4. finance performance day - ey · april 2016 4. finance performance day finance holding ... unit...

TRANSCRIPT

4. Finance Performance DayDas Forum für aktuelle Finance-, Controlling- undBI-Themen6. April – Köln / 20. April – Stuttgart

Page 2

Agenda

Einführung1 09:30

Agile Unternehmensplanung erfolgreich und nachhaltigumsetzen

3

11:15

Best in Class Reporting2 09.35

10:45

5 12:25

Business LunchLive Demo - Reporting mit arcplan sowie tableau6 12:35

April 2016 4. Finance Performance Day

Schlusswort

PAUSELive Demo - Reporting mit arcplan sowie tableau

4

Page 3

Agenda

Einführung1 09:30

Agile Unternehmensplanung erfolgreich und nachhaltigumsetzen

3

11:15

Best in Class Reporting2 09.35

10:45

5 12:25

Business LunchLive Demo - Reporting mit arcplan sowie tableau6 12:35

April 2016 4. Finance Performance Day

Schlusswort

PAUSELive Demo - Reporting mit arcplan sowie tableau

4

Best in Class Reporting

• Wie Digitalisierung das Reporting von morgen verändert• Die Potentiale kontextspezifischer Daten-Visualisierung• Effizienz durch Standardisierung der Informationsdarstellung

Page 5

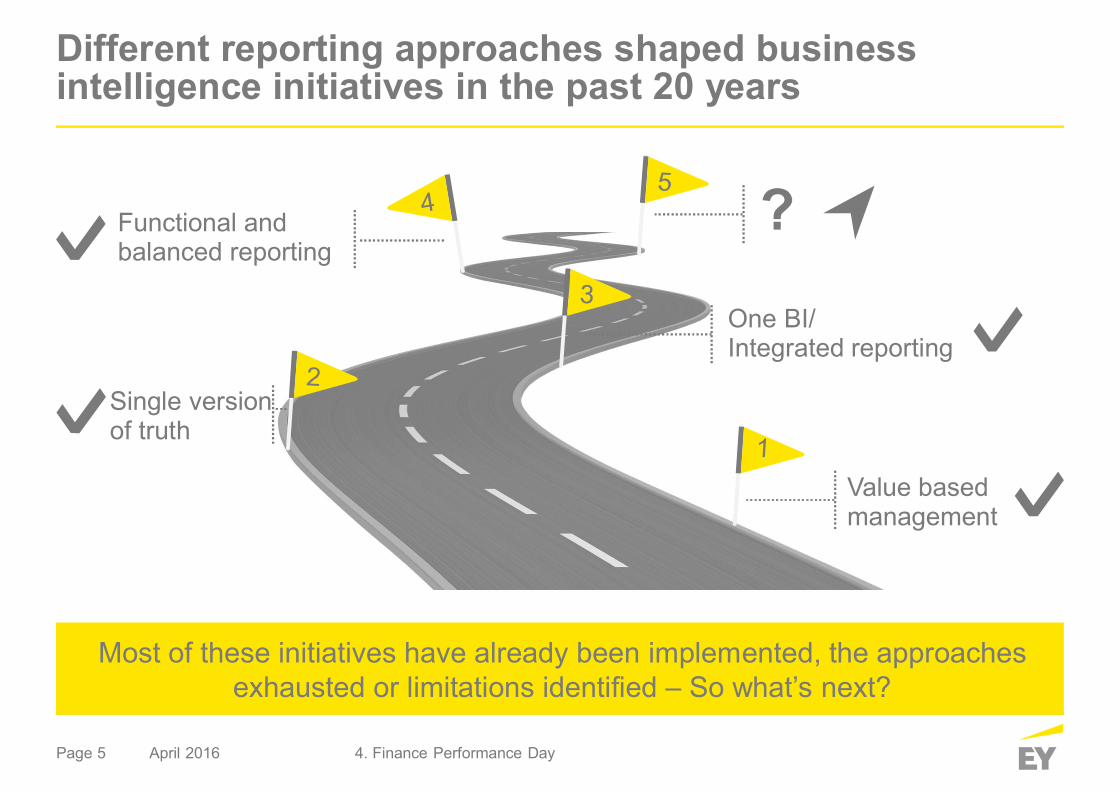

Different reporting approaches shaped businessintelligence initiatives in the past 20 years

Most of these initiatives have already been implemented, the approachesexhausted or limitations identified – So what’s next?

Functional andbalanced reporting

Single versionof truth

Value basedmanagement

One BI/Integrated reporting

?

4. Finance Performance DayApril 2016

Page 6

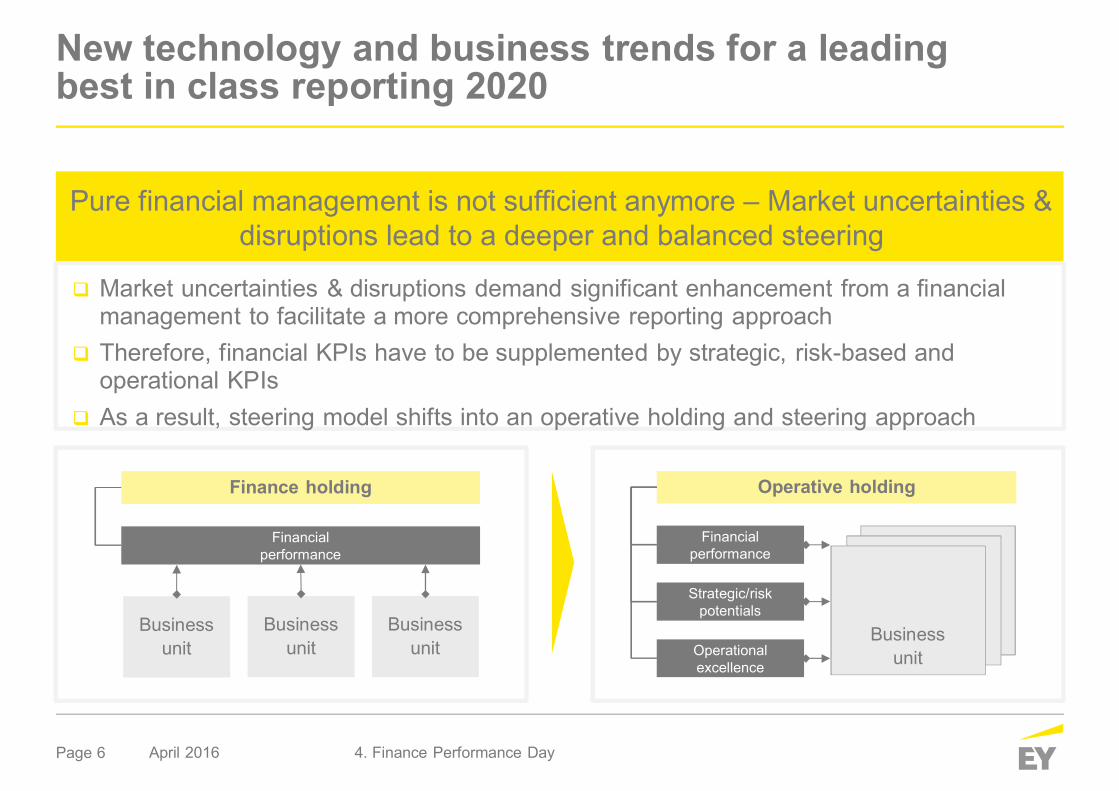

Financialperformance

Operationalexcellence

Strategic/riskpotentials

Businessunit

New technology and business trends for a leadingbest in class reporting 2020

Pure financial management is not sufficient anymore – Market uncertainties &disruptions lead to a deeper and balanced steering

Market uncertainties & disruptions demand significant enhancement from a financialmanagement to facilitate a more comprehensive reporting approachTherefore, financial KPIs have to be supplemented by strategic, risk-based andoperational KPIsAs a result, steering model shifts into an operative holding and steering approach

4. Finance Performance DayApril 2016

Finance holding

Financialperformance

Businessunit

Businessunit

Businessunit

Operative holding

Page 7

Corporate management reporting

Agile reporting analytics

New technology and business trends for a leadingbest in class reporting 2020

Reporting Analytics

Additionally, digitalization of business and innovative reporting technology willsignificantly impact tomorrows reporting

Traditional corporatemanagement reportingremains relevant but clearlyfocus on deeper and balancedsteering

Digitalization drives volume ofsemi-structured andunstructured data

Therefore, a new discipline ofagile reporting analytics isrequired

Analytical platforms allowbetter operative insights,higher forecast accuracy andmore precise monitoring

4. Finance Performance DayApril 2016

Page 8

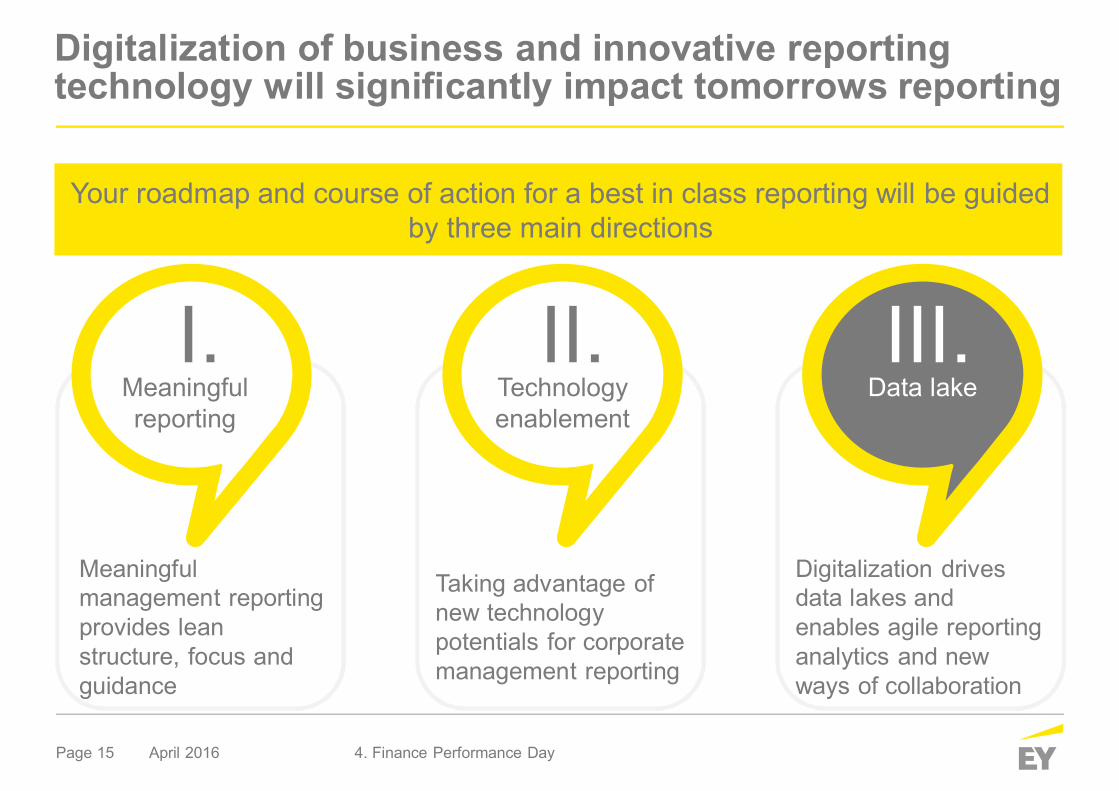

Meaningfulmanagement reportingprovides leanstructure, focus andguidance

Meaningfulreporting

Taking advantage ofnew technologypotentials for corporatemanagement reporting

Technologyenablement

Digitalization drivesdata lakes andenables agile reportinganalytics and newways of collaboration

Datalake

Digitalization of business and innovative reportingtechnology will significantly impact tomorrows reporting

I. II. III.

Your roadmap and course of action for a best in class reportingwill be guided by three main directions

April 2016 4. Finance Performance Day

Page 9

Meaningfulmanagement reportingprovides leanstructure, focus andguidance

Meaningfulreporting

Taking advantage ofnew technologypotentials for corporatemanagement reporting

Technologyenablement

Digitalization drivesdata lakes andenables agile reportinganalytics and newways of collaboration

Datalake

Digitalization of business and innovative reportingtechnology will significantly impact tomorrows reporting

I. II. III.

Your roadmap and course of action for a best in class reportingwill be guided by three main directions

April 2016 4. Finance Performance Day

Page 10

I. Meaningful management reporting provideslean structure, focus and guidance

Accepted lead KPIs between group and business units ensure overall alignment1

Reporting has to clearly reflect responsibilities of business including target achievement1

Reporting has to tell a story that answers the question with regard to what has drivenperformance or what has not3A coherent structure from lead KPI into operational KPIs provides business insights2

The overall effectiveness of management reporting is highly driven by context specificvisualization/notation2Reports should follow a consistent content structure: lead KPIs for responsibilities(dashboard), guided analysis for “operational why” (analysis) , flexible ad hoc for furtherdeep dive (ad hoc)3

4. Finance Performance DayApril 2016

Page 11

I. Meaningful management reporting provideslean structure, focus and guidance

Best in class reporting focuses on lead KPIs and guided analysis fromessential into operational business insights

Reporting reflectsresponsibilities of business

including targetachievement

Coherent structure fromlead into operational KPIs

provides business insights

Ad hocreports

Analysisreports

Dashboardreports

Lead KPI

Reports should followconsistent content

structure: dashboard,analysis, ad hoc

Top-line growth

Benchmarking

Market competitors

Marginimprovement

Capital efficiency

Process efficiency

Processexcellence

Lead KPI

4. Finance Performance DayApril 2016

Topmanagement

Middlemanagement

Functionalmanagement

Page 12

Meaningfulmanagement reportingprovides leanstructure, focus andguidance

Meaningfulreporting

Taking advantage ofnew technologypotentials for corporatemanagement reporting

Technologyenablement

Digitalization drivesdata lakes andenables agile reportinganalytics and newways of collaboration

Data lake

Digitalization of business and innovative reportingtechnology will significantly impact tomorrows reporting

I. II. III.

Your roadmap and course of action for a best in class reportingwill be guided by three main directions

April 2016 4. Finance Performance Day

Page 13

II. Taking advantage of new technology potentials forcorporate management reporting

Modern reporting front-ends act as intelligent interface translating data into meaningfulcontent (any time, any place, on any device)1

Flexible ad hoc requires direct access to raw data, ideally in-memory based1

Automatic rule-based flagging and commenting ensure an accurate variance analysis3

Modern reporting front-ends allow personalization and grant ease of access (anytime,anywhere, on any device)2

Collaborative commenting on the fly or on demand supports timely variance explanations2Modern reporting front-ends provide a powerful toolbox containing KPIs, analysis,dimensions and graphical visualization (define once, re-use and apply consistently)3

4. Finance Performance DayApril 2016

Page 14

Modern reporting technology front-ends foster accurate andtimely business discussions

Automatic rule-basedflagging/commenting for

accurate variance analysis

Modern reporting front-ends allow personalizationand grant ease of access

Flexible ad hoc requiresdirect access to raw data,ideally in-memory based

II. Taking advantage of new technology potentials forcorporate management reporting

Flexible access tomultiple data

Automatedraw dataextraction

Immediate andpersonalizedaccess

Intelligentreportgeneration

Sales

EBIT

Cashflow

…

Orderbacklog

Funnel

Actual

CustomerGroup/

BusinessUnit

ProfitCenter

ProductGroup

Order

4. Finance Performance DayApril 2016

Page 15

Meaningfulmanagement reportingprovides leanstructure, focus andguidance

Meaningfulreporting

Taking advantage ofnew technologypotentials for corporatemanagement reporting

Technologyenablement

Digitalization drivesdata lakes andenables agile reportinganalytics and newways of collaboration

Data lake

Digitalization of business and innovative reportingtechnology will significantly impact tomorrows reporting

Your roadmap and course of action for a best in class reporting will be guidedby three main directions

I. II. III.

April 2016 4. Finance Performance Day

Page 16

Big data will become a complementary element for management reporting to exploreoperational performance and risk drivers1

Discovery analytics allow detection of data patterns1

Predictive analytics enable foresight from historic data3

Key focus is on gaining operational business insights based on semi-structured andunstructured data (e.g. sensor, social media)2

New technology architecture enables near/real-time decision making in a big dataenvironment2Big data has to be managed agile and flexible and therefore differently to classicalwarehouse approaches3

III. Digitalization drives data lakes and enables agilereporting analytics and new ways of collaboration

4. Finance Performance DayApril 2016

Page 17

Big data has to be managed agile andflexible and therefore differently toclassical warehouse approaches

III. Digitalization drives data lakes and enables agilereporting analytics and new ways of collaboration

Big data and new technologies facilitate the use ofcomplementary data for better decision making

Predictiveanalytics

Incoming multipleraw data

Datalake

Real-timeanalytics

Discoveryanalytics

Structured Unstructured

Data lakes enablenew opportunities and potentials

while raising new questions

What does it mean for controlling?

Who is the owner of data?

Who takes care of technology?

4. Finance Performance DayApril 2016

Page 18

Meaningful managementreporting provides leanstructure, focus andguidance

Best in class reportingfocuses on lead KPIs andguided analysis fromessential into operationalbusiness insights

Taking advantage of newtechnology potentials forcorporate managementreporting

Modern reportingtechnology front-endsfoster accurate andtimely businessdiscussions

Digitalization drives datalakes and enables agilereporting analytics andnew ways of collaboration

Big data and newtechnologies empowerthe use of data for betterdecision makingcomplementary tomanagement reporting

Your roadmap and course of action for a best in classreporting will be guided by three main directions

Meaningfulreporting

I.Technologyenablement

II.Datalake

III.

April 2016 4. Finance Performance Day

Is your Information Design leveragingthe gain of Insights from Reporting?

Page 20

Methodical Information Design is everywhere…… but has not yet settled in the business world

April 2016 4. Finance Performance Day

But in the business world we notice alack of methodical information design,because…

Reports are not conveyingmeaningful messagesReports communicate withambiguityReports deliver redundanciesReports lack usability

In many disciplines, people and organizations experience benefits from Methodical InformationDesign:

Construction plansWiring diagramsSI units

TempoTone pitchTime signature

GeographicalcoordinatesCountry CodesGeo Classifications

This has consequences on yourbusiness…

Engineering

Geography

Music

Page 21

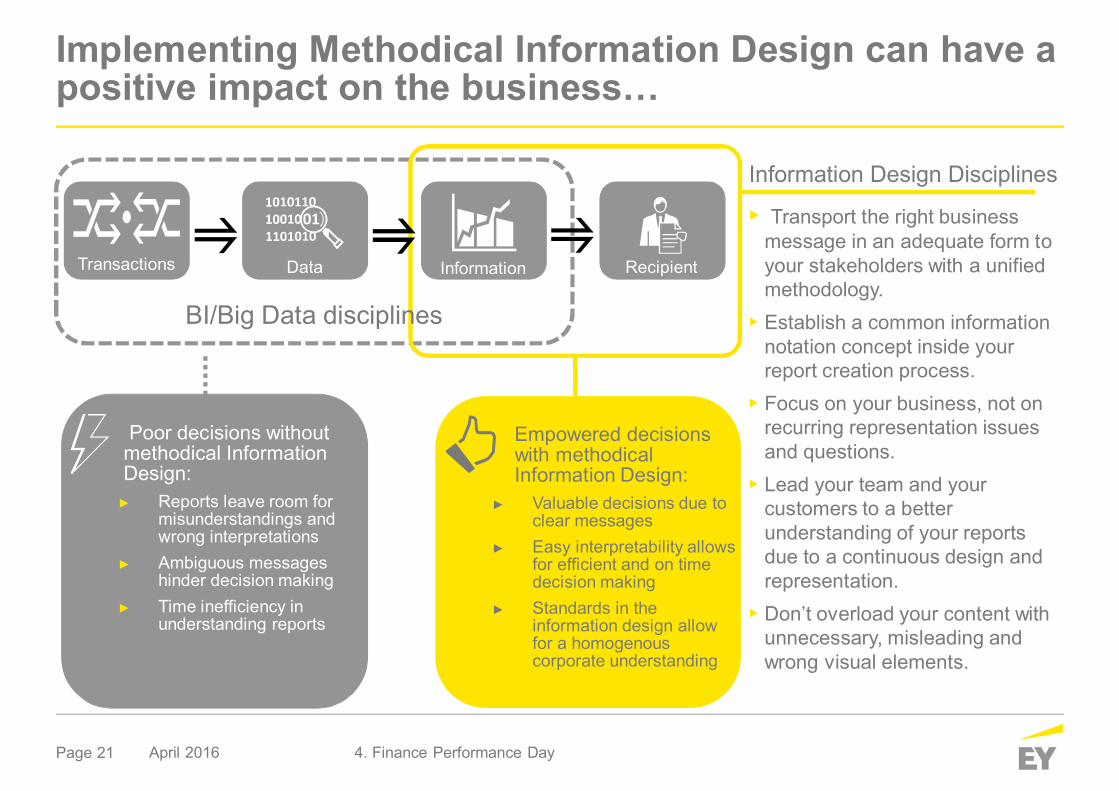

Empowered decisionswith methodicalInformation Design:

Valuable decisions due toclear messagesEasy interpretability allowsfor efficient and on timedecision makingStandards in theinformation design allowfor a homogenouscorporate understanding

Implementing Methodical Information Design can have apositive impact on the business…

April 2016 4. Finance Performance Day

Poor decisions withoutmethodical InformationDesign:

Reports leave room formisunderstandings andwrong interpretationsAmbiguous messageshinder decision makingTime inefficiency inunderstanding reports

Information Design Disciplines

• Transport the right businessmessage in an adequate form toyour stakeholders with a unifiedmethodology.

• Establish a common informationnotation concept inside yourreport creation process.

• Focus on your business, not onrecurring representation issuesand questions.

• Lead your team and yourcustomers to a betterunderstanding of your reportsdue to a continuous design andrepresentation.

• Don’t overload your content withunnecessary, misleading andwrong visual elements.

Transactions Data Information Recipient

BI/Big Data disciplines

Page 22

…but what does it mean?

April 2016 4. Finance Performance Day

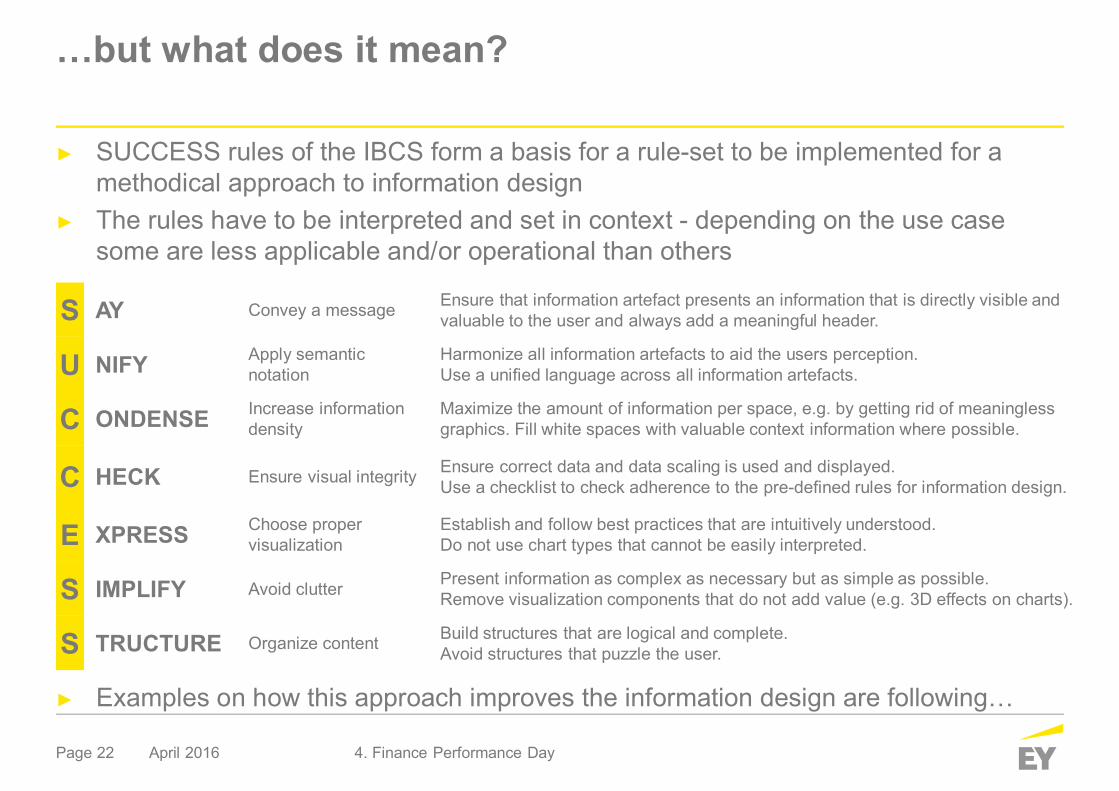

SUCCESS rules of the IBCS form a basis for a rule-set to be implemented for amethodical approach to information designThe rules have to be interpreted and set in context - depending on the use casesome are less applicable and/or operational than others

Examples on how this approach improves the information design are following…

S AY Convey a message Ensure that information artefact presents an information that is directly visible andvaluable to the user and always add a meaningful header.

U NIFY Apply semanticnotation

Harmonize all information artefacts to aid the users perception.Use a unified language across all information artefacts.

C ONDENSE Increase informationdensity

Maximize the amount of information per space, e.g. by getting rid of meaninglessgraphics. Fill white spaces with valuable context information where possible.

C HECK Ensure visual integrity Ensure correct data and data scaling is used and displayed.Use a checklist to check adherence to the pre-defined rules for information design.

E XPRESS Choose propervisualization

Establish and follow best practices that are intuitively understood.Do not use chart types that cannot be easily interpreted.

S IMPLIFY Avoid clutter Present information as complex as necessary but as simple as possible.Remove visualization components that do not add value (e.g. 3D effects on charts).

S TRUCTURE Organize content Build structures that are logical and complete.Avoid structures that puzzle the user.

Page 23

What Percentage-Value does one „box“ stand for?What‘s the message of this chart?

April 2016 4. Finance Performance Day

Source: Otto Group Geschäftsbericht 2014/2015

Page 24

What Percentage-Value does one „box“ stand for?What‘s the message of this chart?

April 2016 4. Finance Performance Day

Source: Otto Group Geschäftsbericht 2014/2015

Two categories (country,year) are mixed

Vague and inconsistentscaling is used

The overall message ofthe chart remains unclear

Page 25

Deutschland holt zwar weiter auf, die USA haben aberweiterhin das höchste BIP-Wachstum

April 2016 4. Finance Performance Day

Small multiples allow fora clear categorization

Correct scaling is usedin all data points

The message of thechart is highlighted

2013Deutschland

Eurozone

USA

Russland

2014Deutschland

Eurozone

USA

Russland

Veränderung des realen BIP gegenüber dem Vorjahr (in Prozent)

+ 0,1 %

- 0,4 %

+ 2,2 %

+ 1,3 %

+ 1,6 %

+ 0,9 %

+ 2,4 %

+ 0,4 %

Page 26

Deutschland holt zwar weiter auf, die USA haben aberweiterhin das höchste BIP-Wachstum

April 2016 4. Finance Performance Day

Small multiples allow fora clear categorization

Correct scaling is usedin all data points

The message of thechart is highlighted

2013Deutschland

Eurozone

USA

Russland

2014Deutschland

Eurozone

USA

Russland

Veränderung des realen BIP gegenüber dem Vorjahr (in Prozent)

+ 0,1 %

- 0,4 %

+ 2,2 %

+ 1,3 %

+ 1,6 %

+ 0,9 %

+ 2,4 %

+ 0,4 %

EXPRESS:A more accurate chart typeis chosen

SAY:The message is highlightedin the header

CHECK:Data Scaling is now correct

SAY:The most interesting datapoint is highlighted

UNIFY:The unified header for all reportscontains all necessary informationabout the chart

Page 27

Nur in Russland war das Wirtschaftswachstum 2014rückläufig

Veränderung des realen BIP gegenüber dem Vorjahr (in Prozent)

April 2016 4. Finance Performance Day

Small multiples allow fora clear categorization

Correct scaling is usedin all data points

The message of thechart is highlighted

Deutschland

2011 2012 2013 2014

Eurozone

2011 2012 2013 2014

USA

2011 2012 2013 2014

Russland

2011 2012 2013 2014

+ 4,3 %+ 3,7 %

+ 0,4 % + 0,1 %

+ 1,6 % + 1,6 %

- 0,8 %- 0,4 %

+ 0,9 %

+ 2,4 %+ 2,2 %+ 2,2 %+ 1,6 %

+ 3,4 %

+ 1,3 %

+ 0,4 %

Page 28

Nur in Russland war das Wirtschaftswachstum 2014rückläufig

Veränderung des realen BIP gegenüber dem Vorjahr (in Prozent)

April 2016 4. Finance Performance Day

Small multiples allow fora clear categorization

Correct scaling is usedin all data points

The message of thechart is highlighted

Deutschland

2011 2012 2013 2014

Eurozone

2011 2012 2013 2014

USA

2011 2012 2013 2014

Russland

2011 2012 2013 2014

+ 4,3 %+ 3,7 %

+ 0,4 % + 0,1 %

+ 1,6 % + 1,6 %

- 0,8 %- 0,4 %

+ 0,9 %

+ 2,4 %+ 2,2 %+ 2,2 %+ 1,6 %

+ 3,4 %

+ 1,3 %

+ 0,4 %

EXPRESSA different chart type ischosen to focus thecomparison on years

CHECK:Data Scaling is now correct

CONDENSE:The room on the slide is used more efficientlyby adding context information about theprevious years 2011 and 2012

SAY:The message is highlightedin the header

SAY:The most interesting datapoints are highlighted

UNIFY:The unified header for all reportscontains all necessary informationabout the chart

Page 29

Can you name the difference between 2/3 & 4/5?

April 2016 4. Finance Performance Day

Is there a difference between2 & 3 or 4 & 5 ?

Please use the Survey Tool!

• 2 = 3, 4 = 5

• 2 = 3, 4 > 5

• 2 > 3, 4 = 5

• 2 > 3, 4 > 5

A

B

C

D

Source: adidas Group Geschäftsbericht 2014

Page 30

Does it get more obvious now?

April 2016 4. Finance Performance Day

1

2

3

4

5

6

Without legend it isvisible that 2 is biggerthan 3

Without legend it isvisible that 4 is exactlyas big as 5

Page 31

Über die Hälfte der Beschäftigten sind in Europaangesiedelt

April 2016 4. Finance Performance Day

Mitarbeiter nach Regionen (zum Jahresende 2014; in Prozent)

Schwellenländer Europas

Nordamerika

Westeuropa

China

Lateinamerika

Andere Asiatische Märkte

33 %

24 %

21 %

8 %

8 %

6 %

Page 32

Über die Hälfte der Beschäftigten sind in Europaangesiedelt

April 2016 4. Finance Performance Day

Mitarbeiter nach Regionen (zum Jahresende 2014; in Prozent)

Schwellenländer Europas

Nordamerika

Westeuropa

China

Lateinamerika

Andere Asiatische Märkte

33 %

24 %

21 %

8 %

8 %

6 %

SAY:The message is highlightedin the header

EXPRESSBy using a different type ofchart it is now possible torealize whether values differor not

SAY:The most interestingdata points arehighlighted

UNIFY:The unified header for all reportscontains all necessary informationabout the chart

Page 33

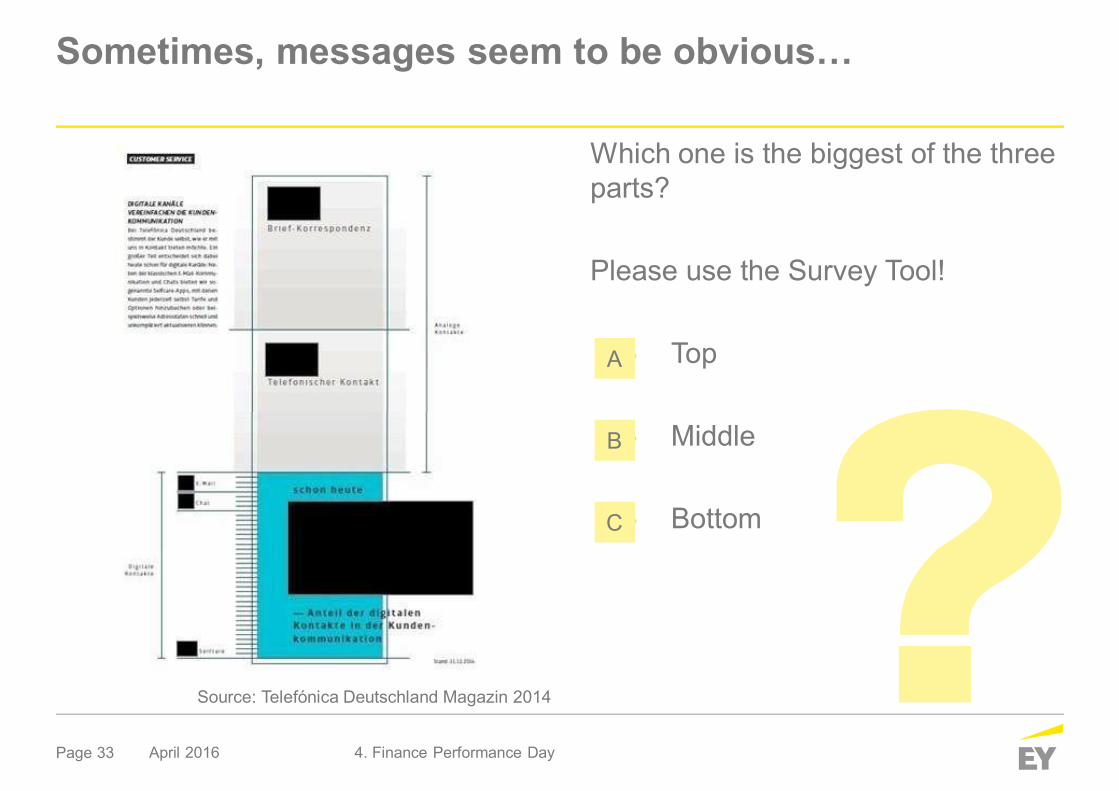

Sometimes, messages seem to be obvious…

April 2016 4. Finance Performance Day

Which one is the biggest of the threeparts?

Please use the Survey Tool!

• Top

• Middle

• Bottom

A

B

C

Source: Telefónica Deutschland Magazin 2014

Page 34

… but the visualization lies to the user

April 2016 4. Finance Performance Day

39% is the smaller numbercompared to 43% but takes moreroom in the chartThe users perception is fooled by aninappropriate graphicalrepresentation

It is possible to stress this part of thechart without displaying wronginformation!Source: Telefónica Deutschland Magazin 2014

Page 35

Digitale Kontakte machten bereits 39% derKommunikation aus

April 2016 4. Finance Performance Day

39 %

43 %

18 % Brief-Korrespondenz

TelefonischerKontakt

Digitale Kontakte

E-Mail 4%Chat 4%

Selfcare 31%

Anteil der Kundenkontakte je Kontaktmedium(Ganzjahreswerte 2014; in Prozent)

Page 36

Digitale Kontakte machten bereits 39% derKommunikation aus

April 2016 4. Finance Performance Day

39 %

43 %

18 % Brief-Korrespondenz

TelefonischerKontakt

Digitale Kontakte

E-Mail 4%Chat 4%

Selfcare 31%SAY:The most interesting datapoint is highlighted

SIMPLIFY:Details are shown onlywhere relevant and ofinterest and omittedotherwise

CHECK:The scaling is now correct

SAY:The message is highlighted inthe header

Anteil der Kundenkontakte je Kontaktmedium(Ganzjahreswerte 2014; in Prozent)

UNIFY:The unified header for all reportscontains all necessary informationabout the chart

Page 37

Before you ask – YES, this applies to tables as well!

April 2016 4. Finance Performance Day

“But I am interested in financialreports – I need to read tables andfigures. Information Design does notapply to this!”

Yes, it does! Tables with figurescan be supported with visualelements to convey an easilyunderstandable message!

Page 38

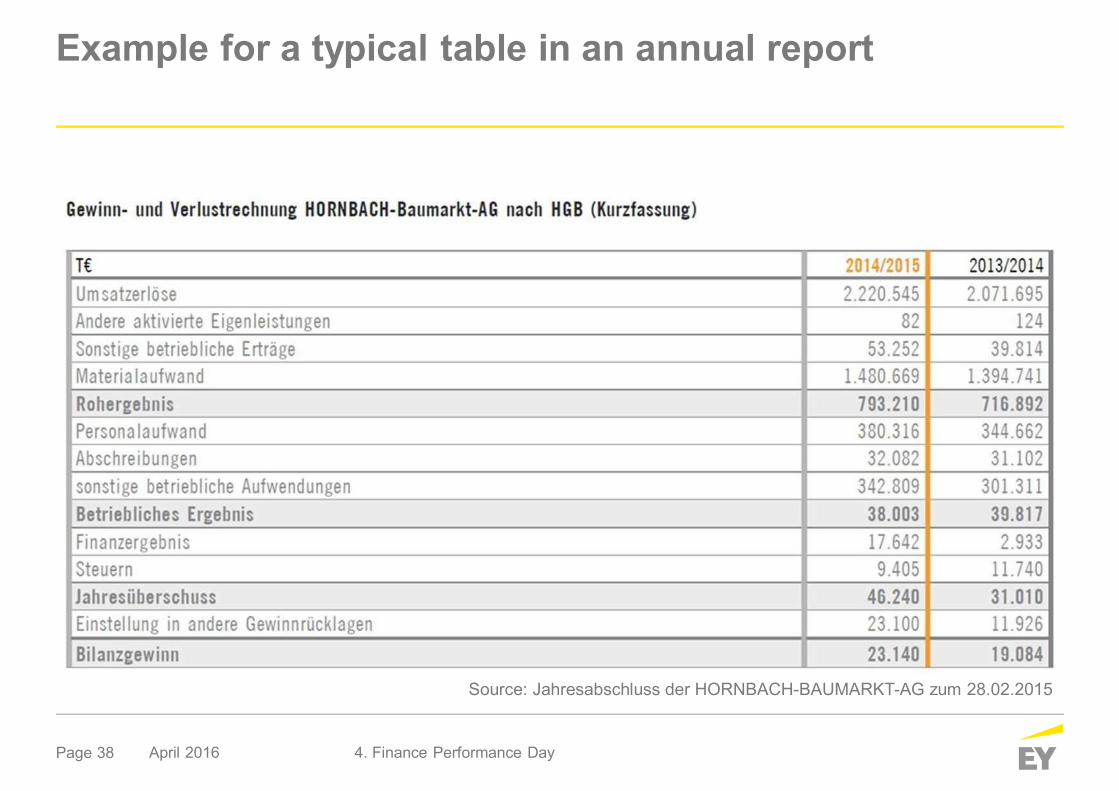

Example for a typical table in an annual report

April 2016 4. Finance Performance Day

Source: Jahresabschluss der HORNBACH-BAUMARKT-AG zum 28.02.2015

Page 39

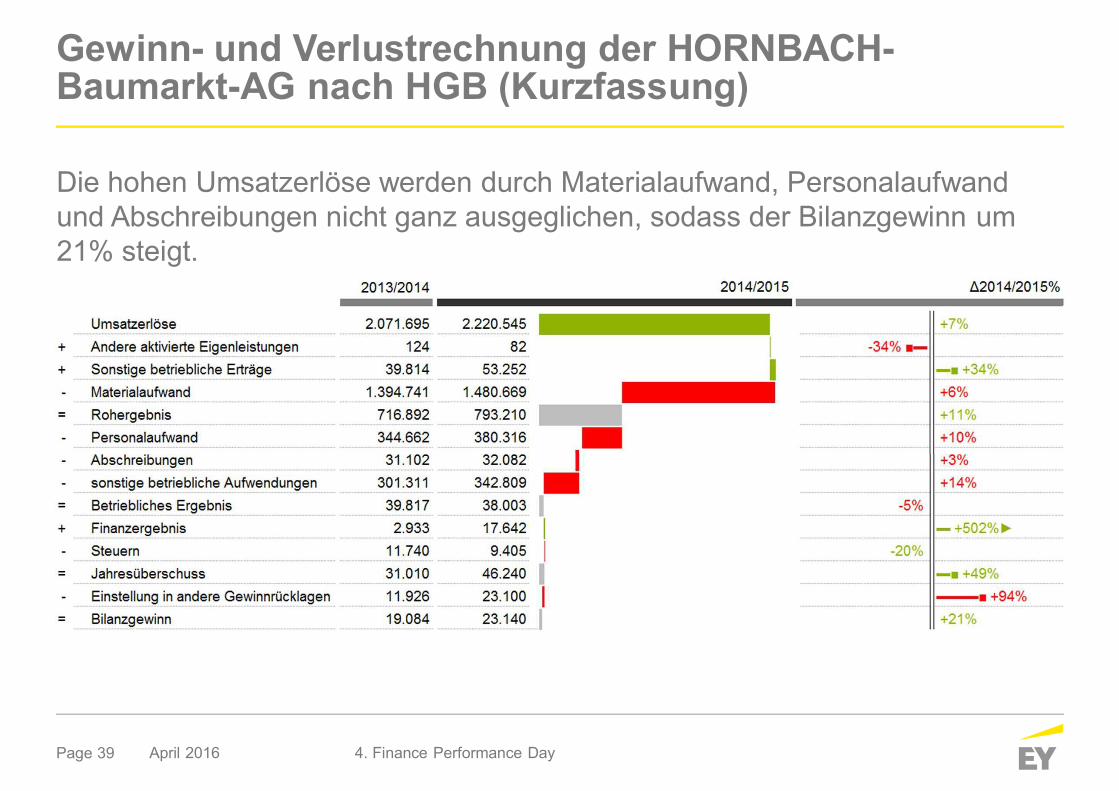

Gewinn- und Verlustrechnung der HORNBACH-Baumarkt-AG nach HGB (Kurzfassung)

April 2016 4. Finance Performance Day

Die hohen Umsatzerlöse werden durch Materialaufwand, Personalaufwandund Abschreibungen nicht ganz ausgeglichen, sodass der Bilanzgewinn um21% steigt.

Page 40

Gewinn- und Verlustrechnung der HORNBACH-Baumarkt-AG nach HGB (Kurzfassung)

April 2016 4. Finance Performance Day

Die hohen Umsatzerlöse werden durch Materialaufwand, Personalaufwand undAbschreibungen nicht ganz ausgeglichen, sodass der Bilanzgewinn um 21% steigt.

STRUCTURE:Ascending years are sortedleft to right

SAY:Header tells the conclusion ofthe chart

SAY:The high numbers arevisualized so that the user caneasily focus on the importantparts

STRUCTURE:It is made visible how thecategories relate to each other

UNIFYRed and green color are usedas they are well knownsymbols for „good“ and „bad“

Page 41

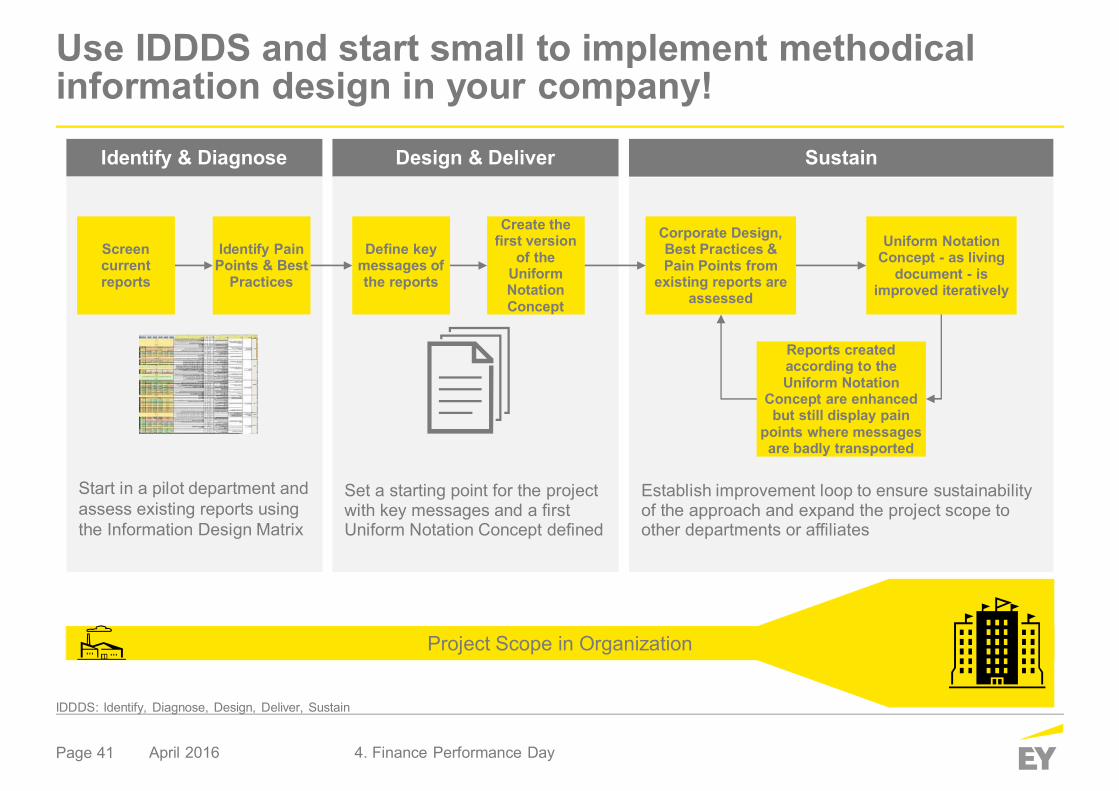

Use IDDDS and start small to implement methodicalinformation design in your company!

April 2016 4. Finance Performance Day

Identify & Diagnose Design & Deliver Sustain

Start in a pilot department andassess existing reports usingthe Information Design Matrix

Set a starting point for the projectwith key messages and a firstUniform Notation Concept defined

Establish improvement loop to ensure sustainabilityof the approach and expand the project scope toother departments or affiliates

Define keymessages ofthe reports

Create thefirst version

of theUniformNotationConcept

Identify PainPoints & Best

Practices

Screencurrentreports

Corporate Design,Best Practices &Pain Points from

existing reports areassessed

Uniform NotationConcept - as living

document - isimproved iteratively

Reports createdaccording to theUniform Notation

Concept are enhancedbut still display pain

points where messagesare badly transported

Project Scope in Organization

IDDDS: Identify, Diagnose, Design, Deliver, Sustain

Page 42 April 2016 4. Finance Performance Day

The efficiency of BI depends on interpretability of theresulting reports…

… and thus can be improved with Methodical InformationDesign

Page 43

Ihre Ansprechpartner

April 2016 4. Finance Performance Day

Oliver Becker

Partner

Ernst & Young GmbHWirtschaftsprüfungsgesellschaft

Graf-Adolf-Platz 15 40213DüsseldorfTelefon +49 211 9352 18655Mobil +49 (160) 939 [email protected]

Damir Zubobiv

Executive Director

Ernst & Young GmbHWirtschaftsprüfungsgesellschaft

Theodor-Heuss-Anlage 268165 MannheimTelefon +49 621 4208 20112Mobil +49 (160) 939 [email protected]

Page 44

Agenda

Einführung1 09:30

Agile Unternehmensplanung erfolgreich und nachhaltigumsetzen

3

11:15

Best in Class Reporting2 09.35

10:45

5 12:25

Business LunchLive Demo - Reporting mit arcplan sowie tableau6 12:35

April 2016 4. Finance Performance Day

Schlusswort

PAUSELive Demo - Reporting mit arcplan sowie tableau

4

Page 45

Ihre Ansprechpartner

April 2016 4. Finance Performance Day

Alexandra Knestel

Manager - arcplan

Ernst & Young GmbHWirtschaftsprüfungsgesellschaft

Arnulfstraße 5980636 MünchenTelefon +49 9352 16022Mobil +49 (160) 939 [email protected]

Matthias Kopp

Senior - tableau

Ernst & Young GmbHWirtschaftsprüfungsgesellschaftStuttgart F61Flughafenstraße 6170629 StuttgartTelefon +49 711 9881 19104Mobil +49 (160) 939 [email protected]

Page 46

Agenda

Einführung1 09:30

Agile Unternehmensplanung erfolgreich und nachhaltigumsetzen

3

11:15

Best in Class Reporting2 09.35

10:45

5 12:25

Business LunchLive Demo - Reporting mit arcplan sowie tableau6 12:35

April 2016 4. Finance Performance Day

Schlusswort

PAUSELive Demo - Reporting mit arcplan sowie tableau

4

Page 47

Agile Unternehmensplanung erfolgreich und nachhaltigumsetzen - Agenda

April 2016 4. Finance Performance Day

I. How does agile planning look like?• Leading practices and current trends• What’s next?• Agile Planning implemented – Client example

II. How can agile planning be implementedsuccessfully?

• Implementation strategy• Rapid prototyping• Organizational requirements

Page 48

Companies with a distinct target setting process andbinding targets reduce process cycle times and effort

I. How does agile planning look like?Established leading practices

April 2016

Focused target setting and driver based planning on an appropriate level ofdetail are key levers to significantly improve planning

Driver based planning helps to focus planning efforts,increase understanding of performance and link

planning with strategy

Customer AnalysisDashboard

Revenue

Direct Costs

OPEX

Value driversFinancial KPI

Revenue AnalysisExisting

customers

Customersacquired

Customerschurned

Averageconsumption

Number ofcustomers

Sales price

Net promoterscore

First callresolution

OnlineRating

Strategic initiativesValue Creation Strategy

Improve CustomerExperience

Strategic indicators

Implement efficientservice processes

Enhance consumptiontransparency for customers

Optimize support structure

Group

Division

BU

ProfitCenter

Mid-termPlan Budget

StrategicUpdate

UpdateTargetsagreed andallocated

Supporting process

Main process

Reconciliation

Top-down allocationPlanning activity

TargetSetting

Planapproved

S&OP

Integration

Negotiation/iteration

Demand Demand

Supply

Demand

Supply Supply

Demand

4. Finance Performance Day

Page 49

A rolling forecasting can be done in alternative ways,sticking to annual planning time frames if required

I. How does agile planning look like?Current trends

April 2016

Rolling forecasting and a continuous way of planning improve visibility andreduce effort of annual planning cycle

Planning occasions building upon each othercontinuously will result in a faster annual planning -

budget as a “snapshot”

1st Review

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4QYear x Year x+1

2nd Review

3rd Review

4th Review

Annual plan

Actuals

2nd Review

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4QYear x Year x+1

3rd Review

4th Review

Forecast

Alternative to rolling forecast

Rolling forecast

1st ReviewAnnual plan

Mid-term planAll drivers to be

updated

BudgetBreakdown by seasonality

and reference data

RollingforecastMajor 5 -7

drivers to beupdated

Commondrivermodel

4. Finance Performance Day

Page 50

I. How does agile planning look like?What’s next?

April 2016

Pre-filled throughdriver analytics

KPIs

Data

Driver based planning(DBP)

Pre-built DBP using rule-baseddriver analytics

Manual Plan build

Machine learning & artificial intelligence

Pre-built DBP using analyticsfactory

HR costs

Headcount

Salary per Head

Travel Expense

LaborExpenses Fringe % of Salaries

Training cost as% of salary

Travel Expenseper Headcount

50

50k

18%

5%

3.075.000

50 x 50025.000

3.100.000

Prepare Build Deploy Consume

ERP

Datawarehouse

External

Analyticsfactory

Pre-populatevalues

Planningapp

Materialdriver

Planning analytics maturity Methods of planning analytics

Analytics and digitalization have significant potential to shift paradigms inplanning, budgeting and forecasting

4. Finance Performance Day

Page 51

A two-layer solution architecture enables aggregated,driver based planning and accurate calculations based

on details

Data layer

I. How does agile planning look like?Agile Planning implemented – Client Example

April 2016

Leading practices enabled by state-of-the-art IT transform planning into ahighly flexible, business centered steering instrument

Fast & flexible planning model enables analysis anddiscussion of several scenarios, budget breakdown after

approval

Aggregation Distribution &Disaggregation Transformation

Cost & activity types Cost centers

Revenue planning

Driver 1 Driver 2 Driver 3…OPEX planning

Driver 4 Driver 5 Driver 6

Product costing

Planning layer

SAP ERPBudget

(SAP ERP)FC0 Driver basedplanning tool

Detailed budgetingin SAP ERP

Aug Sep Oct Nov DecNov … Jan Feb

Budget(SAPERP)

Budget(SAP ERP)

Driver basedplanning model

FC0FC1

FC2

Load data fromprevious budget

Load newbudgetdata

Results

FunctionalInput

(S&OP)

Approval

Decoupling mid-term planning from budgeting in SAP ERP

4. Finance Performance Day

Page 52

A company specific planning framework consists of different,purpose specific planning & forecasting models

II. How can agile planning be implemented successfully?Implementation strategy

April 2016

Successful implementation will always be based on strategy and scope whichmatch the individual circumstances of a company

The best fitting implementation strategy depends ondiversity of businesses and on degree of autonomy

within a group

Corporate model

BusinessSegment

model

Externalmodel

Common dimensions& structuresCommon logics

Revenue planningVariable costsSpecific OPEX

Immaterial businesseswith own planningHighly specializedplanning requirements

Focus on needsof GroupMainly financial content

Focus on BusinessSegment needsSpecific per BusinessSegment

Left out of commonplanning frameworkto manage complexity

Type ofmodel Focus of model Model contents

The businesssegment model

The consolidation& corporate model

The full solutionmodel The proof of concept

model

HighLowLow

High

Business autonomy

4. Finance Performance Day

Page 53

II. How can agile planning be implemented successfully?Implementation strategy – Client example

April 2016

How to build a highly flexible,business specific planningapproach while exploitingsynergies from harmonizationof common requirements?

Most suitable planningapproaches and methods fordifferent businesses andfunctions

Common approach foroverhead and balance sheetplanning

Automated transfer of subplans into common profit &loss and cash flow statementstructures

Overhead planning Balance Sheet Cash Flow

Corporate Planning Framework

Sellingexpense

Revenue

Cost ofproduction

Warranties

Value driver

Salesvolume

Net Priceper unit

Marketvolume

Own marketshare

GDP growth

Householdincome

Marketingspend

DemandvolumeProduct/

volume mix

Gross priceGLU

Averageoptions

Gross priceper unit

Discountfactor

Customerloyalty

Sales newcars

Sales usedcars

Aftersales

KPI Analytics

Sales & Marketing Engineering Manufacturing New businessesRevenue,

volumes & marginMarketing

costs

…

Target setting,cycle planning

Programplanning

…

Purchasing

COGS

…

Connected car

On demandservices

…

A modular planning model balances high degree of harmonization andconsideration of business specific requirements

4. Finance Performance Day

Page 54

Successful prototyping requires a solid functionaldesign before start of iterative implementation

II. How can agile planning be implemented successfully?Rapid prototyping

April 2016

An iterative prototyping approach increases usability and shortensimplementation through constant end user involvement

Functionalities covering groups of connectedrequirements are developed in iteration cycles based on

regular feedback

Techn. Design TestingBuild

Prototype 1

Design &Proof of Concept

Test &Feedback

Prototype 2

Prototype 3

Prototype 1

Prototype 2

Prototype 3

Build &adjust

Functional design Implementation Go Live &Support

Requirements

Cycle

Schedule

Showcase + Feedback

4. Finance Performance Day

Page 55

Typical tasks to manage a common planning frameworkrequire a mix of finance, IT and operations professionals

II. How can agile planning be implemented successfully?Organizational requirements

April 2016

A common planning framework requires an appropriate governance andsupport organization to be sustainable and add value

Centralized governance will achieve tangible costsavings by balancing consistency and individual

requirements

Cost reduction throughplanning optimization

Cost and complexity after planningoptimization

Costs withoutcentral governance

Costs with centralgovernance

Low

High

Time

Process & Technology

Manages planning processthrough specialized expertresourcesLeverages technology

Change management

Maintains consistency offrameworkProvides centralized one stopshop for end user

Data management

Safeguards on-going dataintegrity & qualityAssesses impact beforechanges

Continuous improvement

Looks for opportunities tofurther improveAdvises users in case ofchanging requirements

Training/On-boarding

Delivers on-going trainingsessionsMaintains methods andpolicies

Decision support

Assists users with ad hocanalysisProvides analytics

4. Finance Performance Day

Page 56

Ihre Ansprechpartner

April 2016 4. Finance Performance Day

Csaba Orban

Partner

Ernst & Young GmbHWirtschaftsprüfungsgesellschaft

Mergenthalerallee 3-565760 EschbornTelefon +49 6196 996 20275Mobil +49 (160) 939 [email protected]

Page 57

Agenda

Einführung1 09:30

Agile Unternehmensplanung erfolgreich und nachhaltigumsetzen

3

11:15

Best in Class Reporting2 09.35

10:45

5 12:25

Business LunchLive Demo - Reporting mit arcplan sowie tableau6 12:35

April 2016 4. Finance Performance Day

Schlusswort

PAUSELive Demo - Reporting mit arcplan sowie tableau

4

Page 58

Hinweise zu dieser Präsentation

Die im Rahmen dieser Präsentation zur Verfügung gestellten Informationen können naturgemäß wederallumfassend noch auf die speziellen Bedürfnisse eines bestimmten Einzelfalls zugeschnitten sein. Siebegründen keine Beratung, keine andere Form rechtsverbindlicher Auskünfte oder ein rechtsverbindlichesAngebot unsererseits.Diese Präsentation beruht auf dem Rechtsstand zum Zeitpunkt des Datums dieser Präsentation und gibt unsereInterpretation der relevanten gesetzlichen Bestimmungen und die hierzu ergangene Rechtsprechung wieder.Im Zeitablauf treten Änderungen bei Gesetzen, der Interpretation von Rechtsquellen sowie in derRechtsprechung ein. Derartige Änderungen können eine Fortschreibung dieser Präsentation erforderlich machen.Wir weisen ausdrücklich darauf hin, dass wir ohne gesonderten Auftrag nicht verpflichtet sind, diese Präsentationaufgrund einer Änderung der zugrunde liegenden Fakten bzw. Annahmen oder Änderungen in der Gesetzgebungoder Rechtsprechung zu überprüfen und gegebenenfalls fortzuschreiben.Wir übernehmen keine Gewährleistung oder Garantie für Richtigkeit oder Vollständigkeit der Inhalte dieserPräsentation. Soweit gesetzlich zulässig, übernehmen wir keine Haftung für ein Tun oder Unterlassen, das Sieallein auf Informationen aus dieser Präsentation gestützt haben. Dies gilt auch dann, wenn diese Informationenungenau oder unrichtig gewesen sein sollten.

April 2016 4. Finance Performance Day