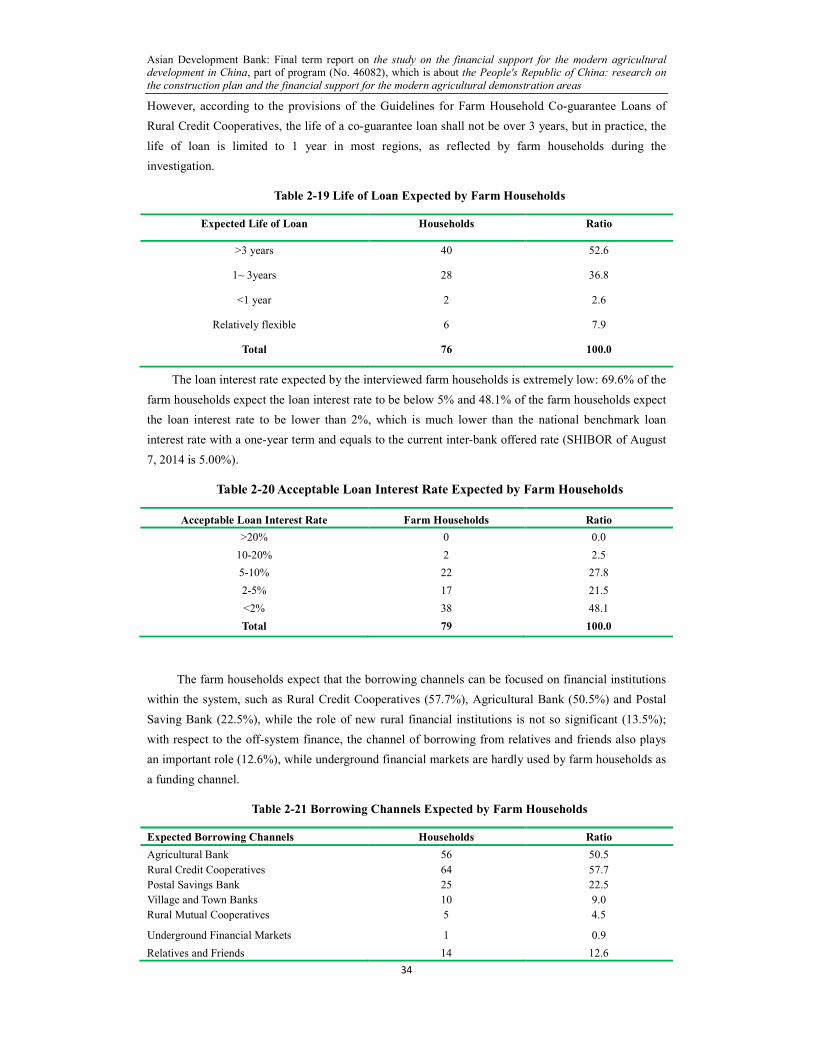

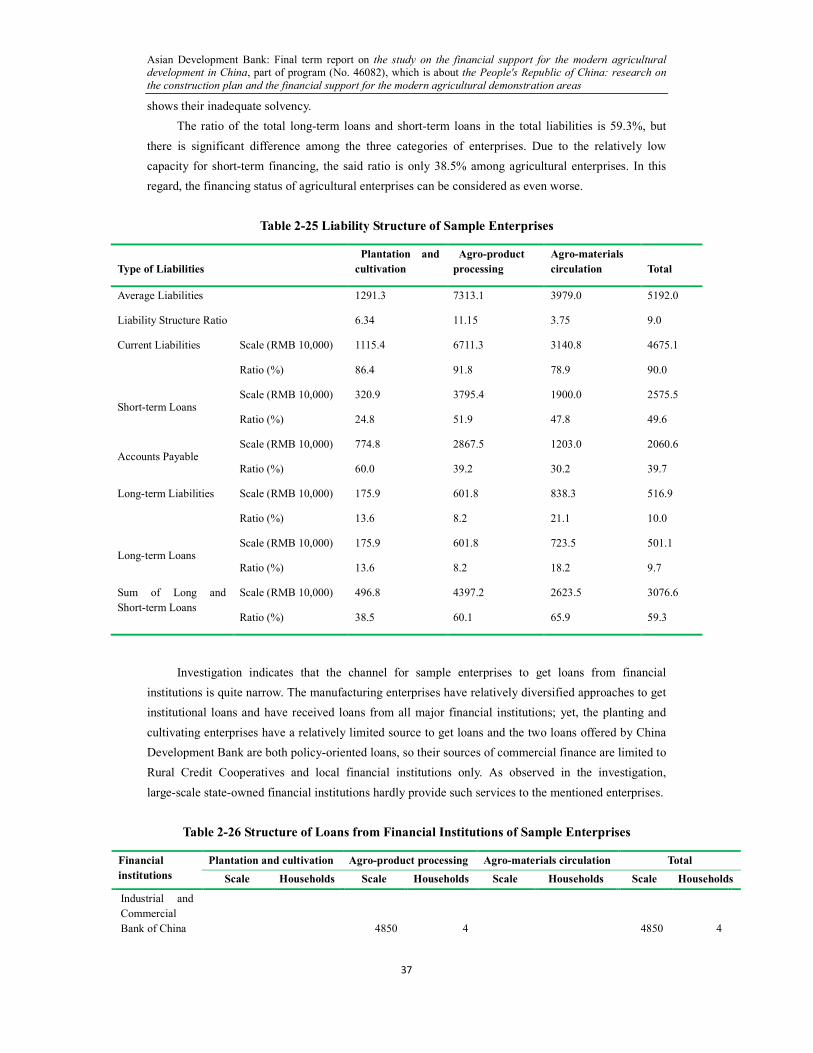

46082-001: study on the financial support for modern ... · chapter 1 rural financial development...

TRANSCRIPT

Technical Assistance Consultant’s Report

This consultant’s report does not necessarily reflect the views of ADB or the Government concerned, and ADB and the Government cannot be held liable for its contents. (For project preparatory technical assistance: All the views expressed herein may not be incorporated into the proposed project’s design.

Project Number: 46082 September 2015

PRC: Study on Modern Agriculture Demonstration Area Planning and Financial Support Mobilization – Study on the Financial Support for Modern Agricultural Development in the People’s Republic of China Financed by the Technical Assistance Special Fund

Prepared by Xia Ying

Institute of Agricultural Economics and Development, Chinese Academy of Agricultural Sciences

Beijing, PRC

For the Department of Development and Planning, Ministry of Agriculture

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

1

Study on the Financial Support for Modern

Agricultural Development in the People's Republic of China

Final Report

Xia Ying

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

2

Catalogue

Introduction ....................................................................................................................................... 5

Chapter 1 Rural Financial Development Theories and Policies in China ...................................... 6

1.1 Basic theories of rural finance ............................................................................................. 6

1.1.1 Summary of three main rural financial theories ....................................................... 6

1.1.2 Selection of financing channels in rural financial market ........................................ 6

1.1.3 Performance evaluation of rural financial institutions ............................................. 7

1.1.4 Construction and reform of rural financial systems ................................................. 8

1.2 Financial support policies on agricultural development in China ..................................... 10

1.2.1 Fiscal policies ......................................................................................................... 10

1.2.2 Policies of tax reduction and exemption ................................................................ 13

1.2.3 Policies of differential interest rates ....................................................................... 14

Chapter 2 Current Situation of Investment and Financing of Chinese Modern Agriculture:

Taking Representative MADAs as Example ................................................................................... 16

2.1 Major suppliers of agricultural investments and financing in China ................................ 16

2.2 The supply status of agricultural investment and financing in recent years ...................... 18

2.2.1 Fiscal input ............................................................................................................. 18

2.2.2 Credit ...................................................................................................................... 20

2.2.3 Insurance ................................................................................................................ 29

2.3 Investment and financing demands in agriculture ............................................................. 30

2.3.1 Farms and large specialized households ................................................................ 30

2.3.2 Agricultural enterprises .......................................................................................... 35

2.4 Features and problems of supply and demand of agricultural funds ................................. 38

Chapter 3 Practical Explorations of Financial Support for the Development of Modern

Agriculture: the Perspective of Product Innovation and Service Innovation .................................. 43

3.1 Mortgage and guaranteed Loans ....................................................................................... 43

3.1.1 The practice of rural land financialization in Chongqing Municipality ................. 43

3.1.2 The practice of land revenue guaranteed loans in Jilin Province ........................... 45

3.1.3 Financial innovation in the reform of the collective forest rights in Fujian Province

......................................................................................................................................... 47

3.2 Combined loans by the interaction between government, banks and insurers .................. 48

3.2.1 “Tiandong Model” .................................................................................................. 48

3.2.2 “Shouguang Model” ............................................................................................... 50

3.3 Loans for cooperatives with joint guarantee: the case of Beijing ..................................... 51

3.3.1 Cooperative loans with joint guarantee by cooperatives ........................................ 51

3.3.2 Cooperative member loans with joint guarantee by cooperative members ............ 52

3.4 The various models of supply chain financing .................................................................. 53

3.4.1 Grain supply chain loans jointly supported by financial enterprises in Henan

Province .......................................................................................................................... 53

3.4.2 Wuliming model of supply chain finance created by Longjiang Bank and COFCO

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

3

......................................................................................................................................... 54

3.5 Construction of rural credit system: the case of Lishui City of Zhejiang Province .......... 55

3.6 A typical example of rural financial payment system reform: Shouguang City of

Shandong Province ................................................................................................................. 55

3.7 Commentary ...................................................................................................................... 57

3.7.1 Financialization of resources assets such as farmland ........................................... 57

3.7.2 Supply chain finance .............................................................................................. 58

3.7.3 Loans jointly guaranteed by specialized cooperatives ........................................... 59

3.7.4 The model of loans jointly guaranteed by the government and the banks ............. 60

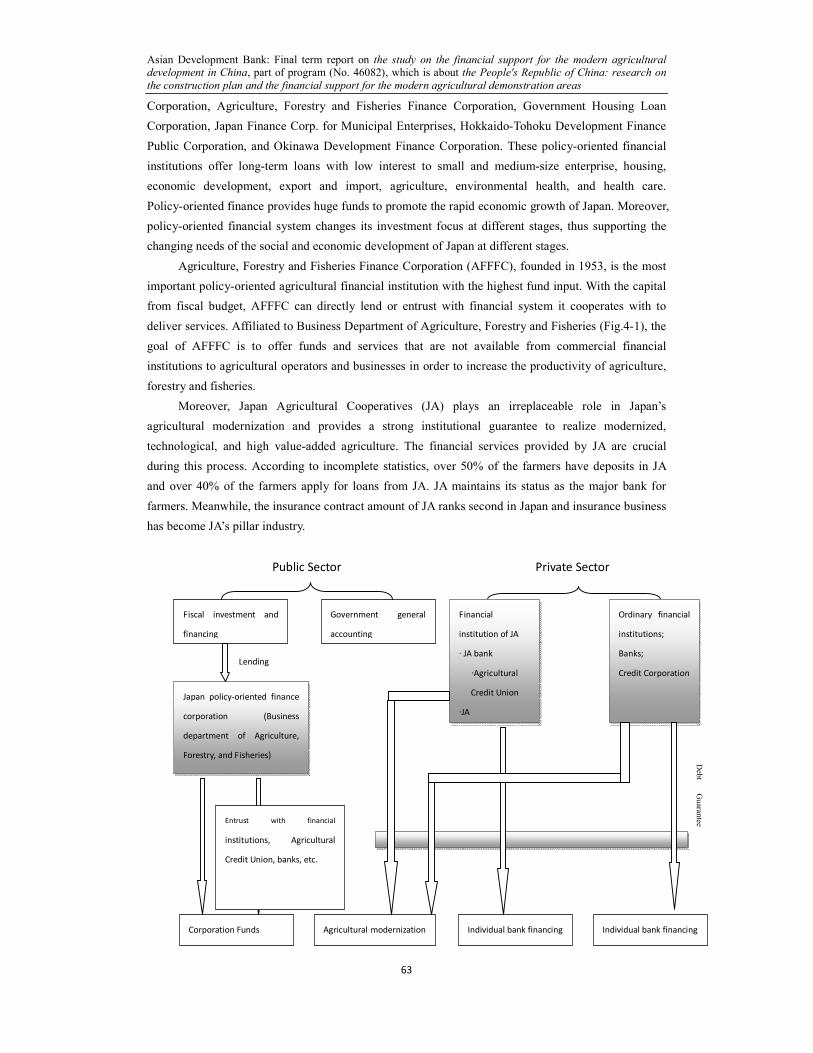

Chapter 4 Financial Support for Modern Agricultural Development: International Experiences 61

4.1 Agricultural financial service system of developed economies: organizations and

functions .................................................................................................................................. 61

4.1.1 Policy-oriented financial institutions play a major role in building a complete and

diversified agricultural financial system. ........................................................................ 61

4.1.2 Diversified agricultural policy-oriented financing methods well-matched with the

functions of institutions ................................................................................................... 64

4.1.3 Powerful policy-oriented financial system: co-existence of strength and pressures

of transformation ............................................................................................................. 66

4.2 Operation system and mechanism analysis of agricultural finance in major countries ..... 67

4.2.1 Fiscal support to agricultural financing by governments of developed economies 67

4.2.2 Cooperation among credit cooperatives: models and risk control ......................... 69

4.2.3 Cooperation between public sectors and private sectors to expand agricultural

financing channels ........................................................................................................... 71

4.2.4 Development mechanism that promotes value chain finance ................................ 71

4.2.5 Institutional mechanism that promotes the development agricultural

policy-oriented insurance ................................................................................................ 73

4.2.6 Establishment of agricultural development funds (ADF) ...................................... 73

4.2.7 Professional risk management and budget management, and assessment of the

progress towards policy goals ......................................................................................... 74

4.2.8 Adjustment of support focus and support method in accordance with social and

economic development.................................................................................................... 75

4.3 Conclusions and Lessons .................................................................................................. 75

4.3.1 Conclusions ............................................................................................................ 75

4.3.2 Lessons ................................................................................................................... 76

Chapter 5 Construction of Modern Agriculture Financial Support System and Supporting

Measures ......................................................................................................................................... 78

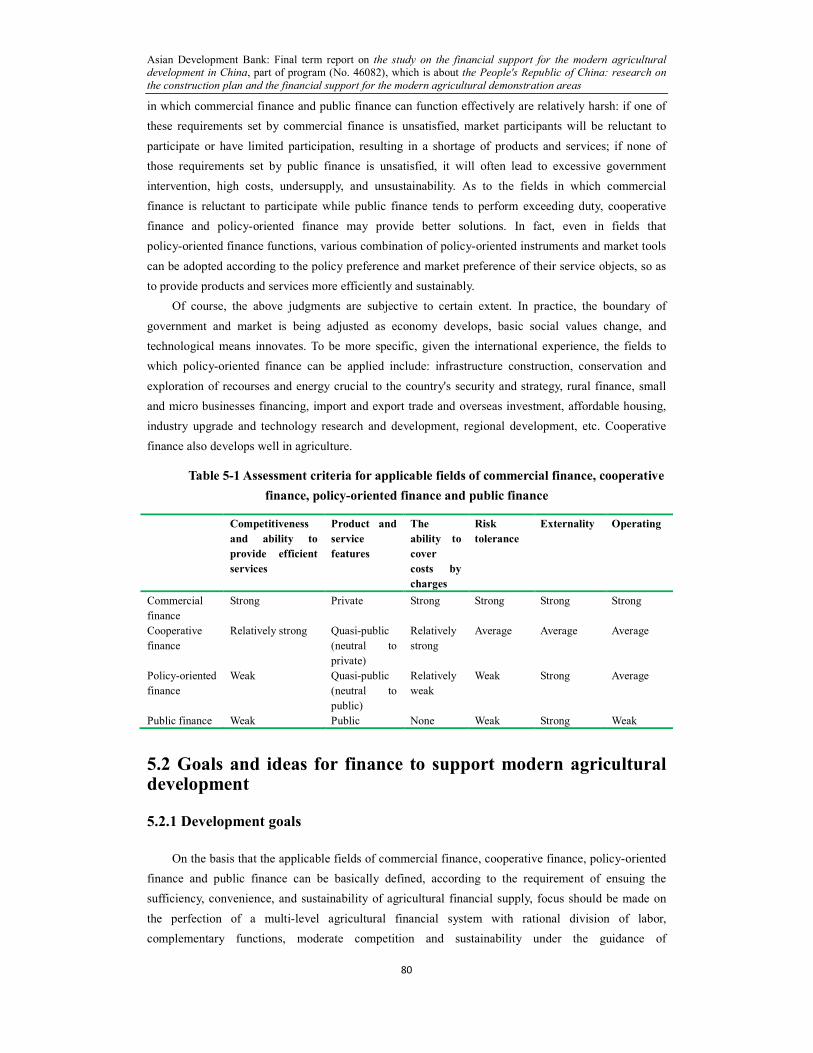

5.1 Modes of agricultural financing and functions ................................................................. 78

5.2 Goals and ideas for finance to support modern agricultural development ........................ 80

5.2.1 Development goals ................................................................................................. 80

5.2.2 Construction ideas .................................................................................................. 81

5.3 Content of the construction of modern agriculture financial support system .................... 82

5.3.1 Commercial financial institutions .......................................................................... 82

5.3.2 Policy-oriented agricultural finance ....................................................................... 83

5.3.3 Cooperative finance ............................................................................................... 85

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

4

5.4 Supporting measures: comprehensive reforms on land, social security and rural finance 87

5.4.1 Perfection of existing agricultural financial system ............................................... 87

5.4.2 Binding rural land system reform, social security system reform and financial

system reform together .................................................................................................... 88

Chapter 6 Conclusions and Policy Suggestions ........................................................................... 89

6.1 Main conclusions .............................................................................................................. 89

6.1.1 On the conception and positioning of agricultural and rural finance ..................... 89

6.1.2 China has basically established an agricultural and rural financial system

combining policy-oriented finance, commercial finance, and rural cooperative finance.

......................................................................................................................................... 91

6.1.3 Formal financial institutions are the major suppliers of agricultural and rural

financial services in China, while private loans cannot be neglected. ............................ 91

6.1.4 Problems of insufficient supply, inconvenience, and poor sustainability exist in the

development of China’s agricultural finance .................................................................. 92

6.2 Suggestions on promoting the development of agricultural finance in China’s MADAs . 93

6.2.1 Institutional construction ........................................................................................ 93

6.2.2 Mechanism innovation and business innovation .................................................... 95

6.2.3 Institution building ................................................................................................. 96

6.2.4 To promoting construction of trustworthy culture for agricultural and rural

financial development ..................................................................................................... 97

References ....................................................................................................................................... 98

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

5

Introduction

This is the final report on financial support for modern agriculture in China, which is part of the

ADB program: “The People's Republic of China: research on the construction plan and the financial

support for the modern agricultural demonstrated zones” (program number: 46082). Based on field

surveys in the five modern agriculture demonstration counties and official materials and data from

other demonstrations zones of rural financial reforms, the report analyzes the current situations of

financial services for Chinese modern agriculture, summarizes the progress and experiences of rural

financial innovation, and explores existing problems. Successful international experiences of

developing countries of financial support for modern agriculture and policies and measures of relevant

international organizations are also summarized and used as reference for policies recommendations on

improving financial support for modern agriculture in China.

Some of the major conceptions which are broadly used in this report are defined here:

Rural Financial System: it refers to the financial system which is composed of various banking

institutions at and under county level and provides financial support for rural economic activities,

including rural industrial development, agricultural infrastructure construction and rural consumption.

Rural finance is not exactly the same as agricultural finance, which covers much more fields than the

latter, while some of the functions of agricultural finance are implemented by urban financial

institutions. Policy financial institutions are important in the system of financial support for modern

agriculture, basically because agriculture is weak and fundamental in national economic system.

Policy agricultural finance: it is understood in two aspects. On the one hand, it refers to

policy-oriented finance, which are specific invention or steering policies to introduce financial services

into agriculture. It works on those rural financial institutions by financial instruments, some of which

are interest subsidy for loans, direct loans by policy financial institutions, subsidy on subsidy guarantee

charges, policy agricultural insurance, etc. On the other hand, it refers to the specific policy financial

institutions such as the national agricultural development bank, which assume the state policies and

strategies and aim at the shortcomings of commercial or cooperative financial institutions. In sum,

policy agricultural finance refers to those fiscal appropriation and loans to agricultural finance guided

by national and local policies.

Modern agriculture demonstration zones: These are those state-level modern agriculture

demonstrations specifically certified by MOA, which aim at realizing national strategy and solving

problems comprehensively.

Supply and demand Main bodies of rural finance: The supply main bodies of rural finance

(including credit money and product service) include: state-owned commercial banks, cooperative or

shareholding banks, agriculture-related dragon-head companies, intermediary financial institutions

(such as insurance, pension institutions, guarantee companies). The demand main bodies of rural

finance are those market participants within county scope, which are farm households, family farms,

specialized households, agricultural cooperative, agricultural companies, and agricultural service

companies.

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

6

Chapter 1 Rural Financial Development Theories and Policies in China

1.1 Basic theories of rural finance

1.1.1 Summary of three main rural financial theories

In western economies, rural financial development theory is derived from general financial

development theory, and discusses the relationship between financial development of the rural areas in

developing countries, and agricultural development and non-agricultural development and other areas

such as the income growth of rural residents, and poverty elimination. Traditionally, there are two

representative theories about rural financial development: agriculture subsidized credit paradigm and

rural financial systems paradigm. Actually, these two theories are opposite. Although each has its own

shortcomings because of some biases, both are still meaningful for further researches. With the

improvement of previous research methods, new rural financial theory based on those two theories is

proposed. The new theory has the same importance as Hayek’s local knowledge theory and Stieglitz’s

imperfectly competitive market theory, whose theories have great impact on directing modern rural

financial development. During many years of development, the system of rural financial theory has

taken shape. Currently, the rural financial theory consists of three main branch theories: the agriculture

credit subsidy theory, rural financial market theory and imperfect competition market theory. These

three theories have already become the theoretical basis of China rural financial research. In recent

years, there is a debate related to the financial repression and financial deepening and financial

restriction in the academia. Essentially, the debate is related to the application of these three theories to

the selection of rural financial market system.

Briefly, the three theories of rural financial market development center on the same key issue,

that is how government plays its role in promoting rural economic growth in rural financial markets.

Because the agriculture credit subsidy theory relies too much on government, the theory brings about

two negative effects. The theory accelerates the development of rural economy at the beginning.

However, it is also criticized because of poor performance on poverty alleviation and financial

inefficiency, etc. The theory advocates the financial deepening proposal without the premise of stable

economy in rural areas, thus suffering market failure and other defects. The imperfectly competitive

market theory, proposed in late 20th century, is based on the information economics theory. The theory

discriminates the function of credit market, capital market and other markets in detail, and proposes a

moderate government intervention under the market operation mechanism. The views of the

imperfectly competitive market theory match the advancing gradually reform. Domestic scholars

compare the three theories, and most of them agree that imperfectly competitive market theory is

development direction of China’s rural financial market. According to the experience of international

agricultural modernization countries, such as America, France and Japan, agriculture credit subsidy

theory is no longer a mainstream theory (Ding, 2010).

1.1.2 Selection of financing channels in rural financial market

The rural financing channels are an important issue of researches on rural financial development.

Generally, there are two financing channels in rural areas: formal financial intermediaries and informal

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

7

financial intermediaries.

About the causes of credit difficulty of rural formal financial institutions, according to Indian

economic experts Subrata Ghatak and Ken Ingersent, most farmers are excluded from credit market

because profit-seeking formal rural financial institutions have not enough branches but high operation

costs. Therefore, in order to meet the rural financial demand, developing countries should increase

credit supply and build a multilayered rural financial system to increase the rural financial supply.

Adams (1988) mentioned two important criteria in his evaluation criterion for rural financial

system. They are the number of people who offers rural official financial service and the service quality

of the financial institutions, both of which prove low coverage of rural finance. Based on our country’s

situation, Han Jun mentions that it is difficult for the main entities of China’s rural economy to get

credit support from formal financial institutions, because the low fiscal agricultural support leads to the

unbalanced development of rural financial organizations. Zhou (2004) also pointed financial

organizations are not necessary the financial organization that neared farm households, thus the

operation cost to obtain these farm households’ information is high for financial organizations.

Moreover, the lack of contract implementation mechanism of farmers and other adverse reasons as well

make rural financing difficult.

Because of difficulties of formal financing in rural areas, Chinese scholars began to discuss

informal financing channels. Yaron (1997) and World Bank (2004) believed that lots of ranchers and

the rich got agriculture credit; however, the poor always met their financing demands from informal

financial institutions. Besley (2001), Khandker (2003), Wen (2001) and other experts believed informal

financial market is the main financing channel for farm households, especially the poor ones in some

countries. Lou (2009) used impulse response function and variance decomposition of time series

analysis, combined with the statistics of Zhejiang province in the years from 1978 to 2007, and

believed there is a close relationship and long-term equilibrium between the rural finance in Zhejiang

province, private finance and rural economic growth. Also, Lou believed that rural finance has adverse

effects on economic growth, whereas, private financial supports has remarkable economic effects.

Other researchers found that micro-credit organizations had become another financing channel

for the rural financial market. Zeller (2001) believed micro-credit organizations can meet the farmers’

financing demands in terms of credit scale, interest rate pricing, regulatory system, risk management,

etc., especially for the poor farmers. World Bank (1997) and Washington Conference (2003) considered

that micro-credit had become the main innovation model of farmer financing. For now, the financial

model of Grameen Bank has been applied in more than 100 countries.

1.1.3 Performance evaluation of rural financial institutions

The above mentioned assumptions and policy proposal for the three rural financial theories

implicate the evaluation criterion of rural finance. For example, the amount of agricultural credit and

the credit approval speed are the standards to measure the performance of rural financial institutions.

However, actually this evaluation criterion has negative effects on enhancing the vitality of rural

financial institution and its sustainability. Based on the rural finance investigation of emerging

developing countries, Yaron (1992), rural finance consultant of World Bank and other consultants also

thought the performance of rural finance development should be evaluated with two main ways. The

first way is the contribution of rural finance to economic development, and Yaron (1992) proposed two

criteria to measure such contribution: i) the growth of agricultural production measured by the

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

8

contribution of rural finance; ii) the effect of rural finance on rural economic fairness. The second way

is the independence and sustainability of rural financial market. However, it is difficult to propose a

comprehensive and reasonable criterion to evaluate the performance of financial institutions because of

the small business volume, narrowed business areas and low efficiency of rural financial institutions.

Additionally, compared with other financial institutions, rural financial institutions have special service

targets. Based on these reasons, Yaron (1992) thought the success of rural financial market should be

evaluated from two aspects in accordance with the real situation of rural financial market and financial

institution development:

(1) The service scope of rural finance: The contribution of rural finance to the rural economic

growth and economic fairness has something to do with the service scope of rural finance. In other

words, the contribution is related to the rural financial service coverage to rural finance target

customers. The rural finance service scope is a comprehensive index that can estimate the degree of

penetration of the rural financial market and evaluate the service quality of rural finance. Additionally,

the service scopes can also reflect the depth and breadth of rural finance development. Yaron, Benjamin

and Piprek (1997) refined the rural finance service into the amount of deposits and checking accounts,

the average value of saving and checking accounts, the variety of products or services, the number of

branches, the percentage of farmer who use rural finance service, etc.

(2) The self-sustaining ability of rural finance: Generally, a financial institution’s revenue should

exceed its expenditure, which is the requirement for the institution to keep operation. The

self-sustaining ability of rural finance is a composite index. Revenue includes interests obtained from

business activities and subsidies for the rural financial institution. Expenditure includes operating

expenditure, opportunity cost, etc. The subsidy dependence of rural financial institutions is an index for

self-sustaining ability that can be used to measure the operational ability of rural finance. Zeller and

Megor (2002) thought the welfare effects of rural financial system should also be considered as an

index to measure the self-sustaining ability.

1.1.4 Construction and reform of rural financial systems

This part focuses on formal and informal financial institutions. Germids (1990) and Besley (1994)

considered that rural financial market consisted of formal, quasi-formal and informal financial

institution. In this section, rural financial institutions are only divided into formal financial institution

and informal financial institution.

As to formal financial institution, Chinese scholar Li (2000) believed that because China rural

financial institutions developed slowly, farmer cannot get loans with low interest rates on time. As a

result, the credit demand of the farmer is repressed. Peng (2001) pointed that rural financial system

construction in China lagged behind seriously. After Zhang (2008) analyzed the weaknesses of China’s

rural financial institutions in inadequate capital scale, capital allocation ability, and ability to provide a

variety of financial services, he proposed that the function of Agricultural Development Bank of China,

commercial financial institutions and Rural Credit Cooperative should be strengthened and highlighted.

For the rural financial intermediary, Zeller (2003) analyzed the comparative advantages of every kind

of rural financial intermediary, and thought the union of different kinds of rural financial institutions

should be strengthened and promoted. In his opinion, the bank that located in the countryside, mutual

aid team and self-help group are level one; credit union and small bank are level two and commercial

bank, nationalized bank and multi-national bank are level three.

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

9

As to informal financial institutions, as the informal financial market has become the main

financing channel for farmers especially for the poor farmers, more and more researchers are giving

attention to this market and analyze the reasons why informal financial intermediaries emerge from

every aspect. Heiko Schrader, a Germany researcher, referred informal finance as the finance market

beyond the control of national credit system and relevant financial regulations. Anders Isaksson (2002)

pointed out that private finance is the financial activity occurs without government supervision. It is a

rational response to policy distortion and financial repression. Because of the institutional

discrimination and bias against government’s credit allocation system under the financial repression, a

private financial market system is required. However, Thierry Pairault proposed that the development

of private finance in every country and region is the result of personal economy development. Steel

(1997) pointed out that the reason for the private finance development is that private finance can use

their advantages to get impeccable personal information in the local area. Therefore, private finance

solves the problem of information asymmetry that formal finance cannot deal with. Germidis Dimitri

(1990) thought one of the characteristics of informal finance is that there is a connection from simple

credit arrangements to complex mechanism of financial intermediary between the debtor, creditor and

saver.

Lin (2003) and other Chinese scholars has constructed a financial market model to prove that the

segmentation of financial market and informal finance market are the result of the interaction between

creditors of medium and small-sized business, creditors of informal financial institutions and creditors

of informal institutions. Also, they thought that adverse selection and moral hazard caused by

information asymmetry are the main reasons to boom private finance. In their opinion, financial

repression is only a catalyst. Lin et al.’s researches explained the reason why private finance also exists

in some countries with financial liberalization. Ren (2003) pointed out that the booming of private

finance is attributed to the replacement or changing of existing policy, or created by the new policy.

The booming of private finance is the result of the institutional change in finance. Cui (2006) said the

weakness of formal rural finance service in China is the reason for the development of private finance.

Zhang (2001) used the new institutional economics as a research method, and he believed private

finance satisfies the demand for finance of China’s private economy. Kellee Tsai (2001) used China as

a research sample. He compared the development path of private finance and the development path of

regional economy of Changle, Hui’an, Wenzhou and Zhengzhou areas, and concluded that the reason

why there is a difference in financial development in different areas is that local governments

implement differentiated policy to private economy. Tsai’s has the same opinion as Zhang, and they

both think that private finance is a form of private economy.

Based on China’s financial policies and the situation of private finance, Chinese scholars begin to

discuss the legality of usury, a production of private finance. Cao (2000), Wen (2002), Li and Shi (2003)

et al believed that usury is very popular in private finance, and it has really adverse effects on rural

development. However, Jiang (1996), Shi (1998), Mao (2002) et al support the rationality of high

interest rates, and they propose to give private finance a legal status.

As to the management of rural private finance, some scholars believe rural informal finance

should replace informal finance, because informal rural finance has high interest rates and low

efficiency. On the contrary, some scholars think there is a lack of formal rural financial system, while

informal financial system adapts to the rural environment; it is the major way for farmers to obtain

financial service. Hoffand Stiglitz (1996) thought formal financial institutions should connect rural

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

10

formal finance with informal finance by choosing local agents in rural areas, loaning funds to informal

creditors and the latter again loans these funds to farmers, and making pawns.

1.2 Financial support policies on agricultural development in China

The financial policies to support agricultural development can be divided into three categories:

the fiscal support policies, preferential tax policies and differential interest rate policies. These policies

are mainly targeted on the reform of rural financial institutions, the support for the development of new

rural financial institutions, the measures to encourage the increase of agricultural credit, premium

subsidy for agricultural insurance, discount interest to help the poor, and so on.

1.2.1 Fiscal policies

1. Support policies and measures aiming at rural financial institution reform. First of all

there is the support on the the shareholding reform of Agricultural Bank of China. During the process

of the reform, the core capital adequacy ratio of Agricultural Bank of China is increased by receiving a

sum of dollars equivalent with 130 billion RMB Yuan from Central Huijin Investment Ltd. Besides, the

Cental Huijin Investment Ltd has help the agricultural bank improve its asset quality by supporting it to

dispose a sum of 815.7 billion yuan non-performing loans (NPL). Secondly, the reform of RCCs (rural

credit cooperatives) was supported. Subsidies of a total of 8.85 billion Yuan have been given to RCCs

that suffered losses resulting from implementation of inflation-proof savings during 1994 to 1997. In

addition, it was made clear that the service expenditure of provincial united cooperatives should be

allocated to grass root cooperatives, which means that part of the provincial united cooperatives’

income cannot be taxed. Thirdly, the state Agricultural Development Bank was built and supported to

expand its business scope so as to strengthening its role of policy-oriented supporting for agriculture.

2. Targeted cost subsidies for new rural financial institutions. Since the new rural financial

institutions is just established for a short period of time and they have to face big financial pressure at

the initial stage, the Ministry of Finance began to subsidize some qualified new rural financial

institutions to release their financial pressure since 2008. According to the Interim Measure for

New-type Rural Financial Institutions Targeted Cost Subsidies from Central Finance enacted by the

Ministry of Finance in 2010, some rural financial institutions will get a subsidy of 2% of their loan

average balance of the previous year only on the condition that the loan companies and rural fund

mutual cooperatives have achieved a year-on-year growth in loan average balance of the previous year

and met the regulatory index required by China Banking Regulatory Commission (CBRC), or village

and town banks have achieved a year-on-year growth in loan average balance of the previous year, the

loan-to-deposit ratio at the end of the previous year is higher than 50%, and has met the regulatory

index required by CBRC. In 2010, the Ministry of Finance included the financial institution outlets in

western area where basic financial services are weak into the subsidy plan.

The Interim Measure for New-type Rural Financial Institutions Targeted Cost Subsidies

(hereafter refer to as the “measure”) was enacted by the Ministry of Finance on March 28th

2014, and

began to take effect on April 11th

2014. Meanwhile, the Interim Measure for New-type Rural Financial

Institutions Targeted Cost Subsidies from Central Finance [Finance (2010) No. 42] enacted by the

Ministry of Finance in 2010 was abolished. The new “measure” shows that qualified new rural

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

11

financial institutions, which refers to the village and town banks, loan companies and rural fund mutual

cooperatives authorized by the CBRC in the new “measure”, can get a subsidy of 2% of their loan

average balance of the current year from the financial departments. The amount of the subsidy should

be borne in proportion by the central and local finance. The allocation proportions of central and local

finance in eastern, central and western China are 7:3, 8:2 and 9:1 respectively. In the new “measure”,

the specific requirements for financial institutions to get this subsidy are as follows: a year-on-year

growth of loan average balance of the same year; the annual average loan-to-deposit ratio of village

and town banks is equal to or higher than 50%; the proportion of the average balance of agricultural

loans and loan average balance of small and micro enterprises is 70% of all the loans of the same year

or higher, etc.

3. The policy of loan with subsidized interest. First of all, there is the policy of interest subsidy

for poverty alleviation. In order to direct the financial capital into poor rural areas, money from the

central finance has been arranged as subsidy for loans to the poor since 1998. Meanwhile, the system of

interest subsidy for the loan for the poor central finance continues to be reformed and improved, and

thus the capital sources are enlarged. By the end of 2009, a total of 8.15 billion yuan the central finance

had allocated for the discount interest, and stimulated the issuance of over a 200 billion yuan loan for

supporting the poor. Secondly, there is the policy of interest subsidy for loans by local-level

governments. Taking Hainan province as example, to lower the financing cost of farmers, this province

has implemented the interest subsidy policy for small loans by farmers. Farmers’ small loans less than

100 thousand yuan can get the lower interest rate from the government, among which, the provincial

finance undertakes 5%, and the proportion of discount interest of the local city is decided by the local

governments according to their financial situation. The interest rate assumed by farmers of Danzhou

City is 1.5%, and that of Dongfang City is 1%. According to statistics, the number of farm households

who have applied for small loans less than 100 thousand yuan reached 56.7, amounting to 1.906 billion

yuan for the whole Hainan province in 2013. This province had paid government-funded interest

subsidy to 53.3 thousand households, amounting to 109 million yuan in that year, which effectively

alleviated the financing difficulties of farmers in their agricultural production and living.

4. Special funds for loan guarantee. In the policy documents about the innovation of

agricultural financial products and financial services, mortgage loan business involved with contractual

right of rural land and the right to use of cartilage are frequently referred, which have effectively

expended the coverage of mortgage guarantees[1]

. What’s more, the policies particularly encourage

local governments with necessary conditions to set up financing guarantee companies funded by these

governments, or allocate a specific fund quota from the existing financing guarantee companies to offer

guarantee services to new agricultural business entities; in addition, the polies emphasize that the

banking financial institutions should strengthen their cooperation with guarantee institutions that deal

with the guarantee business for new agricultural business entities, appropriately expand the amplifying

times of guarantee deposits, promote the financing model of “loan plus insurance”, and satisfy the

capital demands of new agricultural business entities[2]

. Therefore, supporting the development of

agricultural guarantee institutions by the government is one of the important routes for agricultural

[1]

Promote the innovation of rural financial products and services (Banking issued [2008] No. 295). [2]

The guide suggestion on the financial service for new agricultural business entities such as family farm (Banking

issued [2014] No. 42)

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

12

financial products and the businesses innovation, so as to effectively strengthen the services that

financial institutions offer to agriculture, rural areas and farmers. At the local government level,

guarantee institutions funded by government has become a common practice to service agriculture,

rural areas and farmers. In the five counties investigated, each has guarantee companies backed by the

government. For instance, Fujin city of Heilongjiang province has established Fujin Jinxing

Agricultural Guarantee Company, a public institution affiliated to the municipal finance bureau; Helan

county has established a small loan guarantee center for the unemployed, which is affiliated to the

bureau of labor and employment service of this county, and provides guarantee services for rural

women, undergraduates, scientific special commissioners to start their business or obtain a job..

Tiandong county of Guangxi Zhuang Autonomous Region has established a financing guarantee

company financed by the government in 2009 to support the agriculture of Tiandong County, and it

inclines to offer guarantee services for comparatively large agricultural loans. After a two-time capital

increase, the capital of this company now has reached 30 million yuan. The rural commercial banks and

village and town banks that cooperate with it provide a tenfold credit ceiling, which means that the

amount of loan reaches 300 million yuan. In addition, the government of Hainan province actively

explores the way to establish guarantee funds supported by provincial finance to benefit farmers, to

deal with agricultural loans without mortgage, and to attract more financial capitals to the agricultural

field by means of credit guarantee.

5. Policy-oriented funds for agricultural insurance. In 2007, the Ministry of Finance enacted

Measures of Management on Pilot Areas of Agricultural Insurance Premium Subsidies from Central

Finance, and launched the pilot work for agricultural insurance premium subsidies, offering premium

subsidies to five crops of six provinces. The central and local governments bear 25% of the premium of

the pilot insurance types respectively, and the remaining 50% was borne by the farmers, or jointly

borne by the farmer, dragon-head enterprises and the financial department at the provincial, municipal

and county level. Since then, the central finance has been expanding the subsidy areas continuously,

raising the subsidy proportion and increasing the variety of subsidy insurance. Over these years, the

investment in subsidies has been increasing continuously (The subsidies from central finance is 2.133

billion yuan in 2007, 4.869 billion yuan in 2008, 5.965 billion yuan in 2009, and 6.776 billion in 2010).

At present, except for Hong Kong, Macao and Taiwan, the 31 provinces (autonomous regions,

municipalities directly under the Central Government) of the Mainland China has entered the track of

policy-oriented agricultural insurance pilot. There are up to 15 types of insurance related to national

economy and people’s livelihood and supported by the central finance, covering all the main food

production areas. The agricultural insurance subsidy has become a significant measure for finance of

all levels to integrate all efforts of financing to support the agriculture, rural areas and farmers.

6. Reward and subsidy policies for agricultural loans of financial institutions. To motivate

financial institutions to issue agricultural loans, the central and local governments have implemented

various financial reward and subsidy policies. In 2009, the Ministry of Finance enacted The Temporary

Measure of Incentive Funds Management for Increment of Agricultural Loans from the Financial

Institutions at County Level, and launched the pilot work of rewarding agricultural loan increment of

financial institutions at county level. As for the financial institutions at county level, if the average

balance of agricultural loan of the previous year has realized a year-on-year growth of more than 15%,

the 2% of the part that exceed the 15% will be rewarded, so as to stimulate the endogenous impetus of

financial institutions to increase the amount of agricultural loans. In 2010, the Ministry of Finance

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

13

further improved the pilot policy, and expanded the pilot range to 18 provinces (autonomous regions).

Each local government has made corresponding risk compensation policy or incentive policy in order

to encourage financing institutions to increase the amount of agricultural loans. For instance, Hainan

province gives a 1.5% risk compensation and 0.5% reward to small discount-interest loans of famers

offered by financial institutions. In 2013, the whole Hainan province cashed the risk compensation of

20.504 million yuan and the reward of 7.5395 million yuan. In 2012, Tiandong county of Guangxi

Zhuang Autonomous Region offered a reward of 1.06 million yuan to rural commercial banks, postal

saving banks and rural banks apart from the a 7.57 million yuan reward from national finance. What’s

more, the financing guarantee companies assist in agricultural development of Tiandong County

received a reward of 120 thousand yuan for guarantee loans according to its business volume. In

addition, Tiandong County allocated a special fund of 7.8 million yuan to establish the risk

compensation fund for small credit loans and financing risk compensation for rural property mortgage.

These funds provided 153 thousand yuan for the compensation of non-performing loans of Hongxiang

Rural Fund Mutual Cooperative and local Agricultural Bank.

7. Improvement of matched financial institutions. In terms of finance-related accounting

system, the Ministry of Finance has relaxed conditions for the write-off of bad agricultural loans of

financial institutions, and has authorized the financial institutions to restructure, reduce, or exempt

some qualified agricultural loans, and reduce or exempt the principal and interest in the table where

appropriate. As to the performance appraisals of financial institutions, the index of agricultural loan and

other elements have been included in the performance appraisals as bonus points.

1.2.2 Policies of tax reduction and exemption

1. The tax preference for agricultural financial institutions. According to relevant national

regulations[3]

, the interest income of financial institutions who issue small credit loans no more than 50

thousand yuan to the farmers are exempted from business tax; as to rural credit cooperatives, village

and town banks, rural fund mutual cooperatives, loan companies, and rural cooperative banks and rural

commercial banks whose institution with legal person is located in the county or lower-level areas, the

business tax only should be levied at a 3% preferential tax rate; the qualified guarantee institutions that

support agriculture and rural areas are exempted from business tax for three years; rural commercial

banks and village and town banks can enjoy a 15% corporate income tax reduction. According to the

regulations in the Notification of Pre-tax Deduction Policies for Loan-loss Reserves of Agricultural

Loans of Financial Enterprises and Loans of Small and Medium-sized Enterprises, the loan-loss

reserves of agricultural loans of financial enterprises and loans of small and medium-sized enterprises

should be deducted before tax.

2. The tax preference for special agriculture-related business. The interest income of

financial institutions from farmers’ small loans is exempted from business tax. When calculating the

taxable amount of incomes, only 90% of the interest income of financial institutions from farmers’

small loans, is calculated. As specified in the Notification of Pre-tax Deduction Policies for Loan-loss

Reserves of Agricultural Loans of Financial Enterprises and Loans of Small and Medium-sized

Enterprises enacted by Ministry of Finance, as to the premium income of insurance companies who

[3]

Notification about rural finance related to tax policy enacted by the Ministry of Finance ( Finance and Tax

[2010] No. 4)

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

14

provide insurance business to planting industry and breeding industry, only 90% of income is

calculated when calculating the taxable income amount. For insurance companies who operate certain

types of insurance in planting industry and receive premium subsidies from central and local finance,

the catastrophe risk reserves are written down according to no more than 25% of the premium income

of the insurance that receive subsidies of the current year, and can be deducted before the corporate

income tax based on actual situation.

1.2.3 Policies of differential interest rates

1. Lower reserve requirement ratios are implemented for small and medium rural financial

institutions. In order to ensure the sufficiency of rural credit fund, in the context that the liquidity

should be retrenched, rural credit cooperatives can still implement a lower reserve requirement ratio.

Since 2010, People’s Bank of China has up-regulated the legal reserve requirement ratio for many

times. Among these up-regulations, three times are targeted to such small and medium-sized legal

entities as the rural credit cooperatives. At present, the preferential reserve requirement ratio of rural

credit cooperatives is 6% lower than big commercial banks. What’s more, the reserve requirement ratio

implemented by rural credit cooperatives with a higher proportion of agricultural loans and small

capital scale is 7% lower than big commercial banks. Meanwhile, the legal reserve requirement ratio of

the village and town banks is the same as that of local rural credit cooperatives.

2. The marketization of loan interest rate is steadily advanced so as to lower the financing

costs of new agricultural business entities. The floating interest rate cap of rural credit cooperative’s

loans can be extended to 2.3 times of the benchmark interest rate for loan. In terms of the interest rate

of new rural financial institutions, People’s Bank of China has enacted the Guidance on Offering

Financial Services to New Agricultural Business Entities Such as Family Farmers (issued by People's

Bank of China [2014] No. 42). In this guidance, for eligible new agricultural business entities whose

local government has introduced government-funded interest discount and risk compensation policies

and who have received loans by mortgage or impawn or by introducing insurance or guarantee

mechanism, etc., the interest rate should be lower than the average loan interest rate of the same type

and the same level in the institution in principle. In addition, the banking financial institutions

shouldn’t charge additional fees apart from the loan interest rate, and shouldn’t conduct tie-in sales

with other financial products or attach other conditions to increase the financing cost. In summary,

these measures aim at reducing the financing cost for new agricultural business entities practically.

3. Specific policy measures are implemented on the principle of “certain proportion of

newly increased deposits should be used locally”. In 2009, People’s Bank of China and China

Banking Regulatory Commission (CBRC) unitedly formulated the Assessment Method for

Encouraging County-level Financial Institutions to Use a Certain Proportion of the Newly Increased

Deposits in Local Loans (for Trial Implementation), and the pilot work has been conducted in some

counties since 2011.

4. Management of agricultural reloan is improved. In recent years, By drawing upon the

experience of using agricultural reloan, the People’s Bank of China has strengthened the adjustment of

the quota of agricultural reloan among different areas, with more quota allocated to the west and the

major grain production areas. Meanwhile, the village and town banks are also included in the range of

agricultural reloan. In the busy season of spring plantation in 2010, the amount of agricultural reloan in

the west and major grain production areas was adjusted and increased to 10 billion yuan. After the

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

15

increase, the proportion of re-loan amount for supporting agriculture in these areas was up to 93% of

the whole nation. The agricultural reloan plays an active role in expanding the quota of agricultural

credit loans. In 2013, the range of applying for agricultural reloan was widened and this policy has

been promoted nationwide[4]

. Furthermore, each branch was required to reinforce the monitoring and

assessment of the service effect of re-loan for supporting agriculture, in order to take better advantage

of the function of the re-loan for supporting agriculture; that is to guide rural financial institutions to

raise the size of credit loan for the agriculture, rural areas and farmers.

[4]

Widening the range of re-loan for supporting agriculture (Issued by People’s Bank of China[2013] No. 58)

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

16

Chapter 2 Current Situation of Investment and Financing of Chinese Modern Agriculture: Taking

Representative MADAs as Example

The main sources of agricultural fund can be divided into four parts: fiscal investments, financial

industrial loans, social funds financing, and self-owned fund. In this part, only the first two parts are

discussed. The fiscal and financial funds have diversified forms in reality, which generally include

non-reimbursable grants (e.g., fiscal investments and fiscal subsidies), low cost loans (e.g., loans with

fiscally subsidized interest, various kinds of policy-oriented bank loans, loans guaranteed by the

policy-oriented guarantee institutions), and commercial loans.

Due to the characteristics of agriculture and compared with manufacturing and service industry,

agriculture has the features of “high-risk, high-cost, long-cycle and low-benefit. Accordingly, these

features also apply to investment in agriculture. Therefore, as to commercial finance, its investments in

agriculture do not conform to general market rules, resulting in limitations in commercial finance’s

support for agriculture. However, from the national perspective, as a fundamental industry, the intensity

and breadth of agricultural investment cannot be neglected. Thus, the government has enacted various

preferential policies about agricultural investments, to encourage and guide various funds to invest in

agriculture, and that is why most agricultural funds are more or less policy-related.

2.1 Major suppliers of agricultural investments and financing in

China

Government agencies (mainly fiscal department and functional departments related to

agriculture), commercial banks, policy-oriented financial institutions are the major suppliers of

agricultural investments and financing in China.

1. Government agencies. The main investment and financing suppliers among government

agencies are fiscal department, the system of Development and Reform Commission, agricultural

department, forestry department, water conservancy department, transportation department and so on.

Due to the limited local financial strength, the county-level fiscal department has little investment and

financing capacity for agriculture. Currently, fiscal investments in agriculture are mainly in the form of

transfer payment of specific fiscal funds issued by central and provincial fiscal departments, among

which central finance plays the dominate role. Of these departments, special funds of agricultural

department, finance department and the system of National Development and Reform Commission take

a comparatively large proportion; most of the capital of water conservancy department is used to

govern rivers and lakes, whereas, the capital of water conservancy construction of farmer lands take a

small proportion; a small amount of the road construction capital of transportation department is used

in rural low-grade road construction.

2. Commercial banks. Only the Agricultural Bank of China and China Development Bank have

scaled agricultural financing among the state-owned commercial banks.

3. Policy-oriented financial institutions. At present, there are several channels through which

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

17

policy-oriented agricultural financing activities can be carried:

--National policy-oriented financial institutions. Since 2007, China has launched a new round of

reform for the financial system with the emphasis on reform of the policy-oriented banks. With the help

of the reform, China Development Bank has entered the development stage of commercialized

operation, and it is no longer a policy-oriented bank. Thus, currently, on national level, there is one

agricultural policy-oriented financial institution in China— Agricultural Development Bank of China.

--Policy-oriented guarantee institutions. Meanwhile, the policy-oriented guarantee business has

achieved a breakthrough as well. China National Economic Technique Investment & Guarantee

Company was established in 1993. Around 1995, some specialized credit guarantee institutions was

established successively in some provinces and cities. Hence, taking the opportunity of credit guarantee

for medium and small-sized enterprises, the industry of policy-oriented guarantee developed rapidly

everywhere. Accordingly, the agricultural policy-oriented guarantee also started to develop.

--Innovation-oriented budget outlays such as government funds and special funds. Apart from the

development of policy-oriented financing institutions mentioned above, the budget outlays of the

governments at all levels also have some leverage and play a guide role to some extent, and function as

a kind of policy-oriented financing. What’s more, these outlays are oriented to agriculture, high-tech

enterprise, medium and small-sized enterprises, housing, etc. For instance, the special fund for medium

and small-sized enterprises development arranged by central budget can take the approach of discount

interest loan, capital injection, etc.; the guidance fund for the commercialization of national research

findings can take the approach of setting sub-fund for venture capital investment, risk compensation of

loans, etc.; the guidance fund for the venture capital investment of small and medium-sized

technology-based enterprise can take the approach of phased-based equity participation, follow-up

investment, risk subsidy, etc.

--Local government financing-platform companies. In response to the impact of international

financial crisis, China launched a large-scale economic stimulus package in 2009. In order to meet the

capital demand for this plan, local government at all levels had established various financing platforms

one after another. There were no more than 8000 local financing platforms in 2008, whereas, that

number reached ten thousand in 2010. The main purpose of these financing platforms is to raise fund

for local economic construction or social development, and the main method to raise fund is bank loans.

More than 50% of the credit capital is used for the construction of road and municipal infrastructure,

and a small proportion is used in agricultural infrastructure construction.

Apart from these channels mentioned above, the agriculture-related business of Postal Saving

Bank is also policy-oriented to some extent, but profitability is still its main goal and it places extra

emphasis on the operation model of commercial financial intermediary.

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

18

2.2 The supply status of agricultural investment and financing in

recent years

2.2.1 Fiscal input

The fiscal departments at all levels have been increasing their support for agriculture in recent

years in China, and the methods and the effect are being improved. The amount of various

agriculture-related funds is huge. Among these funds, agricultural expenditure and the expenditure of

the comprehensive agricultural development are the two expenditures directly used in agricultural

production. These expenditures accounted for 51.6% of the fund for supporting agriculture (Table 2-1).

Table 2-1 Status of Financial Support for Agriculture in China

Items 2008 2009 2010 2011 2012 2013

Agriculture 2090.5 3826.9 3949.4 4434.4

Forestry 377.3 532.1 667.3 744.6

Water conservancy 1086.8 1519.6 1856.5 2279.2

South to North Water Transfer 78.4 63.9

Poverty alleviation 322.9 374.8 423.5 493.3

Overall development of agriculture 271.8 286.8 337.8 381.7

Comprehensive rural reform 607.9 645.8

Other expenses from agriculture,

forestry, and water conservancy 208.8 287.3

Total 4288.9 6720.4 8129.6 9330.2

Proportion of funds directly used in

agricultural production

55.1 61.2 52.7 51.6

Data source: Financial Yearbook of China of the corresponding year

Note: a small amount of the capital for poverty alleviation and comprehensive rural reform is used in direct

agricultural production, which is ignored here.

According to the field investigation, the fiscal support in various regions, especially in the major

grain producing areas, has played a significant role in the development of agriculture. For instance, the

proportion of local fiscal revenue of Fujin City has been less than 20% of the total fiscal revenue over

the years; in 2013, that proportion was only 14.1% (Table 2-2).

Table 2-2 General Financial Status of Fujin City

Unit: Hundred million yuan, %

Year Total financial revenue Grant from

the higher authority

Proportion of grant

from the higher authority

Public finance

expenditures

2009 12.2 10.6 86.6 12.1

2010 19.3 16.4 85.1 19.2

2011 21.0 17.0 81.0 20.8

2012 26.4 21.6 81.8 26.2

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

19

2013 27.1 23.3 85.9 27.0

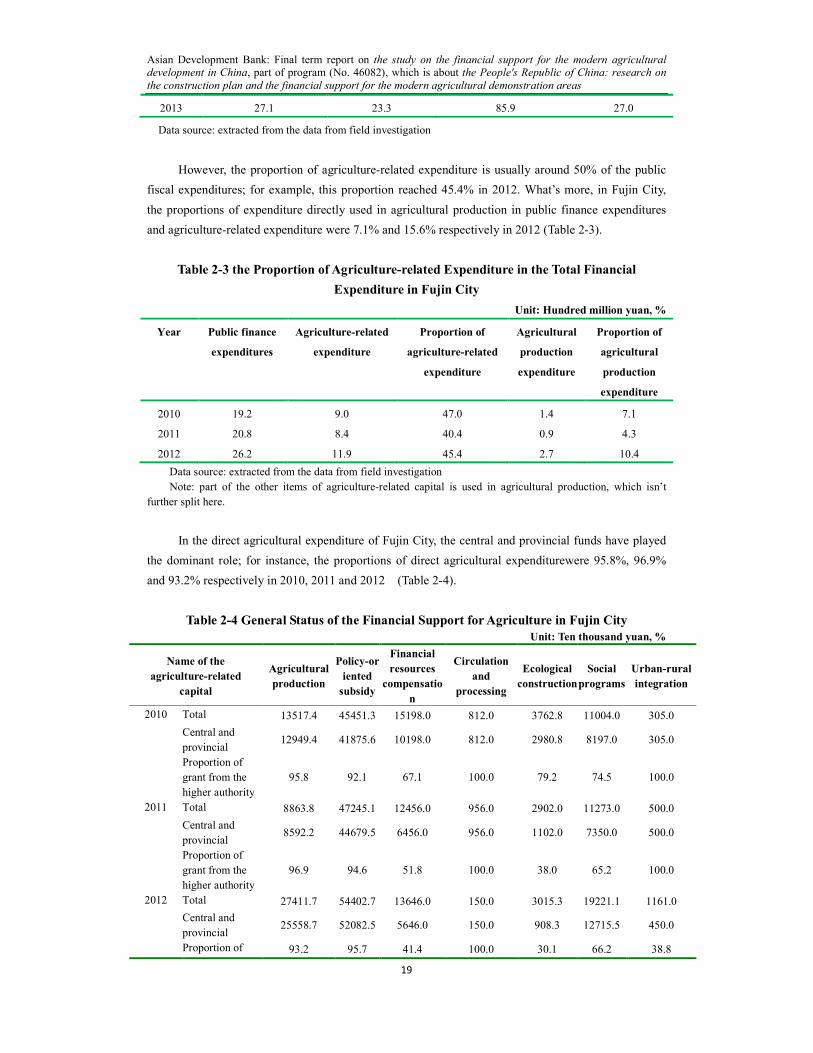

Data source: extracted from the data from field investigation

However, the proportion of agriculture-related expenditure is usually around 50% of the public

fiscal expenditures; for example, this proportion reached 45.4% in 2012. What’s more, in Fujin City,

the proportions of expenditure directly used in agricultural production in public finance expenditures

and agriculture-related expenditure were 7.1% and 15.6% respectively in 2012 (Table 2-3).

Table 2-3 the Proportion of Agriculture-related Expenditure in the Total Financial

Expenditure in Fujin City

Unit: Hundred million yuan, %

Year Public finance

expenditures

Agriculture-related

expenditure

Proportion of

agriculture-related

expenditure

Agricultural

production

expenditure

Proportion of

agricultural

production

expenditure

2010 19.2 9.0 47.0 1.4 7.1

2011 20.8 8.4 40.4 0.9 4.3

2012 26.2 11.9 45.4 2.7 10.4

Data source: extracted from the data from field investigation

Note: part of the other items of agriculture-related capital is used in agricultural production, which isn’t

further split here.

In the direct agricultural expenditure of Fujin City, the central and provincial funds have played

the dominant role; for instance, the proportions of direct agricultural expenditurewere 95.8%, 96.9%

and 93.2% respectively in 2010, 2011 and 2012 (Table 2-4).

Table 2-4 General Status of the Financial Support for Agriculture in Fujin City

Unit: Ten thousand yuan, %

Name of the

agriculture-related

capital

Agricultural

production

Policy-or

iented

subsidy

Financial

resources

compensatio

n

Circulation

and

processing

Ecological

construction

Social

programs

Urban-rural

integration

2010 Total 13517.4 45451.3 15198.0 812.0 3762.8 11004.0 305.0

Central and

provincial 12949.4 41875.6 10198.0 812.0 2980.8 8197.0 305.0

Proportion of

grant from the

higher authority

95.8 92.1 67.1 100.0 79.2 74.5 100.0

2011 Total 8863.8 47245.1 12456.0 956.0 2902.0 11273.0 500.0

Central and

provincial 8592.2 44679.5 6456.0 956.0 1102.0 7350.0 500.0

Proportion of

grant from the

higher authority

96.9 94.6 51.8 100.0 38.0 65.2 100.0

2012 Total 27411.7 54402.7 13646.0 150.0 3015.3 19221.1 1161.0

Central and

provincial 25558.7 52082.5 5646.0 150.0 908.3 12715.5 450.0

Proportion of 93.2 95.7 41.4 100.0 30.1 66.2 38.8

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

20

grant from the

higher authority

Data source: extracted from the data from field investigation

In addition, the fiscal support for agriculture-related financial institutions is almost the same as

that for agricultural production expenditures in Fujin City. The fiscal fund of county level accounts for

less than 20% of the premium subsidy of agricultural insurance, and 25% of the reward for

agriculture-related loan increment of county-level financial institutions (Table 2-5).

Table 2-5 Fiscal Expenditure on Agricultural Finance in Fujin City

Unit: Ten thousand yuan

Year

Award for agriculture-related

loan increment of county-level

financial institutions

Premium subsidy

of agricultural

insurance

2010 Total 2740 513.1

Central and provincial 2054.2 425.2

Proportion of grant from the higher authority 75.0 82.9

2011 Total 256.1 640.5

Central and provincial 192.1 524.8

Proportion of grant from the higher authority 75.0 81.9

2012 Total 563.4 1035.1

Central and provincial 422.5 844.8

Proportion of grant from the higher authority 75.0 81.6

Data source: extracted from the data from field investigation

Note: Fujin City has no new-type rural financial institution, so the financial expenditure doesn’t include the

targeted cost subsidies for new-type rural financial institutions.

2.2.2 Credit

The agriculture-related business of banking industry has been improved in recent years, and the

financial products are becoming richer and richer. At the end of 2013, the agriculture-related loan

balance of banking financial institutions (excluding bills) was 20880 billion yuan with a year-on-year

growth of 18.4%, and was 4.5% higher than the growth rate of other loans during the same period

(Figure 3-3). The capital and financial strength of the rural credit cooperatives has been reinforced

continually, with significant profit growth for nine consecutive years, and its capacity for supporting

agriculture is growing. The three types of new rural financial institutions: the village and town banks,

loan companies and rural fund mutual cooperatives are making continuous development and the

competitiveness of rural financial market is being improved continually. By the end of 2013, the loan

balance of these three institutions was 365.1 billion yuan with a year-on-year growth of 56%. The

financial services have covered all the towns nationwide1.

Taking the year of 2011 as example, the proportion of the loans directly used in agricultural

production in various loans reached 9.84% (Table 2-6).

1 The People’s Bank of China, The financial stability report of China in 2014

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

21

Table 2-6 Rural Loans in RMB and Foreign Currencies of Chinese Financial Institutions

Balance of the

current period

Proportion

in various loans

Increment of

the current

year

Proportion

in various

loans

2011

Agriculture, forestry, animal husbandry,

side-line production and fishery 20220.2 3.54 2587.7 3.29

Fundamental construction of farmland 958.2 0.17 108.9 0.14

Agricultural product processing 5943.6

1.04

1390.1 1.77

Agricultural means of production 3118 0.55 817.7 1.04

Agricultural materials and

circulation of agricultural by-products 6347.4 1.11 585 0.74

Agricultural science and technology 210.2 0.04 20.8 0.03

Rural infrastructure construction 10000.4 1.75 2241 2.85

Subtotal 46798 8.20 7751.2 9.84

Others 73671 12.91 14757.2 18.74

Total 120469 21.10 22508.4 28.58

2012

Agriculture, forestry, animal husbandry,

side-line production and fishery 6699 0.99 888 0.98

Fundamental construction of farmland 1176 0.17 220 0.24

Agricultural product processing 7318 1.08 1110 1.22

Agricultural means of production 3629 0.54 583 0.64

Agricultural materials and circulation of

agricultural by-products 7315 1.08 1001 1.10

Agricultural science and technology 255 0.04 64 0.07

Rural infrastructure construction 11236 1.66 1455 1.60

Subtotal 37628 5.57 5321 5.85

Others 71645 10.60 13647 15.00

Total 109273 16.17 18968 20.85

Data source: Finance Yearbook of China of the corresponding year

As to the accessibility of agricultural financial services, at the end of 2013, there have been 468

rural commercial banks, 122 rural cooperative banks, 1803 rural credit cooperatives and 987 village

and town banks (Table 2-7).

Table 2-7 Outlets of Agriculture-related Financial Institutions at the End of 2012

Name of the institution Number Number of business outlets Number of employees

Rural credit cooperatives 1927 49034 502829

Rural commercial banks 337 19910 220042

Rural cooperative banks 147 5463 55822

Village and town banks 800 1426 30508

Loan companies 14 14 111

Rural fund mutual cooperatives 49 49 421

Total 3274 75896 809733

Data source: CBRC (China Banking Regulatory Commission)

Asian Development Bank: Final term report on the study on the financial support for the modern agricultural development in China, part of program (No. 46082), which is about the People's Republic of China: research on

the construction plan and the financial support for the modern agricultural demonstration areas

22