4q10 disclosure and results

TRANSCRIPT

1March 22, 2011

Earnings Release Conference Call– 4Q10

Agenda

Ricardo Ribeiro Gontijo

Roberto Senna

CEO

4Q10 Highlights

Operating Highlights

2

COO

Carlos Wollenweber

CFO | IR

Operating Highlights

Financial Highlights

4Q10 Highlights

� Direcional announces launches and sales record in 4Q10

We launched a PSV (% Direcional) of R$ 415 million. Two projects in the segment of 0-3 minimum wages, with a total PSV of

R$ 190 million, two projects in Manaus with PSV of R$ 96 million, a new project in Belo Horizonte with PSV of R$ 87 million

and a new project in Porto Velho with PSV of R$ 42 million. Contracted Sales (% Direcional) were R$ 406 million,

representing a 38% of Sales Over Supply.

� Projects of 0-3 Minimum Wage (Minha Casa, Minha Vida Program)

Bairro Carioca Project in the City of Rio de Janeiro, with PSV of R$ 114.2 million and 2,240 units, and Jardim Alterosa Project,

in Ribeirão das Neves, with PSV of R$ 75.4 million and 1,640 units. Direcional hired in the year a total PSV of R$ 380 million

and 7,391 units.

3

and 7,391 units.

� Follow on

In February of 2011 we successfully completed our primary and secondary offering of 28 million shares. The net inflow of

cash for the company was R$ 223 million, which guarantees the support of healthy growth for next years, increases

significantly our daily float and increases our visibility and coverage by analysts. Today we have seven banks covering the

Company.

� Management Team

4 Q10 - Human Resources Director of and Regional Superintendents of SP / RJ and DF / RO / PA

Operating Highlights

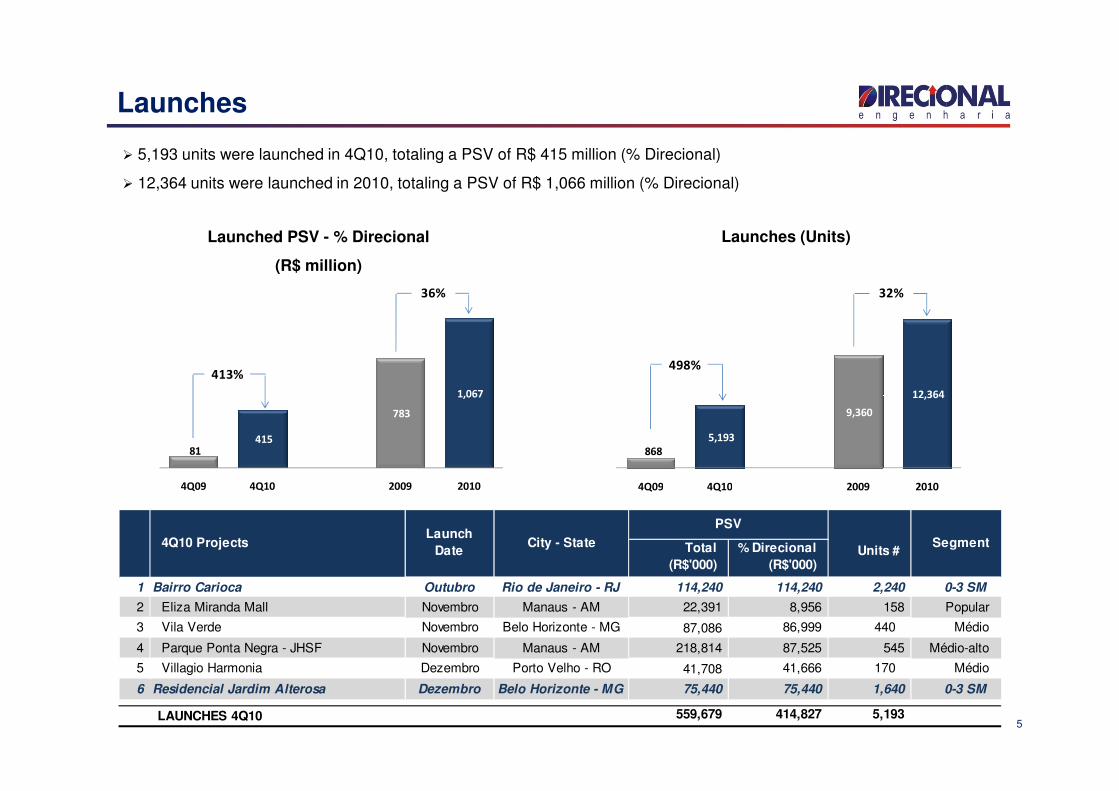

Launches

Ricardo Ribeiro Gontijo Operating Highlights

4

� Launches

� Sales

� Land bank

� Inventory

Launches

� 5,193 units were launched in 4Q10, totaling a PSV of R$ 415 million (% Direcional)

� 12,364 units were launched in 2010, totaling a PSV of R$ 1,066 million (% Direcional)

Launched PSV - % Direcional

(R$ million)

Launches (Units)

1,067

36%

413%

12,364

32%

498%

5

81 415

783

1,067

4Q09 4Q10 2009 2010

868

5,193

9,360

12,364

4Q09 4Q10 2009 2010

Total

(R$'000)

% Direcional

(R$'000)

1 Bairro Carioca Outubro Rio de Janeiro - RJ 114,240 114,240 2,240 0-3 SM

2 Eliza Miranda Mall Novembro Manaus - AM 22,391 8,956 158 Popular

3 Vila Verde Novembro Belo Horizonte - MG 87,086 86,999 440 Médio

4 Parque Ponta Negra - JHSF Novembro Manaus - AM 218,814 87,525 545 Médio-alto

5 Villagio Harmonia Dezembro Porto Velho - RO 41,708 41,666 170 Médio

6 Residencial Jardim Alterosa Dezembro Belo Horizonte - MG 75,440 75,440 1,640 0-3 SM

559,679 414,827 5,193

4Q10 ProjectsLaunch

DateCity - State Segment

Units #

LAUNCHES 4Q10

PSV

Launches Breakdown

Launches

(Segment Breakdown)

Launches

(Geographic Breakdown)

56.0%

17.0% 13.0%

50.0%

44.0%

12.0%

11.0%83.0%75.0%

39.0%

4Q09 4Q10 2009 2010

74.7%

39.0%

59.8%

100.0%

3.0%

40.0%

28.1%

11.7%20.0% 5.1%

10.5%1.0% 7.0%

4Q09 4Q10 2009 2010

6

Vila Verde Parque Ponta NegraEliza Miranda Mall

Villagio Harmonia

Bairro Carioca

Jardim Alterosa

4Q09 4Q10 2009 2010

North Mid-west Southeast

4Q09 4Q10 2009 2010

0-3 MW Popular Medium Upper Middle

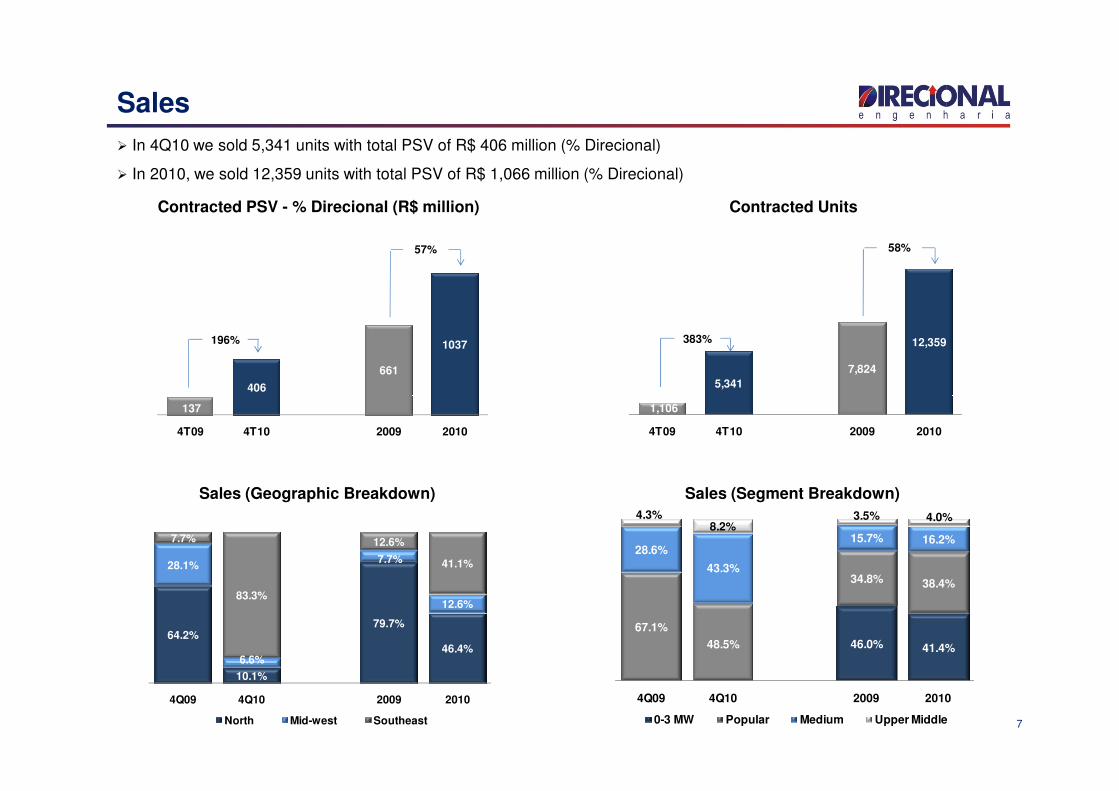

Sales

Contracted PSV - % Direcional (R$ million) Contracted Units

� In 4Q10 we sold 5,341 units with total PSV of R$ 406 million (% Direcional)

� In 2010, we sold 12,359 units with total PSV of R$ 1,066 million (% Direcional)

406

661

1037

57%

196%

5,341

7,824

12,359

58%

383%

7

Sales (Geographic Breakdown) Sales (Segment Breakdown)

137

4T09 4T10 2009 2010

1,106

4T09 4T10 2009 2010

64.2%

10.1%

79.7%

46.4%

28.1%

6.6%

7.7%

12.6%

7.7%

83.3%

12.6%

41.1%

4Q09 4Q10 2009 2010

North Mid-west Southeast

46.0% 41.4%

67.1%

48.5%

34.8% 38.4%

28.6%

43.3%

15.7% 16.2%

4.3%8.2%

3.5% 4.0%

4Q09 4Q10 2009 2010

0-3 MW Popular Medium Upper Middle

36.0%38.3%

20.5%

24.2%

19.4%20.8%

27.6%

4Q09 1Q10 2Q10* 3Q10 4Q10*

With 0-3 MW projects Without 0-3 MW projects

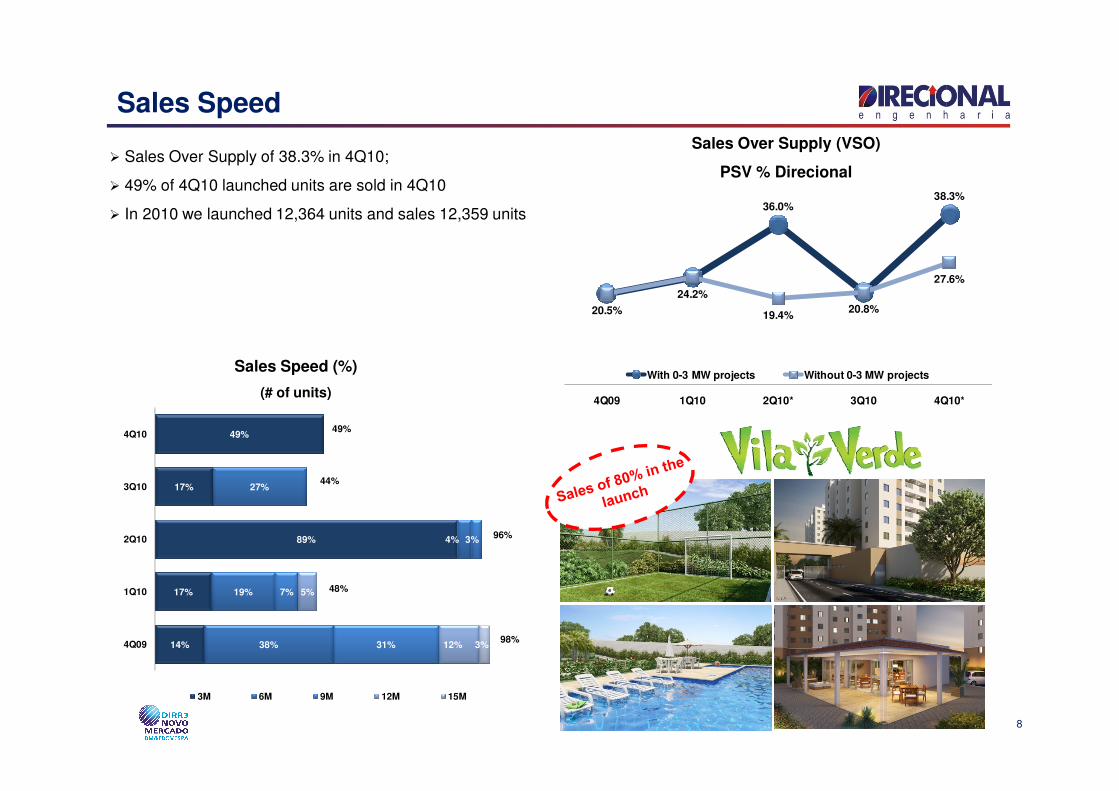

Sales Speed

� Sales Over Supply of 38.3% in 4Q10;

� 49% of 4Q10 launched units are sold in 4Q10

� In 2010 we launched 12,364 units and sales 12,359 units

Sales Over Supply (VSO)

PSV % Direcional

Sales Speed (%)

(# of units)

14%

17%

89%

17%

49%

38%

19%

4%

27%

31%

7%

3%

12%

5%

3%4Q09

1Q10

2Q10

3Q10

4Q10

3M 6M 9M 12M 15M

44%

96%

48%

98%

49%

4Q09 1Q10 2Q10* 3Q10 4Q10*

8

(# of units)

6,311

6,756

313

356

225

3Q10 AQUIRED LANDS REVIEW OF LAUNCHES IN LAND BANK

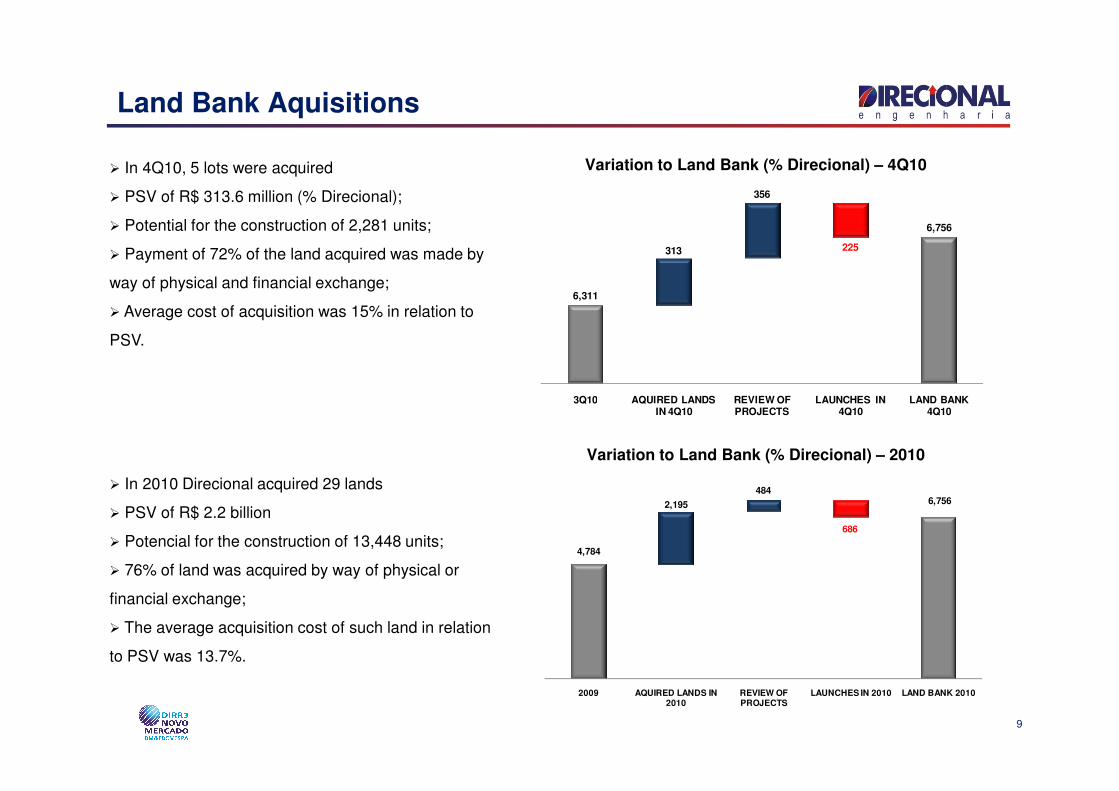

Land Bank Aquisitions

� In 4Q10, 5 lots were acquired

� PSV of R$ 313.6 million (% Direcional);

� Potential for the construction of 2,281 units;

� Payment of 72% of the land acquired was made by

way of physical and financial exchange;

� Average cost of acquisition was 15% in relation to

PSV.

Variation to Land Bank (% Direcional) – 4Q10

3Q10 AQUIRED LANDS IN 4Q10

REVIEW OF PROJECTS

LAUNCHES IN 4Q10

LAND BANK 4Q10

9

� In 2010 Direcional acquired 29 lands

� PSV of R$ 2.2 billion

� Potencial for the construction of 13,448 units;

� 76% of land was acquired by way of physical or

financial exchange;

� The average acquisition cost of such land in relation

to PSV was 13.7%.

Variation to Land Bank (% Direcional) – 2010

4,784

6,7562,195

484

686

2009 AQUIRED LANDS IN 2010

REVIEW OF PROJECTS

LAUNCHES IN 2010 LAND BANK 2010

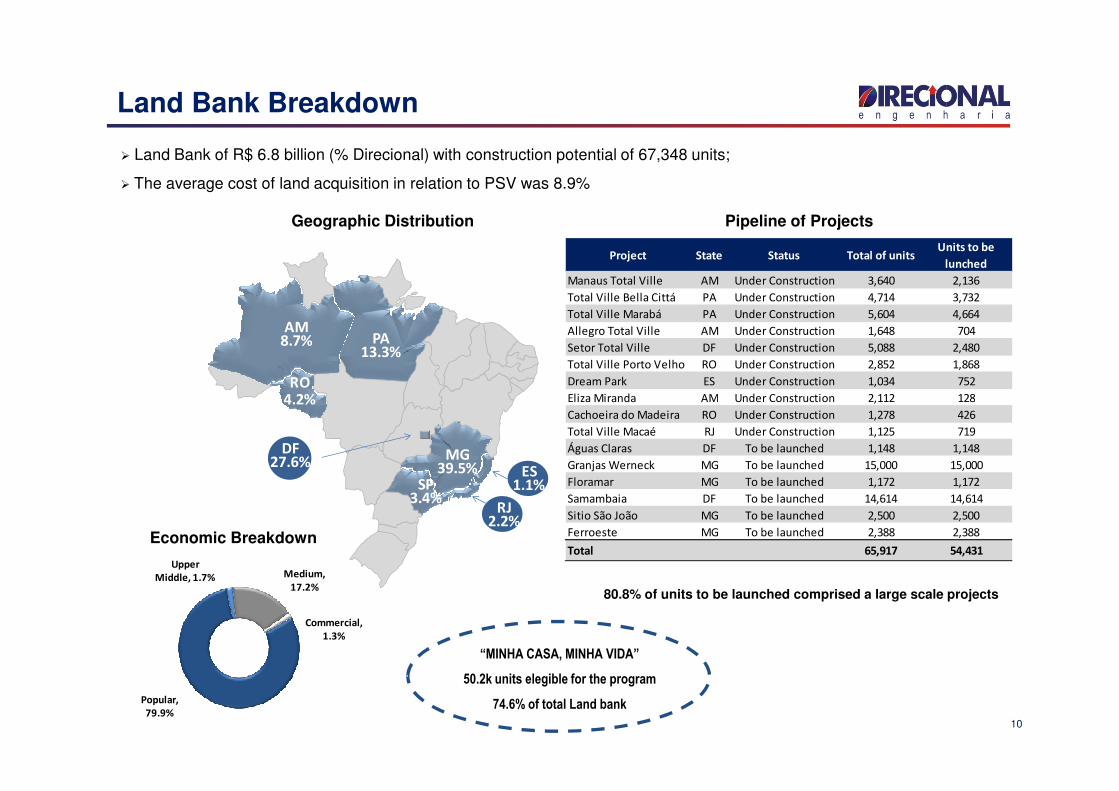

Land Bank Breakdown

� Land Bank of R$ 6.8 billion (% Direcional) with construction potential of 67,348 units;

� The average cost of land acquisition in relation to PSV was 8.9%

Geographic Distribution Pipeline of Projects

AM8.7%

RO4.2%

PA13.3%

Project State Status Total of unitsUnits to be

lunched

Manaus Total Ville AM Under Construction 3,640 2,136

Total Ville Bella Cittá PA Under Construction 4,714 3,732

Total Ville Marabá PA Under Construction 5,604 4,664

Allegro Total Ville AM Under Construction 1,648 704

Setor Total Ville DF Under Construction 5,088 2,480

Total Ville Porto Velho RO Under Construction 2,852 1,868

Dream Park ES Under Construction 1,034 752

Eliza Miranda AM Under Construction 2,112 128

10

“MINHA CASA, MINHA VIDA”

50.2k units elegible for the program

74.6% of total Land bank

Economic Breakdown

80.8% of units to be launched comprised a large scale projects

1

ES1.1%

MG39.5%

4.2%

SP3.4%

DF27.6%

RJ2.2%

Popular,

79.9%

Upper

Middle, 1.7% Medium,

17.2%

Commercial,

1.3%

Eliza Miranda AM Under Construction 2,112 128

Cachoeira do Madeira RO Under Construction 1,278 426

Total Ville Macaé RJ Under Construction 1,125 719

Águas Claras DF To be launched 1,148 1,148

Granjas Werneck MG To be launched 15,000 15,000

Floramar MG To be launched 1,172 1,172

Samambaia DF To be launched 14,614 14,614

Sitio São João MG To be launched 2,500 2,500

Ferroeste MG To be launched 2,388 2,388

Total 65,917 54,431

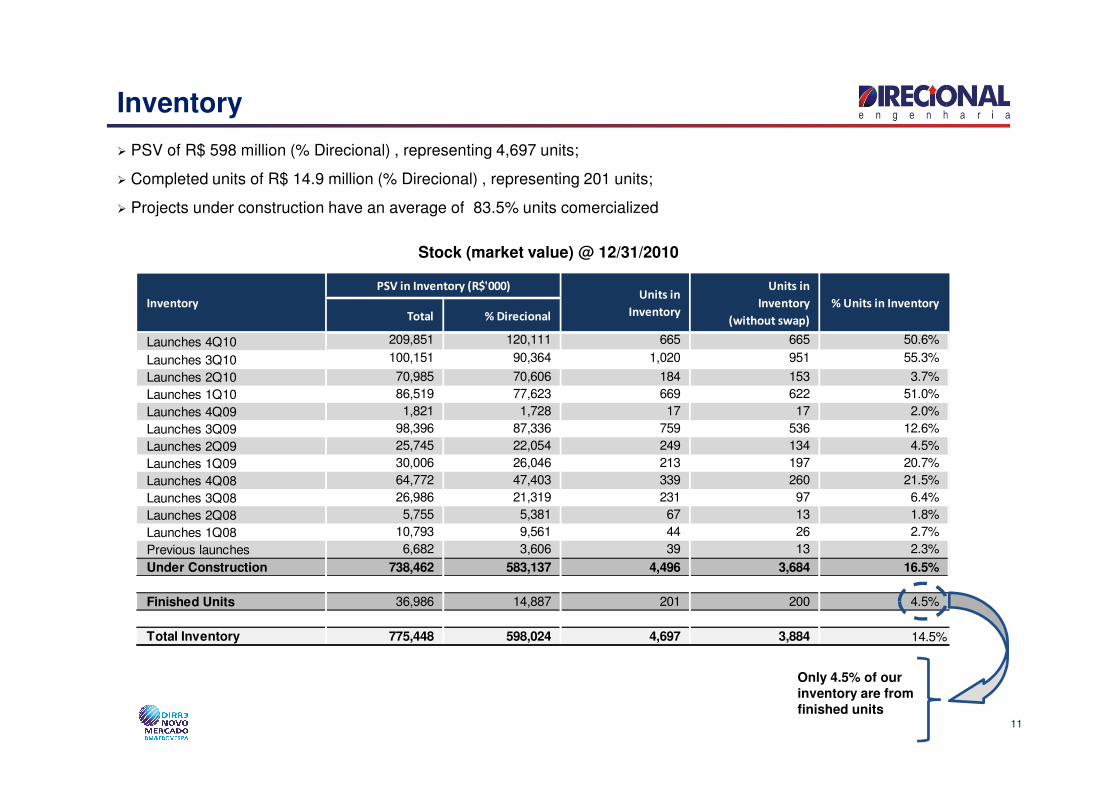

Total % Direcional

Launches 4Q10 209,851 120,111 665 665 50.6%

Launches 3Q10 100,151 90,364 1,020 951 55.3%

Launches 2Q10 70,985 70,606 184 153 3.7%

Launches 1Q10 86,519 77,623 669 622 51.0%

Inventory

PSV in Inventory (R$'000)Units in

Inventory

Units in

Inventory

(without swap)

% Units in Inventory

Inventory

� PSV of R$ 598 million (% Direcional) , representing 4,697 units;

� Completed units of R$ 14.9 million (% Direcional) , representing 201 units;

� Projects under construction have an average of 83.5% units comercialized

Stock (market value) @ 12/31/2010

Launches 1Q10 86,519 77,623 669 622 51.0%

Launches 4Q09 1,821 1,728 17 17 2.0%

Launches 3Q09 98,396 87,336 759 536 12.6%

Launches 2Q09 25,745 22,054 249 134 4.5%

Launches 1Q09 30,006 26,046 213 197 20.7%

Launches 4Q08 64,772 47,403 339 260 21.5%

Launches 3Q08 26,986 21,319 231 97 6.4%

Launches 2Q08 5,755 5,381 67 13 1.8%

Launches 1Q08 10,793 9,561 44 26 2.7%

Previous launches 6,682 3,606 39 13 2.3%

Under Construction 738,462 583,137 4,496 3,684 16.5%

Finished Units 36,986 14,887 201 200 4.5%

Total Inventory 775,448 598,024 4,697 3,884 14.5%

11

Only 4.5% of ourinventory are fromfinished units

Delivered Units in 4Q10

Completed Projects - 4Q10 City - State UnitsTotal PSV

(R$'000)

Direcional PSV

(R$'000)Segment

Grand Prix Manaus - AM 192 42,026 36,983 Medium

Paradiso Club Taguatinga - DF 358 61,111 59,950 Medium

Paradiso Uno Taguatinga - DF 42 10,156 9,963 Medium

Maura Valadares Belo Horizonte - MG 72 30,479 18,755 Upper Middle

Le Parc de France Belo Horizonte - MG 36 10,155 9,962 Medium

Al Mare Macaé - RJ 172 29,585 14,792 Medium

Vivere Campinas - SP 88 34,746 17,373 Upper Middle

Total 960 218,258 167,778

12

Grand PrixParadiso Club Al MareParadiso Club Le Parc de France

Financial Highlights

Financial Performance

Carlos Wollenweber Financial Highlights

13

� Financial Performance

� Liquidity

� Results to be Recognized

� Share’s Performance

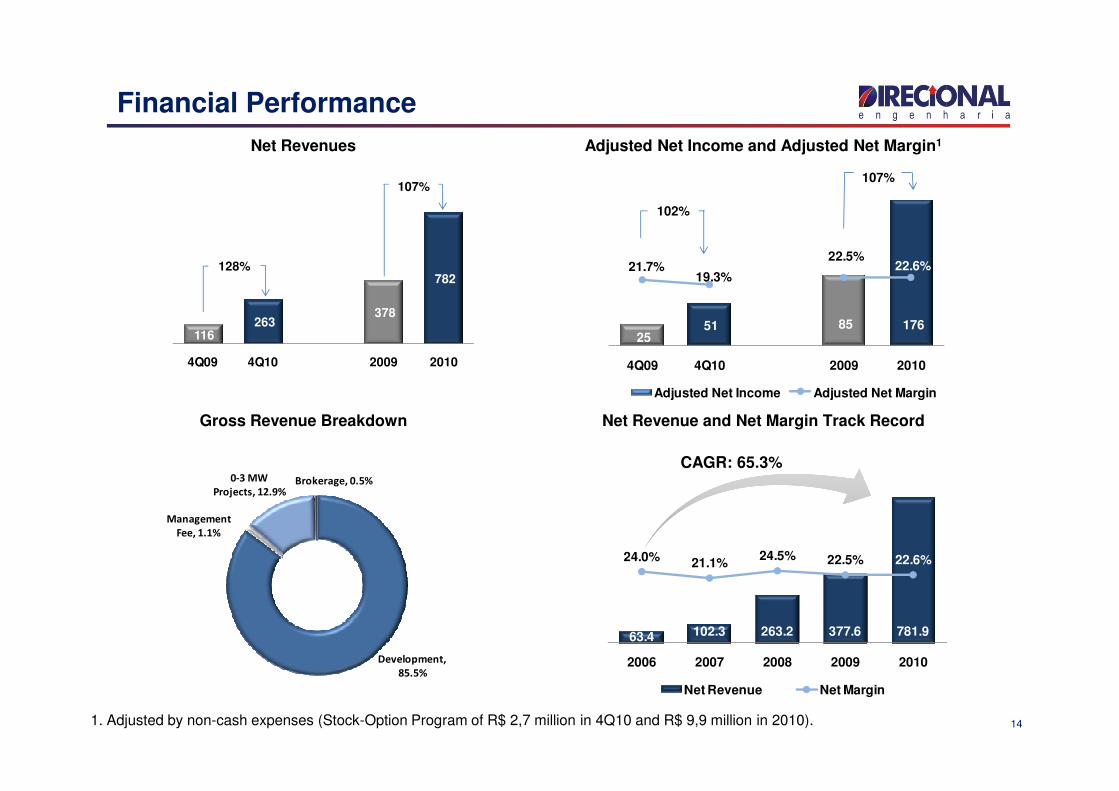

25 51 85 176

21.7%19.3%

22.5%22.6%

4Q09 4Q10 2009 2010

Adjusted Net Income Adjusted Net Margin

102%

107%

Financial Performance

Net Revenues Adjusted Net Income and Adjusted Net Margin1

116 263

378

782

4Q09 4Q10 2009 2010

128%

107%

Adjusted Net Income Adjusted Net Margin

63.4 102.3 263.2 377.6 781.9

24.0% 21.1%24.5% 22.5% 22.6%

2006 2007 2008 2009 2010

Net Revenue Net Margin

141. Adjusted by non-cash expenses (Stock-Option Program of R$ 2,7 million in 4Q10 and R$ 9,9 million in 2010).

CAGR: 65.3%

Development,

85.5%

Management

Fee, 1.1%

0-3 MW

Projects, 12.9%Brokerage, 0.5%

Gross Revenue Breakdown Net Revenue and Net Margin Track Record

8.7

17.4 21.8

50.0

4Q09 4Q10 2009 2010

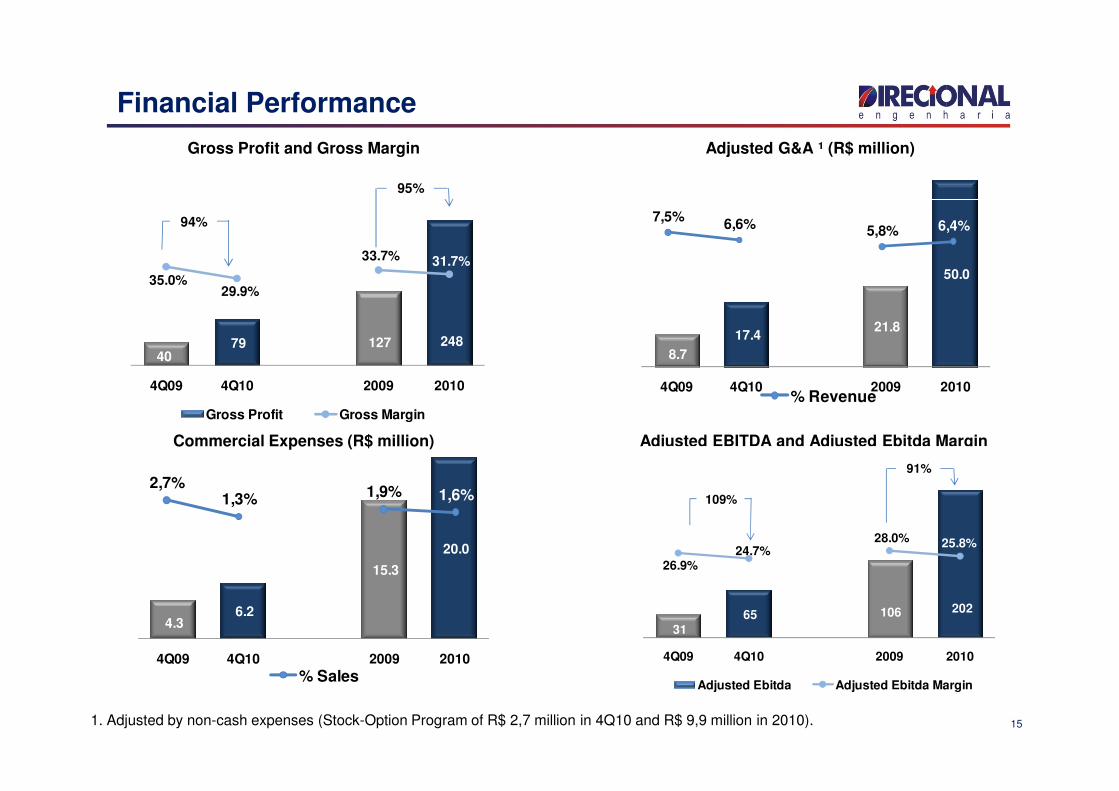

Financial Performance

Gross Profit and Gross Margin Adjusted G&A ¹ (R$ million)

7,5%6,6% 5,8% 6,4%

40 79 127 248

35.0%29.9%

33.7% 31.7%

4Q09 4Q10 2009 2010

94%

95%

% Revenue

4.3 6.2

15.3

20.0

4Q09 4Q10 2009 2010

15

Adjusted EBITDA and Adjusted Ebitda MarginCommercial Expenses (R$ million)

2,7%1,3% 1,9% 1,6%

Gross Profit Gross Margin

% Revenue

% Sales

31 65 106 202

26.9%24.7%

28.0% 25.8%

4Q09 4Q10 2009 2010

Adjusted Ebitda Adjusted Ebitda Margin

109%

91%

1. Adjusted by non-cash expenses (Stock-Option Program of R$ 2,7 million in 4Q10 and R$ 9,9 million in 2010).

Cash Position

Loans and Financing

(ex- securitization)

Cash Position 4Q09 3Q10 4Q10 ∆∆∆∆ % ∆∆∆∆ %

(R$'000) (a) (b) (c) (c/a) (c/b)

Loans and Financing 123,298 245,724 302,374 145% 23%

SFH 108,056 184,243 226,056 109.2% 22.7%

Securitization of receivables 13,109 53,097 46,843 257.3% -11.8%

FINAME and others 2,133 8,384 8,882 316.4% 5.9%

Working Capital 0 0 20,593 100.0% 100.0%

Cash and Cash Equivalents 313,881 235,075 190,852 -39.2% -18.8%

Net debt -190,583 10,649 111,522 -158.5% 947.3%

Net debt - ex securitization -190,583 -43,665 57,208 -158.5% -231.0%

Net debt / Shareholder's Equity -29.0% 1.4% 14.1% -148.5%

SFH, 88.5%

FINAME and Leasing, 3.5%

Working Capital, 8.1%

161. Cash Burn: variation of the net debt (-) equity increases

2. 2Q10 * : adjusted by co-obligation in the securitization of receivables, amounting R$ 54.3 million

Amortization Schedule (R$ million) Cash Burn¹ (R$ million)

Net debt / Ebitda -1.8x 0.1x 0.5x

13

45

28 27

15

2522

33

41

19

86

101

54

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10* 3Q10 4Q10*

122

59

102

20

2011 2012 2013 +2014

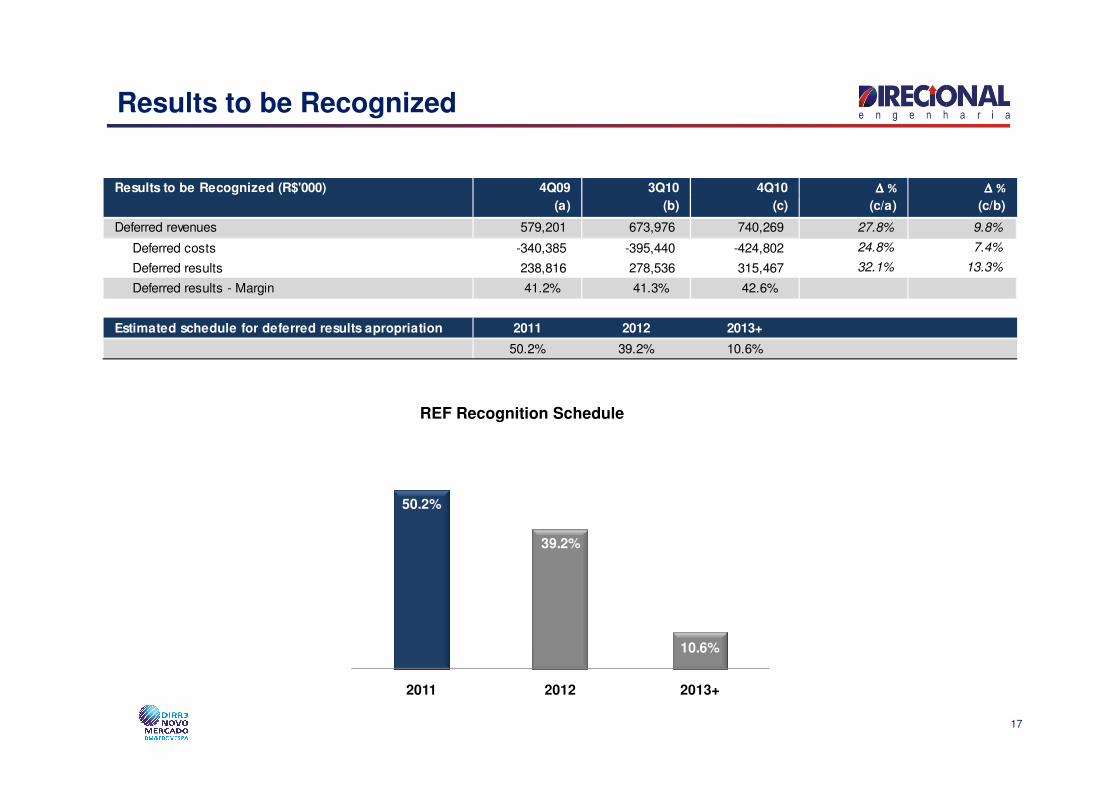

Results to be Recognized

Results to be Recognized (R$'000) 4Q09 3Q10 4Q10 ∆∆∆∆ % ∆∆∆∆ %

(a) (b) (c) (c/a) (c/b)

Deferred revenues 579,201 673,976 740,269 27.8% 9.8%

Deferred costs -340,385 -395,440 -424,802 24.8% 7.4%

Deferred results 238,816 278,536 315,467 32.1% 13.3%

Deferred results - Margin 41.2% 41.3% 42.6%

Estimated schedule for deferred results apropriation 2011 2012 2013+

50.2% 39.2% 10.6%

17

REF Recognition Schedule

50.2%

39.2%

10.6%

2011 2012 2013+

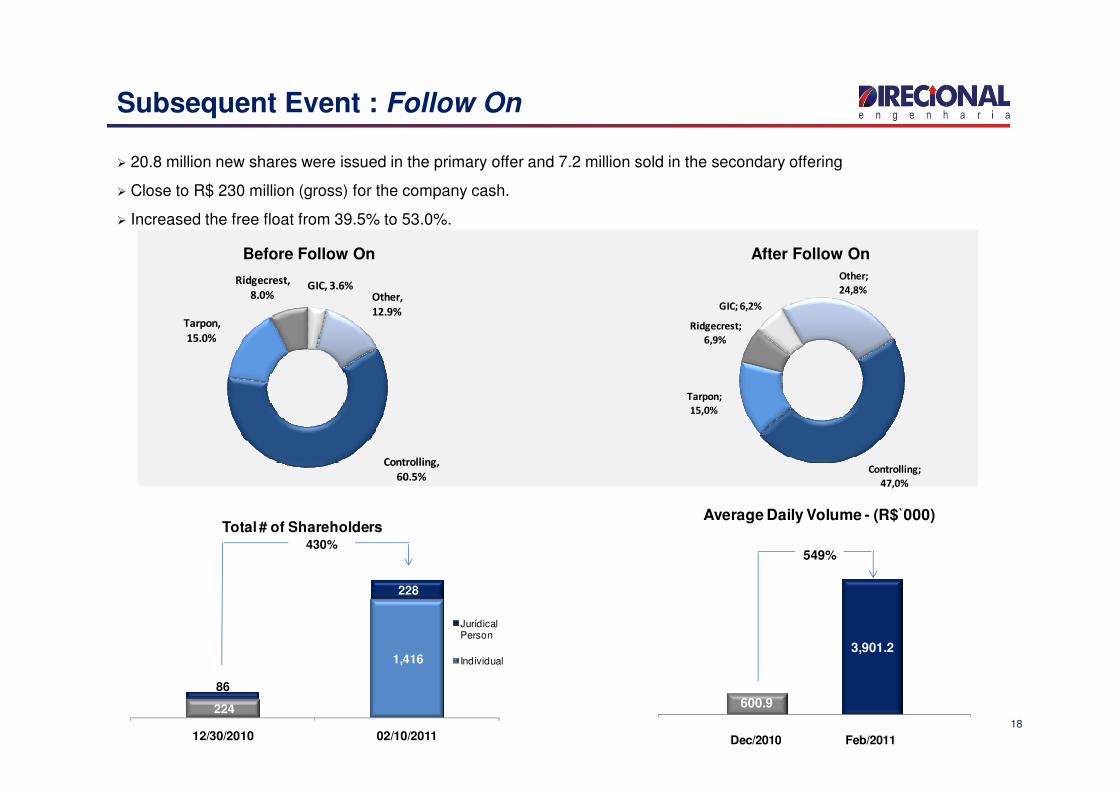

Subsequent Event : Follow On

� 20.8 million new shares were issued in the primary offer and 7.2 million sold in the secondary offering

� Close to R$ 230 million (gross) for the company cash.

� Increased the free float from 39.5% to 53.0%.

Before Follow On After Follow On

Tarpon,

15.0%

Ridgecrest,

8.0%GIC, 3.6%

Other,

12.9%

Tarpon;

Ridgecrest;

6,9%

GIC; 6,2%

Other;

24,8%

224

1,416

86

228

12/30/2010 02/10/2011

Total # of Shareholders

Jurídical Person

Individual

430%

18

600.9

3,901.2

Average Daily Volume - (R$`000)

549%

Dec/2010 Feb/2011

Controlling,

60.5%Controlling;

47,0%

Tarpon;

15,0%

Share’s Performance - 2010

Base 100

DIRR3 = +17.7%|R$13.49

IMOB = +10.5%|1,037 pt.

IBOV = +1.0%|69,305 pt.

100

110

120

130

19

70

80

90

100

30

-dez

11

-jan

19

-jan

28

-jan

5-f

ev

17

-fev

25

-fev

5-m

ar

15

-mar

23

-mar

31

-mar

8-a

br

16

-ab

r

26

-ab

r

4-m

ai

12

-mai

20

-mai

28

-mai

7-j

un

15

-ju

n

23

-ju

n

1-j

ul

12

-ju

l

20

-ju

l

28

-ju

l

5-a

go

13

-ago

23

-ago

31

-ago

9-s

et

17

-set

27

-set

5-o

ut

14

-ou

t

22

-ou

t

1-n

ov

10

-no

v

19

-no

v

29

-no

v

7-d

ez

15

-dez

23

-dez

IBOV DIRR3 IMOB

Disclaimer

This presentation contains certain forward-looking statements concerning the business prospects, projections of

20

operating and financial results and growth potential of the Company, which are based on management’s currentexpectations and estimates of the future performance of the Company. Although the Company believes suchforward-looking statements are based on reasonable assumptions, it can give no assurance that its expectations willbe achieved. Expectations and estimates that are based on the future prospects of the Company are highlydependent upon market behavior, Brazil’s political and economic situation, existing and future regulations of theindustry and international markets and, therefore, are subject to changes outside the Company’s and management’scontrol. The Company undertakes no obligation to update any information contained herein or to revise any forward-looking statement as a result of new information, future events or other information.

Contact

Carlos Wollenweber

CFO | IR Officer

Lucas Bousas

IR Analyst

21

IR Analyst

www.direcional.com.br

(55 31) 3214-6200

(55 31) 3214-6450