46359txt 001.pdf, page 29 @ preflight ( untitled )1 chairman’s report 2008/2009 a more challenging...

TRANSCRIPT

ANNUAL REVIEW& Buyers’ Report

2008 - 2009

AGM

The Society’s 135th AGM will be held at The Queen Elizabeth II Conference

Centre, Broad Sanctuary, Westminster, London SW1P 3EE on Thursday,

11th June 2009 at 5.30pm.

Extract from a member’s letter following the 2008 AGM

I am a long-standing member but had not made it to the AGM before. It feltlike a family occasion, unlike other AGMs, but I suppose that is the happyeffect of being mutual. I was impressed by the....open-minded approach toquestions from the floor, and the good participation of all on the platform.

CommitteeRay Bowden Chairman

Sarah Evans Deputy Chairman *Oliver Johnson Chief ExecutiveStephen Bourne *Warren LeamingKatherine Douglas Luke Nunneley*Guy de Froment Michael SchusterGeorge Jeffrey Mike Thompson

*Co-opted members

Executive ManagementOliver Johnson Chief Executive

Liz Cerroti Member Services Sebastian Payne MW BuyingKathryn Harvey Marketing Richard Shorrocks FinanceDavid Marsh Information Systems Peter Styne Operations

David Caunce Company Secretary

Contents of this ReportChairman’s Report 1

Finance Report 14

Wine Buyers’ Report 17

Financial Statements 30

Cover: Award for WineMerchant of the Year,Decanter 2008

Our own delivery fleet outsidethe new loading bay

1

Chairman’s Report 2008/2009

A more challenging year

• As foreseen in last year’s Chairman’s Report, 2008 was a challenging year for the wine trade. The value of the pound fellsharply, duty rates increased by more than inflation, and turmoil in the financial markets led to recession

• Financial market turmoil did, however, bring increased recognition of the strength of the mutual business model

• And, notwithstanding a bigger than expected fall in our cash balances, The Society coped well with the challenges

• Decanter readers voted us ‘Wine Merchant of the Year’, we were International Wine Challenge’s ‘Wine Club of the Year’, and we won several regional wine awards

• At Stevenage, the fourth warehouse was completed on time andto budget, the website facilities were steadily enhanced, and energy efficiency was greatly improved

Extract from the October 2008 issue of Decanter

Everyone seems to have a soft spot for The Wine Society – even those that arenot members of this historic club get misty-eyed when they refer to it.

The year ahead

Economic conditions seem unlikely to improve greatly in the yearahead, but this has been built into our plans, belts have beentightened, and member support remains very strong. Once again,we expect to provide members with high quality, fairly pricedwines, and the highest possible level of service.

A personal note

At the June AGM I will be stepping down as Chairman after 17 years, and I retire from the Committee in June 2010, after 37 years. I will greatly miss my close involvement in this greatorganisation, but succession plans are well in hand and with yourcontinuing support The Society will go from strength to strength.

2

The Society’s mutuality

In the 1996-97 Report, at the time when the demutualisation ofmany Building Societies was in full swing, I commented howlittle the reasons driving that movement (diversification, growthby acquisition, trading with non-members, sourcing new capital,etc) applied to The Society.

A plc aims to maximise profits earned from customers in order tomaximise the dividends paid to a different group of people, theshareholders, and, it seems in some cases in more recent years, topay large bonuses to senior staff.

With the spectacular collapse of many of these demutualisedbusinesses, it is a good time to remind members again of theprecious inheritance of The Society’s mutuality.

Ever since its inception in 1874, The Society has aimed to provideits members with quality wines at all price levels and with thehighest possible level of service. Each member owns one share,only members can buy from The Society, and there are no staffbonuses. There is, thus, no conflict between customer andshareholder, no pressure to maximise profits, and no pressure tojeopardise long-term strategy to protect short-term returns toshareholders, or employees.

The core values of The Society are honesty, vinous authority andindependence, and a real care for members’ interests.

To deliver these values, The Society must be run as efficiently asits most efficient competitor. A report on mutuality by a leadingfirm of accountants a decade ago highlighted the following fouringredients for success.

Protecting, enhancing, and demonstrating the benefits of membership

Identifying the required level of resources and showing that any surplus is usedin members’ interests

Clear and strong management

Educating members to the benefits

Your Committee and Executive strive constantly on all four fronts.Members, we hope, buy as much of their wine from The Societyas possible, and spread the word.

The adverse external factors

These charts summarise the three main challenges faced by thewine trade in 2008. We were impacted by all of them.

Most significantly, as the first chart indicates, the pound has fallendramatically against the euro compared to its stable level of theprevious five years (there was a similar fall against the dollar).Consequently, the sterling cost of wine has increased by about30% and prices across the market have had to rise. This also meansthat for every £1m of wine which we bought before last year, weneed to spend £1.3m to replace it in our stocks when we sell it.

The middle chart shows how Government policy on taxingalcohol has changed. Up until 2008 duty rose in line with theretail prices index (RPI), but in March 2008 the Chancellor raisedduty by more than the RPI and again raised duties in hisemergency budget in November. Although the latter wascounterbalanced by a reduction in the rate of VAT, it wasannounced that the increase will not be reversed when the VATrate reverts to 17.5% later in 2009. Furthermore, the Governmenthas said it will increase duty by inflation plus 2% in future years.

These pressures come at a time when the wine market ismaturing anyway, so it is hardly surprising that, after decades ofgrowth, the total value of UK wine sales has levelled off.

The third chart illustrates the volatile nature of the en primeurmarket. Demand was high in 2001 and 2006, reflecting thepopular 2000 and 2005 vintages, but much lower in 2008.

3

Sterling fell sharply Duty increases v RPI En primeur sales

4

Trading results

A glance at the profit and loss account might lead to theconclusion that 2008/9 was a buoyant trading year rather than achallenging one, with reported turnover of £77.7m comparedwith £62.7m in 2007/8 and a profit of £1.7m.

The numbers, however, reflect the fact that accountingconventions require en primeur sales to be recorded in the yearwhen the wine is delivered, normally two years after members havepurchased it. The financial accounts therefore include the sale ofwines from the highly successful 2005 vintage.

The en primeur wines actually purchased by members in 2008/9were mainly those of the less favoured 2007 vintage (theexceptional 2007 Rhône wines fall into 2009/10), and it is thesethat are included in the internal management accounts, used tomonitor monthly trends and inform decision making.

These accounts showed approximately unchanged sales in theyear, and a small trading loss. The latter was mainly the result oflower en primeur sales, and partly the result of efforts to hold downprices in the face of the ever-declining pound.

In 2009/10, when the 2005 en primeur sales drop out of thefigures, the financial accounts will show a fall in sales, but we willneed to generate the trading surplus required to finance theincreased cost of replacing stock at lower exchange rates.

Wine

With our extensive reserves of older stocks and the quality ofmid-priced wines steadily increasing, there was no shortage of

excellent wines to offer members.

Lists

The four Lists contain the core selectionof our wines and, although manymembers now use the website, we knowthat many also use the Lists as the startingpoint for ordering.

The 70 or so ‘Society’ wines, along with‘The Society’s Exhibition’ range of some

Christmas List 2008

5

45 wines (shown below), continue to play a central role inmembers’ selections. These are excellent wines and we receivemuch appreciative comment on their quality. One of the mostimportant applications of the buyers’ expertise is choosing andblending these wines. They aim to offer, at two price levels, winesthat will not disappoint and which capture the essence of theirorigins. They come from trusted suppliers and their choicereflects teamwork between grower and Society buyer.

The big fall in the value of sterling in 2008 seems to have ledsome retailers to downgrade some of their own-label wines inorder to meet price points. The Society’s position is different: wewill not sell wine that is dull and likely to disappoint.

Fine Wine Lists

These lists have been expanded in order to present a wider rangeof special occasion wines from the classic wine regions of theworld. Prices range from just under £10 up to the most expensiveBordeaux first growths at £250. Members responded well andwere especially attracted to the many mixed cases included.

The Society’s Exhibition…

The Society’s Exhibition wines are from specific vintages and specific suppliers, and thesedetails appear on their labels

Blanc de Blancs ChampagneHaut-MédocPomerol PauillacMargauxSt Aubin RougeSavigny-lès-Beaune Juliénas FleurieCairanne VacqueyrasGigondasChâteauneuf-du-PapeFrench CabernetTuscan RedChianti Classico

Rioja ReservaVictoria Shiraz Margaret River Cab. MerlotCentral Otago Pinot NoirMarlborough Pinot Noir Chilean Merlot Old Vine ZinfandelSonoma Cab. Sauv.St Aubin BlancChablis 1er CruSt Aubin 1er CruPouilly FuméRiesling Hermitage BlancGrüner VeltlinerS African Chenin Blanc

SA Sauvignon BlancTasmanian ChardonnayNew Zealand ChardonnayCasablanca ChardonnaySauternesManzanilla Pasada Viejo Oloroso Sherry Viejo Oloroso Dulce Tawny PortCrusted PortGrande Champagne CognacSingle Speyside MaltSingle Islay MaltSingle Orkney Malt

Wines on the web and by e-mail

The development of The Society’s website continues apace, withincreased information, easy search facilities, and the addition ofwines that are available in volumes too small to justify putting inthe Lists (ends of range, small-scale purchases, minority interestwines, etc).

From time to time, members, identified from their purchasingpatterns, receive emails attracting their attention to wines fromparticular regions. Members can opt out of such emails, but fewdo, and they have generally proved to be very popular.

Wine Without Fuss (WWF) & the Vintage Cellar Plan (VCP)

These schemes are designed to appeal to members who prefer totap in directly to the buyers’ choices. Members receive regulardeliveries for everyday drinking (WWF) or build up ‘cellars’ forfuture drinking (VCP). Information is available in the Lists, on thewebsite, or by calling Member Services.

Regional offers

The buyers travel extensively to source wine for these offers, andit was gratifying that The Society won awards for its selectionfrom Portugal, Chile, and Alsace during the year.

The offers give an overview of the region of origin with winesthroughout the price range. There were 14 such offers last year, aselection of which are illustrated on the opposite page.

To comment on just three of them:

The Portuguese offer in July was associated with a PortugueseWine Dinner in London and an article in SocietyNews by CharlesMetcalfe, including the offer of a new book on Portugal writtenby him and his wife, Kathryn McWhirter.

The Italian Collection was the biggest range of Italian wines wehad ever offered, and resulted from several buyer visits and manycomparative tastings.

The Côtes de Bordeaux Offer presented wines from some of theouter regions of Bordeaux, where value for money had not beenadversely impacted by the fine wine boom associated with thebetter-known Claret communes.

6

7

CA0508

Featuring First Releasesfrom Ridge, Frog’s Leap, Au Bon Climat,Stag’s Leap and Seghesio

CA L I FORN I AThe Society’s selection of the Golden State’s best wines,

from £5.75 to £75 per bottle

South AmericaThe wine world’s most

dynamic continent

• Chile: carmenère comes ofage, superb 2007 sauvignonblancs and the world’s bestvalue pinot noirs

• Argentina’s top wines arebetter value than ever

• Uruguay’s tannat is tamed

For the second consecutive year TheWine Society has been named bestChilean Specialist 2007-2008 by The InternationalWine Challenge.

AM0208

AUSTRALIA’SR E G I O N A L H E R O E S

Our choice of the best wines from the top growers

Includes new releases of Amon-Ra, Penfolds Grange, D’Arenberg Dead Arm, Leeuwin Art Series Chardonnay and Kooyong Pinot Noir

AZ0408 March 2008

JL0708

The Wine SocietyWines of Portugal’s

National Retailer 2008

THE DELICIOUS NEW 2007 VINTAGE AND OUTSTANDING 2004 AND 2006 CHIANTIS AND BAROLOS

IB0808 August 2008

INCLUDES THE SOCIETY’S FIRST RELEASES OF:2005 ORNELLAIA AND SASSICAIA

THE ITALIANCOLLECTION

MM0908

Outstanding winesfrom the South ofFrance: from theDordogne to theCôte d’Azur

TheMagicalMidi

AS0508

A perfect vintage revisited 2005

A L S A C E

B E S T C L A R E T B U Y Sfor 2008

Includes great 2005 buys, aninsider’s tip on 2001 Pomeroland a special collector’s casefeaturing Châteaux Lafleur,L’Evangile and Trotanoy

TC0208 February 2008 BC0208 February 2008

Cru Beaujolais 2006DELICIOUSLY RIPE, SILKY WINES FOR BEAUJOLAIS LOVERS

Society wines Exhibition wines Championship wines

Covers of a sample of theRegional Offers

Illustrations from three ofthe thematic offers

Thematic offers

These are well suited to everyday occasions and seasonal needssuch as parties and gifts. Examples were: Wines for SummerDrinking, The Society Wines and Exhibition Wines, Light Winesfor Summer, Wines for Christmas, Gift Lists, and the very popularWine Championship offer of wines that shone in the annualcomprehensive blind tasting carried out by the buyers.

Investments for the future

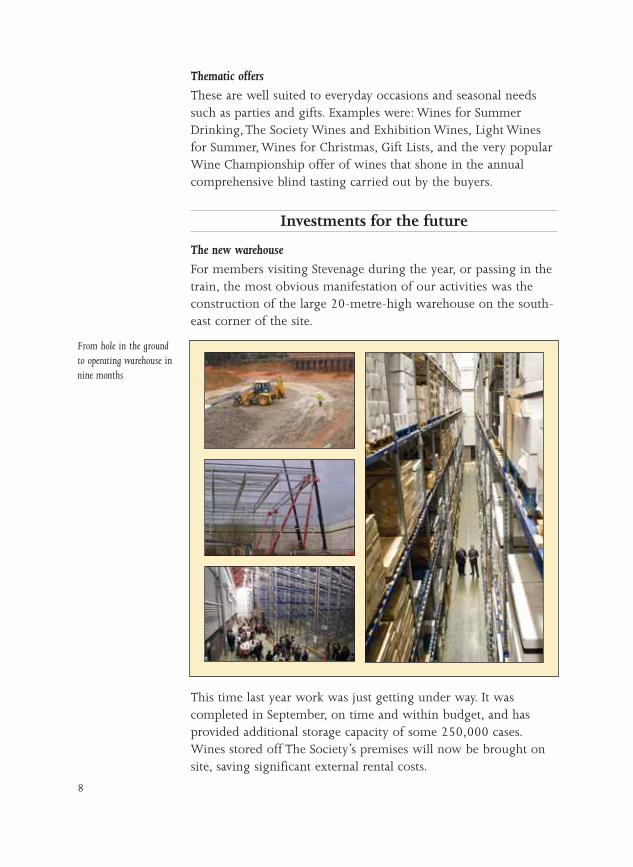

The new warehouse

For members visiting Stevenage during the year, or passing in thetrain, the most obvious manifestation of our activities was theconstruction of the large 20-metre-high warehouse on the south-east corner of the site.

This time last year work was just getting under way. It wascompleted in September, on time and within budget, and hasprovided additional storage capacity of some 250,000 cases.Wines stored off The Society’s premises will now be brought onsite, saving significant external rental costs.

8

From hole in the groundto operating warehouse innine months

The second phase of the project is due for completion in June. Itinvolves relocating some 300,000 cases within the site, theconstruction of a more streamlined bottle picking unit, and animproved despatch system. The result will be greater efficiencyand a capacity to accommodate the gradual growth of The Society.

Energy savings and forest conservation

The detailed attention given to energy saving during the design ofthe new warehouse delivered even better results than weexpected. This led us, with the help of the Carbon Trust, into afull energy survey of the existing buildings. The three resultingprojects will deliver a two-and-a-half-year payback on the£200,000 invested in them.

Keen-eyed members will also have spotted that almost all ourpublications now carry the Forest Stewardship Council logo,reflecting our switch to paper from managed forests and recycledwood fibre.

The website: www.thewinesociety.com

Following a re-launch of the site in 2007, the focus in 2008/9was on improving the existing facilities and adding new ones.There are now some 6,000 pages on the site with wines, winenotes, details of the various services offered by The Society, andarticles giving information on many aspects of wine and winebuying. The economics and facility of this mode ofcommunication enable so much more information both to beconveyed and to be made more easily accessible than is possiblein paper form, though, as noted earlier, we still see an importantrole being played by the printed word.

New and improved facilities include: order tracking, fine wineadvice, a new home page, better navigation and search, a site tour,video content, interactive maps of tasting venues, SocietyNewsarticles, a wish list, paperless direct debit facilities for WWF, VCPand reserves, PDF wine notes, and press articles on The Societyand its wines.

A sample of images from various web pages is shown on thefollowing page.

9

10

Running The Society

Committee

There were 15 meetings of the full Committee during the year,including three half-day strategy sessions at Stevenage. The ChiefExecutive, Deputy Chairman and I also met each month toexchange views and debate topical and strategic issues.

Committee meeting agendas always include the monthly financialreport and a Chief Executive’s report, accompanied by reportsfrom the heads of each department (Finance, Member Services,Marketing, Buying, Operations, and Information Systems). Non-regular items this year included: the development of the website,two in-depth departmental reports, progress reports on the newwarehouse, plans for the subsequent site reorganisation, theFrench shop in Montreuil, The Society’s Pension Scheme, and theimpact of a weakening pound on pricing policy.

The five Subcommittees, each chaired by a different member ofthe Committee, held a further 19 meetings in total. These non-executive Subcommittees discuss issues in more depth.

At the 2008 AGM Stephen Bourne, the Chief Executive ofCambridge University Press, was elected to the Committeefollowing the retirement of John Cruse. Since then Warren

Some images from TheSociety’s website

Leaming, a senior compliance officer, and Guy de Froment, aVice-Chairman of an Investment Management firm, have been co-opted on to the Committee.

Executives and staff

The average number of full-time equivalent staff during the yearwas 199. They report to the six Executives, who in turn report tothe Chief Executive.

More challenging times bring more challenging jobs and it is agreat pleasure to be able to report that the issues arising weretackled energetically and resourcefully by all.

I would like to mention Richard Shorrocks, our Head of Finance,who not only ran the finance function during the year but alsoled the energy conservation initiatives and oversaw the planningaspects associated with the new warehouse.

And three long-serving members of staff retired: Ron Bracey, oneof our cellar team leaders, after 42 years (featured in theNovember news), Michael O’Shea the site maintenance engineerafter 32 years, and David Timperley one of our delivery drivers atthe Warrington depot, after 20 years.

Members

We could not repeat the successful 2007 Summer Open Daybecause the building contractors were on the site, but we planone for 2009 when there will be an opportunity to inspect thenew warehouse and the new bottle picking and despatch areas.

We did, however, meet members at tastings and at the AGM, aswell as at specially convened members’ meetings.

A varied range of tastings was held throughout the country, thelocations of which can be seen from the map on the website.

11

Michael O’Shea David TimperleyRichard Shorrocks

12

Many of these tastings are attended by our suppliers, who greatlyappreciate the opportunity to meet and talk with members, asillustrated by the following extract from a letter received inFebruary 2009.

I knew by experience that London was by far the best place in the world tomeet the greatest number of wine connoisseurs. It once more proved true. Ithoroughly enjoyed the audience [at a Society tasting] and the settingwas just wonderful.

Paul Pontallier, General Director Château Margaux

Members’ meetings, attended by a selection of Committeemembers and management, provide the Committee with regularfeedback on all aspects of The Society’s affairs. These supplementinformation from more formal focus groups and surveys.

One question we are always keen to explore is the extent towhich members relate to The Society as a mutual, sharing a senseof ownership and belonging, rather than just as a favouredsupplier. We find, on average, that at the beginning of a meetingthe split is about 50:50, but by the end it is at least 80:20!Encouragingly, the change stems more from the comments ofmembers present than from what we say.

The other general observation, which often surprises thosepresent, is how differently members use The Society: some forfine wines or everyday wines only, some use only the Lists, othersonly the Offers, some use only the web, and so on.

Sign off

This report is my 17th and last as your Chairman, as I will bestepping down at the AGM in June prior to retiring from theCommittee, under the age rule, in 2010. I joined The Society in1965, was elected to the Committee in 1973, became Treasurer in1976, and Chairman in 1992.

Much has changed since 1973/74 when The Society owned noland or buildings, had an overdraft of £2.5m (in today’s pounds),offered a much narrower range of wines and services, andreceived most of its orders by post.

13

It has been a great privilege to have worked with five ChiefExecutives (Desmond Moseley, Barry Sutton, Ian Ronald, JohnPearmund, and Oliver Johnson), 25 Elected Committee membersand 37 Committee co-optees, the Heads of Departments andseveral hundred members of staff, all dedicated to and caringabout The Society: a true team effort. I also owe particular thanksto my two predecessors, Edmund Penning-Rowsell andChristopher Bradshaw, whose dedication to The Society wasinspirational and from whom I learned so much, and to JohnCruse, the former Deputy Chairman, with whom I worked for 14years as a fellow officer and for 26 years in total.

The Society owes so much to those who laid such strongfoundations in its earliest days, and I often think with someaffection of Mr Robert Brudenell Carter, one of the three foundersof The Society. He was a distinguished ophthalmic surgeon, aleader writer for The Times, and a fellow of The Medical Society ofLondon, the coal cellar of which housed The Society’s first winestocks (no doubt thanks to his connection). He was Treasurer ofthe Society from 1874 to 1895, and Chairman from 1895 to1915. An interesting insight into Victorian attitudes comes fromthe fact that his 23-inch obituary in The Times in 1918 didn’t evenmention his central involvement in The Wine Society!

It is thanks to Mr Brudenell Carter’s account of the origins of The

picture of our early history. Only a minority of members willhave seen this, so we are distributing it, along with the originalstatement of the ‘Object of The Society’ and a Bateman cartoon onthe pleasures of wine, in a leaflet accompanying this AnnualReview.

The greatest pleasure of the job has been getting to know somany members through meetings, tastings, AGMs, andcorrespondence. I have signed over 150,000 individual welcomeletters, corresponded with some 1,500 members, and I haveenjoyed enormously discovering just how congenial andsupportive our membership is.

Thank you for that support and for your encouragement.

R A Y B O W D E N C h a i r m a n

Society, first published in a 1913 List, that we have such a clear

Finance Report

Overview

2008 presented a number of significant challenges for the wineindustry. Most significant was the further depreciation of sterlingagainst the euro and the US dollar: the currencies in which almostall our wine purchases are made. Over the past 18 months or so,sterling has fallen by about 30% against both these currencies. Wehedge our forward purchase commitments in an effort to reducethe exposure to unknown currency variations but, during theyear, the cost of the wine we purchased increased significantly. Atthe same time we faced above-inflation rises in duty on winesand spirits.

As a consequence, and in order to continue to offer to membersthe quality and range of wines they expect from The Society, wehad to increase prices. The fall in the value of sterling was sparkedby turmoil in world financial markets and the recognition that theUK was entering a period of recession. The dual impact of thesefactors meant that the volume of wine purchased by memberswas slightly down on the previous year, though average spend permember was slightly up.

Financial Reporting Standard 5 (FRS5) requires that the sale ofwine is recognised in the financial statements of The Society onlywhen it is ready for delivery to members. Therefore, in any year,our financial statements include not only the sale of day-to-daywine for immediate delivery, but also those wines originally ‘sold’to members en primeur and ready for delivery during the year. Theresults for 2008/9 therefore include not only regular sales tomembers but also the results of the highly acclaimed 2005 enprimeur vintage, making year-on-year comparisons difficult. Afurther complication arises because 2008/9 was a 53 weekperiod, compared to a 52 week period in the previous year.Where relevant, comparative figures in this Finance Report havebeen adjusted for this additional week in arriving at year-on-yearmovements.

14

Profit and Loss account

Turnover for the year was £77.7m, 21% ahead of the prior year,largely reflecting the take-up by members of the 2005 vintage.Gross profit was £13.5m. The gross profit margin fell from 19%last year to 17%, partly as a result of a change in the mix of salesto members and partly due to the higher sterling cost of thewines we bought.

Administrative expenses were 9% ahead of last year, partly due tohigher depreciation, reflecting the increase in fixed assets, andpartly due to higher staff costs, reflecting a higher headcount.However, the bulk of the increase related to establishment costsincluding outside storage, insurance and rent and rates. Theamount included for rates was particularly high compared to theprior year as a consequence of a reassessment this year and arelease of a provision in the accounts for 2007/8.

The figure for “Other income and charges” at £0.35m was muchreduced compared to the prior year principally because bankinterest receivable fell as we used our cash balances, built up overa number of years, in the building and fitting out of the newwarehouse (see Note 4 to the financial statements).

Dividends and taxation

The Committee declared a dividend of 8% and this wastransferred to the accumulated profit and loss account. The Societymade a profit after tax of £1.7m (2007/8 £1.8m) and a retainedprofit of £0.6m (2007/8 £0.75m).

Balance sheet

The balance sheet shows a number of significant changescompared to the prior year reflecting ordinary movements in thebusiness, the building and fit-out of the new warehouse andfactors relating to accounting for the 2005 vintage under FRS5.

Work on warehouse 4 was completed in the year and £4.3m wasadded to fixed assets, including £3.2m for construction worksand £1.1m for fittings and equipment. Other additions to fixedassets during the year included £0.2m on computer equipmentand £0.2m on energy saving initiatives, taking total additions to£4.8m (see Note 7 to the financial statements).

15

The work on the warehouse was paid for out of cash. Cash wasalso used to finance the purchase of additional stocks and inreducing creditors. Consequently total cash and deposits fell from£10.2m in 2008 to £1.8m at 30 January 2009. The sitereorganisation is estimated to cost £1.2m, of which we hadcommitted to £0.7m at the balance sheet date.

Other significant movements in the balance sheet are largelyattributable to accounting for the 2005 vintage, as amounts whichwere previously held in prepayments and accrued income, stock,and in accruals and deferred income were unwound and the salesto members were recognised.

Pensions

There were no material changes in either the defined benefitpension scheme (DB Scheme) or the defined contribution scheme(DC Scheme) during the year. However, we adopted theAmendment to FRS17 which has had an effect on the way inwhich some of the elements of the DB Scheme are valued. TheSociety has chosen not to restate the corresponding amounts forthe previous period, shown in note 12 to the financial statements,as the effect is immaterial.

During the year a triennial actuarial valuation of the DB Schemewas carried out by the Scheme Actuary. This reported a deficit asat 1 February 2008 of £2.3m. With the fall of equity marketssince then, that deficit would be significantly higher if assessedtoday. Agreement has been reached between the Trustees of thePension Scheme and The Society to make good the £2.3m deficitover a period of years in accordance with pension legislation.

As a consequence, The Society made an additional contribution of£0.45m to the DB Scheme just prior to the year end.

Consistent with the prior year, The Society contributed 17.5% ofpensionable salaries to the DB Scheme, while memberscontributed 6%. The Society also contributed £60,000 to the DCScheme in the course of the year (2007/8 £45,000).

S A R A H E VA N S D e p u t y C h a i r m a n

16

Wine Buyers’ Report

Two handicaps have been imposed on wine drinkers during thelast year or so, both unwelcome at a time of worldwide recession.The first is the devaluation of sterling by about 30% against thecurrencies in which we buy most of our wine, the euro and the

US dollar (the latter includesSouth America). Secondly, thesteady increases in excise duty,which will increase tax by 2%above the rate of inflation for thenext four years.

Your buyers have been negotiatinghard with suppliers, many ofwhom are making special effortsto keep custom in the much-valued UK market, even thoughthey can often get better prices

elsewhere. But at the ‘business’ end of wine producing, priceshave increased little over the past decade at the cellar door, andgrowers have little room to manoeuvre unless they make winethat is frankly not worth drinking. There will be some very dismalwines indeed being sold in the UK from outlets that lower theirstandards to the floor. The purpose of wine is to give pleasure, soThe Wine Society will not lower its quality standards, though wewill look for genuine value for money where it can be found.

Three areas that look particularly attractive for value this comingyear are Chile, regional Spain (outside Rioja) and the South ofFrance, particularly Languedoc and Roussillon, but there areexcellent buys to be found in all wine regions as buyers’ regionalcomments suggest below.

S E B A S T I A N P A Y N E M W

Alsace

Johnny Hugel celebrated his 60th vintage in 2008 and, although Ihave tasted little, the indications are very promising. In the

17

The Marqués de Arínzanobarrel cellar at ChiviteWinery in Navarra

meantime, Johnny’s 59th vintage (2007) is exceptional across allstyles and for every grape variety. An offer of the best of these will

be mailed in July. For those less patient, our own-labelwines are all currently 2007s and are excellent, and nowinclude an Exhibition Gewurztraminer from Hugel.

Alsace wines keep extremely well, as those who boughtRolly-Gassmann’s 1990 riesling from the Christmas Listcan testify. Among older vintages, 1998s are now at theirbest, as are those from 2000. The higher acidity of 2001and 2002 means these needed longer to come roundand are not yet at their peak. The 2005s, bathed insunlight, are glorious and most already give muchpleasure, but my wine of the moment is a riesling fromthe slightly forgotten 2004 vintage. It is Josmeyer’s les

Pierrets, the elder brother of the Exhibition Riesling which theymake for us.

M A R C E L O R F O R D - W I L L I A M S

Argentina

2008 is very mixed. Despite extremely difficult weather somesurprisingly attractive wines have been produced. InMendoza, a year’s annual rainfall, 220mm, fell in Marchand was followed by a frost on 17th April. Somevineyards were harvested before the rain and these havemade lovely wines. Only those producers whorigorously sorted the good from the bad have madeacceptable wines. Dominio del Plata, which producesour own-label wine, is an example. Owner andwinemaker Susana Balbo offered some excellent vats ofmalbec from which we blended The Society’s Malbec,which has turned out exceptionally well.

T O B Y M O R R H A L L

Australia

South Australia – despite a record heat-wave at vintage time,2008 was a relatively mild season, suiting white grapes. The realstandout on my trip in November was Clare Valley riesling:

18

Jean Hugel celebrated his60th vintage in 2008

Susana Balbo of Dominio delPlata makes The Society’sArgentine Malbec

aromatically intense, harmonious and, in thewords of Jeffrey Grosset, ‘having the edge’.The current List also covers McLaren Vale andBarossa reds from the brilliant 2006 vintage,which are excellent now.

Western Australia – 2005 cabernet-merlotsare delicious to drink now and we highlyrecommend Margaret River chardonnay fromthe cool 2006 vintage. Leeuwin’s 2006 will

go down as one of the estate’s best.

Victoria – the effects of the devastating bushfires earlier this yearwill be felt by inhabitants for a long time. One small blessing isthat, while vineyards were damaged in the Yarra Valley, themajority of the state’s plantings survived. The fires came within20km of Tahbilk’s old vineyards and winemaker Alister Purbrick isnow facing the prospect of smoke-tainted grapes.

P I E R R E M A N S O U R

Austria

Willi Bründlmayer sets the benchmark for Austrian fine wine. Hemakes our Exhibition Grüner Veltliner, and we have featured arange of his wines over the year. Many members will have methim at our Wine Fair tasting in May and understood why he isone of our favoured Austrian producers. Keep an eye out for moreof his wines over the coming year.

J O A N N A L O C K E M W

Beaujolais

The question of What is Beaujolais? is presently exercising theminds of many growers in this picturesque part of France.Plummeting sales of Nouveau have removed a valuable safetycushion and led to failed businesses and vanishing vineyards. Yetthere are also plenty of growers who, spurred on by the excellent2005 vintage, are making some of the best wines this region hasever produced, though admittedly in a style that might baffletraditional customers.

19

Jeff Grosset: the king ofClare Valley riesling

The cru system does not exist for nothing, and as quality rises, thedifferences between the crus become more marked. FredericBurrier of Beauregard and Guillaume de Castelnau of Louis Jadotboth make outstanding Moulin-à-Vent. As a result of their efforts,it is likely that some of the best vineyards will get premier cru status.

The 2005 vintage has certainly left its mark and the wines todayare getting better and better. Louis Jadot’s single-vineyard Moulin-à-Vents are outstanding in this vintage and offer fantastic value.2006 was almost as good. 2007 is the vintage of the moment:more classic, fruitier and hugely enjoyable. All three Society ownlabels are from 2007 and are strongly recommended.

M O - W

Bordeaux

As this report goes to print, we have yet to make comprehensivetastings of 2008 Clarets. It was a late vintage with most of thebetter growths picking in the October sunshine. The quality of theyear was made by good autumn weather from mid-Septemberonwards. August and early September had been drab and damp, asholidaymakers may remember, though July was dry and fine.There will be considerable disparity between well-placedvineyards and growers who work hard in the vineyard, and thoseless favoured whose grapes ripen later and those who do notprune hard and take care of their vines. The best wines will haveattractive sweet fruit and fat combined with a certain fresh acidityand tannin. There are certain similarities with the late vintagesending in 8: 1998, 1988 and 1978, although enormous progresshas been made in vineyard management in the past 30 years.Prices of more famous classed growths have risen inexorably inrecent years, but we are seeing that the recession is forcing 2008prices down to more reasonable levels.

We already know that 2008 is a very good year for dry whites, aswas 2007, though the crop is 30% smaller. The quantity ofSauternes will be tiny in 2008, so it was lucky for growers thatthe 2007s were so good.

Although I believe the recession should bring a welcomecorrection in pricing classed growths, we should remember thatthe prices of Claret for more modest appellations have remained

20

pretty static for years. We have found some outstanding buys fromhigh achievers in the vineyards of the Côtes (Blaye, Bourg, Franc,Castillon, etc.) and many of these wines have the advantage ofbeing ready to drink earlier than classed growths. 2006, 2005,2004 and 2003 are all looking good.

2004 classed-growth Clarets are progressing well, with fine aromaand balance, and look good value. The hot 2003 vintage wines aresweet and rich though they have less finesse. 2002, 2001 andeven the very fine 2000 vintage need further keeping. 1999 isperfect now. 1998 and many 1995 Clarets still seem young, butthe classic 1996s are starting to show very well. 1997s should bedrunk up and 1990s and 1989s should both be delicious but norush.

Sauternes has enjoyed a wonderful serious of vintages. 2001 isoutstanding, but 2005 and 2007 will be very fine and 2003exceptionally rich.

S P

Burgundy

We reserve judgement of the 2008 until after the spring, whenthe malolactic fermentation is finished.

In 2007, despite a year of varied weather and a harvest that beganvery early at the end of August, the wines are classic in style. Byclassic, I mean a year when ripeness is achieved at moderate levelsof alcohol, 12–13%, and where aromas are intense and lively.2007 has produced fresh, mineral white wines in the style of2004 but with more concentration. Most red wines have a similarfreshness to them, with pure pinot aromas. Yet this would not beBurgundy if there were not a few exceptions. Some red-wineproducers whose vineyards were healthy waited for the pinot toripen further and made quite round and succulent wines. Suchwas the case for Denis Bachelet, Jean-Marie Fourrier and Jean-Marc Vincent. The wines of the Mâconnais are particularlysuccessful: the combination of a warm region and a cooler yearproduced ripe wines but with a welcome freshness.

For red wines, the ripe and succulent 2000 vintage has beendrinking well for a number of years, but the lighter and

21

beautifully fragrant 2001 has begun to sweeten and soften uprecently. The 2003s have turned out muchbetter than expected and most are drinkingwell now. Jean Grivot’s 2003s are sensational;some of the very best of the vintage. They arerich and supported by powerful butcontrolled tannins and may behave like thevery ripe 1949s, the best of which are stilldelicious now. Most 2004s need a year or soto bloom, while the perfect 2005s are so wellbalanced that the more modest wines can beenjoyed now. Most white wines from all butthe most backward producers are drinkable

three or four years from the vintage.

T M

Champagne

‘There’s ever a slip…’ Not so long ago, the fears in Champagnewere about shortages. The plans for extending the area ofproduction go ahead but with falling sales some readjustmentswill have to be made. Quality, though, is at an all-time highthanks to a run of very good vintages and some well-groundedpolicies from the best houses.

If 1996 remains a textbook vintage, there is growing pleasure tobe had from 1998, now coming into its own. As in Burgundy,2002 is a very good vintage for Champagne and so was 2000,with its profile of seduction and charm. Pol Roger and Bollingerare releasing their 2000s this year and both will be offered by TheSociety.

There is of course more to fizz than Champagne and mentionmust be made of Gratien & Meyer in Saumur and Antech inLimoux, which have both responded brilliantly with supportduring the currency devaluation. Both Crémant de Loire andLimoux are outstanding this year.

M O - W

22

Jean Grivot: ‘outstanding2003s’

Chile

The 2008 vintage turned out well in Chile. After one of thecoldest and driest winters for 40 years, spring continued in thesame fashion, with frost in Casablanca on the 7th and 18thOctober, but March and April were a little warmer than usual.

Each year, Chilean producers introduce new varieties or pioneernew regions. This year we have shipped our first sauvignon gris,the pink-skinned, slightly melon-flavoured variant of sauvignonblanc, and our first pinotnoir rosado. Limarí isbecoming the region forchardonnay which istauter and more mineralthan examples fromelsewhere. The Maycaswines are excellent.

The new El Polilla rangeoffers excellent value for money. The wines are also made fromorganically grown grapes and are certified to have been made by asocially responsible company. The documentation was checked bydifferent administrations in at least three countries and held upthe shipment, but the wines are here and are worth the wait!

T M

England

The 2007 English whites and rosés that we are currently offeringfrom Three Choirs vineyard in Newent, Gloucester, are ofexcellent quality. After bumper volumes in 2006, production fromEnglish vineyards in the past two vintages has dropped, but thequality of the wines remains remarkably high and keenly priced.

Mike Roberts in Sussex continues to produce award-winningwhite and rosé sparkling wines. Demand for wine from his 30-acre Ridgeview Estate is now so strong that he buys in grapesproduced under his control from other vineyards in Sussex andKent.

M A R K B U C K E N H A M

23

Right: Vines and cacti of LimariValley, Chile

Germany

2008 is a vintage that has mostly yielded flavourful Kabinettwines with concentrated fruit and racy acidity; these are piquantwines that vastly exceed the expectations we had for them duringa wet September and early October. There are only smallquantities of Spätlesen and Auslesen.

Luckily, The Society and its members bought plenty of the moreabundant and utterly delicious 2007 vintage last year. Many of theestate wines will go on improving in bottle, despite their lowalcohol, for 10–20 years. We have small quantities of wines fromearlier vintages like 2005 to be offered this year which will showhow well riesling ages.

S P

Hungary

Hungary has had a tough time economically recently but its wineindustry is in good shape. Membership of euroland has broughtits challenges, most recently for exports, but it has also broughtenormous benefits. That, coupled with a fine autumn whichseems to have turned an expected sow’s ear into a silk purse,makes this a good time to buy Hungarian wine.

The everyday wines offer fresh, aromatic flavours and are modestin alcohol and price. 2008 could be a great year for the fine sweetwines of Tokaji and we will continue to offer the best from thisrejuvenated region.

We have tasted some superb reds and look forward to introducingthese when the exchange rate is more favourable.

J L

Italy

In a recent offer celebrating the 2005 vintage, I said that all thegreat wine regions of the world had made exceptional wine thatyear except Italy. As with all generalisations, there are some notedexceptions that prove the rule. Barolo and Barbaresco can be verygood indeed in 2005; Sassicaia is outstanding, escaping the rainthat fell in Chianti Classico; Sardinian reds were good, too.

24

2004, however, was a great year in many regions. Brunello diMontalcino, released early this year, is exceptional, as were the

Chianti Classico Riservas and great wines of Piedmont.Allegrini’s Amarone and La Poja are wonderful. 2004 hassimilarities, in terms of balance and ageworthiness, with1999 in those regions, whose wines are now perfect. 2006is looking promising for Chianti Classico and several wineswill appear in the List for the first time this year.

More recently, 2007 was an exceptionally hot, dry vintageproducing ripe, rich reds but noticeably finer than theprevious very hot year, 2003. 2008 also looks goodthroughout Italy but is particularly successful in the south.

Currently, good whites come from Barberani’s Orvieto andPallavicini’s Frascati. For good-value reds, choose 2006 Barbera,2004 Copertino and The Society’s Montepulciano.

S P

Languedoc & Roussillon

A lax approach to viticulture remains all too prevalent in manycircles in the south of France and was definitely the wrong optionin 2008. Most vineyards suffered from rot and mildew and thesouth was no exception. Indeed, many growers here are unusedto such things, took no precautions, and saw their crops wipedout. Conscientious growers, though, are rarely caught out.Holidays were cancelled and growers will never have worked ashard as they did to bring in the 2008 vintage. Some wereunlucky: Faugères, for example, was hit by hail, which greatlyreduced the size of the crop. However, some parts of the Midi sawno rain at all and drought was the problem. A perfect Indiansummer saved the harvest. The first of the 2008 whites and pinksare delicious and easily as good as in 2007. 2008 reds are likelyto be good too, but in the meantime, the 2007 reds, as in theRhône valley, are outstanding. The wine of the moment is therecently launched Society Corbières from the 2007 vintage.

M O - W

25

Franco Allegrini: superbAmarone in Veneto

26

Loire

The Loire has done it again. Against all theodds, our early tastings suggest a good 2008vintage, especially for sauvignon blanc. Thewines have wonderful fresh acidity but withlovely balancing fruit. The reds are deliciouslyforward and fruity.

The Loire has benefited from a run of goodvintages, and this year we will be offeringwines from the past seven:

2002: a fine, elegant, classically styled vintage, with wonderfulharmony and balance. Jacques Pareuil’s Saumur blanc is a snip,even at today’s exchange rate.

2003: delicious, ripe dessert wines; full-bodied, atypically ripe,sweet-fruited reds.

2004: a classic vintage, with Muscadets particularly fine. TryCuvée Centenaire from Chéreau-Carré.

2005: even better for reds than 2003, with succulent ripe fruitand a little more acidity; a fine, riper vintage for whites,producing some excellent top-end sauvignons which are lovelynow. We bought more of the excellent Pouilly-Fumé fromChâteau de Tracy.

2006: another ripe sauvignon vintage, where the top winescombine wonderful almost peachy fruit with fine acidity andtypically modest alcohol. Thierry Merlin Cherrier’s ChêneMarchand – available in bottle or magnum – is wonderfullyseductive now but will keep, too.

2007: unexpectedly good for sauvignon and fruity, forward reds.The sauvignons have lovely fresh acidity and even the ‘little’ wineswill drink well into this year, as will the very good Muscadetsfrom Vinet and Chéreau-Carré.

2008: the joys of an Indian summer: ripe-tasting but freshsauvignon blanc and Vouvray; charming, fruit-driven reds.

J L

The 2007 harvest in theLoire: good for sauvignonand fruity, forward reds

New Zealand

Members are buying more New Zealand wine than before – areflection of the quality and pleasure that these wines bring – and2008 was the biggest harvest ever. This put a great deal ofpressure on wineries, especially in Marlborough. The quality-driven growers with their own winemaking equipment, whowere prepared to select only the ripest sauvignon, made lovelywines. Our tastings havebeen extensive to ensure ourList reflects the bestsauvignons of the vintage,avoiding the many diluteexamples which are aninevitable consequence ofsuch high yields. WitherHills, Hunters, Seresin andDog Point shine in 2008.

New Zealand pinot noir continues to shake up the wine world.We are so convinced of both the quality and regional differencesacross both islands that later this year members will be able tochoose from three Exhibition pinots, from Marlborough,Martinborough and Central Otago.

P M

Port

By the time you receive this review, we should be puttingtogether our 2007 Vintage Port opening offer, due to be mailed inlate summer. This will be the first declared vintage since 2003,and is eagerly awaited. For current drinking, The Society’sExhibition Crusted Port, bottled in 2004, remains excellent valueand is highly recommended.

M B

Portugal

We were delighted at members’ response to our increased activitywith Portugal last year, and we aim to build on that. The Douro isthe leading light, producing fabulous, perfumed wines across all

27

Right: Dog Point vineyards inMarlborough, New Zealand

price levels – from Crasto (which we justcan’t get enough of!) to premium winesfrom both up-and-coming and famoussuppliers. The 2005s are delicious now. TryPassadouro’s for a taste of the old vines thatmake the Douro valley so special.

For everyday, look no further than theAlentejo – you cannot go wrong with DavidBaverstock’s delicious range at Esporão – and

the Ribatejo, where we rate Lagoalva’s easy-drinking red highly.

J L

Rhône

The most important influence in the Rhône is the Mistral, a coldand mostly dry wind that blows from the north. A year when itfails to blow is rarely good; in 2007, it blew in the spring andthen, crucially, throughout September and October, helping tocreate the greatest vintage for a generation. In 2008, whengrowers from Côte-Rôtie to the Ventoux were in a state of despair,the Mistral again returned to save the day. Early tastings arepromising, but few if any of the 2008s will ever match themajesty of 2007.

The vintage of the moment is 2004, largely ignored and caughtbetween the idiosyncrasies of 2003 and power of 2005. TheChâteauneufs, not far behind 2005 but less tannic, are comingout of their shells and are delicious. Syrahs from the north areelegantly poised and perfect now. The wine to drink now isChave’s Saint Joseph Offerus which was picked by all the buyersin a blind tasting in January.

M O - W

South Africa

There’s never been a better time to visit this part of our List. Thepound/rand rate does yo-yo a bit, but has tended to average inour favour in recent months. That, coupled with the fact that theSouth Africans, keen to build their growing market, often selltheir wines in sterling anyway, makes Cape wines exceptionally

28

Treading the grapes atQuinta do Crasto, Portugal

good value. Wine quality has been getting better and better, andvalue for money is hard to beat. Rising stars such as Carl van derMerwe at Quoin Rock/Glenhurst, and Gottfried Mocke at CapeChamonix are showing what can be done with cleaned-upvineyards, well-informed but intuitive winemaking, and aninclusive attitude towards their employees. Old favourites such asMeerlust, Klein Constantia, and Kanonkop are also at the top oftheir game. Kanonkop has swept the board with awards in SouthAfrica over the last year, and we will be offering a selection oftheir wines over the next few months.

J L

Spain

Spanish winemakers are some of the most creative and dynamicin the world. As the overall standard has increased, the less-fashionable regions, like Navarra, Calatayud and Alicante, areoffering outstanding value for money. Here we have extended ourList, and the garnachas from Cruz de Piedra and Malumbres aredelicious now. It is also a good time to buy Rioja; we offer twoexcellent vintages (2004 and 2005) – the crianzas are ready todrink but the reservas are best held for another year or so.

P M

USA

Pinot noir is an increasingly important partof our range, from the delicious, fresh-tastingwines of Oregon – where we cannotrecommend Eric Lemelson’s wines highlyenough – to the generally richer, riper stylesof California. If you missed our Californiaoffer and US tasting this year, look out formore wines as the year progresses.

2005 produced fabulous reds in California,with the richness and concentration one expects in most vintageshere, but with fine balance adding a touch of class, making theseour best-buy tip for 2009/10.

J L

29

Eric Lemelson makesdelicious Oregon pinot noir

30

Financial Statements

P R O F I T A N D L O S S A C C O U N T

for the year ended 30 January 2009

Notes 2008/09 2007/08

£’000 £’000

Turnover 1 77,731 62,716

Less: Value added tax (10,982) (9,109)

66,749 53,607

Cost of sales (53,224) (41,674)

Gross profit 13,525 11,933

Administrative expenses 2 (12,137) (10,969)

Operating profit 1,388 964

Other income and charges 4 354 839

Profit on ordinary activities before taxation 1,742 1,803

Taxation 6 (79) 6

Profit after taxation 1,663 1,809

M E M O R A N D U M O F A P P R O P R I A T I O N

2008/09 2007/08

£’000 £’000

Profit after taxation 1,663 1,809

Dividends appropriated during the period 5 (1,043) (1,060)

Retained Profit 620 749

All operations are continuing.

The accompanying accounting policies and notes form an integral part of these financial

statements.

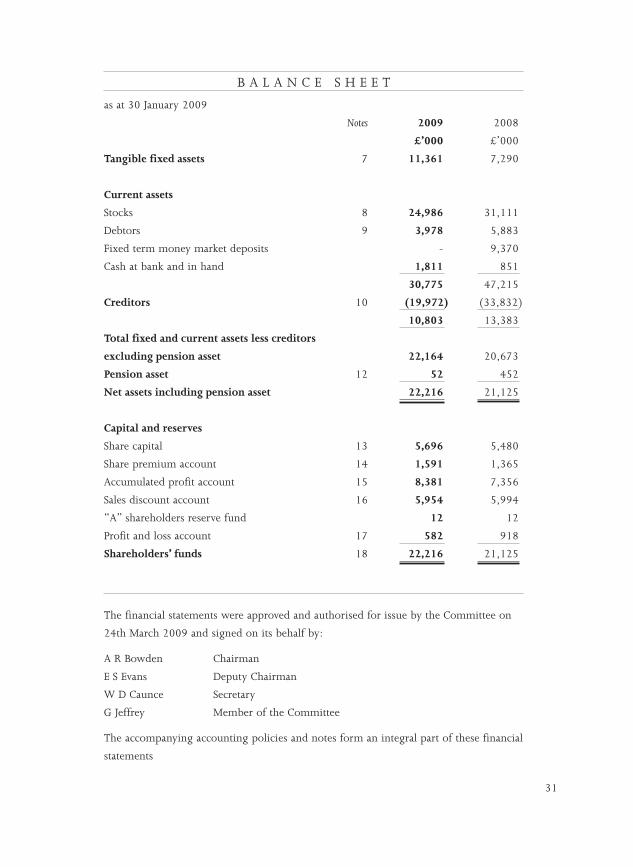

B A L A N C E S H E E T

as at 30 January 2009

Notes 2009 2008

£’000 £’000

Tangible fixed assets 7 11,361 7,290

Current assets

Stocks 8 24,986 31,111

Debtors 9 3,978 5,883

Fixed term money market deposits - 9,370

Cash at bank and in hand 1,811 851

30,775 47,215

Creditors 10 (19,972) (33,832)

10,803 13,383

Total fixed and current assets less creditors

excluding pension asset 22,164 20,673

Pension asset 12 52 452

Net assets including pension asset 22,216 21,125

Capital and reserves

Share capital 13 5,696 5,480

Share premium account 14 1,591 1,365

Accumulated profit account 15 8,381 7,356

Sales discount account 16 5,954 5,994

“A” shareholders reserve fund 12 12

Profit and loss account 17 582 918

Shareholders’ funds 18 22,216 21,125

The financial statements were approved and authorised for issue by the Committee on

24th March 2009 and signed on its behalf by:

A R Bowden Chairman

E S Evans Deputy Chairman

W D Caunce Secretary

G Jeffrey Member of the Committee

The accompanying accounting policies and notes form an integral part of these financial

statements

31

C A S H F L O W S T A T E M E N T

for the year ended 30 January 2009

Notes 2008/09 2007/08

£’000 £’000

Net cash (outflow)/inflow from

operating activities 21 (4,231) 1,280

Returns on investments and servicing of finance

Rent received 77 78

Interest received 227 592

Cash inflow from returns on investments

and servicing of finance 304 670

Taxation

UK tax paid (60) (180)

Capital expenditure

Purchase of tangible fixed assets (4,807) (1,511)

Cash (outflow)/inflow before management of

liquid resources and financing (8,794) 259

Management of liquid resources

Movement out of/(into) money market deposits 9,370 (1,195)

Financing

Shares issued to new members 452 442

Shares cancelled (68) (60)

Net cash inflow from financing 384 382

Increase/(decrease) in cash in the year 22 960 (554)

32

S T A T E M E N T O F T O T A L R E C O G N I S E D G A I N SA N D L O S S E S

for the year ended 30 January 2009

Notes 2008/09 2007/08

£’000 £’000

Profits attributable to members for the year 1,663 1,809

Net actuarial loss relating to the pension scheme 12 (1,061) (543)

Deferred taxation movement on pension

scheme surplus 105 (119)

Total gains recognised since the last

financial statements 707 1,147

N O T E S T O T H E F I N A N C I A L S T A T E M E N T S

for the year ended 30 January 2009

1 Principal accounting policiesThe financial statements have been prepared under the historical costconvention and in accordance with applicable United Kingdom accountingstandards.

The Committee has reviewed the principal accounting policies summarisedbelow and considers, given the requirements of Financial Reporting Standard(FRS) 5, they are the most appropriate for The Society. These policies haveremained unchanged from the prior year with the exception of the changes tothe pension arrangements outlined below.

a) TurnoverTurnover represents all sales to members and is inclusive of Customs andExcise duty and value added tax and is recognised when the goods or servicesare supplied to members.

b) DepreciationDepreciation is provided on all tangible fixed assets, apart from freehold land,at rates calculated to write off the cost less estimated residual value of eachasset, on a straight-line basis, over its expected useful life, which is reviewedannually. The rates used are as follows:

Freehold buildings 2.5 – 10%Equipment, furniture and fittings 10 – 50%Motor vehicles 50%Assets under construction No depreciation

is charged on these assets

33

N OT E S TO T H E F I NA N C I A L S TAT E M E N T S

for the year ended 30 January 2009

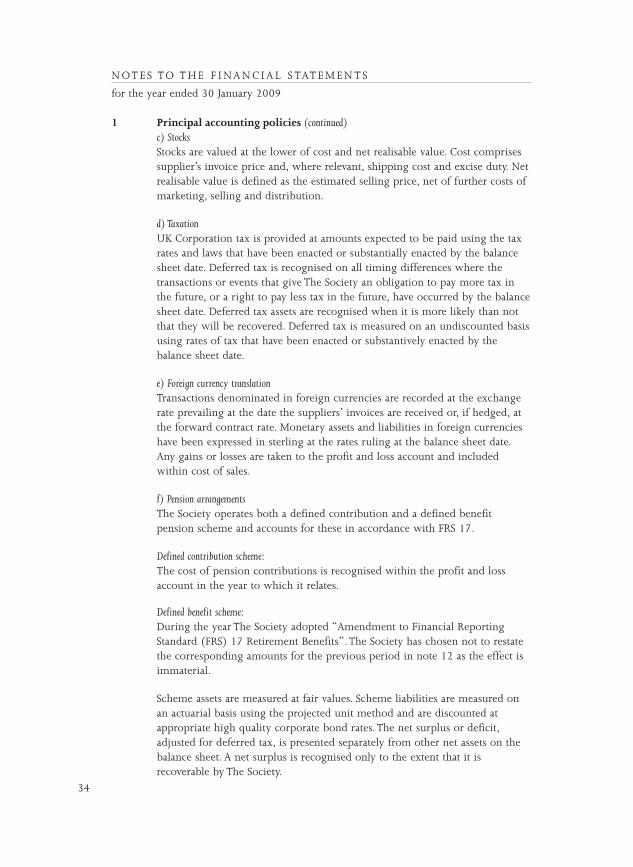

1 Principal accounting policies (continued)c) StocksStocks are valued at the lower of cost and net realisable value. Cost comprisessupplier’s invoice price and, where relevant, shipping cost and excise duty. Netrealisable value is defined as the estimated selling price, net of further costs ofmarketing, selling and distribution.

d) TaxationUK Corporation tax is provided at amounts expected to be paid using the taxrates and laws that have been enacted or substantially enacted by the balancesheet date. Deferred tax is recognised on all timing differences where thetransactions or events that give The Society an obligation to pay more tax inthe future, or a right to pay less tax in the future, have occurred by the balancesheet date. Deferred tax assets are recognised when it is more likely than notthat they will be recovered. Deferred tax is measured on an undiscounted basisusing rates of tax that have been enacted or substantively enacted by thebalance sheet date.

e) Foreign currency translationTransactions denominated in foreign currencies are recorded at the exchangerate prevailing at the date the suppliers’ invoices are received or, if hedged, atthe forward contract rate. Monetary assets and liabilities in foreign currencieshave been expressed in sterling at the rates ruling at the balance sheet date.Any gains or losses are taken to the profit and loss account and includedwithin cost of sales.

f) Pension arrangementsThe Society operates both a defined contribution and a defined benefitpension scheme and accounts for these in accordance with FRS 17.

Defined contribution scheme:The cost of pension contributions is recognised within the profit and lossaccount in the year to which it relates.

Defined benefit scheme:During the year The Society adopted “Amendment to Financial ReportingStandard (FRS) 17 Retirement Benefits”. The Society has chosen not to restatethe corresponding amounts for the previous period in note 12 as the effect isimmaterial.

Scheme assets are measured at fair values. Scheme liabilities are measured onan actuarial basis using the projected unit method and are discounted atappropriate high quality corporate bond rates. The net surplus or deficit,adjusted for deferred tax, is presented separately from other net assets on thebalance sheet. A net surplus is recognised only to the extent that it isrecoverable by The Society.

34

N OT E S TO T H E F I NA N C I A L S TAT E M E N T S

for the year ended 30 January 2009

1 Principal accounting policies (continued)The current service cost and costs from settlements and curtailments arecharged against operating profit. Past service costs are spread over the perioduntil the benefit increases vest. Interest on the scheme liabilities and theexpected return on scheme assets are included in other financeincome/charges. Actuarial gains and losses are reported in the statement oftotal recognised gains and losses. Retirement benefits other than pensions areaccounted for in the same way.

g) Lease agreementsOperating lease rentals are charged to the profit and loss account as incurred.

For assets leased to third parties on operating leases, the lease rentals are takento income on a straight line basis over the term of the lease, and whereappropriate, the asset is depreciated using the straight line method.

h) Financial instrumentsFinancial liabilities and equity instruments are classified according to thesubstance of the contractual arrangements entered into. An equity instrumentis any contract that evidences a residual interest in the assets of the entity afterdeducting all of its financial liabilities.

Where the contractual obligations of financial instruments (including sharecapital) are equivalent to a similar debt instrument, those financial instrumentsare classed as financial liabilities. Whilst The Society’s share capital,accumulated profit and sales discount accounts, attributable to individualmembers, is payable on demand to the member’s estate on their death andthus contains debt characteristics, the overall incidence of such payments issufficiently low and the amount of such payments is sufficiently small toregard the account balances as being substantially equity in nature.

35

N OT E S TO T H E F I NA N C I A L S TAT E M E N T S

for the year ended 30 January 2009

2 Administrative expenses comprise: 2008/09 2007/08

£’000 £’000

Depreciation 736 661

Fees of Committee members:

- Chairman and Deputy Chairman 45 45

- Other Committee members 42 43

Auditor remuneration - audit services 32 27

- other services 16 13

Wages and salaries 4,631 4,240

Social security costs 352 318

Defined benefit pension current service costs 535 551

Defined contribution pension costs 60 45

Establishment costs 1,773 1,332

Other operating costs 3,915 3,694

12,137 10,969

Other services supplied by the auditors related to taxation and accountancyadvice.

3 Employees 2008/09 2007/08

Number NumberThe average number of full time equivalent permanent and temporary employees during the year was: 203 194

2008/09 2007/08

£’000 £’000

Staff costs during the year amounted to:

Wages and salaries – administration 4,631 4,240

Wages and salaries – transport 654 620

Social security costs 403 368

Defined benefit pension current service costs (note 12) 535 551

Defined contribution pension costs (note 12) 60 45

6,283 5,824

Included in administrative expenses 5,578 5,154

Transport staff costs included in cost of sales 705 670

6,283 5,824

36

N OT E S TO T H E F I NA N C I A L S TAT E M E N T S

for the year ended 30 January 2009

4 Other income and charges comprise: 2008/09 2007/08

£’000 £’000

Rent receivable under operating leases 77 78

Bank interest receivable 227 592

Other financial income (note 12) 50 169

354 839

5 Dividends 2008/09 2007/08

£’000 £’000

Transfer to accumulated profit account (note 15) 1,043 1,060

6 Taxation 2008/09 2007/08

£’000 £’000

UK corporation tax at 21% (2007/08: 20%)

based on the taxable profit for the year 63 60

Total current taxation 63 60

Adjustment in respect of prior year - 3

Deferred taxation (note 11) 16 (69)

Taxation charge/(credit) on profit

on ordinary activities 79 (6)

The tax assessed for the period is lower than the applicable rate of corporation

tax in the UK of 21% (2007/08: 20%). The differences are explained as

follows:

2008/09 2007/08

£’000 £’000

Profit before taxation 1,742 1,803

Dividends appropriated to members (1,043) (1,060)

Retained profit before taxation 699 743

Retained profit before tax multiplied by the applicable rate

of corporation tax in the UK of 21% (2007/08: 20%) 147 149

37

N OT E S TO T H E F I NA N C I A L S TAT E M E N T S

for the year ended 30 January 2009

6 Taxation (continued) 2008/09 2007/08

£’000 £’000

Effect of:

Expenses not deductible for tax purposes 4 14

Adjustment for pension contributions allowed,

as opposed to charged (116) (212)

Excess of depreciation and profit on disposal of

assets over capital allowances 27 110

Other adjustments 1 (1)

Total current taxation 63 60

7 Tangible fixed assets

Freehold Equipment,

land and furniture Motor

buildings and fittings vehicles Total

£’000 £’000 £’000 £’000

Cost

25 January 2008 9,168 6,654 6 15,828

Additions 3,174 1,633 - 4,807

Disposals - (113) - (113)

30 January 2009 12,342 8,174 6 20,522

Depreciation

25 January 2008 3,068 5,468 2 8,538

Charge for the year 247 486 3 736

Disposals - (113) - (113)

30 January 2009 3,315 5,841 5 9,161

Net book value

30 January 2009 9,027 2,333 1 11,361

25 January 2008 6,100 1,186 4 7,290

Freehold land and buildings include land at a cost of £2,422,000 (2008: £2,422,000)

which has not been depreciated. In the prior year assets under construction, included

within freehold land and buildings, at a cost of £540,000 were not depreciated.

38

N OT E S TO T H E F I NA N C I A L S TAT E M E N T S

for the year ended 30 January 2009

8 Stocks 2009 2008

£’000 £’000

Stocks consist of goods purchased for resale,

held as follows:

In bond and overseas 23,531 29,808

Duty paid 1,455 1,303

24,986 31,111

9 Debtors 2009 2008

£’000 £’000

Trade debtors 288 624

Deferred tax asset (note 11) 41 57

Other debtors 216 130

Prepayments and accrued income 3,433 5,072

3,978 5,883

10 Creditors 2009 2008

£’000 £’000

Payments received on account from members 1,492 1,487

Trade creditors 2,892 5,769

Corporation tax 63 60

Other taxes and social security 1,750 2,555

Accruals and deferred income 13,775 23,961

19,972 33,832

11 Provisions for liabilities and charges 2009 2008

£’000 £’000

Deferred taxation at 22% (2008: 21%) is

fully provided in the accounts as follows:

Accelerated capital allowances (31) (47)

Short term timing differences (10) (10)

Included in debtors (note 9) (41) (57)

The movement in the provision during the year of £16,000 was charged to

the profit and loss account. In 2007/08 £69,000 was credited to the profit

and loss account (see note 6).

39

N OT E S TO T H E F I NA N C I A L S TAT E M E N T S

for the year ended 30 January 2009

12 Pension schemes

Defined contribution scheme

Since January 2007, employees have been offered membership of The Society’s

stakeholder pension plan, a defined contribution scheme. During the year The

Society paid £60,000 (2007/08: £45,000) into the scheme. There were no

outstanding or prepaid contributions at the balance sheet date.

Defined benefit scheme

The Society operates a defined benefit pension scheme for the benefit of

employees. The scheme’s funds are administered by Trustees and are

independent of The Society’s finances. Contributions are paid to the scheme in

accordance with the recommendations of an independent actuarial adviser. The

scheme is closed to new entrants.

A full actuarial valuation of the scheme was carried out as at 1st February

2008, which is currently being finalised. The valuation indicates a scheme

deficit of £2.3m.

The scheme data from the valuation was updated at 30 January 2009 by an

independent qualified actuary in accordance with FRS 17. Under FRS 17,

which is calculated on a different basis to the full actuarial valuation, the

scheme has a surplus of £0.07m.

The major assumptions used for the actuarial valuation were:

2009 2008 2007

Salary growth 4.8% 5.1% 4.6%

Pension increases

Pre 1997 service 3.0% 3.0% 3.0%

1997 to 2005 service 3.7% 3.5% 3.1%

Post 2005 service 2.4% 2.3% 2.2%

Discount rate 6.8% 5.9% 5.2%

Price inflation 3.8% 3.6% 3.1%

Life expectancy of male aged 65

at the accounting date 23.0 years 22.8 years 21.0 years

Life expectancy of male aged 65,

20 years after the accounting date 26.0 years 25.9 years 22.1 years

The actuarial tables used for life expectancy were Pna00 medium cohort with

an underpin of 1.5% for future improvements.

40

N OT E S TO T H E F I NA N C I A L S TAT E M E N T S

for the year ended 30 January 2009

12 Pension scheme (continued)

The expected rate of return on the scheme assets and their distribution

were:

2009 2009 2008 2008 2007 2007

Expected Fair value Expected Fair value Expected Fair value

Return £’000 Return £’000 Return £’000

(pa) (pa)

Equities 6.5% 9,807 6.5% 10,268 6.5% 11,084

Corporate Bonds 6.8% 2,476 5.9% 2,808 5.2% 774

Gilts 4.5% 2,574 4.5% 3,163 4.5% 1,662

Cash 2.1% 900 4.5% 1,125 5.5% 2,508

AVCs 6.8% 138 5.9% 149 5.2% 154

15,895 17,513 16,182

The current allocation of the scheme assets is

as follows:

2009 2008 2007

Equity instruments 62% 59% 68%

Debt instruments 32% 34% 15%

Other 6% 7% 17%

100% 100% 100%

To ascertain the assumptions for the expected long term rate of return on assets, TheSociety considered the current level of expected returns on risk free investments(primarily Government bonds), the historical level of the risk premium associated withthe other asset classes in which the portfolio is invested and the expectations for futurereturns of each asset class.

The amount recognised in the balance sheet is as follows:

2009 2008 2007

Fair value of scheme assets 15,895 17,513 16,182

Present value of scheme

liabilities (15,828) (16,941) (16,175)

Surplus 67 572 7

Related deferred tax liability (15) (120) (1)

Net asset 52 452 6

41

N OT E S TO T H E F I NA N C I A L S TAT E M E N T S

for the year ended 30 January 2009

12 Pension scheme (continued)

During the year, contributions by The Society of £1.041m (2007/08: £1.490m) were

made to the scheme including an additional contribution of £0.45m. The contributions

during the year were 17.5% of pensionable salary and it is expected that future

contributions will be at a rate of 18.5% of pensionable salaries plus any additional

deficit contributions as agreed between The Society and the Trustees of the scheme.

Amount charged to operating profit:

2008/09 2007/08

£’000 £’000

Employer’s part of current service cost 535 551

Included in finance income:

2008/09 2007/08

£’000 £’000

Expected return on scheme assets 1,059 1,021

Interest on pension scheme liabilities (1,009) (852)

Net credit to finance income 50 169

Net amount charged to the profit and loss account 485 382

Changes in the present value of the defined benefit obligation are as

follows:

2008/09 2007/08

£’000 £’000

Opening defined benefit obligation 16,941 16,175

Employer’s part of current service cost 535 551

Interest cost 1,009 852

Contributions from scheme members 197 191

Actuarial gain (FRS 17 discount rate

higher than expected) (2,431) (491)

Benefits paid (423) (337)

Closing defined benefit obligation 15,828 16,941

42

N OT E S TO T H E F I NA N C I A L S TAT E M E N T S

for the year ended 30 January 2009

12 Pension scheme (continued)

Changes in the fair value of the scheme assets are as follows:

2008/09 2007/08

£’000 £’000

Opening fair value of scheme assets 17,513 16,182

Expected return on scheme assets 1,059 1,021

Actuarial loss (actual return less expected return) (3,492) (1,034)

Contributions by The Society 1,041 1,490

Contributions by scheme members 197 191

Benefits paid (423) (337)

Closing fair value of scheme assets 15,895 17,513

The actual return on the scheme assets over the year was a loss of £2.433m

(2007/08: loss of £0.013m). The amount recognised outside the profit and

loss account in the statement of total recognised gains and losses for 2008/09

is a loss of £1.061m (2007/08: loss of £0.543m). The cumulative amount

recognised outside the profit and loss account at 30 January 2009 is a loss of

£4.94m.

The funding position of the scheme at 30 January 2009 and the previous

four years is as follows:

2009 2008 2007 2006 2005

£000 £000 £000 £000 £000

Fair value of scheme

assets 15,895 17,513 16,182 14,082 10,509

Present value of defined

benefit obligation (15,828) (16,941) (16,175) (16,013) (13,084)

Scheme surplus/

(deficit) 67 572 7 (1,931) (2,575)

As permitted under the amended Financial Reporting Standard (FRS) 17, The

Society has chosen not to restate the corresponding amounts for the fair value

of the assets in the previous periods as the effect is immaterial; the assets for

these periods are stated at market value.

43

N OT E S TO T H E F I NA N C I A L S TAT E M E N T S

for the year ended 30 January 2009

12 Pension scheme (continued)

The history of experience adjustments has been:

2008/09 2007/08 2006/07 2005/06 2004/05

Experience adjustments on scheme assets:

Amount of actuarial (loss)/gain

(£’000) (3,492) (1,034) 314 1,426 381

Percentage of scheme assets (22%) (6%) 2% 10% 4%

Experience adjustments on

scheme liabilities:

Amount of (loss)/gain (£’000) (95) - - 434 (11)

Percentage of the present value

of the Scheme liabilities (1%) - - 3% (0%)

13 Share capital 2009 2008

£’000 £’000

25 January 2008 5,480 5,270

Additions 226 221

5,706 5,491

Cancellation of shares (10) (11)

30 January 2009 5,696 5,480

Representing Number Number

“A” shares of £20 each 18,569 18,605

“B” shares of £20 each 266,202 255,406

284,771 274,011

14 Share premium account 2009 2008

£’000 £’000

25 January 2008 1,365 1,144

Share premium additions to share capital 226 221

30 January 2009 1,591 1,365

44

N OT E S TO T H E F I NA N C I A L S TAT E M E N T S

for the year ended 30 January 2009

15 Accumulated profit account 2009 2008

£’000 £’000

25 January 2008 7,356 6,313

Cancellation of shares (18) (17)

7,338 6,296

Dividends appropriated from the profit

and loss account 1,043 1,060

30 January 2009 8,381 7,356

16 Sales discount account 2009 2008

£’000 £’000

25 January 2008 5,994 6,026

Cancellation of shares (40) (32)

30 January 2009 5,954 5,994

17 Profit and loss account 2009 2008

£’000 £’000

25 January 2008 918 831

Actuarial losses recognised (net of deferred taxation) (956) (662)

Profit after taxation 1,663 1,809

Dividends appropriated in the period (1,043) (1,060)

30 January 2009 582 918

18 Reconciliation of movement 2009 2008

in shareholders’ funds £’000 £’000

Retained profit for the year 620 749

Dividends appropriated 1,043 1,060

1,663 1,809

New shares issued - nominal value 226 221

- share premium 226 221

Cancellation of shares (68) (60)

Opening shareholders’ funds 21,125 19,596

Actuarial losses recognised (net of deferred taxation) (956) (662)

Closing shareholders’ funds 22,216 21,125

45

N OT E S TO T H E F I NA N C I A L S TAT E M E N T S

for the year ended 30 January 2009

19 Operating leases

During the year, The Society paid £203,000 (2007/08: £178,000) in respect

of operating leases, all of which related to motor vehicles and office

equipment.

At 30 January 2009 The Society had annual commitments under non-

cancellable operating leases as follows which expire:

2009 2008Motor Motor

vehicles and vehicles andoffice office

equipment equipment

£’000 £’000

Within one year 107 10

Between one and five years 79 163

186 173

20 Foreign currency purchase commitments

At the balance sheet date The Society had outstanding forward currency

purchase commitments amounting to

£12,050,000 (2008: £8,290,000).

21 Reconciliation of operating profit 2008/09 2007/08

to net cash flow from operating activities £’000 £’000

Operating profit 1,388 964

Depreciation 736 661

Decrease/(increase) in stocks 6,125 (8,390)

Decrease in debtors 1,889 2,904

(Decrease)/increase in creditors (13,863) 6,080

Excess of employer pension contributions

paid over charge to profit (506) (939)

Net cash (outflow)/inflow from

operating activities (4,231) 1,280

46

N OT E S TO T H E F I NA N C I A L S TAT E M E N T S

for the year ended 30 January 2009

22 Analysis and reconciliation of net funds 2008/09 2007/08

£’000 £’000

Cash at bank and in hand 851 1,405

Fixed term money market deposits 9,370 8,175

Net funds at beginning of year 10,221 9,580

Increase/(decrease) in cash in the year 960 (554)

Movement in fixed term money market deposits (9,370) 1,195

Change in net funds resulting from cash flows (8,410) 641

Net funds at end of year 1,811 10,221

Represented by

Cash at bank and in hand 1,811 851

Fixed term money market deposits - 9,370

Net funds at end of year 1,811 10,221

47

C O M M I T T E E ’ S R E S P O N S I B I L I T I E S