20160815 centrelink age pension asset test changes · financial group ltd abn 76 006 637 225 | afsl...

TRANSCRIPT

GAVIN MARTIN Financial Advisor | Cornerstone Wealth

2016 Centrelink Age Pension Asset Test Changes 1st Jan 2017

Gavin Martin Financial Adviser Cornerstone Wealth

Phil Watson Digital Marketing Coordinator Christian Super

DisclaimerGavin Martin and Cornerstone Wealth are Authorised Representatives of Lonsdale Financial Group Ltd ABN 76 006 637 225 | AFSL 246934 The content of this presentation is general advice only and does not take into account your financial circumstances, needs and objectives. Before making any decision based on this presentation, you should assess your own circumstances or seek advice from a financial planner and seek tax advice from a registered tax agent. Information is current at the date of issue and may change. © Cornerstone Wealth 2016. All rights reserved. No part of this presentation may be reproduced in any form without the prior permission of the copyright owners.

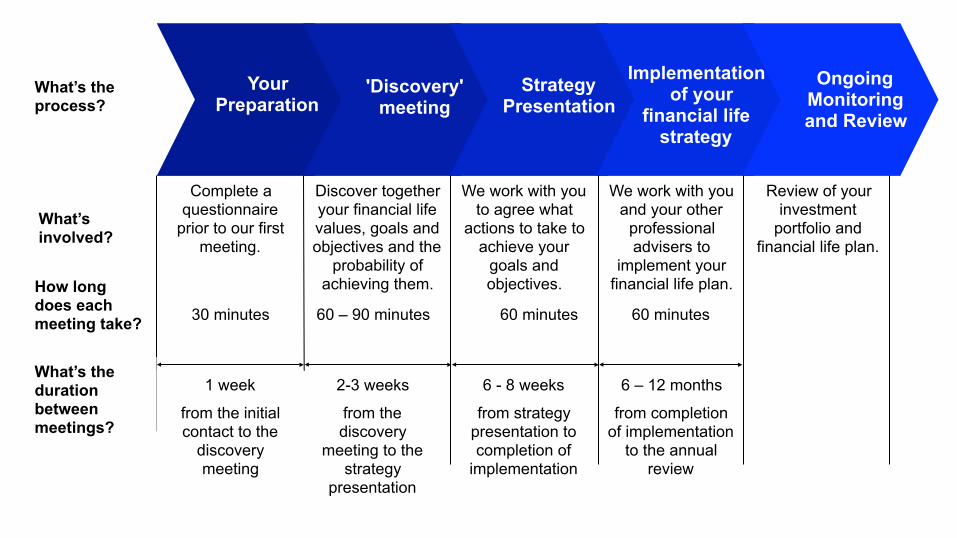

Your Preparation

'Discovery' meeting

Strategy Presentation

Implementation of your

financial life strategy

Ongoing Monitoring and Review

Complete a questionnaire

prior to our first meeting.

Discover together your financial life values, goals and objectives and the

probability of achieving them.

We work with you to agree what

actions to take to achieve your

goals and objectives.

We work with you and your other

professional advisers to

implement your financial life plan.

Review of your investment

portfolio and financial life plan.

6 - 8 weeks

from strategy presentation to completion of

implementation

6 – 12 months

from completion of implementation

to the annual review

How long does each meeting take?

What’s involved?

What’s the process?

30 minutes 60 – 90 minutes 60 minutes 60 minutes

What’s the duration between meetings?

1 week

from the initial contact to the

discovery meeting

2-3 weeks

from the discovery

meeting to the strategy

presentation

Retirement Planning

25th July 2016

1. When 2. How much 3. Phases

Retirement Planning WebinarsHow to

Transition to Retirement

17th August 2015

1. Salary Sacrifice 2. Pensions 3. Tax free income

Capital Gains and Wealth

Transfer

7th September 2015

1. Tax on asset sales

2. Maximise Estate

Centrelink changes 1st

January 2017

15th August 2016

1. The changes 2. Effects on you 3. What to do

www.cornerstonewealth.com.au/retire2016

2015 Recording for now

www.cornerstonewealth.com.au/retire2016

2016 Centrelink Age Pension Asset

Test Changes1st January 2017

2015 Applying for the

Centrelink Age Pension

2015 Centrelink Income and

Asset Strategies

Work Bonus

www.cornerstonewealth.com.au/centrelink2016

Questions?If you have questions during the webinar...

Please use the Chat/Question section on the panel on the right hand side of your screen. I’ll answer your question where it relates to the current topic or defer it to the end of the presentation if that works better.

What is your Age poll?

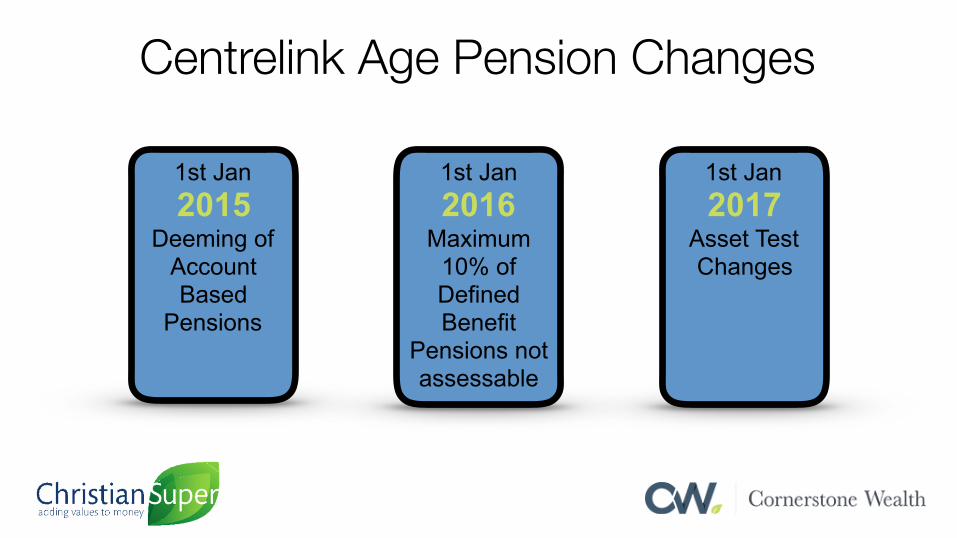

Centrelink Age Pension Changes

1st Jan 2015

Deeming of Account Based

Pensions

1st Jan 2016

Maximum 10% of Defined Benefit

Pensions not assessable

1st Jan 2017

Asset Test Changes

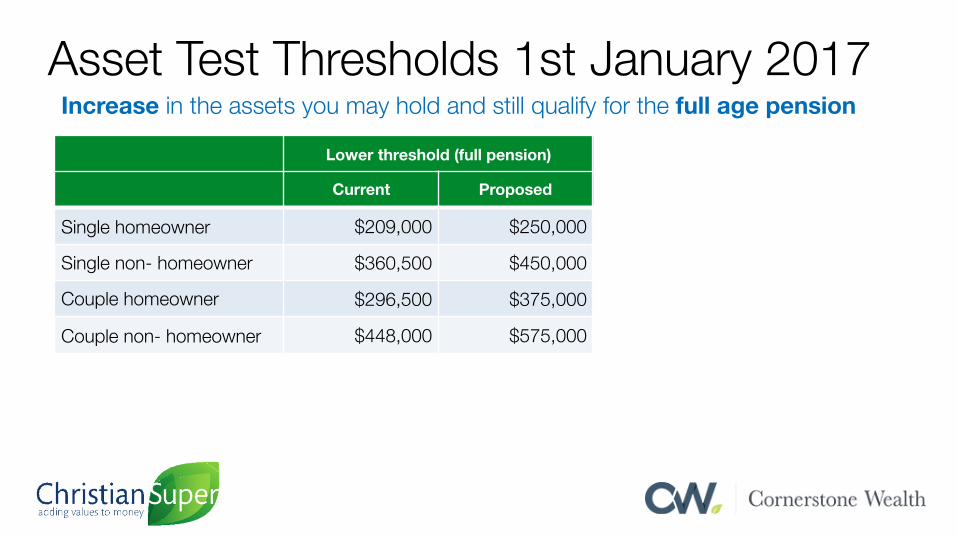

Asset Test Thresholds 1st January 2017Lower threshold (full pension) Cut-off threshold (no pension payable)

Current Proposed Current Proposed

Single homeowner $209,000 $250,000 $791,750 $547,000

Single non- homeowner $360,500 $450,000 $943,250 $747,000

Couple homeowner $296,500 $375,000 $1,175,000 $823,000

Couple non- homeowner $448,000 $575,000 $1,326,500 $1,023,000

Increase in the assets you may hold and still qualify for the full age pension

Taper Rate Changes 1st January 2017Lower threshold (full pension) Cut-off threshold (no pension payable)

Current Proposed Current Proposed

Single homeowner $209,000 $250,000 $791,750 $547,000

Single non- homeowner $360,500 $450,000 $943,250 $747,000

Couple homeowner $296,500 $375,000 $1,175,000 $823,000

Couple non- homeowner $448,000 $575,000 $1,326,500 $1,023,000

Increase in the taper rate means the full age pension reduces faster

You lose $1.50 in age pension for every $1,000 in assets you hold above these current limits. From 1 January 2017 you will lose $3.00 in your pension for every $1,000 you have above the new limits.

Pension $1.50 / fnPension $3.00 / fn

Taper Rate Changes 1st January 2017Lower threshold (full pension) Cut-off threshold (no pension payable)

Current Proposed Current Proposed

Single homeowner $209,000 $250,000 $791,750 $547,000

Single non- homeowner $360,500 $450,000 $943,250 $747,000

Couple homeowner $296,500 $375,000 $1,175,000 $823,000

Couple non- homeowner $448,000 $575,000 $1,326,500 $1,023,000

Increase in the taper rate means the full age pension reduces faster

You lose $1.50 in age pension for every $1,000 in assets you hold above these current limits. From 1 January 2017 you will lose $3.00 in your pension for every $1,000 you have above the new limits.

Age Pension - Taper rate how does it workPensions reduce at double the rate

House $600,000

Ralph 68 years Single

Cash $27,000 Christian Pension

$400,000

Shares $100,000

Not Asset Tested

Car & Contents $20,000Christian Pension $400,000Cash $27,000Shares $100,000Total Assessable assets $547,000Lower asset threshold $209,000Assets over the threshold $338,000Taper rate $1.50 per $1,000 $507.00Maximum pension $873.90Current fortnightly Pension $366.90

$250,000 Proposed threshold$297,000

$891 Taper rate $3 per $1,000$873.90 Maximum pension

Nil Proposed Pension

$9,539 p.a. lost

Car & Contents $20,000

Age Pension - Taper rate how does it workPensions reduce at double the rate

House $800,000

Cash $20,000 Christian Pension

$600,000

Shares $100,000

Not Asset Tested

Car & contents $20,000Christian Pensions $600,000Cash $20,000Shares $100,000Total Assessable assets $740,000

Lower asset threshold $296,500Assets over the threshold $443,500Taper rate $1.50 per $1,000 $665.25Maximum pension $1,317.40Current fortnightly Pension $652.15

$375,000 Proposed threshold$365,000$1,095.00 Taper rate $3 per $1,000$1,317.40 Maximum pension

$222.40 Proposed Pension

$11,174 p.a. lost

Sally & Sam 68 & 72 years Married

Car & Contents $20,000

Impact - homeowner couples

*Based on projected pension rates at 1 January 2017.

Impact - homeowner single

*Based on projected pension rates at 1 January 2017.

What can you do?Consider your options

• Reduce spending • Increase withdrawals from income streams

Increased withdrawals - couple homeowners

What can you do?Consider your options

• Reduce spending • Increase withdrawals from income streams• Employment income - work bonus $6,500 p.a. • Asset Test reduction Strategies

Keith The economics behind divesting

yourself of cash assets (i.e.

spend, give away within the

limits etc) to meet the lower

threshold

• For every $100,000 over the lower Assets Test threshold the Age Pension is currently reduced by $3,900 p.a.($100,000/$1,000 x 1.5 x 26)

• Doubling the taper rate will also double the reduction to$7,800 p.a. or 7.80%.

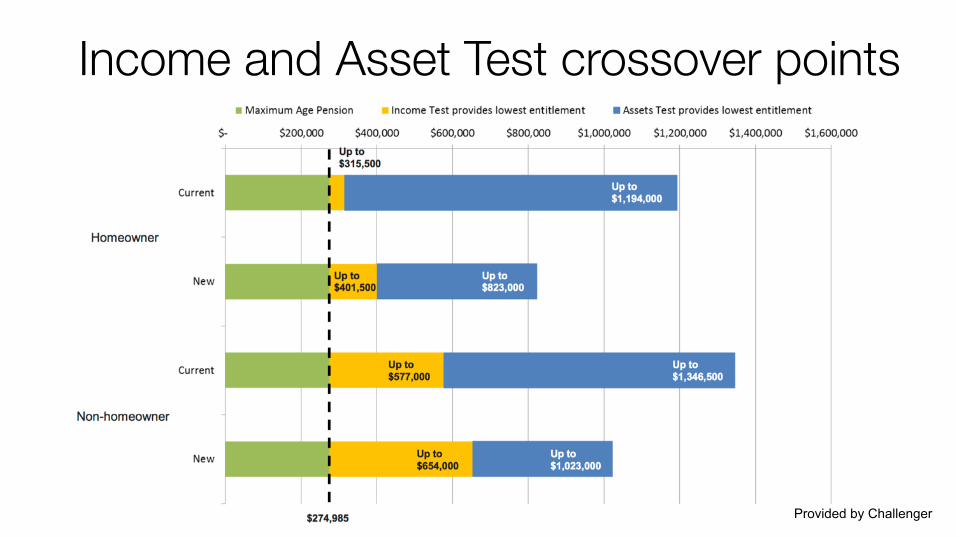

Income and Asset Test crossover points

Provided by Challenger

Asset Test Reduction StrategiesBe sure to weigh the pros of cons of your options

• Update your assets listed with Centrelink (e.g. cars) • Spend money (house improvements, holidays) • Gift money ($10,000 / year or $30,000 over 5 years) • Super for spouse less than Age Pension age • Funeral bond / prepaid funeral expenses • Annuity with < 100% Residual Capital Value

What is an Annuity?There are various types and conditions

• Source of income for a defined period • Regular income not subject to market movements. • Can complement both the Age Pension and other investments

like an account-based pension. • Can have some social security benefits • Two type of annuities:

• Term annuities • Lifetime annuities

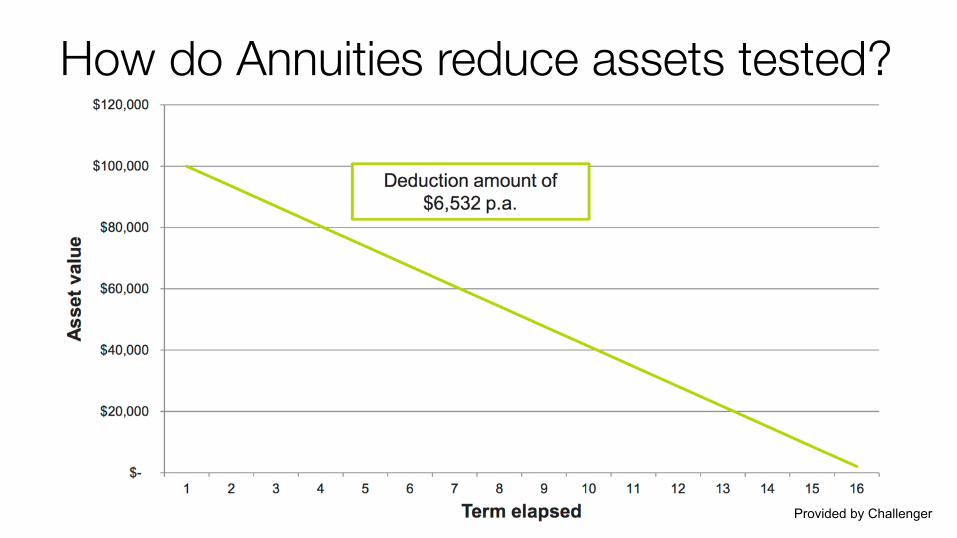

How do Annuities reduce assets tested?

Provided by Challenger

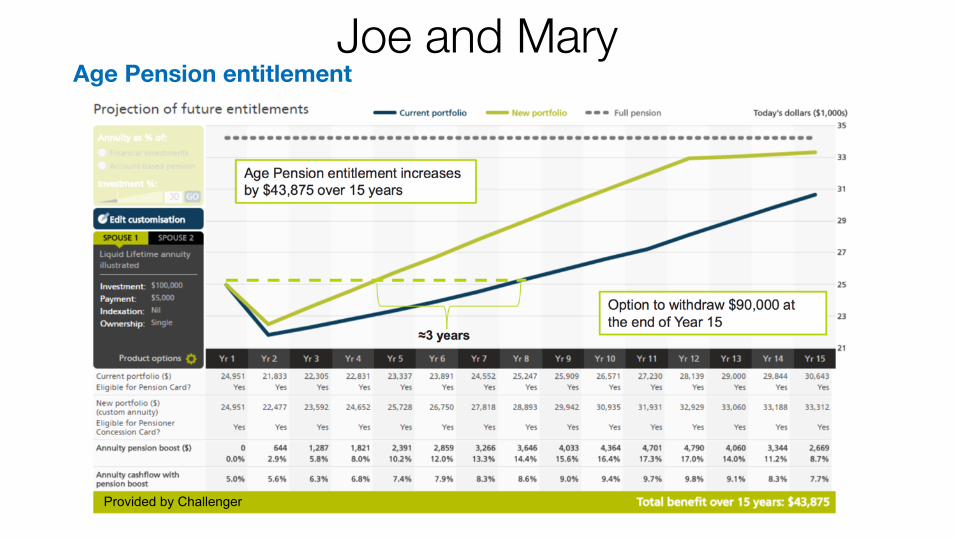

Joe and MaryBoosting the age pension

• Tim (aged 70) and Sarah (aged 65) are a couple and own their home • They have $250,000 each in account-based pensions (commenced in

July 2015) drawing the minimum payment • Their investor risk profile is 50% defensive and 50% growth • They have $20,000 in personal assets and $10,000 in cash • They are entitled to a combined Age Pension of $24,951 p.a. (20th

March 2016 rate) under the Assets Test

Joe and MaryAge Pension entitlement

Provided by Challenger

Joe and MaryAge Pension entitlement

Provided by Challenger

Annuity considerationsBoosting the age pension

• Limitation of what you can take out as a lump sum • Locking in a fixed level of return • Over the long term, an annuity might pay less than a market linked

investment • Increase in interest rates can reduce the withdrawal value

Further ResourcesChristian Super

• Help Desk 1300 360 907 • www.christiansuper.com.au

Cornerstone Wealth • Webinars

• http://cornerstonewealth.com.au/centrelink2016 • http://cornerstonewealth.com.au/retire2016

• Personal Financial Advice • Lodge an enquiry via www.cornerstonewealth.com.au and I will contact you • Call 1300 275 428 (1300 ASK GAV) to book an initial consultation