21 - 1 copyright 2003 pearson education canada inc. chapter 21 completing the audit

TRANSCRIPT

21 - 1Copyright 2003 Pearson Education Canada Inc.

CHAPTER 21Completing the

Audit

21 - 2Copyright 2003 Pearson Education Canada Inc.

Audit Completion ProceduresAudit Completion ProceduresSearch for unrecorded contingent liabilities.

What is acontingent liability and what are the relevant related

GAAPrecommendations?

21 - 3Copyright 2003 Pearson Education Canada Inc.

Audit Completion ProceduresAudit Completion ProceduresSearch for unrecorded contingent liabilities.

What is acontingent

liability and what are the relevant

GAAPrecommenda-

tions?

a potential futureobligation to an outside party for an unknown amount resulting from activities that havealready taken place

21 - 4Copyright 2003 Pearson Education Canada Inc.

Audit Completion ProceduresAudit Completion ProceduresSearch for unrecorded contingent liabilities.

likely and reasonably estimated - accrual

likely and not estimable - footnote disclosure

not determinable - footnote disclosure

unlikely - no financial statement or disclosure unless significant adverse effect

What is acontingent

liability and what are the relevant

GAAPrecommenda-

tions?

21 - 5Copyright 2003 Pearson Education Canada Inc.

Audit Completion ProceduresAudit Completion ProceduresSearch for unrecorded contingent liabilities.

Footnote disclosureshould describe the contingency and theopinion of legalcounsel or manage-ment regarding theexpected outcome.

What is acontingent

liability and what are the related

GAAPrecommenda-

tions?

21 - 6Copyright 2003 Pearson Education Canada Inc.

Audit Completion ProceduresAudit Completion ProceduresSearch for unrecorded contingent liabilities.- enquire of management

21 - 7Copyright 2003 Pearson Education Canada Inc.

Audit Completion ProceduresAudit Completion Procedures

Search for unrecorded contingent liabilities.- enquire of management- review: ~ client copies of Revenue Canada correspondence ~ minutes of board and shareholder meetings ~ invoices from client lawyers ~ existing audit workpapers ~ contracts, agreements, etc.

21 - 8Copyright 2003 Pearson Education Canada Inc.

Audit Completion ProceduresAudit Completion ProceduresSearch for unrecorded contingent liabilities.- enquire of management- review: ~ client copies of Revenue Canada correspondence ~ minutes of board and shareholder meetings ~ invoices from client lawyers ~ existing audit work papers ~ contracts, agreements, etc.- obtain letters of confirmation from all client lawyers

Jill Auditor, CA

Joe Lawyer Canada48

21 - 9Copyright 2003 Pearson Education Canada Inc.

Lawyer EnquiryLawyer Enquiry

The auditor should ask the client to prepare a letter (on client letterhead, signed by client officer) asking the lawyer to respond directly to the auditor concerning:

21 - 10Copyright 2003 Pearson Education Canada Inc.

Lawyer EnquiryLawyer Enquiry

The auditor should ask the client to prepare a letter (on client letterhead, signed by client officer) asking the lawyer to respond directly to the client with a copy to theauditor concerning:- client’s description of the nature & current status of all outstanding & possible claims with which the lawyer has been involved

21 - 11Copyright 2003 Pearson Education Canada Inc.

The auditor should ask the client to prepare a letter (on client letterhead, signed by client officer) asking the lawyer to respond directly to the auditor concerning:- client’s description of the nature & current status of all outstanding & possible claims with which the lawyer has been involved- client’s evaluation of the amount & likelihood of loss or gain for each listed outstanding & possible claim

Lawyer EnquiryLawyer Enquiry

21 - 12Copyright 2003 Pearson Education Canada Inc.

The auditor should ask the client to prepare a letter (on client letterhead, signed by client officer) asking the lawyer to respond directly to the auditor concerning:- client’s description of the nature & current status of all outstanding & possible claims with which the lawyer has been involved- client’s evaluation of the amount & likelihood of loss or gain for each listed outstanding & possible claim- any unlisted or potential items, or whether the status of each claim or assessment

Lawyer EnquiryLawyer Enquiry

21 - 13Copyright 2003 Pearson Education Canada Inc.

If an lawyer refuses to respond or refuses to provide adequate information, the audit opinion

will be qualified or denied.

Lawyer EnquiryLawyer Enquiry

21 - 14Copyright 2003 Pearson Education Canada Inc.

Review for Subsequent EventsReview for Subsequent Events

?

21 - 15Copyright 2003 Pearson Education Canada Inc.

Review for Subsequent EventsReview for Subsequent Events

12/31 2/14 2/28

balance sheet field work report date completion issue date

period under audit subsequent events period

Subsequent events are events or trans-actions having a material effect on

the financial statements thatoccur after the balance sheet

date but before fieldwork completion.

21 - 16Copyright 2003 Pearson Education Canada Inc.

12/31 2/14 2/28

balance sheet field work report date completion issue date

period under audit subsequent events period

Types of Subsequent EventsTypes of Subsequent Events1.events that provide additional evidence about conditions that existed at the balance sheet date (e.g., settlement of liabilities, realiza- tion of assets)

21 - 17Copyright 2003 Pearson Education Canada Inc.

12/31 2/14 2/28

balance sheet field work report date completion issue date

period under audit subsequent events period

1.events that provide additional evidence about conditions that existed at the balance sheet date (e.g., settlement of liabilities, realiza- tion of assets)

Types of Subsequent EventsTypes of Subsequent Events

Client financial statements for the periodunder audit must be adjusted to reflectthis subsequent event information.

21 - 18Copyright 2003 Pearson Education Canada Inc.

12/31 2/14 2/28

balance sheet field work report date completion issue date

period under audit subsequent events period

2. events that occur after the balance sheet date and do not relate to condi- tions that existed at year-end (e.g., bond/stock issue, acquisition, fire/flood loss, major customer/vendor bankruptcy)

Types of Subsequent EventsTypes of Subsequent Events

21 - 19Copyright 2003 Pearson Education Canada Inc.

12/31 2/14 2/28

balance sheet field work report date completion issue date

period under audit subsequent events period

2. events that occur after the balance sheet date and do not relate to condi- tions that existed at year-end

disclose

These subsequent events must be disclosed in the footnotes of the period under audit. Theauditor may also consider:- pro forma financial statements

Types of Subsequent EventsTypes of Subsequent Events

21 - 20Copyright 2003 Pearson Education Canada Inc.

Review for Subsequent EventsReview for Subsequent Events

Whatauditing

procedureswill identifysubsequent

events?

21 - 21Copyright 2003 Pearson Education Canada Inc.

Subsequent Events Auditing ProceduresSubsequent Events Auditing Procedures

Near field work completion, auditors should:- read post-balance sheet interim statements and records

Ace Company

Financial Statements

For the month ofJanuary 2005

21 - 22Copyright 2003 Pearson Education Canada Inc.

Subsequent Events Auditing ProceduresSubsequent Events Auditing Procedures

Near field work completion, auditors should:- read post-balance sheet interim statements and records- obtain a management representation letter and discuss with management: ~ contingent liabilities ~ significant changes in owners’ equity ~ items accounted for on tentative data ~ unusual adjustments in subsequent period

21 - 23Copyright 2003 Pearson Education Canada Inc.

Subsequent Events Auditing ProceduresSubsequent Events Auditing Procedures Near field work completion, auditors should:- read post-balance sheet interim statements and records- obtain a management representation letter- read minutes of board and shareholder meetings that have occurred since year-end

21 - 24Copyright 2003 Pearson Education Canada Inc.

Joe Lawyer

Jill Auditor, CA

Subsequent Events Auditing ProceduresSubsequent Events Auditing Procedures Near field work completion, auditors should:- read post-balance sheet interim statements and records- obtain a management representation letter- read minutes of board and shareholder meetings that have occurred since year-end- obtain letter from client’s lawyer

Canada 48

21 - 25Copyright 2003 Pearson Education Canada Inc.

12/31 2/14 2/28

balance sheet field work report date completion issue date

period under audit subsequent events period

Whatresponsibility

does the auditorhave for

subsequentevents that

occur betweenfield work

completion andthe issue date?

21 - 26Copyright 2003 Pearson Education Canada Inc.

12/31 2/14 2/28

balance sheet field work report date completion issue date

period under audit subsequent events period

- the auditor is not responsible for dis- covering subsequent events during this period

Whatresponsibility

does the auditorhave for

subsequentevents that

occur betweenfield work

completion and

the issue date?

21 - 27Copyright 2003 Pearson Education Canada Inc.

12/31 2/14 2/28

balance sheet field work report date completion issue date

period under audit subsequent events period

- the auditor is not responsible for dis- covering subsequent events during this period

- if, however, auditors learn of a subsequent event during this period, they are responsible for ensuring correcting accounting for it

Whatresponsibility

does the auditorhave for

subsequentevents that

occur betweenfield work

completion andthe issue date?

21 - 28Copyright 2003 Pearson Education Canada Inc.

If auditors learn of a subsequent event during this period, they are responsible for

its disclosure.

12/31 2/14 2/28

balance sheet field work report date completion issue date

period under audit subsequent events period

The auditors then have two options:- expand all subsequent events tests to the date of the event and change the report date to the date of the event (e.g., 2/21)

21 - 29Copyright 2003 Pearson Education Canada Inc.

If auditors learn of a subsequent event during this period, they are responsible for

its disclosure.12/31 2/14 2/28

balance sheet field work report date completion issue date

period under audit subsequent events period

The auditors then have two options:- expand all subsequent events tests to the date of the event and change the report date to the date of the event (e.g., 2/21)- restrict testing only to matters relating to the new event and dual-date the report:

Taylor & Tower, CAsFebruary 14, 2005, except for Note 3, as to which the date is February 21, 2005

21 - 30Copyright 2003 Pearson Education Canada Inc.

12/31 2/14 2/28

balance sheet field work report date completion issue date

period under audit subsequent events period

The auditors then have two options:- expand all subsequent events tests to the date of the event and change the report date to the date of the event (e.g., 2/21)- restrict testing only to matters relating to the new event and dual-date the report

What are the trade-offsbetween these options?

21 - 31Copyright 2003 Pearson Education Canada Inc.

Whatresponsibility

does the auditor

have for subsequentevents that occur afterthe issue

date?

period subsequent events period under audit

12/31 2/14 2/28

balance sheet field work report date completion issue date

21 - 32Copyright 2003 Pearson Education Canada Inc.

Whatresponsibility

does the auditor

have for subsequentevents that occur afterthe issue

date?

period subsequent events period under audit

12/31 2/14 2/28

balance sheet field work report date completion issue date

Auditors have no obligation toperform additional proceduresafter the report date unlessthey become aware of factsthat existed at the report date.

21 - 33Copyright 2003 Pearson Education Canada Inc.

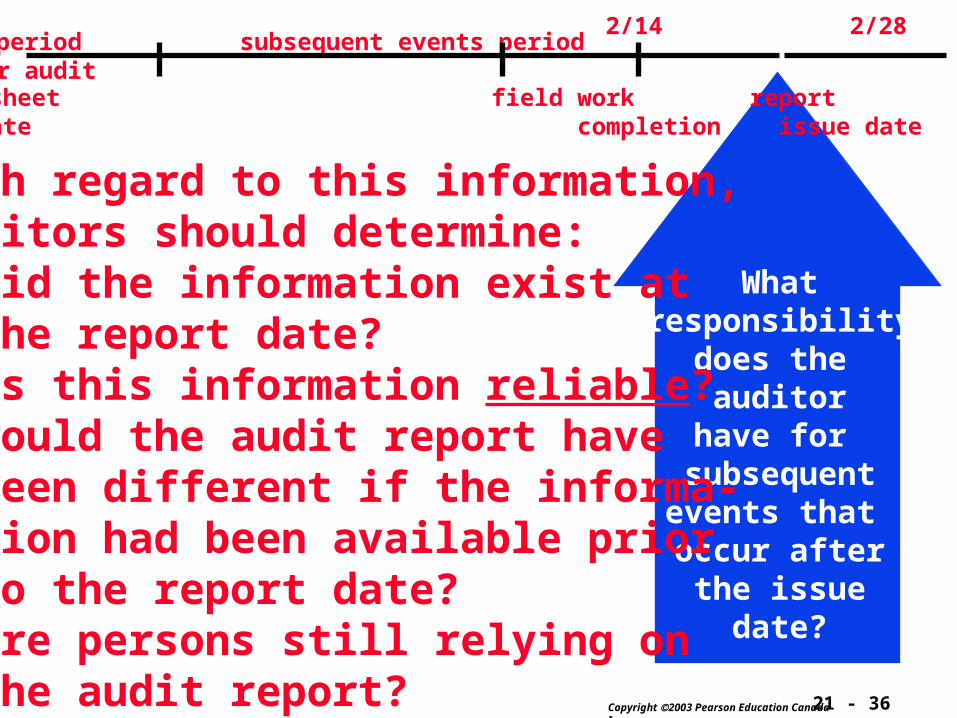

Whatresponsibility

does the auditor

have for subsequentevents that occur afterthe issue

date?

With regard to this information,auditors should determine:- did the information exist at the report date?

period subsequent events period under audit

12/31 2/14 2/28

balance sheet field work report date completion issue date

21 - 34Copyright 2003 Pearson Education Canada Inc.

Whatresponsibility

does the auditor

have for subsequentevents that occur afterthe issue

date?

With regard to this information,auditors should determine:- did the information exist at the report date?- is the information reliable?

period subsequent events period under audit

12/31 2/14 2/28

balance sheet field work report date completion issue date

21 - 35Copyright 2003 Pearson Education Canada Inc.

Whatresponsibility

does the auditor

have for subsequentevents that occur afterthe issue

date?

With regard to this information,auditors should determine:- did the information exist at the report date?- is the information reliable?- would the audit report have been different if the informa- tion had been available prior to the report date?

period subsequent events period under audit

12/31 2/14 2/28

balance sheet field work report date completion issue date

21 - 36Copyright 2003 Pearson Education Canada Inc.

Whatresponsibility

does the auditor

have for subsequentevents that occur afterthe issue

date?

With regard to this information,auditors should determine:- did the information exist at the report date?- is this information reliable?- would the audit report have been different if the informa- tion had been available prior to the report date?- are persons still relying on the audit report?

period subsequent events period under audit

12/31 2/14 2/28

balance sheet field work report date completion issue date

21 - 37Copyright 2003 Pearson Education Canada Inc.

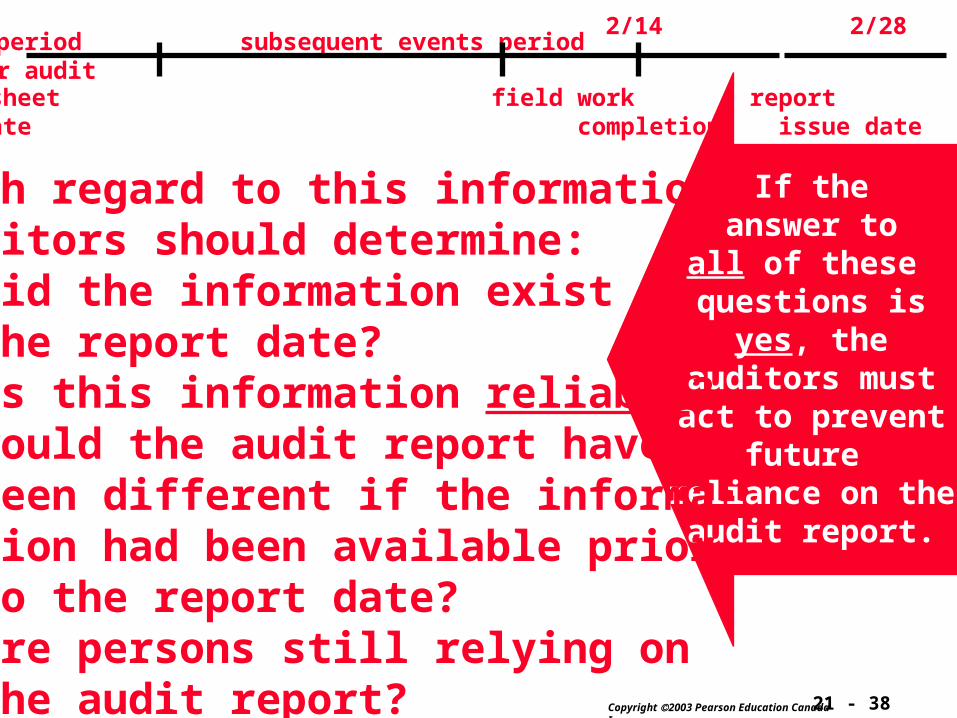

If theanswer to

any of these questions is

no, theauditors donot need to

take anyaction.

With regard to this information,auditors should determine:- did the information exist at the report date?- is this information reliable?- would the audit report have been different if the informa- tion had been available prior to the report date?- are persons still relying on the audit report?

period subsequent events period under audit

12/31 2/14 2/28

balance sheet field work report date completion issue date

21 - 38Copyright 2003 Pearson Education Canada Inc.

If theanswer to

all of these questions is

yes, theauditors mustact to prevent

future reliance on the

audit report.

With regard to this information,auditors should determine:- did the information exist at the report date?- is this information reliable?- would the audit report have been different if the informa- tion had been available prior to the report date?- are persons still relying on the audit report?

period subsequent events period under audit

12/31 2/14 2/28

balance sheet field work report date completion issue date

21 - 39Copyright 2003 Pearson Education Canada Inc.

How do auditors How do auditors prevent future prevent future reliancereliance on a on a previously-issuedpreviously-issued

audit report?audit report?

Auditors’ Report

ggsfggsfrrff fsfftershj dytudtyiuhhfd fjty7yhrngag dgaroihaongn faidfnad faosdfnandsfafd

ggsfggsfrrff fsfftershj dytudtyiuhhfd fjty7yhrngag dgaroihaongn faidfnad faosdfnandsfafd

ggsfggsfrrff fsfftershj dytudtyiuhhfd fjty7yhrngag dgaroihaongn faidfnad faosdfnandsfafd

ggsfggsfrrff fsfftershj dytudtyiuhhfd fjty7yhrngag dgaroihaongn faidfnad faosdfnandsfafd

ggsfggsfrrff fsfftershj dytudtyiuhhfd fjty7yhrngag dgaroihaongn faidfnad faosdfnandsfafd

ggsfggsfrrff fsfftershj dytudtyiuhhfd fjty7yhrngag dgaroihaongn faidfnad faosdfnandsfafd

ggsfggsfrrff fsfftershj dytudtyiuhhfd fjty7yhrngag dgaroihaongn faidfnad faosdfnandsfafd

ggsfggsfrrff fsfftershj dytudtyiuhhfd fjty7yhrngag dgaroihaongn faidfnad faosdfnandsfafd

ggsfggsfrrff fsfftershj dytudtyiuhhfd fjty7yhrngag dgaroihaongn faidfnad faosdfnandsfafd

21 - 40Copyright 2003 Pearson Education Canada Inc.

the client must reviseand reissue the

financial statements

How do auditors How do auditors prevent future prevent future reliancereliance on a on a previously-issuedpreviously-issued

audit report?audit report?If the financial statement effect of the subsequently-discovered information

can be determined promptly

21 - 41Copyright 2003 Pearson Education Canada Inc.

the client must notify persons known to be (and those likely to be) relying

on the financial statements

How do auditors How do auditors prevent future prevent future reliancereliance on a on a previously-issuedpreviously-issued

audit report?audit report?If the financial statement effect of the subsequently-discovered information

cannot be determined promptly

21 - 42Copyright 2003 Pearson Education Canada Inc.

What should the auditor do if the client What should the auditor do if the client refusesrefuses to reissue the statements or contact to reissue the statements or contact

those relying on the auditors’ report?those relying on the auditors’ report?

reviseand

reissue?NO!

21 - 43Copyright 2003 Pearson Education Canada Inc.

What should the auditor do if the client What should the auditor do if the client refusesrefuses to reissue the statements or contact to reissue the statements or contact

those relying on the auditors’ report?those relying on the auditors’ report?

-first, notify the audit committee, or other body, such as the board, of management’s refusal

21 - 44Copyright 2003 Pearson Education Canada Inc.

What should the auditor do if the client What should the auditor do if the client refusesrefuses to reissue the statements or contact to reissue the statements or contact

those relying on the auditors’ report?those relying on the auditors’ report?- first, notify the audit committee, etc. of management’s refusal- then: ~ inform client management that the audit report may no longer be associated with the statements

21 - 45Copyright 2003 Pearson Education Canada Inc.

What should the auditor do if the client What should the auditor do if the client refusesrefuses to reissue the statements or contact to reissue the statements or contact

those relying on the auditors’ report?those relying on the auditors’ report?

- first, notify the audit committee, etc. of management’s refusal- then: ~ inform client management that the audit report may no longer be associated with the statements ~ consider obtaining legal advice

21 - 46Copyright 2003 Pearson Education Canada Inc.

What should the auditor do if the client What should the auditor do if the client refusesrefuses to reissue the statements or contact to reissue the statements or contact

those relying on the auditors’ report?those relying on the auditors’ report?- first, notify the audit committee, etc. of management’s refusal- then: ~ inform client management that the audit report may no longer be associated with the statements ~ consider obtaining legal advice ~ consider the appropriateness of other actions such as withdrawing

21 - 47Copyright 2003 Pearson Education Canada Inc.

Client Representation LetterClient Representation Letter

?

21 - 48Copyright 2003 Pearson Education Canada Inc.

Client Representation LetterClient Representation Letter

The auditor must obtain a letter from the client documenting the client’s represen-tations during the engagement.

% $@!!!}{ @@?”{+&*##@

ClientRepresentation

Letter

% $@!!!}{ @@?”{+&*##@

21 - 49Copyright 2003 Pearson Education Canada Inc.

Client Representation LetterClient Representation Letter

The auditor must obtain a letter from the client documenting the client’s represen-tations during the engagement.

The primary purposes are to:- confirm and document oral statements- reduce auditor-client misunderstanding- remind management of its responsibili- ty for the financial statements

21 - 50Copyright 2003 Pearson Education Canada Inc.

Client Representation LetterClient Representation LetterThe auditor must obtain a letter from the client documenting the client’s represen-tations during the engagement.

The primary purposes are to:- confirm and document oral statements- reduce auditor-client misunderstanding- remind management of responsibilitiesThe letter should be signed by the clientCFO and CEO and dated with the fieldwork completion date.

21 - 51Copyright 2003 Pearson Education Canada Inc.

Client Representation LetterClient Representation Letter

If the client refuses toIf the client refuses togive the auditor a give the auditor a

representation letter, representation letter, the auditor must the auditor must qualifyqualify

or or denydeny the opinion. the opinion.

probable

21 - 52Copyright 2003 Pearson Education Canada Inc.

Final Audit StepsFinal Audit Steps

1. Incorporating all audit evidence, materiality, and judgment, the auditor draws overall conclusions and prepares the audit report.

21 - 53Copyright 2003 Pearson Education Canada Inc.

Final Audit StepsFinal Audit Steps1. Incorporating all audit evidence, materiality, and judgment, the auditor draws overall conclusions and prepares the audit report.2. The auditor prepares the management letter.

?

21 - 54Copyright 2003 Pearson Education Canada Inc.

Final Audit StepsFinal Audit Steps1. Incorporating all audit evidence, materiality, and judgment, the auditor draws overall conclusions and prepares the audit report.2. The auditor prepares the management letter.

recommendations forimproving the client business

21 - 55Copyright 2003 Pearson Education Canada Inc.

Final Audit StepsFinal Audit Steps1. Incorporating all audit evidence, materiality, and judgment, the auditor draws overall conclusions and prepares the audit report.2. The auditor prepares the management letter.3. The auditor communicates the results to the audit committee/management and gives them the audit report and management letter.

21 - 56Copyright 2003 Pearson Education Canada Inc.

GAAS GAAS suggestssuggests that auditors to that auditors to communicate (oral or written) to audit communicate (oral or written) to audit

committees, etc.:committees, etc.:

- the auditor’s responsibilities under GAAS

21 - 57Copyright 2003 Pearson Education Canada Inc.

GAAS suggests that auditors GAAS suggests that auditors communicate (oral or written) to audit communicate (oral or written) to audit

committees, etc.:committees, etc.:

- the auditor’s responsibilities under GAAS- significant accounting policies selected, & judgments used by management

21 - 58Copyright 2003 Pearson Education Canada Inc.

GAAS suggests that auditors GAAS suggests that auditors communicate (oral or written) to audit communicate (oral or written) to audit

committees, etc.:committees, etc.:- the auditor’s responsibilities under GAAS- significant accounting policies selected, & judgments used by management- audit planning

21 - 59Copyright 2003 Pearson Education Canada Inc.

GAAS suggests that auditors GAAS suggests that auditors communicate (oral or written) to audit communicate (oral or written) to audit

committees, etc.:committees, etc.:- the auditor’s responsibilities under GAAS- significant accounting policies selected, & judgments used by management- audit planning- disagreements with management

21 - 60Copyright 2003 Pearson Education Canada Inc.

GAAS suggests that auditors GAAS suggests that auditors communicate (oral or written) to audit communicate (oral or written) to audit

committees, etc.:committees, etc.:- the auditor’s responsibilities under GAAS- significant accounting policies selected, & judgments used by management- audit planning- disagreements with management- difficulties in performing the audit

21 - 61Copyright 2003 Pearson Education Canada Inc.

GAAS suggests that auditors GAAS suggests that auditors communicate (oral or written) to audit communicate (oral or written) to audit

committees, etc.:committees, etc.:- the auditor’s responsibilities under GAAS- significant accounting policies selected, & judgments used by management- audit planning- disagreements with management- difficulties in performing the audit- consultations with other accountants

21 - 62Copyright 2003 Pearson Education Canada Inc.

What are the What are the requiredrequired communications with the communications with the

audit committee, etc.?audit committee, etc.?

21 - 63Copyright 2003 Pearson Education Canada Inc.

What are other suggested What are other suggested communications with the communications with the

audit committee?audit committee?

- significant deficiencies in internal control- misstatements that are other than trivial- illegal or possible illegal acts