2018 market analysis update - cranberry township

TRANSCRIPT

2018 Market Analysis Update

1

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

2018 MARKET ANALYSIS UPDATE

Introduction ......................................................................................................................................3

The Study Area ..................................................................................................................................4

The Demographic Environment ..........................................................................................................5

Key Demographic Observations ..................................................................................................5

New Housing Development Trends ................................................................................................... 15

The Workforce ................................................................................................................................. 18

Worker Inflow/Outflow ............................................................................................................ 18

2010-2015 Commuter Trends .................................................................................................... 18

2017 Employment Trends ......................................................................................................... 18

The Economy ................................................................................................................................... 22

Industry Mix and Job Growth .................................................................................................... 22

Job Earnings ............................................................................................................................. 26

Location Quotient ..................................................................................................................... 26

Shift-Share Analysis .................................................................................................................. 30

The Retail Market ............................................................................................................................ 32

The Commercial Market ................................................................................................................... 38

Regional Economic Opportunities ..................................................................................................... 44

Growth of the Marcellus Shale Industry in the Region ....................................................................... 44

Ethane Cracker Related Opportunities .............................................................................................. 49

Business Retention and Recruitment Recommendations ................................................................... 51

2

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

INTRODUCTION

Located in Butler County, Pennsylvania, Cranberry Township continues to be one of the fastest growing

municipalities in the state. From 2010-2014, Cranberry surpassed McCandless Township as the

municipality with the largest population in the Cranberry Corridor. The Cranberry Corridor consists of

Adams, Cranberry, Jackson, Marshall, McCandless, and Pine townships and Seven Fields Borough. In 2009,

Cranberry included a market analysis (the 2007 Market Analysis) in its comprehensive plan update as a

tool to guide decision-making in developing the Cranberry Plan, the township’s 25-year comprehensive

plan. The 2007 Market Analysis was designed to answer the following questions.

1. Who lives in the Township and what are their demographic characteristics?

2. Who lives here and works there, and who lives there and works here?

3. Who are the Township’s regional competitors and how does the Township compare to

those areas?

4. What are the growth trends in the Township and its competitive areas?

5. What is the economic profile of the Township and its larger economic region?

6. What local and regional assets and strengths can be leveraged to create new business

opportunities in the region?

7. What is the expected impact of the new or planned business operations in the Township?

8. What are the Township’s greatest weaknesses/challenges to economic growth?

9. What level of business development can the Township support, and what types of

businesses should be targeted?

As part the Township’s economic development strategy, it was determined that the key indicators

evaluated in the original market assessment would be updated at three-year intervals to measure the

effectiveness of the Township’s economic development strategy. The 2018 Market Analysis Update

provides indicators to measure five key areas:

1. Demographic Environment

2. Workforce (Inflow/Outflow and Age)

3. Economy (Jobs, Earnings, and Employment Trends)

4. Retail Market

5. Commercial Market

This 2018 Market Analysis is intended to provide an update to Cranberry Township’s 2015 Market Analysis

to better reflect current economic realities and incorporate changes in local demographics and overall

business climate occurring over the last three years. The 2018 Market Analysis provides an overview of

current and emerging real estate and demographic trends associated with Cranberry’s retail, housing and

commercial markets, as well as identifying opportunities for industrial growth relative to the Marcellus

Shale industry and future cracker plant in Beaver County.

3

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

THE STUDY AREA

The study area for the Market Analysis was established in 2007 with the initial assessment; the 2018

analysis remains consistent with that approach. The Market Analysis was designed to look at indicators

and trends, as well as to present peer-to-peer comparisons with competitive areas and micro-to-macro

comparisons to the Township’s larger economic region. Based on growth patterns and anecdotal

information, it was determined that areas in the region most competitive to the Township from both

residential and business standpoints are: (1) the City of Pittsburgh; (2) the Monroeville/Murrysville

Corridor; (3) the North Washington Corridor; and (4) the Airport Corridor. As with the previous market

analysis, this update presents peer-to-peer comparisons of the Township with these areas to identify

comparative strengths and weaknesses in its ability to attract new residents and businesses.

In addition to peer-to-peer comparisons, this market assessment update also compares Cranberry

Township to a larger economic region that includes Butler and Allegheny counties, and select adjacent

municipalities in Beaver, Westmoreland, and Washington counties.

FIGURE 1. CORRIDORS SELECTED FOR COMPARATIVE ASSESSMENT

4

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

THE DEMOGRAPHIC ENVIRONMENT

The residents of the Cranberry provide the talent and skills of the Township’s employment base and are

the consumer base for goods and services in the area. Analyzing the Township’s demographic trends

present indicators of the market for future housing and commercial development. Residents are the

workforce that supports existing business and industry and, in today’s economy, residents are also a

knowledge resource that serves to attract new businesses to the area resulting in higher salaries

commensurate with local knowledge and skills.

Tables 1 - 7 present a comparative overview of seven key indicators comparing Cranberry’s well-being to

its competitive communities.

KEY DEMOGRAPHIC OBSERVATIONS

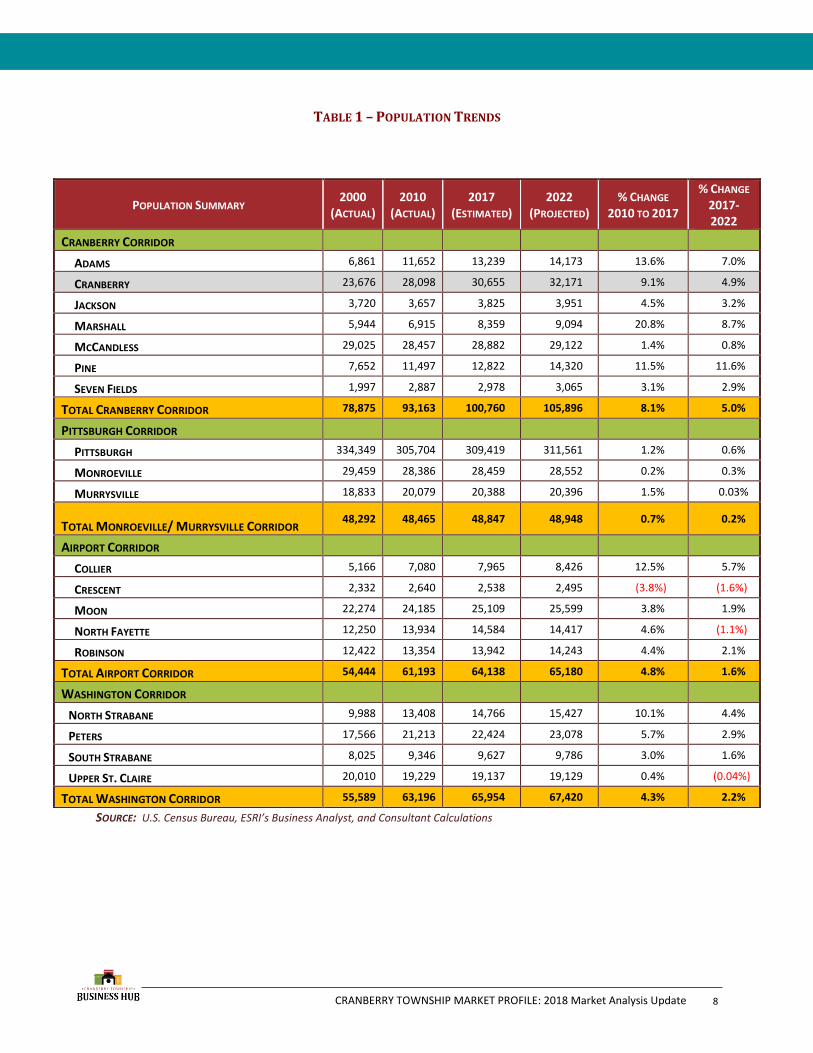

• Trends in the Cranberry Corridor’s population growth are a key indicator of its attractiveness to new

residents and businesses. From 2000-2010, the Cranberry Corridor outpaced its peer corridors,

increasing from 78,875 to 93,163 – the largest population gain in the region. Since 2010, Cranberry

Township has experienced steady growth and surpassed McCandless Township as the most populous

Township in the Cranberry Corridor with 30,655 residents. Absent new development, baseline

population projections through 2022 show continued growth, with a total population of 32,171.

• Nearly one third of the 100,000+ residents in the Cranberry Corridor live in Cranberry Township. The

Cranberry Corridor is anticipated to attract the greatest number of new residents over the next four

years, with a population growth of 5,136, and Cranberry Township’s growth will account for 1,516 of

the new residents.

• As part of The Cranberry Plan, Cranberry Township evaluated three potential growth scenarios and

projected likely population change with each. The scenario - most similar to the new zoning

regulations that resulted from the Plan – was selected as the desirable vision for Cranberry Township’s

future. This preferred scenario established benchmarks for growth within the community including a

target population of 50,011 by 2030. Within seven years of the established growth scenario

benchmarks, Cranberry Township’s population grew by 2,557 new residents and achieved 61% of its

targeted population. The Township’s progressive growth is indicative of its relative attractiveness to

new residents.

• From 2010-2017, Cranberry Township experienced a faster rate of growth in households than any

other community within the study area. The Township attracted 913 new households, followed by

Marshall Township and Pine Township at 526 households and 464 households, respectively. Over the

next four years, Cranberry’s family-friendly community, affordable housing, and employment

opportunities is anticipated to attract 554 new households. This increase will account for 42% of the

total household growth in the Cranberry Corridor.

•

5

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

• Since 2010, Cranberry Township and Pine Township are the only communities within the

Cranberry Corridor to maintain or increase the size of their households. From 2010 -2017, Pine

Township’s household size remained 2.92, whereas Cranberry Township’s household size

increased from 2.72 to 2.73.

• Household income is a quantitative measure of the economic well-being of a community and is

an indicator of the spending power of residents, as well as an indicator of the quality of jobs that

are available to residents. The Cranberry Corridor possesses the highest median household

income compared to its peers, averaging $111,349. The Washington Corridor and

Monroeville/Murrysville Corridor trail behind at $90,451 and $77,448, respectively. Since 2010,

the median household income in Cranberry Township has increased from $84,007 to $104,618 in

2017. In comparison, the median household income in 2017 for Pennsylvania and the United

States was $56,184 and $56,124, respectively. This trend is expected to continue through 2022 as

Cranberry’s median household income will be approximately $47,000 higher than the median

household income of Pennsylvania and the United States. This income difference can be

attributed to numerous factors including Cranberry’s lively business market, access to family-

sustaining jobs, and low taxes.

• A key factor in a community’s attractiveness is a housing supply that matches the needs of an

increasingly diverse population. Historically, most housing units in the Cranberry Corridor were

owner occupied and this trend is expected to continue through 2022. In 2017, Cranberry

Township had 11,859 housing units and 9,297 of those units were owner occupied. Over the next

four years, the number of housing units in Cranberry Township is expected to grow to 12,496,

with 9,771 of those units being owner occupied. As a transient-oriented area, the City of

Pittsburgh possesses the smallest number of owner occupied units, accounting for only 62,006 of

the 159,810 housing units. With housing options as a consideration for potential new knowledge

workers, Cranberry Township should promote its diversified housing stock and affordable family-

friendly housing units.

• Apart from the City of Pittsburgh, Cranberry Township is home to youngest population throughout

the entire study area. Densely populated urban areas typically attract a younger population; such

is the case in Cranberry Township, which has a median age of 39. The City of Pittsburgh, for

comparison, has a median age of 34. The presence of younger residents represents a population

likely to have children and raise families; therefore, their consistency is critical to the Township’s

economic well-being. It will be important for Cranberry to continually evaluate quality of life

factors such as affordable housing, low cost of living, and lively business climate to maintain and

attract young professional and families.

• ESRI measures the diversity of a community using a “diversity index” that indicates the probability

that two people in the same community would be from the same race/ethnic group. A

community’s diversity index captures the racial and ethnical diversity in a single number, 0 to 100,

6

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

with a national average of 65. Cranberry Township has taken great strides to diversify the

community, and those efforts are noticeable by the change in diversity index from 2000 (7.7) to

2017 (16.8). Cranberry’s increased diversity over the past decade is an indication that the

Township has a relative appeal to diverse populations. Although Cranberry Township is not as

diverse as metropolitan areas such as the City of Pittsburgh (55.5), the Township should continue

to implement the diversity strategies identified in The Cranberry Plan Update 2015 to create an

inclusionary environment that provides a comprehensive cultural experience for all residents.

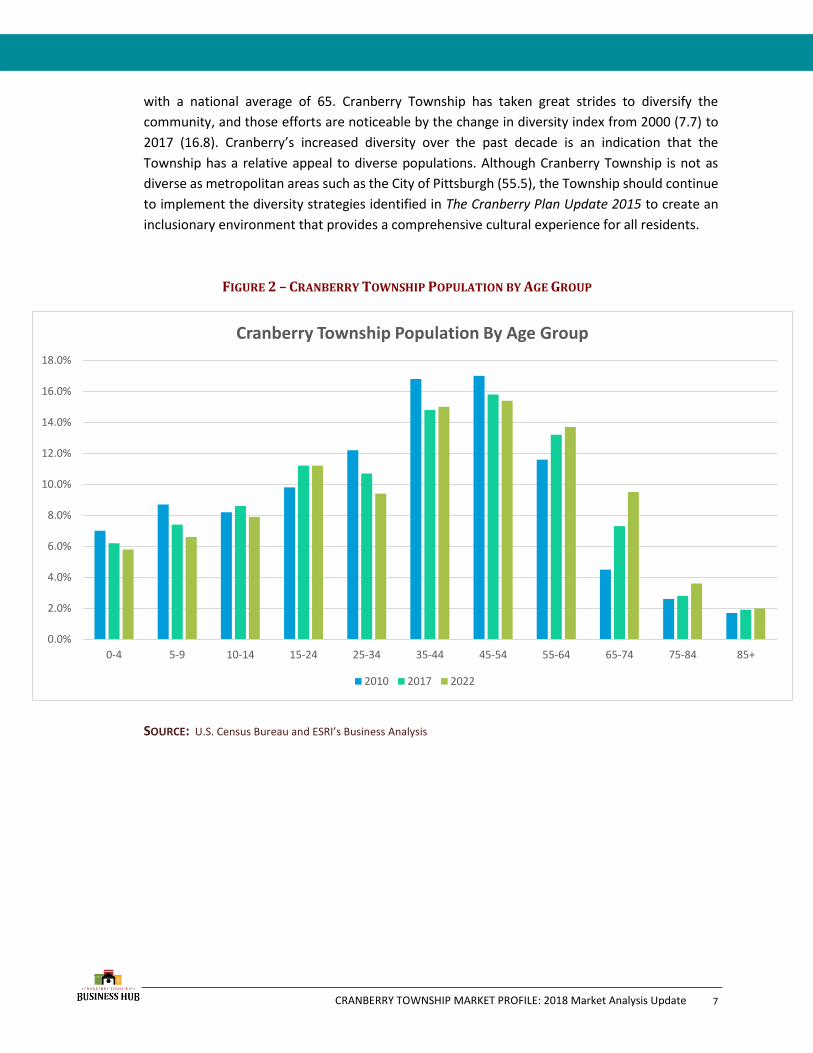

FIGURE 2 – CRANBERRY TOWNSHIP POPULATION BY AGE GROUP

SOURCE: U.S. Census Bureau and ESRI’s Business Analysis

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

0-4 5-9 10-14 15-24 25-34 35-44 45-54 55-64 65-74 75-84 85+

Cranberry Township Population By Age Group

2010 2017 2022

7

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

TABLE 1 – POPULATION TRENDS

SOURCE: U.S. Census Bureau, ESRI’s Business Analyst, and Consultant Calculations

POPULATION SUMMARY 2000

(ACTUAL) 2010

(ACTUAL) 2017

(ESTIMATED) 2022

(PROJECTED) % CHANGE

2010 TO 2017

% CHANGE 2017-2022

CRANBERRY CORRIDOR

ADAMS 6,861 11,652 13,239 14,173 13.6% 7.0%

CRANBERRY 23,676 28,098 30,655 32,171 9.1% 4.9%

JACKSON 3,720 3,657 3,825 3,951 4.5% 3.2%

MARSHALL 5,944 6,915 8,359 9,094 20.8% 8.7%

MCCANDLESS 29,025 28,457 28,882 29,122 1.4% 0.8%

PINE 7,652 11,497 12,822 14,320 11.5% 11.6%

SEVEN FIELDS 1,997 2,887 2,978 3,065 3.1% 2.9%

TOTAL CRANBERRY CORRIDOR 78,875 93,163 100,760 105,896 8.1% 5.0%

PITTSBURGH CORRIDOR

PITTSBURGH 334,349 305,704 309,419 311,561 1.2% 0.6%

MONROEVILLE 29,459 28,386 28,459 28,552 0.2% 0.3%

MURRYSVILLE 18,833 20,079 20,388 20,396 1.5% 0.03%

TOTAL MONROEVILLE/ MURRYSVILLE CORRIDOR 48,292 48,465 48,847 48,948 0.7% 0.2%

AIRPORT CORRIDOR

COLLIER 5,166 7,080 7,965 8,426 12.5% 5.7%

CRESCENT 2,332 2,640 2,538 2,495 (3.8%) (1.6%)

MOON 22,274 24,185 25,109 25,599 3.8% 1.9%

NORTH FAYETTE 12,250 13,934 14,584 14,417 4.6% (1.1%)

ROBINSON 12,422 13,354 13,942 14,243 4.4% 2.1%

TOTAL AIRPORT CORRIDOR 54,444 61,193 64,138 65,180 4.8% 1.6%

WASHINGTON CORRIDOR

NORTH STRABANE 9,988 13,408 14,766 15,427 10.1% 4.4%

PETERS 17,566 21,213 22,424 23,078 5.7% 2.9%

SOUTH STRABANE 8,025 9,346 9,627 9,786 3.0% 1.6%

UPPER ST. CLAIRE 20,010 19,229 19,137 19,129 0.4% (0.04%)

TOTAL WASHINGTON CORRIDOR 55,589 63,196 65,954 67,420 4.3% 2.2%

8

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

TABLE 2 – HOUSEHOLDS

SOURCE: U.S. Census Bureau, ESRI’s Business Analyst, and Consultant Calculations

2000 (ACTUAL)

2010 (ACTUAL)

2017 (ESTIMATED)

2022 (PROJECTED)

NUMERIC

CHANGE (2010 TO

2017)

% CHANGE 2010 TO

2017

% CHANGE 2017 TO

2022

CRANBERRY CORRIDOR

ADAMS 2,352 4,389 5,036 5,414 647 14.7% 7.5%

CRANBERRY 8,367 10,248 11,161 11,715 913 8.9% 4.9%

JACKSON 1,386 1,423 1,503 1,559 80 5.6% 3.7%

MARSHALL 1,929 2,415 2,941 3,201 526 21.7% 8.8%

MCCANDLESS 11,153 11,659 11,947 12,107 288 2.4% 1.3%

PINE 2,401 3,933 4,387 4,630 454 11.5% 5.5%

SEVEN FIELDS 760 1,186 1,236 1,276 50 4.2% 3.2%

TOTAL CRANBERRY

CORRIDOR 28,348 35,253 36,804 38,113 1,551 4.4% 3.5%

PITTSBURGH CORRIDOR

PITTSBURGH 143,695 136,217 138,152 139,560 -1,935 (1.4%) 1.0%

MONROEVILLE 12,432 12,612 12,732 12,813 120 0.9% 0.6%

MURRYSVILLE 7,087 7,917 8,100 8,115 183 2.3% 0.1%

TOTAL MONROEVILLE/ MURRYSVILLE CORRIDOR 19,519 20,529 20,832 20,928 1,010 1.4% 0.4%

AIRPORT CORRIDOR

COLLIER 2,168 3,095 3,501 3,714 406 13.1% 6.0%

CRESCENT 891 1,067 1,034 1,020 -33 (3.1%) (1.3%)

MOON 8,441 9,646 10,036 10,252 390 4.0% 2.1%

NORTH FAYETTE 5,003 5,810 6,110 6,276 300 5.1% 2.7%

ROBINSON 4,905 5,652 5,947 6,102 295 5.3% 2.6%

TOTAL AIRPORT CORRIDOR 21,408 25,270 26,628 27,364 1,358 5.3% 2.7%

WASHINGTON CORRIDOR

NORTH STRABANE 3,947 5,432 6,012 6,298 580 10.6% 4.7%

PETERS 6,026 7,292 7,699 7,918 407 5.5% 2.8%

SOUTH STRABANE 3,335 4,256 4,400 4,480 144 3.3% 1.8%

UPPER ST. CLAIRE 6,944 6,976 6,992 7,013 16 0.2% 0.3%

TOTAL WASHINGTON

CORRIDOR 20,252 23,956 25,103 25,709 1,147 4.7% 2.4%

9

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

TABLE 3 – HOUSEHOLD SIZE

SOURCE: U.S. Census Bureau, ESRI’s Business Analyst, and Consultant Calculations

2000 (ACTUAL)

2010 (ACTUAL)

2017 (ESTIMATED)

2022 (PROJECTED)

% CHANGE 2010 TO

2017

% CHANGE 2017-2022

CRANBERRY CORRIDOR

ADAMS 2.84 2.64 2.61 2.60 (1.13%) (0.38%)

CRANBERRY 2.81 2.72 2.73 2.73 (0.36%) 0.00%

JACKSON 2.60 2.50 2.48 2.47 (0.80%) (0.40%)

MARSHALL 3.07 2.86 2.84 2.84 (0.69%) 0.00%

MCCANDLESS 2.49 2.36 2.33 2.32 (1.27%) (0.42%)

PINE 3.14 2.92 2.92 2.93 0.00% 0.34%

SEVEN FIELDS 2.58 2.43 2.41 2.40 (0.82%) (0.41%)

CRANBERRY CORRIDOR AVERAGE 2.79 2.63 2.62 2.61 (0.62%) (0.18%)

PITTSBURGH CORRIDOR PITTSBURGH 2.17 2.07 2.06 2.05 (0.48%) (0.48%)

PITTSBURGH CORRIDOR AVERAGE 2.17 2.07 2.06 2.05 (0.48%) (0.48%)

MONROEVILLE 2.29 2.21 2.19 2.19 (1.36%) 0.00%

MURRYSVILLE 2.63 2.51 2.49 2.49 (0.79%) 0.00%

MONROEVILLE/MURRYSVILLE CORRIDOR AVERAGE 2.46 2.36 2.34 2.34 (1.08%) 0.00%

AIRPORT CORRIDOR COLLIER 2.37 2.28 2.27 2.26 (0.43%) (0.44%)

CRESCENT 2.61 2.47 2.45 2.44 (0.41%) (0.40%)

MOON 2.44 2.37 2.36 2.36 (0.81%) 0.00%

NORTH FAYETTE 2.43 2.40 2.39 2.38 (0.41%) (0.41%)

ROBINSON 2.44 2.31 2.29 2.28 (0.86%) (0.43%)

AIRPORT CORRIDOR AVERAGE 2.46 2.37 2.35 2.34 (0.58%) (0.33%)

WASHINGTON CORRIDOR NORTH STRABANE 2.45 2.43 2.42 2.42 (0.41%) 0.00%

PETERS 2.87 2.88 2.88 2.89 0.00% 0.34%

SOUTH STRABANE 2.34 2.17 2.17 2.16 0.00% (0.46%)

UPPER ST. CLAIRE 2.82 2.75 2.73 2.72 (0.72%) (0.36%)

WASHINGTON CORRIDOR AVERAGE 2.62 2.56 2.55 2.54 (0.28%) (0.16%)

10

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

TABLE 4 – MEDIAN HOUSEHOLD INCOME

SOURCE: U.S. Census Bureau, ESRI’s Business Analyst, and Consultant Calculations

2000 (ACTUAL)

2010 (ESTIMATED)

2017 (ESTIMATED

2022 (PROJECTED)

% CHANGE 2010 TO 2017

% CHANGE

2017 TO 2022

CRANBERRY CORRIDOR

ADAMS $64,382 $78,098 $103,511 $113,706 32.5% 9.8%

CRANBERRY $66,994 $84,007 $104,618 $110,238 24.5% 5.3%

JACKSON $47,155 $55,486 $68,831 $79,085 24.0% 14.9%

MARSHALL $102,270 $121,198 $153,639 $157,571 26.7% 2.5%

MCCANDLESS $62,183 $71,867 $84,261 $92,975 17.2% 10.3%

PINE $86,692 $109,540 $158,389 $165,102 44.5% 4.2%

SEVEN FIELDS $66,818 $79,825 $106,196 $115,273 33.4% 8.5%

TOTAL CRANBERRY CORRIDOR AVERAGE $70,928 $85,717 $111,349 $119,135 28.9% 7.9%

PITTSBURGH CORRIDOR

PITTSBURGH $28,666 $38,446 $40,535 $45,357 5.4% 11.8%

MONROEVILLE/MURRYSVILLE CORRIDOR

MONROEVILLE $44,509 $55,902 $62,288 $69,731 11.4% 11.9%

MURRYSVILLE $63,091 $75,936 $92,609 $99,610 21.1% 7.5%

TOTAL MONROEVILLE/ MURRYSVILLE

CORRIDOR AVERAGE $53,800 $65,919 $77,448 $84,670 16.2% 9.7%

AIRPORT CORRIDOR

COLLIER $41,056 $57,301 $69,039 $80,073 20.4% 15.9%

CRESCENT $49,465 $65,255 $64,382 $76,057 (1.3%) 18.1%

MOON $57,208 $68,592 $77,265 $85,508 12.6% 10.6%

NORTH FAYETTE $51,534 $63,547 $73,206 $81,746 15.2% 11.6%

ROBINSON $55,061 $73,531 $77,605 $87,029 5.5% 12.1%

TOTAL AIRPORT CORRIDOR AVERAGE $50,865 $65,645 $72,299 $82,082 3.0% 21.6%

WASHINGTON CORRIDOR

NORTH STRABANE $50,635 $65,533 $76,719 $83,796 17.0% 9.2%

PETERS $77,100 $89,065 $108,306 $113,576 21.6% 4.8%

SOUTH STRABANE $42,604 $57,769 $59,952 $66,647 3.7% 11.1%

UPPER ST. CLAIRE $85,280 $100,805 $116,830 $121,404 15.9% 3.9%

TOTAL WASHINGTON CORRIDOR AVERAGE $63,905 $78,293 $90,451 $96,355 11.6% 5.8%

11

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

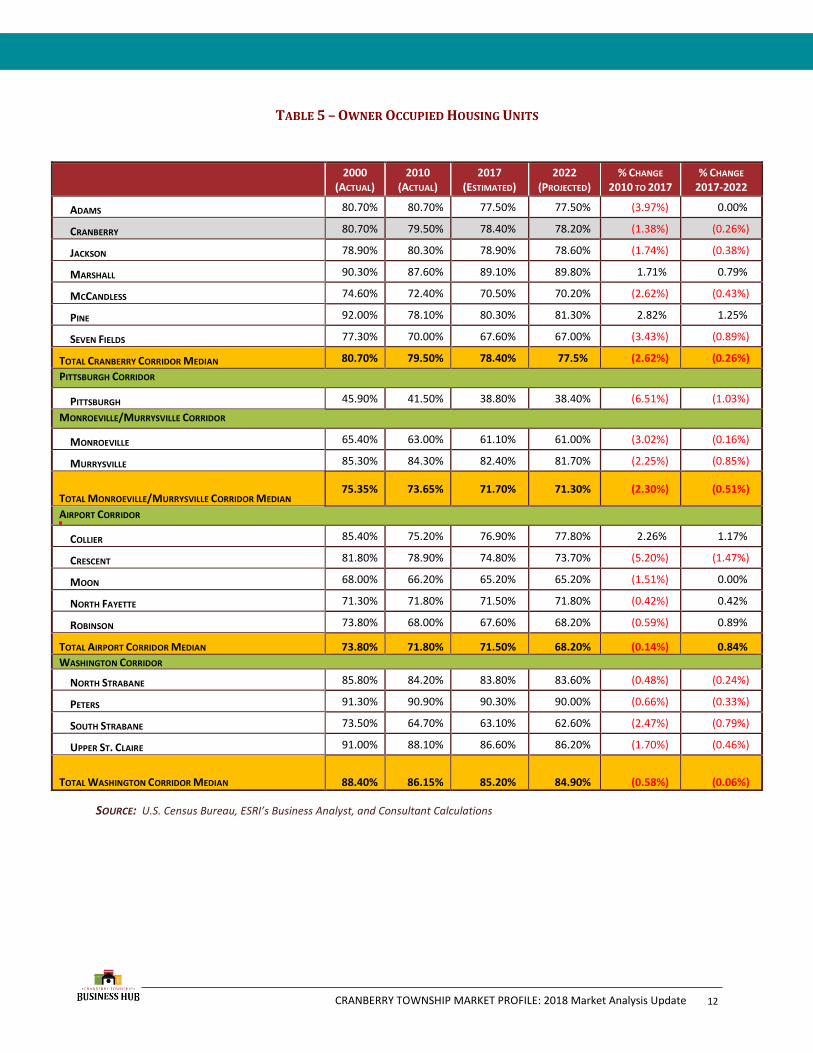

TABLE 5 – OWNER OCCUPIED HOUSING UNITS

SOURCE: U.S. Census Bureau, ESRI’s Business Analyst, and Consultant Calculations

2000 (ACTUAL)

2010 (ACTUAL)

2017 (ESTIMATED)

2022 (PROJECTED)

% CHANGE 2010 TO 2017

% CHANGE 2017-2022

ADAMS 80.70% 80.70% 77.50% 77.50% (3.97%) 0.00%

CRANBERRY 80.70% 79.50% 78.40% 78.20% (1.38%) (0.26%)

JACKSON 78.90% 80.30% 78.90% 78.60% (1.74%) (0.38%)

MARSHALL 90.30% 87.60% 89.10% 89.80% 1.71% 0.79%

MCCANDLESS 74.60% 72.40% 70.50% 70.20% (2.62%) (0.43%)

PINE 92.00% 78.10% 80.30% 81.30% 2.82% 1.25%

SEVEN FIELDS 77.30% 70.00% 67.60% 67.00% (3.43%) (0.89%)

TOTAL CRANBERRY CORRIDOR MEDIAN 80.70% 79.50% 78.40% 77.5% (2.62%) (0.26%)

PITTSBURGH CORRIDOR

PITTSBURGH 45.90% 41.50% 38.80% 38.40% (6.51%) (1.03%)

MONROEVILLE/MURRYSVILLE CORRIDOR

MONROEVILLE 65.40% 63.00% 61.10% 61.00% (3.02%) (0.16%)

MURRYSVILLE 85.30% 84.30% 82.40% 81.70% (2.25%) (0.85%)

TOTAL MONROEVILLE/MURRYSVILLE CORRIDOR MEDIAN 75.35% 73.65% 71.70% 71.30% (2.30%) (0.51%)

AIRPORT CORRIDOR

COLLIER 85.40% 75.20% 76.90% 77.80% 2.26% 1.17%

CRESCENT 81.80% 78.90% 74.80% 73.70% (5.20%) (1.47%)

MOON 68.00% 66.20% 65.20% 65.20% (1.51%) 0.00%

NORTH FAYETTE 71.30% 71.80% 71.50% 71.80% (0.42%) 0.42%

ROBINSON 73.80% 68.00% 67.60% 68.20% (0.59%) 0.89%

TOTAL AIRPORT CORRIDOR MEDIAN 73.80% 71.80% 71.50% 68.20% (0.14%) 0.84%

WASHINGTON CORRIDOR

NORTH STRABANE 85.80% 84.20% 83.80% 83.60% (0.48%) (0.24%)

PETERS 91.30% 90.90% 90.30% 90.00% (0.66%) (0.33%)

SOUTH STRABANE 73.50% 64.70% 63.10% 62.60% (2.47%) (0.79%)

UPPER ST. CLAIRE 91.00% 88.10% 86.60% 86.20% (1.70%) (0.46%)

TOTAL WASHINGTON CORRIDOR MEDIAN 88.40% 86.15% 85.20% 84.90% (0.58%) (0.06%)

12

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

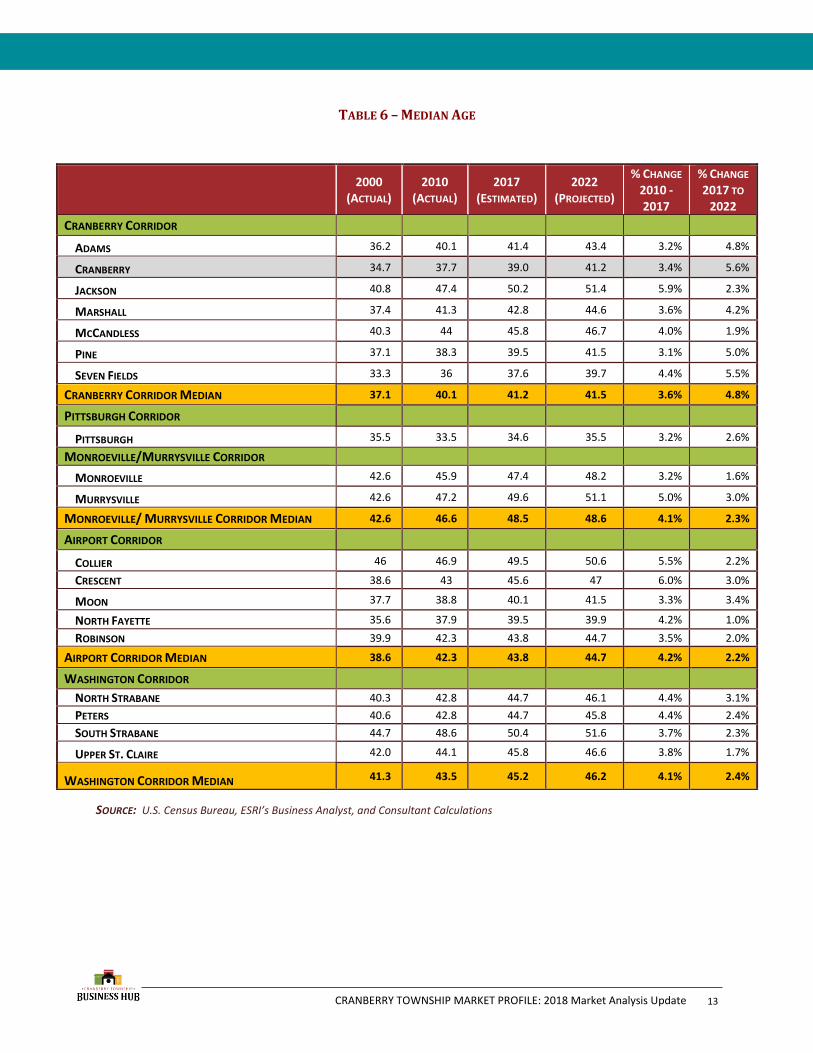

TABLE 6 – MEDIAN AGE

SOURCE: U.S. Census Bureau, ESRI’s Business Analyst, and Consultant Calculations

2000 (ACTUAL)

2010 (ACTUAL)

2017 (ESTIMATED)

2022 (PROJECTED)

% CHANGE 2010 -2017

% CHANGE 2017 TO

2022

CRANBERRY CORRIDOR

ADAMS 36.2 40.1 41.4 43.4 3.2% 4.8%

CRANBERRY 34.7 37.7 39.0 41.2 3.4% 5.6%

JACKSON 40.8 47.4 50.2 51.4 5.9% 2.3%

MARSHALL 37.4 41.3 42.8 44.6 3.6% 4.2%

MCCANDLESS 40.3 44 45.8 46.7 4.0% 1.9%

PINE 37.1 38.3 39.5 41.5 3.1% 5.0%

SEVEN FIELDS 33.3 36 37.6 39.7 4.4% 5.5%

CRANBERRY CORRIDOR MEDIAN 37.1 40.1 41.2 41.5 3.6% 4.8%

PITTSBURGH CORRIDOR

PITTSBURGH 35.5 33.5 34.6 35.5 3.2% 2.6%

MONROEVILLE/MURRYSVILLE CORRIDOR

MONROEVILLE 42.6 45.9 47.4 48.2 3.2% 1.6%

MURRYSVILLE 42.6 47.2 49.6 51.1 5.0% 3.0%

MONROEVILLE/ MURRYSVILLE CORRIDOR MEDIAN 42.6 46.6 48.5 48.6 4.1% 2.3%

AIRPORT CORRIDOR

COLLIER 46 46.9 49.5 50.6 5.5% 2.2%

CRESCENT 38.6 43 45.6 47 6.0% 3.0%

MOON 37.7 38.8 40.1 41.5 3.3% 3.4%

NORTH FAYETTE 35.6 37.9 39.5 39.9 4.2% 1.0%

ROBINSON 39.9 42.3 43.8 44.7 3.5% 2.0%

AIRPORT CORRIDOR MEDIAN 38.6 42.3 43.8 44.7 4.2% 2.2%

WASHINGTON CORRIDOR

NORTH STRABANE 40.3 42.8 44.7 46.1 4.4% 3.1%

PETERS 40.6 42.8 44.7 45.8 4.4% 2.4%

SOUTH STRABANE 44.7 48.6 50.4 51.6 3.7% 2.3%

UPPER ST. CLAIRE 42.0 44.1 45.8 46.6 3.8% 1.7%

WASHINGTON CORRIDOR MEDIAN 41.3 43.5 45.2 46.2 4.1% 2.4%

13

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

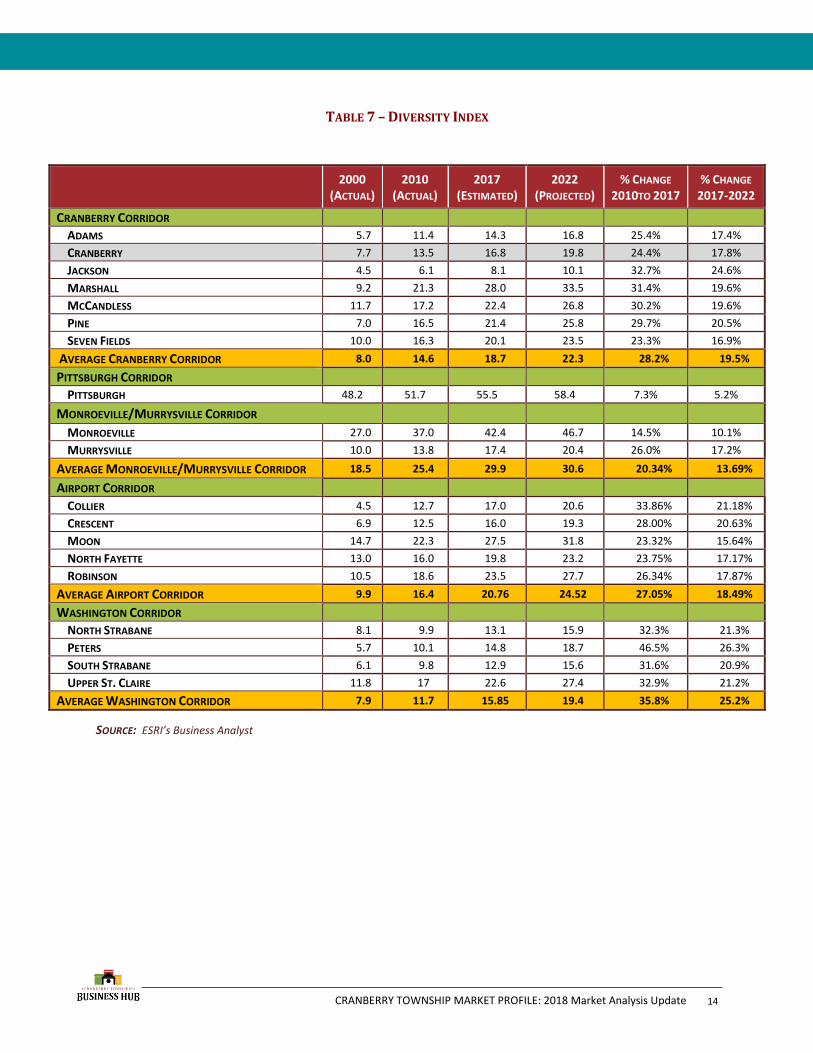

TABLE 7 – DIVERSITY INDEX

SOURCE: ESRI’s Business Analyst

2000 (ACTUAL)

2010 (ACTUAL)

2017 (ESTIMATED)

2022 (PROJECTED)

% CHANGE 2010TO 2017

% CHANGE 2017-2022

CRANBERRY CORRIDOR

ADAMS 5.7 11.4 14.3 16.8 25.4% 17.4%

CRANBERRY 7.7 13.5 16.8 19.8 24.4% 17.8%

JACKSON 4.5 6.1 8.1 10.1 32.7% 24.6%

MARSHALL 9.2 21.3 28.0 33.5 31.4% 19.6%

MCCANDLESS 11.7 17.2 22.4 26.8 30.2% 19.6%

PINE 7.0 16.5 21.4 25.8 29.7% 20.5%

SEVEN FIELDS 10.0 16.3 20.1 23.5 23.3% 16.9%

AVERAGE CRANBERRY CORRIDOR 8.0 14.6 18.7 22.3 28.2% 19.5%

PITTSBURGH CORRIDOR

PITTSBURGH 48.2 51.7 55.5 58.4 7.3% 5.2%

MONROEVILLE/MURRYSVILLE CORRIDOR

MONROEVILLE 27.0 37.0 42.4 46.7 14.5% 10.1%

MURRYSVILLE 10.0 13.8 17.4 20.4 26.0% 17.2%

AVERAGE MONROEVILLE/MURRYSVILLE CORRIDOR 18.5 25.4 29.9 30.6 20.34% 13.69%

AIRPORT CORRIDOR

COLLIER 4.5 12.7 17.0 20.6 33.86% 21.18%

CRESCENT 6.9 12.5 16.0 19.3 28.00% 20.63%

MOON 14.7 22.3 27.5 31.8 23.32% 15.64%

NORTH FAYETTE 13.0 16.0 19.8 23.2 23.75% 17.17%

ROBINSON 10.5 18.6 23.5 27.7 26.34% 17.87%

AVERAGE AIRPORT CORRIDOR 9.9 16.4 20.76 24.52 27.05% 18.49%

WASHINGTON CORRIDOR

NORTH STRABANE 8.1 9.9 13.1 15.9 32.3% 21.3%

PETERS 5.7 10.1 14.8 18.7 46.5% 26.3%

SOUTH STRABANE 6.1 9.8 12.9 15.6 31.6% 20.9%

UPPER ST. CLAIRE 11.8 17 22.6 27.4 32.9% 21.2%

AVERAGE WASHINGTON CORRIDOR 7.9 11.7 15.85 19.4 35.8% 25.2%

14

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

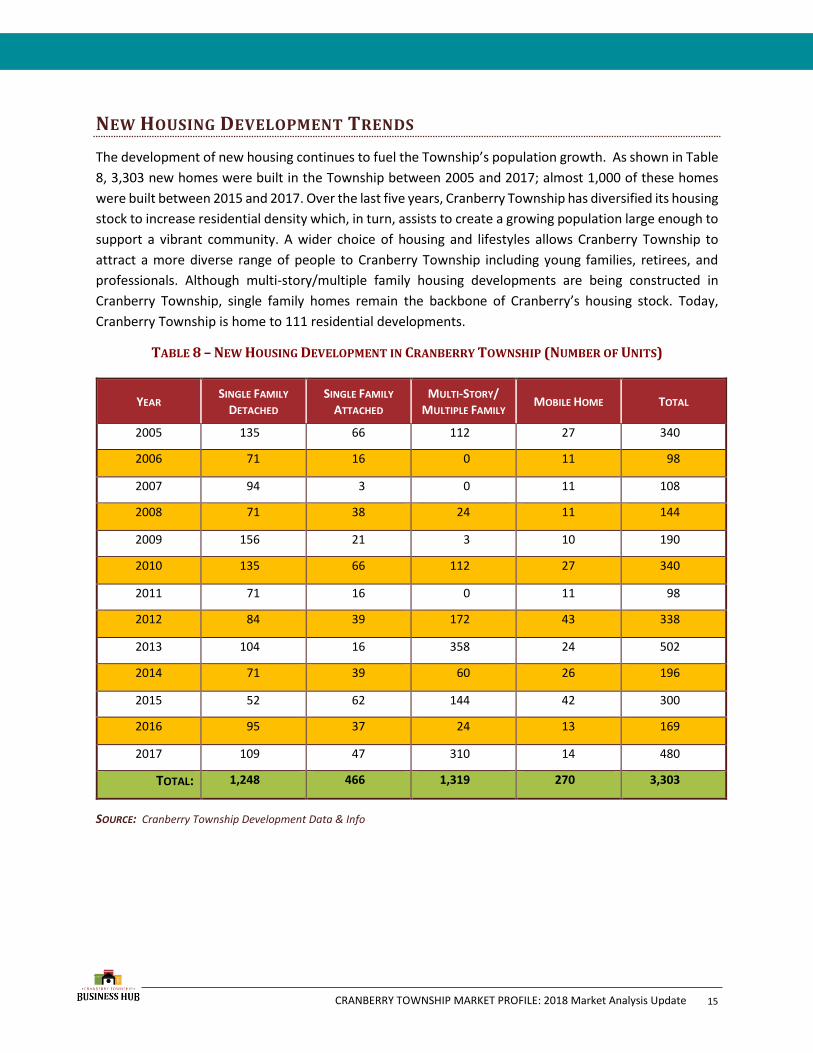

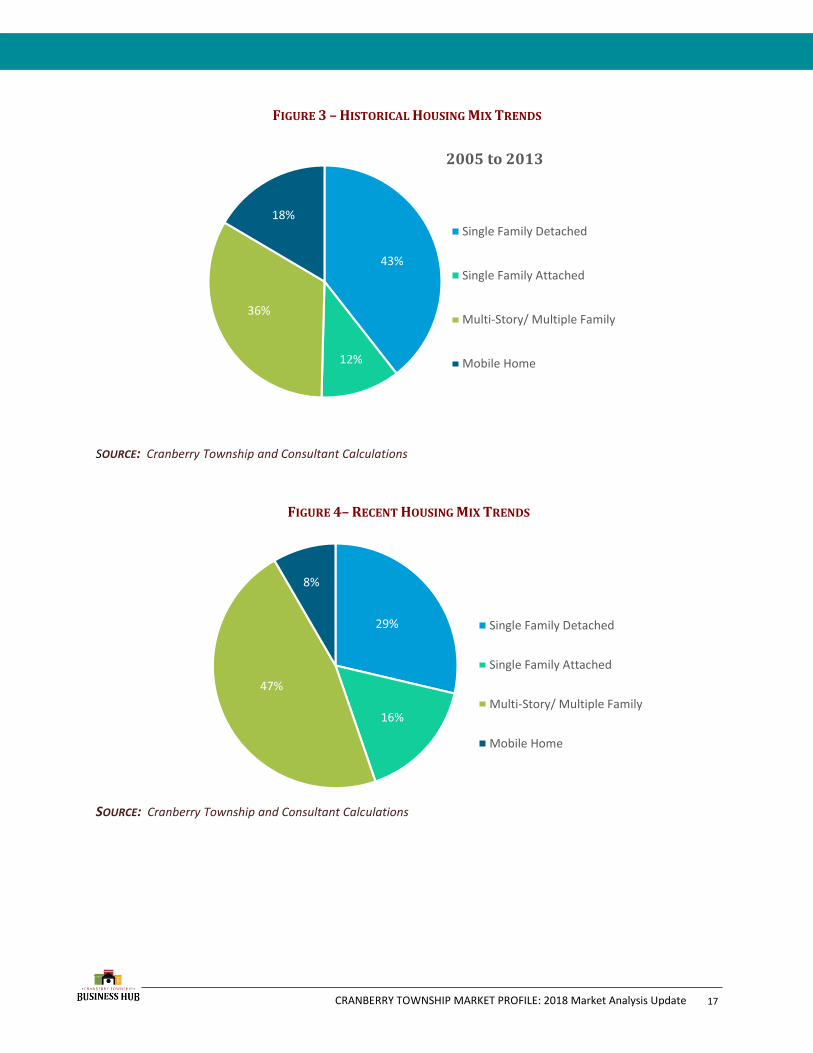

NEW HOUSING DEVELOPMENT TRENDS

The development of new housing continues to fuel the Township’s population growth. As shown in Table

8, 3,303 new homes were built in the Township between 2005 and 2017; almost 1,000 of these homes

were built between 2015 and 2017. Over the last five years, Cranberry Township has diversified its housing

stock to increase residential density which, in turn, assists to create a growing population large enough to

support a vibrant community. A wider choice of housing and lifestyles allows Cranberry Township to

attract a more diverse range of people to Cranberry Township including young families, retirees, and

professionals. Although multi-story/multiple family housing developments are being constructed in

Cranberry Township, single family homes remain the backbone of Cranberry’s housing stock. Today,

Cranberry Township is home to 111 residential developments.

TABLE 8 – NEW HOUSING DEVELOPMENT IN CRANBERRY TOWNSHIP (NUMBER OF UNITS)

YEAR SINGLE FAMILY

DETACHED SINGLE FAMILY

ATTACHED MULTI-STORY/

MULTIPLE FAMILY MOBILE HOME TOTAL

2005 135 66 112 27 340

2006 71 16 0 11 98

2007 94 3 0 11 108

2008 71 38 24 11 144

2009 156 21 3 10 190

2010 135 66 112 27 340

2011 71 16 0 11 98

2012 84 39 172 43 338

2013 104 16 358 24 502

2014 71 39 60 26 196

2015 52 62 144 42 300

2016 95 37 24 13 169

2017 109 47 310 14 480

TOTAL: 1,248 466 1,319 270 3,303

SOURCE: Cranberry Township Development Data & Info

15

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

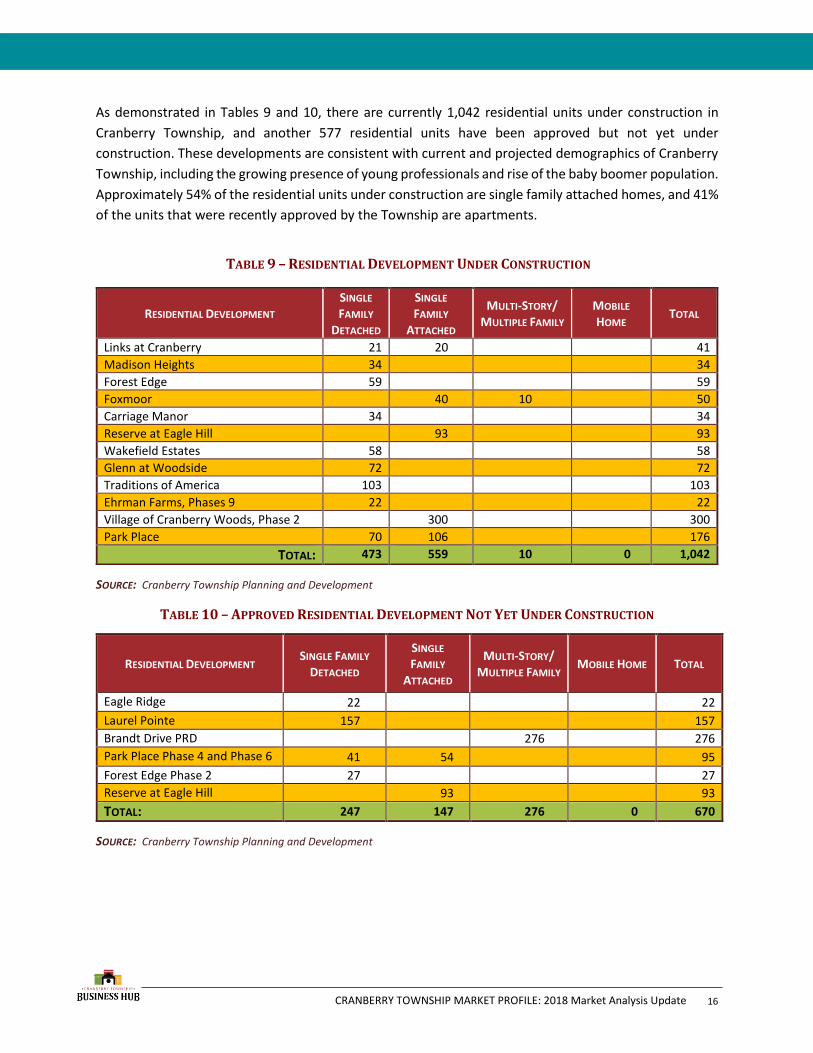

As demonstrated in Tables 9 and 10, there are currently 1,042 residential units under construction in

Cranberry Township, and another 577 residential units have been approved but not yet under

construction. These developments are consistent with current and projected demographics of Cranberry

Township, including the growing presence of young professionals and rise of the baby boomer population.

Approximately 54% of the residential units under construction are single family attached homes, and 41%

of the units that were recently approved by the Township are apartments.

TABLE 9 – RESIDENTIAL DEVELOPMENT UNDER CONSTRUCTION

SOURCE: Cranberry Township Planning and Development

TABLE 10 – APPROVED RESIDENTIAL DEVELOPMENT NOT YET UNDER CONSTRUCTION

SOURCE: Cranberry Township Planning and Development

RESIDENTIAL DEVELOPMENT SINGLE

FAMILY

DETACHED

SINGLE

FAMILY

ATTACHED

MULTI-STORY/

MULTIPLE FAMILY MOBILE

HOME TOTAL

Links at Cranberry 21 20 41

Madison Heights 34 34

Forest Edge 59 59

Foxmoor 40 10 50

Carriage Manor 34 34

Reserve at Eagle Hill 93 93

Wakefield Estates 58 58

Glenn at Woodside 72 72

Traditions of America 103 103

Ehrman Farms, Phases 9 22 22

Village of Cranberry Woods, Phase 2 300 300

Park Place 70 106 176

TOTAL: 473 559 10 0 1,042

RESIDENTIAL DEVELOPMENT SINGLE FAMILY

DETACHED

SINGLE

FAMILY

ATTACHED

MULTI-STORY/

MULTIPLE FAMILY MOBILE HOME TOTAL

Eagle Ridge 22 22

Laurel Pointe 157 157

Brandt Drive PRD 276 276

Park Place Phase 4 and Phase 6 41 54 95

Forest Edge Phase 2 27 27

Reserve at Eagle Hill 93 93

TOTAL: 247 147 276 0 670

16

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

FIGURE 3 – HISTORICAL HOUSING MIX TRENDS

SOURCE: Cranberry Township and Consultant Calculations

SOURCE: Cranberry Township and Consultant Calculations

43%

12%

36%

18%Single Family Detached

Single Family Attached

Multi-Story/ Multiple Family

Mobile Home

2005 to 2013

29%

16%

47%

8%

Single Family Detached

Single Family Attached

Multi-Story/ Multiple Family

Mobile Home

FIGURE 4– RECENT HOUSING MIX TRENDS

17

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

THE WORKFORCE

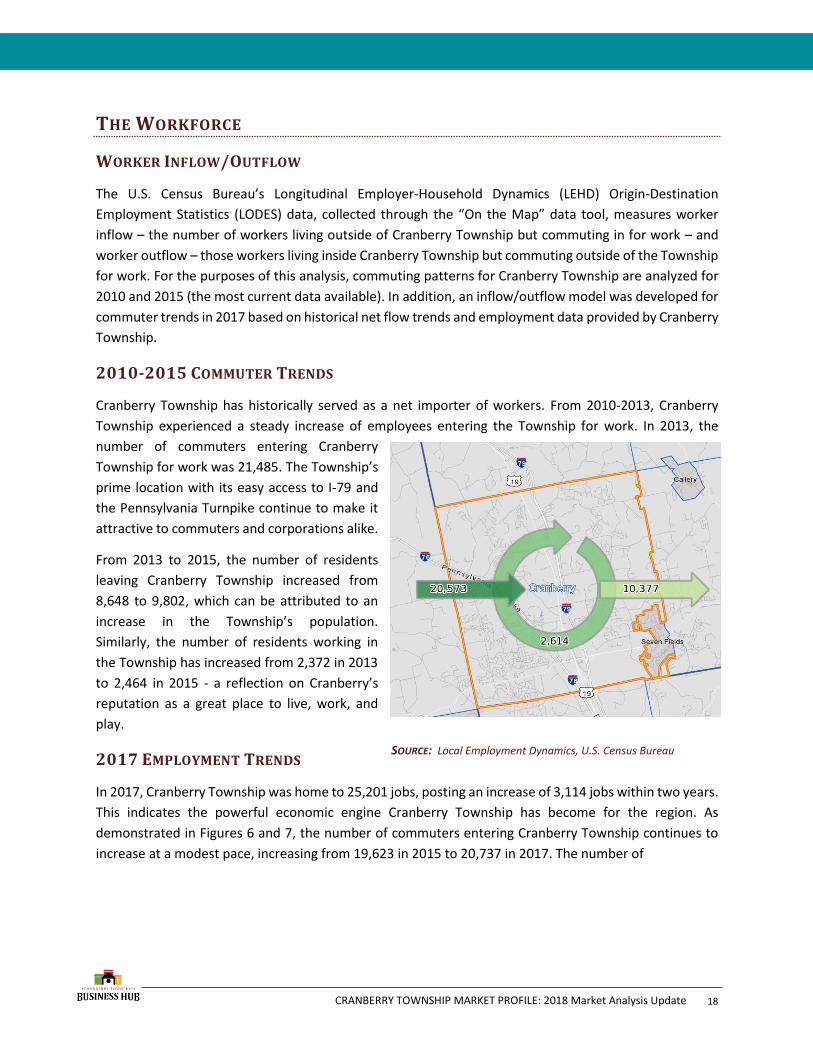

WORKER INFLOW/OUTFLOW

The U.S. Census Bureau’s Longitudinal Employer-Household Dynamics (LEHD) Origin-Destination

Employment Statistics (LODES) data, collected through the “On the Map” data tool, measures worker

inflow – the number of workers living outside of Cranberry Township but commuting in for work – and

worker outflow – those workers living inside Cranberry Township but commuting outside of the Township

for work. For the purposes of this analysis, commuting patterns for Cranberry Township are analyzed for

2010 and 2015 (the most current data available). In addition, an inflow/outflow model was developed for

commuter trends in 2017 based on historical net flow trends and employment data provided by Cranberry

Township.

2010-2015 COMMUTER TRENDS

Cranberry Township has historically served as a net importer of workers. From 2010-2013, Cranberry

Township experienced a steady increase of employees entering the Township for work. In 2013, the

number of commuters entering Cranberry

Township for work was 21,485. The Township’s

prime location with its easy access to I-79 and

the Pennsylvania Turnpike continue to make it

attractive to commuters and corporations alike.

From 2013 to 2015, the number of residents

leaving Cranberry Township increased from

8,648 to 9,802, which can be attributed to an

increase in the Township’s population.

Similarly, the number of residents working in

the Township has increased from 2,372 in 2013

to 2,464 in 2015 - a reflection on Cranberry’s

reputation as a great place to live, work, and

play.

2017 EMPLOYMENT TRENDS

In 2017, Cranberry Township was home to 25,201 jobs, posting an increase of 3,114 jobs within two years.

This indicates the powerful economic engine Cranberry Township has become for the region. As

demonstrated in Figures 6 and 7, the number of commuters entering Cranberry Township continues to

increase at a modest pace, increasing from 19,623 in 2015 to 20,737 in 2017. The number of

FIGURE 5 – CRANBERRY TOWNSHIP INFLOW/OUTFLOW (2015)

SOURCE: Local Employment Dynamics, U.S. Census Bureau

18

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

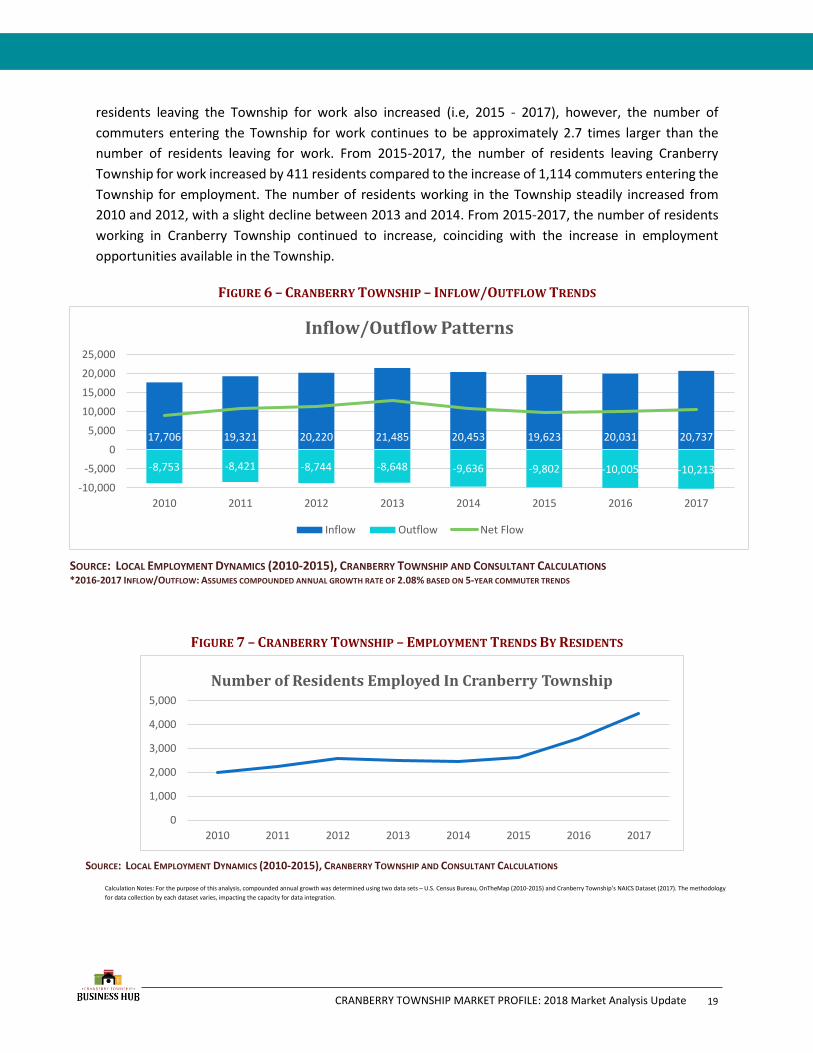

residents leaving the Township for work also increased (i.e, 2015 - 2017), however, the number of

commuters entering the Township for work continues to be approximately 2.7 times larger than the

number of residents leaving for work. From 2015-2017, the number of residents leaving Cranberry

Township for work increased by 411 residents compared to the increase of 1,114 commuters entering the

Township for employment. The number of residents working in the Township steadily increased from

2010 and 2012, with a slight decline between 2013 and 2014. From 2015-2017, the number of residents

working in Cranberry Township continued to increase, coinciding with the increase in employment

opportunities available in the Township.

FIGURE 6 – CRANBERRY TOWNSHIP – INFLOW/OUTFLOW TRENDS

FIGURE 7 – CRANBERRY TOWNSHIP – EMPLOYMENT TRENDS BY RESIDENTS

SOURCE: LOCAL EMPLOYMENT DYNAMICS (2010-2015), CRANBERRY TOWNSHIP AND CONSULTANT CALCULATIONS *2016-2017 INFLOW/OUTFLOW: ASSUMES COMPOUNDED ANNUAL GROWTH RATE OF 2.08% BASED ON 5-YEAR COMMUTER TRENDS

17,706 19,321 20,220 21,485 20,453 19,623 20,031 20,737

-8,753 -8,421 -8,744 -8,648 -9,636 -9,802 -10,005 -10,213

-10,000

-5,000

0

5,000

10,000

15,000

20,000

25,000

2010 2011 2012 2013 2014 2015 2016 2017

Inflow/Outflow Patterns

Inflow Outflow Net Flow

0

1,000

2,000

3,000

4,000

5,000

2010 2011 2012 2013 2014 2015 2016 2017

Number of Residents Employed In Cranberry Township

SOURCE: LOCAL EMPLOYMENT DYNAMICS (2010-2015), CRANBERRY TOWNSHIP AND CONSULTANT CALCULATIONS

Calculation Notes: For the purpose of this analysis, compounded annual growth was determined using two data sets – U.S. Census Bureau, OnTheMap (2010-2015) and Cranberry Township’s NAICS Dataset (2017). The methodology

for data collection by each dataset varies, impacting the capacity for data integration.

19

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

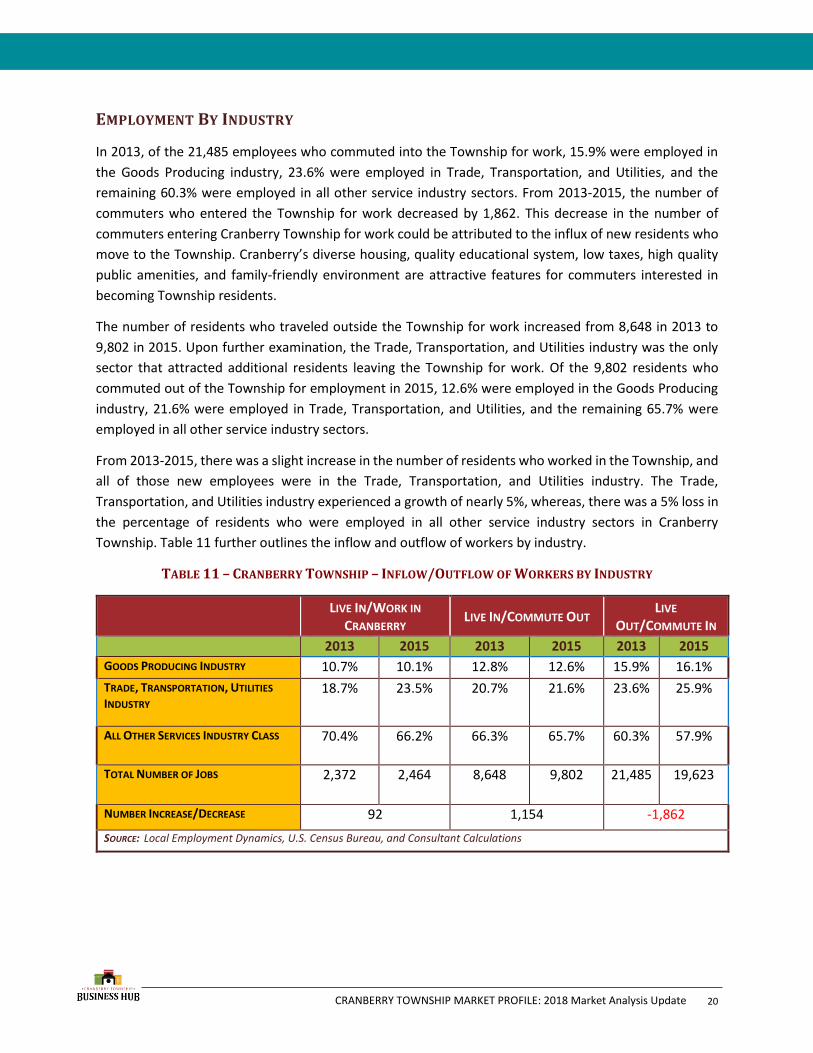

EMPLOYMENT BY INDUSTRY

In 2013, of the 21,485 employees who commuted into the Township for work, 15.9% were employed in

the Goods Producing industry, 23.6% were employed in Trade, Transportation, and Utilities, and the

remaining 60.3% were employed in all other service industry sectors. From 2013-2015, the number of

commuters who entered the Township for work decreased by 1,862. This decrease in the number of

commuters entering Cranberry Township for work could be attributed to the influx of new residents who

move to the Township. Cranberry’s diverse housing, quality educational system, low taxes, high quality

public amenities, and family-friendly environment are attractive features for commuters interested in

becoming Township residents.

The number of residents who traveled outside the Township for work increased from 8,648 in 2013 to

9,802 in 2015. Upon further examination, the Trade, Transportation, and Utilities industry was the only

sector that attracted additional residents leaving the Township for work. Of the 9,802 residents who

commuted out of the Township for employment in 2015, 12.6% were employed in the Goods Producing

industry, 21.6% were employed in Trade, Transportation, and Utilities, and the remaining 65.7% were

employed in all other service industry sectors.

From 2013-2015, there was a slight increase in the number of residents who worked in the Township, and

all of those new employees were in the Trade, Transportation, and Utilities industry. The Trade,

Transportation, and Utilities industry experienced a growth of nearly 5%, whereas, there was a 5% loss in

the percentage of residents who were employed in all other service industry sectors in Cranberry

Township. Table 11 further outlines the inflow and outflow of workers by industry.

TABLE 11 – CRANBERRY TOWNSHIP – INFLOW/OUTFLOW OF WORKERS BY INDUSTRY

LIVE IN/WORK IN

CRANBERRY LIVE IN/COMMUTE OUT

LIVE

OUT/COMMUTE IN

2013 2015 2013 2015 2013 2015

GOODS PRODUCING INDUSTRY 10.7% 10.1% 12.8% 12.6% 15.9% 16.1%

TRADE, TRANSPORTATION, UTILITIES

INDUSTRY 18.7% 23.5% 20.7% 21.6% 23.6% 25.9%

ALL OTHER SERVICES INDUSTRY CLASS 70.4% 66.2% 66.3% 65.7% 60.3% 57.9%

TOTAL NUMBER OF JOBS 2,372 2,464 8,648 9,802 21,485 19,623

NUMBER INCREASE/DECREASE 92 1,154 -1,862

SOURCE: Local Employment Dynamics, U.S. Census Bureau, and Consultant Calculations

20

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

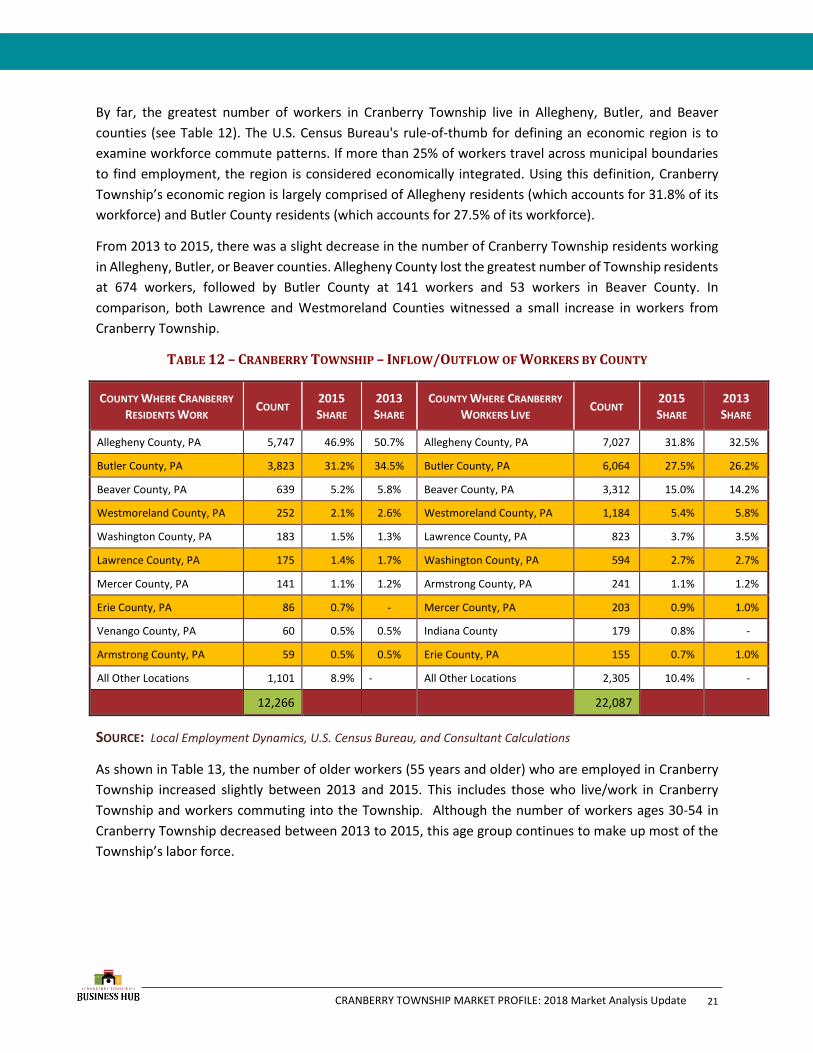

By far, the greatest number of workers in Cranberry Township live in Allegheny, Butler, and Beaver

counties (see Table 12). The U.S. Census Bureau's rule-of-thumb for defining an economic region is to

examine workforce commute patterns. If more than 25% of workers travel across municipal boundaries

to find employment, the region is considered economically integrated. Using this definition, Cranberry

Township’s economic region is largely comprised of Allegheny residents (which accounts for 31.8% of its

workforce) and Butler County residents (which accounts for 27.5% of its workforce).

From 2013 to 2015, there was a slight decrease in the number of Cranberry Township residents working

in Allegheny, Butler, or Beaver counties. Allegheny County lost the greatest number of Township residents

at 674 workers, followed by Butler County at 141 workers and 53 workers in Beaver County. In

comparison, both Lawrence and Westmoreland Counties witnessed a small increase in workers from

Cranberry Township.

TABLE 12 – CRANBERRY TOWNSHIP – INFLOW/OUTFLOW OF WORKERS BY COUNTY

COUNTY WHERE CRANBERRY

RESIDENTS WORK COUNT

2015 SHARE

2013

SHARE COUNTY WHERE CRANBERRY

WORKERS LIVE COUNT

2015 SHARE

2013

SHARE

Allegheny County, PA 5,747 46.9% 50.7% Allegheny County, PA 7,027 31.8% 32.5%

Butler County, PA 3,823 31.2% 34.5% Butler County, PA 6,064 27.5% 26.2%

Beaver County, PA 639 5.2% 5.8% Beaver County, PA 3,312 15.0% 14.2%

Westmoreland County, PA 252 2.1% 2.6% Westmoreland County, PA 1,184 5.4% 5.8%

Washington County, PA 183 1.5% 1.3% Lawrence County, PA 823 3.7% 3.5%

Lawrence County, PA 175 1.4% 1.7% Washington County, PA 594 2.7% 2.7%

Mercer County, PA 141 1.1% 1.2% Armstrong County, PA 241 1.1% 1.2%

Erie County, PA 86 0.7% - Mercer County, PA 203 0.9% 1.0%

Venango County, PA 60 0.5% 0.5% Indiana County 179 0.8% -

Armstrong County, PA 59 0.5% 0.5% Erie County, PA 155 0.7% 1.0%

All Other Locations 1,101 8.9% - All Other Locations 2,305 10.4% -

12,266 22,087

SOURCE: Local Employment Dynamics, U.S. Census Bureau, and Consultant Calculations

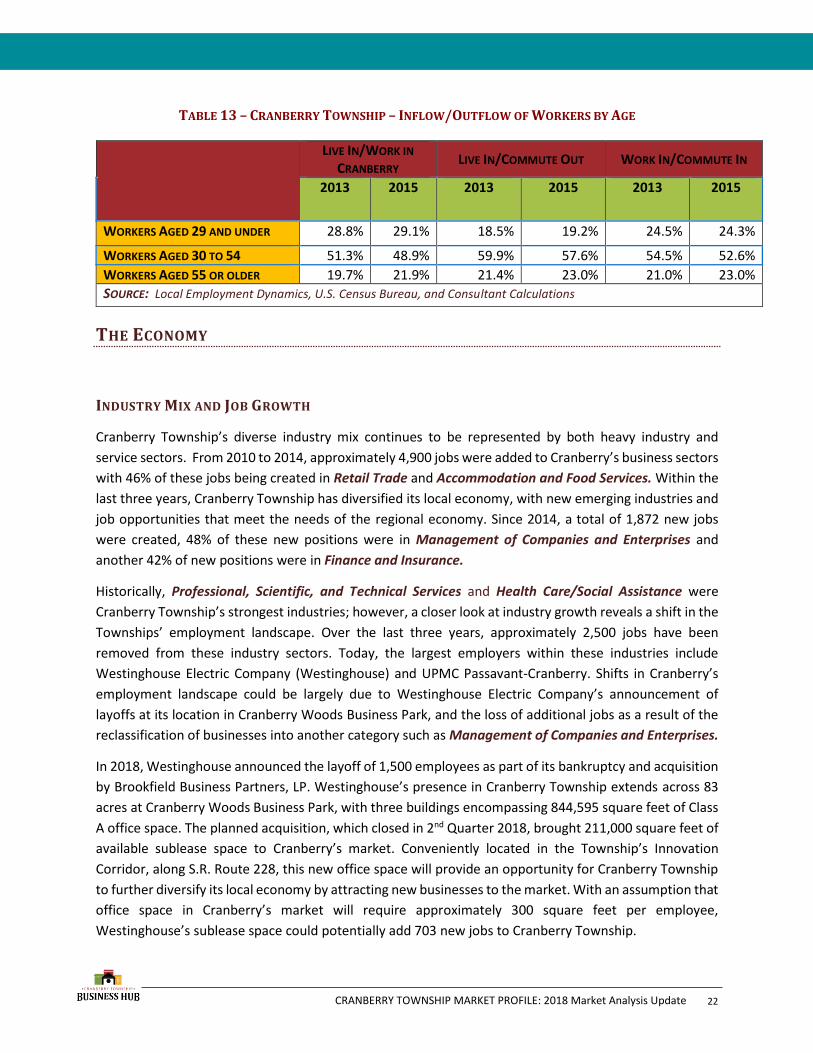

As shown in Table 13, the number of older workers (55 years and older) who are employed in Cranberry

Township increased slightly between 2013 and 2015. This includes those who live/work in Cranberry

Township and workers commuting into the Township. Although the number of workers ages 30-54 in

Cranberry Township decreased between 2013 to 2015, this age group continues to make up most of the

Township’s labor force.

21

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

TABLE 13 – CRANBERRY TOWNSHIP – INFLOW/OUTFLOW OF WORKERS BY AGE

LIVE IN/WORK IN

CRANBERRY LIVE IN/COMMUTE OUT WORK IN/COMMUTE IN

2013 2015 2013 2015 2013 2015

WORKERS AGED 29 AND UNDER 28.8% 29.1% 18.5% 19.2% 24.5% 24.3%

WORKERS AGED 30 TO 54 51.3% 48.9% 59.9% 57.6% 54.5% 52.6%

WORKERS AGED 55 OR OLDER 19.7% 21.9% 21.4% 23.0% 21.0% 23.0%

SOURCE: Local Employment Dynamics, U.S. Census Bureau, and Consultant Calculations

THE ECONOMY

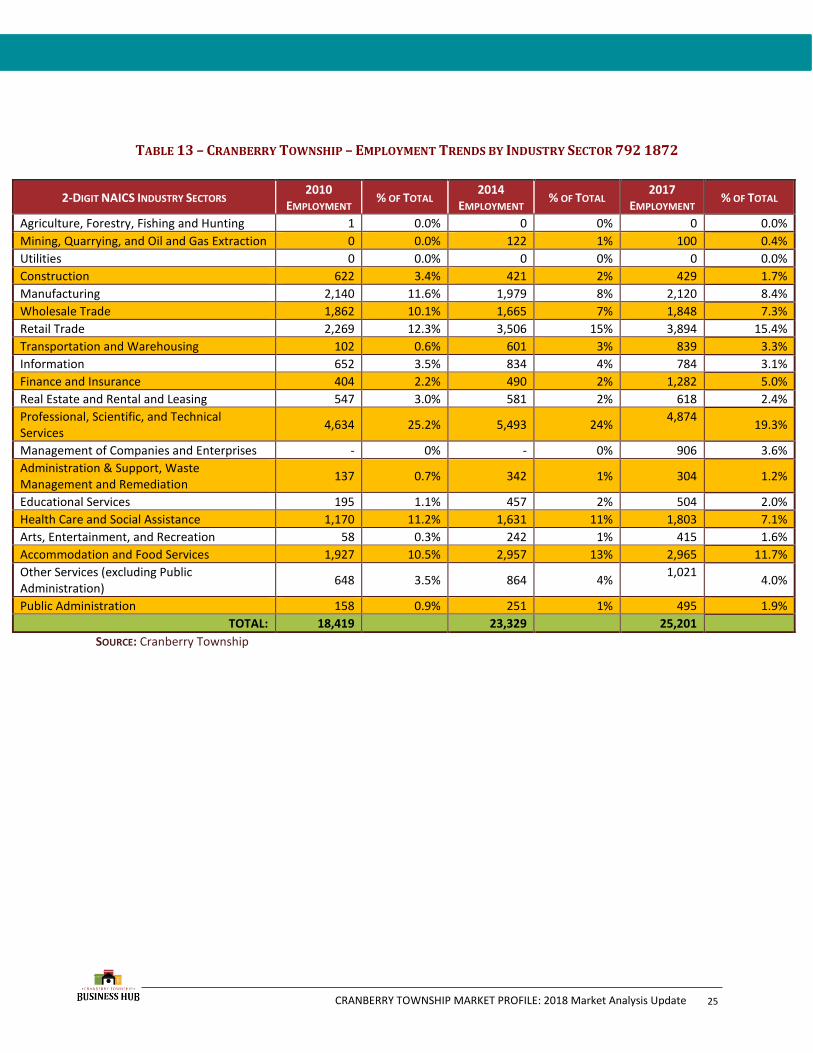

INDUSTRY MIX AND JOB GROWTH

Cranberry Township’s diverse industry mix continues to be represented by both heavy industry and

service sectors. From 2010 to 2014, approximately 4,900 jobs were added to Cranberry’s business sectors

with 46% of these jobs being created in Retail Trade and Accommodation and Food Services. Within the

last three years, Cranberry Township has diversified its local economy, with new emerging industries and

job opportunities that meet the needs of the regional economy. Since 2014, a total of 1,872 new jobs

were created, 48% of these new positions were in Management of Companies and Enterprises and

another 42% of new positions were in Finance and Insurance.

Historically, Professional, Scientific, and Technical Services and Health Care/Social Assistance were

Cranberry Township’s strongest industries; however, a closer look at industry growth reveals a shift in the

Townships’ employment landscape. Over the last three years, approximately 2,500 jobs have been

removed from these industry sectors. Today, the largest employers within these industries include

Westinghouse Electric Company (Westinghouse) and UPMC Passavant-Cranberry. Shifts in Cranberry’s

employment landscape could be largely due to Westinghouse Electric Company’s announcement of

layoffs at its location in Cranberry Woods Business Park, and the loss of additional jobs as a result of the

reclassification of businesses into another category such as Management of Companies and Enterprises.

In 2018, Westinghouse announced the layoff of 1,500 employees as part of its bankruptcy and acquisition

by Brookfield Business Partners, LP. Westinghouse’s presence in Cranberry Township extends across 83

acres at Cranberry Woods Business Park, with three buildings encompassing 844,595 square feet of Class

A office space. The planned acquisition, which closed in 2nd Quarter 2018, brought 211,000 square feet of

available sublease space to Cranberry’s market. Conveniently located in the Township’s Innovation

Corridor, along S.R. Route 228, this new office space will provide an opportunity for Cranberry Township

to further diversify its local economy by attracting new businesses to the market. With an assumption that

office space in Cranberry’s market will require approximately 300 square feet per employee,

Westinghouse’s sublease space could potentially add 703 new jobs to Cranberry Township.

22

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

The following are additional highlights of changes within the Township’s industry sectors during this same

period:

• A large gain in employment included the Management of Companies and Enterprises (906 jobs).

• Retail Trade added 338 jobs from 2014 to 2017; it represents the second largest share of jobs within

the Township (15%).

• Professional, Scientific, and Technical Services continues to provide the largest share of jobs within

the Township (19%).

• Transportation and Warehousing gained 238 new jobs from 2014 to 2017. This industry has

undergone rapid expansion in the last seven years with a total of 737 new positions. This significant

increase in activity, 238 jobs, could be a result of:

o E-commerce growth and increased number of competitors.

o

o Cranberry’s proximity to major market areas in the Mid-Atlantic region, and access to major

transportation and commercial shipping arteries.

• Healthcare and Social Assistance gained 172 jobs from 2014 to 2017; representing a 10.5% increase

in jobs. Cranberry Township’s job growth within this sector is nearly double the national growth rate

of 5.6%. 1

• Mining, Quarrying, and Oil and Gas Extraction Sectors lost 22 jobs from 2014 to 2017; however, this

sector could continue to expand within the next few years, based on the Marcellus Shale drilling

activities, and the proposed cracker plant in Beaver County.

1 Bureau of Labor Statistics, Employment, Hours, and Earnings from the Current Employment Statistics – All Employees Health Care and Social Assistance. 2008-2018.

23

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

FIGURE 7 – JOB GROWTH/LOSS BY INDUSTRY SECTOR IN CRANBERRY TOWNSHIP

SOURCE: Cranberry Township *SHIFTS IN THIS SECTOR COULD BE LARGELY ATTRIBUTED TO WESTINGHOUS ELECTRIC COMPANY’S ANNOUNCED LAYOFFS AT ITS LOCATION IN

CRANBERRY WOODS BUSINESS PARK. THE LOSS OF ADDITIONAL JOBS IS DUE TO THE RECLASSIFICATION OF BUSINESSES INTO OTHER INDUSTRY SECTORS SHOWN HERE.

-800 -600 -400 -200 0 200 400 600 800 1000

Agriculture, Forestry, Fishing and Hunting

Mining, Quarrying, and Oil and Gas Extraction

Utilities

Construction

Manufacturing

Whoelsale Trade

Retail Trade

Transportation and Warehousing

Information

Finance and Insurance

Real Estate and Rental and Leasing

Professional, Scientific, and Technical Services

Management of Companies and Enterprises

Administration & Support, Waste Management and Remediation

Educational Services

Health Care and Social Assistance

Arts, Entertainment, and Recreation

Accomoodation and Food Services

Other Services (excluding Public Administration)

Public Administration

Job Growth and Loss by Industry Sector 2014 to 2017

24

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

TABLE 13 – CRANBERRY TOWNSHIP – EMPLOYMENT TRENDS BY INDUSTRY SECTOR 792 1872

SOURCE: Cranberry Township

2-DIGIT NAICS INDUSTRY SECTORS 2010

EMPLOYMENT % OF TOTAL

2014

EMPLOYMENT % OF TOTAL

2017

EMPLOYMENT % OF TOTAL

Agriculture, Forestry, Fishing and Hunting 1 0.0% 0 0% 0 0.0%

Mining, Quarrying, and Oil and Gas Extraction 0 0.0% 122 1% 100 0.4%

Utilities 0 0.0% 0 0% 0 0.0%

Construction 622 3.4% 421 2% 429 1.7%

Manufacturing 2,140 11.6% 1,979 8% 2,120 8.4%

Wholesale Trade 1,862 10.1% 1,665 7% 1,848 7.3%

Retail Trade 2,269 12.3% 3,506 15% 3,894 15.4%

Transportation and Warehousing 102 0.6% 601 3% 839 3.3%

Information 652 3.5% 834 4% 784 3.1%

Finance and Insurance 404 2.2% 490 2% 1,282 5.0%

Real Estate and Rental and Leasing 547 3.0% 581 2% 618 2.4%

Professional, Scientific, and Technical Services

4,634 25.2% 5,493 24% 4,874

19.3%

Management of Companies and Enterprises - 0% - 0% 906 3.6%

Administration & Support, Waste Management and Remediation

137 0.7% 342 1% 304 1.2%

Educational Services 195 1.1% 457 2% 504 2.0%

Health Care and Social Assistance 1,170 11.2% 1,631 11% 1,803 7.1%

Arts, Entertainment, and Recreation 58 0.3% 242 1% 415 1.6%

Accommodation and Food Services 1,927 10.5% 2,957 13% 2,965 11.7%

Other Services (excluding Public Administration)

648 3.5% 864 4% 1,021

4.0%

Public Administration 158 0.9% 251 1% 495 1.9%

TOTAL: 18,419 23,329 25,201

25

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

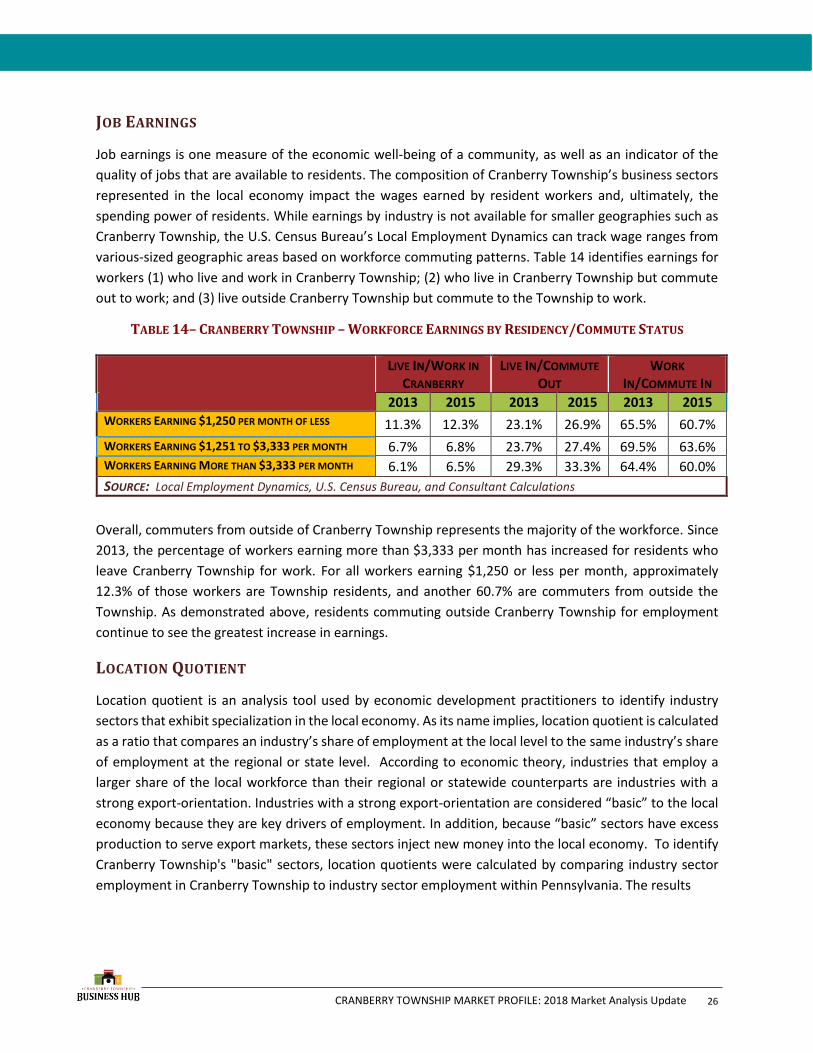

JOB EARNINGS

Job earnings is one measure of the economic well-being of a community, as well as an indicator of the

quality of jobs that are available to residents. The composition of Cranberry Township’s business sectors

represented in the local economy impact the wages earned by resident workers and, ultimately, the

spending power of residents. While earnings by industry is not available for smaller geographies such as

Cranberry Township, the U.S. Census Bureau’s Local Employment Dynamics can track wage ranges from

various-sized geographic areas based on workforce commuting patterns. Table 14 identifies earnings for

workers (1) who live and work in Cranberry Township; (2) who live in Cranberry Township but commute

out to work; and (3) live outside Cranberry Township but commute to the Township to work.

TABLE 14– CRANBERRY TOWNSHIP – WORKFORCE EARNINGS BY RESIDENCY/COMMUTE STATUS

LIVE IN/WORK IN

CRANBERRY LIVE IN/COMMUTE

OUT WORK

IN/COMMUTE IN

2013 2015 2013 2015 2013 2015 WORKERS EARNING $1,250 PER MONTH OF LESS 11.3% 12.3% 23.1% 26.9% 65.5% 60.7%

WORKERS EARNING $1,251 TO $3,333 PER MONTH 6.7% 6.8% 23.7% 27.4% 69.5% 63.6% WORKERS EARNING MORE THAN $3,333 PER MONTH 6.1% 6.5% 29.3% 33.3% 64.4% 60.0%

SOURCE: Local Employment Dynamics, U.S. Census Bureau, and Consultant Calculations

Overall, commuters from outside of Cranberry Township represents the majority of the workforce. Since

2013, the percentage of workers earning more than $3,333 per month has increased for residents who

leave Cranberry Township for work. For all workers earning $1,250 or less per month, approximately

12.3% of those workers are Township residents, and another 60.7% are commuters from outside the

Township. As demonstrated above, residents commuting outside Cranberry Township for employment

continue to see the greatest increase in earnings.

LOCATION QUOTIENT

Location quotient is an analysis tool used by economic development practitioners to identify industry

sectors that exhibit specialization in the local economy. As its name implies, location quotient is calculated

as a ratio that compares an industry’s share of employment at the local level to the same industry’s share

of employment at the regional or state level. According to economic theory, industries that employ a

larger share of the local workforce than their regional or statewide counterparts are industries with a

strong export-orientation. Industries with a strong export-orientation are considered “basic” to the local

economy because they are key drivers of employment. In addition, because “basic” sectors have excess

production to serve export markets, these sectors inject new money into the local economy. To identify

Cranberry Township's "basic" sectors, location quotients were calculated by comparing industry sector

employment in Cranberry Township to industry sector employment within Pennsylvania. The results

26

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

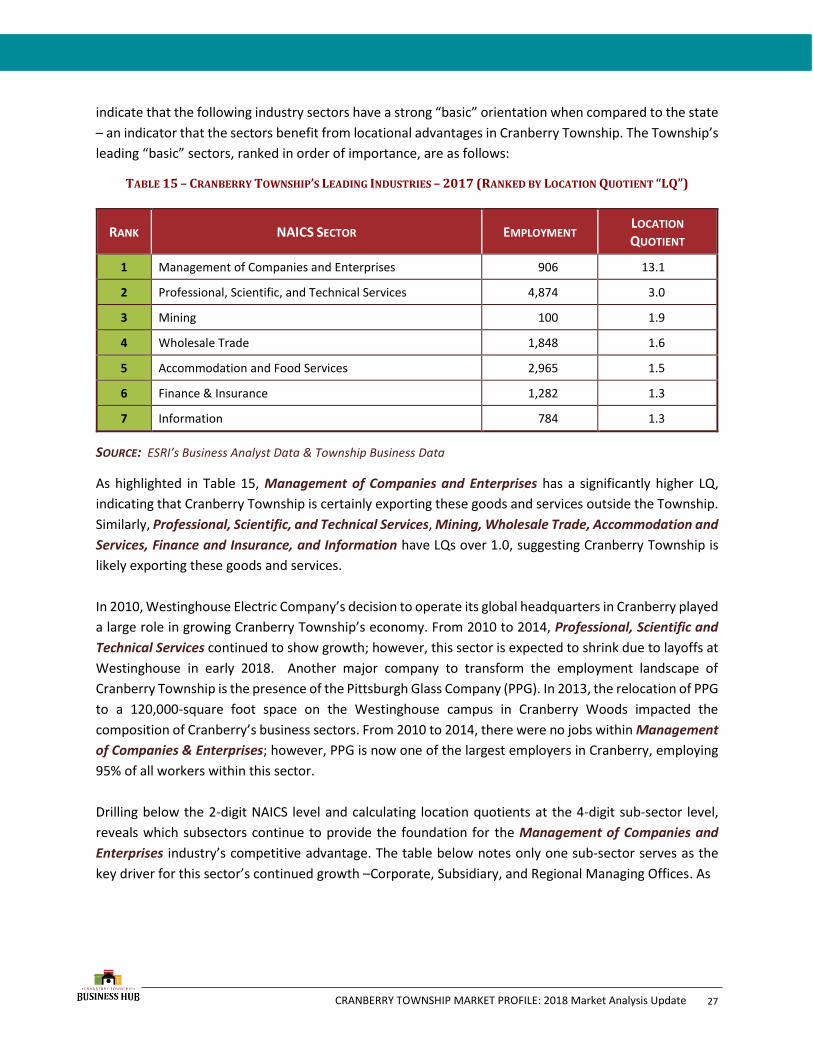

indicate that the following industry sectors have a strong “basic” orientation when compared to the state

– an indicator that the sectors benefit from locational advantages in Cranberry Township. The Township’s

leading “basic” sectors, ranked in order of importance, are as follows:

TABLE 15 – CRANBERRY TOWNSHIP’S LEADING INDUSTRIES – 2017 (RANKED BY LOCATION QUOTIENT “LQ”)

RANK NAICS SECTOR EMPLOYMENT LOCATION

QUOTIENT

1 Management of Companies and Enterprises 906 13.1

2 Professional, Scientific, and Technical Services 4,874 3.0

3 Mining 100 1.9

4 Wholesale Trade 1,848 1.6

5 Accommodation and Food Services 2,965 1.5

6 Finance & Insurance 1,282 1.3

7 Information 784 1.3

SOURCE: ESRI’s Business Analyst Data & Township Business Data

As highlighted in Table 15, Management of Companies and Enterprises has a significantly higher LQ,

indicating that Cranberry Township is certainly exporting these goods and services outside the Township.

Similarly, Professional, Scientific, and Technical Services, Mining, Wholesale Trade, Accommodation and

Services, Finance and Insurance, and Information have LQs over 1.0, suggesting Cranberry Township is

likely exporting these goods and services.

In 2010, Westinghouse Electric Company’s decision to operate its global headquarters in Cranberry played

a large role in growing Cranberry Township’s economy. From 2010 to 2014, Professional, Scientific and

Technical Services continued to show growth; however, this sector is expected to shrink due to layoffs at

Westinghouse in early 2018. Another major company to transform the employment landscape of

Cranberry Township is the presence of the Pittsburgh Glass Company (PPG). In 2013, the relocation of PPG

to a 120,000-square foot space on the Westinghouse campus in Cranberry Woods impacted the

composition of Cranberry’s business sectors. From 2010 to 2014, there were no jobs within Management

of Companies & Enterprises; however, PPG is now one of the largest employers in Cranberry, employing

95% of all workers within this sector.

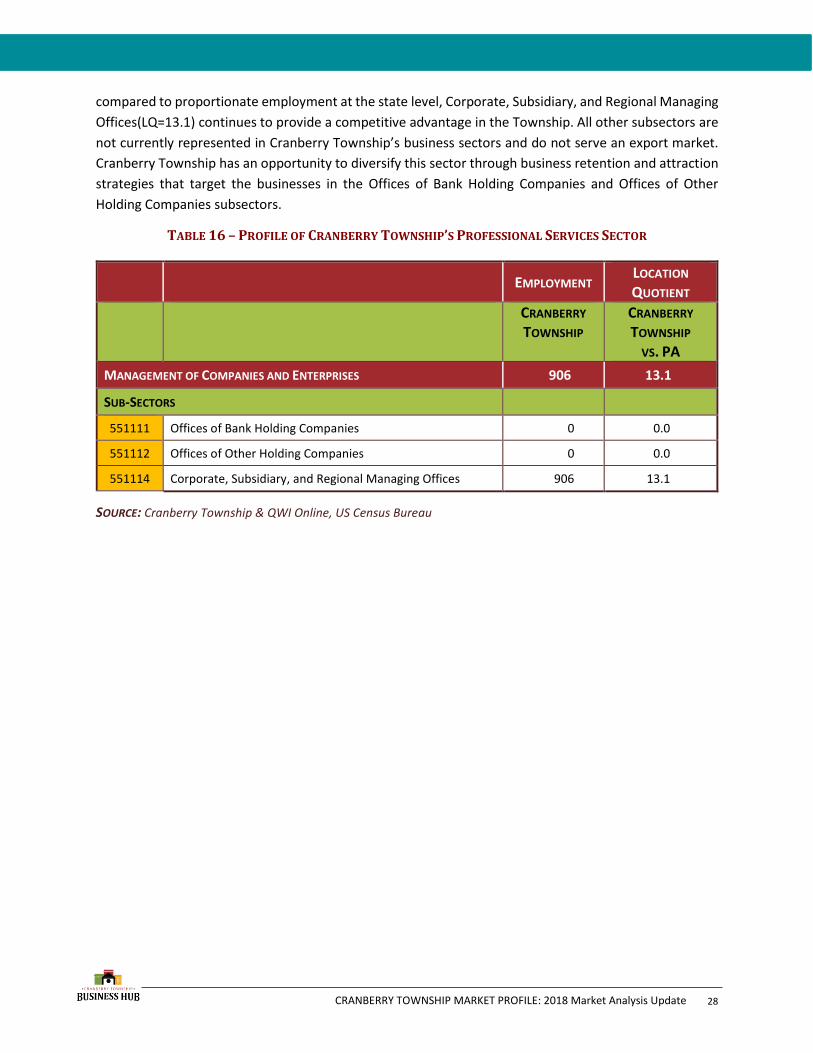

Drilling below the 2-digit NAICS level and calculating location quotients at the 4-digit sub-sector level,

reveals which subsectors continue to provide the foundation for the Management of Companies and

Enterprises industry’s competitive advantage. The table below notes only one sub-sector serves as the

key driver for this sector’s continued growth –Corporate, Subsidiary, and Regional Managing Offices. As

27

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

compared to proportionate employment at the state level, Corporate, Subsidiary, and Regional Managing

Offices(LQ=13.1) continues to provide a competitive advantage in the Township. All other subsectors are

not currently represented in Cranberry Township’s business sectors and do not serve an export market.

Cranberry Township has an opportunity to diversify this sector through business retention and attraction

strategies that target the businesses in the Offices of Bank Holding Companies and Offices of Other

Holding Companies subsectors.

TABLE 16 – PROFILE OF CRANBERRY TOWNSHIP’S PROFESSIONAL SERVICES SECTOR

EMPLOYMENT LOCATION

QUOTIENT CRANBERRY

TOWNSHIP CRANBERRY

TOWNSHIP VS. PA

MANAGEMENT OF COMPANIES AND ENTERPRISES 906 13.1

SUB-SECTORS

551111 Offices of Bank Holding Companies 0 0.0

551112 Offices of Other Holding Companies 0 0.0

551114 Corporate, Subsidiary, and Regional Managing Offices 906 13.1

SOURCE: Cranberry Township & QWI Online, US Census Bureau

28

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

TABLE 17– LOCATION QUOTIENTS BY INDUSTRY SECTOR (2017)

JOBS BY INDUSTRY TYPE (2-DIGIT NAICS) EMPLOYMENT LQ

AGRICULTURE, FORESTRY, FISHING AND HUNTING - 0.0

MINING 100 1.9

UTILITIES - 0.0

CONSTRUCTION 429 0.4

MANUFACTURING 2,120 0.9

WHOLESALE TRADE 1,848 1.6

RETAIL TRADE 3,894 1.2

TRANSPORTATION AND WAREHOUSING 839 0.8

INFORMATION 784 1.3

REAL ESTATE AND RENTAL AND LEASING 618 1.2

PROFESSIONAL, SCIENTIFIC, AND TECHNICAL SERVICES 4,874 3.0

MANAGEMENT OF COMPANIES AND ENTERPRISES 906 13.0

ADMINISTRATION & SUPPORT, WASTE MANAGEMENT AND REMEDIATION 304 0.5

EDUCATIONAL SERVICES 504 0.3

HEALTH CARE AND SOCIAL ASSISTANCE 1,803 0.4

ARTS, ENTERTAINMENT, AND RECREATION 415 0.9

ACCOMMODATION AND FOOD SERVICES 2,965 1.5

OTHER SERVICES (EXCLUDING PUBLIC ADMINISTRATION 1,021 0.7

PUBIC ADMINISTRATION 495 0.3

MANAGEMENT OF COMPANIES AND ENTERPRISES — 0.0

SOURCE: Cranberry Township, ESRI’s Business Analyst Data, and Consultant Calculations

29

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

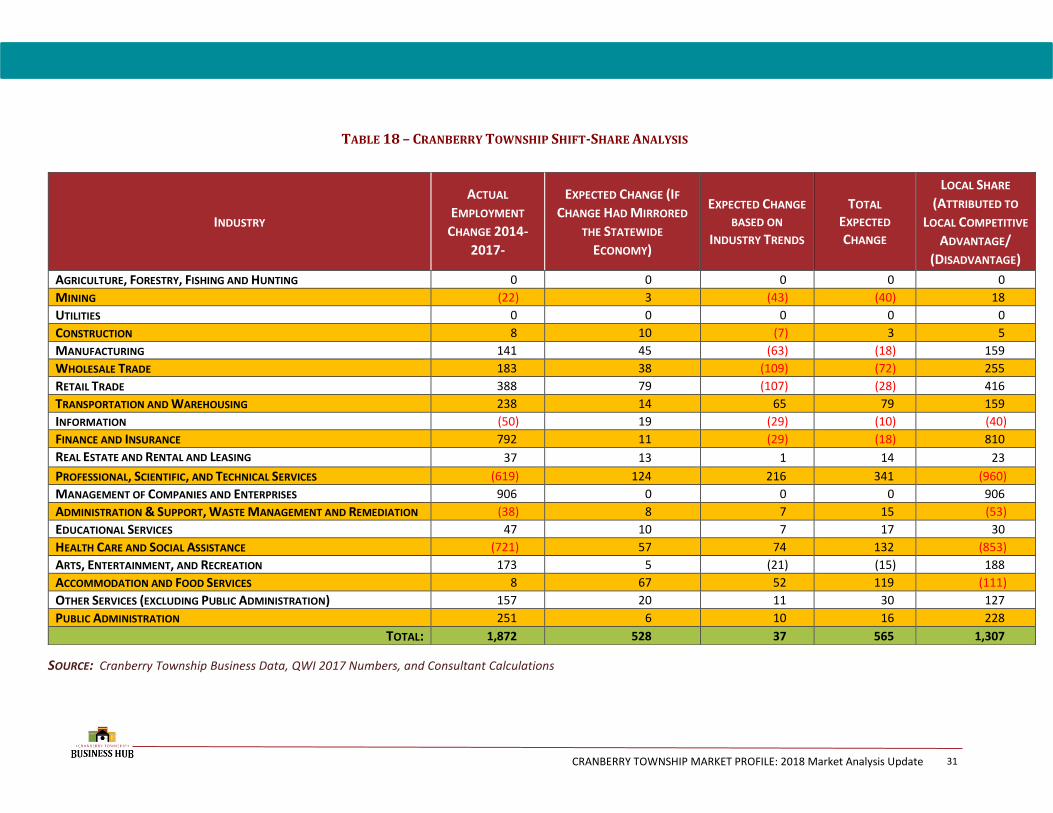

SHIFT-SHARE ANALYSIS

Building from the location quotient technique that establishes which local industries are key drivers of the

local economy, shift-share analysis begins to uncover the factors that influence an industry’s growth

trend. Shift-share analysis compares employment trends in the Township to employment changes in the

state to attribute employment growth and/or decline in any industry sector to three (3) components of

growth: state share, industry mix share, and local share. The analysis quantifies the “share” of

employment change that can be attributed to each component.

1. STATE SHARE – State share represents the number of jobs that would have been created (or lost)

in the Township had the local economy mirrored statewide trends.

2. INDUSTRY MIX SHARE – Industry mix share represents the number of jobs that would have been

created (or lost) in the Township had the local economy changed at the rate of the regional

economy and had individual industry employment mirrored regional trends.

3. LOCAL SHARE – Local share represents the number of jobs the Township may have gained because

local industry sectors outpaced their regional counterparts in terms of job creation. Local share

also estimates the number of jobs the Township may have lost because local industry sectors

could not keep pace with regional job growth. In shift-share analysis, industries are considered to

have local competitive advantage if their rate of job growth outpaces regional employment

growth in the same industry sector. Industries that have a strong local competitive advantage -

and are deemed “key drivers” of economic growth based on their location quotient – should be

central to a community's economic development strategy.

The results of the shift-share analysis for Cranberry Township are featured in Table 18. A positive number

under “local competitive advantage” indicates that local industry growth outpaced industry growth at the

regional level – a sign of competitive advantage. A negative number indicates that local conditions may

not support continued job growth because the local industry did not keep pace with regional industry

growth.

The results of the shift-share analysis show that of 1,872 new jobs created in Cranberry Township between

2014 and 2017, an estimated 28% (or 528), can be attributed to growth in the statewide economy, with

the remaining growth attributed to attractiveness factors specific to Cranberry Township.

Over this three-year period, the statewide economy posted 2.3% percent employment growth. In

contrast, the Township posted 8% growth in employment over the same period - far outpacing the

statewide trend. Sectors that recorded growth largely due to local attractiveness factors include

Management of Companies and Enterprises, Finance and Insurance, Retail Trade, and Wholesale Trade.

30

Pennsylvania 2018

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

TABLE 18 – CRANBERRY TOWNSHIP SHIFT-SHARE ANALYSIS

SOURCE: Cranberry Township Business Data, QWI 2017 Numbers, and Consultant Calculations

INDUSTRY

ACTUAL

EMPLOYMENT

CHANGE 2014-

2017-

EXPECTED CHANGE (IF

CHANGE HAD MIRRORED

THE STATEWIDE

ECONOMY)

EXPECTED CHANGE

BASED ON

INDUSTRY TRENDS

TOTAL

EXPECTED

CHANGE

LOCAL SHARE

(ATTRIBUTED TO

LOCAL COMPETITIVE

ADVANTAGE/

(DISADVANTAGE)

AGRICULTURE, FORESTRY, FISHING AND HUNTING 0 0 0 0 0

MINING (22) 3 (43) (40) 18

UTILITIES 0 0 0 0 0

CONSTRUCTION 8 10 (7) 3 5

MANUFACTURING 141 45 (63) (18) 159

WHOLESALE TRADE 183 38 (109) (72) 255

RETAIL TRADE 388 79 (107) (28) 416

TRANSPORTATION AND WAREHOUSING 238 14 65 79 159

INFORMATION (50) 19 (29) (10) (40)

FINANCE AND INSURANCE 792 11 (29) (18) 810

REAL ESTATE AND RENTAL AND LEASING 37 13 1 14 23

PROFESSIONAL, SCIENTIFIC, AND TECHNICAL SERVICES (619) 124 216 341 (960)

MANAGEMENT OF COMPANIES AND ENTERPRISES 906 0 0 0 906

ADMINISTRATION & SUPPORT, WASTE MANAGEMENT AND REMEDIATION (38) 8 7 15 (53)

EDUCATIONAL SERVICES 47 10 7 17 30

HEALTH CARE AND SOCIAL ASSISTANCE (721) 57 74 132 (853)

ARTS, ENTERTAINMENT, AND RECREATION 173 5 (21) (15) 188

ACCOMMODATION AND FOOD SERVICES 8 67 52 119 (111)

OTHER SERVICES (EXCLUDING PUBLIC ADMINISTRATION) 157 20 11 30 127

PUBLIC ADMINISTRATION 251 6 10 16 228

TOTAL: 1,872 528 37 565 1,307

31

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

THE RETAIL MARKET

To assess the retail market potential in Cranberry Township, five study areas were examined:

• Cranberry Township – was used as the base geography for measuring local retail sales.

• 5-Mile, 10-Mile, and 15-Mile Radii – represents the capture range identified by the

International Council of Shopping Centers for regional retail centers.

• Cranberry Draw Area – the most likely draw area for Cranberry Township as spatially

calculated using a gravity model that measures the likelihood that residents in surrounding areas

will drive to Cranberry to shop based on the distance they have to travel and the concentration

of retail options in the Township as compared to retail options in surrounding areas (see map on

following page).

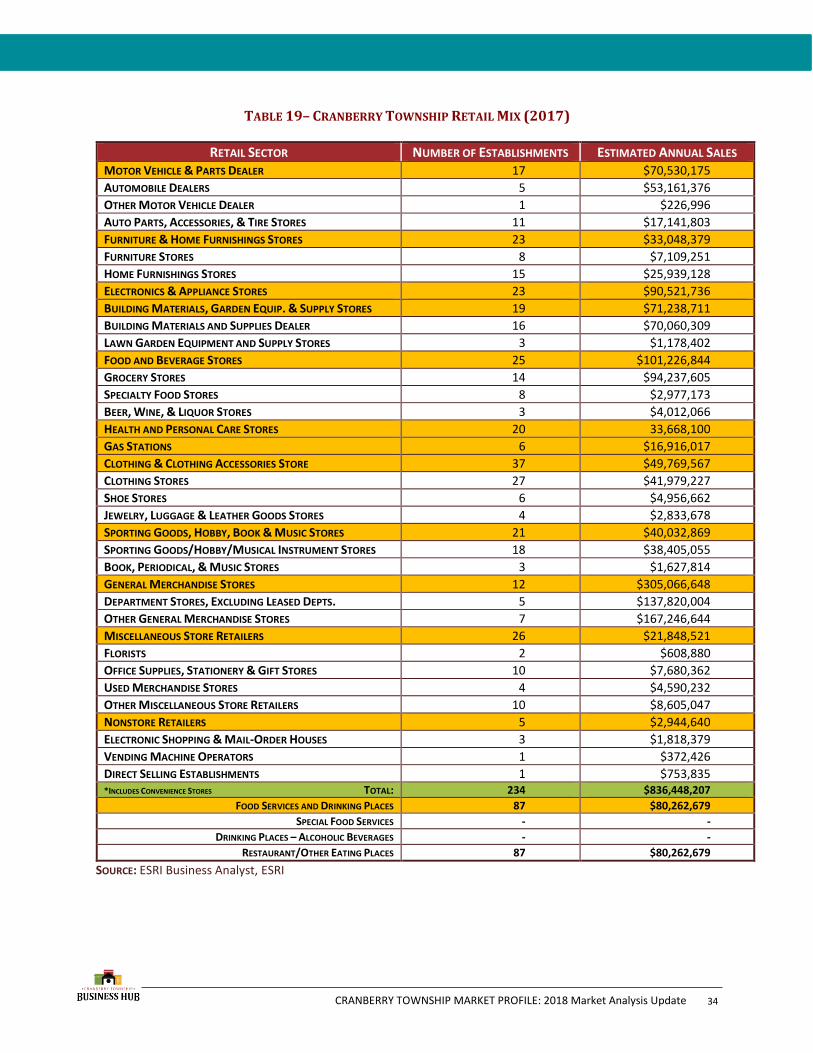

In 2017, there were 234 retail establishments in Cranberry Township with annual sales estimated at over

$836 million. In addition, there were 87 restaurants in the Township with annual sales estimated at over

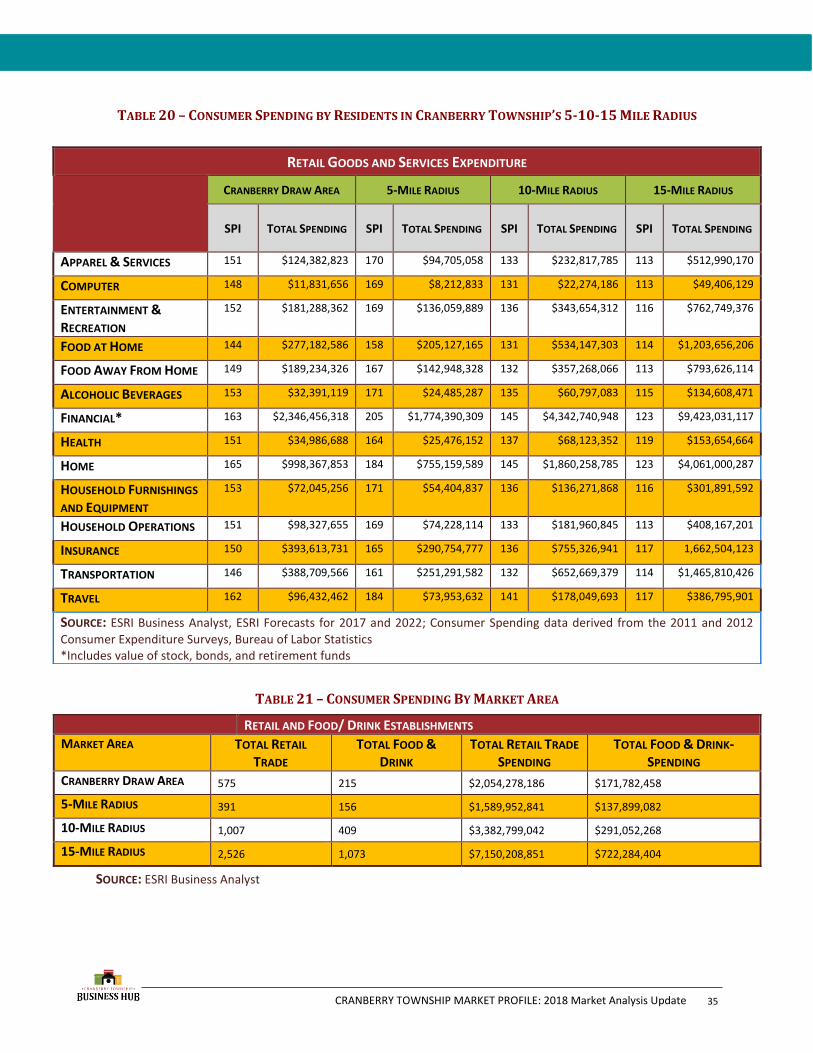

$80 million. Table 19 provides a snapshot of the distribution of those sales. Tables 20 -21 provide a

snapshot of the spending power of residents in the Cranberry Draw Area, as well as the 5-10-15 mile radii.

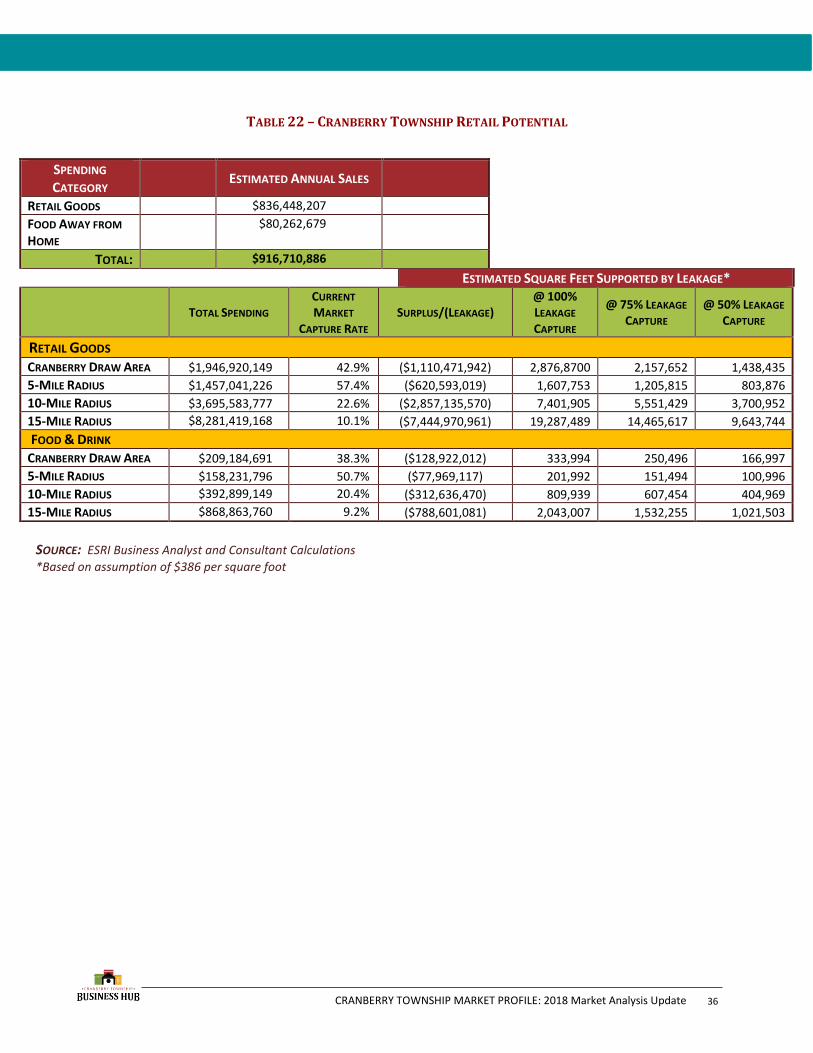

Table 22 provides a detailed overview of the estimated surplus and leakage of retail spending for each of

the above study areas comparing retail sales to spending in each area.

32

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

FIGURE 8 – THE RETAIL STUDY AREAS

33

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

TABLE 19– CRANBERRY TOWNSHIP RETAIL MIX (2017)

RETAIL SECTOR NUMBER OF ESTABLISHMENTS ESTIMATED ANNUAL SALES MOTOR VEHICLE & PARTS DEALER 17 $70,530,175

AUTOMOBILE DEALERS 5 $53,161,376

OTHER MOTOR VEHICLE DEALER 1 $226,996

AUTO PARTS, ACCESSORIES, & TIRE STORES 11 $17,141,803

FURNITURE & HOME FURNISHINGS STORES 23 $33,048,379

FURNITURE STORES 8 $7,109,251

HOME FURNISHINGS STORES 15 $25,939,128

ELECTRONICS & APPLIANCE STORES 23 $90,521,736

BUILDING MATERIALS, GARDEN EQUIP. & SUPPLY STORES 19 $71,238,711

BUILDING MATERIALS AND SUPPLIES DEALER 16 $70,060,309

LAWN GARDEN EQUIPMENT AND SUPPLY STORES 3 $1,178,402

FOOD AND BEVERAGE STORES 25 $101,226,844

GROCERY STORES 14 $94,237,605

SPECIALTY FOOD STORES 8 $2,977,173

BEER, WINE, & LIQUOR STORES 3 $4,012,066

HEALTH AND PERSONAL CARE STORES 20 33,668,100

GAS STATIONS 6 $16,916,017

CLOTHING & CLOTHING ACCESSORIES STORE 37 $49,769,567

CLOTHING STORES 27 $41,979,227

SHOE STORES 6 $4,956,662

JEWELRY, LUGGAGE & LEATHER GOODS STORES 4 $2,833,678

SPORTING GOODS, HOBBY, BOOK & MUSIC STORES 21 $40,032,869

SPORTING GOODS/HOBBY/MUSICAL INSTRUMENT STORES 18 $38,405,055

BOOK, PERIODICAL, & MUSIC STORES 3 $1,627,814

GENERAL MERCHANDISE STORES 12 $305,066,648

DEPARTMENT STORES, EXCLUDING LEASED DEPTS. 5 $137,820,004

OTHER GENERAL MERCHANDISE STORES 7 $167,246,644

MISCELLANEOUS STORE RETAILERS 26 $21,848,521

FLORISTS 2 $608,880

OFFICE SUPPLIES, STATIONERY & GIFT STORES 10 $7,680,362

USED MERCHANDISE STORES 4 $4,590,232

OTHER MISCELLANEOUS STORE RETAILERS 10 $8,605,047

NONSTORE RETAILERS 5 $2,944,640

ELECTRONIC SHOPPING & MAIL-ORDER HOUSES 3 $1,818,379

VENDING MACHINE OPERATORS 1 $372,426

DIRECT SELLING ESTABLISHMENTS 1 $753,835 *INCLUDES CONVENIENCE STORES TOTAL: 234 $836,448,207

FOOD SERVICES AND DRINKING PLACES 87 $80,262,679

SPECIAL FOOD SERVICES - -

DRINKING PLACES – ALCOHOLIC BEVERAGES - -

RESTAURANT/OTHER EATING PLACES 87 $80,262,679

SOURCE: ESRI Business Analyst, ESRI

34

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

TABLE 20 – CONSUMER SPENDING BY RESIDENTS IN CRANBERRY TOWNSHIP’S 5-10-15 MILE RADIUS

TABLE 21 – CONSUMER SPENDING BY MARKET AREA

SOURCE: ESRI Business Analyst

RETAIL GOODS AND SERVICES EXPENDITURE

CRANBERRY DRAW AREA 5-MILE RADIUS 10-MILE RADIUS 15-MILE RADIUS

SPI TOTAL SPENDING SPI TOTAL SPENDING SPI TOTAL SPENDING SPI TOTAL SPENDING

APPAREL & SERVICES 151 $124,382,823 170 $94,705,058 133 $232,817,785 113 $512,990,170

COMPUTER 148 $11,831,656 169 $8,212,833 131 $22,274,186 113 $49,406,129

ENTERTAINMENT &

RECREATION

152 $181,288,362 169 $136,059,889 136 $343,654,312 116 $762,749,376

FOOD AT HOME 144 $277,182,586 158 $205,127,165 131 $534,147,303 114 $1,203,656,206

FOOD AWAY FROM HOME 149 $189,234,326 167 $142,948,328 132 $357,268,066 113 $793,626,114

ALCOHOLIC BEVERAGES 153 $32,391,119 171 $24,485,287 135 $60,797,083 115 $134,608,471

FINANCIAL* 163 $2,346,456,318 205 $1,774,390,309 145 $4,342,740,948 123 $9,423,031,117

HEALTH 151 $34,986,688 164 $25,476,152 137 $68,123,352 119 $153,654,664

HOME 165 $998,367,853 184 $755,159,589 145 $1,860,258,785 123 $4,061,000,287

HOUSEHOLD FURNISHINGS

AND EQUIPMENT

153 $72,045,256 171 $54,404,837 136 $136,271,868 116 $301,891,592

HOUSEHOLD OPERATIONS 151 $98,327,655 169 $74,228,114 133 $181,960,845 113 $408,167,201

INSURANCE 150 $393,613,731 165 $290,754,777 136 $755,326,941 117 1,662,504,123

TRANSPORTATION 146 $388,709,566 161 $251,291,582 132 $652,669,379 114 $1,465,810,426

TRAVEL 162 $96,432,462 184 $73,953,632 141 $178,049,693 117 $386,795,901

SOURCE: ESRI Business Analyst, ESRI Forecasts for 2017 and 2022; Consumer Spending data derived from the 2011 and 2012

Consumer Expenditure Surveys, Bureau of Labor Statistics *Includes value of stock, bonds, and retirement funds

RETAIL AND FOOD/ DRINK ESTABLISHMENTS MARKET AREA TOTAL RETAIL

TRADE TOTAL FOOD &

DRINK TOTAL RETAIL TRADE

SPENDING TOTAL FOOD & DRINK-

SPENDING

CRANBERRY DRAW AREA 575 215 $2,054,278,186 $171,782,458

5-MILE RADIUS 391 156 $1,589,952,841 $137,899,082

10-MILE RADIUS 1,007 409 $3,382,799,042 $291,052,268

15-MILE RADIUS 2,526 1,073 $7,150,208,851 $722,284,404

35

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

TABLE 22 – CRANBERRY TOWNSHIP RETAIL POTENTIAL

SPENDING

CATEGORY ESTIMATED ANNUAL SALES

RETAIL GOODS $836,448,207

FOOD AWAY FROM

HOME

$80,262,679

TOTAL: $916,710,886

ESTIMATED SQUARE FEET SUPPORTED BY LEAKAGE*

TOTAL SPENDING CURRENT

MARKET

CAPTURE RATE SURPLUS/(LEAKAGE)

@ 100%

LEAKAGE

CAPTURE

@ 75% LEAKAGE

CAPTURE @ 50% LEAKAGE

CAPTURE

RETAIL GOODS CRANBERRY DRAW AREA $1,946,920,149 42.9% ($1,110,471,942) 2,876,8700 2,157,652 1,438,435

5-MILE RADIUS $1,457,041,226 57.4% ($620,593,019) 1,607,753 1,205,815 803,876

10-MILE RADIUS $3,695,583,777 22.6% ($2,857,135,570) 7,401,905 5,551,429 3,700,952

15-MILE RADIUS $8,281,419,168 10.1% ($7,444,970,961) 19,287,489 14,465,617 9,643,744

FOOD & DRINK CRANBERRY DRAW AREA $209,184,691 38.3% ($128,922,012) 333,994 250,496 166,997

5-MILE RADIUS $158,231,796 50.7% ($77,969,117) 201,992 151,494 100,996

10-MILE RADIUS $392,899,149 20.4% ($312,636,470) 809,939 607,454 404,969

15-MILE RADIUS $868,863,760 9.2% ($788,601,081) 2,043,007 1,532,255 1,021,503

SOURCE: ESRI Business Analyst and Consultant Calculations

*Based on assumption of $386 per square foot

36

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

Cranberry Township retail establishments currently capture around 43% of consumer spending within the

Cranberry Draw Area. Assuming that the Cranberry Draw Area is the primary market area for the

Township, the Township could potentially support an additional 1,438,435 square feet of retail space if it

captured 50% of the current estimated leakage. Given the same assumptions, the Township could

potentially support an additional 166, 997 feet of restaurant space.

Within a 10-mile radius, the township’s retail establishments capture around 23% of consumer spending.

While there is an estimated leakage of $3 billion in consumer spending within a 10-mile radius of

Cranberry Township, a significant portion of the

leakage is likely attributed to consumers in the

southern portion of the radius, as illustrated in

Figure 9. The proximity of these consumers to

retail amenities in the northern portion of the

Pittsburgh metropolitan area means stiff

competition for retail establishments in Cranberry

Township.

Sales estimates in Table 22 reflect all sales by local

establishments; however, the surplus/leakage

estimates include household spending only and

are not reflective of the spending of the 19,623

workers who commute to Cranberry Township to

work each day. To put this in perspective, if half of

those workers spend $30 per week in Cranberry

Township, that spending could support as much as

39,650 square feet of additional space (see Table

23).

It should be noted that the estimates of retail

potential are based solely on statistical calculations

and do not take into consideration other variable

factors such as the age and curb appeal of competitive retail centers, the curb appeal of new development,

changes in the economy and spending, and marketing, etc.

FIGURE 9 – DISTRIBUTION OF HOUSEHOLDS

37

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

TABLE 23- COMMUTER SPENDING POTENTIAL

MARKET POTENTIAL BY COMMUTERS

TOTAL COMMUTERS (2015) 19,623

50% CAPTURE RATE 9,811

AVG. WEEKLY EXPENDITURE $30.00

TOTAL SPENDING POTENTIAL $15,305,160

COST PER SQUARE FOOTAGE $386.00

SQUARE FOOTAGE SUPPORTED BY COMMUTERS 39,650 SQ. FT.

SOURCE: Consultant Calculations

THE COMMERCIAL MARKET

The commercial real estate market includes offices, retail centers, hotels, and other properties used for

business purposes. As stated in the previous 2012

Market Analysis Update, the 2008 economic

downturn impacted the commercial real estate

market forcing many businesses to downsize or close

their doors. New construction was sluggish due to

lending restrictions imposed by federal regulators. As

of 2012, the commercial real estate market had begun

to stabilize due to the limited supply, and growth in

the economy. One indicator of the health of the

commercial real estate market is the real estate index

published by The Society of Industrial and Office

Realtors (SIOR). The index is based on a survey of SIOR

members, which are asked to characterize the

strength or weakness of property markets across 10

major categories, including recent leasing activity,

trends in asking rents, trends in vacancy rates,

concession packages, site acquisition activity, and

development activity. An SIOR index value of 100

represents a well-balanced market for industrial and office property. An index value significantly lower

than 100 indicates weak market conditions.

During the 4th Quarter of 2017, the SIOR Commercial Real Estate Index (CREI) grew 3.2 points from the

previous quarter, achieving an office index of 113.8. This steady increase can be attributed to the

construction of new office and industrial spaces, which are projected to reach the historical average for

new building development. Private service-oriented industries, similar to many of the business sectors

SOURCE: Grubb & Ellis

FIGURE 10 – OFFICE SUBMARKETS

38

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

represented in Cranberry’s local economy, provided the majority of new positions in 2017 including

101,000 new professional and business service positions; 99,100 health care and social assistance

opportunities; and 24,000 new positions in financial services throughout the United States.

Similarly, the industrial index rose to 136.3 during the 4th quarter of 2017, representing a 3.5%gain year-

over-year. The increased demand for industrial space is a result of international trade and on-line

shopping, which is diverting space from retail centers to warehouses. The industrial index has hovered

over the 100-point value for the past 13 months indicating the strong demand for industrial space.

The commercial real estate advisory firm Newmark Grubb Knight Frank reports that the Pittsburgh Region

was one of the 10 cities with the highest percentage of new jobs in occupations that pay a living-wage.

This information was obtained from a study completed by CareerBuilder.com. Within the Pittsburgh

Region, office vacancy during the 4th quarter of 2017 was 16.9%. In comparison, the vacancy rate for

Pittsburgh’s Industrial Market was 7.9% during this same period. The Northern Submarket was slightly

lower at 15.1% vacancy. In the 4th quarter of 2017, Cranberry Township reported a 3.2% unemployment

rate compared to 4.8% in Pennsylvania and 4.1% nationwide. The prominence of three (3) primary sectors

– health care, education, and energy – continue to stabilize metropolitan Pittsburgh’s labor market and

fuel demand for Class A office space.

In 4th quarter of 2016, asking rent for Class A office space in the North Suburbs, a suburban submarket of

Pittsburgh that includes Cranberry Township, was $24.82 per square foot. By the end of the 4th quarter of

2017, asking rent increased to $25.26. During this same time, the asking rent for Class B commercial office

space increased from $19.56 per square foot to 20.63 per square foot.

TABLE 24 - TRENDS FOR PITTSBURGH OFFICE MARKET – 4TH QUARTER 2017

TRENDS FOR PITTSBURGH OFFICE MARKET 4TH QUARTER 2017

ASKING RENT (PRICE/SF)

SUBMARKETS TOTAL INVENTORY

SF VACANT %

NET ABSORPTION

YTD CLASS A CLASS B

CBD 20,293,397 14.5% 260,809 $29.73 $21.70

Fringe 6,499,416 19.2% -52,025 $26.76 $23.30

CBD/FRINGE

TOTAL: 26,792,813 15.6% 208,784 $29.54 $22.53

East 3,164,785 24.6% 39,232 $22.79 $16.67

North 7,486,361 15.1% -248,681 $25.26 $20.47

Oakland/East End

2,490,689 4.0% 47,411 $29.66 $20.63

Parkway West 8,656,709 21.9% 159,383 $23.57 $19.79

South 5,420,408 19.0% 35,670 $22.75 $18.54

SUBURBAN TOTAL: 27,218,952 18.1% -196,324 $23.68 $19.06

PITTSBURGH 54,011,765 16.9% 218,156 $25.88 $21.14

SOURCE: Pittsburgh 4Q17 Office Market – Newmark Grubb Knight Frank Research

39

CRANBERRY TOWNSHIP MARKET PROFILE: 2018 Market Analysis Update

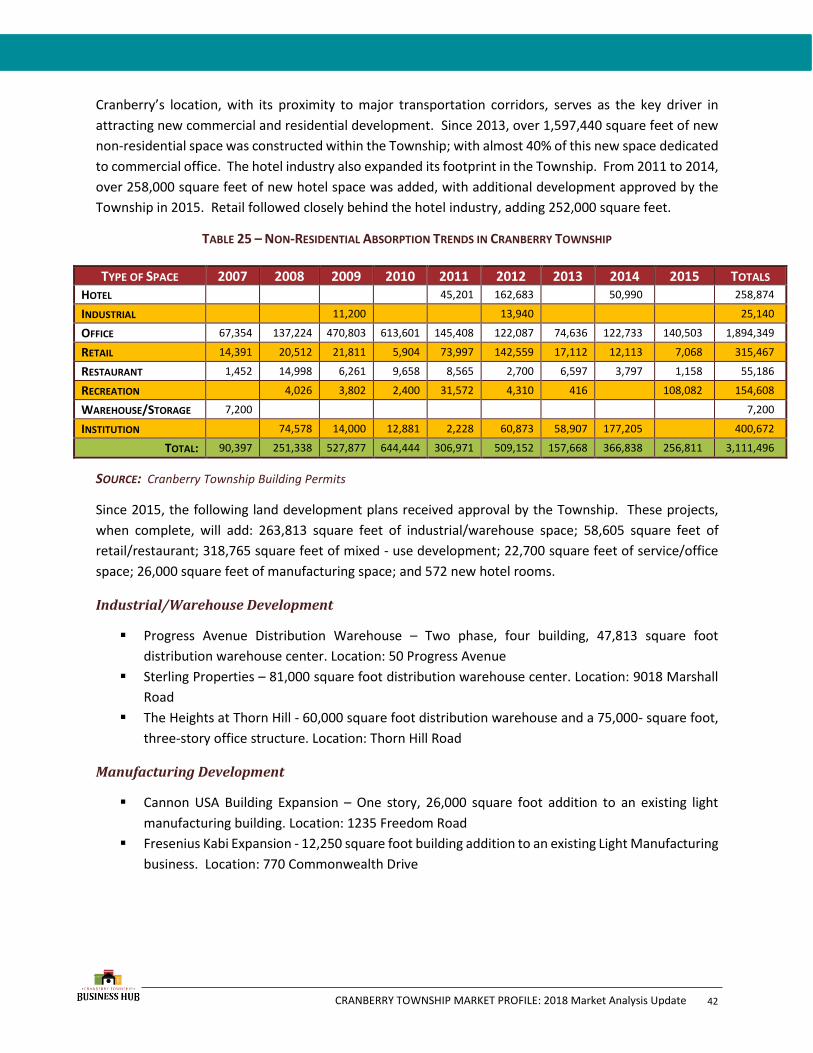

While lease rates speak indirectly to the balance between supply and demand, net absorption provides a

more informative snapshot of health within any real estate market. Fundamentally, net absorption

measures the change in occupied square footage over a period of time. Net absorption can be either

positive or negative, depending upon the pace of leasing activity and new construction. Positive net

absorption occurs when space has been taken off the market (i.e. through new leases and lease renewals)

at a faster pace than square footage has been added to the market through new construction or lease

terminations. In this scenario, demand exceeds supply, which pushes vacancy rates down and asking rents

up. In contrast, negative net absorption occurs when more square footage has been added to the market

than is absorbed through leasing activity. In this scenario, supply exceeds demand, which pushes vacancy

rates up and places downward pressure on asking rents.

The Newmark Grubb Knight Frank Office Trends Report referenced for this market assessment update

calculates net absorption based on physical occupancies and vacancies – i.e. when a tenant moves in or

out of a given space. Given the lag time that can exist between leasing transactions and physical

occupancy/vacancy, net absorption for the 4th quarter 2017 (as reflected in Table 24) may speak more to

market demand in the previous three quarters. The table shows year to date (YTD) net absorption for the

Pittsburgh CBD and suburbs. During the 4th quarter of 2017, the CBD’s net absorption was 260,809 square

feet, which indicates a period of steady demand for leasing activity. During this same quarter, the

suburban market overall was also active, except for the North submarket. Included in this North

submarket is Westinghouse Electric Company, which placed 315,000 square feet of sublease space into

the market.

The North Suburbs, which includes Cranberry Township, had a negative YTD net absorption of 248,681