2r5 j!': 10 f;° 3 i 6 loi`~ t 'te - scac | securities...

TRANSCRIPT

S!„ at rI i LF L A

2r5 J!' : 10 F ;° 3 I 6

LOi`~ t 'T E

UNITED STATES DISTRICT COURTEASTERN DISTRICT OF LOUISIAN A

ROBERT THOMAS, Individually and On Behalf ofAll Others Similarly Situated,

Plaintiff,

vs .

OCA INC. (F/K/A ORTHODONTIC CENTERS OFAMERICA, INC .), BARTHOLOMEW F .PALMISANO, SR ., BARTHOLOMEW F .PALMISANO, JR., and DAVID E. VERRET ,

Defendants .

CIVIL ACTIQ P"

05 _ 222 pCLASS ACTION COMPLAINT

IMAG*5JURY TRIAL DE NbE

Plaintiff, Robert Thomas ("Plaintiff'), individually and on behalf of all other person s

similarly situated, by his undersigned attorneys, for his complaint against defendants, alleges the

following based upon personal knowledge as to himself and his own acts, and information and belie f

as to all other matters, based upon, inter alia, the investigation conducted by and through his

attorneys, which included, among other things, a review of the defendants' public documents ,

conference calls and announcements made by defendants, United States Securities and Exchang e

Commission ("SEC") filings, wire and press releases published by and regarding OCA, Inc . (F/K/A

Orthodontic Centers of America, Inc .)("OCA" or the "Company") securities analysts' reports an d

1250I .._.

advisories about the Company, and information readily obtainable on the Internet . Plaintiff believes

that substantial evidentiary support will exist for the allegations set forth herein after a reasonabl e

opportunity for discovery .

NATURE OF THE ACTION

1 . This is a federal class action on behalf of purchasers of the publicly traded securitie s

of OCA between May 18, 2004 and June 6, 2005, (the "Class Period"), seeking to pursue remedie s

under the Securities Exchange Act of 1934 (the "Exchange Act") .

2. OCA provides business services to orthodontic and pediat ric dental practices in the

United States . The complaint alleges that defendants' Class Period representations regarding OC A

were materially false and misleading when made for the following reasons : (1) that the Compan y

materially overstated patient receivables reported during 2004 ; (2) that the Company improperl y

recorded journal ent ries in the Company's ledger; (3) that the Company lacked adequate interna l

controls ; (4) that the Company's financial results were in violation of Generally Accepte d

Accounting Principles ("GAAP") ; and (5 ) as a result of the foregoing, the Company ' s financia l

results were materially inflated at all relevant times .

3 . On June 7, 2005, prior to the opening of the market, OCA announced that it had

identified certain errors in its calculation of patient receivables reported during 2004, and ha d

determined that the amount of patient receivables reported at each of March 31, June 30 an d

September 30, 2004 was overstated by material amounts . News of this shocked the market . Shares

of OCA fell $1 .55 per share or 38 .4 percent, on June 7, 2005, closing at $2 .48 per share .

-2-

JURISDICTION AND VENUE

4. The claims asserted herein arise under and pursuant to Sections 10(b) and 20(a) o f

the Exchange Act, (15 U .S .C. §§ 78j(b) and 78t (a)), and Rule 10b-5 promulgated thereunder (1 7

C.F.R. § 240. 10b-5) .

5 . This Court has ju ri sdiction over the subject matter of this action pursuant to § 27 of

the Exchange Act (15 U .S .C. § 78aa) and 28 U .S .C . § 1331 .

6 . Venue is proper in this Judicial District pursuant to § 27 of the Exchange Act, 1 5

U.S .C. § 78aa and 28 U.S .C. § 1391(b) . Many of the acts and transactions alleged herein, including

the preparation and dissemination of materially false and misleading information, occurred i n

substantial part in this Judicial District . Additionally, the Company maintains a principal executiv e

office in this Judicial District .

7 . In connection with the acts, conduct and other wrongs alleged in this complaint ,

defendants, directly or indirectly, used the means and instrumentalities of interstate commerce,

including but not limited to, the United States mails, interstate telephone communications and th e

facilities of the national securities exchange .

PARTIES

8 . Plaintiff, Robert Thomas, as set forth in the accompanying certification, incorporate d

by reference herein, purchased OCA securities at artificially inflated prices during the Class Perio d

and has been damaged thereby .

9 . Defendant OCA is aDelaware corporation with its principal place of business locate d

at 3850 N. Causeway Boulevard, Suite 800, Metairie, Louisiana 70002 .

-3-

10 . Defendant Bartholomew F. Palmisano, Sr. ("Palmisano Sr.") was, at all relevant

times , the Company's Chairman, President and Chief Executive Officer .

11 . Defendant Bartholomew F. Palmisano, Jr . ("Palmisano Jr.") was, at all relevant times ,

the Company's Chief Operating Officer .

12 . Defendant David E. Verret ("Verret") was, at all relevant times , the Company's Chie f

Financial Officer and Senior Vice President of Finance .

13 . Defendants Palmisano Sr ., Palmisano Jr. and Verret are collectively referred to

hereinafter as the "Individual Defendants ." The Individual Defendants, because of their position s

with the Company , possessed the power and authority to control the contents of OCA's quarterly

reports, press releases and presentations to securities analysts, money and portfolio managers an d

institutional investors, i .e ., the market . Each defendant was provided with copies of the Company' s

reports and press releases alleged herein to be misleading prior to or shortly after their issuance an d

had the ability and opportunity to prevent their issuance or cause them to be corrected . Because of

their positions and access to material non-public information available to them but not to the public ,

each of these defendants knew that the adverse facts specified herein had not been disclosed to an d

were being concealed from the public and that the positive representations which were being mad e

were then materially false and misleading . The Individual Defendants are liable for the fals e

statements pleaded herein, as those statements were each "group-published" information, the resul t

of the collective actions of the Individual Defendants .

PLAINTIFF'S CLASS ACTION ALLEGATION S

14. Plaintiff brings this action as a class action pursuant to Federal Rule of Civi l

Procedure 23(a) and (b)(3) on behalf of a Class, consisting of all those who purchased the securitie s

-4-

of OCA between May 18, 2004 and June 6, 2005, inclusive (the "Class Period") and who wer e

damaged thereby. Excluded from the Class are defendants, the officers and directors of the

Company, at all relevant times, members of their immediate families and their legal representatives ,

heirs, successors or assigns and any entity in which defendants have or had a controlling interest .

15. The members of the Class are so numerous that joinder of all members is imprac-

ticable . Throughout the Class Period, OCA's securities were actively traded on the New York Stoc k

Exchange . While the exact number of Class members is unknown to Plaintiff at this time and ca n

only be ascertained through appropriate discovery, Plaintiff believes that there are hundreds o r

thousands of members in the proposed Class . Record owners and other members of the Class ma y

be identified from records maintained by OCA or its transfer agent and may be notified of the

pendency of this action by mail, using the form of notice similar to that customarily used in securitie s

class actions .

16 . Plaintiff's claims are typical of the claims of the members of the Class as all member s

of the Class are similarly affected by defendants' wrongful conduct in violation of federal law tha t

is complained of herein .

17 . Plaintiff will fairly and adequately protect the interests of the members of the Clas s

and has retained counsel competent and experienced in class and securities litigation .

18 . Common questions of law and fact exist as to all members of the Class an d

predominate over any questions solely affecting individual members of the Class . Among the

questions of law and fact common to the Class are :

(a) whether the federal securities laws were violated by defendants' acts as alleged

herein ;

-5-

(b) whether statements made by defendants to the investing public during the Clas s

Pe riod misrepresented material facts about the business , operations and management of OCA ; and

(c) to what extent the members of the Class have sustained damages and the proper

measure of damages .

19 . A class action is superior to all other available methods for the fair and efficien t

adjudication of this controversy since joinder of all members is impracticable . Furthermore, as th e

damages suffered by individual Class members may be relatively small, the expense and burden o f

individual litigation make it impossible for members of the Class to individually redress the wrong s

done to them . There will be no difficulty in the management of this action as a class action .

SUBSTANTIVE ALLEGATIONS

Background

20. OCA provides business services to orthodontic and pediatric dental practices in th e

United States . The Company provides affiliated practices with a range of operational, purchasing ,

financial , marketing , administrative , and other business services , as well as capital and proprietary

information systems . It generally provides its services to affiliated practices under long-ter m

service , consulting , or management service agreements , with terms that typically range from 20 years

to 25 years. In addition, the Company offers training, office leasing and construction, an d

information technology support services . As of December 31, 2004, the Company ha d

approximately 565 affiliated centers in the United States and internationally . The Company' s

customer base comprises orthodontic and pediatric dental practices operating in 46 states and in

international locations .Materially False And Misleading

Statements Issued During The Class Period

-6-

21 . The Class Period commences on May 18, 2004 . At that time, OCA announced that

it had adopted Financial Accounting Standards Board ("FASB") Interpretation No. 46R ,

"Consolidation of Variable Interest Entities - an Interpretation of ARB No. 51" ("FIN 46R"), whic h

required the consolidation of financial results of va riable interest entities ("VIEs") in certain

circumstances if a company had an ownership, contractual or other financial interests in the VIEs .

Additionally, the Company also announced its preliminary financial results for the first quarter o f

2004, the period ending March 31, 2004 . In the press release, the Company, in relevant part, stated :

"We are now making the necessary changes to our financialreporting," said Bart F . Palmisano, Sr ., President, Chairman andChief Executive Officer. "We believe the changes in our accountingand financial reporting under FIN 46R simplify our accounting andmake it more transparent for our shareholders and other stakeholdersto measure our progress . Although this changes the way we recognizeour revenue, it does not affect our cash flows, which continue to behealthy. This is a watershed event for OCA because it permits us toreport our results on a basis that is more consistent with the way wemanage the business and our relationships with our affiliatedpractices . "

As a result of the Company's adoption of FIN 46R, the Company wasrequired to make a number of changes in its accounting and financialstatement presentation effective as of January 1, 2004, including thefollowing :

-- Patient revenue. The Company will now record patient revenueunder patient contracts between affiliated practices and theirpatients, rather than the fee revenue portion that represented theCompany's service fees . The Company will now recognize patientrevenue on a straight -line basis over the term of treatment(which averages about 25 months), except that a portion ofpatient contracts relating to retainers will be recognized in thefinal month of treatment when braces are removed and retainersare provided to patients . This eliminates the recognition ofrevenue related to the retainers over the term of treatment, whichresulted in increasing unbilled service fees receivable under theCompany's prior revenue recognition policy .

-7-

-- Amounts retained by affiliated practices . The portion of patientrevenue that is retained by affiliated practices will now be reflectedas an expense in the Company's condensed consolidated statementsof income .

-- Patient receivables . The Company will now record patientreceivables owed to affiliated practices under their patientcontracts. It will no longer record service fees receivable,including service fees receivable relating to the final retainerpayment. This change will cause patient receivables to moreclosely match the actual timing of billing and collection forretainers, which is typically in the final month of treatment. TheCompany will also no longer record the financed practice-relatedexpense portion of service fees receivable . Practice-relatedexpenses will be expensed on the Company's condensedconsolidated income statement, and to the extent that an affiliatedpractice repays its portion of these amounts, it will result in adecrease in amounts retained by affiliated practices.

In conjunction with the Company's normal quarterly review process,the Company and its independent auditors continue to analyze theimpact of adopting FIN 46R on the Company's financial results .Based on its preliminary analysis, the Company currently estimatesthat, after applying its adoption of FIN 46R, for the first quarter of2004, estimated patient revenue was $110 .9 million, generatingestimated after-tax income of approximately $7 .2 million, or $0 .14per diluted share, before a cumulative effect of accounting change,which the Company currently estimates to be $72 .3 million, net ofincome tax benefit . On a pro forma basis as if the Company'sadoption of FIN 46R and change in revenue recognition wereeffective as of January 1, 2003, the Company currently estimates thatfor the first quarter of 2003 pro forma patient revenue was $112 .9million, generating estimated after-tax income of $6 .7 million, or$0.13 per diluted share . These pro forma results reflect an estimated12% increase in patient revenue from the Company's base affiliatedpractices and a corresponding decrease in patient revenue fromnon-performing practices that are engaged in litigation with theCompany and/or ceased to pay service fees .(Emphasis added.)

-8-

22 . On May 20, 2004, OCA issued a press release entitled "OCA Files Form 10-Q an d

Announces Financial Results For the First Quarter of 2004 ." Therein, the Company , in relevant part ,

stated :

As previously announced, the Company has adopted FinancialAccounting Standards Board Interpretation No . 46R, "Consolidationof Variable Interest Entities - an Interpretation of ARB No . 51" ("FIN46R"). The financial information included in this release for the firstquarter of 2004 reflects the Company's adoption of F IN 46R, andincludes the Company's Condensed Consolidated Statements ofIncome, Condensed Consolidated Balance Sheets and CondensedConsolidated Statements of Cash Flows .

Bart F. Palmisano, Sr ., the Company's Chief Executive Officer,

commented, "We continue to make progress on a number of fronts

that are important to the long range future of the Company, includingimproved transparency of our accounting . We have a core group of

practices with highly motivated doctors who value their relationshipwith us . This successful base business gives us the means and the

opportunity to transform OCA into an international business services

company. Through OCA OutSource, we are already well on our way

to providing business services to general dentists with physicians to

follow later in the year. Driving this effort is OCA's unique

experience and the valuable franchise we created over the past ten

years by developing a comprehensive suite of services that can now

be offered to the full spectrum of medical professionals . We are very

excited about the world of opportunity we have before us . "

As previously announced, the Company has made a number ofchanges in its accounting and financial statement presentationeffective as of January 1, 2004, in connection with its adoption of F IN46R. These include :

- CONSOLIDATION. The Company now consolidates the assets,liabilities , equity and financial results of its affiliated practices, otherthan non -performing practices that are engaged in litigation with theCompany and /or have ceased paying service fees .

-9-

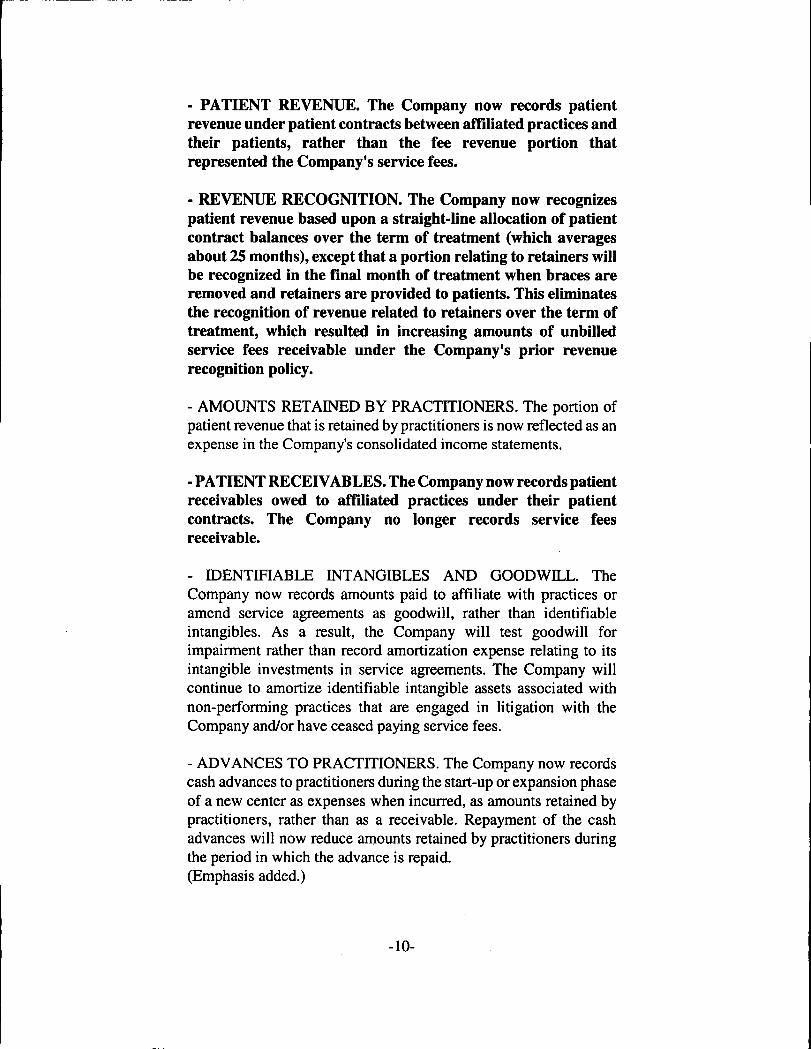

- PATIENT REVENUE . The Company now records patientrevenue under patient contracts between affiliated practices andtheir patients , rather than the fee revenue portion thatrepresented the Company's service fees .

- REVENUE RECOGNITION. The Company now recognizespatient revenue based upon a straight- line allocation of patientcontract balances over the term of treatment (which averagesabout 25 months ), except that a portion relating to retainers willbe recognized in the final month of treatment when braces areremoved and retainers are provided to patients . This eliminatesthe recognition of revenue related to retainers over the term oftreatment, which resulted in increasing amounts of unbilledservice fees receivable under the Company's prior revenuerecognition policy.

- AMOUNTS RETAINED BY PRACTITIONERS. The portion ofpatient revenue that is retained by practitioners is now reflected as anexpense in the Company's consolidated income statements .

- PATIENT RECEIVABLES . The Company now records patientreceivables owed to affiliated practices under their patientcontracts . The Company no longer records service feesreceivable .

- IDENTIFIABLE INTANGIBLES AND GOODWILL . TheCompany now records amounts paid to affiliate with practices oramend serv ice agreements as goodwill , rather than identifiableintangibles . As a result, the Company will test goodwill forimpairment rather than record amortization expense relating to itsintangible investments in service agreements . The Company willcontinue to amort ize identifiable intangible assets associated withnon-performing practices that are engaged in litigation with theCompany and /or have ceased paying service fees .

- ADVANCES TO PRACTITIONERS . The Company now recordscash advances to practitioners du ring the start-up or expansion phaseof a new center as expenses when incurred , as amounts retained bypractitioners, rather than as a receivable . Repayment of the c ashadvances will now reduce amounts retained by practitioners du ringthe period in which the advance is repaid .(Emphasis added .)

-10-

23 . Additionally, on May 20, 2004, the Company filed its quarterly report with the SE C

on Form 10-Q. The Company's Form 10-Q was signed by the Palmisano Sr . and Verret and

reaffirmed its previously announced financial results . With respect to its financial results, the

Company represented :

In the opinion of management, all normal and recurring adjustments,except for the adjustments resulting from the adoption of F IN 46 asdefined below, considered necessary for a fair presentation have beenincluded .

24 . On August 10, 2004, OCA issued a press release entitled "OCA Reports Secon d

Quarter 2004 Results . " The Company reported revenues of $104 .3 million and net income of $2 . 3

million or $0.05 diluted net income per share . Commenting on these results, defendant Palmisano

Sr. stated :

We are pleased with our results for the second quarter and first halfof 2004. Our base business continued to improve, as comparablepractice patient revenue increased in both the second quarter and thefirst six months of 2004 compared to the same periods of 2003 on apro forma basis . We intend to build on this success by continuing ourstrategy of growing our base business and expanding ouropportunities with OCA OutSource. We are optimistic about ourprospects for the future .

25. On August 9, 2004, the Company filed its quarterly report with the SEC on For m

10-Q. The Company's Form 10-Q was signed by the Palmisano Sr. and Verret and reported th e

aforementioned financial results . With respect to its financial results, the Company represented :

In the opinion of management, all normal and recurring adjustments,except for the adjustments resulting from the adoption of FIN 46R (asdefined below), considered necessary for a fair presentation have beenincluded.

-11-

26. On November 15, 2004, OCA issued a press release entitled "OCA Provides

Preliminary Financial Information for Third Quarter of 2004 ." Therein, the Company, in relevan t

part, stated :

For the quarter ended September 30, 2004 , the Company currentlyanticipates that :

-- Patient revenue was $104 .0 million, reflecting strong demand fororthodontic services from the Company's affiliated practices despiteweather-related disruptions in Gulf-coast areas in which the Companyhas a number of affiliated practices .

-- Comparable patient revenue for practices for which the Companyrecorded revenue throughout the third quarter of 2004 and 2003increased 2 .6% compared to the same period of 2003 on a pro formabasis as if the Company's change in accounting principle under F IN46R was effective as of January 1, 2003 ("Pro Forma Basis") .

-- Earnings per share, excluding provision for assets associated withinactive practices, loss on sale of assets, asset impairments and othernon-recurring and extraordinary charges and write-offs, is expectedto range from $0 .10 to $0.13 per share .

For the nine months ended September 30, 2004, the Companycurrently anticipates that :-- Patient revenue was $319 .2 million .

-- Comparable patient revenue for practices for which the Companyrecorded revenue throughout the nine months ended September 30,2004 and 2003 increased 7 .8% compared to the same period of 2003on a Pro Forma Basis .

-- Earnings per share, excluding the cumulative effect of a change inaccounting principle, provision for assets associated with inactivepractices, loss on sale of assets, asset impairments and othernon-recurring and extraordinary charges and write-offs, is expectedto range from $0 .31 to $0.34 per share .

-12-

27. On December 23, 2004, OCA announced its financial results for the third quarter of

2004 . The Company reported revenues of $104 .0 million and adjusted net income, excludin g

charges, of $6 .1 million, or $0 .12 per diluted share . The press release, in relevant part, stated :

For the three months ended September 30, 2004 :

-- Patient revenue was $104 .0 million, reflecting strong demand fororthodontic services from the Company's affiliated practices despiteweather-related disruptions in Florida and other Gulf-coast areas inwhich the Company has a number of affiliated practices .

-- The Company recorded a $13 .5 million non-cash charge toincrease the allowance for assets associated with inactive practicesand a $1 .7 million loss on sale of assets in connection with practices'buyouts of their service agreements, resulting in a net loss of $3 .5million, or $0.07 net loss per diluted share . This compares with netincome for the third quarter of 2003 of $4 .3 million, or $0 .09 perdiluted share, on a pro forma basis as if the Company's change inaccounting principle under F IN 46R was effective as of January 1,2003 ("Pro Forma Basis"), and $11 .9 million, or $0.24 per dilutedshare, on an actual basis .

-- Adjusted net income, excluding those charges, was $6 .1 million,or $0 .12 per diluted share . For the third quarter of 2003, adjusted netincome was $4 .8 million, or $0.09 per diluted share, on a Pro FormaBasis, and $12.4 million, or $0.25 per diluted share, on an actualbasis .

-- The $13.5 million non-cash provision for assets associated withinactive practices reflects management's assessment of thecollectibility of those assets, in light of certain recent settlementpayments to OCA and a recent court award to OCA that weresignificantly less than the net book value of the goodwill,identifiable intangibles and other assets associated with the relatedinactive practices. It also reflects renewed efforts by the Company totry to settle pending litigation on mutually agreeable terms .

-- The Company's results were also affected by increased startuplosses associated with the Company's strategy of continuedinvestment in de novo centers, which typically incur operating lossesduring the centers' first 12 to 18 months of operation as they build a

-13-

patient base . During the third quarter of 2004, de novo centers thathad been operating for 18 months or less and had not begun togenerate operating profits on a cash basis ("De Novo Centers")generated $1 .1 million of operating losses, an increase of 164 .1%compared to the third quarter of 2003 .

28 . Additionally, Defendant Palmisano Sr ., commenting on the results, stated :

We are pleased with our operational results for the third quarter of2004, which reflected strong contribution by our base affiliatedpractices. Excluding a noncash provision and loss on sale, ouroperations produced increased earnings over the third quarter of 2003on a pro forma basis . Although the past three years presented somesignificant challenges, as we worked to integrate OrthAlliance'saffiliated practices into our system and address related litigation, Ibelieve that we are well positioned to capitalize on our strengths andgrow our business .

29. On December 23, 2004, the Company filed its quarterly report with the SEC on Form

10-Q. The Company's Form 10-Q was signed by Palmisano Sr . and Verret and reported th e

aforementioned financial results . With respect to its financial results, the Company represented :

In the opinion of management, all normal and recurring adjustments,except for the adjustments resulting from the adoption of FIN 46R (asdefined below), considered necessary for a fair presentation have beenincluded .

30. The statements contained in 19[21-29 were materially false and misleading when

made because defendants failed to disclose or indicate the following : (1) that the Company

materially overstated patient receivables reported during 2004 ; (2) that the Company improperly

recorded journal entries in the Company's ledger ; (3) that the Company lacked adequate internal

controls ; (4) that the Company's financial results were in violation of Generally Accepte d

Accounting Principles ; and (5) as a result of the foregoing, the Company's financial results wer e

materially inflated at all relevant times .

-14-

The Truth Begins to Emerge

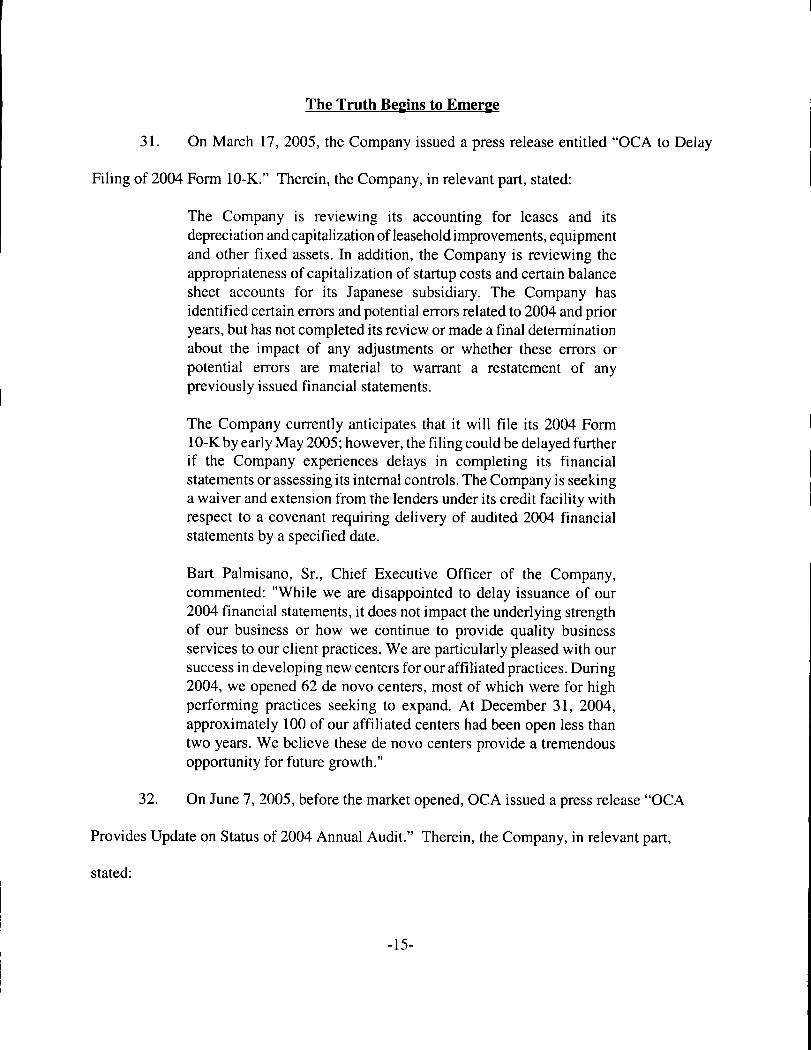

31 . On March 17, 2005, the Company issued a press release entitled "OCA to Dela y

Filing of 2004 Form 10-K ." Therein, the Company, in relevant part, stated :

The Company is reviewing its accounting for leases and itsdepreciation and capitalization of leasehold improvements, equipmentand other fixed assets . In addition, the Company is reviewing theappropriateness of capitalization of startup costs and certain balancesheet accounts for its Japanese subsidiary . The Company hasidentified certain errors and potential errors related to 2004 and prioryears, but has not completed its review or made a final determinationabout the impact of any adjustments or whether these errors orpotential errors are material to warrant a restatement of anypreviously issued financial statements .

The Company currently anticipates that it will file its 2004 Form10-K by early May 2005 ; however, the filing could be delayed furtherif the Company experiences delays in completing its financialstatements or assessing its internal controls . The Company is seekinga waiver and extension from the lenders under its credit facility withrespect to a covenant requiring delivery of audited 2004 financialstatements by a specified date .

Bart Palmisano, Sr ., Chief Executive Officer of the Company,commented: "While we are disappointed to delay issuance of our2004 financial statements, it does not impact the underlying strengthof our business or how we continue to provide quality businessservices to our client practices . We are particularly pleased with oursuccess in developing new centers for our affiliated practices . During2004, we opened 62 de novo centers, most of which were for highperforming practices seeking to expand . At December 31, 2004,approximately 100 of our affiliated centers had been open less thantwo years . We believe these de novo centers provide a tremendousopportunity for future growth . "

32 . On June 7, 2005, before the market opened, OCA issued a press release "OC A

Provides Update on Status of 2004 Annual Audit." Therein, the Company, in relevant part ,

stated :

-15-

OCA, Inc. (NYSE :OCA) today announced that its bank lenders haveagreed to extend until June 30, 2005 the deadlines under OCA'ssenior credit facility for filing its 2004 Form 10-K and Form 10-Q forthe first quarter of 2005. The Company anticipates further delay incompleting its 2004 financial close process and audit and in filing theForm 10-K and Form 10-Q, and is currently in discussions with itslenders about obtaining an additional extension and waiver. OCA hasengaged Alvarez & Marsal, LLC, a leading corporate advisory firm,to facilitate discussions with the Company's lenders and to assist withfinance, audit and other management functions .

The extension under the credit facility limits the amount that theCompany may borrow under its revolving line of credit until it filesthe Form 10-K and Form 10-Q. To provide the Company withadditional capital and liquidity, OCA's Chief Executive Officer, BartF. Palmisano, Sr., has committed to extend a $2 .0 million unsecuredloan to the Company. Mr. Palmisano also has terminated theCompany's lease of an aircraft owned by an affiliate of Mr .Palmisano, saving the Company an estimated $1 .1 million of leaseand operating costs annually. The Company is also temporarilycurtailing the capital-intensive development of de novo centers,which typically require expenditures of about $350,000 to $380,000to develop in the United States . The Company developed 55 de novooffices in 2004 and 15 de novo offices during the first quarter of2005, and had 13 de novo offices in development at March 31, 2005 .

Bart F . Palmisano , Sr., OCA 's Chief Executive Officer , President andChairman , commented, "Our core business remains strong and we arefully committed to ensuring that our affiliated practices have theservices and support they need to continue providing high quality careto their patients . I am confident that the decisive actions being takenby OCA 's Board and management will strengthen the Company andimprove its financial flexibility . "

The Company also announced that it has identified certain errorsin its calculation of patient receivables reported during 2004, andhas determined that the amount of patient receivables reportedat each of March 31, June 30 and September 30, 2004 wasoverstated by material amounts. The Company continues toreview these receivables and their impact on patient revenue, andhas not yet determined the amount by which they wereoverstated . The Company's Audit Committee has concluded that,due to these overstatements , these previously issued quarterl y

-16-

financial statements will need to be restated and should no longerbe relied upon . The Company is also reviewing a number of otheraccounting matters and accounts, and has identified a number ofpotential prior period financial statement account errors . Thesematters do not impact the amounts reported to affiliatedpractices because these are determined on a cash basis. TheCompany is working with its current and former independentregistered accounting firms to refine its estimates of potentialadjustments.

The Company also announced that its Board of Directors hasappointed a Special Committee to review certain journal entriesrecorded in the Company's general ledger, the circumstances inwhich they originated and their impact on the Company'sfinancial statements. In addition, the Special Committee isreviewing certain alleged changes in data provided to theCompany's independent registered public accounting firm . TheSpecial Committee, comprised of independent directors AshtonJ. Ryan, Jr. and Kevin M. Dolan, is engaging special counsel toadvise it in connection with the review . Pending completion of theinternal review, the Company has placed Bartholomew F .Palmisano, Jr ., the Company's Chief Operating Officer, onadministrative leave .

Ashton J. Ryan, Jr., Chairman of the Board's Special Committee,said, "We are assembling an experienced team of lawyers andaccountants to assist the Special Committee with its review . We willgather the facts as promptly as we can and take whatever action isappropriate . "

Bart F. Palmisano, Sr., commented further, "I pledge my personalcooperation, along with that of the entire management team, as theSpecial Committee conducts its review . "

The Company also announced that it has entered into an agreementto settle lawsuits and disputes pending between its subsidiary,OrthAlliance, Inc ., and 60 affiliated practitioners who represent 54affiliated practices . Under the terms of the settlement agreement, thepractices bought out of their service agreements with OrthAllianceand all parties agreed to dismiss their claims . The Companyanticipates that this settlement will result in a non-cash loss-on-saleof assets estimated at $6 .1 million, net of income tax benefit, durin g

-17-

the fourth quarter of 2004, in connection with the write-off ofintangibles, goodwill and other assets associated with these practices .(Emphasis added.)

33 . News of this shocked the market . Shares of OCA fell $1 .55 per share or 38 .4 percent ,

on June 7, 2005, closing at $2 .48 per share .

OCA'S VIOLATION OF GAAP RULES IN ITSFINANCIAL REPORTS FILED WITH THE SEC

37. These financial statements and the statements about them were false and misleading ,

as such financial information was not prepared in conformity with GAAP, nor was the financia l

information a fair presentation of the Company 's operations due to the Company's improper

accounting for and disclosure about its revenues , in violation of GAAP and SEC rules .

38. GAAP are those principles recognized by the accounting profession as the

conventions, rules and procedures necessary to define accepted accounting practice at a particula r

time. Regulation S-X (17 C .F.R . § 210.4-01(a) ( 1)) states that financial statements filed with the

SEC which are not prepared in compliance with GAAP are presumed to be misleading an d

inaccurate . Regulation S-X requires that inte rim financial statements must also comply with GAAP,

with the exception that interim financial statements need not include disclosure which would be

duplicative of disclosures accompanying annual financial statements . 17 C.F.R . § 210.10-01(a) .

39 . Given these accounting irregularities, the Company announced financial result s

that were in violation of GAAP and the following p rinciples :

(a) The principle that "interim financial reporting should be based upon the sam e

accounting principles and practices used to prepare annual financial statements" was violated (AP B

No . 28,110) ;

-18-

(b) The principle that "financial reporting should provide information that is useful t o

present to potential investors and creditors and other users in making rational investment, credit, an d

similar decisions" was violated (FASB Statement of Concepts No . 1,134) ;

(c) The principle that "financial reporting should provide information about the economi c

resources of an enterprise, the claims to those resources, and effects of transactions, events, and

circumstances that change resources and claims to those resources" was violated (FASB Statement

of Concepts No. 1,140) ;

(d) The principle that "financial reporting should provide information about a n

enterprise 's financial performance du ring a pe riod" was violated (FASB Statement of Concepts No .

1,142) ;

(e) The principle that "completeness, meaning that nothing is left out of the informatio n

that may be necessary to ensure that it validly represents underlying events and conditions" was

violated (FASB Statement of Concepts No. 2,179) ;

(f) The principle that "financial reporting should be reliable in that it represents what i t

purports to represent" was violated (FASB Statement of Concepts No . 2,1158-59) ; and

(g) The principle that "conservatism be used as a prudent reaction to uncertainty to try

to ensure that uncertainties and risks inherent in business situations are adequately considered" was

violated. (FASB Statement of Concepts No . 2,195) .

40. The adverse information concealed by defendants during the Class Period and

detailed above was in violation of Item 303 of Regulation S-K under the federal securities law (1 7

C.F.R. 229.303) .

-19-

41 . Moreover, the adverse information concealed by defendants during the Class Perio d

and detailed above was in violation of SEC Regulation S-X, which states that "financial statements

filed with the SEC which are not prepared in compliance with GAAP are presumed to be misleadin g

and inaccurate." SEC Regulation S-X also required that "interim financial statements [i .e ., Form

10-Qs] must also comply with GAAP." 17 C.F.R. § 210 .10-01(a) .

UNDISCLOSED ADVERSE FACT S

34. The market for OCA' s securities was open , well-developed and efficient at al l

relevant times . As a result of these materially false and misleading statements and failures t o

disclose, OCA's securities traded at artificially inflated prices during the Class Period. Plaintiff and

other members of the Class purchased or otherwise acquired OCA securities relying upon th e

integri ty of the market price of OCA' s secu rities and market information relating to OCA, and hav e

been damaged thereby .

35 . During the Class Period, defendants materially misled the investing public, thereby

inflating the price of OCA's securities, by publicly issuing false and misleading statements an d

omitting to disclose material facts necessary to make defendants' statements, as set forth herein, no t

false and misleading. Said statements and omissions were materially false and misleading in that

they failed to disclose material adverse information and misrepresented the truth about the Company ,

its business and operations, as alleged herein .

36. At all relevant times, the mate rial misrepresentations and omissions pa rt icularized

in this Complaint directly or proximately caused or were a substantial contributing cause of th e

damages sustained by Plaintiff and other members of the Class . As described herein , during the

Class Period, defendants made or caused to be made a series of materially false or misleadin g

-20-

statements about OCA's business, prospects and operations . These material misstatements and

omissions had the cause and effect of creating in the market an unrealistically positive assessmen t

of OCA and its business, prospects and operations, thus causing the Company's securities to b e

overvalued and artificially inflated at all relevant times . Defendants' materially false and misleadin g

statements during the Class Period resulted in Plaintiff and other members of the Class purchasin g

the Company' s secu rities at artificially inflated prices , thus causing the damages complained of

herein .

LOSS CAUSATION

37. Defendants' wrongful conduct, as alleged herein, directly and proximately caused th e

economic loss suffered by Plaintiff and the Class .

38 . During the Class Pe riod , Plaintiff and the Class purchased secu ri ties of OCA at

artificially inflated prices and were damaged thereby . The price of OCA common stock decline d

when the misrepresentations made to the market, and/or the information alleged herein to have bee n

concealed from the market, and/or the effects thereof, were revealed, causing investors' losses .

ADDITIONAL SCIENTER ALLEGATION S

39 . As alleged herein, defendants acted with scienter in that defendants knew that the

public documents and statements issued or disseminated in the name of the Company were

materially false and misleading; knew that such statements or documents would be issued o r

disseminated to the investing public; and knowingly and substantially participated or acquiesced i n

the issuance or dissemination of such statements or documents as primary violations of the federal

securities laws . As set forth elsewhere herein in detail, defendants, by virtue of their receipt of

information reflecting the true facts regarding OCA, their control over, and/or receipt and/or

-21-

modification of OCA allegedly mate ri ally misleading misstatements and/or their associations wit h

the Company which made them privy to confidential proprietary information concerning OCA ,

participated in the fraudulent scheme alleged herein .

40. Defendants knew and/or recklessly disregarded the falsity and misleading nature o f

the information which they caused to be disseminated to the investing public . The ongoing

fraudulent scheme described in this complaint could not have been perpetrated over a substantia l

period of time, as has occurred, without the knowledge and complicity of the personnel at the highes t

level of the Company, including the Individual Defendants .

Applicability Of Presumption Of Reliance :Fraud-On-The-Market Doctrin e

41 . At all relevant times, the market for OCA securities was an efficient market for th e

following reasons, among others :

(a) OCA stock met the requirements for listing , and was listed and actively trade d

on the New York Stock Exchange, a highly efficient and automated market ;

(b) As a regulated issuer , OCA filed periodic public reports with the SEC and th e

New York Stock Exchange ;

(c) OCA regularly communicated with public investors via established marke t

communication mechanisms, including through regular disseminations of press releases on th e

national circuits of major newswire services and through other wide-ranging public disclosures, suc h

as communications with the financial press and other similar reporting services ; and

(d) OCA was followed by several securities analysts employed by major brokerage

firms who wrote reports which were distributed to the sales force and certain customers of thei r

-22-

respective brokerage firms . Each of these reports was publicly available and entered the publi c

marketplace .

42. As a result of the foregoing, the market for OCA securities promptly digested curren t

information regarding OCA from all publicly-available sources and reflected such information i n

OCA stock price. Under these circumstances, all purchasers of OCA securities during the Clas s

Pe riod suffered similar injury through their purchase of OCA securities at art ificially inflated p rices

and a presumption of reliance applies .

NO SAFE HARBO R

43. The statutory safe harbor provided for forward-looking statements under certai n

circumstances does not apply to any of the allegedly false statements pleaded in this complaint .

Many of the specific statements pleaded herein were not identified as "forward-looking statements "

when made . To the extent there were any forward-looking statements, there were no meaningfu l

cautionary statements identifying important factors that could cause actual results to diffe r

materially from those in the purportedly forward-looking statements . Alternatively, to the extent that

the statutory safe harbor does apply to any forward-looking statements pleaded herein, defendant s

are liable for those false forward-looking statements because at the time each of those forward-

looking statements was made, the particular speaker knew that the particular forward-lookin g

statement was false, and/or the forward-looking statement was authorized and/or approved by a n

executive officer of OCA who knew that those statements were false when made .

-23-

FIRST CLAIMViolation Of Section 10(b) Of

The Exchange Act Against And Rule 10b-5Promulgated Thereunder Against All Defendants

44. Plaintiff repeats and realleges each and every allegation contained above as if fully

set forth herein .

45 . During the Class Period, defendants carried out a plan, scheme and course of conduc t

which was intended to and, throughout the Class Period, did : (I) deceive the investing public ,

including Plaintiff and other Class members, as alleged herein ; and (ii) cause Plaintiff and othe r

members of the Class to purchase OCA securities at artificially inflated prices . In furtherance of thi s

unlawful scheme, plan and course of conduct, defendants, and each of them, took the actions se t

forth herein .

46 . Defendants (a) employed devices, schemes, and artifices to defraud; (b) made untrue

statements of material fact and/or omitted to state material facts necessary to make the statement s

not misleading; and (c) engaged in acts, practices, and a course of business which operated as a frau d

and deceit upon the purchasers of the Company 's securities in an effort to maintain artificially high

market pri ces for OCA securities in violation of Section 10(b) of the Exchange Act and Rule lOb-5 .

All defendants are sued either as primary participants in the wrongful and illegal conduct charge d

herein or as controlling persons as alleged below .

47. Defendants, individually and in concert, directly and indirectly, by the use, means or

instrumentalities of interstate commerce and/or of the mails, engaged and participated in a

continuous course of conduct to conceal adverse material information about the business, operation s

and future prospects of OCA as specified herein .

-24-

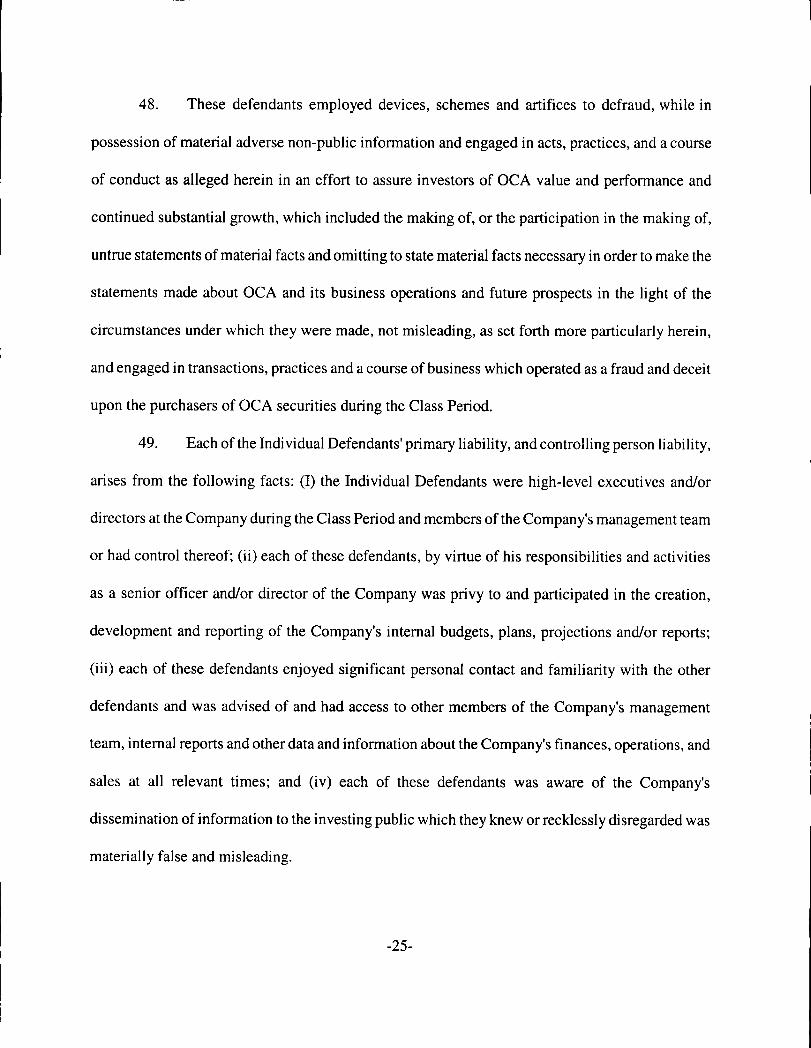

48 . These defendants employed devices, schemes and artifices to defraud, while i n

possession of material adverse non-public information and engaged in acts, practices, and a course

of conduct as alleged herein in an effo rt to assure investors of OCA value and performance an d

continued substantial growth, which included the making of, or the participation in the making of ,

untrue statements of material facts and omitting to state material facts necessary in order to make the

statements made about OCA and its business operations and future prospects in the light of th e

circumstances under which they were made, not misleading, as set forth more particularly herein ,

and engaged in transactions, practices and a course of business which operated as a fraud and decei t

upon the purchasers of OCA securities du ring the Class Period .

49. Each of the Individual Defendants' primary liability, and controlling person liability ,

arises from the following facts : (I) the Individual Defendants were high-level executives and/o r

directors at the Company during the Class Period and members of the Company's management tea m

or had control thereof; (ii) each of these defendants, by virtue of his responsibilities and activitie s

as a senior officer and/or director of the Company was privy to and participated in the creation ,

development and reporting of the Company's internal budgets, plans, projections and/or reports ;

(iii) each of these defendants enjoyed significant personal contact and familiarity with the othe r

defendants and was advised of and had access to other members of the Company's management

team, internal reports and other data and information about the Company's finances, operations, an d

sales at all relevant times ; and (iv) each of these defendants was aware of the Company' s

dissemination of information to the investing public which they knew or recklessly disregarded wa s

materially false and misleading .

-25-

50. The defendants had actual knowledge of the misrepresentations and omissions o f

material facts set forth herein, or acted with reckless disregard for the truth in that they failed to

ascertain and to disclose such facts, even though such facts were available to them . Such defendants '

mate rial misrepresentations and/or omissions were done knowingly or recklessly and for the purpos e

and effect of concealing OCA's operating condition and future business prospects from the investin g

public and supporting the artificially inflated price of its securities . As demonstrated by defendants '

overstatements and misstatements of the Company 's business, operations and earn ings throughout

the Class Period, defendants, if they did not have actual knowledge of the misrepresentations an d

omissions alleged, were reckless in failing to obtain such knowledge by deliberately refraining fro m

taking those steps necessary to discover whether those statements were false or misleading .

51 . As a result of the dissemination of the materially false and misleading informatio n

and failure to disclose materi al facts, as set fo rth above, the market price of OCA secu rities was

artificially inflated during the Class Period. In ignorance of the fact that market prices of OCA' s

publicly-traded securities were artificially inflated, and relying directly or indirectly on the false and

misleading statements made by defendants, or upon the integrity of the market in which the securitie s

trades, and/or on the absence of material adverse information that was known to or recklessl y

disregarded by defendants but not disclosed in public statements by defendants during the Clas s

Period, Plaintiff and the other members of the Class acquired OCA securities during the Class Period

at artificially high prices and were damaged thereby .

52. At the time of said misrepresentations and omissions, Plaintiff and other member s

of the Class were ignorant of their falsity, and believed them to be true . Had Plaintiff and the other

members of the Class and the marketplace known the truth regarding the problems that OCA was

-26-

experiencing, which were not disclosed by defendants, Plaintiff and other members of the Class

would not have purchased or otherwise acquired their OCA secu rities , or, if they had acquired suc h

securities during the Class Period, they would not have done so at the artificially inflated price s

which they paid .

53. By virtue of the foregoing, defendants have violated Section 10(b) of the Exchang e

Act, and Rule 10b-5 promulgated thereunder.

54. As a direct and proximate result of defendants' wrongful conduct, Plaintiff and th e

other members of the Class suffered damages in connection with their respective purchases and sale s

of the Company's securities during the Class Period .

SECOND CLAIMViolation Of Section 20(a) Of

The Exchange Act Against the Individual Defendants

55 . Plaintiff repeats and realleges each and every allegation contained above as if fully

set forth herein .

56 . The Individual Defendants acted as controlling persons of OCA within the meaning

of Section 20(a) of the Exchange Act as alleged herein . By virtue of their high-level positions, an d

their ownership and contractual rights, participation in and/or awareness of the Company's operation s

and/or intimate knowledge of the false financial statements filed by the Company with the SEC an d

disseminated to the investing public, the Individual Defendants had the power to influence an d

control and did influence and control, directly or indirectly, the decision-making of the Company ,

including the content and dissemination of the various statements which Plaintiff contend are false

and misleading . The Individual Defendants were provided with or had unlimited access to copie s

of the Company's reports, press releases, public filings and other statements alleged by Plaintiff t o

-27-

be misleading prior to and/or shortly after these statements were issued and had the ability to preven t

the issuance of the statements or cause the statements to be corrected .

57. In particular, each of these defendants had direct and supervisory involvement in the

day-to-day operations of the Company and, therefore, is presumed to have had the power to contro l

or influence the particular transactions giving rise to the securities violations as alleged herein, an d

exercised the same .

58 . As set forth above, OCA and the Individual Defendants each violated Section 10(b )

and Rule 10b-5 by their acts and omissions as alleged in this Complaint . By virtue of their position s

as controlling persons, the Individual Defendants are liable pursuant to Section 20(a) of th e

Exchange Act . As a direct and proximate result of defendants' wrongful conduct, Plaintiff and othe r

members of the Class suffered damages in connection with their purchases of the Company' s

securities during the Class Period .

WHEREFORE , Plaintiff prays for relief and judgment, as follows :

(a) Determining that this action is a proper class action, designating Plaintiff as Lead

Plaintiff and cert ifying Plaintiff as a class representative under Rule 23 of the Federal Rules of Civi l

Procedure and Plaintiff's counsel as Lead Counsel ;

(b) Awarding compensatory damages in favor of Plaintiff and the other Clas s

members against all defendants, jointly and severally, for all damages sustained as a result of

defendants' wrongdoing, in an amount to be proven at trial, including interest thereon ;

(c) Awarding Plaintiff and the Class their reasonable costs and expenses incurred in

this action, including counsel fees and expert fees ; and

(d) Such other and further relief as the Court may deem just and proper .

-28-

JURY TRIAL DEMANDED

Plaintiff hereby demands a trial by jury .

Dated: June 10, 2005ALLAN KA R & A SOCIATES , P.L.L.C.

By:Allan Kanner (La. Bar No . 20580)Conlee S . Whiteley (La. Bar No. 22678701 Camp StreetNew Orleans , LA 70130(504) 524-5777

SCHIFFRIN & BARROWAY, LLPMarc A. TopazRichard A . ManiskasTamara Skvirsk y280 King of Prussia Rd.Radnor, PA 19087(610) 667-7706

Attorneys for Plaintiff

-29-

gkAJIgVn CMR`I FICA'T t

Y, (Mr/Ma.) ,,, (°plamtiff ') declaim tsnd~c pes~aJty

of perjury, as to Rt:o claims asserted rmdar the federal securldes laws, that:

1 . Plaiin'iff has reviewed the oomplairtt and autharizod the oomziena =oat of

an actian on Plaintiffs bell

2. Plaintiff did not purchase tb~ rity that is t a mlj eat of this action at

the dircctioii of plainti$'e counsel or in order td partkdpato in this private salon .

3 . Pleinti js willing to smve as a representative putty au behalf of the atria,

including providing testraany at depoeitlau and trial, if necessary ,

4. P1ainws tr notions in tC A . w~e, of sooarities dwing the

Class Period spe ed in The Complaint are as folloMvs (usc aM ional sheet if t ocsaaty) :

Date f skiff Purchaeeel # pf, Shares gold riceY/j 0, 41 a 0 ::~ 0& ~, V7

5. During the tbroo yearn prior to the date of this Cer eate, Plaintiff has net

sou& to cave or served as a representative party for a class in an aotion filed under the

federal scauritles laws. [Or, *1.aintifl'ha,a served as a class repr scWntiva in the action(s)

listed as follows" ]

6 . Plaintiiwill not accept any payment for oe vixag a® a raproaer tsfive patty

on behalf of the class begot d the Plaintifs pro ra a share of any recovery . =Opt ands

reasonable costs and expenses (including lost wages) directly relating to he

representation of the class as ordered or approved by the court

I declare wider pealty of *my that the foregoing is true and ogrect.

ti ig . day of tK ,2000 Sip Ns= 114AIA4; ~?tint ISr ne : d18 j" asks