3.1 global supply chain agile models improvement ... · pdf fileimprovement opportunities for...

TRANSCRIPT

3.1 Global Supply Chain – Agile Models

Improvement opportunities for supply chains of

Australian FMCG companies

Peter Griffiths Partner

KPMG

Introduction

Supply chain collaboration

New customer engagement models

Alternative retail distribution and fulfilment models

Peter Griffiths, Partner, KPMG 2

Traditional supply chain models are challenged by having all parties work with linear planning and replenishment processes

Traditional Approach with Information Latency and Demand Distortion

Batch Systems Siloed Supply

Chain

Skewed Demand

Signals

MFG DCs T1 Suppliers T2 Suppliers

1 Day/Hours

3 Days

Stores

Consumers

3 Days 3 Days 3 Days 3 Days

Factories

Information Lead Time & Flow Legend: Material Lead Time & Flow

DCs

7 Days 7 Days 7 Days 7 Days

Peter Griffiths, Partner, KPMG

Demand driven supply chains and the use of cloud platforms allow all participants to work as one virtual organisation as part of a common network

End to End Lead Time and Flow*

Approach Material Information

Traditional 15 days 29 days

Demand Driven 15 days 1 day

Peter Griffiths, Partner, KPMG

All participants connected in a network model with real time visibility of demand

Factories

DCs

Stores

MFG DCs

T1 Suppliers Consumers

T2 Suppliers

3 D

ays

3 Days

* Example scenario with each entity having a weekly planning process

Information Lead Time & Flow Legend:

Material Lead Time & Flow

Companies operate in a networked

fashion

Demand signal is synchronised

across all companies

Elimination of information latency

Real time visibility of changes in

demand and supply

4

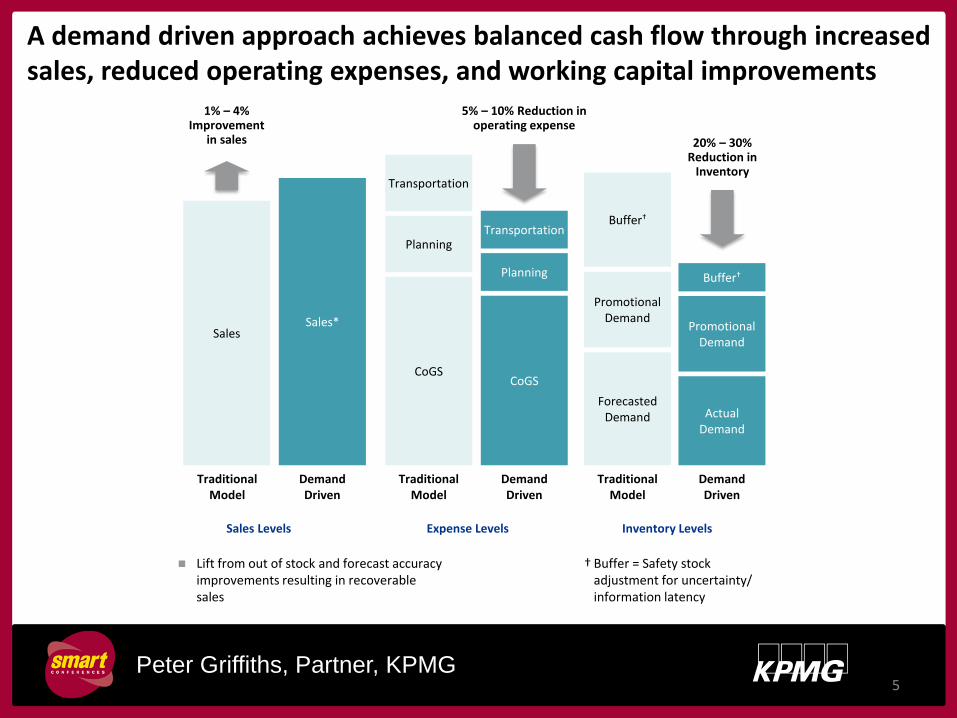

A demand driven approach achieves balanced cash flow through increased sales, reduced operating expenses, and working capital improvements

Lift from out of stock and forecast accuracy improvements resulting in recoverable sales

† Buffer = Safety stock adjustment for uncertainty/ information latency

Sales

1% – 4% Improvement

in sales

Sales*

Traditional Model

Demand Driven

Sales Levels

CoGS

Planning

Transportation

5% – 10% Reduction in operating expense

CoGS

Planning

Transportation

Traditional Model

Demand Driven

Expense Levels

Forecasted Demand

Promotional Demand

Buffer†

20% – 30% Reduction in

Inventory

Actual Demand

Promotional Demand

Buffer†

Traditional Model

Demand Driven

Inventory Levels

5 Peter Griffiths, Partner, KPMG

Peter Griffiths, Partner, KPMG

Upstream and downstream benefits of collaboration in supply chains

U

pst

ream

Do

wn

stream

Reduced inventory holdings Lower cost of ownership Improved asset utilisation Optimised distribution Improved supply chain

responsiveness

Improved customer service Lower cost to serve Quicker time to market Lower store inventories Improved responsiveness

6

Collaboration Arrangement

Joint Business

Plan

Sales Forecasting

Order Planning /

Forecasting

Order Generation

Order Fulfilment

Exception Management

Performance Assessment

Consumer

Introduction

Supply chain collaboration

New customer engagement models

Alternative retail distribution and fulfilment models

Peter Griffiths, Partner, KPMG 7

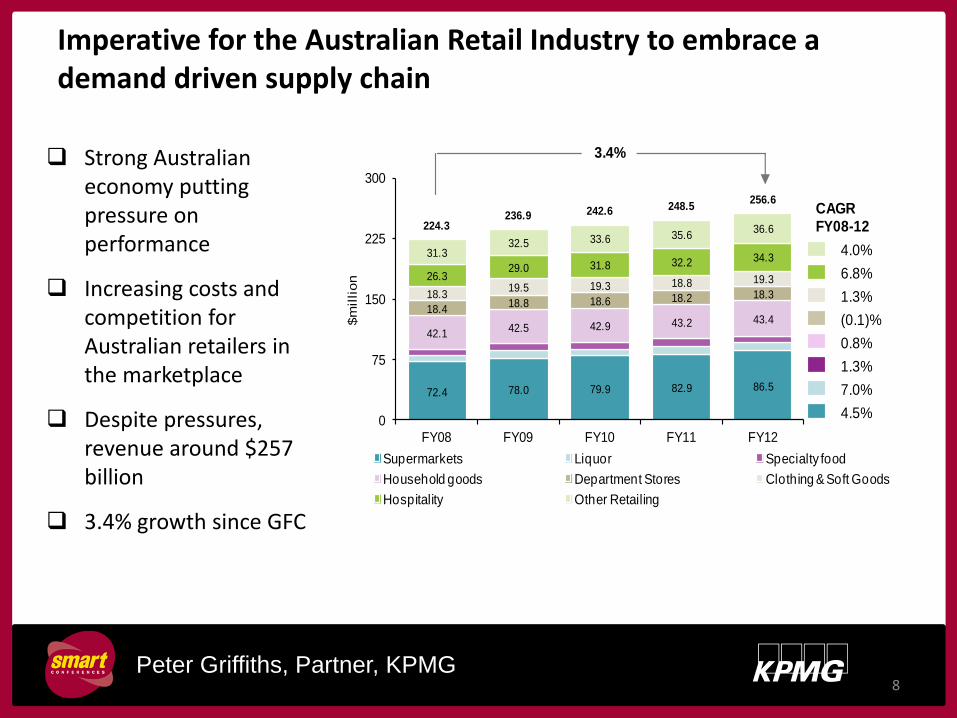

Imperative for the Australian Retail Industry to embrace a demand driven supply chain

3.4%

CAGRFY08-12

4.0%

6.8%

1.3%

(0.1)%

0.8%

1.3%

7.0%

4.5%

72.4 78.0 79.9 82.9 86.5

42.142.5 42.9 43.2 43.4

18.418.8 18.6 18.2 18.318.319.5 19.3 18.8 19.326.329.0 31.8 32.2 34.331.332.5 33.6 35.6

36.6224.3236.9 242.6 248.5

256.6

0

75

150

225

300

FY08 FY09 FY10 FY11 FY12

$m

illion

Supermarkets Liquor Specialty food

Household goods Department Stores Clothing & Soft Goods

Hospitality Other Retailing

Strong Australian economy putting pressure on performance

Increasing costs and competition for Australian retailers in the marketplace

Despite pressures, revenue around $257 billion

3.4% growth since GFC

Peter Griffiths, Partner, KPMG 8

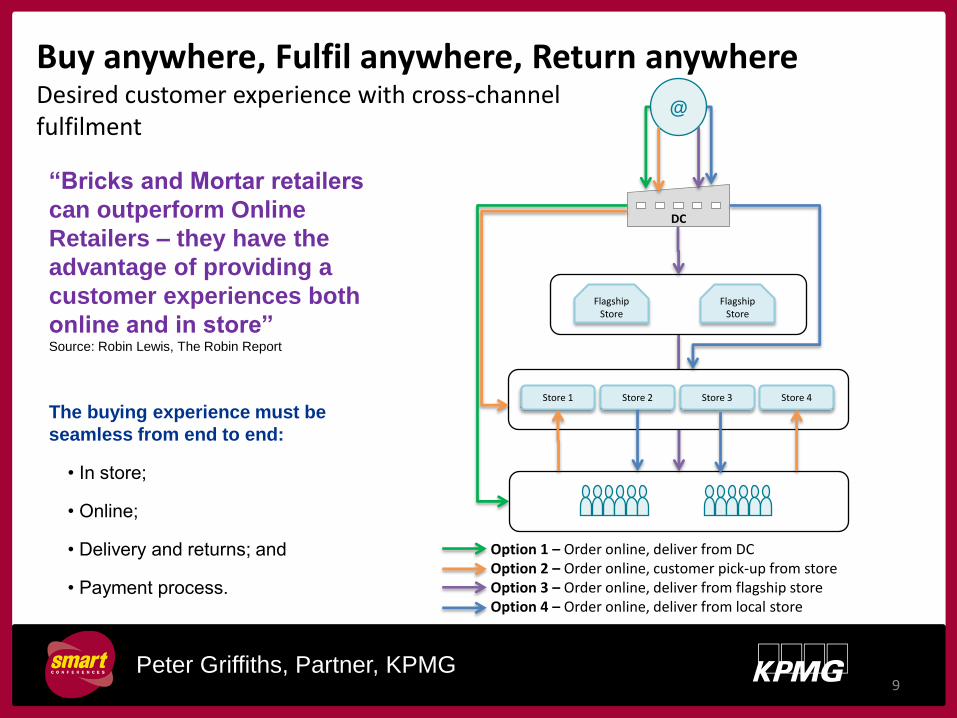

“Bricks and Mortar retailers

can outperform Online

Retailers – they have the

advantage of providing a

customer experiences both

online and in store” Source: Robin Lewis, The Robin Report

The buying experience must be

seamless from end to end:

• In store;

• Online;

• Delivery and returns; and

• Payment process.

@

DC

Flagship Store

Flagship Store

Store 1 Store 2 Store 3 Store 4

Option 1 – Order online, deliver from DC Option 2 – Order online, customer pick-up from store Option 3 – Order online, deliver from flagship store Option 4 – Order online, deliver from local store

Buy anywhere, Fulfil anywhere, Return anywhere Desired customer experience with cross-channel fulfilment

9 Peter Griffiths, Partner, KPMG

What is omni-channel?

10 Peter Griffiths, Partner, KPMG

Store Online

Multi-channel

Store Online

Omni-channel

“Separate strategies to

maximise customer sales

in each channel”

“Integrated strategies to

maximise customer

experience with the

brand”

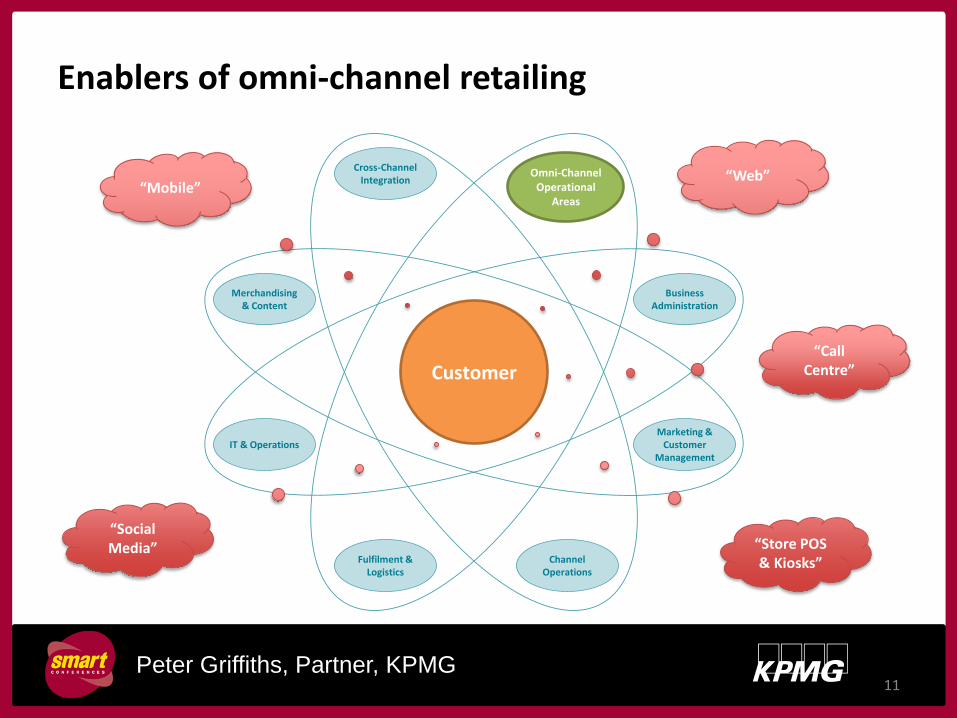

Enablers of omni-channel retailing

Peter Griffiths, Partner, KPMG

Customer

Merchandising & Content

Business Administration

Fulfilment & Logistics

Channel Operations

Cross-Channel Integration

Omni-Channel Operational

Areas

IT & Operations Marketing &

Customer Management

“Web”

“Call Centre”

“Store POS & Kiosks”

“Mobile”

“Social Media”

11

As retailers offerings become more mature their omni-channel strategy needs to evolve

Peter Griffiths, Partner, KPMG

Stage 2

Align

Fundamentals

Sync your basic

value propositions

Stage 3

Achieve

Proficiency

Focus on customer

facing processes

and adept in

foundational

activities

Stage 1

Create

Presence

Get new

channels up

and running

Stage 5

Optimise

Operating

Model

Established

repeatable

processes and

optimisation of

resources at

organisational level

Drive cross-channel

collaboration and

capabilities

Stage 4

Leverage

Across

Channels

12

Introduction

Supply chain collaboration

New customer engagement models

Alternative retail distribution and fulfilment models

Peter Griffiths, Partner, KPMG 13

Peter Griffiths, Partner, KPMG

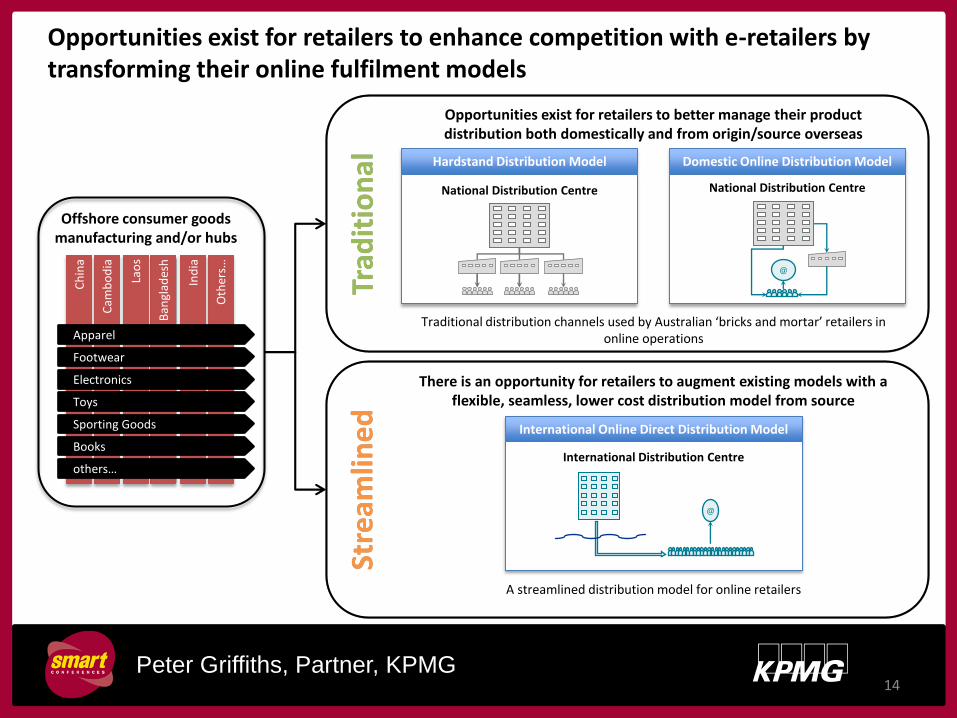

Opportunities exist for retailers to enhance competition with e-retailers by transforming their online fulfilment models

Hardstand Distribution Model

National Distribution Centre

Domestic Online Distribution Model

National Distribution Centre

@

Opportunities exist for retailers to better manage their product distribution both domestically and from origin/source overseas

Traditional distribution channels used by Australian ‘bricks and mortar’ retailers in online operations

There is an opportunity for retailers to augment existing models with a flexible, seamless, lower cost distribution model from source

A streamlined distribution model for online retailers

Cam

bo

dia

Ch

ina

Ban

glad

esh

Lao

s

Oth

ers…

Ind

ia

Apparel

Footwear

Electronics

Toys

Sporting Goods

Books

others…

Offshore consumer goods manufacturing and/or hubs

International Online Direct Distribution Model

International Distribution Centre

@

Trad

itio

nal

St

ream

line

d

14

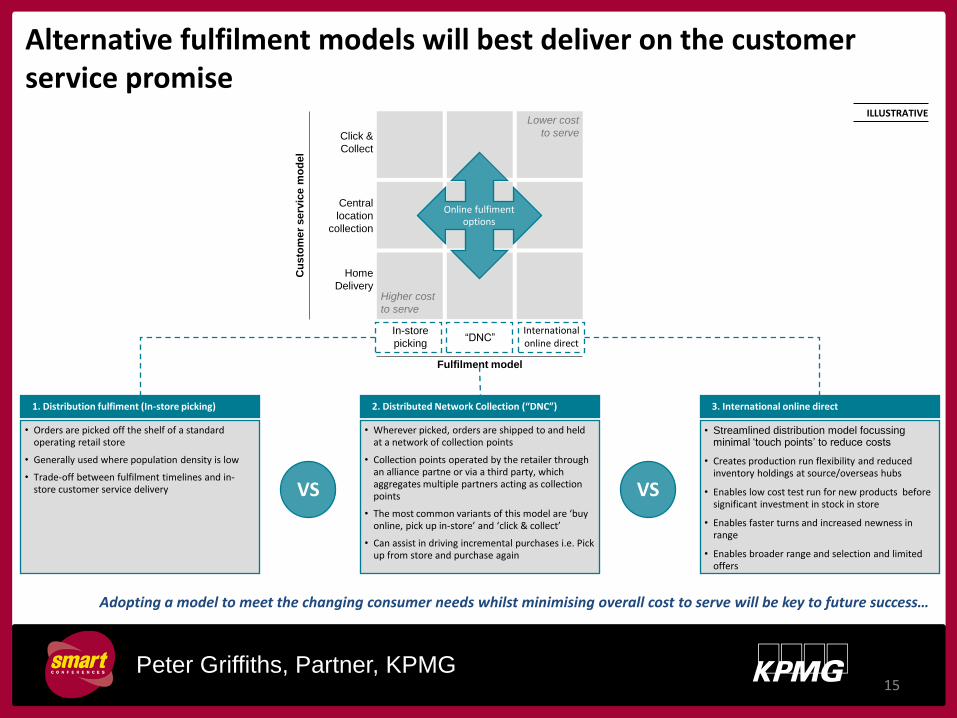

Alternative fulfilment models will best deliver on the customer service promise

Peter Griffiths, Partner, KPMG

Click &

Collect

Central

location

collection

Home

Delivery

Cu

sto

mer

serv

ice m

od

el

Online fulfiment options

In-store

picking “DNC”

International online direct

Fulfilment model

Higher cost

to serve

Lower cost

to serve

1. Distribution fulfiment (In-store picking) 2. Distributed Network Collection (“DNC”) 3. International online direct

• Orders are picked off the shelf of a standard operating retail store

• Generally used where population density is low

• Trade-off between fulfilment timelines and in-store customer service delivery

• Wherever picked, orders are shipped to and held at a network of collection points

• Collection points operated by the retailer through an alliance partne or via a third party, which aggregates multiple partners acting as collection points

• The most common variants of this model are ‘buy online, pick up in-store’ and ‘click & collect’

• Can assist in driving incremental purchases i.e. Pick up from store and purchase again

• Streamlined distribution model focussing minimal ‘touch points’ to reduce costs

• Creates production run flexibility and reduced inventory holdings at source/overseas hubs

• Enables low cost test run for new products before significant investment in stock in store

• Enables faster turns and increased newness in range

• Enables broader range and selection and limited offers

VS VS

ILLUSTRATIVE

Adopting a model to meet the changing consumer needs whilst minimising overall cost to serve will be key to future success…

15

Peter Griffiths, Partner, KPMG

Centralised

fulfilment

Supplier

Drop Ship

Distribution

fulfilment

Distribution

Network

Collection

Flexible

fulfilment

Pick & pack from centralised location

Pick & pack from stores

Original online fulfilment model

initiated by UK retailer Tesco

Orders shipped to and held at a

network of collection points regardless

of pick & pack location

Orders passed directly to supplier who

ships from a central stock location

direct to the customer

Inventory from all stores and

warehouses becomes available both

in-store and online

Warehousing, transportation, pick and

pack, order management and other

services are outsourced to a specialist

third party logistics provider

Outsourced

fulfilment

(3PL providers)

Simple, with inventory and operations

all in one place

Suits retailers with large store

networks with heavy and relatively

inexpensive products, such as grocery

Simple model including ‘buy online,

pick up in-store’ and ‘click and collect’

Drives incremental purchases i.e. Pick

up from store and purchase again

No overheads / storage costs

Suits retailers with extended range,

non-stocked items, big and bulky or

specialised merchandise

Erases lost sales stemming from

inventory being out of stock online but

available in-store

Transport costs often better than

available directly

No economic cost-cycle vulnerability or

staffing challenges

Not built for scale

Based on existing infrastructure

Can be expensive

Maintaining accurate inventory at store

level and forecasting two sets of

demand is difficult

Some convenience for consumer

compromised as still required to go to

store

Managing order allocation and

inventory availability is difficult

Often forced transport costs

Stock availability vulnerability

Requires ‘integrated’ real time

inventory management systems

Often forced transport costs

Varying degrees of technology

proliferation and transparency

Fulfilment model Description Benefits Weaknesses

16

What will these alternative fulfilment models deliver?

Peter Griffiths, Partner, KPMG

Operational blueprint in support of omni-channel strategy

Operational

Blueprint

Assess current capabilities and

infrastructure;

Develop and prioritise future

state; and

Determine capability gaps and

change strategy.

Execution

Roadmap &

Business Case

Define options and enabling projects;

Develop Business Case; and

Develop Implementation Roadmap.

Benchmarking and comparator

analysis;

Understand customers needs and

expectations;

Engage stakeholders and understand

expectations;

Define value proposition and strategic

objectives; and

Develop customer experience

scenarios.

Strategy

Definition

17

Customer Value

Alignment

Channel Design

Network Optimisation

Manufacturing Operations

Warehouse & Transport

Operations

Sourcing & Merchandise

Replenishment

Information Systems

Performance Management

Organisation Processes

STRATEGIC

TACTICAL

OPERATIONAL

SUPPORT

Summary

Cloud networking is simplifying and removing barriers to information sharing in supply chain networks

New go to market strategies emerging with omni-channel shopping

New, agile retail distribution and fulfilment models required to get product to consumers in quicker timeframes

Peter Griffiths, Partner, KPMG

Peter Griffiths

Partner

KPMG Management Consulting Tel +61 3 9288 5319 [email protected]

18

The information contained herein is of a general nature and is not intended to address the

circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough

examination of the particular situation. The views and opinions contained in the presentation / paper are those of the author and do not necessarily represent the views and

opinions of KPMG, an Australian partnership, part of the KPMG International network. The author disclaims all liability to any person or entity in respect to any consequences of

anything done, or omitted to be done.