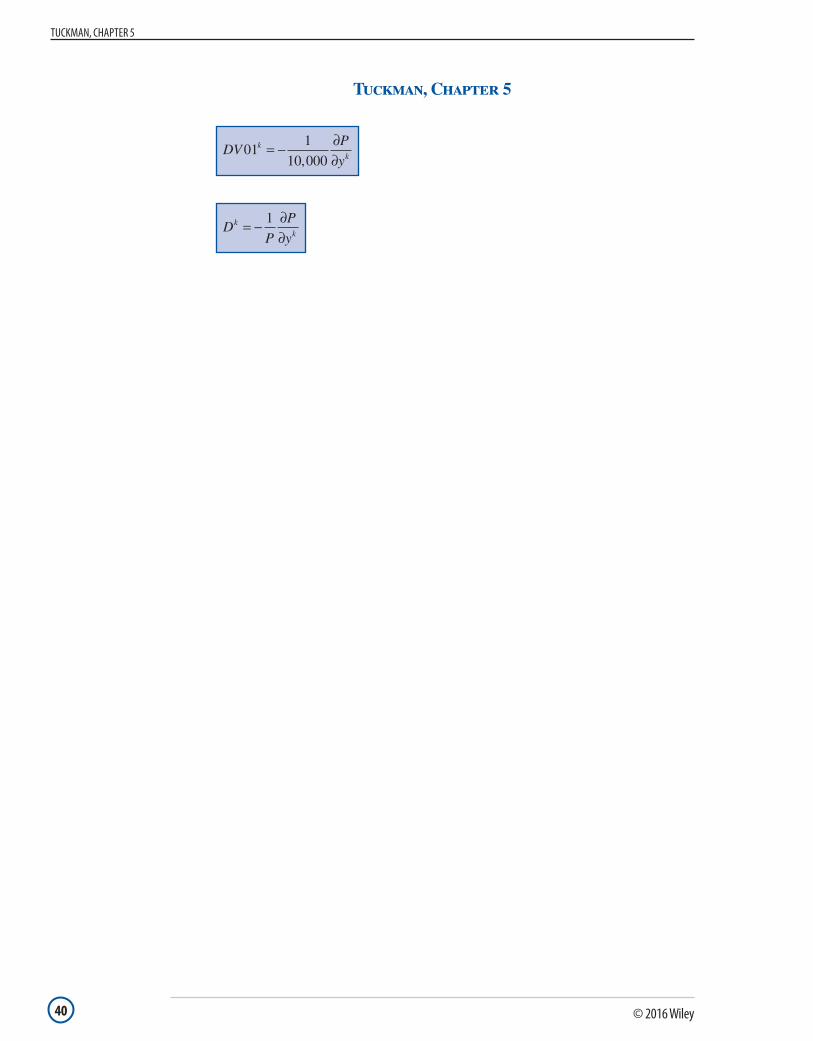

tuCkMan, CHapter 5

© 2016 Wiley 40

Tuckman, Chapter 5

DVP

yk

k01

1

10 000= − ∂

∂,

DP

P

yk

k= − ∂

∂1

© 2016 Wiley 41

SCHroeCk, CHapter 5

Schroeck, Chapter 5

UL EA PD LRLR PD= ⋅ ⋅ + ⋅σ σ2 2 2

UL UL ULP i j ij i jj

n

i

n

===

∑∑ ω ω ρ11

WILEY END USER LICENSEAGREEMENT

Go to www.wiley.com/go/eula to access Wiley’s ebookEULA.