a few tricks up its sleeve - ose...

TRANSCRIPT

Equity Research France 360_CR 360 Report

IMPORTANT. Please refer to the last page of this report for “Important disclosures” and analyst(s) certifications.

F Full report

keplercheuvreux.com This research is the product of Kepler Cheuvreux, which is authorised and regulated by the Autorité des Marché Financiers in France.

OSE Immunotherapeutics

France | Pharma & biotech | MCAP EUR 95.9m

20 February 2017

x

A few tricks up its sleeve

Buy (None) Target price EUR 9.00 Current price

Up/downside

Change in TP

Change in EPS none

EUR 6.71

34.1%

none

none 2016E

Main author

Thomas Guillot Equity Research Analyst

[email protected] +33 1 70 98 85 27 Pharma & biotech research team Biographies at the end of the report

What’s it all about? OSE Immunotherapeutics is a biotechnology company specialised in immunotherapy for the treatment of autoimmune diseases and cancer. Our analysis suggests positive optionality for the company thanks to its strong and diversified pipeline. Its strategy consists of out-licensing its non-core assets to rapidly monetise them while externalising all clinical development costs to minimise the related opex. The company’s leading product, Tedopi (currently in phase III), aims to reach the market in 2020, and we estimate peak sales of half a billion euros for this asset. Our in-depth valuation of the company suggests that the street is only including Tedopi, while the company has three under-the-radar, early-stage assets with significant potential.

Kepler Cheuvreux and the issuer have agreed that Kepler Cheuvreux will produce and disseminate investment research on the said issuer as a service to the issuer.

OSE Immunotherapeutics Buy TP EUR 9.00

2 keplercheuvreux.com

360

in 1 minute

Investment case summary We initiate coverage on OSE Immunotherapeutics with a Buy rating.

Tedopi is an asset in late-stage development for the treatment of NSCLC in

2L/3L. We believe that Tedopi is likely to gain value until the phase III

results are released in 2018, as momentum is set to increase. Moreover,

pending Tedopi’s results, we think the advancement of early-stage assets

will also add value to OSE Immunotherapeutics.

Key findings of the report We recommend buying OSE Immunotherapeutics, as we believe Tedopi is

not fairly valued right now, and early-stage assets are not even included in

the company’s value:

We agree with the market that most of the company’s value is in

the Tedopi asset, which presents a risky profile inherent to all

therapeutic vaccines in oncology.

However, even with a 33% probability of success, we are

convinced that the market is not assigning a fair value to Tedopi.

Moreover, we believe that the street does not value the potential

of early-stage assets like FR104 (phase I in partnership with J&J)

and also overlooks Effi-7 (at pre-clinical stage, in partnership with

Servier), which is under the market’s radar screen.

Also, the proprietary product Effi-DEM is a first-in-class candidate

targeting an innovative pathway, with similar potential to that of

the current CKI blockbusters. Although not yet clinically validated,

we believe Effi-DEM is likely to boost OSE Immunotherapeutics’

value in the near future.

Valuation model Our in-depth valuation is based on the potential of: 1) a cautious

positioning of Tedopi in third-line treatment of NSCLC HLA-A2 positive

patient population; 2) FR104 solely in RA (while not taking into account

other potential indications); and 3) Effi-7 in the treatment of ulcerative

colitis. We adopt a discount rate of 15%, in line with our biotech universe.

Our valuation stands at EUR9 per share, and we initiate coverage on OSE

Immunotherapeutics with a Buy rating.

OSE Immunotherapeutics Buy TP EUR 9.00

3 keplercheuvreux.com

Company summary Market data

OSE Immunotherapeutics is a biopharmaceutical company specialised in the development of immunotherapy dedicated to the treatment of cancer and auto-immune diseases. The company's main asset is Tedopi, a therapeutic vaccine developed in NSCLC, currently in phase III, with pivotal results expected in late 2018. Other clinical-stage assets include FR104 which has been out-licensed to J&J as well as Effi-7 in which Servier has an opt-in license option.

Bloomberg Reuters Market cap (EUR) Free float (%) No. of shares outstanding (m) 3m avg. daily vol (EURm) YTD abs. performance 52-week high (EUR) 52-week low (EUR)

OSE FP OSE.PA

95.9m 52.0

14 0

-5.2% 8.15 5.70

Management Key shareholders

Dominique Costantini, CEO

Alexis Peyroles, COO

Maryvonne Hiance, VP, Strategy

Emile Loria 30.6% Dominique Constantini 13.0% Guy Chateain 1.9%

Strengths Weaknesses

One of the fews that has a phase III immunotherapy asset Already monetised non core early-stage assets Effi-DEM is a promising candidate Experienced management

Tedopi is a highly risky development Early-stage nature of the rest of the pipeline Need to sign commercial deal for Tedopi

Opportunities Threats

Tedopi will provide solid value creation if successful NSCLC is a large market Out-licensed candidates bring cash in-flow (FR104/Effi-7) Strong balance sheet

Strong competitive environment for Tedopi in NSCLC Phase III failure for Tedopi/Effi-dem Pricing anticancer therapies

Key financials (please see the end of this report for full financials) Per share data (EUR) 2015 2016E 2017E 2018E

EPS adj and fully diluted -0.01 0.28 -0.66 -0.70

Cash flow per share -0.41 0.51 -0.78 -0.85

Book value per share 4.44 3.92 2.92 2.87

DPS 0.00 0.00 0.00 0.00

Valuation

P/E adjusted and fully diluted na 23.7 na na

P/CF na 13.1 na na

P/BV 2.2 1.7 2.3 2.3

Dividend yield (%) 0.0% 0.0% 0.0% 0.0%

FCF yield (%) -4.3% 7.6% -11.7% -12.6%

EV/Sales 25.3 3.9 na na

EV/EBITDA na 19.9 na na

EV/EBIT na 19.9 na na

Income statement (EURm)

Sales 5.1 20.3 0.0 0.0

% Change +chg 300.1% -chg na

EBITDA adjusted -3.8 4.0 -11.2 -12.1

EBIT adjusted -3.8 4.0 -11.2 -12.1

Adjusted EBIT margin (%) -74.1% 19.7% na na

Net profit reported -0.2 4.0 -9.4 -10.0

Net profit adjusted -0.2 4.0 -9.4 -10.0

Cash flow statement (EURm)

CF from operating activities -5.9 7.3 -11.2 -12.1

Capex 0.0 0.0 0.0 0.0

Free cash flow -5.9 7.3 -11.2 -12.1

Balance sheet (EURm)

Intangible assets 61.1 45.6 57.5 83.9

Tangible assets 0.1 0.1 0.1 0.1

Fin. & other non-current assets 0.1 0.1 0.1 0.1

Total shareholders' equity 63.4 56.0 41.7 41.0

Pension provisions 0.0 0.0 0.0 0.0

Liabilities and provisions 21.9 19.4 34.3 49.3

Net financial debt -9.0 -16.3 -5.1 7.0

Working capital requirement 8.1 4.0 -1.0 -6.0

Invested capital 8.2 4.1 -0.9 -5.9

Ratios

ROE na 6.8% -19.2% -24.3%

ROIC na 43.7% -477.6% na

EV/IC 15.6 19.6 na na

Gearing -14.2% -29.1% -12.2% 17.1%

1 year performance 2011

5.5

6.0

6.5

7.0

7.5

8.0

8.5

Feb 16 May 16 Aug 16 Nov 16 Feb 17Price DJ Stoxx 600 (rebased)

OSE Immunotherapeutics Buy TP EUR 9.00

4 keplercheuvreux.com

Investment case in six charts

Chart 1: OSE Immunotherapeutics portfolio

Chart 2: Overall survival of phase II with Tedopi

Source: OSE Immunotherapeutics Source: Kepler Cheuvreux

Chart 3: Mechanisms of action Effi-DEM

Chart 4: Mechanisms of action FR104

Source: Kepler Cheuvreux Source: Kepler Cheuvreux

Chart 5: Mechanisms of action Effi-7

Chart 6: SOP (EURm)

Source: Kepler Cheuvreux Source: Kepler Cheuvreux

FR104

EFFi-7

Tedopi®

Effi-DEM

Cancer

Immunosuppression

AutoimmuneInflammatory diseases

Allograft rejection

Immune activation and regulationSurvival functionCensored

Time survived (days)

Cu

mu

lati

ve

su

rviv

al

1.0

0.8

0.6

0.4

0.2

0200 400 600 800 1,000

EUR131m

EUR97m EUR12m EUR6m

EUR17m

-

20

40

60

80

100

120

140

160

rNPV Tedopi rNPV FR104 rNPV Effi-7Net cash position Base case

OSE Immunotherapeutics Buy TP EUR 9.00

5 keplercheuvreux.com

Contents

Investment case in six charts 4

Investment case summary 7

Paving the way for value creation 7

Cancer immunotherapy: the core focus 7

FR104 and Effi-7: already monetised 8

Initiating coverage with a Buy rating and a TP of EUR9 8

Paving the way for value creation 9

An attractive pipeline emerged from the merger 9

Unity is strength 10

Strategy: quickly provide value creation from non-core assets 11

Cancer immunotherapy: the core focus 12

Tedopi: a multi-epitope cancer vaccine 12

Tedopi target NSCLC: the largest cancer market 14

Promising phase II needs to be confirmed 18

Effi-DEM: the future immune-oncology blockbuster? 26

FR104 and Effi-7: already monetised 34

FR104: a ground-breaking opportunity in autoimmune diseases 34

J&J: a landmark partner for FR104 36

FR104: looking to grab a piece of the large RA market 37

Competitive environment in CD80/CD28 pathway 41

Effi-7: already monetised to Servier, the right strategic option? 43

Deconstructing the forecasts 48

Cancer drug pricing 48

Tedopi: a place in 2L/3L NSCLC 49

FR104 in RA 51

Effi-7: next milestone payment in five years 53

Initiating coverage with a Buy rating 55

Main risks for Tedopi: finding the right partner for EU/US commercialisation 55

Main assumptions of our rNPV for Tedopi 56

rNPV of Tedopi in NSCLC (EUR97m) 57

rNPV of FR104 in RA (EUR12) 58

rNPV of Effi-7 in UC (EUR6m) 60

SOP summary 61

OSE Immunotherapeutics Buy TP EUR 9.00

6 keplercheuvreux.com

Appendices 62

Shareholders 62

Key people 62

Immune system functions 63

Use of the immune system to fight diseases: immunotherapy 65

Immunotherapy applied to cancer 66

Immunotherapy applied to autoimmune diseases 71

Research ratings and important disclosures 76

Legal and disclosure information 79

OSE Immunotherapeutics Buy TP EUR 9.00

7 keplercheuvreux.com

Investment case summary We initiate coverage on OSE Immunotherapeutics with a Buy rating and a target

price of EUR9. Even though we perceive Tedopi as a highly risky asset (we

believe the product has a 33% chance of succeeding), we think that OSE

Immunotherapeutics’ main candidate is currently undervalued. Moreover, we

feel confident about the prospect of early-stage candidates. We think that the

pipeline is likely to drive value creation until the end of 2018 and the phase III

results of Tedopi, which will be a landmark event for the company. Until then, we

think that the advancement of Effi-DEM, FR104 and Effi-7 will provide

momentum for the company.

Paving the way for value creation

OSE Immunotherapeutics was set up in June 2016 with the merger between

Effimune and OSE Pharma. This led to the creation of a strong player in

immunotherapy with a diversified range of solid blockbuster therapeutic candidates.

The diversification of its pipeline allowed the company to reduce the development

risk inherent to immunotherapy.

Thanks to the merger, OSE Immunotherapeutics is now developing its portfolio both

for autoimmune and oncology conditions. The company’s leading asset is Tedopi, a

therapeutic vaccine provided by OSE Pharma and developed in lung cancer. The

candidate is currently in phase III of development with clinical data expected as

soon as 2018. Effimune provided the rest of the portfolio, which is made up of:

1) Effi-DEM, a preclinical-stage new generation of checkpoint inhibitors developed

in oncology; 2) FR104, a clinical-stage candidate developed in rheumatoid arthritis

and out-licensed to J&J; and 3) Effi-7, a preclinical-stage candidate developed in

autoimmune diseases and out-licensed to Servier.

Cancer immunotherapy: the core focus

OSE Immunotherapeutics mainly focuses on immunotherapy applied to oncology.

The company currently has two proprietary owned products under development:

1) Tedopi, a therapeutic vaccine currently in phase III for the treatment of lung

cancer; and 2) Effi-DEM, a preclinical stage immunotherapy, modulating the tumour

microenvironment.

Tedopi’s phase III results are expected in late-2018. If positive, the product is likely

to boost the value of OSE Immunotherapeutics. That said, we question the prospects

of the asset, due to: 1) the notoriously risky field of therapeutic vaccines applied to

oncology; 2) the fierce competitive environment of late-stage NSCLC candidates;

and 3) the lack of clinical evidence with statistical significance shown in phase II

by Tedopi.

However, we are optimistic about Effi-DEM’s prospects. We believe Effi-DEM is an

under-the-radar asset with the potential to become a blockbuster. Although not yet

clinically validated, based on the scientific literature and preclinical data, we believe

targeting SIRPαpathway holds promise.

OSE Immunotherapeutics Buy TP EUR 9.00

8 keplercheuvreux.com

FR104 and Effi-7: already monetised

FR104 and Effi-7 are two monoclonal antibodies developed for the treatment of

autoimmune diseases. Both assets have already been out-licensed to partners by

OSE Immunotherapeutics.

A partnership agreement has been reached with J&J in relation to FR104, providing

a EUR10m opt-in option payment to OSE Immunotherapeutics in July 2016. In the

event of clinical success, FR104 is likely to become a blockbuster with solid activity

both in rheumatology and in transplant complication management. FR104 is no

longer a source of cost and now represents a cash inflow opportunity for OSE

Immunotherapeutics. Indeed, following its opt-in options, J&J will fund all the

development costs as of now. Therefore, FR104 is now a potential source of cash-in

for OSE Immunotherapeutics.

OSE Immunotherapeutics secured EFFI-7 through an out-license deal with Servier in

December 2016 with an opt-in option after the completion of phase II. Funding until

phase II is also partly secured thanks to a consortium led by OSE

Immunotherapeutics.

We believe these two assets will provide sufficient funding to the company to

finance EFFI-DEM development, therefore significantly derisking the group’s profile.

Initiating coverage with a Buy rating and a TP of EUR9

Our valuation of OSE Immunotherapeutics focuses on three candidates: Tedopi,

FR104, and Effi-7. Even though we do not include Effi-DEM, due to its preclinical

early-stage development, we have emphasised the potential of this candidate and

will look closely at its future development.

We think that OSE Immunotherapeutics is likely to out-license Tedopi in all

territories and will only retain milestone payments and royalties based on

commercial performance. Hence, we do not see any commercial structure or facility

emerging from the company for Tedopi. For FR104, we forecast the royalties and

milestones resulting from the J&J partnership. We are confident that even though

the development time will be lengthy, the candidate has a good chance of reaching

blockbuster status in the event of clinical success, due to its potential in in a broad

range of autoimmune conditions.

The next major milestone will be the positive or negative outcome of the phase III

trial of Tedopi in 2018. In the event of clinical or regulatory failure, we think that the

company is likely to pursue the development of Effi-DEM, thanks to the financing

provided by FR104, and to a lesser degree by Effi-7. We think that the current

valuation does not include the potential of early-stage assets, but it also undervalues

Tedopi. We initiate coverage with a Buy rating and a target price of EUR9.

OSE Immunotherapeutics Buy TP EUR 9.00

9 keplercheuvreux.com

Paving the way for value creation OSE Immunotherapeutics was created in June 2016 through the merger of

Effimune and OSE Pharma, establishing a strong player in immunotherapy with a

diversified range of solid blockbuster therapeutic candidates. The diversification

of its pipeline allowed the company to reduce the development risks inherent to

immunotherapy.

Thanks to the merger, OSE Immunotherapeutics is now developing its portfolio

both for autoimmune and oncology conditions. Its leading asset is Tedopi, a

therapeutic vaccine provided by OSE Pharma and developed in lung cancer. The

candidate is currently in phase III of development with clinical data expected as

soon as 2018. Effimune provided the rest of the portfolio, which is made up of: 1)

Effi-DEM, a preclinical stage new generation of checkpoint inhibitors developed

in oncology; 2) FR104, a clinical-stage candidate developed in rheumatoid

arthritis and out-licensed to J&J; and 3) Effi-7, a preclinical-stage candidate

developed in autoimmune diseases and out-licensed to Servier.

An attractive pipeline emerged from the merger

OSE Pharma history OSE Pharma was founded in April 2012 by Emile Loria and Dominique Costantini.

The two managers created the structure to further develop Tedopi, a lung cancer

therapeutic vaccine that has been under clinical-stage development since 2003.

Tedopi was developed first by Epimmune before a takeover by IDM pharma in 2005,

followed by Takeda in 2007.

Following the acquisition of IDM by Takeda, some of IDM’s assets, including Tedopi,

were deprioritised, and their development halted. Emile Loria decided to pursue the

development of Tedopi. Thanks to positive phase IIb results in specific lung cancer

populations, OSE Pharma decided to seek financing to start a phase III trial and

carried out an IPO in March 2015, raising EUR21.1m.

Effimune history Effimune was founded in 2007 in Nantes, France. The company is a spin-off of

INSERM and the Institute of Transplantation, Urology and Nephrology (ITUN) in

Nantes. Effimune is specialised in immune regulation for clinical application in auto-

immune, transplants, and immuno-oncology (IO).

Thanks to its preliminary research highlighting key immuno-regulator receptors,

Effimune managed to develop three product candidates: FR104, Effi-7, and

Effi-DEM.

Effimune sought to raise EUR5m in 2015 and up to EUR20m in 2016 to speed up its

internal development pipeline. According to the street, due to the lack of financing

solutions and tough equity market conditions, Effimune agreed to merge with OSE

Pharma to form OSE Immunotherapeutics, a leading group with two areas of

expertise: immunology and oncology.

Effimune brought three assets: FR104, Effi-7 and Effi-DEM

OSE Immunotherapeutics Buy TP EUR 9.00

10 keplercheuvreux.com

A diversified pipeline Thanks to the merger, OSE Immunotherapeutics has a well-diversified pipeline, both

in oncology and autoimmune diseases.

Chart 7: OSE Immunotherapeutics’ pipeline

Note: (1) checkpoint inhibitors (PD-1/PD-L1) Source: Kepler Cheuvreux, OSE Immunotherapeutics

Unity is strength

In February 2016, OSE Pharma announced its intention to merge with Effimune. The

purpose of the merger was to create a balanced portfolio in immunotherapy. At the

time, OSE Pharma only had one asset, Tedopi, in late-stage development in lung

cancer, while Effimune had three early-stage candidates. The merger resulted in a

balanced and less risky pipeline portfolio. The all-stock operation closed in June

2016. It resulted in an entity named OSE Immunotherapeutics and 71%-owned by

ex-OSE Pharma shareholders and 29% owned by ex-Effimune shareholders.

Whereas OSE Pharma solely focused on oncology, Effimune has specialised in

restoring the balance of the immune system for oncology and autoimmune diseases.

Thanks to the acquisition of Effimune, OSE Pharma has significantly expanded its

pipeline toward other mechanisms of action and other targeted therapeutic areas.

Chart 8: OSE Immunotherapeutics aims to rebalance the immune system

Source: OSE Immunotherapeutics

Product Mechanism of action Indications Status Related party

Preclinical I II III Reg.

Oncology

Tedopi Multi-epitope cancer vaccine NSCLC - HLA-A2+ Expected registration: 2019

Tedopi + CKI(1) Multi-epitope cancer vaccine NSCLC - HLA-A2+ Expected phase II start: 2017

Effi-DEM SIRP-α inhibitor Solid tumours Expected start clinical stage: H2 2018

Autoimmune diseases

FR104 Anti CD-28 Rheumatoid arthritis Expected start phase II: H2 2017/2018

Effi-7 Anti IL-7 Ulcerative collitis Expected start clinical stage: H2 2018

Clinical Phase

FR104

EFFi-7

Tedopi®

Effi-DEM

Cancer

Immunosuppression

AutoimmuneInflammatory diseases

Allograft rejection

Immune activation and regulation

OSE Immunotherapeutics aims to modulate the immune system to tackle severe immune-related conditions

OSE Immunotherapeutics Buy TP EUR 9.00

11 keplercheuvreux.com

Strategy: quickly provide value creation from non-core assets

We estimate that OSE Immunotherapeutics has sufficient funding until end-2018

with a cash position that we estimate at c. EUR19m. After that, all will depend on

the outcome of Tedopi.

The positive cash position has been made possible thanks to the IPO in 2015

(EUR21.1m raised) and the monetisation of the proprietary assets to partners

through licensing (EUR20.25m added in 2016).

OSE Immunotherapeutics has adopted a cash-in strategy by out-licensing its non-

core assets at an early stage of development. Hence, the company has decided to

partner up for its autoimmune diseases candidates FR104 (J&J) and Effi-7 (Servier)

while keeping the rights for its oncology pipeline (Tedopi and Effi-DEM). While

derisking the company’s profile, this strategy also has its limitations, as OSE

Immunotherapeutics retains a smaller percentage of the value of these assets at an

early stage.

Table 1: Value share figures for Biotech/Pharma deals

Licensor (OSE Immunotherapeutics)

Licensee (Servier / J&J)

Preclinical (Effi-7) 10-20% 80-90% IND (FR104) 20-40% 60-80% Phase IIb/III 40-60% 40-60% Approval 60-80% 20-40%

Source: Bogdan and Villiger

OSE Immunotherapeutics has chosen to outsource most of its R&D development

costs, which gives the company flexibility in its resource allocation. Thus, to perform

its clinical trials and manufacture its drug candidates, OSE Immunotherapeutics uses

contract research organisations (CROs) and contract manufacturing organisations

(CMOs). For example, for Tedopi, the phase III trial is conducted by CRO Simbec

Orion, while production of Tedopi is outsourced to PPL (APIs) and Bacinex

(formulation). To limit its R&D expenses, OSE Immunotherapeutics has chosen to

pay its services provider with stock options. We expect this type of payment to be

moderately dilutive for the company in the near future.

Cash is sufficient until the results of Tedopi in phase III

OSE Immunotherapeutics Buy TP EUR 9.00

12 keplercheuvreux.com

Cancer immunotherapy: the core focus OSE Immunotherapeutics mainly focuses on immunotherapy applied to

oncology. The company currently has two proprietary products under

development: 1) Tedopi, a therapeutic vaccine currently in phase III for the

treatment of lung cancer; and 2) Effi-DEM, a preclinical stage immunotherapy,

modulating the tumour microenvironment.

Tedopi’s phase III results are expected in late-2018. If positive, the product is

likely to boost the value of OSE Immunotherapeutics. That said, we are cautious

on the asset’s prospects, due to: 1) the notoriously risky field of therapeutic

vaccines applied to oncology; 2) the fierce competitive environment of late-

stage NSCLC candidates; and 3) the lack of clinical evidence with statistical

significance shown in phase II by Tedopi.

However, we are optimistic about Effi-DEM, which we believe is an under-the-

radar asset with the potential to become a blockbuster. Although not yet

clinically validated, based on the scientific literature and preclinical data, we

believe that targeting the SIRPαpathway holds promise.

Tedopi: a multi-epitope cancer vaccine

Tedopi is a cancer vaccine that is being developed in non-small lung cancer (NSCLC)

and currently in phase III of development with final results expected in 2018.

Historical development Tedopi, also named OSE-2101, was initially developed by Epimmune between 2001

and 2006. The development of the project was led by Emile Loria, one of the

founders of OSE Pharma. In 2006, Epimmune merged with IDM Pharma before

being taken over by the Japanese pharmaceutical company Takeda in 2009.

Over 2011-12, Emile Loria decided to acquire OSE-2101’s IP from Takeda and the

technology dedicated to this asset (named Memopi) to launch OSE Pharma.

Mechanism of action Tedopi has been engineered to selectively target the Human Leukocytes Antigen

(HLA) of class I (HLA-A2). HLA is a similar name for major histocompatibility

complex (MHC). MHC are cell-surface proteins responsible of the interaction of

antigen-presenting cells (APC) and effector lymphocytes cells (like CD4+ or CD8+).

OSE Immunotherapeutics Buy TP EUR 9.00

13 keplercheuvreux.com

Chart 9: Major histocompatibility complex (MHC) class I and II

Source: Nature

HLA-A2 is a serotype (subcategory) of MHC type I, which is the MHC that triggers

the education of the CD8+ T cells. This serotype is present in 45% of the population,

according to OSE Immunotherapeutics. Due to this moderate frequency, Tedopi

has received orphan drug status in the US.

Tedopi is an off-the-shelf therapeutic vaccine comprising nine epitopes that address

five well-known tumour-associated antigens (TAAs). The tenth synthetic peptide is

the pan-DR epitope (PADRE), a well-known helper T-Lymphocyte (HTL) epitope

included to increase the magnitude and duration of cytotoxic T-lymphocyte (CTLs)

responses. All these epitopes were designed to selectively recognise the HLA-A2

serotype.

Accordingly, Tedopi was designed to induce CTL responses against TAAs frequently

observed in NSCLC (non-small cell lung cancer), such as:

Carcinoembryonic antigens (CEA): glycoproteins involved in cell adhesion, which is present in c. 70% of lung cancers.

P53: Protein p53 is common in cancer and gained functions that help to contribute to malignant progression. The mutation of p53 is present in 40-50% of NSCLC (Korst & Crystal, 2003).

HER-2/neu: HER2 is a member of the human epidermal growth factor receptor (HER/EGFR). This glycoprotein is involved in cellular expansion for some cancer cells. This mutation is found in 22-50% of NSCLC (Korst & Krystal, 2003).

MAGE-2 (melanoma-associated antigen 2): MAGE-2 genes are almost universally expressed in body tissues.

MAGE-3 (melanoma-associated antigen 3): Like MAGE-2, this antigen is expressed in many types of cancer.

All of these mutations are considered as poor prognosis factors for the development

of the cancer, notably in NSCLC. The originality of Tedopi’s formulation is its ability

to generate an immune response against ten epitopes present in five antigens while

traditional therapeutic vaccine formulations only target one antigen.

Peptide Glyco

CD8+

T cellCD4*T cell

MHCClass I

MHCClass II

Antigen-presenting cell

Diverse TCR

Tedopi targets five TAAs evenly found in NSCLC

OSE Immunotherapeutics Buy TP EUR 9.00

14 keplercheuvreux.com

Moreover, Tedopi does not induce B-cell responses, contrary to therapeutic

vaccines based on one or several antigens and only trigger T cell responses thanks to

its specific traits.

A notorious, high-risk field Note that cancer vaccine therapies have suffered numerous setbacks over the past

decade due to the insufficient response they provided. Many companies have faced

clinical development setbacks, in particular in peptide-based vaccines.

Table 2:Recent outcome of peptide-based cancer vaccine

Product Company Formulation Cancer Status Outcome Cause

GV1001 KAEL-GemVax Co Telomerase peptide-based vaccine

Pancreatic cancer Abandoned (June 2013) Failure Efficacy

Stimuvax Merck KGaA / Oncothyreon MUC1-antigen specific

NSCLC Abandoned (December 2012) Failure Efficacy

NeuVax Galena Biopharma HER2-directed cancer immunotherapy

Breast cancer Discontinued (June 2016) uncertain Efficacy

PAS Cancer Advances Anti-G17 & (Gly) G17 vaccine

Pancreatic cancer PIII completed results uncertain n.a. GIST PIII completed results uncertain n.a.

IMA901 Immatics Multipeptide cancer vaccine Renal cell carcinoma PIII (September 2015) Failure Efficacy

Elpamotide/ OTS-102 OncoTherapy Science VEGFR2 epitope based vaccine Pancreatic cancer PIII Failure Efficacy

Source: Kepler Cheuvreux

Only one cancer vaccine has been approved so far by the FDA: Provenge (by

Dendreon, which is now part of Valeant), for its use in prostate cancer. However, the

commercial prospects of the vaccine have been limited due to manufacturing and

logistical issues that have impeded the commercialisation of the product.

Immatics, a German company that developed a multi-epitope based vaccine like

Tedopi, failed to reproduce positive phase II results in its pivotal phase III. The

setback was due to the change of phase III design compared to phase II.

Tedopi target NSCLC: the largest cancer market

Tumour grades at a glance Tumours are an evolving disease and patients are screened according to their grade.

The tumour grade refers to the description of a tumour based on what cancer cells

and tumour tissue look like. This provides doctors with valuable indications about

how quickly a tumour is likely to grow and spread to other parts of the body. While

some types of cancer have their own grading systems, tumours are generally graded

as 1, 2, or 3. A low-grade cancer is likely to grow and spread more slowly than a high-

grade one.

An early diagnosis significantly increases the overall chances of survival

Numerous therapeutic vaccines failed to reproduce early-stage promises

OSE Immunotherapeutics Buy TP EUR 9.00

15 keplercheuvreux.com

Chart 10: Cancer grades

Chart 11: Cancer stages

Source: National Cancer Institute Source: National Cancer Institute

Cancers in the initial stage (grade 1) are the least malignant tumours and are

associated with long-term survival. Cancer cells tend to be growing slowly and

exhibit an almost normal appearance. Importantly, surgery alone can be an effective

treatment for this grade of tumour. Grade 2 cancer cells look slightly abnormal and

tumours grow faster than in the previous grade. The distinction between grades 2

and 3 is not always clear-cut. Nevertheless, the cells of a grade 3 tumour look very

different to normal cells and grow fast in disorganised, irregular patterns. Grade 3

cancer cells start to spread to nearby healthy tissue.

NSCLC at a glance NSCLC (non-small-cell lung cancer) represent 85% of total lung cancer. Tobacco

smoking is by far the leading cause of lung cancer. According to the American Cancer

Society, 80% of lung cancers are thought to be linked to smoking. The number of

cases has reached 560,000 patients in the world’s seven major markets (the US,

Japan, France, Germany, Italy, Spain and UK). Globally, it represents nearly 1.8m

cases. Lung cancer accounts for 20% of all cancer-related deaths and is involved in

1.6m deaths each year, three times more than breast and colorectal cancers

combined (1.3m deaths).

There are three main kinds of NSCLC depending on the type of cancer cell:

adenorcarcinoma (non-squamous cells), squamous cell carcinoma, and large cell lung

cancer. Despite the recent improvement in the treatment and management of

NSCLC thanks to the emergence of immunotherapies, there is still a high unmet

medical need for late-stage cancer (IIIB/IV).

Grade 1

Cancer cells look very similar to

normal cells and are growing

slowly

Grade 2

Cancer cells look unlike normal cells and are

growing more quickly than

normal

Grade 3

Cancer cells look very abnormal

and are growing quickly

1

2

3

Stage 1

The cancer is small and has not spread anywhere

else

Stage 2

The cancer has grown but has not spread

Stage 3

The cancer is larger and may have spread to the

surrounding tissues and/or the lymph nodes

1 2

3

Stage 4

The cancer has spread from where it started to at least one other body

organ

4

The higher the grade, the more dangerous the tumour

OSE Immunotherapeutics Buy TP EUR 9.00

16 keplercheuvreux.com

Table 3: NSCLC treatment and overall survival

Stage Treatment Five-year survival rate at diagnosis

Stage Ia Surgery, consisting of removing either the affected part of the lung or the whole lung. If surgery is not possible, radiotherapy is recommended

49%

Stage Ib Surgery, possibly followed by chemotherapy. If surgery is not possible, radiotherapy is recommended 45%

Stage II Surgery followed by chemotherapy. If surgery is not possible, radiotherapy is recommended 30%

Stage IIIa Chemotherapy, possibly combined with surgery or radiotherapy 14% Stage IIIb Chemotherapy combined with radiotherapy, surgery is an exception 5%

Stage IV Chemotherapy may be combined with other types of treatments (“targeted therapy” on particular mutations for instance)

1%

Source: Cancer.gov, OSE Immunotherapeutics

According to the NIH, 57% of patients are diagnosed with lung cancer at a later

stage when survival chances are lower. Tedopi aims to target the large NSCLC

market for the second and third-line treatment of advanced stage lung cancer.

Treatment of late-stage NSCLC

Usually, early-stage (stage I to II) treatment of NSCLC starts with removal surgery if

the tumour is found to be resecable and the patient is able to tolerate surgery.

Patients often receive radiotherapy and/or chemotherapy or targeted therapy to

avoid tumour relapse. In the event of tumour progression, physicians usually use

chemotherapy as a combination of platinum-based agents (cisplatin or carboplatin)

and other chemotherapy agents called taxans (e.g. Taxotere from Sanofi).

The recent approval of CKIs (checkpoint inhibitors) has led the guideline writers to

significantly change their recommendations. Previously, Taxotere (docetaxel) was

considered to be a standard second-line option and was often used for subsequent

therapy in patients whose cancer had progressed on first-line platinum-based

chemotherapy regimens.

Fierce competition in late-stage NSCLC Checkpoint inhibitors (CKIs) are the new standard of care in 2L

The competitive landscape in immune-oncology (IO) is extremely complex and fast-

moving. Nowadays, the new standards of care in 2L are the CKIs as part of the new

immuno-therapy paradigm. In the US, the NCCN guidelines have recommended

CKIs as preferred agents against Taxotere (docetaxel) based on improved overall

survival rates, higher response rates, longer duration of response, and fewer adverse

events compared with docetaxel therapy. The European guidelines also indicated a

preference for the use of CKIs in the event of positive PD-L1 histology.

NSCLC treatments: a personalised approach

Another aspect of the market to bear in mind is the upcoming maturity of targeted

therapies. NSCLC may be classified according to the mutations as follows:

OSE Immunotherapeutics Buy TP EUR 9.00

17 keplercheuvreux.com

Chart 12: NSCLC types

Source: Roche

Non-squamous cell carcinomas (adenocarcinoma) represent almost 65% of

NSCLC. Within this category, the past couple of years have seen the emergence

of targeted therapies, which are usually developed along with a biomarker to

diagnose the mutation.

Targeted treatments are being developed to overcome the aberrant oncogenic

pathways of these mutant genes. Several epidermal growth factor receptor (EGFR)

and anaplastic lymphoma kinase (ALK) inhibitors have now been approved that

demonstrate a large magnitude of durable overall response rate (ORR) in patients

with NSCLC who harbour certain EGFR mutations and ALK rearrangements.

For instance, Iressa from AstraZeneca has been approved as the first-line treatment

of advanced EGFR+ NSCLC. Other gene-mutation-related treatments have been

approved (e.g. Xalkori for ALK+ cancer) or are being developed (e.g. Tafinlar for

BRAF mutations in NSCLC).

A new generation of treatment is also emerging: Tagrisso from AstraZeneca is a new

generation of targeted therapies for second-line EGFR specific T790M gene

mutation adenocarcinoma. The Aura3 phase III enrolled 419 patients and data

showed an impressive improvement in progression-free survival after 5.7 months

compared to chemotherapy. For patients with brain metastasis, PFS was 8.5 months

with Tagrisso versus 4.2 months for the chemotherapy-based regiment.

AstraZeneca is beginning the life-cycle management phase of this new therapy and

is planning to develop the Tagrisso in 1L EGFR-positive mutation.

12%

11%

4%

1%

1%

19% 18%

35%

KRAS+ adenocarcinoma

EGFR+ adenocarcinoma

ALK+ adenocarcinoma

HER2+ adenocarcinoma

BRAF+ adenocarcinoma

Unknown adenocarcinoma

large cell carcinoma

squamous cell carcinoma

OSE Immunotherapeutics Buy TP EUR 9.00

18 keplercheuvreux.com

Neoantigen vaccines: the biggest threat for Tedopi?

Neoantigen therapeutic vaccine development is a growing paradigm to restore a

specific T cell response against cancer. With advancement in genome sequencing, it

is now possible to identify a new class of tumour-specific antigens derived from

mutated proteins (called neo-antigens) that are only present in the tumour.

This approach differs from that of OSE Immunotherapeutics whose vaccines include

tumour-associated antigen epitopes that are usually found in tumour cells but not in

every tumour’s phenotype. Meanwhile, Tedopi is likely to have a varied impact on

most of the tumours that it targets.

Conversely, these “neoantigens” should provide highly specific targets for

antitumour immunity and create more specific T cell responses. Although many

challenges remain in producing and testing neoantigen-based vaccines customised

for each patient, a neoantigen vaccine offers a promising new approach to induce

highly focused antitumour T cells aimed at eradicating cancer cells.

Table 4: Neoantigen vaccines under development

Company name Product Phase Indication Comments

Gritstone Oncology n.a. Research Lung cancer Established in 2015 with a USD102m series A BioNtech IVAC Phase I Breast cancer/

melanoma In September 2016, BioNtech signed a deal agreement with Genentech

for the development of its mRNA based neoantigen technology Vaccibody VB10.16 HPV-16 cancer-drive,

therapy Raised EUR24m in December 2016 through a private placement

Moderna Therapeutics/ Merck

n.a. Research n.a. Largest funded-biotech ever with more than USD1.4bn financing

Neon Therapeutics NEO-PV-01 Phase I Melanoma, NSCLC and bladder cancer

First patients of the phase I enrolled in November 2016

Source: Kepler Cheuvreux

Overall, we perceive the NSCLC market as a challenging, highly competitive

market with the emergence of breakthrough therapy in the near future. A

personalised approach (kinase inhibitors), a specific cancer approach (neoantigen

vaccines) and the modulation of other immune pathways (tumour

microenvironment, NK cells) are likely to lead to a high degree of competition. Most

of these treatments will be used in combination and not in monotherapy to

strengthen their therapeutic effect.

Promising phase II needs to be confirmed

Phase II showed promising clinical data, with an unconventional design In 2008, Epimmune, the former owner of Tedopi, released the results of the phase II.

The trial enrolled 135 patients, of which 64 were found to be HLA-A2+. These

patients received Tedopi while the HLA-A2 negative patients served as observation.

Hence, Tedopi was used as a second-line treatment in this phase II trial. The

primary endpoint was the comparison of overall survival and secondary endpoints

included progression-free survival and T-cell response to vaccine epitopes.

Tedopi has already been developed in two phase I/II clinical trials and one phase II trial for NSCLC patients.

The therapeutic vaccine showed a strong overall survival threshold.

We think that neoantigen vaccines are more promising treatments than Tedopi but early-stage

OSE Immunotherapeutics Buy TP EUR 9.00

19 keplercheuvreux.com

Tedopi was well tolerated during the trial, with no significant adverse events

observed in hematopoietic, gastrointestinal, ocular, or neurological functions.

Table 5: Overview of phase II results of Tedopi

Arm Number of patients

Median survival (months)

p-value 1- year survival

p-value Response rate (CR&PR)

HLA-2 + 64 17.3 not significant (p=0.063)

59% not significant (p=0.089)

3%

HLA-2 - 72 12 49% n.a.

Source: OSE Immunotherapeutics

Longer survival was associated with a higher number of positive responses to

epitopes in the HLA-A2+ arm. Hence, patients responding to 0 or 1 epitope had an

overall survival of 406 ± 58 days. Those responding to two or three epitopes had a

median survival of 778 ± 72 days, and those responding to four to five epitopes had a

median survival of 875±67 days. Nearly 85% of the tested patients responded to at

least two epitopes and 64% of the population responded to at least three epitopes,

39% to four or more, and 18% to five or more out of ten.

Even though OSE Immunotherapeutics did not reach the primary endpoints, the

company decided to pursue the work done by Epimmune for the following reasons:

HLA-2 positive is an unfavourable survival prognosis (Nagata et al, 2009). According to So et al, its expression in NSCLC is likely to be one of the mechanisms of escape from immune surveillance. Hence, OSE Immunotherapeutics suggest the phase II results may have met its primary endpoint if both arms had been HLA-2 positive.

A 17.3-month median survival rate is an extended lifetime in late-stage cancer (stage III/IV). To consolidate this argument, OSE Immunotherapeutics emphasised that advanced metastases represented 67% of HLA-2+ group population which is a poor prognosis of disease.

A sub-analysis demonstrated potential interest for patients presenting brain metastasis, a poor survival prognosis.

Long-term survival was also very interesting, with a 59% survival rate at one year

and a 25% survival rate at four years. While the five-year survival rate for stage IV

patients is 1% and 5% for stage IIIb, the overall response rate was only 3% (two

partial responses).

Meanwhile, it seems that Tedopi does not shrink the size of the tumour, contrary

to current CKIs, but it manages to control the evolution of metastasis.

OSE Immunotherapeutics Buy TP EUR 9.00

20 keplercheuvreux.com

Chart 13: Overall survival of HLA-A2–positive patients who received vaccines

Source: OSE Immunotherapeutics

That said, we bear in mind the controversial phase II design trial due to:

1. The selected patient population: HLA-2 positive versus HLA-2 negative patients non homogenous, contrary to what was designed in phase III.

2. Tedopi being used as a 2L therapy and not compared with a controlled active arm (e.g. in replacement of Taxotere).

3. The tiny sample of population in the phase II (n=135), of which 64 were in the active arm.

Hence, we question the capacity of OSE Immunotherapeutics to reproduce the

promise seen in phase IIb.

Despite these question marks, OSE Immunotherapeutics planned to launch a phase

III trial including only HLA-2 patients.

What needs to be proved in phase III? First, some definitions:

Progression-free survival (PFS): Time from random assignment until death or first documented relapse, categorised as either locoregional (primary site or regional nodes) failure, distant metastasis or death.

Overall survival (OS): The percentage of people in a study or treatment group who remain alive for a certain period of time after they started treatment of the disease.

Hazard ratios (HR): The ratio of the hazard rate in one group (e.g. a group of treated patients) to the hazard rate in another group (e.g. an untreated control group of patients). The hazard rate is the probability of a specified event, such as death or cancer recurrence, occurring during a short time interval. The hazard ratio, therefore, is a measure of the relative probability of an event occurring at any given point in time.

ORR (overall response rate): ORR is defined as the proportion of patients who achieve a complete or partial response against a clinical trial treatment.

Survival functionCensored

Time survived (days)

Cu

mu

lati

ve

su

rviv

al

1.0

0.8

0.6

0.4

0.2

0200 400 600 800 1,000

The design of phase II may jeopardise the reading of the results

OSE Immunotherapeutics Buy TP EUR 9.00

21 keplercheuvreux.com

Comparison with current checkpoint inhibitors Checkpoint inhibitors targeting the immune escape system from tumours are now

considered as the standard of care for the treatment of second line NSCLC after

progression with chemotherapy (e.g. docetaxel).

Opdivo from BMS (March 2015) and Keytruda from Merck (October 2015), two anti

PD-1, and one anti PD-L1 Tecentriq from Roche (October 2016) received all the

approvals in second line, leading to a fierce competitive environment.

These nodes were allowed thanks to a significant demonstration of the overall

survival benefit we highlight below.

OS

E Im

mu

no

B

uy

T

P E

UR

10

22

k

ep

lerch

eu

vre

ux

.com

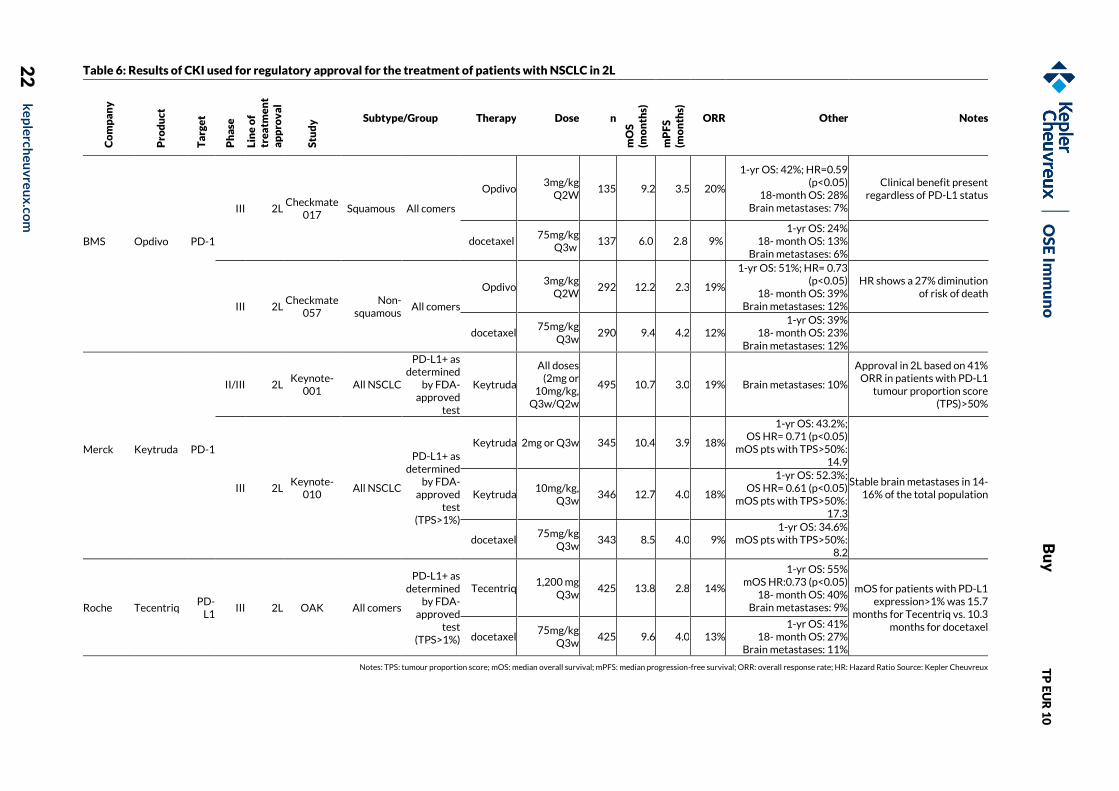

Table 6: Results of CKI used for regulatory approval for the treatment of patients with NSCLC in 2L

Co

mp

an

y

Pro

du

ct

Ta

rge

t

Ph

ase

Lin

e o

f tr

ea

tme

nt

ap

pro

va

l

Stu

dy

Subtype/Group Therapy Dose n

mO

S

(mo

nth

s)

mP

FS

(m

on

ths)

ORR Other Notes

BMS

Opdivo

PD-1

III 2L Checkmate

017 Squamous All comers

Opdivo 3mg/kg

Q2W 135 9.2 3.5 20%

1-yr OS: 42%; HR=0.59 (p<0.05)

18-month OS: 28% Brain metastases: 7%

Clinical benefit present regardless of PD-L1 status

docetaxel 75mg/kg

Q3w 137 6.0 2.8 9%

1-yr OS: 24% 18- month OS: 13%

Brain metastases: 6%

III 2L Checkmate

057 Non-

squamous All comers

Opdivo 3mg/kg

Q2W 292 12.2 2.3 19%

1-yr OS: 51%; HR= 0.73 (p<0.05)

18- month OS: 39% Brain metastases: 12%

HR shows a 27% diminution of risk of death

docetaxel 75mg/kg

Q3w 290 9.4 4.2 12%

1-yr OS: 39% 18- month OS: 23%

Brain metastases: 12%

Merck

Keytruda

PD-1

II/III 2L Keynote-

001 All NSCLC

PD-L1+ as determined

by FDA-approved

test

Keytruda

All doses (2mg or

10mg/kg, Q3w/Q2w

495 10.7 3.0 19% Brain metastases: 10%

Approval in 2L based on 41% ORR in patients with PD-L1

tumour proportion score (TPS)>50%

III 2L Keynote-

010 All NSCLC

PD-L1+ as determined

by FDA-approved

test (TPS>1%)

Keytruda 2mg or Q3w 345 10.4 3.9 18%

1-yr OS: 43.2%; OS HR= 0.71 (p<0.05)

mOS pts with TPS>50%: 14.9

Stable brain metastases in 14-16% of the total population Keytruda

10mg/kg, Q3w

346 12.7 4.0 18%

1-yr OS: 52.3%; OS HR= 0.61 (p<0.05)

mOS pts with TPS>50%: 17.3

docetaxel 75mg/kg

Q3w 343 8.5 4.0 9%

1-yr OS: 34.6% mOS pts with TPS>50%:

8.2

Roche Tecentriq PD-

L1 III 2L OAK All comers

PD-L1+ as determined

by FDA-approved

test (TPS>1%)

Tecentriq 1,200 mg

Q3w 425 13.8 2.8 14%

1-yr OS: 55% mOS HR:0.73 (p<0.05)

18- month OS: 40% Brain metastases: 9%

mOS for patients with PD-L1 expression>1% was 15.7

months for Tecentriq vs. 10.3 months for docetaxel

docetaxel 75mg/kg

Q3w 425 9.6 4.0 13%

1-yr OS: 41% 18- month OS: 27%

Brain metastases: 11%

Notes: TPS: tumour proportion score; mOS: median overall survival; mPFS: median progression-free survival; ORR: overall response rate; HR: Hazard Ratio Source: Kepler Cheuvreux

OSE Immunotherapeutics Buy TP EUR 9.00

23 keplercheuvreux.com

Keytruda have shown higher amplitude of difference versus OSE

Immunotherapeutics in overall survival in the Keynote-010 based on TPS> 50%.

Hence the OS was 17.3 months in the highest dose-range arm versus 8.2 months in

the compared arm. The overall response rate is much higher in the CKI arms than in

the phase II study including Tedopi.

Usually, regulatory agencies (FDA and EMA) focus on the comparison of OS for

the approval of oncology drug candidates. But it is worth notice that all recent

CKI approvals were also based on the partial/complete response rate and the

duration of response (the percentage of patients whose cancer shrinks or disappears

after treatment).

A meta-analysis of ORR, PFS and OS in advanced NSCLC trial (Blumenthal et al)

realised by the FDA, recently showed a patient-level association between response

and PFS and OS and a trial-level association between ORR and PFS, but not OS.

Accordingly, FDA guidance suggests that PFS is not well-correlated with overall

survival (OS) in NSCLC. OS is increasingly the gold standard with regulators and IO

companies – Roche developing Tecentriq has stated that it thinks it is the strongest,

most reliable endpoint in PD-L1 trials, and the one most likely to show the true

measure of patient benefit.

Therefore, we think Tedopi will need to show similar mOS while reaching

statistical significance versus the controlled arm in its phase III trial in order to get

the nod from the regulatory agencies.

Atalante 1: the phase III pivotal trial OSE Immunotherapeutics started the pivotal phase III Atalante 1 trial in January

2016. The design of the trial was approved by both the FDA and EMA in June 2014.

The primary endpoint is overall survival at two years and secondary endpoints

include PFS, ORR, tolerance and quality-of-life. OSE Immunotherapeutics expect to

enrol 500 patients across the US (20% of patient inclusion) and Europe (80% of

patient inclusion). Preliminary results are expected in 2018.

In case of positive results, the company expect a regulatory filing in 2019 both in

the US and in Europe.

The design of the study aims to show survival benefits versus Taxotere in second-

line or in third-line in the event of the use of a CKIs in second line.

This is an important difference compared to what was realised during phase II as

Tedopi was used as a second line therapy following chemotherapy.

The location countries will be the following: United States, Czech Republic, France,

Germany, Hungary, Italy, Poland, Spain, and the United Kingdom. As most of the

patients in US and EU5 countries will receive CKI, which is the new standard of

care for NSCLC, we expect the product will be injected following a CKI treatment

except in central and eastern European countries. Hence, we expect a final

regulatory labelling closer to a 3L following the use of a CKI rather than in 2L. It

also means that Tedopi will need to prove a superior effect versus Taxotere in

third line.

OSE Immunotherapeutics Buy TP EUR 9.00

24 keplercheuvreux.com

We bear in mind that PD-L1/PD-1 inhibitors showed a strong one-year OS rate in 2L

trials with a range between 42% to 55% for the PD-L1+ patients in second line,

similar to what was seen with Tedopi (59%) in phase II. Therefore, we consider the

design of the trial to be much more robust, but also significantly more risky for

Tedopi, and we remain cautious on the probability of clinical and commercial

success for the candidate.

To NSCLC in monotherapy…and beyond? Strategic approaches to oncology research targets:

The immune system through immuno-modulators.

The tumour itself (through radiotherapy, chemotherapy and tumour-targeting therapies).

So far, systemic treatments have associated immuno-modulators with treatment

targeting the tumours. However, this has raised some concerns as scientists gain a

better understanding of the tumour microenvironment.

The main issue in immuno-oncology is the ability of tumour cells to activate a

defence mechanism through the active CKIs of the immune-response. Inhibitors of

those checkpoint blockades allow the immune-response against cancer cells to be

restored. However, the complexity and heterogeneity of tumours, and their ability

to develop resistance to single-agent treatments, have fuelled research into

immunology combination therapy for cancer.

A second issue is the weak immunogenicity of tumours, as they are derived from the

body’s own cells. This is true with NSCLC, which is renowned for its weak immunity.

Overcoming resistance and restoring a functional immune surveillance system

requires the leveraging of multiple, complementary mechanisms of action and

agents that act in multiple phases of the cancer-immunity cycle.

The emerging scientific and clinical consensus is that in the future patients will

require both approaches to:

Generate a targeted immune response (e.g. through cancer vaccines like Tedopi).

Disrupt the checkpoint blockade (PD-1/PD-L1) and enhance the activity of activated T cells (OX-40 agonist).

Lower the tumour-associated microenvironment down regulating effect (e.g. with Effi-Dem).

Mechanisms of defence of tumour cells lead to IO treatment failures

OSE Immunotherapeutics Buy TP EUR 9.00

25 keplercheuvreux.com

Chart 14: Rationale for Tedopi and checkpoint inhibitor combination

Source: OSE Immunotherapeutics

Combinations have the potential to address different escape and activation

mechanisms. It is widely thought that these combination therapies based on the use

of cancer vaccines and checkpoint inhibitors could significantly expand the

effectiveness of immuno-oncology by:

Targeting complementary pathways.

Establishing synergistic effects.

Overcoming resistance to monotherapy.

Having a long-lasting effect.

Improving the risk- benefit profile of administered treatments.

In the past, immunotherapy was used primarily as an adjunct to radiotherapy,

chemotherapy or as a complement to surgical resection; however, the new

combination treatments are expected to become the new standard of care for the

treatment of cancer.

OSE Immunotherapeutics is currently preparing a combination study between

Tedopi and a CKI with a launch planned in H2 2017/early 2018. The company expect

to sign a scientific agreement to co-develop Tedopi with a CKI developer partner.

We expect this partner to be one of the marketed owners of CKI meaning BMS

(Opdivo), Merck &Co (Keytruda) or Roche (Tecentriq).

There is a rationale behind combining Tedopi with a CKI. Therefore, we believe the

future development of combination represents a significant upside opportunity

for OSE Immunotherapeutics in the life-cycle-management of Tedopi.

Other potential prospects Tedopi may potentially show efficacy in other tumours, in particular the non-

immunogenic one, also called cold tumour. Hence, in the event of failure in NSCLC,

OSE Immunotherapeutic may orientate its candidates towards cancers such as

pancreas or bladder cancers. The company has not disclosed any development plans

for now.

Activation of tumour-specific T cells

Tumour elimination

Tumour cell

Tumour cell CD80CD86

CD80CD86

CD28

CTLA-4

T cell

Epitope

Costimulatory Signal 2

Activation of tumour-specific T cells

Cell inhibition

Tumour cell

Tumour cell CD80CD86

CD80CD86

CD28

CTLA-4

T cell

Epitope

Costimulatory Signal 2

PD-1 T cells traffic to tumour

PD-1 PD-1PD-L1 PD-L1

Combinations key to successful treatment of cancer

OSE Immunotherapeutics Buy TP EUR 9.00

26 keplercheuvreux.com

Effi-DEM: the future immune-oncology blockbuster?

.

Myeloid-derived cell modulation holds promise Recently approved immune-modulator for the treatment of cancer primarily

explored the T-cell mechanisms corresponding to the adaptive immune system. It

has shown a durable control cancer in some patients by manipulating T cells with

checkpoint inhibitors (primarily PD-1/PD-L1) or co-stimulatory signals (OX-40).

Some of the agents covering these pathways became notorious blockbusters, such

as Opdivo from BMS or Keytruda from Merck&Co.

However, the benefit of these T cell modulating therapies only benefit a small number

of patients, as only 15% of patients respond to these modulators (e.g. checkmate-459

study with Opdivo in NSCLC). Hence, different checkpoints are utilised by different

cell types that contribute to the potency of anti-tumour immune response. Each

tumour being individualised, different tumours utilise different checkpoints.

Since the emergence of immune-therapy as a new paradigm with which to

treat cancer, the large pharmaceutical companies have focused on a small

number of checkpoint inhibitors mainly present in the cancer cells/effector T cells’

(CD8+) interaction.

Chart 15: Fierce competition in the Tumour/T cell checkpoint blockade

Source: Compugen

Effi-DEM is a preclinical candidate targeting the CD47/SIRPα interaction

between myeloid-derived cells and cancer cells. Also, although not yet clinically validated and based on scientific literature and

preclinical date delivered by OSE Immunotherapeutics, we believe targeting the SIRPα CKIs is promising.

OSE Immunotherapeutics Buy TP EUR 9.00

27 keplercheuvreux.com

Today, non-effector cell mechanisms such as myeloid cells are at the forefront of

research to explore new pathways to decrease relapse of tumours and enhance

the response rate for non-responding patients.

Hence, modern tumour immunotherapy is likely to consist of an association between

T cell modulators to release their brake (e.g. PD-1/PD-L1) and an inhibitor of the

suppressive cells in the tumour microenvironment.

OSE Immunotherapeutics aims to develop next-generation CKI targeting myeloid

cells (tumour associated macrophage (TAMs) and myeloid-derived suppressor cells

(MDSCs)) by binding the SIRPα/CD47 interaction.

Chart 16: T-cell effector mechanism for checkpoint (e.g.

Keytruda/Opdivo)

Chart 17: Non effector cell mechanisms (e.g. Effi-DEM)

Note: Non-exhaustive list of MOA Source: Kepler Cheuvreux, adapted from BMS Note: Non-exhaustive list of MOA Source: Kepler Cheuvreux, adapted from BMS

CD47 is shown to overexpress in almost all human cancers examined to date and its

high expression is associated with a poor prognosis of cancer survival.

A very large body of robust preclinical data and early clinical data indicate

CD47/SIRPα pathway as a very promising immuno-oncology target with PD-1-like

potential for treating a broad range of cancers. The solid science and substantial

potential of CD47/SIRPα-targeting have attracted significant industry interest.

Multiple CD47-targeting agents are in development from early discovery to

Phase 1 stage.

Tumour promotion by myeloid-derived cells Macrophages as effector cells

Macrophages are a type of white blood cell typically broken down into two subtypes

depending on their role in either healing (M2) or immune function (M1).

Macrophages are found in tissues throughout the body, but they originate from

monocytes that enter the tissue from blood vessels when damage is incurred by

surrounding cells.

In a classic immunologic model, M1 macrophages carry out their immune function by

recognising foreign pathogens, engulfing them in a process known as phagocytosis

and initiating a cascade of chemical signals that promote inflammation and recruit

the adaptive immune system. Healing macrophages, classified as M2 macrophages,

typically arrive two days after the initiation of an immune response to decrease

T cellActivating checkpointCD137GITROX40

Inhibitory checkpointCTLA4PD1/PDL1Lag3

Inhibitory checkpointCD73CSF1RIDOCTLA4SIRa

RegulatoryT cell

Tumour associated macrophage Dendritic cell

(APC

OSE Immunotherapeutics Buy TP EUR 9.00

28 keplercheuvreux.com

inflammation, increase the formation of new blood vessels, and facilitate tissue

following the elimination of pathogens.

Role of myeloid suppressive cells

Experimental studies indicate that myeloid cells modulate key cancer-associated

activities, including immune evasion, and affect virtually all types of cancer therapy.

Myeloid suppressive cells, including tumour associated macrophages (TAM/M2

macrophage) and myeloid-derived suppressor cells (MDSC), represent an abundant

immune cell type in the microenvironment of solid tumours, where they promote

tumour growth, metastases, angiogenesis, inhibiting anti-tumour immune responses.

Normally, common myeloid progenitor (also called immature myeloid cells) migrate

to different peripheral organs, where they differentiate exclusively into dendritic

cells and macrophages type M1 or polymorphonuclear cells (also named

granulocytes). However, several factors produced in many pathological conditions

promote the accumulation of immature myeloid cells, prevent their differentiation

and induce their activation. These cells exhibit immunosuppressive functions after

activation and were named MDSC (Gabrilovich et al, 2007).

According to the literature, MDSC reduce activated T-cell number and inhibit their

function by multiple mechanisms including depletion of L-arginin by arginase-1

(ARG1), production of NO (nitric oxide).

The second category of myeloid cells, called TAMs, is found to be involved in almost

all of the tumour development pathways:

Tumour cell proliferation.

Angiogenesis (formation of cancer vessels).

Tumour cell invasion.

Immunosuppression.

TAMs cells play an important role in tumour progression

OSE Immunotherapeutics Buy TP EUR 9.00

29 keplercheuvreux.com

Chart 18: The role of myeloid cells in cancer

Source: Engblom et al, 2016

Therefore, there is a certain rationale behind the development of TAM and MDSC

checkpoint inhibitors due to the following reasons:

TAMs and MDSCs are immunosuppressive and act by inhibiting CD8 T cell responses while enhancing recruitment and differentiation of regulatory T cells or Tregs.

TAMs and MDSCs are often correlated with a poor prognosis in cancer patients.

Consequently, targeting myeloid cells could overcome the limitations of current

treatment options, whose activity is inhibited by myeloid-derived cells.

Mechanism of action of Effi-DEM Effi-DEM has a dual effect. It operates through macrophages (innate immune

system) and may exert downstream effects on the adaptive immune system (T cells)

in the tumour environment. Hence, it presents a competitive advantage by acting

on both the adaptive and innate immune systems.

Reactivation of macrophages

Myeloid cells selectively express SIRPα, an immune tyrosine associated inhibitory

receptor (also named CD172a), which controls myeloid functions.

The ligand of SIRPα is CD47. CD47 is expressed in almost all normal human cells. In

case of tumour, it may be an up-regulation of CD47 which leads to several adverse

effects for the immune-control of the tumour. Expression of CD47, and its

interaction with SIRPα, leads to the inhibition of macrophage activation and protects

cancer cells from phagocytosis (the macrophage aims to “eat” the cancer cells).

Therefore, it allows cancer cells to proliferate. Hence, CD47 send a “don’t eat me”

signal to the patrolling macrophages type M1, which is being bound by EFFI-DEM.

OSE Immunotherapeutics Buy TP EUR 9.00

30 keplercheuvreux.com

Chart 19: SIRPα inhibitor (Effi-DEM) allow phagocytosis to be reactivated

Source: Trillium Therapeutics

Reactivation of T cell functions while blocking MDSC/TAMs

TAMs and MDSCs are an important component of the tumour microenvironment

and play a major role in creating the immunosuppressive environment that enables

tumour development. Blocking SIRPα allow MDSCs to differentiate into non-

suppressive tumour cells. According to the literature, it also promotes human

subtype M1 macrophages, which has antitumour effects (pro-inflammatory), while

decreasing the M2 subtype (pro-tumoural effect)

Hence, Effi-DEM may be a first-in-class product tackling myeloid suppressive cells

(MDSC, TAM) while promoting macrophages phagocytosis and therefore dendritic

cell function.

Chart 20: Mechanism of action of Effi-DEM

Source: OSE Immunotherapeutics

The myeloid cell modulation: a hotspot in the biotech space We emphasised that Effi-DEM may be a first-in-class product targeting the SIRPα

receptor. However, there are several players already involved in early-stage

development of inhibitor of its ligand CD47. While in our knowledge no other

OSE Immunotherapeutics Buy TP EUR 9.00

31 keplercheuvreux.com

company target the SIRPα ligand, several anti-CD-47 are being studied by other

biotechnology companies.

Table 7: Competitive environment for Effi-DEM in CD47/ SIRPα pathway

Company Indication Drug Development stage

Note

Celgene/Inhibrx Hematologic malignancies

CC900002 (CD47 mAb) Phase I Celgene acquired CC900002 from Inhibrx for a USD500m deal size in 2012

Trillium Therapeutics Hematologic malignancies

TTI-621(CD47 mAb) Phase I Listed company MC: c. CAD55m

Stanford University Solid tumours CD47 mAb Phase I Tioma Therapeutics Cancer Anti CD47 mAb Pre-clinical Raised USD86m in series A financing in August

2016 led by Novo Venture, Roche and GSK Venture arms

Alexo Therapeutics Cancer SIRPα variants that antagonise CD47 Pre-clinical Raised USD36m in a Series A in May 2015 led by venBio

Forty Seven Hematologic malignancies

Hu5F9-G4, humanised anti- CD-47 mAb Phase I Raised USD75m is a series A in February 2016

Novimmune B-Cell leukaemia/ lymphoma

NI1701 (bispecific CD19xCD47) Pre-clinical Privately-held Swiss biotech founded in 1998

Source: Kepler Cheuvreux

CD47 topic is currently a hotspot in the biotechnology industry. According to data

pooled with EvaluatePharma, FortySeven and Tioma Therapeutics, series A funding

has been among the top ten for a decade in the oncology space (based on a sample of

429 companies).

Competitive advantage versus current CD47 inhibitor

One main difference between both approaches is the targets. CD47 is present in the

tumour while SIRPαis particularly abundant in the myeloid cells. The difference of

location allows Effi-DEM to act on the innate immune function by activating the

phagocytosis and priming the adaptive immune response through the blockade of

MDSCs immunosuppressive function.

Additionally, one major advantage is the selectivity of Effi-DEM for SIRPα. While

CD47 has other binders than SIRPα, which may lead to several off-target effects,

SIRPαsolely binds CD47. Hence, according to OSE Immunotherapeutics, a better

safety clinical profile of Effi-DEM may result from this particular selectivity.

Indeed, CD47 is found in almost all healthy cells, notably red blood cells. CD47 can

interact with the secreted protein thrombospondin-1 (TSP1), in addition to SIRPα

(Expert Opin Ther Targets 2013). Upon binding to TSP1, CD47 transduces signals

that alter cellular calcium, cyclic nucleotide, integrin, and growth factor signalling

and control cell fate, viability, and resistance to stress.

Hence, targeting CD47 is likely to induce potential side effects including altered

blood pressure (Bauer et al, 2010), haemolytic anaemia, and prothrombotic or

antithrombotic activities (Isenber et al, 2008). Another potential side effect which

may be lower by selectively binding SIRPα, is the abundance of CD47 in red blood

cells. This is important, as targeted therapies for CD47 have been found to induce

anaemia and get lower bio-distribution. Hence, the therapeutic window for anti-

CD47 is particularly low.

Effi-DEM is likely to show a better safety profile than peers

OSE Immunotherapeutics Buy TP EUR 9.00

32 keplercheuvreux.com

Safety concerns about anti-CD47 have been recently emphasised through the

drop in the share price of Trillium Therapeutics. On 2 November 2016, Trillium

saw a 52% pullback after its ASH abstract revealed cases of liver toxicity and

thrombocytopenia in the highest dose of 0.3mg/kg in TTI-621’s phase I dose-

escalation trial.

Due to its original mechanism of action, we are enthusiastic about the prospect of

Effi-DEM.

Effi-DEM: an IO blockbuster candidate? So far, OSE Immunotherapeutics has released pre-clinical datasets that have

demonstrated the ability of Effi-DEM to inhibit breast cancer growth in

monotherapy. The company used animal models (murine) to carry out these

preliminary tests.

Chart 21: Inhibition of breast cancer growth (1)

Chart 22: Inhibition of breast cancer growth (2)

Source: OSE Immunotherapeutics Source: OSE Immunotherapeutics

The company has also shown a synergistic effect with an anti PD-L1 antibody in

melanoma and HCC (hepatocarcinoma) as well as a big effect with 4-1BB (co-

stimulatory molecule for T cell) in HCC.

Chart 23: Synergy with PD-L1

Chart 24: Synergy with 4-1BB agonist

Source: OSE Immunotherapeutics Source: OSE Immunotherapeutics

CTRL Ab (n=16)aSIRPa (n=13)

Days

Tu

mo

ur

vo

lum

e(m

m3)

1,500

1,250

1,000

750

500

250

0 5 10 15 20 25 30 350

Control Ab Anti-SIRPa

Week 4

Tu

mo

ur

vo

lum

e

(mm

^3

)

P< 0.01

80

60

40

20

0

800

600

400

200

0

300

200

100

0

1,500

1,000

500

0

Tu

mo

ur

vo

lum

e

(mm

^3

)

Tu

mo

ur

vo

lum

e

(mm

^3

)

Tu

mo

ur

vo

lum

e

(mm

^3

)

Control Ab Anti-SIRPa

Control Ab Anti-SIRPaControl Ab Anti-SIRPa

Week 5

Week 2 Week 3

P< 0.01

P< 0.001 P< 0.05

Ctrl Ab

SIRPa Ab

Time (days)

Pe

rce

nt

surv

iva

l

100

80

60

40

20

0 10 15 20 25 30 35 400

PD-L1 Ab

Combination

5

CTRL AbaSIRPa

Days

Pe

rce

nt

surv

iva

l

100

80

60

40

20

0 10 20 30 40 50 60 700

4-1BB AbCombinationP < 0.05 P < 0.01

OSE Immunotherapeutics Buy TP EUR 9.00

33 keplercheuvreux.com

We think SIRPαmay reveal its potential with such a combination as there is a

rationale to target both the innate and the immune system to avoid immune escape

mechanisms.

Thanks to these positive preclinical data, OSE Immunotherapeutics expects to

enter into clinical by the end of 2018.

That being said, we highlight specific risks that may arise as part of the development

of Effi-DEM:

The CD47/SIRPα pathway is not yet a clinically validated target. Clinical safety concern arised from Trillium Therapeutics following the phase I update, while efficacy data has not yet been released.

Effi-DEM is far from the cusp to reach clinical-stage status as it plans to enter clinical stage in H2 2018; besides, other competitors may arise from there.

While Effi-DEM may limit the safety issue of CD47 inhibitors, OSE Immunotherapeutics did not release any preclinical safety data and there is no evidence that the CKIs will enter the clinical stage.

Intellectual property

So far, Effi-DEM has been protected by three families of patents. The first patents

were granted by the European patent office (EPO) in April 2016. A second family is

being examined by the EPO and the filing date was October 2015. Regarding the US,

a first patent application was initiated in May 2016.

Our analysis suggests positive optionality for OSE Immunotherapeutics’ Effi-DEM

programme.

We think Effi-DEM and modulations of MDSCs through SIRPα/CD47 pathway are

still under the radar for most investors in Europe but are a new hotspot in the US.

Despite positive preclinical data, notably in combination, we think investors do not

sufficiently value this early-stage asset.

OSE Immunotherapeutics Buy TP EUR 9.00

34 keplercheuvreux.com

FR104 and Effi-7: already monetised FR104 and Effi-7 are two monoclonal antibodies developed in autoimmune

diseases. Both assets have already been out-licensed to partners by OSE

Immunotherapeutics.

FR104 has been partnered with J&J, providing a EUR10m opt-in option

payment to OSE Immunotherapeutics in July 2016. In the event of clinical

success, FR104 is likely to become a blockbuster with strong activity both in

rheumatology as well as in transplant complication management. FR104 is no

longer a source of cost but, conversely, a cash inflow opportunity for OSE

Immunotherapeutics. Indeed, J&J, following its opt-in options, will fund all

development costs starting from now. Therefore, FR104 is a potential source

of cash-in for OSE Immunotherapeutics.

OSE Immunotherapeutics secured EFFI-7 through an out-license deal with

Servier in December 2016 with an opt-in option after the completion of phase II.

Funding until phase II is also partly secured thanks to a consortium led by OSE

Immunotherapeutics.

We believe these two assets will provide sufficient funding to the company to

finance EFFI-DEM development, therefore significantly derisking the profile of

OSE Immunotherapeutics.

FR104: a ground-breaking opportunity in autoimmune diseases

The role of Treg cells Accumulating scientific data demonstrate that regulatory T-cells (Treg), a

subpopulation of CD4+ T-cells, play an important role in dampening the immune

response. Treg cells appear to suppress the action of other T-cell subsets by a number

of mechanisms. Suppression by Treg is thought to involve the anti-inflammatory

cytokines IL-10 and transforming growth factor beta (TGF-β). Reduced expression of

both molecules, as well as decreased proliferation of the regulatory CD4+ T-cell

subsets producing IL-10, have been demonstrated in RA patients.

Thus, there is a scientific rationale for the use of Treg for the treatment of RA, as it

might allow the T-cell homeostasis to be maintained.

FR104 modulates Treg to enhance autoimmune conditions.