2018 roadshow presentation...of legislative decree february 24, 1998, no. 58, declares that, to the...

TRANSCRIPT

2018Roadshow Presentation

Roadshow Presentation - September 20182

These statements are related, among others, to the intent, belief or current expectations of the customer base, estimates regarding future growth in the different business lines and the global business, market share, financial results and other aspects of the activities and situation relating to the Company.

Such forward-looking statements are not guarantees of future performance and involve risks and uncertainties, and actual results may differ materially from those expressed in or implied by these forward-looking statements as a result of various factors, many of which are beyond the ability of DiaSorin S.p.A. to control or estimate precisely.The Company does not undertake to update or otherwise revise any forecasts or objectives presented herein, except in compliance with the disclosure obligations applicable to companies whose shares are listed on a stock exchange.

Piergiorgio Pedron, the Officer Responsible for the preparation of corporate financial reports of DiaSorin S.p.A., in accordance with the second subsection of art. 154-bis, part IV, title III, second paragraph, section V-bis, of Legislative Decree February 24, 1998, no. 58, declares that, to the best of his knowledge, the financial information included in the present document corresponds to book of accounts and book-keeping entries of the Company.

Disclaimer

Roadshow Presentation - September 20183

We operate in two IVD segments

26%ONCOLOGY & ENDOCRINOLOGY

3%DRUG MONITORING 6%

ALLERGY

7%AUTOIMMUNITY

7%BONE & MINERAL

15%CARDIAC MARKERS

5%GI STOOL TESTING

13%INFECTIOUS DISEASES

18%HEPATITIS & RETROVIRUS

57%INFECTIOUS DISEASES

3%INHERITED DISEASES

5%TRANSPLANT

9%CANCER

11%HISTOLOGY

15%BLOOD SCREENING

Immunodiagnostics: ~ 18% of IVD market Molecular Diagnostics: ~ 12% of IVD market

Roadshow Presentation - September 20184

Where we are

Roadshow Presentation - September 20185

Revenues and EBITDA

434 435 444

499

569

637

775

170 163 160 185

217 238

300

2012 2013 2014 2015 2016 2017 2019*

Revenues EBITDA * 2019 Company Guidance

Data in €/mln

Roadshow Presentation - September 2018

Immunodiagnostics

Roadshow Presentation - September 20187

Area ofopportunity

ME

NU

AUTOMATION

SIGNAL TECHNOLOGY

RIA

ELISA

RIA

BENCH-TOPSOLUTIONS

(~ 200 ASSAYS)

FIRST AUTOMATEDSYSTEMS

FULLY AUTOMATEDSYSTEMS

FULL CONNECTIVITY(Immuno+Clinical Chemistry)

CLIA

Immunoassay innovation: 1970-2016

Roadshow Presentation - September 20188

LIAISON family platforms

Magnetic particles

CalibratorsDiluent

Each test hasits specific cartridge

100 samples for each cartridge

Same raw materialfor routine and specialty tests

New in 2019

LAS

Roadshow Presentation - September 20189

Installed base evolution

LAS

2009 2010 2011 2012 2013 2014 2015 2016 2017

3,641 4,078 4,135 4,197 4,207 4,044 3,880

128 605 1,075 1,665

2,292 3,518

+682 +437 +57 +62 +10 -163

+128 +477 +470 +590 +627

2,959

3,641

4,206 4,740

5,272 5,872

6,336

7,398

3,999

2,863

6,862

+571

-45 -119

+655

Roadshow Presentation - September 201810

Men

u

ONCOLOGY

TUMOUR MARKERS

CEA

Free PSA

Total PSA

CA 15-3

CA 125 II

CA 19-9

TPA-M

NSE

S100

AFP

Tg

Tg Gen II(*)

hCG/ß-hCG

ß2-Microglobulin

TK

Calcitonin

ENDOCRINOLOGY

THYROID

TSH (3rd Gen.)

Free T3

Free T4

T3

T4

Tg

Tg Gen II(*)

Anti-Tg

Anti-TPO

GROWTHhGHIGF-I

ADRENAL FUNCTIONACTHCortisolDHEA-S

ANAEMIAFerritinFolate(*)Vitamin B12(*)

DIABETESC-PeptideInsulin

REPRODUCTIVE

ENDOCRINOLOGY

LH

FSH

Prolactin

Progesterone

Testosterone

Estradiol

hCG/ß-hCG

Androstenedione

SHBG

BONE & MINERAL

25-OH Vitamin D TOTAL

N-TACT PTH II

Menu positioning: 118 tests - the broadest CLIA menu

Men

u

INFECTIOUS DISEASE

EBV

EBV IgM

VCA IgG

EBNA IgG

EA IgG

H.PYLORI

H. Pylori IgG

TREPONEMA

Treponema Screen

SEPSIS

BRAHMS PCT II Gen

TORCH

Toxo IgG

Toxo IgM

Toxo IgG Avidity

Rubella IgG

Rubella IgM

CMV IgG

CMV IgM

CMV IgG Avidity

HSV-1/2 IgG

HSV-1 IgG

HSV-2 IgG

HSV-1/2 IgM

BORRELIA

Borrelia burgdorferi IgG

Borrelia burgdorferi IgM

MEASLES & MUMPS

Measles IgG

Measles IgM

Mumps IgG

Mumps IgM

VZV

VZV IgG

VZV IgM

VIRAL HEPATITIS

& RETROVIRUSES

HBsAg

HBsAg Quant

HBsAg Confirmatory test

Anti- HBs

Anti- HBs plus

Anti- HBc

HBc IgM

HBeAg

Anti-HBe

Anti-HAV

HAV IgM

HCV Ab

HIV Ab/Ag

HT HTLV I/II

CHAGAS

Chagas IgG

Men

u

STOOL DIAGNOSTICS

C. difficile GDH

C. difficile Toxin A and B

H. pylori SA

EHEC

Rotavirus

Adenovirus

Calprotectin

Campylobacter

INFECTIOUS DISEASE

Zika IgM

PARVOVIRUS

Parvovirus B19 IgG

Parvovirus B19 IgM

BORDETELLA

Bordetella pertussis

Toxin IgG

Bordetella pertussis

Toxin IgA

MYCOPLASMA

Mycoplasma pneumoniae

IgG

Mycoplasma pneumoniae

IgM

CHLAMYDIA

Chlamydia T. IgG

Chlamydia T. IgA

QuantiFERON

QuantiFERON TB Gold

Plus (*)

CHRONIC KIDNEY

DISEASE

1-84 PTH

Osteocalcin

BAP OSTASE

1,25 dihydroxy Vitamin D

ENDOCRINOLOGY

HYPERTENSION

Direct Renin

Aldosterone

VIRAL HEPATITIS

& RETROVIRUSES

Anti-HDV

Men

u

CHRONIC KIDNEY DISEASES

FGF-23

Ratio (Vitamin D 1,25-PTH 1,84)

Sclerostin (*)

* Under development

Roadshow Presentation - September 201811

Menu positioning: 118 tests - the broadest CLIA menuM

enu

ONCOLOGY

TUMOUR MARKERS

CEA

Free PSA

Total PSA

CA 15-3

CA 125 II

CA 19-9

TPA-M

NSE

S100

AFP

Tg

Tg Gen II

hCG/ß-hCG

ß2-Microglobulin

TK

Calcitonin

ENDOCRINOLOGY

THYROID

TSH (3rd Gen.)

Free T3

Free T4

T3

T4

Tg

Tg Gen II

Anti-Tg

Anti-TPO

GROWTH

hGH

IGF-I

ADRENAL FUNCTION

ACTH

Cortisol

DHEA-S

ANAEMIA

Ferritin

DIABETES

C-Peptide

Insulin

REPRODUCTIVE ENDO-

CRINOLOGY

LH

FSH

Prolactin Progesterone

Testosterone

Estradiol

hCG/ß-hCG

Androstenedione

SHBG

BONE & MINERAL

25-OH Vitamin D TOTAL

N-TACT PTH II

Men

u

INFECTIOUS DISEASE

EBV

EBV IgM

VCA IgG

EBNA IgG

EA IgG

H.PYLORI

H. Pylori IgG

TREPONEMA

Treponema Screen

SEPSIS

BRAHMS PCT II Gen

TORCH

Toxo IgG

Toxo IgM

Toxo IgG Avidity

Rubella IgG

Rubella IgM

CMV IgG

CMV IgM

CMV IgG Avidity

HSV-1/2 IgG

HSV-1 IgG

HSV-2 IgG

HSV-1/2 IgM

BORRELIA

Borrelia burgdorferi IgG

Borrelia burgdorferi IgM

MEASLES & MUMPS

Measles IgG

Measles IgM

Mumps IgG

Mumps IgM

VZV

VZV IgG

VZV IgM

VIRAL HEPATITIS

& RETROVIRUSES

HBsAg

HBsAg Quant

HBsAg Confirmatory test

Anti- HBs II

Anti- HBs II plus

Anti- HBc

HBc IgM

HBeAg

Anti-HBe

Anti-HAV

HAV IgM

HCV Ab

HIV Ab/Ag

HT HTLV I/II

CHAGAS

Chagas IgG

Men

u

STOOL DIAGNOSTICS

C. difficile GDH

C. difficile Toxin A and B

H. pylori SA

EHEC

Rotavirus

Adenovirus

Calprotectin

Campylobacter

INFECTIOUS DISEASE

Zika IgM

PARVOVIRUS

Parvovirus B19 IgG

Parvovirus B19 IgM

BORDETELLA

Bordetella pertussis

Toxin IgG

Bordetella pertussis

Toxin IgA

MYCOPLASMA

Mycoplasma pneumoniae

IgG

Mycoplasma pneumoniae

IgM

CHLAMYDIA

Chlamydia T. IgG

Chlamydia T. IgA

CHRONIC KIDNEY

DISEASE

1-84 PTH

Osteocalcin

BAP OSTASE

1,25 dihydroxy Vitamin D

ENDOCRINOLOGY

HYPERTENSION

Direct Renin

Aldosterone

VIRAL HEPATITIS

& RETROVIRUSES

Anti-HDV

Men

u

CHRONIC KIDNEY DISEASES

FGF-23

Ratio (Vitamin D 1,25-PTH 1,84)

Sclerostin (*)

Vitamin K (*)

* Under development

Me too tests

#46

Differentiating specialties

#28Investigational markers

#2

High volume specialties

#42

Roadshow Presentation - September 201812

Where we plan to invest R&D money

Differentiating specialties Me too testsHigh volume specialtiesInvestigational Markers

2

29

62

28

42 46

2

6 2

2017: DiaSorin products available

2018-2019: DiaSorin new tests

# tests of the main competitorwithin the area

22

Roadshow Presentation - September 201813

1998 2006

VITAMIN D

EBV PANEL (4)

DIRECT RENIN

BORRELLIA

HSV 1 IGG

TORCH (11)

PARVOVIRUS (2)

PARVOVIRUS (2)

BORDETELLA

ZIKA IGM

FGF 23

MUMPS IGM

1,25 VITAMIN D

STOOL DX ASSAYS (8)

ALDOSTERON

DIRECT RENIN

CHLAMIDIA T. (2)

MEASLES IGM

ALDOSTERON

MYCOPLASMA (2)

HSV 2 IGG

VZV IGG

TREPONEMA

2007 20082010

20112012

20132014

2015

2016

2017

DiaSorin «First» : Fully Automated CLIA assays

> 45 times «First»in the last 10 years

Roadshow Presentation - September 201814

Development of Differentiating Specialty Tests

R&D Pipeline

Internal Development

Leverage on LIAISONContent & Technology

Products creating complementary opportunities that

should generate €/mln 25-50 each

Development ofdifferentiatingspecialty tests

Access to partner’s specialties

e.g.ZIKA Test

B·R·A·H·M·S

Differentiating specialties

New from 2019

Roadshow Presentation - September 201815

LIAISON XS: the opportunity

Moderate to Highcomplexity POLs

Professional Medical Service Institution

These POLs use Instruments normally found in Hospitals and Private Labs

Basic Medical Service Institution

27,467

COMPLIANCE

PPM

11,721

5,767

18,296

37,763

UNRATED HOSPITAL9,440

8,966

MATERNAL & CHILD HEALTHCARE STATION

3,071

CDC

3,484

75,964 ACCREDITATION

WAIVER

PUBLIC TOWNSHIP

HOSPITAL

CLASS 2 HOSPITALCLASS 1 HOSPITAL

PUBLIC COMMUNITY MEDICALSERVICE CENTER

7,700

2,155CLASS 3 HOSPITAL

Roadshow Presentation - September 2018

Molecular Diagnostics

Roadshow Presentation - September 201817

ME

NU

AUTOMATION

AMPLIFICATION / DETECTION

PCR Singlex

Multiplex

- Arrays

- Sequencing

Technologies in the Molecular Diagnostic Market

Area ofopportunity

Area ofopportunity

Roadshow Presentation - September 201818

Platforms in the Molecular Diagnostic Market

Point of Care systems

CLIAwaived

Limited menu (e.g. FLU)

Singletarget

Multiplex

Direct AmplificationDisc (DAD)

Multiplex Disc Universal Disc (UD)

Total Lab Automation

New Project

Limited menu(HCV, HIV, HBV, HPV, CT/NG)

High throughput systemsBenchtop systems

DiaSorin positioning

Roadshow Presentation - September 201819

Our technology: Liaison MDX

Direct Amplification Disc(DAD)

8 reaction wellLow to Mid Volume

96 reaction wellHigh Volume

Universal Disc(UD)

Compact. Powerful. Expandable.Technology

Unique technology developed by 3M, with no extraction required

VersatileSame platform, multiple discs

PCR Based

ASRs & Kits

Roadshow Presentation - September 201820

DiaSorin menu positioning

Analyte Specific Reagents(ASRs for US market only)

Real-time PCR assays for quantitative,qualitative and multi-analyte detection

Infectious Disease Transplant Inherited Diseases

Respiratory

Meningitis Vector Borne

Monitoring CoagulationWomen’s

Health/STIHAI/ Gastro

12 61

ASRs

Lab Developed Tests (LDT)

Roadshow Presentation - September 201821

Molecular kits and ASRs

ASRs

ASRs

KitsKits

Kits

Produced by manufacturer rigorously tested for safety and efficacy in clinical trials for “approval or clearance”

Sold as separate components instead of a kit, building blocks or “active ingredients” of LDT

Manufactured in compliance with cGMPs to help ensure quality

Level of complexity given to approved test

Highly complex to Clia Waived

ASRs

Roadshow Presentation - September 201822

Molecular Kits Pipeline Strategy

Competitive Intensity

Leve

l of D

iffe

ren

tiat

ion

3 years pipeline strategy

RESISTANCE ASSAYS

ATYPICAL PNEUMONIA

M. GENITALIUM

VZV

ENTERIC PANELS

GROUP B

STREP

CONGENITAL

CMV

BORDETELLA

VectorBorne

MENINGITIS

HSV - MC/C

VAGINOSIS

Differentiating specialties Me too testsHigh volume specialtiesInvestigational Markers 3-5 years pipeline strategy

Kits

Avg. # 2 new Kits / Year

Roadshow Presentation - September 201823

Avg. # 4 new ASRs / YearReagents ASRs

2017 - 2019 2019 - beyond

InfectiousDisease

Immuno-compromised

Respiratory

ResistanceVector-Borne

Gastro-intestinalinfections

Genetics

ASRs Pipeline Strategy

Differentiating specialties

Roadshow Presentation - September 201824

Europe: Options in High Throughput testing

Viral Load Monitoring

HIVHepatitis B VirusHepatitis C Virus

Big PlayersEstablished Systems

Well ServedHighly Competitive

Very Late Entry

Established PlayersCompetitive Arena

Barriers to Entry (HPV)Rapidly Eroding Price

No Clear LeaderBig Players AbsentImprove WorkflowMore Stable Price

DS knows this Market

Post Transplantation offers path to entry

Women’s Health

CT/NG/TVHPV

Post Transplantation

CMV/EBV/BKVHSV/VZV

HHV6/HHV8/AdenoParvo/JCV

Roadshow Presentation - September 201825

Europe Molecular Post Transplant

Instrument forextraction/PCR set up

Provide complete transplant menu

11 transplant assays

CMV

EBV

BKV

HSV 1

HSV 2

VZV

HHV6

HHV8

ADENOVIRUS

PARVOVIRUS

JCVLIAISON MDX forAmplification

Strategy

Roadshow Presentation - September 201826

Post TransplantationPanel

Immuno ID Assays

Existing DiaSorinMarket Share 37%

MDX PANEL

Expand cross selling opportunity IMMUNO-MDXwith most complete panel

CMVEBVHSV 1HSV 2

CMVEBVHSV 1HSV 2VZVBKV

VZVTOXOPARVOVIRUS

ADENOVIRUSPARVOVIRUSHHV6HHV8JCV

Europe: IMMUNO - MDX Synergy

Market size estimates:~100 €/mln

Roadshow Presentation - September 2018

Mid-term objectives

Roadshow Presentation - September 201828

1

2

3

4

5

6

7

2019 targets

Solid growth of the Immunoassay franchise with addition of innovative and differentiating new products Revenues

~ 775 €/mln

CAGR 16-19: ~ +11%

2019 Company Guidance

EBITDA295-300 €/mln

EBITDA Margin: ~ 38.5%

CAGR 16-19: ~ +11%

NET RESULT160-165 €/mln

On sales: ~ 21.0%

CAGR 16-19: ~ +13%

CUMULATIVE FREE CASH FLOW

465-475 €/mln

Launch of Liaison XS allows penetration of the small labs/POLs segment

QIAGEN partnership demonstrates that DiaSorin is seen well posi-tioned to serve the Specialty market also by other large IVD players

Conversion of SIEMENS’ Elisa customers base to LIAISON XL/XS platforms

Molecular Diagnostics is a second leg and will offer lots of opportunities to develop Specialty ID products

Strong financial performance driven by solid margins in both segments (IA and Molecular)

Committed to targeted bolt on acquisitions to strengthen our product portfolio or allow access to new customers in consolidated markets

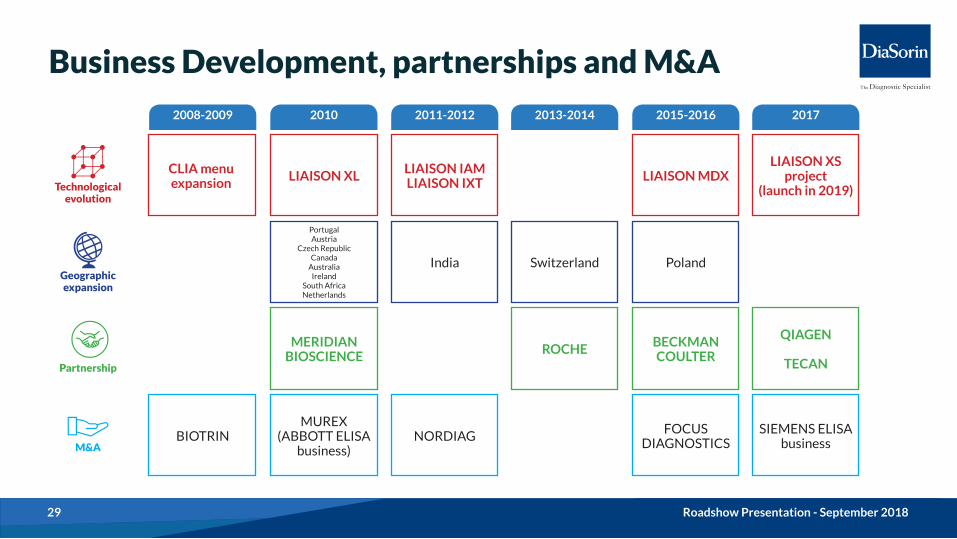

Roadshow Presentation - September 201829

2008-2009 2010 2011-2012 2015-20162013-2014 2017

CLIA menuexpansionTechnological

evolution

Geographicexpansion

Partnership

M&A

LIAISON XL

MERIDIANBIOSCIENCE

PortugalAustria

Czech RepublicCanada

AustraliaIreland

South AfricaNetherlands

India

BIOTRINMUREX

(ABBOTT ELISA business)

NORDIAG FOCUSDIAGNOSTICS

SIEMENS ELISAbusiness

Switzerland Poland

ROCHE BECKMANCOULTER

QIAGEN

TECAN

LIAISON IAMLIAISON IXT LIAISON MDX

LIAISON XSproject

(launch in 2019)

Business Development, partnerships and M&A

Roadshow Presentation - September 2018

Q2 and H1 2018 Results

Roadshow Presentation - September 201831

Highlights

FCF

REVENUES /mln 166.7 (*) +3.0% +6.7%

EBITDA /mln 64.9 +1.9% +6.5%

EBITDA MARGIN

-44 bps

38.9%

25.5%

+26.7%/mln 42.5NET R ESULT

+ /mln 103.7NFP (**)

Q2’18

MO

LECU

LAR HSV (US market)

Extended cutaneous and mucocutaneous lesion swabs claims to cerebrospinal fluid (CSF) and genital lesion swab

KIT Infectious diseases

+7.6%+4.8%CLIA EX VIT D 25 OH

-3.9%-9.1%VIT D 25 OH

+31.3%+26.0%ELISA TESTS

+1.9%-3.1%MOLECULAR TESTS

-0.2%-2.7%INSTRUMENTS & OTHER REV.

H1’18

/mln 331.2 (*)

/mln 128.2

/mln 80.9

/mln 69.2

+3.7% +9.0%

+10.5% +6.9%

-3.3% -10.3%

+27.9% +22.2%

+12.1%+1.6%

+1.4%-2.2%

+1.6% +7.9%

-82 bps

+38.7%

+24.4%

+21.7%

ASRsReagents specific to bacterial target carried by ticks

Anaplasma phagocytophilum

Ehrlichia

BabesiaIM

MU

NO PCT II GEN (US market)

Clearance from the FDA to market the LIAISON BRAHMS PCT II GEN assay for Sepsis’ diagnosis through the quantitative determination of procalcitonin (PCT)

Infectious diseases-10 bps -40 bps

39.3% +39.1%

@ CER@ curr

* Revenues include Siemens’s ELISA business contribution (consolidated as of Sept 2017)** NFP does not include debts vs. shareholders for special dividends for €/mln 98.4

@ curr

% ON R EVENUES

HDV (CE mark)

Clearance from CE Notified Body to market the LIAISON XL Murex Anti-HDV, for Hepatitis Delta detection. After the launch DiaSorin will be the player with the widest menu in the Hepatitis and Retrovirus area and the first company to launch this test on CLIA

Hepatitis & Retrovirus

~ +9% at CER vs 2017 (°)from ~ +11% at CER

~ +12% at CER vs 2017 (°)from ~ +13% at CER

(°) 2017 /US$ avg. exchange rate = 1.13

FY 2018

EBITDA

REVENUES 3-years plan guidanceconfirmed

3-years plan guidance confirmed

FY 2019

+13.3%

@ CER

COMPANY GUIDANCE

PRODUCT DEVELOPMENT

Roadshow Presentation - September 201832

Q2 and H1 2018 revenues growth

@ CER

@ currTotal Group revenues +3.0%

+6.7%

• Vitamin D volumes slowdown (mainly US)• Unfavorable ordering pattern affected instruments

sales in China and ASRs sales in the US• Suspension of a Zika tender in Brazil, due to the

end of the infection’s emergency• FOREX: - /mln 16.7

+3.7%

+9.0%

•All CLIA tests, net of Vitamin D•Siemens’s ELISA business (acquired in Sept

2017)•Molecular kits recorded a double-digit growth

CLIA ex Vitamin D tests +4.8%

+7.6%

Vitamin D test (CLIA) -9.1%

-3.9%

CLI

A

ELISA tests (*) +26.0%

+31.3%

Instruments & Consumables

-2.7%

-0.2%

Molecular Diagnostic tests -3.1%

+1.9%

+6.9%

+10.5%

-10.3%

-3.3%

+22.2%

+27.9%

-2.2%

+1.4%

+1.6%

+12.1%

@ CER

@ curr

@ CER

@ curr

@ CER

@ curr

@ CER

@ curr

@ CER

@ curr

* Including the contribution of Siemens’s ELISA business, consolidated as of September 2017

EUROPE & AFRICA

Germany +22.0%

+14.1%

+22.7%

+15.2%

Italy +8.7% +9.6%

France +17.9%

NORTH AMERICA

USA -4.5%

-4.3%

+16.4%

-0.1%

+0.5%

ASIA PACIFIC

China

Distributors

Australia

-0.8%

+18.2%

+20.4%

+9.5%

+0.0%

+19.6%

+28.6%

+12.4%

LATIN AMERICA

Brazil

Distributors

+3.5%

+3.7%

+5.0%

+1.8%

Mexico +7.1% +2.6%

+2.3% -2.4%

Growth driven by Siemens’ ELISA business acquisition and CLIA ex Vit D tests. Negative Vitamin D contribution (mainly price pressure)

Positive performance driven by CLIA ex Vit D tests

Increase in all CLIA tests

Positive contribution from CLIA ex Vit D, offset by lower Vitamin D (mainly volumes) and ASR sales (ordering pattern)

Growth in CLIA tests, partially offset by lower Murex Elisa and Instruments sales (ordering pattern)

Growth driven by Siemens’ ELISA business and instruments

sales

Upward trend in CLIA tests and growth from Siemens’ ELISA business

Positive performance of CLIA tests partially offset by a negative trend in MUREX sales and the suspension of a Zika tender

Positive performance driven by CLIA tests

Positive performance driven by instruments sales and Siemens’ ELISA business partially offset by CLIA sales downward

Managerial outlook on reported data; Change QoQ and HoH @ CER

Q2’18 vs. Q2’17 H1’18 vs. H1’17

Q2’18 vs. Q2’17 H1’18 vs. H1’17

Q2’18 vs. Q2’17 H1’18 vs. H1’17

Roadshow Presentation - September 201833

H1 2018 revenues breakdownby technology

CLIA tests

66.8%

Instruments & consumables

11.7%Molecular

diagnostic tests9.6%

ELISA tests11.9%

CLIA tests65.6%

ELISA tests14.0%

Moleculardiagnostic tests

Instruments & consumables

by geography

North America

32.4%

Latin America

7.3%

Asia Pacific17.6%

Europe & Africa42.7%

North America28.1%

Latin America

6.4%

Asia Pacific18.3%

Europe & Africa47.2%

(*) Revenues include Siemens’ ELISA business acquired on Sept 29, 2017

H1’18 (*)

H1’17

H1’18 (*)

H1’17

11.0%

9.4%

Roadshow Presentation - September 201834

Installed base expansion7,398 7,501 7,623

+116

-13

+123

-1

@ Dec 31, 2017 @ March 31, 2018 @ June 30, 2018

Q2 and H1 2018 Results

-14

3,880 3,867 3,866

3,518 3,634 3,757

+239

Roadshow Presentation - September 201835

Q2 and H1 2018 profitability profile

+7.9%

H1’18 EBITDA upward compared to H1’17 notwithstanding:

• some one-off costs related to a legal action concerning the introduction of certain future products in the US market (approx. /mln 2.0)

and to the closure of the Irish site

• FOREX negative impact (- /mln 7.9)

EBITDA ( /MLN)

EBITDA MARGIN

+1.9%

-44 bps

Change %

+1.6%

-82 bps

Change %

39.1%

Q2’18 EBITDA MARGIN confirms the strong profitability achieved in Q1’18

+6.5%

39.3%

126.2 128.2

39.5% 38.7%

63.7 64.9

39.4% 38.9%

H1’18Q2’17 Q2’18 H1’17

@ CER

@ CER -10 bps -40 bps

Roadshow Presentation - September 2018

Business Development

Roadshow Presentation - September 201837

Business and product development

Rationale

Technology

Impact on revenues

in China in the US

Increase penetration in big labs

Immuno (CLIA)

Increase penetration in big labs

Launch Hepatitis & Retroviruses

panel

PARTNERSHIPS

Market share: conversion from ELISA to CLIA

Immuno (ELISA)

New market opportunities leveraging on

QFT technology

Immuno (CLIA)

Immuno (CLIA) Molecular

(Extraction)

Extraction for European post transplantation

strategy

PORTFOLIO ACQUISITION

NEW PRODUCT CO-DEVELOPMENT NEW PLATFORMS DEVELOPMENT

Immuno (CLIA) Immuno (CLIA)

Beyond 2019

2019

2018

2017

Access to new mkt segment:POLs (US)

Class I-II hospitals (China)

Hub and Spoke (EU)

Roadshow Presentation - September 2018

2017 -2019 guidance

Roadshow Presentation - September 201839

2017-2019 guidance

1 Solid growth of Immunoassay franchise with addition of innovative and differentiating new products

2 Launch of LIAISON XS allows penetration of the small labs/POLs segment

QIAGEN partnership demonstrates that DiaSorin is seen well positioned to serve the Specialty market also by other large IVD players

3

5 Molecular Diagnostics is a second leg and will offer lots of opportunities to develop Specialty ID products

Conversion of SIEMENS’ Elisa customers base to LIAISON XL/XS platforms 4

6 Strong financial performance driven by solid margins in both segments (Immunoassay and Molecular)

2018 2016

637.5

+12.0% reported

+13.1% @ CER

2016

~ +9% @ CER

2017

2017-2019 STRATEGIC GOALS GUIDANCE DATA IN €/MLN

Committed to targeted bolt on acquisitions to strengthen our product portfolio or allow access to new customers in consolidated markets

7

ACTUAL RESULTS DATA IN €/MLN

2017

569.3

217.3

REVENUES

E BITDA

2019

237.9

+9.5% reported

+11.5% @ CER 2016

E BITDA REPORTED

241.2

+11.0% reported

+13.0% @ CER

2016

EBITDA ADJUSTED (*)

3-years plan guidance confirmed

E BITDA

3-years plan guidance confirmed

~ +12% @ CER

2017

REVENUES

(*) Managerial outlook on reported data: net of positive contribution from acquisition of Siemens’ ELISA business and non recurring costs related to closing of Irish facility

Roadshow Presentation - September 2018

Annexes

Roadshow Presentation - September 201841

Income Statement

Net revenues

Gross profit

Gros s Margin

S&M

R&D

G&A

Total operating expenses

% on sales

Other operating income (expense)

EBIT

E BIT margin

Net financial income (expense)

Profit before taxes

Income taxes

Net result

EBITDA

EBITDA margin

Data in million2017 2018 amount %

161.8 166.7 +4.9 +3.0%

111.3 115.6 +4.4 +3.9%

68.8% 69.4% +60 bps

(30.3) (33.3) -3.0 +9.9%

(11.4) (10.6) +0.8 -7.4%

(17.0) (16.8) +0.1 -0.8%

(58. 7) (60.7 ) -2.0 +3.5%

(36.3)% (36. 4)% -15 bps

(1.4) (2.7) -1.2 +84.7%

51.2 52.3 +1.1 +2.2%

31.6% 31.4% -26 bps

(1.3) 2.2 +3.6 n.m.

49.8 54.5 +4.7 +9.4%

(16.3) (12.0) +4.3 -26.2%

33.6 42.5 +9.0 +26.7%

63.7 64.9 +1.2 +1.9%

39.4% 38.9% - 44 bps

Q2 Change

2017 2018 amount %

319.3 331.2 +11.9 +3.7%

219.2 226.8 +7.6 +3.5%

68.7% 68.5% -16 bps

(60.1) (65.0) -4.9 +8.2%

(21.6) (22.2) -0.7 +3.1%

(33.0) (31.9) +1.0 -3. 2%

(114.6) (119.2) -4.5 +3.9%

(35.9)% (36.0)% -7 bps

(3.4) (4.7) -1.2 +36.6%

101.2 103.0 +1.9 +1.9%

31.7% 31.1% -57 bps

(3.0) 1.3 +4.3 n.m.

98.2 104.3 +6.1 +6.3%

(31.8) (23.5) +8.3 -26.1%

66.4 80.9 +14.4 +21.7%

126.2 128.2 +2.0 +1.6%

39.5% 38.7% -82 bps

H1 Change

Roadshow Presentation - September 201842

Balance Sheet

Goodwill and intangibles assets 344.4 356.1 +11.7

Property, plant and equipment 92.3 89.7 -2.6

Other non-current assets 23.8 24.9 +1.1

Net working capital 190.7 211.9 +21.1

Assets held for sale 4.0 - -4.0

Other non-current liabilities (62.5) (63.0) -0.4

Net Invested Capital 592.7 619.6 +26.9

Net Financial Position 149.3 103.7 -45.6

Debts vs. shareholders for special dividends - 98.4 +98.4

Total Shareholders' equity 742.0 624. 8 -117.1

ChangeData in million 12/31/17 06/30/18

Roadshow Presentation - September 201843

Cash Flow Statement

2017 2018

172.8 172.3 -0.4

25.8 50.8 +25.0

(9.1) (10.9) -1.8

(59.4) (115.1) -55.7

(1.0) (0.7) +0.3

(43.7) (75.9) -32.2

(21.1) 8.2 +29.3

(64.8) (67.7) -2.9

107.9 104.6 -3.3

Q2 Change2017 2018

130.5 159.3 +28.9

77.0 88.4 +11.4

(17.1) (21.0) -3.8

(60.2) (118.6) -58.4

(1.1) (4.5) -3.4

(1.4) (55.6) -54.2

(21.1) 0.9 +22.0

(22.5) (54.8) -32.2

107.9 104.6 -3.3

H1 Change

Cash and cash equivalents at the beginning of the period

Operating activities

Investing activities

Financing activities

Acquisitions of companies and business operations

Net change in cash and cash equivalents before investments in financial assets

Divestment/(Investment) in financial assets

Net change in cas h and cas h equivalents

Cash and cash equivalents at the end of the period

Data in million

Roadshow Presentation - September 201844