7th annual andean conference - marzo 2013

DESCRIPTION

7th Annual Andean Conference - Marzo 2013TRANSCRIPT

NUEVAPOLAR

March 2013

Santiago, Chile

7th ANNUAL ANDEAN

CONFERENCE 2013

Company Overview

Where do we come from

October 2012: US$280 millions capital increase

May 2012: Agreement with Chile´s Customer Protection Agency (SERNAC , Class action)

November 2011: Settlement

with creditors is reached

August 2011: New CEO is appointed (Patricio Lecaros)

July 2011: New Board of Director takes office

Jun 2011: La Polar goes into a severe financial crisis

3

Aconcagua Plan

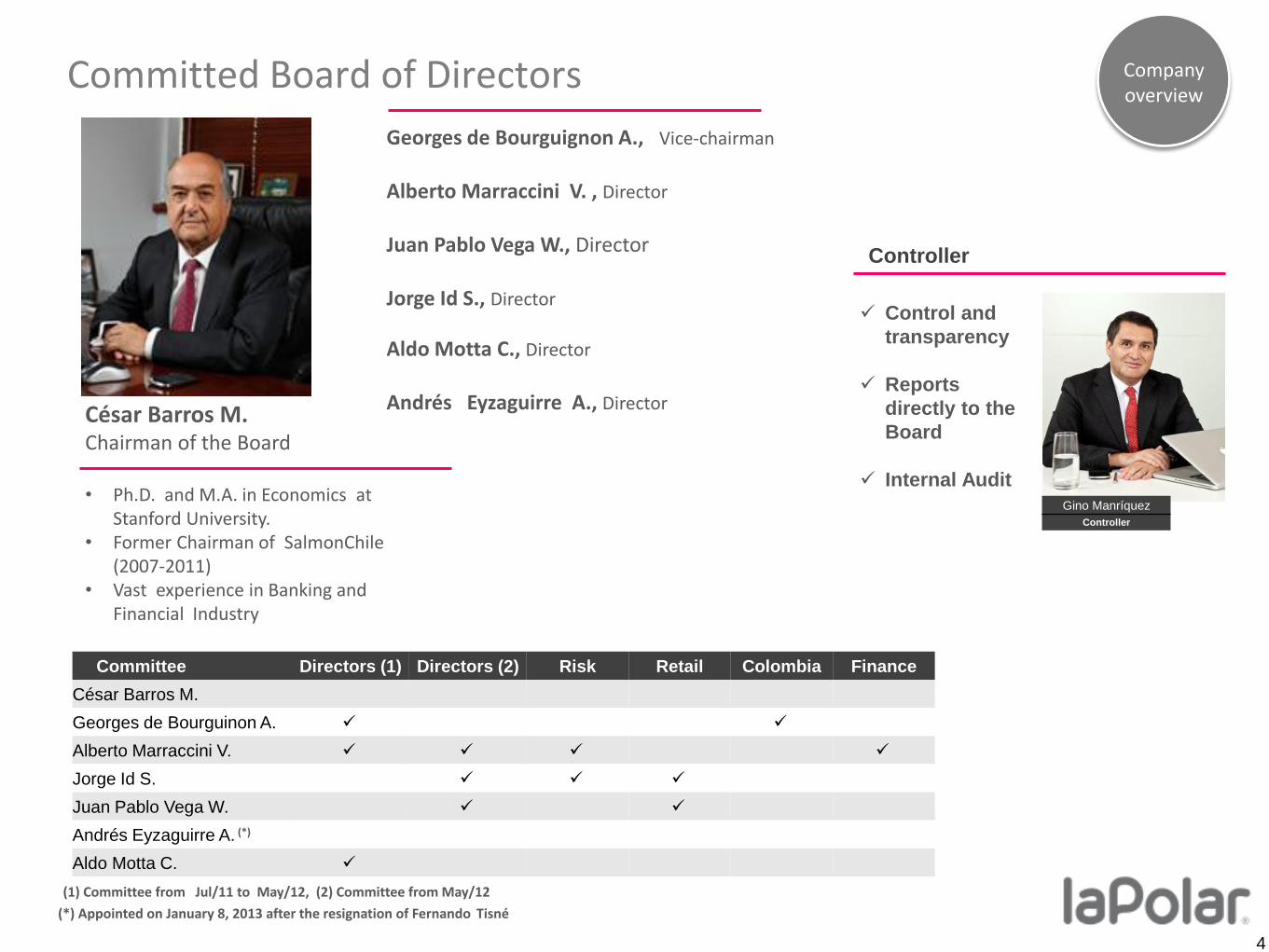

Committed Board of Directors Company overview

Gino Manríquez

Controller

Controller

Control and

transparency

Reports

directly to the

Board

Internal Audit

Committee Directors (1) Directors (2) Risk Retail Colombia Finance

César Barros M.

Georges de Bourguinon A.

Alberto Marraccini V.

Jorge Id S.

Juan Pablo Vega W.

Andrés Eyzaguirre A. (*)

Aldo Motta C.

Georges de Bourguignon A., Vice-chairman

Alberto Marraccini V. , Director

Juan Pablo Vega W., Director Jorge Id S., Director

Aldo Motta C., Director

Andrés Eyzaguirre A., Director

César Barros M. Chairman of the Board • Ph.D. and M.A. in Economics at

Stanford University. • Former Chairman of SalmonChile

(2007-2011) • Vast experience in Banking and

Financial Industry

4

(*) Appointed on January 8, 2013 after the resignation of Fernando Tisné

(1) Committee from Jul/11 to May/12, (2) Committee from May/12

First-class team with a strong experience in the industry

New Management Team

Francisco

Martínez

CEO Colombia

Andrés Molina

Apparel Mngr.

Rodrigo Karmy

Home and Electronics

Mngr.

Eduardo Lobos

Planning Mngr.

Marcelo Acosta

Sales and Distrib.

Mngr.

Carlos Arredondo

Logistics Mngr.

Sergio López

Risk Mngr.

Claudio Sierpe

Costumers and Payment

Mngr.

Fernado Silva

Insurance Brokerage

Mngr.

Enrique Vitar

Collecting Mngr

Álvaro Araya

CFO

Ricardo Rubio

IT Mngr.

Olivia Brito

H.R. Mngr.

Rodrigo Nazer

Marketing Mngr.

Andrés Escabini

Legal Mngr.

Colombia CEO

Patricio Lecaros

CEO

CEO

+ 23 years of exp. Ripley, C&I, Quintec

+ 11 years of exp. SQM

+ 17 years of exp. Ripley, Hites

+ 16 years of exp. Epson Chile

+ 18 years of exp. Falabella

+ 22 years of exp. La Polar, BCI + 21 years of exp.

Ripley Johnson

+ 20 years of exp. Ripley + 30 years of exp.

Hites and Scotiabank

+ 27 years of exp. Din, Conosur,

Ripley

+ 34 years of exp. Banco Estado, others

+ 28 years of exp. Banefe, B. Falab.,

Johnson

+ 21 years of exp. Servipag and Corpgroup

+ 27 years of exp. Salcobrand

+ 9 years exp. La Polar

+ 11 years of exp. V. Undurraga

Company overview

5

… with 9% Market Share in Sales

4th Player in Department Stores …

Market Share by Revenues (Sept 2012 LTM)

Monthly Revenues by Selling Space (Sept 2012 LTM) Number of Department Stores

Relevant Market Share in Chile

The retail market in Chile has significant

barriers to entry

La Polar has smaller stores, with an

average of 4,021 m2 per store

Source: Company Reports

N° UF/M2

Source: Company reports

Cencosud: includes Johnson and A. Paris

UF Unidad de Fomentto (Indexed Unit of Account Chilean Peso)

6

Company overview

6

Avg.

4,021m2 Avg..

6,777m2

Avg.

6,634m2 Avg.

2,967m2

Avg..

6,384m2

Avg.

6,214m2

For more information about the Chilean Retail Industry please see

appendix 2

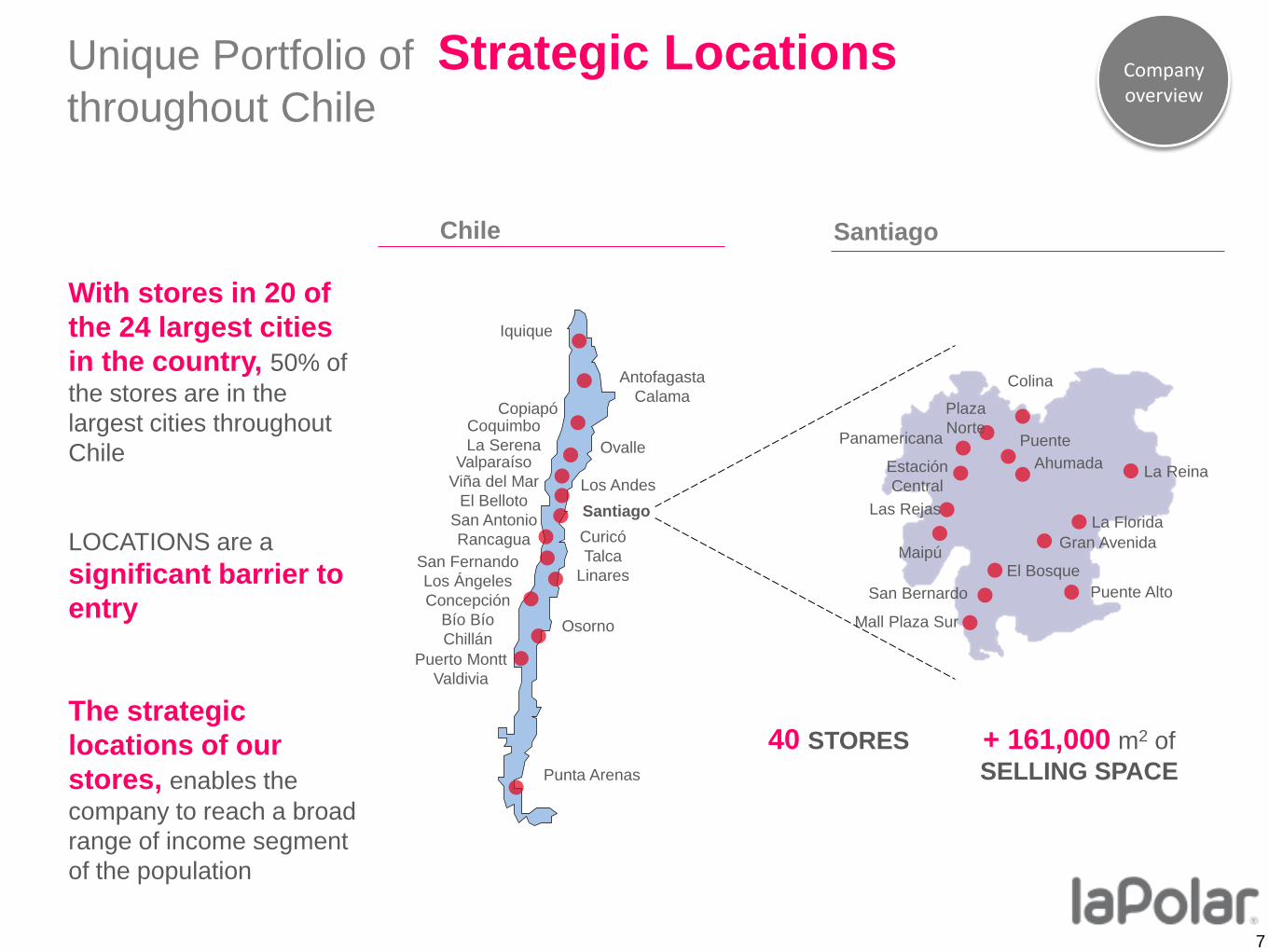

Unique Portfolio of Strategic Locations throughout Chile

Chile

40 STORES

Iquique

Antofagasta

Calama

Punta Arenas

Copiapó

Osorno

Puerto Montt

Valdivia

Coquimbo

La Serena Ovalle Valparaíso

Viña del Mar

El Belloto

San Antonio

Rancagua

Los Andes

Santiago

San Fernando

Los Ángeles

Concepción

Bío Bío

Chillán

Curicó

Talca

Linares

Colina

Plaza

Norte

Estación

Central

Puente

Ahumada

Las Rejas

Maipú

Panamericana

La Reina

La Florida

Gran Avenida

Puente Alto

Mall Plaza Sur

San Bernardo

El Bosque

+ 161,000 m2 of

SELLING SPACE

LOCATIONS are a

significant barrier to

entry

The strategic

locations of our

stores, enables the

company to reach a broad

range of income segment

of the population

Santiago

With stores in 20 of

the 24 largest cities

in the country, 50% of

the stores are in the

largest cities throughout

Chile

Company overview

7

La Polar, a strong Brand Rebounding Established in 1920, the brand has been present in the Chilean market for almost a century

Sales show a significant recovery, reaffirming our BRAND VALUE

Customers are one of the most valuable asset of the company

December 22/2012 was the best- selling day in LA POLAR HISTORY

Company Overview

Revenues Performance, a strong recovery after the crisis Same Stores Sales($ billion)

8

Business Overview

New Business Model … … Retail the Core Business of the Company New products – brand mix

55% sales from Apparel and Shoes

30% sales from Private Labels

New store concept

US$40 million in Capex in the next 2 years, for remodeling stores

Searching for new premium customers

Business overview

10

Monthly Revenues (recovering the focus in retail) UF/m2” % of Revenues

by Source

Attracting new customers

New credit card

New credit policy

New collection policy

Business overview

New Visa / Master La Polar credit card

New Benefit Plan

La Polar Credit Card approved by SBIF

New financial regulations in Chile

Aconcagua Plan

Decrease Risk rate (1)

Reducing the financial risk…

12%

Source: La Polar

453,473 customers with LA POLAR CREDIT CARD (TLP) with debt

11

(1) Provisions stocks /Gross receivables

Capex Program (US$ millions)

Capex Program for 2013 and 2014

Remodeling 14 stores in Chile of aprox. 100,000 m2

Opening 6-8 new stores in Colombia

12

2013-2014

Chile

Remodeling and others 50

Colombia

New stores 60

Total 110

Remodeling Stores in Chile 2013 -2014 100,000 m2 with a CAPEX US$40 million

13

Jan-13

2 stores

April-13

3 stores 1 store

Jun-13 Aug-13

3 stores 7 stores

First half 2014

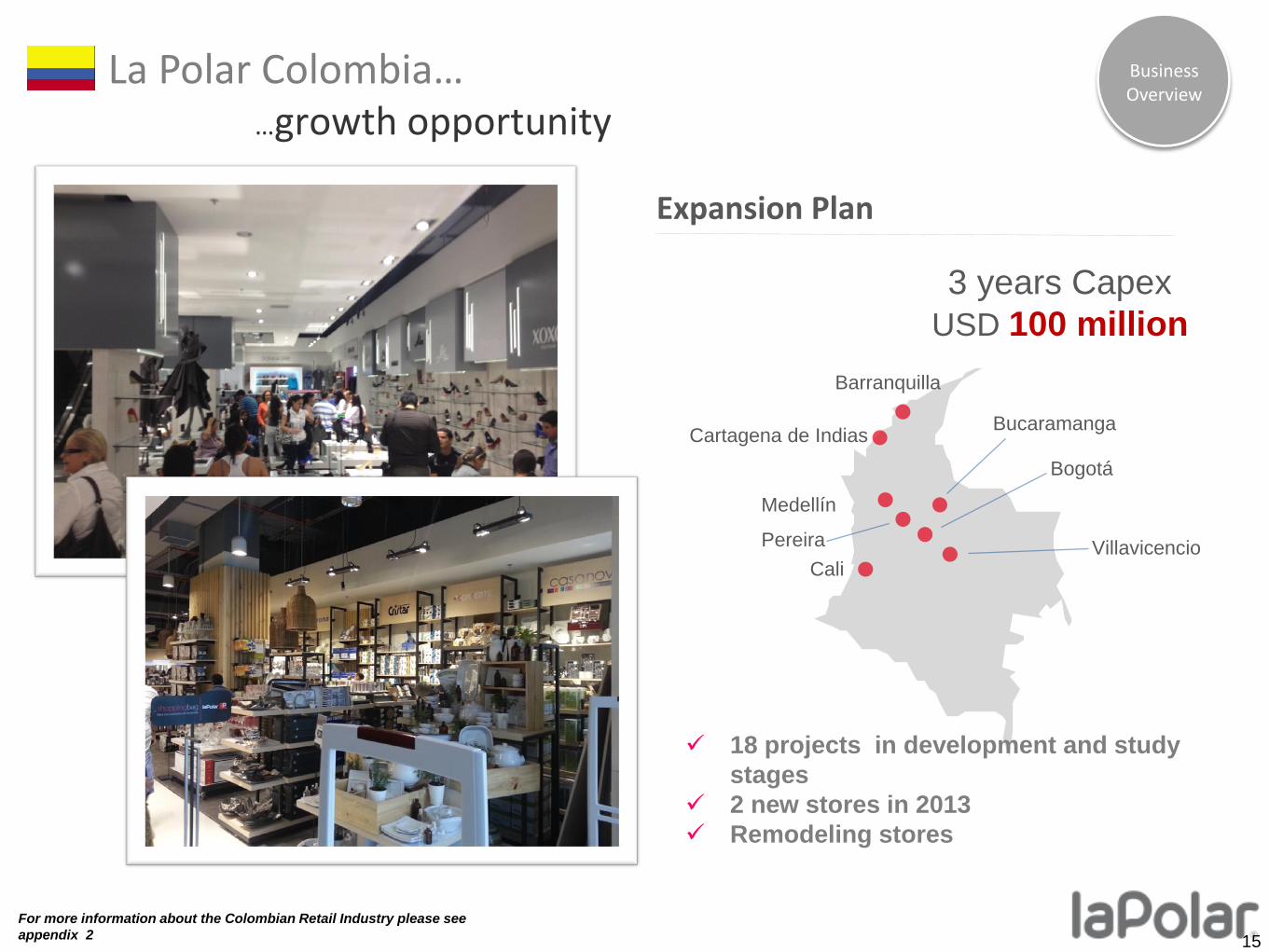

La Polar Colombia… …growth opportunity

Stores

Floresta

Opening: November 2011

Los Molinos

Opening: October 2011

Centro Mayor

Opening: October 2010

Carabobo

Opening: August 2011

Bucaramanga

Mall Cacique

Opening : November 2012

Area of 6,103 m2

Business Overview

New Store

14

La Polar Colombia… …growth opportunity

Expansion Plan

Barranquilla

Cartagena de Indias

Medellín

Pereira

Cali Villavicencio

Bogotá

Bucaramanga

18 projects in development and study

stages

2 new stores in 2013

Remodeling stores

3 years Capex

USD 100 million

Business Overview

15

For more information about the Colombian Retail Industry please see

appendix 2

Aconcagua Strategic Plan

Aconcagua

La Polar has set specific goals for the Chilean operation, for the short and medium term, to be achieved in 2014

Strategic Plan

17

ACONCAGUA Sept. 2012 LTM

Monthly retail revenues in Chile (UF/M2) 10 6.5

Retail Direct Margin 30% 21%

Apparel and shoes (% sales retail) 55% 54%

Private labels (% sales retail) 30% 23%

SG&A expenses / Retail revenues 30% 39%

Financial revenues/retail revenues 30% 23%

Risk rate 12% 15%

Sales % with LP credit card 50% 49%

Retail Ebitda margin 10% -5.3%>

Financial Highlights

Plan Aconcagua

Financial Performance Key indicators show an increase in revenues

Income Statement Retail Sales in Chile

Ajusted EBITDA Margin (1) over Chile Retail

(1) EBITDA adjusted nonrecurring expenses

(2) Business Plan

CLP Billion Plan Aconcagua

(2)

(2)

+7% +4%

19

Company overview Financial Highlights

+5%

19

(CLP Billion) 1Q ’12 2Q ’12 3Q ’12

REVENUES 81.1 91.6 86.5

Retail 64.8 76.4 72.1

Financial 16.3 15.2 14.4

Gross profit -7.2 20.4 19.7

EBITDA -32.4 -5.5 -8.9

Chile -29.8 -2.2 -5.4

Colombia -2.7 -3.3 -3.5

Adjusted EBITDA (1)

-10.6 -4.7 -7

Chile -6.9 -1.4 -3.5

Colombia -2.7 -3.3 -3.5

Net Earnings -34.9 -10.2 -13.6

Financial Debt Restructuring

Financial Debt

Bond Amortization Profile (CLP$ billion)

20 20

Senior Bond

Amortization Semiannual starting in

2015

Interests From 2013 to 2022 with

a rate between 4% and 10%

Junior Bond (UF)

Amortization One coupon in 2032

Interests No interest payments

Tranche C (PS 27)

Amortization Semiannual starting in

July 2018 until July 2024

Interests BCP 10 Rate + 1% starting

July 31, 2013

Deuda antigua:

• Créditos

Bancarios • Bonos • Efectos de

Comercio

$ 445

PS 27 $ 25

Bono Junior

$ 249

PS 27

$ 25

Bono Senior

$ 196

Co

nve

nio

Ju

dic

ial P

reve

nti

vo

14,1 %

Bono Senior

$ 136

Utilidad Senior:

$ 60

$ 18

Utilidad

Junior:

$ 231

$ 20

CJP separa la deuda en 2 Bonos. Senior y Junior

18,1%

9,6%

Deuda total: $470

Nueva Deuda se contabiliza a descuento

Diferencial con valor nominal es utilidad

del ejercicio.

Tasa Descuento

Deuda IFRS:

$174

Utilidad IFRS:

$296

IFRS, valorización nueva deuda descontando flujos

a tasas de mercado.

Tasa promedio:

14,9%

PS 27 : $5

69%

7 %

81%

7 nov 2011 16 oct 2012

CJP: Convenio Judicial Preventivo firmado el 7 de noviembre del 2011

PS 27: Crédito Banco BCI, garantizado en 1,82 veces con Cartera Normal de La Polar

HIGHLIGHTS

NEXT STEPS

1Q 2013: New web page for Investors www.nueva-polar.cl

March 20, 2013: 2012 Financial Statements

March 22, 2013: Conference Call 4Q 2012 Results

Investor Relations Contact: María Paz Ortega,,Head of Investor Relations Phone (562) 2383226 ([email protected])

22

December 2012: release credit card restrictions from

regulator (SBIF)

December 2012: New Senior and Junior bond filling as

part of the Settlement

January 2013: NUEVAPOLAR part of the IPSA

Chilean Stock Exchange Index

January 2013: Customer Compensation Plan

(SERNAC)

January 2013: Remodeling (Ahumada and Gran

Avenida)

Appendix 1

Full renovation of the apparel department

New mix of exclusive brands 2.0

Increase square meters of exclusive brands in stores

Improvements in the purchasing process

New design department

New mix of private brands and local suppliers

Products

24

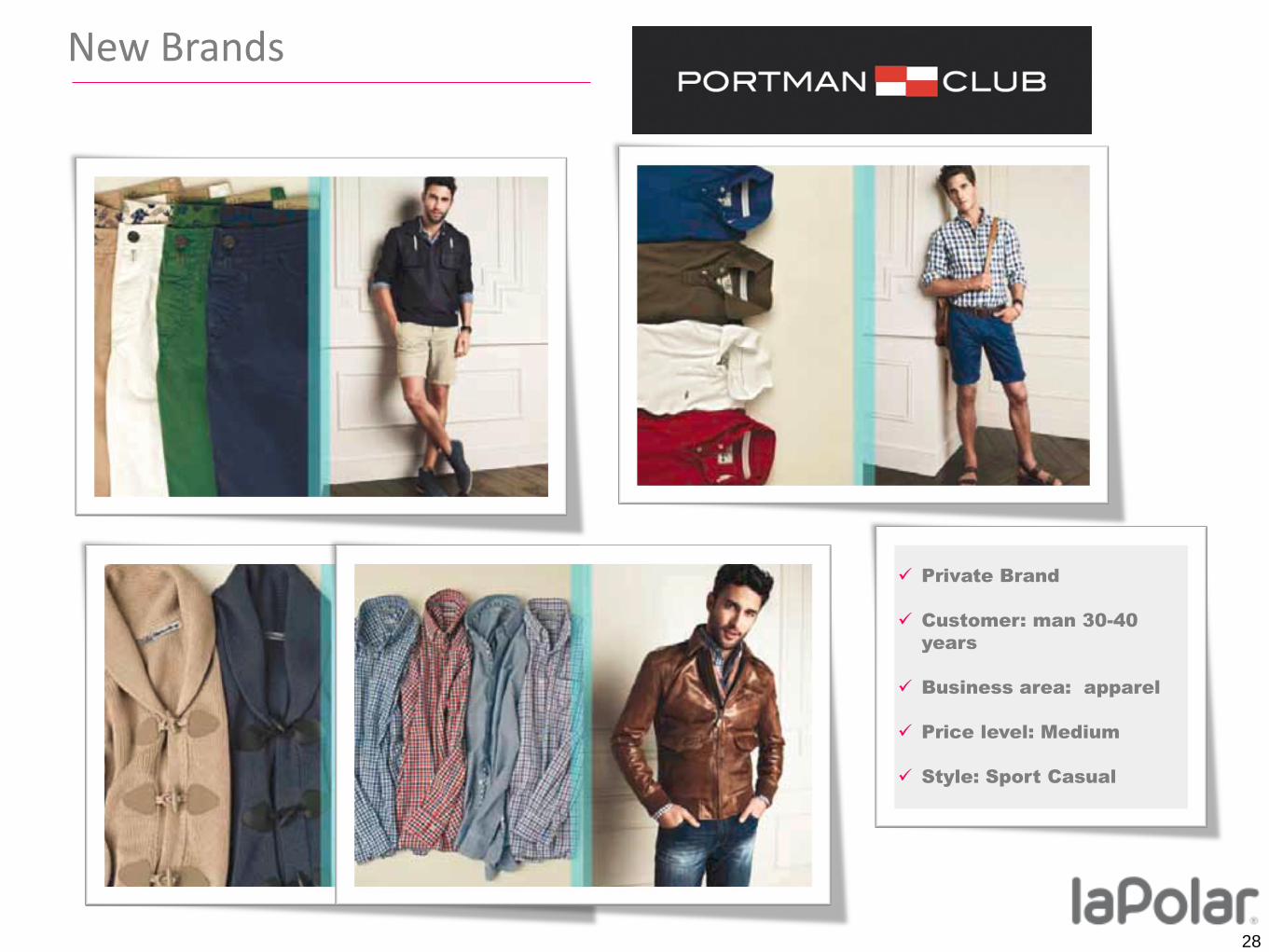

New Brands

Private Brand

Customer: woman 28-35

years

Business area: apparel,

accesories, shoes,

handbags and home

Price level: Medium–High

Style: Sport Fashion

251

}

Private Brand

Customer: women 18-25 years

Business area: apparel, and shoes

Price level: Medium–High

Style: Sport casual

New Brands

26

Private Brand

Customer: woman and man

18-25 years

Business area: apparel

Price level: Medium – High

Style: Sport Casual

New Brands

27

New Brands

}

Private Brand

Customer: man 30-40

years

Business area: apparel

Price level: Medium

Style: Sport Casual

28

New Store Proposal

Change of image/ layout

Remodeling 100.000 m2 in

the next 2 years

Capex: USD 40 MM

1st place award: Shop window of the year by the Santiago Chamber of Commerce

29

Store proposal main goals are….

Increase sales and returns by m2

Improve visual merchandising to make more efficient takeoffs spaces

Upgrade stores

Increase market share

30

This presentation contains forward-looking statements, including statements

regarding the intent, belief or current expectations of the Company and its

management. The forward-looking statements are not guarantee of future

performance and involves a number of risks and uncertainties including, but not

limited to, the risks detailed in the company’s financial statements, and the fact

that actual results could differ materially from those indicated by such forward-

looking statements.

Disclaimer