360° insights - elliott davisnon-gaap measures. under regulation g, companies that use non-gaap...

TRANSCRIPT

Quarterly Accounting Update - Q4

What’s Inside?

Selected highlights...........FASB update.....................Regulatory update............Other developments......On the horizon...............Appendices....................

346

101422

elliottdavis.com

360° INSIGHTS

Welcome to the Fourth Quarter issue of our Quarterly Accounting Update. Each quarter, we will provide you with up-to-date information for consideration in your financial reporting and disclosures. Our goal is for you to have current, relevant information available prior to finalizing your financial reporting deliverables. This update is organized as follows:

Selected Highlights

This section includes an executive summary of selected items and/or hot topics covered in this update.

FASB Update

This section includes an overview of selected Accounting Standards Updates (ASUs) issued during the period.

Regulatory Update

This section includes an overview of selected updates, releases, rules and actions during the period that might impact financial information, operations and/or governance.

Other Developments

This section includes an overview of other developments, actions, and projects of the FASB, PCC, EITF and/or other rulemaking organizations.

On the Horizon

This section includes an overview of selected projects and exposure drafts of the FASB.

Appendices

• A – Important Implementation Dates • B – Illustrative Disclosures for Recently Issued Accounting Pronouncements • C – North Carolina Tax Rate Disclosure Example

Quarterly Accounting Update: Selected Highlights

Simplifying the Classification of Deferred Income Taxes

In November, the FASB amended its guidance on presentation of deferred tax assets and deferred tax liabilities as part of its “simplification initiative.” ASU 2015-17 amends U.S. GAAP to require that deferred tax assets and deferred tax liabilities be classified as noncurrent in a classified balance sheet.

Find out more about this change in the FASB Update section.

Crowdfunding Rules Approved

In October, the SEC issued the final version of its crowdfunding rules, finalizing the two-year old proposal from the JOBS Act. The rules tighten some investment limits, while giving first-time crowdfunding issuers a reprieve from the toughest accounting requirements.

Read more about these issues in the Regulatory Update section.

New Lease Accounting Rules to be Issued Soon

The FASB’s standard to end a decades-old practice of keeping lease costs off company balance sheets will become effective in 2019 for public companies. The closely-watched project, which has provoked much debate, will be completed and published in early 2016.

More information on these proposals can be found in the On the Horizon section.

Quarterly Accounting Update: FASB Update

The following selected Accounting Standards Updates (ASUs) were issued by the Financial Accounting Standards Board (FASB) during the fourth quarter. A complete list of all ASUs issued or effective in 2015 is included in Appendix A.

New Guidance for Recognition and Measurement of Financial Instruments

Affects: All Entities

On January 5, 2016, the FASB issued ASU 2016-01, Recognition and Measurement of Financial Assets and Financial Liabilities, to address certain aspects of recognition, measurement, presentation, and disclosure of financial instruments. The ASU affects public and private companies, not-for-profit organizations, and employee benefit plans that hold financial assets or owe financial liabilities.

The new guidance makes targeted improvements to existing U.S. generally accepted accounting principles (GAAP) by:

• Requiring equity investments (except those accounted for under the equity method of accounting, or those that result in consolidation of the investee) to be measured at fair value with changes in fair value recognized in net income

• Requiring public business entities to use the exit price notion when measuring the fair value of financial instruments for disclosure purposes

• Requiring separate presentation of financial assets and financial liabilities by measurement category and form of financial asset (i.e., securities or loans and receivables) on the balance sheet or the accompanying notes to the financial statements

• Eliminating the requirement to disclose the fair value of financial instruments measured at amortized cost for organizations that are not public business entities

• Eliminating the requirement for public business entities to disclose the method(s) and significant assumptions used to estimate the fair value that is required to be disclosed for financial instruments measured at amortized cost on the balance sheet, and

• Requiring a reporting organization to present separately in other comprehensive income the portion of the total change in the fair value of a liability resulting from a change in the instrument-specific credit risk (also referred to as “own credit”) when the organization has elected to measure the liability at fair value in accordance with the fair value option for financial instruments.

Effective Dates

For public companies the new guidance is effective for fiscal years beginning after December 15, 2017, including interim periods within those fiscal years. For private companies, not-for-profit organizations, and employee benefit plans, the guidance becomes effective for fiscal years beginning after December 15, 2018, and for interim periods within fiscal years beginning after December 15, 2019.

The ASU permits early adoption of the own credit provision (referenced above). Additionally, it permits early adoption of the provision that exempts private companies and not-for-profit organizations from having to disclose fair value information about financial instruments measured at amortized cost.

Classification of Deferred Income Taxes Simplified

Affects: All Entities

On November 20, 2015, the FASB issued ASU 2015-17, Balance Sheet Classification of Deferred Taxes, to simplify classification of deferred tax assets (DTAs) and deferred tax liabilities (DTLs). Under current guidance, companies are required to separate DTLs and DTAs into a net current amount and a net noncurrent amount for each tax-paying jurisdiction. DTLs and DTAs are classified as current or noncurrent based on the classification of the related asset or liability for financial reporting. The amendments issued in November require that the net total of DTLs and DTAs be classified as noncurrent in a classified balance sheet and apply to all companies that present a classified balance sheet. Noncurrent balance sheet presentation of all deferred taxes also eliminates the requirement to allocate a valuation allowance on a pro rata basis between gross current and noncurrent DTAs.

Effective Dates

For public business entities, the amendments are effective for financial statements issued for annual periods beginning after December 15, 2016, and interim periods within those annual periods.

For all other entities, the amendments are effective for financial statements issued for annual periods beginning after December 15, 2017, and interim periods within annual periods beginning after December 15, 2018.

The guidance can be adopted by all entities for any interim or annual financial statements that have not been issued. In addition, entities are permitted to apply the amendments either prospectively or retrospectively to all periods presented.

If the guidance is applied prospectively, the entity should disclose in the first interim and first annual period of change, the nature of and reason for the change in accounting principle and a statement that prior periods were not retrospectively adjusted. If the guidance is applied retrospectively, the entity should disclose in the first interim and first annual period of change, the nature of and reason for the change in accounting principle, and quantitative information about the effects of the accounting change on prior periods.

Quarterly Accounting Update: Regulatory Update

SEC Comment Letter Trends

The Security and Exchange Commission (SEC) staff’s 2015 comment letters continued to focus on Management’s Discussion and Analysis (MD&A). Although MD&A should provide stakeholders with an opportunity to look at the business through the eyes of management, SEC staff comments indicate some company disclosures do not meet this objective and, in some cases, fail to provide information that allows investors to assess the likelihood that past performance will be indicative of future performance.

In addition, the SEC staff targeted internal control over financial reporting. When a registrant discloses revisions for immaterial accounting errors, the SEC staff has questioned what control deficiencies were identified, and whether the severity of the deficiency was appropriately evaluated. The staff is not only concerned with the magnitude of the errors but also the volume of activity that reasonably could have been exposed to the deficiency, often referred to as the “could” factor.

The SEC staff has also focused attention on disclosures related to areas that require significant judgments and estimates such as the following:

• Impairments – The SEC staff has asked for details of companies’ quantitative impairment tests and the related assumptions. The SEC staff has also asked registrants to disclose additional quantitative and qualitative information for reporting units whose fair values are not substantially in excess of their carrying amounts (“at risk” reporting units), including the sensitivity of the impairment conclusion to changes in the key assumptions.

• Reportable segments – The most predominant issues for this area related to appropriate identification of operating segments and the aggregation of operating segments into reportable segments. The SEC staff may request a company’s analysis of the qualitative (e.g., class of customer) and quantitative criteria used to aggregate operating segments.

• Business combinations – These disclosures should enable users to evaluate the nature and financial effects of a business combination. SEC staff comments have focused on: o Purchase price allocations, including questions about the determination of fair value

and the key assumptions used; o Measurement period adjustments and timeliness of information that resulted in the

adjustments; o Allocation of goodwill to reporting units and the relationship to a company’s

operating segment disclosures; and o Factors considered in determining whether a transaction was the purchase of assets

or a business.

SEC Commissioner Discusses Cybersecurity Risks for Smaller Companies

In an article published in the Autumn 2015 edition of the Cyber Security Review, SEC Commissioner Luis Aguilar noted that while cybersecurity is clearly a concern that the entire business community shares, it represents an especially large threat to smaller businesses.

The article also notes that small and midsize businesses (“SMBs”) are not just targets of cybercrime, they are its principal target with the majority of all targeted cyberattacks last year directed at SMBs. Even more disconcerting is the fact that cybercrime represents an existential threat for SMBs. It has been estimated that half of the small businesses that suffer a cyberattack go out of business within six months as a result.

Aguilar noted the following steps as potential solutions from government agencies and/or other organizations to help SMBs overcome their resource constraints to address the issue:

• Provide SMBs with More Guidance About Cybersecurity • Identify Ways of Fostering Economies of Scale for Cybersecurity Solutions • Provide SMBs with Additional Resources for Cybersecurity • Devote Additional Resources to Fighting Cybercrime

The increased attention to cybersecurity is representative of a broader trend to focus on risk management.

SEC Chair Notes Corp Fin is Investigating Use of Non-GAAP Measures

SEC Chair Mary Jo White recently noted that companies have become more aggressive during recent years in adjusting their earnings numbers to present investors with better-looking financial results.

The SEC’s Division of Corporation Finance (Corp Fin) is trying to make sure that non-GAAP measures are not misleading investors as they review company filings. Specifically, Corp Fin is focusing on whether disclosure about the use of non-GAAP measures is really adequate and whether companies are properly disclosing why they think non-GAAP earnings numbers are useful to investors.

SEC Working on IFRS Proposal

The SEC is planning to issue a proposal in 2016 to let companies voluntarily provide financial information reported in International Financial Reporting Standards (IFRS) in addition to their financial statements in U.S. GAAP. The SEC staff is working on a recommendation for the proposal that is expected to say that the IFRS information does not need to be a complete set of financial statements. The information also will not need to be audited, and it would eliminate some Regulation G requirements, which deal with non-GAAP measures. Under Regulation G, companies that use non-GAAP financial information in their regulatory filings must reconcile the differences between the non-GAAP measures—in this case, IFRS—and U.S. GAAP. James Schnurr, the SEC’s chief accountant, first floated the idea of supplemental IFRS information in December 2014. Schnurr said the SEC wants to see if IFRS can be used more widely in the U.S. without dramatically increasing the cost of preparing financial statements and SEC filings.

JOBS Act Crowdfunding Rules Approved

On October 30, 2015, the SEC issued the final version of its crowdfunding rules, finalizing the two-year old proposal from the JOBS Act. The rules tighten some investment limits, while giving first-time crowdfunding issuers a reprieve from the toughest accounting requirements. The rules go into effect 180 days after publication in the Federal Register, which normally occurs within a few weeks of a rule’s publication on the SEC’s website.

The rules spell out requirements for companies, funding platforms and investors making use of the new exemption. Issuers can raise up to $1 million a year in group-based equity financing through SEC-registered intermediaries, who can be either brokers or a new type of entity called a funding portal. The intermediaries are allowed under the rules to take equity stakes as compensation for facilitating the deals, a change from the original proposal in 2013. In addition, intermediaries must be licensed by the Financial Industry Regulatory Authority (FINRA).

Companies must comply with three tiers of disclosure, based on the size of the offering. Companies raising less than $100,000 must show investors their federal income tax returns certified by the chief executive. If a company is raising between $100,000 and $500,000, it must have its financial statements reviewed by an independent public accountant. For offerings above $500,000, the company must provide audited financial statements, unless the offering is the first time the company is raising capital using the crowdfunding process, in which case it needs only to have the financials reviewed by an independent accountant. All financial statements must be prepared in accordance with U.S. GAAP.

Investors do not need to be accredited to participate in offerings regulated by the rules. The amount they can invest in a given year is determined by their income and net worth. The rules limit an individual with an income or net worth below $100,000 to investing either $2,000 or 5 percent of the lesser of their net worth or income. Someone above that wealth threshold can put 10 percent of the lesser of their income or net worth into crowdfunding deals, up to $100,000 a year. Securities bought through crowdfunding deals cannot be resold for a year.

Lead Partner Identification Rule Is Released

On December 15, 2015, the Public Company Accounting Oversight Board (PCAOB) unanimously approved a final rule requiring audit firms to name the engagement partner and other accounting firms that participated in an audit.

The disclosure will have to be made on a new form titled “Auditor Reporting of Certain Audit Participants,” or Form AP. When naming the other firms that took part in an audit, the lead audit firm will have to state the extent of their work. For accounting firms that participated in 5 percent or more in the audit work, the name and location of the participating firm and the percentage of total audit hours must be disclosed on the form. If accounting firms took part in less than 5 percent of the total audit work, the lead firm has to disclose the number of other accounting firms that participated in the audit and the aggregate percentage of total audit hours of the participating firms.

The yearly reporting requirement becomes effective for auditor reports issued on or after January 31, 2017, for the identification of the engagement partner. The disclosure of the other firms in the audit will become effective after June 30, 2017. The Form AP will have to be filed within 35 days of the submission of the client’s 10-K filing, which includes the auditor’s report.

The SEC is required to approve PCAOB rules and standards, and it is expected to endorse the rule in early 2016. The PCAOB is planning to issue interpretive guidance to help auditors with the new rules shortly after SEC approval of the final release. COSO Program to Certify Financial Executives for Internal Control Framework

The Committee of Sponsoring Organizations of the Treadway Commission (COSO) has begun a program to certify internal auditors, accountants, and other financial executives for their knowledge in designing and installing internal control systems that follow COSO’s Internal Control—Integrated Framework.

The course is offered by COSO’s five sponsoring organizations: the American Accounting Association (AAA), the American Institute of Certified Public Accountants (AICPA), Financial Executives International (FEI), the Institute of Management Accountants (IMA), and the Institute of Internal Auditors (IIA). The IIA and AICPA are offering three-day workshops throughout 2016.

The Integrated Framework was updated in 2013 after originally being released in 1992 as a guide for designing and implementing internal controls.

Quarterly Accounting Update: Other Developments

North Carolina Tax Reform Law Impacts Deferred Tax Assets and Liabilities

On July 23, 2013, North Carolina Governor Pat McCrory signed a major tax reform bill into law that lowered the North Carolina corporate income tax rate among other things. Specifically, the corporate income tax rate was reduced from 6.9% to 6% in 2014 and to 5% in 2015. The rate will be further reduced to 4% during the 2016 tax year and to 3% for post-2016 tax years provided that specified revenue growth targets are reached.

On July 28, 2015, McCrory announced the final revenue figures for the fiscal year ended on June 30, 2015 reveal that North Carolina had a $445 million revenue surplus. Thus, the state met the necessary revenue target for fiscal year 2014-2015 to lower the corporate income tax rate from 5 percent to 4 percent effective for tax years beginning on or after January 1, 2016. The rate will be decreased for post-2016 tax years if the net general fund tax collections for fiscal year 2015-2016 exceed $20.975 billion.

These collection targets that trigger additional rate decreases must be considered in determining the amount of deferred tax assets/liabilities. For accounting purposes, when it is considered to be more likely than not the tax rate changes will be implemented, the enacted changes in tax laws and rates that become effective for a particular future year(s) are to be considered in determining the tax rate to apply to temporary differences reversing in that year(s). The effect on deferred tax assets and liabilities from an enacted change in tax laws or rates is recognized in income from continuing operations in the period of enactment (date tax legislation signed into law) regardless of whether the tax legislation is retroactive or prospective.

The excerpt of the rate reduction trigger criteria from the final enacted legislation can be accessed at: http://www.ncleg.net/EnactedLegislation/Statutes/PDF/BySection/Chapter_105/GS_105-130.3C.pdf

An Update on the New Revenue Recognition Standard

The FASB and International Accounting Standards Board (IASB) published their landmark revenue recognition standards in May 2014. However, since its issuance, some companies and their auditors have expressed concern that the FASB introduced too much principles-based guidance for U.S. companies to effectively adopt. In addition, some critics have said they need more implementation guidance. Others have said there was too little time for them to confidently plan for the standard’s effective date.

In response to those implementation concerns, the FASB and the IASB decided at a meeting in February, 2015, to propose revisions to clarify the standard to reduce diversity in practice. Both Boards agreed that amendments to the guidance are needed to reduce the potential for diversity in practice. But, in general, the FASB decided to propose more changes than the IASB did. `

Effective Date Deferred

On July 22, 2015, the IASB approved a one-year deferral of the effective date of its revenue standard, IFRS 15, to January 1, 2018. On August 12, 2015, the FASB issued ASU 2015-14, Revenue from Contracts with Customers (Topic 606): Deferral of the Effective Date, to delay the effective date of the revenue standard by one year. As a result, the standard will be effective for public entities for annual periods beginning after December 15, 2017 and interim periods therein. Nonpublic entities will be required to adopt the standard for annual reporting periods beginning after December 15, 2018 and interim periods within annual periods beginning after December 15, 2019. All entities will be allowed to adopt the standard as early as the original public entity effective date (i.e., annual periods beginning after December 15, 2016).

Licenses of Intellectual Property

Although the Boards agreed on many substantive clarifications, the FASB decided to propose further clarifications in the guidance:

• Under the FASB proposal, when an entity grants a license to symbolic intellectual property, it is presumed that the entity’s promise to the customer in granting a license includes undertaking activities that significantly affect the utility of the intellectual property to which the customer has rights. Intellectual property is considered symbolic when it does not have significant stand-alone functionality, such as brands, team or trade names, or logos.

• The FASB decided to clarify that, in some cases, an entity would need to determine the nature of a license that is not a separate performance obligation in order to appropriately apply the general guidance on whether a performance obligation is satisfied over time or at a point in time and/or to determine the appropriate measure of progress for a combined performance obligation that includes a license.

• The FASB decided to clarify that certain contractual restrictions are attributes of the license and therefore do not affect the identification of promised goods or services in the contract.

Identifying Performance Obligations

The Boards agreed to add some illustrative examples to clarify how to apply the guidance on identifying performance obligations. However, the FASB decided to propose further amendments to address implementation issues about:

• Identifying promised goods or services that would be subject to the separation guidance. • Application of the guidance related to the concept of “distinct in the context of the contract.” • Accounting for shipping and handling activities.

Principal-Versus-Agent Considerations

The Boards agreed to identical proposals to address how an entity should assess whether it is the principal or the agent in contracts that include three or more parties. The proposals would clarify that an entity should evaluate whether it is the principal or the agent for each specified good or service (i.e., each good or service or bundle of distinct goods or services that is distinct) promised in a contract with a customer. In addition, the proposals would add guidance to help entities determine the nature of promises in a contract. Specifically, the proposed guidance would require an entity to (1) identify the specified goods or services (or bundles of goods or services), including rights to goods or services from a third party, and (2) determine whether it controls each specified good or service before each good or service (or right to a third-party good or service) is transferred to the customer.

In addition to clarifying the guidance on principal-versus-agent considerations, the proposals would amend certain illustrative examples in the standard (and add new ones) to clarify how an entity would assess whether it is the principal or the agent in a revenue transaction.

Measurement Guidance Published for Government Investment Pools

On December 23, 2015, the Governmental Accounting Standards Board (GASB) issued Statement 79, Certain External Investment Pools and Pool Participants, to address how some investment pools used by state and local governments should measure their holdings. The GASB issued the statement in response to the SEC’s amended rules for money market funds, which become effective in April 2016. The investment pools used by state and local governments technically are not money funds and not regulated by the SEC, but because so many of them operate like the funds, the GASB wanted to keep its guidance for the pools current with the SEC’s rule changes. Governments use the pools much like businesses and other private-sector organizations use money market funds. The governments often will pool their investment activities and purchase short-term, high-grade investments.

Statement 79 permits external investment pools and governments that participate in them to measure pool investments at amortized cost if its participants can buy and redeem shares at a stable price of $1, the pool’s investments are in high-grade, short-term instruments, and the holdings can be sold relatively quickly to satisfy redemptions. Pools that cannot meet those criteria have to follow the guidance in Statement 31, Accounting and Financial Reporting for Certain Investments and for External Investment Pools.

The requirements of Statement 79 are effective for reporting periods beginning after June 15, 2015, except for certain provisions on portfolio quality, custodial credit risk, and shadow pricing. Those provisions are effective for reporting periods beginning after December 15, 2015. Earlier application is encouraged.

GASB Issues Amendments to Pension Guidance

On December 11, 2015, GASB Statement 78, Pensions Provided Through Certain Multiple-Employer Defined Benefit Pension Plans, was issued to assist governments that participate in certain private or federally sponsored multiple-employer defined benefit pension plans. The standard addresses the employer accounting and financial reporting requirements for the pension plans. The GASB issued Statement 78 to ease the application of Statement 68, Accounting and Financial Reporting for Pensions, by governments that participate in multi-employer plans, such as Taft-Hartley plans or similar types of pensions.

Statement 78 excludes some pensions provided to employees of state or local governmental employers through a cost-sharing, multiple-employer pension from applying Statement 68. To qualify for the exclusion, the plan cannot be a state or local government plan, must be used to provide defined benefit pensions to government and nongovernment employees, and cannot be dominated by one or more of its government participants. The exclusion is necessary because some governments that participate in multi-employer plans cannot obtain the measurements they need from the plans for preparing their financial statements.

The requirements of Statement 78 are effective for reporting periods beginning after December 15, 2015. Earlier application is encouraged.

Quarterly Accounting Update: On the Horizon

The following selected FASB exposure drafts and projects are outstanding as of December 31, 2015.

FASB Simplification Initiative

The FASB’s Simplification Initiative is a tightly-focused initiative to make narrow-scope simplifications and improvements to accounting standards through a series of short-term projects. The projects included in the initiative are intended to improve or maintain the usefulness of the information reported to investors while reducing cost and complexity in financial reporting. In addition to the Simplification Initiative, the FASB recently completed several projects, and currently is working on several projects, that are intended to reduce cost and complexity in financial reporting. The FASB launched the initiative earlier this year to reduce the cost and complexity of financial reporting by making targeted changes to U.S. GAAP while maintaining or improving the usefulness of information for investors.

Balance Sheet Classification of Debt

This project is expected to reduce cost and complexity by replacing the existing fact-pattern specific guidance with a principle to classify debt as current or noncurrent based on the contractual terms of a debt arrangement and an organization’s current compliance with debt covenants. An exposure draft is expected in the first quarter of 2016.

Employee Share-Based Payments

A proposed ASU would allow an employer to repurchase more of an employee’s shares than it can today for tax withholding purposes without triggering liability accounting and would require that any cash paid for these repurchases be classified as a financing activity on the statement of cash flows. The proposal also would provide a policy election to account for forfeitures as they occur. Further, it would require all income tax effects when awards vest or are settled to be recognized in income rather than through additional paid-in capital (APIC) in certain cases. That is, APIC pools would be eliminated. In addition, it would require awards with put features that are contingent on an event within an employee’s control to be classified as equity until it is probable that the event will occur. It also would give private companies the option to use two practical expedients for estimating an award’s expected term and measuring liability classified awards.

Equity Method Accounting

A proposed ASU would simplify the equity method of accounting by eliminating the requirement that an investor identify, account for and make disclosures about the difference between the cost basis of an investment and its proportional interest in the equity of the investee (i.e., a basis difference). As a result, investors would no longer have to estimate the fair value of an investee’s assets and liabilities to allocate basis differences and track adjustments related to basis differences. The FASB also proposed eliminating the requirement to account for an equity method investment retrospectively when an investor increases its ownership interest in a non-consolidated subsidiary to a level that qualifies for the equity method.

Financial Instruments

The FASB continues to work on its financial instruments project. This project took on heightened significance in the wake of the 2008 financial crisis and once was considered an essential international accounting convergence project. Negotiations with the IASB to write global accounting guidelines have since fallen apart, and the amendments the FASB plans to publish in 2016 are expected to change U.S. GAAP and not match the IASB’s revisions to its standards. The project has three primary areas that are being individually addressed, (1) recognition and measurement, (2), impairment and (3) hedging.

Recognition and Measurement

On January 5, 2016, the FASB issued ASU 2016-01, Recognition and Measurement of Financial Assets and Financial Liabilities, to improve and simplify the recognition and measurement of financial instruments. A discussion of the new ASU is included in the FASB Update section.

Impairment

U.S. GAAP currently accounts for credit impairment using an “incurred loss” model. Because the existing impairment model delays recognition of the credit loss until the loss is probable (or has been incurred), many have argued that the model fails to alert investors to expected credit losses in a timely manner. Some have recommended that standard setters explore alternatives to the incurred loss model that would use more forward-looking information.

In December 2012, the FASB issued its proposed Accounting Standards Update which set forth a “current expected credit loss” (CECL) model. This model will replace the multiple impairment models that currently exist for debt instruments in U.S. GAAP. The CECL model uses a single “expected credit loss” measurement objective for the allowance for credit loss. Under this model, the allowance for lifetime expected credit losses, when combined with the reported balance of the debt instrument, would reflect management’s estimate of the cash flows it expects to collect, based on its assessment of credit risk as of the reporting date. The FASB has completed its major decisions in this area, and expects to issue a final standard during the first quarter of 2016.

Public businesses that meet the definition of an SEC filer will be required to apply the guidance for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. Other public business entities will be required to apply the guidance for fiscal years beginning after December 15, 2019, including interim periods within those fiscal years.

Entities that are not public business entities—including private companies, not-for-profit organizations, and employee benefit plans within the scope of FASB guidance on plan accounting—will be required to apply the guidance for fiscal years beginning after December 15, 2019, and interim periods within fiscal years beginning after December 15, 2020.

Early application of the guidance will be permitted for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years.

Hedging

At its June 29, 2015, meeting, the FASB made a number of tentative decisions that would significantly modify certain aspects of the existing hedge accounting model. The FASB directed the staff to draft a proposed ASU, which will likely be issued in early 2016. The objective of this project is to make targeted improvements to the hedge accounting model based on feedback received from preparers, auditors, users, and other stakeholders. The FASB will consider opportunities to align with IFRS 9, Financial Instruments, which was issued in 2013.

Leases

In 2006, the FASB and the International Accounting Standards Board (IASB) identified major convergence projects intended to improve and converge U.S. GAAP and IFRS. As part of that effort, the two Boards issued two proposals to revise lease accounting, one in 2010 and a revised proposal in 2013. The Boards began re-deliberations in September 2013 to address the concerns raised by stakeholders.

On November 11, 2015, the FASB voted to proceed with finalizing the new lease accounting standard. Although some aspects of the initial proposal have changed, and convergence between the FASB and IASB appears unlikely, the key objective, to bring most leases on balance sheet, will be achieved in the final standard. The final ASU is expected to be published in early 2016.

Lessee Accounting Model

The FASB decided on a dual approach for classifying leases based on criteria similar to current U.S. GAAP—rejecting classification based on the nature of the underlying asset, as had been proposed in the 2013 revised proposal. Under this approach, a lessee will account for most existing capital/finance leases as Type A leases (that is, recognizing amortization of the right-of-use (ROU) asset separately from interest on the lease liability) and most existing operating leases as Type B leases (with costs presented as lease expense and recognized on a straight-line basis in the income statement over the lease term).

The final standard will require a lease to be classified as a Type A lease when (1) payments represent substantially all of the fair value of the asset, (2) the lease term is for a major portion of the asset’s economic life, (3) purchase of the asset is considered a bargain, or (4) title transfer is automatic at the end of the lease. The fair value and economic life tests are expected to be similar to the 90% and 75% tests under existing U.S. GAAP guidance, albeit without the bright lines.

The lessee will recognize a ROU asset and a lease liability for both Type A leases and Type B leases. The only exception to this presentation will be for short-term leases (i.e., a term of one year or less), which would not be recognized on a lessee’s balance sheet.

Lessor Accounting Model

A lessor will determine lease classification (Type A versus Type B) on the basis of whether the lease is effectively a financing or a sale, rather than an operating lease (i.e., on the concept underlying existing U.S. GAAP). A lessor would make that determination by assessing whether the lease transfers

substantially all the risks and rewards incidental to ownership of the underlying asset. For financing arrangements (Type A leases) or sales, the balance sheet would reflect a lease receivable and the lessor’s residual interest. Lessors would classify all other leases as Type B, with income statement and balance sheet treatment similar to today’s operating leases.

Transition

The new lease standard will be implemented using a modified retrospective approach. Under this approach, lessees and lessors will compute lease assets and liabilities based on the remaining payments for leases existing at, or entered into after, the beginning of the earliest comparative period presented in the financial statements (the date of initial application). In addition, a lessee may elect specified transition relief provisions. These relief provisions, which must be elected collectively and applied consistently, would allow lessees to:

o Not reassess whether any expired or existing contracts are, or contain, leases o Not reassess the lease classification for any expired or existing leases (i.e., capital

leases could be assumed to be Type A leases and operating leases Type B) o Not reassess initial direct costs for any existing leases (that is, whether those costs

would have qualified for capitalization under the new standard)

Effective Dates

For public companies, the upcoming standard will be effective for fiscal years (and interim periods within those fiscal years) beginning after December 15, 2018; for private companies, the standard will be effective for annual periods beginning after December 15, 2019. Early adoption will be permitted for all companies and organizations upon issuance of the standard.

Disclosure Framework

The objective and primary focus of this project is to improve the effectiveness of disclosures in notes to financial statements by clearly communicating the information that is most important to users of each entity’s financial statements. Although reducing the volume of the notes to financial statements is not the primary focus, the FASB hopes that a sharper focus on important information will result in reduced volume in most cases. On March 4, 2014, the FASB issued an Exposure Draft, Conceptual Framework for Financial Reporting: Chapter 8 Notes to Financial Statements, intended to improve its process for evaluating existing and future disclosure requirements in notes to financial statements. Specifically, it addresses the FASB’s process for identifying relevant information and the limits on information that should be included in notes to financial statements. If approved, it would become part of the FASB’s Conceptual Framework, which provides the foundation for making standard-setting decisions.

On September 24, 2015, the FASB issued two proposals—one about the use of materiality by reporting entities, Assessing Whether Disclosures Are Material, and the other amending the Conceptual Framework’s definition of materiality, Conceptual Framework for Financial Reporting Chapter 3: Qualitative Characteristics of Useful Financial Information. These two proposals were issued to help

entities decide what information should be included in their footnotes without bogging them down with extra details.

The main provisions would draw attention to the role materiality plays in making decisions about disclosures. More specifically, the proposed ASU explains that: (a) materiality would be applied to quantitative and qualitative disclosures individually and in the aggregate in the context of the financial statements as a whole; therefore, some, all, or none of the requirements in a disclosure Section may be material; (b) materiality would be identified as a legal concept; and (c) omitting a disclosure of immaterial information would not be an accounting error.

Financial Statements of Not-for-Profit Entities

On April 22, 2015, the FASB issued a proposal that would significantly change the financial statements of not-for-profit (NFP) entities, including business-oriented health care entities. The proposal would require NFPs to present two rather than three net asset classes and standardized measures of operating performance. It also would change how NFPs report cash flows, classify expenses and provide information about liquidity. Business-oriented health care NFPs would no longer be allowed to present a performance indicator as a U.S. GAAP measure. The FASB has said that, before finalizing the guidance for NFPs, it will consider its decisions on related projects such as its research on financial performance reporting and improving classification guidance for the statement of cash flows. However, the proposal has attracted wide attention, and criticism, and some of the critics are from the group that helped develop the proposal, the FASB’s Not-for-Profit Advisory Council.

Prepaid Stored Value Cards

On April 30, 2015, the FASB issued a proposal that would require entities (typically banks or other financial institutions) that issue certain prepaid stored-value cards that are redeemable only from third-party merchants for goods or services, cash or a combination of the two to recognize breakage, which is the value that is not redeemed by cardholders. Under that proposal, an issuer’s liability for the cards would be considered a financial liability.

Clarifying the Definition of a Business

This project is intended to clarify the definition of a business with the objective of addressing whether transactions involving in-substance nonfinancial assets (held directly or in a subsidiary) should be accounted for as acquisitions (or disposals) of nonfinancial assets or as acquisitions (or disposals) of businesses. The project will include clarifying the guidance for partial sales or transfers and the corresponding acquisition of partial interests in a nonfinancial asset or assets.

Clarifying Certain Existing Principles on Statement of Cash Flows

In November 1987, the FASB issued FASB Statement No. 95, Statement of Cash Flows. Statement 95 was later codified in Accounting Standards Codification (ASC) 230, Statement of Cash Flows. Recently, FASB staff research indicated that there was diversity in practice with respect to the classification of certain cash receipts and payments. The FASB staff’s research also indicated that the primary reasons for the

diversity in classification is the result of lack of specific accounting guidance and inconsistent application of the existing principles within ASC 230. This project will include clarifying existing principles in ASC 230 on how to classify cash receipts and cash payments. As part of the project, the FASB staff will research potential additional disclosures that could result in increased relevance for users.

Accounting for Interest Income Associated with the Purchase of Callable Debt Securities

At its meeting on September 16, the FASB voted to add to its technical agenda a project to require disclosures about interest income on purchased debt securities and loans. The FASB discussed whether to amend the scope of the project to include the amortization period for purchased callable debt securities, for example, municipal bonds. The FASB decided to amortize all premiums to the first call date and all discounts to the maturity date.

The Board further directed the FASB staff to research the disclosure requirements related to the accounting for interest income on callable debt securities and callable loans. The Board also directed the FASB staff to consider whether and how to limit the scope of the instruments subject to the change.

EITF Agenda Items

At its November 2015 meeting, the FASB's Emerging Issues Task Force (EITF) discussed four Issues and reached final consensuses on three of them. It also reached a consensus-for-exposure on eight of the nine issues being considered as part of its Issue on statement of cash flows classification.

Final Consensuses

• Issue 15-B—Recognition of Breakage for Certain Prepaid Stored-Value Cards: Issuers of certain prepaid stored-value products redeemable for goods, services, and/or cash will derecognize their obligations proportionately as the prepaid products are redeemed if it expects to be entitled to a breakage amount, or when redemption is remote if the entity does not expect to be entitled to a breakage amount. This model is consistent with the breakage model under ASC 606, Revenue from Contracts with Customers. The final consensus will follow the same transition method and effective date as ASC 606, except early adoption will be permitted upon the issuance of the final ASU.

• Issue 15-D—Effect of Derivative Contract Novations on Existing Hedge Accounting Relationships: A change in the counterparty to a derivative instrument (often referred to as a “novation”), in and of itself, will not require the dedesignation of the hedge accounting relationship. The new guidance will be applied prospectively. However, entities have the option to adopt the guidance on a modified retrospective basis as of the earliest period presented for all hedge relationships that were dedesignated due to novations.

• Issue 15-E—Contingent Put and Call Options in Debt Instruments: A contingent put or call option embedded in a debt instrument will be evaluated for possible separate accounting as a derivative instrument under ASC 815, Derivative and Hedging, without regard to the nature of the exercise contingency, even if the contingent event is unrelated to interest rates and credit

risk. Entities will adopt the guidance on a modified retrospective basis and will be permitted to elect the fair value option at transition for the affected debt instruments.

Consensus-for-Exposure

• Issue 15-F—Statement of Cash Flows: Classification of Certain Cash Receipts and Cash Payments: In April, the FASB asked the EITF to address nine specific cash flow classification issues (i.e., operating, investing, or financing activities) under ASC 230, Statement of Cash Flows. The Task Force has discussed eight of the nine issues during its June and September 2015 meetings. At its November meeting, the Task Force discussed the issue on restricted cash and directed the staff to perform additional research. For the remaining eight issues, the Task Force affirmed its previous tentative decisions and reached a consensus-for-exposure. The following is a summary of the nine issues being addressed as part of this Issue:

o Issue 1 – Payments for debt prepayment or extinguishment: Financing o Issue 2 – Settlement of zero-coupon bonds: Operating (payment attributable to interest)

and financing (payment attributable to principal) o Issue 3 – Contingent consideration payments made after a business combination:

Financing (payment equal to or below fair value of initial contingent consideration liability) and operating (excess amount)

o Issue 4 – Changes in restricted cash: No consensus reached; still in deliberation o Issue 5 – Proceeds from the settlement of insurance claims: Classify based on the nature

of the insured loss o Issue 6 – Proceeds from the settlement of corporate owned life insurance (COLI):

Investing; premiums can be classified as investing and/or operating o Issue 7 – Distributions received from equity method investees: Operating (distributions

up to cumulative equity earnings to date) and investing (amount in excess of cumulative earnings to date)

o Issue 8(a) – Presentation of beneficial interests received in securitization transactions: Disclose beneficial interests received as noncash activity

o Issue 8(b) – Cash receipts from beneficial interests in securitized trade receivables: Investing

o Issue 9 – Application of the predominance principle: Apply when lacking specific guidance and cash flows are not separately identifiable

PCC Activities

The Private Company Council (PCC) met on December 4, 2015, and discussed the following issues:

• PCC Issue 15-01— Effective Date and Transition Guidance The PCC reached a final consensus for the issuance of a standard to remove the effective dates for the following four ASUs:

o ASU 2014-02, Intangibles—Goodwill and Other o ASU 2014-03, Derivatives and Hedging

o ASU 2014-07, Applying Variable Interest Entities Guidance to Common Control Leasing Arrangements

o ASU 2014-18, Accounting for Identifiable Intangible Assets in a Business Combination The FASB will meet in the near future to consider endorsement of the final consensus.

• PCC Issue 15-02—Agenda Paper—Applying VIE Guidance to Entities Under Common Control The PCC voted to add a project to its agenda concerning the application of Variable Interest Entities (VIE) guidance to companies under common control that are not already addressed in ASU 2014-07, Applying Variable Interest Entities Guidance to Common Control Leasing Arrangements. The PCC directed the FASB staff to work with private company stakeholders to develop examples to help clarify application of VIE guidance to such situations.

• Disclosure Framework—Income Taxes The PCC discussed the FASB’s Disclosure Framework review of income taxes and provided feedback on tentative decisions to date. The PCC disagreed with the FASB’s tentative decision to require a rate reconciliation for private companies.

APPENDIX A

Important Implementation Dates

The following table contains significant implementation dates and deadlines for FASB/EITF/PCC and GASB standards.

FASB/EITF/PCC Implementation Dates Pronouncement Affects Effective Date and Transition

ASU 2016-01, Recognition and Measurement of Financial Assets and Financial Liabilities

All entities For public companies the amendments are effective for fiscal years beginning after December 15, 2017, including interim periods within those fiscal years.

For private companies, not-for-profit organizations, and employee benefit plans, the standard becomes effective for fiscal years beginning after December 15, 2018, and for interim periods within fiscal years beginning after December 15, 2019.

ASU 2015-17, Balance Sheet Classification of Deferred Taxes

All entities For public business entities, the amendments are effective for financial statements issued for annual periods beginning after December 15, 2016, and interim periods within those annual periods.

For all other entities, the amendments are effective for financial statements issued for annual periods beginning after December 15, 2017, and interim periods within annual periods beginning after December 15, 2018.

Pronouncement Affects Effective Date and Transition

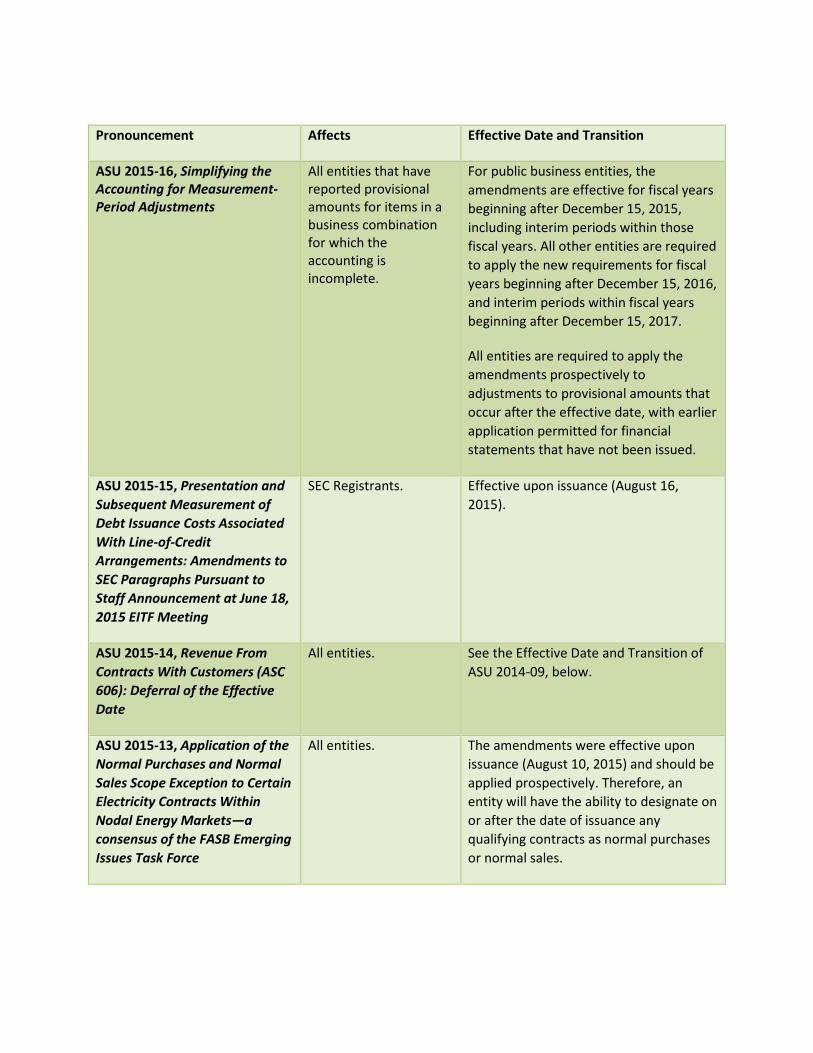

ASU 2015-16, Simplifying the Accounting for Measurement-Period Adjustments

All entities that have reported provisional amounts for items in a business combination for which the accounting is incomplete.

For public business entities, the amendments are effective for fiscal years beginning after December 15, 2015, including interim periods within those fiscal years. All other entities are required to apply the new requirements for fiscal years beginning after December 15, 2016, and interim periods within fiscal years beginning after December 15, 2017.

All entities are required to apply the amendments prospectively to adjustments to provisional amounts that occur after the effective date, with earlier application permitted for financial statements that have not been issued.

ASU 2015-15, Presentation and Subsequent Measurement of Debt Issuance Costs Associated With Line-of-Credit Arrangements: Amendments to SEC Paragraphs Pursuant to Staff Announcement at June 18, 2015 EITF Meeting

SEC Registrants. Effective upon issuance (August 16, 2015).

ASU 2015-14, Revenue From Contracts With Customers (ASC 606): Deferral of the Effective Date

All entities. See the Effective Date and Transition of ASU 2014-09, below.

ASU 2015-13, Application of the Normal Purchases and Normal Sales Scope Exception to Certain Electricity Contracts Within Nodal Energy Markets—a consensus of the FASB Emerging Issues Task Force

All entities. The amendments were effective upon issuance (August 10, 2015) and should be applied prospectively. Therefore, an entity will have the ability to designate on or after the date of issuance any qualifying contracts as normal purchases or normal sales.

Pronouncement Affects Effective Date and Transition

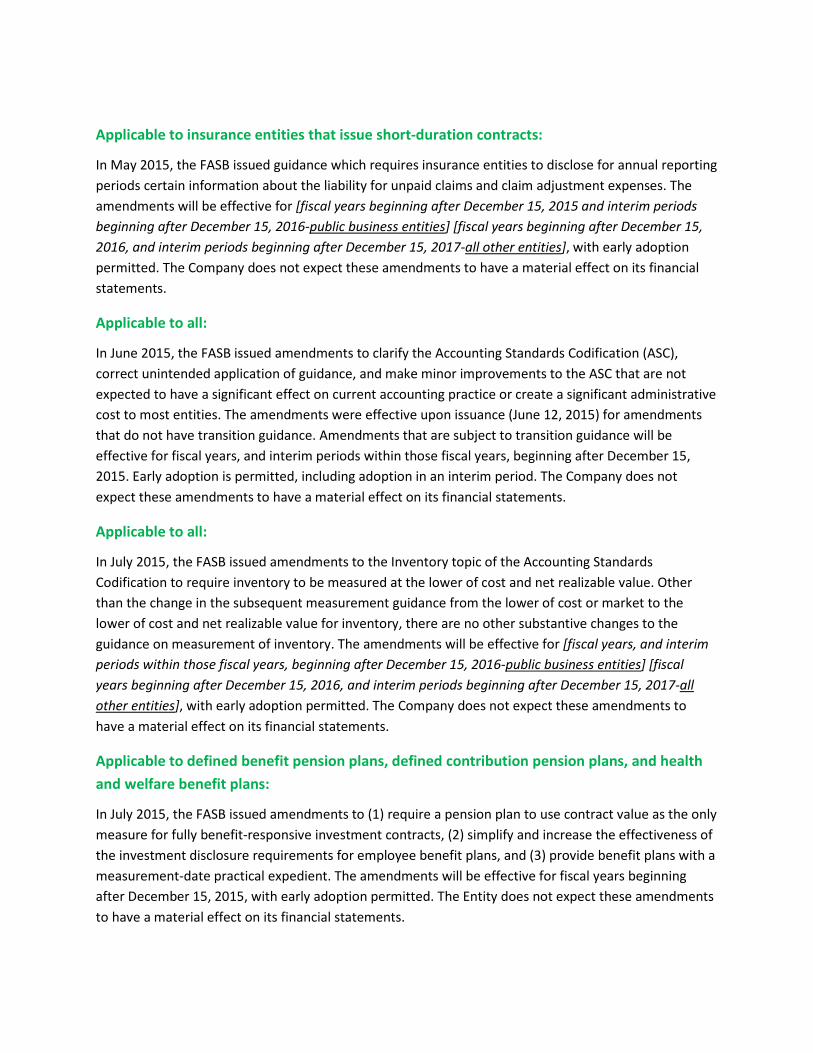

ASU 2015-12, (Part I) Fully Benefit-Responsive Investment Contracts, (Part II) Plan Investment Disclosures, (Part III) Measurement Date Practical Expedient

Defined Contribution Pension Plans, Defined Benefit Pension Plans, and Health and Welfare Benefit Plans

The amendments in all three are effective for fiscal years beginning after December 15, 2015; early adoption is permitted. An entity should apply the amendments in parts I and II retrospectively to all financial statements presented, while the amendments in part III should be applied prospectively.

ASU 2015-11, Simplifying the Measurement of Inventory

All entities. For public business entities, the amendments are effective for fiscal years beginning after December 15, 2016, including interim periods within those fiscal years. For all other entities, the amendments are effective for fiscal years beginning after December 15, 2016, and interim periods within fiscal years beginning after December 15, 2017. The amendments should be applied prospectively with earlier application permitted as of the beginning of an interim or annual reporting period.

ASU 2015-10, Technical Corrections and Improvements

All entities. Effective upon issuance (June 12, 2015) for amendments that do not have transition guidance. Amendments that are subject to transition guidance: effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2015.

ASU 2015-09, Disclosures about Short-Duration Contracts

Insurance entities that issue short-duration contracts as defined in FASB ASC 944, Financial Services—Insurance.

For public business entities, the amendments are effective for annual periods beginning after December 15, 2015, and interim periods within annual periods beginning after December 15, 2016. For all other entities, the amendments are effective for annual periods beginning after December 15, 2016, and interim periods within annual periods beginning after December 15, 2017.

Pronouncement Affects Effective Date and Transition

ASU 2015-08, Pushdown Accounting—Amendments to SEC Paragraphs Pursuant to Staff Accounting Bulletin No. 115 (SEC Update)

None. None.

ASU 2015-07, Disclosures for Investments in Certain Entities That Calculate Net Asset Value per Share (or Its Equivalent)

Entities that elect to use the NAV practical expedient.

For public business entities the amendments are effective for fiscal years beginning after December 15, 2015, and interim periods within those fiscal years. For all other entities, the amendments are effective for fiscal years beginning after December 15, 2016, and interim periods within those fiscal years. Earlier application is permitted.

ASU 2015-06, Effects on Historical Earnings per Unit of Master Limited Partnership Dropdown Transactions

Master limited partnerships.

Effective for fiscal years beginning after December 15, 2015, and interim periods within those fiscal years. Earlier application is permitted.

ASU 2015-05, Customer’s Accounting for Fees Paid in a Cloud Computing Arrangement

All entities. For public business entities, the amendments will be effective for annual periods, including interim periods within those annual periods, beginning after December 15, 2015. For all other entities, the amendments will be effective for annual periods beginning after December 15, 2015, and interim periods in annual periods beginning after December 15, 2016. Early adoption is permitted for all entities.

Pronouncement Affects Effective Date and Transition

ASU 2015-04, Practical Expedient for the Measurement Date of an Employer’s Defined Benefit Obligation and Plan Assets

All entities. The amendments are effective for public business entities for financial statements issued for fiscal years beginning after December 15, 2015, and interim periods within those fiscal years. For all other entities, the amendments are effective for financial statements issued for fiscal years beginning after December 15, 2016, and interim periods within fiscal years beginning after December 15, 2017. Earlier application is permitted.

ASU 2015-03, Simplifying the Presentation of Debt Issuance Costs

All entities. For public business entities, the amendments are effective for financial statements issued for fiscal years beginning after December 15, 2015, and interim periods within those fiscal years. For all other entities, the amendments are effective for financial statements issued for fiscal years beginning after December 15, 2015, and interim periods within fiscal years beginning after December 15, 2016. Early adoption is permitted for financial statements that have not been previously issued.

Pronouncement Affects Effective Date and Transition

ASU 2015-02, Amendments to the Consolidation Analysis

All entities. Effective for public business entities for fiscal years, and for interim periods within those fiscal years, beginning after December 15, 2015. For all other entities, the amendments are effective for fiscal years beginning after December 15, 2016, and for interim periods within fiscal years beginning after December 15, 2017. Early adoption is permitted, including adoption in an interim period. If an entity early adopts the amendments in an interim period, any adjustments should be reflected as of the beginning of the fiscal year that includes that interim period.

A reporting entity may apply the amendments using a modified retrospective approach by recording a cumulative-effect adjustment to equity as of the beginning of the fiscal year of adoption. A reporting entity also may apply the amendments retrospectively.

ASU 2015-01, Simplifying Income Statement Presentation by Eliminating the Concept of Extraordinary Items

All entities. Effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2015. A reporting entity may apply the amendments prospectively. A reporting entity also may apply the amendments retrospectively to all prior periods presented in the financial statements. Early adoption is permitted provided that the guidance is applied from the beginning of the fiscal year of adoption. The effective date is the same for both public business entities and all other entities.

Pronouncement Affects Effective Date and Transition

ASU 2014-18, Accounting for Identifiable Intangible Assets in a Business Combination—a consensus of the Private Company Council

All entities except public business entities, as defined in the Master Glossary of the FASB Accounting Standards Codification, not-for-profit entities, and employee benefit plans.

If the first in-scope transaction occurs in the first fiscal year beginning after December 15, 2015, the elective adoption will be effective for that fiscal year’s annual financial reporting and all interim and annual periods thereafter. If the first in-scope transaction occurs in fiscal years beginning after December 15, 2016, the elective adoption will be effective in the interim period that includes the date of that first in-scope transaction and subsequent interim and annual periods thereafter. Early application is permitted for any interim and annual financial statements that have not yet been made available for issuance.

ASU 2014-17, Pushdown Accounting

All entities. Effective on November 18, 2014. After the effective date, an acquired entity can make an election to apply the guidance to future change-in-control events or to its most recent change-in-control event. However, if the financial statements for the period in which the most recent change-in-control event occurred already have been issued or made available to be issued, the application of this guidance would be treated as a change in accounting principle.

Pronouncement Affects Effective Date and Transition

ASU 2014-16, Determining Whether the Host Contract in a Hybrid Financial Instrument Issued in the Form of a Share is More Akin to Debt or to Equity

All entities that are issuers of, or investors in, hybrid financial instruments that are issued in the form of a share.

Effective for public business entities for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2015. For all other entities, the amendments are effective for fiscal years beginning after December 15, 2016. Early adoption is permitted. If an entity early adopts the amendments in an interim period, any adjustments should be reflected as of the beginning of the fiscal year that includes that interim period.

Entities should apply the guidance on a modified retrospective basis (cumulative-effect retained earnings adjustment as of the beginning of the year of adoption) to existing hybrid instruments issued in the form of a share as of the beginning of the fiscal year for which this ASU is effective. Retrospective application is permitted to all relevant prior periods.

ASU 2014-15, Disclosure of Uncertainties About and an Entity’s Ability to Continue as a Going Concern

All entities. Effective for the annual period ending after December 15, 2016, and for annual periods and interim periods thereafter. Early application is permitted.

Pronouncement Affects Effective Date and Transition

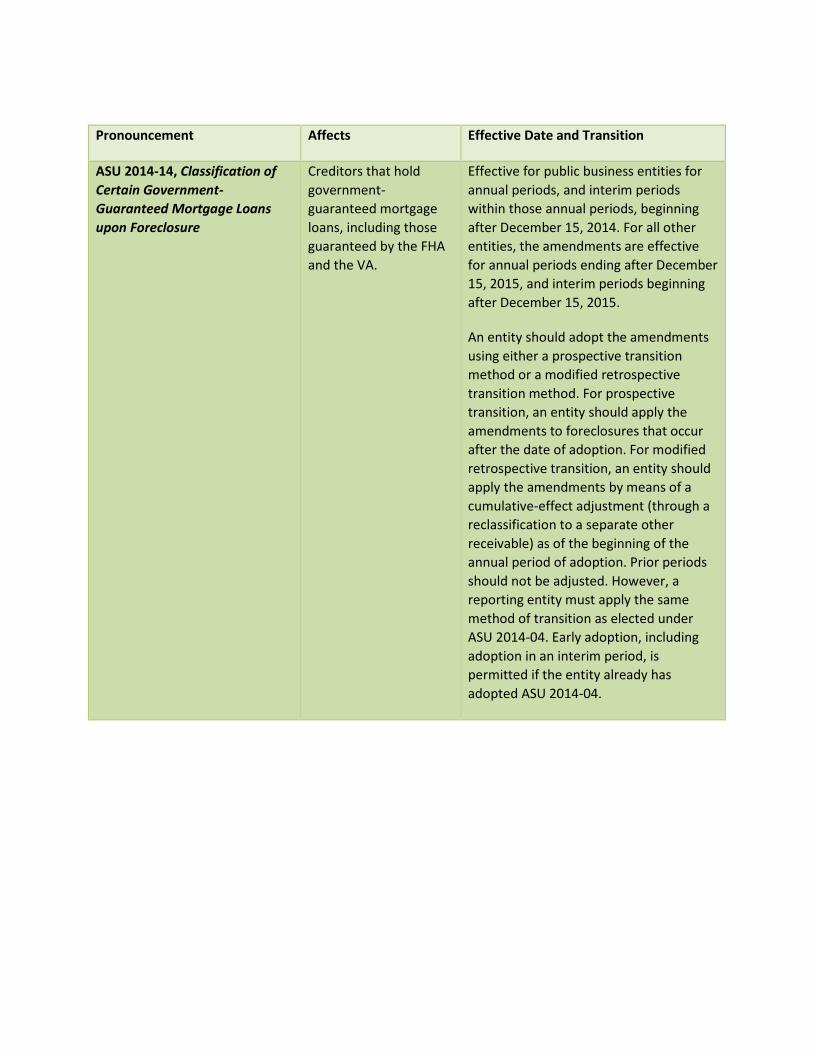

ASU 2014-14, Classification of Certain Government-Guaranteed Mortgage Loans upon Foreclosure

Creditors that hold government-guaranteed mortgage loans, including those guaranteed by the FHA and the VA.

Effective for public business entities for annual periods, and interim periods within those annual periods, beginning after December 15, 2014. For all other entities, the amendments are effective for annual periods ending after December 15, 2015, and interim periods beginning after December 15, 2015.

An entity should adopt the amendments using either a prospective transition method or a modified retrospective transition method. For prospective transition, an entity should apply the amendments to foreclosures that occur after the date of adoption. For modified retrospective transition, an entity should apply the amendments by means of a cumulative-effect adjustment (through a reclassification to a separate other receivable) as of the beginning of the annual period of adoption. Prior periods should not be adjusted. However, a reporting entity must apply the same method of transition as elected under ASU 2014-04. Early adoption, including adoption in an interim period, is permitted if the entity already has adopted ASU 2014-04.

Pronouncement Affects Effective Date and Transition

ASU 2014-12, Accounting for Share-Based Payments When the Terms of an Award Provide That a Performance Target Could Be Achieved after the Requisite Service Period

Entities that issue share-based payments when the terms of an award stipulate that a performance target could be achieved after an employee completes the requisite service period.

Effective for all entities for annual periods and interim periods within those annual periods beginning after December 15, 2015. Early adoption is permitted.

Entities may apply the amendments either (a) prospectively to all awards granted or modified after the effective date or (b) retrospectively to all awards with performance targets that are outstanding as of the beginning of the earliest annual period presented in the financial statements and to all new or modified awards thereafter. If retrospective transition is adopted, the cumulative effect as of the beginning of the earliest annual period presented in the financial statements should be recognized as an adjustment to the opening retained earnings balance at that date.

Pronouncement Affects Effective Date and Transition

ASU 2014-11, Repurchase-to-Maturity Transactions, Repurchase Financings, and Disclosures

Entities that enter into repurchase agreements, securities lending transactions, and repo-to-maturity transactions.

Effective for public business entities for the first interim or annual period beginning after December 15, 2014. For all other entities, the accounting changes are effective for annual periods beginning after December 15, 2014, and interim periods beginning after December 15, 2015. An entity is required to present changes in accounting for transactions outstanding on the effective date as a cumulative-effect adjustment to retained earnings as of the beginning of the period of adoption. Earlier application for a public business entity is prohibited; however, all other entities may elect to apply the requirements for interim periods beginning after December 15, 2014.

For public business entities, the disclosure for certain transactions accounted for as a sale is required to be presented for interim and annual periods beginning after December 15, 2014, and the disclosure for repurchase agreements, securities lending transactions, and repurchase-to-maturity transactions accounted for as secured borrowings is required to be presented for annual periods beginning after December 15, 2014, and for interim periods beginning after March 15, 2015. For all other entities, both new disclosures are required to be presented for annual periods beginning after December 15, 2014, and interim periods beginning after December 15, 2015.

Pronouncement Affects Effective Date and Transition

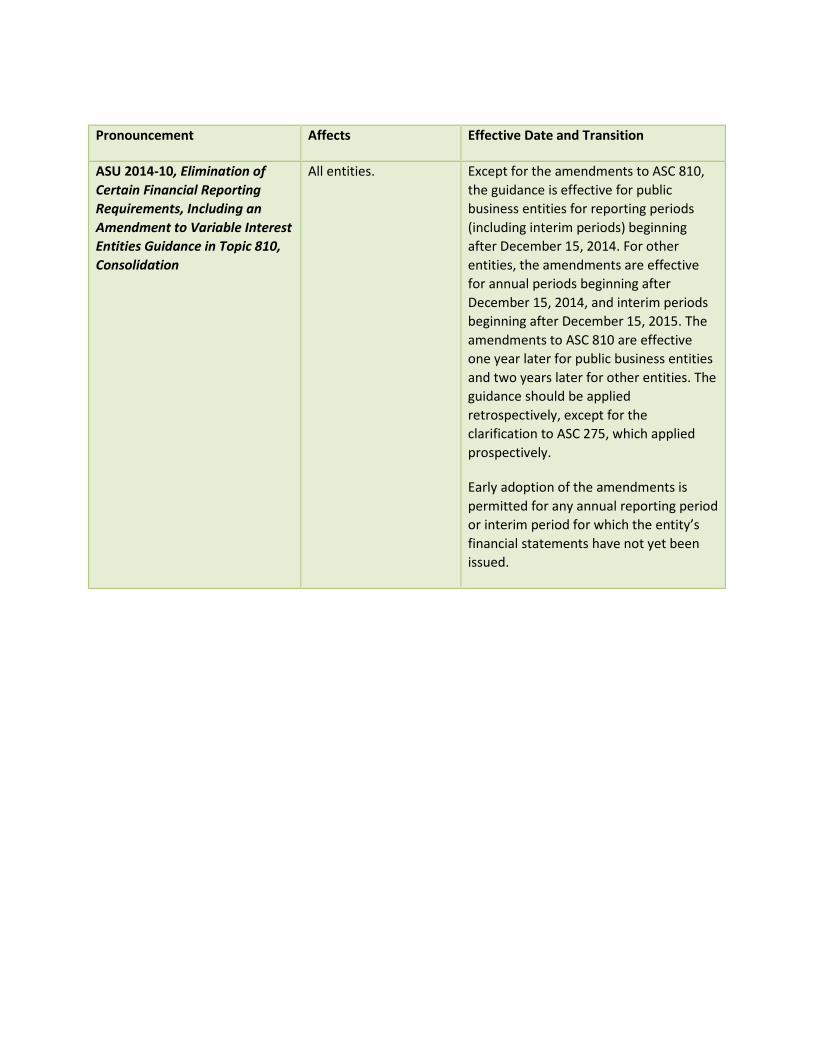

ASU 2014-10, Elimination of Certain Financial Reporting Requirements, Including an Amendment to Variable Interest Entities Guidance in Topic 810, Consolidation

All entities. Except for the amendments to ASC 810, the guidance is effective for public business entities for reporting periods (including interim periods) beginning after December 15, 2014. For other entities, the amendments are effective for annual periods beginning after December 15, 2014, and interim periods beginning after December 15, 2015. The amendments to ASC 810 are effective one year later for public business entities and two years later for other entities. The guidance should be applied retrospectively, except for the clarification to ASC 275, which applied prospectively.

Early adoption of the amendments is permitted for any annual reporting period or interim period for which the entity’s financial statements have not yet been issued.

Pronouncement Affects Effective Date and Transition

ASU 2014-09, Revenue from Contracts with Customers

All entities. For public business entities, certain not-for-profit entities, and certain employee benefit plans, the ASU is effective for annual reporting periods (including interim reporting periods within those periods) beginning after December 15, 2017. Early application is permitted only as of annual reporting periods (including interim reporting periods within those periods) beginning after December 15, 2016.

For all other entities, the ASU is effective for annual reporting periods beginning after December 15, 2018, and interim reporting periods within annual reporting periods beginning after December 15, 2019. All other entities may apply the ASU early as of an annual reporting period beginning after December 15, 2016, including interim reporting periods within that reporting period. All other entities also may apply the guidance in the ASU early as of an annual reporting period beginning after December 15, 2016, and interim reporting periods within annual reporting periods beginning one year after the annual reporting period in which the entity first applies the guidance in the ASU.

An entity should apply the guidance either retrospectively to each prior reporting period presented or retrospectively with the cumulative effect of initially applying guidance at the date of initial application.

Pronouncement Affects Effective Date and Transition

ASU 2014-08, Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity

All entities. Effective for public business entities (and not-for-profit entities that issue securities or are conduit bond obligors) in annual periods beginning on or after December 15, 2014, and interim periods within those annual periods. For all other entities, the guidance is effective in annual periods beginning on or after December 15, 2014, and interim periods beginning on or after December 15, 2015. The guidance is applied prospectively to new disposals and new classifications of disposal groups as held for sale after the effective date.

All entities may early adopt the guidance for new disposals (or new classifications as held for sale) that have not been reported in financial statements previously issued or available for issuance.

ASU 2014-07, Applying Variable Interest Entities Guidance to Common Control Leasing Arrangements—a consensus of the Private Company Council

All entities except public business entities, as defined in the Master Glossary of the FASB Accounting Standards Codification, not-for-profit entities, and employee benefit plans.

Effective for annual periods beginning after December 15, 2014, and interim periods within annual periods beginning after December 15, 2015. Early application is permitted, including application to any period for which the entity’s annual or interim financial statements have not yet been made available for issuance. A private company will apply the alternative, when elected, using a full retrospective approach in which financial statements for each individual prior period presented and the opening balances of the earliest period presented would be adjusted to reflect the period-specific effects of applying the proposed amendments.

Pronouncement Affects Effective Date and Transition

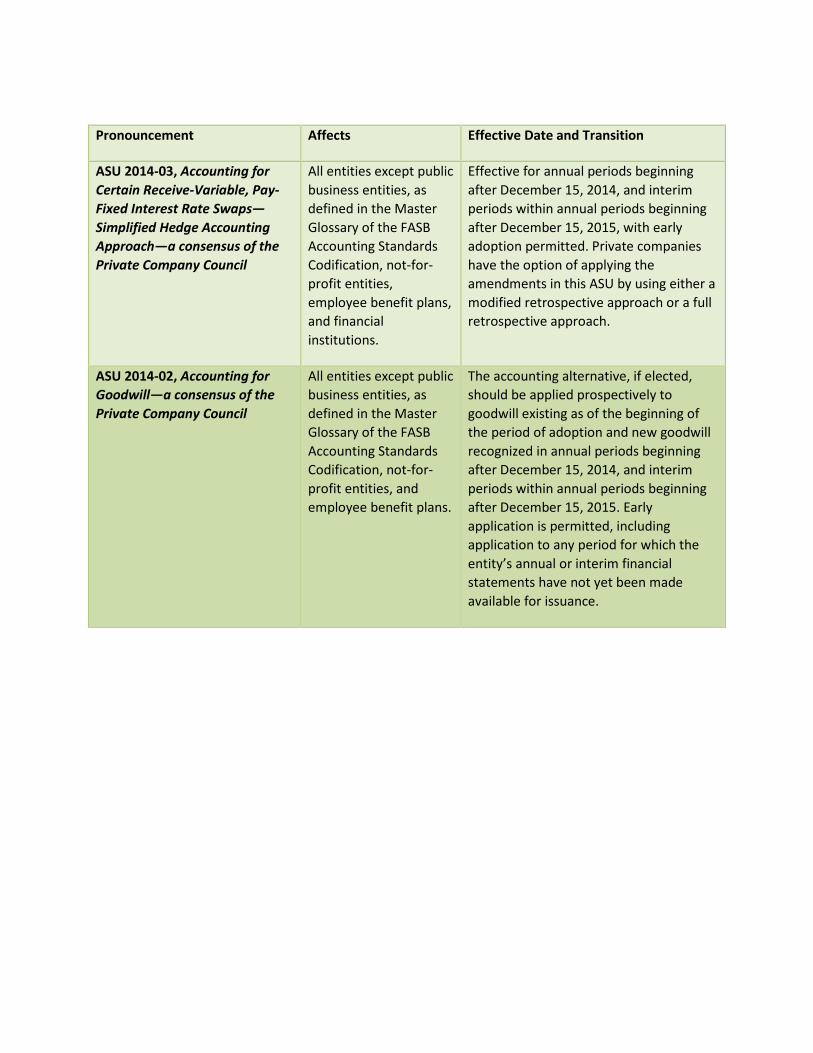

ASU 2014-03, Accounting for Certain Receive-Variable, Pay-Fixed Interest Rate Swaps—Simplified Hedge Accounting Approach—a consensus of the Private Company Council

All entities except public business entities, as defined in the Master Glossary of the FASB Accounting Standards Codification, not-for-profit entities, employee benefit plans, and financial institutions.

Effective for annual periods beginning after December 15, 2014, and interim periods within annual periods beginning after December 15, 2015, with early adoption permitted. Private companies have the option of applying the amendments in this ASU by using either a modified retrospective approach or a full retrospective approach.

ASU 2014-02, Accounting for Goodwill—a consensus of the Private Company Council

All entities except public business entities, as defined in the Master Glossary of the FASB Accounting Standards Codification, not-for-profit entities, and employee benefit plans.

The accounting alternative, if elected, should be applied prospectively to goodwill existing as of the beginning of the period of adoption and new goodwill recognized in annual periods beginning after December 15, 2014, and interim periods within annual periods beginning after December 15, 2015. Early application is permitted, including application to any period for which the entity’s annual or interim financial statements have not yet been made available for issuance.

Pronouncement Affects Effective Date and Transition

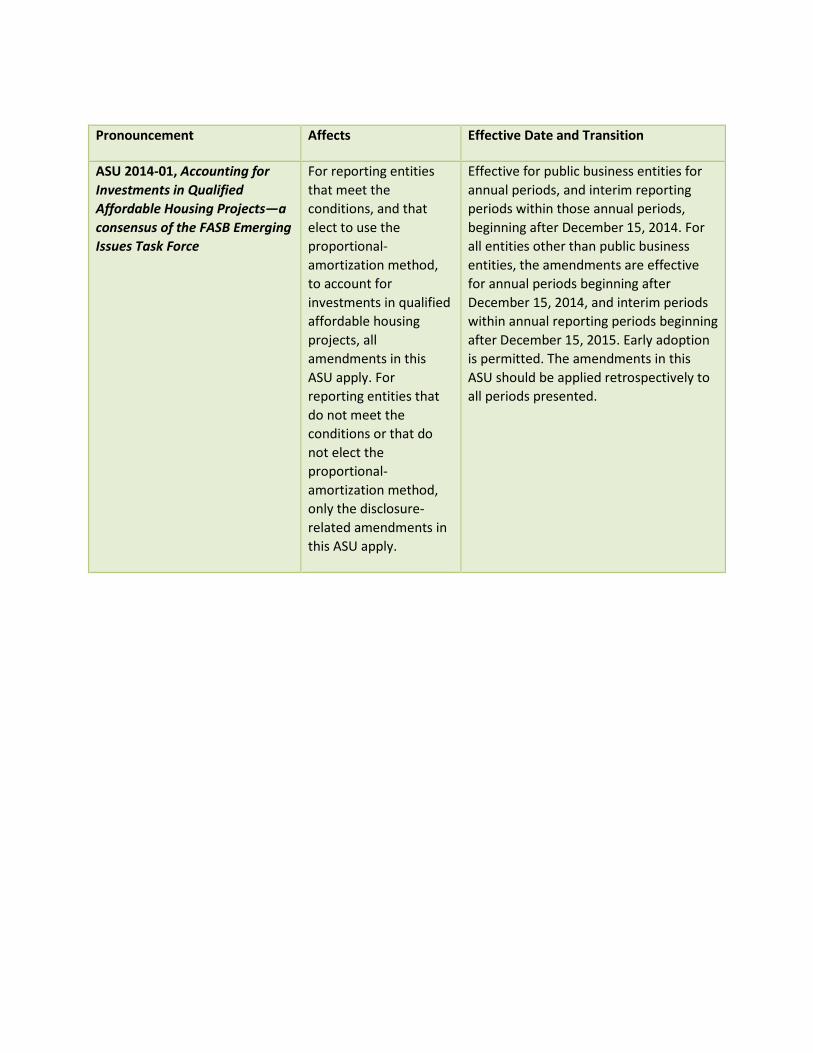

ASU 2014-01, Accounting for Investments in Qualified Affordable Housing Projects—a consensus of the FASB Emerging Issues Task Force

For reporting entities that meet the conditions, and that elect to use the proportional-amortization method, to account for investments in qualified affordable housing projects, all amendments in this ASU apply. For reporting entities that do not meet the conditions or that do not elect the proportional-amortization method, only the disclosure-related amendments in this ASU apply.

Effective for public business entities for annual periods, and interim reporting periods within those annual periods, beginning after December 15, 2014. For all entities other than public business entities, the amendments are effective for annual periods beginning after December 15, 2014, and interim periods within annual reporting periods beginning after December 15, 2015. Early adoption is permitted. The amendments in this ASU should be applied retrospectively to all periods presented.

GASB Implementation Dates Pronouncement Affects Effective Date and Transition

Statement 79, Certain External Investment Pools and Pool Participants

Governmental entities. Effective for reporting periods beginning after June 15, 2015, except for certain provisions on portfolio quality, custodial credit risk, and shadow pricing. Those provisions are effective for reporting periods beginning after December 15, 2015. Earlier application is encouraged.

Statement 78, Pensions Provided Through Certain Multiple-Employer Defined Benefit Pension Plans

Governmental entities. Effective for reporting periods beginning after December 15, 2015. Earlier application is encouraged.

Statement 77, Tax Abatement Disclosures

Governmental entities. Effective for reporting periods beginning after December 15, 2015. Earlier application is encouraged.

Statement 76, The Hierarchy of Generally Accepted Accounting Principles for State and Local Governments

Governmental entities. Effective for reporting periods beginning after June 15, 2015. Earlier application is encouraged.

Statement 75, Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions

Governmental entities. Effective for fiscal years beginning after June 15, 2017. Early adoption is encouraged.

Statement 74, Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans

Governmental entities. Effective for financial statements for periods beginning after June 15, 2016. Early adoption is encouraged.

Pronouncement Affects Effective Date and Transition

Statement 73, Accounting and Financial Reporting for Pensions and Related Assets That Are Not within the Scope of GASB Statement 68, and Amendments to Certain Provisions of GASB Statements 67 and 68

Governmental entities. Effective for fiscal years beginning after June 15, 2015—except those provisions that address employers and governmental nonemployer contributing entities for pensions that are not within the scope of Statement 68, which are effective for financial statements for fiscal years beginning after June 15, 2016. Early adoption is encouraged.

Statement 72, Fair Value Measurement and Application

Governmental entities. Effective for financial statements for periods beginning after June 15, 2015. Early adoption is encouraged.

Statement 71, Pension Transition for Contributions Made Subsequent to the Measurement Date

Governmental entities Effective for fiscal years beginning after June 15, 2014.

Statement 68, Accounting and Financial Reporting for Pensions—an amendment of GASB Statement No. 27

Governmental entities Effective for financial statements for fiscal years beginning after June 15, 2014. Early application is encouraged.

APPENDIX B

Illustrative Disclosures for Recently Issued Accounting Pronouncements

For the Quarter Ended December 31, 2015

The illustrative disclosures below are presented in plain English. Please review each disclosure for its applicability to your organization and the need for disclosure in your organization’s financial statements.