a general equilibrium model of supply chain...

TRANSCRIPT

A General Equilibrium Model of Supply ChainInteractions and Risk Propagation

John Birge and Jing Wu1

1University of Chicago Booth School of Business

SCF Symposium, Madrid

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 1 / 29

S&P 500 Supply Chain Network

ADI

A

ANSS

FLEX

JBL

NTAP

SNPS

XLNX

CSC

AA

CSX

FLR

ORCL

PPG

ASH

AAP

BWA

DLPH

FBHS

HON

ITW

JCI

MMM

PCAR

SHWAAPL

ADBE

AKAM

APH

ATVI

AVGO

AVT

BRCM

CBS

CSCO

CTXS

DD

DOV

EA

EMR

EQIX

FB

FFIV

FISV

GLW

GOOG

INTC

IP

LLTC

MCHP

MOLX

MRVL

MU

MXIM

NUAN

NVDA

NXPI

QCOM

RAX

SNDK

STX

SWK

SWKS

TDC

TEL

TXN

VIAB

VMW

WDAY

WDC

ABT

ABC

ACT

ALXN

AMGN

BAX

BCR

BIIBBLL

CCK

CTSH

MCK

MWV

PRGO

TMO

UPS

WAT

AMZN

ACN

CRM

MSFT

JNJ

PFE

AMAT

ADP

BMC

JNPR

ADS

ADSK

AEE

PWR

DOW

AEP

KSU

FLS

AES

AET

AGCO

AGN

EXPE

ALB

UNP

ALTR

ALV

IBM

PX

INTU

AMP

IPG

CL

EL

GRMN

HAS

K

LVLT

MATNKE

NWL

PG

RHT

VFC

AN

F

GM

DELL

HPQ

AON

KBR

APA

OGE

BHI

APC

HRS

WGP

APD

ARG

ENR

IR

KMB

NSC

PEP

SLB

XOM

KLAC

AVP

IFF

CREE

EMC

GD

SYMC

VRSN

AXP

TRIP

VRSK

AZO

BA

BEAV

CA

COL

DCI

GE

LLL

NOC

PCP

PH

PLL

RS

RTN

ST

TDG

TXT

UTX

WPZ

CERN

HSP

DDR

BBBY

MHK

VAL

WHR

BBY

LINTA

MSI

S

SIRI

T

BDX

DHR

LYB

QGEN

RKT

BG

BMY

CELG

FRX

GILD

LIFE

LLY

MRK

MYL

REGN

VRTX

BSX

BTU

C

CAG

CAH

CAM

CAT

IEP

NUE

PLDROP

TRMB

TW

WAB

WAG

CBI

NLSN

CCE

CPB

DPS

KO

MDLZ

MNST

CCL

CE

EMN

CF

CFN

ACMP

CHK

ETE

ETP

NBR

PXP

CHKP

CHRW

CHTR

CI

N

JOY

CLF

CLR

CLX

CMCSA

DOX

CMI

CMS

CNA

CNH

SNA

CNP

CNX

COH

COST

BX

CHD

ECL

ESRX

GIS

HFC

HNZ

KRFT

MKC

SIG

SJM

TAP

TSN

VZ

XRX

COV

TYC

CPA

CTL

SNI

TWX

EPD

CVI

MMP

PAA

SXL

CVS

HRL

HSY

MJN

CVX

COP

CQP

DO

ESV

IHS

JEC

LNG

MWE

QEP

RIG

TSO

D

DAL

DE

LEA

DG

SIAL

DISCA

DISH

LMT

DKS

UA

DLTR

DNR

DRC

RRC

VLO

DTE

DTV

DUK

TWC

BWP

DVN

HP

EBAY

EFX

EIX

PVH

EOG

WLL

PXD

XEC

ETR

EXC

DFS

MA

FAST

FCX

KMI

PNW

XEL

FDO

FDX

BPL

FE

FL

FMC

FTI

FTR

SBAC

NEE

GPC

GPS

GGP

GRA

GWW

XYL

HD

HES

CXO

HOG

VHI

HOLX

IT

WIN

HRB

HSIC

HTZ

HUM

OC

IDXXILMN

INGR

LBTYA

IRMISRG

JBHT

JCP

FOSL

RL

JPM

KMP

KSS

L

LEN

LKQ

VAR

LNKD

LOW

LUK

MAS

MOS

PNR

LTD

LULU

LUV

M

KORS

URBN

MDT

MLM

MO

MON

ARE

MPC

PM

GAS

DLR

VMED

YHOO

MSM

MTD

MUR

HAL

NBL

NE

NEM

NFG

NFLX

NI

NOV

NRG

NU

NVE

OCN

OII

OKS

OMC

ORLY

OXY

PAYX

SPLS

TKR

TRW

PETM

ONXX

PII

PPL

RAI

RJF

RMD

ROK

RSG

AMT

SBH

SCG

SHLD

SO

SRE

STZ

SYK

SYY

CCI

FNF

TGT

TJX

TOL

TSCO

URI

UALULTA

VMC

WFM

WLK

WLP

WM

WMT

BEAM

WRB

WSM

WU

KR

EPB

Y

ZMH

SCCO

WMBSE

ED

SWNSTJEW

EQT

OKE

WFT

EEP TIF

CPNSRCL

BMRNXRAY

LNT

POM

ADI

A

ANSS

FLEX

JBL

NTAP

SNPS

XLNX

CSC

AA

CSX

FLR

ORCL

PPG

ASH

AAP

BWA

DLPH

FBHS

HON

ITW

JCI

MMM

PCAR

SHWAAPL

ADBE

AKAM

APH

ATVI

AVGO

AVT

BRCM

CBS

CSCO

CTXS

DD

DOV

EA

EMR

EQIX

FB

FFIV

FISV

GLW

GOOG

INTC

IP

LLTC

MCHP

MOLX

MRVL

MU

MXIM

NUAN

NVDA

NXPI

QCOM

RAX

SNDK

STX

SWK

SWKS

TDC

TEL

TXN

VIAB

VMW

WDAY

WDC

ABT

ABC

ACT

ALXN

AMGN

BAX

BCR

BIIBBLL

CCK

CTSH

MCK

MWV

PRGO

TMO

UPS

WAT

AMZN

ACN

CRM

MSFT

JNJ

PFE

AMAT

ADP

BMC

JNPR

ADS

ADSK

AEE

PWR

DOW

AEP

KSU

FLS

AES

AET

AGCO

AGN

EXPE

ALB

UNP

ALTR

ALV

IBM

PX

INTU

AMP

IPG

CL

EL

GRMN

HAS

K

LVLT

MATNKE

NWL

PG

RHT

VFC

AN

F

GM

DELL

HPQ

AON

KBR

APA

OGE

BHI

APC

HRS

WGP

APD

ARG

ENR

IR

KMB

NSC

PEP

SLB

XOM

KLAC

AVP

IFF

CREE

EMC

GD

SYMC

VRSN

AXP

TRIP

VRSK

AZO

BA

BEAV

CA

COL

DCI

GE

LLL

NOC

PCP

PH

PLL

RS

RTN

ST

TDG

TXT

UTX

WPZ

CERN

HSP

DDR

BBBY

MHK

VAL

WHR

BBY

LINTA

MSI

S

SIRI

T

BDX

DHR

LYB

QGEN

RKT

BG

BMY

CELG

FRX

GILD

LIFE

LLY

MRK

MYL

REGN

VRTX

BSX

BTU

C

CAG

CAH

CAM

CAT

IEP

NUE

PLDROP

TRMB

TW

WAB

WAG

CBI

NLSN

CCE

CPB

DPS

KO

MDLZ

MNST

CCL

CE

EMN

CF

CFN

ACMP

CHK

ETE

ETP

NBR

PXP

CHKP

CHRW

CHTR

CI

N

JOY

CLF

CLR

CLX

CMCSA

DOX

CMI

CMS

CNA

CNH

SNA

CNP

CNX

COH

COST

BX

CHD

ECL

ESRX

GIS

HFC

HNZ

KRFT

MKC

SIG

SJM

TAP

TSN

VZ

XRX

COV

TYC

CPA

CTL

SNI

TWX

EPD

CVI

MMP

PAA

SXL

CVS

HRL

HSY

MJN

CVX

COP

CQP

DO

ESV

IHS

JEC

LNG

MWE

QEP

RIG

TSO

D

DAL

DE

LEA

DG

SIAL

DISCA

DISH

LMT

DKS

UA

DLTR

DNR

DRC

RRC

VLO

DTE

DTV

DUK

TWC

BWP

DVN

HP

EBAY

EFX

EIX

PVH

EOG

WLL

PXD

XEC

ETR

EXC

DFS

MA

FAST

FCX

KMI

PNW

XEL

FDO

FDX

BPL

FE

FL

FMC

FTI

FTR

SBAC

NEE

GPC

GPS

GGP

GRA

GWW

XYL

HD

HES

CXO

HOG

VHI

HOLX

IT

WIN

HRB

HSIC

HTZ

HUM

OC

IDXXILMN

INGR

LBTYA

IRMISRG

JBHT

JCP

FOSL

RL

JPM

KMP

KSS

L

LEN

LKQ

VAR

LNKD

LOW

LUK

MAS

MOS

PNR

LTD

LULU

LUV

M

KORS

URBN

MDT

MLM

MO

MON

ARE

MPC

PM

GAS

DLR

VMED

YHOO

MSM

MTD

MUR

HAL

NBL

NE

NEM

NFG

NFLX

NI

NOV

NRG

NU

NVE

OCN

OII

OKS

OMC

ORLY

OXY

PAYX

SPLS

TKR

TRW

PETM

ONXX

PII

PPL

RAI

RJF

RMD

ROK

RSG

AMT

SBH

SCG

SHLD

SO

SRE

STZ

SYK

SYY

CCI

FNF

TGT

TJX

TOL

TSCO

URI

UALULTA

VMC

WFM

WLK

WLP

WM

WMT

BEAM

WRB

WSM

WU

KR

EPB

Y

ZMH

SCCO

WMBSE

ED

SWNSTJEW

EQT

OKE

WFT

EEP TIF

CPNSRCL

BMRNXRAY

LNT

POM

Figure: Who are my customers (left) and suppliers (right)

Green: Manufacturing, Blue: Transportation Warehousing, Red: Wholesale Retail

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 2 / 29

Outline

Empirical Observations: Propagation of risk on two levels (direct andindirect)

1st-order effects (direct propagation)

2nd-order effects (systematic risk)

Equilibrium Network Model

Implications of the Model

Conclusions and Future Directions

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 3 / 29

Empirical Observations

Pricing and Risk Basics

Model of share price at time t:

pt =∞∑s=0

e−(rs+δs )sds

Expected dividends ds

Depends on supply chain partners (first-order).Changes may be delayed due to inattention or invisibility.

Risk premium, δs

Depends on multiplicity of connections to transmit risk (second-order).Reliability issues may create nonlinear effects on the risk of network position.

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 4 / 29

Literature

Literature

1st-order effects

Industry level: Menzly & Ozbas (2007), Shahrur, Becker, & Rosenfeld (2010),Fruin, Osiol, & Wang (2012).

Firm level: Hendricks & Singhal (2003), Cohen & Frazzini (2008), Atalay,Hortacsu, & Syverson (2013, working).

2nd-order effects

Asset pricing: Sharpe (1964), Lintner (1965), Fama & French (1993).

Network risk: Acemoglu, Carvalho, Ozdaglar, & Tahbaz-Salehi (2012),Anupindi & Akella (1993), Cachon, Randall, & Schmidt (2007), Ahern (2012),Carvalho and Gabaix (2013), Kelly, Lustig, & Nieuwerburgh (2013, working),Herskovic (2014, working).

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 5 / 29

Data

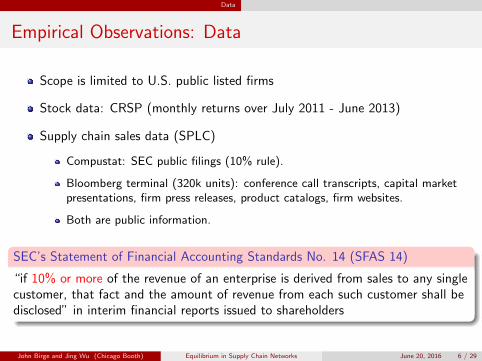

Empirical Observations: Data

Scope is limited to U.S. public listed firms

Stock data: CRSP (monthly returns over July 2011 - June 2013)

Supply chain sales data (SPLC)

Compustat: SEC public filings (10% rule).

Bloomberg terminal (320k units): conference call transcripts, capital marketpresentations, firm press releases, product catalogs, firm websites.

Both are public information.

SEC’s Statement of Financial Accounting Standards No. 14 (SFAS 14)

“if 10% or more of the revenue of an enterprise is derived from sales to any singlecustomer, that fact and the amount of revenue from each such customer shall bedisclosed” in interim financial reports issued to shareholders

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 6 / 29

Data First-order Effects

Example Relationship

Customer to SupplierCalloway Golf/Coastcast (Cohen and Frazzini (2008))

Calloway misses earning forecase by half ($0.36 from $0.70).

Calloway’s stock price drops 30%.

Coastcast share price (50% of sales to Calloway) unchanged for one month.

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 7 / 29

Data First-order Effects

Example Relationship

Supplier to Customer

Philips/Sony/Ericsson v. Nokia

Fire in Philips plant, key chip supplier for Nokia and Ericsson, in March 2000.

Philips states 1-week shutdown, then revises to 6 weeks.

Nokia (multi-sourcing) reacts quickly.

Ericsson (single sourcing) reacts slowly, lost $2.34B, acquired by Sony.

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 8 / 29

Data First-order Effects

First-order Effects

w inij denotes the supplier weight of j as a fraction of i ’s procurement.

woutij denotes the customer weight of j as a fraction of i ’s sales.

w inij =

salesjiProcurement i

=salesji∑Nk=1 saleski

,woutij =

salesijSales i

=salesij∑Nk=1 salesik

.

ri,t is the return of firm i in month t.

The following specification is tested:

ri,t = α + β1ri,t−1 + β2

∑j

w inij rj,t−1 + β3

∑j

woutij rj,t−1

+β4

∑j

w inij rj,t + β5

∑j

woutij rj,t + εi,t (1)

Hypothesis:

Suppliers’ and customers’ concurrent performance relates to the firm.Supplier momentum (one-month lag) may be related to firm performance(following Cohen and Frazzini (2008)).

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 9 / 29

Data First-order Effects

First-order Effects

Results

Table: Fama-Macbeth Regression of Concurrent Returns and Momentum.

α ri,t−1∑

j winij rj,t−1

∑j w

outij rj,t−1

∑j w

inij rj,t

∑j w

outij rj,t

Ave. Coef -0.001 -0.088*** 0.036** 0.024 0.399*** 0.755***(T-Stat) (-0.96) (-11.06) (2.17) (0.95) (20.90) (3.12)

Ave. Coef 0.009*** -0.090*** 0.057*** 0.004(T-Stat) (10.38) (-9.08) (2.96) (0.09)

Ave. Coef 0.009*** -0.047***(T-Stat) (10.53) (-6.96)

Ave. Coef 0.008*** 0.022**(T-Stat) (11.09) (1.83)

Ave. Coef 0.008*** -0.040(T-Stat) (10.92) (-0.66)

Ave. Coef 0.003*** 0.619***(T-Stat) (3.61) (37.25)

Ave. Coef -0.002** 0.992***(T-Stat) (-2.26) (4.54)

Ave. Coef 0.004*** 0.018* 0.625***(T-Stat) (4.51) (1.57) (36.44)

Ave. Coef -0.002* 0.001 1.001***(T-Stat) (-1.92) (0.0274) (4.51)

Ave. Coef -0.001* 0.393*** 0.744***(T-Stat) (-1.80) (22.48) (3.20)

*p-value<10%, **p-value<5%, ***p-value<1%

Controls: MKT, SMB, HML, MOM, cross-firm effect, industry effect.

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 10 / 29

Data Second-order Effects

Second-order Effects

Assumption

Acemoglu, Carvalho, Ozdaglar, & Tahbaz-Salehi (2012) (and the extension later)finds that microeconomic idiosyncratic shocks lead to aggregate flucturations,which meansA firm’s systematic risk is formed from the aggregation of idiosyncratic shocks.

Effects of connections may be nonlinear due to interactions - riskdiversification or aggregation?

Firm level shocks may be exogenously correlated due to geographicalproximity and sector proximity.

A manufacturer (e.g., Nokia) may have diversification incentives to add anindependent supplier to increase reliability (reduce systematic risk exposurewith greater centrality).A distributor (e.g., a beverage distributor) may have concentration incentivesto add similar suppliers (e.g., French wineries) to build on existing capabilities(increase systematic risk exposure with greater centrality).

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 11 / 29

Data Second-order Effects

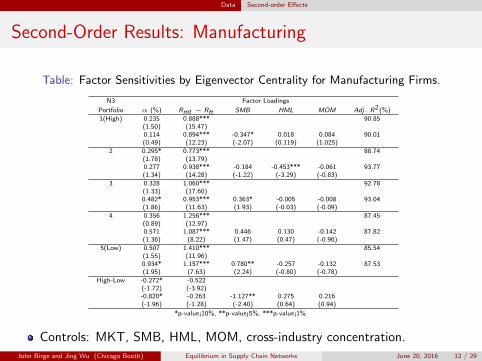

Second-Order Results: Manufacturing

Table: Factor Sensitivities by Eigenvector Centrality for Manufacturing Firms.

N3 Factor Loadings

Portfolio α (%) Rmt − Rft SMB HML MOM Adj. R2(%)

1(High) 0.235 0.888*** 90.85(1.50) (15.47)0.114 0.894*** -0.347* 0.018 0.084 90.01(0.49) (12.23) (-2.07) (0.119) (1.025)

2 0.295* 0.773*** 88.74(1.78) (13.79)0.277 0.938*** -0.184 -0.453*** -0.061 93.77(1.34) (14.28) (-1.22) (-3.29) (-0.83)

3 0.328 1.060*** 92.78(1.33) (17.60)0.482* 0.953*** 0.363* -0.005 -0.008 93.04(1.86) (11.63) (1.93) (-0.03) (-0.09)

4 0.356 1.256*** 87.45(0.89) (12.97)0.571 1.087*** 0.446 0.130 -0.142 87.82(1.36) (8.22) (1.47) (0.47) (-0.96)

5(Low) 0.507 1.410*** 85.54(1.55) (11.96)0.934* 1.157*** 0.780** -0.257 -0.132 87.53(1.95) (7.63) (2.24) (-0.80) (-0.78)

High-Low -0.272* -0.522(-1.72) (-3.92)-0.820* -0.263 -1.127** 0.275 0.216(-1.96) (-1.28) (-2.40) (0.64) (0.94)

*p-value¡10%, **p-value¡5%, ***p-value¡1%

Controls: MKT, SMB, HML, MOM, cross-industry concentration.

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 12 / 29

Data Second-order Effects

Second-Order Results: Logistics

Table: Factor Sensitivities by Eigenvector Centrality Centrality for Logistics Firms.

N4 Factor Loadings

Portfolio Alpha(%) Rmt − Rft SMB HML MOM Adj. R2(%)

1(High) 1.314*** 0.747*** 84.93(3.26) (7.62)

1.428*** 0.768*** 0.006 -0.589 0.024 86.43(3.44) (5.85) (0.02) (-2.14) (-0.16)

2 0.894*** 0.671*** 70.41(3.78) (11.67)

0.916*** 0.976*** 0.034 -0.502 0.031 72.32(2.41) (8.13) (0.13) (-1.99) (0.23)

3 0.812** 0.964*** 83.05(2.23) (10.89)

0.801** 0.758*** -0.140 -0.152 0.164 83.75(3.36) (10.03) (-0.81) (-0.96) (1.93)

4 0.708** 0.857*** 86.41(2.50) (12.40)

0.669** 0.916*** -0.171 -0.190 0.019 85.49(2.14) (9.26) (-0.75) (-0.92) (0.17)

5(Low) 0.759 0.776*** 69.60(1.44) (6.03)0.485 0.942*** -0.548 0.141 0.048 67.70(0.84) (5.17) (-1.31) (0.37) (0.23)

High-Low 0.556 -0.029(1.53) (-0.20)0.975* -0.175 0.553 -0.730 -0.024(1.93) (-0.90) (1.24) (-1.69) (-0.11)

*p-value¡10%, **p-value¡5%, ***p-value¡1%

Controls: MKT, SMB, HML, MOM, cross-industry concentration.

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 13 / 29

Data Second-order Effects

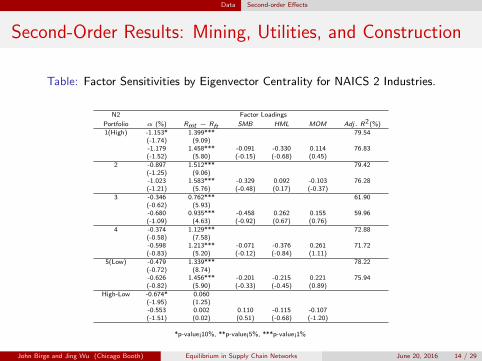

Second-Order Results: Mining, Utilities, and Construction

Table: Factor Sensitivities by Eigenvector Centrality for NAICS 2 Industries.

N2 Factor Loadings

Portfolio α (%) Rmt − Rft SMB HML MOM Adj. R2(%)

1(High) -1.153* 1.399*** 79.54(-1.74) (9.09)-1.179 1.458*** -0.091 -0.330 0.114 76.83(-1.52) (5.80) (-0.15) (-0.68) (0.45)

2 -0.897 1.512*** 79.42(-1.25) (9.06)-1.023 1.583*** -0.329 0.092 -0.103 76.28(-1.21) (5.76) (-0.48) (0.17) (-0.37)

3 -0.346 0.762*** 61.90(-0.62) (5.93)-0.680 0.935*** -0.458 0.262 0.155 59.96(-1.09) (4.63) (-0.92) (0.67) (0.76)

4 -0.374 1.129*** 72.88(-0.58) (7.58)-0.598 1.213*** -0.071 -0.376 0.261 71.72(-0.83) (5.20) (-0.12) (-0.84) (1.11)

5(Low) -0.479 1.339*** 78.22(-0.72) (8.74)-0.626 1.456*** -0.201 -0.215 0.221 75.94(-0.82) (5.90) (-0.33) (-0.45) (0.89)

High-Low -0.674* 0.060(-1.95) (1.25)-0.553 0.002 0.110 -0.115 -0.107(-1.51) (0.02) (0.51) (-0.68) (-1.20)

*p-value¡10%, **p-value¡5%, ***p-value¡1%

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 14 / 29

Data Second-order Effects

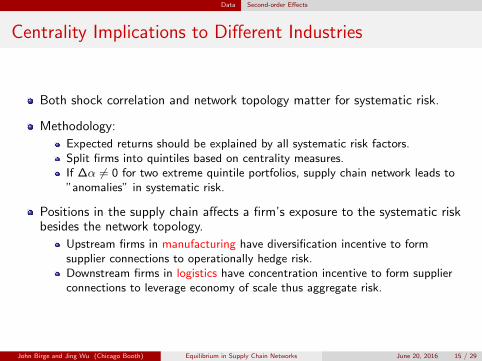

Centrality Implications to Different Industries

Both shock correlation and network topology matter for systematic risk.

Methodology:

Expected returns should be explained by all systematic risk factors.Split firms into quintiles based on centrality measures.If ∆α 6= 0 for two extreme quintile portfolios, supply chain network leads to”anomalies” in systematic risk.

Positions in the supply chain affects a firm’s exposure to the systematic riskbesides the network topology.

Upstream firms in manufacturing have diversification incentive to formsupplier connections to operationally hedge risk.Downstream firms in logistics have concentration incentive to form supplierconnections to leverage economy of scale thus aggregate risk.

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 15 / 29

Equilibrium Network Model

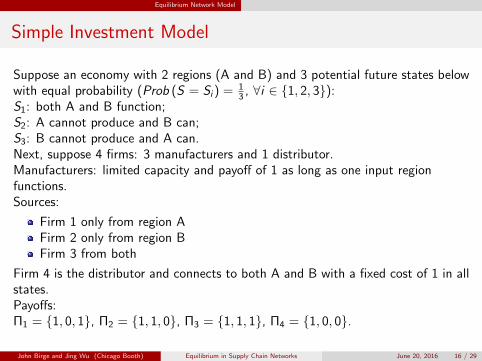

Simple Investment Model

Suppose an economy with 2 regions (A and B) and 3 potential future states belowwith equal probability (Prob (S = Si ) = 1

3 , ∀i ∈ 1, 2, 3):S1: both A and B function;S2: A cannot produce and B can;S3: B cannot produce and A can.Next, suppose 4 firms: 3 manufacturers and 1 distributor.Manufacturers: limited capacity and payoff of 1 as long as one input regionfunctions.Sources:

Firm 1 only from region AFirm 2 only from region BFirm 3 from both

Firm 4 is the distributor and connects to both A and B with a fixed cost of 1 in allstates.Payoffs:Π1 = 1, 0, 1, Π2 = 1, 1, 0, Π3 = 1, 1, 1, Π4 = 1, 0, 0.

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 16 / 29

Equilibrium Network Model

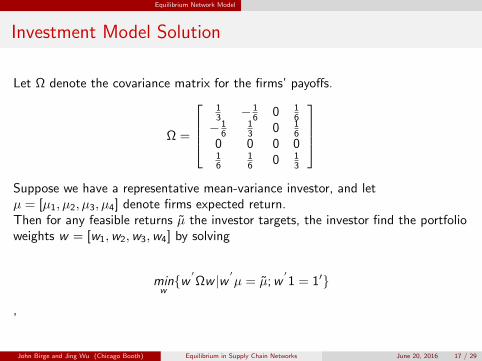

Investment Model Solution

Let Ω denote the covariance matrix for the firms’ payoffs.

Ω =

13 − 1

6 0 16

− 16

13 0 1

60 0 0 016

16 0 1

3

Suppose we have a representative mean-variance investor, and letµ = [µ1, µ2, µ3, µ4] denote firms expected return.Then for any feasible returns µ the investor targets, the investor find the portfolioweights w = [w1,w2,w3,w4] by solving

minww′Ωw |w

′µ = µ;w

′1 = 1′

,

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 17 / 29

Equilibrium Network Model

Simple Investment Results

The result of the equilibrium of investment is:µ1

µ2

µ3

µ4

=1

λ1

16w1 + 1

6w416w1 + 1

6w4

013w1 + 1

3w4

+λ2

λ1

Therefore,µ3 < µ1 = µ2 < µ4

i.e. the manufacturers have lower risk than the distributor, and the dual sourcingmanufacturer is less risky than the single sourcing manufacturer.Questions:

Does this result generalize to a broader classs of networks and what are otherempirical implications?Are the output representations consistent with an equilibrium model ofproduction?

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 18 / 29

Equilibrium Network Model

Equilibrium Network Model and Relationship to Literature

Previous literature focus on the sector level only.

Lucas (1977) argues that microeconomic shocks would average out at theaggregated level proportional to 1√

n.

Acemoglu et al. (2012) suggests Lucas (1977) only holds under symmetricnetwork structure, and microeconomic shocks may lead to aggregatedfluctuations in asymmetric networks.

The change in the density of firm level connections is not captured.

We build a supply chain network model using two-level nested productionfunction capturing both the firm-level and sector-level connections.

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 19 / 29

Equilibrium Network Model

Model Setup

An extension of Acemoglu et al. 2012

n industry sectors (S1, S2, ..., and Sn).

Firms in the same sector have the same Cobb-Douglas CRS productionfunction to produce perfectly substitutable products.

Supply chain relationships are established ex-ante.

xklij : output from firm l in sector j that inputs to firm k in sector i .

xi =∑

k∈Sixki : output from firm k in sector i .

xij =∑

k∈Si

∑l∈Sj

xklij : the production from sector j to sector i .

xi =∑

k∈Sixki : sector i ’s total production.

A unit labor allocating to to each firm (lki ) in each sector (li ), i.e.li =

∑k∈Si

lki and∑n

i=1 li = 1.

Consumption from by firm k in sector i is cki , and ci =∑

k∈Sicki .

Total consumption / GDP / labor wage is h.

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 20 / 29

Equilibrium Network Model

Competitive Equilibrium

A competitive equilibrium of economy

We define a competitive equilibrium of economy with n sectors consisting of prices(pi , i ∈ 1, ..., n), wage h, consumption bundle

(ci =

∑k∈Si

cki ,∀i , k ∈ Si), and

quantities(lki , x

ki , x

klij ,∀i , j , k, l

)such that

1 the representative consumer maximizes her utility;2 the firms in each sector maximizes their profits (0 in expectation);3 the labor and good markets clear at both levels, i.e. for any firm k in any

sector i , and for any sector i ,

xki = cki +n∑

j=1

∑l∈Sj

x lkji ,∑k∈Si

lki = li

xi = ci +n∑

j=1

xji ,n∑

i=1

li = 1

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 21 / 29

Equilibrium Network Model

Household and Firm Problems

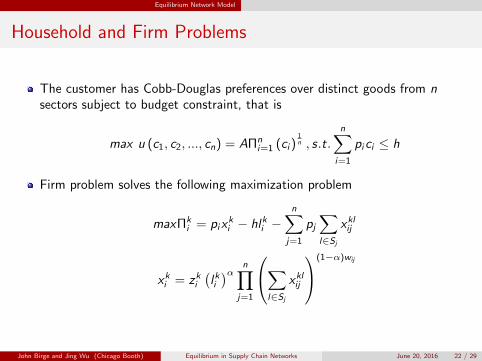

The customer has Cobb-Douglas preferences over distinct goods from nsectors subject to budget constraint, that is

max u (c1, c2, ..., cn) = AΠni=1 (ci )

1n , s.t.

n∑i=1

pici ≤ h

Firm problem solves the following maximization problem

maxΠki = pix

ki − hlki −

n∑j=1

pj∑l∈Sj

xklij

xki = zki(lki)α n∏

j=1

∑l∈Sj

xklij

(1−α)wij

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 22 / 29

Equilibrium Network Model

From Firm Connections to Sector Connections

Since firms face the same input prices and own the same productiontechnology, they will choose the same proportions of inputs:∑

l∈Sj

xklij = γki xij , lki = γki li

where γki =

∑l∈Sj

xklij

xij=

lkili

is the firm’s sector share.

Firm-level networks determine the shape of the sector shock distribution.

The Origin of Sector Shock

In sector i ’s output, i.e. xi = zi (li )α∏n

j=1 (xij)(1−α)wij , the sector productivity

shock is a sum of firm level shocks, weighted by each firm’s sector share.

zi =∑k∈Si

γki zki

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 23 / 29

Equilibrium Network Model

From Firm Connetions to Sector Connetions

Firm-level connections affect the sector shock through the distribution of thefirm’s sector share γki .

Define the influence vector as v′

= αn 1′

[I − (1− α)W ]−1 satisfyingvi = pixi∑n

i=1 pixithus

∑ni=1 vi = 1.

Supply Chain Network Systematic Risk

The aggregate output is a influence vector weighted sum of sector-specificproductivity shocks below.

y = lnh = v′ε

where ε is a column vector with εi = lnzi = ln(∑

k∈Sizki γ

ki

). The volatility of the

aggregate output (the systematic risk) is

Var [y ] = Var[v′ε]

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 24 / 29

Equilibrium Network Model

Sparse v.s. Dense Supply Chain Networks

Sector B

Sector A

Sector B

Sector A

The firm’s sector share γki in the left case would have higher variance on thedistribution than the right case.Similar to Proposition 4 in Acemoglu et al. (2015), the expected total output

E [y ] decreases when Var[v′ε]

increases, i.e.

1. Supply Chain Network and Sector Performance

For concave production functions, a sparse firm-level supply chain network resultsin less total sector output than a dense network.

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 25 / 29

Equilibrium Network Model

Simulation

Step 1 (Relationship-formation): Each firm chooses a set of suppliers.Ex-ante the market is perfectly competitive.Step 2 (Input-acquisition): Each firm draws i.i.d. production shock. Inputquantity depends on the supplier actual production.The dense network has a low sector weight variance (std 0.0001 v.s. 0.0023).

2. Supply Chain Network and Firm Volatility

A sparse network results in more volatile firm production than a dense network.

8.8 9 9.2 9.4 9.6 9.8 10 10.2 10.4 10.6

x 10−3

0

200

400

600

800

1000

1200

0 0.005 0.01 0.015 0.02 0.025 0.03 0.0350

200

400

600

800

1000

1200

1400

Figure: Sector Weight γki Distribution (Left: 80% of Suppliers, Right: 2% of Suppliers).

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 26 / 29

Equilibrium Network Model

Simulation (cont.)

Both cases exhibit sizable and systematic deviations from the normaldistribution (2%: heavy left tail, 80%: heavy right tail).Only the sector weight with modest connection density is normal distributed.

Sufficient Statistics for Firm Production Variation

With firm-level supply chain connection variation, there is no guarantee that thefirm-level production is normally distributed.

−4 −3 −2 −1 0 1 2 3 49

9.2

9.4

9.6

9.8

10

10.2

10.4

10.6

10.8x 10−3

Standard Normal Quantiles

Qua

ntile

s of

Inpu

t Sam

ple

QQ Plot of Sample Data versus Standard Normal

−4 −3 −2 −1 0 1 2 3 40

0.005

0.01

0.015

0.02

0.025

Standard Normal Quantiles

Qua

ntile

s of

Inpu

t Sam

ple

QQ Plot of Sample Data versus Standard Normal

Figure: Q-Q Plot of the Sector Weight γki Distribution (Left: 80% of Suppliers, Right:

2% of Suppliers).John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 27 / 29

Equilibrium Network Model

More Concentrated Economic Activities during Crisis.

Core: most (eigenvector) central firms; Periphery: least central firms.Force-directed layout algorithm (Fruchterman and Reingold 1991).Left: network in July 2007; Right: network in June 2009.Economic activities for June 2009 supply chain network are moreconcentrated than July 2007.

Figure: Network in July 2007

Figure: Network in June 2009

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 28 / 29

Conclusions & Future Directions

Conclusions and Future Directions

Evidence of concurrent supplier and customer effects plus suppliermomentum effects on returns.

Investors’ limited attention to supplier firms relative to customer firms.Gradual diffusion of supply chain information downstream as opposed toupstream.

Evidence of decreasing returns to centrality in manufacturing and increasingreturns to centrality in logistics.

Supply chain structure is an ex-ante determined and ex-post identifiable sourcefor systematic risk.Upper-stream utility, mining, and construction firms behave similarly asmanufacturing.

Equilibrium model of firms connecting across sectors

Natural hedging decisions from manufacturersLower volatility effect for manufacturers implies conditions for increasingconections to cause lower risk for upstream and higher risk for downstream

Future DirectionsAdditional empirical tests (including default propagation)Incorporate of investment into the model formulation

John Birge and Jing Wu (Chicago Booth) Equilibrium in Supply Chain Networks June 20, 2016 29 / 29