2017 new home buyer's guide

TRANSCRIPT

DOCUMENTATION

DOWN PAYMENT

CREDITSCORE

INCOMEGDS

TDS&

NEW

HO

ME

BU

YER’

S G

UID

E

Meet Ted. He’s thinking of getting his own place soon, but has no clue about the mortgage process. All he does know is that he wants to get the best loan possible when the time comes!

NEW

HO

ME

BU

YER’

S G

UID

E

ASSET Veri�cationBank statementsInvestmentsRSPs

DEBT Veri�cationCredit card and loan statementsMortgage Statement

PROPERTY Veri�cationPurchase AgreementMLS Listing

DOCUMENTATION

INCOME Veri�cationPay stubsT4’sAny other form of income such as child support, alimony, bonuses, overtime, etc.Notice of Assessments or Tax Returns

NEW

HO

ME

BU

YER’

S G

UID

E

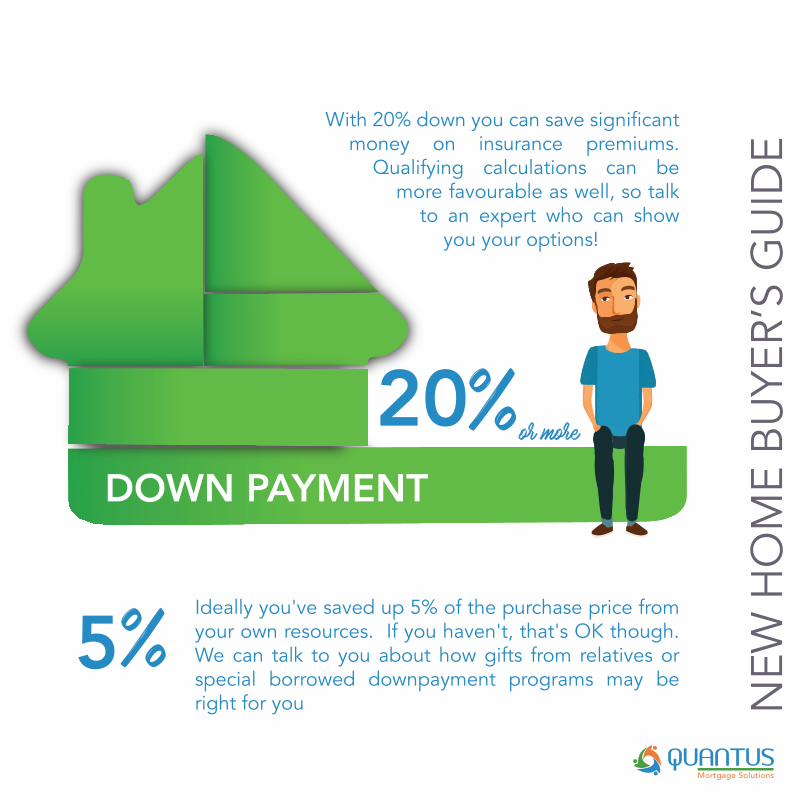

20DOWN PAYMENT

%

With 20% down you can save signi�cant money on insurance premiums.

Qualifying calculations can be more favourable as well, so talk

to an expert who can show you your options!

5% Ideally you've saved up 5% of the purchase price from your own resources. If you haven't, that's OK though. We can talk to you about how gifts from relatives or special borrowed downpayment programs may be right for you

or more

NEW

HO

ME

BU

YER’

S G

UID

E 2yearsThe ideal mortgage borrower has had the same job for over

INCOMEYes! I’ve been at my job for 2 and a half years!

*Less than 2 years? That’s ok; we have a mortgage program for you.

NEW

HO

ME

BU

YER’

S G

UID

E

SCORE

EXCELLENT

VERY GOOD

GOOD

FAIR

POOR

740+

680 - 740

620 - 680

580 - 620

>580

CREDITSCORE

Do you have a low score? Not to worry! A mortgage professional can provide you tips on how to improve your score.

GDS

TDS NEW

HO

ME

BU

YER’

S G

UID

E

Household Expenses / IncomeGROSS DEBT SERVICE

Total Expenses / IncomeTOTAL DEBT SERVICE < 32%

< 40%Income

Housing Expenses + Credit card interest + Car payments + Loan expenses

Income

Mortgage payments + Property taxes +Heating costs + Condo Fees (if applicable)

&