3q11 results - fleury medicina e saúderi.fleury.com.br/fleury/web/arquivos/3q11...

TRANSCRIPT

TODOS OS DIREITOS RESERVADOS – 2011

3Q11 Results

November, 2011

FLRY3

The 15th most innovative Brazilian company by

“Epoca Negocios” magazine.

Disclaimer

This presentation may contain forward-looking statements. Such statements are not statements ofhistorical facts and reflect the beliefs and expectations of the Company s management. The words“anticipates”, “believes”, “estimates”, “expects”, “forecasts”, “plans”, “predicts”, “project”, “targets”and similar words are intended to identify these statements, which necessarily involve known andunknown risks and uncertainties. Known risks and uncertainties include but are not limited to theimpact of competitive services and pricing market acceptance of services, service transactions by theCompany and its competitors, regulatory approval, currency fluctuations, changes in service mixoffered, and other risks described in the Company s registration statement. Forward-lookingstatements speak only as of the date they are made and the Fleury Group does not undertake anyobligation to update them in light of new information or future developments.

All figures are compared to 3Q2010

except when stated otherwise

Operational Highlights

3

The new areas “Customer Intimacy” and “Organizational Culture” have been added tothe structure, reporting directly to the CEO. The reason is to reinforce the clear linkbetween growth and improved relationship with clients and physicians.

Grupo Fleury launched the Corporate University’s new building, with 1600 m2 and acapacity to train 300 persons simultaneously. This initiative reflects one of Grupo Fleury’smost important beliefs: to allow the Company to keep Sustainable Growth whileestablishing leading edge quality standards and reinforcing market differentiation.

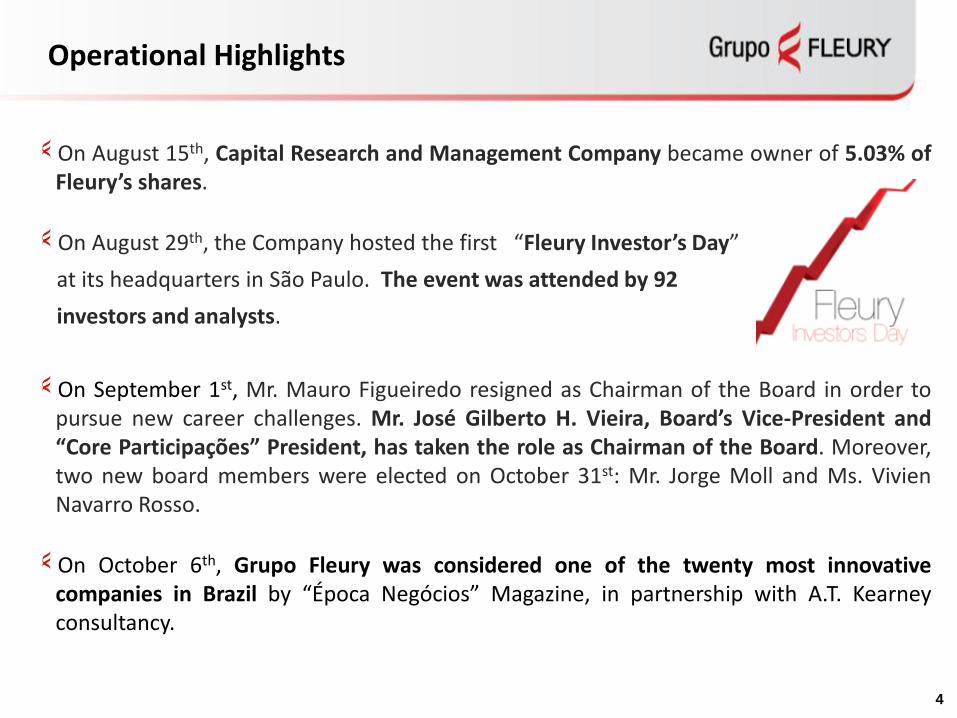

On August 15th, Capital Research and Management Company became owner of 5.03% ofFleury’s shares.

On August 29th, the Company hosted the first “Fleury Investor’s Day”

at its headquarters in São Paulo. The event was attended by 92

investors and analysts.

On September 1st, Mr. Mauro Figueiredo resigned as Chairman of the Board in order topursue new career challenges. Mr. José Gilberto H. Vieira, Board’s Vice-President and“Core Participações” President, has taken the role as Chairman of the Board. Moreover,two new board members were elected on October 31st: Mr. Jorge Moll and Ms. VivienNavarro Rosso.

On October 6th, Grupo Fleury was considered one of the twenty most innovativecompanies in Brazil by “Época Negócios” Magazine, in partnership with A.T. Kearneyconsultancy.

Operational Highlights

4

Financial Highlights

5

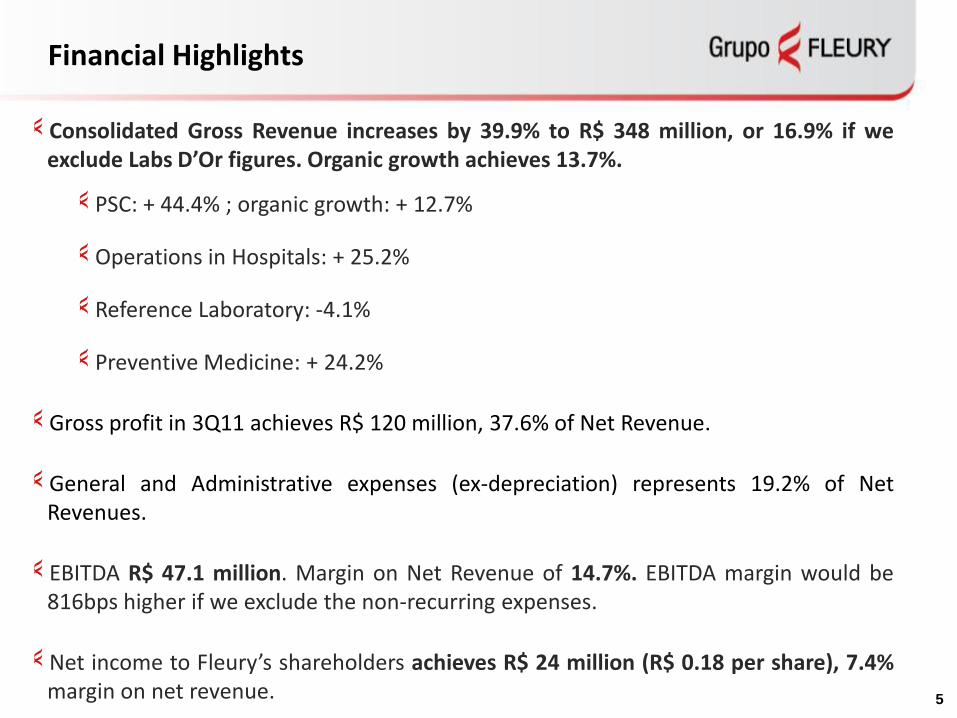

Consolidated Gross Revenue increases by 39.9% to R$ 348 million, or 16.9% if weexclude Labs D’Or figures. Organic growth achieves 13.7%.

PSC: + 44.4% ; organic growth: + 12.7%

Operations in Hospitals: + 25.2%

Reference Laboratory: -4.1%

Preventive Medicine: + 24.2%

Gross profit in 3Q11 achieves R$ 120 million, 37.6% of Net Revenue.

General and Administrative expenses (ex-depreciation) represents 19.2% of NetRevenues.

EBITDA R$ 47.1 million. Margin on Net Revenue of 14.7%. EBITDA margin would be816bps higher if we exclude the non-recurring expenses.

Net income to Fleury’s shareholders achieves R$ 24 million (R$ 0.18 per share), 7.4%margin on net revenue.

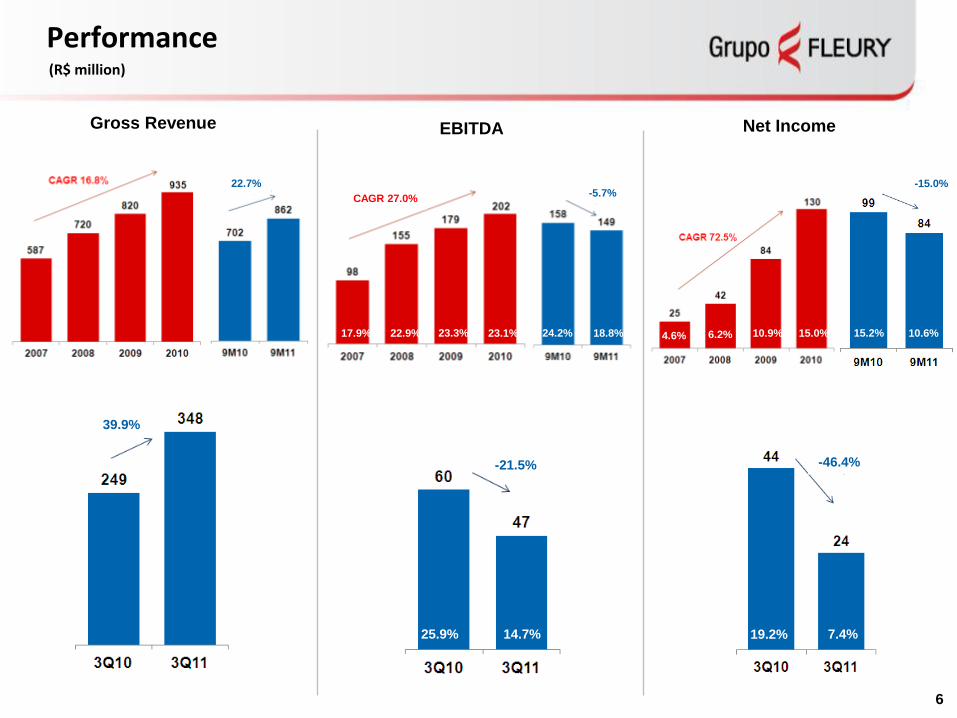

Performance(R$ million)

6

Gross Revenue EBITDA Net Income

25.9% 14.7% 19.2% 7.4%

17.9% 22.9% 23.3% 23.1% 24.2% 18.8% 4.6% 6.2% 10.9% 15.0% 15.2% 10.6%

22.7%

39.9%

-5.7%

-21.5%

-15.0%

-46.4%

CAGR 27.0%

7

Gross Revenue 3Q11

¹ Clinical Trials

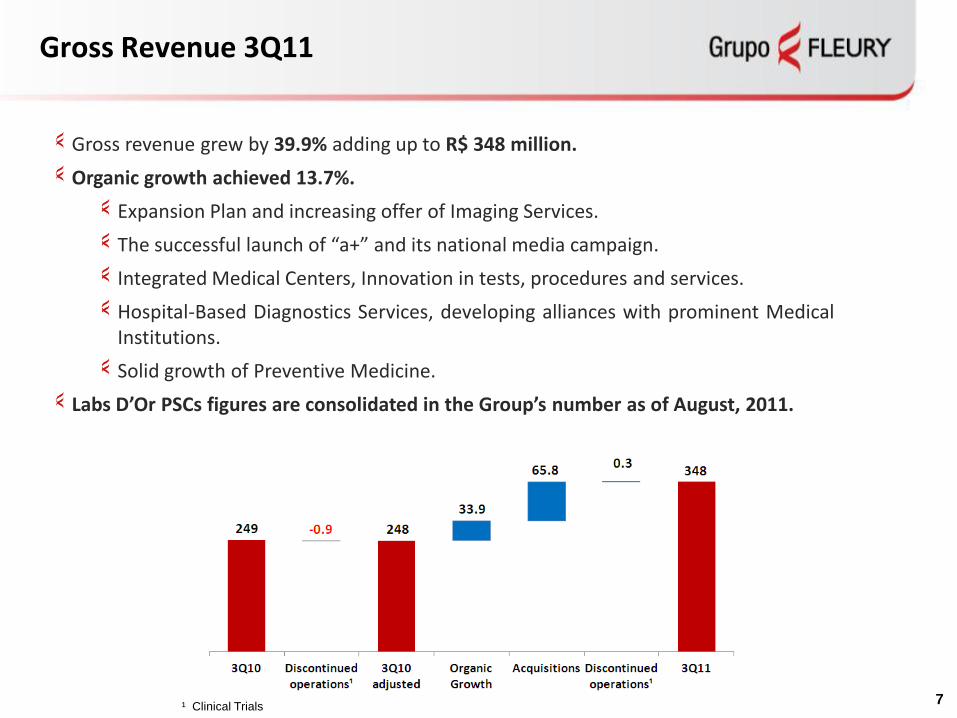

Gross revenue grew by 39.9% adding up to R$ 348 million.

Organic growth achieved 13.7%.

Expansion Plan and increasing offer of Imaging Services.

The successful launch of “a+” and its national media campaign.

Integrated Medical Centers, Innovation in tests, procedures and services.

Hospital-Based Diagnostics Services, developing alliances with prominent MedicalInstitutions.

Solid growth of Preventive Medicine.

Labs D’Or PSCs figures are consolidated in the Group’s number as of August, 2011.

8

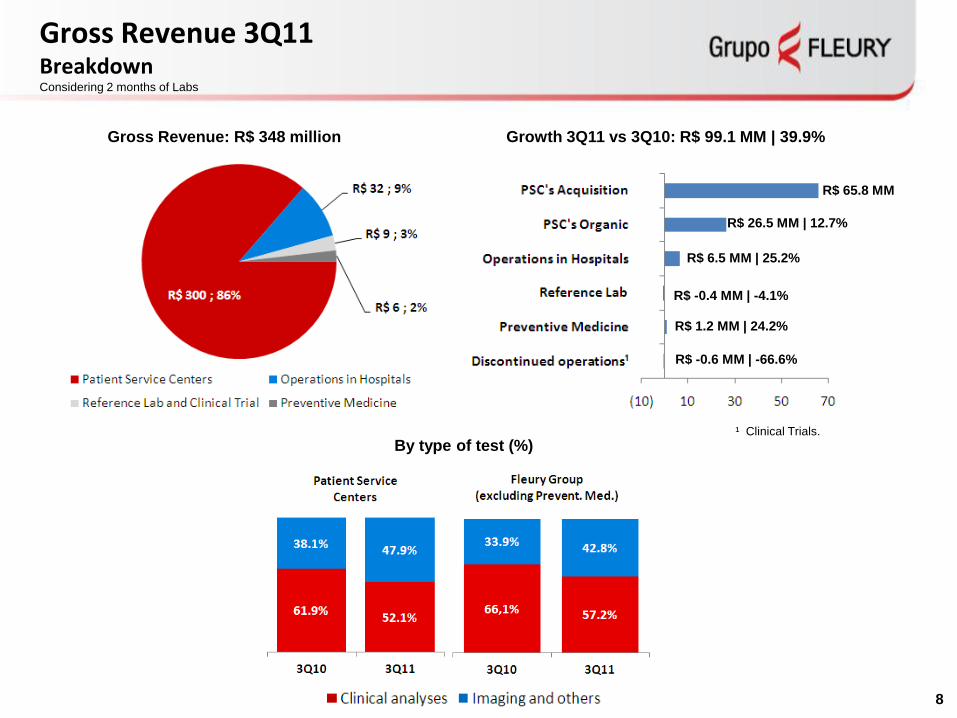

Gross Revenue 3Q11 Breakdown

Gross Revenue: R$ 348 million Growth 3Q11 vs 3Q10: R$ 99.1 MM | 39.9%

R$ 65.8 MM

R$ 6.5 MM | 25.2%

R$ -0.4 MM | -4.1%

R$ 1.2 MM | 24.2%

R$ -0.6 MM | -66.6%

¹ Clinical Trials.

R$ 26.5 MM | 12.7%

Considering 2 months of Labs

By type of test (%)

Patient Service CenterBusiness lines performance

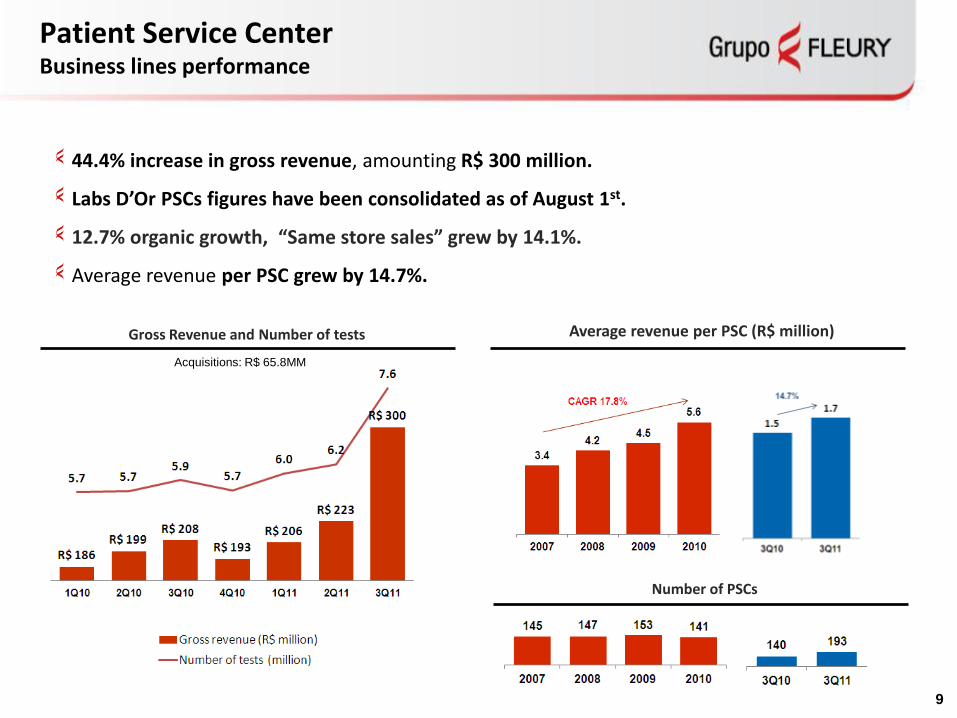

44.4% increase in gross revenue, amounting R$ 300 million.

Labs D’Or PSCs figures have been consolidated as of August 1st.

12.7% organic growth, “Same store sales” grew by 14.1%.

Average revenue per PSC grew by 14.7%.

Gross Revenue and Number of tests

9

Average revenue per PSC (R$ million)

Number of PSCs

Acquisitions: R$ 65.8MM

Patient Service CenterBusiness lines performance

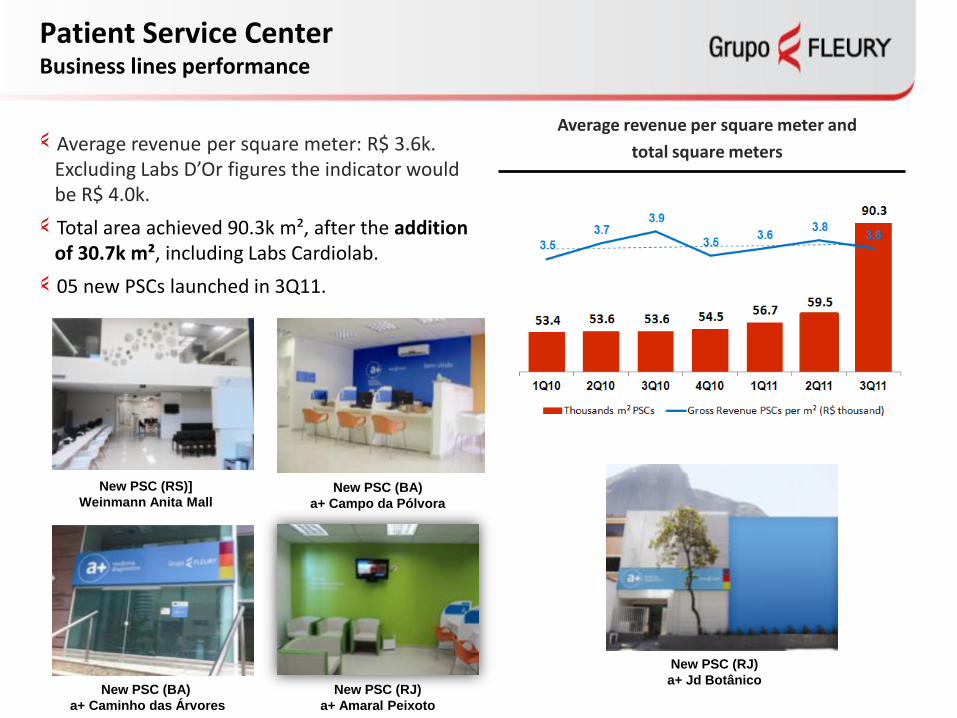

Average revenue per square meter: R$ 3.6k. Excluding Labs D’Or figures the indicator would be R$ 4.0k.

Total area achieved 90.3k m², after the addition of 30.7k m², including Labs Cardiolab.

05 new PSCs launched in 3Q11.

Average revenue per square meter and

total square meters

New PSC (RS)]

Weinmann Anita Mall

New PSC (RJ)

a+ Jd BotânicoNew PSC (RJ)

a+ Amaral Peixoto

New PSC (BA)

a+ Caminho das Árvores

New PSC (BA)

a+ Campo da Pólvora

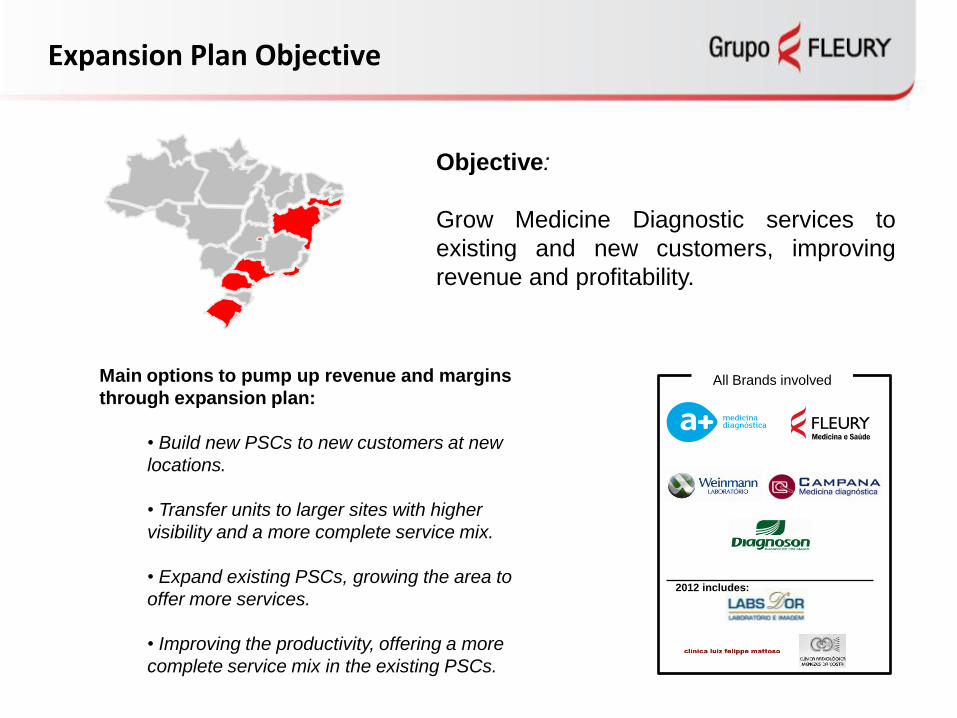

Expansion Plan Objective

All Brands involved

2012 includes:

Main options to pump up revenue and margins

through expansion plan:

• Build new PSCs to new customers at new

locations.

• Transfer units to larger sites with higher

visibility and a more complete service mix.

• Expand existing PSCs, growing the area to

offer more services.

• Improving the productivity, offering a more

complete service mix in the existing PSCs.

Objective:

Grow Medicine Diagnostic services to

existing and new customers, improving

revenue and profitability.

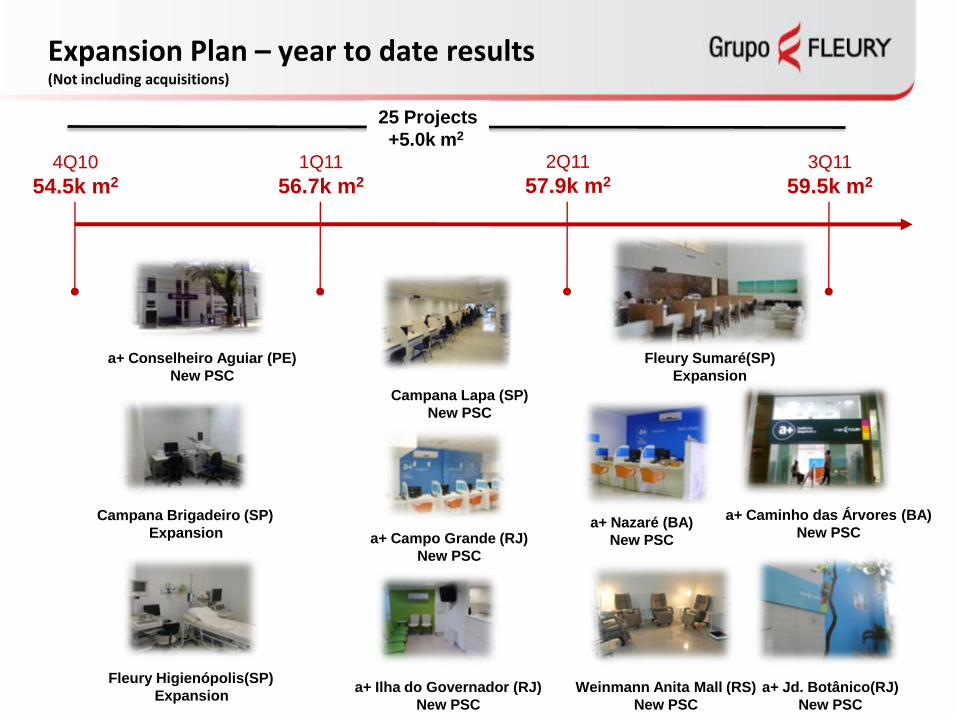

Expansion Plan – year to date results(Not including acquisitions)

4Q10

54.5k m2

1Q11

56.7k m2

2Q11

57.9k m2

3Q11

59.5k m2

a+ Conselheiro Aguiar (PE)

New PSC

Campana Brigadeiro (SP)

Expansion

Campana Lapa (SP)

New PSC

a+ Campo Grande (RJ)

New PSC

a+ Ilha do Governador (RJ)

New PSC

Fleury Sumaré(SP)

Expansion

a+ Nazaré (BA)

New PSC

a+ Jd. Botânico(RJ)

New PSC

a+ Caminho das Árvores (BA)

New PSC

Weinmann Anita Mall (RS)

New PSC

Fleury Higienópolis(SP)

Expansion

25 Projects

+5.0k m2

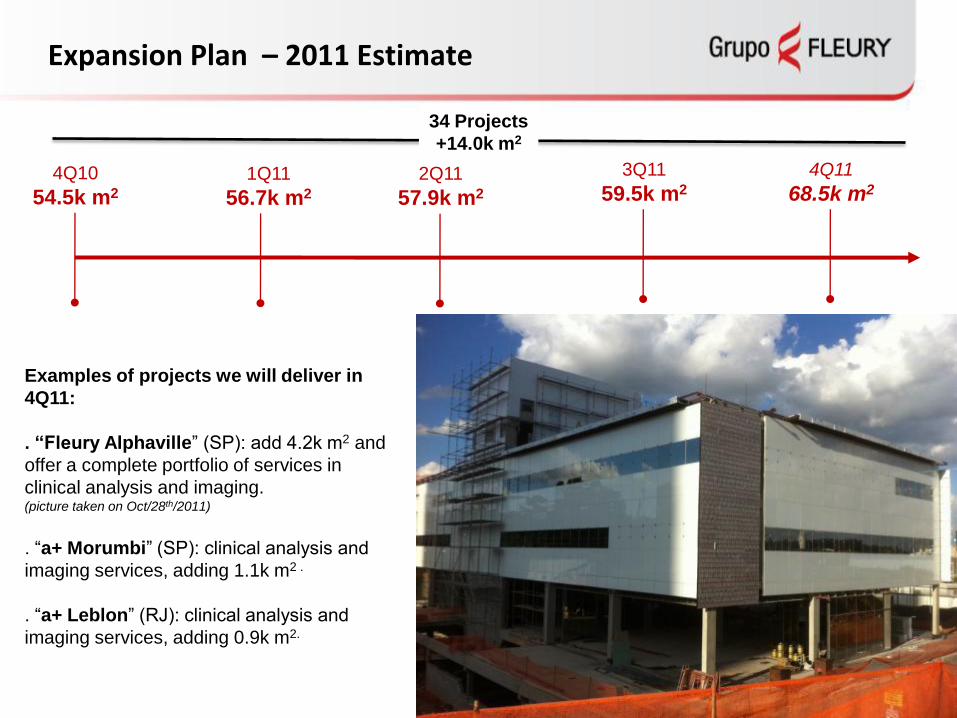

Expansion Plan – 2011 Estimate

4Q10

54.5k m2

1Q11

56.7k m2

2Q11

57.9k m2

3Q11

59.5k m2

34 Projects

+14.0k m2

4Q11

68.5k m2

Examples of projects we will deliver in

4Q11:

. “Fleury Alphaville” (SP): add 4.2k m2 and

offer a complete portfolio of services in

clinical analysis and imaging. (picture taken on Oct/28th/2011)

. “a+ Morumbi” (SP): clinical analysis and

imaging services, adding 1.1k m2 .

. “a+ Leblon” (RJ): clinical analysis and

imaging services, adding 0.9k m2.

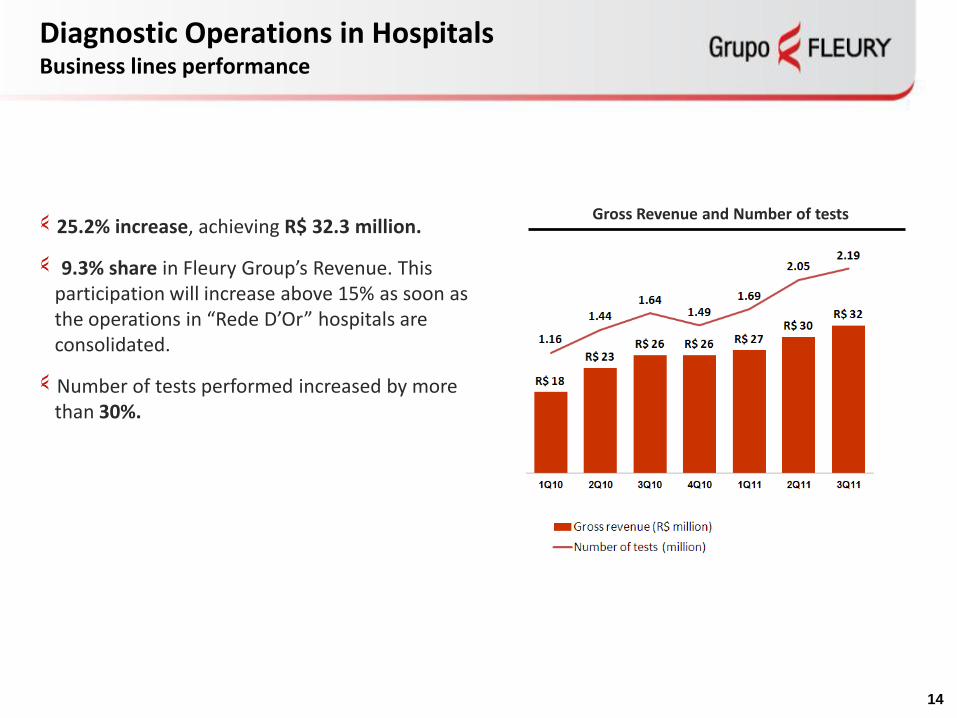

Diagnostic Operations in HospitalsBusiness lines performance

25.2% increase, achieving R$ 32.3 million.

9.3% share in Fleury Group’s Revenue. This participation will increase above 15% as soon as the operations in “Rede D’Or” hospitals are consolidated.

Number of tests performed increased by more than 30%.

14

Gross Revenue and Number of tests

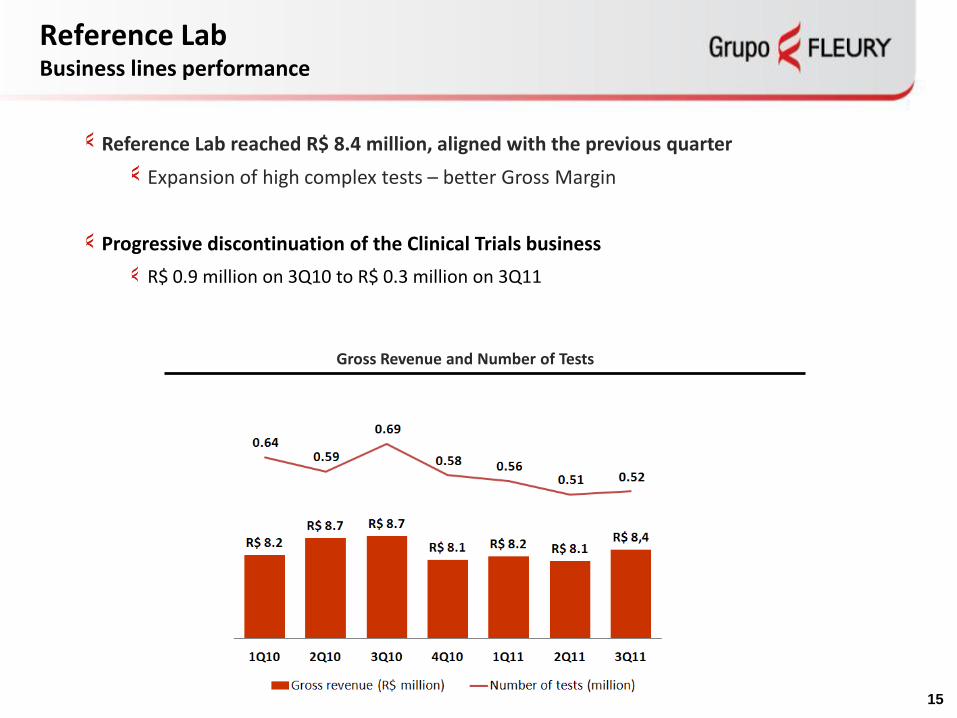

Reference Lab Business lines performance

15

Reference Lab reached R$ 8.4 million, aligned with the previous quarter

Expansion of high complex tests – better Gross Margin

Progressive discontinuation of the Clinical Trials business

R$ 0.9 million on 3Q10 to R$ 0.3 million on 3Q11

Gross Revenue and Number of Tests

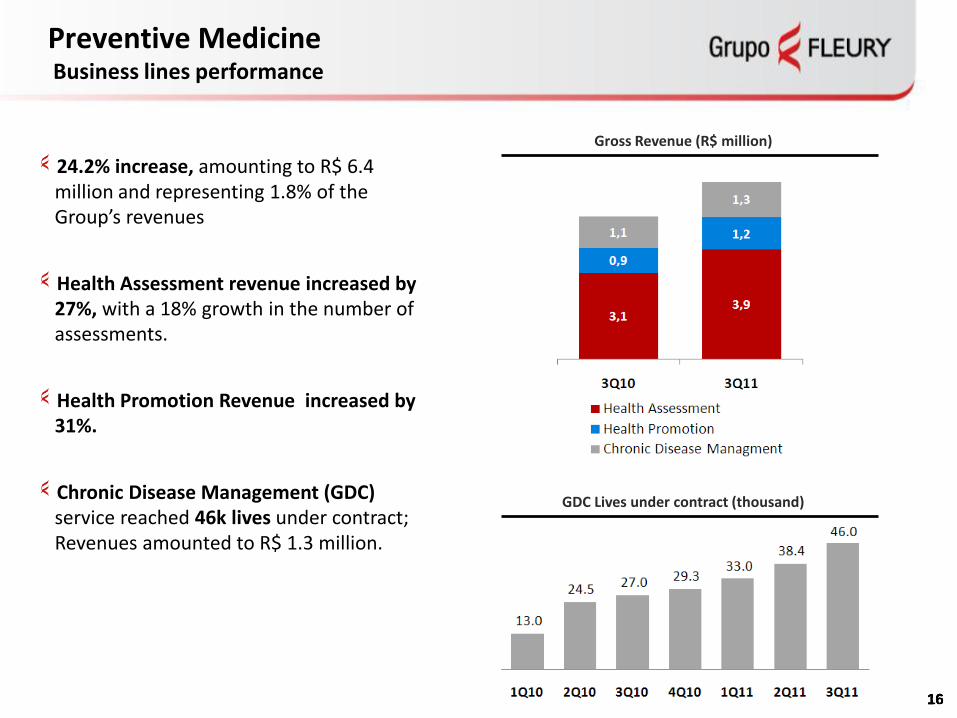

Preventive MedicineBusiness lines performance

1616

24.2% increase, amounting to R$ 6.4 million and representing 1.8% of the Group’s revenues

Health Assessment revenue increased by 27%, with a 18% growth in the number of assessments.

Health Promotion Revenue increased by 31%.

Chronic Disease Management (GDC) service reached 46k lives under contract; Revenues amounted to R$ 1.3 million.

1616

Gross Revenue (R$ million)

GDC Lives under contract (thousand)

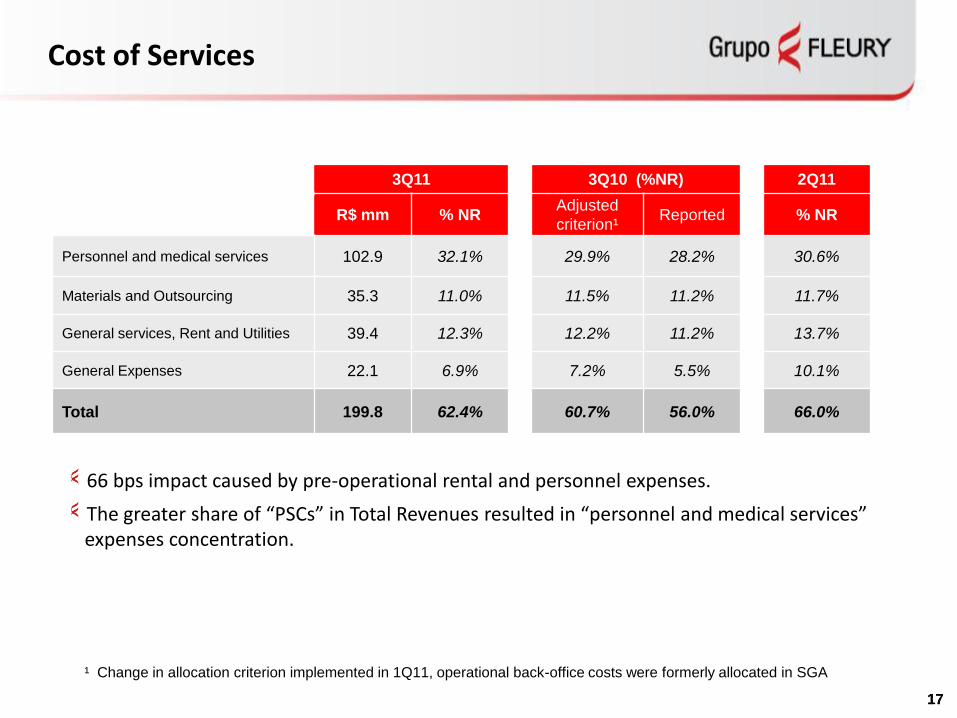

Cost of Services

1717

3Q11 3Q10 (%NR) 2Q11

R$ mm % NRAdjusted

criterion¹Reported % NR

Personnel and medical services 102.9 32.1% 29.9% 28.2% 30.6%

Materials and Outsourcing 35.3 11.0% 11.5% 11.2% 11.7%

General services, Rent and Utilities 39.4 12.3% 12.2% 11.2% 13.7%

General Expenses 22.1 6.9% 7.2% 5.5% 10.1%

Total 199.8 62.4% 60.7% 56.0% 66.0%

¹ Change in allocation criterion implemented in 1Q11, operational back-office costs were formerly allocated in SGA

66 bps impact caused by pre-operational rental and personnel expenses.

The greater share of “PSCs” in Total Revenues resulted in “personnel and medical services” expenses concentration.

Gross Margin

1818

Gross profit has reached R$ 120.3 million, a 32% increase over adjusted 3Q10

37.6% of Net Revenue (170 bps decrease)

Gross Margin to Net Revenue

Benefit by cost line, normalizing allocation criterion (%)

Operating Expenses

1919

Non recurring events:

“a+” Marketing campaign amounted approximately R$ 6 million, an impact of 187bps in margin.

“Labs D’or” acquisition fees were R$ 8 million, or a 250bps impact in margin.

The cash recovery effort net impact was 250bps as receivables written-off.

Depreciation – R$ 19.3 million, compared to R$ 8.3 million in 3Q10. Assets write-off have an impact of R$ 5.8 million in this quarter.

¹ Change in allocation criterion implemented in 1Q11, operational back-office costs were formerly allocated in SGA

3Q11 3Q10 (%NR) 2Q11

R$ mm % NRAdjusted

criterion¹Reported % NR

General and administrative 61.5 19.2% 15.2% 19.9% 11.7%

Other operating expenses (revenue), net 12.0 3.7% (0.4%) (0.4%) 0.7%

Contingency provision (0.3) (0.1%) (1.4%) (1.4%) 0.5%

Operating Expenses (ex-depreciation) 73.2 22.9% 13.4% 18.1% 12.9%

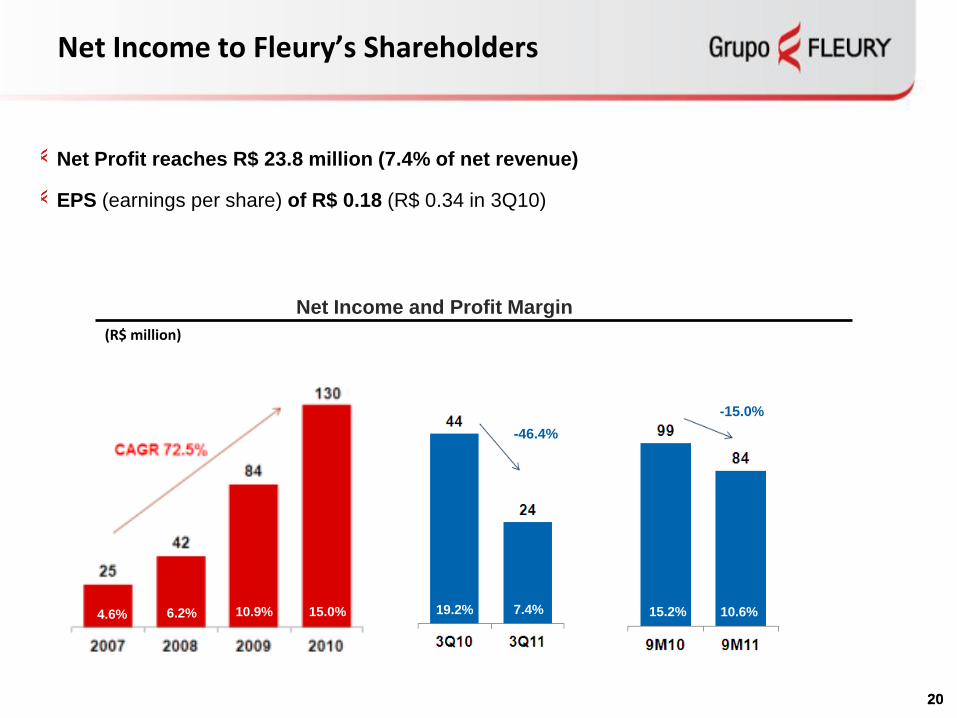

Net Income to Fleury’s Shareholders

2020

Net Profit reaches R$ 23.8 million (7.4% of net revenue)

EPS (earnings per share) of R$ 0.18 (R$ 0.34 in 3Q10)

Net Income and Profit Margin

(R$ million)

19.2% 7.4%4.6% 6.2% 10.9% 15.0% 15.2% 10.6%

-15.0%

-46.4%

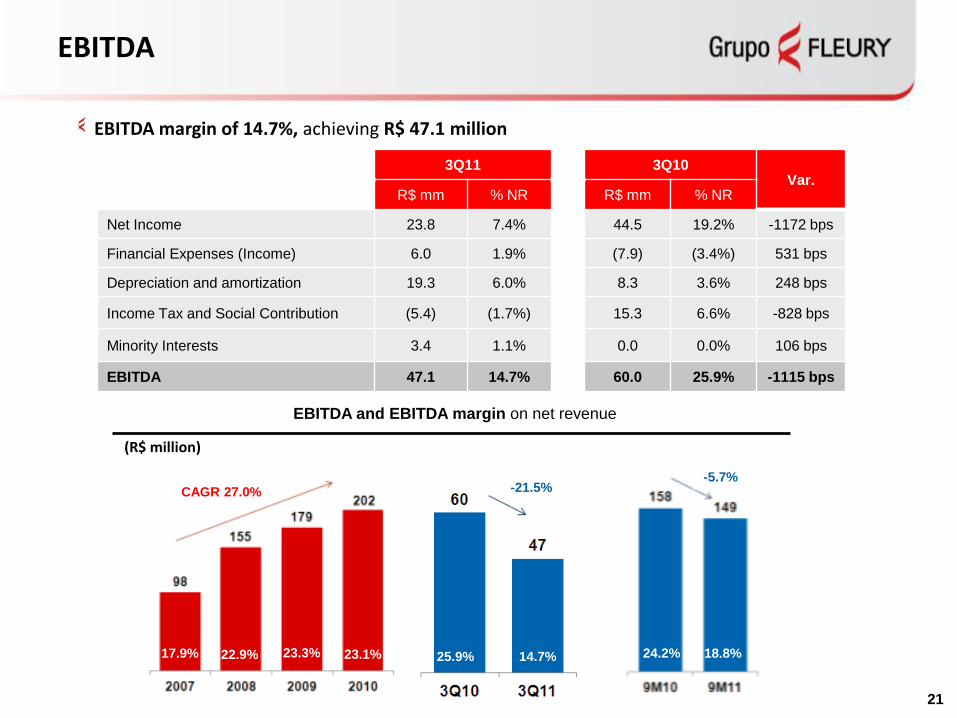

EBITDA

EBITDA margin of 14.7%, achieving R$ 47.1 million

EBITDA and EBITDA margin on net revenue

21

3Q11 3Q10Var.

R$ mm % NR R$ mm % NR

Net Income 23.8 7.4% 44.5 19.2% -1172 bps

Financial Expenses (Income) 6.0 1.9% (7.9) (3.4%) 531 bps

Depreciation and amortization 19.3 6.0% 8.3 3.6% 248 bps

Income Tax and Social Contribution (5.4) (1.7%) 15.3 6.6% -828 bps

Minority Interests 3.4 1.1% 0.0 0.0% 106 bps

EBITDA 47.1 14.7% 60.0 25.9% -1115 bps

(R$ million)

25.9% 14.7%17.9% 22.9% 23.3% 23.1% 24.2% 18.8%

-5.7%-21.5%CAGR 27.0%

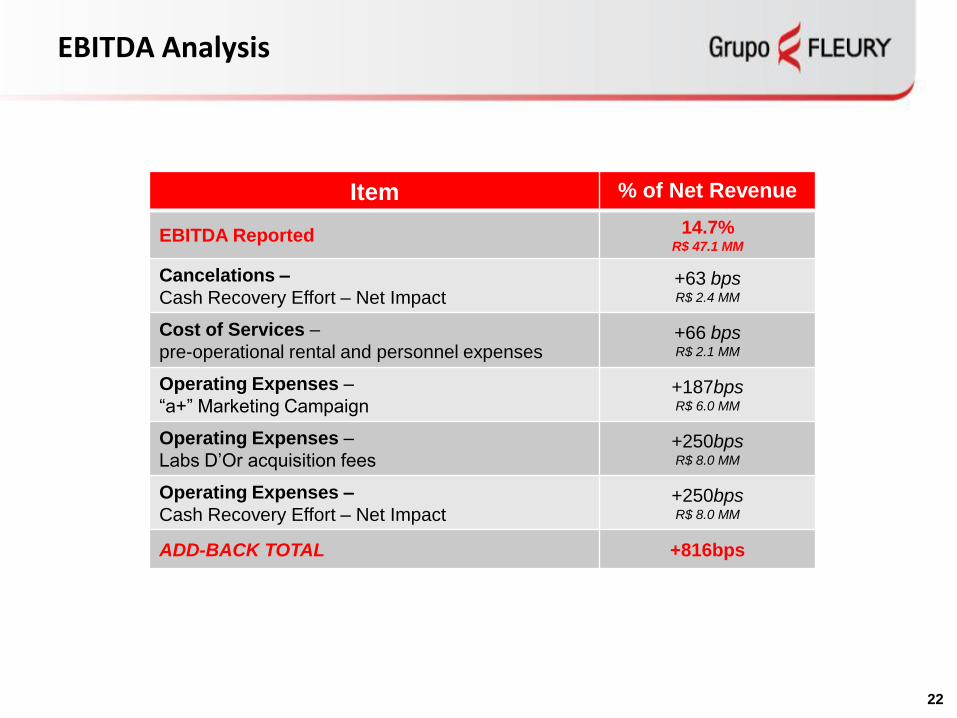

EBITDA Analysis

17.9% 22.9%

22

23.1% 21.9%22.0%

Item % of Net Revenue

EBITDA Reported 14.7%R$ 47.1 MM

Cancelations –

Cash Recovery Effort – Net Impact+63 bpsR$ 2.4 MM

Cost of Services –

pre-operational rental and personnel expenses+66 bpsR$ 2.1 MM

Operating Expenses –

“a+” Marketing Campaign+187bpsR$ 6.0 MM

Operating Expenses –

Labs D’Or acquisition fees+250bpsR$ 8.0 MM

Operating Expenses –

Cash Recovery Effort – Net Impact+250bpsR$ 8.0 MM

ADD-BACK TOTAL +816bps

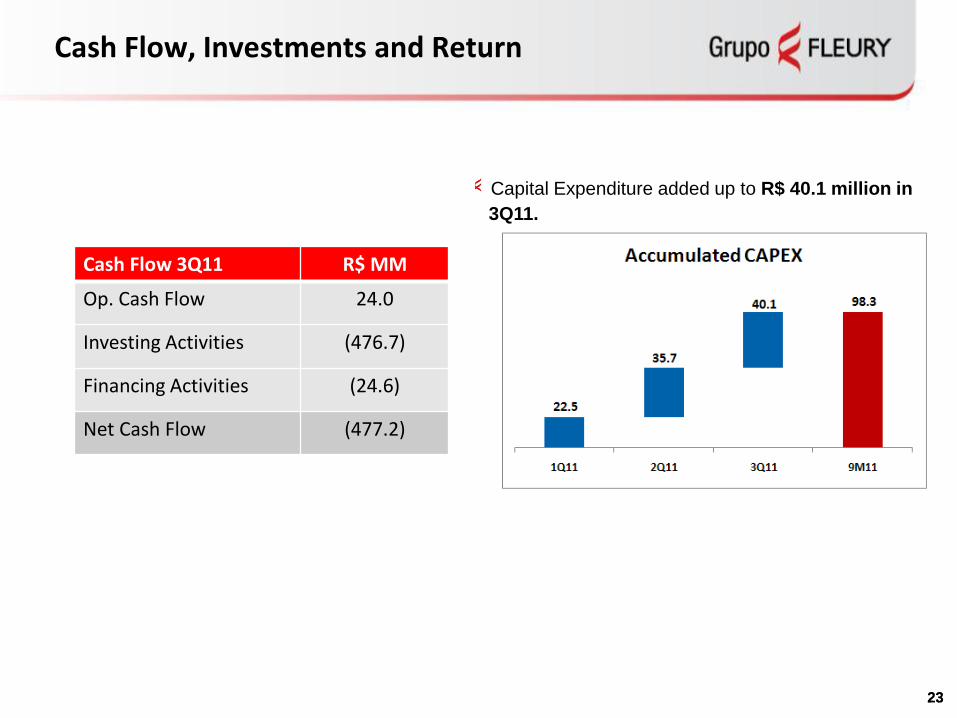

Cash Flow, Investments and Return

2323

Capital Expenditure added up to R$ 40.1 million in

3Q11.

Cash Flow 3Q11 R$ MM

Op. Cash Flow 24.0

Investing Activities (476.7)

Financing Activities (24.6)

Net Cash Flow (477.2)

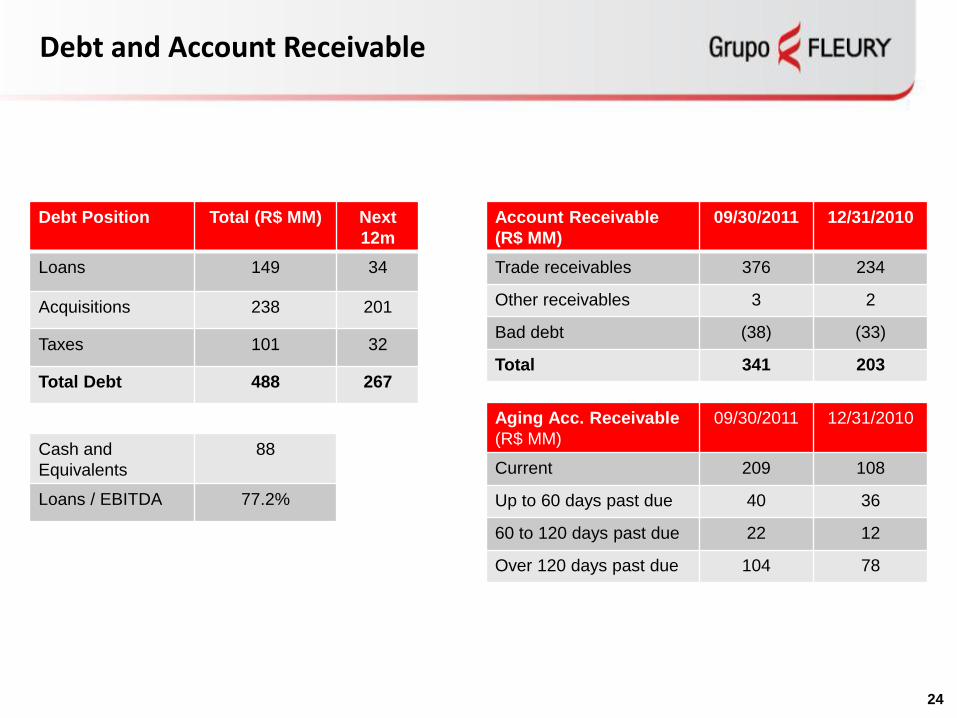

Debt and Account Receivable

Debt Position Total (R$ MM) Next

12m

Loans 149 34

Acquisitions 238 201

Taxes 101 32

Total Debt 488 267

Cash and

Equivalents

88

Loans / EBITDA 77.2%

24

Account Receivable

(R$ MM)

09/30/2011 12/31/2010

Trade receivables 376 234

Other receivables 3 2

Bad debt (38) (33)

Total 341 203

Aging Acc. Receivable

(R$ MM)

09/30/2011 12/31/2010

Current 209 108

Up to 60 days past due 40 36

60 to 120 days past due 22 12

Over 120 days past due 104 78

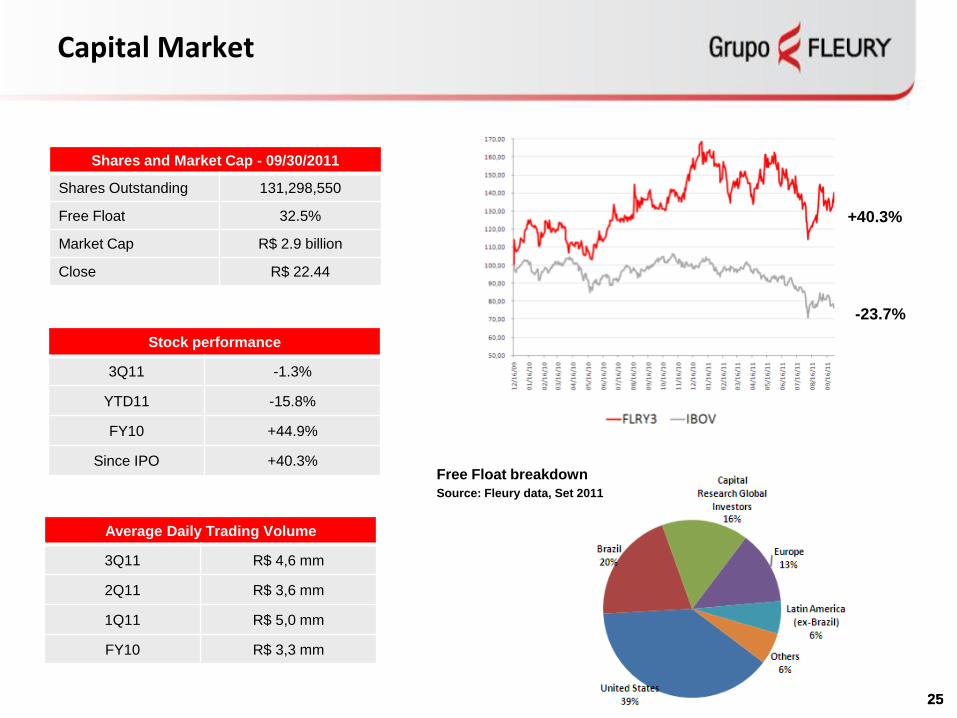

Capital Market

2525

+40.3%

-23.7%

Shares and Market Cap - 09/30/2011

Shares Outstanding 131,298,550

Free Float 32.5%

Market Cap R$ 2.9 billion

Close R$ 22.44

Stock performance

3Q11 -1.3%

YTD11 -15.8%

FY10 +44.9%

Since IPO +40.3%

Average Daily Trading Volume

3Q11 R$ 4,6 mm

2Q11 R$ 3,6 mm

1Q11 R$ 5,0 mm

FY10 R$ 3,3 mm

Free Float breakdown

Source: Fleury data, Set 2011

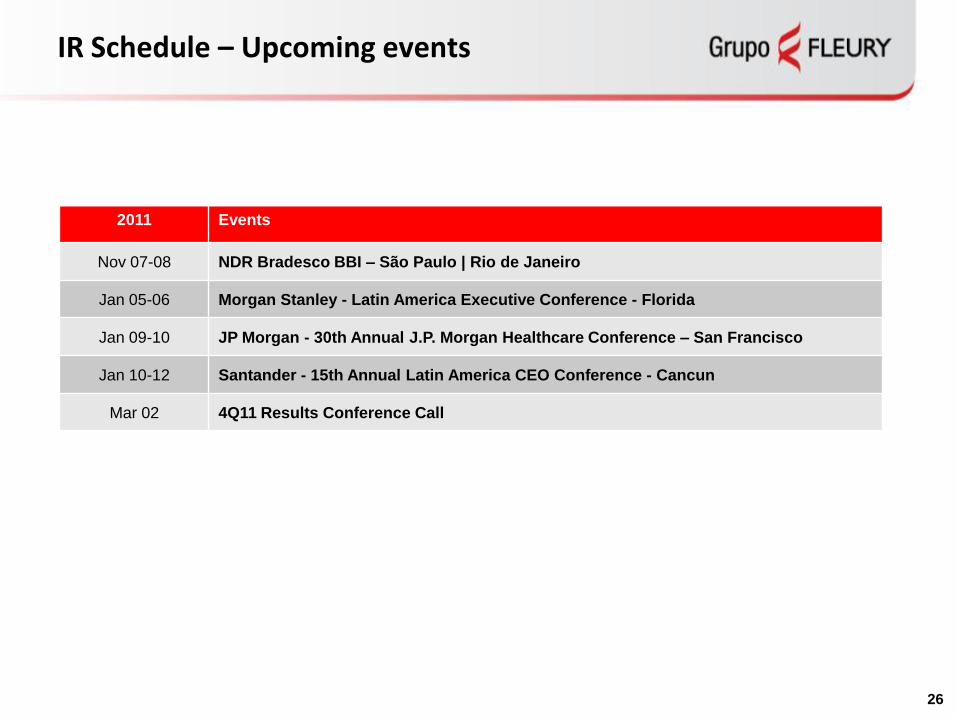

IR Schedule – Upcoming events

2011 Events

Nov 07-08 NDR Bradesco BBI – São Paulo | Rio de Janeiro

Jan 05-06 Morgan Stanley - Latin America Executive Conference - Florida

Jan 09-10 JP Morgan - 30th Annual J.P. Morgan Healthcare Conference – San Francisco

Jan 10-12 Santander - 15th Annual Latin America CEO Conference - Cancun

Mar 02 4Q11 Results Conference Call

26