7 joint and coordinated audit - sai of colombia y peru.ppt

TRANSCRIPT

SPECIA AUDITSPECIAL AUDITOF THE BINATIONAL AUTONOMOUS

AUTHORITY OF THE WATER SYSTEM OF LAKEAUTHORITY OF THE WATER SYSTEM OF LAKE TITICACA, DESAGUADERO RIVER, POOPO LAKE AND SALT LAKE OF COIPASA ALTLAKE, AND SALT LAKE OF COIPASA - ALT

JANUARY 1996- DECEMBER 2006JANUARY 1996 DECEMBER 2006

I ORIGIN OF AUDITI. ORIGIN OF AUDIT

Through Binational Memorandum dated October 6Through Binational Memorandum dated October 6,2006, executed by the Ministers of Foreign Affairs ofBolivia and Peru, a binational audit of the ten-yearperformance of the Binational A tonomo s A thorit ofperformance of the Binational Autonomous Authority ofthe Water System of Lake Titicaca, Desaguadero River,Poopo Lake, and Salt Lake of Coipasa (ALT) was

d b d dagreed to be conducted.

2 1 GENERAL OBJECTIVE

II. OBJECTIVES AND SCOPE OF AUDIT

2.1 GENERAL OBJECTIVE

Determine the following: (1) binational projects and otherworks conducted by the ALT are related to the BinationalMaster Plan of the TDPS Water System in its severalstages; (2) These projects and works were conductedstages; (2) These projects and works were conductedaccording to the annual operating plans; and (3) Thefinancial resources allocated to the ALT by theG t f P d B li i f ti fGovernments of Peru and Bolivia for execution ofinvestment projects were used under the conditions andprocedures of financial management set forth in theprocedures of financial management set forth in theRegulations of Economic and Financial Management.Furthermore, determine if the ALT is meeting its sector-

l t d f ti i t l drelated functions concerning natural resources andenvironmental management.

2.2 SPECIFIC OBJECTIVES

2.2.1 Determine if binational projects and other works conducted bythe ALT and related to the Binational Master Plan of the TDPSW t S t i it l t d t d iWater System in its several stages were conducted inaccordance with the annual operating plans; determine if theseprojects and works were conducted within the quality, cost andi i d h i f h M Pl itime requirements and assess the impact of the Master Plan inthe objective of the project.

2 2 2 D t i if th f L i ti d Ad i i t ti2.2.2 Determine if the processes of Logistics and AdministrativeManagement of the allocated resources are within theframework of the regulations applicable to the project and meetthe criteria of cost efficiency efficiency and effectivenessthe criteria of cost-efficiency, efficiency and effectiveness.

III. SCOPE OF THE AUDIT

A Special Audit will be conducted from January 1, 1996 toDecember 31, 2006 and under the Peruvian Government AuditS d d (NAGU) d B li i G A di S d dStandards (NAGU) and Bolivian Government Audit Standards(NAG) as well as the Generally Accepted Audit Standards (GAAS).Consequently, this audit shall comprise selective checking ofq y, p goperations and records of the areas related to the project executionand management of the financial resources allocated by theGovernments of Peru and Bolivia for said periodGovernments of Peru and Bolivia for said period.

PARTICIPANTSPARTICIPANTS

REPRESENTATIVES OF THE COMPTROLLERSHIP GENERAL OF THE REPUBLIC OF PERU

SENIOR MANAGEMENT- SENIOR MANAGEMENT- AUDITING COMMITTEE

REPRESENTATIVES OF THE COMPTROLLERSHIP GENERAL OF THE REPUBLICREPRESENTATIVES OF THE COMPTROLLERSHIP GENERAL OF THE REPUBLIC OF BOLIVIA - SENIOR MANAGEMENT- AUDITING COMMITTEEAUDITING COMMITTEE

ALT ORGANIZATIONAL CHART

MINISTRY OF FOREIGN AFFAIRSPERU BOLIVIA

CHIEF EXECUTIVE OFFICER PERU BOLIVIA

Julián Isaac Barra Catacora (Eng.)

INTERNAL AUDITAlejandro Araoz E. (B.Sc.)

UNIT OF COMPREHENSIVE MANAGEMENT OF WATER RESOURCES

Freddy Lucio Loza de la Cruz (B.Sc.)

UNIT OF MASTER PLAN MANAGEMENTLuis Alberto Sánchez Aragones (Eng.)

PLANNING AND FINANCINGLuis Montes de Oca P. (B.Sc.)

MANAGEMENTAgustín Romero Estuco (CPA)

LEGAL COUNSELLINGCarlos Salamanca (B.Sc.)

ACCOUNTANCY AND TREASURYEdwin Fernández Pérez (B.Sc.)

HUMAN RESOURCESMapy Casapia Olaguivel (B.Sc.)

PROCUREMENT AND ANCILLARY

ADMINISTRATIVE AFFAIRSCarlos Salamanca Clavijo (B.Sc.)

LEGAL/TECHNICAL REGULATIONSEnrique Peñaranda Ulloa (B.Sc.)

PROCUREMENT AND ANCILLARY SERVICES

Marco Rivarola Frisancho

WAREHOUSESRoger Rosales Lozada

FIXED ASSETS

The ALT is located in the City of La Paz - Bolivia (CalleSanchez Lima No. 2653 – Sopocachi) and according toArticle 10 of the Bylaws, the Organization has thisFIXED ASSETS

Marco Zeballos Serna

SAFETY AND SECURITYJuan Martínez Velasco

Article 10 of the Bylaws, the Organization has thisstructure.

The Chief Executive Officer is Peruvian; the remainingofficers are partly Bolivian and partly Peruvian

IV DESCRIPTION OF THE ENTITY

1. The Entity

IV. DESCRIPTION OF THE ENTITY

The Binational Autonomous Authority of the Water System of LakeTiticaca Desaguadero River Poopo Lake and Salt Lake of CoipasaTiticaca, Desaguadero River, Poopo Lake, and Salt Lake of Coipasa(ALT) is an international public law entity with complete autonomy indecision-making and management in the technical, administrative-economic and financial spheres.economic and financial spheres.

The ALT is functionally and politically subordinated to the Ministries ofForeign Affairs of Peru and Bolivia. The ALT Chairman is under thegdirect supervision of the Chancellors of both countries and follows andmeets the joint political provisions thereof.

Article 1 of the Economic Financial Regulations states that the ALT: "is an

2. Economic Financial Management

Article 1 of the Economic Financial Regulations states that the ALT: is aninternational public law entity regulated by its own economic, financial, andresource management systems." These resources, according to Article 2,result from the following sources:result from the following sources:

• Allocation from the Governments of the Republics of Peru and Bolivia,agreed by the parties

• Self-generated management income• Non-refundable technical and financial cooperation of local andp

international organisations and international agencies• Donations and/or grants• Credits secured by government guarantee• Credits secured by government guarantee• Capital assets, goods and issues from national and international

conventions

3 Description and Cost of the Project3. Description and Cost of the Project

According to the document: "Updated Summary" of the BinationalProtection Master Plan ALT issued in August 1996 the works required forProtection Master Plan – ALT issued in August 1996, the works required forbasic regulation of the regional water system include:

• A control section in the International Bridge comprising 3 double-panelwagon gates (12.00 m x 5.00 m) and two channeling dams along the first300 m from the existing road to the gatesg g

• A 39-km channel dredged along the lake between Desaguadero andAguallamaya, with a trapezoid transverse cross-section base of 20 m anda slope of 5/1a slope of 5/1

• A control section in Aguallamaya comprising 4 gates (3 gates of 12.00 mx 5.00 m, and 1 gate of 2.00 m x 5.00) and a 2,100-m dam doublyoperating as dam and foundation for the road Jesus de Machaca Sanoperating as dam and foundation for the road Jesus de Machaca – SanAndres de Machaca

• 7 km for conditioning of the river bed by downstream dredging theA ll t l tiAguallamaya control section

V. LEGAL BASIS

Bylaws of the Binational Autonomous Authority of the Water System ofLake Titicaca, Desaguadero River, Poopo Lake, and Salt Lake ofCoipasa, approved by Legislative Resolution 26873 dated November 12,p pp y g1997.

Use of Funds and Records

Regulations for Economic and Financial Management of the BinationalAutonomous Authority of the Water System of Lake Titicaca,

S f CDesaguadero River, Poopo Lake, and Salt Lake of Coipasa, approved byLegislative Resolution 26873 dated November 12, 1997.

CRITICAL WORKS CONSIDEREDCRITICAL WORKS CONSIDERED IN THE MASTER PLAN

a) International Bridge Control Section (Regulation Work for Lake Titicaca))

. Gates

. Dams

b) Channel in the Desaguadero Lake (Dredging)

c) Aguallamaya Control Section. Gates. Dams. Dredging

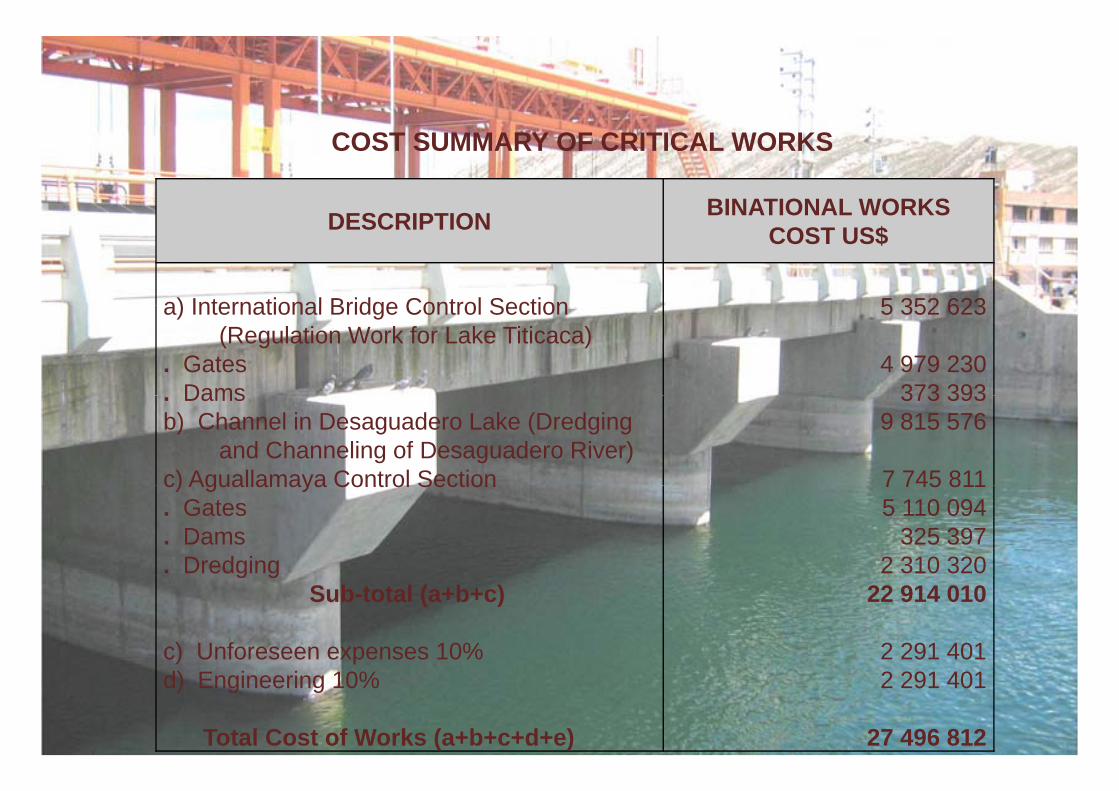

DESCRIPTION BINATIONAL WORKS

COST SUMMARY OF CRITICAL WORKS

DESCRIPTION COST US$

a) International Bridge Control Section 5 352 623a) International Bridge Control Section (Regulation Work for Lake Titicaca)

. GatesDams

5 352 623

4 979 230373 393. Dams

b) Channel in Desaguadero Lake (Dredging and Channeling of Desaguadero River)

c) Aguallamaya Control Section

373 3939 815 576

7 745 811c) Aguallamaya Control Section . Gates. Dams. Dredging

7 745 8115 110 094

325 3972 310 320g g

Sub-total (a+b+c)

c) Unforeseen expenses 10%

22 914 010

2 291 401d) Engineering 10%

Total Cost of Works (a+b+c+d+e)

2 291 401

27 496 812

CURRENT STATUS OF CIVIL WORKS

DESCRIPTION COST US$ STATUS$

BINATIONAL COMPONENTINTERNATIONAL BRIDGE CONTROL GATES (Regulation Work for Lake Titicaca) 5,352,623 Work completed (*)AGUALLAMAYA LAKE CHANNEL (Dredging) 9,815,576 Work in progress (*)AGUALLAMAYA CONTROL GATES 7,745,811 Not started (*)

NATIONAL WORKSLA JOYA CONTROL WORKS 2,081,000 Not startedSOLEDAD LAKE BYPASS CHANNEL 402,000 Not startedUPGRADE OF LA JOYA‐BURGUILLOS‐URU URU LAKE STRETCH 2,910,000 Not startedSOLEDAD LAKE DRAINAGE CHANNEL 517,000 Not startedURU URU LAKE DRAINAGE CHANNEL 950,000 Not startedSUB‐TOTAL 29 774 010SUB‐TOTAL 29,774,010UNFORESEEN EXPENSES 10% 2,977,401ENGINEERING STUDIES 10% 2,977,401TOTAL COST OF CIVIL WORKS 35,728,812Note

(*) Updated Summary of Master Plan as of August 2006

ALT MAIN WORKSALT MAIN WORKS

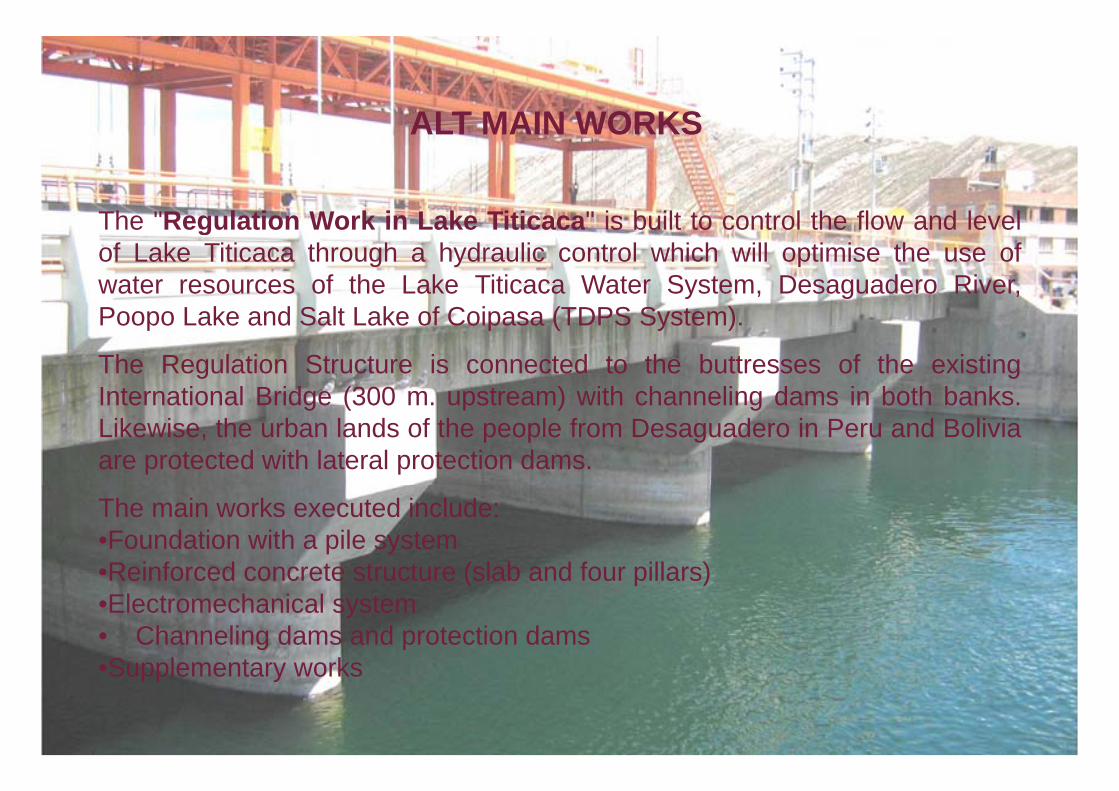

The "Regulation Work in Lake Titicaca" is built to control the flow and levelThe "Regulation Work in Lake Titicaca" is built to control the flow and levelof Lake Titicaca through a hydraulic control which will optimise the use ofwater resources of the Lake Titicaca Water System, Desaguadero River,Poopo Lake and Salt Lake of Coipasa (TDPS System).

The Regulation Structure is connected to the buttresses of the existingInternational Bridge (300 m upstream) with channeling dams in both banksInternational Bridge (300 m. upstream) with channeling dams in both banks.Likewise, the urban lands of the people from Desaguadero in Peru and Boliviaare protected with lateral protection dams.

The main works executed include:•Foundation with a pile system•Reinforced concrete structure (slab and four pillars)Reinforced concrete structure (slab and four pillars)•Electromechanical system• Channeling dams and protection dams•Supplementary works•Supplementary works

DOCUMENT DATE DESCRIPTIONDOCUMENT DATE DESCRIPTION

Work Contract JUL/01/1997Has been signed by the Binational Authority of the TDPS Water System and CEFOISA - E. REYNA C. S.A. for the execution of Regulation Works in Lake TiticacaRegulation Works in Lake Titicaca

Addendum 1 JUL/01/1997Supersedes the provisions in first paragraph of Clause 18 of the Agreement where the submittal of a bond or bank guarantee is defined as performance bond.

Addendum 2 OCT/16/1997

Extends the date of commencement of the Works for no later than November 15, 1997, without acknowledging any general expenses or other benefits in favor of the Contractor. This is so because the C t t ill i t d bt i it l l th i ti t t iContractor will register and obtain its legal authorization to operate in Bolivia, and this requirement was not considered in the Bidding Terms.

Determines the Economic Intervention in the Work and the application terms since there has been a gap in the work progress above 25% in

Addendum 3 MAY/18/1998terms since there has been a gap in the work progress above 25% in relation to the schedule of works, and since the Contractor did not timely mobilize the equipment required to execute the work, particularly the equipment concerning pile-fixing.

G SIMA PERU S A ( b ) lAddendum 4 JUN/16/1999

Grants to SIMA - PERU S.A. (sub-contractor) a supplementary advance payment of US$ 142,474.21 for equipment and material import for the hoisting system components of the Regulation Work in Lake Titicaca, based on the submittal of a letter of guarantee .

The work "First-Stage Dredging and Channeling of DesaguaderoRiver" considered in the Master Plan of the Autonomous Authority ofRiver considered in the Master Plan of the Autonomous Authority ofLake Titicaca, Desaguadero River, Poopo Lake, and Salt Lake ofCoipasa (ALT) comprises reconditioning of the Desaguadero river bed,by digging up a trapezoid cross-section with a base of 20 m andslopes of 1:5 up to the mark Km 37+200 in the stretch of Laguna, andother trapezoid cross-section with a base of 20 m and slopes of 1:2 upp p pto the mark Km 67+764, which was later changed to a width of 40 m.

This digging shall allow for a maximum flow of 250 m3/s throughThis digging shall allow for a maximum flow of 250 m3/s throughDesaguadero River. This flow shall be reached when the Lake Titicacalevel is above the 3810.79-masl level, which involves a total earthmovement of 3,516,754.97 m3 to reach the section structure anddesign grazing starting at the 3806.00-masl level of the floor of thegates located in the International Bridge in Desaguadero.g g g

The goal of the Desaguadero River Dredging is to dig up the loose material in the Aguallamaya Lake Channel from the mark Km 0+000 in the Internationalthe Aguallamaya Lake Channel from the mark Km 0 000 in the International Bridge to the mark Km 37+200 in Aguallamaya (a place where the water body of Lake Titicaca ends) and from this mark by the Desaguadero River to the mark Km 67+764 in Nazacara.

Works are scheduled to start in Nazacara, that is to say, a downstream-upstream direction for the construction process.p p

STRETCH STARTPROGRESS

ENDPROGRESS

SCHEDULED VOLUME COMMENTSPROGRESS PROGRESS VOLUME

Aguallamaya Channel 0+000 37+200 902,831.70 ORLT – AguallamayaDesaguadero River 37+200 67+764 2,565,777.70 Aguallamaya – Nazacara

LOCATION AND ORGANIZATION OF WORK

The Auditing Committees of Peru and Bolivia were provided with spaciousThe Auditing Committees of Peru and Bolivia were provided with spaciouspremises within the ALT, equipped with a printer, photocopier, two desktops andfurniture.

Following the arrangements made in La Paz, it was agreed that the audit periodwill be January 1996 - December 2006 according to the BinationalMemorandum dated October 6, 2006. Furthermore, it was agreed that the

h i l i f h i j f h M Pl d h itechnical issues of the investment projects of the Master Plan and theirenvironmental impact will be responsibility of the CGRP and the work executionfinancial assessment of income and expenses shall be the responsibility of theCG f th R bli f B li iCG of the Republic of Bolivia.

The sample to assess, the "Regulation Work in Lake Titicaca" and the "FirstStage Dredging and Channeling of Desaguadero River" were selected becauseg g g g gof the work progress and complaints. As to the Bolivian part, the financialauditors stated in the Audit Planning Memorandum (MPA) that the ALT controlfacility was inefficient to select the samples; therefore, the sample reached a95% ratio.

MEMBERS OF THE BOLIVIAN AUDITING COMMITTEE

MEMBERS OF THE PERUVIAN AUDITING COMMITTEE

In Bolivia a request for information from the entity is

REQUESTS FOR INFORMATION

In Bolivia a request for information from the entity ismade orally, and only when it is absolutely necessary or when it is necessary toreiterate a request, it is made in writing, which is a completely different procedurethan in Peru As this was a particular case the request was made in writing andthan in Peru. As this was a particular case, the request was made in writing andwas duly signed by the auditor in charge in the Peruvian part, and by thesupervisor of the Bolivian part.

The requests for information at the level of Ministries or other hierarchicalinstances were made through the Line Managers (Peru) or Assistant Comptrollers(Bolivia), depending on the case.( ), p g

Due to administrative deficiencies, the ALT's reply to requests submitted by theCommittee was slow, and sometimes never answered.

According to the Planning Memorandum approved by both Comptrollers the

AUDIT TERMS

According to the Planning Memorandum approved by both Comptrollers, thePeruvian Committee was scheduled to complete its field work on May 8, 2008;however, due to the Auditing Committee´s work limitations, an extension wasapproved until May 20 2008approved until May 20, 2008.

The Bolivian Committee is still working. By means of Note SCAE/1654/2008dated May 26, 2008, the Comptroller General of the Republic of Bolivia OsvaldoE. Gutierrez Ortiz informed the Comptroller General of the Republic of Peru thatthe standardisation of the audit conclusions was still pending since the review ofth fi i l t till i th f it i ti t d th t ththe financial aspects was still in progress; therefore, it is estimated that theAuditing Committee's responsible staff of the Comptrollership General of theRepublic of Bolivia will travel to the City of Lima to put an end to this matter.

INSPECTION VISITS AND PROCEDURES

An on site visit to the critical works included in the Master Plan was made onFebruary 21, 2008 with the participation of representatives of bothComptrollerships General and the ALT. It was also agreed that the inspectionvisits to the works should be jointly made as often as possible. Thus theinspection visits to the work "First-Stage Dredging and Channeling ofDesaguadero River" and the inspection visits to the assets (machinery) werejointly made.

The procedures have been developed in the same way in Peru and Bolivia,and this is reflected in the work documents. Similar coding is used in Boliviaand Peru.and Peru.

ASPECTS TO BE ASSESSED BY EACHASPECTS TO BE ASSESSED BY EACH COMPTROLLERSHIP GENERAL

THE PERUVIAN COMMITTEE ASSESSED THE TECHNICAL ISSUESINCLUDING SUSTAINABILITY OF TECHNICAL APPRAISALS ADDITIONALINCLUDING SUSTAINABILITY OF TECHNICAL APPRAISALS, ADDITIONALBUDGETS AND TERM EXTENSIONS.

THE BOLIVIAN COMMITTEE ANALYSED THE FINANCIAL EXPENSESINCLUDING EXPENSES AND PAYMENT VOUCHERS OF APPRAISALSINCLUDING EXPENSES AND PAYMENT VOUCHERS OF APPRAISALS,ADDITIONAL BUDGETS AND TECHNICAL AND ECONOMIC SETTLEMENTOF THE WORKS.

INSPECTIONS

FINDINGS AND REPORTING

After some appraisals were made, it was evident that Bolivian auditors donot usually report findings, but prepare a draft report which is submitted tothe authorities allegedly responsible for said issues so they can providethe authorities allegedly responsible for said issues so they can providethe required clarifications. A Final Report is then submitted.

Th ft t i iti ll d ith th ffi i h fThen, after some arrangements are initially made with the officers in charge ofboth Committees, a report is prepared; however, after the audit, someirregularities were disclosed which deserved the filing of civil and criminalproceedings Therefore lawyers will be required to prepare special reports andproceedings. Therefore, lawyers will be required to prepare special reports andinform of their work involved in this matter.

CONCLUSIONS

1. At present the planning stage is completed.p p g g p2. The Peruvian Committee is still assessing the technical aspects of the

works selected in the sample.

3. In the case of Bolivia, sampling was more complex because this countryhas internal guidelines for financial sampling, and in this particular case,according to Guideline G/AU-016, "Sampling in Audit", the risk of the controlstructure is high. For this reason, it is still doing field work and reviewingthe financial aspects of the ALT.

4 O th fi ld k i l t d th t d di ti f i d4. Once the field work is completed, the standardisation of expenses incurredin appraisals, additional budgets and economic and technical settlement ofthe works shall be conducted.

5. Assessments are still in progress to determine the sustainability of the useof public resources.