a fleet facing a demanding society … fleet facing a demanding society ... and four times dearer...

TRANSCRIPT

1

A FLEET FACING A DEMANDING SOCIETY

International Seminar of Government & International Seminar of Government & Oil/Shipping Industry Cooperation Moving Oil/Shipping Industry Cooperation Moving

F d T thF d T th

ARNALDO ARCADIERARNALDO ARCADIERExecutive ManagerExecutive Manager

TRANSPETROTRANSPETRO

01

NOVEMBER 2009NOVEMBER 2009

Forward TogetherForward Together

TRANSPETROTRANSPETRO

PETROBRAS TRANSPORTATION AND LOGISTICS ENTERPRISEPETROBRAS TRANSPORTATION AND LOGISTICS ENTERPRISEACTIVITIES: TRANSPORTATION AND STORAGE OF CRUDE, OIL ACTIVITIES: TRANSPORTATION AND STORAGE OF CRUDE, OIL

PRODUCTS, NATURAL GAS AND BIOFUELSPRODUCTS, NATURAL GAS AND BIOFUELS

59 Million tons shipped by sea

670 Million m3 of crude, oil products and

ethanol

53 vessels53 vessels2.9 Million DWT2.9 Million DWT

02

47 Terminals47 Terminals10.3 Million m³ 10.3 Million m³

7,100 km7,100 kmOil PipelinesOil Pipelines

4,400 Km 4,400 Km Gas PipelinesGas Pipelines

TRANSPETRO SHIPPING TRANSPETRO SHIPPING

Typical Operations

03

COASTAL AND OCEAN NAVIGATIONS COASTAL AND OCEAN NAVIGATIONS –– NT PIRAJUÍNT PIRAJUÍ

04

INLAND NAVIGATION INLAND NAVIGATION –– NT NILZANT NILZA

05

OFSHORE BUNKERING OFSHORE BUNKERING –– NT MAÍSANT MAÍSA

06

2

OFFLOADING OPERATIONS WITH DP SHUTTLE TANKERSOFFLOADING OPERATIONS WITH DP SHUTTLE TANKERSNT ATAULFO ALVESNT ATAULFO ALVES

07

FSO IN SANTOS BASIN FSO IN SANTOS BASIN –– NT AVARÉNT AVARÉ

08

SHIP TO SHIPSHIP TO SHIP

09

LPG CARRIERS LPG CARRIERS –– NT GUAPORÉNT GUAPORÉ

10

PLATFORM SUPPLY VESSEL (PSV) PLATFORM SUPPLY VESSEL (PSV) –– TANGARÁTANGARÁ

11

SINGLE POINT MONOBUOY SINGLE POINT MONOBUOY –– NT BROTASNT BROTAS

12

3

FPSO/FSO OFFLOADING FPSO/FSO OFFLOADING –– OCEANIC TERMINALSOCEANIC TERMINALS

13

MARITIME INDUSTRIES CHALLENGESMARITIME INDUSTRIES CHALLENGES

Shipmanagers Shipowners

Port State Authorities

Flag State Authorities

Traders & Brokers

Maritime Terminals

IMO

Insurance Companies Classification

SocietiesShareholders Crews

Society

14

OPERATIONAL COMMITMENTSOPERATIONAL COMMITMENTS

HSE•Injury Rates Reduction •Nutrition and Physical Activities Program•Contingence Plans

SMT•Medical Prevention in Transpetro•Alcohol and Drugs Politics

15

g

Crew Management - 2300 Seamen

Training •Courses and Seminars•Cadets and Apprentices (Electricians and similars)

Key Performance Indicators

HSEHSE

HSE – Nutrition and Physical Activities Program• Started in 2006• Up to now 1500 seamen attended • Onboard visit of Nutrition and Physical Professionals• Evaluation for Glycemia, Tobacco, Overweight, Hypertension, Sedentarism• Healthy food

16

HSE – Contingency Plans - Influenza A (H1N1)• Kit for Individual Protection distributed for all the fleet• Masks, gloves, cloth protections, caps• Hygienical Behaviors Procedures• Antiviral Medicine distribution• Permanent Medical Orientation – 24 h / 7 days

COURSES AND SEMINARSCOURSES AND SEMINARS

Human Factor - 31 Courses with the participation of 539 employees

(sea and shore teams)

Risk Management - 8 Courses with the participation of 160 employees

(sea and shore teams)

17

Rating Seminars - 17 Courses with participation of 470 seamen

Onboard Training – Covering both officials and rating (average of 280 seamen per year)

FIRST WOMAN TO BE A CAPTAIN IN BRAZILIAN MARINE MERCHANTFIRST WOMAN TO BE A CAPTAIN IN BRAZILIAN MARINE MERCHANT

18

4

ONLINE FLEET POSITION CONTROL ONLINE FLEET POSITION CONTROL -- GEOABASTGEOABAST

19

ONLINE FLEET POSITION CONTROL ONLINE FLEET POSITION CONTROL -- GEOABASTGEOABAST

20

CNCO CNCO –– NATIONAL OPERATIONAL CONTROL CENTERNATIONAL OPERATIONAL CONTROL CENTER

21

BRAZILBRAZIL –– PETROBRASPETROBRAS

PROMEFFleet Modernization and

Expansion Program

22

GOVERNMENT GUIDELINESGOVERNMENT GUIDELINES

• All opportunities must be used to foster

national development and ensure the

well-being of Brazilians.

• Oil must be deployed as a tool for• Oil must be deployed as a tool for

generating jobs and incomes.

23

PROMEFPROMEF –– TRAJECTORYTRAJECTORY

PROMEFFleet Modernization and Expansion Program

24

5

SHIPPING HIGHLIGHTSSHIPPING HIGHLIGHTS

• 80% of world trade is carried on ships.

• In Brazil, trade handled by ships reaches 95%, with less than 4%

currently carried under the Brazilian flag.

• Last year, Brazil spent

US$ 16 billion on shipping andUS$ 16 billion on shipping, and

Petrobras spent US$ 2 billion

on charters.

25

SHIPBUILDING INDUSTRYSHIPBUILDING INDUSTRY

• The global portfolio reported by

shipyards is more than 8,000 vessels.

• This capacity is tightly clustered in

Korea, China and Japan.

• Investments in Shipbuilding reach

US$ 140 billion a year.

• The world’s second-largest

shipbuilder during the 1970s, Brazil

has slipped behind.

26

SHIPBUILDING INDUSTRYSHIPBUILDING INDUSTRY

27

SHIPBUILDING INDUSTRYSHIPBUILDING INDUSTRY

28

COASTLINE AND MAIN RIVERSCOASTLINE AND MAIN RIVERS

Brazil needs ships.

• 95% of its foreign trade

depends on maritime

transportation

• 8 000 km (5 000 miles) of

29

• 8,000 km (5,000 miles) of

coastline

• 42,000 km (26,000 miles) of

navigable rivers

BRAZILIAN CASE OF GLOBAL COMPETITIVENESS BRAZILIAN CASE OF GLOBAL COMPETITIVENESS -- EMBRAEREMBRAER

30

6

TASKS AND CHALLENGESTASKS AND CHALLENGES

31

TASKS AND CHALLENGESTASKS AND CHALLENGES

32

TASKS AND CHALLENGESTASKS AND CHALLENGES

• To reconstruct Brazil’s shipbuilding industry on competitive bases.

• To re-shape the logic underpinning Brazil’s transportation matrix.

• Almost 60% of Brazil’s transportation matrix is road-based, which is twice as

expensive as rail transportation, and four times dearer than maritime

transportation.

• New vessels required for coastal shipping and ocean going transportation.

• Qualify the work force.Qualify the work force.

• Exclusive financing through the Merchant Marine Fund (FMM).

33

TASKS AND CHALLENGESTASKS AND CHALLENGES

34

THE PATH TO GLOBAL COMPETITIVENESSTHE PATH TO GLOBAL COMPETITIVENESS

Shipyard facilities and TechnologyShipyard facilities and Technology

Longitudinal sleepway

Dry dock

Technology

Assembling

10 – 50 toncrane

100 – 300 toncrane / goliath

500 – 1500 ton crane / goliath

Manual/opticalcutting

Plasma cuttingsemiautom.

welding

Laser cuttingrobbot welding

CAD CAD/CAM CAD/CAM/CIM

35

Liftingcapacity

Steel processing

I T

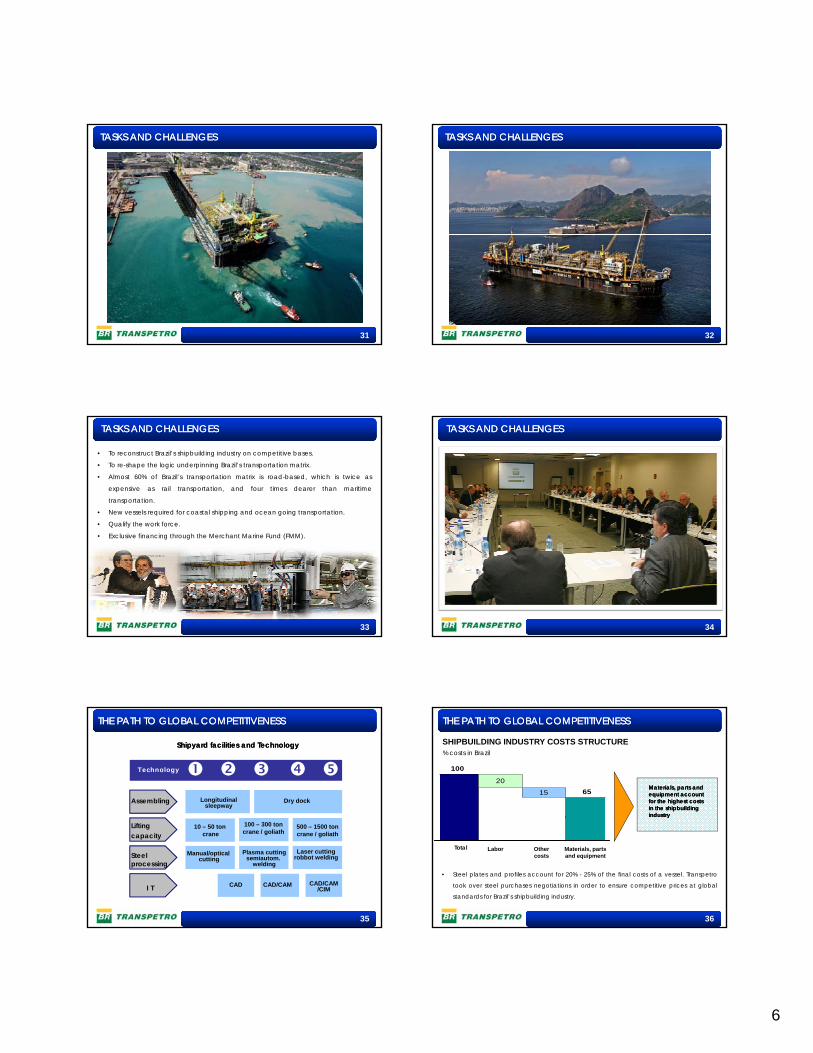

SHIPBUILDING INDUSTRY COSTS STRUCTURE% costs in Brazil

Materials, parts and Materials, parts and equipment account equipment account for the highest costs for the highest costs in the shipbuilding in the shipbuilding industry industry

THE PATH TO GLOBAL COMPETITIVENESSTHE PATH TO GLOBAL COMPETITIVENESS

20

15

100

65

Total Labor Other costs

Materials, parts and equipment

yy

• Steel plates and profiles account for 20% - 25% of the final costs of a vessel. Transpetro

took over steel purchases negotiations in order to ensure competitive prices at global

standards for Brazil’s shipbuilding industry.

36

7

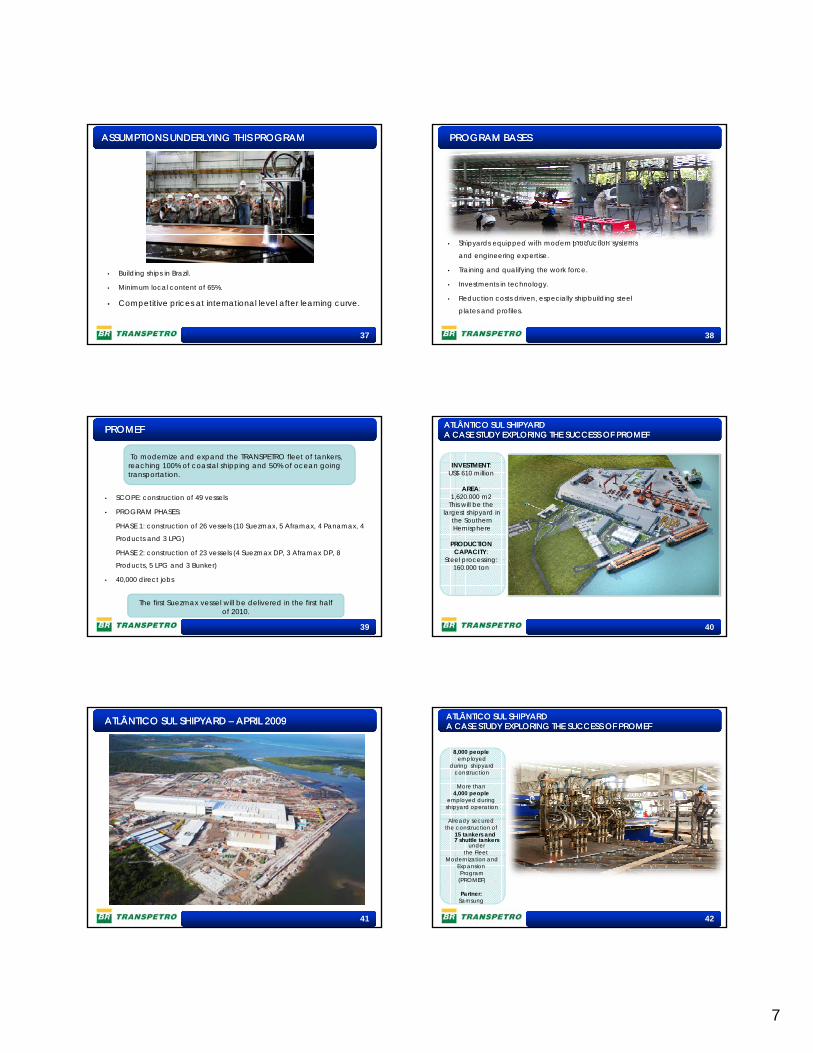

ASSUMPTIONS UNDERLYING THIS PROGRAMASSUMPTIONS UNDERLYING THIS PROGRAM

• Building ships in Brazil.

• Minimum local content of 65%.

• Competitive prices at international level after learning curve.

37

PROGRAM BASESPROGRAM BASES

• Shipyards equipped with modern production systems

and engineering expertise.

• Training and qualifying the work force.

• Investments in technology.

• Reduction costs driven, especially shipbuilding steel

plates and profiles.

38

PROMEFPROMEF

To modernize and expand the TRANSPETRO fleet of tankers, reaching 100% of coastal shipping and 50% of ocean going transportation.

• SCOPE: construction of 49 vessels

• PROGRAM PHASES:

PHASE 1: construction of 26 vessels (10 Suezmax 5 Aframax 4 Panamax 4 PHASE 1: construction of 26 vessels (10 Suezmax, 5 Aframax, 4 Panamax, 4

Products and 3 LPG)

PHASE 2: construction of 23 vessels (4 Suezmax DP, 3 Aframax DP, 8

Products, 5 LPG and 3 Bunker)

• 40,000 direct jobs

The first Suezmax vessel will be delivered in the first half of 2010.

39

ATLÂNTICO SUL SHIPYARDATLÂNTICO SUL SHIPYARDA CASE STUDY EXPLORING THE SUCCESS OF PROMEF A CASE STUDY EXPLORING THE SUCCESS OF PROMEF

INVESTMENT: US$ 610 million

AREA: 1,620.000 m2

This will be thelargest shipyard in

the SouthernH i hHemisphere

PRODUCTIONCAPACITY:

Steel processing: 160.000 ton

40

ATLÂNTICO SUL SHIPYARD ATLÂNTICO SUL SHIPYARD –– APRIL 2009APRIL 2009

41

8,000 peopleemployed

during shipyardconstruction

More than 4,000 people

employed duringshipyard operation

ATLÂNTICO SUL SHIPYARDATLÂNTICO SUL SHIPYARDA CASE STUDY EXPLORING THE SUCCESS OF PROMEF A CASE STUDY EXPLORING THE SUCCESS OF PROMEF

Already secured the construction of

15 tankers and 7 shuttle tankers

under the Fleet

Modernization andExpansionProgram

(PROMEF)

Partner:Samsung

42

8

ATLÂNTICO SUL SHIPYARDATLÂNTICO SUL SHIPYARDFIRST BLOCKS IN THE DRYFIRST BLOCKS IN THE DRY--DOCK (JUNE 2009)DOCK (JUNE 2009)

43

ATLÂNTICO SUL SHIPYARD ATLÂNTICO SUL SHIPYARD GENERAL VIEW OF PANEL LINE FACILITIESGENERAL VIEW OF PANEL LINE FACILITIES

44

ATLÂNTICO SUL SHIPYARD ATLÂNTICO SUL SHIPYARD –– DRYDRY--DOCKDOCK

45

ATLÂNTICO SUL SHIPYARD ATLÂNTICO SUL SHIPYARD DRYDRY--DOCK VIEW (SEPTEMBER 2009)DOCK VIEW (SEPTEMBER 2009)

46

ATLÂNTICO SUL SHIPYARD ATLÂNTICO SUL SHIPYARD KEEL LAYING (SEPTEMBER 2009)KEEL LAYING (SEPTEMBER 2009)

47

ATLÂNTICO SUL SHIPYARD ATLÂNTICO SUL SHIPYARD KEEL LAYING (SEPTEMBER 2009)KEEL LAYING (SEPTEMBER 2009)

48

9

ATLÂNTICO SUL SHIPYARD ATLÂNTICO SUL SHIPYARD KEEL LAYING (SEPTEMBER 2009)KEEL LAYING (SEPTEMBER 2009)

49

ATLÂNTICO SUL SHIPYARD ATLÂNTICO SUL SHIPYARD ASSEMBLY WORK IN PROGRESS (OCTOBER 2009)ASSEMBLY WORK IN PROGRESS (OCTOBER 2009)

50

MAUÁ SHIPYARD MAUÁ SHIPYARD –– PREPRE--ASSEMBLY ACTIVITIESASSEMBLY ACTIVITIES

51

MAUÁ SHIPYARD MAUÁ SHIPYARD –– PREPRE--ASSEMBLY SHOPASSEMBLY SHOP

52

MAUÁ SHIPYARD MAUÁ SHIPYARD –– DOUBLE BOTTOM BLOCKSDOUBLE BOTTOM BLOCKS

53

MAUÁ SHIPYARD MAUÁ SHIPYARD –– BLOCKS AT THE SLIPWAYBLOCKS AT THE SLIPWAY

54

10

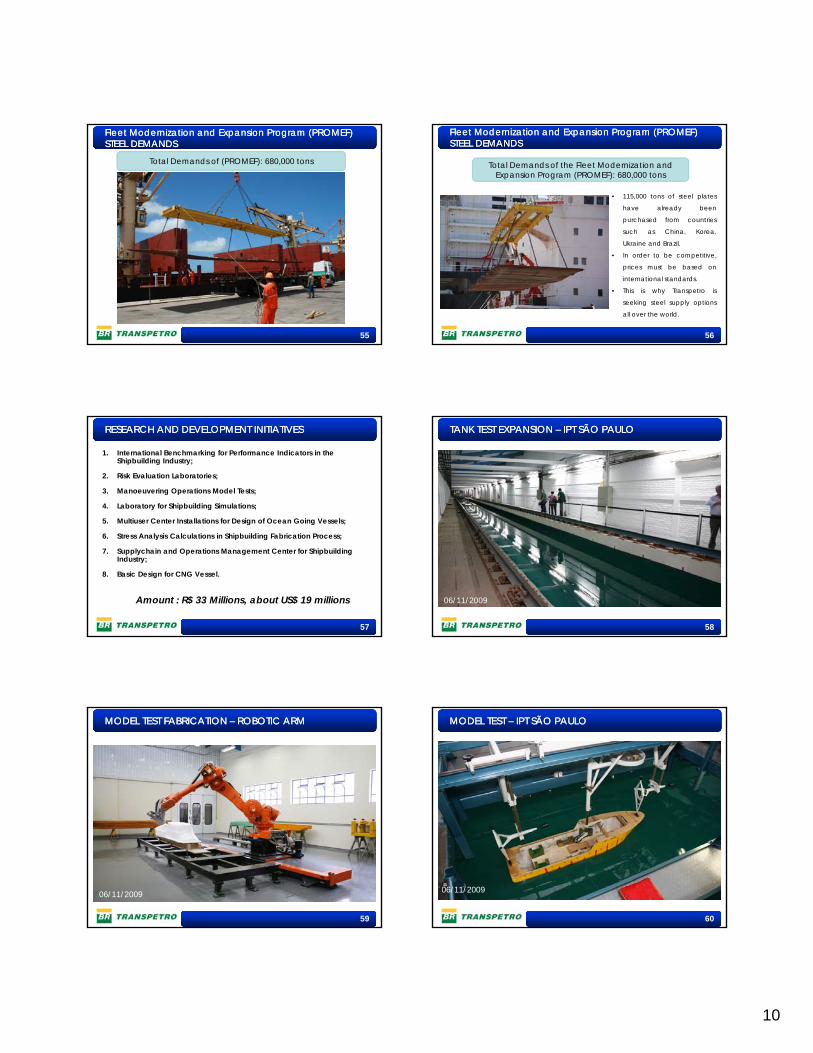

Total Demands of (PROMEF): 680,000 tons

Fleet Modernization and Expansion Program (Fleet Modernization and Expansion Program (PROMEFPROMEF) ) STEEL DEMANDSSTEEL DEMANDS

55

Total Demands of the Fleet Modernization and Expansion Program (PROMEF): 680,000 tons

Fleet Modernization and Expansion Program (PROMEF) Fleet Modernization and Expansion Program (PROMEF) STEEL DEMANDSSTEEL DEMANDS

• 115,000 tons of steel plates

have already been

purchased from countries

such as China, Korea,

Ukraine and Brazil.

• In order to be competitive,

prices must be based on

international standards.

• This is why Transpetro is

seeking steel supply options

all over the world.

56

1. International Benchmarking for Performance Indicators in the Shipbuilding Industry;

2. Risk Evaluation Laboratories;

3. Manoeuvering Operations Model Tests;

4. Laboratory for Shipbuilding Simulations;

5. Multiuser Center Installations for Design of Ocean Going Vessels;

RESEARCH AND DEVELOPMENT INITIATIVESRESEARCH AND DEVELOPMENT INITIATIVES

6. Stress Analysis Calculations in Shipbuilding Fabrication Process;

7. Supplychain and Operations Management Center for Shipbuilding Industry;

8. Basic Design for CNG Vessel.

Amount : R$ 33 Millions, about US$ 19 millions

57

TANK TEST EXPANSION TANK TEST EXPANSION –– IPT SÃO PAULOIPT SÃO PAULO

06/11/2009

58

MODEL TEST FABRICATION MODEL TEST FABRICATION –– ROBOTIC ARMROBOTIC ARM

06/11/2009

59

MODEL TEST MODEL TEST –– IPT SÃO PAULOIPT SÃO PAULO

06/11/2009

60

11

BRASIL BRASIL –– NEW OPPORTUNITIESNEW OPPORTUNITIES

61

OPPORTUNITIES FOR REPAIR SHIPYARDS AND EQUIPMENT INDUSTRIES OPPORTUNITIES FOR REPAIR SHIPYARDS AND EQUIPMENT INDUSTRIES

• Construction of repair shipyards – each

year 4,600 ships sail along the Brazilian

coastline, where no modern repair

facilities are available.

E t bli h t i l i • Establish enterprises supplying

equipment, parts, services and repair for

shipyards and shipowners.

Main maritime trades

62

OPPORTUNITIES FOR SHIPYARDS OPPORTUNITIES FOR SHIPYARDS –– NEW BUILDINGS NEW BUILDINGS

• The 49 ships planned through the Fleet Modernization and Expansion Program

(PROMEF) are insufficient, unable to respond in full to future demands prompted

by Brazil’s pre-salt oilfields and the expansion of the biofuels market, including

ethanol.

• The development of the pre-salt oilfields and investments in biofuels are triggering

additional demands for ships, platforms, rigs, FPSOs and supply boats.

• Petrobras will sign contracts covering 40

drilling rigs, 70 tankers,146 supply boats and

10 FPSOs.

• Brazil’s National Shipbuilding Industry

Association estimates that orders from this

sector will reach 214 new vessels by 2015.

63

Shipbuilding in Brazil must reach competitivess at a world level, bein necessary to overcome challenges

related to steel plates price, labour productivity, R&D and equipment supplies Transpetro through

SHIPBUILDING SECTOR SUSTEINABILITY IN BRAZILSHIPBUILDING SECTOR SUSTEINABILITY IN BRAZIL

R&D and equipment supplies. Transpetro through PROMEF – Fleet Modernization and Expansion

Program - is promoting the first steps of this process and its continuity will lead Brazil to have a modern

and susteinable shipbuilding industry.

64

CHALLENGE OPPORTUNITYOPPORTUNITY

ENTREPRENEURSHIPENTREPRENEURSHIP

PARTNERSHIPPARTNERSHIP

MANY THANKSMANY THANKS

CAPACITYCAPACITYTECHNOLOGYTECHNOLOGY

www.transpetro.com.br

65