2q15 earnings presentation

TRANSCRIPT

1

Earnings Release | Conference Call – 2Q15

August 11th, 2015

2

Agenda

Ricardo Ribeiro

Vice President

Fernando Ramos

CFO and IR Officer

Operational Highlights

Financial Highlights

Highlights

Development’s contracted sales reached a PSV of R$ 112 million,a significant growth when compared to 1Q15;

In 1H15, 46% of launches and 41% of contracted saleswere in the low-income segment;

2015 year-to-date, more than R$ 100 million of cashflow to the shareholders, being R$ 67 million throughdividends and R$ 35 million through a share buybackprogram (total yield of approximately 20%, consideringthe currently share price);

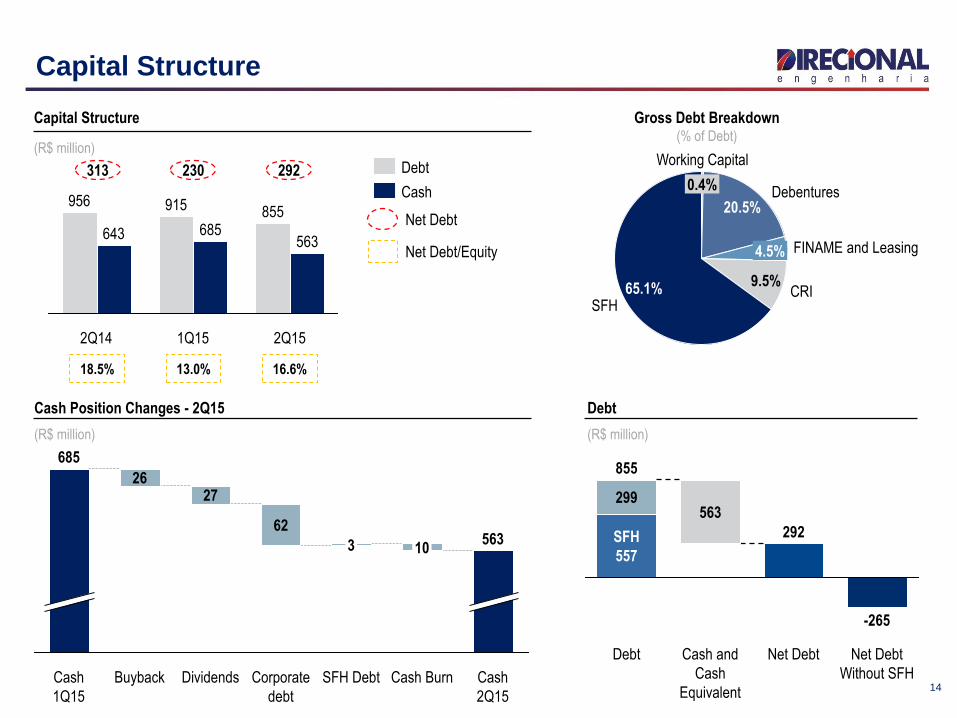

Strong capital structure, with net debt to equity of 16.6%, one of the lowest of the industry;

By the end of 2Q15, the deferred sales revenue totaled R$ 2.9 billion, most of which, R$ 2.4 billion, refers to MCMV Level 1 projects.

3

Launches

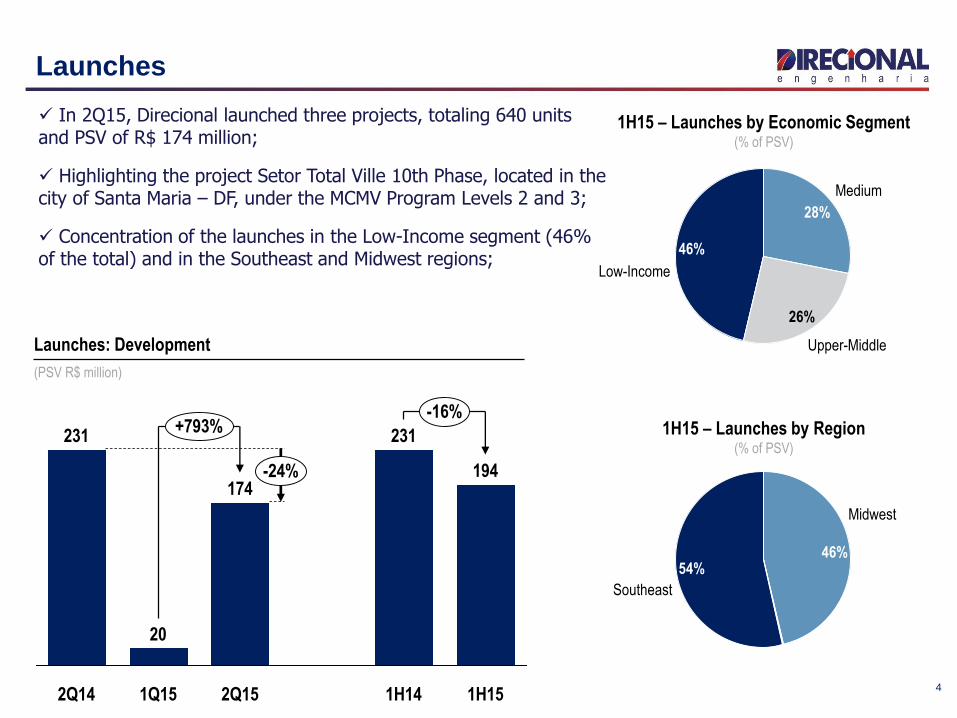

174

2Q15

231

1H14

231

1Q15

20

2Q14

-24%

+793%-16%

1H15

194

Launches: Development

(PSV R$ million)

In 2Q15, Direcional launched three projects, totaling 640 units and PSV of R$ 174 million;

Highlighting the project Setor Total Ville 10th Phase, located in the city of Santa Maria – DF, under the MCMV Program Levels 2 and 3;

Concentration of the launches in the Low-Income segment (46% of the total) and in the Southeast and Midwest regions;

1H15 – Launches by Region(% of PSV)

Southeast

54%

Midwest

46%

1H15 – Launches by Economic Segment(% of PSV)

Upper-Middle

26%

Medium

28%

Low-Income

46%

4

Contracted Sales

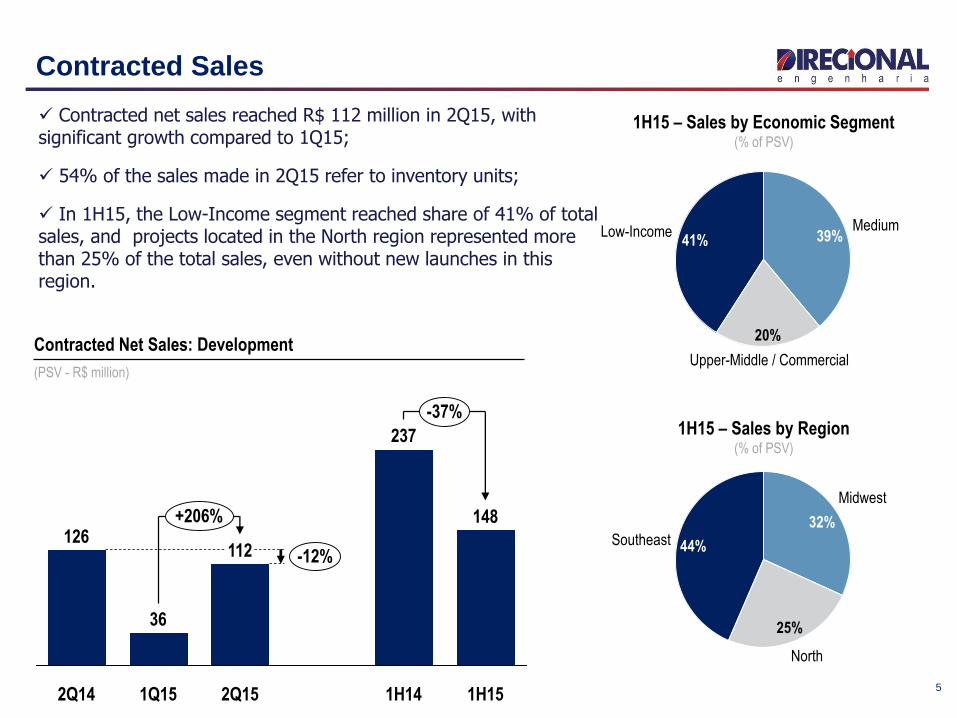

-12%

+206%

-37%

1H15

148

1H14

237

2Q15

112

1Q15

36

2Q14

126

Contracted Net Sales: Development

(PSV - R$ million)

Contracted net sales reached R$ 112 million in 2Q15, with significant growth compared to 1Q15;

54% of the sales made in 2Q15 refer to inventory units;

In 1H15, the Low-Income segment reached share of 41% of total sales, and projects located in the North region represented more than 25% of the total sales, even without new launches in this region.

Southeast 44%

North

25%

Midwest

32%

1H15 – Sales by Region(% of PSV)

41% 39%

20%

Low-Income

Upper-Middle / Commercial

Medium

1H15 – Sales by Economic Segment(% of PSV)

5

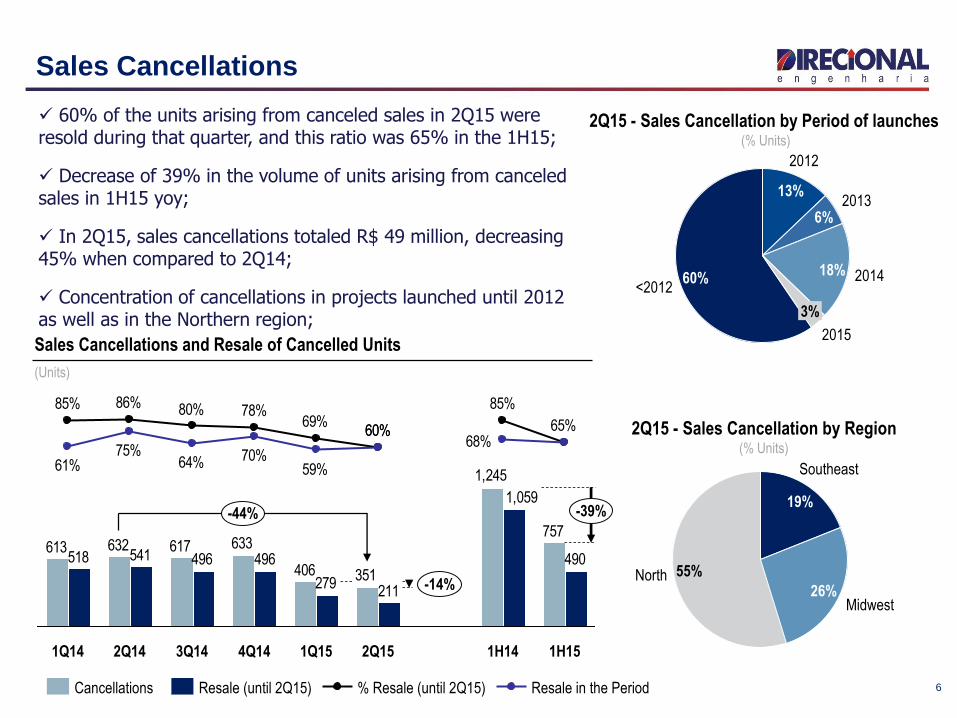

Sales Cancellations

2Q15 - Sales Cancellation by Region(% Units)

2Q15 - Sales Cancellation by Period of launches(% Units)

Sales Cancellations and Resale of Cancelled Units

(Units)

757

351406

633617632613

1,245

490

211279

496496541518

1,059

85%

60%69%

78%80%86%85%

65%68%

60%

59%70%64%

75%61%

-14%

-39%

1H151H142Q152Q141Q14

-44%

1Q154Q143Q14

Resale in the Period% Resale (until 2Q15)Resale (until 2Q15)Cancellations

2014

3%

2015

18%

20136%

2012

13%

<201260%

55%North

Southeast

26%

19%

Midwest

60% of the units arising from canceled sales in 2Q15 were resold during that quarter, and this ratio was 65% in the 1H15;

Decrease of 39% in the volume of units arising from canceled sales in 1H15 yoy;

In 2Q15, sales cancellations totaled R$ 49 million, decreasing 45% when compared to 2Q14;

Concentration of cancellations in projects launched until 2012 as well as in the Northern region;

6

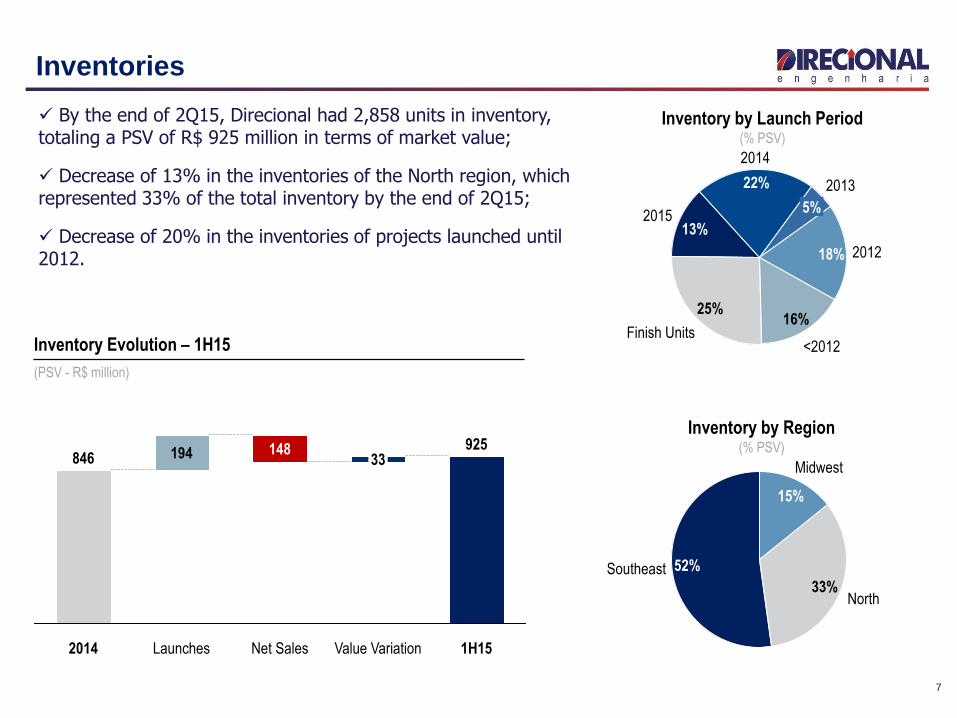

Inventories

Inventory by Region(% PSV)

Inventory Evolution – 1H15

(PSV - R$ million)

Inventory by Launch Period(% PSV)

Net Sales

148

Launches

194

2014

846

1H15

925

Value Variation

33

<2012

16%

201218%

2013

5%

2014

22%

201513%

25%

Finish Units

33%Southeast 52%

15%

North

Midwest

By the end of 2Q15, Direcional had 2,858 units in inventory, totaling a PSV of R$ 925 million in terms of market value;

Decrease of 13% in the inventories of the North region, which represented 33% of the total inventory by the end of 2Q15;

Decrease of 20% in the inventories of projects launched until 2012.

7

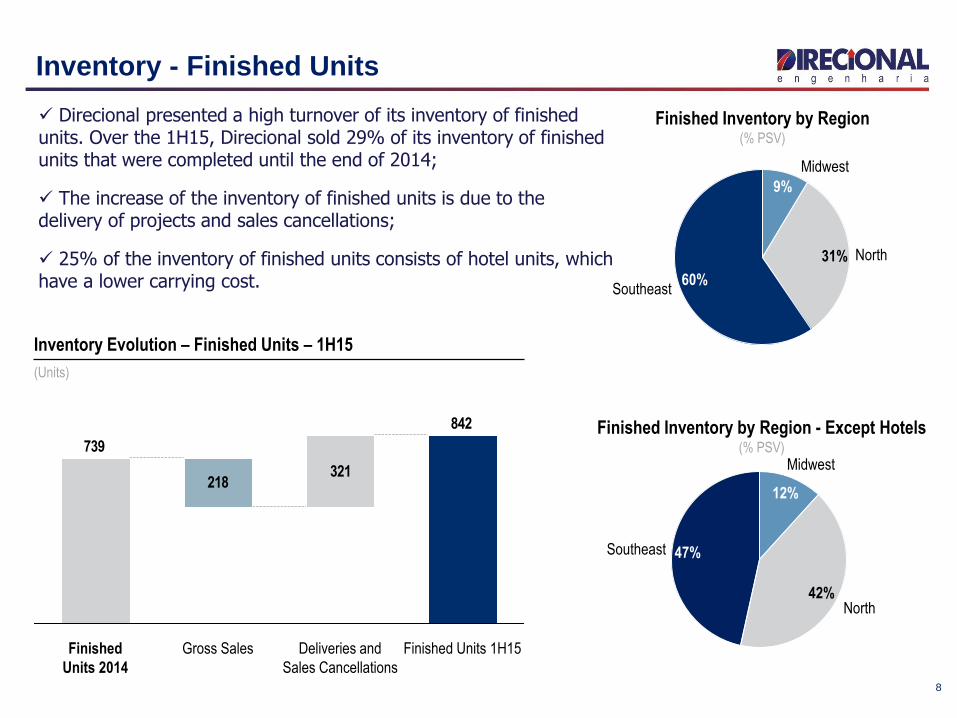

Inventory - Finished Units

Finished Inventory by Region - Except Hotels(% PSV)

Inventory Evolution – Finished Units – 1H15

(Units)

Finished Inventory by Region(% PSV)

47%

North

Midwest

Southeast

42%

12%

9%

Midwest

31%

Southeast

North

60%

Direcional presented a high turnover of its inventory of finished units. Over the 1H15, Direcional sold 29% of its inventory of finished units that were completed until the end of 2014;

The increase of the inventory of finished units is due to the delivery of projects and sales cancellations;

25% of the inventory of finished units consists of hotel units, which have a lower carrying cost.

8

321218

842

739

Finished

Units 2014

Deliveries and

Sales Cancellations

Gross Sales Finished Units 1H15

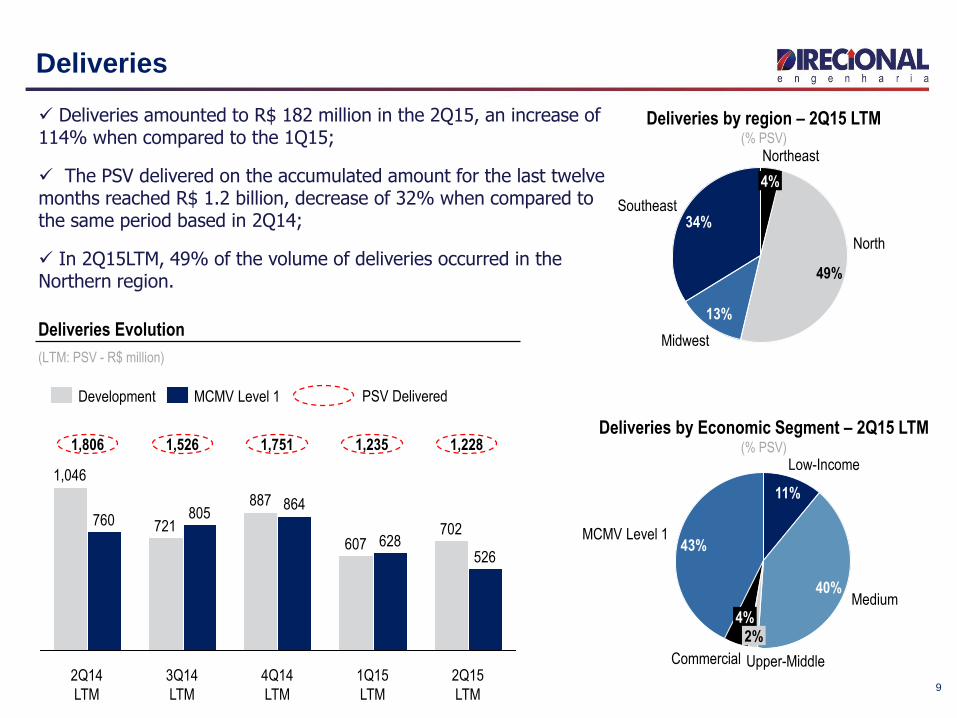

Deliveries

Deliveries Evolution

(LTM: PSV - R$ million)

Deliveries by Economic Segment – 2Q15 LTM(% PSV)

Deliveries by region – 2Q15 LTM(% PSV)

13%

Midwest

34%

49%

North

Southeast

4%

Northeast

4%

Upper-Middle

2%

Medium40%

Low-Income

11%

MCMV Level 1

Commercial

43%

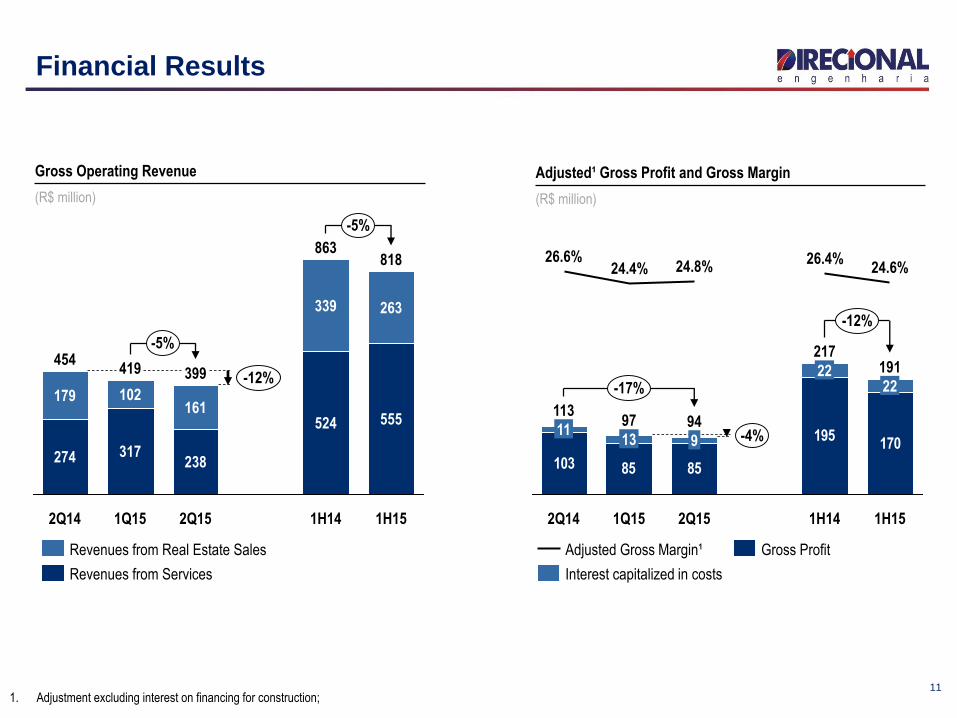

Deliveries amounted to R$ 182 million in the 2Q15, an increase of 114% when compared to the 1Q15;

The PSV delivered on the accumulated amount for the last twelve months reached R$ 1.2 billion, decrease of 32% when compared to the same period based in 2Q14;

In 2Q15LTM, 49% of the volume of deliveries occurred in the Northern region.

864

607 628702

526

3Q14

LTM

4Q14

LTM

1Q15

LTM

2Q15

LTM

1,046

760 721805

887

2Q14

LTM

Development MCMV Level 1

1,806

PSV Delivered

1,526 1,751 1,235 1,228

9

Fernando Ramos

CFO and IR Officer

Financial Highlights

10

Financial Results

1. Adjustment excluding interest on financing for construction;

Gross Operating Revenue

(R$ million)

Adjusted¹ Gross Profit and Gross Margin

(R$ million)

317

2Q14

102

419

1Q15

818

238

555

399

2Q15

339

524

863

1H14

263

-5%

-5%

-12%

1H15

274

179

454

161

Revenues from Real Estate Sales

Revenues from Services

103 85 85

195170

113

2Q14

11

26.6%

-12%

-4%

22

217

24.6%

1H14

191

1H15

-17%

26.4%

94

9

2Q151Q15

24.8%

97

13

24.4%

22

Adjusted Gross Margin¹

Interest capitalized in costs

Gross Profit

11

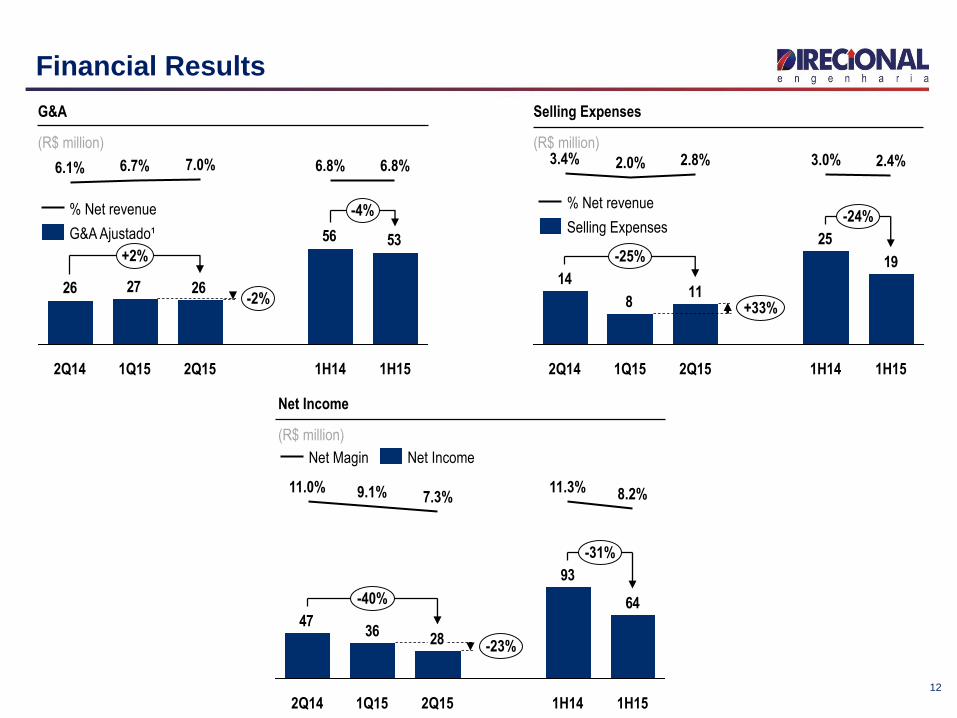

G&A

(R$ million)

Selling Expenses

(R$ million)

Net Income

(R$ million)

Financial Results

5356

262726

1Q15

6.7%

2Q14

6.1%

-4%

-2%

+2%

1H15

6.8%

1H14

6.8%

2Q15

7.0%

G&A Ajustado¹

% Net revenue

64

93

2836

47

-31%

-23%

-40%

1H15

8.2%

1H14

11.3%

2Q15

7.3%

1Q15

9.1%

2Q14

11.0%

Net IncomeNet Magin

19

25

118

14

3.0%

2Q15 1H14

2.4%

1H15

-25%

+33%

-24%

2.8%

1Q15

2.0%

2Q14

3.4%

% Net revenue

Selling Expenses

12

Cash Flow Generation

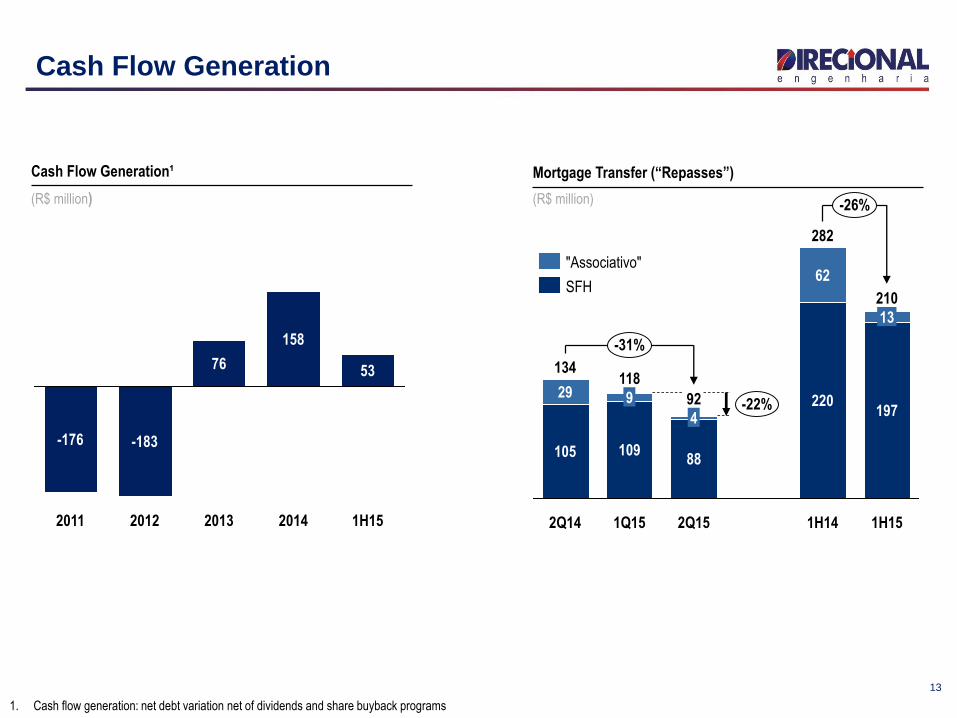

Cash Flow Generation¹

(R$ million)

1. Cash flow generation: net debt variation net of dividends and share buyback programs

Mortgage Transfer (“Repasses”)

(R$ million)

2011

-176

53

2014

158

2013

76

2012

-183

1H15

9

2Q14

220

1H14

13

62

2Q15

92

88

4

1Q15

118

109

29

134

105

282

-22%

1H15

-26%

-31%

210

197

"Associativo"

SFH

13

Capital Structure

Capital Structure

(R$ million)

313

18.5% 13.0% 16.6%

230 292

855

2Q15

685563

915

1Q152Q14

643

956

Debt

Cash

Gross Debt Breakdown(% of Debt)

292

-265

Debt Net Debt

Without SFH

Net DebtCash and

Cash

Equivalent

563

SFH

557

299

855

Debt

(R$ million)

9.5%CRI

SFH65.1%

0.4%

20.5%

Working Capital

Debentures

4.5% FINAME and Leasing

14

563

26

Cash

1Q15

Buyback Corporate

debt

685

Cash

2Q15

SFH Debt Cash Burn

10

27

62

Dividends

3

Cash Position Changes - 2Q15

(R$ million)

Net Debt

Net Debt/Equity

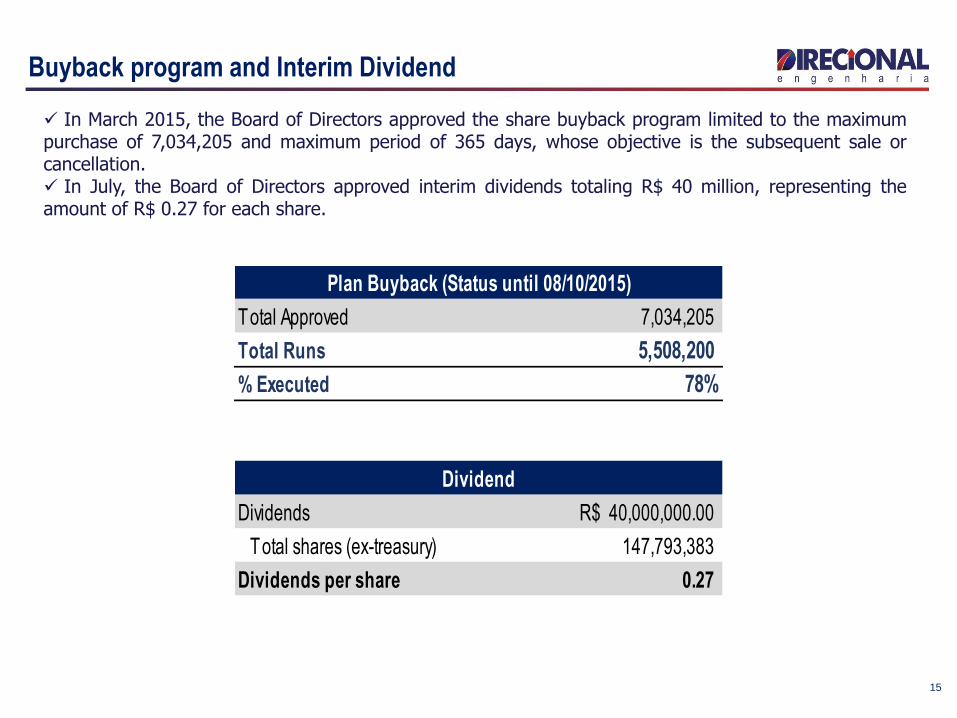

Buyback program and Interim Dividend

In March 2015, the Board of Directors approved the share buyback program limited to the maximumpurchase of 7,034,205 and maximum period of 365 days, whose objective is the subsequent sale orcancellation. In July, the Board of Directors approved interim dividends totaling R$ 40 million, representing theamount of R$ 0.27 for each share.

15

Total Approved 7,034,205

Total Runs 5,508,200

% Executed 78%

Dividends 40,000,000.00R$

Total shares (ex-treasury) 147,793,383

Dividends per share 0.27

Plan Buyback (Status until 08/10/2015)

Dividend

Disclosure and Contacts

This presentation contains certain forward-looking statements concerning the business prospects, projections of

operating and financial results and growth potential of the Company, which are based on management’s current

expectations and estimates of the future performance of the Company. Although the Company believes such

forward-looking statements are based on reasonable assumptions, it can give no assurance that its expectations

will be achieved. Expectations and estimates that are based on the future prospects of the Company are highly

dependent upon market behavior, Brazil’s political and economic situation, existing and future regulations of the

industry and international markets and, therefore, are subject to changes outside the Company’s and

management’s control. The Company undertakes no obligation to update any information contained herein or to

revise any forward-looking statement as a result of new information, future events or other information.

www.direcional.com.b/ir

(55 31) 3431-5509

(55 31) 3431-5510

(55 31) 3431-5511

Fernando José Mancio Ramos

CFO | IR Officer

IR Office

16