3. consumer brand adoption process in services an empirical study on retail banking-2.pdf

TRANSCRIPT

CONSUMER BRAND ADOPTION PROCESS IN SERVICES: AN EMPIRICAL STUDY ON RETAIL

BANKING

Dr. Ritesh K. Patel

Assistant Professor,

Nirma University (Institute of Law)

ABSTRACT

Keywords: Brand Adoption Process, Consumer Adoption, Adoption in Services, Retail Banking, Brand

Adoption in Banks, Services Adoption.

Introduction:

Adoption is an individual’s decision to become a regular user of a product. It is sequence of events

beginning with consumer awareness of a new product leading to trial usage and culminating in full and regular

use of the new product. Over time the adoption process resembles a bell curve formed by innovators, early

adopters, and the majority of consumers, late adopters, and laggards.

An innovation is any good, service, or idea that is perceived by someone as new. The idea may

have a long history, but it is an innovation to the person who sees it as new. Innovations take time to spread

through the social system.

The consumer-adoption process focuses on the mental process through which an individual passes

from first hearing about an innovation to final adoption. Adopters of new products have been observed to

move through five stages:

1. Awareness -The consumer becomes aware of the innovation but lacks information about it.

2. Interest-The consumer is stimulated to seek information about the innovation.

3. Evaluation -The consumer considers whether to try the innovation.

4. Trial-The consumer tries the innovation to improve his or her estimate of its value.

5. Adoption -The consumer decides to make full and regular use of the innovation.

The new-product marketer should facilitate movement through these stages. A portable electric-

dishwasher manufacturer might discover that many consumers are stuck in the interest stage; they do not buy

because of their uncertainty and the large investment cost. But these same consumers would be willing to use

an electric-dishwasher on a trial basis for a small monthly fee. The manufacturer should consider offering a

trial-use plan with option to buy.

Factors Influencing the Adoption Process Adoption according to Rogers and Shoemaker (1971) is the decision to use and accept an innovation

in the form of a new idea, product or service. People differ in their approach towards change. Some differ in

adopting new fashion, some in adopting new appliances, some doctors are hesitant to apply new medicines

and still some farmers do not apply new implements. This is called adoption culture. After the early adoption,

they increase the use and then others follow. Others are late adopters by nature. Let us categorize these

customers into three units:

One who are early adopters. They are very quick in their response. These people are venture some and

willing to try new ideas. In fact they are innovators in life and early adopters.

Adoption is an individual’s decision to become a regular user of a product. How do potential

customers learn about new products, try them, and adopt or reject them? The consumer adoption

process is later followed by the consumer loyalty process, which is the concern of the established

producer. Years ago, new product marketers used a mass market approach to launch products. This

approach had two main drawbacks: It called for heavy marketing expenditures, and it involved many

wasted exposures. These drawbacks led to a second approach, heavy user target marketing. This

approach makes sense, provided that heavy users are identifiable and are early adopters. However,

even within the heavy user group, many heavy users are loyal to existing brands. New product

marketers now aim at consumers who are early adopters. In the current research the researcher has

tried to study the consumer brand adoption process in the context of retail banking environment

Secondly Early Majority. They are very careful people and take time to adopt things. They tend to

collect information about the change or the product, study carefully and then adopt on the basis of their

merits.

The third ones are late majority and traditionalists. They are the ones who adopt late and then use the

product1.

As marketing managers, we must study the demographics, the psychographics and media

characteristics of the product and also keep the theme of advertising message on these lines. We must find the

innovators of the product and also opinion leaders and keeping in view the financial stature of the consumers

and their category. Then there are certain areas where product change is imminent and quicker while some

areas change or innovation in the product is least desired or welcomed

Personal Influence Plays A Key Role

In case of some of the products, depending to which category they belong to , personal influence and

selling is very important. Demonstrations, experimentation, and even free use is given to influence the change

in product or its innovation. Cosmetic items, food items and items in use of household are subject to personal

selling.

Characteristics Of The Innovation Affects The Rate Of Adoption Some products are quick in innovation, such as fashion items or the ones that bring a direct change in

our status etc. Some product takes long to adoption like technical products or automobiles etc.

Internal Brand adoption is seen seriously in services organization because brand adoption (also

referred to as alignment or engagement) is about making sure the employees (and close stakeholders, such as

franchise staff, call centres or intermediaries) of an organization completely understand the organization’s

brand, and what it stands for — and how it connects to their daily job responsibilities. Brand Adoption

programs are undertaken with employees to make sure their activities on a day to day basis are contributing to

a consistent customer experience based upon the attributes (see definition) of the brand.

Literature Review Brand equity in general is defined as “a set of brand assets and liabilities linked to brand, its name or

symbol that add to or subtract from the value provided by a product or service to a firm and/or the firm’s

customers” (Aaker, 1991, p.15). However, consumer based brand equity is defined as consumer’s different

response between a focal brand, and an unbranded product when both have the same level of marketing

stimuli and product attributes (Yoo and Donthu, 2001). Conceptualizing brand equity from a consumer

perspective is worth examining as it offers specific guidelines for marketing strategies and tactics (Aaker and

Keller, 1993). Though the concept of brand equity has many definitions and forms, the construct collectively

consists of four dimensions such as brand loyalty, brand awareness, perceived quality of brand and brand

associations (Aaker, 1991 and Aaker and Keller, 1993). There is empirical evidence from the existing

literature that these our dimensions substantially measure brand. Therefore, in the present study an attempt has

been made to explore the outcomes of the consumer behavior in relation to brand equity incorporating four

dimensions.

Brand Loyalty is defined as “attachment that a consumer has to a brand” (Aaker 1991, p. 39). The

concept of brand loyalty usually denotes a favorable attitude towards a brand resulting in the repeat purchases

o the same brand over a period of time (Rossiter and Percy, 1987). Based on the attitude perspective, brand

loyalty is defined as ‘the tendency to be loyal to focal brand, which is demonstrated with an intention to buy

the brand as a primary choice” (Yoo and Donthu, 2001, p.3). Very few studies focused on the aspect of brand

equity and its relation to the selection of bank.

H0_01: Customer’s Loyalty and customer’s decision to recommend the bank to others are not

independent to each other.

H1_01: Customer’s loyalty and customer’s decision to recommend the bank to others are dependent

on each other.

Brand awareness is defined as “the ability of a buyer to recognize or recall that a brand is member of

a certain product category” (Aaker, 1991, p.61). It often represents the consumer’s ability to identify or

recognize the brand (Rossiter and Percy, 1987). Brand awareness in conceptualized as an output of both brand

recognition and brand recall (Keller, 2004).

Brand recognition related to consumer’s ability to confirm a prior exposure to the brand when it is

given as a cue (Keller, 2004).

Brand recall relates to the consumer’s ability to retrieve the brand when the product category or some

other type of product is given as a cue (Keller, 2004). In general, consumers tend to adopt a decision rule to

buy only familiar and well-established brands.

H0_02: Level of ‘Brand Awareness’ of bank does not lead to consumer’s readiness to use future

products/services of the bank.

H1_02: Level of ‘Brand Awareness’ of bank leads to consumer’s readiness to use future

products/services of the bank.

Brand perceived quality is the “consumer’s judgment about a product’s overall excellence or

superiority” (Zeithaml, 1988, p.3). It is therefore the consumer’s subjective evaluation of the product quality

thus differentiating a particular brand from other competing brands. Brand name is a key quality indicator,

which enhances the brand’s perceived quality (Balaji and Supriya 2006).

H0_03: Bank’s service quality and consumer’s loyalty are not correlated.

H1_03: Bank’s service quality and consumer’s loyalty are correlated.

Brand associations are often referred to as “anything linked in memory to a brand” (Aaker, 1991,

p.109). A brand association depicts a level of strength, and that the linked to a brand from the association will

be stronger when it is based on many experiences or exposure to communications, and when a network of

other links supports it (Aaker, 1991). From the consumer’s perspective, brand association adds value to the

consumer by providing a reason for consumers to adopt the brand and by creating positive attitude among the

consumers (Aaker, 1991).

H0_04: Bank’s ‘Brand Association’ does not influence on customer satisfaction.

H1_04: Bank’s ‘Brand Association’ does influence on customer satisfaction.

Consumers’ overall evaluation of a brand depends upon the attitudes they form towards that brand,

often referred as brand attitudes (Wilkie, 1986). Attitudes are important as they form the basis or the consumer

behavior. Attitudes are viewed as a function of the salient belies that a consumer has about the brand with

certain attributes and the evaluative judgment of those beliefs (Fisbein and Ajzen, 1975). Therefore, a

consumer’s brand loyalty depends on attitude towards a bank brand. Attitude is defined as an individual’s

evaluative effect about performing a target behavior (Fishbein and Ajzen, 1975). The attitudinal belie towards

adoption can be measured by five perceived attributes such as relative advantage, compatibility, complexity,

trialability and result demonstrability (Taylor and Todd, 1995). These attributes are proposed originally in the

diffusion of innovations framework (Rogers, 1983). A Conceptual framework of current study for the brand

adoption in Retail Banking is presented below (see Figure 1).

Figure 1: Conceptual Framework of Brand Adoption in Retail Banking

Attitude Factors:

Relative advantage is referred to as the degree to which an innovation s perceived as being better than

the ‘idea’ it supersedes (Roger, 1995). The perception of an innovation as advantageous by an individual is

Brand Equity Factors:

Brand Loyalty Brand Awareness Perceived Quality Brand

Association

Attitude Factors:

Relative Advantage Compatibility Complexity Trialability Result

Demonstrability

Brand Adoption in Retail Banking

more important that the objective advantage of the innovation itself (Rogers, 1995 and Gregor and Jones,

1999). In determining the adoption patterns, relative advantage has been identified as a key determinant in

extant literature. The degree of relative advantage is often measured in economic terms. However, Social

prestige, convenience and satisfaction are also considered to be important factors (Rogers, 1995). Therefore, it

has been found that the brand adopters invariably perceive relative advantage in terms of the economic

benefits that accrue and improvements that are afforded to their social status and convenience (Gregor and

Jones, 1999). In general, the greater the perceived relative advantage of an adoption, the more rapid will be its

rate of adoption and customer satisfaction (Agarwal and Prasad, 1998 and Gregor and Jones, 1999). Thus the

present study postulates that the more individual perceives the advantage of adopting a bank brand, the greater

the customer satisfaction.

H0_05: ‘Relative Advantage’ perceived in a bank brand does not influence customer’s response to

competitive moves by competitors.

H1_05: ‘Relative Advantage’ perceived in a bank brand influence customer’s response to competitive

moves by competitors.

Compatibility is the degree to which an innovation is perceived as being consistent with the existing

values, past experiences and the needs of the potential adopters (Rogers, 1995). An innovation is more likely

to be adopted when it is compatible with the individual’s professional responsibilities and value system.

Innovations that are compatible with the prevalent values and norms of a social system will be adopted more

rapidly than those that are incompatible (Rogers and Shoemaker, 1971 and Gregor and Jones, 1999). If an

individual perceives that the bank brand is compatible with the existing values, the likelihood of his

satisfaction is going to increase.

H0_06: The compatibility of a bank brand is not related to satisfaction of the customer.

H1_06: The compatibility of a bank brand is related to satisfaction of the customer.

Complexity is the degree to which an innovation is perceived as difficult to understand and use

(Roger, 1995). From the extant studies, it is evident that consumers readily adopt those which require less

technical skills and operational efforts (Cooper and Zmud, 1990). It is evident from the existing literature that

new ideas are adopted readily if they are simple, than those innovations that require the adopter to develop

new skills and understanding (Ndubisi and Chukwunonso, 2005). The above discussion leads to following

hypothesis:

H0_07: Complexity level of operating a bank account and customer satisfaction with a bank brand is

not correlated.

H1_07 Complexity level of operating a bank account and customer satisfaction with a bank brand are

correlated.

Trialability is the degree to which and innovation may be experimented with on a limited basis

(Rogers, 1995). If potential adopters are allowed to experiment, it results in rapid adoption by increasing the

‘comfortability’ level of the individuals. An adoption that is trialable denotes less uncertainty for an individual

to adopt (Ndubisi and Chukwunonso, 2005). Therefore, the ability to experiment or try with the global brands

before actual purchase would enhance its rate of adoption.

H0_08: The trialable nature of the bank brand does not affect the customer’s future purchase

intentions.

H1_08: The trialable nature of the bank brand does affect the customer’s future purchase intentions.

Result Demonstrability is the degree to which the results of an innovation are visible to others

(Rogers, 1995). The perception of an innovation that the benefits offered by its actual adoption are clearly

visible to others would enhance its likelihood of its adoption quickly. Thus the more the perception of the

consumers that brand would offer more communicable benefits to others members of a social system; the

rapid is its rate of adoption.

H0_09: The result demonstrability of a bank brand and satisfaction level of the customers is

independent with each other.

H1_09: Result Demonstrability of a bank brand and Satisfaction level of the customers are

correlated.

Research Design

The researchers have used exploratory research design to find out the determinants of corporate brand

image in banking industry. The researchers have used non-probability based convenience sampling method to

draw samples from the population of banks. The market surveys were conducted in six major cities of Gujarat,

Ahmedabad, Vadodara, Surat, Rajkot, Jamnagar and Bhavnagar. Seven major bank brands in Gujarat from

public, private and foreign banking sector, i.e., ICICI, HDFC, AXIS, Bank of Baroda (BOB), State Bank of

India (SBI), CITI and HSBC banks were selected as subjects of current study. The researcher has approached

1050 customers of these banks for filling out the survey forms. Most of the questions were constructed using

likert scale techniques to measure the customer’s angriness towards current practices of their bank brand.

Data Analysis & Interpretations

Here we will study each instrument of the two dimensions i.e. Brand Equity Factors and

Brand Attitude Factors separately one by and will find out its effect on the brand adoption in retail banks. Let us

find out the answers one by one:

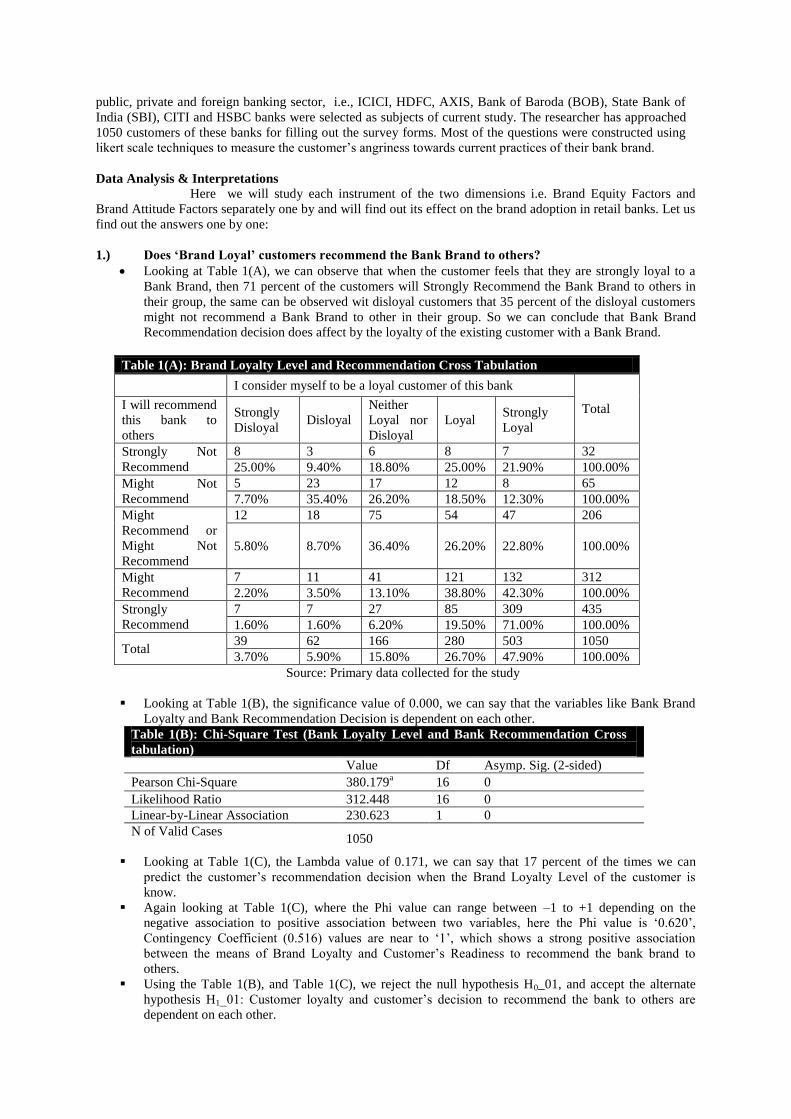

1.) Does ‘Brand Loyal’ customers recommend the Bank Brand to others?

Looking at Table 1(A), we can observe that when the customer feels that they are strongly loyal to a

Bank Brand, then 71 percent of the customers will Strongly Recommend the Bank Brand to others in

their group, the same can be observed wit disloyal customers that 35 percent of the disloyal customers

might not recommend a Bank Brand to other in their group. So we can conclude that Bank Brand

Recommendation decision does affect by the loyalty of the existing customer with a Bank Brand.

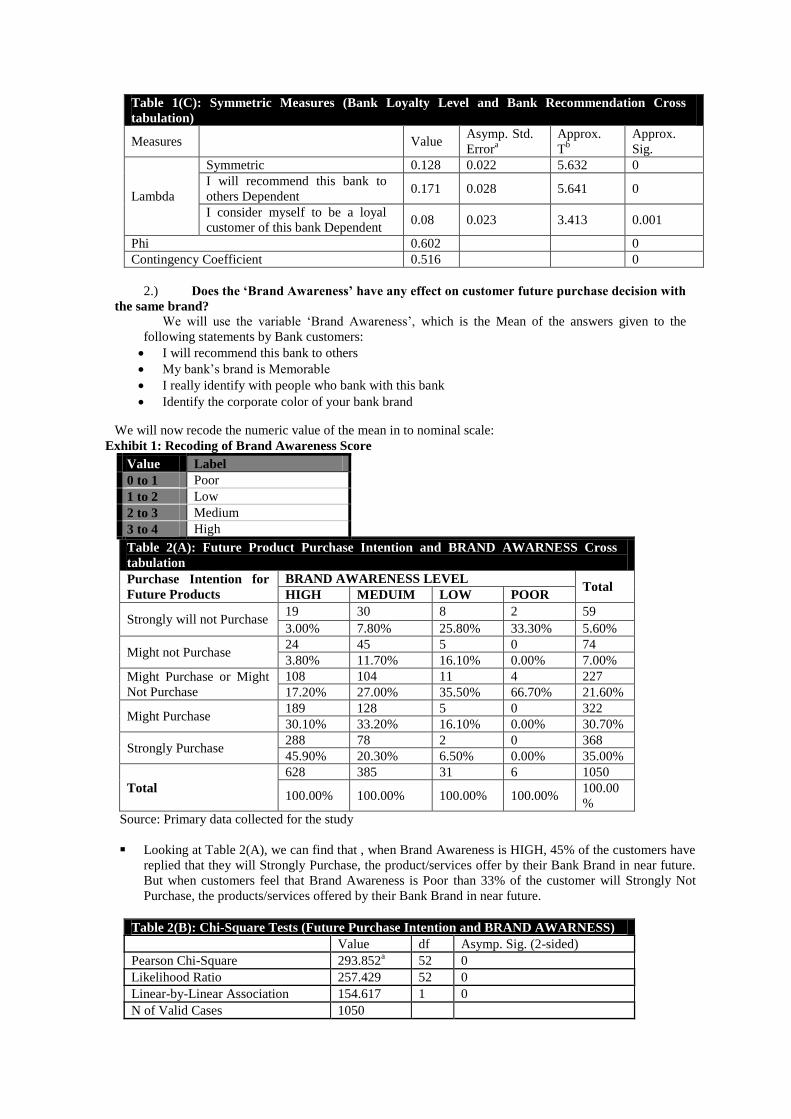

Table 1(A): Brand Loyalty Level and Recommendation Cross Tabulation

I consider myself to be a loyal customer of this bank

Total I will recommend

this bank to

others

Strongly

Disloyal Disloyal

Neither

Loyal nor

Disloyal

Loyal Strongly

Loyal

Strongly Not

Recommend

8 3 6 8 7 32

25.00% 9.40% 18.80% 25.00% 21.90% 100.00%

Might Not

Recommend

5 23 17 12 8 65

7.70% 35.40% 26.20% 18.50% 12.30% 100.00%

Might

Recommend or

Might Not

Recommend

12 18 75 54 47 206

5.80% 8.70% 36.40% 26.20% 22.80% 100.00%

Might

Recommend

7 11 41 121 132 312

2.20% 3.50% 13.10% 38.80% 42.30% 100.00%

Strongly

Recommend

7 7 27 85 309 435

1.60% 1.60% 6.20% 19.50% 71.00% 100.00%

Total 39 62 166 280 503 1050

3.70% 5.90% 15.80% 26.70% 47.90% 100.00%

Source: Primary data collected for the study

Looking at Table 1(B), the significance value of 0.000, we can say that the variables like Bank Brand

Loyalty and Bank Recommendation Decision is dependent on each other.

Table 1(B): Chi-Square Test (Bank Loyalty Level and Bank Recommendation Cross

tabulation)

Value Df Asymp. Sig. (2-sided)

Pearson Chi-Square 380.179a 16 0

Likelihood Ratio 312.448 16 0

Linear-by-Linear Association 230.623 1 0

N of Valid Cases

1050

Looking at Table 1(C), the Lambda value of 0.171, we can say that 17 percent of the times we can

predict the customer’s recommendation decision when the Brand Loyalty Level of the customer is

know.

Again looking at Table 1(C), where the Phi value can range between –1 to +1 depending on the

negative association to positive association between two variables, here the Phi value is ‘0.620’,

Contingency Coefficient (0.516) values are near to ‘1’, which shows a strong positive association

between the means of Brand Loyalty and Customer’s Readiness to recommend the bank brand to

others.

Using the Table 1(B), and Table 1(C), we reject the null hypothesis H0_01, and accept the alternate

hypothesis H1_01: Customer loyalty and customer’s decision to recommend the bank to others are

dependent on each other.

Table 1(C): Symmetric Measures (Bank Loyalty Level and Bank Recommendation Cross

tabulation)

Measures Value Asymp. Std.

Errora

Approx.

Tb

Approx.

Sig.

Lambda

Symmetric 0.128 0.022 5.632 0

I will recommend this bank to

others Dependent 0.171 0.028 5.641 0

I consider myself to be a loyal

customer of this bank Dependent 0.08 0.023 3.413 0.001

Phi 0.602 0

Contingency Coefficient 0.516 0

2.) Does the ‘Brand Awareness’ have any effect on customer future purchase decision with

the same brand? We will use the variable ‘Brand Awareness’, which is the Mean of the answers given to the

following statements by Bank customers:

I will recommend this bank to others

My bank’s brand is Memorable

I really identify with people who bank with this bank

Identify the corporate color of your bank brand

We will now recode the numeric value of the mean in to nominal scale:

Exhibit 1: Recoding of Brand Awareness Score

Value Label

0 to 1 Poor

1 to 2 Low

2 to 3 Medium

3 to 4 High

Table 2(A): Future Product Purchase Intention and BRAND AWARNESS Cross

tabulation

Purchase Intention for

Future Products

BRAND AWARENESS LEVEL Total

HIGH MEDUIM LOW POOR

Strongly will not Purchase 19 30 8 2 59

3.00% 7.80% 25.80% 33.30% 5.60%

Might not Purchase 24 45 5 0 74

3.80% 11.70% 16.10% 0.00% 7.00%

Might Purchase or Might

Not Purchase

108 104 11 4 227

17.20% 27.00% 35.50% 66.70% 21.60%

Might Purchase 189 128 5 0 322

30.10% 33.20% 16.10% 0.00% 30.70%

Strongly Purchase 288 78 2 0 368

45.90% 20.30% 6.50% 0.00% 35.00%

Total

628 385 31 6 1050

100.00% 100.00% 100.00% 100.00% 100.00

%

Source: Primary data collected for the study

Looking at Table 2(A), we can find that , when Brand Awareness is HIGH, 45% of the customers have

replied that they will Strongly Purchase, the product/services offer by their Bank Brand in near future.

But when customers feel that Brand Awareness is Poor than 33% of the customer will Strongly Not

Purchase, the products/services offered by their Bank Brand in near future.

Table 2(B): Chi-Square Tests (Future Purchase Intention and BRAND AWARNESS)

Value df Asymp. Sig. (2-sided)

Pearson Chi-Square 293.852a 52 0

Likelihood Ratio 257.429 52 0

Linear-by-Linear Association 154.617 1 0

N of Valid Cases 1050

a. 28 cells (40.0%) have expected count less than 5. The minimum expected count is .11.

Looking at Table 2(B), we can find the Significance of 0.000, which indicates Bank Brand Awareness

and Customers Readiness to Purchase Future Products/Services are correlated with each other.

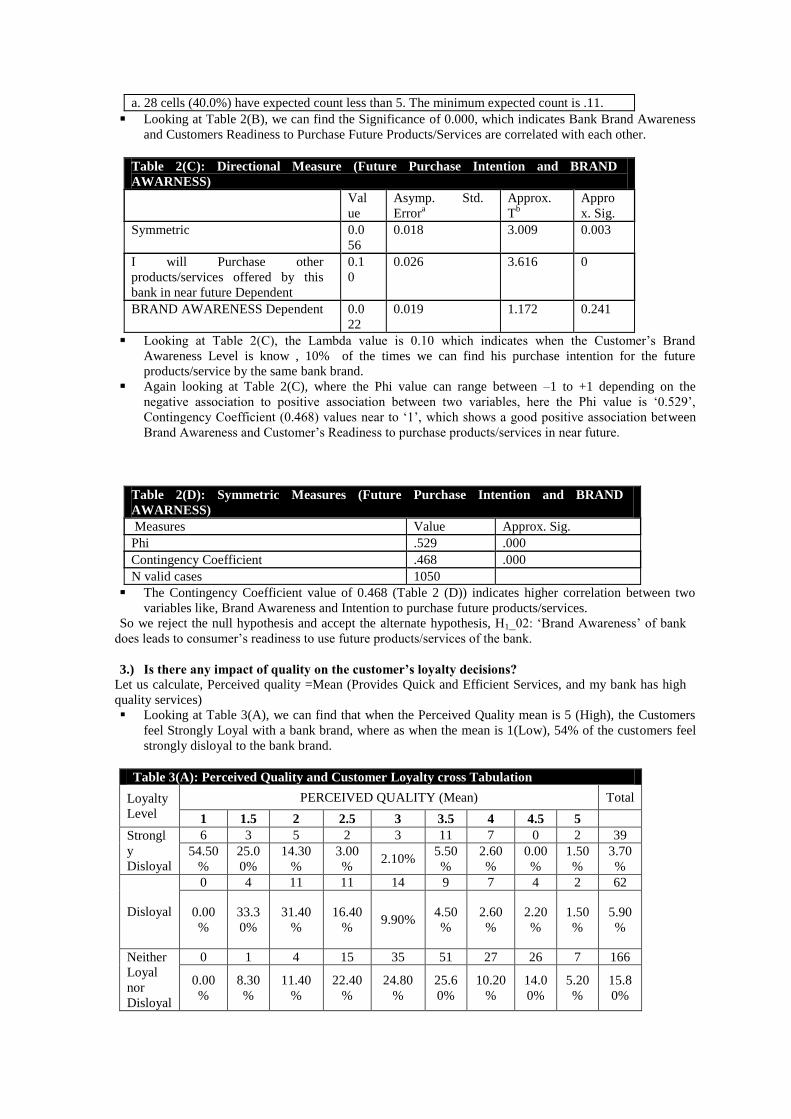

Table 2(C): Directional Measure (Future Purchase Intention and BRAND

AWARNESS)

Val

ue

Asymp. Std.

Errora

Approx.

Tb

Appro

x. Sig.

Symmetric 0.0

56

0.018 3.009 0.003

I will Purchase other

products/services offered by this

bank in near future Dependent

0.1

0

0.026 3.616 0

BRAND AWARENESS Dependent 0.0

22

0.019 1.172 0.241

Looking at Table 2(C), the Lambda value is 0.10 which indicates when the Customer’s Brand

Awareness Level is know , 10% of the times we can find his purchase intention for the future

products/service by the same bank brand.

Again looking at Table 2(C), where the Phi value can range between –1 to +1 depending on the

negative association to positive association between two variables, here the Phi value is ‘0.529’,

Contingency Coefficient (0.468) values near to ‘1’, which shows a good positive association between

Brand Awareness and Customer’s Readiness to purchase products/services in near future.

Table 2(D): Symmetric Measures (Future Purchase Intention and BRAND

AWARNESS)

Measures Value Approx. Sig.

Phi .529 .000

Contingency Coefficient .468 .000

N valid cases 1050

The Contingency Coefficient value of 0.468 (Table 2 (D)) indicates higher correlation between two

variables like, Brand Awareness and Intention to purchase future products/services.

So we reject the null hypothesis and accept the alternate hypothesis, H1_02: ‘Brand Awareness’ of bank

does leads to consumer’s readiness to use future products/services of the bank.

3.) Is there any impact of quality on the customer’s loyalty decisions?

Let us calculate, Perceived quality =Mean (Provides Quick and Efficient Services, and my bank has high

quality services)

Looking at Table 3(A), we can find that when the Perceived Quality mean is 5 (High), the Customers

feel Strongly Loyal with a bank brand, where as when the mean is 1(Low), 54% of the customers feel

strongly disloyal to the bank brand.

Table 3(A): Perceived Quality and Customer Loyalty cross Tabulation

Loyalty

Level

PERCEIVED QUALITY (Mean) Total

1 1.5 2 2.5 3 3.5 4 4.5 5

Strongl

y

Disloyal

6 3 5 2 3 11 7 0 2 39

54.50

%

25.0

0%

14.30

%

3.00

% 2.10%

5.50

%

2.60

%

0.00

%

1.50

%

3.70

%

Disloyal

0 4 11 11 14 9 7 4 2 62

0.00

%

33.3

0%

31.40

%

16.40

% 9.90%

4.50

%

2.60

%

2.20

%

1.50

%

5.90

%

Neither

Loyal

nor

Disloyal

0 1 4 15 35 51 27 26 7 166

0.00

%

8.30

%

11.40

%

22.40

%

24.80

%

25.6

0%

10.20

%

14.0

0%

5.20

%

15.8

0%

Loyal

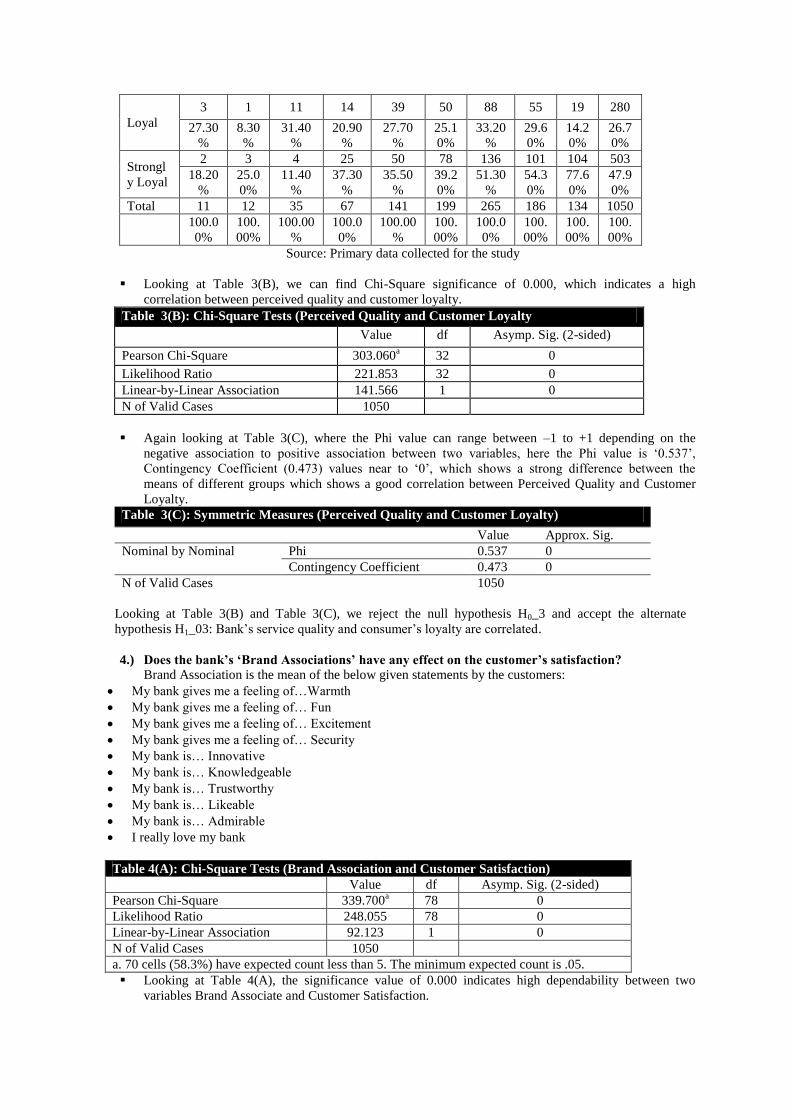

3 1 11 14 39 50 88 55 19 280

27.30

%

8.30

%

31.40

%

20.90

%

27.70

%

25.1

0%

33.20

%

29.6

0%

14.2

0%

26.7

0%

Strongl

y Loyal

2 3 4 25 50 78 136 101 104 503

18.20

%

25.0

0%

11.40

%

37.30

%

35.50

%

39.2

0%

51.30

%

54.3

0%

77.6

0%

47.9

0%

Total 11 12 35 67 141 199 265 186 134 1050

100.0

0%

100.

00%

100.00

%

100.0

0%

100.00

%

100.

00%

100.0

0%

100.

00%

100.

00%

100.

00%

Source: Primary data collected for the study

Looking at Table 3(B), we can find Chi-Square significance of 0.000, which indicates a high

correlation between perceived quality and customer loyalty.

Table 3(B): Chi-Square Tests (Perceived Quality and Customer Loyalty)

Value df Asymp. Sig. (2-sided)

Pearson Chi-Square 303.060a 32 0

Likelihood Ratio 221.853 32 0

Linear-by-Linear Association 141.566 1 0

N of Valid Cases 1050

Again looking at Table 3(C), where the Phi value can range between –1 to +1 depending on the

negative association to positive association between two variables, here the Phi value is ‘0.537’,

Contingency Coefficient (0.473) values near to ‘0’, which shows a strong difference between the

means of different groups which shows a good correlation between Perceived Quality and Customer

Loyalty.

Table 3(C): Symmetric Measures (Perceived Quality and Customer Loyalty)

Value Approx. Sig.

Nominal by Nominal Phi 0.537 0

Contingency Coefficient 0.473 0

N of Valid Cases 1050

Looking at Table 3(B) and Table 3(C), we reject the null hypothesis H0_3 and accept the alternate

hypothesis H1_03: Bank’s service quality and consumer’s loyalty are correlated.

4.) Does the bank’s ‘Brand Associations’ have any effect on the customer’s satisfaction?

Brand Association is the mean of the below given statements by the customers:

My bank gives me a feeling of…Warmth

My bank gives me a feeling of… Fun

My bank gives me a feeling of… Excitement

My bank gives me a feeling of… Security

My bank is… Innovative

My bank is… Knowledgeable

My bank is… Trustworthy

My bank is… Likeable

My bank is… Admirable

I really love my bank

Table 4(A): Chi-Square Tests (Brand Association and Customer Satisfaction)

Value df Asymp. Sig. (2-sided)

Pearson Chi-Square 339.700a 78 0

Likelihood Ratio 248.055 78 0

Linear-by-Linear Association 92.123 1 0

N of Valid Cases 1050

a. 70 cells (58.3%) have expected count less than 5. The minimum expected count is .05.

Looking at Table 4(A), the significance value of 0.000 indicates high dependability between two

variables Brand Associate and Customer Satisfaction.

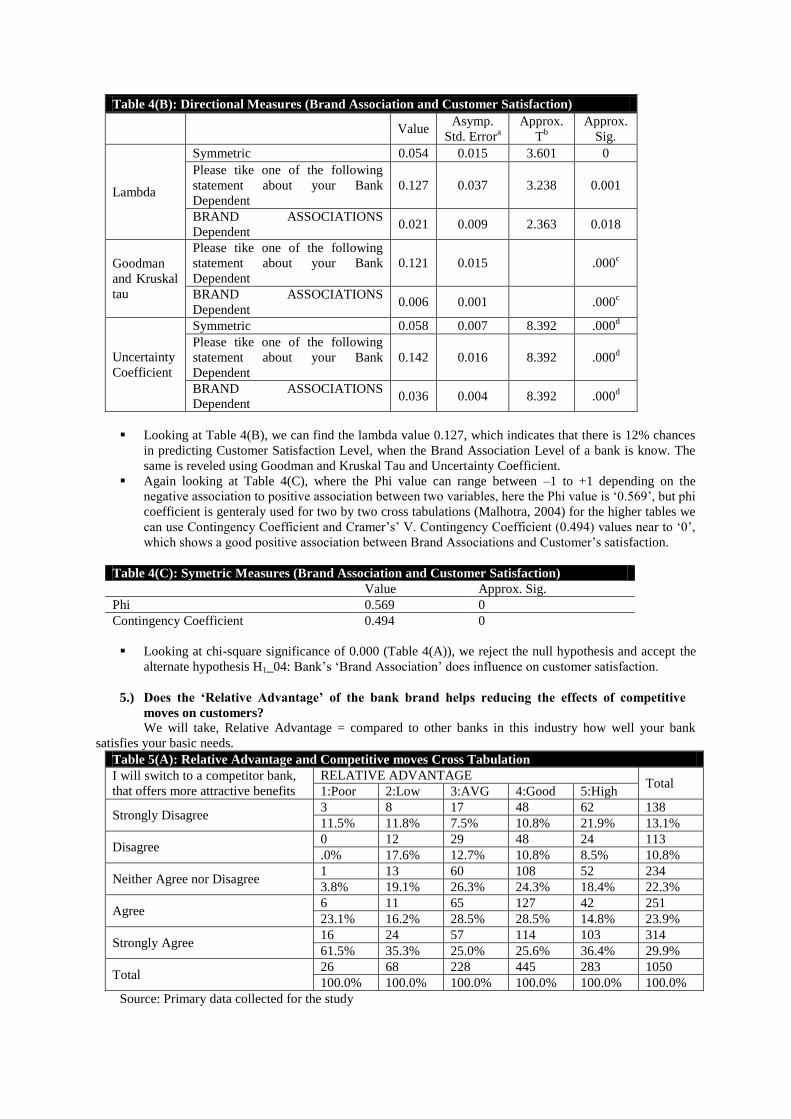

Table 4(B): Directional Measures (Brand Association and Customer Satisfaction)

Value Asymp.

Std. Errora

Approx.

Tb

Approx.

Sig.

Lambda

Symmetric 0.054 0.015 3.601 0

Please tike one of the following

statement about your Bank

Dependent

0.127 0.037 3.238 0.001

BRAND ASSOCIATIONS

Dependent 0.021 0.009 2.363 0.018

Goodman

and Kruskal

tau

Please tike one of the following

statement about your Bank

Dependent

0.121 0.015 .000c

BRAND ASSOCIATIONS

Dependent 0.006 0.001 .000

c

Uncertainty

Coefficient

Symmetric 0.058 0.007 8.392 .000d

Please tike one of the following

statement about your Bank

Dependent

0.142 0.016 8.392 .000d

BRAND ASSOCIATIONS

Dependent 0.036 0.004 8.392 .000

d

Looking at Table 4(B), we can find the lambda value 0.127, which indicates that there is 12% chances

in predicting Customer Satisfaction Level, when the Brand Association Level of a bank is know. The

same is reveled using Goodman and Kruskal Tau and Uncertainty Coefficient.

Again looking at Table 4(C), where the Phi value can range between –1 to +1 depending on the

negative association to positive association between two variables, here the Phi value is ‘0.569’, but phi

coefficient is genteraly used for two by two cross tabulations (Malhotra, 2004) for the higher tables we

can use Contingency Coefficient and Cramer’s’ V. Contingency Coefficient (0.494) values near to ‘0’,

which shows a good positive association between Brand Associations and Customer’s satisfaction.

Table 4(C): Symetric Measures (Brand Association and Customer Satisfaction)

Value Approx. Sig.

Phi 0.569 0

Contingency Coefficient 0.494 0

Looking at chi-square significance of 0.000 (Table 4(A)), we reject the null hypothesis and accept the

alternate hypothesis H1_04: Bank’s ‘Brand Association’ does influence on customer satisfaction.

5.) Does the ‘Relative Advantage’ of the bank brand helps reducing the effects of competitive

moves on customers?

We will take, Relative Advantage = compared to other banks in this industry how well your bank

satisfies your basic needs.

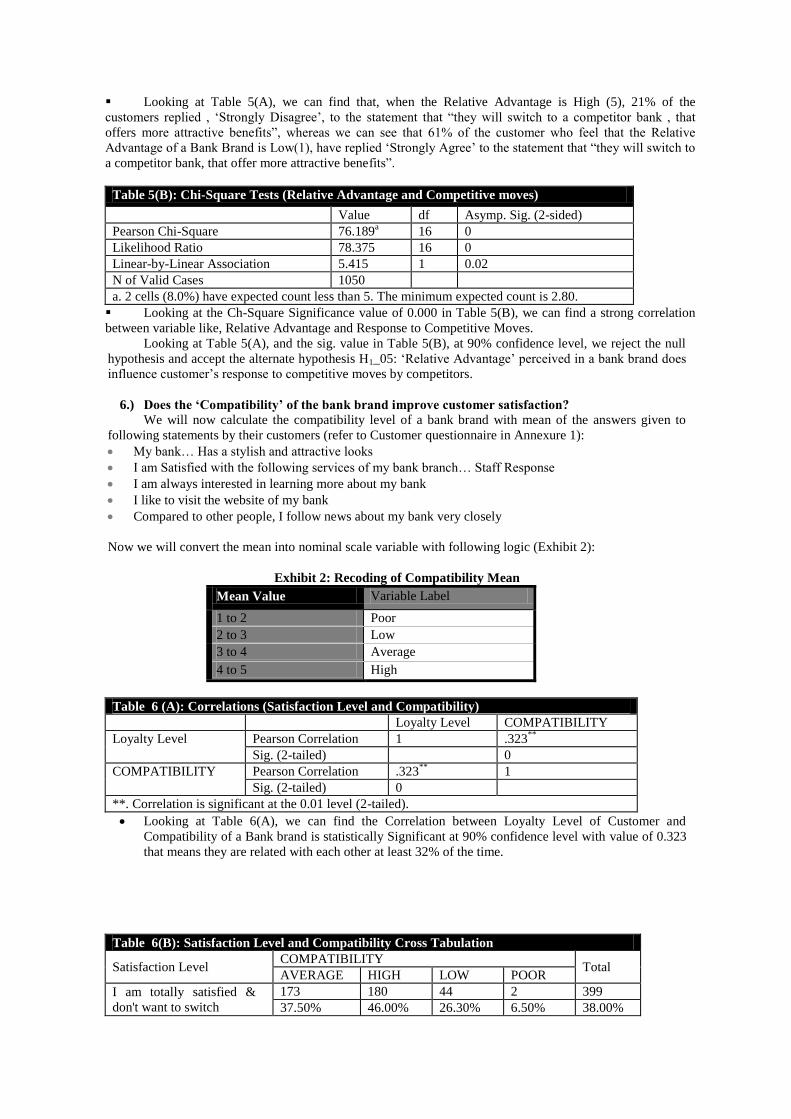

Table 5(A): Relative Advantage and Competitive moves Cross Tabulation

I will switch to a competitor bank,

that offers more attractive benefits

RELATIVE ADVANTAGE Total

1:Poor 2:Low 3:AVG 4:Good 5:High

Strongly Disagree 3 8 17 48 62 138

11.5% 11.8% 7.5% 10.8% 21.9% 13.1%

Disagree 0 12 29 48 24 113

.0% 17.6% 12.7% 10.8% 8.5% 10.8%

Neither Agree nor Disagree 1 13 60 108 52 234

3.8% 19.1% 26.3% 24.3% 18.4% 22.3%

Agree 6 11 65 127 42 251

23.1% 16.2% 28.5% 28.5% 14.8% 23.9%

Strongly Agree 16 24 57 114 103 314

61.5% 35.3% 25.0% 25.6% 36.4% 29.9%

Total 26 68 228 445 283 1050

100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Source: Primary data collected for the study

Looking at Table 5(A), we can find that, when the Relative Advantage is High (5), 21% of the

customers replied , ‘Strongly Disagree’, to the statement that “they will switch to a competitor bank , that

offers more attractive benefits”, whereas we can see that 61% of the customer who feel that the Relative

Advantage of a Bank Brand is Low(1), have replied ‘Strongly Agree’ to the statement that “they will switch to

a competitor bank, that offer more attractive benefits”.

Table 5(B): Chi-Square Tests (Relative Advantage and Competitive moves)

Value df Asymp. Sig. (2-sided)

Pearson Chi-Square 76.189a 16 0

Likelihood Ratio 78.375 16 0

Linear-by-Linear Association 5.415 1 0.02

N of Valid Cases 1050

a. 2 cells (8.0%) have expected count less than 5. The minimum expected count is 2.80.

Looking at the Ch-Square Significance value of 0.000 in Table 5(B), we can find a strong correlation

between variable like, Relative Advantage and Response to Competitive Moves.

Looking at Table 5(A), and the sig. value in Table 5(B), at 90% confidence level, we reject the null

hypothesis and accept the alternate hypothesis H1_05: ‘Relative Advantage’ perceived in a bank brand does

influence customer’s response to competitive moves by competitors.

6.) Does the ‘Compatibility’ of the bank brand improve customer satisfaction?

We will now calculate the compatibility level of a bank brand with mean of the answers given to

following statements by their customers (refer to Customer questionnaire in Annexure 1):

My bank… Has a stylish and attractive looks

I am Satisfied with the following services of my bank branch… Staff Response

I am always interested in learning more about my bank

I like to visit the website of my bank

Compared to other people, I follow news about my bank very closely

Now we will convert the mean into nominal scale variable with following logic (Exhibit 2):

Exhibit 2: Recoding of Compatibility Mean

Mean Value Variable Label

1 to 2 Poor

2 to 3 Low

3 to 4 Average

4 to 5 High

Table 6 (A): Correlations (Satisfaction Level and Compatibility)

Loyalty Level COMPATIBILITY

Loyalty Level Pearson Correlation 1 .323**

Sig. (2-tailed) 0

COMPATIBILITY Pearson Correlation .323**

1

Sig. (2-tailed) 0

**. Correlation is significant at the 0.01 level (2-tailed).

Looking at Table 6(A), we can find the Correlation between Loyalty Level of Customer and

Compatibility of a Bank brand is statistically Significant at 90% confidence level with value of 0.323

that means they are related with each other at least 32% of the time.

Table 6(B): Satisfaction Level and Compatibility Cross Tabulation

Satisfaction Level COMPATIBILITY

Total AVERAGE HIGH LOW POOR

I am totally satisfied &

don't want to switch

173 180 44 2 399

37.50% 46.00% 26.30% 6.50% 38.00%

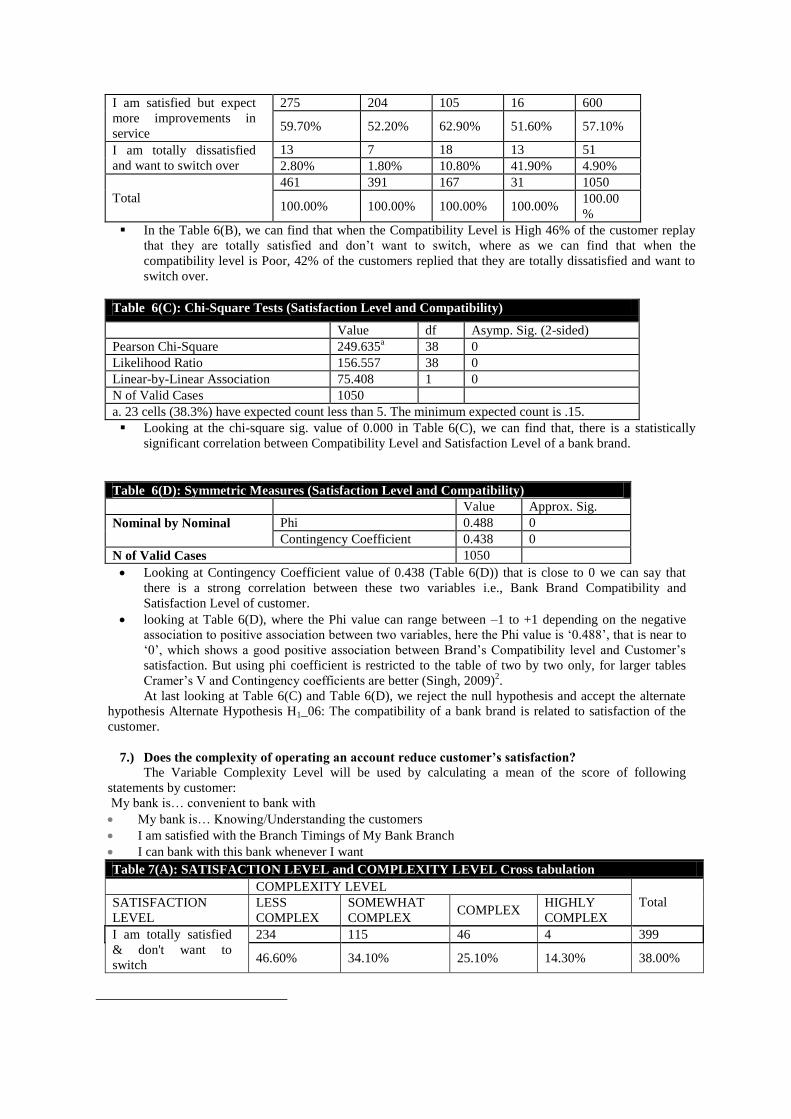

I am satisfied but expect

more improvements in

service

275 204 105 16 600

59.70% 52.20% 62.90% 51.60% 57.10%

I am totally dissatisfied

and want to switch over

13 7 18 13 51

2.80% 1.80% 10.80% 41.90% 4.90%

Total

461 391 167 31 1050

100.00% 100.00% 100.00% 100.00% 100.00

%

In the Table 6(B), we can find that when the Compatibility Level is High 46% of the customer replay

that they are totally satisfied and don’t want to switch, where as we can find that when the

compatibility level is Poor, 42% of the customers replied that they are totally dissatisfied and want to

switch over.

Table 6(C): Chi-Square Tests (Satisfaction Level and Compatibility)

Value df Asymp. Sig. (2-sided)

Pearson Chi-Square 249.635a 38 0

Likelihood Ratio 156.557 38 0

Linear-by-Linear Association 75.408 1 0

N of Valid Cases 1050

a. 23 cells (38.3%) have expected count less than 5. The minimum expected count is .15.

Looking at the chi-square sig. value of 0.000 in Table 6(C), we can find that, there is a statistically

significant correlation between Compatibility Level and Satisfaction Level of a bank brand.

Table 6(D): Symmetric Measures (Satisfaction Level and Compatibility)

Value Approx. Sig.

Nominal by Nominal Phi 0.488 0

Contingency Coefficient 0.438 0

N of Valid Cases 1050

Looking at Contingency Coefficient value of 0.438 (Table 6(D)) that is close to 0 we can say that

there is a strong correlation between these two variables i.e., Bank Brand Compatibility and

Satisfaction Level of customer.

looking at Table 6(D), where the Phi value can range between –1 to +1 depending on the negative

association to positive association between two variables, here the Phi value is ‘0.488’, that is near to

‘0’, which shows a good positive association between Brand’s Compatibility level and Customer’s

satisfaction. But using phi coefficient is restricted to the table of two by two only, for larger tables

Cramer’s V and Contingency coefficients are better (Singh, 2009)2.

At last looking at Table 6(C) and Table 6(D), we reject the null hypothesis and accept the alternate

hypothesis Alternate Hypothesis H1_06: The compatibility of a bank brand is related to satisfaction of the

customer.

7.) Does the complexity of operating an account reduce customer’s satisfaction?

The Variable Complexity Level will be used by calculating a mean of the score of following

statements by customer:

My bank is… convenient to bank with

My bank is… Knowing/Understanding the customers

I am satisfied with the Branch Timings of My Bank Branch

I can bank with this bank whenever I want

Table 7(A): SATISFACTION LEVEL and COMPLEXITY LEVEL Cross tabulation

COMPLEXITY LEVEL

Total SATISFACTION

LEVEL

LESS

COMPLEX

SOMEWHAT

COMPLEX COMPLEX

HIGHLY

COMPLEX

I am totally satisfied

& don't want to

switch

234 115 46 4 399

46.60% 34.10% 25.10% 14.30% 38.00%

I am satisfied but

expect more

improvements in

service

261 205 121 13 600

52.00% 60.80% 66.10% 46.40% 57.10%

I am totally

dissatisfied and want

to switch over

7 17 16 11 51

1.40% 5.00% 8.70% 39.30% 4.90%

Total 502 337 183 28 1050

100.00% 100.00% 100.00% 100.00% 100.00%

Looking at Table 7(A), we can find that when the customer find that the complexity level is high, then

39.3% of the customers replied that he is totally dissatisfied and want to switch over, well where as

when the complexity level is Less Complex, 46.6% of the Respondents replied that I am totally

satisfied and don’t want to switch.

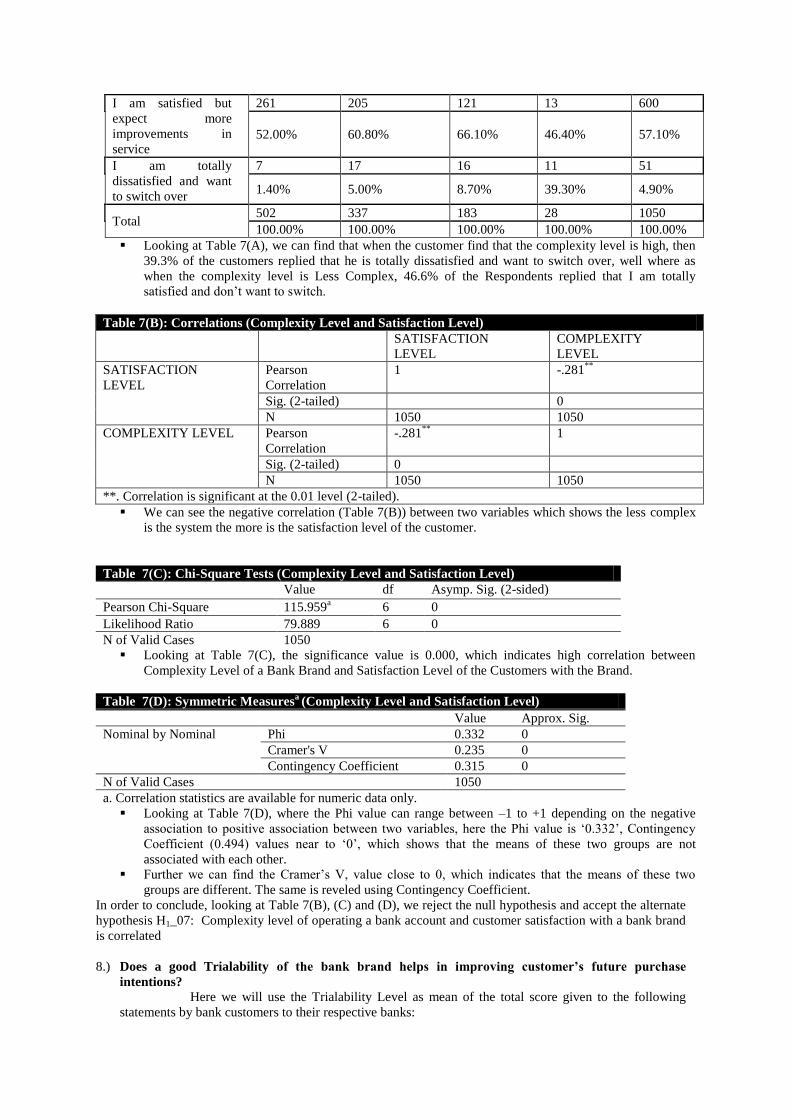

Table 7(B): Correlations (Complexity Level and Satisfaction Level)

SATISFACTION

LEVEL

COMPLEXITY

LEVEL

SATISFACTION

LEVEL

Pearson

Correlation

1 -.281**

Sig. (2-tailed) 0

N 1050 1050

COMPLEXITY LEVEL Pearson

Correlation

-.281**

1

Sig. (2-tailed) 0

N 1050 1050

**. Correlation is significant at the 0.01 level (2-tailed).

We can see the negative correlation (Table 7(B)) between two variables which shows the less complex

is the system the more is the satisfaction level of the customer.

Table 7(C): Chi-Square Tests (Complexity Level and Satisfaction Level)

Value df Asymp. Sig. (2-sided)

Pearson Chi-Square 115.959a 6 0

Likelihood Ratio 79.889 6 0

N of Valid Cases 1050

Looking at Table 7(C), the significance value is 0.000, which indicates high correlation between

Complexity Level of a Bank Brand and Satisfaction Level of the Customers with the Brand.

Table 7(D): Symmetric Measuresa (Complexity Level and Satisfaction Level)

Value Approx. Sig.

Nominal by Nominal Phi 0.332 0

Cramer's V 0.235 0

Contingency Coefficient 0.315 0

N of Valid Cases 1050

a. Correlation statistics are available for numeric data only.

Looking at Table 7(D), where the Phi value can range between –1 to +1 depending on the negative

association to positive association between two variables, here the Phi value is ‘0.332’, Contingency

Coefficient (0.494) values near to ‘0’, which shows that the means of these two groups are not

associated with each other.

Further we can find the Cramer’s V, value close to 0, which indicates that the means of these two

groups are different. The same is reveled using Contingency Coefficient.

In order to conclude, looking at Table 7(B), (C) and (D), we reject the null hypothesis and accept the alternate

hypothesis H1_07: Complexity level of operating a bank account and customer satisfaction with a bank brand

is correlated

8.) Does a good Trialability of the bank brand helps in improving customer’s future purchase

intentions? Here we will use the Trialability Level as mean of the total score given to the following

statements by bank customers to their respective banks:

My bank brand is… Adaptable (Q11.d)

My bank Branch is… Easily Reachable (Q14.a)

Table 8(A): Purchase Intention for Future Products/Services and TRIALABILITY LEVEL Cross

tabulation

Purchase Intention for

Future Products/Services

TRIALABILITY LEVEL Total

1 1.5 2 2.5 3 3.5 4 4.5 5

Strongly will not Purchase 2 3 4 12 6 4 15 10 3 59

15% 21% 13% 24% 5% 3% 6% 4% 2% 6%

Might not Purchase 0 1 2 1 15 15 16 20 4 74

0% 7% 6% 2% 12% 12% 7% 8% 2% 7%

Might Purchase or Might

Not Purchase

8 4 11 4 42 31 56 46 25 227

62% 29% 34% 8% 32% 26% 24% 18% 13% 22%

Might Purchase 2 0 6 21 28 44 101 70 50 322

15% 0% 19% 41% 22% 36% 43% 27% 26% 31%

Strongly Purchase 1 6 9 13 39 27 48 114 111 368

8% 43% 28% 25% 30% 22% 20% 44% 58% 35%

Total 13 14 32 51 130 121 236 260 193 1050

100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Looking at Table 8(A), we can find that as the Trialability Level of the Bank Brand increases, the

satisfaction level of the customer is also increases. For the Trialability Level of 5, 55% of the

customers responded that they will strongly purchase the products/services offered by the same bank

brand in near future.

Table 8(B): Chi-Square Tests: (Purchase Intention for Future Products/Services and

TRIALABILITY LEVEL)

Value df Asymp. Sig. (2-sided)

Pearson Chi-Square 187.768a 32 0

Likelihood Ratio 178.09 32 0

Linear-by-Linear Association 63.402 1 0

N of Valid Cases 1050

Looking at the chi-square significance of 0.000 (Table 8(B)), we can conclude that the relationship

between the Trialability Level of a bank brand and the customer satisfaction with the same bank brand

is significant.

Table 8(C): Directional Measures (Purchase Intention for Future Products/Services and

TRIALABILITY LEVEL)

Lambda Value Asymp. Std.

Errora

Approx. Tb Approx. Sig.

Symmetric .092 .019 4.675 .000

Future Purchase Intention

Dependent

.132 .026 4.768 .000

TRIALABILITY Dependent .058 .021 2.674 .008

Looking at Table 8(C), lambda value of 0.132, we can say that 13% of the times we can predict

customers Future Purchase Intention when the Trialability Level of a Bank Brand is known. Also the

Contingency Coefficient value close to 1 shows better correlation between these two variables.

Table 8(D): Symmetric Measures (Purchase Intention for Future Products/Services and

TRIALABILITY LEVEL)

Value Asymp. Std.

Errora

Approx.

Tb

Approx.

Sig.

Nominal by

Nominal

Phi 0.423 0

Cramer's V 0.211 0

Contingency

Coefficient 0.389 0

Interval by

Interval Pearson's R 0.246 0.031 8.211 .000

c

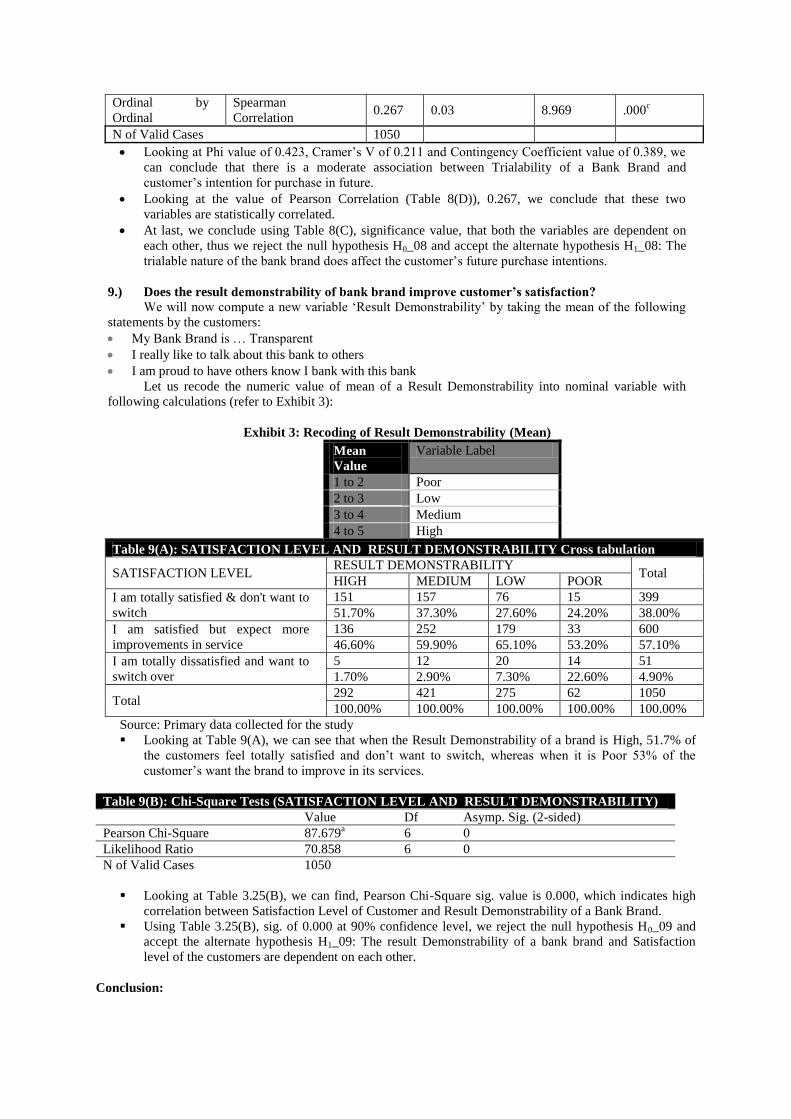

Ordinal by

Ordinal

Spearman

Correlation 0.267 0.03 8.969 .000

c

N of Valid Cases 1050

Looking at Phi value of 0.423, Cramer’s V of 0.211 and Contingency Coefficient value of 0.389, we

can conclude that there is a moderate association between Trialability of a Bank Brand and

customer’s intention for purchase in future.

Looking at the value of Pearson Correlation (Table 8(D)), 0.267, we conclude that these two

variables are statistically correlated.

At last, we conclude using Table 8(C), significance value, that both the variables are dependent on

each other, thus we reject the null hypothesis H0_08 and accept the alternate hypothesis H1_08: The

trialable nature of the bank brand does affect the customer’s future purchase intentions.

9.) Does the result demonstrability of bank brand improve customer’s satisfaction?

We will now compute a new variable ‘Result Demonstrability’ by taking the mean of the following

statements by the customers:

My Bank Brand is … Transparent

I really like to talk about this bank to others

I am proud to have others know I bank with this bank

Let us recode the numeric value of mean of a Result Demonstrability into nominal variable with

following calculations (refer to Exhibit 3):

Exhibit 3: Recoding of Result Demonstrability (Mean)

Mean

Value

Variable Label

1 to 2 Poor

2 to 3 Low

3 to 4 Medium

4 to 5 High

Table 9(A): SATISFACTION LEVEL AND RESULT DEMONSTRABILITY Cross tabulation

SATISFACTION LEVEL RESULT DEMONSTRABILITY

Total HIGH MEDIUM LOW POOR

I am totally satisfied & don't want to

switch

151 157 76 15 399

51.70% 37.30% 27.60% 24.20% 38.00%

I am satisfied but expect more

improvements in service

136 252 179 33 600

46.60% 59.90% 65.10% 53.20% 57.10%

I am totally dissatisfied and want to

switch over

5 12 20 14 51

1.70% 2.90% 7.30% 22.60% 4.90%

Total 292 421 275 62 1050

100.00% 100.00% 100.00% 100.00% 100.00%

Source: Primary data collected for the study

Looking at Table 9(A), we can see that when the Result Demonstrability of a brand is High, 51.7% of

the customers feel totally satisfied and don’t want to switch, whereas when it is Poor 53% of the

customer’s want the brand to improve in its services.

Table 9(B): Chi-Square Tests (SATISFACTION LEVEL AND RESULT DEMONSTRABILITY)

Value Df Asymp. Sig. (2-sided)

Pearson Chi-Square 87.679a 6 0

Likelihood Ratio 70.858 6 0

N of Valid Cases 1050

Looking at Table 3.25(B), we can find, Pearson Chi-Square sig. value is 0.000, which indicates high

correlation between Satisfaction Level of Customer and Result Demonstrability of a Bank Brand.

Using Table 3.25(B), sig. of 0.000 at 90% confidence level, we reject the null hypothesis H0_09 and

accept the alternate hypothesis H1_09: The result Demonstrability of a bank brand and Satisfaction

level of the customers are dependent on each other.

Conclusion:

Looking at the data analysis, we can conclude that dimensions like Brand Equity Factors (Brand

Loyalty, Brand Awareness, Perceived Quality, Brand Association) and Attitude Factors (Relative Advantage,

Compatibility, Complexity, Trialability, Result Demonstrability) plays an import role in the adoption of bank

brands in retail banking. Hence bank marketers shall focus more and more on these two dimensions while

designing their marketing strategies. Markets can follow the conceptual model of this study to design their

marketing strategies for retail banking customers (Refer Figure 1: Conceptual Framework of Brand Adoption

in Retail banking).The bank markers can focus on each of the instrument separately and shall draw their

market offering to satisfy these instruments separately. Say for example AXIS bank offers priority banking

services to those customers who maintain an average quarterly balance of 100000 Rs. and provides them

separate and unique facilities such as home banking solutions, separate customer help desk for priority

customers, etc. The banks shall try to improve on the attitude factors such as complexity and Trialability of

their banking products. Say for example banks can create simple processes to open an account or to open a

fixed deposits account, etc. off course banks cannot provide trial facilities looking at the nature of the product

but they can provide free demonstration of their internet banking, mobile banking and phone banking services

on Saturday and Sundays after banking hours in order to improve the Trialability of these services among

consumers of banks.

The academic implications of the study are still need to be proved by working on the validity of the

model by future research. The future researchers can use this model to test the validity of the same model on

other related services industry such as Airlines, Hotels, Hospitals, Insurance, Tourism, etc.

References:

1. Aaker David A (1991), Managing Brand Equity, Free Press, New York

2. Aaker David (2000), Brand Leadership, The Free Press, New York.

3. Aaker David A and Keller Kevin L (1993), “Interpreting Cross-Cultural Replications of Brand

Extension Research”, International Journal of Research in Marketing, Vol. 10, No. 1, pp. 55-59.

4. Agarwal R and Prasad J (1998), “A Conceptual and Operational Definition of Personal

Innovativeness in the Domain of Information Technology”, Information Systems Research, Vol. 9,

No. 2, pp. 204-215.

5. Auken Van (2007), Branding, Jaico Publishing House, Mumbai.

6. Balaji M and Supriya M (2006), "Understanding Corporate Brands and Corporate Branding",

Marketing Mastermind, Dec., India.

7. Cooper R B and Zmud R W (1990), “Information Technology Implementation Research: A

Technological Diffusion Approach ”, Management Science, Vol. 36, No. 2, pp. 123-39.

8. Day George S, Shocker Allan D and Srivastava Rajendra (1979), “Customer-Oriented Approaches

to Identify Product Markets”, Journal of Marketing, Vol. 43, May, pp. 8-19.

9. Fishbein M and Ajzen I (1975), Belief, Attitude, Intention and Behavior: An Introduction to

Theory and Research, Addison-Wesley, New York.

10. Gregor S and Jones K (1999), “Beef Selling Online: Diffusion Theory Applied”, Information

Technology and People, Vo. 12, No.1, pp. 71-85.

11. Keller Kevin (2004), “Building, Measuring, and Managing Brand Equity.” Pearson Education,

Delhi.

12. Kothari C R (2004), Research Methodology – Methods & Techniques, New Age International

Pvt. Ltd., New Delhi.

13. Kotler Phillp (2003), Marketing Management, Pearson Education, Mumbai, India.

14. Malhotra Naresh K (2004), Marketing Research, Pearson Education, Delhi.

15. Nargundkar Rajendra (2008), Marketing Research – Text and Cases, Tata McGraw-Hill,Delhi.

16. Ndubisi N O and Chukwunonso N C (2005), “Diffusion of Landscaping services: A Two Nation

Study of Determinant Factors”, Management of Environmental Quality: An International Journal,

Vol. 16, No. 4, pp. 143-154.

17. Rao Rama M (2005), Services Marketing, Pearson Education, Delhi.

18. Rogers E M (1983), Diffusion of Innovations, 3rd Ed., Free Press, New York.

19. Rogers E M (1995), Diffusion of Innovations, 4th Ed., Free Press, New York

20. Rogers E M and Shoemaker F F (1971), Communication of Innovations, Free Press, New York.

21. Rossister J R and Percy L (1987), Advertising and Promotion Management, McGraw-Hill, New

York.

22. Taylor S and Todd P (1995), “Understanding Information Technology Usage: A Test of

Competing Models”, Information Systems Research, Vol. 6, No. 2, pp. 144-176.

23. Yoo B and Donthu N (2001), “Developing and validating a Multidimensional Consumer-Based

Brand Equity Scale”, Journal of Business Research, Vol.52, No.1, pp. 1-14.

24. Wilkie W (1986), Consumer Behavior, John Wiley & Sons Inc., New York.

25. Zeithaml V A (1988), “Consumer Perceptions of Price, Quality and Value: A Means-End Model

and synthesis of Evidence”, Journal of Marketing, Vol. 52, No.7, pp. 2-22