3 t10 aes eletropaulo

TRANSCRIPT

3Q10 Results

November, 2010

• EBITDA totalized R$ 489 million, 9.8% higher than 3Q09 • Net income of R$ 289 million in 3Q10, 22.7% higher than 3Q09

• Higher energy volume compared to 3Q09: captive 2.0% and free market 16.8%

• Losses: commercial losses 100 bps lower than 3Q09• Collection rate level above 100% in 3Q10

• São Paulo Municipality Agreement: partially receipt of 2nd

installment in the amount of R$ 37.5 million

• Positive tariff readjustment index of 8,00% to 2010/2011 cycle, with an average effect of 1,62% to the consumers

• Public hearing due to discuss third tariff review cycle methodology on going

FinancialFinancial

OperationalOperational

One-off effectOne-off effect

RegulatoryRegulatory

3

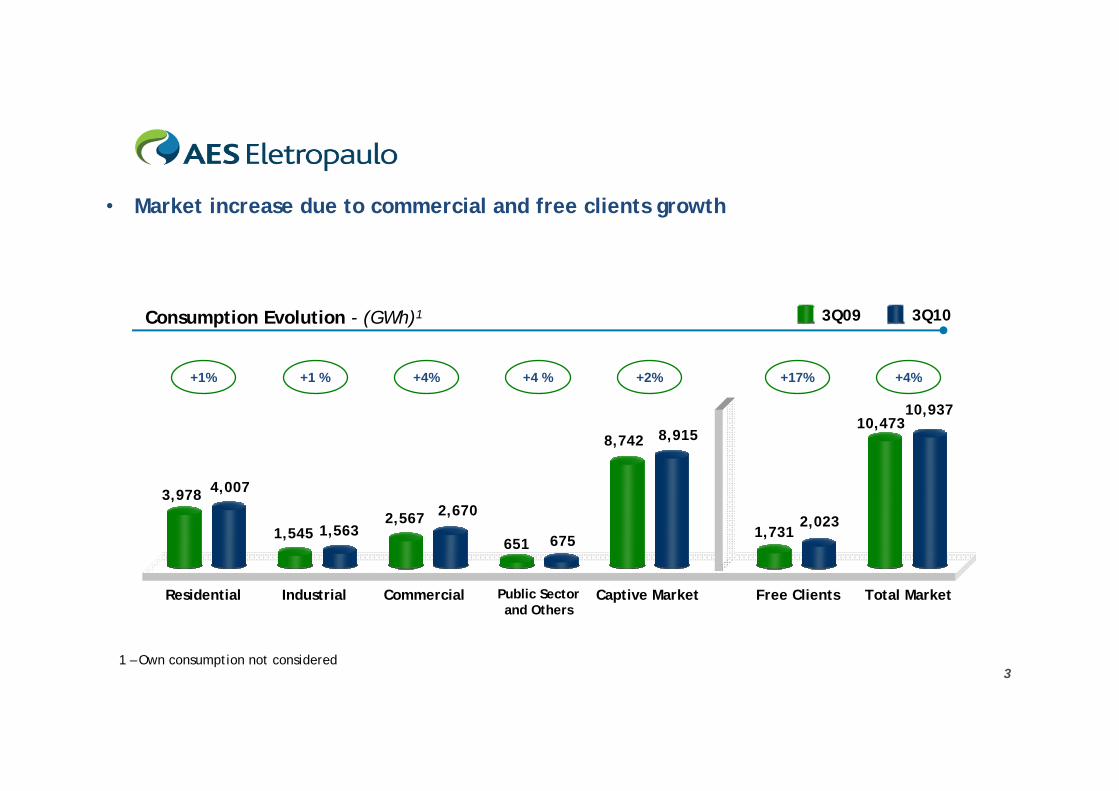

Consumption Evolution - (GWh)1 3Q103Q09

• Market increase due to commercial and free clients growth

Free Clients

1,7312,023

Captive Market

8,742 8,915

Residential Industrial Commercial Public Sector and Others

Total Market

651

2,5671,545

3,978

10,473

675

4,007

1,5632,670

10,937

+1% +4% +4 % +2% +4%+1 % +17%

1 – Own consumption not considered

4

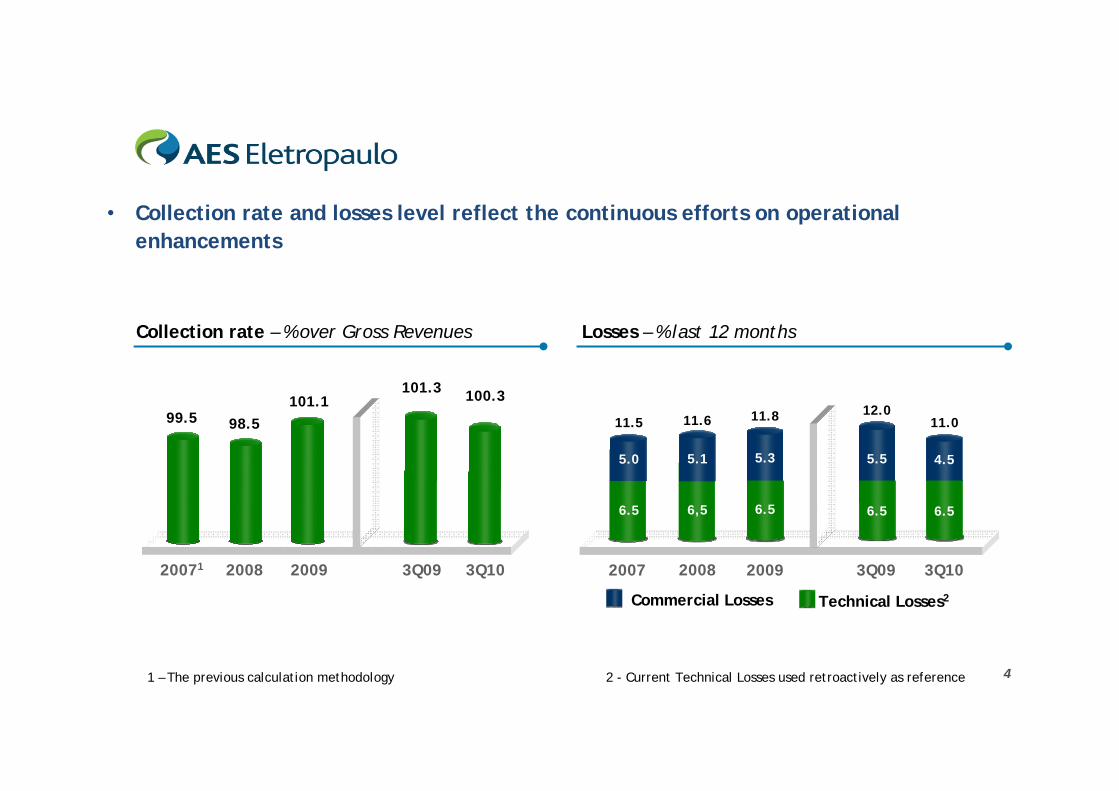

98.5

20092008 3Q09

100.3

3Q10

101.3101.1

99.5

20071 2008

5.1

6,5

11.6

3Q10

4.5

6.5

11.0

3Q09

6.5

5.5

12.0

2007

5.0

6.5

11.5

5.0

6.5

2009

5.3

6.5

11.8

6.5

5.3

6.5

Collection rate – % over Gross Revenues Losses – % last 12 months

1 – The previous calculation methodology 2 - Current Technical Losses used retroactively as reference

Commercial Losses Technical Losses2

• Collection rate and losses level reflect the continuous efforts on operational enhancements

5

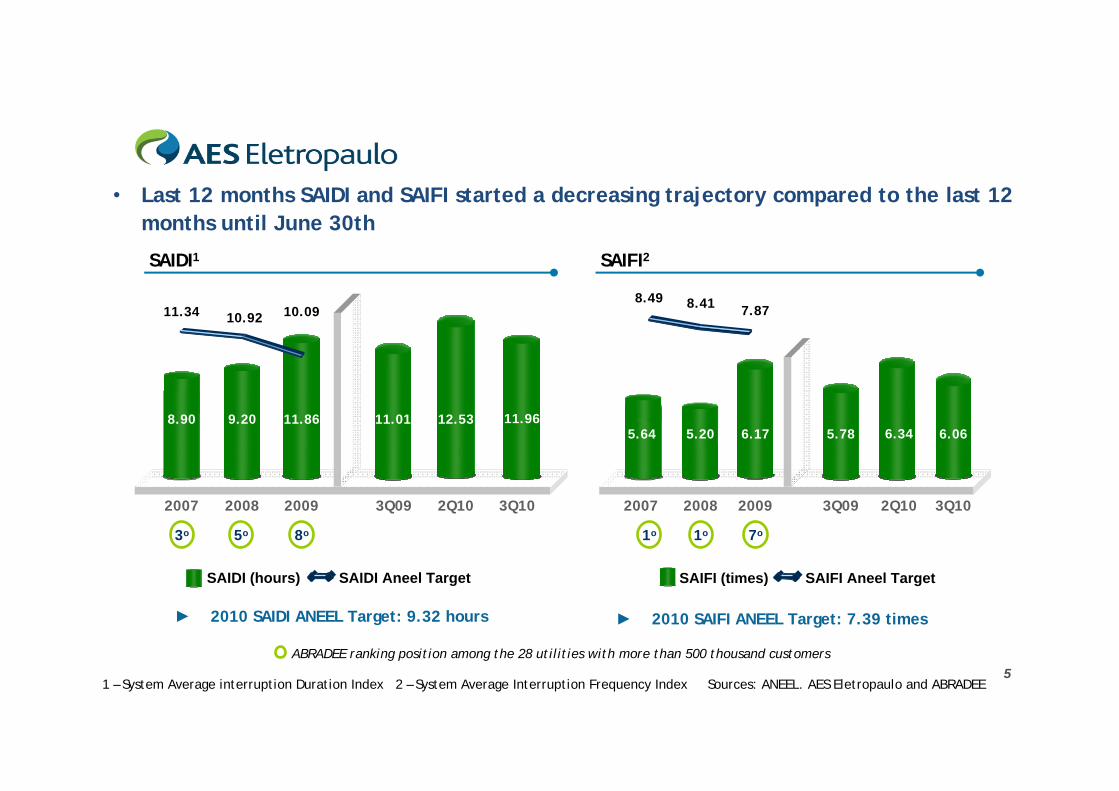

• Last 12 months SAIDI and SAIFI started a decreasing trajectory compared to the last 12 months until June 30th

SAIFI2SAIDI1

1 – System Average interruption Duration Index 2 – System Average Interruption Frequency Index Sources: ANEEL. AES Eletropaulo and ABRADEE

ABRADEE ranking position among the 28 utilities with more than 500 thousand customers

► 2010 SAIDI ANEEL Target: 9.32 hours ► 2010 SAIFI ANEEL Target: 7.39 times

SAIDI (hours) SAIDI Aneel Target SAIFI (times) SAIFI Aneel Target

9.208.90

2007 2008 3Q10

11.34 10.92

2009

3o

3Q09

5o

11.86

10.09

11.01

8o

2Q10

11,9611.96

2007 2009 3Q09

7.878.49 8.41

3Q10

1o

5.64 5.78

2008

6.17 6,736.06

1o 7o

5.20

2Q10

12.536.34

6

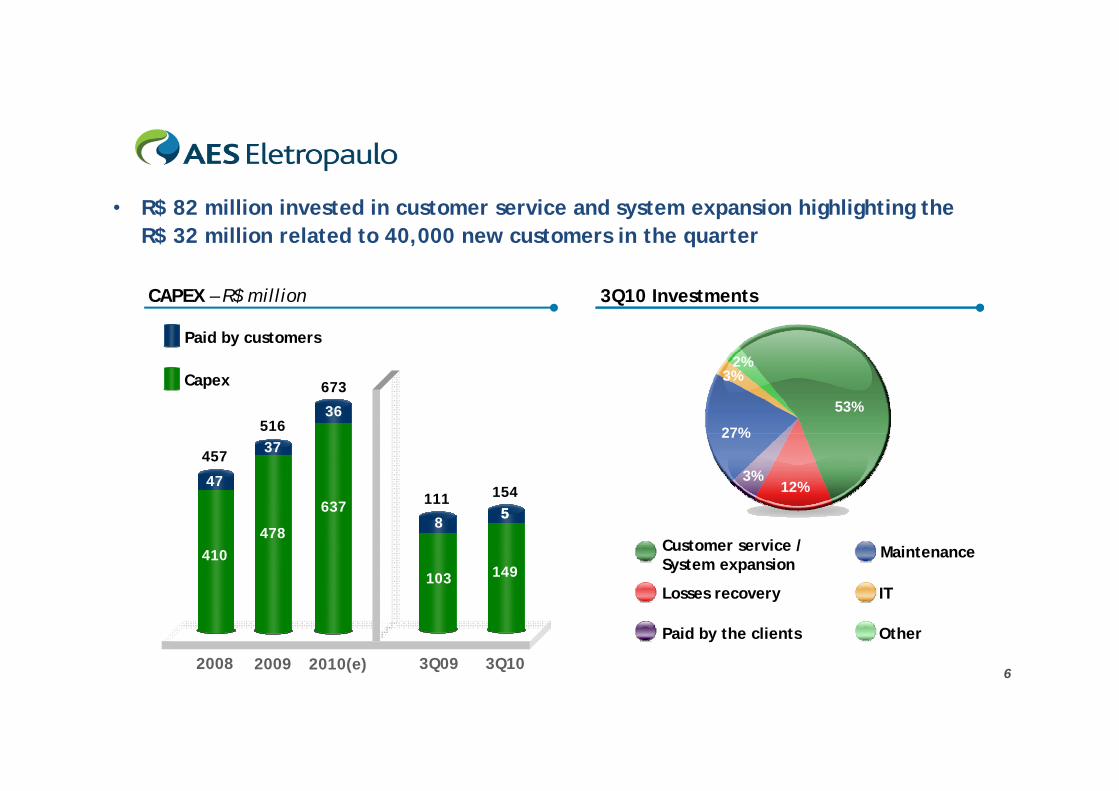

3Q10 Investments

2008

103

111

8

3Q09

149

1545

3Q102009 2010(e)

• R$ 82 million invested in customer service and system expansion highlighting the R$ 32 million related to 40,000 new customers in the quarter

410

457

47

516

478

37

637

36

673

CAPEX – R$ million

Paid by customers

Capex

Customer service / System expansion

Paid by the clients

Losses recovery

Maintenance

IT

Other

5

12%

27%

53%

3%

3%2%

7

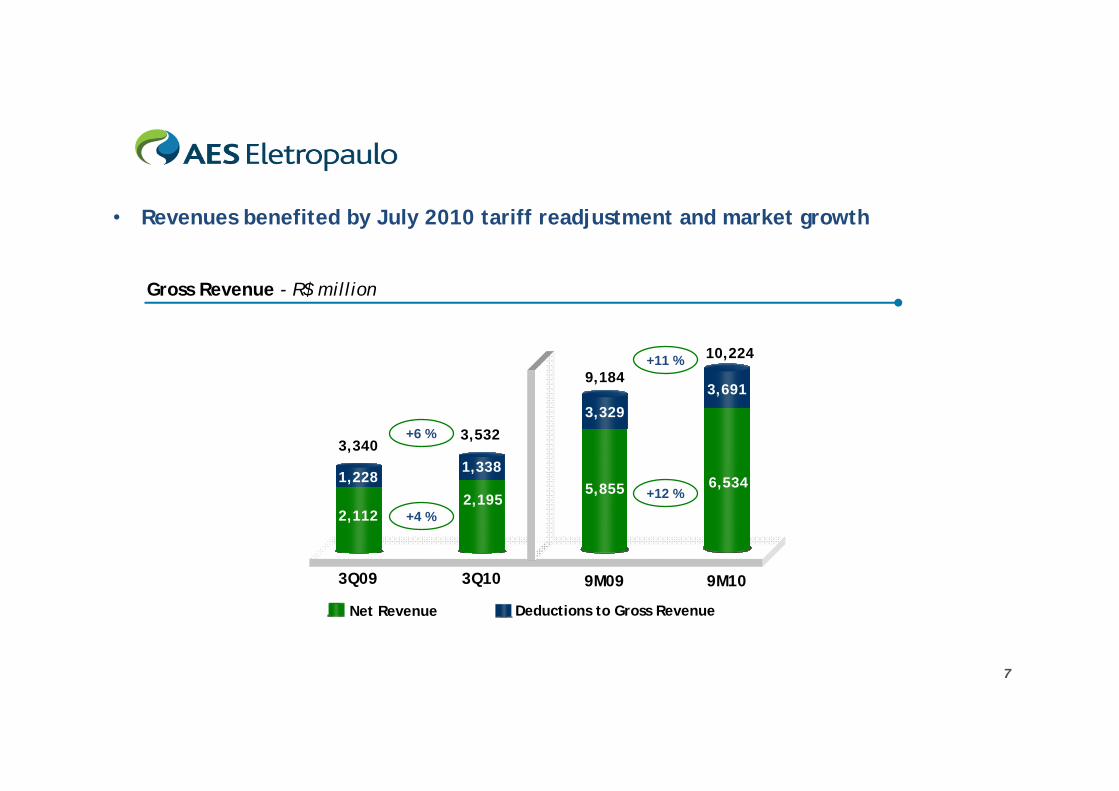

• Revenues benefited by July 2010 tariff readjustment and market growth

Gross Revenue - R$ million

3Q09 3Q10

1,228

2,112

3,3401,338

2,195

3,532+6 %

+4 %

9M09 9M10

3,329

5,855

9,1843,691

6,534

10,224+11 %

+12 %

Deductions to Gross RevenueNet Revenue

8

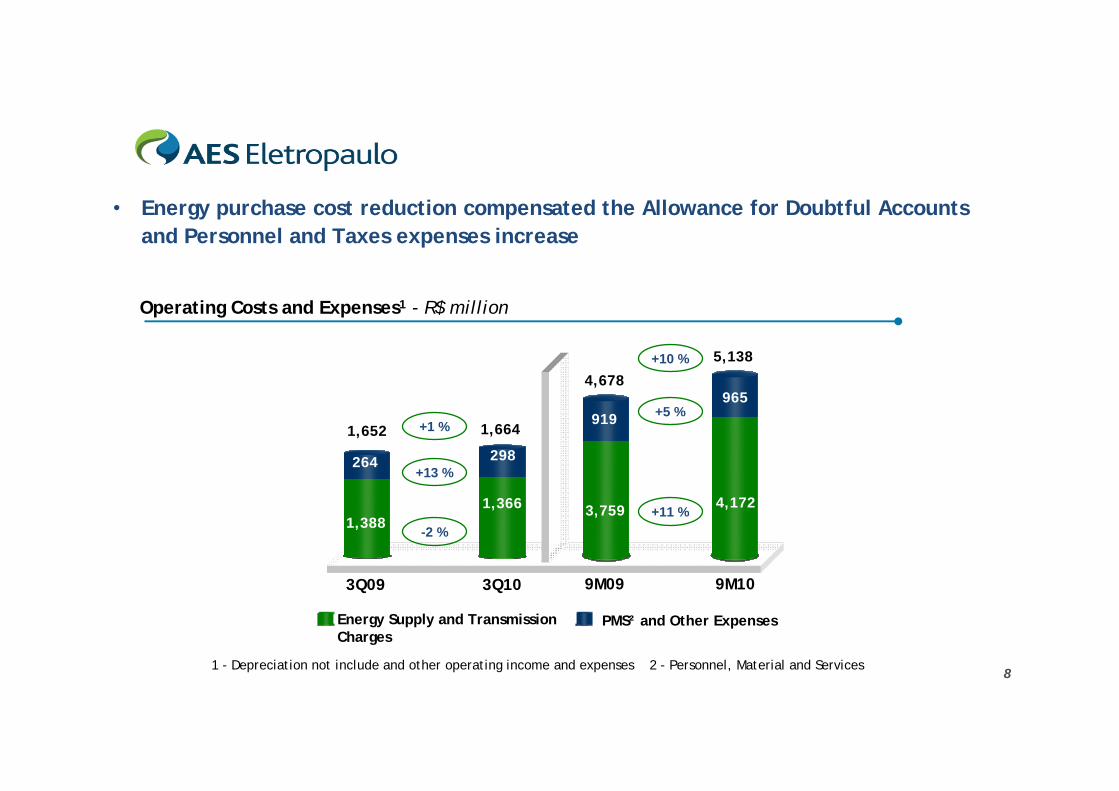

• Energy purchase cost reduction compensated the Allowance for Doubtful Accounts and Personnel and Taxes expenses increase

Operating Costs and Expenses1 - R$ million

3Q09 3Q10

264

1,388

1,652

298

1,366

1,664+1 %

+13 %

-2 %

9M09 9M10

919

3,759

4,678965

4,172

5,138+10 %

+5 %

+11 %

PMS² and Other ExpensesEnergy Supply and Transmission Charges

1 - Depreciation not include and other operating income and expenses 2 - Personnel, Material and Services

9

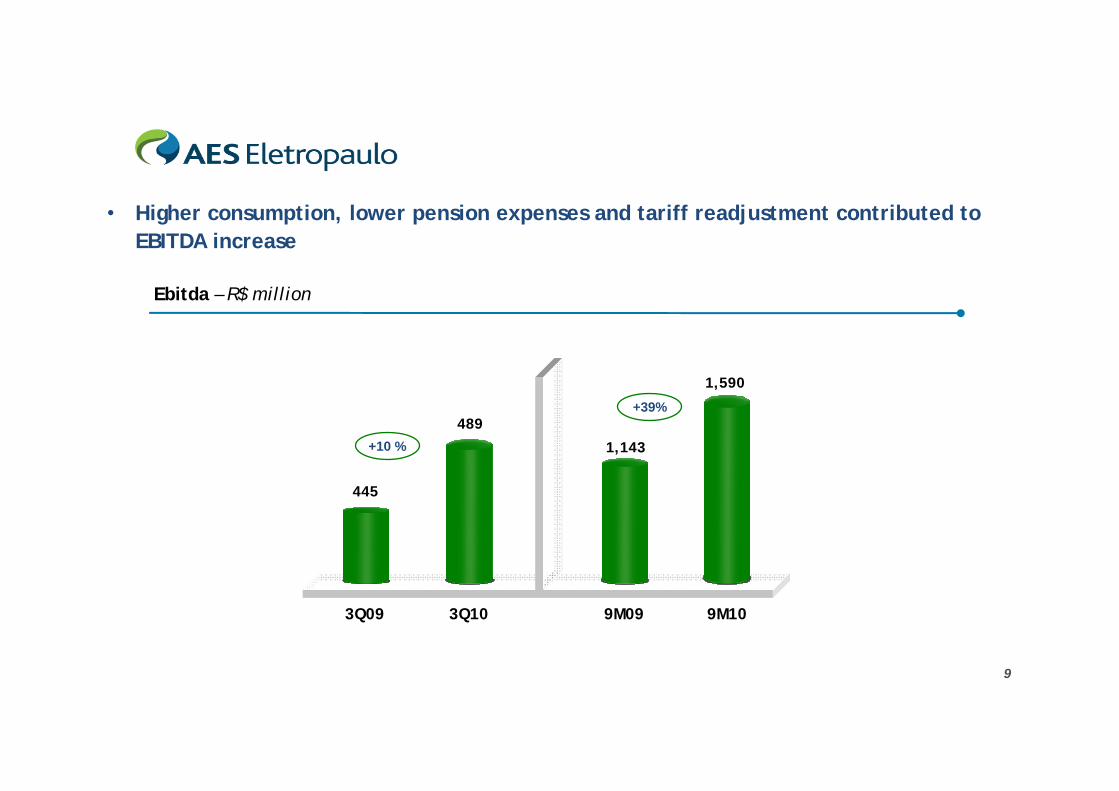

• Higher consumption, lower pension expenses and tariff readjustment contributed to EBITDA increase

3Q09 3Q10

+10 %

9M09 9M10

+39%

445

489

1,143

1,590

Ebitda – R$ million

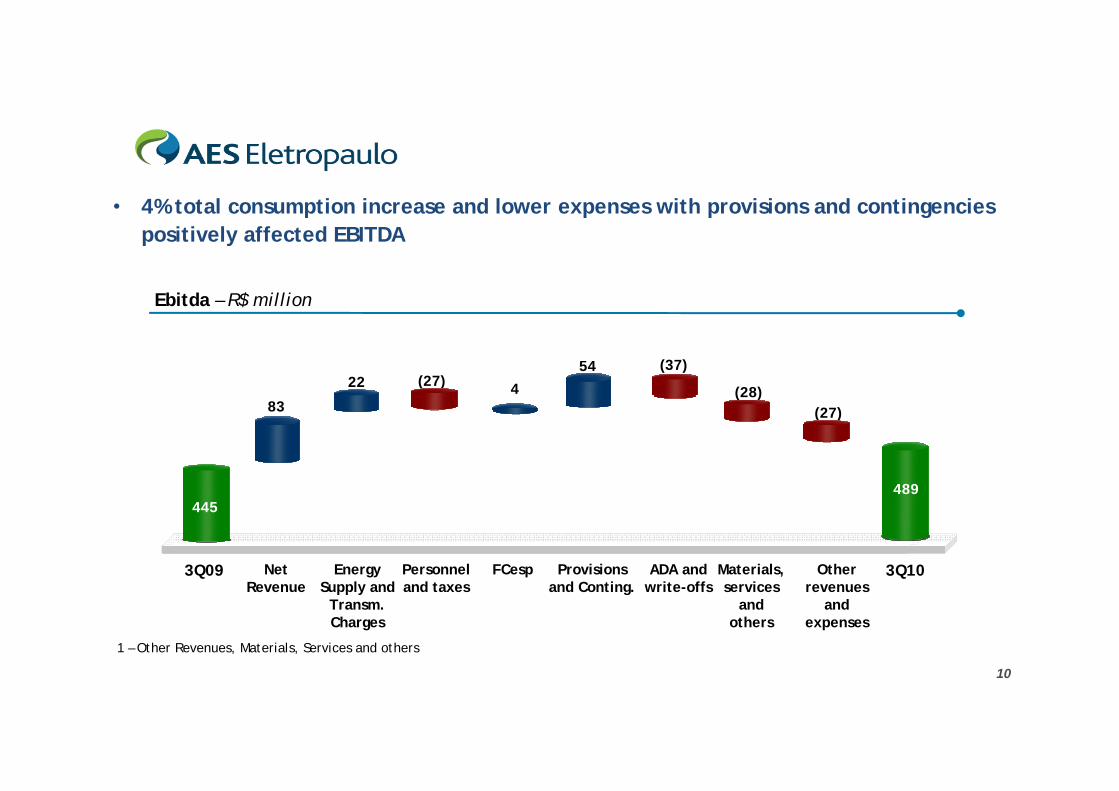

10

3Q103Q09

• 4% total consumption increase and lower expenses with provisions and contingencies positively affected EBITDA

Ebitda – R$ million

1 – Other Revenues, Materials, Services and others

Other revenues

and expenses

FCespNetRevenue

Energy Supply and

Transm. Charges

Personnel and taxes

ADA andwrite-offs

Materials, services

and others

489

83

445

4

54 (37)22 (27)

(28)(27)

Provisions and Conting.

11

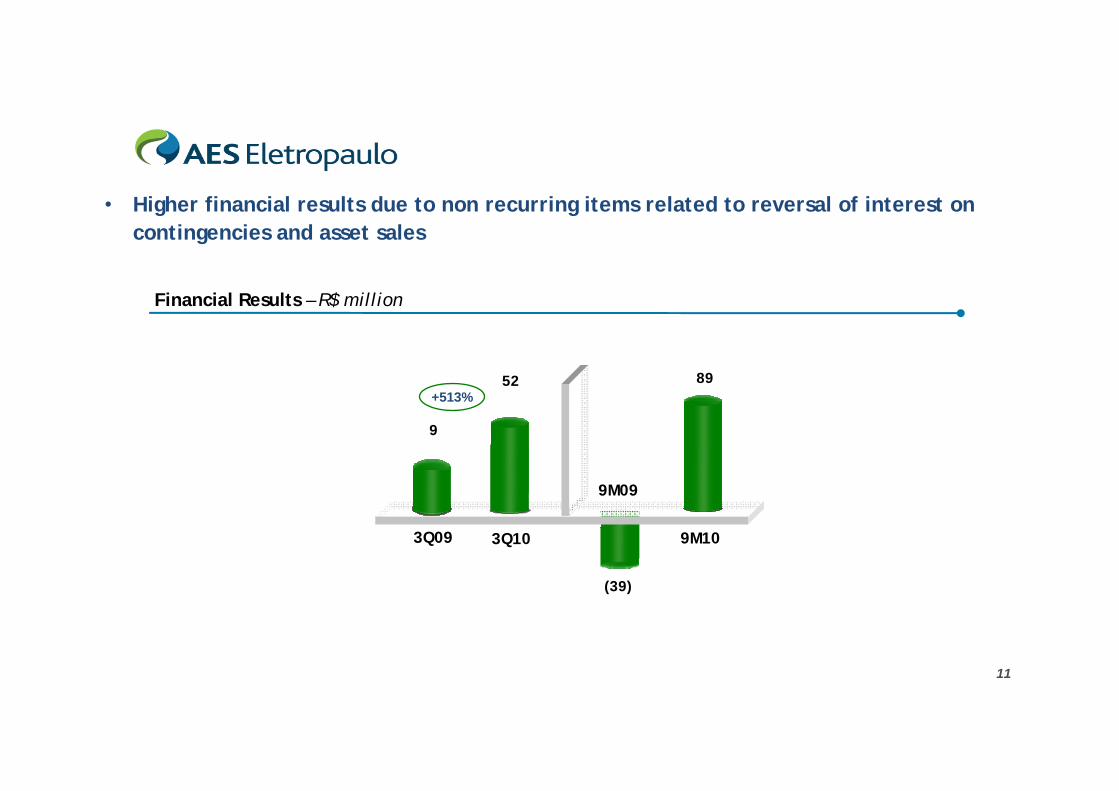

3Q10

• Higher financial results due to non recurring items related to reversal of interest on contingencies and asset sales

52

(39)

89

9M09

9M10

9

3Q09

+513%

Financial Results – R$ million

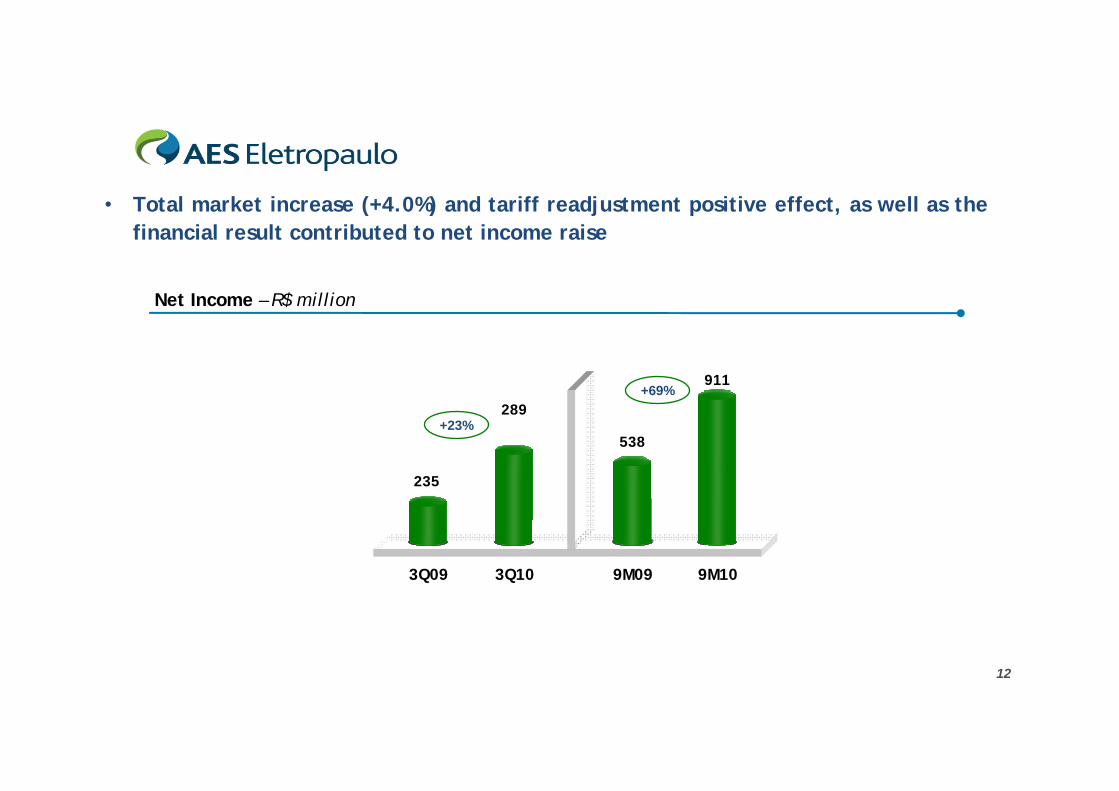

12

3Q09 3Q10

+23%289

• Total market increase (+4.0%) and tariff readjustment positive effect, as well as the financial result contributed to net income raise

9M09

538

9M10

911+69%

235

Net Income – R$ million

13

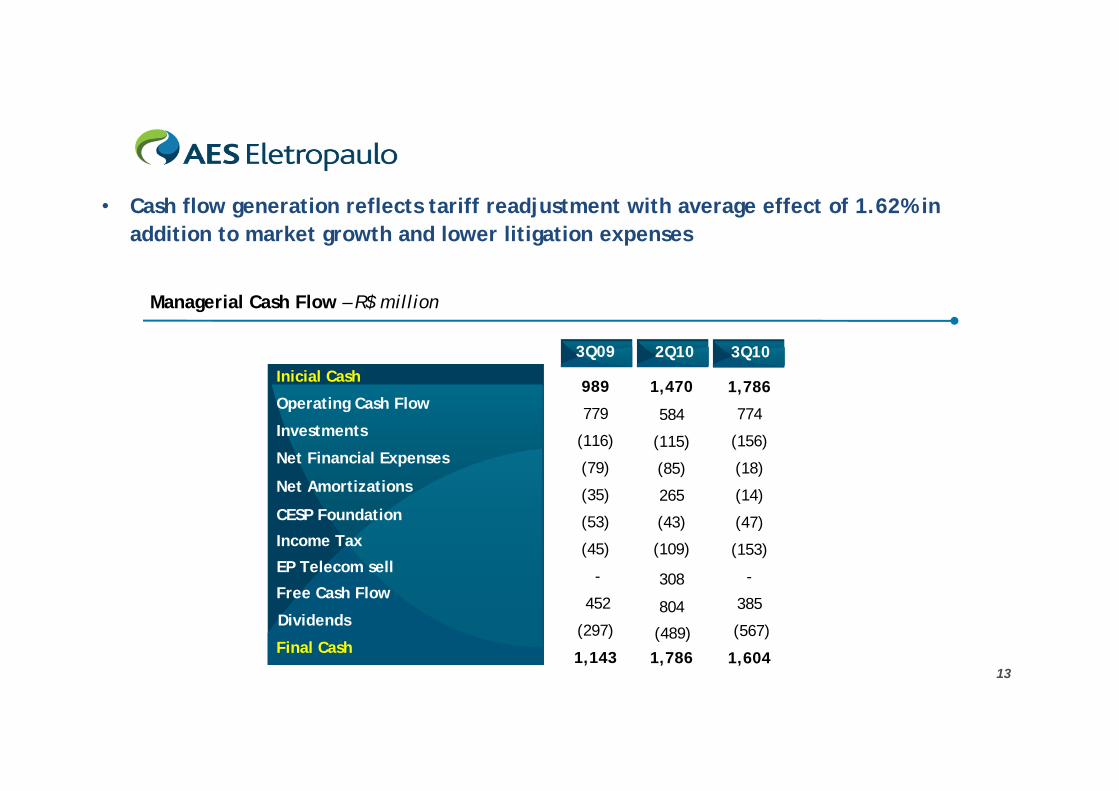

• Cash flow generation reflects tariff readjustment with average effect of 1.62% in addition to market growth and lower litigation expenses

3Q09

989

779

(116)

(79)

(35)

(53)

(45)

452

1,143

(297)

3Q10

-

2Q10

1,470

584

(115)

(85)

265

(43)

(109)

804

1,786(489)

308

Managerial Cash Flow – R$ million

Inicial Cash

Operating Cash Flow

Investments

Net Financial Expenses

Net Amortizations

CESP Foundation

Income Tax

Dividends

Free Cash Flow

Final Cash

EP Telecom sell

1,786

774

(156)

(18)

(14)

(47)

(153)

385

1,604

(567)

-

14

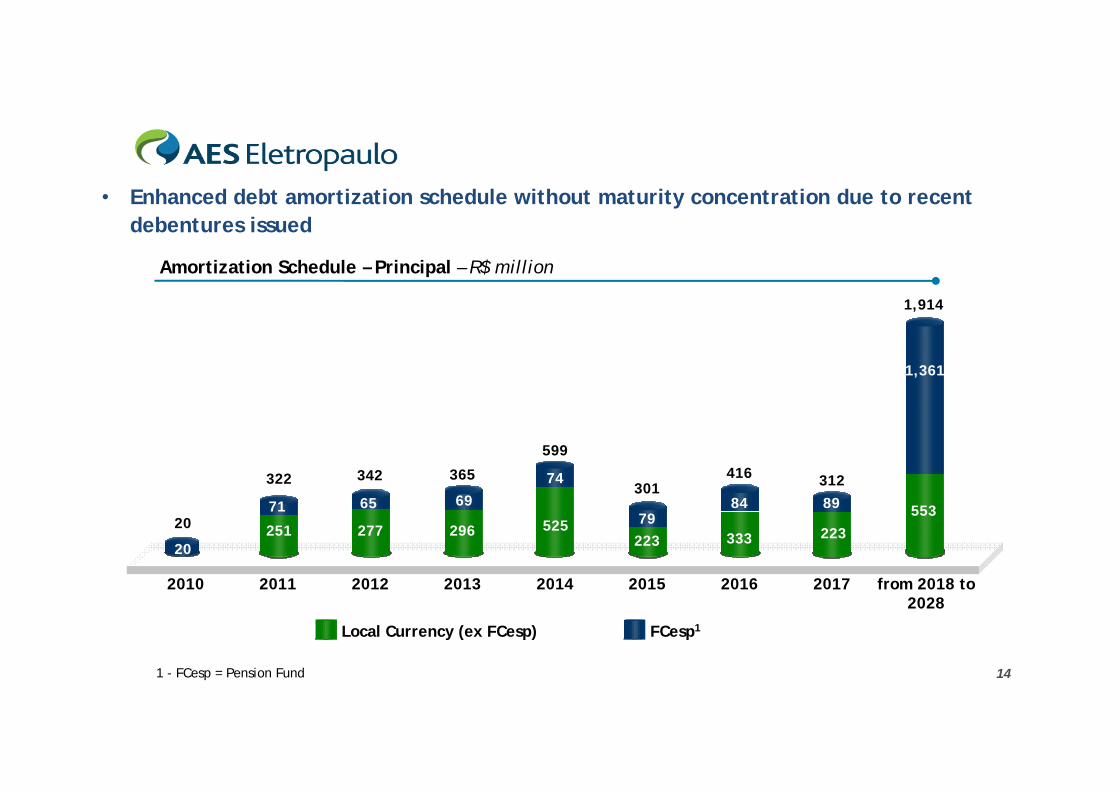

• Enhanced debt amortization schedule without maturity concentration due to recent debentures issued

Amortization Schedule – Principal – R$ million

Local Currency (ex FCesp) FCesp1

2010 2011 2012 2013 2014 2015 from 2018 to 2028

20172016

524251 277 296 525

223

553

56

1,361

6520

322 342 365

599

301

1,914

312

333

416

71 6974

7984 89

22320

1 - FCesp = Pension Fund

15

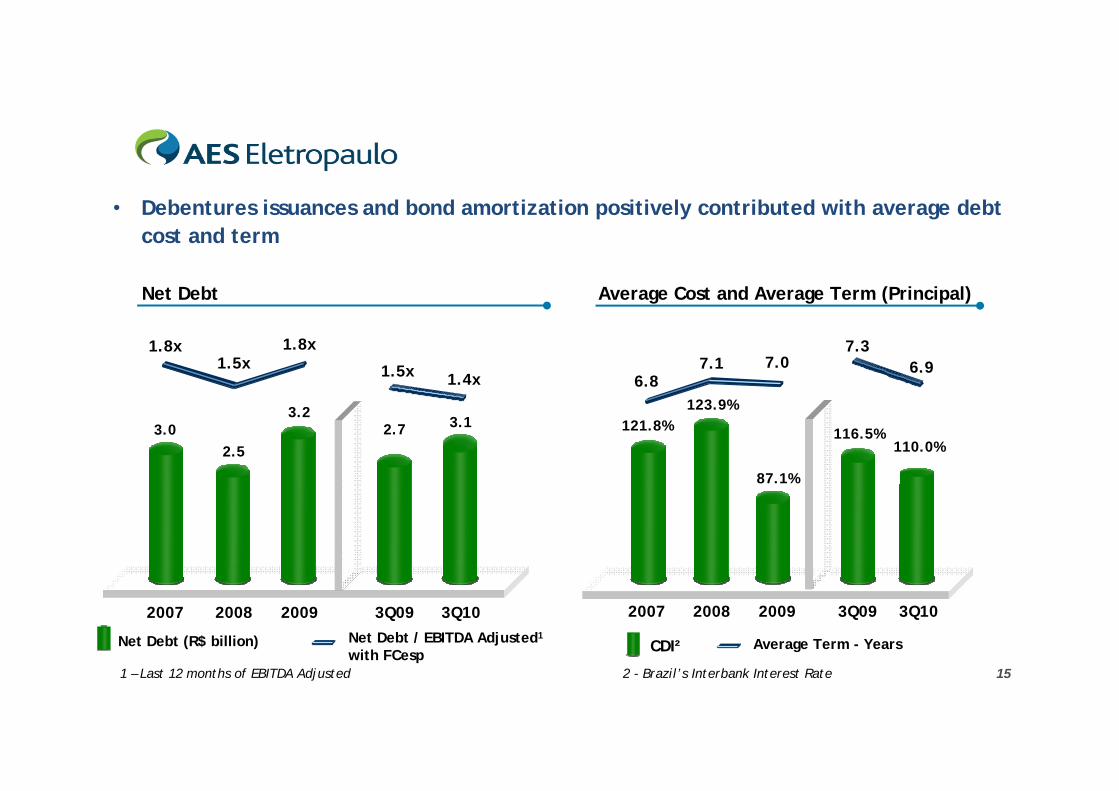

• Debentures issuances and bond amortization positively contributed with average debt cost and term

2007

3.0

2008

2.5

1.8x1.5x

1.8x

3.1

1.5x

3Q10

2.7

3Q09

1.4x

2009

3.2

6.87.1 7.0 6.9

2007

121.8%

2008

123.9%

3Q10

110.0%

3Q09

116.5%

2009

87.1%

7.3

Net Debt Average Cost and Average Term (Principal)

CDI² Average Term - YearsNet Debt (R$ billion) Net Debt / EBITDA Adjusted1

with FCesp1 – Last 12 months of EBITDA Adjusted 2 - Brazil’s Interbank Interest Rate

The statements contained in this document with regard to the business prospects, projected operating and financial results, and growth potential are merely forecasts based on the expectations of the Company’s Management in relation to its future performance.

Such estimates are highly dependent on market behavior and on the conditions affecting Brazil’s macroeconomic performance as well as the electric sector and international market, and they are therefore subject to changes.

3Q10 Results