3pl pricing trends and practices - chainalytics

TRANSCRIPT

3PL Pricing Trends and Practices

Dr. Chris Caplice - MIT Matthew Harding – Chainalytics

October 3, 2011

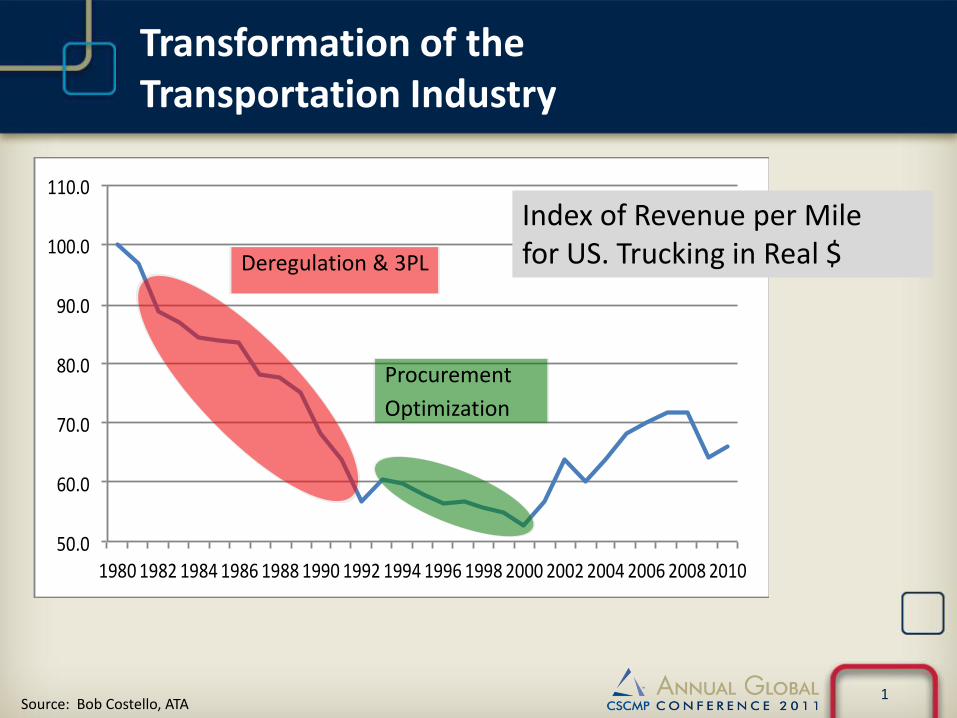

50.0

60.0

70.0

80.0

90.0

100.0

110.0

1980198219841986198819901992199419961998200020022004200620082010

Index of Revenue per Mile for US. Trucking in Real $ Deregulation & 3PL

Procurement

Optimization

Source: Bob Costello, ATA 1

Transformation of the Transportation Industry

Transformation of the Transportation Industry

“We’ve moved from being a trucking company that has technology to basically a technology company that just happens to

have trucks,”

Scott Davis, CEO UPS

Transformation of the Transportation Industry

• Evolution of Critical Skills Required for 3PLs

– Operational Expertise

• Expected for all 3PLs today

• Essentially the price of entry

– Analytical Expertise

• Serves as a competitive differentiator

• Allows for de-commoditization of services

• Provides opportunity for greater margins

3

Why are 3PLs different?

• 3PLs have a unique view into the market

S1

C1

C4

C3

C2

S2

Each shipper has a limited view of only those carriers that they work with and they only see how

they work with them!

Each carrier has a limited view of only those shippers that they work with and how they work with

them!

3PL

3PLs are uniquely positioned between shippers and carriers.

4

Rate “Trough” 2009-2010

Fuel Shock 2010-2011

Note that the line haul rates are still below 2006 levels!

1st Level of Analysis: Historical Rates

5

1st Level of Analysis: Historical Rates

$1.390

$1.400

$1.410

$1.420

$1.430

$1.440

$1.450

$1.460

$1.470

$1.480

$1.490

$1.500

$1.510

$1.520

$1.530

$1.540

Oct-06

Jan-07

Apr-07

Jul-0

7

Oct-07

Jan-08

Apr-08

Jul-0

8

Oct-08

Jan-09

Apr-09

Jul-0

9

Oct-09

Jan-10

Apr-10

Jul-1

0

Oct-10

Jan-11

Apr-11

CostperM

ile

LinehaulCostPerMileforLHDV

LinehaulCPM

6

• Objective: – Develop an estimate of the “contract market” cost per load for

truckload transportation for any mode, lane, and condition.

• Technique: – Collect a large set of transactional cost data from multiple

companies

– Harmonize and standardize the data set

– Estimate the ‘best-fit’ line between all of the observations using regression

– Isolate the impact on CPL for individual factors (distance, equipment, etc.)

• Output: – Snapshot comparison of each firm’s lanes to the “contract

market”

– Tool to estimate ‘contract market” rates for new lanes

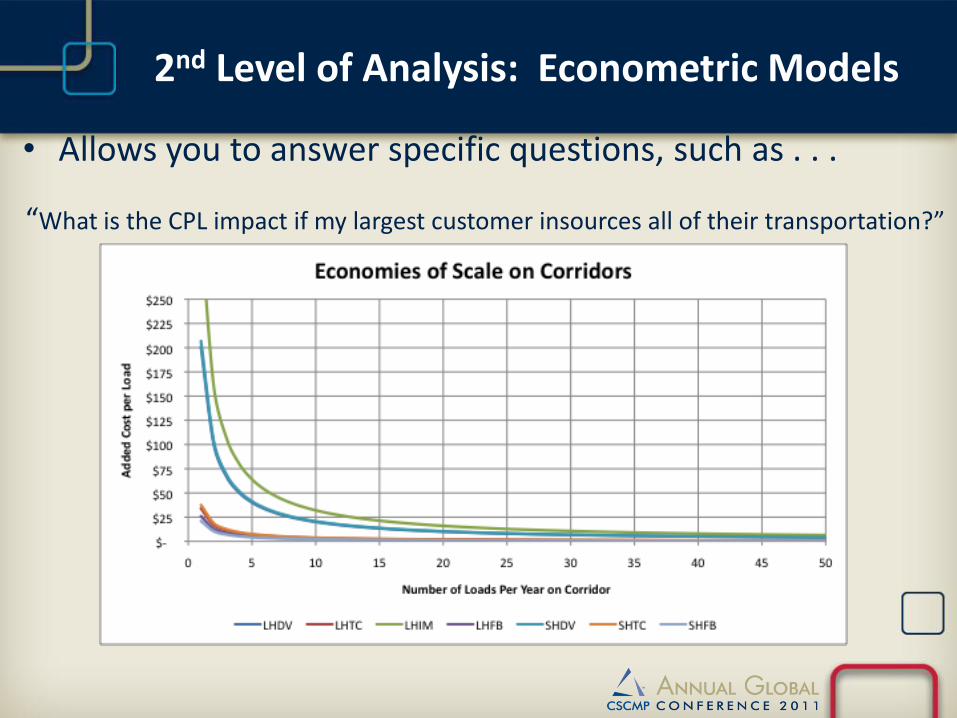

2nd Level of Analysis: Econometric Models

• Example, portion of the current Longhaul Dry Van model: (“All In” rates with fuel @ $3.00 per gallon)

CPL = $722 + $1.34 (Distance) + $200 / (AnnualCorridorVolume) + $64 (MultiStopFlag) . . .

• Two unique benefits of this approach – Ability to isolate the impact of individual factors

– Ability to quantify the regional effect at a very detailed level

2nd Level of Analysis: Econometric Models

• Allows you to answer specific questions, such as . . .

“What is the CPL impact if my largest customer insources all of their transportation?”

2nd Level of Analysis: Econometric Models

• How can we capture the backhaul effect? – Created >100 Regional Value Flags across North America – Each captures financial impact of starting/ending a trip in that area – Each shipment is flagged to its origin and destination location – Smaller areas (3DZ) are mapped to these regions

What are the benefits?

– Enables us to estimate rates on lanes where we have no history – O&D effects are isolated

– Allows for very detailed mapping of regional value effects – good for site location

2nd Level of Analysis: Econometric Models

Heat Map of LHDV Rate Imbalances

2nd Level of Analysis: Econometric Models

3rd Level of Analysis: Sense-Making

• Most 3PLs do not realize the value of their own data

• Value in combining different data sources

– Procurement (bid) data

– Transactional shipment records

– Policy and practices

• Provides opportunity for “Sense-Making”

– How do policies & practices influence rates?

– How should fuel be managed?

– How should my pricing be aligned?

12

Freight Markets are Vast

FOR-HIRE DOMESTIC MARKET Approx. $300B

Understanding the effects of perfect competition & truckload contracts

2010 Transport Topics

Top 10 Truckload Carriers

~12B

Chainalytics Truckload

Benchmarking

Consortium

~23B

“Large” $210MM

Shipper

13

0

20

40

60

80

100

120

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

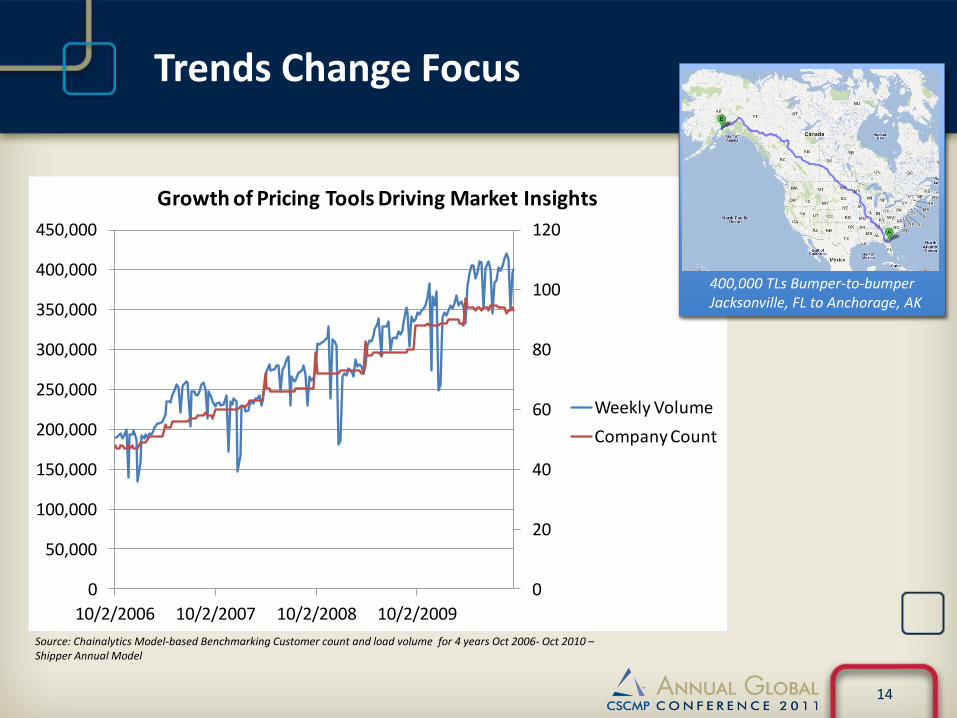

10/2/2006 10/2/2007 10/2/2008 10/2/2009

Growth of Pricing Tools Driving Market Insights

Weekly Volume

Company Count

Trends Change Focus

400,000 TLs Bumper-to-bumper Jacksonville, FL to Anchorage, AK

Source: Chainalytics Model-based Benchmarking Customer count and load volume for 4 years Oct 2006- Oct 2010 – Shipper Annual Model

14

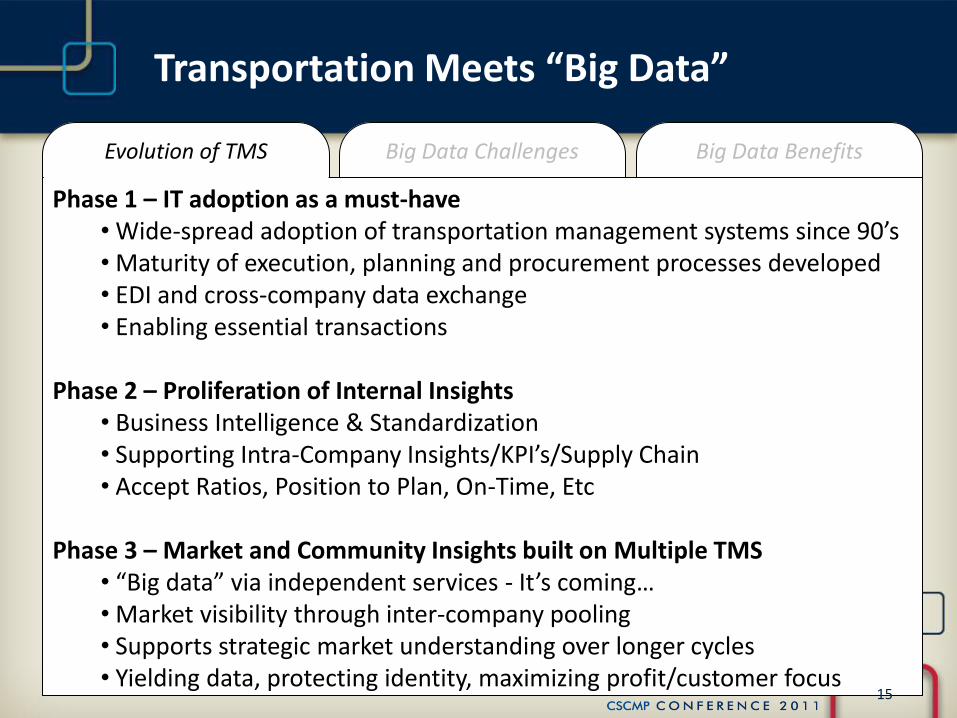

Transportation Meets “Big Data”

Evolution of TMS Big Data Challenges Big Data Benefits

Phase 1 – IT adoption as a must-have • Wide-spread adoption of transportation management systems since 90’s • Maturity of execution, planning and procurement processes developed • EDI and cross-company data exchange • Enabling essential transactions

Phase 2 – Proliferation of Internal Insights

• Business Intelligence & Standardization • Supporting Intra-Company Insights/KPI’s/Supply Chain • Accept Ratios, Position to Plan, On-Time, Etc

Phase 3 – Market and Community Insights built on Multiple TMS

• “Big data” via independent services - It’s coming… • Market visibility through inter-company pooling • Supports strategic market understanding over longer cycles • Yielding data, protecting identity, maximizing profit/customer focus

15

Evolution of TMS Big Data Challenges Big Data Benefits

The Focus of Independents Data Throughput /Technology

• Capture • Storage • Distribution

Process/Intellect

• Analytics • Research • Relevance

Innovative Service & Application

• Pricing Support • Visualization • Sharing • Searching • Trending • Community Development • Integrating In/Outflows

Transportation Meets “Big Data”

16

Evolution of TMS Big Data Challenges Big Data Benefits

Quantitative Analysis -Pricing Benchmarks -Business Trends -Fuel Impacts -Regional Seasonality -Customer Solutions -Industry Specific Focus - Surveys - Cost / Service Tradeoffs - Buyer Market Identity - Contractual Choice - Debunking Common Myths

Supporting Execution, Planning & Strategy

- Load Planning - Procurement Strategy - Account Management - Network Design - Facility Location - Policy Changes

Transportation Meets “Big Data”

17

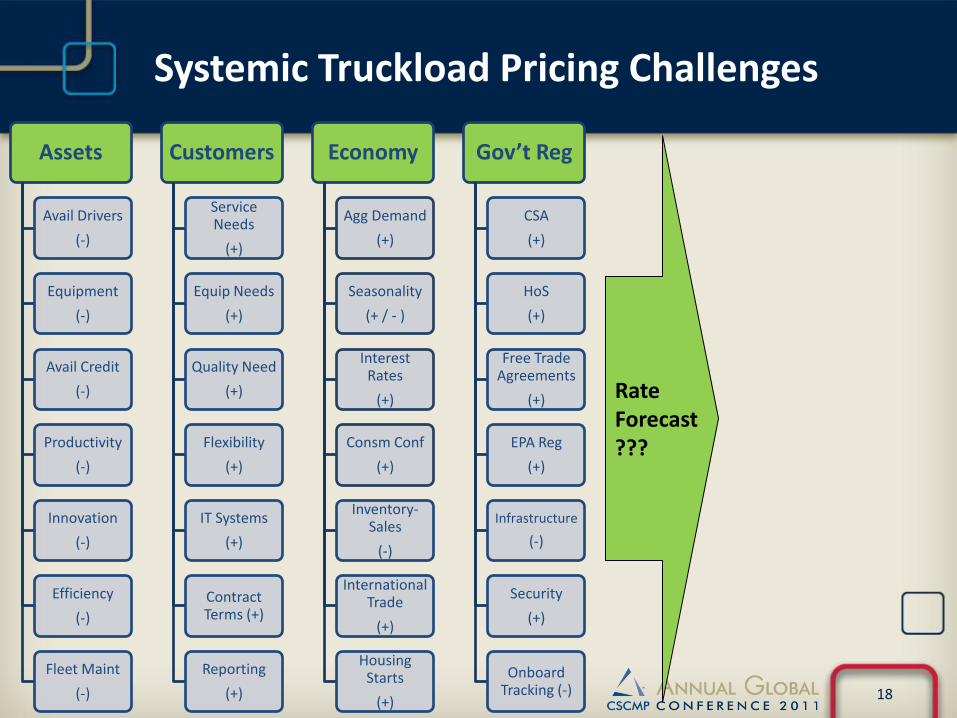

Systemic Truckload Pricing Challenges

Assets

Avail Drivers

(-)

Equipment

(-)

Avail Credit

(-)

Productivity

(-)

Innovation

(-)

Efficiency

(-)

Fleet Maint

(-)

Customers

Service Needs

(+)

Equip Needs

(+)

Quality Need

(+)

Flexibility

(+)

IT Systems

(+)

Contract Terms (+)

Reporting

(+)

Economy

Agg Demand

(+)

Seasonality

(+ / - )

Interest Rates

(+)

Consm Conf

(+)

Inventory-Sales

(-)

International Trade

(+)

Housing Starts

(+)

Gov’t Reg

CSA

(+)

HoS

(+)

Free Trade Agreements

(+)

EPA Reg

(+)

Infrastructure

(-)

Security

(+)

Onboard Tracking (-)

Rate Forecast ???

18

Assets

Avail Drivers

(-)

Equipment

(-)

Avail Credit

(-)

Productivity

(-)

Innovation

(-)

Efficiency

(-)

Fleet Maint

(-)

Customers

Service Needs

(+)

Equip Needs

(+)

Quality Need

(+)

Flexibility

(+)

IT Systems

(+)

Contract Terms (+)

Reporting

(+)

Economy

Agg Demand

(+)

Seasonality

(+ / - )

Interest Rates

(+)

Consm Conf

(+)

Inventory-Sales

(-)

International Trade

(+)

Housing Starts

(+)

Gov’t Reg

CSA

(+)

HoS

(+)

Free Trade Agreements

(+)

EPA

(+)

Infrastructure

(-)

Security

(+)

Onboard Tracking (-)

Systemic Truckload Pricing Challenges

Rate Forecast

Reality: Cause and Effect relationships are too numerous, complex and dynamic Big Data Concept: Multi-cyclical approach to defray interdependencies and isolate systemic relationships

19

Developing Aggregate Insights

Going beyond the transaction to yield strategic insight… A single econometric model generates ~50MM possible benchmarks Since January 1.4B 3PL Benchmarks Created

Big Data

Customer

Carrier

Geography

Policy

Seasonal

Effects

Service

20

The Basics

$-

$200

$400

$600

$800

$1,000

$1,200

Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11

Philadelphia - Chicago Dry Van

All-In

Fuel

Linehaul

21

Trends in 3PL Buy-side Spot vs. Contract Rates

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Sep

-10

Oct

-10

No

v-10

Dec

-10

Jan

-11

Feb

-11

Mar

-11

Ap

r-1

1

May

-11

Jun

-11

Jul-

11

Au

g-1

1

Per

cen

tage

to M

arke

t Annual Market

Contract Rates

Spot Rates

Source: Chainalytics Model-based Benchmarking 3PL Annual Market Models – September 2011 Release

22

y = 0.0006x + 1.9153R² = 0.7475

$-

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

0 1000 2000 3000 4000 5000

DO

E -

#2 D

iese

l

Weekly Spot Volume

Correlation - Weekly Spot Market Volume to Price of Diesel

Diesel Price

Linear (Diesel Price)

Relationships and Market Effects

Source: Chainalytics Model-based Benchmarking 3PL Annual Market Models – September 2011 Release

23

Relationships and Market Effects

y = 0.0006x + 1.9153R² = 0.7475

$-

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

0 1000 2000 3000 4000 5000

DO

E -

#2 D

iese

l

Weekly Spot Volume

Correlation - Weekly Spot Market Volume to Price of Diesel

Diesel Price

Linear (Diesel Price)

Source: Chainalytics Model-based Benchmarking 3PL Annual Market Models – September 2011 Release

24

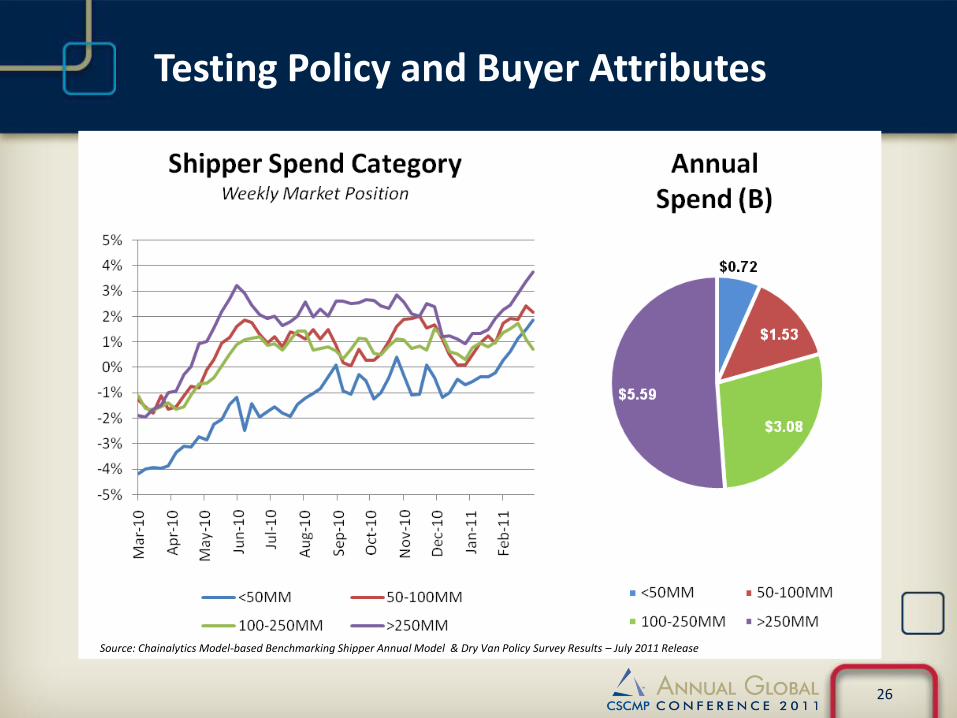

Testing Policy and Buyer Attributes

Source: Chainalytics Model-based Benchmarking Shipper Annual Model & Dry Van Policy Survey Results – July 2011 Release

25

Testing Policy and Buyer Attributes

Source: Chainalytics Model-based Benchmarking Shipper Annual Model & Dry Van Policy Survey Results – July 2011 Release

26

Testing Policy and Buyer Attributes

Source: Chainalytics Model-based Benchmarking Shipper Annual Model & Dry Van Policy Survey Results – July 2011 Release

27

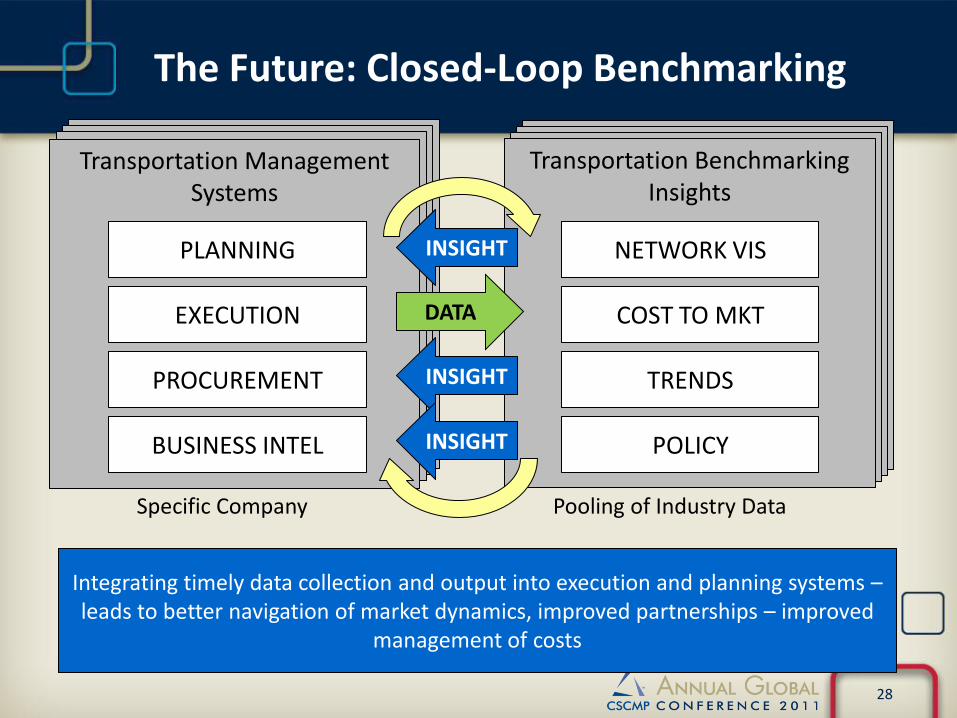

Transportation Benchmarking

Insights Transportation Benchmarking

Insights Transportation Benchmarking

Insights

Transportation Benchmarking

Insights Transportation Benchmarking

Insights Transportation Benchmarking

Insights Transportation Management

Systems

The Future: Closed-Loop Benchmarking

PLANNING

EXECUTION

PROCUREMENT

BUSINESS INTEL

Transportation Benchmarking Insights

COST TO MKT

NETWORK VIS

TRENDS

Specific Company Pooling of Industry Data

DATA

INSIGHT

INSIGHT

INSIGHT POLICY

Integrating timely data collection and output into execution and planning systems – leads to better navigation of market dynamics, improved partnerships – improved

management of costs

28

Final remarks

• Markets are too complex and too dynamic to efficiently rationalize in isolation

• Buyer strengths grounded in adaptation

– Strategies are highly cyclical

– Core capacity and leverage offset by fragmentation and regional focus

• 3PLs need to be aware of new frontier of “Big Data” concepts

– Many are now adopting multiple sources into planning and execution systems

– Insights provide valuable opportunities to better manage volatility and customer relationships

– Essential to growth as uses become more common

29