401(k) plan asset allocation, account balances, and … · 401(k) plan asset allocation, account...

TRANSCRIPT

A research report from the EBRI Education and Research Fund © 2017 Employee Benefit Research Institute

August 3, 2017 • No. 436

401(k) Plan Asset Allocation, Account Balances, and Loan

Activity in 2015

By Jack VanDerhei, EBRI; Sarah Holden, ICI; Luis Alonso, EBRI; and Steven Bass, ICI

A T A G L A N C E

The bulk of 401(k) assets were invested in stocks. On average, at year-end 2015, 66 percent of 401(k)

participants’ assets were invested in equity securities through equity funds, the equity portion of balanced

funds, and company stock. Twenty-seven percent was in fixed-income securities such as stable-value

investments, bond funds, and money funds.

More 401(k) plan participants held equities at year-end 2015 than before the financial market

crisis (year-end 2007), and most had the majority of their accounts invested in equities. For

example, about three-quarters of participants in their 20s had more than 80 percent of their 401(k) plan

accounts invested in equities at year-end 2015, up from less than half of participants in their 20s at year-end

2007. Overall, more than 90 percent of 401(k) participants had at least some investment in equities at year-end

2015.

Nearly 65 percent of 401(k) plans, covering nearly three-quarters of 401(k) plan participants,

included target-date funds in their investment lineup at year-end 2015. At year-end 2015, 20 percent

of the assets in the EBRI/ICI 401(k) database were invested in target-date funds and about half of 401(k)

participants in the database held target-date funds. Also known as lifecycle funds, these funds are designed to

offer a diversified portfolio that automatically rebalances to be more focused on income over time.

A majority of new or recent hires invested their 401(k) assets in balanced funds, including target-

date funds. For example, at year-end 2015, 70 percent of recently hired participants held balanced funds in

their 401(k) plan accounts. Balanced funds comprised 41 percent of the account balances of recently hired

401(k) participants at year-end 2015. A significant subset of that balanced fund category is invested in target-

date funds. At year-end 2015, 34 percent of the account balances of recently hired participants were invested in

target-date funds.

401(k) participants’ investment in company stock continued at historically low levels. Less than

7 percent of 401(k) assets were invested in company stock at year-end 2015, roughly the same share as in

2012, 2013, and 2014. This share has fallen by 63 percent since 1999 when company stock accounted for

19 percent of assets. Recently hired 401(k) participants contributed to this trend: they tend to be less likely to

hold company stock. At year-end 2015, about one-quarter of recently hired 401(k) plan participants in plans

offering company stock held company stock, compared with about 43 percent of all 401(k) participants.

401(k) participants were less likely to have loans outstanding at year-end 2015 than at year-end

2014. At year-end 2015, 18 percent of all 401(k) participants who were eligible for loans had loans outstanding

against their 401(k) plan accounts, down from 20 percent at year-end 2014. Loans outstanding amounted to

ebri.org Issue Brief • August 3, 2017 • No. 436 2

12 percent of the remaining account balance, on average, at year-end 2015, up 1 percentage point from year-

end 2014. Loan amounts also edged up a bit in 2015.

The year-end 2015 average 401(k) plan account balance in the database was 3.8 percent lower

than the year before, reflecting in large part the changing composition of the sample rather than

the experience of typical 401(k) participants in 2015. To understand changes in 401(k) participants’

average account balances, it is important to analyze a sample of consistent participants. For 401(k) participants

present in both 2014 and 2015, the average account balance increased by 3.1 percent. As with previous

EBRI/ICI updates, analysis of a sample of consistent 401(k) plan participants is expected to be published later

this year.

The average 401(k) plan account balance tends to increase with participant age and tenure. For

example, at year-end 2015, participants in their 40s with more than two to five years of tenure had an average

401(k) plan account balance of close to $35,000, compared with an average 401(k) plan account balance of

more than $280,000 among participants in their 60s with more than 30 years of tenure.

ebri.org Issue Brief • August 3, 2017 • No. 436 3

Jack VanDerhei is director of Research at the Employee Benefit Research Institute (EBRI). Sarah Holden is senior

director of Retirement and Investor Research at the Investment Company Institute (ICI). Luis Alonso is director of

Information Technology and Research Databases at EBRI. Steven Bass is an associate economist at ICI. This Issue Brief

was written with assistance from the Institute’s research and editorial staffs. Any views expressed in this report are

those of the authors, and should not be ascribed to the officers, trustees, or other sponsors of EBRI, EBRI-ERF, or their

staffs. Neither EBRI nor EBRI-ERF lobbies or takes positions on specific policy proposals. EBRI invites comment on this

research.

Suggested citation: Jack VanDerhei, Sarah Holden, Luis Alonso, and Steven Bass. “401(k) Plan Asset Allocation,

Account Balances, and Loan Activity in 2015.” EBRI Issue Brief, no. 426, and ICI Research Perspective, Vol. 23, no. 6

(August 2017).

Copyright Information: This report is copyrighted by the Employee Benefit Research Institute (EBRI) and by the

Investment Company Institute (ICI). It may be used without permission but citation of the source is required.

Report availability: This report is available on the Internet at www.ebri.org and at www.ici.org

Since 1996, the Employee Benefit Research Institute (EBRI) and the Investment Company Institute (ICI) have worked

together on collecting and analyzing annual data on millions of 401(k) plan participants’ accounts. This report reflects

the year-end 2015 update of these data and EBRI’s and ICI’s ongoing research into 401(k) plan participants’ activity.

Table of Contents Introduction .......................................................................................................................................................... 7

EBRI/ICI 401(k) Database ...................................................................................................................................... 7

Sources and Types of Data ................................................................................................................................. 7

Investment Options ........................................................................................................................................... 7

About the EBRI/ICI Database ................................................................................................................................. 8

Distribution of Plans, Participants, and Assets by Plan Size .................................................................................... 8

About Changes in Account Balances ...................................................................................................................... 10

Relationship of EBRI/ICI 401(k) Database Plans to the Universe of All 401(k) Plans .............................................. 10

Age and Tenure of 401(k) Plan Participants ....................................................................................................... 10

Year-End 2015 Snapshot of 401(k) Participants’ Account Balances .......................................................................... 10

Factors That Affect 401(k) Participants’ Account Balances ................................................................................... 10

Definition of 401(k) Plan Account Balance .......................................................................................................... 13

Size of 401(k) Plan Account Balances .................................................................................................................... 13

Relationship of Age and Tenure to 401(k) Plan Account Balances ........................................................................ 13

Relationship Between 401(k) Plan Account Balances and Salary .......................................................................... 17

Year-End 2015 Snapshot of 401(k) Participants’ Asset Allocation ............................................................................. 17

Changes in Asset Allocation Between Year-End 2014 and Year-End 2015 ............................................................. 21

Asset Allocation and Participant Age .................................................................................................................. 21

Asset Allocation and Investment Options ........................................................................................................... 21

Asset Allocation by Investment Options and Age, Salary, and Plan Size ................................................................ 21

Distribution of Equity Fund Allocations and Participant Exposure to Equities ......................................................... 23

Asset Allocation to Equity Funds .................................................................................................................... 23

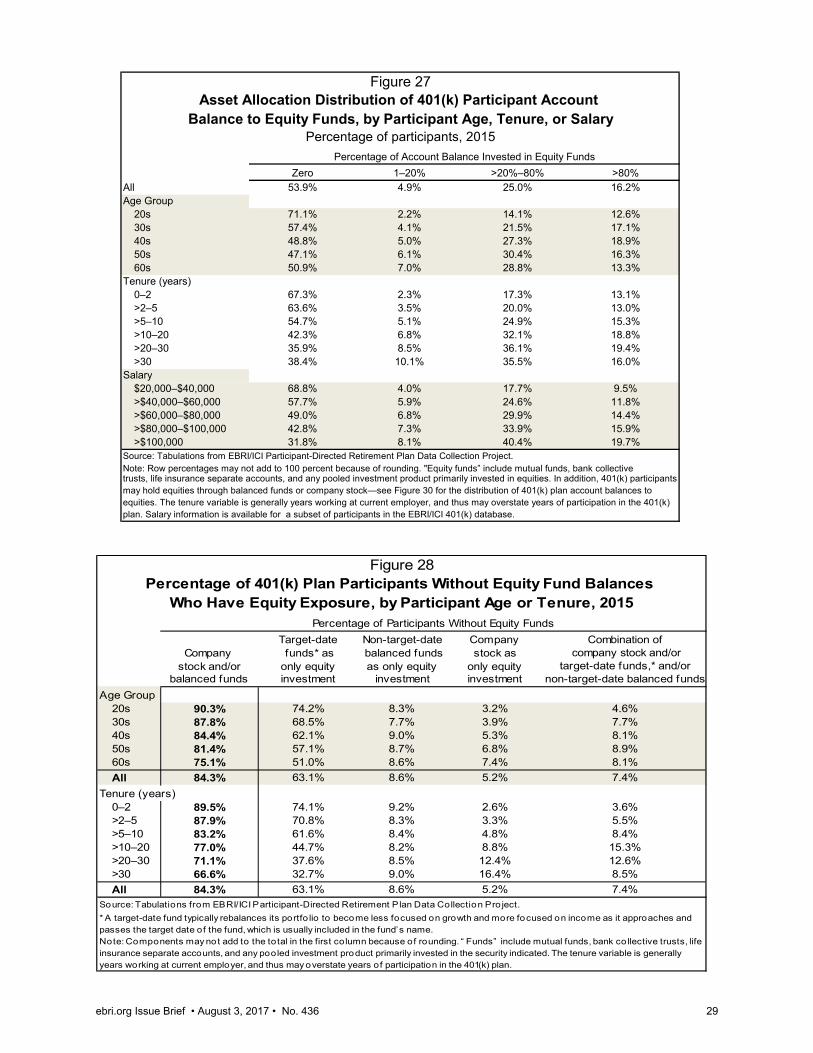

Asset Allocation of 401(k) Plan Participants Without Equity Funds .................................................................... 28

ebri.org Issue Brief • August 3, 2017 • No. 436 4

Asset Allocation to Equities ........................................................................................................................... 28

Changes in Concentrations in Equities Since the Financial Crisis ....................................................................... 28

Distribution of 401(k) Participants’ Balanced Fund Allocations by Age .................................................................. 28

Distribution of 401(k) Participants’ Company Stock Allocations ............................................................................ 31

Asset Allocations of Recently Hired Participants .............................................................................................. 31

Year-End 2015 Snapshot of 401(k) Plan Loan Activity ............................................................................................. 35

Availability and Use of 401(k) Plan Loans by Plan Size ........................................................................................ 35

401(k) Plan Loan Activity Varies with Participant Age, Tenure, Account Balance, and Salary .................................. 35

Average Loan Balances .................................................................................................................................... 35

References ......................................................................................................................................................... 499

Endnotes .......................................................................................................................................................... 555

Figures

Figure 1, 401(k) Plan Characteristics, by Number of Plan Participants, 2015 ............................................................... 9

Figure 2, Distribution of 401(k) Plans, Participants, and Assets ................................................................................ 9

Figure 3, 401(k) Plan Characteristics, by Plan Assets, 2015 ....................................................................................... 9

Figure 4, EBRI/ICI 401(k) Database Represents a Wide Cross Section of the 401(k) Universe ................................... 11

Figure 5, 401(k) Participants Represent a Range of Ages ........................................................................................ 12

Figure 6, 401(k) Participants Represent a Range of Job Tenures ............................................................................ 12

Figure 7, Domestic Stock and Bond Market Indexes ............................................................................................... 14

Figure 8, Percent Change in Total Return Indexes .................................................................................................. 14

Figure 9, Snapshot of Year-End 401(k) Plan Account Balances ................................................................................ 15

Figure 10, Distribution of 401(k) Plan Account Balances, by Size of Account Balance ............................................ 16

Figure 11, Age Composition of Selected 401(k) Plan Account Balance Categories ................................................. 16

Figure 12, Tenure Composition of Selected 401(k) Plan Account Balance Categories ................................................. 18

Figure 13, 401(k) Plan Account Balances Increase With Participant Age and Tenure ................................................. 18

Figure 14, 401(k) Plan Account Balances Less Than $10,000, by Participant Age and Tenure .................................... 19

Figure 15, 401(k) Plan Account Balances Greater Than $100,000, by Participant Age and Tenure .......................... 19

Figure 16, Median 401(k) Plan Account Balance Among Longer-Tenured Participants, by Age and Salary, 2015 .......... 20

Figure 17, Ratio of 401(k) Plan Account Balance to Salary, by Participant Age and Tenure ..................................... 20

Figure 18, Ratio of 401(k) Plan Account Balance to Salary for Participants in Their 20s, by Tenure....................... 22

Figure 19, Ratio of 401(k) Plan Account Balance to Salary for Participants in Their 60s, by Tenure....................... 22

Figure 20, 401(k) Plan Assets Are Concentrated in Equities ..................................................................................... 23

ebri.org Issue Brief • August 3, 2017 • No. 436 5

Figure 21, Average Asset Allocation of 401(k) Plan Accounts, by Participant Age ...................................................... 24

Figure 22, Distribution of 401(k) Plans, Participants, and Assets, by Investment Options, 2015 ................................. 24

Figure 23, Average Asset Allocation of 401(k) Plan Accounts, by Participant Age and Investment Options .................. 25

Figure 24, Average Asset Allocation of 401(k) Plan Accounts, by Participant Salary and Investment Options ............... 26

Figure 25, Average Asset Allocation of 401(k) Plan Accounts, by Plan Size and Investment Options ........................... 27

Figure 26, Asset Allocation Distribution of 401(k) Participant Account Balance to Equity Funds, by Participant Age ...... 27

Figure 27, Asset Allocation Distribution of 401(k) Participant Account Balance to Equity Funds, by Participant Age,

Tenure, or Salary .................................................................................................................................... 29

Figure 28, Percentage of 401(k) Plan Participants Without Equity Fund Balances Who Have Equity Exposure, by

Participant Age or Tenure, 2015 ............................................................................................................... 29

Figure 29, Average Asset Allocation for 401(k) Plan Participants Without Equity Fund Balances, by Participant Age or

Tenure ................................................................................................................................................... 30

Figure 30, Asset Allocation to Equities Varied Widely Among 401(k) Plan Participants ............................................... 32

Figure 31, Exposure to Equities Increased Among 401(k) Participants Between 2007 and 2015 ................................. 32

Figure 32, Asset Allocation Distribution of 401(k) Participant Account Balance to Balanced Funds, by Age .................. 33

Figure 33, Asset Allocation Distribution of 401(k) Participant Account Balance to Balanced Funds, by Tenure ............. 34

Figure 34, Asset Allocation Distribution of 401(k) Participant Account Balance to Company Stock in 401(k) Plans With

Company Stock, by Participant Age .......................................................................................................... 35

Figure 35, Many Recently Hired 401(k) Plan Participants Hold Balanced Funds ......................................................... 35

Figure 36, Many Recently Hired 401(k) Plan Participants Hold Target-Date Balanced Funds ...................................... 37

Figure 37, Many Recently Hired 401(k) Participants Hold High Concentrations in Balanced Funds .............................. 38

Figure 38, Many Recently Hired 401(k) Participants Hold High Concentrations in Target-Date Funds .......................... 40

Figure 39, Asset Allocation Distribution of 401(k) Plan Account Balance to Balanced Funds Among Recently Hired

Participants, by Participant Age ................................................................................................................ 41

Figure 40, Average Asset Allocation of 401(k) Plan Accounts, by Participant Age Among Recently Hired 401(k) Plan

Participants With Two or Fewer Years of Tenure ....................................................................................... 42

Figure 41, Recently Hired 401(k) Participants Tend to Be Less Likely to Hold Company Stock ...................................... 42

Figure 42, New 401(k) Participants Tend Not to Hold High Concentrations in Company Stock ................................ 43

Figure 43, Asset Allocation Distribution of Recently Hired 401(k) Participant Account Balance to Company Stock in

401(k) Plans With Company Stock, by Participant Age ............................................................................... 43

Figure 44, Percentage of 401(k) Plans Offering Loans, by Plan Size, 2015 ............................................................ 44

Figure 45, Percentage of Eligible 401(k) Plan Participants With 401(k) Plan Loans, by Plan Size, 2015 ................... 44

ebri.org Issue Brief • August 3, 2017 • No. 436 6

Figure 46, 401(k) Loan Balances as a Percentage of 401(k) Plan Account Balances for Participants With 401(k)

Loans, by Plan Size, 2015 ........................................................................................................................ 45

Figure 47, Few 401(k) Participants Had Outstanding 401(k) Loans; Loans Tended to Be Small, Selected Years ....... 45

Figure 48, 401(k) Loan Activity Varied Across 401(k) Plan Participants ..................................................................... 46

Figure 49, 401(k) Loan Balances .............................................................................................................................. 47

Figure 50, 401(k) Loan Amounts Varied Across 401(k) Participants ......................................................................... 48

Figure 51, Loans From 401(k) Plans Tended to Be Small ........................................................................................ 47

ebri.org Issue Brief • August 3, 2017 • No. 436 7

401(k) Plan Asset Allocation, Account Balances, and Loan

Activity in 2015

By Jack VanDerhei, EBRI; Sarah Holden, ICI; Luis Alonso, EBRI; and Steven Bass, ICI

Introduction

Over the past three decades, 401(k) plans have become the most widespread private-sector employer-sponsored

retirement plan in the United States.1 In 2015, an estimated 54 million American workers were active 401(k) plan

participants.2 By year-end 2015, 401(k) plan assets had grown to $4.4 trillion, representing 19 percent of all retirement

assets.3

In an ongoing collaborative effort, the Employee Benefit Research Institute (EBRI)4 and the Investment Company

Institute (ICI)5 collect annual data on millions of 401(k) plan participants as a means to examine how these participants

manage their 401(k) plan accounts. This report is an update of EBRI’s and ICI’s ongoing research into 401(k) plan

participants’ activity through year-end 2015.6 The report is divided into four sections: the first describes the EBRI/ICI

401(k) database; the second presents a snapshot of participant account balances at year-end 2015; the third looks at

participants’ asset allocations, including analysis of 401(k) participants’ use of target-date, or lifecycle, funds; and the

fourth focuses on participants’ 401(k) loan activity.

EBRI/ICI 401(k) Database

Sources and Types of Data

Several recordkeeping organizations provided records on active participants in 401(k) plans at year-end 2015. These

plan recordkeepers include mutual fund companies, banks, insurance companies, and consulting firms. Although the

EBRI/ICI project has collected data from 1996 through 2015, the universe of data providers may vary from year to

year. In addition, the plans with any given provider may change from year to year, which changes the plans provided.

Thus, aggregate figures in this report generally should not be used to estimate time trends.

Records were encrypted before inclusion in the database to conceal the identity of employers and employees, but were

coded so that both could be tracked by researchers over multiple years.7 Data provided for each participant included

date of birth, from which an age group is assigned; date of hire, from which a tenure range is assigned; outstanding

loan balance; funds in the participant’s investment portfolios; and asset values attributed to those funds. An account

balance for each participant is the sum of the participant’s assets in all funds.8 Plan balances are constructed as the

sum of all participant balances in the plan. Plan size is estimated as the sum of active participants in the plan and, as

such, does not necessarily represent the total number of employees at the sponsoring firm.

Within the year-end 2015 EBRI/ICI database, it is possible to link individuals across plans across a majority of the

recordkeepers. This improves the identification of active participants and resulted in the reclassification of 1.1 million

participant accounts that were multiple accounts owned by single individuals. This procedure allows EBRI and ICI to

begin to consolidate account balances for individuals across data providers to provide a more accurate estimate of

average account balances per individual.9

Investment Options

Investment options are grouped into eight broad categories.10

Equity funds consist of pooled investments primarily invested in stocks, including equity mutual funds, bank

collective trusts, life insurance separate accounts, and other pooled investments.

Bond funds are any pooled account primarily invested in bonds.

ebri.org Issue Brief • August 3, 2017 • No. 436 8

Balanced funds are pooled accounts invested in both stocks and bonds. They are classified into two

subcategories: target-date funds and non–target-date balanced funds.

A target-date fund pursues a long-term investment strategy, using a mix of asset classes, or asset allocation,

that the fund provider adjusts to become less focused on growth and more focused on income over time.11

Non–target-date balanced funds include asset allocation, or hybrid, funds in addition to lifestyle funds.12

Company stock is equity in the plan’s sponsor (the employer).

Money funds consist of those funds designed to maintain a stable share price.

Stable-value products, such as guaranteed investment contracts (GICs)13 and other stable-value

funds,14 are reported as one category.

Other is the residual for other investments, such as real estate funds.

Unknown, which is the final category, consists of assets that could not be identified.15

About the EBRI/ICI Database

The EBRI/ICI Participant-Directed Retirement Plan Data Collection Project is the largest, most representative repository

of information about individual 401(k) plan participant accounts. As of December 31, 2015, the EBRI/ICI database

included statistical information about:

• 26.1 million 401(k) plan participants, in

• 101,625 employer-sponsored 401(k) plans, holding

• $1.9 trillion in assets.

The 2015 EBRI/ICI database covers 48 percent of the universe of 401(k) plan participants, 18 percent of plans, and

43 percent of 401(k) plan assets. The EBRI/ICI project is unique because it includes data provided by a wide variety of

plan recordkeepers and, therefore, represents the activity of participants in 401(k) plans of varying sizes—from very

large corporations to small businesses—with a variety of investment options.

Distribution of Plans, Participants, and Assets by Plan Size

The 2015 EBRI/ICI 401(k) database contains information on 101,625 401(k) plans with $1.9 trillion in assets and

26.1 million participants (Figure 1). As in the 401(k) universe at large, most of the plans in the database are small:

59 percent of the plans have 25 or fewer participants, and 24 percent have 26 to 100 participants (Figure 2). In

contrast, only 2 percent of the plans have more than 2,500 participants.

However, participants and assets are concentrated in large plans. For example, 66 percent of participants are in plans

with more than 2,500 participants, and these same plans account for 68 percent of all plan assets.

Because most of the plans have a small number of participants, the asset size for many plans is modest. One-quarter of

the plans have assets of $250,000 or less, and another 29 percent have plan assets between $250,001 and $1,250,000

(Figure 3).

Number of Plan Participants Total Plans Total Participants Total Assets* Average Account Balance1–10 37,299 183,472 $15,199,012,058 $82,84111–25 22,661 379,336 $29,231,758,328 $77,06026–50 14,176 510,903 $37,160,101,117 $72,73451–100 9,918 704,912 $48,369,878,150 $68,618101–250 7,863 1,241,634 $80,931,056,172 $65,181251–500 3,691 1,297,953 $81,319,803,031 $62,652501–1000 2,458 1,724,490 $113,626,446,289 $65,8901,001–2,500 1,906 2,969,211 $211,861,220,666 $71,3532,501–5,000 818 2,883,401 $211,488,103,027 $73,3475,001–10,000 457 3,149,425 $239,898,519,944 $76,172> 10,000 378 11,091,709 $848,198,372,615 $76,471

All 101,625 26,136,446 $1,917,284,271,397 $73,357Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project.Note: The median account balance at year-end 2015 was $16,732.

Total Plan Assets Total Plans Total Participants Total Assets* Average Account Balance$0-$250 25,421 165,084 $2,281,392,080 $13,820$250-$625 15,208 215,627 $6,404,566,546 $29,702$625-$1,250 14,719 326,062 $13,376,319,694 $41,024$1,250-$2,500 14,572 537,251 $26,038,716,458 $48,467$2,500-$6,250 14,360 1,064,449 $56,569,883,213 $53,145$6,250-$12,500 6,661 1,134,792 $58,420,112,123 $51,481$12,500-$25,000 4,006 1,339,327 $70,309,390,837 $52,496$25,000-$62,500 3,205 2,302,859 $124,609,075,745 $54,111$62,500-$125,000 1,391 2,114,232 $122,791,809,419 $58,079$125,000-$250,000 923 2,503,912 $161,576,476,861 $64,530>$250,000 1,159 14,432,851 $1,274,906,528,419 $88,334All 101,625 26,136,446 1,917,284,271,397 $73,357Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project.Note: The median account balance at year-end 2015 was $16,732.* Assets do not add to the total because of rounding.

Figure 3401(k) Plan Characteristics, by Plan Assets, 2015

Figure 1401(k) Plan Characteristics, by Number of Plan Participants, 2015

* Assets do not add to the total because of rounding.

0.4%

42.4% 44.2%

1.3%

23.1%23.5%

15.7%

27.7% 25.4%

23.7%

4.7% 4.5%

59.0%

2.2% 2.3%

Plans Participants Assets

1–2526–100101–2,5002,501–10,000>10,000

Number of Plan Participants

Figure 2Distribution of 401(k) Plans, Participants, and Assets

Percentage of plans, participants, and assets by number of plan participants, 2015

Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project.

ebri.org Issue Brief • August 3, 2017 • No. 436 9

ebri.org Issue Brief • August 3, 2017 • No. 436 10

About Changes in Account Balances

When analyzing the change in participant account balances over time, it is important to have a consistent sample.

Comparing average account balances across different year-end snapshots can lead to false conclusions. For example,

the addition of a large number of new plans with smaller balances to the database would tend to pull down the average

account balance. This could then be mistakenly described as an indication that balances are declining, but actually

would tell us nothing about consistently participating workers. Similarly, the aggregate average account balance would

tend to be pulled down if a large number of older participants retired. In addition, changes in the sample of

recordkeepers and changes in the set of plans for which they keep records also can influence the change in aggregate

average account balance. Thus, to ascertain what is happening to 401(k) participants’ account balances, a set of

consistent participants must be analyzed. Future research will examine linked data to analyze the consistent sample of

participants in the EBRI/ICI data collection effort.

Although the average account balance for the entire database at year-end 2015 is lower than the average account

balance at year-end 2014, this is entirely the result of participants and plans entering and leaving the database. Among

the sample of participants who were present in the database in both 2014 and 2015, the average account balance

increased by 3.1 percent between year-end 2014 and year-end 2015, from $83,175 to $85,729.16

Relationship of EBRI/ICI 401(k) Database Plans to the Universe of All 401(k) Plans

The 2015 EBRI/ICI 401(k) database is a representative sample of the estimated universe of 401(k) plans. At year-end

2015, all 401(k) plans held a total of $4.4 trillion in assets, and the database represents about 43 percent of that

total.17 The database also covers 48 percent of the universe of active 401(k) plan participants and 18 percent of all

401(k) plans.18 The distribution of assets, participants, and plans in the database for 2015 is similar to the universe of

plans as reported by the U.S. Department of Labor (Figure 4).19

Age and Tenure of 401(k) Plan Participants

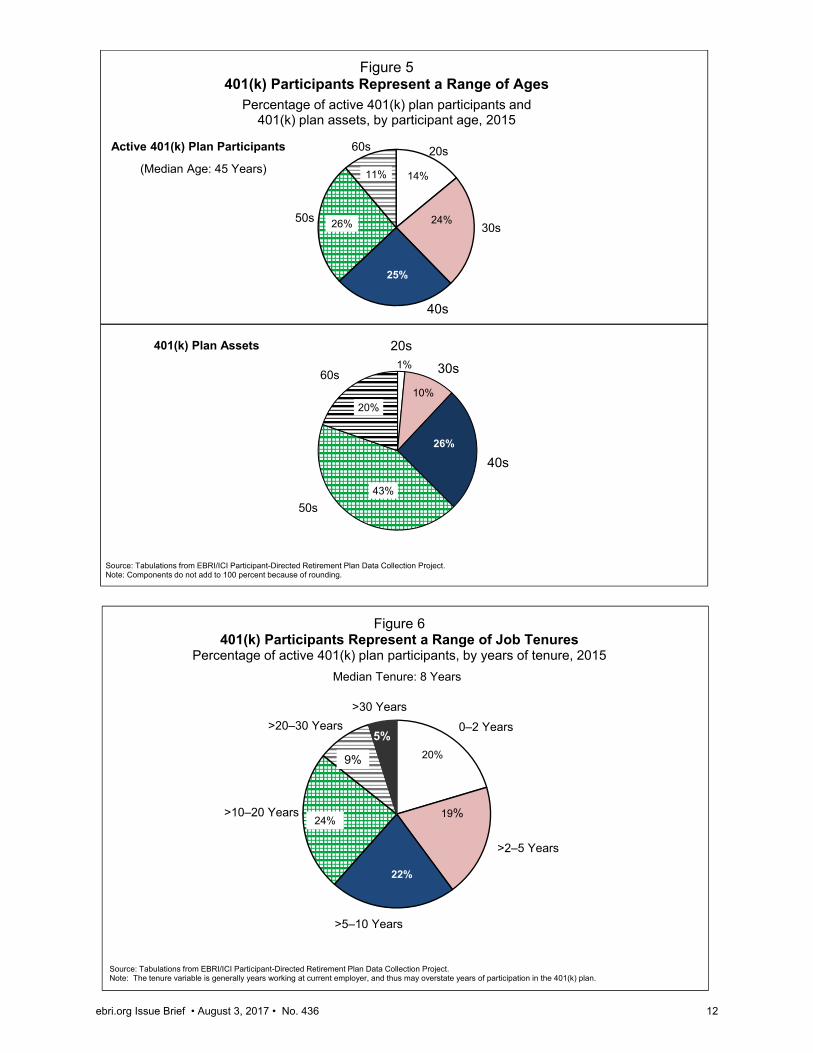

The database includes 401(k) participants across a wide range of age and tenure groups. At year-end 2015, 49 percent

of participants were in their 30s or 40s, while 14 percent of participants were in their 20s, 26 percent were in their 50s,

and 11 percent were in their 60s (Figure 5, upper panel). The median age of the participants in the 2015 database is

45 years, down from 46 years in 2014. Because older participants tend to have larger account balances, assets in the

database are more concentrated among the older 401(k) participant groups. At year-end 2015, 63 percent of 401(k)

plan assets were held by participants in their 50s or 60s, while 11 percent of 401(k) plan assets were held by

participants in their 20s or 30s (Figure 5, lower panel). Participants in 401(k) plans represent a wide range of job

tenure experiences. In 2015, 39 percent of the participants in the database had five or fewer years of tenure and

5 percent had more than 30 years of tenure (Figure 6). The median tenure at the current employer was eight years in

2015, the same as in 2014.

Year-End 2015 Snapshot of 401(k) Participants’ Account Balances

Factors That Affect 401(k) Participants’ Account Balances

In any given year, the change in a participant’s account balance in the database is the sum of three factors:

New contributions by the participant, the employer, or both;

Total investment return on account balances, which depends on the performance of financial markets and on

the allocation of assets in an individual’s account; and

Withdrawals, borrowing, and loan repayments.

0.1915319 19.153190.1548561 15.4856050.0773281 7.73280610.2011285 20.1128490.3751555 37.51555

Sources: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project and U.S. Department of Labor

Figure 4EBRI/ICI 401(k) Database Represents

a Wide Cross Section of the 401(k) Universe

401(k) plan characteristics by number of participants: EBRI/ICI 401(k) database in 2015 versus 2014 DOL Form 5500 for all 401(k) plans

0

20

40

60

80

100

100 or fewer 101 to 500 501 to 1,000 1,001 to 5,000 >5,000Number of plan participants

Plan AssetsPercentage of plan assets

2014 Form 5500

2015 EBRI/ICI

0

20

40

60

80

100

100 or fewer 101 to 500 501 to 1,000 1,001 to 5,000 >5,000Number of plan participants

ParticipantsPercentage of participants

2015 EBRI/ICI

2014 Form 5500

0

20

40

60

80

100

100 or fewer 101 to 500 501 to 1,000 1,001 to 5,000 >5,000Number of plan participants

PlansPercentage of plans

2015 EBRI/ICI

2014 Form 5500

ebri.org Issue Brief • August 3, 2017 • No. 436 11

20s

30s50s

60s

11%

26%

25%

24%

14%(Median Age: 45 Years)

Active 401(k) Plan Participants

40s

Figure 5401(k) Participants Represent a Range of Ages

Percentage of active 401(k) plan participants and 401(k) plan assets, by participant age, 2015

1%

10%

26%

43%

20%

60s

50s

20s

40s

401(k) Plan Assets

Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project.Note: Components do not add to 100 percent because of rounding.

30s

0–2 Years

>2–5 Years

>5–10 Years

>10–20 Years

>20–30 Years

>30 Years

Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project.Note: The tenure variable is generally years working at current employer, and thus may overstate years of participation in the 401(k) plan.

20%

19%

22%

9%

5%

24%

Figure 6401(k) Participants Represent a Range of Job Tenures

Percentage of active 401(k) plan participants, by years of tenure, 2015

Median Tenure: 8 Years

ebri.org Issue Brief • August 3, 2017 • No. 436 12

ebri.org Issue Brief • August 3, 2017 • No. 436 13

The change in any individual participant’s account balance in the database is influenced by the magnitude of these

three factors relative to the starting account balance.20 For example, a contribution of a given dollar amount produces a

larger growth rate when added to a smaller account. On the other hand, investment returns of a given percentage

produce larger dollar increases (or decreases) when compounded on a larger asset base.

Asset allocation also influences investment returns and changes in assets. For example, stocks (as measured by the

S&P 500 total return index) increased 1.4 percent during 2015, while bonds (as measured by the Barclays Capital U.S.

Aggregate Bond Index) increased 0.5 percent (Figures 7 and 8).

Definition of 401(k) Plan Account Balance

As a cross section, or snapshot, of the entire population of 401(k) plan participants, the database includes 401(k)

participants who are young and those who are new to their jobs, as well as older participants and those who have been

with their current employers for many years. These annual updates of the database provide snapshots of 401(k) plan

account balances, asset allocation, and loan activity across wide cross sections of participants.

However, the cross-sectional analysis is not well suited to addressing the question of the impact of participation in

401(k) plans over time. Cross sections change in composition over time because the selection of data providers and

sample of plans using a given provider vary from year to year and because 401(k) participants join or leave plans.21 In

addition, the database contains only the account balances held in the 401(k) plans at participants’ current employers.

Retirement savings held in plans at previous employers or rolled over into individual retirement accounts (IRAs) are not

included in the analysis.22 Furthermore, account balances are net of unpaid loan balances. Because of all these factors,

it is not correct to presume that the change in the average or median account balance for the database as a whole

reflects the experience of “typical” 401(k) plan participants.

Size of 401(k) Plan Account Balances

At year-end 2015, the average account balance was $73,357 and the median account balance was $16,732 (Figure 9),

but balances varied widely. For example, about three-quarters of the participants in the 2015 EBRI/ICI 401(k) database

had account balances that were lower than $73,357, the size of the average account balance. In fact, 41.3 percent of

participants had account balances of less than $10,000, while 19.3 percent of participants had account balances greater

than $100,000 (Figure 10). The variation in account balances partly reflects the effects of participant age, tenure,

salary, contribution behavior, rollovers from other plans, asset allocation, withdrawals, loan activity, and employer

contribution rates. This paper examines the relationship between account balances and participants’ age, tenure, and

salary.

Relationship of Age and Tenure to 401(k) Plan Account Balances

Age and account balance are positively correlated among participants covered by the 2015 database.23 Examination of

the age composition of account balances finds that 54 percent of participants with account balances of less than

$10,000 were in their 20s or 30s (Figure 11). Similarly, 61 percent of participants with account balances greater than

$100,000 were in their 50s or 60s. The positive correlation between age and account balance is expected because

younger workers are likely to have lower incomes and to have had less time to accumulate a balance with their current

employer. In addition, they are less likely to have rollovers from a previous employer’s plan in their current plan

accounts.

Account balance and tenure are also positively correlated among participants in the 2015 database. A participant’s

tenure with an employer serves as a proxy for the length of time a worker has participated in the 401(k) plan.24 Indeed,

66 percent of participants with account balances of less than $10,000 had five or fewer years of tenure, while

75 percent of participants with account balances greater than $100,000 had more than 10 years of tenure

(Figure 12).25

Month-end level, a December 2002 to December 2016

ebri.org Issue Brief • August 3, 2017 • No. 436 14

$37,323

$55,502

$39,885

$65,454

$45,519

$60,329 $63,929

$72,383

$76,293 $73,357

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

1996 1999 2002 2007 2008 2010 2012 2013 2014 2015

Figure 9Snapshot of Year-End 401(k) Plan Account Balances

401(k) plan participant account balances,a selected yearsb

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

1996 1999 2002 2007 2008 2010 2012 2013 2014 2015

Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project.a Account balances are participant account balances held in 401(k) plans at the participants' current employers and are net of plan loans. Retirement savings held in plans at previous employers or rolled over into IRAs are not included.b The sample of participants changes over time.

Median(mid-point)

Average

ebri.org Issue Brief • August 3, 2017 • No. 436 15

41.3%

11.9%

7.3%5.1%

3.9% 3.1% 2.5% 2.1% 1.8% 1.6%

9.1% 10.2%

Size of Account Balance

Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project.Note: At year-end 2015, the average account balance among all 26.1 million 401(k) particiants was $73,357; the median account balance was $16,732. Account balances are participant account balances held in 401(k) plans at the participants’ current employers and are net of plan loans. Retirement savings held in plans at previous employers or rolled over into IRAs are not included. Components may not add to 100 percent because of rounding.

Figure 10Distribution of 401(k) Plan Account Balances, by Size of Account Balance

Percentage of participants with account balances in specified ranges, 2015

27%

4% <0.5%

27%

26%

10%

21%

29%

29%

17%

29%

43%

8% 12%18%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Size of Account Balance

60s

50s

40s

30s

20s

Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project.Note: Account balances are participant account balances held in 401(k) plans at the participants’ current employers and are net of plan loans. Retirement savings held in plans at previous employers or rolled over into IRAs are not included. Percentages may not add to 100 percent because of rounding.

Less Than $10,000 >$40,000–$50,000 More Than $100,000

Age Group

Figure 11Age Composition of Selected 401(k) Plan Account Balance CategoriesPercentage of participants with account balances in specified ranges, 2015

ebri.org Issue Brief • August 3, 2017 • No. 436 16

ebri.org Issue Brief • August 3, 2017 • No. 436 17

Examining the interaction of both age and tenure with account balances reveals that, for a given age group, average

account balances tend to increase with tenure. For example, the average account balance of participants in their 60s

with up to two years of tenure was $37,976, compared with $280,976 for participants in their 60s with more than 30

years of tenure (Figure 13).26 Similarly, the average account balance of participants in their 40s with up to two years of

tenure was $19,088, compared with $158,182 for participants in their 40s with more than 20 years of tenure.

The distribution of account balances underscores the effects of age and tenure on account balances. In a given age

group, shorter tenure tends to mean that a higher percentage of participants will have account balances of less than

$10,000. For example, 88 percent of participants in their 20s with two or fewer years of tenure had account balances of

less than $10,000 in 2015, compared with 55 percent of participants in their 20s with between five and 10 years of

tenure (Figure 14). Older workers display a similar pattern. For example, 59 percent of participants in their 60s with

two or fewer years of tenure had account balances of less than $10,000. In contrast, less than one-sixth of those in

their 60s with more than 20 years of tenure had account balances of less than $10,000.27

In a given age group, longer tenure tends to mean that a higher percentage of participants will have account balances

greater than $100,000. For example, 20 percent of participants in their 60s with five to 10 years of tenure had account

balances in excess of $100,000 in 2015 (Figure 15). However, 46 percent of participants in their 60s with between

20 and 30 years of tenure with their current employer had account balances greater than $100,000. The percentage

increases to 57 percent for participants in their 60s with more than 30 years of tenure.

Relationship Between 401(k) Plan Account Balances and Salary

Participants’ account balances vary not only with age and tenure, but also with salary. Figure 16 reports the account

balances of longer-tenured participants at their current employers’ 401(k) plans. Retirement savings held at previous

employers or amounts rolled over to IRAs are not included in the analysis. To capture as long a savings history as

possible, only longer-tenured participants are included in this analysis. However, it is important to note that the tenure

variable indicates the time that individuals have been with their current employers and may not reflect the length of

time they have participated in a 401(k) plan. One reason that job tenure may not reflect length of participation in the

401(k) plan, particularly among older participants, is that the proposed regulations for 401(k) plans were not introduced

until 1981.28

Older, longer-tenured, and higher-income participants tend to have larger account balances, which are important for

meeting their income-replacement needs in retirement.29 For longer-tenured participants in their 20s with salaries

between $20,000 and $40,000, the median account balance was $6,764 in 2015 (Figure 16). Longer-tenured

participants in their 20s earning more than $80,000 to $100,000 had a median account balance of $50,348, while those

earning more than $100,000 had a median account balance of $40,378. Among longer-tenured participants in their 60s

with $20,000 to $40,000 in salary in 2015, the median account balance was $60,585. For longer-tenured participants in

their 60s earning more than $100,000, the median account balance was $376,091.

The ratio of participant account balance to salary tends to be positively correlated with age and tenure.30 Participants in

their 50s and 60s—having had more time to accumulate assets—tended to have higher ratios, while those in their 20s

had the lowest ratios (Figure 17). In addition, for any given age and tenure combination, the ratio of account balance

to salary varies somewhat with salary. For example, among participants in their 20s, the ratio tends to increase slightly

with salary for low-to-moderate salary groups (Figure 18). However, at high salary levels the ratio tends to decline

somewhat. A similar pattern occurs among participants in their 60s (Figure 19).31

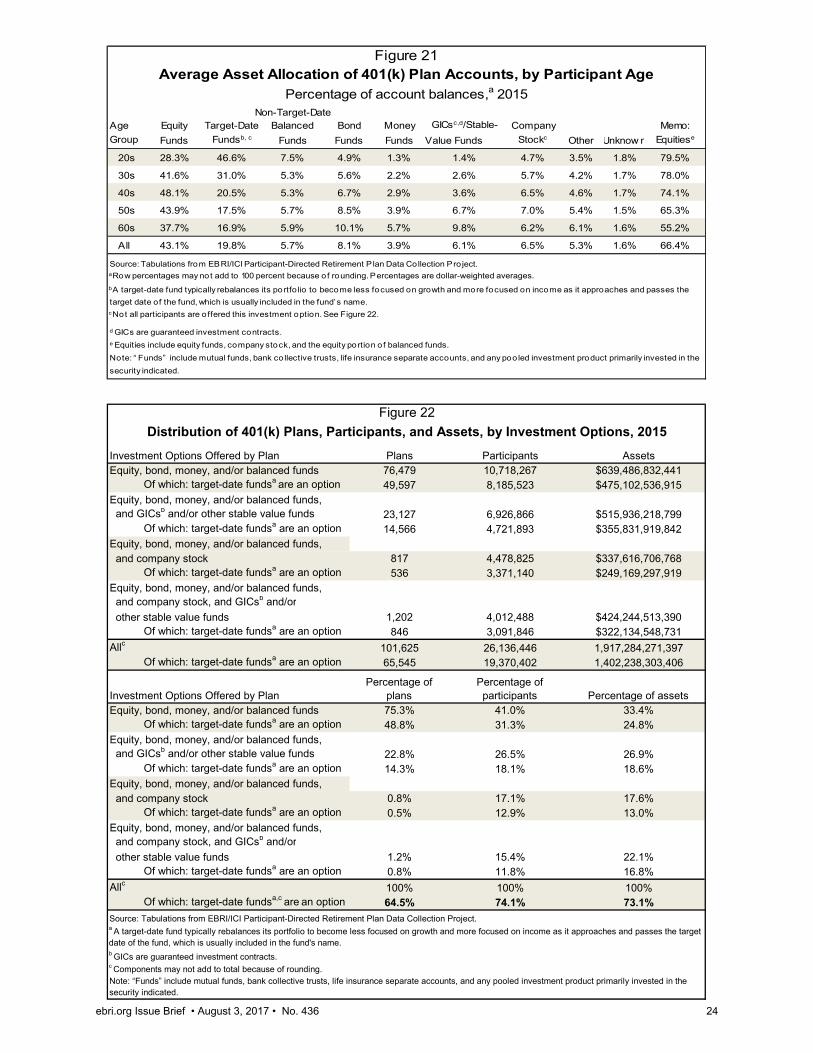

Year-End 2015 Snapshot of 401(k) Participants’ Asset Allocation

At year-end 2015, 43 percent of 401(k) plan participants’ account balances were invested in equity funds, on average,

the same as in 2014, and compared with 44 percent at year-end 2013, 37 percent at year-end 2008, and 48 percent at

year-end 2007 (Figure 20). Altogether, equity securities—equity funds, the equity portion of balanced funds,32 and

company stock—represented 66 percent of 401(k) plan participants’ assets at year-end 2015 (Figure 21).

40%

9% 3%

26%

18%6%

18%

28%

17%

12%

31%

38%

3%10%

23%

1%4%

14%

Less Than $10,000 >$40,000–$50,000 More Than $100,000

Size of Account Balance

Figure 12Tenure Composition of Selected 401(k) Plan Account Balance Categories

Percentage of participants with account balances in specified ranges, 2015

>30 Years

>20–30 Years

>10–20 Years

>5–10 Years

>2–5 Years

0–2 Years

Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project.Note: Percentages may not add to 100 percent because of rounding. Account balances are participant account balances held in 401(k) plans at the participants’ current employers and are net of plan loans. Retirement savings held in plans at previous employers or rolled over into IRAs are not included. The tenure variable is generally years working at current employer, and thus may overstate years of participation in the 401(k) plan.

Tenure

ebri.org Issue Brief • August 3, 2017 • No. 436 18

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0–2 >2–5 >5–10 >10–20 >20–30 >30

Years of Tenure

20s

30s

60s40s

50s

Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project.Note: Account balances are participant account balances held in 401(k) plans at the participants’ current employers and are net of plan loans. Retirement savings held in plans at previous employers or rolled over into IRAs are not included.The tenure variable is generally years working at current employer, and thus may overstate years of participation in the 401(k) plan.

Figure 14401(k) Plan Account Balances Less Than $10,000, by Participant Age and Tenure

Percentage of participants with account balances less than $10,000 at year-end 2015

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0–2 >2–5 >5–10 >10–20 >20–30 >30

Years of Tenure

20s

30s

40s

50s

60s

Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project.Note: Account balances are participant account balances held in 401(k) plans at the participants’ current employers and are net of plan loans. Retirement savings held in plans at previous employers or rolled over into IRAs are not included. The tenure variable is generally years working at current employer, and thus may overstate years of participation in the 401(k) plan.

Figure 15401(k) Plan Account Balances Greater Than $100,000,

by Participant Age and TenurePercentage of participants with account balances

greater than $100,000 at year-end 2015

ebri.org Issue Brief • August 3, 2017 • No. 436 19

Salary Range 20s 30s 40s 50s 60s

$20,000–$40,000 $6,764 $19,797 $52,783 $78,077 $60,585

>$40,000–$60,000 $15,225 $33,715 $74,541 $109,075 $95,357

>$60,000–$80,000 $29,126 $57,952 $119,778 $174,458 $149,997

>$80,000–$100,000 $50,348 $89,604 $179,981 $255,631 $222,328

>$100,000 $40,378 $141,511 $305,302 $420,852 $376,091Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project.

b Longer-tenured participants are used in this analysis to capture the longest possible work and savings history (see note a). The tenure variable tends to be years with the current employer rather than years of participation in the 401(k) plan. One reason that job tenure may not reflect length of participation in the 401(k) plan, particularly among older participants, is that the proposed regulations for 401(k) plans were not introduced until 1981.

Figure 16Median 401(k) Plan Account Balancea Among Longer-Tenuredb

Participants, by Age and Salary, 2015

Participant Age Group

a Account balances are participant account balances held in 401(k) plans at the participants’ current employers and are net of plan loans. Retirement savings held in plans at previous employers or rolled over into IRAs are not included.

0%

50%

100%

150%

200%

250%

300%

0–2 >2–5 >5–10 >10–20 >20–30 >30

Years of Tenure

Figure 17Ratio of 401(k) Plan Account Balance to Salary,

by Participant Age and TenurePercentage, 2015

50s

40s

60s

30s

20s

Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project.Note: Account balances are participant account balances held in 401(k) plans at the participants’ current employers and are net of plan loans. Retirement savings held in plans at previous employers or rolled over into IRAs are not included. The tenure variable is generally years working at current employer, and thus may overstate years of participation in the 401(k) plan.

ebri.org Issue Brief • August 3, 2017 • No. 436 20

ebri.org Issue Brief • August 3, 2017 • No. 436 21

Changes in Asset Allocation Between Year-End 2014 and Year-End 2015

Investment performance likely explains a good deal of the fluctuation in 401(k) participants’ asset allocations over time.

Much of the movement in the largest component, equity funds, tends to reflect overall equity market prices, which

generally rose from 2003 through 2007, dropped in 2008, rose from 2009 through 2010, moderated in 2011, rose from

2012 through 2014, and moderated in 2015 (Figures 7, 8, and 20). At year-end 2015, equity funds were 43 percent of

the assets in the EBRI/ICI 401(k) database, the same as in 2014. Balanced funds, which invest in both equities and

fixed-income securities, increased slightly in share, accounting for 26 percent of the assets in the database at year-end

2015. Despite minor shifts, most 401(k) participants appeared not to have made dramatic shifts in their asset

allocations in 2015.33

Asset Allocation and Participant Age

As in previous years, the database for year-end 2015 shows that participants’ asset allocation varied considerably with

age.34 Younger participants tended to favor equity funds and balanced funds, while older participants were more likely

to invest in fixed-income securities such as bond funds, GICs and other stable-value funds, or money funds (Figure 21).

For example, among participants in their 20s, the average allocation to equity and balanced funds was more than

80 percent of assets, compared with about 60 percent of assets among participants in their 60s.

Younger participants had consistently higher allocations to target-date funds. A target-date, or lifecycle, fund pursues a

long-term investment strategy, using a mix of asset classes that follow a predetermined reallocation, typically

rebalancing to shift its focus from growth to income as the fund approaches and passes its target date.35 At year-end

2015, 20 percent of 401(k) assets in the database were invested in target-date funds, up from 18 percent at year-end

2014.36 Among participants in their 20s, 47 percent of their 401(k) assets were invested in target-date funds at year-

end 2015; among participants in their 60s, 17 percent of their 401(k) assets were invested in target-date funds.

Asset Allocation and Investment Options

The investment options that a plan offers can significantly affect how participants allocate their 401(k) assets. Figure 22

presents the distribution of plans, participants, and assets by four combinations of investment offerings.

The first category is the base group, which consists of plans that offer neither company stock nor GICs or other stable-

value funds. Forty-one percent of participants in the 2015 EBRI/ICI 401(k) database were in these plans, which

generally offer equity funds, bond funds, money funds, and balanced funds as investment options.

Another 27 percent of participants were in plans that offer GICs and other stable-value funds as an investment option,

in addition to the base options.

Alternatively, 17 percent of participants were in plans that offer company stock but no stable-value products, while the

remaining 15 percent of participants were in plans that offered both company stock and stable-value products in

addition to the base options.

Target-date funds were available in 65 percent of the 401(k) plans in the year-end 2015 database (Figure 22).37 These

plans offered target-date funds to 74 percent of the participants in the database.38 Among participants who were

offered target-date funds, 67 percent held them at year-end 2015. Target-date fund assets represented 27 percent of

the assets of plans offering such funds in their investment lineups.

Asset Allocation by Investment Options and Age, Salary, and Plan Size

Asset allocation also varies with participant age; Figure 23 demonstrates this with an analysis of asset allocation by

investment options and also by participant age. Because asset allocation is influenced by the investment options

available to participants, Figure 24 presents asset allocation by salary range and by investment options. Salary

information is available for a subset of participants in the 2015 EBRI/ICI 401(k) database.

0%

10%

20%

30%

40%

50%

60%

70%

Salary Range

Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project.Note: Account balances are participant account balances held in 401(k) plans at the participants’ current employers and are net of plan loans. Retirement savings held in plans at previous employers or rolled over into IRAs are not included. The tenure variable is generally years working at current employer, and thus may overstate years of participation in the 401(k) plan.

0–2 Years

>2–5 Years

>5–10 Years

Figure 18Ratio of 401(k) Plan Account Balance to Salary for Participants in Their 20s, by Tenure

Percentage, 2015

0%

50%

100%

150%

200%

250%

300%

350%

400%

Salary Range

Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project.Note: Account balances are participant account balances held in 401(k) plans at the participants’ current employers and are net of plan loans. Retirement savings held in plans at previous employers or rolled over into IRAs are not included. The tenure variable is generally years working at current employer, and thus may overstate years of participation in the 401(k) plan.

0–2 Years

>2–5 Years

>5–10 Years

>10–20 Years>20 Years

Figure 19Ratio of 401(k) Plan Account Balance to Salary for Participants in Their 60s, by Tenure

Percentage, 2015

ebri.org Issue Brief • August 3, 2017 • No. 436 22

ebri.org Issue Brief • August 3, 2017 • No. 436 23

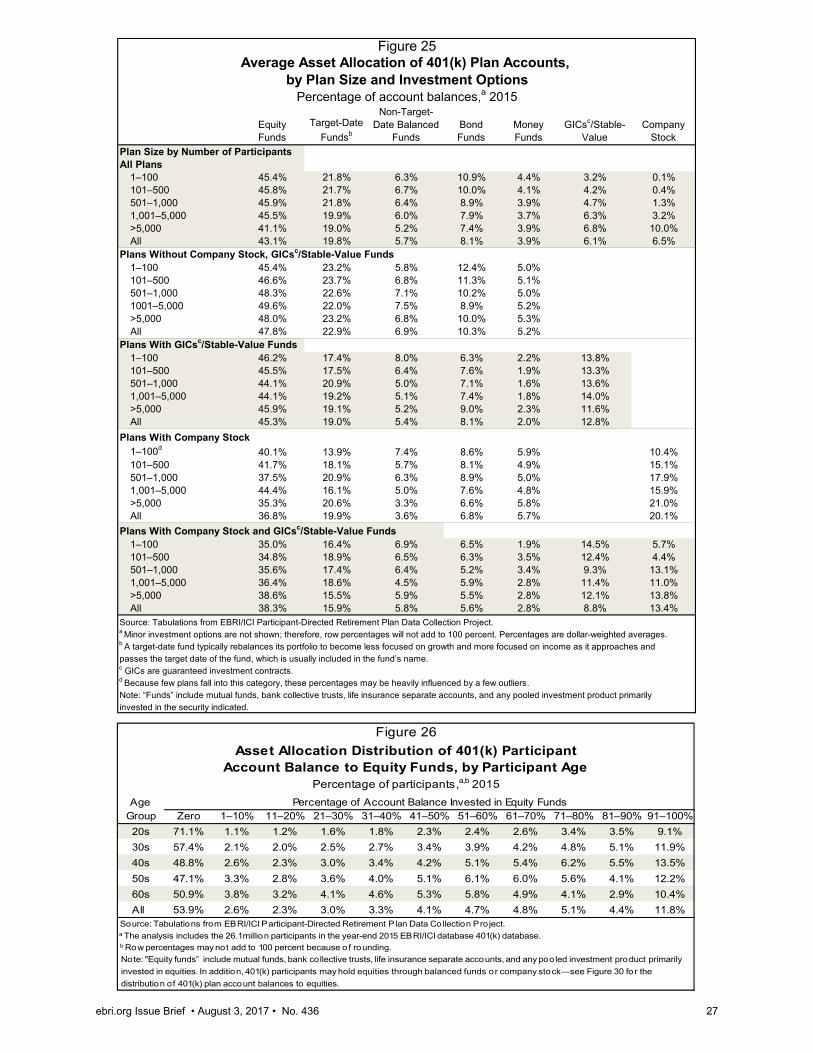

Participant asset allocation also varies with plan size (Figure 25, top panel), but much of the variation can be explained

by differences in the investment options offered by plan sponsors. For example, the percentage of plan assets invested

in company stock rises with plan size, in part, because few small plans offered company stock as an investment option.

For example, 1 percent of participants in small plans (100 participants or fewer) were offered company stock as an

investment option, while 51 percent of participants in plans with more than 5,000 participants were offered company

stock as an investment option in 2015. Thus, to analyze the potential effect of plan size, the remaining panels of Figure

25 group plans by investment options and plan size.

Distribution of Equity Fund Allocations and Participant Exposure to Equities

Participants in 401(k) plans may hold equities through a variety of options including equity funds, company stock, and

balanced funds. This section focuses first on the investing pattern of 401(k) plan participants with respect to equity

funds. The asset allocation of participants without equity funds is explored next, because 401(k) participants holding no

equity funds may hold equities in the form of company stock or through balanced funds. Finally, the overall investment

in equities across all 401(k) plan participants is presented.

Asset Allocation to Equity Funds

The year-end 2015 EBRI/ICI 401(k) database shows that, on average, 43 percent of participant account balances were

allocated to equity funds (Figure 21), which is one way to hold equities. However, individual asset allocations varied

widely across participants. For example, 54 percent of participants held no equity funds, while about 16 percent of

participants held more than 80 percent of their balances in equity funds (Figures 26 and 27).

Furthermore, the percentage of participants holding no equity funds varied with age, with 71 percent of participants in

their 20s, 49 percent of participants in their 40s, and 51 percent of participants in their 60s holding no equity funds.

The percentage of 401(k) participants holding no equity funds also varied with tenure—participants with five or fewer

years of tenure were more likely not to be invested in equity funds (Figure 27). The percentage of participants holding

no equity funds tends to fall as salary increases.

Investment Options Offered by Plan Plans Participants AssetsEquity, bond, money, and/or balanced funds 76,479 10,718,267 $639,486,832,441

Of which: target-date fundsa are an option 49,597 8,185,523 $475,102,536,915Equity, bond, money, and/or balanced funds, and GICsb and/or other stable value funds 23,127 6,926,866 $515,936,218,799

Of which: target-date fundsa are an option 14,566 4,721,893 $355,831,919,842Equity, bond, money, and/or balanced funds, and company stock 817 4,478,825 $337,616,706,768

Of which: target-date fundsa are an option 536 3,371,140 $249,169,297,919Equity, bond, money, and/or balanced funds, and company stock, and GICsb and/or

other stable value funds 1,202 4,012,488 $424,244,513,390 Of which: target-date fundsa are an option 846 3,091,846 $322,134,548,731

Allc 101,625 26,136,446 1,917,284,271,397 Of which: target-date fundsa are an option 65,545 19,370,402 1,402,238,303,406

Investment Options Offered by PlanEquity, bond, money, and/or balanced funds 75.3% 41.0% 33.4%

Of which: target-date fundsa are an option 48.8% 31.3% 24.8%Equity, bond, money, and/or balanced funds, and GICsb and/or other stable value funds 22.8% 26.5% 26.9%

Of which: target-date fundsa are an option 14.3% 18.1% 18.6%Equity, bond, money, and/or balanced funds, and company stock 0.8% 17.1% 17.6%

Of which: target-date fundsa are an option 0.5% 12.9% 13.0%Equity, bond, money, and/or balanced funds, and company stock, and GICsb and/or

other stable value funds 1.2% 15.4% 22.1% Of which: target-date fundsa are an option 0.8% 11.8% 16.8%

Allc 100% 100% 100% Of which: target-date fundsa,c are an option 64.5% 74.1% 73.1%

Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project.

b GICs are guaranteed investment contracts.c Components may not add to total because of rounding.Note: “Funds” include mutual funds, bank collective trusts, life insurance separate accounts, and any pooled investment product primarily invested in the security indicated.

Figure 22

Distribution of 401(k) Plans, Participants, and Assets, by Investment Options, 2015

Percentage of plans

Percentage of participants Percentage of assets

a A target-date fund typically rebalances its portfolio to become less focused on growth and more focused on income as it approaches and passes the target date of the fund, which is usually included in the fund's name.

Non-Target-DateAge Equity Target-Date Balanced Bond M oney GICsc,d/Stable- Com pany Memo:

Group Funds Fundsb, c Funds Funds Funds Value Funds Stockc Other Unknow n Equitiese

20s 28.3% 46.6% 7.5% 4.9% 1.3% 1.4% 4.7% 3.5% 1.8% 79.5%

30s 41.6% 31.0% 5.3% 5.6% 2.2% 2.6% 5.7% 4.2% 1.7% 78.0%

40s 48.1% 20.5% 5.3% 6.7% 2.9% 3.6% 6.5% 4.6% 1.7% 74.1%

50s 43.9% 17.5% 5.7% 8.5% 3.9% 6.7% 7.0% 5.4% 1.5% 65.3%

60s 37.7% 16.9% 5.9% 10.1% 5.7% 9.8% 6.2% 6.1% 1.6% 55.2%

All 43.1% 19.8% 5.7% 8.1% 3.9% 6.1% 6.5% 5.3% 1.6% 66.4%

Figure 21Average Asset Allocation of 401(k) Plan Accounts, by Participant Age

Percentage of account balances,a 2015

Source: Tabulations from EBRI/ICI Participant-Directed Retirement P lan Data Collection Pro ject.a Row percentages may not add to 1 00 percent because o f rounding. Percentages are dollar-weighted averages.

b A target-date fund typically rebalances its portfo lio to become less focused on growth and more focused on income as it approaches and passes the

target date of the fund, which is usually included in the fund’s name. c Not all participants are o ffered this investment option. See Figure 22.

d GICs are guaranteed investment contracts. e Equities include equity funds, company stock, and the equity portion o f balanced funds.

Note: “ Funds” include mutual funds, bank co llective trusts, life insurance separate accounts, and any poo led investment product primarily invested in the

security indicated.

ebri.org Issue Brief • August 3, 2017 • No. 436 24

Equ

ityTa

rget

-Dat

eN

on-T

arge

t-Dat

eB

ond

Mon

eyG

ICsc

/Sta

ble-

Com

pany

Fund

sFu

ndsb

Bal

ance

d Fu

nds

Fund

sFu

nds

Val

ue F

unds

Sto

ckIn

vest

men

t O

pti

on

s, A

ll A

ges

Equ

ity, b

ond,

mon

ey, a

nd/o

rba

lanc

ed fu

nds

47.8

%22

.9%

6.9%

10.3

%5.

2%E

quity

, bon

d, m

oney

, and

/or

bala

nced

fund

s; a

nd G

ICsc a

nd/o

r ot

her s

tabl

e-va

lue

fund

s45

.3%

19.0

%5.

4%8.

1%2.

0%12

.8%

Equ

ity, b

ond,

mon

ey, a

nd/o

r ba

lanc

ed fu

nds;

and

com

pany

sto

ck36

.8%

19.9

%3.

6%6.

8%5.

7%20

.1%

Equ

ity, b

ond,

mon

ey, a

nd/o

rba

lanc

ed fu

nds,

com

pany

sto

ck; a

nd

GIC

sc and

/or o

ther

sta

ble-

valu

e fu

nds

38.3

%15

.9%

5.8%

5.6%

2.8%

8.8%

13.4

%P

lan

s W

ith

ou

t C

om

pan

y S

tock

, an

d G

ICs,

c an

d/o

r O

ther

Sta

ble

-Val

ue

Fu

nd

s A

ge G

roup

20s

29.0

%50

.4%

8.4%

4.9%

1.8%

30s

43.8

%34

.7%

6.6%

6.5%

2.8%

40s

52.2

%23

.4%

6.4%

8.0%

3.7%

50s

49.7

%20

.9%

6.7%

10.9

%5.

1%60

s43

.6%

19.9

%7.

3%13

.9%

7.7%

Pla

ns

Wit

h G

ICs

c an

d/o

r O

ther

Sta

ble

-Val

ue

Fu

nd

s20

s32

.6%

40.6

%9.

0%6.

2%0.

9%3.

5%30

s45

.0%

28.1

%5.

3%6.

7%1.

4%5.

8%40

s51

.0%

19.4

%4.

9%7.

4%1.

9%7.

9%50

s46

.3%

17.4

%5.

3%8.

4%2.

1%13

.3%

60s

38.1

%16

.5%

5.9%

9.2%

2.5%

20.2

%P

lan

s W

ith

Co

mp

any

Sto

ck20

s21

.4%

48.4

%5.

0%4.

5%1.

4%16

.2%

30s

35.4

%31

.4%

3.1%

4.4%

2.9%

18.3

%40

s41

.3%

20.3

%3.

1%5.

7%4.

1%20

.0%

50s

37.2

%17

.2%

3.9%

7.5%

5.9%

20.6

%60

s32

.1%

16.7

%3.

8%8.

7%9.

2%20

.4%

Pla

ns

Wit

h C

om

pan

y S

tock

an

d G

ICs,

c an

d/o

r O

ther

Sta

ble

-Val

ue

Fu

nd

s20

s27

.9%

46.3

%6.

1%3.

3%0.

8%2.

7%8.

7%30

s39

.3%

28.2

%5.

4%4.

0%1.

6%5.

1%11

.2%

40s

44.1

%17

.5%

5.9%

4.8%

2.1%

7.2%

12.9

%50

s38

.4%

13.3

%5.

9%6.

1%2.

8%13

.1%

13.9

%60

s31

.8%

12.9

%5.

4%6.

4%4.

3%18

.6%

13.8

%S

ourc

e: T

abul

atio

ns fr

om E

BR

I/IC

I Par

ticip

ant-D

irect

ed R

etire

men

t Pla

n D

ata

Col

lect

ion

Pro

ject

.a M

inor

inve

stm

ent o

ptio

ns a

re n

ot s

how

n; th

eref

ore,

row

per

cent

ages

will

not

add

to 1

00 p

erce

nt. P

erce

ntag

es a

re d

olla

r-w

eigh

ted

aver

ages

.

usua

lly in

clud

ed in

the

fund

’s n

ame.

c G

ICs

are

guar

ante

ed in

vest

men

t con

tract

s.

Figu

re 2

3A

vera

ge

Ass

et A

lloca

tio

n o

f 40

1(k)

Pla

n A

cco

un

ts, b

y P

arti

cip

ant

Ag

e an

d In

vest

men

t O

pti

on

sP

erce

ntag

e of

acc

ount

bal

ance

s,a 2

015

Not

e: "F

unds

" inc

lude

mut

ual f

unds

, ban

k co

llect

ive

trust

s, li

fe in

sura

nce

sepa

rate

acc

ount

s, a

nd a

ny p

oole

d in

vest

men

t pro

duct

prim

arily

inve

sted

in th

e se

curit

y in

dica

ted.

b A

targ

et-d

ate

fund

typi

cally

reba

lanc

es it

s po

rtfol

io to

bec

ome

less

focu

sed

on g

row

th a

nd m

ore

focu

sed

on in

com

e as

it a

ppro

ache

s an

d pa

sses

the

targ

et d

ate

of th

e fu

nd, w

hich

is

ebri.org Issue Brief • August 3, 2017 • No. 436 25

Equ

ityTa

rget

-dat

eN

on-T

arge

t-dat

eB

ond

Mon

eyG

ICsd /S

tabl

e-C

ompa

nyS

alar

ybFu

nds

Fund

scB

alan

ced

Fund

sFu

nds

Fund

sV

alue

Fun

dsS

tock

Pla

ns

Wit

ho

ut

Co

mp

any

Sto

ck, G

ICs,

d o

r O

ther

Sta

ble

-Val

ue

Fu

nd

s$2

0,00

0–$4

0,00

041

.8%

30.9

%7.

2%8.

8%7.

8%>$

40,0

00–$

60,0

0040

.3%

29.9

%8.

2%9.

1%7.

5%>$

60,0

00–$

80,0

0044

.0%

26.6

%7.

8%9.

9%6.

7%>$

80,0

00–$

100,

000

47.5

%23

.0%

7.9%

10.6

%6.

1%>$

100,

000

52.4

%18

.4%

6.9%

10.6

%5.

7%A

ll47

.8%

22.9

%6.

9%10

.3%

5.2%

Pla

ns

Wit

h G

ICs

d an

d/o

r O

ther

Sta

ble

-Val

ue

Fu

nd

s$2

0,00

0–$4

0,00

035

.8%

32.7

%3.

9%7.

4%1.

4%13

.8%

>$40

,000

–$60

,000

37.2

%28

.2%

4.2%

8.5%

1.7%

13.1

%>$

60,0

00–$

80,0

0041

.7%

23.7

%4.

6%8.

9%2.

0%11

.6%

>$80

,000

–$10

0,00

043

.9%

22.6

%4.

6%9.

2%2.

0%11

.0%

>$10

0,00

049

.9%

17.6

%3.

6%8.

7%1.

9%11

.8%

All

45.3

%19

.0%

5.4%

8.1%

2.0%

12.8

%P

lan

s W

ith

Co

mp

any

Sto

ck$2

0,00

0–$4

0,00

033

.2%

14.8

%5.

0%7.

2%4.

1%30

.8%

>$40

,000

–$60

,000

30.0

%23

.9%

4.8%

7.0%

5.9%

22.1

%>$

60,0

00–$

80,0

0031

.6%

26.2

%4.

6%7.

3%5.

2%18

.2%

>$80

,000

–$10

0,00

035

.2%

23.1

%4.

4%8.

2%5.

0%16

.8%

>$10

0,00

041

.6%

17.5

%3.

4%9.

1%4.

8%14

.8%

All

36.8

%19

.9%

3.6%

6.8%

5.7%

20.1

%P

lan

s W

ith

Co

mp

any

Sto

ck a

nd

GIC

sd a

nd

/or

Oth

er S

tab

le-V

alu

e F

un

ds

$20,

000–

$40,

000

34.7

%20

.1%

3.8%

4.8%

1.8%

13.8

%13

.2%

>$40

,000

–$60

,000

35.2

%20

.8%

5.6%

5.7%

2.0%

12.8

%14

.1%

>$60

,000

–$80

,000

35.3

%20

.3%

5.8%

5.2%

2.4%

12.7

%13

.8%

>$80

,000

–$10

0,00

036

.1%

18.9

%7.

2%5.

1%2.

6%13

.1%

12.9

%>$

100,

000

39.9

%15

.8%

6.3%

5.5%

2.9%

11.4

%11

.6%

All

38.3

%15

.9%

5.8%

5.6%

2.8%

8.8%

13.4

%S

ourc

e: T

abul

atio

ns fr

om E

BR

I/IC

I Par

ticip

ant-D

irect

ed R

etire

men

t Pla

n D

ata

Col

lect

ion

Pro

ject

.a M

inor

inve

stm

ent o

ptio

ns a

re n

ot s

how

n; th

eref

ore,

row

per

cent

ages

will

not

add

to 1

00 p

erce

nt. P

erce

ntag

es a

re d

olla

r-w

eigh

ed a

vera

ges.

b Sal

ary

info

rmat

ion

is a

vaila

ble

for a

sub

set o

f par

ticip

ants

in th

e E

BR

I/IC

I dat

abas

e 40

1(k)

dat

abas

e.c A

targ

et-d

ate

fund

typi

cally

reba

lanc

es it

s po

rtfol

io to

bec

ome

less

focu

sed

on g

row

th a

nd m

ore

focu

sed

on in

com

e as

it a

ppro

ache

s an

d pa

sses

the

targ

et d

ate

of th

e fu

nd, w

hich

isus

ually

incl

uded

in th

e fu

nd’s

nam

e.d G

ICs

are

guar

ante

ed in

vest

men

t con

tract

s.N

ote:

“Fun

ds” i

nclu

de m

utua

l fun

ds, b

ank

colle

ctiv

e tru

sts,

life

insu

ranc

e se

para

te a

ccou

nts,

and

any

poo

led

inve

stm

ent p

rodu

ct p

rimar

ily in

vest

ed in

the

secu

rity

indi

cate

d.

Figu

re 2

4A

vera

ge

Ass

et A

lloca

tio

n o

f 40

1(k)

Pla

n A

cco

un

ts, b

y P

arti

cip

ant

Sal

ary

and

Inve

stm

ent

Op

tio

ns

Per

cent

age

of a

ccou

nt b

alan

ces,

a 201

5

ebri.org Issue Brief • August 3, 2017 • No. 436 26

Equity Funds

Target-Date

Fundsb