2h16 telecom industry outlook

TRANSCRIPT

Telecom Service Solid downside support and decent growth potential

In late phase of LTE era: Consumption diverging and becoming rational

LTE technology came to Korea in end-2011. Nearly five years later, the domestic telecom service industry is now entering the late phase of the LTE era. During the initial high-growth phase, early adopters purchased expensive handsets and subscribed to high-priced rate plans. Now, telecom service consumption trends are changing. 1) First, consumption is diverging, with the gap between telcos’ average rates and MVNO rates widening further this year, compared to 2012. 2) Second, consumers are becoming more rational. Low- to mid-end handset purchases out of all purchases are estimated to be near 30%, from less than 10% in 2012. In addition, the cumulative number of subscribers who have chosen a rate discount in lieu of subsidies has surpassed 10% of overall mobile subscribers.

Risks from telecom plan restrictions; Opportunities from growing data usage and business expansion

The most serious threat to telcos in 2H should be downward pressure on plan prices. Once the new National Assembly takes office in June, a revision to the handset distribution act and a bill related to telecom plan restrictions will likely be proposed. With ARPU growth slowing and service rate discounts being booked as sales discounts, telcos must find ways to deal with the growing pressure to lower telecom bills. In our view, they could point to the following facts to justify current rates: 1) Telecom expenses as a percentage of household spending have steadily decreased over the past decade. 2) Handset purchase expenses are a bigger driver of household spending growth than service plans. 3) Data plans are cheaper in Korea than in other countries.

On the bright side, we believe telcos will find opportunities from high-priced rate plans amid growing data usage. In addition, telcos are expanding aggressively into new business areas, with a particular growing influence in the media business. Furthermore, capitalizing on nationwide IoT networks, telcos are planning full-swing launch of low-power wide-area network (LPWAN) services.

2H: Attractive dividend payout; Aggressive expansion; Retain Overweight

Free cash flow at domestic telcos is improving markedly. Capex has been on the downswing in the era of advanced telecom technology, while variable costs have also decreased due to stable marketing competition. Given stable earnings and ample cash flow, we expect telcos to show attractive dividend payout. If shares correct due to regulatory risks, high dividend yields should provide downside support. Telcos’ growth prospects also appear decent in light of their aggressive business expansion.

We retain our Overweight rating on the telecom sector. In the short term, we recommend KT in light of its high earnings visibility and dividend growth. And from a longer-term perspective (through the end of the year), we recommend SK Telecom (SKT) given its high dividend payout and aggressive business expansion.

Overweight (Maintain)

2H16 Outlook Report

June 3, 2016

Mirae Asset Daewoo Co., Ltd.

[Telecom Service / Media]

Jee-hyun Moon

+822-768-3615

Nu-ri Ha

+822-768-4130

Korean telecom service industry index long-term trend: Key variables are ARPU,

dividends, and new businesses

Note: KOSPI divided by 50 to show on same axis as telecom index; Telecom index is FTSE Korea Telecom Index;

Source: Thomson Reuters, respective companies’ data, Mirae Asset Daewoo Research

25

30

35

40

45

50

28,000

30,500

33,000

35,500

38,000

04 05 06 07 08 09 10 11 12 13 14 15 16F 17F 18F

(p)(W)

Average ARPU of three big telcos (L)

Telecom service industry index (R)

KOSPI/50 (R)LTE introduction

[Increased dividends; New businesses]Downside support, growth potential

Telecom sector trading range

may rise

Telecom Service

2

June 3, 2016

Mirae Asset Daewoo Research

C O N T E N T S

Industry trends: Entering late phase of LTE era 3 1. Consumption diverging 3 2. Consumers becoming increasingly rational 4 3. Cash utilization 5

Risks in 2H: Regulations 6 1. Pressure to cut telecom rates 6 2. How to handle growing pressure to lower monthly bills 7

Opportunities in 2H16: Growth strategy 9 1. Wireless 9 2. Media 14 3. Internet of Things (IoT) 20

Investment & valuation 22 1. Attractive dividend yields 22 2. Investment strategy 23 3. Valuation comparison 24

KT (030200 KS) 25 SK Telecom (017670 KS) 28 LG Uplus (032640 KS) 31

Telecom Service

3

June 3, 2016

Mirae Asset Daewoo Research

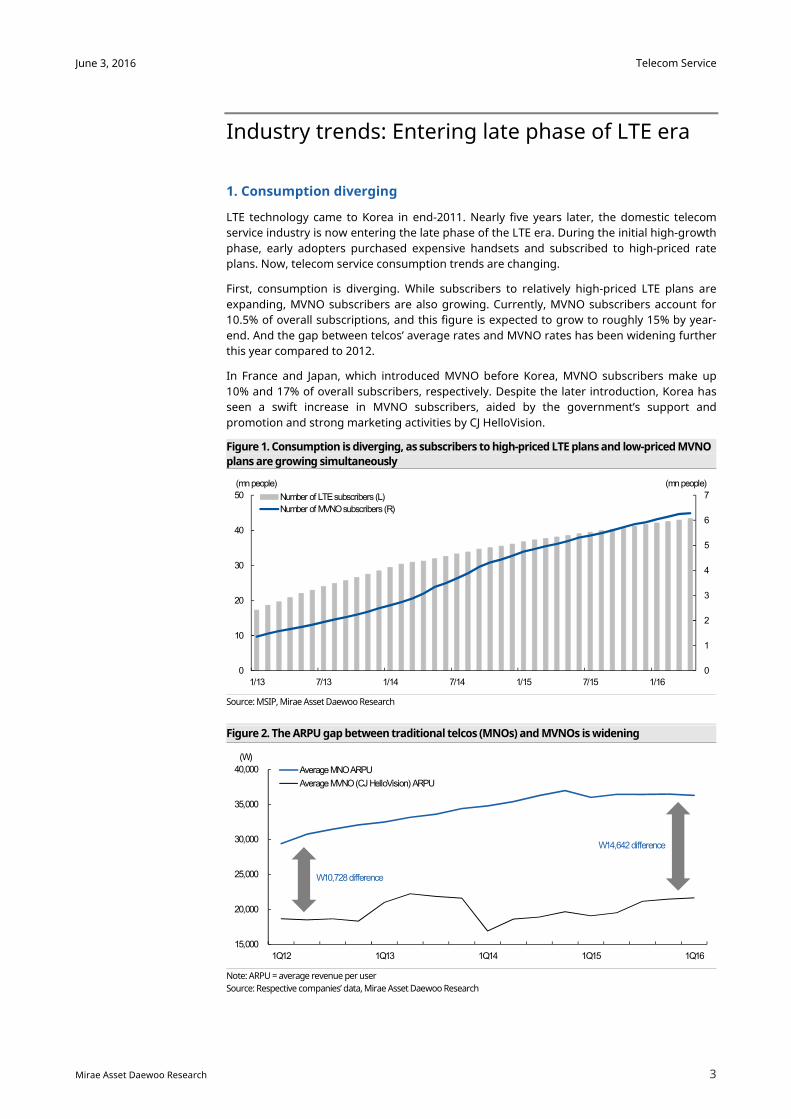

Industry trends: Entering late phase of LTE era

1. Consumption diverging

LTE technology came to Korea in end-2011. Nearly five years later, the domestic telecom

service industry is now entering the late phase of the LTE era. During the initial high-growth

phase, early adopters purchased expensive handsets and subscribed to high-priced rate

plans. Now, telecom service consumption trends are changing.

First, consumption is diverging. While subscribers to relatively high-priced LTE plans are

expanding, MVNO subscribers are also growing. Currently, MVNO subscribers account for

10.5% of overall subscriptions, and this figure is expected to grow to roughly 15% by year-

end. And the gap between telcos’ average rates and MVNO rates has been widening further

this year compared to 2012.

In France and Japan, which introduced MVNO before Korea, MVNO subscribers make up

10% and 17% of overall subscribers, respectively. Despite the later introduction, Korea has

seen a swift increase in MVNO subscribers, aided by the government’s support and

promotion and strong marketing activities by CJ HelloVision.

Figure 1. Consumption is diverging, as subscribers to high-priced LTE plans and low-priced MVNO

plans are growing simultaneously

Source: MSIP, Mirae Asset Daewoo Research

Figure 2. The ARPU gap between traditional telcos (MNOs) and MVNOs is widening

Note: ARPU = average revenue per user

Source: Respective companies’ data, Mirae Asset Daewoo Research

0

1

2

3

4

5

6

7

0

10

20

30

40

50

1/13 7/13 1/14 7/14 1/15 7/15 1/16

(mn people)(mn people)

Number of LTE subscribers (L)

Number of MVNO subscribers (R)

W10,728 difference

W14,642 difference

15,000

20,000

25,000

30,000

35,000

40,000

1Q12 1Q13 1Q14 1Q15 1Q16

(W)

Average MNO ARPU

Average MVNO (CJ HelloVision) ARPU

Telecom Service

4

June 3, 2016

Mirae Asset Daewoo Research

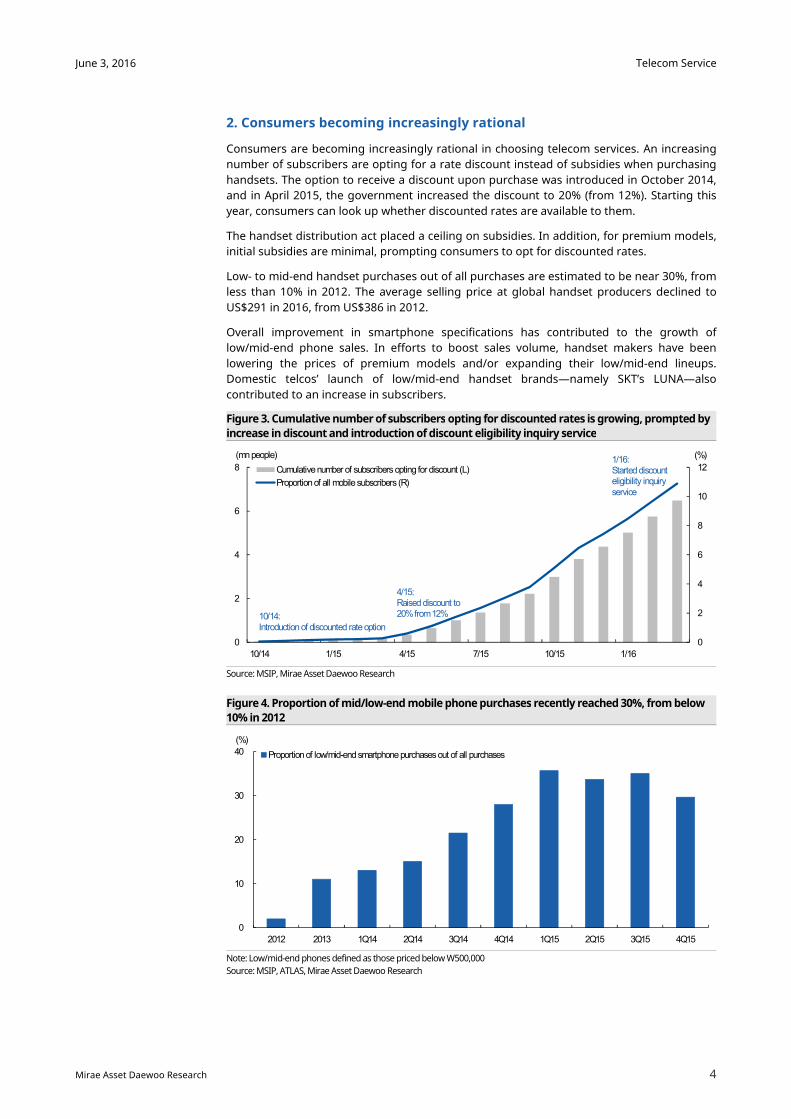

2. Consumers becoming increasingly rational

Consumers are becoming increasingly rational in choosing telecom services. An increasing

number of subscribers are opting for a rate discount instead of subsidies when purchasing

handsets. The option to receive a discount upon purchase was introduced in October 2014,

and in April 2015, the government increased the discount to 20% (from 12%). Starting this

year, consumers can look up whether discounted rates are available to them.

The handset distribution act placed a ceiling on subsidies. In addition, for premium models,

initial subsidies are minimal, prompting consumers to opt for discounted rates.

Low- to mid-end handset purchases out of all purchases are estimated to be near 30%, from

less than 10% in 2012. The average selling price at global handset producers declined to

US$291 in 2016, from US$386 in 2012.

Overall improvement in smartphone specifications has contributed to the growth of

low/mid-end phone sales. In efforts to boost sales volume, handset makers have been

lowering the prices of premium models and/or expanding their low/mid-end lineups.

Domestic telcos’ launch of low/mid-end handset brands—namely SKT’s LUNA—also

contributed to an increase in subscribers.

Figure 3. Cumulative number of subscribers opting for discounted rates is growing, prompted by

increase in discount and introduction of discount eligibility inquiry service

Source: MSIP, Mirae Asset Daewoo Research

Figure 4. Proportion of mid/low-end mobile phone purchases recently reached 30%, from below

10% in 2012

Note: Low/mid-end phones defined as those priced below W500,000

Source: MSIP, ATLAS, Mirae Asset Daewoo Research

0

10

20

30

40

2012 2013 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

(%)

Proportion of low/mid-end smartphone purchases out of all purchases

0

2

4

6

8

10

12

0

2

4

6

8

10/14 1/15 4/15 7/15 10/15 1/16

(%)(mn people)

Cumulative number of subscribers opting for discount (L)

Proportion of all mobile subscribers (R)

4/15:Raised discount to20% from 12%

1/16:Started discounteligibility inquiryservice

10/14:Introductionof discounted rate option

Telecom Service

5

June 3, 2016

Mirae Asset Daewoo Research

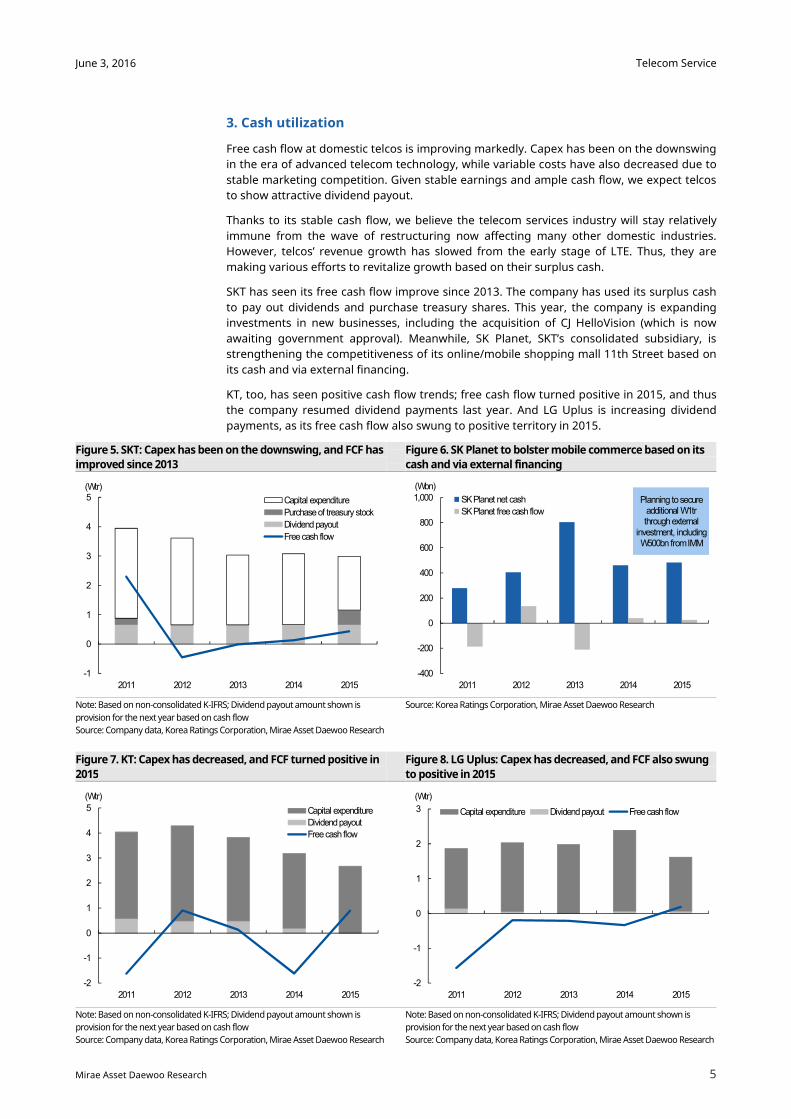

3. Cash utilization

Free cash flow at domestic telcos is improving markedly. Capex has been on the downswing

in the era of advanced telecom technology, while variable costs have also decreased due to

stable marketing competition. Given stable earnings and ample cash flow, we expect telcos

to show attractive dividend payout.

Thanks to its stable cash flow, we believe the telecom services industry will stay relatively

immune from the wave of restructuring now affecting many other domestic industries.

However, telcos’ revenue growth has slowed from the early stage of LTE. Thus, they are

making various efforts to revitalize growth based on their surplus cash.

SKT has seen its free cash flow improve since 2013. The company has used its surplus cash

to pay out dividends and purchase treasury shares. This year, the company is expanding

investments in new businesses, including the acquisition of CJ HelloVision (which is now

awaiting government approval). Meanwhile, SK Planet, SKT’s consolidated subsidiary, is

strengthening the competitiveness of its online/mobile shopping mall 11th Street based on

its cash and via external financing.

KT, too, has seen positive cash flow trends; free cash flow turned positive in 2015, and thus

the company resumed dividend payments last year. And LG Uplus is increasing dividend

payments, as its free cash flow also swung to positive territory in 2015.

Figure 5. SKT: Capex has been on the downswing, and FCF has

improved since 2013

Figure 6. SK Planet to bolster mobile commerce based on its

cash and via external financing

Note: Based on non-consolidated K-IFRS; Dividend payout amount shown is

provision for the next year based on cash flow

Source: Company data, Korea Ratings Corporation, Mirae Asset Daewoo Research

Source: Korea Ratings Corporation, Mirae Asset Daewoo Research

Figure 7. KT: Capex has decreased, and FCF turned positive in

2015

Figure 8. LG Uplus: Capex has decreased, and FCF also swung

to positive in 2015

Note: Based on non-consolidated K-IFRS; Dividend payout amount shown is

provision for the next year based on cash flow

Source: Company data, Korea Ratings Corporation, Mirae Asset Daewoo Research

Note: Based on non-consolidated K-IFRS; Dividend payout amount shown is

provision for the next year based on cash flow

Source: Company data, Korea Ratings Corporation, Mirae Asset Daewoo Research

-1

0

1

2

3

4

5

2011 2012 2013 2014 2015

(Wtr)

Capital expenditure

Purchase of treasury stock

Dividend payout

Free cash flow

-2

-1

0

1

2

3

4

5

2011 2012 2013 2014 2015

(Wtr)

Capital expenditure

Dividend payout

Free cash flow

-2

-1

0

1

2

3

2011 2012 2013 2014 2015

(Wtr)

Capital expenditure Dividend payout Free cash flow

-400

-200

0

200

400

600

800

1,000

2011 2012 2013 2014 2015

(Wbn)

SK Planet net cash

SK Planet free cash flow

Planning to secure additional W1tr through external

investment, including W500bn from IMM

Telecom Service

6

June 3, 2016

Mirae Asset Daewoo Research

Risks in 2H: Regulations

1. Pressure to cut telecom rates

The most serious threat to telcos in 2H should be downward pressure on plan prices. Once

the new National Assembly takes office in June, a revision to the handset distribution act

and a bill related to telecom plan restrictions will likely be proposed. As of now, both the

ruling and opposition parties have agreed on the necessity of revising the handset

distribution law to ease households’ telecommunications cost burden.

In addition to a separate subsidy disclosure scheme and separation of phone distribution

and phone services, measures to abolish the base fee and apply caps on handset subsidies

are also being discussed. Such policy trends should negatively affect telcos’ earnings.

With regard to potential abolition of the base fee, the plans that include base fees are

mostly usage-based schemes that were more common in the past, when voice calling was

popular. Today’s data-centric tariff schemes are mostly fixed-rate plans that do not charge

base fees. As such, abolition of the base fee would likely not have a meaningful impact on

telcos’ earnings.

SKT’s standard plan sets its base fee at W11,000 (or W12,100, including the surtax), with

voice calls charged at W1.8/s (inclusive of 50 free text messages). The National Assembly has

also set the base fee target at W11,000. Subscribers are mostly feature phone users,

because the data rate (W0.25/0.5KB) is not attractive to smartphone users. Meanwhile, the

carrier’s Band Data plans (for LTE services) are offered in eight different tiers (according to

the amount of data), and a fixed sum is charged depending on the tiers. These plans do not

charge base fees.

As the amount of subsidies given to handset buyers is already lower than the subsidy cap

on average, and call/data plan discounts are being opted for widely (by subscribers that

choose to buy phones without subsidies), removing subsidy caps is unlikely to have as

strong an impact on telcos as the mounting pressure to lower telecom bills.

Table 1. Telecom-related bills (estimate)

The Minjoo Saenuri People's Party Justice Party

Plan/ Position

Submit revisions to MCTDSIA Submit revisions to MCTDSIA Recognize the need to revise MCTDSIA

Recognize the need to revise MCTDSIA

Details 1. Removal of subsidiary caps 1. Removal of subsidiary caps

* The People's Party and the Justice Party have yet to state their views on MCTDSIA revisions, except that they did not believe

the revision would effectively lower household mobile bills.

- Lower household mobile bills - Encourage price competition

2. Removal of base fees 2. Reduction in base fees

- Lower household mobile bills - Reduce household mobile bills

3. Separation of subsidies (carriers

and manufacturers) 3. Separation of subsidies

(carriers and manufacturers)

- Ensure transparent business

practices of carriers and their

retailers

- Ensure transparent business practices of carriers and their

retailers

4. Introduction of the blacklist system

- Prevent collusion between carriers

and manufacturers

- Promote fair competition

Source: Media reports, Mirae Asset Daewoo Research

Figure 9. Simple usage-based monthly plan with base fee of

W11,000

Figure 10. Data-centric monthly plan with no separate base

fee

Source: SKT, Mirae Asset Daewoo Research Source: SKT, Mirae Asset Daewoo Research

Telecom Service

7

June 3, 2016

Mirae Asset Daewoo Research

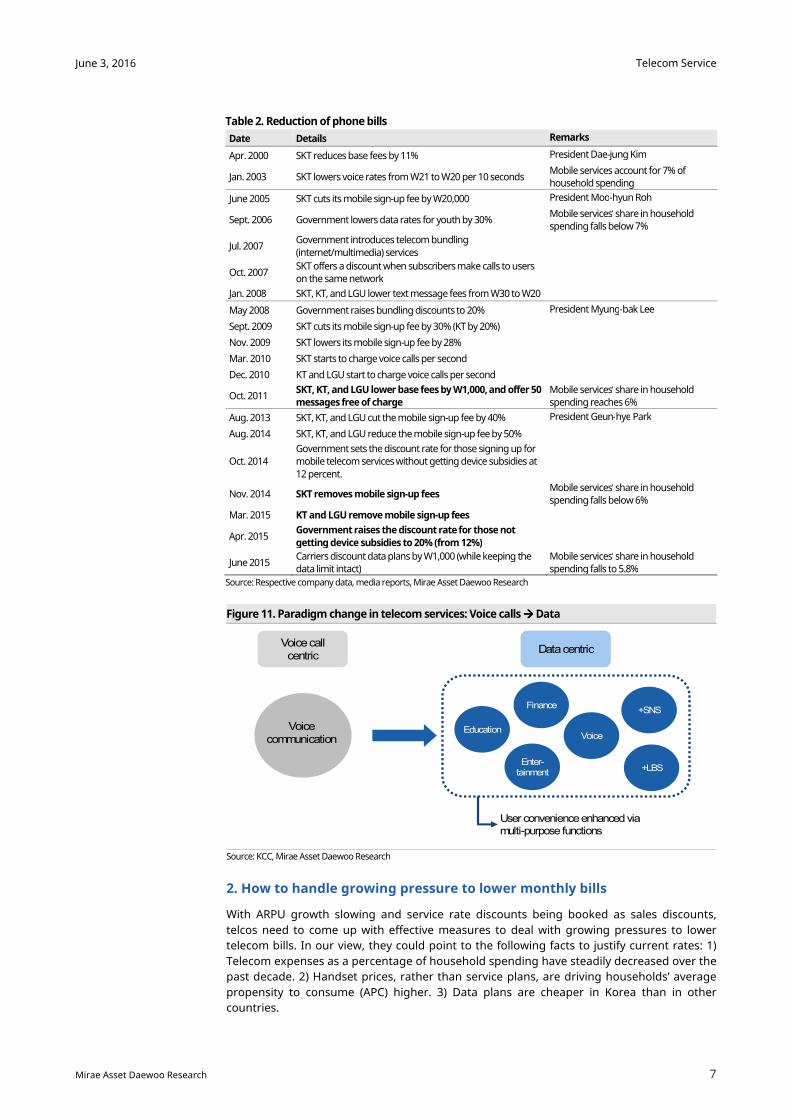

Table 2. Reduction of phone bills

Date Details Remarks

Apr. 2000 SKT reduces base fees by 11% President Dae-jung Kim

Jan. 2003 SKT lowers voice rates from W21 to W20 per 10 seconds Mobile services account for 7% of household spending

June 2005 SKT cuts its mobile sign-up fee by W20,000 President Moo-hyun Roh

Sept. 2006 Government lowers data rates for youth by 30% Mobile services’ share in household spending falls below 7%

Jul. 2007 Government introduces telecom bundling

(internet/multimedia) services

Oct. 2007 SKT offers a discount when subscribers make calls to users on the same network

Jan. 2008 SKT, KT, and LGU lower text message fees from W30 to W20

May 2008 Government raises bundling discounts to 20% President Myung-bak Lee

Sept. 2009 SKT cuts its mobile sign-up fee by 30% (KT by 20%)

Nov. 2009 SKT lowers its mobile sign-up fee by 28%

Mar. 2010 SKT starts to charge voice calls per second

Dec. 2010 KT and LGU start to charge voice calls per second

Oct. 2011 SKT, KT, and LGU lower base fees by W1,000, and offer 50 messages free of charge

Mobile services’ share in household spending reaches 6%

Aug. 2013 SKT, KT, and LGU cut the mobile sign-up fee by 40% President Geun-hye Park

Aug. 2014 SKT, KT, and LGU reduce the mobile sign-up fee by 50%

Oct. 2014 Government sets the discount rate for those signing up for mobile telecom services without getting device subsidies at

12 percent.

Nov. 2014 SKT removes mobile sign-up fees Mobile services’ share in household spending falls below 6%

Mar. 2015 KT and LGU remove mobile sign-up fees

Apr. 2015 Government raises the discount rate for those not

getting device subsidies to 20% (from 12%)

June 2015 Carriers discount data plans by W1,000 (while keeping the data limit intact)

Mobile services’ share in household spending falls to 5.8%

Source: Respective company data, media reports, Mirae Asset Daewoo Research

Figure 11. Paradigm change in telecom services: Voice calls ���� Data

Source: KCC, Mirae Asset Daewoo Research

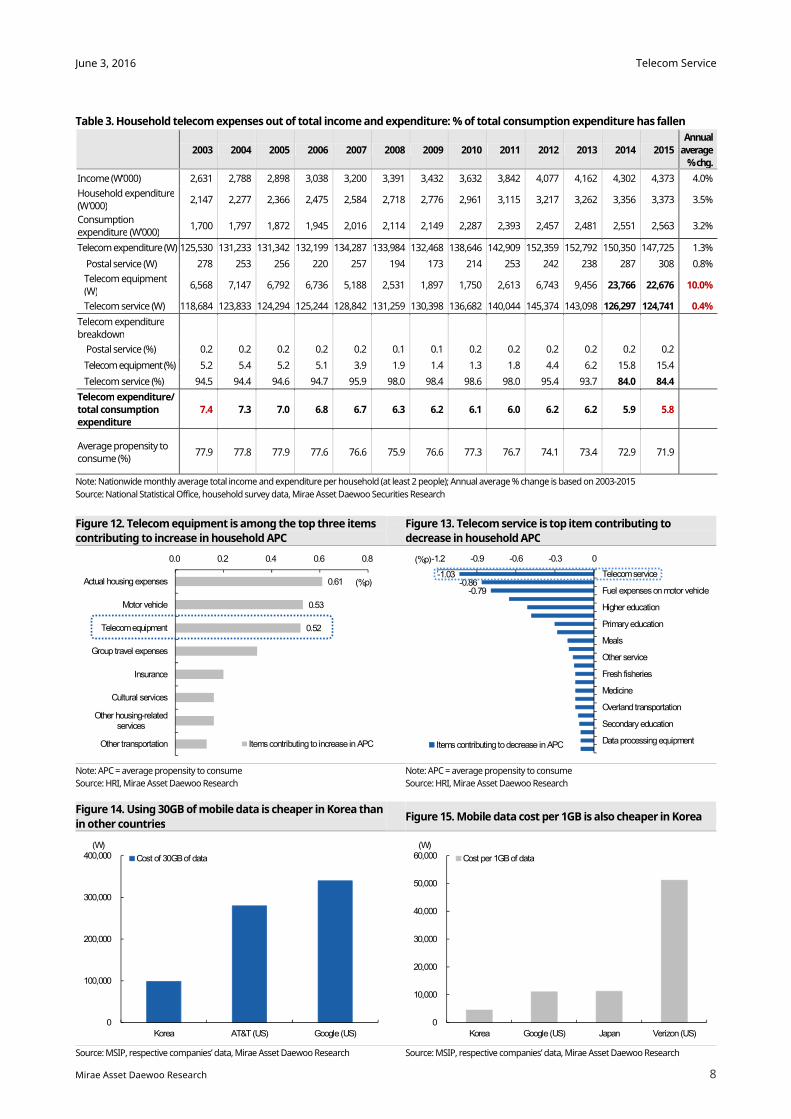

2. How to handle growing pressure to lower monthly bills

With ARPU growth slowing and service rate discounts being booked as sales discounts,

telcos need to come up with effective measures to deal with growing pressures to lower

telecom bills. In our view, they could point to the following facts to justify current rates: 1)

Telecom expenses as a percentage of household spending have steadily decreased over the

past decade. 2) Handset prices, rather than service plans, are driving households’ average

propensity to consume (APC) higher. 3) Data plans are cheaper in Korea than in other

countries.

Voice callcentric

Data centric

Education

Finance+SNS

+LBS

Voice

Enter-tainment

User convenienceenhanced via multi-purpose functions

Voice communication

Telecom Service

8

June 3, 2016

Mirae Asset Daewoo Research

Table 3. Household telecom expenses out of total income and expenditure: % of total consumption expenditure has fallen

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Annual

average % chg.

Income (W’000) 2,631 2,788 2,898 3,038 3,200 3,391 3,432 3,632 3,842 4,077 4,162 4,302 4,373 4.0%

Household expenditure (W’000)

2,147 2,277 2,366 2,475 2,584 2,718 2,776 2,961 3,115 3,217 3,262 3,356 3,373 3.5%

Consumption expenditure (W’000)

1,700 1,797 1,872 1,945 2,016 2,114 2,149 2,287 2,393 2,457 2,481 2,551 2,563 3.2%

Telecom expenditure (W) 125,530 131,233 131,342 132,199 134,287 133,984 132,468 138,646 142,909 152,359 152,792 150,350 147,725 1.3%

Postal service (W) 278 253 256 220 257 194 173 214 253 242 238 287 308 0.8%

Telecom equipment (W)

6,568 7,147 6,792 6,736 5,188 2,531 1,897 1,750 2,613 6,743 9,456 23,766 22,676 10.0%

Telecom service (W) 118,684 123,833 124,294 125,244 128,842 131,259 130,398 136,682 140,044 145,374 143,098 126,297 124,741 0.4%

Telecom expenditure breakdown

Postal service (%) 0.2 0.2 0.2 0.2 0.2 0.1 0.1 0.2 0.2 0.2 0.2 0.2 0.2

Telecom equipment (%) 5.2 5.4 5.2 5.1 3.9 1.9 1.4 1.3 1.8 4.4 6.2 15.8 15.4

Telecom service (%) 94.5 94.4 94.6 94.7 95.9 98.0 98.4 98.6 98.0 95.4 93.7 84.0 84.4

Telecom expenditure/ total consumption expenditure

7.4 7.3 7.0 6.8 6.7 6.3 6.2 6.1 6.0 6.2 6.2 5.9 5.8

Average propensity to consume (%)

77.9 77.8 77.9 77.6 76.6 75.9 76.6 77.3 76.7 74.1 73.4 72.9 71.9

Note: Nationwide monthly average total income and expenditure per household (at least 2 people); Annual average % change is based on 2003-2015

Source: National Statistical Office, household survey data, Mirae Asset Daewoo Securities Research

Figure 12. Telecom equipment is among the top three items

contributing to increase in household APC

Figure 13. Telecom service is top item contributing to

decrease in household APC

Note: APC = average propensity to consume

Source: HRI, Mirae Asset Daewoo Research

Note: APC = average propensity to consume

Source: HRI, Mirae Asset Daewoo Research

Figure 14. Using 30GB of mobile data is cheaper in Korea than

in other countries Figure 15. Mobile data cost per 1GB is also cheaper in Korea

Source: MSIP, respective companies’ data, Mirae Asset Daewoo Research Source: MSIP, respective companies’ data, Mirae Asset Daewoo Research

0

100,000

200,000

300,000

400,000

Korea AT&T (US) Google (US)

(W)

Cost of 30GB of data

0

10,000

20,000

30,000

40,000

50,000

60,000

Korea Google (US) Japan Verizon (US)

(W)

Cost per 1GB of data

0.61

0.53

0.52

0.0 0.2 0.4 0.6 0.8

Actual housing expenses

Motor vehicle

Telecom equipment

Group travel expenses

Insurance

Cultural services

Other housing-relatedservices

Other transportation

(%p)

Items contributing to increase in APC

-1.03-0.86

-0.79

-1.2 -0.9 -0.6 -0.3 0

Telecom service

Fuel expenses on motor vehicle

Higher education

Primary education

Meals

Other service

Fresh fisheries

Medicine

Overland transportation

Secondary education

Data processing equipment

(%p)

Items contributing to decrease in APC

Telecom Service

9

June 3, 2016

Mirae Asset Daewoo Research

Opportunities in 2H16: Growth strategy

1. Wireless

1) Wireless service

We believe one of the biggest opportunities for telcos is higher prices driven by higher data

usage. In April 2016, monthly LTE data usage per subscriber was up 33.3% YoY to 4.66GB.

Following the launch of data-oriented plans in May 2015, the average price level of data

plans slightly fell, whereas the amount of data available remained unchanged. Since then,

the number of subscribers has decreased for plans priced at W60,000 or above, but has

increased for plans priced in the W40,000-W50,000 range. In the short term, this is likely to

have an adverse effect on overall average prices.

In the medium term, however, we believe lower prices have eased the entry barrier to data

usage. The availability of plans offering more data at lower price points has made it easier

for customers, who previously used 2GB per month, to sharply increase their monthly usage

to 5GB.

At present, we believe video streaming accounts for roughly 80% of data usage. Every year,

data consumption tends to pick up in the third quarter, when the professional baseball

season gets underway. This year, several global sporting events are scheduled to take place,

including the Euro 2016 in June and the Rio 2016 Summer Olympics in August. Given the

huge popularity of these events and the differences in time zones, we expect to see a pickup

in data demand for mobile VOD.

Figure 16. Trend in LTE data usage per subscriber: Nearly 5GB per month

Source: MSIP, Mirae Asset Daewoo Research

Figure 17. Subscriptions to W40,000-W50,000 monthly plans—corresponding to monthly LTE data

usage of 5GB-6GB—have increased recently

Source: MSIP, media reports, Mirae Asset Daewoo Research

1

2

3

4

5

Jan. Feb. Mar. Apr. May Jun. Jul. Aug. Sep. Oct. Nov. Dec.

(GB)

2012 2013 2014 2015 2016

0

20

40

60

80

Jul-Sep 14 10/14 12/14 1/15 3/15 5/15 7/15 9/15 11/15 12/15 1/16 2/16 3/16

(%)Below W30,000 Between W40,000 and W50,000 Over W60,000

Handset distribution law

takes effect

Launchof data-centric monthly

plans

Telecom Service

10

June 3, 2016

Mirae Asset Daewoo Research

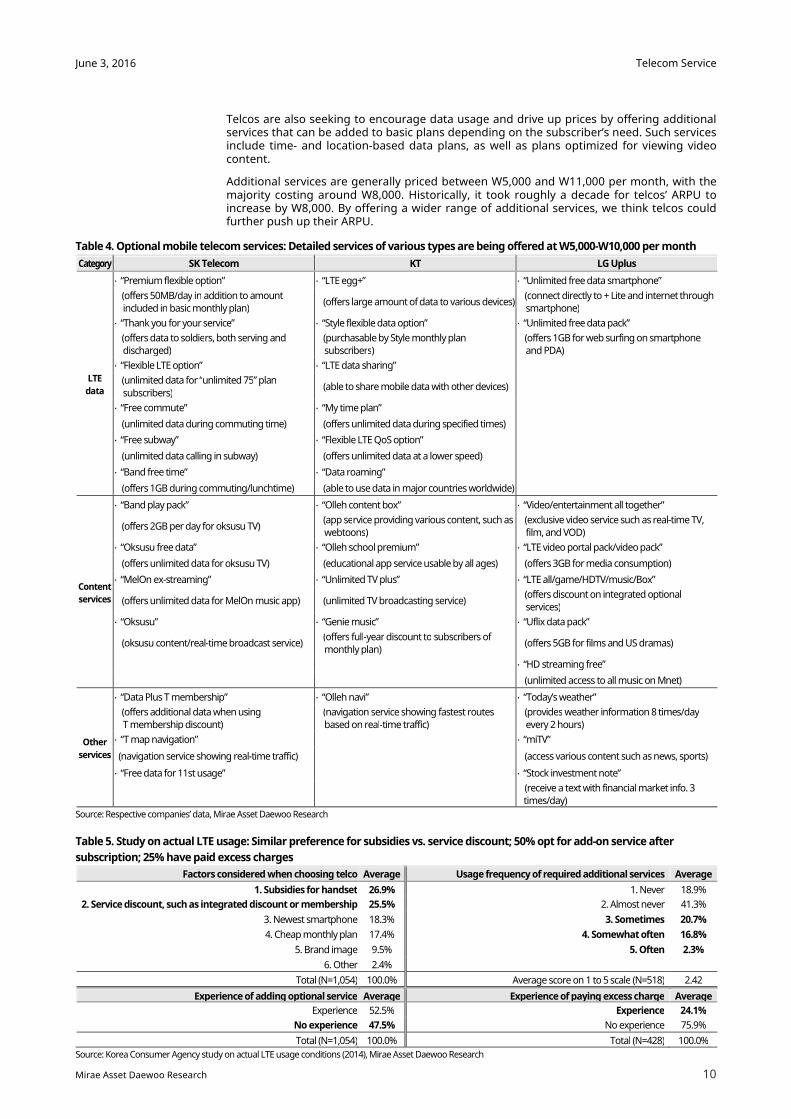

Telcos are also seeking to encourage data usage and drive up prices by offering additional services that can be added to basic plans depending on the subscriber’s need. Such services include time- and location-based data plans, as well as plans optimized for viewing video content.

Additional services are generally priced between W5,000 and W11,000 per month, with the majority costing around W8,000. Historically, it took roughly a decade for telcos’ ARPU to increase by W8,000. By offering a wider range of additional services, we think telcos could further push up their ARPU.

Table 4. Optional mobile telecom services: Detailed services of various types are being offered at W5,000-W10,000 per month

Category SK Telecom KT LG Uplus

LTE

data

∙ “Premium flexible option” ∙ “LTE egg+” ∙ “Unlimited free data smartphone”

(offers 50MB/day in addition to amount included in basic monthly plan)

(offers large amount of data to various devices) (connect directly to + Lite and internet through

smartphone)

∙ “Thank you for your service” ∙ “Style flexible data option” ∙ “Unlimited free data pack”

(offers data to soldiers, both serving and discharged)

(purchasable by Style monthly plan subscribers)

(offers 1GB for web surfing on smartphone and PDA)

∙ “Flexible LTE option” ∙ “LTE data sharing”

(unlimited data for “unlimited 75” plan

subscribers) (able to share mobile data with other devices)

∙ “Free commute” ∙ “My time plan”

(unlimited data during commuting time) (offers unlimited data during specified times)

∙ “Free subway” ∙ “Flexible LTE QoS option”

(unlimited data calling in subway) (offers unlimited data at a lower speed)

∙ “Band free time” ∙ “Data roaming”

(offers 1GB during commuting/lunchtime) (able to use data in major countries worldwide)

Content

services

∙ “Band play pack” ∙ “Olleh content box” ∙ “Video/entertainment all together”

(offers 2GB per day for oksusu TV) (app service providing various content, such as

webtoons) (exclusive video service such as real-time TV,

film, and VOD)

∙ “Oksusu free data” ∙ “Olleh school premium” ∙ “LTE video portal pack/video pack”

(offers unlimited data for oksusu TV) (educational app service usable by all ages) (offers 3GB for media consumption)

∙ “MelOn ex-streaming” ∙ “Unlimited TV plus” ∙ “LTE all/game/HDTV/music/Box”

(offers unlimited data for MelOn music app) (unlimited TV broadcasting service) (offers discount on integrated optional

services)

∙ “Oksusu” ∙ “Genie music” ∙ “Uflix data pack”

(oksusu content/real-time broadcast service) (offers full-year discount to subscribers of

monthly plan) (offers 5GB for films and US dramas)

∙ “HD streaming free”

(unlimited access to all music on Mnet)

Other

services

∙ “Data Plus T membership” ∙ “Olleh navi” ∙ “Today’s weather”

(offers additional data when using T membership discount)

(navigation service showing fastest routes based on real-time traffic)

(provides weather information 8 times/day every 2 hours)

∙ “T map navigation” ∙ “miTV”

(navigation service showing real-time traffic) (access various content such as news, sports)

∙ “Free data for 11st usage” ∙ “Stock investment note”

(receive a text with financial market info. 3 times/day)

Source: Respective companies’ data, Mirae Asset Daewoo Research

Table 5. Study on actual LTE usage: Similar preference for subsidies vs. service discount; 50% opt for add-on service after

subscription; 25% have paid excess charges

Factors considered when choosing telco Average Usage frequency of required additional services Average

1. Subsidies for handset 26.9% 1. Never 18.9%

2. Service discount, such as integrated discount or membership 25.5% 2. Almost never 41.3%

3. Newest smartphone 18.3% 3. Sometimes 20.7%

4. Cheap monthly plan 17.4% 4. Somewhat often 16.8%

5. Brand image 9.5% 5. Often 2.3%

6. Other 2.4%

Total (N=1,054) 100.0% Average score on 1 to 5 scale (N=518) 2.42

Experience of adding optional service Average Experience of paying excess charge Average

Experience 52.5% Experience 24.1%

No experience 47.5% No experience 75.9%

Total (N=1,054) 100.0% Total (N=428) 100.0%

Source: Korea Consumer Agency study on actual LTE usage conditions (2014), Mirae Asset Daewoo Research

Telecom Service

11

June 3, 2016

Mirae Asset Daewoo Research

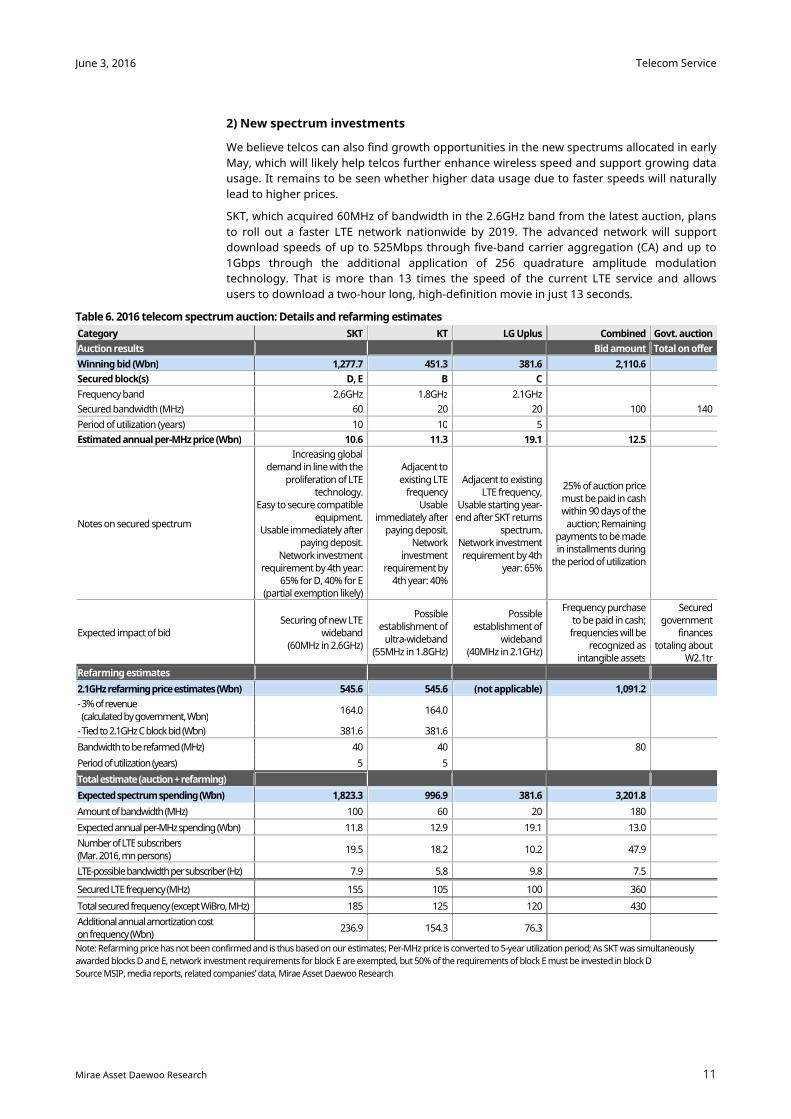

2) New spectrum investments

We believe telcos can also find growth opportunities in the new spectrums allocated in early

May, which will likely help telcos further enhance wireless speed and support growing data

usage. It remains to be seen whether higher data usage due to faster speeds will naturally

lead to higher prices.

SKT, which acquired 60MHz of bandwidth in the 2.6GHz band from the latest auction, plans

to roll out a faster LTE network nationwide by 2019. The advanced network will support

download speeds of up to 525Mbps through five-band carrier aggregation (CA) and up to

1Gbps through the additional application of 256 quadrature amplitude modulation

technology. That is more than 13 times the speed of the current LTE service and allows

users to download a two-hour long, high-definition movie in just 13 seconds.

Table 6. 2016 telecom spectrum auction: Details and refarming estimates

Category SKT KT LG Uplus Combined Govt. auction

Auction results Bid amount Total on offer

Winning bid (Wbn) 1,277.7 451.3 381.6 2,110.6 Secured block(s) D, E B C

Frequency band 2.6GHz 1.8GHz 2.1GHz

Secured bandwidth (MHz) 60 20 20 100 140

Period of utilization (years) 10 10 5

Estimated annual per-MHz price (Wbn) 10.6 11.3 19.1 12.5

Notes on secured spectrum

Increasing global demand in line with the

proliferation of LTE technology.

Easy to secure compatible equipment.

Usable immediately after paying deposit.

Network investment requirement by 4th year:

65% for D, 40% for E (partial exemption likely)

Adjacent to

existing LTE frequency

Usable immediately after

paying deposit. Network

investment requirement by

4th year: 40%

Adjacent to existing LTE frequency,

Usable starting year-end after SKT returns

spectrum. Network investment

requirement by 4th year: 65%

25% of auction price must be paid in cash within 90 days of the

auction; Remaining payments to be made in installments during

the period of utilization

Expected impact of bid Securing of new LTE

wideband (60MHz in 2.6GHz)

Possible establishment of

ultra-wideband (55MHz in 1.8GHz)

Possible establishment of

wideband (40MHz in 2.1GHz)

Frequency purchase to be paid in cash; frequencies will be

recognized as intangible assets

Secured government

finances totaling about

W2.1tr

Refarming estimates

2.1GHz refarming price estimates (Wbn) 545.6 545.6 (not applicable) 1,091.2 - 3% of revenue

(calculated by government, Wbn) 164.0 164.0

- Tied to 2.1GHz C block bid (Wbn) 381.6 381.6

Bandwidth to be refarmed (MHz) 40 40 80

Period of utilization (years) 5 5

Total estimate (auction + refarming)

Expected spectrum spending (Wbn) 1,823.3 996.9 381.6 3,201.8

Amount of bandwidth (MHz) 100 60 20 180

Expected annual per-MHz spending (Wbn) 11.8 12.9 19.1 13.0

Number of LTE subscribers (Mar. 2016, mn persons)

19.5 18.2 10.2 47.9

LTE-possible bandwidth per subscriber (Hz) 7.9 5.8 9.8 7.5

Secured LTE frequency (MHz) 155 105 100 360

Total secured frequency (except WiBro, MHz) 185 125 120 430

Additional annual amortization cost on frequency (Wbn)

236.9 154.3 76.3

Note: Refarming price has not been confirmed and is thus based on our estimates; Per-MHz price is converted to 5-year utilization period; As SKT was simultaneously

awarded blocks D and E, network investment requirements for block E are exempted, but 50% of the requirements of block E must be invested in block D

Source MSIP, media reports, related companies’ data, Mirae Asset Daewoo Research

Telecom Service

12

June 3, 2016

Mirae Asset Daewoo Research

Figure 18. Newly allocated spectrums will likely help telcos further enhance wireless speed and

support growing data usage

Source: Mirae Asset Daewoo Research

3) Preparing for the 5G age

Domestic telcos are getting ready for the upcoming commercialization of 5G technology in

2020. Large-scale investments have not yet taken place, as the technology is not

standardized and still in the testing stages.

That said, with a trial service planned for the 2018 PyeongChang Winter Olympic Games, we

think domestic telcos will likely move ahead of other countries in developing 5G networks.

The 2018 trial service is targeting a speed of 10Gbps using an eight-band CA technology

that combines eight frequencies with 100MHz bandwidths. That would be 33 times faster

than the current maximum speed of LTE (300Mbps). As the official partner of the

Pyeongchang Olympics, KT plans to showcase a number of 5G-based media services, such

as virtual ski-jumping and video recording using drones.

Table 7. 5G trial service specifications for 2018 (expected)

5G trial service category Technology standard

Frequency bandwidth 800MHz (100MHz * 8CA)

Number of MIMO index Max 8

Frame structure Independent structure

Channel coding Low-density parity-check (LDPC) code

5G-LTE linkage method 5G-LTE inter-link (necessary) and 5G solely (selective)

Subcarrier interval 75kHz

Duplexing method Dynamic time division duplex (Dynamic TDD)

Up-/downwind link structure Hybrid beam forming structure

Note: CA = Carrier Aggregation, MIMO = multiple-input and multiple-output

Source: The Fourth 5G Strategy and Planning Committee, etnews, Mirae Asset Daewoo Research

Figure 19. 5G standardization and preparation timeline of three big telcos; Commercialization

expected in 2020

Source: ITU, respective companies’ data, Mirae Asset Daewoo Research

Telecom Service

13

June 3, 2016

Mirae Asset Daewoo Research

Figure 20. KT’s plan for demonstrating 5G service at 2018 Pyeongchang Winter Olympics

Source: Company data, Mirae Asset Daewoo Research

Telecom Service

14

June 3, 2016

Mirae Asset Daewoo Research

2. Media

1) Pay-TV to reach an inflection point

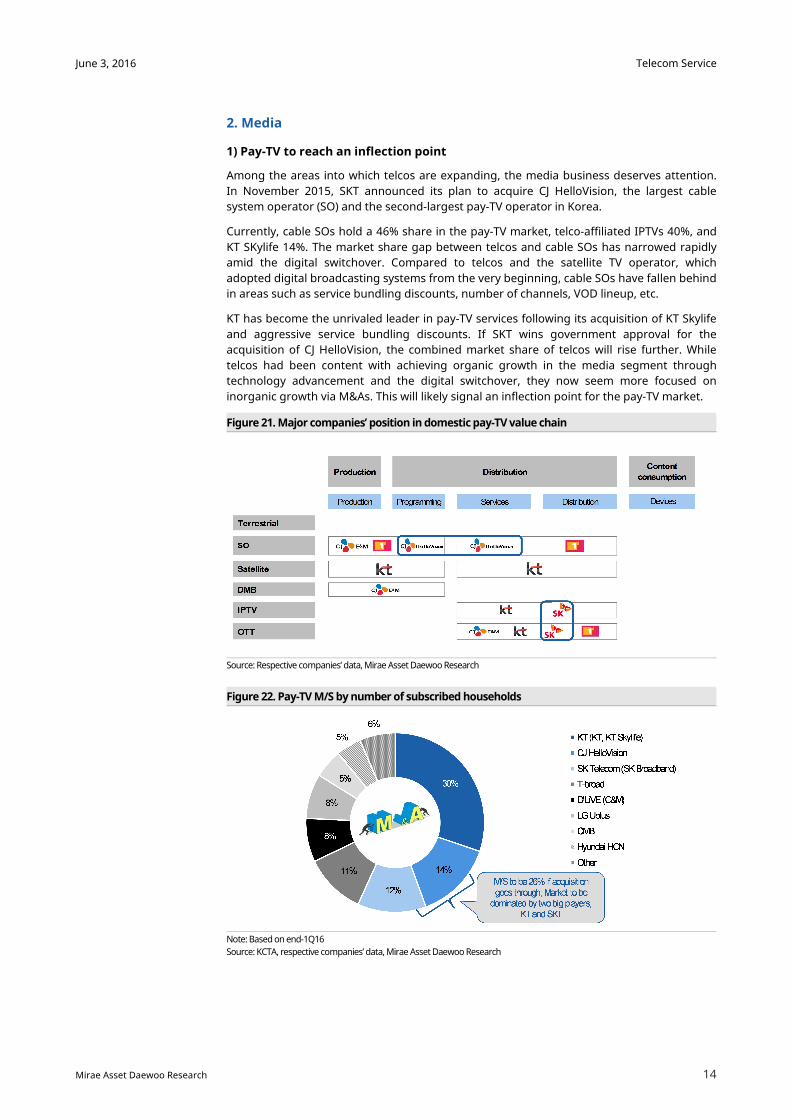

Among the areas into which telcos are expanding, the media business deserves attention.

In November 2015, SKT announced its plan to acquire CJ HelloVision, the largest cable

system operator (SO) and the second-largest pay-TV operator in Korea.

Currently, cable SOs hold a 46% share in the pay-TV market, telco-affiliated IPTVs 40%, and

KT SKylife 14%. The market share gap between telcos and cable SOs has narrowed rapidly

amid the digital switchover. Compared to telcos and the satellite TV operator, which

adopted digital broadcasting systems from the very beginning, cable SOs have fallen behind

in areas such as service bundling discounts, number of channels, VOD lineup, etc.

KT has become the unrivaled leader in pay-TV services following its acquisition of KT Skylife

and aggressive service bundling discounts. If SKT wins government approval for the

acquisition of CJ HelloVision, the combined market share of telcos will rise further. While

telcos had been content with achieving organic growth in the media segment through

technology advancement and the digital switchover, they now seem more focused on

inorganic growth via M&As. This will likely signal an inflection point for the pay-TV market.

Figure 21. Major companies’ position in domestic pay-TV value chain

Source: Respective companies’ data, Mirae Asset Daewoo Research

Figure 22. Pay-TV M/S by number of subscribed households

Note: Based on end-1Q16

Source: KCTA, respective companies’ data, Mirae Asset Daewoo Research

Telecom Service

15

June 3, 2016

Mirae Asset Daewoo Research

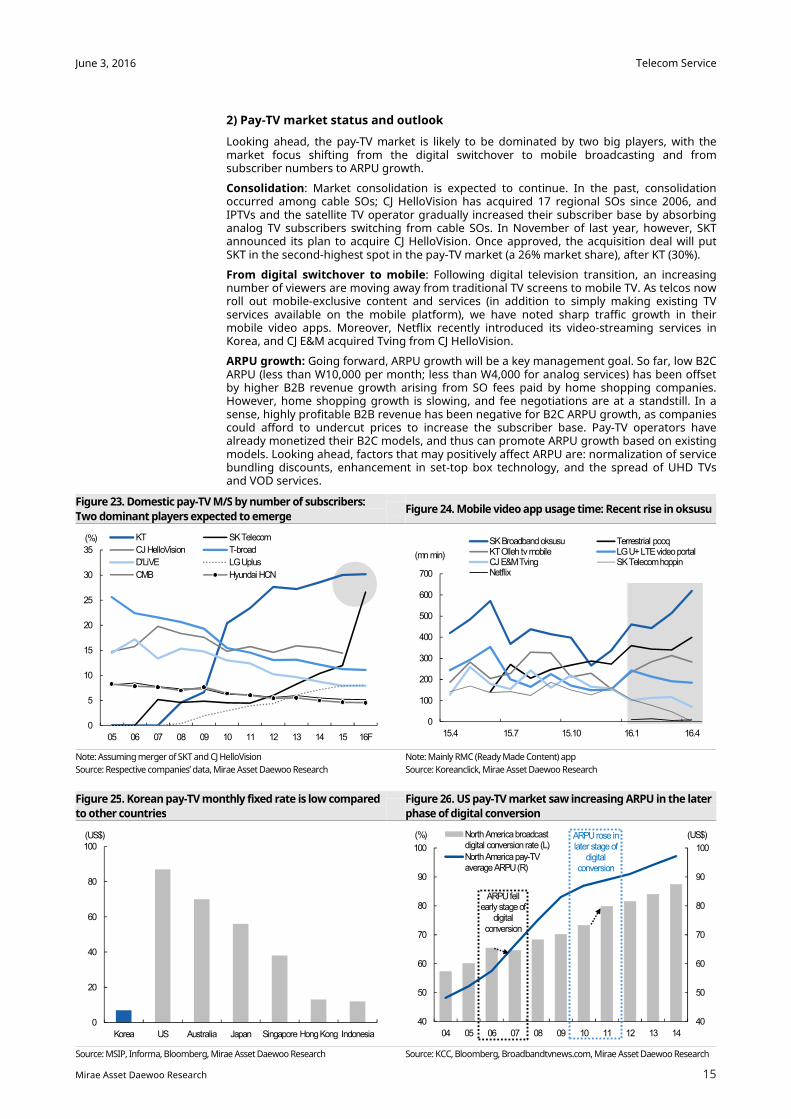

2) Pay-TV market status and outlook

Looking ahead, the pay-TV market is likely to be dominated by two big players, with the market focus shifting from the digital switchover to mobile broadcasting and from subscriber numbers to ARPU growth.

Consolidation: Market consolidation is expected to continue. In the past, consolidation occurred among cable SOs; CJ HelloVision has acquired 17 regional SOs since 2006, and IPTVs and the satellite TV operator gradually increased their subscriber base by absorbing analog TV subscribers switching from cable SOs. In November of last year, however, SKT announced its plan to acquire CJ HelloVision. Once approved, the acquisition deal will put SKT in the second-highest spot in the pay-TV market (a 26% market share), after KT (30%).

From digital switchover to mobile: Following digital television transition, an increasing number of viewers are moving away from traditional TV screens to mobile TV. As telcos now roll out mobile-exclusive content and services (in addition to simply making existing TV services available on the mobile platform), we have noted sharp traffic growth in their mobile video apps. Moreover, Netflix recently introduced its video-streaming services in Korea, and CJ E&M acquired Tving from CJ HelloVision.

ARPU growth: Going forward, ARPU growth will be a key management goal. So far, low B2C ARPU (less than W10,000 per month; less than W4,000 for analog services) has been offset by higher B2B revenue growth arising from SO fees paid by home shopping companies. However, home shopping growth is slowing, and fee negotiations are at a standstill. In a sense, highly profitable B2B revenue has been negative for B2C ARPU growth, as companies could afford to undercut prices to increase the subscriber base. Pay-TV operators have already monetized their B2C models, and thus can promote ARPU growth based on existing models. Looking ahead, factors that may positively affect ARPU are: normalization of service bundling discounts, enhancement in set-top box technology, and the spread of UHD TVs and VOD services.

Figure 23. Domestic pay-TV M/S by number of subscribers:

Two dominant players expected to emerge Figure 24. Mobile video app usage time: Recent rise in oksusu

Note: Assuming merger of SKT and CJ HelloVision

Source: Respective companies’ data, Mirae Asset Daewoo Research

Note: Mainly RMC (Ready Made Content) app

Source: Koreanclick, Mirae Asset Daewoo Research

Figure 25. Korean pay-TV monthly fixed rate is low compared

to other countries

Figure 26. US pay-TV market saw increasing ARPU in the later

phase of digital conversion

Source: MSIP, Informa, Bloomberg, Mirae Asset Daewoo Research Source: KCC, Bloomberg, Broadbandtvnews.com, Mirae Asset Daewoo Research

40

50

60

70

80

90

100

40

50

60

70

80

90

100

04 05 06 07 08 09 10 11 12 13 14

(US$)(%) North America broadcastdigital conversion rate (L)

North America pay-TVaverage ARPU (R)

ARPU fell early stage of

digital conversion

ARPU rose in later stage of

digital conversion

0

5

10

15

20

25

30

35

05 06 07 08 09 10 11 12 13 14 15 16F

(%) KT SK Telecom

CJ HelloVision T-broad

D'LiVE LG Uplus

CMB Hyundai HCN

0

20

40

60

80

100

Korea US Australia Japan Singapore Hong Kong Indonesia

(US$)

0

100

200

300

400

500

600

700

15.4 15.7 15.10 16.1 16.4

(mn min)

SK Broadband oksusu Terrestrial pooqKT Olleh tv mobile LG U+ LTE video portalCJ E&M Tving SK Telecom hoppinNetflix

Telecom Service

16

June 3, 2016

Mirae Asset Daewoo Research

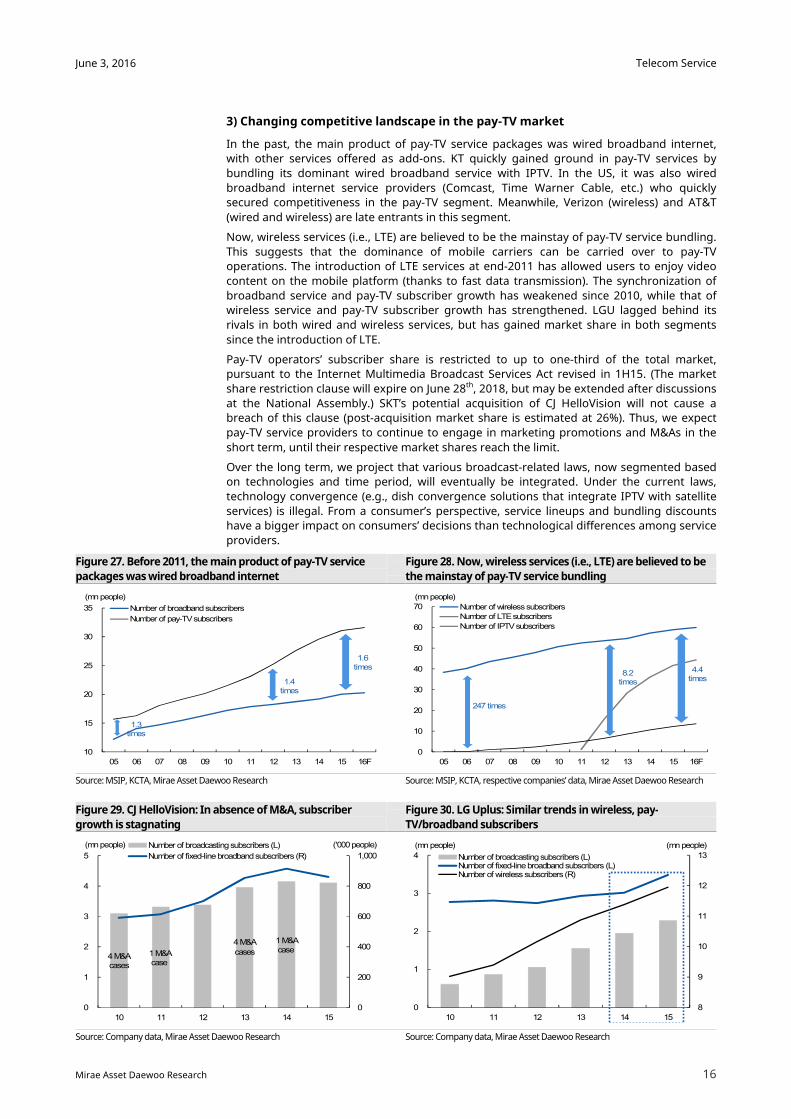

3) Changing competitive landscape in the pay-TV market

In the past, the main product of pay-TV service packages was wired broadband internet,

with other services offered as add-ons. KT quickly gained ground in pay-TV services by

bundling its dominant wired broadband service with IPTV. In the US, it was also wired

broadband internet service providers (Comcast, Time Warner Cable, etc.) who quickly

secured competitiveness in the pay-TV segment. Meanwhile, Verizon (wireless) and AT&T

(wired and wireless) are late entrants in this segment.

Now, wireless services (i.e., LTE) are believed to be the mainstay of pay-TV service bundling.

This suggests that the dominance of mobile carriers can be carried over to pay-TV

operations. The introduction of LTE services at end-2011 has allowed users to enjoy video

content on the mobile platform (thanks to fast data transmission). The synchronization of

broadband service and pay-TV subscriber growth has weakened since 2010, while that of

wireless service and pay-TV subscriber growth has strengthened. LGU lagged behind its

rivals in both wired and wireless services, but has gained market share in both segments

since the introduction of LTE.

Pay-TV operators’ subscriber share is restricted to up to one-third of the total market,

pursuant to the Internet Multimedia Broadcast Services Act revised in 1H15. (The market

share restriction clause will expire on June 28th, 2018, but may be extended after discussions

at the National Assembly.) SKT’s potential acquisition of CJ HelloVision will not cause a

breach of this clause (post-acquisition market share is estimated at 26%). Thus, we expect

pay-TV service providers to continue to engage in marketing promotions and M&As in the

short term, until their respective market shares reach the limit.

Over the long term, we project that various broadcast-related laws, now segmented based

on technologies and time period, will eventually be integrated. Under the current laws,

technology convergence (e.g., dish convergence solutions that integrate IPTV with satellite

services) is illegal. From a consumer’s perspective, service lineups and bundling discounts

have a bigger impact on consumers’ decisions than technological differences among service

providers.

Figure 27. Before 2011, the main product of pay-TV service

packages was wired broadband internet

Figure 28. Now, wireless services (i.e., LTE) are believed to be

the mainstay of pay-TV service bundling

Source: MSIP, KCTA, Mirae Asset Daewoo Research Source: MSIP, KCTA, respective companies’ data, Mirae Asset Daewoo Research

Figure 29. CJ HelloVision: In absence of M&A, subscriber

growth is stagnating

Figure 30. LG Uplus: Similar trends in wireless, pay-

TV/broadband subscribers

Source: Company data, Mirae Asset Daewoo Research Source: Company data, Mirae Asset Daewoo Research

1.3times

1.6times

1.4times

10

15

20

25

30

35

05 06 07 08 09 10 11 12 13 14 15 16F

(mn people)

Number of broadband subscribers

Number of pay-TV subscribers

247 times

8.2times

4.4 times

0

10

20

30

40

50

60

70

05 06 07 08 09 10 11 12 13 14 15 16F

(mn people)

Number of wireless subscribersNumber of LTE subscribers

Number of IPTV subscribers

4 M&A cases

1 M&Acase

4 M&A cases

1 M&Acase

0

200

400

600

800

1,000

0

1

2

3

4

5

10 11 12 13 14 15

('000 people)(mn people) Number of broadcasting subscribers (L)

Number of fixed-line broadband subscribers (R)

8

9

10

11

12

13

0

1

2

3

4

10 11 12 13 14 15

(mn people)(mn people)

Number of broadcasting subscribers (L)Number of fixed-line broadband subscribers (L)Number of wireless subscribers (R)

Telecom Service

17

June 3, 2016

Mirae Asset Daewoo Research

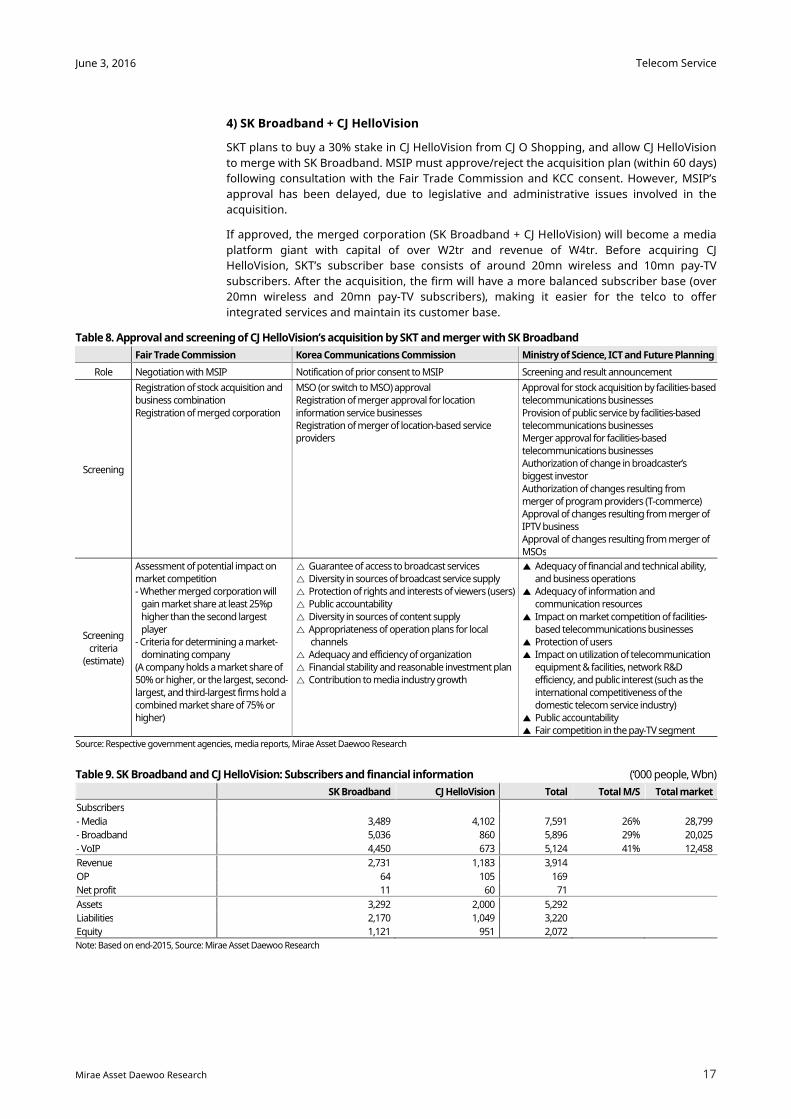

4) SK Broadband + CJ HelloVision

SKT plans to buy a 30% stake in CJ HelloVision from CJ O Shopping, and allow CJ HelloVision

to merge with SK Broadband. MSIP must approve/reject the acquisition plan (within 60 days)

following consultation with the Fair Trade Commission and KCC consent. However, MSIP’s

approval has been delayed, due to legislative and administrative issues involved in the

acquisition.

If approved, the merged corporation (SK Broadband + CJ HelloVision) will become a media

platform giant with capital of over W2tr and revenue of W4tr. Before acquiring CJ

HelloVision, SKT’s subscriber base consists of around 20mn wireless and 10mn pay-TV

subscribers. After the acquisition, the firm will have a more balanced subscriber base (over

20mn wireless and 20mn pay-TV subscribers), making it easier for the telco to offer

integrated services and maintain its customer base.

Table 8. Approval and screening of CJ HelloVision’s acquisition by SKT and merger with SK Broadband

Fair Trade Commission Korea Communications Commission Ministry of Science, ICT and Future Planning

Role Negotiation with MSIP Notification of prior consent to MSIP Screening and result announcement

Screening

Registration of stock acquisition and business combination

Registration of merged corporation

MSO (or switch to MSO) approval Registration of merger approval for location

information service businesses Registration of merger of location-based service providers

Approval for stock acquisition by facilities-based telecommunications businesses

Provision of public service by facilities-based telecommunications businesses Merger approval for facilities-based telecommunications businesses Authorization of change in broadcaster’s biggest investor

Authorization of changes resulting from merger of program providers (T-commerce) Approval of changes resulting from merger of IPTV business Approval of changes resulting from merger of MSOs

Screening

criteria (estimate)

Assessment of potential impact on market competition - Whether merged corporation will

gain market share at least 25%p

higher than the second largest player

- Criteria for determining a market-dominating company

(A company holds a market share of 50% or higher, or the largest, second-

largest, and third-largest firms hold a combined market share of 75% or higher)

△ Guarantee of access to broadcast services △ Diversity in sources of broadcast service supply △ Protection of rights and interests of viewers (users) △ Public accountability

△ Diversity in sources of content supply △ Appropriateness of operation plans for local

channels △ Adequacy and efficiency of organization △ Financial stability and reasonable investment plan △ Contribution to media industry growth

▲ Adequacy of financial and technical ability, and business operations

▲ Adequacy of information and communication resources

▲ Impact on market competition of facilities-based telecommunications businesses

▲ Protection of users ▲ Impact on utilization of telecommunication

equipment & facilities, network R&D efficiency, and public interest (such as the

international competitiveness of the domestic telecom service industry)

▲ Public accountability ▲ Fair competition in the pay-TV segment

Source: Respective government agencies, media reports, Mirae Asset Daewoo Research

Table 9. SK Broadband and CJ HelloVision: Subscribers and financial information (‘000 people, Wbn)

SK Broadband CJ HelloVision Total Total M/S Total market

Subscribers

- Media 3,489 4,102 7,591 26% 28,799

- Broadband 5,036 860 5,896 29% 20,025

- VoIP 4,450 673 5,124 41% 12,458

Revenue 2,731 1,183 3,914

OP 64 105 169

Net profit 11 60 71

Assets 3,292 2,000 5,292

Liabilities 2,170 1,049 3,220

Equity 1,121 951 2,072

Note: Based on end-2015, Source: Mirae Asset Daewoo Research

Telecom Service

18

June 3, 2016

Mirae Asset Daewoo Research

Figure 31. After acquisition of CJ HelloVision, SKT will have a more balanced subscriber base

Note: Based on end-1Q16; For computation; Assumed pay-TV subscribing households consist of three people

Source: Respective companies’ data, Mirae Asset Daewoo Research

5) Next media

In terms of telcos’ approach to the media business, they can either mimic or differentiate

themselves from conventional media firms.

Conventional firms focus on improving content competitiveness. Netflix, whose new media

platform and big data curation services gives it a technological advantage, expanded into in-

house content production in order to deliver a second phase of growth. Once a company

achieves subscriber expansion, starting an in-house content business is advantageous, as it

should take a shorter time to retrieve investments than it would with a small subscriber

base.

Telcos are able to differentiate themselves on the back of their wireless communications

technologies, including: 1) big data, which analyzes and maximizes efficiency of complicated

digital media ecosystems, 2) interactive media businesses based on 5G networks (e.g.,

virtual reality), and 3) media cloud streaming, which will be necessary to replay large

content at high quality.

These new media businesses will be based on telcos’ conventional business model (e.g.,

data traffic-based plans). Indeed, currently, 80% of LTE data is being used to play videos

(media). In other words, expansion of the media business seems necessary to boost the

growth of telecom services.

Figure 32. Telcos are revitalizing the content business

through expansion of the media value chain

Figure 33. Expecting big data analysis and service

improvement through platform enhancement

Source: SK Broadband, Mirae Asset Daewoo Research Source: SK Broadband, Mirae Asset Daewoo Research

0

10

20

30

SK TelecomIndividual mobile

SK BroadbandPay-TV households * 3

SK TelecomIndividual mobile

SK Broadband + CJ HelloVisionPay-TV households * 3

(mn people) Subscriber basis

Afteracquisition

Telecom Service

19

June 3, 2016

Mirae Asset Daewoo Research

Figure 34. Telcos expected to play a significant role in VR value

chain and ecosystem

Figure 35. Telcos may use their wireless communications

technologies to enter media cloud streaming business

Source: Nasmedia, KT, Mirae Asset Daewoo Research Source: Entrix, SKT, Mirae Asset Daewoo Research

Figure 36. Vision of new media in 5G era

Source: SKT, Mirae Asset Daewoo Research

Table 10. Content and related investments by telcos

SKT KT LG Uplus

Service

∙ SK B tv, B tv mobile

3.68mn IPTV subscribers (+ CJ HelloVision: 4.15mn; pay-TV market share: 26%)

∙ KT Olleh tv, Olleh tv mobile

∙ 6.72mn IPTV subscribers + Skylife (pay-TV market share: 30%)

∙ U+ tv G, LTE video portal

∙ 2.38mn IPTV subscribers (pay-TV market share: 8%)

Content

∙ Channel-specific content (CJ E&M, JTBC, etc.)

∙ Movies/dramas, sports/leisure, documentary, foreign (around 80 channels)

∙ B tv kidzone: Animation

∙ Joint investment/production with CJ E&M

∙ Broadcasting 60 Disney programs

∙ Secured 4,000 DreamWorks titles (including

VOD)

∙ Broadest full HD channel lineup 160,000 VODs

∙ Children’s and educational content

∙ Most free movie content

∙ Exclusive contract with Sony Pictures; Simultaneous broadcast of US dramas

∙ Uflix provides around 22,000 recent movies and

popular HBO dramas

∙ 20,000 animations, 12,000 kids’ programs, etc.

∙ Exclusive distributor of NBC Universal content in Korea (simultaneous broadcast)

∙ Providing popular Japanese (in partnership with Fuji Television) and Chinese dramas

Multi-channel network (MCN)

∙ Operating mobile MCN platform Hotzil ∙ Providing in-house content produced in partnership with DIA TV

∙ Opened Power YouTuber service

Virtual reality (VR)

∙ Providing 360-degree VR services ∙ Planning in-house production of VR movies ∙ Providing AR and VR integrated content and T

Real platform

∙ Providing 360-degree VR real-time content for KT Wiz baseball team

∙ Planning to provide 200 pieces of VR mobile

content this year

∙ Operating VR game promotion center ∙ Working to provide VR VODs ∙ Planning to produce VR content for adults

Strategy

∙ Planning to establish a content production

fund (W320bn) for in-house content production after acquisition of CJ HelloVision

∙ Planning to invest W5tr in content over the next five years

∙ Offering premium services (GIGA UHD) targeting high-end customers

∙ Increasing OTS subscribers (bundling with

Skylife)

∙ Increasing ARPU by launching video data plans

∙ Increasing the number of high-end customers

(UHD IPTV, etc.)

Note: Number of subscribers is as of end-March for CJ HelloVision and as of end-April for others

Source: Company data, media reports, Mirae Asset Daewoo Research

Telecom Service

20

June 3, 2016

Mirae Asset Daewoo Research

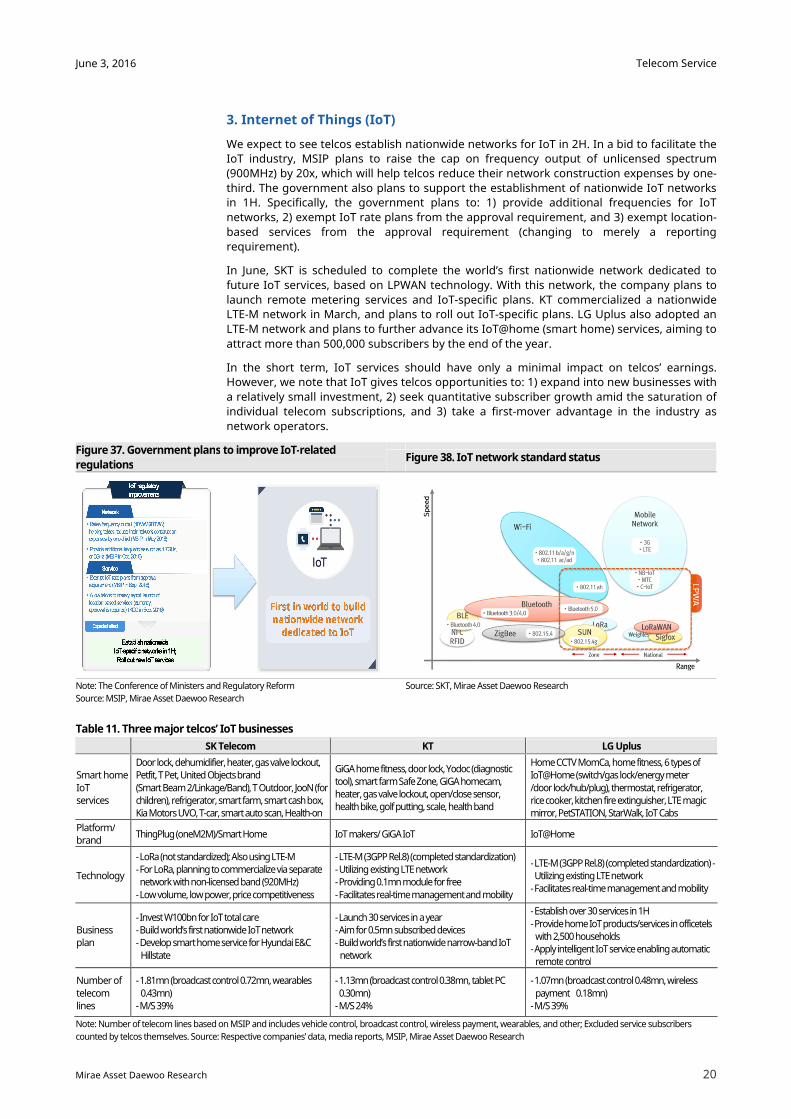

3. Internet of Things (IoT)

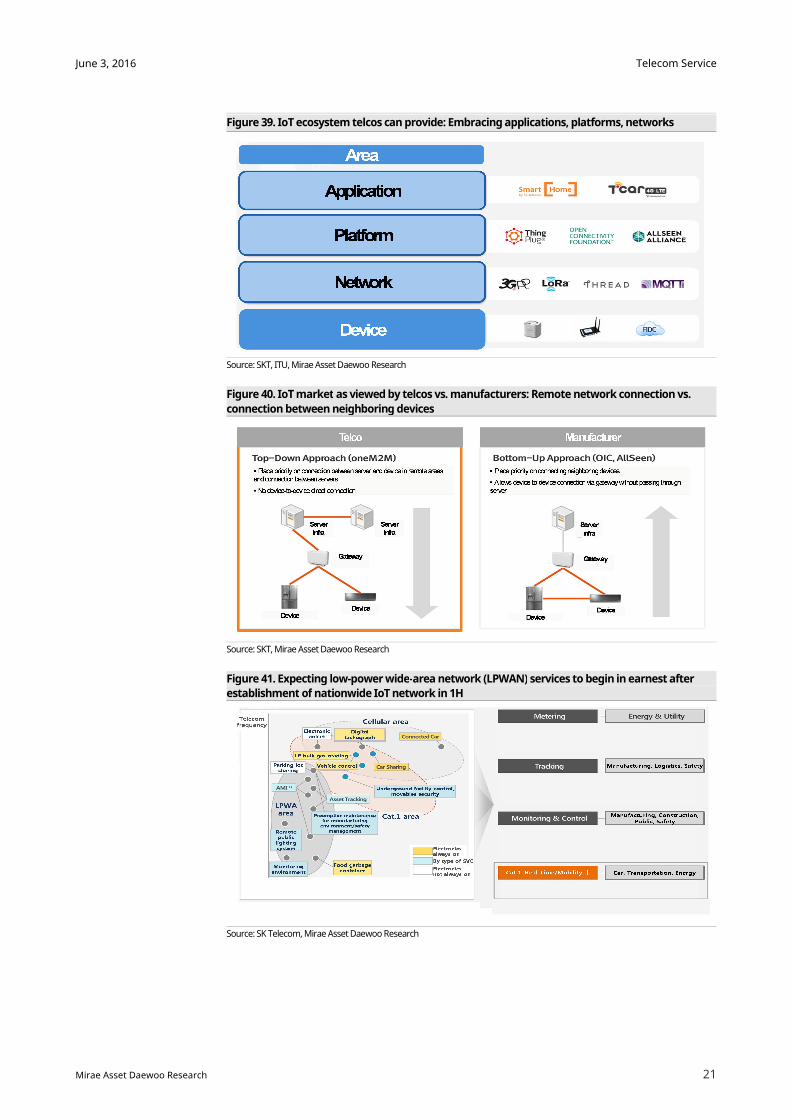

We expect to see telcos establish nationwide networks for IoT in 2H. In a bid to facilitate the

IoT industry, MSIP plans to raise the cap on frequency output of unlicensed spectrum

(900MHz) by 20x, which will help telcos reduce their network construction expenses by one-

third. The government also plans to support the establishment of nationwide IoT networks

in 1H. Specifically, the government plans to: 1) provide additional frequencies for IoT

networks, 2) exempt IoT rate plans from the approval requirement, and 3) exempt location-

based services from the approval requirement (changing to merely a reporting

requirement).

In June, SKT is scheduled to complete the world’s first nationwide network dedicated to

future IoT services, based on LPWAN technology. With this network, the company plans to

launch remote metering services and IoT-specific plans. KT commercialized a nationwide

LTE-M network in March, and plans to roll out IoT-specific plans. LG Uplus also adopted an

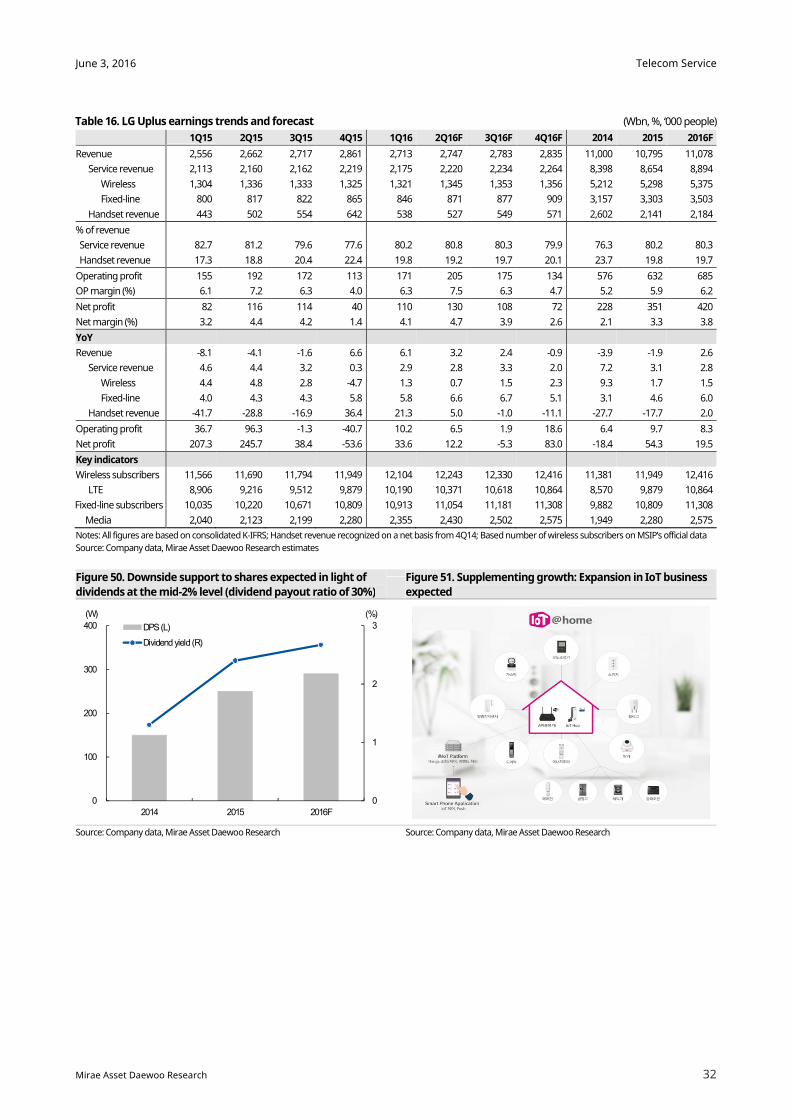

LTE-M network and plans to further advance its IoT@home (smart home) services, aiming to

attract more than 500,000 subscribers by the end of the year.

In the short term, IoT services should have only a minimal impact on telcos’ earnings.

However, we note that IoT gives telcos opportunities to: 1) expand into new businesses with

a relatively small investment, 2) seek quantitative subscriber growth amid the saturation of

individual telecom subscriptions, and 3) take a first-mover advantage in the industry as

network operators.

Figure 37. Government plans to improve IoT-related

regulations Figure 38. IoT network standard status

Note: The Conference of Ministers and Regulatory Reform

Source: MSIP, Mirae Asset Daewoo Research

Source: SKT, Mirae Asset Daewoo Research

Table 11. Three major telcos’ IoT businesses

SK Telecom KT LG Uplus

Smart home

IoT services

Door lock, dehumidifier, heater, gas valve lockout, Petfit, T Pet, United Objects brand

(Smart Beam 2/Linkage/Band), T Outdoor, JooN (for children), refrigerator, smart farm, smart cash box, Kia Motors UVO, T-car, smart auto scan, Health-on

GiGA home fitness, door lock, Yodoc (diagnostic tool), smart farm Safe Zone, GiGA homecam, heater, gas valve lockout, open/close sensor, health bike, golf putting, scale, health band

Home CCTV MomCa, home fitness, 6 types of IoT@Home (switch/gas lock/energy meter

/door lock/hub/plug), thermostat, refrigerator, rice cooker, kitchen fire extinguisher, LTE magic mirror, PetSTATION, StarWalk, IoT Cabs

Platform/ brand

ThingPlug (oneM2M)/Smart Home IoT makers/ GiGA IoT IoT@Home

Technology

- LoRa (not standardized); Also using LTE-M - For LoRa, planning to commercialize via separate network with non-licensed band (920MHz)

- Low volume, low power, price competitiveness

- LTE-M (3GPP Rel.8) (completed standardization) - Utilizing existing LTE network - Providing 0.1mn module for free

- Facilitates real-time management and mobility

- LTE-M (3GPP Rel.8) (completed standardization) -Utilizing existing LTE network

- Facilitates real-time management and mobility

Business plan

- Invest W100bn for IoT total care - Build world’s first nationwide IoT network - Develop smart home service for Hyundai E&C

Hillstate

- Launch 30 services in a year - Aim for 0.5mn subscribed devices - Build world’s first nationwide narrow-band IoT

network

- Establish over 30 services in 1H

- Provide home IoT products/services in officetels with 2,500 households

- Apply intelligent IoT service enabling automatic remote control

Number of

telecom lines

- 1.81mn (broadcast control 0.72mn, wearables

0.43mn) - M/S 39%

- 1.13mn (broadcast control 0.38mn, tablet PC

0.30mn) - M/S 24%

- 1.07mn (broadcast control 0.48mn, wireless

payment 0.18mn) - M/S 39%

Note: Number of telecom lines based on MSIP and includes vehicle control, broadcast control, wireless payment, wearables, and other; Excluded service subscribers

counted by telcos themselves. Source: Respective companies’ data, media reports, MSIP, Mirae Asset Daewoo Research

Telecom Service

21

June 3, 2016

Mirae Asset Daewoo Research

Figure 39. IoT ecosystem telcos can provide: Embracing applications, platforms, networks

Source: SKT, ITU, Mirae Asset Daewoo Research

Figure 40. IoT market as viewed by telcos vs. manufacturers: Remote network connection vs.

connection between neighboring devices

Source: SKT, Mirae Asset Daewoo Research

Figure 41. Expecting low-power wide-area network (LPWAN) services to begin in earnest after

establishment of nationwide IoT network in 1H

Source: SK Telecom, Mirae Asset Daewoo Research

Telecom Service

22

June 3, 2016

Mirae Asset Daewoo Research

Investment & valuation

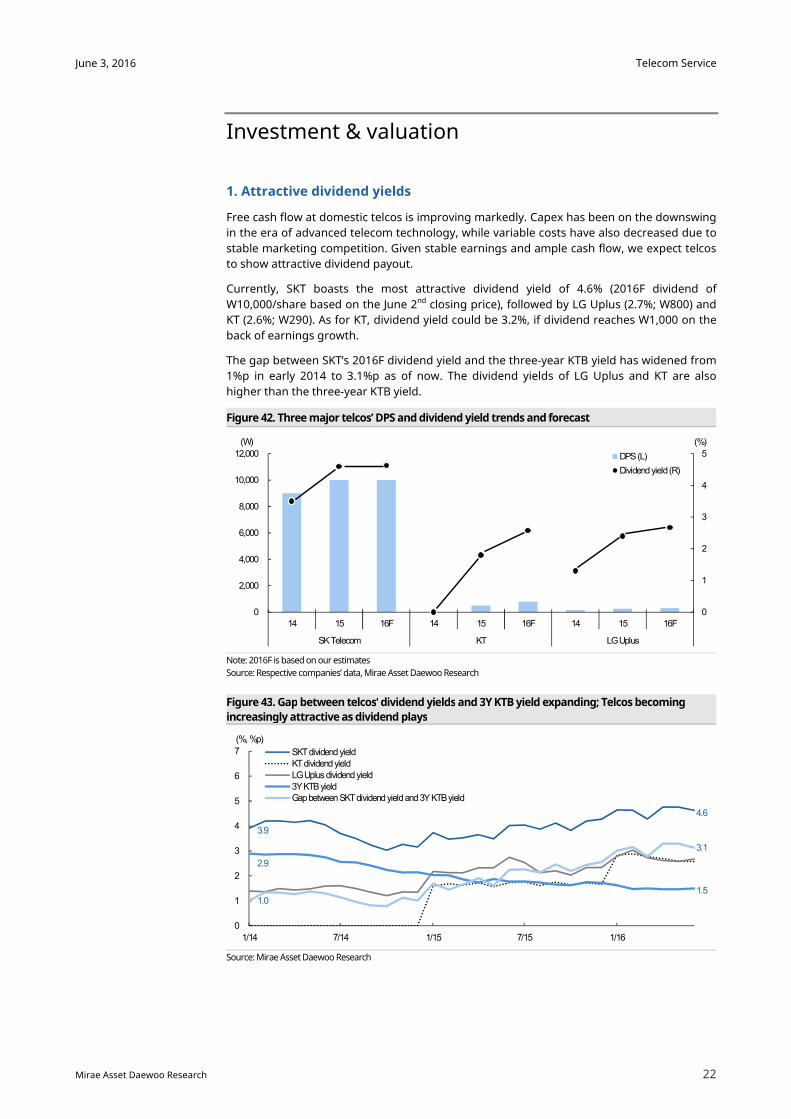

1. Attractive dividend yields

Free cash flow at domestic telcos is improving markedly. Capex has been on the downswing

in the era of advanced telecom technology, while variable costs have also decreased due to

stable marketing competition. Given stable earnings and ample cash flow, we expect telcos

to show attractive dividend payout.

Currently, SKT boasts the most attractive dividend yield of 4.6% (2016F dividend of

W10,000/share based on the June 2nd closing price), followed by LG Uplus (2.7%; W800) and

KT (2.6%; W290). As for KT, dividend yield could be 3.2%, if dividend reaches W1,000 on the

back of earnings growth.

The gap between SKT’s 2016F dividend yield and the three-year KTB yield has widened from

1%p in early 2014 to 3.1%p as of now. The dividend yields of LG Uplus and KT are also

higher than the three-year KTB yield.

Figure 42. Three major telcos’ DPS and dividend yield trends and forecast

Note: 2016F is based on our estimates

Source: Respective companies’ data, Mirae Asset Daewoo Research

Figure 43. Gap between telcos’ dividend yields and 3Y KTB yield expanding; Telcos becoming

increasingly attractive as dividend plays

Source: Mirae Asset Daewoo Research

0

1

2

3

4

5

0

2,000

4,000

6,000

8,000

10,000

12,000

14 15 16F 14 15 16F 14 15 16F

SK Telecom KT LG Uplus

(%)(W)

DPS (L)

Dividend yield (R)

3.9

4.6

2.9

1.5 1.0

3.1

0

1

2

3

4

5

6

7

1/14 7/14 1/15 7/15 1/16

(%, %p)

SKT dividend yieldKT dividend yieldLG Uplus dividend yield3Y KTB yieldGap between SKT dividend yield and 3Y KTB yield

Telecom Service

23

June 3, 2016

Mirae Asset Daewoo Research

2. Investment strategy

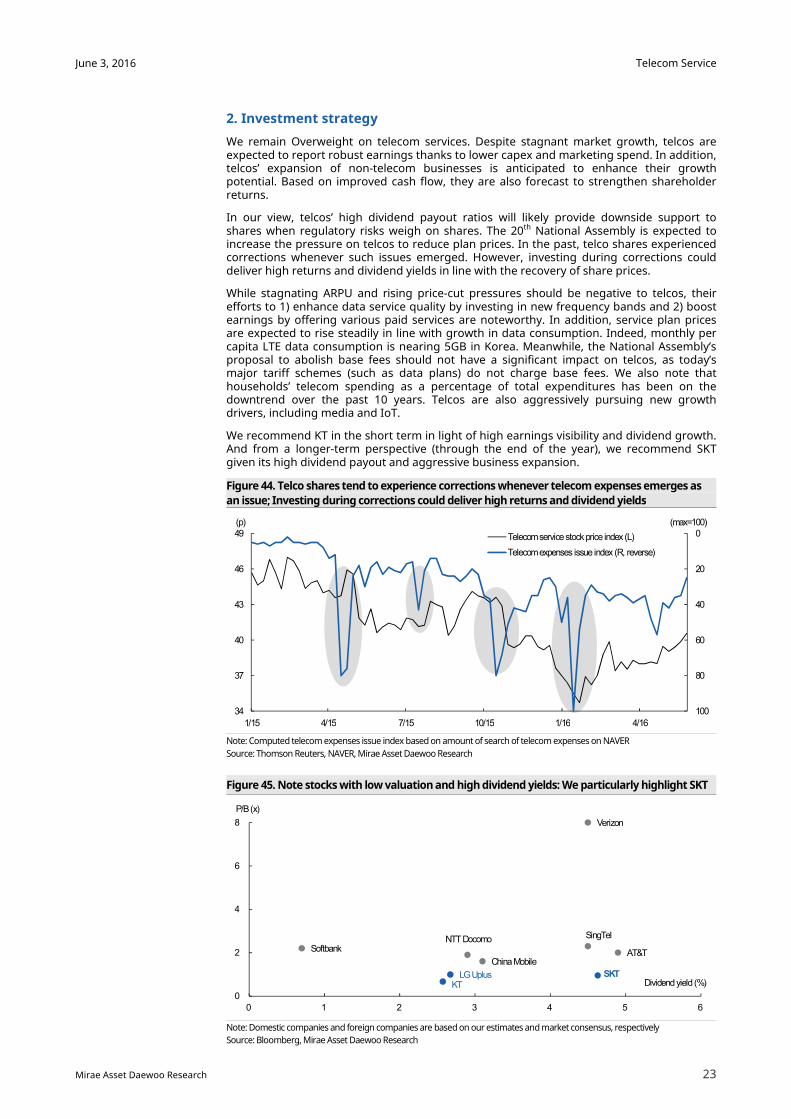

We remain Overweight on telecom services. Despite stagnant market growth, telcos are expected to report robust earnings thanks to lower capex and marketing spend. In addition, telcos’ expansion of non-telecom businesses is anticipated to enhance their growth potential. Based on improved cash flow, they are also forecast to strengthen shareholder returns.

In our view, telcos’ high dividend payout ratios will likely provide downside support to shares when regulatory risks weigh on shares. The 20th National Assembly is expected to increase the pressure on telcos to reduce plan prices. In the past, telco shares experienced corrections whenever such issues emerged. However, investing during corrections could deliver high returns and dividend yields in line with the recovery of share prices.

While stagnating ARPU and rising price-cut pressures should be negative to telcos, their efforts to 1) enhance data service quality by investing in new frequency bands and 2) boost earnings by offering various paid services are noteworthy. In addition, service plan prices are expected to rise steadily in line with growth in data consumption. Indeed, monthly per capita LTE data consumption is nearing 5GB in Korea. Meanwhile, the National Assembly’s proposal to abolish base fees should not have a significant impact on telcos, as today’s major tariff schemes (such as data plans) do not charge base fees. We also note that households’ telecom spending as a percentage of total expenditures has been on the downtrend over the past 10 years. Telcos are also aggressively pursuing new growth drivers, including media and IoT.

We recommend KT in the short term in light of high earnings visibility and dividend growth. And from a longer-term perspective (through the end of the year), we recommend SKT given its high dividend payout and aggressive business expansion.

Figure 44. Telco shares tend to experience corrections whenever telecom expenses emerges as

an issue; Investing during corrections could deliver high returns and dividend yields

Note: Computed telecom expenses issue index based on amount of search of telecom expenses on NAVER

Source: Thomson Reuters, NAVER, Mirae Asset Daewoo Research

Figure 45. Note stocks with low valuation and high dividend yields: We particularly highlight SKT

Note: Domestic companies and foreign companies are based on our estimates and market consensus, respectively

Source: Bloomberg, Mirae Asset Daewoo Research

0

20

40

60

80

10034

37

40

43

46

49

1/15 4/15 7/15 10/15 1/16 4/16

(max=100)(p)

Telecom service stock price index (L)

Telecom expenses issue index (R, reverse)

SKT

KTLG Uplus

Verizon

AT&T

SingTelNTT DocomoSoftbank

China Mobile

0

2

4

6

8

0 1 2 3 4 5 6

P/B (x)

Dividend yield (%)

Telecom Service

24

June 3, 2016

Mirae Asset Daewoo Research

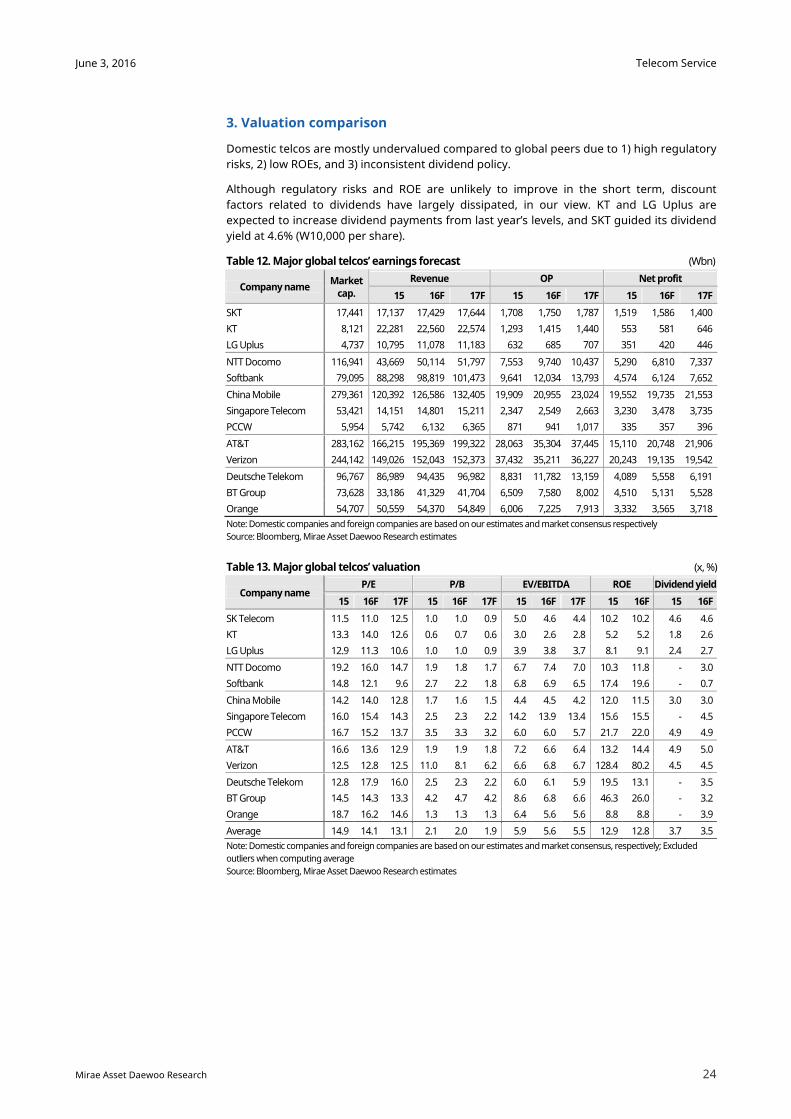

3. Valuation comparison

Domestic telcos are mostly undervalued compared to global peers due to 1) high regulatory

risks, 2) low ROEs, and 3) inconsistent dividend policy.

Although regulatory risks and ROE are unlikely to improve in the short term, discount

factors related to dividends have largely dissipated, in our view. KT and LG Uplus are

expected to increase dividend payments from last year’s levels, and SKT guided its dividend

yield at 4.6% (W10,000 per share).

Table 12. Major global telcos’ earnings forecast (Wbn)

Company name Market

cap.

Revenue OP Net profit

15 16F 17F 15 16F 17F 15 16F 17F

SKT 17,441 17,137 17,429 17,644 1,708 1,750 1,787 1,519 1,586 1,400

KT 8,121 22,281 22,560 22,574 1,293 1,415 1,440 553 581 646

LG Uplus 4,737 10,795 11,078 11,183 632 685 707 351 420 446

NTT Docomo 116,941 43,669 50,114 51,797 7,553 9,740 10,437 5,290 6,810 7,337

Softbank 79,095 88,298 98,819 101,473 9,641 12,034 13,793 4,574 6,124 7,652

China Mobile 279,361 120,392 126,586 132,405 19,909 20,955 23,024 19,552 19,735 21,553

Singapore Telecom 53,421 14,151 14,801 15,211 2,347 2,549 2,663 3,230 3,478 3,735

PCCW 5,954 5,742 6,132 6,365 871 941 1,017 335 357 396

AT&T 283,162 166,215 195,369 199,322 28,063 35,304 37,445 15,110 20,748 21,906

Verizon 244,142 149,026 152,043 152,373 37,432 35,211 36,227 20,243 19,135 19,542

Deutsche Telekom 96,767 86,989 94,435 96,982 8,831 11,782 13,159 4,089 5,558 6,191

BT Group 73,628 33,186 41,329 41,704 6,509 7,580 8,002 4,510 5,131 5,528

Orange 54,707 50,559 54,370 54,849 6,006 7,225 7,913 3,332 3,565 3,718

Note: Domestic companies and foreign companies are based on our estimates and market consensus respectively

Source: Bloomberg, Mirae Asset Daewoo Research estimates

Table 13. Major global telcos’ valuation (x, %)

Company name P/E P/B EV/EBITDA ROE Dividend yield

15 16F 17F 15 16F 17F 15 16F 17F 15 16F 15 16F

SK Telecom 11.5 11.0 12.5 1.0 1.0 0.9 5.0 4.6 4.4 10.2 10.2 4.6 4.6

KT 13.3 14.0 12.6 0.6 0.7 0.6 3.0 2.6 2.8 5.2 5.2 1.8 2.6

LG Uplus 12.9 11.3 10.6 1.0 1.0 0.9 3.9 3.8 3.7 8.1 9.1 2.4 2.7

NTT Docomo 19.2 16.0 14.7 1.9 1.8 1.7 6.7 7.4 7.0 10.3 11.8 - 3.0

Softbank 14.8 12.1 9.6 2.7 2.2 1.8 6.8 6.9 6.5 17.4 19.6 - 0.7

China Mobile 14.2 14.0 12.8 1.7 1.6 1.5 4.4 4.5 4.2 12.0 11.5 3.0 3.0

Singapore Telecom 16.0 15.4 14.3 2.5 2.3 2.2 14.2 13.9 13.4 15.6 15.5 - 4.5

PCCW 16.7 15.2 13.7 3.5 3.3 3.2 6.0 6.0 5.7 21.7 22.0 4.9 4.9

AT&T 16.6 13.6 12.9 1.9 1.9 1.8 7.2 6.6 6.4 13.2 14.4 4.9 5.0

Verizon 12.5 12.8 12.5 11.0 8.1 6.2 6.6 6.8 6.7 128.4 80.2 4.5 4.5

Deutsche Telekom 12.8 17.9 16.0 2.5 2.3 2.2 6.0 6.1 5.9 19.5 13.1 - 3.5

BT Group 14.5 14.3 13.3 4.2 4.7 4.2 8.6 6.8 6.6 46.3 26.0 - 3.2

Orange 18.7 16.2 14.6 1.3 1.3 1.3 6.4 5.6 5.6 8.8 8.8 - 3.9

Average 14.9 14.1 13.1 2.1 2.0 1.9 5.9 5.6 5.5 12.9 12.8 3.7 3.5

Note: Domestic companies and foreign companies are based on our estimates and market consensus, respectively; Excluded

outliers when computing average

Source: Bloomberg, Mirae Asset Daewoo Research estimates

Telecom Service

25

June 3, 2016

Mirae Asset Daewoo Research

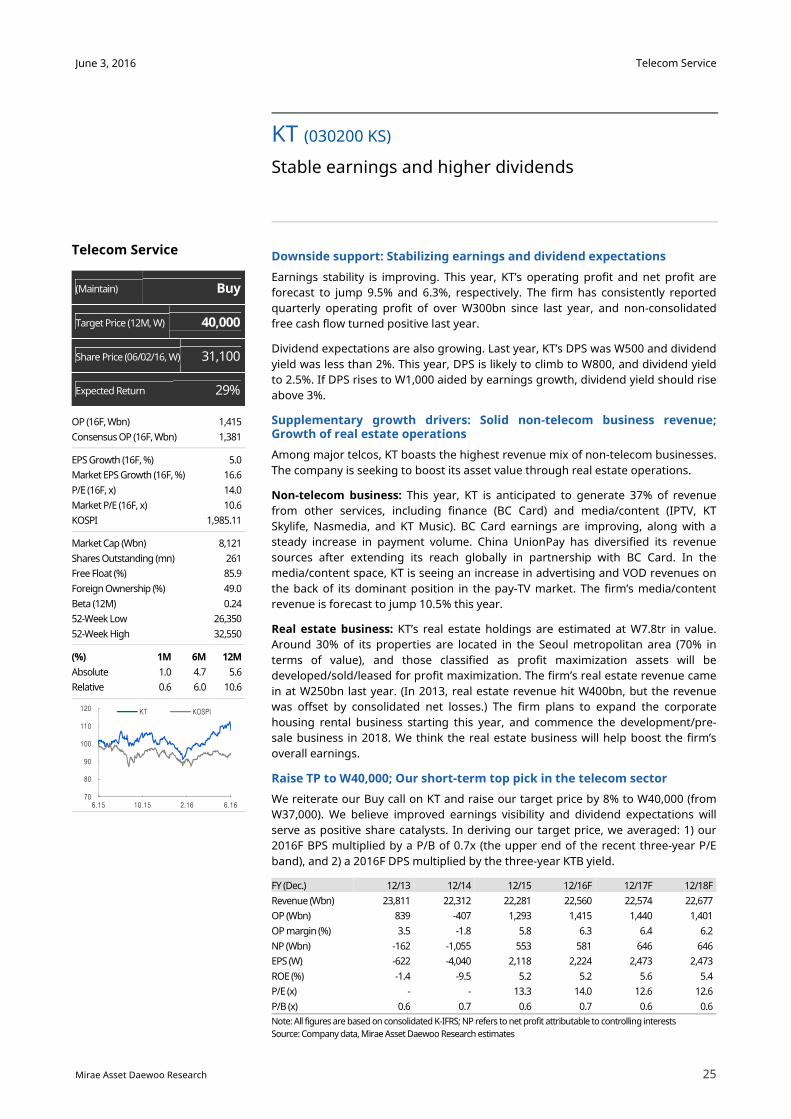

Downside support: Stabilizing earnings and dividend expectations

Earnings stability is improving. This year, KT’s operating profit and net profit are

forecast to jump 9.5% and 6.3%, respectively. The firm has consistently reported

quarterly operating profit of over W300bn since last year, and non-consolidated

free cash flow turned positive last year.

Dividend expectations are also growing. Last year, KT’s DPS was W500 and dividend

yield was less than 2%. This year, DPS is likely to climb to W800, and dividend yield

to 2.5%. If DPS rises to W1,000 aided by earnings growth, dividend yield should rise

above 3%.

Supplementary growth drivers: Solid non-telecom business revenue; Growth of real estate operations

Among major telcos, KT boasts the highest revenue mix of non-telecom businesses.

The company is seeking to boost its asset value through real estate operations.

Non-telecom business: This year, KT is anticipated to generate 37% of revenue

from other services, including finance (BC Card) and media/content (IPTV, KT

Skylife, Nasmedia, and KT Music). BC Card earnings are improving, along with a

steady increase in payment volume. China UnionPay has diversified its revenue

sources after extending its reach globally in partnership with BC Card. In the

media/content space, KT is seeing an increase in advertising and VOD revenues on

the back of its dominant position in the pay-TV market. The firm’s media/content

revenue is forecast to jump 10.5% this year.

Real estate business: KT’s real estate holdings are estimated at W7.8tr in value.

Around 30% of its properties are located in the Seoul metropolitan area (70% in

terms of value), and those classified as profit maximization assets will be

developed/sold/leased for profit maximization. The firm’s real estate revenue came

in at W250bn last year. (In 2013, real estate revenue hit W400bn, but the revenue

was offset by consolidated net losses.) The firm plans to expand the corporate

housing rental business starting this year, and commence the development/pre-

sale business in 2018. We think the real estate business will help boost the firm’s

overall earnings.

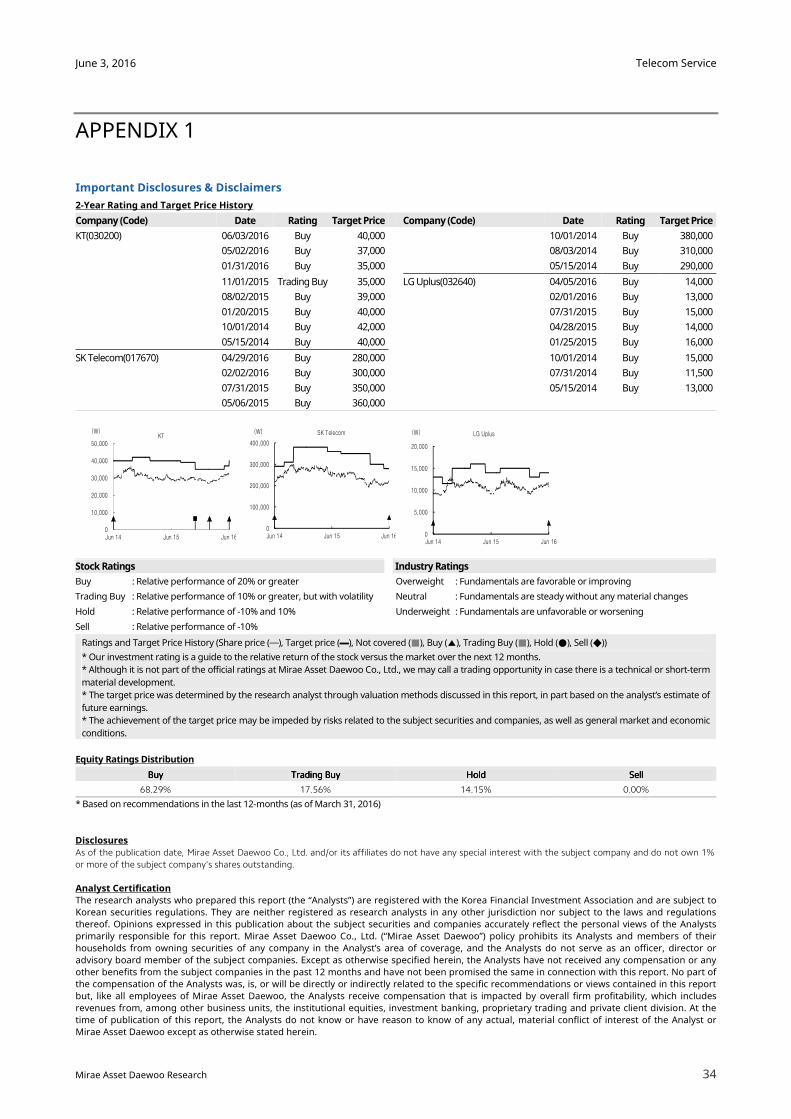

Raise TP to W40,000; Our short-term top pick in the telecom sector

We reiterate our Buy call on KT and raise our target price by 8% to W40,000 (from

W37,000). We believe improved earnings visibility and dividend expectations will

serve as positive share catalysts. In deriving our target price, we averaged: 1) our

2016F BPS multiplied by a P/B of 0.7x (the upper end of the recent three-year P/E

band), and 2) a 2016F DPS multiplied by the three-year KTB yield.

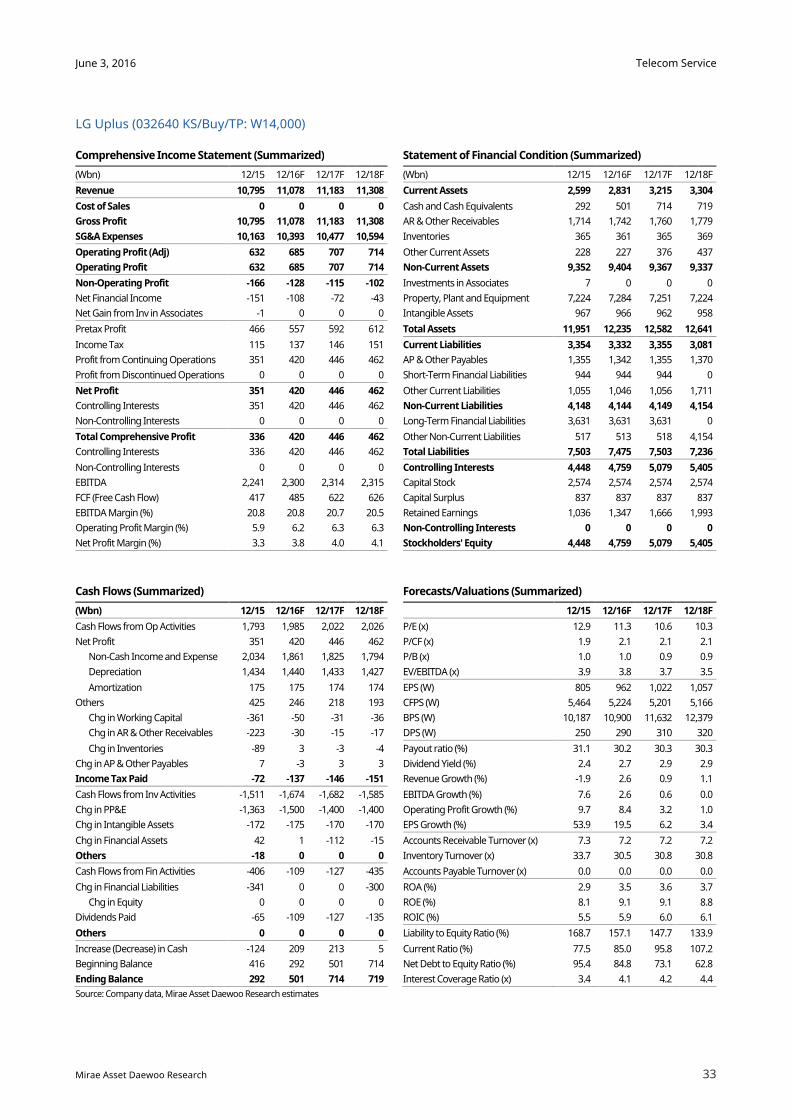

KT (030200 KS)

Stable earnings and higher dividends

FY (Dec.) 12/13 12/14 12/15 12/16F 12/17F 12/18F

Revenue (Wbn) 23,811 22,312 22,281 22,560 22,574 22,677

OP (Wbn) 839 -407 1,293 1,415 1,440 1,401

OP margin (%) 3.5 -1.8 5.8 6.3 6.4 6.2

NP (Wbn) -162 -1,055 553 581 646 646

EPS (W) -622 -4,040 2,118 2,224 2,473 2,473

ROE (%) -1.4 -9.5 5.2 5.2 5.6 5.4

P/E (x) - - 13.3 14.0 12.6 12.6

P/B (x) 0.6 0.7 0.6 0.7 0.6 0.6

Note: All figures are based on consolidated K-IFRS; NP refers to net profit attributable to controlling interests

Source: Company data, Mirae Asset Daewoo Research estimates

Telecom Service

(Maintain) Buy

Target Price (12M, W) 40,000

Share Price (06/02/16, W) 31,100

Expected Return 29%

OP (16F, Wbn) 1,415

Consensus OP (16F, Wbn) 1,381

EPS Growth (16F, %) 5.0

Market EPS Growth (16F, %) 16.6

P/E (16F, x) 14.0

Market P/E (16F, x) 10.6

KOSPI 1,985.11

Market Cap (Wbn) 8,121

Shares Outstanding (mn) 261

Free Float (%) 85.9

Foreign Ownership (%) 49.0

Beta (12M) 0.24

52-Week Low 26,350

52-Week High 32,550

(%) 1M 6M 12M

Absolute 1.0 4.7 5.6

Relative 0.6 6.0 10.6

70

80

90

100

110

120

6.15 10.15 2.16 6.16

KT KOSPI

Telecom Service

26

June 3, 2016

KDB Daewoo Securities Research

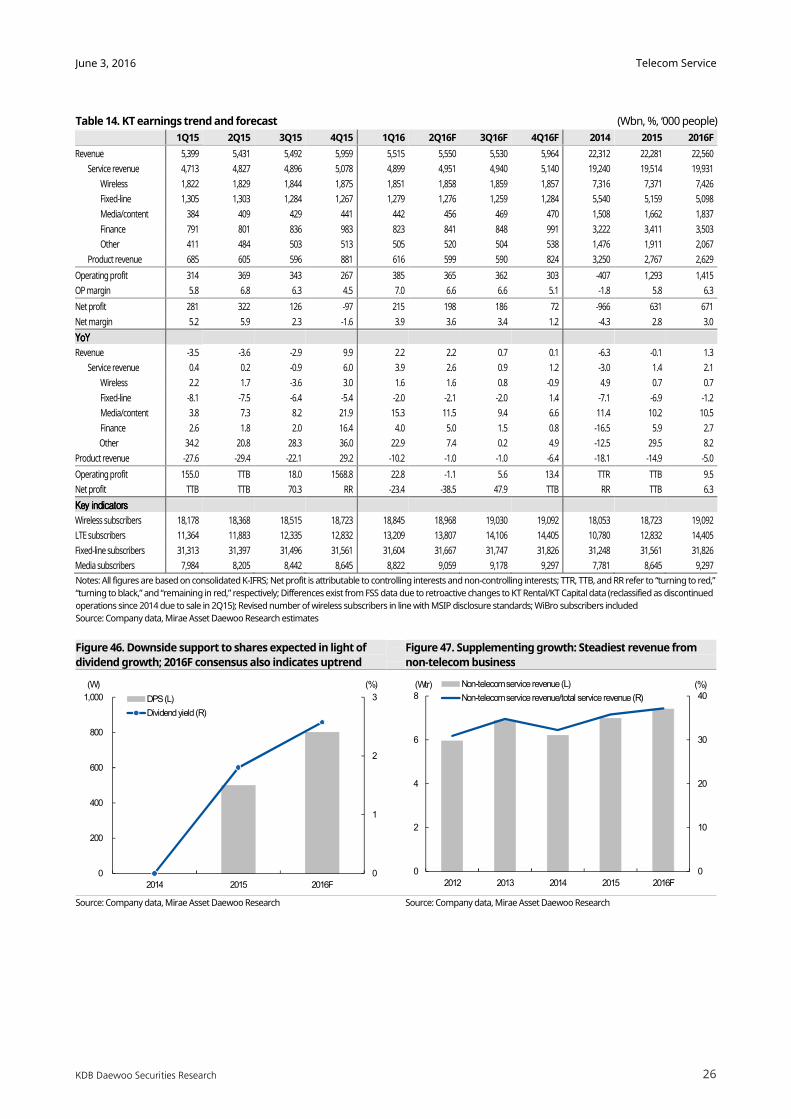

Table 14. KT earnings trend and forecast (Wbn, %, ‘000 people)

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16F 3Q16F 4Q16F 2014 2015 2016F

Revenue 5,399 5,431 5,492 5,959 5,515 5,550 5,530 5,964 22,312 22,281 22,560

Service revenue 4,713 4,827 4,896 5,078 4,899 4,951 4,940 5,140 19,240 19,514 19,931

Wireless 1,822 1,829 1,844 1,875 1,851 1,858 1,859 1,857 7,316 7,371 7,426

Fixed-line 1,305 1,303 1,284 1,267 1,279 1,276 1,259 1,284 5,540 5,159 5,098

Media/content 384 409 429 441 442 456 469 470 1,508 1,662 1,837

Finance 791 801 836 983 823 841 848 991 3,222 3,411 3,503

Other 411 484 503 513 505 520 504 538 1,476 1,911 2,067

Product revenue 685 605 596 881 616 599 590 824 3,250 2,767 2,629

Operating profit 314 369 343 267 385 365 362 303 -407 1,293 1,415

OP margin 5.8 6.8 6.3 4.5 7.0 6.6 6.6 5.1 -1.8 5.8 6.3

Net profit 281 322 126 -97 215 198 186 72 -966 631 671

Net margin 5.2 5.9 2.3 -1.6 3.9 3.6 3.4 1.2 -4.3 2.8 3.0

YoYYoYYoYYoY

Revenue -3.5 -3.6 -2.9 9.9 2.2 2.2 0.7 0.1 -6.3 -0.1 1.3

Service revenue 0.4 0.2 -0.9 6.0 3.9 2.6 0.9 1.2 -3.0 1.4 2.1

Wireless 2.2 1.7 -3.6 3.0 1.6 1.6 0.8 -0.9 4.9 0.7 0.7

Fixed-line -8.1 -7.5 -6.4 -5.4 -2.0 -2.1 -2.0 1.4 -7.1 -6.9 -1.2

Media/content 3.8 7.3 8.2 21.9 15.3 11.5 9.4 6.6 11.4 10.2 10.5

Finance 2.6 1.8 2.0 16.4 4.0 5.0 1.5 0.8 -16.5 5.9 2.7

Other 34.2 20.8 28.3 36.0 22.9 7.4 0.2 4.9 -12.5 29.5 8.2

Product revenue -27.6 -29.4 -22.1 29.2 -10.2 -1.0 -1.0 -6.4 -18.1 -14.9 -5.0

Operating profit 155.0 TTB 18.0 1568.8 22.8 -1.1 5.6 13.4 TTR TTB 9.5

Net profit TTB TTB 70.3 RR -23.4 -38.5 47.9 TTB RR TTB 6.3

Key indicatorsKey indicatorsKey indicatorsKey indicators

Wireless subscribers 18,178 18,368 18,515 18,723 18,845 18,968 19,030 19,092 18,053 18,723 19,092

LTE subscribers 11,364 11,883 12,335 12,832 13,209 13,807 14,106 14,405 10,780 12,832 14,405

Fixed-line subscribers 31,313 31,397 31,496 31,561 31,604 31,667 31,747 31,826 31,248 31,561 31,826

Media subscribers 7,984 8,205 8,442 8,645 8,822 9,059 9,178 9,297 7,781 8,645 9,297

Notes: All figures are based on consolidated K-IFRS; Net profit is attributable to controlling interests and non-controlling interests; TTR, TTB, and RR refer to “turning to red,”

“turning to black,” and “remaining in red,” respectively; Differences exist from FSS data due to retroactive changes to KT Rental/KT Capital data (reclassified as discontinued

operations since 2014 due to sale in 2Q15); Revised number of wireless subscribers in line with MSIP disclosure standards; WiBro subscribers included

Source: Company data, Mirae Asset Daewoo Research estimates

Figure 46. Downside support to shares expected in light of

dividend growth; 2016F consensus also indicates uptrend

Figure 47. Supplementing growth: Steadiest revenue from

non-telecom business

Source: Company data, Mirae Asset Daewoo Research Source: Company data, Mirae Asset Daewoo Research

0

10

20

30

40

0

2

4

6

8

2012 2013 2014 2015 2016F

(%)(Wtr) Non-telecom service revenue (L)

Non-telecom service revenue/total service revenue (R)

0

1

2

3

0

200

400

600

800

1,000

2014 2015 2016F

(%)(W)

DPS (L)

Dividend yield (R)

Telecom Service

27

June 3, 2016

Mirae Asset Daewoo Research

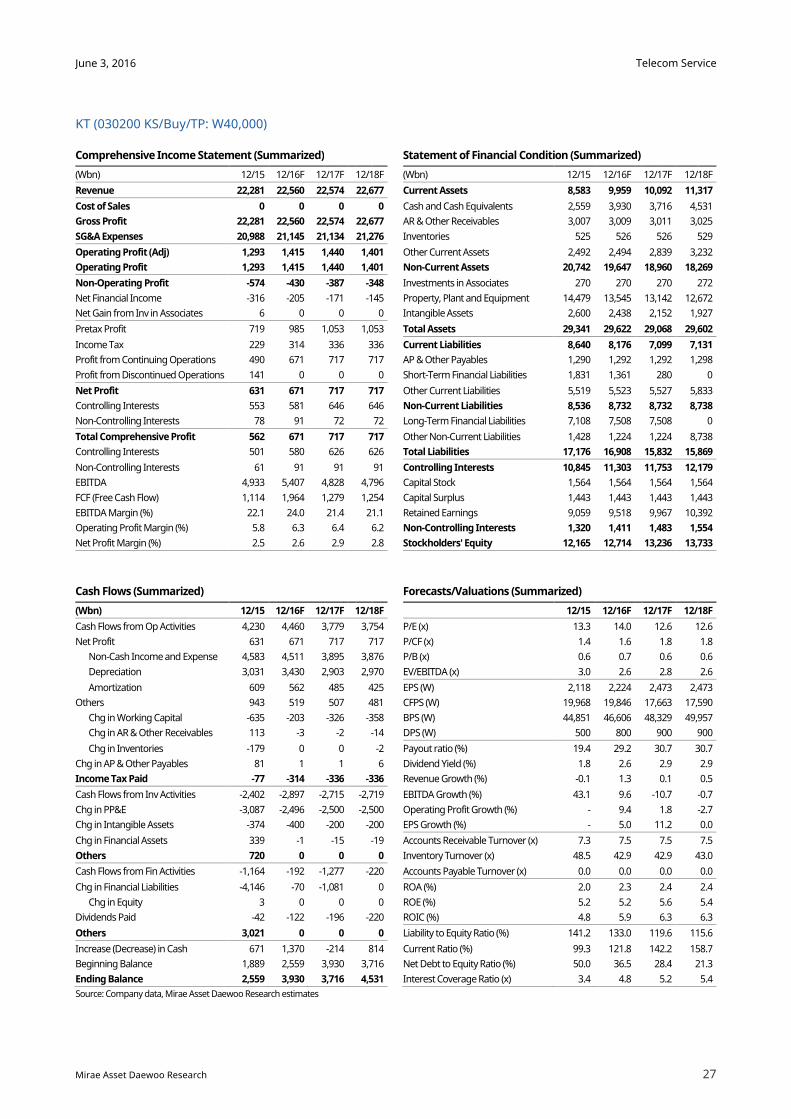

KT (030200 KS/Buy/TP: W40,000)

Comprehensive Income Statement (Summarized) Statement of Financial Condition (Summarized)

(Wbn) 12/15 12/16F 12/17F 12/18F (Wbn) 12/15 12/16F 12/17F 12/18F

Revenue 22,281 22,560 22,574 22,677 Current Assets 8,583 9,959 10,092 11,317

Cost of Sales 0 0 0 0 Cash and Cash Equivalents 2,559 3,930 3,716 4,531

Gross Profit 22,281 22,560 22,574 22,677 AR & Other Receivables 3,007 3,009 3,011 3,025

SG&A Expenses 20,988 21,145 21,134 21,276 Inventories 525 526 526 529

Operating Profit (Adj) 1,293 1,415 1,440 1,401 Other Current Assets 2,492 2,494 2,839 3,232

Operating Profit 1,293 1,415 1,440 1,401 Non-Current Assets 20,742 19,647 18,960 18,269

Non-Operating Profit -574 -430 -387 -348 Investments in Associates 270 270 270 272

Net Financial Income -316 -205 -171 -145 Property, Plant and Equipment 14,479 13,545 13,142 12,672

Net Gain from Inv in Associates 6 0 0 0 Intangible Assets 2,600 2,438 2,152 1,927

Pretax Profit 719 985 1,053 1,053 Total Assets 29,341 29,622 29,068 29,602

Income Tax 229 314 336 336 Current Liabilities 8,640 8,176 7,099 7,131

Profit from Continuing Operations 490 671 717 717 AP & Other Payables 1,290 1,292 1,292 1,298

Profit from Discontinued Operations 141 0 0 0 Short-Term Financial Liabilities 1,831 1,361 280 0

Net Profit 631 671 717 717 Other Current Liabilities 5,519 5,523 5,527 5,833

Controlling Interests 553 581 646 646 Non-Current Liabilities 8,536 8,732 8,732 8,738

Non-Controlling Interests 78 91 72 72 Long-Term Financial Liabilities 7,108 7,508 7,508 0

Total Comprehensive Profit 562 671 717 717 Other Non-Current Liabilities 1,428 1,224 1,224 8,738

Controlling Interests 501 580 626 626 Total Liabilities 17,176 16,908 15,832 15,869

Non-Controlling Interests 61 91 91 91 Controlling Interests 10,845 11,303 11,753 12,179

EBITDA 4,933 5,407 4,828 4,796 Capital Stock 1,564 1,564 1,564 1,564

FCF (Free Cash Flow) 1,114 1,964 1,279 1,254 Capital Surplus 1,443 1,443 1,443 1,443