20170404 - strategic outlook event (kelowna) · • since early 2000’s • us growth -...

TRANSCRIPT

Our Speakers

Rob Edel Chief Investment Officer

John Nicola Chairman & CEO

Our Speakers

Rob Edel Chief Investment Officer

Mark Therriault Chairman & CEO Mark Therriault Financial Advisor

Who We Are Founded in 1994

$4.8 billion in AUM

Vancouver, Toronto, Kelowna, Richmond

Budgeting Cash Flow and Compensation

Estate And Succession

Planning Legal Coordination And

Document Retention

Coordination of Tax Planning

Philanthropic Giving And

Management

Asset Allocation And Investment Management

Insurance Placement And Management

Coordination &

Management

Our Focus: Total Integration of Financial & Wealth Management Strategies

2017 Market Outlook

Rob Edel Chief Investment Officer

Our Agenda

2016 in Review Investment Strategies

Dr. Trump

Treatment Options

Economic Diagnosis

Make the Economy Great Again

2016 in Review S&P 500

Trump Bump

Election Uncertainty Search For

Yield Recession

Fears

Brexit Trump Elected

2016 in Review U.S. 10 Year Treasury Bond Yields

Trump Bump

Election Uncertainty

Search For Yield

Recession Fears

Brexit Trump Elected

U.S. GDP Purchasing Manager Index

2016 in Review U.S. Economy

New Jobs NFIB Small Business Optimism

WSJ – July 30, 2016

2016 in Review U.S. GDP

Symptom: • Why isn’t the economy great?

4.1% 3.8% 2.7% 2.1%

Economic Diagnosis Why the Economy isn’t “Great”

Economic Diagnosis Doctor Robert Gordon – Productivity Slowdown

WSJ – Aug 10, 2016

Dr. Robert Gordon Productivity Slowdown • Supply-side secular stagnation • Productivity gains from IT over • Norm is lower productivity

“We wanted flying cars, but instead we got 140 characters.” - Peter Thiel

Economic Diagnosis Doctor Larry Summers – Secular Stagnation

Dr. Larry Summers Secular Stagnation

• Not enough demand • Leads to lower investment • Lack of demand creates lack of supply • Need to borrow more – fiscal stimulus

Business Insider – Aug 17, 2106

Economic Diagnosis Doctor’s Reinhart & Rogoff – De-leveraging

Dr. Carmen Reinhart Dr. Kenneth Rogoff Deleveraging

• Too much debt • Deleveraging takes 8 years • Recoveries are weaker

https://www.newyorkfed.org/microeconomics/hhdc.html

Recession

• Deleveraging made recession worse • But GDP Growth was slowing

well before deleveraging began • Debt increased because GDP slowed

WSJ – Oct 6, 2016

Economic Diagnosis Doctor Mervyn King – Savings Glut

Dr. Mervyn King Savings Glut

• Unsustainable trade imbalance • Since early 2000’s

• US growth - consumption • Asia/Europe growth - Exports • US consumer add debt • China buy US Treasury’s

• Lower US interest rates • Lower US inflation WSJ – Nov 16, 2016

Treatment Options Dr. Trump or Mr. Burns

POSSIBLE OUTCOMES OF A TRUMP PRESIDENCY AT VARIOUS PLACES ON THE RISK CURVE

NUCLEAR WAR

BRINGING EMBARASMENT TO AMERICA ON THE WORLD

STAGE

GOOD DEALS

SOME COOL INFRASTRUCTURE

STUFF

MEXICO PAYING FOR THE WALL

Treatment Options Dr. Trump or Mr. Burns

Business Insider

Probability

Return + -

TRUMP IMPEACHED DUE TO RUSSIAN COLLUSION

TRADE WAR WITH CHINA

This presentation is not an endorsement of President Trump or an endorsement of any of President Trump’s policies. NWM has had no contact with any Russian foreign nationals in the past, nor do we

intend to in the future. Any statements to the contrary are fake news.

Treatment Options Dr. Trump or Mr. Burns – Five Pillars

TRUMP UNIVERSITY FACULTY OF ECONOMICS

JP Morgan Eye on the Market – Michael Cembalest Jan 23, 2017

George Mason University • Regulations across 22 industries reduce GDP 0.8%/yr. • Economy would be 25% larger if no regulations since 1980

World Bank - Ease of Doing Business Report • U.S. 51/190 for starting a business • 2012 – 40 days to get a construction permit • 2016 – 81 days

1950 – 5% of workers required a license or certificate 2016 – 30%

Treatment Options Dr. Trump or Mr. Burns – Deregulation

WSJ – Nov 28, 2016

U.S. companies hold $2 trillion offshore

Treatment Options Dr. Trump or Mr. Burns – Tax Reform

JP Morgan Eye On The Market Michael Cembalest Feb 8, 2017

Bloomberg – Jan 11, 2017

Average U.S. commuter wastes over 40 hours/yr.

waiting in traffic

$1 trillion spent over 10 years Moody’s Analytics:

Every $1= $1.21 in GDP

Treatment Options Dr. Trump or Mr. Burns – Infrastructure Spending

WSJ Mar 10, 2017

$1 trillion = +5% to Debt $4.6 trillion = ~ +25% to Debt

The Daily Shot – Aug 24, 2016

The 1%

Top 2-5%

Top 1%

Treatment Options Dr. Trump or Mr. Burns – Trade

$347 Billion

$69 Billion

$65 Billion

$63 Billion

• U.S. Trade Deficit ~ $500 billion • Not just Tariffs - VAT • U.S. Exporter pay VAT • Foreign Exporters get a VAT Credit

Treatment Options Dr. Trump or Mr. Burns – Trade

Oxford University • Nearly 50% of U.S. Jobs will be automated in 20 years

McKinsey &Co. • 45% of today’s activities can be automated • But less then 5% can be full automated

Deloitte • Automation could lift global productivity 0.8% - 1.4%/yr

over next 50 years

Pew Research - 2020-2040 • Working population +0.3% • 500,000 less +0.1% • 1,000,000 less -0.1%

Treatment Options Dr. Trump or Mr. Burns – Immigration

Pew Research • 8 million undocumented workers • 5% of civilian workforce • 92% between 18-64 years old • 70% in Agriculture and Construction

Treatment Options Make the Economy Great Again - Education

Math U.S. #38 of 71

Canada #9 of 71

Reading U.S. #39 of 71

Canada #3 of 71

Science U.S. #24 of 71

Canada #7 of 71

WSJ – Dec 8, 2016

President’s Council of Advisors on Science and Technology U.S. will need ~1 million more STEM professionals over next decade than will currently produce. Need to increase STEM degrees by 34%.

Treatment Options Make the Economy Great Again - Healthcare

The 2016 Long-Term Budget Outlook

Treatment Options Make the Economy Great Again – Entitlement Spending

WSJ – Aug 21, 2016

Low/Negative Interest Rates • Lowers consumer confidence – communicate fear • Hurts savers • Increases wealth gap – low rates helps financial assets

Treatment Options Make the Economy Great Again – Monetary Policy

Monetary Policy • Need to normalize interest rates • If only U.S. then US$ will increase

Trade • Need to balance trade flows • China, but also Germany

Treatment Options Make the Economy Great Again – Oil

WSJ – Apr 6, 2017

Treatment Options Make the Economy Great Again – Monetary Policy

The Daily Shot - Mar 30, 2017

Treatment Options Make the Economy Great Again – Monetary Policy

The Daily Shot – Apr 6, 2017

Treatment Options Make the Economy Great Again – Monetary Policy

http://www.canadianbusiness.com/economy/canadas-50-most-important-economic-charts-for-2016/

Treatment Options Make the Economy Great Again – Monetary Policy

http://www.canadianbusiness.com/economy/canadas-50-most-important-economic-charts-for-2016/

Investment Strategies Equities – Bull Market

Strategas – Mar 20, 2017

Second Longest Fourth Highest

Investment Strategies Equities

WSJ - Jan 27, 2017 RBC - Jonathan Golub “In Defense of Trump Rally – Dec 13, 2016

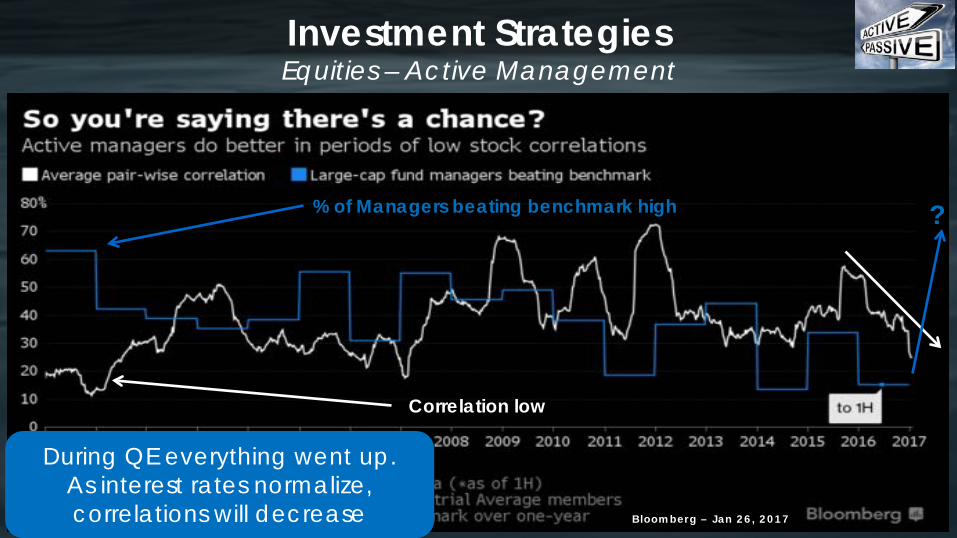

Investment Strategies Equities – Active Management

Bloomberg – Jan 26, 2017

Correlation low

% of Managers beating benchmark high ?

During QE everything went up. As interest rates normalize, correlations will decrease

Economy starting to reflate Trump policies could help Risks are too the upside Monetary policy to finally normalize Equities in the short term Active Management Diversification!

Summary

Financial Advisor/Partner

Mark Therriault

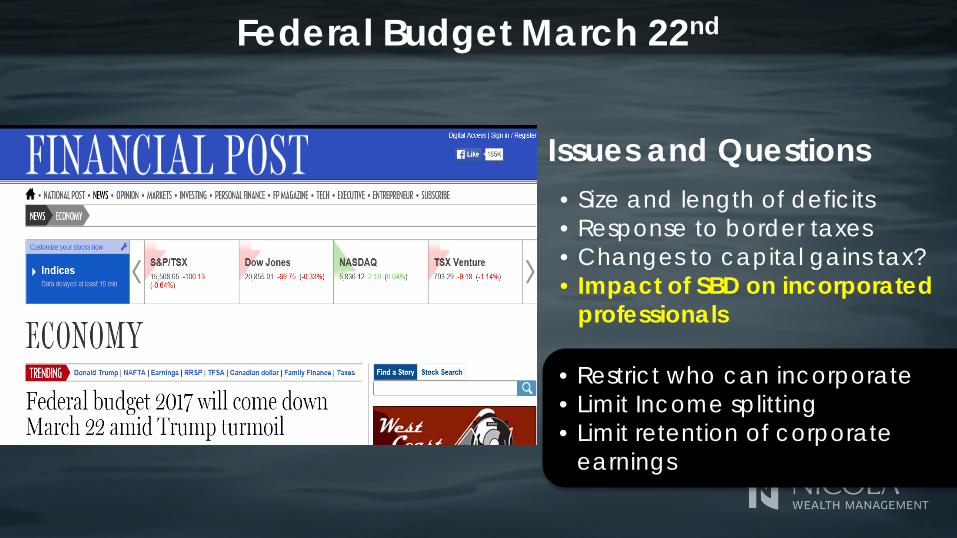

Federal Budget March 22nd

Issues and Questions

• Size and length of deficits • Response to border taxes • Changes to capital gains tax? • Impact of SBD on incorporated

professionals

• Restrict who can incorporate • Limit Income splitting • Limit retention of corporate

earnings

A Genius Bromance

Daniel Kahneman • Introvert • Holocaust Survivor • Psychologist • Taught at UBC • Nobel Prize 2002 in

Economics

Amos Tversky • Extrovert • Israeli Sabra • Psychologist • Taught at Stanford • Died before Nobel

prize

Loss Avoidance

Win 85%

Lose 15% Guaranteed Win Majority

Guaranteed Loss

Win 15%

Lose 85% Majority

Seven Habits of Highly Ineffective Investors

We’re in the Gifted Program

80% Think they are in the top 50%

Over-Optimism

Gambling with House Money

Can we up the minimum

bet?

Investors increase their aggressiveness when they win first.

Increase risk when market rises

Reduce risk when market drops

Gambling with House Money

Can we up the minimum

bet?

4-5% annual loss of return

The Impact of Emotion in Investing

Emotional Investing

5.8%

1.8%

Fund Investor

Vanguard Value Fund 10-year return (01/2017)

Name Fund Investor

Vanguard Growth Stock

Index 8.1% 5.3%

Vanguard Small Cap

Value Index 7.5% 4.2%

Vanguard Small Cap

Growth index 8.1% 7.2%

http://www.theglobeandmail.com/globe-investor/investment-ideas/strategy-lab/index-investing/how-factor-based-investors-take-bigger-risks/article34179810/

-2.8%

-0.9%

-3.2%

Managing Assets More Efficiently

Canadian Equities, 16.7%

High Yield Bonds, 7.3%

Preferred Shares, 4.5%

Alternative Strategies, 15.0%

Real Estate, 20.0%

Mortgages, 11.0%

Bonds, 9.0%

Foreign Bonds, 5.4%

Cash, 4.0%

Foreign Equities, 12.1%

11.4%

Re-Balance

-7.5%

7.48% Blended

2015

• Prices were down 35% • Yields were up more than 50% • Taxes on income 20% less than interest (equal to

bonds paying 8%) • Good chance of capital recovery over five years

What Happened ?

A Tale of Two Shares

7.9% after fees

5.3% before fees Purchases at

depressed prices

35% recovery

The Vulcan Investor

• Good investor behaviour is difficult • 90% of investors do not earn the benchmarks • Volatility can bring on bad behaviour • Diversification is both safe and effective • Picking quality assets takes time and patience

Behaviour and Diversification

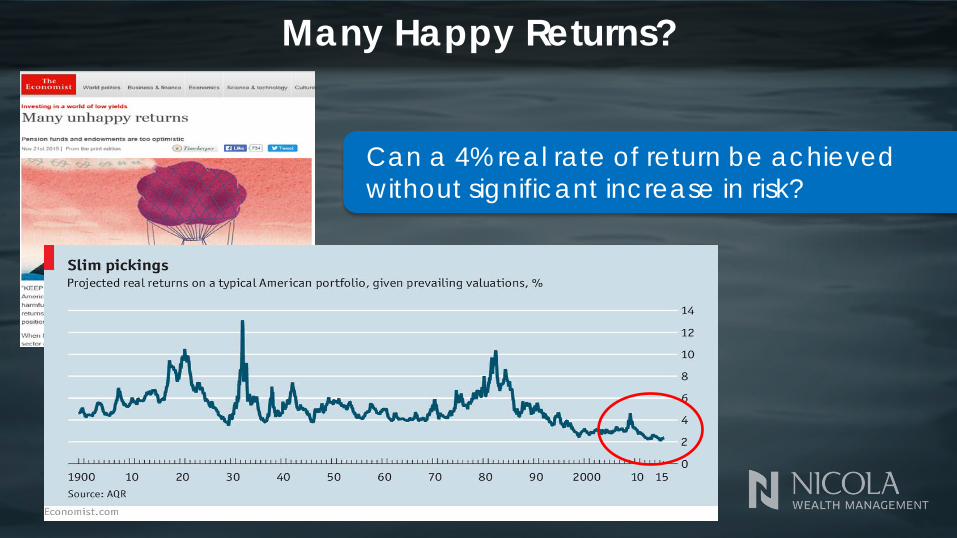

Many Happy Returns?

Can a 4% real rate of return be achieved without significant increase in risk?

Passive vs. Active Investing

146,000 results

How Do ETFs Compare Over 10 Years?

10% 10% 22%

10%

0%10%20%30%40%50%60%70%80%90%

100%

Canadianequities

Canadian Bonds S&P 500 MSCI

ETFFunds1st and 2nd quartile over ten years

Active vs. Passive Investing

What is an Active Manager? • 2007 Yale Study (Updated 2013 FAJ) • Cremers and Petajisto • Focused positions (example

Oakmark Select with 20 positions) • Not always within the benchmark • Different trading strategies and not

market weighted

Passive vs. Active: Another Side

Can you find this?

6.9%( .54% MER)

11.7%(.53% MER)

Active vs. Passive Investing

4.03%

6.84% 7.73%

Average Return, 5 years

ETFs NWM Active Client Returns

Dalbar Effect means Average investor

lower than this

Disciplined rebalancing creates results better

than buy/hold

CAN CI Bal Inc (PSG) 100/100 (PS1) Trimark Glbl Balanced Cl Srs P USD IG/GWL Balanced GIF 75/100 A

TD Advantage Balanced Portfolio-A BMO Asset Allocation - A RBC Bal Fund Series A

Sour

ce: G

lob

eInv

esto

rGol

d A

pr 4

, 201

6

Beyond Stocks and Bonds

Beyond the 60/40 Approach

Canadian Equities

Foreign Equities

Bonds

Foreign Bonds

High Yield Bonds

First Mortgages

Second Mortgages

Real Estate

Private Equity

Preferred Shares

Alternative Strategies

NWM

Typical NWM Client Asset Allocation

Target Cash Flow (interest, dividends, rents) = 4% - 5% /yr.

Target Long-Term Returns (cash flow + growth) = 7% - 8% /yr. (or 4% above inflation)

Historically Consistent & Stable Returns

4.8% 6.6%

-9.5%

6.3%

13.9%

-22.3%

6.2% 4.3%

-4.4%

10 year returns Volatility Worst QuarterBalanced 60/40 TSX NWM

The right asset allocation well managed Can reduces risk and increase returns

Reduced volatility = better Investor behaviour

Hard Asset Real Estate SPIRE RE LP (2005)

SPIRE US LP (2010)

SPIRE VA LP (2014)

$2 billion gross assets ($1 billion client equity)

Private Equity vs. Public Equity

Northleaf: “Private equity should continue to provide investors with a premium of 3% to 5% relative to

public markets over the long term”

Issues with Private Equity • Large minimum investment • No liquidity for 7 to 10 years • Capital calls and return of capital • Concentration risk

The NWM Private Equity Pool LP

NWM Farmland LP

NWM First

Mortgage Pool

• LTV 50 - 60% • Yield 4-4.5%

NWM Balanced Mortgage Pool

• LTV 70 – 75%

• Yield 5.5% - 6%

NWM Mortgage Pools

Summary

Diversification Know Thyself and Behave Well

Low Cost Active Investing Rebalanced Art History

THANK YOU

This presentation contains the current opinions of the presenter and such opinions are subject to change without notice. This material is distributed for informational purposes only and is not intended to provide legal, accounting, tax or specific investment advice. Please speak to your NWM Advisor regarding your unique situation. Forecasts, estimates, and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. NWM fund returns are quoted net of fund-level expenses. Past performance is not indicative of future results. All investments contain risk and may gain or lose value. NWM is registered as a Portfolio Manager, Exempt Market Dealer and Investment Fund Manager with the required provincial securities’ commissions.

QUESTION & ANSWER