2q14 results presentation

TRANSCRIPT

August 08th, 2014

2Q14 Results

2

Disclaimer

The stand-alone and consolidated financial statements were prepared in accordance with the accounting

principles adopted in Brazil, which include corporation law, the pronouncements, instructions and

interpretations issued by the Accounting Pronouncements Committee (CPC) and the regulations of the

Securities and Exchange Commission of Brazil (CVM), combined with specific legislation issued by the

National Electric Power Agency (ANEEL). As the industry regulator, ANEEL has powers to regulate the

concessions. The results are usually presented in both IFRS and former formats in order to permit

comparisons with other periods. However, the results presented in “Regulatory” format are not audited.

ALUPAR uses the audited results based on the IFRS principles to declare dividends.

The forward-looking statements contained in this document relating to the business outlook, projections of

operational and financial results and the growth prospects of ALUPAR are merely projections, and as such

are based exclusively on management’s expectations for the future of the business. These expectations

depend materially on changes in market conditions and the performance of the Brazilian economy, the

sector and international markets and therefore are subject to change without prior notice.

3

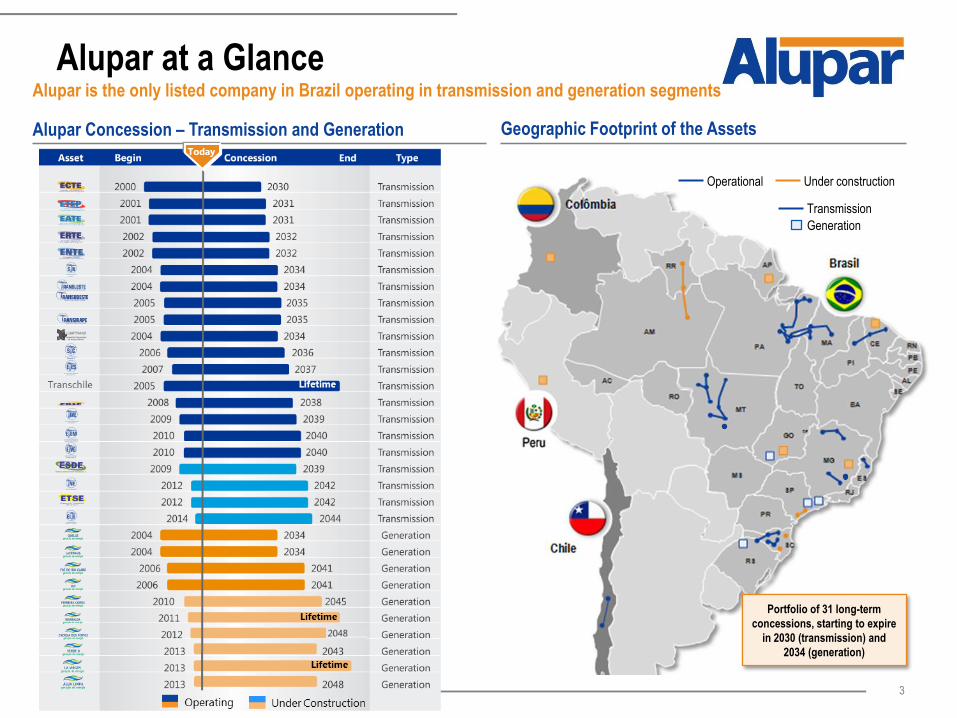

Alupar at a GlanceAlupar is the only listed company in Brazil operating in transmission and generation segments

Geographic Footprint of the Assets

Portfolio of 31 long-term

concessions, starting to expire

in 2030 (transmission) and

2034 (generation)

Alupar Concession – Transmission and Generation

Operational Under construction

Transmission

Generation

4

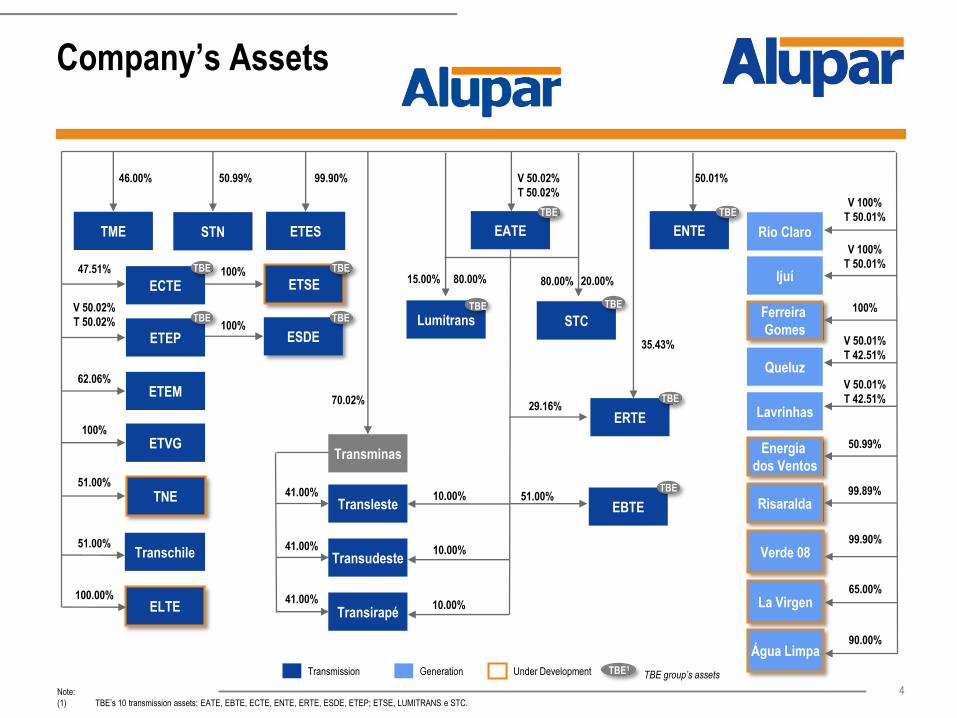

Company’s Assets

Note:

(1) TBE’s 10 transmission assets: EATE, EBTE, ECTE, ENTE, ERTE, ESDE, ETEP; ETSE, LUMITRANS e STC.

Generation Under Development TBE1TBE group’s assetsTransmission

STC

TBE

V 50.01%

T 42.51%

100%

50.01%V 50.02%

T 50.02%V 100%

T 50.01%

70.02%

V 50.01%

T 42.51%

99.90%

41.00%

41.00%

41.00%

Transminas

Lavrinhas

47.51%

50.99%

V 50.02%

T 50.02%

51.00%

80.00%15.00% 80.00% 20.00%

Transirapé

Transleste

Rio Claro

Ijuí

Queluz

Transudeste

Lumitrans

ETES

29.16%

V 100%

T 50.01%

STN ENTEEATE

ECTE

ERTE

ETEP

ETEM62.06%

ETVG

ESDE

Ferreira

Gomes

100%

TNE51.00%

Risaralda99.89%

100%

ETSE100%

46.00%

TME

50.99%Energia

dos Ventos

51.00%Transchile

TBE

TBE

TBE

TBE

TBE

TBE TBE

TBE

10.00%

10.00% Verde 0899.90%

La Virgen65.00%

Água Limpa90.00%

ELTE100.00%

10.00%

EBTE

TBE

35.43%

5

Alupar’s Business Culture

Financial Discipline

Responsible and Sustainable Growth

Efficient Capital Structure

Corporate Governance and Transparency

Skilled and Motivated Team

6

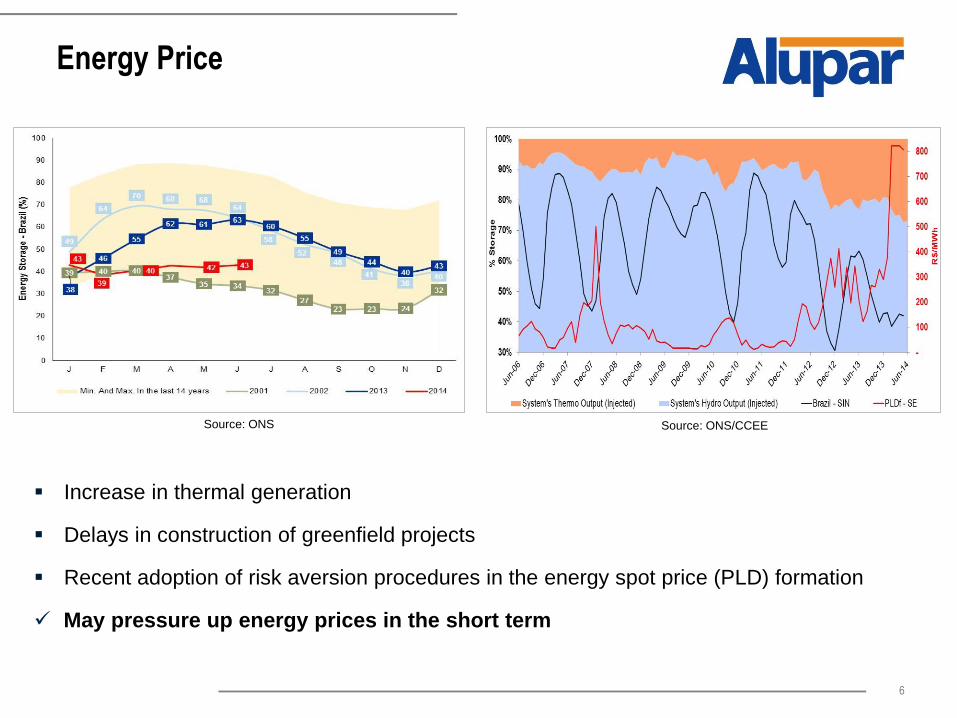

Energy Price

-- Increase in thermal generation

Delays in construction of greenfield projects

Recent adoption of risk aversion procedures in the energy spot price (PLD) formation

May pressure up energy prices in the short term

Source: ONS/CCEESource: ONS

7

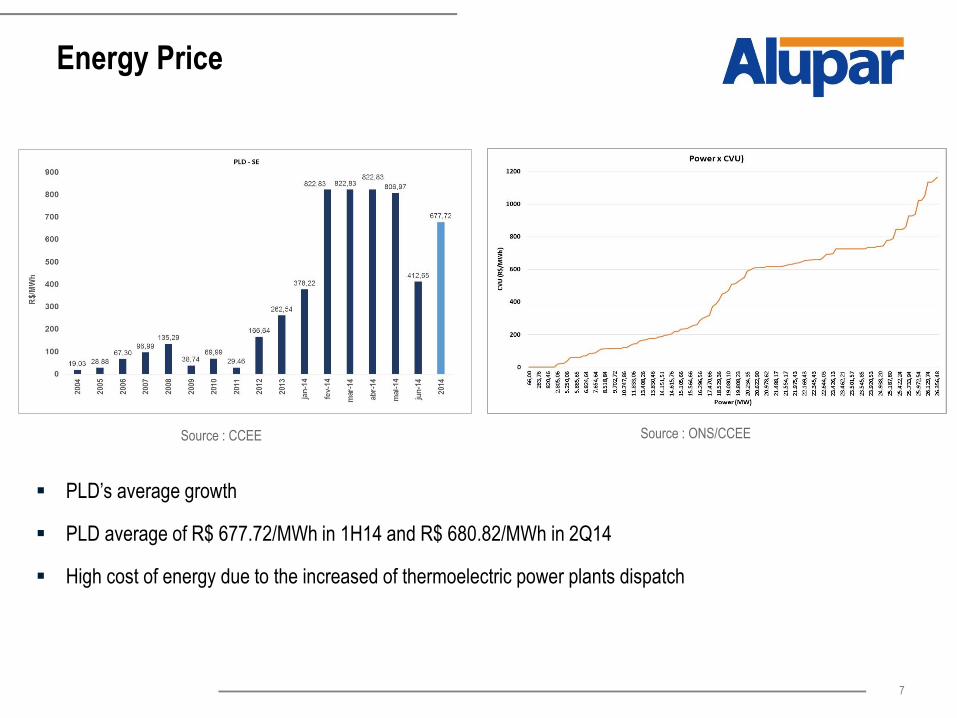

Energy Price

-

Source : ONS/CCEESource : CCEE

PLD’s average growth

PLD average of R$ 677.72/MWh in 1H14 and R$ 680.82/MWh in 2Q14

High cost of energy due to the increased of thermoelectric power plants dispatch

Financial Highlights

9

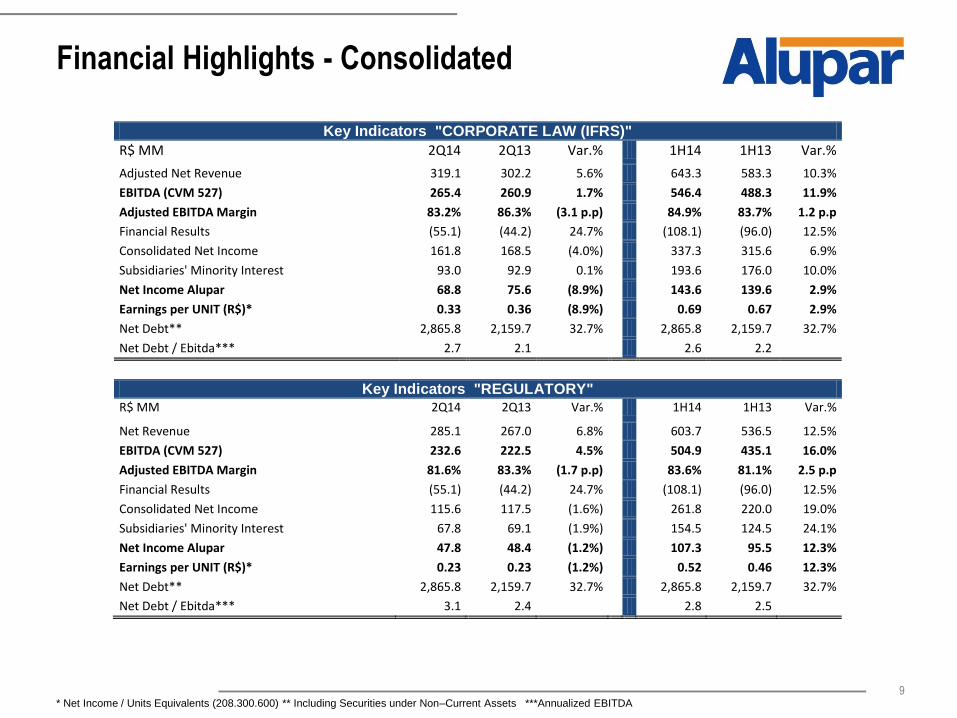

Financial Highlights - Consolidated

Key Indicators "CORPORATE LAW (IFRS)"

R$ MM 2Q14 2Q13 Var.% 1H14 1H13 Var.%

Adjusted Net Revenue 319.1 302.2 5.6% 643.3 583.3 10.3%

EBITDA (CVM 527) 265.4 260.9 1.7% 546.4 488.3 11.9%

Adjusted EBITDA Margin 83.2% 86.3% (3.1 p.p) 84.9% 83.7% 1.2 p.p

Financial Results (55.1) (44.2) 24.7% (108.1) (96.0) 12.5%

Consolidated Net Income 161.8 168.5 (4.0%) 337.3 315.6 6.9%

Subsidiaries' Minority Interest 93.0 92.9 0.1% 193.6 176.0 10.0%

Net Income Alupar 68.8 75.6 (8.9%) 143.6 139.6 2.9%

Earnings per UNIT (R$)* 0.33 0.36 (8.9%) 0.69 0.67 2.9%

Net Debt** 2,865.8 2,159.7 32.7% 2,865.8 2,159.7 32.7%

Net Debt / Ebitda*** 2.7 2.1 2.6 2.2

Key Indicators "REGULATORY" R$ MM 2Q14 2Q13 Var.% 1H14 1H13 Var.%

Net Revenue 285.1 267.0 6.8% 603.7 536.5 12.5%

EBITDA (CVM 527) 232.6 222.5 4.5% 504.9 435.1 16.0%

Adjusted EBITDA Margin 81.6% 83.3% (1.7 p.p) 83.6% 81.1% 2.5 p.p

Financial Results (55.1) (44.2) 24.7% (108.1) (96.0) 12.5%

Consolidated Net Income 115.6 117.5 (1.6%) 261.8 220.0 19.0%

Subsidiaries' Minority Interest 67.8 69.1 (1.9%) 154.5 124.5 24.1%

Net Income Alupar 47.8 48.4 (1.2%) 107.3 95.5 12.3%

Earnings per UNIT (R$)* 0.23 0.23 (1.2%) 0.52 0.46 12.3%

Net Debt** 2,865.8 2,159.7 32.7% 2,865.8 2,159.7 32.7%

Net Debt / Ebitda*** 3.1 2.4 2.8 2.5

* Net Income / Units Equivalents (208.300.600) ** Including Securities under Non–Current Assets ***Annualized EBITDA

10

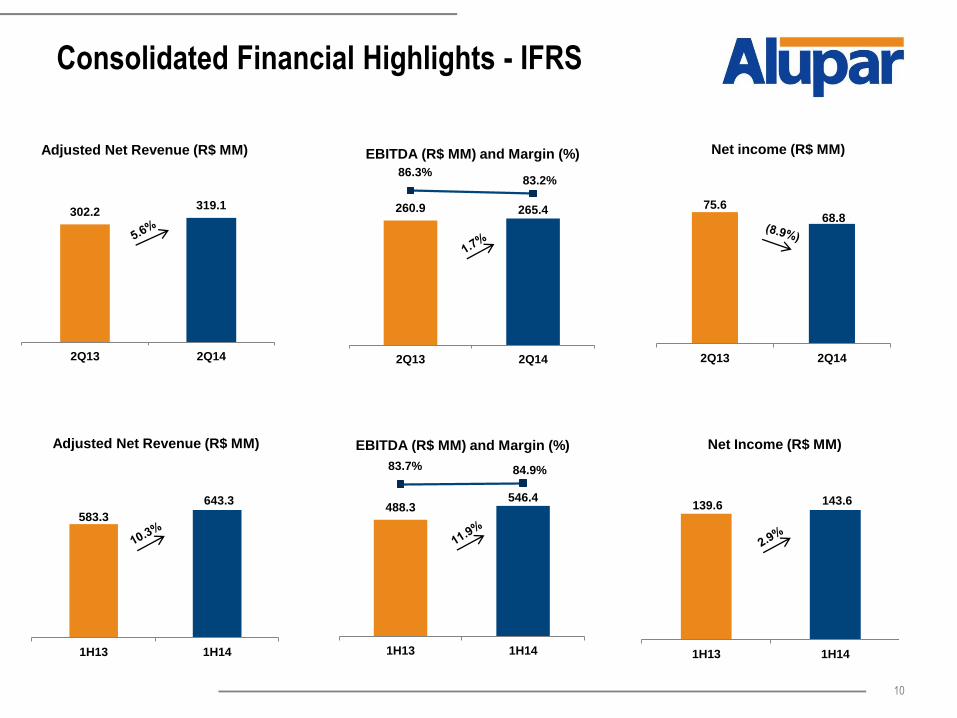

Consolidated Financial Highlights - IFRS

260.9 265.4

86.3%83.2%

2Q13 2Q14

EBITDA (R$ MM) and Margin (%)

75.668.8

2Q13 2Q14

Net income (R$ MM)

302.2319.1

2Q13 2Q14

Adjusted Net Revenue (R$ MM)

139.6 143.6

1H13 1H14

Net Income (R$ MM)

583.3

643.3

1H13 1H14

Adjusted Net Revenue (R$ MM)

488.3546.4

83.7% 84.9%

1H13 1H14

EBITDA (R$ MM) and Margin (%)

11

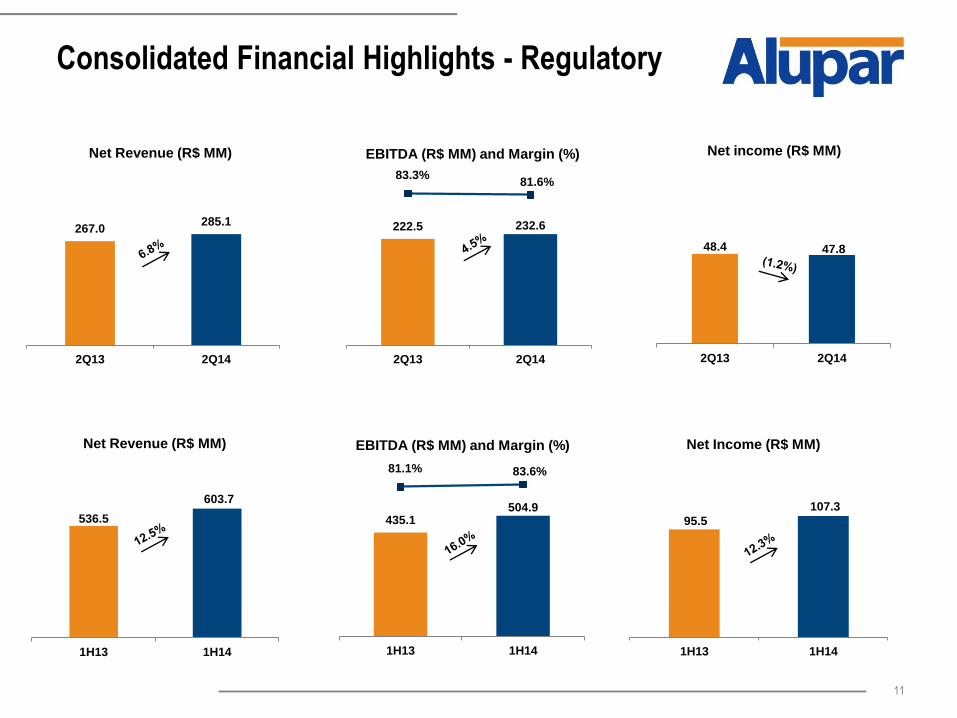

Consolidated Financial Highlights - Regulatory

222.5 232.6

83.3%81.6%

2Q13 2Q14

EBITDA (R$ MM) and Margin (%)

48.4 47.8

2Q13 2Q14

Net income (R$ MM)

267.0285.1

2Q13 2Q14

Net Revenue (R$ MM)

95.5

107.3

1H13 1H14

Net Income (R$ MM)

536.5

603.7

1H13 1H14

Net Revenue (R$ MM)

435.1504.9

81.1% 83.6%

1H13 1H14

EBITDA (R$ MM) and Margin (%)

12

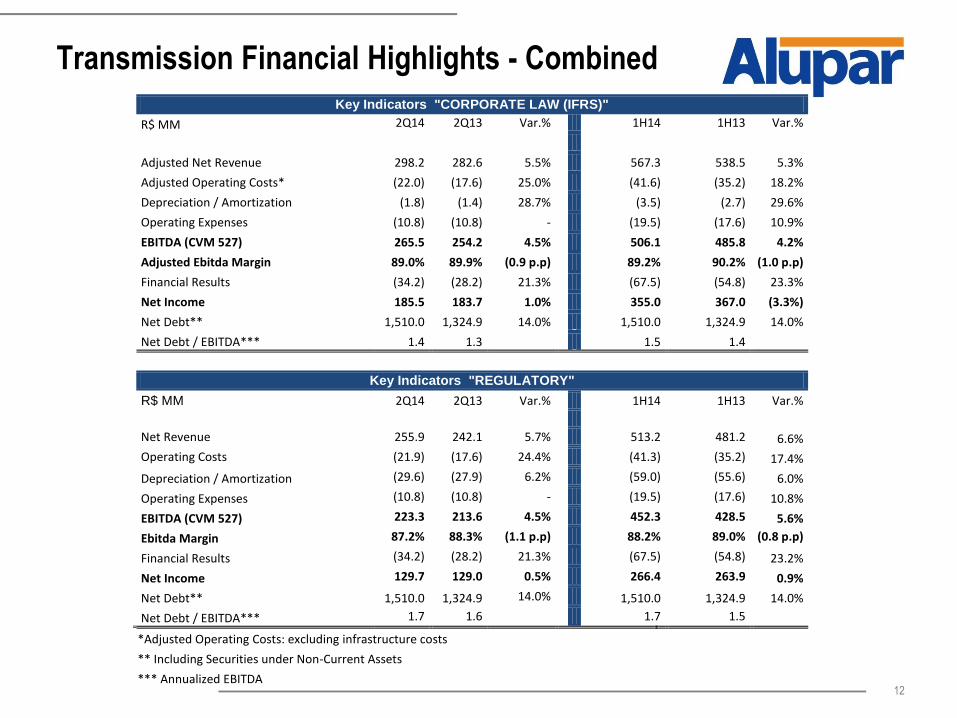

Transmission Financial Highlights - Combined

Key Indicators "CORPORATE LAW (IFRS)"

R$ MM 2Q14 2Q13 Var.% 1H14 1H13 Var.%

Adjusted Net Revenue 298.2 282.6 5.5% 567.3 538.5 5.3%

Adjusted Operating Costs* (22.0) (17.6) 25.0% (41.6) (35.2) 18.2%

Depreciation / Amortization (1.8) (1.4) 28.7% (3.5) (2.7) 29.6%

Operating Expenses (10.8) (10.8) - (19.5) (17.6) 10.9%

EBITDA (CVM 527) 265.5 254.2 4.5% 506.1 485.8 4.2%

Adjusted Ebitda Margin 89.0% 89.9% (0.9 p.p) 89.2% 90.2% (1.0 p.p)

Financial Results (34.2) (28.2) 21.3% (67.5) (54.8) 23.3%

Net Income 185.5 183.7 1.0% 355.0 367.0 (3.3%)

Net Debt** 1,510.0 1,324.9 14.0% 1,510.0 1,324.9 14.0%

Net Debt / EBITDA*** 1.4 1.3 1.5 1.4

Key Indicators "REGULATORY"

R$ MM 2Q14 2Q13 Var.% 1H14 1H13 Var.%

Net Revenue 255.9 242.1 5.7% 513.2 481.2 6.6%

Operating Costs (21.9) (17.6) 24.4% (41.3) (35.2) 17.4%

Depreciation / Amortization (29.6) (27.9) 6.2% (59.0) (55.6) 6.0%

Operating Expenses (10.8) (10.8) - (19.5) (17.6) 10.8%

EBITDA (CVM 527) 223.3 213.6 4.5% 452.3 428.5 5.6%

Ebitda Margin 87.2% 88.3% (1.1 p.p) 88.2% 89.0% (0.8 p.p)

Financial Results (34.2) (28.2) 21.3% (67.5) (54.8) 23.2%

Net Income 129.7 129.0 0.5% 266.4 263.9 0.9%

Net Debt** 1,510.0 1,324.9 14.0% 1,510.0 1,324.9 14.0%

Net Debt / EBITDA*** 1.7 1.6 1.7 1.5

*Adjusted Operating Costs: excluding infrastructure costs

** Including Securities under Non-Current Assets

*** Annualized EBITDA

13

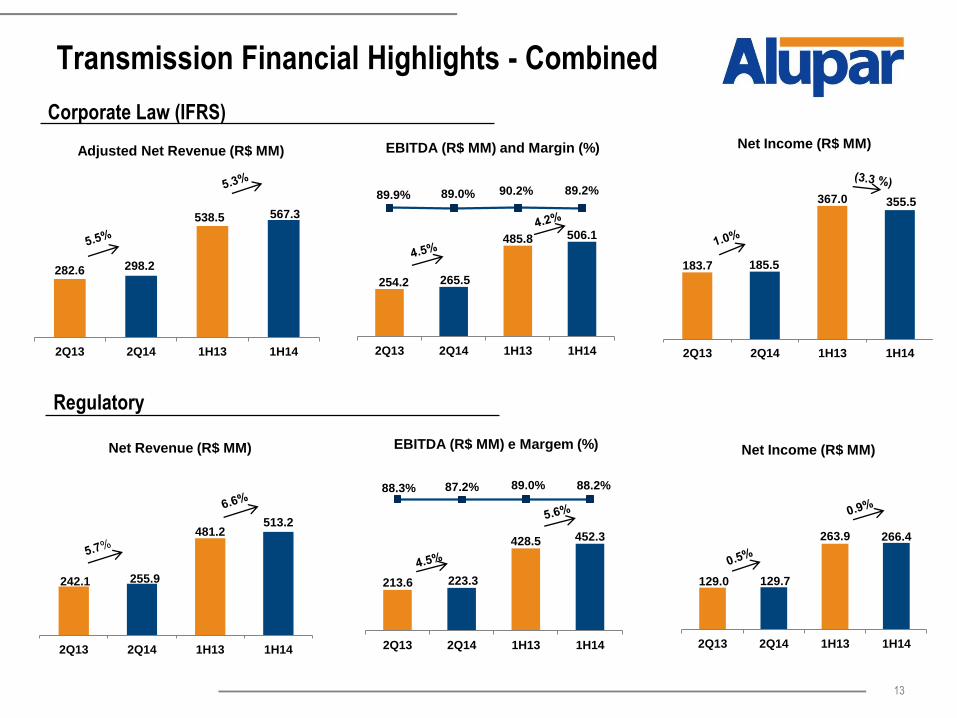

Transmission Financial Highlights - Combined

Corporate Law (IFRS)

282.6 298.2

538.5 567.3

2Q13 2Q14 1H13 1H14

Adjusted Net Revenue (R$ MM)

242.1 255.9

481.2513.2

2Q13 2Q14 1H13 1H14

Net Revenue (R$ MM)

129.0 129.7

263.9 266.4

2Q13 2Q14 1H13 1H14

Net Income (R$ MM)

Regulatory

254.2 265.5

485.8 506.1

89.9% 89.0% 90.2% 89.2%

2Q13 2Q14 1H13 1H14

EBITDA (R$ MM) and Margin (%)

213.6 223.3

428.5 452.3

88.3% 87.2% 89.0% 88.2%

2Q13 2Q14 1H13 1H14

EBITDA (R$ MM) e Margem (%)

183.7 185.5

367.0 355.5

2Q13 2Q14 1H13 1H14

Net Income (R$ MM)

14

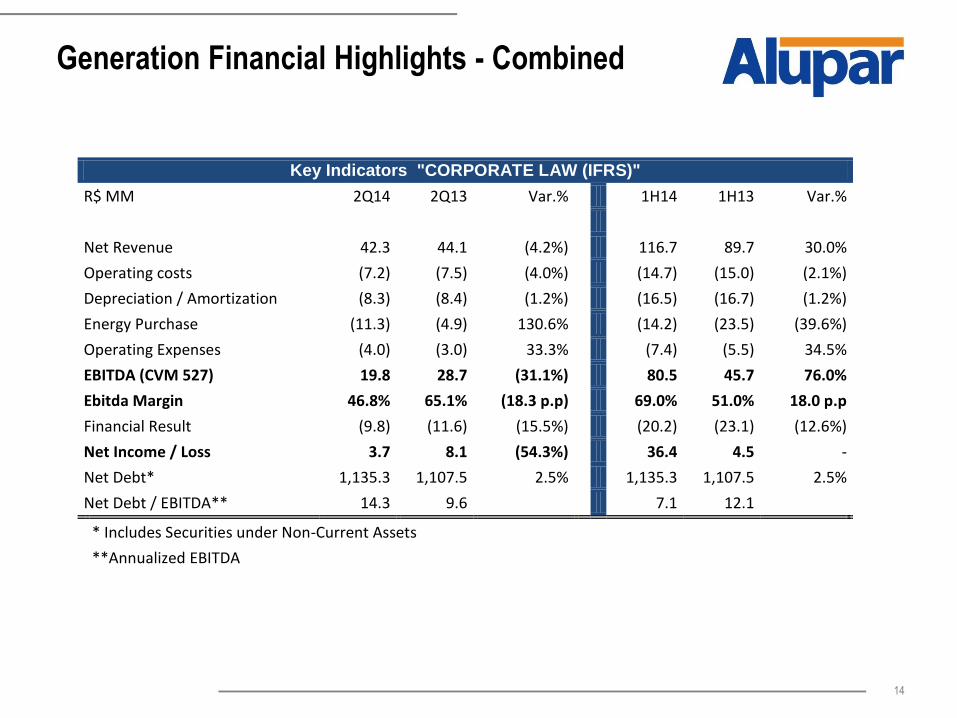

Generation Financial Highlights - Combined

Key Indicators "CORPORATE LAW (IFRS)"

R$ MM 2Q14 2Q13 Var.% 1H14 1H13 Var.%

Net Revenue 42.3 44.1 (4.2%) 116.7 89.7 30.0%

Operating costs (7.2) (7.5) (4.0%) (14.7) (15.0) (2.1%)

Depreciation / Amortization (8.3) (8.4) (1.2%) (16.5) (16.7) (1.2%)

Energy Purchase (11.3) (4.9) 130.6% (14.2) (23.5) (39.6%)

Operating Expenses (4.0) (3.0) 33.3% (7.4) (5.5) 34.5%

EBITDA (CVM 527) 19.8 28.7 (31.1%) 80.5 45.7 76.0%

Ebitda Margin 46.8% 65.1% (18.3 p.p) 69.0% 51.0% 18.0 p.p

Financial Result (9.8) (11.6) (15.5%) (20.2) (23.1) (12.6%)

Net Income / Loss 3.7 8.1 (54.3%) 36.4 4.5 -

Net Debt* 1,135.3 1,107.5 2.5% 1,135.3 1,107.5 2.5%

Net Debt / EBITDA** 14.3 9.6 7.1 12.1

* Includes Securities under Non-Current Assets

**Annualized EBITDA

15

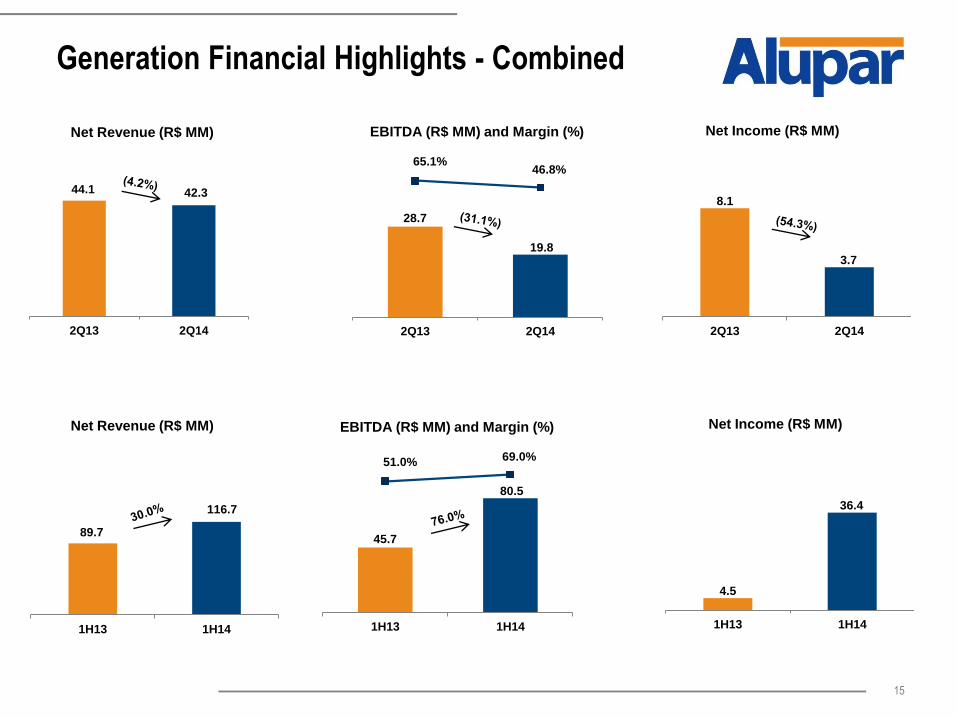

Generation Financial Highlights - Combined

44.1 42.3

2Q13 2Q14

Net Revenue (R$ MM)

89.7

116.7

1H13 1H14

Net Revenue (R$ MM)

28.7

19.8

65.1%46.8%

2Q13 2Q14

EBITDA (R$ MM) and Margin (%)

8.1

3.7

2Q13 2Q14

Net Income (R$ MM)

45.7

80.5

51.0% 69.0%

1H13 1H14

EBITDA (R$ MM) and Margin (%)

4.5

36.4

1H13 1H14

Net Income (R$ MM)

16

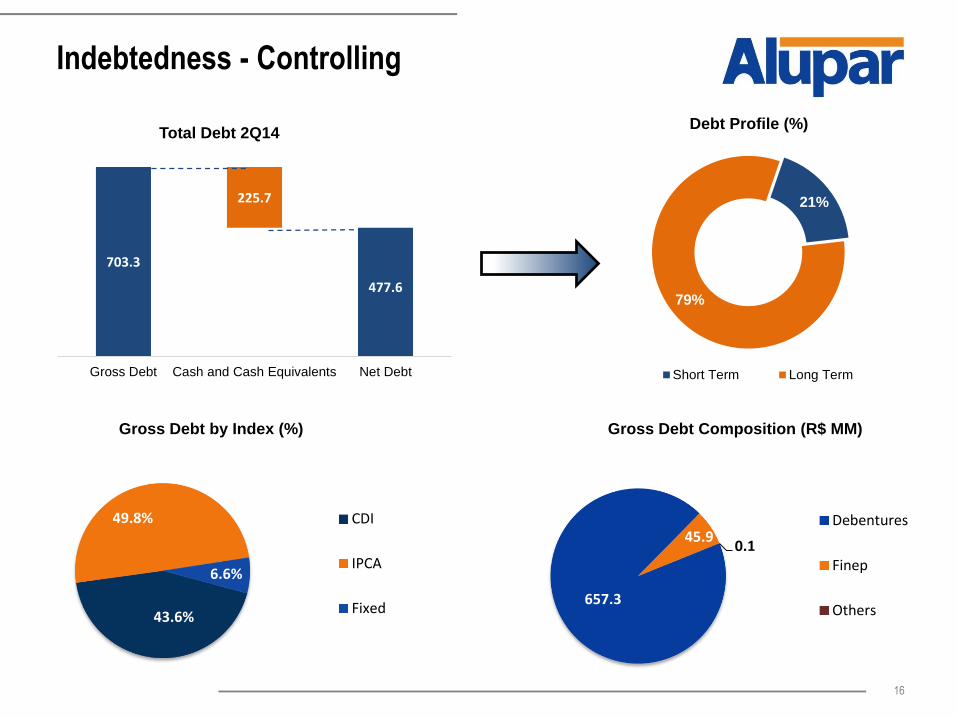

Indebtedness - Controlling

21%

79%

Debt Profile (%)

Short Term Long Term

703.3

477.6

225.7

Gross Debt Cash and Cash Equivalents Net Debt

Total Debt 2Q14

Gross Debt by Index (%) Gross Debt Composition (R$ MM)

43.6%

49.8%

6.6%

CDI

IPCA

Fixed657.3

45.90.1

Debentures

Finep

Others

17

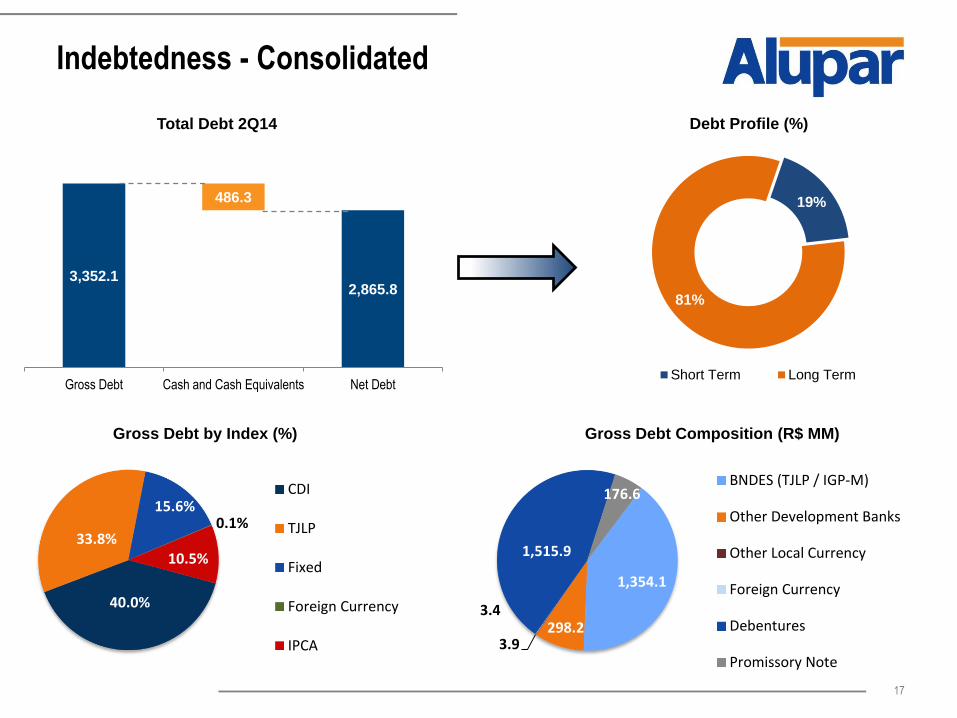

Indebtedness - Consolidated

19%

81%

Debt Profile (%)

Short Term Long Term

3,352.1

486.3

2,865.8

Gross Debt Cash and Cash Equivalents Net Debt

Total Debt 2Q14

Gross Debt by Index (%) Gross Debt Composition (R$ MM)

40.0%

33.8%

15.6%0.1%

10.5%

CDI

TJLP

Fixed

Foreign Currency

IPCA

1,354.1

298.23.9

3.4

1,515.9

176.6BNDES (TJLP / IGP-M)

Other Development Banks

Other Local Currency

Foreign Currency

Debentures

Promissory Note

18

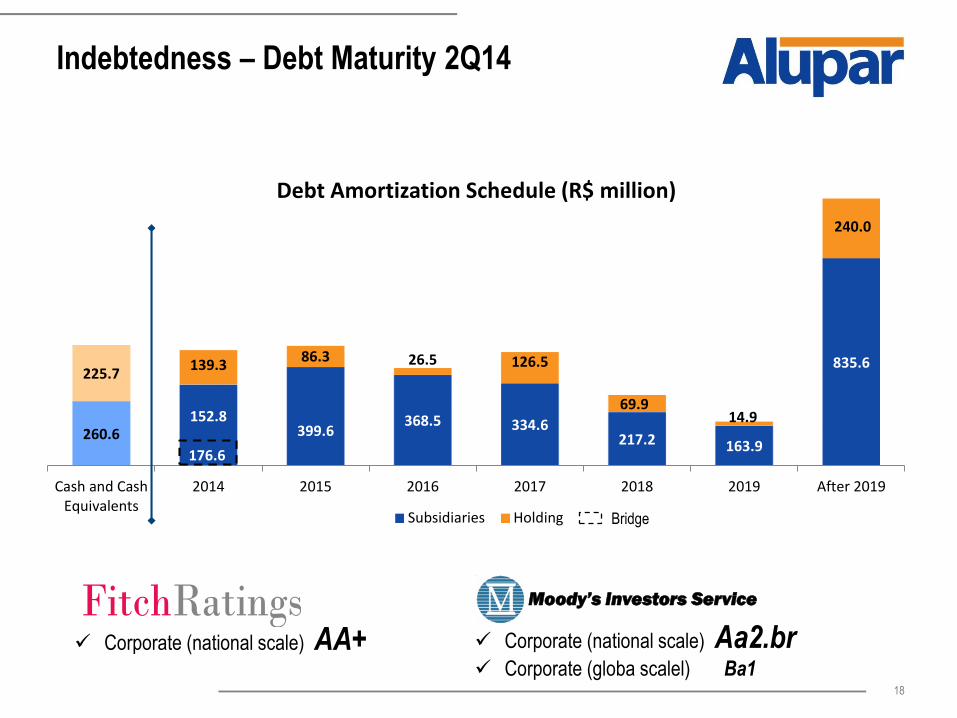

Indebtedness – Debt Maturity 2Q14

Moody’s Investors Service

Corporate (national scale) AA+ Corporate (national scale) Aa2.br Corporate (globa scalel) Ba1

260.6152.8

399.6368.5 334.6

217.2 163.9

835.6225.7

139.386.3 26.5 126.5

69.914.9

240.0

Cash and CashEquivalents

2014 2015 2016 2017 2018 2019 After 2019

Debt Amortization Schedule (R$ million)

Subsidiaries Holding

176.6

Bridge

IR Contacts

José Luiz de Godoy Pereira

IRO

Luiz Coimbra

IR Specialist

Kássia Orsi Amendola

IR Analyst

Tel.: +55 (11) 2184-9600