4-accrual accounting concepts

DESCRIPTION

accounting, WileyTRANSCRIPT

Introduction

chapter 4

Accrual Accounting ConceptsAccounting Matters!

Swapping QuartersA financial reporting system's accuracy depends on answers to some fundamental questions. When was revenue earned or the earnings process complete? And when were expenses really incurred?

Consider this example. One morning a brother and sister opened a lemonade stand in their front yard. As their neighbour left for work, she bought a glass of lemonade for a quarter. Unfortunately, it was a cool day and the kids lived on a quiet cul-de-sac. In short, business was slow.

After an hour with no more customers, the brother decided to buy some lemonade. He passed the neighbour's quarter to his sister and enjoyed a glass. A little later, the sister decided to buy some so she passed the quarter back to her brother. Within an hour, after passing the quarter back and forth, they had finished off the lemonade. They went inside and told their parents they had sold the whole pitcher. Only, they were unable to figure out why, after so many sales, they had only one quarter.

Before being too critical of these siblings, consider this. During the 1990s' boom in dotcom companies' share prices, many were earning revenue by swapping advertising space on their websites. Company A would put an ad on company B's website, and company B would put an ad on company A’s. No money changed hands, but each company recorded revenues and expenses (for the value of the ad space). This didn’t change net earnings or add to cash flow—but it did increase reported revenue.

Recording revenue or expenses in the wrong year is another common transgression. WorldCom stunned financial markets with its admission that it had boosted its 2001 net earnings by billions of dollars by delaying expense recognition until later years. Since then, similar stories have surfaced in both Canada and the United States.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_1.xform?course=crs1562&id=ref (1 of 3)11/02/2008 9:44:29 AM

Introduction

Toronto-based refrigerated-warehouse operator Atlas Cold Storage got into hot water when it had to restate its financial statements for 2001 and 2002. A significant number of expenses were incorrectly recorded as additions to property, plant, and equipment. The result: 2001 net earnings were reduced by $5.2 million, from $11.4 million to $6.2 million, while 2002 net earnings shrunk by $37.4 million, from $19 million to a net loss of $18.4 million.

Why do so many companies violate basic financial reporting rules? Many observers speculate that, as share prices climb, executives feel greater pressure to meet higher earnings expectations. In response, regulators and standard-setters have now made improving revenue recognition and disclosure practices a priority.

The Navigator

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_1.xform?course=crs1562&id=ref (2 of 3)11/02/2008 9:44:29 AM

Introduction

Read Feature Story

Scan Study Objectives

Read Chapter Preview

Read text and answer Before You Go On

Work Using the Decision Toolkit

Review Summary of Study Objectives

Review the Decision Toolkit—A Summary

Work Demonstration Problem

Answer Self-Study Questions

Complete assignments

Copyright © 2008 John Wiley & Sons Canada, Ltd. All rights reserved.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_1.xform?course=crs1562&id=ref (3 of 3)11/02/2008 9:44:29 AM

Study Objectives and Preview

Study Objectives

After studying this chapter, you should be able to:

1. Explain the revenue recognition principle and the matching principle. 2. Prepare adjusting entries for prepayments. 3. Prepare adjusting entries for accruals. 4. Describe the nature and purpose of the adjusted trial balance. 5. Explain the purposes of closing entries.

Preview of Chapter 4

Recording revenues and expenses properly is essential, as indicated in the feature story, because doing otherwise leads to a misstatement of net earnings and related accounts. In this chapter, we introduce you to the accrual accounting concepts that guide the recognition of revenue and the matching of expenses in the appropriate time period.

The chapter is organized as follows:

:44:45 AMhttp://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_2.xform?course=crs1562&id=ref (1 of 2)11/02/2008 9

Study Objectives and Preview

Copyright © 2008 John Wiley & Sons Canada, Ltd. All rights reserved.

:44:45 AMhttp://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_2.xform?course=crs1562&id=ref (2 of 2)11/02/2008 9

Timing Issues

Timing IssuesConsider the following story:

study objective 1Explain the revenue recognition principle and the matching principle.

A grocery store owner from the old country kept his accounts payable on a spindle, accounts receivable on a notepad, and cash in a shoebox. His daughter, a CA, chided him: “I don’t understand how you can run your business this way. How do you know what you’ve earned?”

“Well,” the father replied, “when I arrived in Canada 40 years ago, I had nothing but the pants I was wearing. Today your sister is a doctor, your brother is a teacher, and you are a chartered accountant. Your mother and I have a nice car, a well-furnished house, and a cottage at the lake. We have a good business and everything is paid for. So, you add all that together, subtract the pants, and there's your net earnings.”

Although the old grocer may be correct in his evaluation of how to calculate earnings over his lifetime, most companies need more immediate feedback about how well they are doing. For example, management needs monthly reports on financial results, large corporations present quarterly and annual financial statements to shareholders, and the Canada Revenue Agency requires all businesses to file annual tax returns.

Consequently, accounting divides the economic life of a business into artificial time periods. As indicated in Chapter 2, this is the time period assumption. Accounting time periods are generally one month, one quarter, or one year.

Many accounting transactions affect more than one of these arbitrary time periods. For example, a new building purchased by Loblaw or a new airplane purchased by Air Canada will be used for many years. It does not make sense to expense the full cost of the building or the airplane at the time of purchase, because each will be used for many subsequent periods. Instead, we must determine the impact of each transaction on specific accounting periods.

Determining the amount of revenue and expenses to report in a particular accounting period can be difficult. Generally accepted accounting principles include two principles for recognizing revenue and expenses: the revenue recognition principle and the matching principle.

Revenue Recognition PrincipleThe revenue recognition principle states that revenue must be recognized in the accounting period in which it is earned. In a merchandising company, revenue is considered to be earned when the merchandise is sold (normally

:45:17 AMhttp://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_3.xform?course=crs1562&id=ref (1 of 5)11/02/2008 9

Timing Issues

at the point of sale). In a service company, revenue is considered earned at the time the service is performed.

Revenue recognition is governed by general guidelines and there are a wide variety of interpretations. In general, though, revenue is recognized when the sales effort is substantially complete and collection reasonably assured.

To illustrate, assume a dry-cleaning business cleans clothing on June 30, but customers do not claim and pay for their clothes until the first week of July. Under the revenue recognition principle, revenue is earned in June when the service is performed, not in July when the cash is received. At June 30, the dry-cleaning service would report a receivable on its balance sheet and revenue in its statement of earnings for the service performed.

Improper use of the revenue recognition principle can have devastating consequences for investors. For example, as mentioned in the feature story for Chapter 2, Nortel Network's shares lost a significant portion of their value after investors learned about accounting irregularities related to reported revenue.

Decision ToolkitDecision

CheckpointsInfo Needed for

DecisionTools to Use for

DecisionHow to Evaluate

Results

At what point should the company record revenue?

Need to understand the nature of the company’s business

Revenue should be recorded when earned. For a service company, revenue is earned when a service is performed.

Recognizing revenue too early overstates current period revenue; recognizing it too late understates current period revenue.

Matching PrincipleIn recognizing expenses, a simple rule is followed: “Let the expenses follow the revenues.” Thus, expense recognition is tied to revenue recognition. Consider again the dry-cleaning business mentioned in the last section. Matching expenses with revenues means that the salary expense of performing the cleaning service on June 30 should be reported in the same period in which the service revenue is recognized. The critical issue in expense recognition is determining when the expense contributes to revenue. This may or may not be the same period in which the expense is paid. If the salary incurred on June 30 is not paid until July, the dry cleaner would still report salaries payable on its June 30 balance sheet.

The practice of expense recognition is referred to as the matching principle because it states that efforts

:45:17 AMhttp://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_3.xform?course=crs1562&id=ref (2 of 5)11/02/2008 9

Timing Issues

(expenses) must be matched with accomplishments (revenues). Some expenses are easy to match with revenues. For example, the cost of goods sold can be directly matched to sales revenue in the period in which the sale occurs.

Other costs are more difficult to directly associate with revenue. For example, it is difficult to match administrative salary expense or interest expense with the revenue these help earn. Such costs are normally expensed in the period in which they are incurred. Other examples include costs that help generate revenue over multiple periods of time, such as the amortization of equipment. The association of these types of expense with revenue is less direct than that of cost of goods sold, and we therefore have to make assumptions about how to best allocate these costs to each period. We will learn more about allocating expenses later in this chapter.

Accounting Matters! Management Perspective

Suppose you work for a movie studio. Over what period should the cost of producing a movie be expensed? It should be expensed over the economic life of the movie. But what is its economic life? The filmmaker must estimate how much revenue will be earned from box office sales, DVD sales, television, and games and toys—a period that could be less than a year or many years.

Take, for example, Harry Potter and the Prisoner of Azkaban, released by Warner Bros. in 2004. It cost U.S. $130 million to produce this film, and the film more than recovered this cost in the first two weekends it was released. In fact, all of the Harry Potter movies have broken box office and product sales records. Compare this to The Cat in the Hat, released by Universal Studios in 2003. It cost U.S. $109 million to produce this movie but it has only recovered U.S. $100.4 million to date. These situations illustrate how difficult it can be in real life for companies to properly match expenses to revenues.

:45:17 AMhttp://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_3.xform?course=crs1562&id=ref (3 of 5)11/02/2008 9

Timing Issues

Decision ToolkitDecision

CheckpointsInfo Needed for

DecisionTools to Use for Decision

How to Evaluate Results

At what point should the company record expenses?

Need to understand the nature of the company’s business

Expenses should “follow” revenues—that is, the effort (expense) should be matched with the result (revenue).

Recognizing expenses too early overstates current period expenses; recognizing them too late understates current period expenses.

Accrual Versus Cash Basis of AccountingThe combined application of the revenue recognition principle and the matching principle results in accrual basis accounting. Accrual basis accounting means that transactions that affect a company's financial statements are recorded in the periods in which the events occur, rather than when the company actually receives or pays cash. This means recognizing revenues when they are earned rather than when cash is received. Likewise, expenses are recognized in the period in which services or goods are used or consumed to produce these revenues, rather than when cash is paid. This results in matching revenues that have been earned with the expenses incurred to earn these same revenues.

International Note Although different accounting principles are often used in other countries, the accrual basis of accounting is central to all these principles.

An alternative to the accrual basis is the cash basis. Under cash basis accounting, revenue is recorded only when cash is received, and an expense is recorded only when cash is paid. A statement of earnings presented under the cash basis of accounting does not satisfy generally accepted accounting principles. Why not? Because it fails to record revenue that has been earned but for which cash has not yet been received, thus violating the revenue recognition principle. Similarly, a cash basis statement of earnings fails to match expenses with earned revenues, which violates the matching principle.

Illustration 4-1 compares accrual-based numbers and cash-based numbers, using a simple example. Suppose that

:45:17 AMhttp://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_3.xform?course=crs1562&id=ref (4 of 5)11/02/2008 9

Timing Issues

you own a painting company and you paint a large building during year 1. In year 1, you incur and pay total expenses of $50,000, which includes the cost of the paint and your employees' salaries. You bill your customer $80,000 at the end of year 1, but you are not paid until year 2. On an accrual basis, you would report the revenue during the period earned—year 1—and the expenses would be matched to the period in which the revenues were earned. Thus, your net earnings for year 1 would be $30,000, and no revenue or expense from this project would be reported in year 2. The $30,000 of earnings reported for year 1 provides a useful indication of the profitability of your efforts during that period.

Illustration 4-1

Accrual versus cash basis accounting

If, instead, you were reporting on a cash basis, you would report expenses of $50,000 in year 1 and revenues of $80,000 in year 2. Net earnings for year 1 would be a loss of $50,000, while net earnings for year 2 would be $80,000. While total earnings are the same over the two-year period ($30,000), cash basis measures are not very informative about the results of your efforts during year 1 or year 2.

Copyright © 2008 John Wiley & Sons Canada, Ltd. All rights reserved.

:45:17 AMhttp://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_3.xform?course=crs1562&id=ref (5 of 5)11/02/2008 9

Before You Go On #1

Before You Go On . . .

Review It

1. What are the revenue recognition and matching principles?

2. What are the differences between the cash and accrual bases of accounting?

Copyright © 2008 John Wiley & Sons Canada, Ltd. All rights reserved.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_4.xform?course=crs1562&id=ref11/02/2008 9:45:25 AM

The Basics of Adjusting Entries

The Basics of Adjusting EntriesFor revenues to be recorded in the period in which they are earned, and for expenses to be matched with the revenue they generate, adjusting entries are made to adjust accounts at the end of the accounting period. Adjusting entries make it possible to produce relevant financial information at the end of the accounting period. Thus, the balance sheet reports appropriate assets, liabilities, and shareholders' equity at the statement date, and the statement of earnings shows the proper revenues, expenses, and net earnings (or loss) for the period.

Adjusting entries are necessary because the trial balance—the first pulling together of the transaction data—may not contain complete and up-to-date data. This is true for several reasons:

1. Some events are not journalized daily, because it would not be useful or efficient to do so. Examples are the use of supplies and the earning of wages by employees.

2. Some costs are not journalized during the accounting period, because these costs expire with the passage of time rather than as a result of recurring daily transactions. Examples include insurance and amortization.

3. Some items may be unrecorded. An example is a utility service bill that will not be received until the next accounting period. The bill, however, covers services delivered in the current accounting period.

Adjusting entries are required every time financial statements are prepared. We first analyze each account in the trial balance to see if it is complete and up to date. The analysis requires an understanding of the company's operations and the interrelationship of accounts. Preparing adjusting entries is often a long process. For example, to accumulate the adjustment data, a company may need to count its remaining supplies. It may also need to prepare supporting schedules of insurance policies, rental agreements, and other commitments.

Types of Adjusting EntriesAdjusting entries can be classified as either prepayments or accruals. Each of these classes has two subcategories as shown below:

Prepayments

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_5.xform?course=crs1562&id=ref (1 of 3)11/02/2008 10:06:50 AM

The Basics of Adjusting Entries

1. Prepaid expenses: Expenses paid in cash and recorded as assets before they are used or consumed

2. Unearned revenues: Cash received and recorded as liabilities before revenue is earned

Accruals

1. Accrued expenses: Expenses incurred but not yet paid in cash or recorded

2. Accrued revenues: Revenues earned but not yet received in cash or recorded

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_5.xform?course=crs1562&id=ref (2 of 3)11/02/2008 10:06:50 AM

The Basics of Adjusting Entries

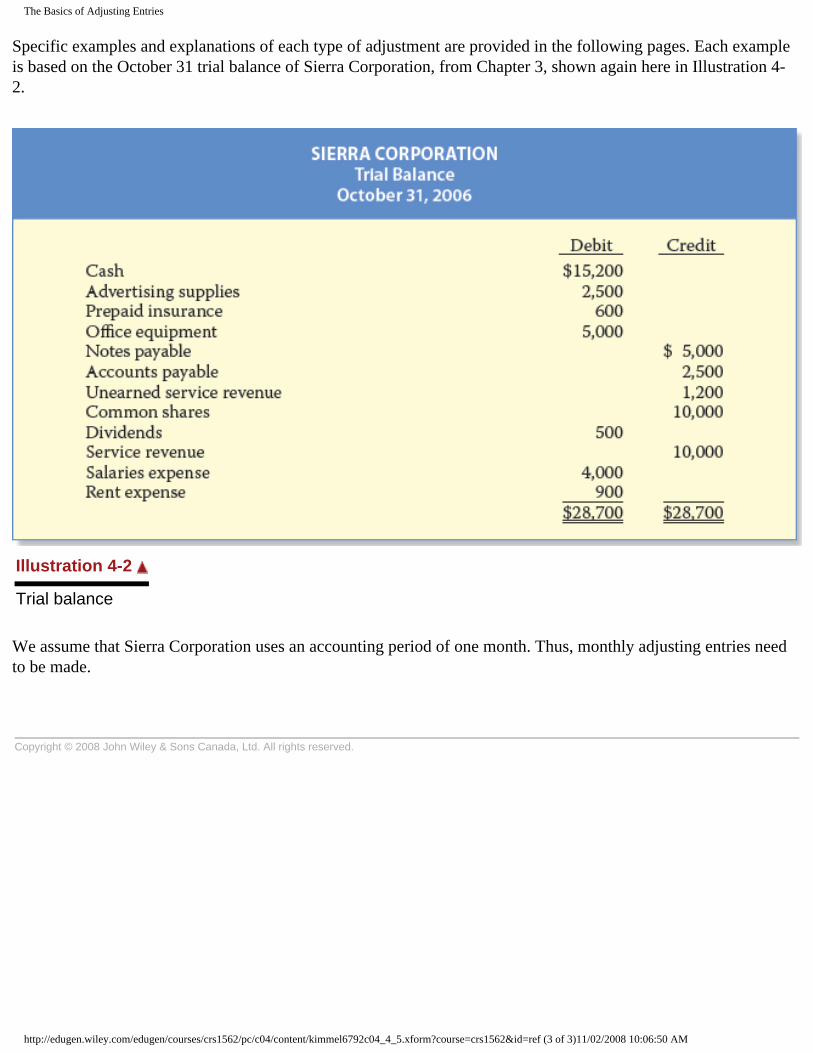

Specific examples and explanations of each type of adjustment are provided in the following pages. Each example is based on the October 31 trial balance of Sierra Corporation, from Chapter 3, shown again here in Illustration 4-2.

Illustration 4-2

Trial balance

We assume that Sierra Corporation uses an accounting period of one month. Thus, monthly adjusting entries need to be made.

Copyright © 2008 John Wiley & Sons Canada, Ltd. All rights reserved.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_5.xform?course=crs1562&id=ref (3 of 3)11/02/2008 10:06:50 AM

Adjusting Entries for Prepayments

Adjusting Entries for PrepaymentsPrepayments are either prepaid expenses or unearned revenues. Adjusting entries for prepayments record the portion of the payment that applies to the current accounting period. This means that for prepaid expenses, the adjusting entry records the expenses which apply to the period. For unearned revenues, the adjusting entry records the revenues earned in the period.

study objective 2Prepare adjusting entries for prepayments.

Prepaid Expenses

Costs that are paid for in cash before they are used are recorded as prepaid expenses. When such a cost is incurred, a prepaid account should be increased (debited)—to show the service or benefit that will be received in the future—and cash should be decreased (credited). Examples of common prepayments are insurance, supplies, and rent. In addition, long-term prepayments are made when long-lived assets, such as buildings and equipment, are purchased.

Helpful Hint A cost can be an asset or an expense. If the cost has future benefits (i.e., the benefits have not yet expired), it is an asset. If the cost has no future benefits (i.e., the benefits have expired), it is an expense.

Prepaid expenses are costs that expire either with the passage of time (e.g., rent and insurance) or through use (e.g., supplies). The expiration of these costs does not require daily entries, which would be impractical and unnecessary. Accordingly, we postpone recognizing these expired costs until financial statements are prepared. At each statement date, adjusting entries are made for two purposes: (1) to record the expenses (expired costs) applicable to the current accounting period, and (2) to show the remaining amounts (unexpired costs) in the asset accounts.

Until prepaid expenses are adjusted, assets are overstated and expenses are understated. If expenses are understated, then net earnings and shareholders' equity will be overstated. As shown below, an adjusting entry for prepaid expenses results in an increase (a debit) to an expense account and a decrease (a credit) to an asset account.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_6.xform?course=crs1562&id=ref (1 of 7)11/02/2008 10:09:45 AM

Adjusting Entries for Prepayments

Let's look in more detail at some specific types of prepaid expenses, beginning with supplies.

Supplies. The purchase of supplies, such as paper, results in an increase (a debit) to an asset account. During the accounting period, supplies are used. Rather than record supplies expense as the supplies are used, supplies expense is recognized at the end of the accounting period. At that time, the company must count the remaining supplies. The difference between the balance in the supplies (asset) account and the actual cost of supplies on hand gives the supplies used (an expense) for that period.

Recall from the facts presented in Chapter 3 that Sierra Corporation purchased advertising supplies costing $2,500 on October 9. The payment was recorded by increasing (debiting) the asset account Advertising Supplies. This account shows a balance of $2,500 in the October 31 trial balance. A count at the close of business on October 31 reveals that $1,000 of supplies are still on hand. Thus, the cost of supplies used is $1,500 ($2,500 – $1,000).

This use of supplies decreases an asset, Advertising Supplies. It also decreases shareholders' equity by increasing an expense account, Advertising Supplies Expense. The use of supplies is recorded as follows:

After the adjusting entry is posted, the two supplies accounts are as follows in T account form:

The asset account Advertising Supplies now shows a balance of $1,000, which is equal to the cost of supplies on hand at the statement date. In addition, Advertising Supplies Expense shows a balance of $1,500, which equals the cost of supplies used in October. If the adjusting entry is not made, October expenses will be understated and net earnings overstated by $1,500. Moreover, as the accounting equation shows, both assets and shareholders' equity will be overstated by $1,500 on the October 31 balance sheet.

Insurance. Companies purchase insurance to protect themselves from losses caused by fire, theft, and

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_6.xform?course=crs1562&id=ref (2 of 7)11/02/2008 10:09:45 AM

Adjusting Entries for Prepayments

unforeseen accidents. Insurance must be paid in advance, often for one year. Insurance payments (premiums) made in advance are normally recorded in the asset account Prepaid Insurance. At the financial statement date, it is necessary to make an adjustment to increase (debit) Insurance Expense and decrease (credit) Prepaid Insurance for the cost of insurance that has expired during the period.

On October 6, Sierra Corporation paid $600 for a one-year insurance policy. Coverage began on October 1. The payment was recorded by increasing (debiting) Prepaid Insurance when it was paid. This account shows a balance of $600 in the October 31 trial balance. An analysis of the insurance policy reveals that $50 of insurance expires each month ($600 ÷ 12 mos.). The expiration of the prepaid insurance would be recorded as follows:

After the adjusting entry is posted, the accounts appear as follows:

The asset Prepaid Insurance shows a balance of $550, which represents the cost that applies to the remaining 11 months of insurance coverage (11 × $50). At the same time, the balance in Insurance Expense is equal to the insurance cost that was used in October. If this adjustment is not made, October expenses will be understated and net earnings overstated by $50. Moreover, both assets and shareholders' equity will be overstated by $50 on the October 31 balance sheet.

Amortization. A company typically owns a variety of assets that have long lives, such as buildings and equipment. Each is recorded as an asset, rather than as an expense, in the year it is acquired because these long-lived assets provide a service for many years. The period of service is referred to as the useful life.

From an accounting standpoint, the acquisition of long-lived assets is essentially a long-term prepayment for services. Similar to other prepaid expenses, there is a need to recognize the cost that has been used (an expense) during the period and to report the unused cost (an asset) at the end of the period. Amortization is the process of allocating the cost of a long-lived asset to expense over its useful life.

One point is very important to understand: Amortization is an allocation concept, not a valuation concept. That is, we amortize an asset to allocate its cost to the periods over which we use it. We are not trying to record a change in the value of the asset. We are only trying to match expenses with the revenues generated in each period.

Calculation of Amortization. A common practice for calculating amortization expense is to divide the cost of the asset by its useful life. This is known as the straight-line method of amortization. Of course, at the time an asset is acquired, its useful life is not known with any certainty. It must therefore be estimated.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_6.xform?course=crs1562&id=ref (3 of 7)11/02/2008 10:09:45 AM

Adjusting Entries for Prepayments

Sierra Corporation purchased office equipment that cost $5,000 on October 3. If its useful life is expected to be five years, annual amortization is $1,000 ($5,000 ÷ 5). In its simplest form, the formula to calculate amortization expense is as follows:

Illustration 4-3

Formula for amortization

Of course, if you are calculating amortization for partial periods, the annual expense amount must be adjusted for the relevant portion of the year. For example, if we wish to determine the amortization for one month, we would multiply the annual result by one-twelth as there are twelve months in a year. Calculating amortization will be refined and examined in more detail in Chapter 9.

For Sierra Corporation, amortization on the office equipment is estimated to be $83 per month ($1,000 × 1/12). Accordingly, amortization for October is recognized by this adjusting entry:

After the adjusting entry is posted, the accounts appear as follows:

The balance in the Accumulated Amortization account will increase by $83 each month until the asset is fully amortized in five years.

As in the case of other prepaid expenses, if this adjusting entry is not made, total assets, shareholders' equity, and net earnings will all be overstated by $83 and amortization expense will be understated by $83.

Statement Presentation. As we learned in Chapter 2, a contra account is an account that is offset against (deducted from) a related account on the statement of earnings or balance sheet. Accumulated Amortization—Office Equipment is a contra asset account. That means it is offset against an asset account (Office Equipment) on the balance sheet. Its normal balance is a credit—the opposite of the normal debit balance of its related account, Office Equipment.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_6.xform?course=crs1562&id=ref (4 of 7)11/02/2008 10:09:45 AM

Adjusting Entries for Prepayments

Helpful Hint Every contra account has increases, decreases, and normal balances that are opposite to those of the account it relates to.

There is a simple reason for using a separate contra account instead of decreasing (crediting) Office Equipment: using this account discloses both the original cost of the equipment and the total estimated cost that has expired to date. In the balance sheet, Accumulated Amortization—Office Equipment is deducted from the related asset account as follows:

Office equipment $5,000 Less: Accumulated amortization—office equipment 83 Net book value 4,917

The difference between the cost of any amortizable asset and its related accumulated amortization is referred to as the net book value, or book value, of that asset. In the above illustration, the book value of the office equipment at the balance sheet date is $4,917. Be sure to understand that, except at acquisition, the book value of the asset and its market value (the price at which it could be sold) are two different values. As noted earlier, the purpose of amortization is not to state an asset's value, but to allocate its cost over time.

Alternative Terminology Book value is also referred to as carrying value.

Unearned Revenues

Cash received before revenue is earned is recorded by increasing (crediting) a liability account for unearned revenue. Items like rent, magazine subscriptions, and customer deposits for future service may result in unearned revenues. Airlines such as Air Canada, for instance, treat receipts from the sale of tickets as unearned revenue until the flight service is provided. Similarly, tuition fees received by universities and colleges before the academic session begins are considered unearned revenue.

Unearned revenues are the opposite of prepaid expenses. Indeed, unearned revenue on the books of one company is likely to be a prepayment on the books of the company that has made the advance payment. For example, if identical accounting periods are assumed, your landlord will have unearned rent revenue when you (the tenant) have prepaid rent.

When a payment is received for services that will be provided in a future accounting period, cash should be increased (debited) and unearned revenue (a liability) should be increased (credited) to recognize the obligation that exists. Unearned revenues are later earned when the service is provided to the customer.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_6.xform?course=crs1562&id=ref (5 of 7)11/02/2008 10:09:45 AM

Adjusting Entries for Prepayments

It is not practical to make daily journal entries as the revenue is earned. Instead, recognition of earned revenue is delayed until the adjustment process. Then an adjusting entry is made to record the revenue that has been earned during the period and to show the liability that remains at the end of the accounting period. Typically, until the adjustment is made, liabilities are overstated and revenues are understated. If revenues are understated, then net earnings and shareholders' equity are also understated. As shown below, the adjusting entry for unearned revenues results in a decrease (a debit) to a liability account and an increase (a credit) to a revenue account.

Sierra Corporation received $1,200 on October 4 from R. Knox for advertising services expected to be completed before the end of next month, November 30. The payment was credited to Unearned Service Revenue, and this liability account shows a balance of $1,200 in the October 31 trial balance. From an evaluation of the work performed by Sierra for Knox during October, it is determined that $400 worth of work was earned in October.

The following adjusting entry is made:

After the adjusting entry is posted, the accounts appear as follows:

The liability Unearned Service Revenue now shows a balance of $800, which represents the remaining advertising services expected to be performed in the future. At the same time, Service Revenue shows total revenue earned in October of $10,400. If this adjustment is not made, revenues and net earnings will be understated by $400 in the statement of earnings. Moreover, liabilities will be overstated by $400 and shareholders' equity will be understated by that amount on the October 31 balance sheet.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_6.xform?course=crs1562&id=ref (6 of 7)11/02/2008 10:09:45 AM

Adjusting Entries for Prepayments

Copyright © 2008 John Wiley & Sons Canada, Ltd. All rights reserved.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_6.xform?course=crs1562&id=ref (7 of 7)11/02/2008 10:09:45 AM

Before You Go On #2

Before You Go On . . .

Review It

1. What are the four types of adjusting entries?

2. What is the effect on assets, liabilities, shareholders' equity, revenues, expenses, and net earnings if an adjusting entry for a prepaid expense is not made?

3. What was the amount of Loblaw's 2003 depreciation expense? What were its accumulated depreciation and net book value as at January 3, 2004? (Hint: These amounts are reported in the notes to the financial statements.) The answers to these questions are provided at the end of this chapter.

4. What is the effect on assets, liabilities, shareholders' equity, revenues, expenses, and net earnings if an adjusting entry for unearned revenue is not made?

Do It

Hammond, Inc.'s general ledger includes these selected accounts on March 31, 2006, before adjusting entries are prepared:

Debit Credit Prepaid insurance $ 3,600 Office supplies 2,800 Office equipment 25,000 Accumulated amortization—office equipment $9,583 Unearned service revenue 9,200

An analysis of the accounts shows the following:

Depreciation expense, $393 million (see Consolidated Statement of Earnings); accumulated depreciation, $2,588 million and net book value, $6,422 million (see note 8 in Notes to the Consolidated Financial Statements).

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_7.xform?course=crs1562&id=ref (1 of 2)11/02/2008 10:10:16 AM

Before You Go On #2

1. The insurance policy is a 12-month policy, effective March 1. 2. Office supplies on hand total $800. 3. The office equipment was purchased April 1, 2004, and is estimated to have a useful life of five

years. 4. Half of the unearned service revenue was earned in March.

Prepare the adjusting entries for the month of March.

Action Plan

Make sure you prepare adjustments for the appropriate time period. Adjusting entries for prepaid expenses require a debit to an expense account and a credit to an asset account. Adjusting entries for unearned revenues require a debit to a liability account and a credit to a revenue account.

Solution

1. Mar. 31 Insurance Expense 300 Prepaid Insurance 300 (To record insurance expired: $3,600 × 1/12) 2. 31 Office Supplies Expense 2,000 Office Supplies 2,000 (To record supplies used: $2,800 − $800)

3. 31 Amortization Expense 417 Accumulated Amortization—Office Equipment 417 (To record monthly amortization: $25,000 ÷ 5 × 1/12) 4. 31 Unearned Service Revenue 4,600 Service Revenue 4,600 (To record revenue earned: $9,200 × 1/2)

Copyright © 2008 John Wiley & Sons Canada, Ltd. All rights reserved.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_7.xform?course=crs1562&id=ref (2 of 2)11/02/2008 10:10:16 AM

Adjusting Entries for Accruals

Adjusting Entries for AccrualsThe second category of adjusting entries is accruals. Adjusting entries for accruals are required in order to record revenues earned, or expenses incurred, in the current accounting period. Accruals have not been recognized through daily entries and thus are not yet reflected in the accounts. Until an accrual adjustment is made, the revenue account (and the related asset account), or the expense account (and the related liability account), is understated. Thus, adjusting entries for accruals will increase both a balance sheet account and a statement of earnings account.

study objective 3Prepare adjusting entries for accruals.

There are two types of adjusting entries for accruals—accrued revenues and accrued expenses. We now look at each type in more detail.

Accrued Revenues

Revenues earned but not yet received in cash or recorded at the statement date are accrued revenues. Accrued revenues may accumulate (accrue) with the passing of time, as in the case of interest revenue. Or they may result from services that have been performed but not yet billed or collected, as in the case of fees. The former are unrecorded because, as when interest is earned, they do not involve daily transactions. The latter may be unrecorded because only a portion of the total service has been provided and the clients will not be billed until the service has been completed.

Alternative Terminology Accrued revenues are also called accrued receivables.

An adjusting entry is required for two purposes: (1) to show the receivable that exists at the balance sheet date, and (2) to record the revenue that has been earned during the period. Until the adjustment is made, both assets and revenues are understated. Consequently, net earnings and shareholders' equity will also be understated. As shown below, an adjusting entry for accrued revenues results in an increase (a debit) to an asset account and an increase (a credit) to a revenue account.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_8.xform?course=crs1562&id=ref (1 of 10)11/02/2008 10:10:42 AM

Adjusting Entries for Accruals

In October, Sierra Corporation earned $200 for advertising services that were not billed to clients before October 31. Because these services have not been billed, they have not been recorded. The adjusting entry would be as follows:

After the adjusting entry is posted, the accounts appear as below:

The asset Accounts Receivable shows that $200 is owed by clients at the balance sheet date. The balance of $10,600 in Service Revenue represents the total revenue earned during the month. If the adjusting entry is not made, assets and shareholders' equity on the balance sheet, and revenues and net earnings on the statement of earnings, will be understated.

In the next accounting period, the clients will be billed. When this occurs, the entry to record the billing should recognize that $200 of revenue earned in October has already been recorded in the October 31 adjusting entry and should not be re-recorded. The subsequent collection of cash from clients will be recorded with an increase (a debit) to Cash and a decrease (a credit) to Accounts Receivable.

Accrued Expenses

Expenses incurred but not yet paid or recorded at the statement date are called accrued expenses. Interest, salaries, and income taxes are common examples of accrued expenses. Accrued expenses result from the same factors as accrued revenues. In fact, an accrued expense on the books of one company is an accrued revenue to another company. For example, the $200 accrual of service revenue for Sierra Corporation discussed above is an accrued

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_8.xform?course=crs1562&id=ref (2 of 10)11/02/2008 10:10:42 AM

Adjusting Entries for Accruals

expense for the client that received the service.

Alternative Terminology Accrued expenses are also called accrued liabilities.

Adjustments for accrued expenses are necessary to (1) record the obligations that exist at the balance sheet date, and (2) recognize the expenses that apply to the current accounting period. Until the adjustment is made, both liabilities and expenses are understated. Consequently, net earnings and shareholders' equity are overstated. An adjusting entry for accrued expenses results in an increase (a debit) to an expense account and an increase (a credit) to a liability account, as shown below:

Helpful Hint To make the illustration easier to understand, a simplified method of interest calculation is used. In reality, interest is calculated using the exact number of days in the interest period and year (365).

Let's look in more detail at some specific types of accrued expenses, beginning with accrued interest.

Interest. Sierra Corporation signed a three-month note payable for $5,000 on October 2. The note requires interest at an annual rate of six percent. The amount of the interest accumulation is determined by three factors: (1) the face value, or principal amount, of the note, (2) the interest rate, which is always expressed as an annual rate, and (3) the length of time the note is outstanding.

In this instance, the total interest due on the $5,000 note at its due date, three months in the future, is $75 ($5,000 × 6% × 3/12), or $25 for one month. Note that the time period is expressed as a fraction of a year. The formula for calculating interest and how it applies to Sierra Corporation for the month of October are shown in Illustration 4-4.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_8.xform?course=crs1562&id=ref (3 of 10)11/02/2008 10:10:42 AM

Adjusting Entries for Accruals

Illustration 4-4

Formula for calculating interest

The accrual of interest at October 31 would be reflected in an adjusting entry as follows:

After the adjusting entry is posted, the accounts appear as follows:

Interest Expense shows the interest charges for the month of October. The amount of interest owed at the statement date is shown in Interest Payable. It will not be paid until the note comes due at the end of three months. The Interest Payable account is used, instead of crediting Notes Payable, to disclose the two different types of obligations—interest and principal—in the accounts and statements. If this adjusting entry is not made, liabilities and interest expense will be understated and net earnings and shareholders' equity will be overstated.

Salaries. Some types of expenses, such as employee salaries, are paid for after the services have been performed. At Sierra Corporation, salaries were last paid on October 20. The next payment of salaries will not occur until November 3. As shown on the calendar in Illustration 4-5, seven as yet unpaid working days remain in October (October 23–27 and October 30–31).

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_8.xform?course=crs1562&id=ref (4 of 10)11/02/2008 10:10:42 AM

Adjusting Entries for Accruals

Illustration 4-5

Calendar showing Sierra Corporation's pay periods

At October 31, the salaries for these seven days represent an accrued expense and a related liability to Sierra. The four employees each receive a salary of $500 a week for a five-day work week, from Monday to Friday, or $100 a day. Thus, accrued salaries at October 31 are $2,800 (7 days × $100/day × 4 employees). This accrual increases a liability, Salaries Payable, and an expense account, Salaries Expense, in the following adjusting entry:

After this adjusting entry is posted, the accounts are as follows:

After this adjustment, the balance in Salaries Expense of $6,800 (17 days × $100/day × 4 employees) is the actual salary expense for October. The balance in Salaries Payable of $2,800 is the amount of the liability for salaries owed as at October 31. If the $2,800 adjustment for salaries is not recorded, Sierra's expenses and liabilities will be understated by $2,800. Net earnings and shareholders' equity will be overstated by $2,800.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_8.xform?course=crs1562&id=ref (5 of 10)11/02/2008 10:10:42 AM

Adjusting Entries for Accruals

At Sierra Corporation, salaries are payable every two weeks. Consequently, the next pay-day is November 3, when total salaries of $4,000 will again be paid. The payment consists of $2,800 of salaries payable at October 31 plus $1,200 of salaries expense for November (3 days × $100/day × 4 employees). Therefore, the following entry is made on November 3:

This entry eliminates the liability for salaries payable that was recorded in the October 31 adjusting entry and records the proper amount of salaries expense for the period between November 1 and November 3.

Income Taxes. For accounting purposes, corporate income taxes must be accrued based on the current period's earnings. Sierra's monthly income taxes payable are estimated to be $250. This accrual increases a liability, Income Tax Payable, and an expense account, Income Tax Expense. The adjusting entry is:

After this adjusting entry is posted, the accounts are as follows:

Corporations, such as Sierra, pay corporate income taxes in monthly instalments. The payment is based on the income tax that was actually payable in the prior year. If there was no prior year, as is the case with Sierra, or if there was no tax payable in the prior year, then no income tax instalment payments are required. However, the liability must still be accrued.

If the adjustment for income taxes is not recorded, Sierra's expenses and liabilities will be understated by $250 and net earnings and shareholders' equity will be overstated by $250.

Summary of Basic RelationshipsThe two basic types of adjusting entries—prepayments and accruals—are summarized below. Take some time to study and analyze the adjusting entries. Be sure to note that each adjusting entry affects one balance sheet account and one statement of earnings account.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_8.xform?course=crs1562&id=ref (6 of 10)11/02/2008 10:10:42 AM

Adjusting Entries for Accruals

Type of Adjustment Reason for Adjustment Accounts before Adjustment Adjusting Entry Prepayments Prepaid expenses Prepaid expenses,

originally recorded in asset accounts, have been used.

Assets overstated; expenses understated

Dr. ExpenseCr. Asset

Unearned revenues Unearned revenues, initially recorded in liability accounts, have been earned.

Liabilities overstated; revenues understated

Dr. LiabilityCr. Revenue

Accruals Accrued revenues Revenues have been earned but not yet received in cash or recorded.

Assets understated; revenues understated

Dr. AssetCr. Revenue

Accrued expenses Expenses have been incurred but not yet paid.

Expenses understated; liabilities understated

Dr. ExpenseCr. Liability

It is important to understand that adjusting entries never involve the Cash account (except for bank reconciliations, which we will study in Chapter 7). In the case of prepayments, cash has already been received or paid and recorded in the original journal entry. The adjusting entry simply reallocates or adjusts amounts between a balance sheet account (e.g., prepaid expenses or unearned revenues) and a statement of earnings account (e.g., expenses or revenues). In the case of accruals, cash will be received or paid in the future and recorded then. The adjusting entry simply records the receivable or payable and the related revenue or expense.

Accounting Matters! Ethics Perspective

In the wake of financial scandals that are still making an impression, the Canadian Securities Administrators introduced requirements in 2005 for management to evaluate the reliability of a company's accounting system and controls. This includes a review of year-end procedures, including the procedures that are used to record recurring and nonrecurring adjusting entries.

This review will include asking such questions as the following: How are the transactions developed, authorized, and checked? What principles does the accounting department use to make adjusting entries? Do the accounting estimates and judgements reflect any biases that would consistently overstate or understate key amounts? Are the proper people involved in the year-end decision-making? All of these, and other similar questions are designed to improve the quality and reliability of financial statements.

Sierra Corporation Illustration

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_8.xform?course=crs1562&id=ref (7 of 10)11/02/2008 10:10:42 AM

Adjusting Entries for Accruals

The journalizing and posting of the adjusting entries described in this chapter for Sierra Corporation on October 31 are shown below and on the following two pages. As you review the general ledger, notice that the adjustments are highlighted in colour.

Note also that an account for retained earnings has been added in the general ledger. Because this is Sierra's first month of operations, there is no balance in the Retained Earnings account. Although accounts with a zero balance are not normally included in the trial balance, we have added it here to make it easier to prepare the statement of retained earnings in the next section. In addition, we will again need to use this account in the section on closing entries later in this chapter.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_8.xform?course=crs1562&id=ref (8 of 10)11/02/2008 10:10:42 AM

Adjusting Entries for Accruals

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_8.xform?course=crs1562&id=ref (9 of 10)11/02/2008 10:10:42 AM

Adjusting Entries for Accruals

Copyright © 2008 John Wiley & Sons Canada, Ltd. All rights reserved.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_8.xform?course=crs1562&id=ref (10 of 10)11/02/2008 10:10:42 AM

Before You Go On #3

Before You Go On . . .

Review It

1. What is the effect on assets, liabilities, shareholders' equity, revenues, expenses, and net earnings if an adjusting entry for accrued revenue is not made?

2. What is the effect on assets, liabilities, shareholders' equity, revenues, expenses, and net earnings if an adjusting entry for an accrued expense is not made?

Do It

Micro Computer Services Inc. began operations on August 1, 2006. Management prepares monthly financial statements. This information is for August:

1. Revenue earned but unrecorded for August totalled $1,100. 2. On August 1, the company borrowed $30,000 from a local bank on a one-year note payable. The

annual interest rate is 5% and interest is payable at maturity. 3. At August 31, the company owed its employees $800 in salaries that will be paid on September 1. 4. Estimated income tax payable for August totalled $275.

Prepare the adjusting entries needed at August 31.

Action Plan

Remember that accruals are entries that were not previously recorded; therefore the adjustment pattern is different from that for prepayments. Adjusting entries for accrued revenues require a debit to a receivable account and a credit to a revenue account. Adjusting entries for accrued expenses require a debit to an expense account and a credit to a liability account.

Solution

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_9.xform?course=crs1562&id=ref (1 of 2)11/02/2008 10:10:59 AM

Before You Go On #3

1. Aug. 31 Accounts Receivable 1,100 Service Revenue 1,100 (To accrue revenue earned but not billed or collected) 2. Aug. 31 Interest Expense 125 Interest Payable 125 (To record accrued interest: $30,000 × 5% × 1/12) 3. Salaries Expense 800 Salaries Payable 800 (To record accrued salaries) 4. Income Tax Expense 275 Income Tax Payable 275 (To record accrued income taxes)

Copyright © 2008 John Wiley & Sons Canada, Ltd. All rights reserved.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_9.xform?course=crs1562&id=ref (2 of 2)11/02/2008 10:10:59 AM

The Adjusted Trial Balance and Financial Statements

The Adjusted Trial Balance and Financial StatementsAfter all adjusting entries have been journalized and posted, another trial balance is prepared from the ledger accounts. This trial balance is called an adjusted trial balance. It shows the balances of all accounts at the end of the accounting period, including those that have been adjusted. The purpose of an adjusted trial balance is to prove the equality of the total debit balances and the total credit balances in the ledger after all adjustments have been made. Because the accounts contain all the data that are needed for financial statements, the adjusted trial balance is the main source for the preparation of financial statements.

study objective 4Describe the nature and purpose of the adjusted trial balance.

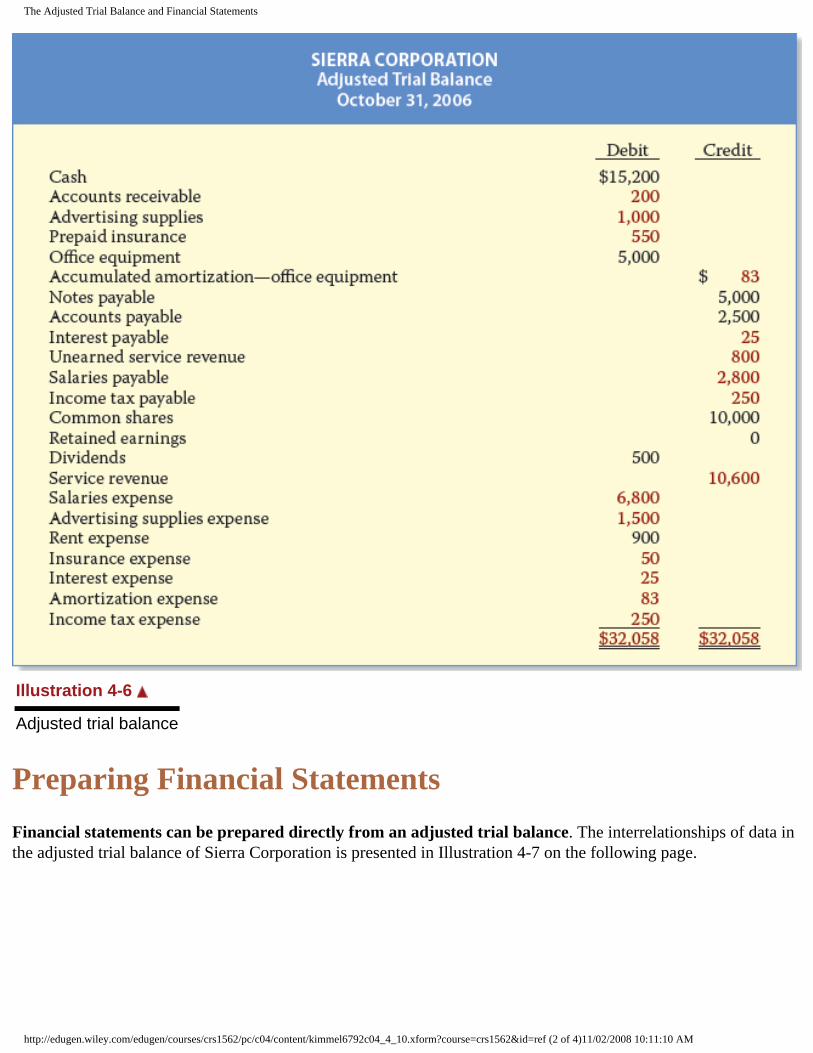

Preparing the Adjusted Trial BalanceThe adjusted trial balance for Sierra Corporation presented in Illustration 4-6 has been prepared from the ledger accounts shown in the previous section. Compare the adjusted trial balance to the unadjusted trial balance presented earlier in the chapter in Illustration 4-2. The amounts affected by the adjusting entries are highlighted in colour.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_10.xform?course=crs1562&id=ref (1 of 4)11/02/2008 10:11:10 AM

The Adjusted Trial Balance and Financial Statements

Illustration 4-6

Adjusted trial balance

Preparing Financial StatementsFinancial statements can be prepared directly from an adjusted trial balance. The interrelationships of data in the adjusted trial balance of Sierra Corporation is presented in Illustration 4-7 on the following page.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_10.xform?course=crs1562&id=ref (2 of 4)11/02/2008 10:11:10 AM

The Adjusted Trial Balance and Financial Statements

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_10.xform?course=crs1562&id=ref (3 of 4)11/02/2008 10:11:10 AM

The Adjusted Trial Balance and Financial Statements

Illustration 4-7

Preparation of the financial statements from the adjusted trial balance

As Illustration 4-7 shows, the statement of earnings is prepared from the revenue and expense accounts. The statement of retained earnings is prepared from the Retained Earnings account, Dividends account, and the net earnings (or net loss) shown in the statement of earnings. The balance sheet is then prepared from the asset, liability, and shareholders' equity accounts. Shareholders' equity includes the ending retained earnings as reported in the statement of retained earnings.

Copyright © 2008 John Wiley & Sons Canada, Ltd. All rights reserved.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_10.xform?course=crs1562&id=ref (4 of 4)11/02/2008 10:11:10 AM

Before You Go On #4

Before You Go On . . .

Review It

1. What is the purpose of an adjusted trial balance?

2. When is an adjusted trial balance prepared?

Copyright © 2008 John Wiley & Sons Canada, Ltd. All rights reserved.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_11.xform?course=crs1562&id=ref11/02/2008 10:11:25 AM

Closing the Books

Closing the BooksIn previous chapters, you learned that revenue and expense accounts and the dividends account are subdivisions of retained earnings, which is reported in the shareholders' equity section of the balance sheet. Because revenues, expenses, and dividends are only for a particular accounting period, they are considered temporary accounts. In contrast, all balance sheet accounts are considered permanent accounts because their balances are carried forward into future accounting periods. Illustration 4-8 identifies the accounts in each category.

Illustration 4-8

Temporary and permanent accounts

study objective 5Explain the purposes of closing entries.

Preparing Closing EntriesAt the end of the accounting period, the temporary account balances are transferred to the permanent shareholders' equity account Retained Earnings through the preparation of closing entries. Closing entries formally record in the general ledger the transfer of the balances in the revenue, expense, and dividends accounts to the Retained Earnings account. In Illustration 4-6, you will note that Retained Earnings has an adjusted balance of zero. Until the closing entries are made, the balance in Retained Earnings will be its balance at the beginning of the period. For Sierra, this is zero because it is Sierra's first year of operations. After closing entries are recorded and posted, the balance in Retained Earnings will reflect its balance at the end of the period. This ending account balance will now be the same as the balance reported in the statement of retained earnings and the balance sheet.

In addition to updating retained earnings to its ending balance, closing entries produce a zero balance in each temporary account. As a result, these accounts are ready to accumulate data about revenues, expenses, and dividends in the next accounting period separately from the data in the prior periods. Permanent accounts are not closed.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_12.xform?course=crs1562&id=ref (1 of 7)11/02/2008 10:11:36 AM

Closing the Books

When closing entries are prepared, each revenue and expense account could be closed directly to Retained Earnings. This is common in computerized accounting systems where the closing process occurs automatically when it is time to start a new accounting period. However, in manual accounting systems, this practice can result in too much detail in the Retained Earnings account. Accordingly, the revenue and expense accounts are first closed to another temporary account, Income Summary. Only the resulting total amount (net earnings or net loss) is transferred from this account to the Retained Earnings account. Illustration 4-9 shows the closing process.

Illustration 4-9

Closing process

To prepare closing entries, four steps are necessary:

1. To close revenue accounts: Debit each individual revenue account for its balance, and credit Income Summary for total revenues.

2. To close expense accounts: Debit Income Summary for total expenses, and credit each individual expense account for its balance.

3. To close Income Summary: Debit Income Summary for the balance in the account (or credit it if there is a net loss), and credit (debit) Retained Earnings.

4. To close dividends: Debit Retained Earnings, and credit Dividends for its balance.

Closing entries can be prepared directly from the general ledger or the adjusted trial balance. If we were to prepare closing entries for Sierra Corporation, we would likely start with the adjusted trial balance presented earlier in the chapter in Illustration 4-6. In Sierra's case, all temporary accounts (Dividends, Service Revenue, and its seven different expense accounts) must be closed.

Even though Retained Earnings is not a temporary account, it will also be involved in the closing process. Remember that the balance presented in the adjusted trial balance for Retained Earnings is the beginning, not ending, balance. This permanent account is not closed but the net earnings (loss) and dividends for the period must be recorded to update the account to its ending balance.

Sierra's general journal, showing its closing entries, and its general ledger, showing the posting of the closing entries, follow:

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_12.xform?course=crs1562&id=ref (2 of 7)11/02/2008 10:11:36 AM

Closing the Books

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_12.xform?course=crs1562&id=ref (3 of 7)11/02/2008 10:11:36 AM

Closing the Books

Stop and check your work after the closing entries are posted: (1) The balance in the Income Summary account, immediately before the final closing entry to transfer the balance to the Retained Earnings account, should equal the net earnings (or net loss) reported in the statement of earnings. (2) All temporary accounts (dividends, revenues, expenses, and income summary) should have zero balances. (3) The balance in the Retained Earnings account should equal the ending balance reported in the statement of retained earnings and balance sheet.

Accounting Matters! Management Perspective

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_12.xform?course=crs1562&id=ref (4 of 7)11/02/2008 10:11:36 AM

Closing the Books

Garry Beattie, CMA and owner of HBM Integrated Technology Inc., believes that the closing process should be completed within five days of the end of the month. Accounting done in a timely, efficient manner through streamlined, computerized accounting systems can save a business time and money. “With good technology, you can provide better information faster,” he says. In fact, Beattie says that studies show that posting journal entries daily can save four hours of work per week. The five-day close is possible for anyone, since many multinational companies, such as Cisco Systems, do it in less than one day.

Source: Rosemary Godin, “Five-Day Close Saves Time on Balance Sheets, Says Halifax CMA,” Bottom Line, January 2003.

Preparing a Post-closing Trial BalanceAfter all closing entries are journalized and posted, another trial balance, called a post-closing trial balance, is prepared from the ledger. We have learned about the unadjusted and adjusted trial balances so far. The last trial balance is the post-closing trial balance, which lists all permanent accounts and their balances after closing entries are journalized and posted. The purpose of this trial balance is to prove the equality of the permanent account balances that are carried forward into the next accounting period. Since all temporary accounts will have zero balances, the post-closing trial balance will contain only permanent—balance sheet—accounts.

Illustration 4-10 shows Sierra Corporation's post-closing trial balance on the following page.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_12.xform?course=crs1562&id=ref (5 of 7)11/02/2008 10:11:36 AM

Closing the Books

Illustration 4-10

Post-closing trial balance

Summary of the Accounting CycleThe required steps in the accounting cycle are shown in Illustration 4-11. You can see that the cycle begins with the analysis of business transactions and ends with the preparation of a post-closing trial balance. The steps in the cycle are done in sequence and are repeated in each accounting period.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_12.xform?course=crs1562&id=ref (6 of 7)11/02/2008 10:11:36 AM

Closing the Books

Illustration 4-11

Required steps in the accounting cycle

Steps 1 to 3 may occur daily during the accounting period, as explained in Chapter 3. Steps 4 to 7 are done on a periodic basis, such as monthly, quarterly, or annually. Steps 8 and 9, closing entries and a post-closing trial balance, are usually prepared only at the end of a company's annual accounting period.

Copyright © 2008 John Wiley & Sons Canada, Ltd. All rights reserved.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_12.xform?course=crs1562&id=ref (7 of 7)11/02/2008 10:11:36 AM

Before You Go On #5

Before You Go On . . .

Review It

1. How do permanent accounts differ from temporary accounts?

2. What four different types of entries are required in closing the books?

3. What financial statement amount will the balance in the Income Summary account equal immediately before it is closed into the Retained Earnings account?

4. What are the content and purpose of a post-closing trial balance?

5. What are the required steps in the accounting cycle?

Do It

The adjusted trial balance for the Nguyen Corporation shows the following: Dividends $5,000; Common Shares $30,000; Retained Earnings $12,000; Service Revenue $18,000; and Operating Expenses $10,000. Prepare the closing entries at December 31.

Action Plan

Debit each individual revenue account for its balance and credit the total to the Income Summary account. Credit each individual expense account for its balance and debit the total to the Income Summary account. Stop and check your work: Does the balance in the Income Summary account equal the reported net earnings (loss)? If there are net earnings, debit the balance in the Income Summary account and credit the amount to the Retained Earnings account (do the opposite if the result is a net loss). Credit the balance in the Dividends account and debit the amount to the Retained Earnings account. Do not close Dividends with the expenses. Stop and check your work: Do the temporary accounts have zero balances? Does the ending Retained Earnings balance equal the balance reported on the statement of retained earnings and balance sheet?

Solution

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_13.xform?course=crs1562&id=ref (1 of 2)11/02/2008 10:13:25 AM

Before You Go On #5

Dec. 31 Service Revenue 18,000 Income Summary 18,000 (To close revenue account)

31 Income Summary 10,000 Operating Expenses 10,000 (To close expense account)

31 Income Summary 8,000 Retained Earnings 8,000 (To close income summary)

31 Retained Earnings 5,000 Dividends 5,000 (To close dividends)

Copyright © 2008 John Wiley & Sons Canada, Ltd. All rights reserved.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_13.xform?course=crs1562&id=ref (2 of 2)11/02/2008 10:13:25 AM

Using the Decision Toolkit

Using the Decision ToolkitFPI (Fishery Products International) Limited is the world's largest seafood supplier. A simplified version of FPI's December 31, 2004, year-end adjusted trial balance is shown below.

Instructions

From the adjusted trial balance, prepare a statement of earnings, statement of retained earnings, and classified balance sheet.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_14.xform?course=crs1562&id=ref (1 of 4)11/02/2008 10:13:36 AM

Using the Decision Toolkit

Solution

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_14.xform?course=crs1562&id=ref (2 of 4)11/02/2008 10:13:36 AM

Using the Decision Toolkit

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_14.xform?course=crs1562&id=ref (3 of 4)11/02/2008 10:13:36 AM

Using the Decision Toolkit

Copyright © 2008 John Wiley & Sons Canada, Ltd. All rights reserved.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_14.xform?course=crs1562&id=ref (4 of 4)11/02/2008 10:13:36 AM

Summary of Study Objectives

Summary of Study Objectives1. Explain the revenue recognition principle and the matching principle. The revenue recognition

principle states that revenue must be recognized in the accounting period in which it is earned. The matching principle states that expenses must be recognized when they make their contribution to revenues.

2. Prepare adjusting entries for prepayments. Adjusting entries for prepayments are required in order to record the portion of the prepayment that applies to the expense incurred or revenue earned in the current accounting period. Prepayments are either prepaid expenses or unearned revenues. The adjusting entry for prepaid expenses results in an increase (a debit) to an expense account and a decrease (a credit) to an asset account. The adjusting entry for unearned revenues results in a decrease (a debit) to a liability account and an increase (a credit) to a revenue account.

3. Prepare adjusting entries for accruals. Adjusting entries for accruals are required in order to record the revenues and expenses that apply to the current accounting period and that have not been recognized through daily entries. Accruals are either accrued revenues or accrued expenses. The adjusting entry for accrued revenues results in an increase (a debit) to an asset account and an increase (a credit) to a revenue account. The adjusting entry for accrued expenses results in an increase (a debit) to an expense account and an increase (a credit) to a liability account.

4. Describe the nature and purpose of the adjusted trial balance. An adjusted trial balance is a trial balance that shows the balances of all accounts at the end of an accounting period, including those that have been adjusted. The purpose of an adjusted trial balance is to show the effects of all financial events that have occurred during the accounting period.

5. Explain the purposes of closing entries. One purpose of closing entries is to update the Retained Earnings account to its end-of-period balance with the results of operations for the period. A second purpose is to enable all temporary accounts (dividends, revenue, and expense accounts) to begin a new period with a zero balance. To accomplish this, entries are made to close each individual revenue and expense account to Income Summary, then Income Summary to Retained Earnings, and finally Dividends to Retained Earnings. Only temporary accounts are closed.

Copyright © 2008 John Wiley & Sons Canada, Ltd. All rights reserved.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_15.xform?course=crs1562&id=ref11/02/2008 10:14:01 AM

Decision ToolkitA Summary

Decision Toolkit—A SummaryDecision

CheckpointsInfo Needed for Decision

Tools to Use for Decision

How to Evaluate Results

At what point should the company record revenue?

Need to understand the nature of the company’s business

Revenue should be recorded when earned. For a service company, revenue is earned when a service is performed.

Recognizing revenue too early overstates current period revenue; recognizing it too late understates current period revenue.

At what point should the company record expenses?

Need to understand the nature of the company’s business

Expenses should “follow” revenues—that is, the effort (expense) should be matched with the result (revenue).

Recognizing expenses too early overstates current period expenses; recognizing them too late understates current period expenses.

Copyright © 2008 John Wiley & Sons Canada, Ltd. All rights reserved.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_16.xform?course=crs1562&id=ref11/02/2008 10:14:09 AM

Demonstration Problem

Demonstration ProblemThe Green Thumb Lawn Care Corporation was incorporated on April 1. At April 30, the trial balance shows the following balances for selected accounts:

Prepaid insurance $3,600 Equipment 30,000 Note payable 20,000 Unearned service revenue 4,200 Service revenue 1,800

Analysis reveals the following additional data about these accounts:

1. Prepaid insurance is the cost of a one-year insurance policy, effective April 1. 2. The equipment is expected to have a useful life of four years. 3. The note payable is dated April 1. It is a six-month, 6% note. Interest is payable on the first of each month. 4. Seven customers paid for the company's six-month, $600 lawn service package beginning in April. These

customers were serviced in April. 5. Lawn services provided to other customers but not billed at April 30 totalled $1,500. 6. Income tax expense for April is estimated to be $100.

Instructions

Prepare the adjusting entries for the month of April.

Action Plan Note that adjustments are being made for only one month. Look at what amounts are currently recorded in the accounts before determining what adjustments are necessary. Show your calculations. Select account titles carefully. Use existing titles wherever possible. Use T accounts to help plan, or check, your adjustments.

Solution to Demonstration Problem

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_17.xform?course=crs1562&id=ref (1 of 2)11/02/2008 10:14:19 AM

Demonstration Problem

Copyright © 2008 John Wiley & Sons Canada, Ltd. All rights reserved.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_17.xform?course=crs1562&id=ref (2 of 2)11/02/2008 10:14:19 AM

Self-Study Questions

Self-Study QuestionsAnswers are at the end of the chapter.

(SO 1) 1. Which principle or assumption states that efforts (expenses) must be recorded with accomplishments (revenues)?

(a) Matching principle(b) Cost principle(c) Time period assumption(d) Revenue recognition principle

(SO 1) 2. Adjusting entries are made to ensure that:

(a) expenses are matched to revenues in the period in which the revenue is generated.(b) revenues are recorded in the period in which they are earned.(c) balance sheet and statement of earnings accounts have correct balances at the end of

an accounting period.(d) All of the above

(SO 2) 3. The trial balance shows Supplies $1,350 and Supplies Expense $0. If $600 of supplies are on hand at the end of the period, the adjusting entry is:

(a) Supplies 600 Supplies Expense 600 (b) Supplies Expense 600 Supplies 600 (c) Supplies 750 Supplies Expense 750 (d) Supplies Expense 750 Supplies 750

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_18.xform?course=crs1562&id=ref (1 of 4)11/02/2008 10:14:28 AM

Self-Study Questions

(SO 2) 4. Frontenac Corp. purchased equipment at the beginning of year 1 for $25,000, which was estimated to have a useful life of 5 years. How much is the equipment's net book value at the end of year 3?

(a) $5,000(b) $10,000(c) $15,000(d) $25,000

(SO 2) 5. On February 1, Magazine City received $600 in advance for ten 12-month subscriptions to Climbing Magazine. What adjusting journal entry should Magazine City make on February 28?

(a) Subscription Revenue 550 Unearned Subscription Revenue 550 (b) Unearned Subscription Revenue 50 Subscription Revenue 50 (c) Unearned Subscription Revenue 550 Subscription Revenue 550 (d) Cash 600 Subscription Revenue 600

(SO 3) 6. A bank has a three-month, $6,000 note receivable, issued on January 1 at an interest rate of 4%. Interest is due at maturity. What adjusting entry should the bank make at the end of January?

(a) Note Receivable 20 Interest Revenue 20 (b) Interest Receivable 60 Interest Revenue 60 (c) Cash 20 Interest Revenue 20 (d) Interest Receivable 20 Interest Revenue 20

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_18.xform?course=crs1562&id=ref (2 of 4)11/02/2008 10:14:28 AM

Self-Study Questions

(SO 3) 7. Kathy Kiska earned a salary of $400 for the last week of September. She will be paid on October 1. The adjusting entry for Kathy's employer at September 30 is:

(a) Salaries Expense 400 Salaries Payable 400 (b) Salaries Expense 400 Cash 400 (c) Salaries Payable 400 Cash 400 (d) No entry is required

(SO 4) 8. Which statement is incorrect concerning the adjusted trial balance?

(a) An adjusted trial balance proves the equality of the total debit balances and the total credit balances in the ledger after all adjustments are made.

(b) The adjusted trial balance is the main source for the preparation of financial statements.

(c) The adjusted trial balance is prepared after the closing entries have been journalized and posted.

(d) The adjusted trial balance is prepared after the adjusting entries have been journalized and posted.

(SO 4) 9. The Retained Earnings account in an unadjusted trial balance is $10,000. Net earnings for the period are $2,500 and dividends are $500. The Retained Earnings account balance in the adjusted trial balance will be:

(a) $9,500.(b) $10,000.(c) $12,000.(d) $12,500.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_18.xform?course=crs1562&id=ref (3 of 4)11/02/2008 10:14:28 AM

Self-Study Questions

(SO 5) 10. Which account will have a zero balance after closing entries have been journalized and posted?

(a) Service Revenue(b) Advertising Supplies(c) Unearned Revenue(d) Accumulated Amortization

(SO 5) 11. Which types of accounts will appear in the post-closing trial balance?

(a) Permanent accounts(b) Temporary accounts(c) Statement of earnings accounts(d) Cash flow statement accounts

Answers to Self-Study Questions1.a 2.d 3.d 4.b 5.b 6.d 7.a 8.c 9.b 10.a 11.a

Copyright © 2008 John Wiley & Sons Canada, Ltd. All rights reserved.

http://edugen.wiley.com/edugen/courses/crs1562/pc/c04/content/kimmel6792c04_4_18.xform?course=crs1562&id=ref (4 of 4)11/02/2008 10:14:28 AM

Questions

Questions(SO 1) 1. Why are adjusting entries needed? Include in your explanation a description of the

assumption and two generally accepted accounting principles that relate to adjusting the accounts.

(SO 1) 2. Tony Galego, a lawyer, accepts a legal engagement in March, does the work in April, bills the client $8,000 in May, and is paid in June. If Galego's law firm prepares monthly financial statements, when should it recognize revenue from this engagement? Why?

(SO 1) 3. In completing the engagement in question 2, Galego incurs $2,000 of expenses that are specifically related to this engagement in March, $2,500 in April, and none in May and June. How much expense should be deducted from revenues in the month(s) the revenue is recognized? Why?