a crisis, what’s the use, what’s the purpose? impact of the crisis on insurance and reinsurance...

TRANSCRIPT

A crisis, what’s the use,what’s the purpose?

Impact of the Crisis on Insurance and Reinsurance

Michel M. LièsMember of the Executive Committee, Swiss Re

Monte Carlo, 8 September 09

Agenda

RVS Monte Carlo 2009Michel M. Liès

Looking back: impact of the crisis on insurance and reinsurance

The here and now

Looking ahead: winners and opportunities

Slide 2

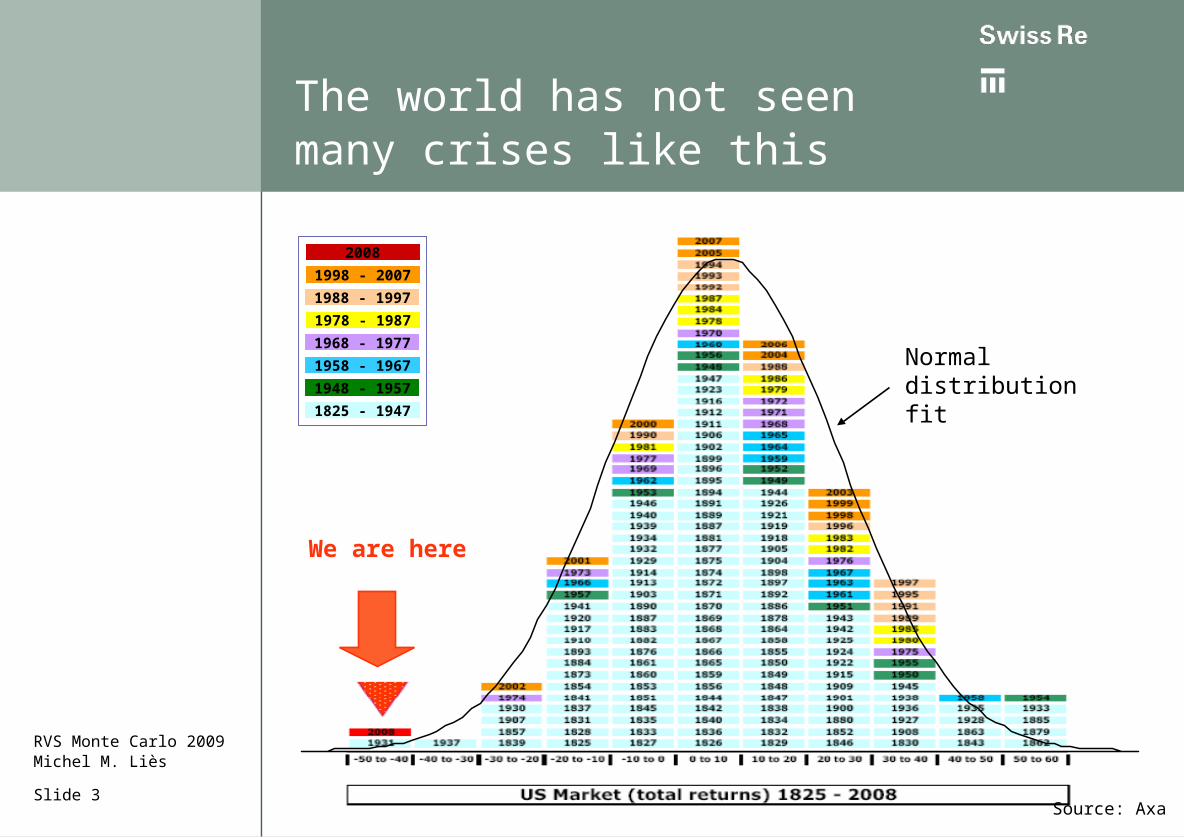

Source: Axa

We are here

Normal distribution fit

1825 - 1947

1948 - 1957

1958 - 1967

1968 - 1977

1978 - 1987

1988 - 1997

1998 - 2007

2008

Slide 3

RVS Monte Carlo 2009Michel M. Liès

The world has not seen many crises like this

Financial Services Industry: after-crisis market value loss

-46%

-44%

-72%

-52%

-38%

-41%

-46%

-50%

-55%

-60%

-45%

-80% -60% -40% -20% 0%

US

Western Europe

Japan

Canada

Australasia

China

India

Other Asia

Central and Eastern Europe

Middle East and Africa

Latin America

Across geographies

-56%

-61%

-75%

-64%

-46%

-36%

-39%

-52%

-80% -60% -40% -20% 0%

Wealth mgmt. & Life insurance

Consumer finance/monolines

Diversifieds/ Bancassurers

Banks

Capital markets players

Service providers

Reinsurance

P&C/Mixed insurance

Across FS sub-industries

Market value loss of top-400 FS companies between 31 July 2007 and 31 December 2008

Source: Datastream, Oliver Wyman

Market value loss was universal across sectors

Slide 4

RVS Monte Carlo 2009Michel M. Liès

Banking versus insurance - systemic crisis versus solvency issue

Issues Insurers Banks

Main problem Losses on investment portfolio and on shareholder capital

Interbank market collapsed

Operational problems Business as “normal”: cover provided and claims paid

Banking system close to collapse

Trust in the system No indication for policyholders losing trust – no run on insurers

Run on the bank prevented by Central banks’ guarantees

Government support Confined to very few cases

Broad intervention of central banks and governments

Slide 5

RVS Monte Carlo 2009Michel M. Liès

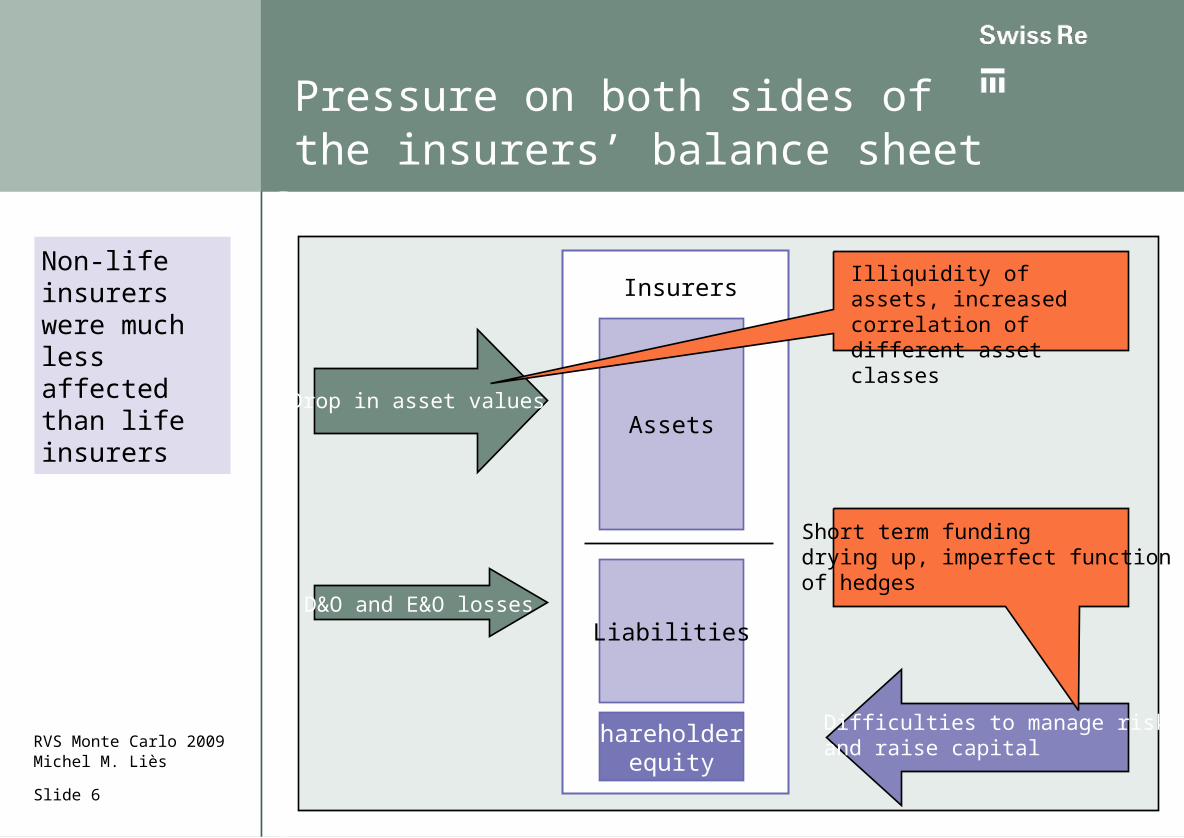

Pressure on both sides of the insurers’ balance sheet

Assets

Liabilities

Insurers

Shareholder equity

Slide 6

Drop in asset values

D&O and E&O losses

Non-life insurers were much less affected than life insurers

Illiquidity of assets, increased correlation of different asset classes

Short term funding drying up, imperfect functionof hedges

Difficulties to manage riskand raise capitalRVS Monte Carlo 2009

Michel M. Liès

Strong drop in shareholder equity

Non-life insurers lost 15-20% and Life insurers 30-40% of their shareholder capital

Capital costs to remain high; access to capital markets likely to remain restricted

Reinsurance is available – but capacities are limited, as well

The government as capital provider of last resort – a wild card

Shareholder’s Equity,Index June 2007=100, USD*

Key aspects

Sources: Company reports, Bloomberg, Swiss Re Economic Research & Consulting

*30 major insurers

60

70

80

90

100

110

Dez 06 J un 07 Dez 07 J un 08 Dez 08 J un 09E

Slide 7

RVS Monte Carlo 2009Michel M. Liès

Agenda

RVS Monte Carlo 2009Michel M. Liès

Looking back: impact of the crisis on insurance and reinsurance

The here and now

Looking ahead: winners and opportunities

Slide 8

The here and now

Slide 9

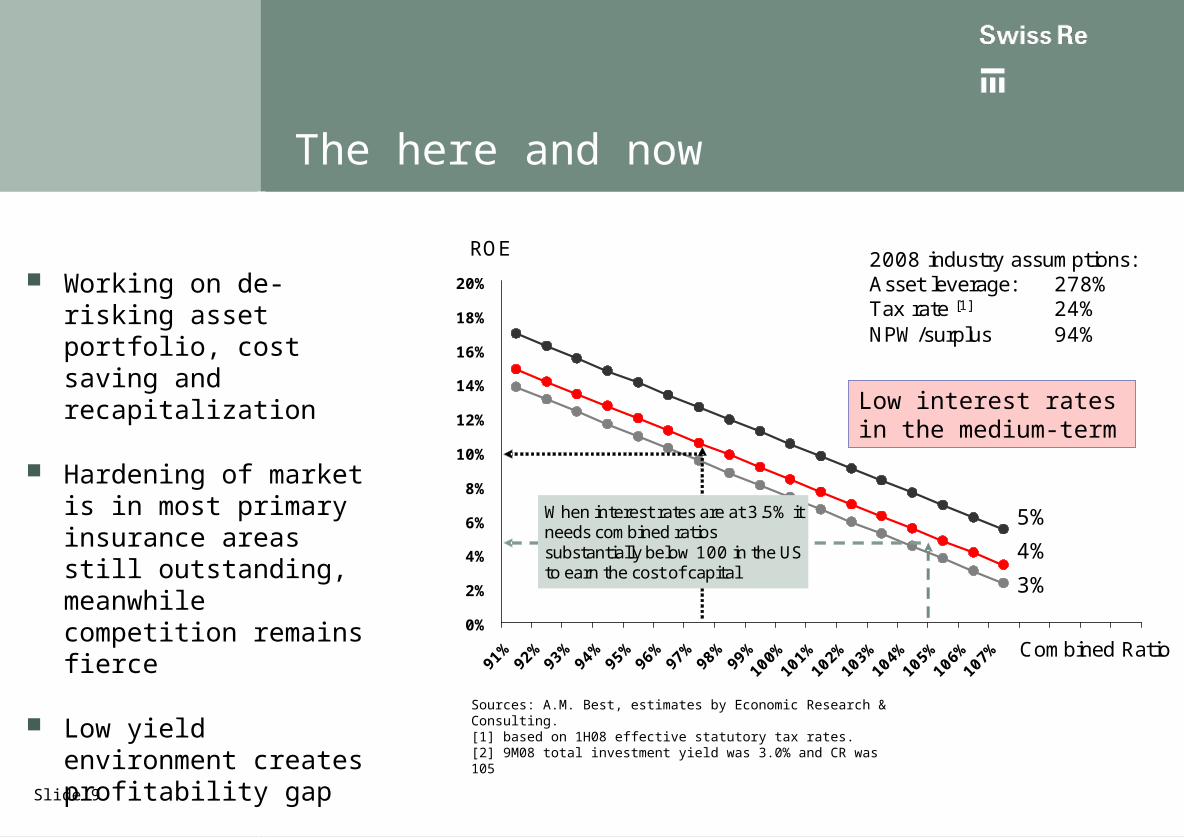

Working on de-risking asset portfolio, cost saving and recapitalization

Hardening of market is in most primary insurance areas still outstanding, meanwhile competition remains fierce

Low yield environment creates profitability gap Sources: A.M. Best, estimates by Economic Research &

Consulting. [1] based on 1H08 effective statutory tax rates. [2] 9M08 total investment yield was 3.0% and CR was 105

Low interest rates in the medium-term

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

91%

92%

93%

94%

95%

96%

97%

98%

99%10

0%10

1%10

2%10

3%10

4%10

5%10

6%10

7% Combined Ratio

2008 industry assumptions:Asset leverage: 278%Tax rate [1] 24%NPW/surplus 94%

ROE

5%

4%

3%

When interest rates are at 3.5% itneeds combined ratios substantially below 100 in the USto earn the cost of capital

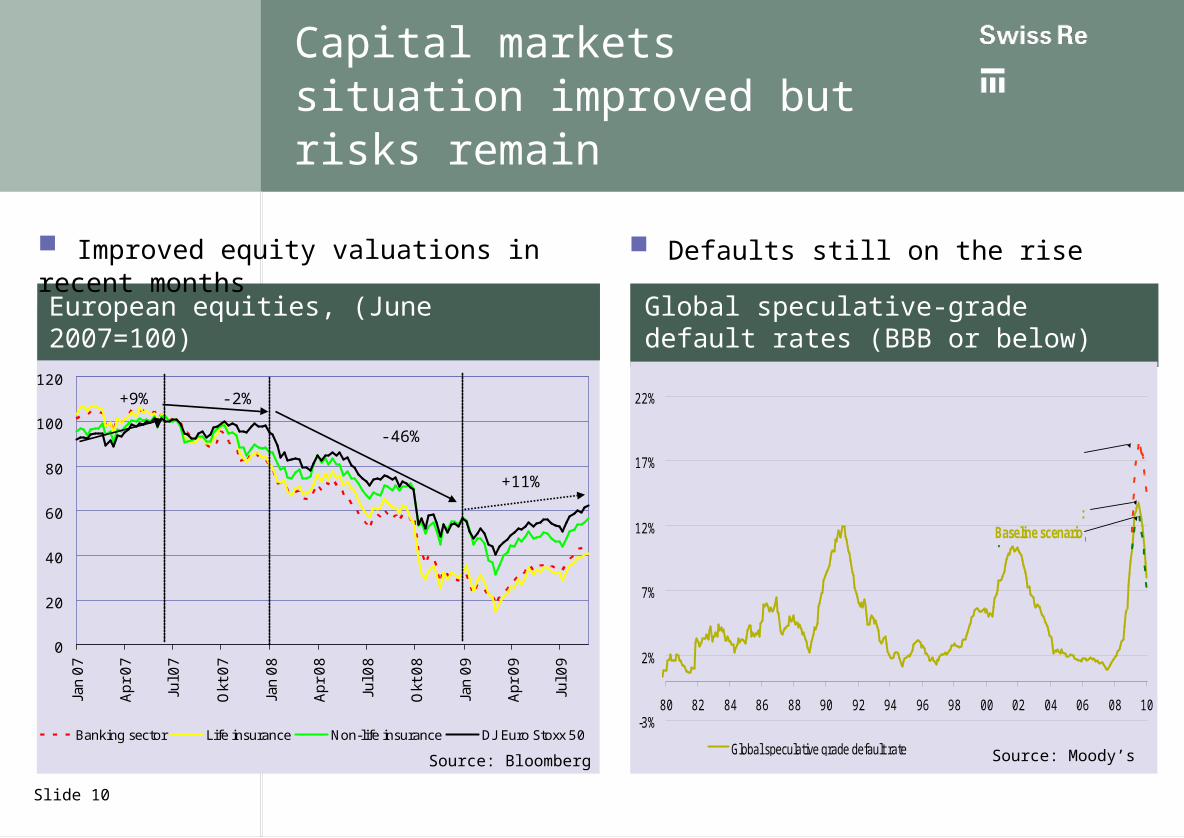

Global speculative-grade default rates (BBB or below)

Capital markets situation improved but risks remain

European equities, (June 2007=100)

0

20

40

60

80

100

120

Jan

07

Apr

07

Jul 0

7

Okt

07

Jan

08

Apr

08

Jul 0

8

Okt

08

Jan

09

Apr

09

Jul 0

9

Banking sector Life insurance Non-life insurance DJ Euro Stoxx 50

+9% -2%

-46%

+11%

Source: Moody’sSource: Bloomberg

-3%

2%

7%

12%

17%

22%

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10

Global speculative grade default rate

Pessimistic scenario

Moody's forecast:Baseline scenarioOptimistic scenario

Improved equity valuations in recent months

Defaults still on the rise

Slide 10

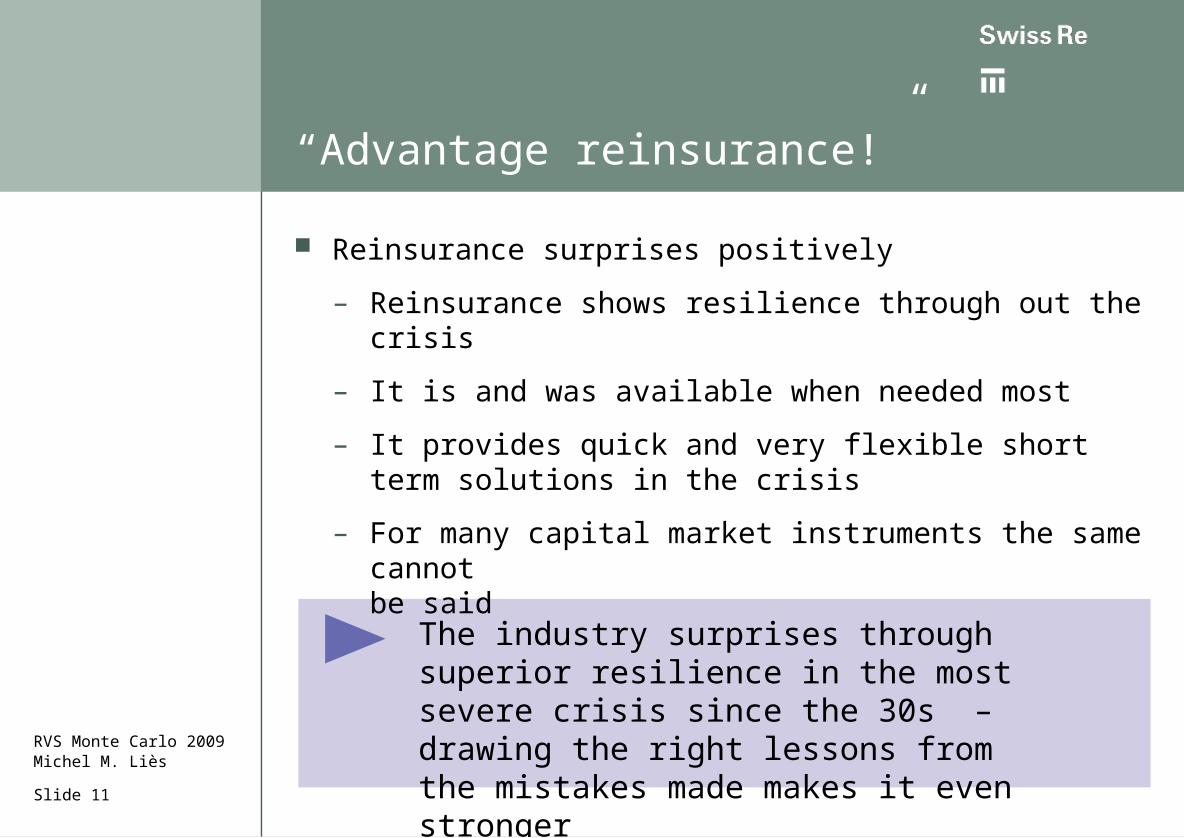

Reinsurance surprises positively

– Reinsurance shows resilience through out the crisis

– It is and was available when needed most

– It provides quick and very flexible short term solutions in the crisis

– For many capital market instruments the same cannotbe said

The industry surprises through superior resilience in the most severe crisis since the 30s – drawing the right lessons from the mistakes made makes it even stronger

“Advantage reinsurance!”

Slide 11

RVS Monte Carlo 2009Michel M. Liès

Agenda

RVS Monte Carlo 2009Michel M. Liès

Looking back: impact of the crisis on insurance and reinsurance

The here and now

Looking ahead: winners and opportunities

Slide 12

Looking ahead

Slide 13

Cost management and solid underwriting remain key for non-life insurance and reinsurance– It is the basis for restoring sustained profitability

– It is needed for getting investors back on board

– If not now, when should we make progress?

Outlook:– Strong capitalisation respectively access to capital at

favourable conditions is key for using investment opportunities and the consolidation opportunity to expand

– The ultimate winners will be those that take action on emerging demand trends

– The current situation demands for vision and clear leadership

Firms will need to quickly refocus from pre-crisis to post-crisis priorities

RVS Monte Carlo 2009Michel M. Liès

Short-term tactical priority

Refine core value proposition and respond to competitor initiatives

Long-term strategic priority

Continually improve competitive positioning in a stable and fast-growing dynamic equilibrium

Required skill set

Exceptional execution

Gearing to controlled growth

Pre-crisis priorities Post-crisis priorities

Source: Swiss Re, Oliver Wyman

Short-term tactical priority

Exploit discontinuities and future-proof business model

Long-term strategic priority

Continually evolve business model to a changing eco-system

Required skill set

Exceptional execution

Cost and risk management, merger and customer integration

Agility and cycle-adaptiveness

Simultaneous strategies to hedge an uncertain environment

Quick re-focus from pre-crisis to post-crisis priorities needed

Slide 14

RVS Monte Carlo 2009Michel M. Liès

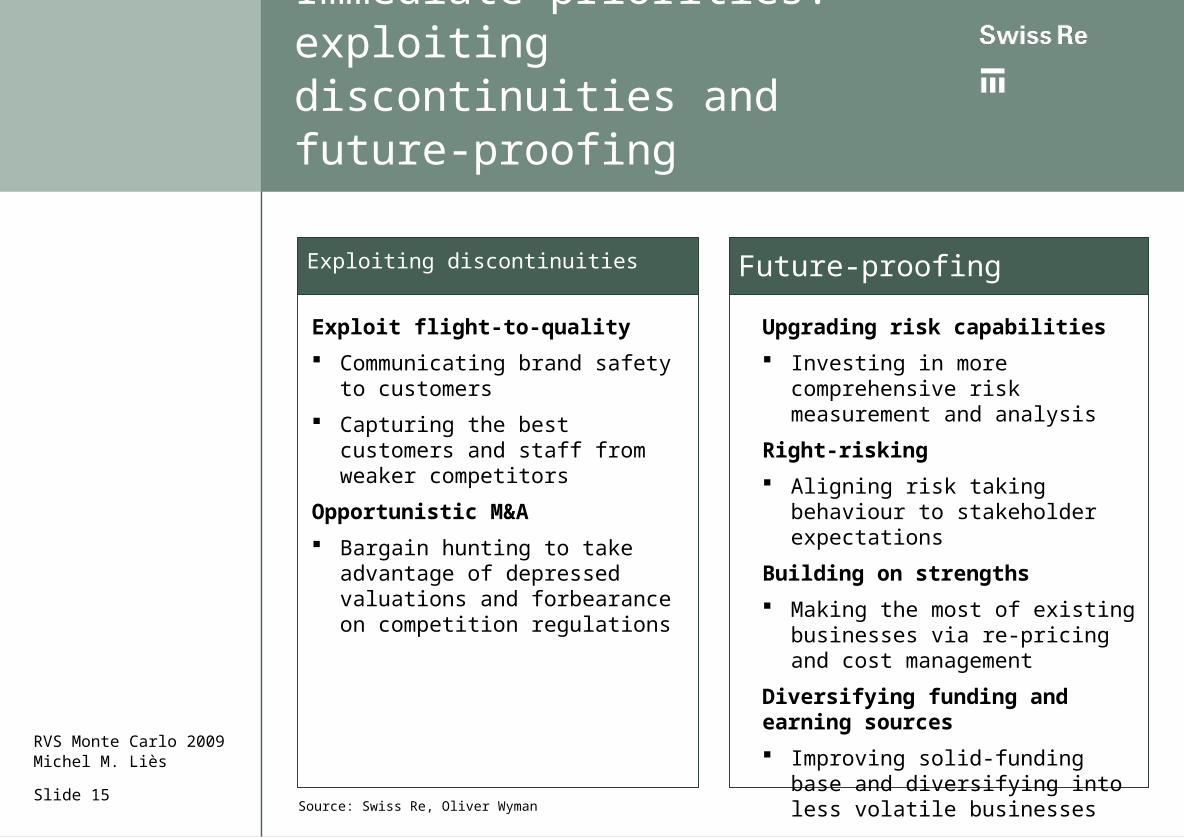

Upgrading risk capabilities

Investing in more comprehensive risk measurement and analysis

Right-risking

Aligning risk taking behaviour to stakeholder expectations

Building on strengths

Making the most of existing businesses via re-pricing and cost management

Diversifying funding and earning sources

Improving solid-funding base and diversifying into less volatile businesses

Exploit flight-to-quality

Communicating brand safety to customers

Capturing the best customers and staff from weaker competitors

Opportunistic M&A

Bargain hunting to take advantage of depressed valuations and forbearance on competition regulations

Source: Swiss Re, Oliver WymanSlide 15

RVS Monte Carlo 2009Michel M. Liès

Exploiting discontinuities Future-proofing

Immediate priorities: exploiting discontinuities and future-proofing

Conclusions

Slide 16

Assets

Liabilities

Insurers

Shareholder equity

Drop in asset values

Drive the prioritieson insurance risks

Participate inthe recovery

Financing opportunities

Focus in insurance shifts from crisis management towards capturing market opportunities

RVS Monte Carlo 2009Michel M. Liès

Manage crisis

Capture opportunities

Ensure capital strengths