第三章

DESCRIPTION

第三章. 期权定价的离散模型 -------- 二叉树方法. Chapter 3. Binomial Tree Methods ------ Discrete Models of Option Pricing. An Example. - PowerPoint PPT PresentationTRANSCRIPT

第三章

期权定价的离散模型 -------- 二叉树方法

Chapter 3

Binomial Tree Methods

------ Discrete Models of Option

Pricing

An Example

Question: When t=0, buying a call option of the stock at with strike price $40 and 1 month maturity. If the risk-free annual interest rate is 12% throughout the period [0, T], how much should the premium for the call option (看涨期权) be?

0 $40S $45u

TS

$35dTS

Example cont.1

(到期日收益) payoff =

Consider a portfolio (投资组合)

0 $40S $45, (45 40) $5u

T TS c

$35, (35 40) $0dT TS c

( )T Tc S K

2S c

Example cont.2

When t=T,

has fixed value $35, no matter S is up or down

45 2*5 35, if ,( ) $35

35 2*0 35, if .T

SV

S

Example cont.3

If risk free interest r =12%, a bank

deposit of B=35/(1+0.01) after 1 month

By arbitrage-free principle

35 1( ) (1 12%) 35 ( )

1 0.01 12T TV B V

0 0( ) ( ).V B V

Example cont.4

That is

Then

This is the investor should pay $2.695 for this stock option.

0 0 0

352 34.65

1 0.01S c B

0

40 34.652.695

2c

Analysis of the Example

① the idea of hedging: it is possible to construct an investment portfolio with S and c such that it is risk-free.

② The option price thus determined (c_0=$2.695) has nothing to do with any individual investor's expectation on the future stock price.

One-Period & Two-State

One-period: assets are traded at t=0 & t=T only, hence the term one period.

Two-state: at t=T the risky asset S has two possible values (states): , with their probabilities satisfying

&u dT TS S

0 Prop ,Prop 1

Prop Prop 1

u dT T T T

u dT T T T

S S S S

S S S S

One-Period & Two-State Model

The model is the simplest model.Consider a market consisting of two assets:

a risky S and a risk-free B If: risky asset and risk free asset known , when t=0, t=T, 2 possibilities Option Price at t=0?

(for strike price K, expired time T)

0

0

,: .

,

uT

T dT

S S uS u d

S S d

tS

0 0,S BtB

Analysis of the Model

0S0

uTS S u

tS - Stock Price, is a stochastic variable

0dTS S d

Up, with probability p

Down, with probability 1-p

where is a stochastic variable.tV

0V0( )u

TV S u K

0( )dTV S d K

Question & Analysis

If known at t=T, how to find out when t=0? Assume the risky asset to be a stock. Since the

stock option price is a random variable, the seller of the option is faced with a risk in selling it. However, the seller can manage the risk by buying certain shares (denoted asΔ) of the stocks to hedge the risk in the option.

This is the idea!

( )T TV S

0V

Δ- Hedging Definition

Definition:

for a given option V, trade Δ shares of the underlying asset S in the opposite direction, so that the portfolio

is risk-free.

V S

Analysis of Δ- Hedging

risk free asset If Π is risk free, then, on t=T,

is risk free. i.e.

so that

0 , 1TB B rT

T T TV S

0T

0T TV S

Analysis of Δ- Hedging cont.

are random variables, when t=T,

both of them have 2 possible values

where are unknown, solve them:

,T TV S

0 0 0

0 0 0

( ),

( ),

uT

dT

V S u V S

V S d V S

0&V

0 ( )

u dT TV V

S u d

Analysis of Δ- Hedging (Probability Measure)

Define a new Probability Measure

Obviously

0 0

1 1 u dT T T

d uV S V V

u d u d

Prob ,

Prob

uu Q T T

dd Q T T

dq S S

u du

q S Su d

0 , 1, 1.u d u dq q q q

Solution of Premium

From the discussion above,

where denotes the expectation of the random variable under the probability measure Q.

0

1( ),QTV E V

( )QTE V

TV

Definition of Discounted Price Let U be a certain risky asset, and B a

risk-free asset, then is called the discounted price 贴现价格 (also known as the relative price 相对价格 ) of the risky asset U

at time t.

/t tU B

0

0

.Q T

T

V VE

B B

Theorem 3.1

Under the probability measure Q, an option's discounted price is its expectation on the expiration date. i.e.

0

0

( ) / , call

( ) / , put

QT T

QT T

E S K BV

B E K S B

Remark

In order to examine the meaning of the probability measure Q, consider S is an underlying risky asset. Calculate

0

00 0

0 0

1

1

Q u dTu T d T

T

SE q S q S

B B

Sd uS u S d

B u d u d B

Risk-Neutral World

Under the probability measure Q, the expected return of a risky asset S at t=T is the same as the return of a risk-free bond. A financial market possessing this property is called a Risk-Neutral World

In a risk-neutral world, no investor demands any compensation for risks, and the expected return of any security is the risk-free interest rate.

Definitions the probability measure Q defined by

is called by risk-neutral measure. The option price given under the risk-

neutral measure is called the risk-neutral price.

Prob ,

Prob

uu Q T T

dd Q T T

dq S S

u du

q S Su d

Definition of Replication

In a market consisted of a risky asset S and a risk-free asset B, if there exists a portfolio

(where α,β are constants, Φ, V are both random variables) such that the value of the portfolio Φ is equal to the value of the option V at t=T,

then Φ is called a replicating portfolio of the option V, then option price

S B

T T TS B V

0 0 0 0V S B

Theorem 3.2

In a market consisted of a risky asset S

and a risk-free asset B,

d<ρ<u is true if and only if

the market is arbitrage-free.

Proof of Theorem 3.2 (1st dir.)

1) arbitrage-free d<ρ<u Suppose ρ>= u, consider the following

portfolio:

Its values at t=0 and at t=T are:

0 0( / )S S B B

0 0 0 0 0

0 0

( / ) 0

( / )T T T

S S B B

S S B B

Proof of Theorem 3.2 (1st dir.) cont.

is a random variable with two possible values:

T

00 0 0

0

00 0 0

0

( ) 0,

( ) 0

uT

T

dT

SS u B u S

B

SS d B d S

B

for uT TS S

for dT TS S

Proof of Theorem 3.2 (1st dir.) cont. -

So that, for the portfolio Φ

That shows that there exists arbitrage opportunity for portfolio Φ, contradiction! to that the market is arbitrage-free.

Same to ρ<=d.

0,T

& Prob 0 Prob 0.dT T TS S

Proof of Theorem 3.2 (2nd dir.)

If market is arbitrage-free, for any portfolio If then In fact, define a risk-neutral measure Q

S B

0 0 0 0, 0,T T TS B S B 0.T T TS B

Prob ,

Prob

uu Q T T

dd Q T T

dq S S

u du

q S Su d

Proof of Theorem 3.2 (2nd dir.) cont.

ThenConsider the expectation of the random

variable

According to the definition of the risk-neutral measure Q,

0 , 1, 1.u d u dq q q q

T( )Q u d

T u T d TE q q

0 0 0 0

0 0 0

( ) ( ) ( )

( ) 0.

QT

d uE S u B S d B

u d u dS B

Proof of Theorem 3.2 (2nd dir.) cont.-

That is,

But Then i.e.

There exists no arbitrage opportunity.

0.u du T d Tq q

0, 0u dT T

0.u dT T

Prob 0 0.T

Theorem 3.2

If the market is arbitrage-free, then there exists a risk-neutral measure Q defined by

such that

Prob ,

Prob

uu Q T T

dd Q T T

dq S S

u du

q S Su d

0

0

( ) / , call

( ) / , put

QT T

QT T

E S K BV

B E K S B

Binomial Tree MethodDivide the option lifetime [0, T] into N

intervals:Suppose the price change of the

underlying asset S in each interval

can be described by the one-period two-state model, then the random movement of S in [0, T] forms a binomial tree

0 10 ... .Nt t t T

1[ , ](0 1)n nt t n N

Binomial Tree Method cont.

This means that if at the initial time the price of the underlying asset is , then at

t=T, will have N+1 possible values

Take call option as example,

the option value at t=T, is also a random variable, with corresponding possible values

0S STS

0 0,1,...

N

NS u d

( )T TV S K

0 0,1,...( )N

NS u d K

Binomial Tree Method Notation

Denote , ( , ),

(0 ,0 ),

n n n nnS S u d V V S t

n N N

ˆ max | 0,0NS u d K N

Binomial Tree

0S u

0S0S d

20S u

0S ud

20S d

……

……

……

……

0NS u

10NS u d

…

0NS u d

…1

0NS ud

0NS d

Possible Values of Option at t=T

0 0 0

ˆˆ0

ˆ 1

,

,

0,

0.

N N N

N N N

N

NN

V S u K S K

V S u d K S K

V

V

Problem Option Pricing by BTM

If are given, how can we determine

in particular

(0 )NV N

1(0 1)NV N

00 0 0( , )?V V S t

Answer to the Problem

With the one period and two-state model, and using backward induction, we can determine

step by step.

N hV

Induction Steps

When are given, to find consider the following one period and two-

state model.

(0 )NV N 1(0 1)NV N

1NS

1N NS u S

11

N NS d S

1NV

( )N NV S K

1 1( )N NV S K

and

Induction Steps cont.

Define a risk-neutral measure Q

Then,So that for any

, 1u d

d uq q q q

u d u d

1

1

1[ (1 ) ] (0 1).N N NV qV q V N

(1 )h h N ˆ

0

1(1 ) ( )

ˆwhen , 0.

N h h l l Nlh

l

N h

hV q q S K

l

V

Induction Steps cont.-

ButDenote Thus

,N N h h l llS S u d

ˆ /q uq (1 )qu q d

ˆ(1 ) 1d

q q

ˆ

0

ˆ

0

(1 )

ˆ(1 ) , ,

ˆ0, .

h lN h l

l

N h h l lhl

hS q q

l

hKV q q

l

European call option valuation formula

Denote

Then the European call option valuation formula is

Especially, h=N, α=0,

0

( , , ) (1 )n

m l l

l

mn m p p p

l

ˆˆ( , , ) ( , , )N h N hh

KV S h q h q

0 0

ˆˆ( ,0) ( , , ) ( , , )N

KV S S N q N q

Discount Factor

Discount Factor satisfies

The financial meaning of the discount factor: to have $1 at t=T (including continuous compound interests), one needs to deposit in bank at t (t<T).

( )r T tTB e

, (0 ), 1.tt T

dBrB t T B

dt

tB

Discount Factor in BTM

in the binomial tree method, trading occurs at discrete times

the compound interests should also be calculated for the discrete case.

Let denote the discrete discount factors. They satisfy the difference equations

(0 )nt t n N

( 0,1,... )nB n N

1 , (0 1), 1.n n n NB B r tB n N B

Discount Factor in BTM cont.

That is

where ρis the growth of the risk-free bond in i.e.

1

1 1 1

1 1

N n

n n N N nB B B

r t r t

[ , ]t t t

1n nB B

Call---Put Parity in discrete form

for the binomial tree method,

the call---put parity (in discrete form) becomes

/N h h N h N hc K p S

European put option valuation formula

Using European call option valuation formula and put---call party, we have

ˆ ˆ( , , ) ( , , )

0 , 0 .

N h N h N hh

Kp S h q S h q

h N N h

Investment vs. Gambling Game

Investing in options can be compared to a gambling game.

Initial stake be . After one game, the stake becomes .

is a random variable. If the expectation

then the gamble is said to be fair

0U

TU

TU

0( )TE U U

Fair Gambling Game - the bet at n-th game, - the next

bet. If under the condition that complete

information of all the previous n-games are available, the expectation of equals the previous stake i.e.,

then we say the gamble is fair.

nU 1nU

1nU

nU

1 1( | ( ))n n nE U U U U

σ-Algebra

denotes complete information of the bets up to n-th game,

and denotes the conditional

expectation of X under condition Y. In mathematics, is called σ-

algebra in stochastic theory

1( )nU U

1 nU U

( | )E X Y

1( )nU U

Martingale

Martingale is often used to refer to a fair gamble.

The bet sequence

that satisfies condition

as a discrete random process, is called a Martingale.

: 0nU n N

1 1( | ( ))n n nE U U U U

Mathematical Definition of Martingale

A sequence is a

Martingale with respect to sequence

if for all n ≥0

: 0nY Y n

: 0nX X n

| |nE Y

1 0 1( | , )n n nE Y X X X Y

Risk-neutral measure vs. Martingale

Under the risk-neutral measure Q, the discount prices of an underlying

asset S, as a discrete

random process, satisfy the equation:

01

( ) , (0 )n n

Qn

t t

S SE S S n N

B B

, ( 0,1 )nt

Sn N

B

Martingale Measure

Hence the discount price sequence of an underlying asset is a martingale.

The risk-neutral measure Q is called the

martingale measure Q equivalent to the probability measure P.

Definition of Equivalence

Probability measure P and probability measure Q are said to be equivalent if and only if for any probability event

(set) there is

i.e. the probability measures P and Q have the same null set.

A

Prob ( ) 0 Prob ( ) 0P Q A A

European option under Martingale

The European option valuation formula under the sense of equivalent Martingale measure Q, can be written as

or

Especially

0( , , )N h

N h N

Qt

t t

S SE S S

B B

0| ( , , )N h N h

h Qt N tV E S K S S

0N Q

NV E S K

Relation of the arbitrage-freeprinciple & Martingale measure

What is the relation between the arbitrage-free principle and the existence of equivalent Martingale measure?

Arbitrage-free principle d< ρ <u

existence of equivalent Martingale measure Q

European option pricing in a risk-neutral world

Theorem 3.3 - the fundamental theorem of asset

pricing If an underlying asset price moves as a

binomial tree, there exists an equivalent Martingale measure if and only if the market is arbitrage-free.

Proof of Theorem 3.3

a risky asset S and a risk-free asset B, “sufficiency” by Theorem 3.2. “necessity”- A portfolio

then what we need to prove is that there must be where $P$ denotes an objective measure.

*

*0if 0, 0, . . Prob ( 0) 1P t

t s t

*Prob ( 0) 0P t

Proof of Theorem 3.3 cont. In fact, let Q- equi. Mart. Meas. of P, then Thus Since P Q , it implies we have therefore Since measure P and measure Q are

equivalent, this means

*0/ /Q

tB E B

* *0 0( ) / 0Q

t tE B B

*Prob ( 0) 1Q t

*Prob ( 0) 1Q t

*Prob ( 0) 0Q t

*Prob ( 0) 0P t

Dividend-Paying

An underlying asset pays dividends in two ways:

1. Pay dividends discretely at certain times in a year;

2. Pay dividends continuously at a certain rate.

This section, the continuous model is considered only

Reason for Studying the ContinuousModel 1

Asset -- foreign currency. exchange rate changes randomly the foreign currency is a risky asset . If it is deposited in a bank in its native country, it

would accrue interests according to the local int.rate

The interest be regards dividend of the "security" this dividend is paid continuously. Therefore, the "dividend rate" is the risk-free interest

rate of the foreign currency in its native country.

Reason for Studying the Continuous Model 2

Suppose the underlying asset is a portfolio of a large number of risky assets.

Since each risky asset in the portfolio pays dividend at a certain rate at certain times, the number of dividend payments for the portfolio would be large, and we can approximate it as continuous payment (dividend rate can be time-dependent).

Example

A company needs to buy M Euro at time t=T to pay a German company. To avoid any loss if Euro goes up, the company buys a call option of M Euro with expiration date t=T at rate K. How much premium should the company pay?

Example cont.

Over the same period, due to the risk-free interest ("dividend"),

1Euro in the local bank can grow to

where q is the risk-free interest rate in a German bank.

1Euro Euro1 ,q t

Example cont.- Therefore the value of 1 Euro in changes

as

Let B be a risk-free Bank of China bond. Its change in is

where and r is the risk-free interest rate in BOC bank.

( / )tS RMB Euro( / )tS u RMB Euro

( / )tS d RMB Euro

[ , ]t t t

[ , ]t t t

1 r t

( ) ( )t tB RMB B RMB

Example cont.--

In each interval , apply Δ-hedging strategy, i.e. to construct a portfolio

and select Δ, such that

is risk-free.

[ , ]t t t

V S t t

Example cont.---

Solve the system,

( )

u ut t t t

t t t t t t d dt t t t

t t t t t

V S uV S

V S d

V S

1, [ ]

( )

u du dt t t t

t t t t tu dt

V VV q V q V

u d S

Example cont.---

We assume dη<ρ<uη, so that

/ /,u d

d uq q

u d u d

0 , 1, 1u d u dq q q q

Example cont.----Since the price of the option at t=T ( in

RMB) is

where M is the required amount of Euro, and K is the agreed exchange rate.

let M=1, similar to before, using backward induction, we can get:

0( ) ( ) , (0 )NT TV M S K M S u d K N

Option Pricing (Dividend, call)

The pricing formula for dividend-paying European call option:

Where

^ ~ˆ( , , ) ( , , )N h

N hh h

S KV h q h q

~~ ^/

,d uq

q qu d

Option Pricing (Dividend, put)

The pricing formula for dividend-paying European put option:

^ ~ˆ( , , ) ( , , )N h

N hh h

SKp h q h q

Binomial Tree Method ofAmerican Option Pricing

American option pricing is different from European option pricing.

At each node

for American option, the price must satisfy the constraint

(1 ,0 )N hS h N N h

( )N h N hV K S

Backward Induction - American option pricing

Therefore for American option pricing (taking put option as example), its backward induction process is: n=N

n=N-1

( ) , 0N NV K S N

11

1max [ (1 ) ], ( ) ,

0

N N N NV qV q V K S

N

Backward Induction cont. If is given, then

where in each step, after A is calculated, it must be

compared with the payoff function B, be the larger of the two, and so on, until is arrived at.

(0 1)N hV N

1 11

1max [ (1 ) ], ( )

(0 1)

N h N h N h N hV qV q V K S

N h

dq

u d

00V

1N hV

A B

Another View of American Option

Suppose ud=1 the underlying asset price

can be written as

For simplicity, let In the plane (S,t) we construct a grid:

0 (0 )n nS S u d n

0 ( , 2, , 2, )n jjS S u j n n n n

0 1.S

American Option Grid

where

NoticeThen American put option pricing:

1

0

0

0

j j

n N

S S

t t t T

, 0, 1, ,

( / ), 0,1, , .

jj

n

S u j

t n t t T N n N

( , ).nj j nV V S t

11 1

1max (1 ) , ( )n n n

j j j jV qV q V K S

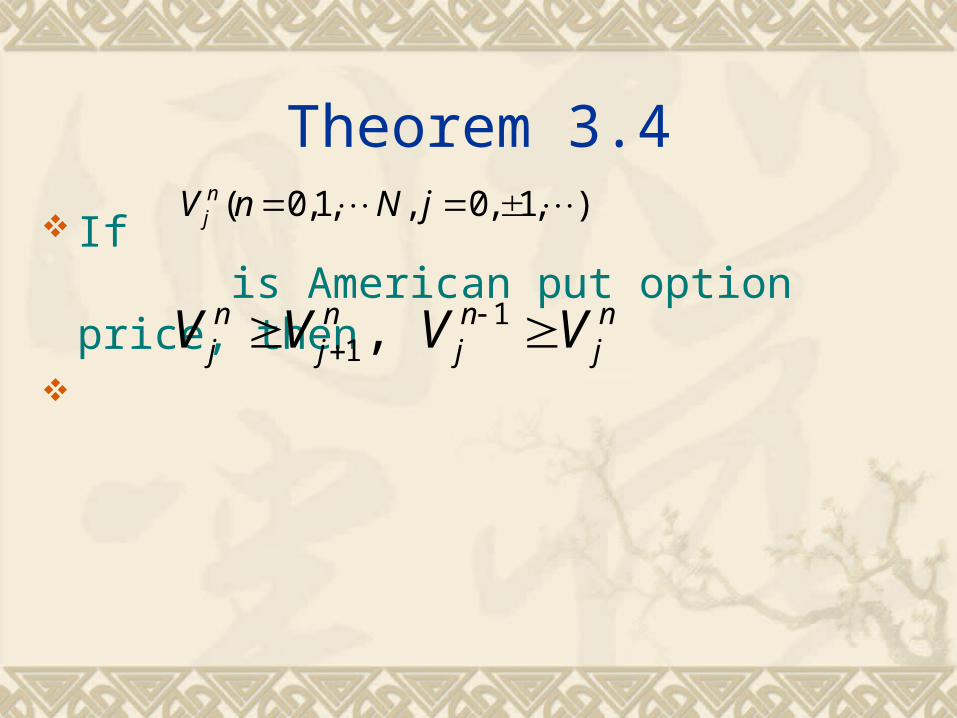

Theorem 3.4

If is American put option price, then

( 0,1, , 0, 1, )njV n N j

11,

n n n nj j j jV V V V

Theorem 3.5

(0 1), . .

when 1,

when ,

when 1,

n n

nn j j

nn j j

nn j j

t n N j j s t

j j V

j j V

j j V

Optimal Exercise Boundary – Free Boundary

t=T t

S

Stopping Region Continuation Region

Optimal Exercise Boundary

2 2

Continuation & Stopping Region In region Σ1, the option value is greater than the payoff

from exercising the option, the option holder should continue to hold the contract rather than early exercising it. Therefore Σ1 is called the continuation region.

In region Σ2, since

which means the option's expected return is less than the risk-free interest rate, the holder should stop the contract, i.e. early exercise the option immediately. Therefore Σ2 is called the stopping region.

1 11 11/ [ (1 ) ]n n n

j j jV qV q V

Optimal Exercise Boundary

is of great importance in finance, as the interface of the continuation and stopping, and is called the optimal exercise boundary.

Theoretically, American option holder should choose a suitable exercise strategy according to the above analysis to avoid loss.

( )S S t

American Call-Put Symmetry

Call-put parity does not hold for American options.

One naturally asks whether there exists other kind of relation between American call and put options.

American Call-Put Symmetry Example

An option as a contract gives its holder the right to exchange cash for stock (call option), or to exchange stock for cash (put option), at the strike price on the expiration date.

American Call-Put Symmetry Example -

We may regard the cash as a risk-free bond earning interests according to the risk-free interest rate, and regard the stock as a risky bond earning risk-free interests according to the dividend rate. Then we can see a certain symmetry exists between the call and put options:

i.e. for options (European or American) with the same expiration date, if the positions of S and K, and the positions of η and ρ are both swapped, the call option price and put option price should be equal.

( , ; , ; ) ( , ; , ; )C S K t P K S t

Theorem 3.6

(call-put symmetry) If ud=1, then for American options with the

same expiration date, relation

is true, where

( , ; , ; ) ( , ; , ; )C S K t P K S t

, (0 ).nt t n N

Theorem 3.7For American options with the same

expiration date, let denote the underlying asset price and strike price for the call (put) option respectively. If

then

where

( ) & ( )c p c pS S K K

/ /p p c cK S S K

( , ; , ; )( , ; , ; ) p pc c

c c p p

P S K tC S K t

S K S K

, (0 ).nt t n N

Summary

1. Have Introduced a discrete model---BTM to describe the underlying asset price movement, and have priced its derivatives (options) using this model.

2. Based on the arbitrage-free principle, using the Δ-hedging technique, have introduced a risk-neutral equivalent martingale measure. The BTM of option pricing has produced a fair valuation that is independent of any individual investor's risk preference.

Summary cont.

3. Using the BTM of American option, we have shown that there exist two regions for American put option: the continuation region and the stopping region, which are separated by the optimal exercise boundary.

4. For American options, although there is no call---put parity, there exists call-put symmetry, as for European options.

作业:P22 、 1 , 2 , 3 , 4