2nd corporate debt investor trip - engie · pdf file2nd corporate debt investor trip buenos...

TRANSCRIPT

2nd Corporate Debt Investor Trip

Buenos Aires, October 2011

Presenter

2

Bernardita infante, CFO

Agenda

3

Chilean electricity sector

overview

Company overview

Financial profile

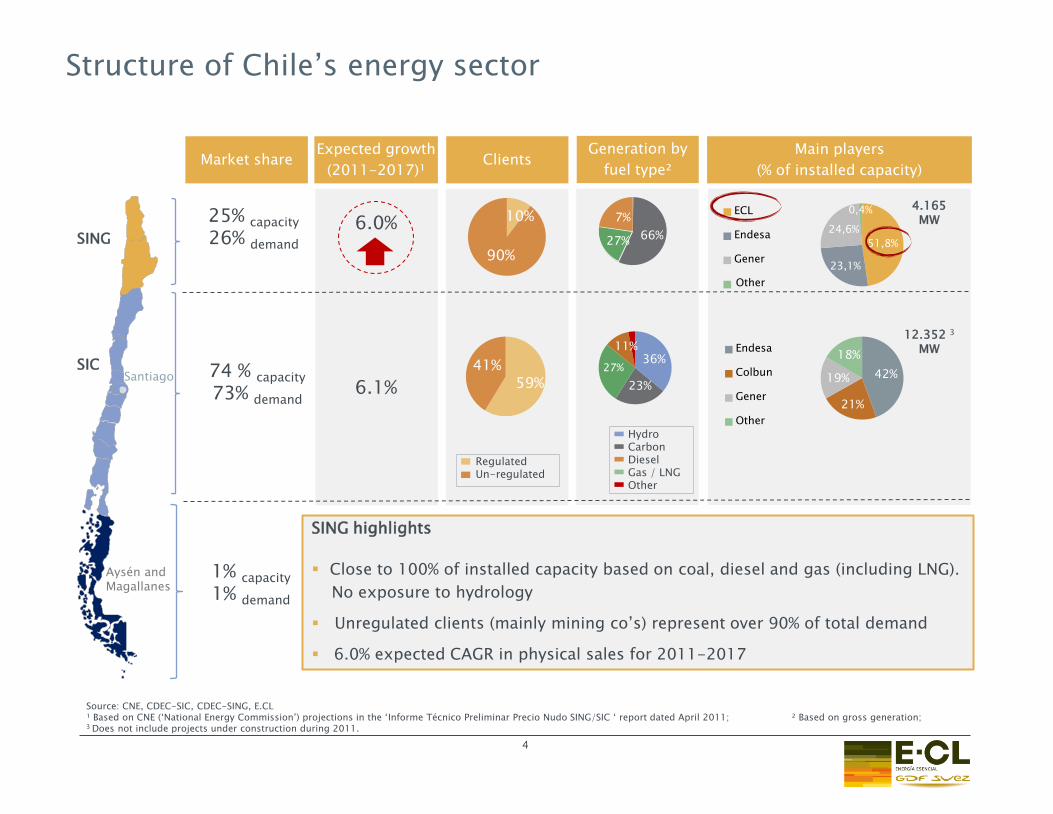

51,8%

23,1%

24,6%

0,4% ECL

Endesa

Gener

Otros Other

10%

90%

Source: CNE, CDEC-SIC, CDEC-SING, E.CL ¹ Based on CNE („National Energy Commission‟) projections in the „Informe Técnico Preliminar Precio Nudo SING/SIC „ report dated April 2011; ² Based on gross generation; 3 Does not include projects under construction during 2011.

Santiago

6.0%

6.1%

SING

SIC

Aysén and Magallanes

Hydro Carbon Diesel Gas / LNG Other

59% 41%

4.165 MW

42%

21%

19%

18% Endesa

Colbun

Gener

Other

12.352 3 MW

4

66% 27%

7%

36%

23%

27%

11%

Market share Expected growth

(2011-2017)¹

Main players

(% of installed capacity) Clients

Generation by

fuel type²

Structure of Chile‟s energy sector

SING highlights

Close to 100% of installed capacity based on coal, diesel and gas (including LNG).

No exposure to hydrology

Unregulated clients (mainly mining co‟s) represent over 90% of total demand

6.0% expected CAGR in physical sales for 2011-2017

25% capacity

26% demand

74 % capacity

73% demand

1% capacity 1% demand

Regulated Un-regulated

5

Evolution of Power Generation, Prices and Demand in the SING

New capacity

Source: CDEC- SING / CNE

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

1994 1996 1998 2000 2002 2004 2006 2008 2010³

SING copper production (kt) SING demand (GWh)

1,5

1,8

1,4 1,4

1,0 1,0

1,1

0,9 0,9 1,0

1,5

1,8

3,2 3,2

2,9

2,3

3,3

17 18 22 20

14

19

30 26 26

31

41

57

67

72

100

62

78

Exposure to mining sector growth ∎ Chile is a global, low-cost copper producer ∎ Low correlation between copper prices and SING demand for electricity.

6

SING copper production (kt), SING Generation (GWh) and commodity prices (US$/lb, bbl)

Source: Cochilco, CNE, Bloomberg ¹ Measured as the standard deviation of the annual changes; ² Calculated as the correlation of the annual changes; ³ Annualized September 2010 data

kt GWh

Volatility¹ Correl. with

energy output²

Copper Production 11.2% 0.87

Copper Price 28.2% (0.40)

Annual average copper price (US$/lb) Annual average WTI price (US$/bbl)

US$ 0

US$ 50

US$ 100

US$ 150

US$ 200

US$ 250

US$ 300

US$ 350

0

200

400

600

800

1.000

1.200

1.400

2004 2005 2006 2007 2008 2009 2010

Coal Nat. Gas Diesel + Fuel Oil

Hydro Spot Contract average¹

SING: installed capacity and generation mix

7

Gross installed capacity by technology - 2011 (MW)

Source: CNE, CDEC ¹Average of contracted energy prices as published by the CNE 2Gas restrictions started in 2004, but were more strictly enforced starting in 2007

Monthly generation (GWh) and energy prices (US$/MWh)

GWh

US$/MWh

Gas restrictions from Argentina²

Source: CDEC-SING (1) AES Gener has an additional 416MW of capacity from the gas turbine in its

643MW CCGT in Salta, Argentina, which is currently unavailable for dispatch to the SING.

(2) Includes 182MW from 100% Endesa-owned Celta, and 781MW from Gas Atacama CCGTs (50% Endesa/50% Southern Cross). (3) LNG supply arrangement between mining companies, GNL Mejillones, E.CL, and

Gas Atacama in place from 05-2010 through 07-2012.

10

781

158 277

330

518

488

531

227

200

250

317

24

21

0

500

1000

1500

2000

2500

E.CL Endesa AES Gener Other

Diesel + Fuel oil

LNG ST

Nat. Gas-Arg.

LNG + Diesel

New coal

Coal

Hydro

1 2

3

ATRACTIVE INDUSTRY

Mature, 100% privatized market

Stable, investor friendly regulatory framework

Strong industry growth prospects

Current Challenges:

•New regulation on emissions from thermoelectric plants stricter limits on particulate matter and gas emissions:

Limits for existing plants: • PM = 50 mg/Nm3 ~ Dec 2013

• SOx = 400 mg/Nm3 ~ Jun 2015 (saturated zones;

e.g., Tocopilla)

• NOx = 500 mg/Nm3 ~ Jun 2016 (unsaturated

zones; e.g., Mejillones)

•Law Nr. 20,257 on Non-Conventional Renewable Energy (“ERNC” Law)

Action / Effects:

•Focus on environmental / social responsibility

•Investing to comply with new emission requirements

•Est. US$164 MM CAPEX in 2011–2015

•Ongoing studies for the potential development renewable power sources

•Environmental approval for additional 2 x 350MW coal capacity in place

•Availability to sell LNG-based generation

•New discussion about 20/20

8

Investment highlights: Attractive industry

Agenda

9

Chilean electricity sector overview

Company overview

Financial profile

37%

32%

15%

0%

16%

Coal

Gas/Diesel

Diesel & F.O.

Hydro

New Coal

44%

38%

18% 1%

CT Hornitos2 (165MW)

Tocopilla port

CT Andina2 (165MW)

TE Mejillones (592MW)

Diesel Arica (14MW)

Diesel Iquique (43MW)

Chapiquiña (10MW)

Mantos Blancos1 (29MW)

C. Tamaya (104MW)

TE Tocopilla (1,004MW)

1 Owned by a mining company but operated by ECL; ² Commercial operations commenced in 2011.

2,159 MW 2011 Gas transmission and

distribution operations

1,796 MW 2010

Collahuasi

Chuquicamata

Escondida

10

El Abra

Gaby

Largest electricity generator in Chile‟s mining dominated northern grid (~ 50% market share)

Installed capacity E.CL assets

Coal Diesel/derivatives Natural Gas Hydro

Technology

Norandino pipeline to Argentina (Salta region)

2,449 kms of high voltage transmission

lines

History and recent developments

11

1913 1981 1993 1996 2002 2009

2011

Electroandina is

founded as an

electricity

generation plant

for

Chuquicamata

(Codelco)

Edelnor is

created as spin-

off of Endesa‟s

assets in

northern Chile

Edelnor is

privatized.

Southern

Electric acquires

control.

Tractebel (now IPR

GDF Suez) acquires

1/3 ownership in

Electroandina.

Codelco retains

2/3s.

Edelnor files for

Chapter 11. GDF

Suez & Codelco

acquire 82%

GDF Suez & Codelco

merge their electricity

generation and gas

transportation assets

in northern Chile

under E.CL (ex-

Edelnor)

International Power (U.K.) & GDF Suez Energy International combine their assets giving origin to the new International Power, a company

with 66GW of installed capacity, 70% controlled by GDF Suez.

Codelco sells its 40% stake in E.CL in a public auction in the Bolsa de Comercio de Santiago for approximately US$ 1 billion.

New ownership structure

1 Considers the 0.7% equity reduction due to retirement of treasury stock acquired by E.CL from shareholders that exercised their dissenter‟s rights in relation to the December 2009 merger.

² 60% owned by E.CL, with the remaining 40% owned by Inversiones Punta de Rieles (Antofagasta Railway PLC).

Chilean Pension

Funds

52.76% 1

CTH²

(165 MW) Distrinor

Electroandina

(1,105 MW)

CTA

(165 MW)

GNAA

(4.5mm m³/day)

GNAC

(4.5mm m³/day)

Electricity generation Gas distribution Gas transportation

(691 MW)

Other Chilean

Institutional

Investors

Foreign

Institutional

Investors

Other

20.14% 13.02% 12.40% 1.68%

12

13

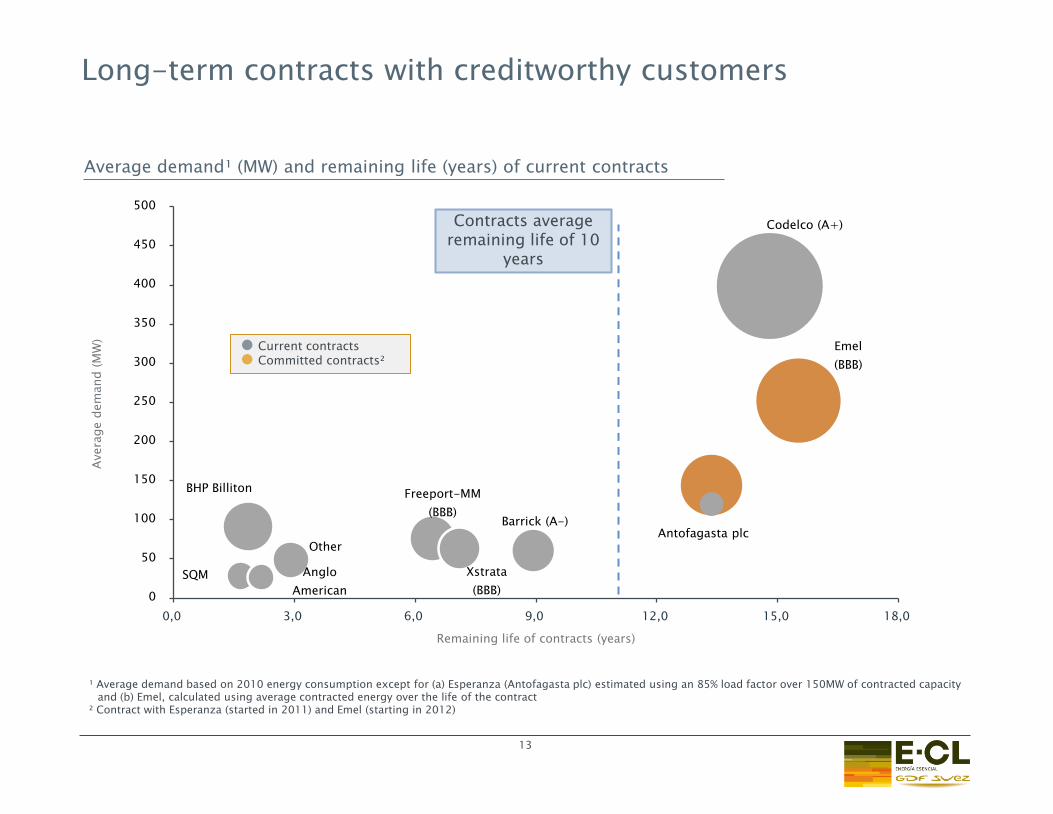

Long-term contracts with creditworthy customers

¹ Average demand based on 2010 energy consumption except for (a) Esperanza (Antofagasta plc) estimated using an 85% load factor over 150MW of contracted capacity and (b) Emel, calculated using average contracted energy over the life of the contract

² Contract with Esperanza (started in 2011) and Emel (starting in 2012)

Codelco (A+)

Freeport-MM

(BBB) Barrick (A-)

BHP Billiton

SQM Anglo

American

Xstrata

(BBB)

Other Antofagasta plc

Emel

(BBB)

0

50

100

150

200

250

300

350

400

450

500

0,0 3,0 6,0 9,0 12,0 15,0 18,0

Avera

ge d

em

and (

MW

)

Remaining life of contracts (years)

Average demand¹ (MW) and remaining life (years) of current contracts

● Current contracts ● Committed contracts²

Contracts average remaining life of 10

years

Long- term contracts , reducing exposure to the volatility of spot market

prices

Tariff index to fuel prices, that mitigate the risk of potential cost

increases.

Define optimal level of contractual obligations, taking into account our

generation capacity by type of fuel.

14

Driver‟s of E-CL ´s commercial policy

Investment highlights: Exposure to mining sector growth

Current challenges:

Growth could be slower in near term: Large investments in green-field copper projects take time to structure;

Significant electricity demand growth expected for 2015/2016 will require new capacity (and/or use of existing CCGTs) for at least 800MW:

Quadra FNX‟s Sierra Gorda; Teck‟s Quebrada Blanca; Collahuasi‟s Phases I & II.

Action / Effects:

Ongoing development of new 375MW coal plant and other projects: Subject to sign PPA for at least 50%

Capitalize on near-term growth: 135MW of new demand from Minera Esperanza starting 2011; 200MW under EMEL contract starting 2012.

Potential future mining projects in the SING

15

Company Proyect Capacity Demand-

MW

Full Capacity-

yr

Antofagasta Minerals Esperanza 130MW Apr-2011

Antofagasta Minerals Antucoya 45MW 2014

Codelco Ministro Hales 80MW 2015

BHP Escondida OGP 80MW 2015

Collahuasi Collahuasi expansion Phase I-II

50-170MW 2015-2018

Quadra FNX Mining Sierra Gorda 190MW 2015

Teck Quebrada Blanca Hip.

210MW 2016

International PBX Ventures

Copaquire 80MW 2017

Investment highlights: Attractive expansion plan

790

2.146 330

651

375

0

500

1000

1500

2000

2500

Current coal and

hydro capacity

CTA/CTH LNG Mejillones Expected base load

capacity

330 MW of coal base generation in 2011

Approx. 200MW commited LNG capacity to supply EMEL, starting 2012; Availability to commit remainder gas capacity at LNG market price beyond 2012.

Environmental approval for 2 x 375MW coal fired power plant in Mejillones + a port facility

Current and expected base capacity (MW)

16

17

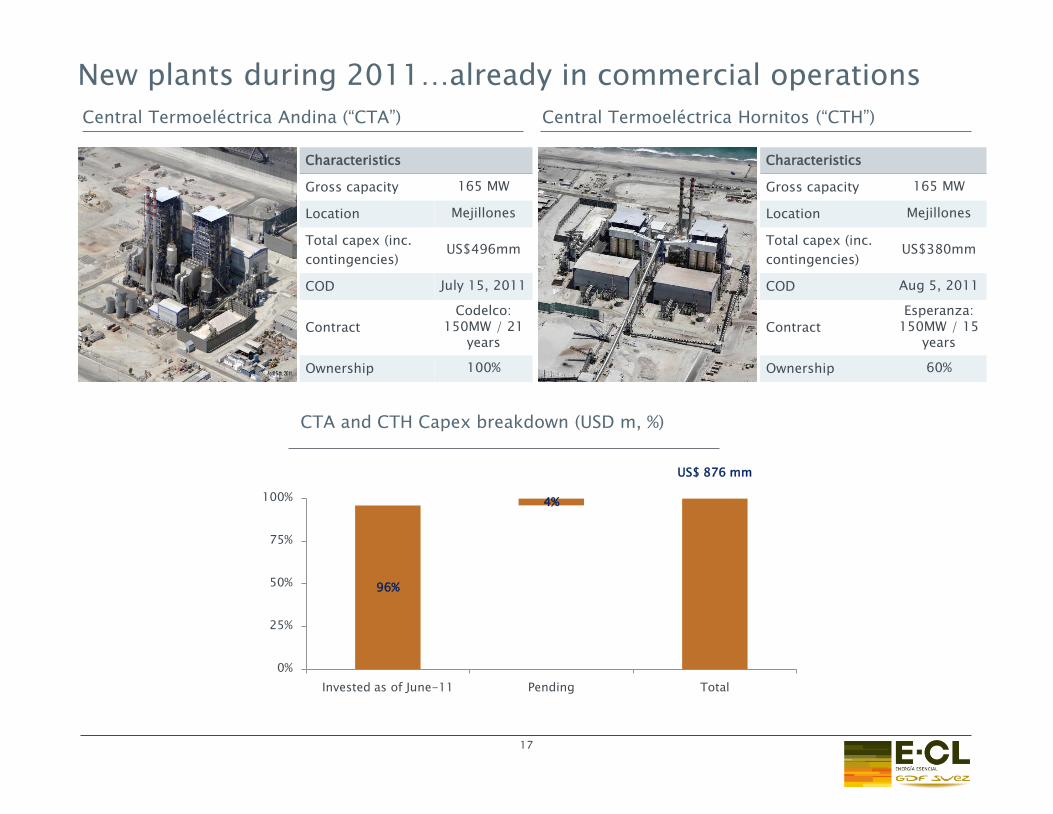

Central Termoeléctrica Andina (“CTA”) Central Termoeléctrica Hornitos (“CTH”)

96%

US$ 876 mm

4%

0%

25%

50%

75%

100%

Invested as of June-11 Pending Total

CTA and CTH Capex breakdown (USD m, %)

Characteristics

Gross capacity 165 MW

Location Mejillones

Total capex (inc.

contingencies) US$496mm

COD July 15, 2011

Contract

Codelco: 150MW / 21

years

Ownership 100%

Characteristics

Gross capacity 165 MW

Location Mejillones

Total capex (inc.

contingencies) US$380mm

COD Aug 5, 2011

Contract

Esperanza: 150MW / 15

years

Ownership 60%

New plants during 2011…already in commercial operations

18

Agenda

19

Chilean electricity sector overview

Company overview

Financial profile

E.CL: Financial Results

20

USD millones FY 10 1H10

1H11

Var. H%

Revenues 1.121 519 633 22%

Operating income 240 119 110 (7%)

Operating margin 21% 23% 17% -

EBITDA 340 167 161 (4%)

Net income 200 79 84 6%

Energy sales (GWh) 7.335 3.554 3.704 4%

2011: Adjustment period to new supply reality in the SING: 840MW of new efficient coal capacity (approx. 40% of average system output) under commissioning/testing in 1H and fully operational by 3Q;

New capacity will displace higher-cost less-efficient generation, pushing marginal energy costs downward;

Marginal energy costs averaged US$175MWh YTD June 30, 2011.

July 15, 2011 CTA commenced commercial operations with Codelco PPA in place

April 2011 CTH‟s PPA with Minera Esperanza commenced.

21

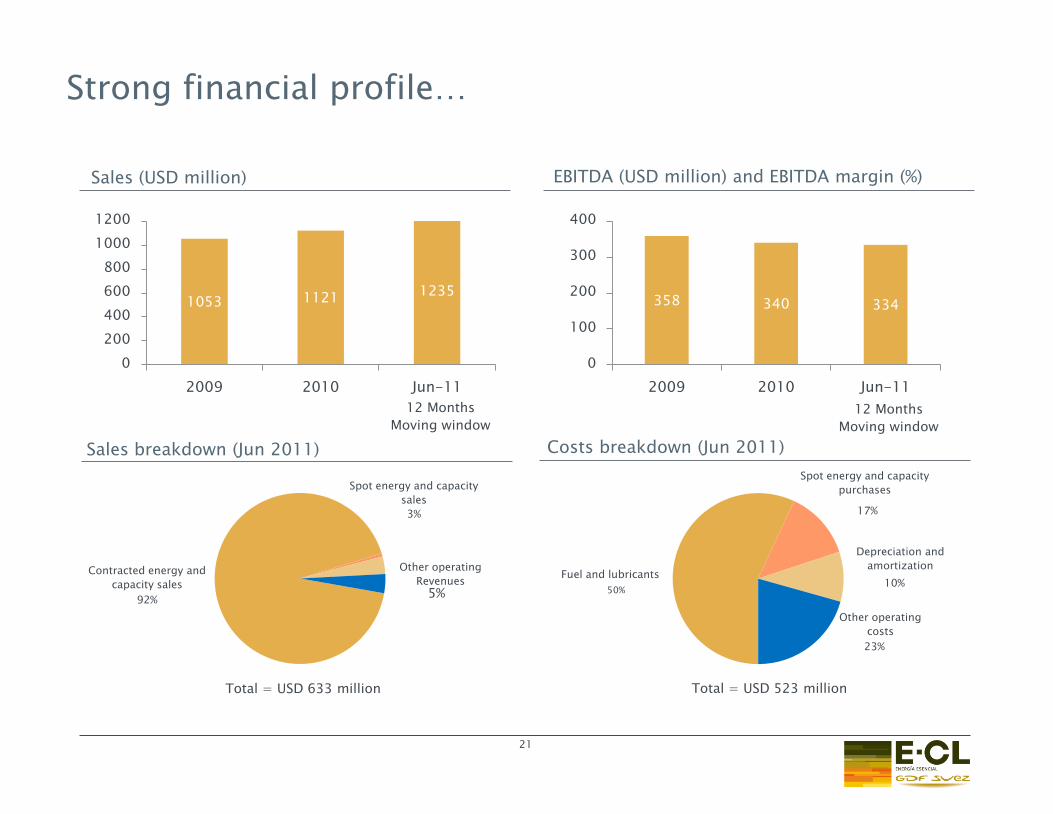

EBITDA (USD million) and EBITDA margin (%) Sales (USD million)

Costs breakdown (Jun 2011)

Total = USD 633 million Total = USD 523 million

Sales breakdown (Jun 2011)

1053 1121 1235

0

200

400

600

800

1000

1200

2009 2010 Jun-11

12 Months

Moving window

358 340 334

0

100

200

300

400

2009 2010 Jun-11

92% 5%

50%

23%

10%

17%

Contracted energy and

capacity sales

Spot energy and capacity

sales

3%

Other operating

Revenues Fuel and lubricants

Spot energy and capacity

purchases

Depreciation and

amortization

Other operating

costs

Strong financial profile…

12 Months

Moving window

22

2,1x 2,2x 2,2x

,0x

1,0x

2,0x

3,0x

2009 2010 Jun-11

1,6x 1,7x 1,7x

,0x

1,0x

2,0x

3,0x

2009 2010 Jun-11

23,2x 24,1x 26,7x

,0x

5,0x

10,0x

15,0x

20,0x

25,0x

2009 2010 Jun-11

Total debt/EBITDA Net debt/EBITDA

EBITDA/Interest expenses Credit ratings

Investment grade international ratings by S&P and Fitch:

S&P: BBB- (Stable Outlook)

Fitch: BBB- (Stable Outlook)

Investment grade local ratings by Fitch, Feller and ICR

Feller: A (Stable Outlook)

Fitch: A (Stable Outlook)

ICR: A (Stable Outlook)

…coupled with a conservative debt structure

12 Months

Moving window 12 Months

Moving window

12 Months

Moving window

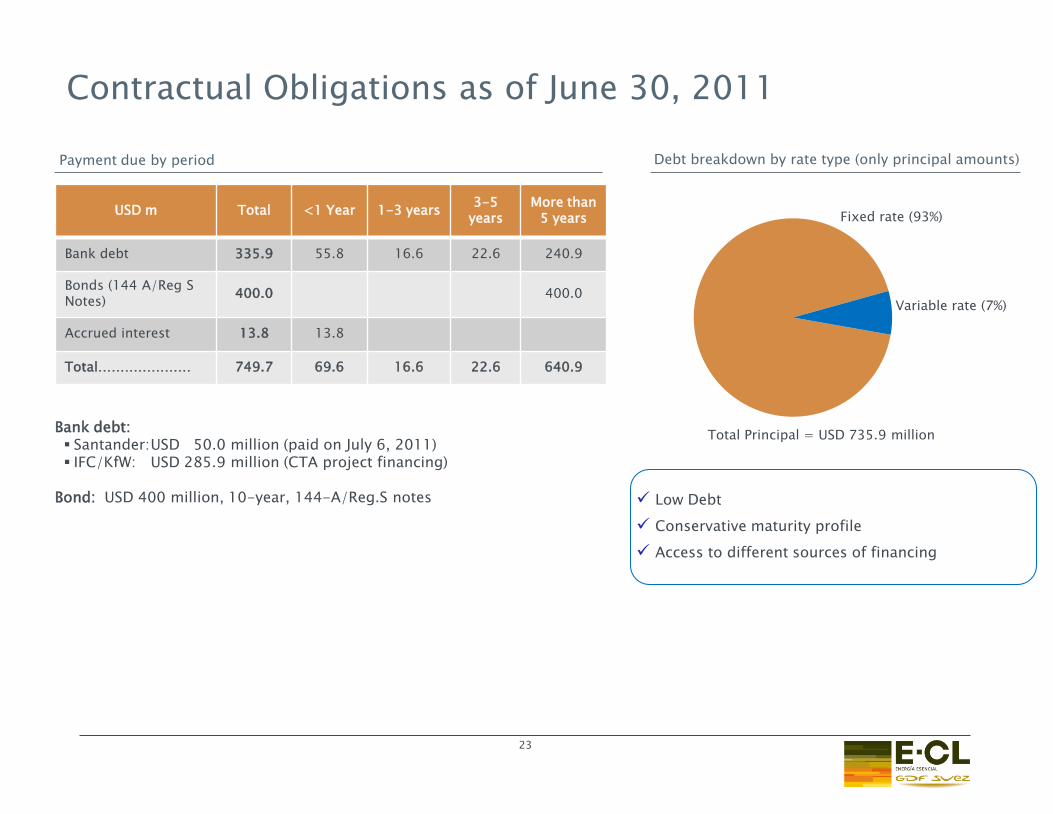

Contractual Obligations as of June 30, 2011

23

USD m Total <1 Year 1-3 years 3-5

years More than

5 years

Bank debt 335.9 55.8 16.6 22.6 240.9

Bonds (144 A/Reg S Notes)

400.0 400.0

Accrued interest 13.8 13.8

Total………………… 749.7 69.6 16.6 22.6 640.9

Bank debt: Santander: USD 50.0 million (paid on July 6, 2011) IFC/KfW: USD 285.9 million (CTA project financing)

Bond: USD 400 million, 10-year, 144-A/Reg.S notes

Payment due by period Debt breakdown by rate type (only principal amounts)

Fixed rate (93%)

Variable rate (7%)

Total Principal = USD 735.9 million

Low Debt

Conservative maturity profile

Access to different sources of financing

An attractive shareholder return

E.CL Share (as of 10/03/2011):

Market Cap: USD 2.456 bn

Price: CH$ 1,215

Source: Bloomberg

24 24

0,243

0,189

0,16

0,075

0,095

0,024

US$ 0,000

US$ 0,050

US$ 0,100

US$ 0,150

US$ 0,200

US$ 0,250

US$ 0,300 Return and Dividend per share

2009 2010

50% payout ratio: dividend paid in 2011 on account of FY2010 = USD 100 million

30% payout ratio

30% provisional dividend on

account of 1H11 net earnings

USD 25 million

2011E

Note: EPS 2011 anualizado