2020 state and local government audit planning ... - aicpa

TRANSCRIPT

2020 State and Local Government Audit Planning Considerations

A Governmental Audit Quality Center Web Event

May 28, 2020

Earning CPE

Disable all pop up blockers

Any answer counts towards CPE credit

Earn credit by responding to 75% of these pop-ups

Click the CPE button at the end of this webcast

A post event e-mail with CPE information will be sent to you

2

Questions? Problems? Contact: 888.777.7077 or [email protected]

More Helpful Hints

Adjust your volume• Be sure your computer’s sound is turned on as well.• Click this button. Slide the control up or down to fit your

needs.

Ask your questions• Feel free to submit content related questions to the

speaker by clicking this button. • Someone is available to assist with your technology and

CPE related questions as well. Download your materials• Access today’s slides and learning materials by clicking

this download button at any time during this presentation.• If you need help accessing these materials send a

message through the Q&A application.

3

Presenters

4

Michelle Watterworth, CPAPlante Moran

Chris Pembrook, CPACrawford & Associates

Flo Ostrum, CPAGrant Thornton

Program Objectives

• Overview of current environment• Impact of COVID-19 pandemic on SLG

financial statement audits• Discuss current auditing and accounting

developments affecting state and local government financial statement audits

• Increase awareness on GAQC and AICPA resources available to help you maintain or improve your audit quality

5

Terminology & Abbreviations

6

Abbreviation AbbreviationASB AICPA Auditing Standards Board IG GASB Implementation GuideAPA Availability Payment Arrangements MD&A Management's discussion and analysisCOVID-19 Novel Coronavirus MSRB Municipal Securities Rule BoardCU Component Unit MTMI More than minimal influenceDC Defined contribution plans OPEB Other post-employment benefitsDB Defined benefit plans PEEC Professional Ethics Executive CommitteeEAQ AICPA Enhancing Audit Quality Initiative PPP Public-Private or Public-Public

PartnershipEMMA Electronic Municipal Market Access RMM Risk of material misstatementET AICPA Code of Professional Conduct section SAS ASB Statement on Auditing StandardF/S Financial statements SCA Service Concession ArrangementsFSAC Financial Statement Attest Client SEC U.S. Securities & Exchange CommissionGAO U.S. Government Accountability Office SLG State and local governmentsGASB Governmental Accounting Standards Board SOC System and organization controlsGFOA Government Finance Officers Association TQA AICPA Technical Questions and Answers

Current Environment

Economy Pre-COVID-19

8

GROWING TAX REVENUES

Q3 & Q4 2019

SALES TAX SPIKES Q3 2019

US SURPASSED LONGEST ECONOMIC RECOVERY

ON RECORD

Economy Post-COVID-19

9

Shutdown of the economy

Unprecedented unemployment

Drastically reduced sales and income taxes expected

Escalating costs to manage public health crisis

Legislative & Regulatory Developments—SEC & MSRB

SEC Statement on COVID-19 Disclosures– The Importance of Disclosure for our Municipal Markets

MSRB Resources– Weekly COVID-19-Related Disclosure Summary

– Daily Municipal Market Trading Report

10

Legislative & Regulatory Developments—Single Audit

COVID-19 implications• Significant influx of

federal funds • Lack of clarity around

whether subject to single audit

• Challenges with new or revised compliance requirements

• Potential for significant changes in processes and controls during the year

• Audit extensions

11

2020 Compliance Supplement without COVID-19 updates expected late June

2020

Possible follow-up addendum

addressing COVID-19 matters in Fall

2020

GAQC June 30th event providing the latest on single audits GAQC member registration and non-member registration.

Federal government response

12

Coronavirus Preparedness and

Response Supplemental

Appropriations Act (March 6, 2020)

Families First Coronavirus Response

Act (March 18,

2020)

CARES Act and

subsequent COVID-19

Relief Package

(March 27 and April 24,

2020)

Single Audit - Challenges due to COVID-19

Timing of the pandemic will introduce many challenges for 2020 single auditsGAQC issued a comprehensive letter to OMBsummarizing the key questions and issues that need to be resolvedAmong those questions are the following:• Which new programs will be subject to the Uniform

Guidance? • What catalog of federal domestic assistance numbers

are associated with new programs?• How will the Compliance Supplement recognize

agency changes to compliance requirements? 13

Panel discussion – What concerns are your clients voicing surrounding the impact of the COVID-19 pandemic?

14

COVID-19 Implications for 2020 SLG F/S Audits

Timing

GAQC Website:

Summary of COVID-19 Related Deadline

Extensions of Audited F/S and Other Reports

Deadlines/Extensions

State or federal-

mandated

EMMA continuing disclosures

GFOA & Other

Certificate Programs

Automatic or Request

Extensions?

Engagement Letters/Audit Contracts

Due dates

Scope of services

Fees

Risk Assessment

New RMMMagnitude

and likelihood of

misstatement

Increased risk

of errors

New or changed

fraud risks

Internal Control

Pre-pandemic Remote Post-

pandemic

Analytics & Estimates

• Historical trends and assumptions may not be relevant in the current environment

• Certain estimates may be significant given current uncertainties

• Additional considerations and testing may be necessary

Specialists/3rd party reporting

Potential for new limitations/ language

Possible impact on reports• SOC 1 control issues

• Valuation issues

Timing

Upfront considerations

Revenue

Declines

Impact of delayed due dates

Management’s Discussion & Analysis – COVID-19 Considerations

23

FYE 2/29/20 and earlier

Currently known facts

section

FYE after 2/29/20

Throughout the MD&A

Subsequent Events – COVID-19 Considerations• For periods ending prior to February 29, 2020,

COVID-19 related events would likely require disclosure.

• Auditors would need to consider the effect on their report for any subsequent events not appropriately recognized in the financial statements.

Going Concern and COVID-19

Going Concern Considerations

Type of entity

Taxingpower

Financial condition

pre-COVIDRecurring

losses

Borrowing capabilities

Accounting Considerations Surrounding COVID-19

26

Operating vs. Nonoperating

Special & Extraordinary Items

Expenditures (modified accrual)

Grant accounting

Changing employee programs (furloughs, etc.)

Increased Emphasis on Noncompliance with Laws and Regulations

27

Reporting requirements

Debt covenants

Minimum fund balance regulations

Pension & OPEB funding

requirements

Budgetary policies and regulations

Compliance with grant programs

Panel discussion –What additional risks do your firms foresee in the coming year? How are you responding?

28

Audit Developments & Practice Issues

Risk Assessmentand

Internal Control

AICPA EAQ initiative - 2020 areas of focus

Auditing Revenue Recognition

SOC Engagements

Engagement Acceptance

COVID-19 Response

30

The 2020 primary area of focus will be COVID-19

AICPA Deferral of Effective Dates

SAS 141, Amendment to the Effective Date of SAS Nos. 134 Through 140 (Issued May 2020)

One year delay issued to provide relief to auditors amid the challenges created by the COVID-19 pandemic

The standards will now be effective for audits of F/S for periods ending on or after December 15, 2021

One change is that early implementation of the standards will now be permitted

The ASB recommends that all these SASs be implemented concurrently

31

Remote Auditing Considerations

• Potential quality issues• Ensure accuracy, completeness, relevance, and

reliability of evidence

• Creative use of technology to accomplish objectives

• Need for enhanced communication

• Timing

32

Internal Controls - Tips in a Changing Environment• Keep things in perspective

• Consider the following:• What’s the length of time new controls were in

place?

• What’s the level of business activity during that time?

33

Internal Controls - Tone at the Top

• What was the message from the government?

• What was the message from key officials (City Manager, Director of Finance, etc.) to accounting personnel?

• Were employees well informed?

• Did employees receive training on a remote working environment?

34

Internal Controls - Obtaining an Understanding

• Usual requirements/variety of tools• Observation (video)

• Inspection (video, scanned documents)

• Inquiry (phone, video, email)

• Reperformance/recalculation

35

Professional Skepticism

AICPA Professional Ethics - Interpretations with Delayed Effective Dates

36

SLG Client Affiliates -ET 1.224.020

• Now effective for fiscal years beginning after 12/15/21

• Implementation guide and practice aid coming in 2nd quarter

Leases - ET 1.260.040

• Now effective for fiscal years beginning after 12/15/20

Information System Services - ET

1.295.145 • Now effective on

1/1/22

PEEC approved effective date extensions of these interpretations.

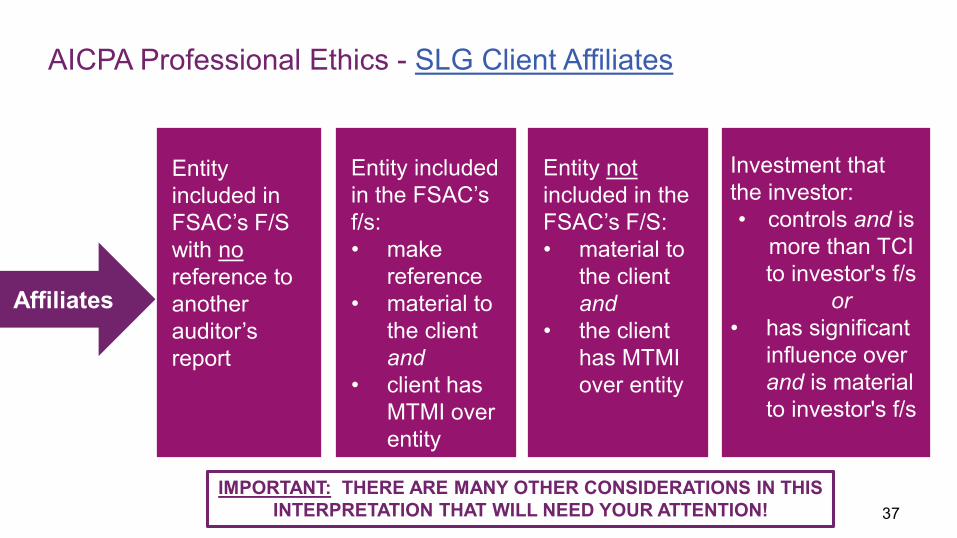

AICPA Professional Ethics - SLG Client Affiliates

37

Entity not included in the FSAC’s F/S:• material to

the client and

• the client has MTMI over entity

Entity included in the FSAC’s f/s: • make

reference• material to

the client and

• client has MTMI over entity

Investment that the investor:• controls and is

more than TCI to investor's f/s

or • has significant

influence over and is material to investor's f/s

IMPORTANT: THERE ARE MANY OTHER CONSIDERATIONS IN THIS INTERPRETATION THAT WILL NEED YOUR ATTENTION!

Entity included in FSAC’s F/S with no reference to another auditor’s report

Affiliates

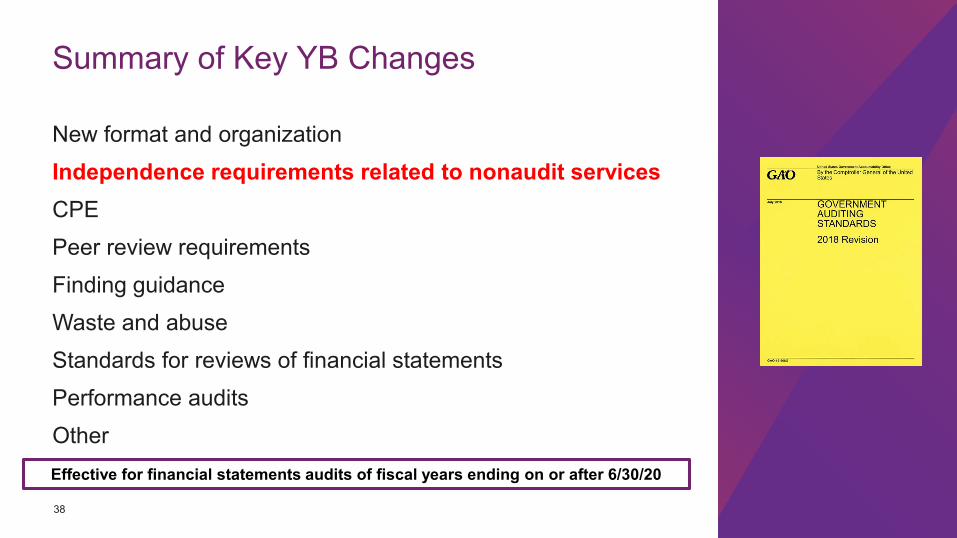

Summary of Key YB Changes

New format and organizationIndependence requirements related to nonaudit servicesCPEPeer review requirementsFinding guidanceWaste and abuseStandards for reviews of financial statementsPerformance auditsOther

38

Effective for financial statements audits of fiscal years ending on or after 6/30/20

Is the nonaudit service preparing the F/S (in their entirety) from a client provided trial balance or underlying accounting records?

Evaluate threat for significance

Is the threat significant?

Document evaluation and

proceed

Identify and apply safeguards

Assess effectiveness of safeguards(s)Is threat eliminated or reduced to an acceptable level?

Independence impairment - Do not proceed

Document nature of threat and any safeguards applied

Proceed

Yes

No

2018 YB Figure 2 - Revised evaluation of nonaudit services related to preparing accounting records and F/S

NEW

39

2018 YB Resources

Take advantage of following archived GAQC Web events to do a deep dive into the 2018 YB• Considering and Documenting Nonaudit Services

under Government Auditing Standards• Understanding the Changes to Yellow Book

Independence• The 2018 Yellow Book: What You Need to Know

Access these Web events

40

AICPA Audit and Accounting Guide, State and Local Governments

41

Key resource for auditors of SLGs; you should be using this Guide!

New edition expected in late Summer

Key changes made:

• Effect of newly effective GASB standards

• Appendix discussing GASB Statement No. 87, Leases

• Appendix discussing SAS Nos. 134, 135, 137, 138, 139 and 140

• Order now at: http://www.aicpastore.com/

Panel discussion – How is the remote working environment affecting your audit engagements?

42

Accounting Developments

GASB 95 - Deferral of Effective Dates

GASB Statement No. 95, Postponement of the Effective Dates of Certain Authoritative Guidance (Issued May 2020)

The following standards are delayed for one year:

• GASB Statements Nos. 83, 84, 88, 89, 90, 91, 92, 93

• Implementation Guide Nos. 2017-3, 2018-1, 2019-1, 2019-2

The following standards are delayed for 18 months:

• GASB Statement No. 87

• Implementation Guide No. 2019-3

44

Early application is permitted

and encouraged to the extent specified in

each originally

issued standard

GASB 84 Implementation

Now effective for December 31, 2020 year ends

To implement or not to implement?

• What has the government done to prepare to date?

• What resources does the government have to finish the implementation process?

Primary government and component unit implementation

45

Implement Now

GASB 84 Implementation

Exposure Draft, Certain Component Unit Criteria, and Accounting and Financial Reporting for Section 457 Plans

• Potential defined contribution plan relief

• 457 Plans

AICPA TQA 6950.23-.24, Auditor Assessment of a Special-Purpose Government's Only Immaterial Fiduciary Fund

Listen to recent GAQC Web event on fiduciary activities for a deeper dive46

GASB 87 - Don’t Wait to Start!

47

Start reviewing existing leases as soon as possible

Implement IC to identify leases &

lease modifications

Update accounting

systems for new information needs

Consider impact on capitalization

policy

Consider impact of reporting lease

liabilities on:

Debt limitationsBond covenants

Grant agreements

Don't forget guidance in IG 2019-3 and 2020-1

GAQC archived web event on leases

GASB 91, Conduit Debt Obligations

48

Clarifies the definition of conduit debt obligations

Establishes conduit debt is not a liability of

the issuer

Issuers make limited

commitments

Sometimes issuers also make

additional voluntary

commitment, which may

require recognition as a

liability

Effective for reporting periods beginning after December 15, 2021

Key clarifications include

the following:

Reporting of intra-entity transfers of assets

between (non)employer contributing entity and DB pension/OPEB plan

within the same financial reporting

entity

Applicability of GASB 73 to assets

accumulated for DB pension/OPEB plans

not administered through qualifying

trusts

Liability recognition for Fiduciary activities

reporting assets accumulated for DB pension/OPEB plans

not administered through a qualifying

trust

Applicability of financial reporting

requirements in GASB 84 to DC

pension/OPEB plans

GASB 92, Omnibus 2020

49

Effective for fiscal years beginning

after 6/15/21

Effective for reporting periods beginning

after 6/15/21

GASB 93, Replacement of Interbank Offered RatesAddresses implication resulting from the replacement of LIBOREffective Dates:• Paragraph 11b first effective for reporting

periods ending January 31, 2022• Paragraphs 13 and 14 first effective for fiscal

years ending June 30, 2022• All remaining paragraphs first effective for

reporting periods ending July 31, 202050

GASB 94, Public-Private and Public-Public Partnerships and Availability Payment ArrangementsFirst effective for fiscal years ending June 30, 2023, with early application encouraged.Provides accounting guidance for PPPs and APAsDefines SCAs as a specific type of PPP and supersedes GASB Statement No. 60, Accounting and Financial Reporting for Service Concession ArrangementsGuidance aligned with GASB Statement No. 8751

GASB IGs

52

Comprehensive Implementation Guide

Guidance in IGs is considered Category B GAAP• All IGs are posted on www.gasb.org

Critical to read and understand

On the Horizon

AICPA ASB - Auditing Standards Early implementation

is permitted.SAS No. Topic AU- C Section Affected Issued

134 Auditor Reporting 700, 701(new), 705, 706 May 2019

135 Omnibus SAS Various May 2019

136 EBP ERISA Audits 703 (new) July 2019

137 Other Information 720 July 2019

Effective for audits of financial statements for periods ending on or after December 15, 2021.

54

AICPA ASB - Auditing Standards

SAS No. Topic AU- C Section Affected Issued

138 Description of the Concept of Materiality

200, 320, 450, 600, 700, 703

December 2019

139Incorporate Auditor Reporting Standards to Various AU-C sections

800, 805, and 810 March 2020

140Incorporate Auditor Reporting Standards to Various AU-C sections

725, 730, 930, 935, and 940 April 2020

141Amendment to the Effective Date of SAS Nos. 134 Through 140

Various April 2020

Effective for audits of financial statements for periods ending on or after December 15, 2021 (except for SAS 141 which is effective upon issuance)

55

Early implementation

is permitted.

GASB Q2 2020 Issuances

56

• Revenue and Expense RecognitionPreliminary

Views

• Financial Reporting Model• Conceptual Framework: Recognition

Exposure Draft

• Certain CU and 457 Plans• Subscription-based IT ArrangementsFinal

GASB Projects – Practice Issues

57

Compensated Absences-

Reexamination of Statement 16

ED expected February 2021

Prior-period Adjustments,

Accounting Changes, and Error Corrections-

Reexamination of Statement 62

ED expected March 2021

Panel discussion - What do you think is the most important takeaway from today’s Web Event?

58

Resources

“Summer Fun” CPE rebroadcast week (all times Eastern) - watch for registration GAQC Alert

Monday, June 15th

• 1-3pm - Considering and Documenting Nonaudit Services under Government Auditing Standards

Tuesday, June 16th

• 11am to 1pm - Single Audit Lightning Round

• 1-3pm - When You Think It, Ink It! Best Practices in Single Audit Documentation

Wednesday, June 17th

• 11am to 1pm - Risk Assessment Considerations in a SLG Financial Statement Audit

• 1-3pm - Using Part 6 of the New Compliance Supplement on Internal Control

Thursday, June 18th

• 11am to 1pm - Heard in the Hallways: Commonly Asked Yellow Book Questions

• 1-3pm – Smart Sampling in a Single Audit

Friday, June 19th • 11am to 1pm - 2020 State and Local Government

Audit Planning Considerations

• 1-3pm - 2020 GAQC Annual Update Webcast

60

A chance to catch up on GAQC events you or your staff missed!

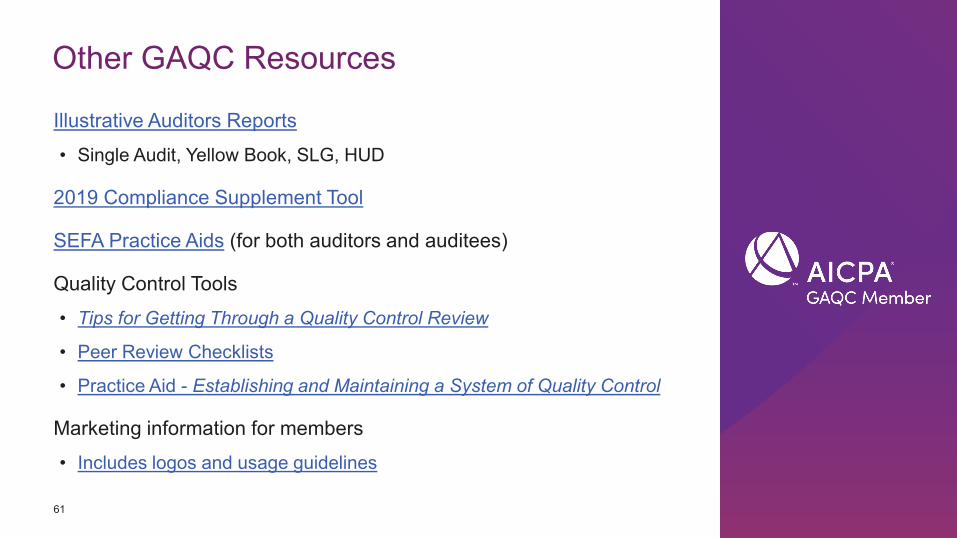

Other GAQC Resources

Illustrative Auditors Reports• Single Audit, Yellow Book, SLG, HUD

2019 Compliance Supplement Tool

SEFA Practice Aids (for both auditors and auditees)

Quality Control Tools• Tips for Getting Through a Quality Control Review

• Peer Review Checklists

• Practice Aid - Establishing and Maintaining a System of Quality Control

Marketing information for members• Includes logos and usage guidelines

61

Other AICPA resources

62

COVID-19 Resource Center

• Includes audit and accounting resources

Audit and Attest Web page

A&A Technical Hotline (877) 242-7212 [email protected]

Ethics Division Web Page (includes AICPA Code)• Ethics Hotline - [email protected] or

888.777.7077

Exam-Based Single Audit Certificates offered at Intermediate and Advancedlevels

Not-for-Profit Certificate Program - On-demand learning program

Not-for-Profit Section - For individuals interested in NFP A&A

EAQ Web site

Peer Review Web page

AICPA 2020 Conferences

63

AICPA Not-for-Profit Industry Conference, June 22-24, 2020, virtual offering only due to COVID-19

AICPA National Governmental Accounting and Auditing Update Conference, August 17 - 18, 2020, virtual offering only due to COVID-19

AICPA National Governmental and Not-for-Profit Training Program, October 19 - 21, 2020, MGM Grand, Las Vegas, NV *

GAQC members get a discount when using code “GAQC” at checkout

*The COVID-19 outbreak may eventually affect whether this event will occur in person or, instead, only virtually. Check the conference web links for the latest information going forward

AICPA - Peer Review - Governmental Checklists

64

Section Number Section Title

20,500 4/2019 (prev. 9/2018) Governmental Audit Engagement Checklist

22,110 4/2019 (prev. 5/2016)

Supplemental Checklist for Review of Audit Engagements Performed in Accordance with Government Auditing Standards (Yellow Book) December 2011 Revision

22,130 4/2019 (prev. 4/2018)

Supplemental Checklist for Review of Audit Engagements of State and Local Governments Participating in Pension Plans and/or Postemployment Benefits Other Than Pensions (OPEB)

Thank youCopyright © 2018 American Institute of CPAs. All rights reserved.