45th annual report 2016 - · pdf filewoolworths employees’ credit union annual report...

TRANSCRIPT

45th Annual Report2016

Membership

LoansPersonal, Car and Home

VISA Credit CardUncomplicated - low interest rate and up to 55 days interest free

Term Deposit AccountsFrom 3 months to 2 years

Easy Access to SavingsVisa Debit Card, rediCard, Cheque book, Internet Banking and ATM’s (NAB, rediATM and BOQ)

Electronic Banking

NetPlus AccountConvenient at-call access to your savings through Internet Banking and ATM’s

Payroll Deposit ServiceHave your pay, or part of your pay, deposited directly into your account to make paying bills easier throughour direct debit system

InsuranceHealth, Car, Home and Contents, Boat, Caravan, Travel, Landlords and Loan Repayment

Financial Planning

TravelLoans, Foreign Currency, VISA Credit card, VISA Debit card, Insurance, Traveller’s cheques and Access Prepaid Mastercard

SureplanPre-paid Funeral Service

Car SearchFree car buying service

List of our Products and Services

BPAY, Telephone, Internet, Bank@Post and Electronic Statements and Mobile Phone Banking (including the WECU app and Android pay)

Exclusively for employees of the Woolworths group and their families - once a member always a member

Goal account, Christmas Club account, Youth and Deeming accounts, Morgage o�set accounts,and Cash Management accounts

3 Woolworths Employees’ Credit Union Annual Report 2016

Contents

Membership

LoansPersonal, Car and Home

VISA Credit CardUncomplicated - low interest rate and up to 55 days interest free

Term Deposit AccountsFrom 3 months to 2 years

Easy Access to SavingsVisa Debit Card, rediCard, Cheque book, Internet Banking and ATM’s (NAB, rediATM and BOQ)

Electronic Banking

NetPlus AccountConvenient at-call access to your savings through Internet Banking and ATM’s

Payroll Deposit ServiceHave your pay, or part of your pay, deposited directly into your account to make paying bills easier throughour direct debit system

InsuranceHealth, Car, Home and Contents, Boat, Caravan, Travel, Landlords and Loan Repayment

Financial Planning

TravelLoans, Foreign Currency, VISA Credit card, VISA Debit card, Insurance, Traveller’s cheques and Access Prepaid Mastercard

SureplanPre-paid Funeral Service

Car SearchFree car buying service

List of our Products and Services

BPAY, Telephone, Internet, Bank@Post and Electronic Statements and Mobile Phone Banking (including the WECU app and Android pay)

Exclusively for employees of the Woolworths group and their families - once a member always a member

Goal account, Christmas Club account, Youth and Deeming accounts, Morgage o�set accounts,and Cash Management accounts

4 ....................................... Notice of ANNuAl GeNerAl MeetiNG

5 ...................................................................... corporAte Directory

6 ........................................................................... cHAirMAN’s report

7 ...............................................................................Director’s report

10 ...............................................................Directors’ DeclArAtioN

11 ................................. AuDitor’s iNDepeNDeNce DeclArAtioN

12 .................................................iNDepeNDeNt AuDitor’s report

14 ................................coMplete set of fiNANciAl stAteMeNts

16 ......................................Notes to tHe fiNANciAl stAteMeNts

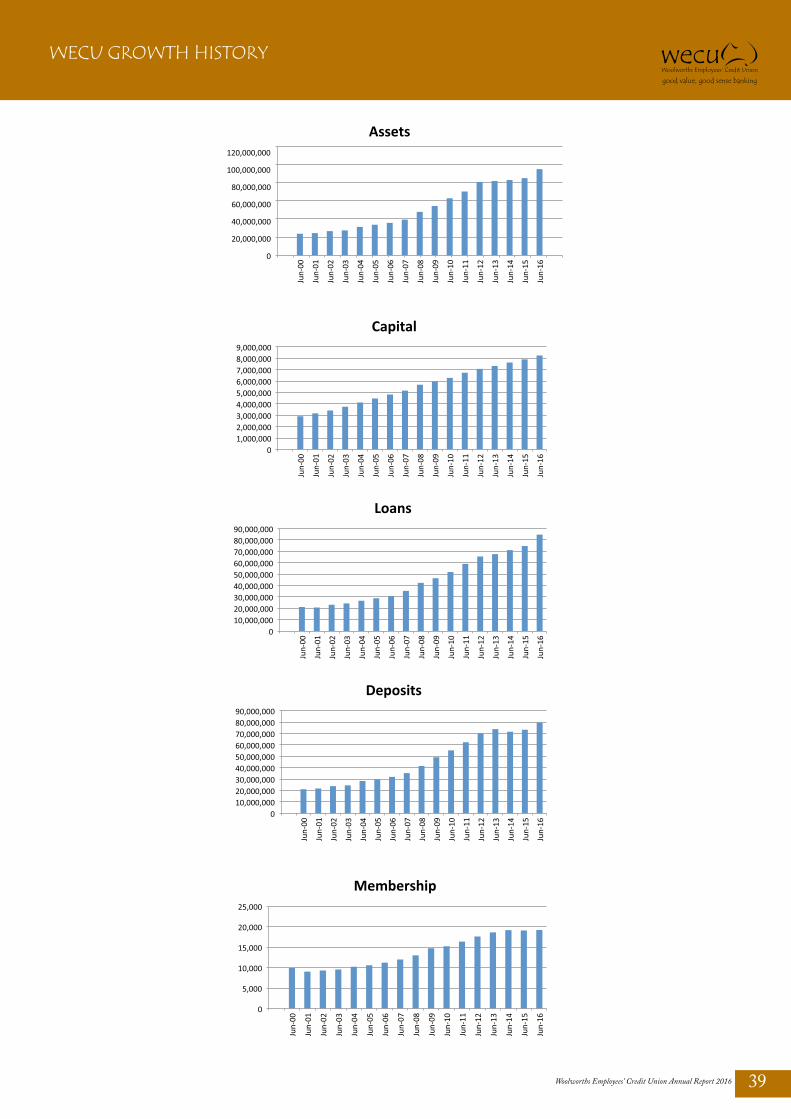

39 ................................................................. Wecu GroWtH History

4 Woolworths Employees’ Credit Union Annual Report 2015

CORPORATE DIRECTORY

Notice is hereby given that the 45th Annual General Meeting of Woolworths Employees’ Credit Union Limited (ABN : 67 087 651 803, AFSL & Australian Credit Licence No.240720 ) will be held at 5.00 pm on Wednesday 2 November 2016 in the Woolworths State Office, 522-550 Wellington Road, Mulgrave, Victoria with links to Norwest NSW and Gepps Cross SA.

AGENDA

1. Welcome and opening by the Chair of the Board. 2. Apologies. 3. Table the Minutes of the 44th Annual General Meeting held on 18 November 2015. 4. Receive the Credit Union’s Annual Report containing the Chairman’s Report, Directors’ Report, Directors’

Declaration, Auditor’s Independence Declaration, Independent Auditor’s Report and Financial Statements for the financial year ended 30 June 2016.

5. Appointment of Directors. 6. To consider other business items.

By order of the Board

Steve Sampson Company Secretary 28th September 2016

4 Woolworths Employees’ Credit Union Annual Report 2016

Notice of ANNuAl GeNerAl MeetiNG

5 Woolworths Employees’ Credit Union Annual Report 2015

CORPORATE DIRECTORY

Woolworths Employees’ Credit Union

Chairman A.E. Parle Deputy Chairman C.J. Milburn Directors W.J. Dumont, C.M.Elliott, K.F. Figueiredo, C. Katsikogianis,

R.A. Perry, P.D. Ryan, A.M. Wilson

Management and Administration

Steve Sampson General Manager Bill McLardie Deputy General Manager Sanjay Unadkat Finance Manager Josephine McCabe Administration Manager Stephen Cook Business Development Manager Klaus Dithmer Compliance Officer and Chief Risk Officer

Branch Staff

VICTORIA Bruce Bello, Tracey Cherubin, David Coutts, Geoff Duncan, Lynette Emerson, Lyndall Heap, Wendy Huang, Mary-Jaine Saylon, Karen Healy,

Pam Sleeman, Vicki Tellatin, Eva Schelling, Amy Simcox,

NEW SOUTH WALES Rosalind Carr, Brendan Flynn, Allison Micallef, Diane Micallef, Donna Myers QUEENSLAND Sue McIntyre

Auditors Grant Thornton Audit Pty Ltd (External) Aspire Accounting Holdings Pty Ltd (Internal)

Solicitors Daniels Bengtsson Pty Ltd Banker CUSCAL

National Australia Bank Affiliation CUSCAL Registered Office 522-550 Wellington Road, Mulgrave, Victoria 3170 Postal Address Private Bag 10, Mulgrave North, Victoria 3170 Office Hours Monday to Friday 8.30 am - 4.30 pm Member Insurance QBE Bond & Package Insurance

QBE Insurance (Australia) Limited QBE Travel Insurance (Australia) Limited Australian Unity Health Limited QBE Mortgage Guarantee Insurance

Financial Planning Bridges Financial Services Pty Ltd

5 Woolworths Employees’ Credit Union Annual Report 2016

corporAte Directory

Hello MeMbers,

2016 was a another significant year in the history of the Woolworths Employees’

Credit Union – established in 1971. WECU celebrated it’s 45th year of operation

on the 20th April. The Credit union initially started as the Safeway Employees’

Credit Union, operating from the Mulgrave Office in Victoria, offering a suite of

basic financial service products to a group of enthusiastic and supportive Safeway

employees and their families.

During this, our 45th year, we have achieved a major milestone in reaching just over

$100 Million in Total Assets; an excellent result, only made possible through the

ongoing support and commitment from our loyal Members.

Thank you to our 19,000 Members.

I am pleased to report on the Credit Union’s activities and performance for the year

ended 30 June 2016:-

• The Board can report on a year of strong growth with a Net Profit increase of 23% over

the prior period and growth in Total Assets of almost 12%. These improved profit results will assist

your Credit Union in developing a greater range of products and benefits for the Membership.

• We created a BPAY Biller facility, for paying and depositing funds on our Visa Credit Card.

• Our Social Media and Google+ communication channels are also becoming increasingly important tools in

promoting the Credit Union to current Members and potential new Members.

• We have extended our Data Mining Analysis through the relationship with our new Business partner,

“Unpuzzle”, and have enhanced our website capability with the help and innovative support of “Epictenet”.

• We created a Member Special Deposit Deeming account and recently launched the Samsung Android Mobile

Phone Banking APP.

During the year Warren Dumont, Chris Milburn and Paul Ryan all celebrated 15 years on the Board as Directors and

we recently welcomed Caryn Katsikogianis and Carmen Elliott to the Board of Directors. Both staff members Sue

McIntyre and Lynette Emerson celebrate 5 years with WECU and Ros Carr was acknowledged for her 15 years of

WECU Service.

I would like to recognise our retiring Directors Phillip Mercieca, Karen Ware and Peter King, and Associate

Directors Sandra Evans and Ryan Liddle, and thank them for their contribution to the Credit Union during their time

on the Board.

Additionally, I would like to thank the Host organisation, Woolworths, for its continued support, my fellow Directors

for giving up their time and expertise in providing direction to the Credit Union and to Steve Sampson and his team

for being professional and passionate in responding to our Members’ needs.

Finally and most importantly l would like to thank our Members for their continued support and loyalty. The WECU

Board and Management look forward to another focused year in 2017 by providing solid and competitive priced

financial benefits to our Membership.

Sincere regards,

Tony Parle

6 Woolworths Employees’ Credit Union Annual Report 2016

cHAirMAN’s report

7 Woolworths Employees’ Credit Union Annual Report 2015

DIRECTORS’ REPORT

Your Directors present their report on the Credit Union for the financial year ended 30 June 2016. The Credit Union is a company registered under the Corporations Act 2001.

DIRECTORS The Directors of the Credit Union at any time during or since the end of the financial year are: NAMES, QUALIFICATIONS, EXPERIENCES AND SPECIAL RESPONSIBILITIES

The Directors retire by rotation and/or as per the Constitution’s Terms of Office provisions.

* MAMI – MEMBER OF AUSTRALASIAN MUTUALS INSTITUTE LTD. * GAICD – GRADUATE OF THE AUSTRALIAN INSTITUTE OF COMPANY DIRECTORS * FCPA – FELLOW OF CERTIFIED PRACTICING ACCOUNTANTS AUSTRALIA * FCA – FELLOW OF THE INSTITUTE OF CHARTERED ACCOUNTANTS AUSTRALIA Directors were in office from the beginning of the financial year until the date of this report, unless otherwise stated. The Company Secretary in office at the end of the year:- S. W. Sampson Diploma in Financial Services FAMI, FFIN, FAIM, JP General Manager since 2009 Company Secretary since 2011

A.E. Parle (Chair) MAMI, FCPA, GAICD Bachelor of Business (Accounting) Director since 1994 Audit Committee Governance & Remuneration Committee Risk Committee

W.J. Dumont MAMI Bachelor of Business (Accounting) Director since 2001 Audit Committee (Chair) Risk Committee (Acting Chair since April 2016)

C. Elliott Bachelor of Commerce Post Graduate Diploma (Managment) Director since September 2016

S.M. Evans MAMI Associate Director 2011 – November 2015

K.F. Figueiredo MAMI Bachelors of Arts in Chemistry Master of Science in Safety Non- executive Director Australia Network on Disability Member of the American Society of Safety Engineers ASSE Director since 2012 Governance & Remuneration Committee Marketing & Development Committee

C. Katsikogiannis Bachelor of Commerce Post Graduate Certificate (Management) Director since August 2016

P.A. Mercieca MAMI Master of Business Administration Director 2010 – November 2015

C.J. Milburn (Deputy Chair) MAMI Director since 2001 Audit Committee Risk Committee

R.D. Liddle MAMI Six Sigma Black Belt Associate Director 2012 – November 2015

R.A. Perry MAMI Six Sigma Black Belt Accenture Industrial Engineering Associate Director November 2014 – November 2015 Director since December 2015 Marketing & Development Committee

P.D. Ryan MAMI Post Graduate Certificate (Management) Director since 2001 Marketing & Development Committee (Chair)

P.J. King MAMI FCA Director 2013 – March 2016

K.L. Ware MAMI Post Graduate Certificate (Management) Diploma in Management Director 2010 – July 2015

A.M. Wilson MAMI GAICD Master of Management Masters in Risk Management Director since 2013 Governance & Remuneration Committee (Chair since December 2015)

7 Woolworths Employees’ Credit Union Annual Report 2016

Director’s report

8 Woolworths Employees’ Credit Union Annual Report 2015

DIRECTORS’ REPORT

DIRECTORS’ BENEFITS

No Director has received or become entitled to receive during, or since the financial year, a benefit because of a contract

made by the Credit Union, controlled Credit Union, or a related body corporate with a Director, a firm of which a Director is

a member or a Credit Union in which a Director has a substantial financial interest, other than that disclosed in note 21 of the

financial report.

REVIEW AND RESULTS OF OPERATIONS

The Credit Union experienced a decrease of 2.94% in operating income during the year and a decrease in

non-interest expenses of 5.69%, resulting in an operating profit (after income tax) of $340,186, presenting a return on assets

of 0.36%. Members’ funds grew by 4.30%. Reserves now stand at $8.25 million, which equates to a capital adequacy level

of 16.75% against the industry minimum requirement of 8%. In the opinion of the Directors, the results for the year were

satisfactory. No dividend has been declared by the Directors.

PRINCIPAL ACTIVITIES

The principal activities of the Credit Union during the year were the provision of retail financial services to members in the

form of taking deposits and giving financial accommodation as prescribed by the Constitution. No significant changes in the

nature of these activities occurred during the year.

SIGNIFICANT CHANGES IN THE STATE OF AFFAIRS

There were no significant changes in the state of affairs of the Credit Union during the financial year.

SIGNIFICANT EVENTS AFTER THE BALANCE DATE

No matters or circumstances have arisen since the end of the year, which significantly affected or may significantly affect the

operations of the Credit Union, the results of those operations, or the state of the affairs of the Credit Union for the financial

year ended 30 June 2016.

LIKELY DEVELOPMENTS AND EXPECTED RESULTS

No other matter, circumstance or likely development in the operations has arisen since the end of the financial year that has

significantly affected or may affect:-

• The operations of the Credit Union;

• The results of those operations; or

• The state of affairs of the Credit Union

in the financial years subsequent to this financial year.

AUDITOR’S INDEPENDENCE

The auditors have provided the declaration of independence to the board as prescribed by the Corporations Act 2001

as set out on page 11.

ROUNDING OF AMOUNTS

The Credit Union is a type of Company referred to in ASIC Corporations (Rounding in Financial/ Directors’ Report)

Instrument 2016/191 and therefore the amounts contained in this report and in the financial report have been rounded to the

nearest dollar, or in certain cases, to the nearest thousand.

8 Woolworths Employees’ Credit Union Annual Report 2016

Director’s report ... coNtiNueD

9 Woolworths Employees’ Credit Union Annual Report 2015

DIRECTORS’ REPORT...CONTINUED

DIRECTOR

ELIGIBLE

ELIGIBLE

ELIGIBLE

ATTENDED

ATTENDED

ELIGIBLE

ELIGIBLE

ATTENDED

A. E. Parle 12 10 4 3 5 3 3 3 24 19 W. J. Dumont 12 8 4 4 5 5 21 17 S. M. Evans (Associate) 6 2 1 1 7 3

K. F. Figueiredo 12 10 2 2 3 3 17 15

P. J. King 9 7 3 3 4 4 16 14 R. D. Liddle (Associate) 6 1 1 0 7 1 P. A. Mercieca 6 3 1 1 7 4 C. J. Milburn 12 11 4 4 5 5 21 20 R. A. Perry 12 11 2 2 14 13 P. D. Ryan 12 11 3 2 15 13

A. M. Wilson 12 9 2 2 14 11

INDEMNIFICATION AND INSURANCE OF DIRECTORS AND OFFICERS

During the year, a premium was paid in respect of a contract insuring Directors and Officers of the Credit Union against liability. The Officers of the Credit Union covered by the insurance contract include the Directors, Executive Officers, Secretary and Employees. In accordance with normal commercial practice, disclosure of the total amount of premium payable under, and the nature of liabilities covered by the insurance contract is prohibited by a confidentiality clause in the contract. No insurance cover has been provided for the benefit of the Auditors of the Credit Union. Signed in accordance with a resolution of the Directors.

ELIGIBLEATTENDED ATTENDEDATTENDED

f

DIRECTORS’ MEETINGS

The numbers of meetings of Directors (including meetings of committees of Directors) eligible to attend during the year and the number of meetings attended by each Director were as follows:

A. E. ParleDirector28 September 2016

C. J. MilburnDirector28 September 2016

MARKETING AND GOVERNANCE ANDBOARD MEETING AUDIT COMMITTEE RISK COMMITTEE DEVELOPMENT REMUNERATION COMMITTEE COMMITTEE TOTAL

9 Woolworths Employees’ Credit Union Annual Report 2016

Director’s report ... coNtiNueD

10 Woolworths Employees’ Credit Union Annual Report 2015

DECLARATION OF FINANCIAL STATEMENTS BY DIRECTORS

THE DIRECTORS OF THE COMPANY DECLARE THAT: 1. The financial statements, comprising the statement of profit or loss and other comprehensive income, statement of

financial position, statement of cash flows, statement of changes in equity, and accompanying notes, are in accordance with the Corporations Act 2001 and: (a) comply with Accounting Standards and the Corporations Regulations 2001; and (b) give a true and fair view of the company’s financial position as at 30 June 2016 and of its performance for the year ended on that date.

2. The company has included in the notes to the financial statements an explicit and unreserved statement of compliance with International Financial Reporting Standards.

3. In the Directors’ opinion, there are reasonable grounds to believe that the company will be able to pay its debts as and when they become due and payable.

This declaration is made in accordance with a resolution of the Board of Directors and is signed for and on behalf of the Directors by:

On behalf of the Board

A. E. Parle Director28 September 2016

10 Woolworths Employees’ Credit Union Annual Report 2016

Directors’ DeclArAtioN

Auditor’s independence declArAtionto tHe directors of WoolWortHs eMployees’ credit union liMited

In accordance with the requirements of section 307C of the Corporations Act 2001, as lead auditor for the audit of

Woolworths Employees’ Credit Union Limited for the year ended 30 June 2016, I declare that, to the best of my

knowledge and belief, there have been:

A no contraventions of the auditor independence requirements of the Corporations Act 2001 in relation to the

audit; and

b no contraventions of any applicable code of professional conduct in relation to the audit.

GRANT THORNTON AUDIT PTY LTD

Chartered Accountants

Madeleine Mattera

Partner - Audit & Assurance

Sydney, 28 September 2016

Grant Thornton Audit Pty Ltd ACN 130 913 594a subsidiary or related entity of Grant Thornton Australia Ltd ABN 41 127 556 389

‘Grant Thornton’ refers to the brand under which the Grant Thornton member firms provide assurance, tax and advisory services to their clients and/or refers to one or more member firms, as the context requires. Grant Thornton Australia Ltd is a member firm of Grant Thornton International Ltd (GTIL). GTIL and the member firms are not a worldwide partnership. GTIL and each member firm is a separate legal entity. Services are delivered by the member firms. GTIL does not provide services to clients. GTIL and its member firms are not agents of, and do not obligate one another and are not liable for one another’s acts or omissions. In the Australian context only, the use of the term ‘Grant Thornton’ may refer to Grant Thornton Australia Limited ABN 41 127 556 389 and its Australian subsidiaries and related entities. GTIL is not an Australian related entity to Grant Thornton Australia Limited.

Liability limited by a scheme approved under Professional Standards Legislation. Liability is limited in those States where a current scheme applies.

Level 17, 383 Kent StreetSydney NSW 2000

Correspondence to: Locked Bag Q800QVB Post OfficeSydney NSW 1230

T +61 2 8297 2400F +61 2 9299 4445E [email protected] www.grantthornton.com.au

11 Woolworths Employees’ Credit Union Annual Report 2016

AuDitor’s iNDepeNDeNce DeclArAtioN

Level 17, 383 Kent StreetSydney NSW 2000

Correspondence to: Locked Bag Q800QVB Post OfficeSydney NSW 1230

T +61 2 8297 2400F +61 2 9299 4445E [email protected] www.grantthornton.com.au

independent Auditor’s reportto tHe MeMbers of WoolWortHs eMployees’ credit union liMited

report on tHe finAnciAl report

We have audited the accompanying financial report of Woolworths Employees’ Credit Union Limited (the “Company”), which comprises the statement of financial position as at 30 June 2016, the statement of profit or loss and other comprehensive income, statement of changes in equity and statement of cash flows for the year then ended, notes comprising a summary of significant accounting policies and other explanatory information and the directors’ declaration of the company.

directors’ responsibility for tHe finAnciAl report

The Directors of the Company are responsible for the preparation of the financial report that gives a true and fair view in accordance with Australian Accounting Standards and the Corporations Act 2001. The Director’ responsibility also includes such internal control as the Directors determine is necessary to enable the preparation of the financial report that gives a true and fair view and is free from material misstatement, whether due to fraud or error. The Directors also state, in the notes to the financial report, in accordance with Accounting Standard AASB 101 Presentation of Financial Statements, the financial statements comply with International Financial Reporting Standards.

Auditor’s responsibility

Our responsibility is to express an opinion on the financial report based on our audit. We conducted our audit in accordance with Australian Auditing Standards. Those standards require us to comply with relevant ethical requirements relating to audit engagements and plan and perform the audit to obtain reasonable assurance whether the financial report is free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial report. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of material misstatement of the financial report, whether due to fraud or error.

In making those risk assessments, the auditor considers internal control relevant to the Company’s preparation of the financial report that gives a true and fair view in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by the Directors, as well as evaluating the overall presentation of the financial report.

12 Woolworths Employees’ Credit Union Annual Report 2016

iNDepeNDeNt AuDitor’s report

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

independence

In conducting our audit, we have complied with the independence requirements of the Corporations Act 2001.

Auditor’s opinion

In our opinion:

A the financial report of Woolworths Employees’ Credit Union Limited is in accordance with the Corporations Act 2001, including:

i giving a true and fair view of the Company’s financial position as at 30 June 2016 and of their performance for the year ended on that date; and

ii complying with Australian Accounting Standards and the Corporations Regulations 2001; and

b the financial report also complies with International Financial Reporting Standards as disclosed in the notes to the financial statements.

GRANT THORNTON AUDIT PTY LTDChartered Accountants

Madeleine Mattera Partner – Audit and Assurance

Sydney, 28 September 2016

Grant Thornton Audit Pty Ltd ACN 130 913 594a subsidiary or related entity of Grant Thornton Australia Ltd ABN 41 127 556 389 ‘Grant Thornton’ refers to the brand under which the Grant Thornton member firms provide assurance, tax and advisory services to their clients and/or refers to one or more member firms, as the context requires. Grant Thornton Australia Ltd is a member firm of Grant Thornton International Ltd (GTIL). GTIL and the member firms are not a worldwide partnership. GTIL and each member firm is a separate legal entity. Services are delivered by the member firms. GTIL does not provide services to clients. GTIL and its member firms are not agents of, and do not obligate one another and are not liable for one another’s acts or omissions. In the Australian context only, the use of the term ‘Grant Thornton’ may refer to Grant Thornton Australia Limited ABN 41 127 556 389 and its Australian subsidiaries and related entities. GTIL is not an Australian related entity to Grant Thornton Australia Limited.

Liability limited by a scheme approved under Professional Standards Legislation. Liability is limited in those States where a current scheme applies.

13 Woolworths Employees’ Credit Union Annual Report 2016

iNDepeNDeNt AuDitor’s report

COMPLETE SET OF FINANCIAL STATEMENTS

13 Woolworths Employees’ Credit Union Annual Report 2015

NOTE 2016 - $ 2015 - $

STATEMENT OF PROFIT OR LOSS & OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 30 JUNE 2016$$

Interest revenue 2 4,577,382 4,843,098 Interest expense 2 (1,585,879) (1,715,366)

Net interest income 2 2,991,503 3,127,732 Fees, commission and other income 2 1,010,192 995,158 TOTAL OPERATING INCOME 4,001,695 4,122,890 Bad and doubtful debts 2 29,768 38,318 Other expenses 2

2 3,489,585 3,693,221

TOTAL EXPENSES 2 3,519,353 3,731,539 Profit before income tax 482,342 391,351 Income tax expense 3 (142,156) (115,682) PROFIT AFTER INCOME TAX

Other comprehensive income 340,186

- 275,669

-

TOTAL COMPREHENSIVE INCOME 340,186 275,669

STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE 2016

ASSETS

Cash 4 5,853,202 3,991,667 Investments at amortised cost 5 7,975,188 9,983,513 Receivables 6 941,201 404,113 Loans and advances 7 84,769,331 74,696,750 Available for sale investments 8 117,697 117,697 Property, plant and equipment 9 233,702 221,329 Intangible assets 10 212,448 243,013 Deferred tax assets 11 - 13,389 Other assets 12 114,952 104,168 TOTAL ASSETS 100,217,721 89,775,639

LIABILITIES

Deposits 14 79,651,416 73,344,358 Payables and other liabilities 15 1,553,955 1,505,180 Due to other financial institutions 16 10,709,999 7,004,683 Current tax liabilities

13 53,423 13,233 Deferred tax liabilities 11 557 -

TOTAL LIABILITIES 91,969,350 81,867,454 NET ASSETS 8,248,371 7,908,185

MEMBERS FUNDS

Retained earnings 7,890,384 7,577,998 General reserve for credit losses 232,107 210,387

Capital Profits Reserve 125,880 119,800 TOTAL MEMBERS FUNDS 8,248,371 7,908,185

These statements should be read in conjunction with the notes to the financial statements. This

14 Woolworths Employees’ Credit Union Annual Report 2016

coMplete set of fiNANciAl stAteMeNts

14 Woolworths Employees’ Credit Union Annual Report 2015

COMPLETE SET OF FINANCIAL STATEMENTS...CONTINUED

NOTE 2016 - $ 2015 - $

STATEMENT OF CASH FLOWS YEAR ENDED 30 JUNE 2016 CASH FLOWS FROM OPERATING ACTIVITIES Interest received 4,583,024 4,854,140 Dividend received 2 16,674 16,674 Interest paid (1,641,263) (1,761,199) Other non interest income received 971,892 926,475 Bad debts recovered 2 12,644 20,043 Payments to suppliers (3,385,322) (3,595,276) Net (increase) decrease in other receivables 6 (542,730) 72,847 Net increase (decrease) in sundry creditors and other liabilities 15 146,301 (590,960) Income tax paid (88,021) (94,139) Net (increase) decrease in investments at amortised cost 5 2,008,325 (1,882,177) Net (increase) in loans and advances 7 (10,052,920) (3,628,329) Net increase in deposits 14 6,307,058 1,790,535

NET CASH FLOWS USED IN OPERATING ACTIVITIES 17 (1,664,338) (3,871,366)

CASH FLOWS FROM INVESTING ACTIVITIES Acquisition of intangible assets 10 (75,857) (101,739) Acquisition of property, plant and equipment 9 (131,785) (60,821) Proceeds from sale of property, plant and equipment 28,199 17,291 NET CASH FLOWS USED IN INVESTING ACTIVITIES (179,443) (145,269)

CASH FLOWS FROM FINANCING ACTIVITIES Net increase in borrowings 16 3,705,316 994,747 NET CASH FLOWS FROM FINANCING ACTIVITIES 3,705,316 994,747 NET INCREASE / (DECREASE) IN CASH HELD 1,861,535 (3,021,888) Cash at beginning of year 3,991,667 7,013,555 CASH AT END OF YEAR 17 5,853,202 3,991,667

This statement should be read in conjunction with the notes to the financial statements.

statemeNt of cHaNges iN equitY for tHe Year eNded 30 JuNe 2016retaiNed earNiNgs

$

geNeral reserve for credit losses

$

capital profits reserve

$

total $

Total at 1 July 2015 7,577,998 210,387 119,800 7,908,185

Total Comprehensive Income for the year 340186 - - 340,186

Transfer to / from Retained Earnings (21,720) 21,720 - -

Transfer to / from Capital Profits Reserve (6,080) - 6,080 -

TOTAL AT 30 JUNE 2016 7,890,384 232,107 125,880 8,248,371

statemeNt of cHaNges iN equitY for tHe Year eNded 30 JuNe 2015retaiNed earNiNgs

$

geNeral reserve for credit losses

$

capital profits reserve

$

total $

Total at 1 July 2014 7,425,752 206,764 - 7,632,516

Total Comprehensive Income for the year 275,669 - - 275,669

Transfer to / from Retained Earnings (3,623) 3,623 - -

Transfer to / from Capital Profits Reserve (119,800) - 119,800 -

TOTAL AT 30 JUNE 2015 7,577,998 210,387 119,800 7,908,185

These statements should be read in conjunction with the notes to the financial statements.

15 Woolworths Employees’ Credit Union Annual Report 2016

coMplete set of fiNANciAl stAteMeNts ...coNtiNueD

1. statemeNt of accouNtiNg policiesThis complete set of financial statements is prepared for Woolworths Employees’ Credit Union for the year ended 30 June 2016. The report was authorised for issue on 28 September 2016 in accordance with a resolution of the board of directors. The Credit Union is a public company incorporated and domicile in Australia. The address of its registered office and its principal place of business is 520-550 Wellington Road, Mulgrave, Victoria 3170. The complete set of financial statements is presented in Australian dollars. The financial report is a general purpose financial report which has been prepared in accordance with the requirements of the Corporations Act 2001, Australian Accounting Standards and other authoritative pronouncements of the Australian Accounting Standards Board. Compliance with Australian Accounting. Standards ensures compliance with the International Financial Reporting Standards (IFRSs) as issued by the International Accounting Standards Board (IASB). The Credit Union is a for-profit entity for the purpose of preparing the financial statements.(a) basis of measuremeNt

The financial statements have been prepared on an accruals basis, and are based on historical costs, which do not take into account changing money values or current values of non current assets. The accounting policies adopted are consistent with those of the previous year unless otherwise stated.(b) classificatioN aNd subsequeNt measuremeNt of fiNaNcial assets

Financial assets and financial liabilities are recognised when the Credit Union becomes a party to the contractual provisions of the financial instrument, and are measured initially at fair value adjusted by transactions costs, except for those carried at fair value through profit or loss, which are measured initially at fair value. Subsequent measurement of financial assets and financial liabilities are described below.Financial assets are derecognised when the contractual rights to the cash flows from the financial asset expire, or when the financial asset and all substantial risks and rewards are transferred. A financial liability is derecognised when it is extinguished, discharged, cancelled or expires.For the purpose of subsequent measurement, financial assets other than those designated and effective as hedging instruments are classified into the following categories upon initial recognition:• loans and receivables• financial assets at fair value through profit or loss (FVTPL)• held-to-maturity (HTM) investments• available-for-sale (AFS) financial assets.The category determines subsequent measurement and whether any resulting income and expense is recognised in profit or loss or in other comprehensive income.All financial assets except for those at FVTPL are subject to review for impairment at least at each reporting date to identify whether there is any objective evidence that a financial asset or a group of financial assets is impaired. Different criteria to determine impairment are applied for each category of financial assets, which are described below.All income and expenses relating to financial assets that are recognised in profit or loss, are presented within finance costs, finance income or other financial items, except for impairment of loans and receivables which is presented within other expenses.(i) loAns And receivAbles

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. After initial recognition, these are measured at amortised cost using the effective interest method, less provision for impairment.

The Credit Union’s cash and cash equivalents, trade and most other receivables fall into this category of financial instruments.

Individually significant receivables are considered for impairment when they are past due or when other objective evidence is received that a specific counterparty will default. Receivables that are not considered to be individually impaired are reviewed for impairment, which are determined by reference to the industry and region of a counterparty and other shared credit risk characteristics. The impairment loss estimate is then based on recent historical counterparty default rates identified by the Credit Union.

(ii) finAnciAl Assets At fvtpl

Financial assets at FVTPL include financial assets that are either classified as held for trading or that meet certain conditions and are designated at FVTPL upon initial recognition. All derivative financial instruments fall into this category, except for those designated and effective as hedging instruments, for which the hedge accounting requirements apply (see below).

Assets in this category are measured at fair value with gains or losses recognised in profit or loss. The fair values of financial assets in this category are determined by reference to active market transactions or using a valuation technique where no active market exists. The Credit Union does not have any financial assets at FVTPL.

(iii) htM investMents

HTM investments are non-derivative financial assets with fixed or determinable payments and fixed maturity other than loans and receivables. Investments are classified as HTM if the Credit Union has the intention and ability to hold them until maturity. The Credit Union currently holds Term deposits, Negotiable Certificates of Deposit (NCD), Floating Rate Notes and Bonds in this category. If more than an insignificant portion of these assets are sold or redeemed early then the asset class will be reclassified as Available for Sale financial assets. HTM investments are measured subsequently at amortised cost using the effective interest method. If there is objective evidence that the investment is impaired, determined by reference to external credit ratings, the financial asset is measured at the present value of estimated future cash flows. Any changes to the carrying amount of the investment, including impairment losses, are recognised in profit or loss.

(iv) AvAilAble for sAle (Afs) finAnciAl Assets

AFS financial assets are non-derivative financial assets that are either designated to this category or do not qualify for inclusion in any of the other categories of financial assets. The Credit Union’s AFS financial assets comprises of the equity investment in Cuscal Limited.

The equity investment in Cuscal Limited is measured at cost less any impairment charges, as its fair value cannot currently be estimated reliably. Impairment charges are recognised in profit or loss.

All other AFS financial assets are measured at fair value. Gains and losses on these assets are recognised in other comprehensive income and reported within the AFS reserve within equity, except for impairment losses, which are recognised in profit or loss. When the asset is disposed of or is determined to be impaired, the cumulative gain or loss recognised in other comprehensive income is reclassified from the equity reserve to profit or loss.

Reversals of impairment losses are recognised in other comprehensive income, except for financial assets that are debt securities which are recognised in profit or loss only if the reversal can be objectively related to an event occurring after the impairment loss was recognised.

16 Woolworths Employees’ Credit Union Annual Report 2016

Notes to tHe fiNANciAl stAteMeNts tHe yeAr eNDeD 30 JuNe 2016

1. statemeNt of accouNtiNg policiesThis complete set of financial statements is prepared for Woolworths Employees’ Credit Union for the year ended 30 June 2016. The report was authorised for issue on 28 September 2016 in accordance with a resolution of the board of directors. The Credit Union is a public company incorporated and domicile in Australia. The address of its registered office and its principal place of business is 520-550 Wellington Road, Mulgrave, Victoria 3170. The complete set of financial statements is presented in Australian dollars. The financial report is a general purpose financial report which has been prepared in accordance with the requirements of the Corporations Act 2001, Australian Accounting Standards and other authoritative pronouncements of the Australian Accounting Standards Board. Compliance with Australian Accounting. Standards ensures compliance with the International Financial Reporting Standards (IFRSs) as issued by the International Accounting Standards Board (IASB). The Credit Union is a for-profit entity for the purpose of preparing the financial statements.(a) basis of measuremeNt

The financial statements have been prepared on an accruals basis, and are based on historical costs, which do not take into account changing money values or current values of non current assets. The accounting policies adopted are consistent with those of the previous year unless otherwise stated.(b) classificatioN aNd subsequeNt measuremeNt of fiNaNcial assets

Financial assets and financial liabilities are recognised when the Credit Union becomes a party to the contractual provisions of the financial instrument, and are measured initially at fair value adjusted by transactions costs, except for those carried at fair value through profit or loss, which are measured initially at fair value. Subsequent measurement of financial assets and financial liabilities are described below.Financial assets are derecognised when the contractual rights to the cash flows from the financial asset expire, or when the financial asset and all substantial risks and rewards are transferred. A financial liability is derecognised when it is extinguished, discharged, cancelled or expires.For the purpose of subsequent measurement, financial assets other than those designated and effective as hedging instruments are classified into the following categories upon initial recognition:• loans and receivables• financial assets at fair value through profit or loss (FVTPL)• held-to-maturity (HTM) investments• available-for-sale (AFS) financial assets.The category determines subsequent measurement and whether any resulting income and expense is recognised in profit or loss or in other comprehensive income.All financial assets except for those at FVTPL are subject to review for impairment at least at each reporting date to identify whether there is any objective evidence that a financial asset or a group of financial assets is impaired. Different criteria to determine impairment are applied for each category of financial assets, which are described below.All income and expenses relating to financial assets that are recognised in profit or loss, are presented within finance costs, finance income or other financial items, except for impairment of loans and receivables which is presented within other expenses.(i) loAns And receivAbles

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. After initial recognition, these are measured at amortised cost using the effective interest method, less provision for impairment.

The Credit Union’s cash and cash equivalents, trade and most other receivables fall into this category of financial instruments.

Individually significant receivables are considered for impairment when they are past due or when other objective evidence is received that a specific counterparty will default. Receivables that are not considered to be individually impaired are reviewed for impairment, which are determined by reference to the industry and region of a counterparty and other shared credit risk characteristics. The impairment loss estimate is then based on recent historical counterparty default rates identified by the Credit Union.

(ii) finAnciAl Assets At fvtpl

Financial assets at FVTPL include financial assets that are either classified as held for trading or that meet certain conditions and are designated at FVTPL upon initial recognition. All derivative financial instruments fall into this category, except for those designated and effective as hedging instruments, for which the hedge accounting requirements apply (see below).

Assets in this category are measured at fair value with gains or losses recognised in profit or loss. The fair values of financial assets in this category are determined by reference to active market transactions or using a valuation technique where no active market exists. The Credit Union does not have any financial assets at FVTPL.

(iii) htM investMents

HTM investments are non-derivative financial assets with fixed or determinable payments and fixed maturity other than loans and receivables. Investments are classified as HTM if the Credit Union has the intention and ability to hold them until maturity. The Credit Union currently holds Term deposits, Negotiable Certificates of Deposit (NCD), Floating Rate Notes and Bonds in this category. If more than an insignificant portion of these assets are sold or redeemed early then the asset class will be reclassified as Available for Sale financial assets. HTM investments are measured subsequently at amortised cost using the effective interest method. If there is objective evidence that the investment is impaired, determined by reference to external credit ratings, the financial asset is measured at the present value of estimated future cash flows. Any changes to the carrying amount of the investment, including impairment losses, are recognised in profit or loss.

(iv) AvAilAble for sAle (Afs) finAnciAl Assets

AFS financial assets are non-derivative financial assets that are either designated to this category or do not qualify for inclusion in any of the other categories of financial assets. The Credit Union’s AFS financial assets comprises of the equity investment in Cuscal Limited.

The equity investment in Cuscal Limited is measured at cost less any impairment charges, as its fair value cannot currently be estimated reliably. Impairment charges are recognised in profit or loss.

All other AFS financial assets are measured at fair value. Gains and losses on these assets are recognised in other comprehensive income and reported within the AFS reserve within equity, except for impairment losses, which are recognised in profit or loss. When the asset is disposed of or is determined to be impaired, the cumulative gain or loss recognised in other comprehensive income is reclassified from the equity reserve to profit or loss.

Reversals of impairment losses are recognised in other comprehensive income, except for financial assets that are debt securities which are recognised in profit or loss only if the reversal can be objectively related to an event occurring after the impairment loss was recognised.

(v) clAssificAtion And subsequent MeAsureMent of finAnciAl liAbilities

The Credit Union’s financial liabilities include borrowings, trade and other payables and derivative financial instruments. Financial liabilities are measured subsequently at amortised cost using the effective interest method, except for financial liabilities held for trading or designated at FVTPL, that are carried subsequently at fair value with gains or losses recognised in profit or loss.

(c) loaNs to members(i) bAsis of recognition

All loans are initially recognised at fair value, net of loan origination fees and inclusive of transaction costs incurred. Loans are subsequently measured at amortised cost. Any difference between the proceeds and the redemption amount is recognised in profit or loss over the period of the loans using the effective interest method.

Loans to members are reported at their recoverable amount representing the aggregate amount of principal and unpaid interest owing to the Credit Union at balance date, less any allowance or provision against impairment for debts considered doubtful. A loan is classified as impaired where recovery of the debt is considered unlikely as determined by the board of directors.

(ii) interest eArned

Term loans – interest is calculated on the basis of the daily balance outstanding and is charged in arrears to a members account on the last day of each month.

Overdraft – interest is calculated initially on the basis of the daily balance outstanding and is charged in arrears to a members account on the last day of each month.

Credit cards – the interest is calculated initially on the basis of the daily balance outstanding and is charged in arrears to a members account on the 26th day of each month, on cash advances and purchases in excess of the payment due date. Purchases are granted up to 55 days interest free until the due date for payment.

Non accrual loan interest – while still legally recoverable, interest is not brought to account as income where the Credit Union is informed that the member has deceased, or, where a loan is impaired.

(iii) loAn originAtion fees And discounts

Loan establishment fees and discounts are initially deferred as part of the loan balance, and are brought to account as income over the expected life of the loan as interest revenue.

(iv) trAnsAction costs

Transaction costs are expenses which are direct and incremental to the establishment of the loan. These costs are initially deferred as part of the loan balance, and are brought to account as a reduction to income over the expected life of the loan as interest revenue.

(v) fees on loAns

The fees charged on loans after origination of the loan are recognized as income when the service is provided or costs are incurred.

(vi) net gAins And losses

Net gains and losses on loans to members to the extent that they arise from the partial transfer of business or on securitisation, do not include impairment write downs or reversals of impairment write downs.

(d) loaN impairmeNt(i) specific And collective provision for iMpAirMent

A provision for losses on impaired loans is recognised when there is objective evidence that the impairment of a loan has occurred. Estimated impairment losses are calculated on either a portfolio basis for loans of similar characteristic, or on an individual basis. The amount provided is determined

by management and the board to recognise the probability of loan amounts not being collected in accordance with terms of the loan agreement. The critical assumptions used in the calculation are set out in Note 7 and Note 25 details the credit risk management approach for loans.

The APRA Prudential Standards require a minimum provision to be maintained, based on specific percentages on the loan balance which are contingent upon the length of time the repayments are in arrears. This approach is used to assess the collective provisions for impairment.

An assessment is made at each balance date to determine whether there is objective evidence that a specific financial asset or a group of financial assets is impaired. Evidence of impairment may include indications that the borrower has defaulted, is experiencing significant financial difficulty, or where the debt has been restructured to reduce the burden on the borrower.

(ii) reserve for credit losses

In addition to the above specific provision, the board has recognised the need to make an allocation from retained earnings to ensure there is an adequate protection for members against the prospect that some members will experience loan repayment difficulties in the future. The reserve is based on estimation of potential risk in the loan portfolio based upon:

• The level of security taken as collateral; and

• The concentration of loans taken by employment type.(iii) renegotiAted loAns

Loans which are subject to renegotiated loan terms which would have otherwise been impaired do not have the repayment arrears diminished and interest continues to accrue to income. Each renegotiated loan is retained at the full arrears position until the normal repayments are reinstated and brought up to date and maintained for a period of 6 months.

(e) bad debts WritteN off

(direct reductioN iN loaN balaNce)

Bad debts are written off from time to time as determined by management and the board of directors when it is reasonable to expect that the recovery of debt is unlikely. Bad debts are written off against the provisions for impairment, if a provision for impairment had previously been recognised. If no provision had been recognised, the write offs are recognised as expenses in profit and loss.

(f) casH aNd liquid assets

Cash comprises cash on hand and demand deposits. Cash equivalents are short term, highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value.

(g) deposits WitH otHer fiNaNcial iNstitutioNs

Term deposits and negotiable certificates of deposit with other financial institutions are unsecured and have a carrying amount equal to their principal amount. Interest is paid on the daily balance at maturity. Interest is recognised when earned. The accrual for interest receivable is calculated on a proportional basis of the expired period of the term of the investment. Interest receivable is included in the amount of receivables in the statement of financial position.

17 Woolworths Employees’ Credit Union Annual Report 2016

Notes to tHe fiNANciAl stAteMeNts ...coNtiNueD

(H) equitY iNVestmeNts aNd otHer securities

Investments in shares are classified as available for sale financial assets where they do not qualify for classification as loans and receivables, or investments held for trading.

Investments in shares which do not have a ready market and are not capable of being reliably valued are recorded at the lower of cost or recoverable amount.

Movements in available for sale asset balances are reflected in equity through the Available for Sale Reserve.

(i) propertY, plaNt aNd equipmeNt

Property, plant and equipment are depreciated on a straight line basis so as to write off the net cost of each asset over its expected useful life to the Credit Union. The useful lives are adjusted if appropriate at each reporting date. Estimated useful lives at reporting date are:-

Leasehold improvements:........ 7 years Plant and equipment:............... 3 to 5 years

(J) iNtaNgible assets

Items of computer software which are not integral to the computer hardware owned by the Credit Union are classified as intangible assets. Computer software is amortised over the expected useful life of the software. These lives range from 3 to 8 years.

(K) member saViNgs

(i) bAsis for MeAsureMent

Member savings and term investments are quoted at the aggregate amount payable to depositors as at the balance date.

(ii) interest pAyAble

Interest on savings is calculated on the daily balance and posted to the accounts periodically, or on maturity of the term deposit. Interest on savings is brought to account on an accrual basis in accordance with the interest rate terms and conditions of each savings and term deposit account, as varied from time to time. The amount of the accrual is shown as part of amounts payable.

(l) due to otHer fiNaNcial iNstitutioNs

Amounts due to other financial institutions are carried at the principal amount. Interest is charged as an expense as it accrues.

(m) accouNts paYable aNd otHer liabilities

Liabilities for trade creditors and accruals are carried at cost, which is the fair value of the consideration to be paid in the future for goods and services received, whether or not billed to the Credit Union.

(N) emploYee eNtitlemeNts

Employee entitlements are not provided for on the Credit Union’s statement of financial position. The credit union is charged a loading on salaries for employee entitlements by the host organisation, Woolworths Limited. Provision for employee entitlements are maintained by Woolworths Limited.

(o) iNcome tax

The income tax expense shown in profit or loss is based on the profit before income tax adjusted for any non tax deductible, or non-assessable items between accounting profit and taxable income. Deferred tax assets and liabilities are recognised using the statement of financial position liability method in respect of temporary differences arising between the tax bases of assets or liabilities and their carrying amounts in the financial statements. Current and deferred tax balances relating to amounts recognised directly in equity.

Deferred tax assets and liabilities are recognised for all temporary differences between carrying amounts of assets and liabilities for financial reporting purposes and their respective tax bases at the rate of income tax applicable to the period in which the benefit will be received or the liability will become payable. These differences are presently assessed at 30%. Deferred tax assets are only brought to account if it is probable that future taxable amounts will be available to utilise those temporary differences. The recognition of these benefits is based on the assumption that no adverse change will occur in income tax legislation; and the anticipation the Credit Union will derive sufficient future assessable income and comply with the conditions of deductibility imposed by the law to permit a income tax benefit to be obtained.

(p) goods aNd serVices tax

As a financial institution the Credit Union is input taxed on all income except for income from commissions and some fees. An input taxed supply is not subject to GST collection, and similarly the GST paid on related or apportioned purchases cannot be recovered. As some income is charged GST, the GST on purchases are generally recovered on a proportionate basis. In addition certain prescribed purchases are subject to reduced input taxed credits (RITC), of which 75% of the GST paid is recoverable.

Revenue, expenses and assets are recognised net of the amount of goods and services tax (GST). To the extent that the full amount of the GST incurred is not recoverable from the Australian Taxation Of- fice (ATO), the GST is recognised as part of the cost of acquisition of the asset or as part of an item of the expense. Receivables and payables are stated with the amount of GST included. The net amount of GST recoverable from, or payable to, the ATO is included as a current asset or current liability in the statement of financial position. Cash flows are included in the cash flow statement on a gross basis. The GST components of cash flows arising from investing and financing activities which are recoverable from, or payable to, the ATO are classified as operating cash flows.

(q) impairmeNt of assets

At t h e reporting date the Credit Union assesses whether there is any indication that individual assets are impaired. Where impairment indicators exist, recoverable amount is determined and impairment losses are recognised in the income statement where the asset’s carrying value exceeds its recoverable amount. Recoverable amount is the higher of an asset’s fair value less costs to sell and value in use. In determining recoverable amount the expected net cash flows have not been discounted to their present value using a market determined risk adjusted discount rate.

(r) rouNdiNg of amouNts

The Credit Union is a type of Company referred to in ASIC Corporations (Rounding in Financial/ Directors’ Report) Instrument 2016/191 and therefore the amounts contained in the directors’ report and financial report have been rounded to the nearest dollar, or in certain cases, to the nearest thousand.

(s) accouNtiNg estimates aNd JudgemeNts

Management have made judgements when applying the Credit Union’s accounting policies with respect to the classification of member withdrawable shares as liabilities. Management have made critical accounting estimates when applying the Credit Union’s accounting policies with respect to the impairment provisions for loans.

18 Woolworths Employees’ Credit Union Annual Report 2016

Notes to tHe fiNANciAl stAteMeNts ...coNtiNueD

(H) equitY iNVestmeNts aNd otHer securities

Investments in shares are classified as available for sale financial assets where they do not qualify for classification as loans and receivables, or investments held for trading.

Investments in shares which do not have a ready market and are not capable of being reliably valued are recorded at the lower of cost or recoverable amount.

Movements in available for sale asset balances are reflected in equity through the Available for Sale Reserve.

(i) propertY, plaNt aNd equipmeNt

Property, plant and equipment are depreciated on a straight line basis so as to write off the net cost of each asset over its expected useful life to the Credit Union. The useful lives are adjusted if appropriate at each reporting date. Estimated useful lives at reporting date are:-

Leasehold improvements:........ 7 years Plant and equipment:............... 3 to 5 years

(J) iNtaNgible assets

Items of computer software which are not integral to the computer hardware owned by the Credit Union are classified as intangible assets. Computer software is amortised over the expected useful life of the software. These lives range from 3 to 8 years.

(K) member saViNgs

(i) bAsis for MeAsureMent

Member savings and term investments are quoted at the aggregate amount payable to depositors as at the balance date.

(ii) interest pAyAble

Interest on savings is calculated on the daily balance and posted to the accounts periodically, or on maturity of the term deposit. Interest on savings is brought to account on an accrual basis in accordance with the interest rate terms and conditions of each savings and term deposit account, as varied from time to time. The amount of the accrual is shown as part of amounts payable.

(l) due to otHer fiNaNcial iNstitutioNs

Amounts due to other financial institutions are carried at the principal amount. Interest is charged as an expense as it accrues.

(m) accouNts paYable aNd otHer liabilities

Liabilities for trade creditors and accruals are carried at cost, which is the fair value of the consideration to be paid in the future for goods and services received, whether or not billed to the Credit Union.

(N) emploYee eNtitlemeNts

Employee entitlements are not provided for on the Credit Union’s statement of financial position. The credit union is charged a loading on salaries for employee entitlements by the host organisation, Woolworths Limited. Provision for employee entitlements are maintained by Woolworths Limited.

(o) iNcome tax

The income tax expense shown in profit or loss is based on the profit before income tax adjusted for any non tax deductible, or non-assessable items between accounting profit and taxable income. Deferred tax assets and liabilities are recognised using the statement of financial position liability method in respect of temporary differences arising between the tax bases of assets or liabilities and their carrying amounts in the financial statements. Current and deferred tax balances relating to amounts recognised directly in equity.

Deferred tax assets and liabilities are recognised for all temporary differences between carrying amounts of assets and liabilities for financial reporting purposes and their respective tax bases at the rate of income tax applicable to the period in which the benefit will be received or the liability will become payable. These differences are presently assessed at 30%. Deferred tax assets are only brought to account if it is probable that future taxable amounts will be available to utilise those temporary differences. The recognition of these benefits is based on the assumption that no adverse change will occur in income tax legislation; and the anticipation the Credit Union will derive sufficient future assessable income and comply with the conditions of deductibility imposed by the law to permit a income tax benefit to be obtained.

(p) goods aNd serVices tax

As a financial institution the Credit Union is input taxed on all income except for income from commissions and some fees. An input taxed supply is not subject to GST collection, and similarly the GST paid on related or apportioned purchases cannot be recovered. As some income is charged GST, the GST on purchases are generally recovered on a proportionate basis. In addition certain prescribed purchases are subject to reduced input taxed credits (RITC), of which 75% of the GST paid is recoverable.

Revenue, expenses and assets are recognised net of the amount of goods and services tax (GST). To the extent that the full amount of the GST incurred is not recoverable from the Australian Taxation Of- fice (ATO), the GST is recognised as part of the cost of acquisition of the asset or as part of an item of the expense. Receivables and payables are stated with the amount of GST included. The net amount of GST recoverable from, or payable to, the ATO is included as a current asset or current liability in the statement of financial position. Cash flows are included in the cash flow statement on a gross basis. The GST components of cash flows arising from investing and financing activities which are recoverable from, or payable to, the ATO are classified as operating cash flows.

(q) impairmeNt of assets

At t h e reporting date the Credit Union assesses whether there is any indication that individual assets are impaired. Where impairment indicators exist, recoverable amount is determined and impairment losses are recognised in the income statement where the asset’s carrying value exceeds its recoverable amount. Recoverable amount is the higher of an asset’s fair value less costs to sell and value in use. In determining recoverable amount the expected net cash flows have not been discounted to their present value using a market determined risk adjusted discount rate.

(r) rouNdiNg of amouNts

The Credit Union is a type of Company referred to in ASIC Corporations (Rounding in Financial/ Directors’ Report) Instrument 2016/191 and therefore the amounts contained in the directors’ report and financial report have been rounded to the nearest dollar, or in certain cases, to the nearest thousand.

(s) accouNtiNg estimates aNd JudgemeNts

Management have made judgements when applying the Credit Union’s accounting policies with respect to the classification of member withdrawable shares as liabilities. Management have made critical accounting estimates when applying the Credit Union’s accounting policies with respect to the impairment provisions for loans.

(t) NeW staNdards applicable for tHe curreNt Year

There were no new or revised accounting standards applicable for financial years commencing from 1 July 2015 that had any significant impact on the financial statements of the Credit Union.

(u) NeW or emergiNg staNdards Not Yet maNdatorY

Certain new accounting standards and interpretations have been published that are not mandatory for the 30th June 2016 reporting period. The Credit union’s assessment of the impact of these new standards and interpretations is set out below. Changes that are not likely to impact the financial report of the Credit Union have not been reported.

AASB Reference Nature of Change Application date Impact on Initial Application

AASB 9 Financial Instruments (December 2015)

Amends the requirements for classification and measurement of financial assets.

Recognition of credit losses are to no longer be dependent on the Credit Union first identifying a credit loss event. The Credit Union will consider a broader range of information when assessing credit risk and measuring expected credit losses including past experience of historical losses for similar financial instruments.

Periods beginning on or after 1 January 2018.

Due to the recent release of these amendments and that adoption is only mandatory for the 30 June 2019 year end, the Credit Union has not yet made a detailed assessment of the impact of these amendments. However, based upon a preliminary assessment, the Standard is not expected to have a material impact upon the transactions and balances recognised when it is first adopted.

AASB 15 Revenue from Contracts with Customers

Revenue from financial instruments is not covered by this new Standard, but AASB 15 establishes a new revenue recognition model for other types of revenue.

Periods beginning on or after 1 January 2018.

Based upon a preliminary assessment, the Standard is not expected to have a material impact upon the transactions and balances recognised when it is first adopted, as few revenue transactions of the credit union are impacted by the new standard.

19 Woolworths Employees’ Credit Union Annual Report 2016

Notes to tHe fiNANciAl stAteMeNts ...coNtiNueD

20 Woolworths Employees’ Credit Union Annual Report 2015

NOTES TO THE FINANCIAL STATEMENTS...CONTINUED

Dividends - Other corporations 16,674 16,674 Gain on sale of non-current assets 8,980 17,291 Fees and commissions - Other fee income 351,580 424,493 - Insurance commissions 311,053 317,448 - Other commissions 141,652 151,395 Bad debts recovered 12,644 20,043 Other income 167,609 47,814

FEES, COMMISSION AND OTHER INCOME 1,010,192 1,102,944

995,158 1,102,944 INTEREST EXPENSE

Bad and doubtful debts 29,768 38,318 Amortisation - Software 106,422 106,626

Depreciation - Property plant and equipment 100,194 117,988 General and administration - Personnel costs 1,727,926 1,748,729 - Other 1,555,043 1,719,878 NON INTEREST EXPENSE 3,519,353 3,731,539 PROFIT BEFORE TAX 482,342 391,351

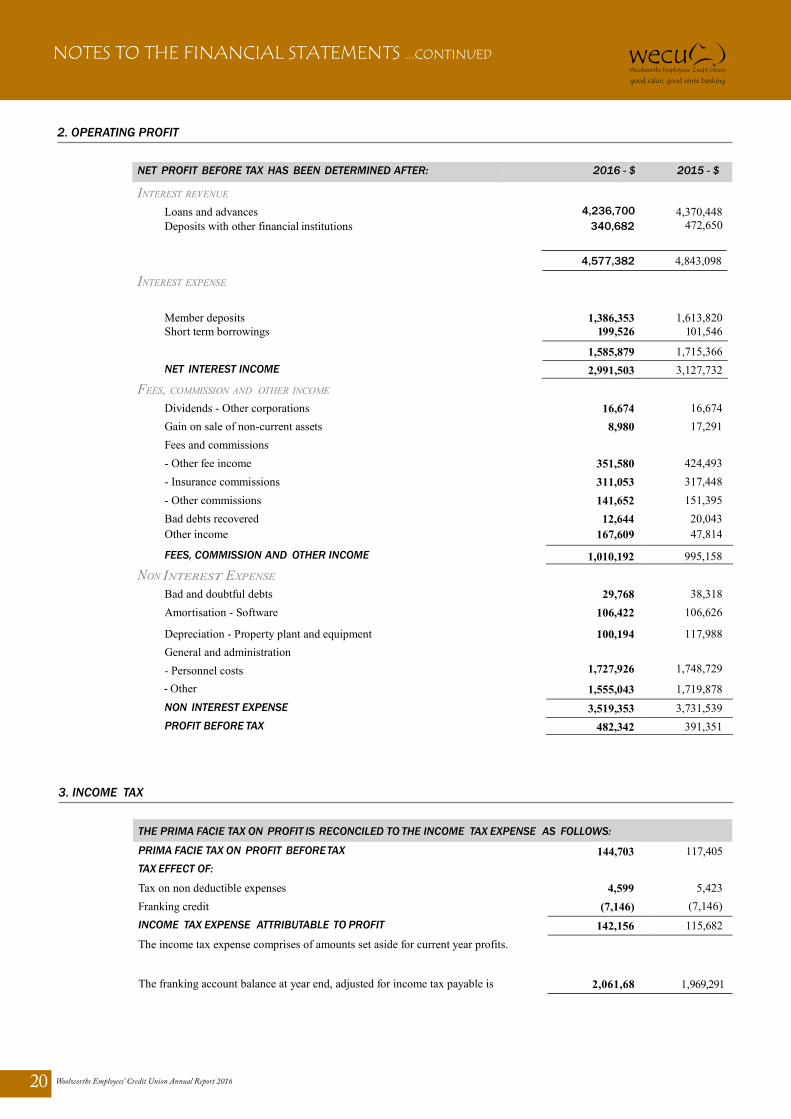

2. OPERATING PROFIT

NET PROFIT BEFORE TAX HAS BEEN DETERMINED AFTER: 2016 - $ 2015 - $

INTEREST REVENUE

Loans and advances Deposits with other financial institutions

4,236,700 340,682

4,370,448 472,650

INTEREST EXPENSE

4,577,382 4,843,098

Member deposits 1,386,353 1,613,820 Short term borrowings 199,526 101,546

1,585,879 1,715,366 NET INTEREST INCOME 2,991,503 3,127,732

FEES, COMMISSION AND OTHER INCOME

NON

3. INCOME TAX

THE PRIMA FACIE TAX ON PROFIT IS RECONCILED TO THE INCOME TAX EXPENSE AS FOLLOWS:

PRIMA FACIE TAX ON PROFIT BEFORE TAX 144,703 117,405 TAX EFFECT OF: Tax on non deductible expenses 4,599 5,423 Franking credit (7,146) (7,146) INCOME TAX EXPENSE ATTRIBUTABLE TO PROFIT 142,156 115,682 The income tax expense comprises of amounts set aside for current year profits.

The franking account balance at year end, adjusted for income tax payable is 2,061,68 1,969,291

20 Woolworths Employees’ Credit Union Annual Report 2016

Notes to tHe fiNANciAl stAteMeNts ...coNtiNueD

NOTES TO THE FINANCIAL STATEMENTS...CONTINUED

4. CASH

21 Woolworths Employees’ Credit Union Annual Report 2015

2016 - $ 2015 - $

Cash on hand 196,190 90,756 Cash at banks 5,657,012 3,900,911

5,853,202 3,991,667

5. INVESTMENTS AT AMORTISED COST

Bonds

4,001,172

5,015,108 Negotiable Certificates Of Deposit 3,974,016 4,968,405

7,975,188 9,983,513

MATURITY ANALYSIS

Not longer than 3 months

4,974,334

4,968,405 Longer than 3 and not longer than 12 months 1,001,259 2,005,422 Longer than 1 year and not longer than 5 years 1,999,595 3,009,686

7,975,188 9,983,513 6. RECEIVABLES

Interest receivable

40,115

45,757

Other receivables 901,086 358,356

941,201 404,113 All receivables are due within 12 months.

7. LOANS AND ADVANCES

Overdrafts

340,322

412,296

Credit card 819,474 779,401 Residential loans 76,684,282 65,237,039 Personal loans 6,956,525 8,318,947 Total loans and advances 84,800,603 74,747,683 Provision for impairment (31,272) (50,933) NET LOANS AND ADVANCES 84,769,331 74,696,750

A) DIRECTORS AND DIRECTOR-RELATED ENTITIES Loans to director-related entities 60,598 823,508

B) MATURITY ANALYSIS

Overdrafts 340,322 412,296 Credit Card 819,474 779,401 Not longer than 3 months 1,796 2,384 Longer than 3 months and not longer than 12 months 307,147 495,312 Longer than 1 month and not longer than 5 years 6,500,672 7,198,790 Longer than 5 years 76,831,192 65,859,500 TOTAL LOANS 84,800,603 74,747,683

21 Woolworths Employees’ Credit Union Annual Report 2016

Notes to tHe fiNANciAl stAteMeNts ...coNtiNueD

NOTES TO THE FINANCIAL STATEMENTS...CONTINUED

7. LOANS AND ADVANCES ...CONTINUED

22 Woolworths Employees’ Credit Union Annual Report 2015

GEOGRAPHICAL CONCENTRATIONS - 2016

HOUSING 2016 - $ OTHER 2016 - $

Victoria 50,142,054 4,640,316 NSW 20,906,531 2,663,449 Tasmania 818,190 133,917 Queensland 3,375,815 483,230 Western Australia 1,069,404 101,227 South Australia - 16,014 Australian Capital Territory 168,063 77,666 Northern Territory 204,225 502

76,684,282 8,116,321

HOUSING 2015 - $ OTHER 2015 - $

Victoria 46,309,479 5,337,079 NSW 14,375,820 3,220,407 Tasmania 866,568 154,638 Queensland 2,181,443 524,612 Western Australia 1,099,669 160,752 South Australia - 34,067 Australian Capital Territory 200,464 77,081 Northern Teritory 203,596 2,008

65,237,039 9,510,644 TRANSFERS OF FINANCIAL ASSETS – OFF BALANCE SHEET LOANS

It is not practicable to value all collateral as at balance date due to the variety of assets and condition. A breakdown of the quality of the residential mortgage security on a portfolio basis is as follows:-

SECURITY HELD AS MORTGAGE AGAINST REAL ESTATE IS ON THE BASIS OF:- - loan to valuation ratio of less than 80% 71,494,822 60,058,228 - loan to valuation ratio of more than 80% but mortgage insured 5,189,460 5,178,811

76,684,282 65,237,039 Where the loan value is less than 80% there is a 20% margin to cover the costs of any sale, or potential value reduction.

D) CONCENTRATION OF LOANS

Loans to members are predominantly to employees of Woolworths Ltd and their families.

GEOGRAPHICAL CONCENTRATIONS - 2015

E) SECURITISED LOANS

The Credit Union acts as an agent for a securitisation entity to arrange and fund loans made directly by the securitisation entity. These loans do not qualify for recognition and are not recognised in the books of the Credit Union at any time. The value of securitised loans under management is set out in Note 23

The Credit Union has an off balance sheet funding facility with Bendigo and Adelaide Bank. This facility replaces securitised loans facility funded through Integris. These loans do not qualify for recognition and are not recognised in the books of the Credit Union at any time. The value of off balance sheet loans under management is set out in Note 24.

C) CREDIT QUALITY - SECURITY HELD AGAINST LOANS 2016 - $ 2015 - $

Secured by mortgage over real estate 76,684,282 65,237,039 Partially secured by goods mortgage 4,292,384 5,083,182 Wholly unsecured 3,823,937 4,427,462

84,800,603 74,747,683

F) TRANSFERS OF FINANCIAL ASSETS - OFF BALANCE SHEET LOANS

22 Woolworths Employees’ Credit Union Annual Report 2016

Notes to tHe fiNANciAl stAteMeNts ...coNtiNueD

NOTES TO THE FINANCIAL STATEMENTS...CONTINUED

7. LOANS AND ADVANCES ...CONTINUED

23 Woolworths Employees’ Credit Union Annual Report 2015

IMPAIRED LOANS WRITTEN OFF:

Amounts written off against provision for impaired loans 49,645 43,508 Total bad debts 49,645 43,508

Bad debts recovered in period 12,644 20,043 Key assumptions in determining the provision for impairment:

The Credit Union has determined the likely impairment loss on loans which have not maintained the loan repayments in accordance with the loan contract, or where there is other evidence of potential impairment such as industrial restructuring, job losses or economic circumstances. In identifying the impairment, the Credit Union is required to estimate the potential impairment using the length of time the loan in arrears and the historical losses arising in past years. Given the relatively small number of impaired loans, the circumstances may vary for each loan over time resulting in higher or lower impairment losses. An estimate is based on the period of impairment. A provision is allowed for specifically identified loans. The policy covering impaired loans and advances is set out in Note 1(D).

ANALYSIS OF LOANS IMPAIRED OR POTENTIALLY IMPAIRED BY CLASS

2016 - $ VALUE OF

IMPAIRED LOANS

2016 - $ PROVISION FOR

IMPAIRMENT

Mortgage - - Personal 49,085 21,289

Credit Card and Overdrafts 69,100 9,983

118,185 31,272

2015 - $ 2015 - $ VALUE OF PROVISION FOR

ANALYSIS OF LOANS IMPAIRED OR POTENTIALLY IMPAIRED BY CLASS IMPAIRED LOANS IMPAIRMENT Mortgage 337,858 -

Personal 165,713 24,419 Credit Card and Overdrafts 108,466 25,874

612,037 50,293

(G) PROVISION FOR IMPAIRMENT 2016 - $ 2015 - $

TOTAL PROVISION COMPRISES: Individual specific provisions 31,272 50,933

31,272 50,933

MOVEMENT IN THE PROVISION FOR IMPAIRMENT: Balance at the beginning of the year 50,933 56,122 Add/(deduct): Transfers from (to) profit or loss (69,306)

(107,379)

(48,697)

(95,478) Bad debts written off provision 49,645 43,508 Balance at end of year 31,272 50,933

23 Woolworths Employees’ Credit Union Annual Report 2016

Notes to tHe fiNANciAl stAteMeNts ...coNtiNueD

NOTES TO THE FINANCIAL STATEMENTS...CONTINUED

7. ...CONTINUED

24 Woolworths Employees’ Credit Union Annual Report 2015

ANALYSIS OF LOANS THAT ARE IMPAIRED OR POTENTIALLY IMPAIRED BASED ON AGE OF REPAYMENTS OUTSTANDING

2016 - $ CARRYING VALUE

2016 - $ PROVISION

Not impaired loans and loans less than 30 days in arrears 84,682,418 -

30 to 90 days in arrears 27,741 - 90 to 180 days in arrears 3,676 3,621 180 to 270 days in arrears 2,150 2,150 270 to 365 days in arrears 15,518 15,518 Over 365 days in arrears - - Overlimit facilities over 14 days 69,100 9,983 TOTAL 84,800,603 31,272

ANALYSIS OF LOANS THAT ARE IMPAIRED OR POTENTIALLY IMPAIRED BASED ON AGE OF REPAYMENTS OUTSTANDING

CARRYING VALUE

2015 - $ PROVISION

Not impaired loans and loans less than 30 days in arrears 74,213,109 -

30 to 90 days in arrears 263,854 - 90 to 180 days in arrears 210,653 3,017 180 to 270 days in arrears 15,765 9,459 270 to 365 days in arrears 6,779 5,423 Over 365 days in arrears 6,519 6,519 Overlimit facilities over 14 days 31,004 25,875 TOTAL 74,747,683 50,293

The impaired loans are generally not secured against residential property. Some impaired loans are secured by bill of sale over motor vehicles or assets of varying value. It is not practicable to determine the fair value of all collateral as at balance date due to the variety of assets and condition.

NON ACCRUAL LOANS

Balances with specific provisions for impairment 34,059 67,612 Specific provision for impairment (31,272) (50,933) NET NON ACCRUAL LOANS 2,787 16,679

There are no restructured loans or assets acquired through enforcement of security.

PAST-DUE LOANS

BALANCE 30,819 262,928 The loans that are past due are not considered for impairment as they are well secured. There were no renegotiated loans during the year.

LOANS AND ADVANCES

2015 - $

2016 - $2016 - $ 2015 - $

24 Woolworths Employees’ Credit Union Annual Report 2016

Notes to tHe fiNANciAl stAteMeNts ...coNtiNueD

NOTES TO THE FINANCIAL STATEMENTS...CONTINUED

25 Woolworths Employees’ Credit Union Annual Report 2015

8. AVAILABLE FOR SALE INVESTMENTS

INVESTMENTS AT COST COMPRISE: 2016 - $ 2015 - $

SHARES IN UNLISTED COMPANIES - AT COST

CUSCAL Primary shares 17,119 17,119 CUSCAL Central banking shares 100,578 100,578