4q 2015 newsletter

DESCRIPTION

ÂTRANSCRIPT

————————————————————————————————————————————–————

Securities offered through Cetera Financial Specialists LLC (doing insurance business in CA as CFGFS Insurance Agency), member FINRA/SIPC. Advisory ser-

vices offered through Cetera Investment Advisers LLC. Cetera entities are under separate ownership from any other named entity.

HOLISTIC NEWS

“Wealth is the ability

to truly experience

life. “

- Henry David

Thoreau

In This Issue

• Economic Overview

• Special Topic: Social

Security

• Important Notes

• 2016 Office Holidays

What’s New at Holistic Wealth Advisors January 2016

HWA Raises $4,000 for St. Catherine’s Center for Children

For many years, the HWA family of staff and clients have generously

donated money and items to the needy children living in orphanages

in Serov, Russia. As many of you know, Stacy and Sam’s children

were adopted from this orphanage just 6 years ago. With the recent

closing of adoptions between the US and Russia, we have found

ourselves searching for a new charitable endeavor to direct our

donations. We are very excited to announce that we are now

partnering with St. Catherine’s Center for Children in Albany, NY.

Its mission is to offer services, treatment, and education to the most

at-risk children in our local communities in order to heal and

preserve their family lives. It operates several shelters in the area

including the Copson House on New Scotland Avenue in Albany for

children ages 6-13.

In December, HWA clients generously embraced this organization with donations totaling

$2,000. HWA provided a 100% match to these donations and were very pleased to present

Bill Gettman and Joanne Morehouse of St. Catherine’s with a check for an additional $2,000.

We look forward to continuing our support of St. Catherine’s throughout the year with

donations of our time and hearts. We hope you will join us in continuing to support this

wonderful organization.

About St. Catherine’s

Dear Friends:

No child should be abused and neglected. No family should be left without a home, or the

fundamental resources needed to survive. No student should go to school without the hope of

learning the skills necessary to succeed in life.

We all agree—these are critical social issues that must be addressed to make our families

healthier and our communities stronger.

St. Catherine’s Center for Children has been serving the Capital Region since 1886, offering

programs and services that address the challenges our children and families face. For those

who depend on us, life is frequently a struggle. We are committed to helping families find

answers to those struggles.

- Bill Gettman, Executive Director

Bill Gettman, Executive Director

of St. Catherine’s, addresses HWA

clients.

Congratulations

Dianna Manger

as the 2015 Raffle

Winner!!

2016 Referral

Raffle Contest!!

For each referral you send to

HWA you will be entered into

our end of year raffle draw-

ing for a $100 gift card!

Do you have a friend,

neighbor, colleague, or

family member that is:

- Retiring?

- Moving?

- Tired of D.I.Y.?

- Ready to invest?

- In need of professional

wealth & retirement

planning?

- If so, please forward

our office number and

email or call our office

with your referral infor-

mation. We will gladly

set up an appointment

and review their person-

al situation.

ECONOMIC UPDATE - Dr. David Kelly

Growth In its final estimate of 3Q 2015 GDP, the BEA showed the U.S. economy expanding at a 2.0%

q/q saar pace. The underlying data show a larger inventory overhang than initially estimated, leading to a

modest revision downward from the second estimate. Inventory accumulation in the first half of the year

deducted 0.7% from 3Q growth, revised up from the initial -1.4% estimate. However, the lower-than-

expected negative impact from inventory accumulation means a stronger headwind to future growth as

the pace of inventory accumulation returns to average levels. Consumption remained strong in 3Q, with

consumer expenditures up 3.0% y/y following a 3.6% increase in 2Q.

Jobs The unemployment rate was unchanged at 5.0% in November. However, payroll additions of 211k,

upward revisions to the prior two months' job gains and an October job openings number of 5.5 million

(the second highest number on record) suggest even further tightening than indicated by the headline

rate. The employment situation allowed the Fed to raise rates last week, and strong aggregate demand in

the economy relative to anemic supply suggests that unemployment will likely fall faster than the Fed

anticipates in 2016.

Profits As the earnings season comes to a close, two of the major themes this year, falling energy prices

and a high U.S. dollar, certainly continued to take a bite out of earnings. Our estimate for y/y S&P 500

earnings per share in 3Q has now fallen 15.2%, but ex-energy has risen by 1.9%. The high dollar has hurt

foreign sales, with only 35% of companies beating revenues estimates. Looking ahead into 2016, these

themes should continue to play out, but the hit from low prices should begin to roll off and lead to

stronger earnings growth.

Inflation Headline consumer prices remained flat in November, in line with consensus expectations,

pulled lower by declining oil and food prices. Headline inflation is now up 0.5% from November 2014,

while the energy index is down 14.7% in the same time. Core CPI inflation increased to 2.0% y/y growth

and improved by 0.1% m/m. With the drag from energy prices set to fade in early 2016, headline inflation

should also move closer to the Fed's 2.0% mandate in the medium term.

Rates The Federal Reserve signaled its confidence in the strength of the U.S. economic recovery by

raising short-term interest rates 0.25% last week. The move was a unanimous decision by the voting

members of the Committee, and it ends seven years of near-zero interest rate policy. The rate increase

had been well communicated to the investing community, so the market reaction to the announcement

was positive, with stocks rallying and Treasury yields remaining relatively stable. But now that the hurdle

of the first rate increase has passed, markets must refocus on the Fed’s expectation for the path of

further interest rate increases.

Risks

- Volatility caused by faster-than-anticipated path of interest rate increases.

- Concerns about a slowing Chinese economy and its ripple effects on emerging markets.

- Deflation worries in other developed economies outside of the U.S.

- Volatility caused by sharp swings in commodity prices and exchange rates.

* Data as of January 4, 2016 - Article provided by JP Morgan

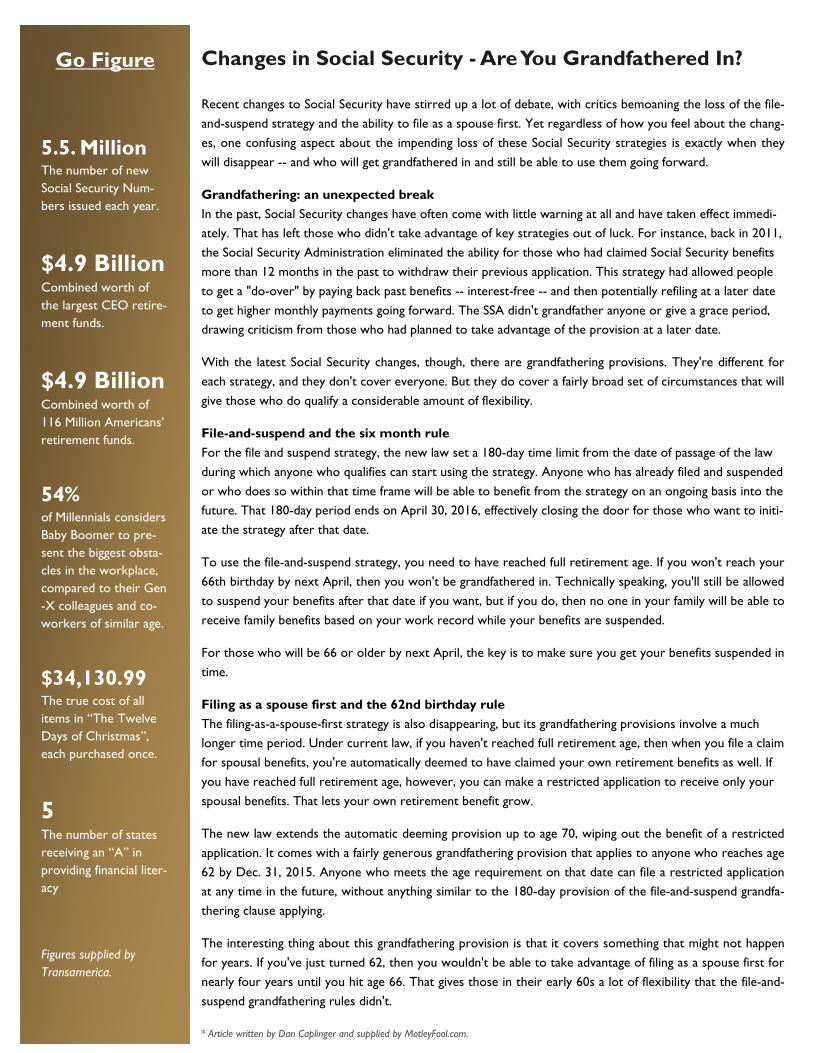

Go Figure

5.5. Million The number of new

Social Security Num-

bers issued each year.

$4.9 Billion Combined worth of

the largest CEO retire-

ment funds.

$4.9 Billion Combined worth of

116 Million Americans’

retirement funds.

54% of Millennials considers

Baby Boomer to pre-

sent the biggest obsta-

cles in the workplace,

compared to their Gen

-X colleagues and co-

workers of similar age.

$34,130.99 The true cost of all

items in “The Twelve

Days of Christmas”,

each purchased once.

5 The number of states

receiving an “A” in

providing financial liter-

acy

Figures supplied by

Transamerica.

Changes in Social Security - Are You Grandfathered In?

Recent changes to Social Security have stirred up a lot of debate, with critics bemoaning the loss of the file-

and-suspend strategy and the ability to file as a spouse first. Yet regardless of how you feel about the chang-

es, one confusing aspect about the impending loss of these Social Security strategies is exactly when they

will disappear -- and who will get grandfathered in and still be able to use them going forward.

Grandfathering: an unexpected break

In the past, Social Security changes have often come with little warning at all and have taken effect immedi-

ately. That has left those who didn't take advantage of key strategies out of luck. For instance, back in 2011,

the Social Security Administration eliminated the ability for those who had claimed Social Security benefits

more than 12 months in the past to withdraw their previous application. This strategy had allowed people

to get a "do-over" by paying back past benefits -- interest-free -- and then potentially refiling at a later date

to get higher monthly payments going forward. The SSA didn't grandfather anyone or give a grace period,

drawing criticism from those who had planned to take advantage of the provision at a later date.

With the latest Social Security changes, though, there are grandfathering provisions. They're different for

each strategy, and they don't cover everyone. But they do cover a fairly broad set of circumstances that will

give those who do qualify a considerable amount of flexibility.

File-and-suspend and the six month rule

For the file and suspend strategy, the new law set a 180-day time limit from the date of passage of the law

during which anyone who qualifies can start using the strategy. Anyone who has already filed and suspended

or who does so within that time frame will be able to benefit from the strategy on an ongoing basis into the

future. That 180-day period ends on April 30, 2016, effectively closing the door for those who want to initi-

ate the strategy after that date.

To use the file-and-suspend strategy, you need to have reached full retirement age. If you won't reach your

66th birthday by next April, then you won't be grandfathered in. Technically speaking, you'll still be allowed

to suspend your benefits after that date if you want, but if you do, then no one in your family will be able to

receive family benefits based on your work record while your benefits are suspended.

For those who will be 66 or older by next April, the key is to make sure you get your benefits suspended in

time.

Filing as a spouse first and the 62nd birthday rule

The filing-as-a-spouse-first strategy is also disappearing, but its grandfathering provisions involve a much

longer time period. Under current law, if you haven't reached full retirement age, then when you file a claim

for spousal benefits, you're automatically deemed to have claimed your own retirement benefits as well. If

you have reached full retirement age, however, you can make a restricted application to receive only your

spousal benefits. That lets your own retirement benefit grow.

The new law extends the automatic deeming provision up to age 70, wiping out the benefit of a restricted

application. It comes with a fairly generous grandfathering provision that applies to anyone who reaches age

62 by Dec. 31, 2015. Anyone who meets the age requirement on that date can file a restricted application

at any time in the future, without anything similar to the 180-day provision of the file-and-suspend grandfa-

thering clause applying.

The interesting thing about this grandfathering provision is that it covers something that might not happen

for years. If you've just turned 62, then you wouldn't be able to take advantage of filing as a spouse first for

nearly four years until you hit age 66. That gives those in their early 60s a lot of flexibility that the file-and-

suspend grandfathering rules didn't.

* Article written by Dan Caplinger and supplied by MotleyFool.com.

Newsletter Courtesy

of Your Holistic Team

Stacy Clifford

Lakshmi Nagarajan

Sarah Blass

Sam Clifford

Raymond Kidalowski

Cynthia Anslow

Sue Donovan

Terence Ruso

H. Paul Thomas

Lillian Helmedach

Rita Young

Sue Miniter

2016 - Important Dates

Your financial account custodians will send your tax documents by these dates:

1099–R : 1/31/16

1099 Tax Package : 1/31/16 - 3/17/16

Form 1099 Revisions: Mid-March 2016

5498: 5/31/16

* Please note most 1099 packets will not be mailed out until the end of February.

2016 - Office Holidays

Please note our office will be closed on the following days:

1/18 - Martin Luther King

2/15 - President’s Day

3/25 - Good Friday

5/30 - Memorial Day

7/4 - Independence Day

9/5 - Labor Day

11/24 & 11/25 - Thanksgiving

12/26 - Christmas Observance

1/2/17 - New Year’s Day

Contact Us Please contact our main office for more information about our services

Holistic Wealth Advisors

19 Clifton Country Road

Suite 3B

Clifton Park, NY 12065

(518) 357-3858

www.holisticwealthny.com