a guide to going public executing a successful ipo in oslo · 2015-08-15 · executing a successful...

TRANSCRIPT

A guide to going public Executing a successful IPO in Oslo

www.pwc.no

Capital Markets and Accounting Advisory Services

Pre-IPO

IPO Post-IPO

Careful thought, preparation and planningare key to a successful IPO

2 A guide to going public

Executing a successful listing in Oslo 3

Content

1. The decision to go public 4

2. Preparing for a successful IPO 8

3. The process of going public 12

4. Listing in Oslo 17

5. Listing requirements of Oslo Børs and Oslo Axess 21

6. Life as a public company 25

PricewaterhouseCoopers AS (“PwC”) is the author of this publication and has got the copyrights. Without written permission of PwC this publication may not be duplicated, copied, distributed or published. This publication has been prepared for information purposes and general guidance on matters of interest only, and does not constitute, or may not be interpreted as professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PwC does not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

4 A guide to going public

1. The decision to go public

What does “going public” mean? It refers to the process of offering securities such as ordinary shares of a privately owned company for sale to the general public. The first time these securities are offered is referred to as an initial public offering, or an IPO. Through the IPO the company can raise new equity to finance its ambitions for growth, as well as allow the shares to be traded in a regulated market.

As IPO market momentum increases, many companies are assessing their readiness to go publicTaking your company public is a transformational event, probably one of the most important your company will go through. Done properly an IPO not only supports your company’s continued growth but it will likely have an impact on the lives and fortunes of everyone involved (owners, employees and investors).

Is going public right for your company?A company usually begins to think about going public when the funding required to meet the demands of its business begins to exceed the company’s ability to raise additional capital through other channels on attractive terms. But simply needing capital does not always mean that going public is the right answer. There are a number of questions that a company should ask itself before deciding to go public.

Executing a successful listing in Oslo 5

The following should be considered before making any decision to go public

Attractive track record? A company that outpaces the industry average in growth will have a better chance of attracting prospective investors than one with marginal or inconsistent growth. Here are some of the most important factors that investors look for in companies: • An attractive product or service, preferably one with a competitive advantage and

sufficientlylargemarket;• Anexperiencedmanagementteam;• Apositivetrendofhistoricalfinancialresults;• Favourablefinancialprospects;• Awellthought-out,focusedbusinessplan;• Strongfinancial,operational,andcompliancecontrols.

Though some companies may not meet all of these criteria, investors may nevertheless perceive these companies as having potential for growth, due to other favourable characteristics (e.g. capable and committed management, and a product or service that is highly visible, unique, or of interest to the public).

Is the company gearing for growth, or will it focus on dividends?

Some companies might not focus on price appreciation after listing but instead on paying out a dividend. How astockisclassifieddependsonseveralfactors,suchaswhereintheindustrylifecycleitis,whatthemacroconditions are, and what industry it belongs to.

Products or services visible and of interest to the investing public?

The established company can answer this question with historical sales data, while the early-stage company must use market research projections and demonstrate product superiority. An early-stage company may also qualify as an IPO candidate due to the uniqueness of its product or service.

Do investors perceive leadership as capable and committed?

It is vital to ensure that the board of directors and management have the right blend of experience and skills to establish a solid corporate governance structure, and ensure that the board committees are operating effectively. To lead a successful IPO, management must be committed to the time and effort involved in meetingofferingrequirements,conductinganalystandotherinvestor-facingmeetings,andprovidingfinancialreports to the shareholders on a timely basis.

Do the benefits outweigh the costs of going public?

For existing shareholders, selling equity generates proceeds today in exchange for giving up at least some degree of control of the company, and a portion of the future returns associated with corporate growth. Raising equity capital in the public markets can also entail substantial upfront costs, such as fees to the investment banks and other advisors’ fees and expenses. Ongoing costs arise from obligations including compliance with market requirements, maintaining a dedicated investor relations function, and more frequent and extensive financialreporting.Whetherthebenefitsoutweighthecostsmaybedifficulttojudgeuntilseveralyearsafteran IPO.

Are the market conditions right? The demand for IPOs can vary dramatically, depending on overall market strength, the market’s current opinion of IPOs, industry economic conditions, technological changes, and many other factors. Stock market volatility is one of the most unpredictable aspects of going public and it makes timing of the IPO a decisive factor in achieving the best possible result. Although it is impossible to accurately forecast the market sentiment, a company must consider the importance of timing and be well prepared to alter its timetable. At any point in time, an IPO window may be open for companies within certain favoured industries, and sometimes the window may be open for companies in all industries. Missing an IPO window by as little as a few weeks can result in a postponed or withdrawn IPO or a lower market valuation.

6 A guide to going public

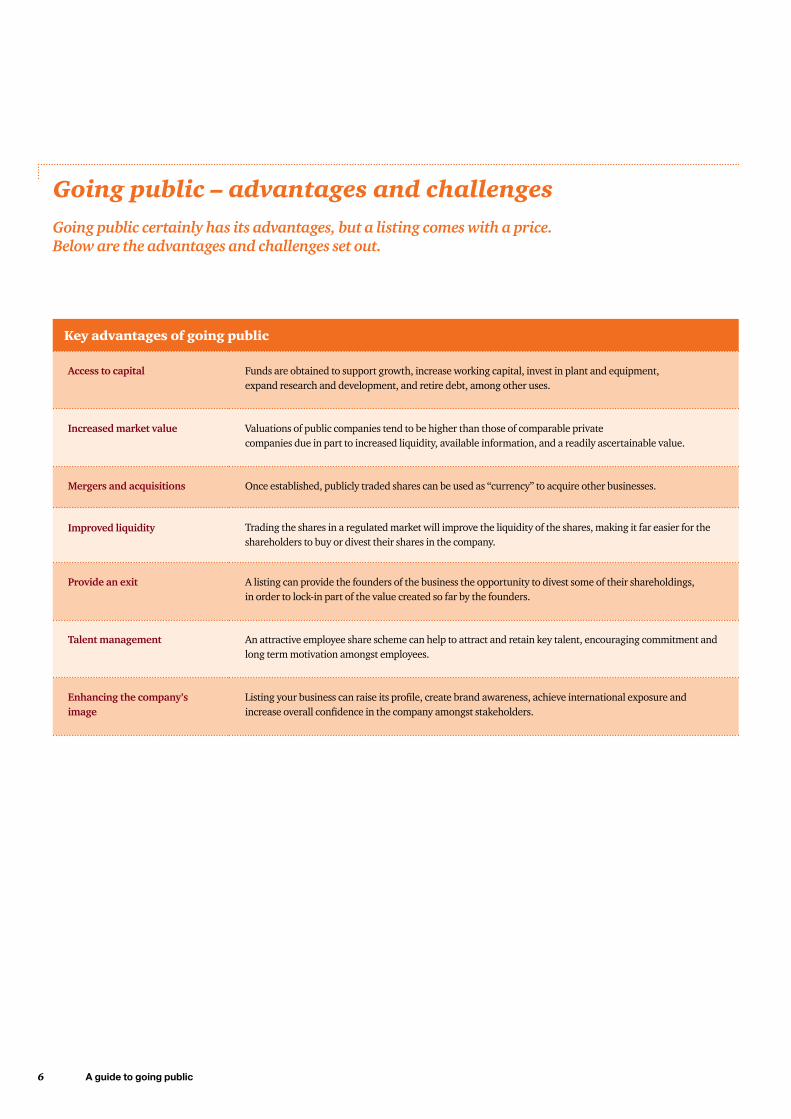

Going public – advantages and challenges Going public certainly has its advantages, but a listing comes with a price. Below are the advantages and challenges set out.

Key advantages of going public

Access to capital Funds are obtained to support growth, increase working capital, invest in plant and equipment, expand research and development, and retire debt, among other uses.

Increased market value Valuations of public companies tend to be higher than those of comparable privatecompanies due in part to increased liquidity, available information, and a readily ascertainable value.

Mergers and acquisitions Once established, publicly traded shares can be used as “currency” to acquire other businesses.

Improved liquidity Trading the shares in a regulated market will improve the liquidity of the shares, making it far easier for the shareholders to buy or divest their shares in the company.

Provide an exit A listing can provide the founders of the business the opportunity to divest some of their shareholdings, in order to lock-in part of the value created so far by the founders.

Talent management An attractive employee share scheme can help to attract and retain key talent, encouraging commitment and long term motivation amongst employees.

Enhancing the company’s image

Listingyourbusinesscanraiseitsprofile,createbrandawareness,achieveinternationalexposureandincreaseoverallconfidenceinthecompanyamongststakeholders.

Executing a successful listing in Oslo 7

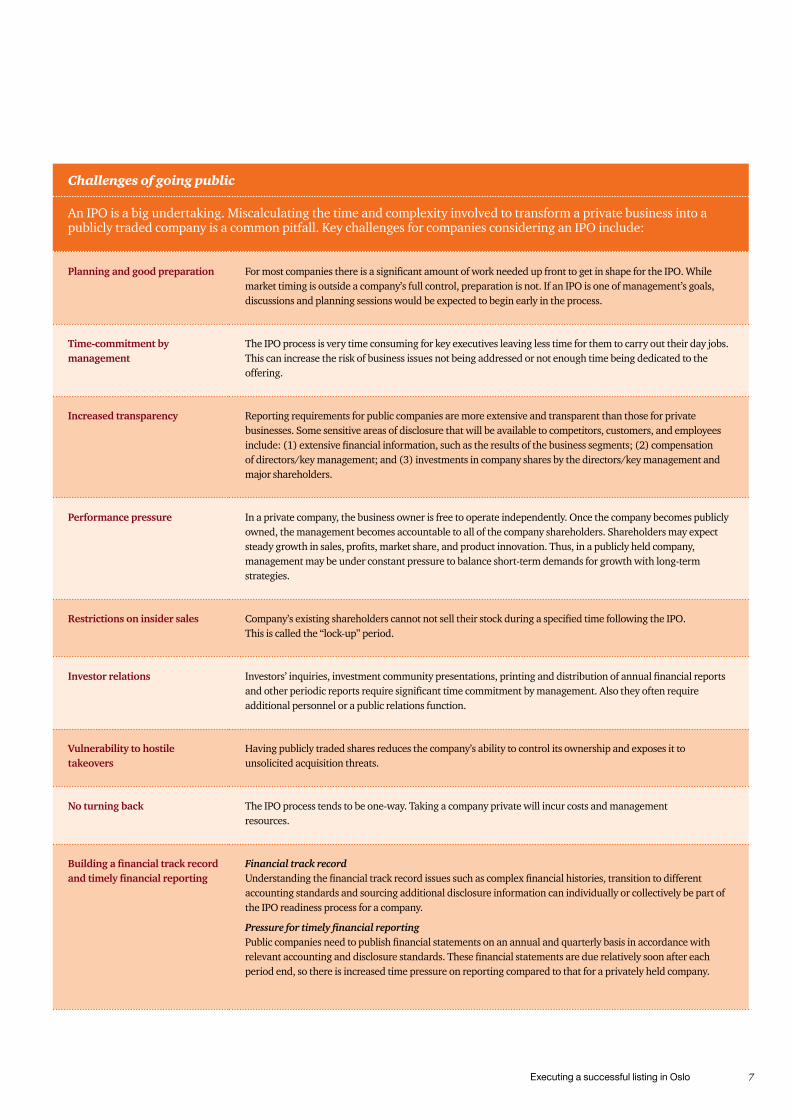

Challenges of going public

An IPO is a big undertaking. Miscalculating the time and complexity involved to transform a private business into a publicly traded company is a common pitfall. Key challenges for companies considering an IPO include:

Planning and good preparation FormostcompaniesthereisasignificantamountofworkneededupfronttogetinshapefortheIPO.Whilemarket timing is outside a company’s full control, preparation is not. If an IPO is one of management’s goals, discussions and planning sessions would be expected to begin early in the process.

Time-commitment by management

The IPO process is very time consuming for key executives leaving less time for them to carry out their day jobs. This can increase the risk of business issues not being addressed or not enough time being dedicated to the offering.

Increased transparency Reporting requirements for public companies are more extensive and transparent than those for private businesses. Some sensitive areas of disclosure that will be available to competitors, customers, and employees include:(1)extensivefinancialinformation,suchastheresultsofthebusinesssegments;(2)compensationofdirectors/keymanagement;and(3)investmentsincompanysharesbythedirectors/keymanagementandmajor shareholders.

Performance pressure In a private company, the business owner is free to operate independently. Once the company becomes publicly owned, the management becomes accountable to all of the company shareholders. Shareholders may expect steadygrowthinsales,profits,marketshare,andproductinnovation.Thus,inapubliclyheldcompany,management may be under constant pressure to balance short-term demands for growth with long-term strategies.

Restrictions on insider sales Company’sexistingshareholderscannotnotselltheirstockduringaspecifiedtimefollowingtheIPO. This is called the “lock-up” period.

Investor relations Investors’inquiries,investmentcommunitypresentations,printinganddistributionofannualfinancialreportsandotherperiodicreportsrequiresignificanttimecommitmentbymanagement.Alsotheyoftenrequireadditional personnel or a public relations function.

Vulnerability to hostile takeovers

Having publicly traded shares reduces the company’s ability to control its ownership and exposes it to unsolicited acquisition threats.

No turning back The IPO process tends to be one-way. Taking a company private will incur costs and management resources.

Building a financial track record and timely financial reporting

Financial track recordUnderstandingthefinancialtrackrecordissuessuchascomplexfinancialhistories,transitiontodifferentaccounting standards and sourcing additional disclosure information can individually or collectively be part of the IPO readiness process for a company.

Pressure for timely financial reportingPubliccompaniesneedtopublishfinancialstatementsonanannualandquarterlybasisinaccordancewithrelevantaccountinganddisclosurestandards.Thesefinancialstatementsareduerelativelysoonaftereachperiod end, so there is increased time pressure on reporting compared to that for a privately held company.

8 A guide to going public

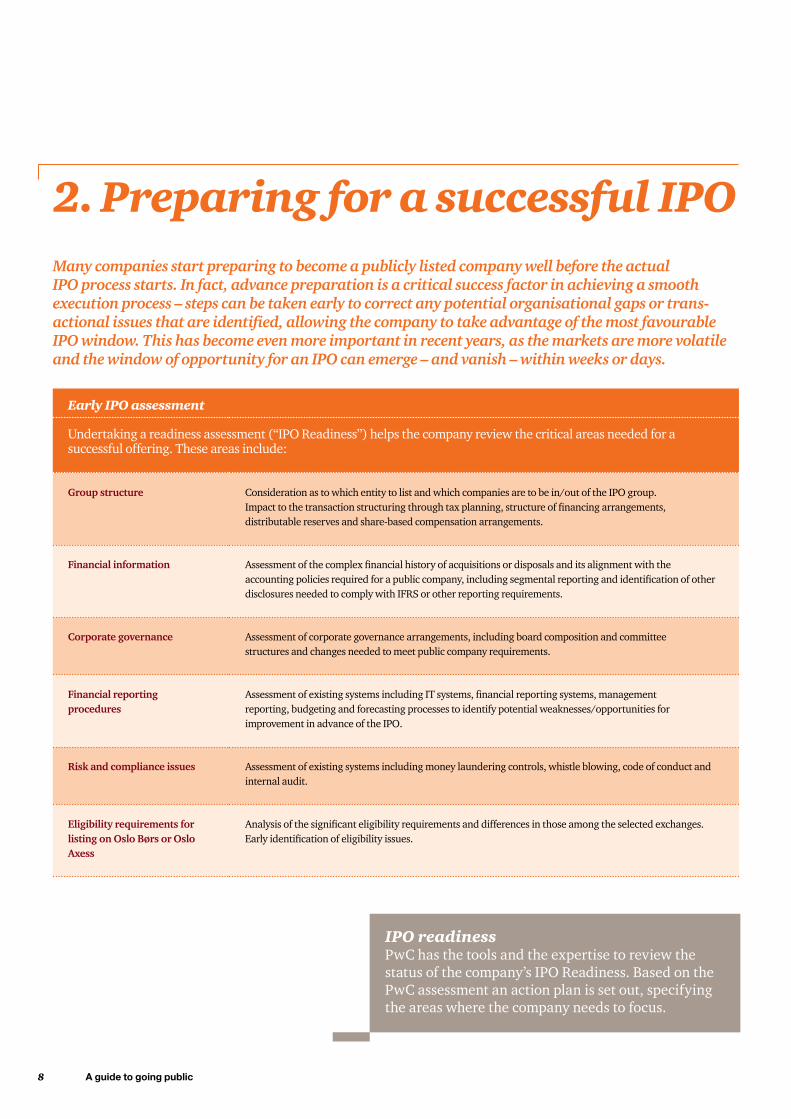

2. Preparing for a successful IPOMany companies start preparing to become a publicly listed company well before the actual IPO process starts. In fact, advance preparation is a critical success factor in achieving a smooth execution process – steps can be taken early to correct any potential organisational gaps or trans-actional issues that are identified, allowing the company to take advantage of the most favourable IPO window. This has become even more important in recent years, as the markets are more volatile and the window of opportunity for an IPO can emerge – and vanish – within weeks or days.

IPO readinessPwC has the tools and the expertise to review the status of the company’s IPO Readiness. Based on the PwC assessment an action plan is set out, specifying the areas where the company needs to focus.

Early IPO assessment

Undertaking a readiness assessment (“IPO Readiness”) helps the company review the critical areas needed for a successful offering. These areas include:

Group structure Consideration as to which entity to list and which companies are to be in/out of the IPO group. Impacttothetransactionstructuringthroughtaxplanning,structureoffinancingarrangements, distributable reserves and share-based compensation arrangements.

Financial information Assessmentofthecomplexfinancialhistoryofacquisitionsordisposalsanditsalignmentwiththeaccountingpoliciesrequiredforapubliccompany,includingsegmentalreportingandidentificationofother disclosures needed to comply with IFRS or other reporting requirements.

Corporate governance Assessment of corporate governance arrangements, including board composition and committee structures and changes needed to meet public company requirements.

Financial reportingprocedures

AssessmentofexistingsystemsincludingITsystems,financialreportingsystems,management reporting, budgeting and forecasting processes to identify potential weaknesses/opportunities for improvement in advance of the IPO.

Risk and compliance issues Assessment of existing systems including money laundering controls, whistle blowing, code of conduct and internal audit.

Eligibility requirements for listing on Oslo Børs or Oslo Axess

Analysisofthesignificanteligibilityrequirementsanddifferencesinthoseamongtheselectedexchanges. Earlyidentificationofeligibilityissues.

Executing a successful listing in Oslo 9

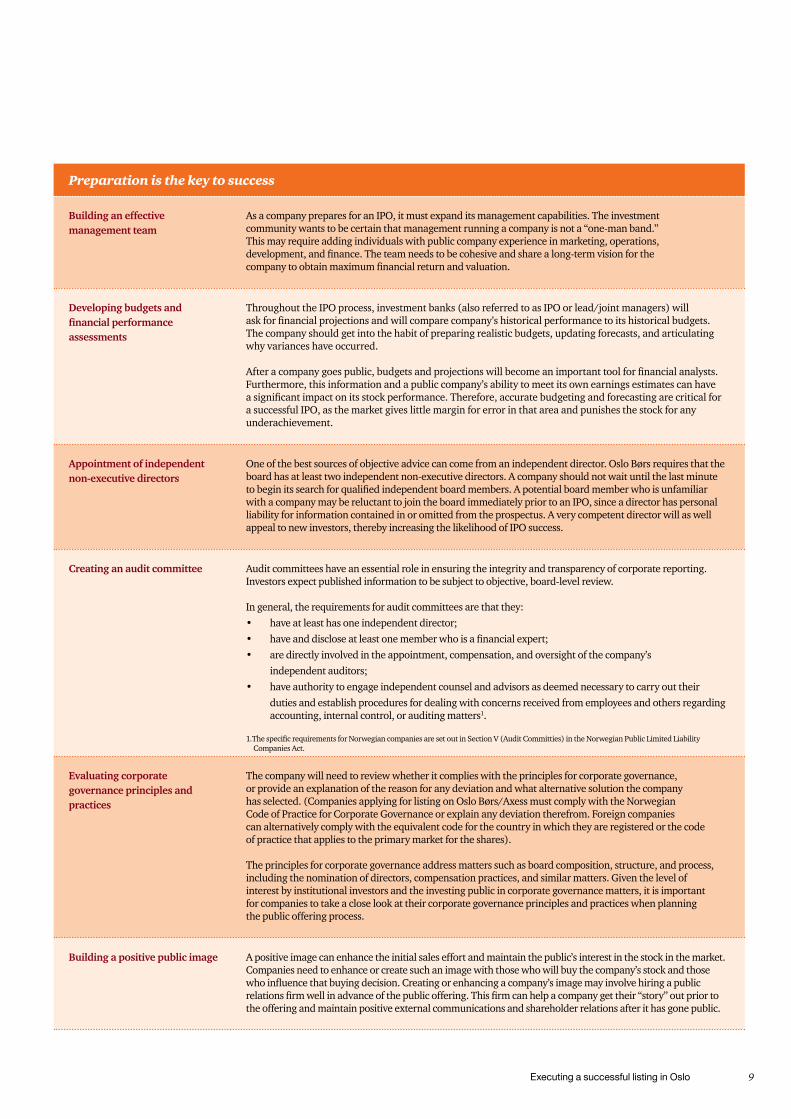

Preparation is the key to success

Building an effective management team

As a company prepares for an IPO, it must expand its management capabilities. The investment community wants to be certain that management running a company is not a “one-man band.” This may require adding individuals with public company experience in marketing, operations, development,andfinance.Theteamneedstobecohesiveandsharealong-termvisionforthe companytoobtainmaximumfinancialreturnandvaluation.

Developing budgets and financial performance assessments

Throughout the IPO process, investment banks (also referred to as IPO or lead/joint managers) will askforfinancialprojectionsandwillcomparecompany’shistoricalperformancetoitshistoricalbudgets. The company should get into the habit of preparing realistic budgets, updating forecasts, and articulating why variances have occurred.

Afteracompanygoespublic,budgetsandprojectionswillbecomeanimportanttoolforfinancialanalysts.Furthermore, this information and a public company’s ability to meet its own earnings estimates can have asignificantimpactonitsstockperformance.Therefore,accuratebudgetingandforecastingarecriticalfor a successful IPO, as the market gives little margin for error in that area and punishes the stock for any underachievement.

Appointment of independent non-executive directors

One of the best sources of objective advice can come from an independent director. Oslo Børs requires that the board has at least two independent non-executive directors. A company should not wait until the last minute tobeginitssearchforqualifiedindependentboardmembers.Apotentialboardmemberwhoisunfamiliarwith a company may be reluctant to join the board immediately prior to an IPO, since a director has personal liability for information contained in or omitted from the prospectus. A very competent director will as well appeal to new investors, thereby increasing the likelihood of IPO success.

Creating an audit committee Audit committees have an essential role in ensuring the integrity and transparency of corporate reporting. Investors expect published information to be subject to objective, board-level review.

In general, the requirements for audit committees are that they: • haveatleasthasoneindependentdirector;• haveanddiscloseatleastonememberwhoisafinancialexpert;• are directly involved in the appointment, compensation, and oversight of the company’s

independentauditors;• have authority to engage independent counsel and advisors as deemed necessary to carry out their

duties and establish procedures for dealing with concerns received from employees and others regarding accounting, internal control, or auditing matters1.

1.ThespecificrequirementsforNorwegiancompaniesaresetoutinSectionV(AuditCommitties)intheNorwegianPublicLimitedLiabilityCompanies Act.

Evaluating corporate governance principles and practices

The company will need to review whether it complies with the principles for corporate governance, or provide an explanation of the reason for any deviation and what alternative solution the company hasselected.(CompaniesapplyingforlistingonOsloBørs/AxessmustcomplywiththeNorwegian Code of Practice for Corporate Governance or explain any deviation therefrom. Foreign companies can alternatively comply with the equivalent code for the country in which they are registered or the code of practice that applies to the primary market for the shares).

The principles for corporate governance address matters such as board composition, structure, and process, including the nomination of directors, compensation practices, and similar matters. Given the level of interest by institutional investors and the investing public in corporate governance matters, it is important for companies to take a close look at their corporate governance principles and practices when planning the public offering process.

Building a positive public image A positive image can enhance the initial sales effort and maintain the public’s interest in the stock in the market. Companies need to enhance or create such an image with those who will buy the company’s stock and those whoinfluencethatbuyingdecision.Creatingorenhancingacompany’simagemayinvolvehiringapublic relationsfirmwellinadvanceofthepublicoffering.Thisfirmcanhelpacompanygettheir“story”outpriortothe offering and maintain positive external communications and shareholder relations after it has gone public.

10 A guide to going public

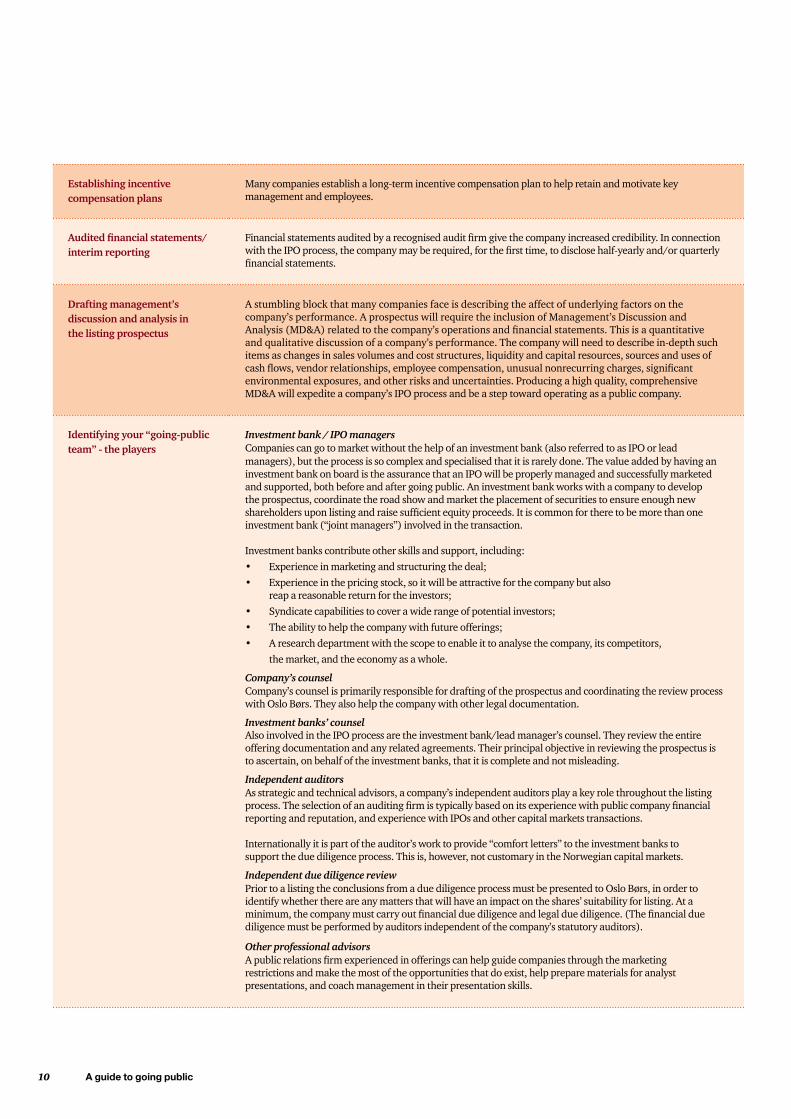

Establishing incentive compensation plans

Many companies establish a long-term incentive compensation plan to help retain and motivate key management and employees.

Audited financial statements/interim reporting

Financialstatementsauditedbyarecognisedauditfirmgivethecompanyincreasedcredibility.InconnectionwiththeIPOprocess,thecompanymayberequired,forthefirsttime,todisclosehalf-yearlyand/orquarterlyfinancialstatements.

Drafting management’s discussion and analysis in the listing prospectus

A stumbling block that many companies face is describing the affect of underlying factors on the company’s performance. A prospectus will require the inclusion of Management’s Discussion and Analysis(MD&A)relatedtothecompany’soperationsandfinancialstatements.Thisisaquantitative and qualitative discussion of a company’s performance. The company will need to describe in-depth such items as changes in sales volumes and cost structures, liquidity and capital resources, sources and uses of cashflows,vendorrelationships,employeecompensation,unusualnonrecurringcharges,significant environmental exposures, and other risks and uncertainties. Producing a high quality, comprehensive MD&A will expedite a company’s IPO process and be a step toward operating as a public company.

Identifying your “going-public team” - the players

Investment bank / IPO managersCompanies can go to market without the help of an investment bank (also referred to as IPO or lead managers), but the process is so complex and specialised that it is rarely done. The value added by having an investment bank on board is the assurance that an IPO will be properly managed and successfully marketed and supported, both before and after going public. An investment bank works with a company to develop the prospectus, coordinate the road show and market the placement of securities to ensure enough new shareholdersuponlistingandraisesufficientequityproceeds.Itiscommonfortheretobemorethanoneinvestment bank (“joint managers”) involved in the transaction.

Investment banks contribute other skills and support, including: • Experienceinmarketingandstructuringthedeal;• Experience in the pricing stock, so it will be attractive for the company but also

reapareasonablereturnfortheinvestors;• Syndicatecapabilitiestocoverawiderangeofpotentialinvestors;• Theabilitytohelpthecompanywithfutureofferings;• A research department with the scope to enable it to analyse the company, its competitors,

the market, and the economy as a whole.

Company’s counsel Company’s counsel is primarily responsible for drafting of the prospectus and coordinating the review process with Oslo Børs. They also help the company with other legal documentation.

Investment banks’ counsel Also involved in the IPO process are the investment bank/lead manager’s counsel. They review the entire offering documentation and any related agreements. Their principal objective in reviewing the prospectus is to ascertain, on behalf of the investment banks, that it is complete and not misleading.

Independent auditors As strategic and technical advisors, a company’s independent auditors play a key role throughout the listing process.Theselectionofanauditingfirmistypicallybasedonitsexperiencewithpubliccompanyfinancialreporting and reputation, and experience with IPOs and other capital markets transactions.

Internationally it is part of the auditor’s work to provide “comfort letters” to the investment banks to supporttheduediligenceprocess.Thisis,however,notcustomaryintheNorwegiancapitalmarkets.

Independent due diligence reviewPrior to a listing the conclusions from a due diligence process must be presented to Oslo Børs, in order to identify whether there are any matters that will have an impact on the shares’ suitability for listing. At a minimum,thecompanymustcarryoutfinancialduediligenceandlegalduediligence.(Thefinancialduediligence must be performed by auditors independent of the company’s statutory auditors).

Other professional advisors Apublicrelationsfirmexperiencedinofferingscanhelpguidecompaniesthroughthemarketing restrictions and make the most of the opportunities that do exist, help prepare materials for analyst presentations, and coach management in their presentation skills.

Executing a successful listing in Oslo 11

“Home state” versus “host state”A company applying for listing on Oslo Børs needs to determinewhetherNorway–oranyothercountryintheEuropean Union/European Economic Area (EU and EEA respectively)–isits“homememberstate”.Thisisbecausethefinancialperiodicreportingrequirementsforlistedcompanies differ for all the EU/EEA member states and the company needs to follow the period reporting requirements in its “home member state”. All companies listed on the Oslo StockExchangemusthaveahomestateeitherinNorwayorin any of the other member states in the EU/EEA. Asageneralrule,Norwayisthehome state for (i) Norwegiancompaniesand(ii)companiesfromoutsidetheEEA that are/will be listed on the Oslo Stock Exchange (so-calledthirdcountryissuers).CompanieswithNorwayastheirhomememberstatewillhavetofollowNorwegianperiodic reporting requirements.

Furthermore,asageneralruleNorwaywillbethe host state forEEA-companies(non-Norwegian)applyingforlistingonOslo Børs. For these companies the reporting requirements in their European home state will take precedence, and Norwegianrequirementsforperiodicfinancialreportingwillgenerally not apply.

ForcompanieswithNorwayasthehomestate,theFinancialSupervisoryAuthorityofNorwaywillhandleandapprovethe listing prospectus. WhetheralistedcompanyhasNorwayasahostorhomestatehasimplicationsfortake-overrules,notificationsoflargeshareholdings as well. A list of companies and their home states is set out on the Oslo Børs’ website.

Establishing incentive compensation plans

Many companies establish a long-term incentive compensation plan to help retain and motivate key management and employees.

Audited financial statements/interim reporting

Financialstatementsauditedbyarecognisedauditfirmgivethecompanyincreasedcredibility.InconnectionwiththeIPOprocess,thecompanymayberequired,forthefirsttime,todisclosehalf-yearlyand/orquarterlyfinancialstatements.

Drafting management’s discussion and analysis in the listing prospectus

A stumbling block that many companies face is describing the affect of underlying factors on the company’s performance. A prospectus will require the inclusion of Management’s Discussion and Analysis(MD&A)relatedtothecompany’soperationsandfinancialstatements.Thisisaquantitative and qualitative discussion of a company’s performance. The company will need to describe in-depth such items as changes in sales volumes and cost structures, liquidity and capital resources, sources and uses of cashflows,vendorrelationships,employeecompensation,unusualnonrecurringcharges,significant environmental exposures, and other risks and uncertainties. Producing a high quality, comprehensive MD&A will expedite a company’s IPO process and be a step toward operating as a public company.

Identifying your “going-public team” - the players

Investment bank / IPO managersCompanies can go to market without the help of an investment bank (also referred to as IPO or lead managers), but the process is so complex and specialised that it is rarely done. The value added by having an investment bank on board is the assurance that an IPO will be properly managed and successfully marketed and supported, both before and after going public. An investment bank works with a company to develop the prospectus, coordinate the road show and market the placement of securities to ensure enough new shareholdersuponlistingandraisesufficientequityproceeds.Itiscommonfortheretobemorethanoneinvestment bank (“joint managers”) involved in the transaction.

Investment banks contribute other skills and support, including: • Experienceinmarketingandstructuringthedeal;• Experience in the pricing stock, so it will be attractive for the company but also

reapareasonablereturnfortheinvestors;• Syndicatecapabilitiestocoverawiderangeofpotentialinvestors;• Theabilitytohelpthecompanywithfutureofferings;• A research department with the scope to enable it to analyse the company, its competitors,

the market, and the economy as a whole.

Company’s counsel Company’s counsel is primarily responsible for drafting of the prospectus and coordinating the review process with Oslo Børs. They also help the company with other legal documentation.

Investment banks’ counsel Also involved in the IPO process are the investment bank/lead manager’s counsel. They review the entire offering documentation and any related agreements. Their principal objective in reviewing the prospectus is to ascertain, on behalf of the investment banks, that it is complete and not misleading.

Independent auditors As strategic and technical advisors, a company’s independent auditors play a key role throughout the listing process.Theselectionofanauditingfirmistypicallybasedonitsexperiencewithpubliccompanyfinancialreporting and reputation, and experience with IPOs and other capital markets transactions.

Internationally it is part of the auditor’s work to provide “comfort letters” to the investment banks to supporttheduediligenceprocess.Thisis,however,notcustomaryintheNorwegiancapitalmarkets.

Independent due diligence reviewPrior to a listing the conclusions from a due diligence process must be presented to Oslo Børs, in order to identify whether there are any matters that will have an impact on the shares’ suitability for listing. At a minimum,thecompanymustcarryoutfinancialduediligenceandlegalduediligence.(Thefinancialduediligence must be performed by auditors independent of the company’s statutory auditors).

Other professional advisors Apublicrelationsfirmexperiencedinofferingscanhelpguidecompaniesthroughthemarketing restrictions and make the most of the opportunities that do exist, help prepare materials for analyst presentations, and coach management in their presentation skills.

12 A guide to going public

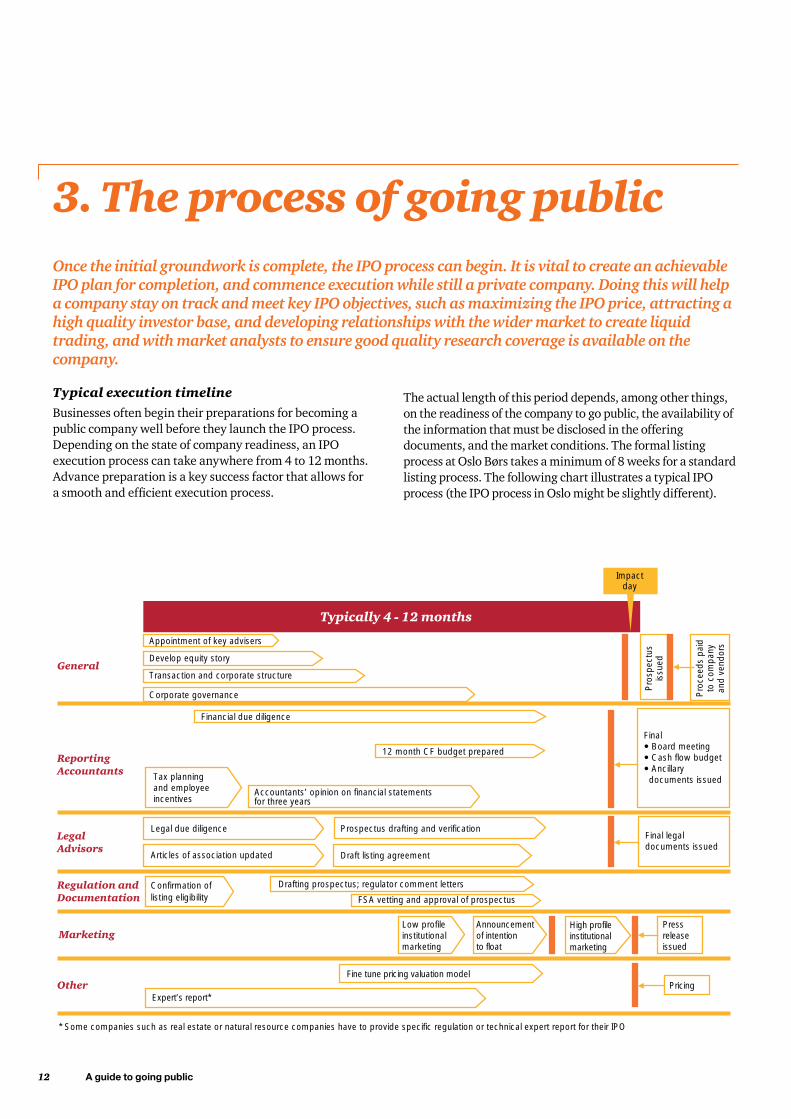

3. The process of going publicOnce the initial groundwork is complete, the IPO process can begin. It is vital to create an achievable IPO plan for completion, and commence execution while still a private company. Doing this will help a company stay on track and meet key IPO objectives, such as maximizing the IPO price, attracting a high quality investor base, and developing relationships with the wider market to create liquid trading, and with market analysts to ensure good quality research coverage is available on the company.

Typical execution timeline

Businesses often begin their preparations for becoming a public company well before they launch the IPO process. Depending on the state of company readiness, an IPO execution process can take anywhere from 4 to 12 months. Advance preparation is a key success factor that allows for asmoothandefficientexecutionprocess.

The actual length of this period depends, among other things, on the readiness of the company to go public, the availability of the information that must be disclosed in the offering documents, and the market conditions. The formal listing process at Oslo Børs takes a minimum of 8 weeks for a standard listing process. The following chart illustrates a typical IPO process (the IPO process in Oslo might be slightly different).

* Some companies such as real estate or natural resource companies have to provide specific regulation or technical expert report for their IPO

Appointment of key advisers

Develop equity story

Transaction and corporate structure

Corporate governance

Financial due diligence

12 month CF budget prepared

Tax planningand employeeincentives

Accountants’ opinion on financial statementsfor three years

Legal due diligence

Articles of association updated

Prospectus drafting and verification

Draft listing agreement

Drafting prospectus; regulator comment lettersConfirmation oflisting eligibility FSA vetting and approval of prospectus

Typically 4 - 12 months

Low profileinstitutionalmarketing

Announcementof intentionto float

High profileinstitutionalmarketing

Pressreleaseissued

PricingFine tune pricing valuation model

Expert’s report*

Final legaldocuments issued

Final Board meeting Cash flow budget Ancillary documents issued

Pro

spec

tus

issu

ed

Pro

ceed

s pa

idto

com

pany

and

vend

ors

Impactday

General

ReportingAccountants

Legal Advisors

Regulation andDocumentation

Marketing

Other

Executing a successful listing in Oslo 13

Once a company reaches a preliminary understanding with its investment banks, the IPO process starts in full force. This phase of the offering should start with a sense of urgency, because the clock is ticking. At the same time as keeping business running as usual, companies and their advisers will need to juggle four tasks and work streams in parallel:

I. Evaluating eligibility for listing

II. Preparationoftheprospectusandfinancialhistoricalinformation, including review and approval by the FinancialSupervisoryAuthorityinNorway

III. Financial and legal due diligence (investigation of the company’s affairs, to be reported to Oslo Børs and the investment banks)

IV. Marketingactivities;i.e.monitoringofmarketconditionsfor pricing purposes and preparation of marketing materials for the road show, and subsequent bookbuilding

Each of these processes has the potential to derail the company on the way to listing if not carried out properly. These work streams are therefore set out in more detail below.

I. Evaluating eligibility for listing

WhenaformallistingprocesswithOsloBørshasbeeninitiated,the review of eligibility of the company for listing will begin. The listingrequirementsaresetoutinmoredetailinsection5–Listing Requirements Oslo Børs and Oslo Axess. The process starts with an introductory report and an introductory meeting, where management of the company and its advisors meet Oslo Børs. A team from Oslo Børs will be dedicated to the company to followupthelistingprocess.Onspecificissues,OsloBørswillrequire–andthecompanywillneedtoprocure–documentationthatthecompanyisincompliancewithspecificlistingcriteria.Matters like board composition, by-laws, audit opinions and cash flowprojectionsaresubjecttoreviewbyOsloBørs.

Holding the kick-off meeting An initial step in the IPO process is arranging an all-hands meeting. This meeting is attended by all membersoftheIPOteam–companymanagement,independent auditors, lead managers, the company’s counsel, and the lead manager’s counsel. The purpose of this initial organisational meeting is to discuss the nature of the offering, coordinate responsibilities for sections of the prospectus, establish a time-table and share information regarding the working group’s availability.

Throughout the IPO process, additional all-hands meetings and/or calls take place to discuss any problems, review drafts of the prospectus, and determine whether the process is on schedule.

In a standard listing process the company will submit an application for listing approximately four weeks after the introductory meeting, and four weeks prior to a scheduled board meeting of Oslo Børs which will handle the formal listing application. From the point of time when the listing application has been submitted, it is public that the company has applied for listing and the company must comply with all legislation relevant to a public company.

Ifthecompanyinsteaddecidestogoforafasttrackorflexibletrack listing, the time from submitting the application until the board meeting of Oslo Børs is reduced to only 4-5 days. The reduced public exposure of the fact that the company has applied for listing is considered favorable for many companies, as this can make the timing of the IPO easier.

14 A guide to going public

II. Preparation of the prospectus and financial historical informationA prospectus in line with EU requirements has to be prepared priortolisting.TheFinancialSupervisoryAuthorityofNorwaywill most often be the competent authority approving the prospectus. Such a prospectus serves mainly two purposes. Primarily the prospectus is a document setting out the terms of the share offering. Secondly, it ensures that all relevant informationisdisseminatedtotheentirefinancialmarketatonce, so that when the company starts reporting all investors are on the same footing.

As a main rule, the prospectus would include three years of auditedfinancialstatementsforthecompany,orlessifthecompany has been in existence for less than three years. Interim financialfiguresmayberequired.Insomeinstancesproformafinancialinformationwillbeneeded,toshowtheeffectofmaterial transactions witch have already taken place or are committedto.Theneedforproformafinancialinformationmost frequently arises in connection with recent business acquisitions.

Risk factors in relation to the company and the offering must be spelled out. Likewise the use of proceeds from the offering, dividend policy, the capital structure of the company and information about the company’s business in general (segments, products, services, markets and so forth) must be disclosed.

Preparing the prospectus is a relatively complicated, time-consuming, technical process requiring substantial planning and coordination. Providing relevant information and complyingwithapplicablerulesinthemostefficientmannerpossible often requires a great deal of effort by the management team, lawyers, and independent accountants and should not be underestimated.

During the preparation process the scheduled timetable for going public can slip, causing a delay in the anticipated offering date. It is therefore imperative that the entire team be thoroughly familiar with the requirements, be cognisant of the deadlines set, regularly assess the status and ensure that reviews are timely.

PriortofinalapprovaloftheprospectusbytheTheFinancialSupervisoryAuthorityinNorway,everyboardmemberofthecompany will have to sign a statement taking responsibility for the prospectus.

Determine the historical financial information to be included in the prospectus Historicalfinancialinformationisavitalpart of the prospectus. The company has to determine what financialinformationistobeincludedinthelistingprospectus. This might mean converting the last twoyearsoffinancialaccountsintoIFRS(orwithother acceptable GAAP). If the issuer has a complex financialhistoryoverthelastthreeyears,itisimportanttoconsiderifadditionalfinancialstatementsneed to be included in the prospectus.

Furthermore, the company would need to prepare an interim report to Oslo Børs prior to listing, which would be subject to a limited scope audit. The rationale is that the company at this stage will need to have both the resources and competence to start reporting quarterly. This interim report may not be required for the prospectus but will be required to be included in the listing application.

Executing a successful listing in Oslo 15

What is “complex financial history”?A‘complexfinancialhistory’ariseswhenevertheexistingstatutoryfinancialaccountsofanissuerdo not provideacomprehensivepictureforinvestorsofthefinancialhistoryoftheoperationsthatitcontrols,orwill control.

Acommonexamplewouldbewhereanewholdingcompanyisformedspecificallyforthepurposeoftheoffering of the securities and that holding company will have either acquired or agreed to acquire a business in which investors are, in substance, being invited to invest. In such circumstances, investors would reasonably expecttoseeincludedintheprospectusthefinancialhistoryoftheunderlyingbusinessinordertobeabletomakeaninformedassessmentoftheassets,liabilities,profitsandlosses,andprospectsoftheissuer.

III. Financial and legal due diligenceThroughout the preparation process, procedures are performed to provide a reasonable ground for belief that, as of the effective date, the company complies with the listing requirements and theprospectuscontainsnosignificantuntrueormisleadinginformation and that no material information has been omitted. These procedures are referred to as due diligence.

Duediligenceprocedures,bothlegalandfinancial,includeadetailed review of the company and its management. These proceduresnormallyincludesitevisits,reviewofsignificantagreementsandcontracts,financialstatements,taxreturns,board of directors’ and shareholders’ meeting minutes, and various analyses of the company and the industry in which it operates. The due diligence advisors also distribute questionnairestothedirectorsandofficers,requestingthem to review, verify, and comment on the information contained in the prospectus draft.

“Keeping current” procedures are performed by the independent auditors to assist the investment banks and underwriters in considering if any material developments have occurredwithrespecttothecompany’sfinancialpositionoroperationssincethedateofthefinancialstatementsincludedinthe prospectus.

Thelegalandfinancialduediligencehastobedonebyinde-pendent lawyers and auditors. The company’s own auditors cannotperformafinancialduediligence.Theresultsfromthedue diligence review are presented to Oslo Børs prior to the submission of the listing application. Any issues brought up in the due diligence process are typically dealt with by either taking steps to correct the issue, or by disclosing the issue in the listing prospectus.

16 A guide to going public

IV. Marketing activities, roadshow and investorsFor potential investors to learn about the company, the investment bank will arrange meetings or “road shows” with financialanalysts,brokers,andpotentialinstitutionalinvestors.

These meetings are generally attended by the company’s CEO andkeymanagementsuchasthechieffinancialofficer,andmay take place in many different locations around the world if the company has an international offering.

The road show is intended to generate excitement and interest in the IPO, and is critical to the success of the offering. It is vital that the management team is well prepared for these meetings. Whilsttheprospectusmustcontainallmaterialinformationrelevant to the offering, the company should not assume that the prospectus is able to “stand on its own” and a company shouldanticipatepotentialquestionsconcerningspecificsaboutits business and be ready to communicate the answers. The credibility projected by a management team in its presentation and its ability to respond to potential investors’ questions will beamajorinfluenceinthesuccessoftheoffering.The“roadshows” represent a critical part of a company’s selling efforts, since it is here that a management team promotes the offering to the institutional investors.

Executing a successful listing in Oslo 17

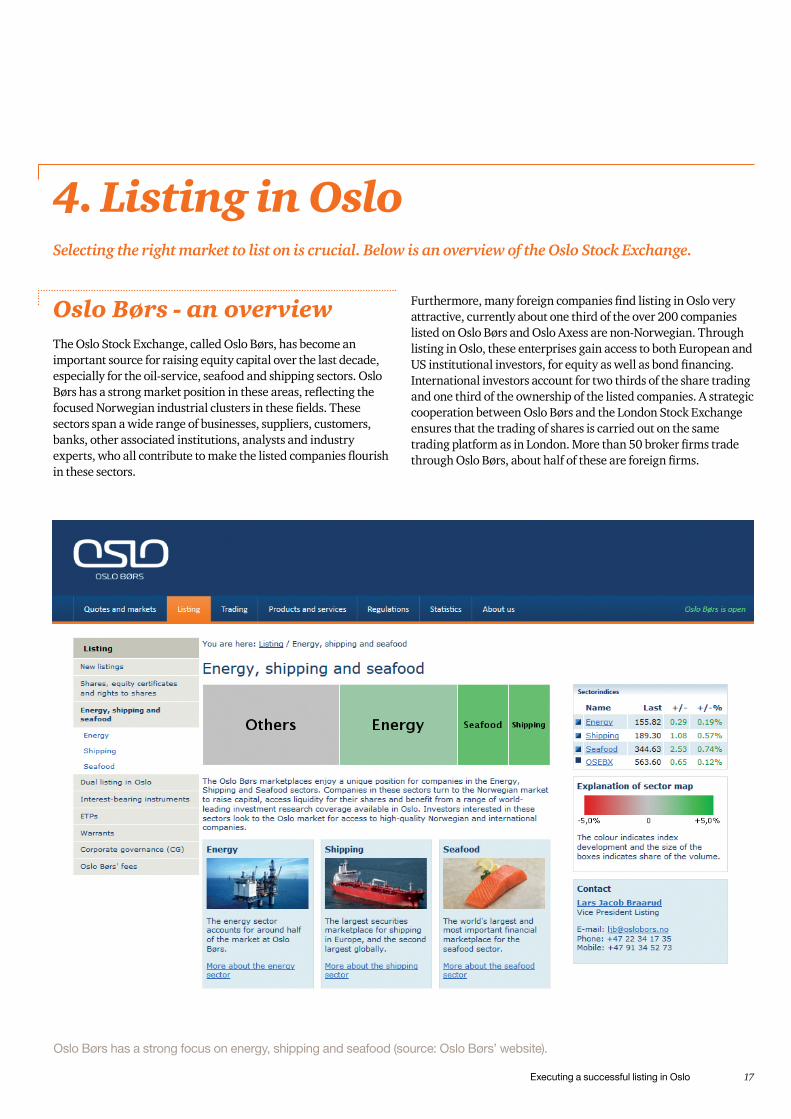

Oslo Børs - an overview The Oslo Stock Exchange, called Oslo Børs, has become an important source for raising equity capital over the last decade, especially for the oil-service, seafood and shipping sectors. Oslo Børshasastrongmarketpositionintheseareas,reflectingthefocusedNorwegianindustrialclustersinthesefields.Thesesectors span a wide range of businesses, suppliers, customers, banks, other associated institutions, analysts and industry experts,whoallcontributetomakethelistedcompaniesflourishin these sectors.

4. Listing in Oslo Selecting the right market to list on is crucial. Below is an overview of the Oslo Stock Exchange.

Furthermore,manyforeigncompaniesfindlistinginOsloveryattractive, currently about one third of the over 200 companies listedonOsloBørsandOsloAxessarenon-Norwegian.Throughlisting in Oslo, these enterprises gain access to both European and USinstitutionalinvestors,forequityaswellasbondfinancing.International investors account for two thirds of the share trading and one third of the ownership of the listed companies. A strategic cooperation between Oslo Børs and the London Stock Exchange ensures that the trading of shares is carried out on the same tradingplatformasinLondon.Morethan50brokerfirmstradethroughOsloBørs,abouthalfoftheseareforeignfirms.

Oslo Børs has a strong focus on energy, shipping and seafood (source: Oslo Børs’ website).

18 A guide to going public

Delivery of shares; “if” or “when issued” InatypicalNorwegianIPOthesharesareadmittedtolistingaftertheyhavebeensubscribed, allotted, fully paid and registered with the Register of Business Enterprises and the Central Securities Depository (VPS).

This means that subscribed investors are exposed to a market risk for a few days before trading can commence. To reduce this risk especially for foreign investors Oslo Børs does, however, allow new shares in an IPO to be listed after they have been subscribed and allotted but prior to being paid and registered,ifcertainstrictconditionsaremet(referredtoas“Ifissued”or“Whenissued”IPOlistings).

In such situations the investment bank will prepay the equity proceeds to the company on behalf of the subscribers–a“softunderwriting”.

The role of the investment bank; “placing power” and “underwriting”Typically a company that has decided to go public engages an investment bank (or several) to help with the listing. This bank is often referred to as “lead manager”, as it coordinates the listing activities (and the syndicate of other banks) and plays the primary role in the launch offering and sale of the issue of securities. The investment banks have access to a pool of potential investors that would in due course be contacted and offered shares in the up-coming listing. This capacity to help the companies issue shares (in the IPO or subsequent to listing) is referred to as the investment banks’ “placing power”.

The investment bank can also act as an “underwriter”, where the bank “underwrites” to take the responsibility and risk for guaranteeing the IPO proceeds from new shareholders just prior to listing,againstanunderwritingfee–asocalled“hardunderwriting”.Incasethesharesarenotfully subscribed by investors, the underwriters bear the risk to have to subscribe for the remaining shares.

UnderwritingislesscommonintheNorwegiancapitalmarketsbutiscommonpracticeabroad.

Oslo Børs has a long history that dates back to 1819.

Executing a successful listing in Oslo 19

Oslo Børs’ listing approvalThe board of Oslo Børs will approve the companyforlistingsubjecttothecompanyfulfillingrelevant listing conditions as set by the Board. Below is an example of such a board resolution:

At its meeting on 23 May 2012, the Board of Directors of Oslo Børs resolved to admit the shares in Selvaag Bolig ASA to listing on Oslo Børs. The Board stipulated that prior to the firstdayoflistingthecompanymustsatisfytherequirementforthenumberofshareholdersasspecifiedinSection2.4.2oftheListingRulesandpublishanapprovedprospectus.InadditionthecompanymustraiseatleastNOK500millionofnewcapitalthroughaplannedshareissuepriortolisting.TheBoardauthorisedtheChiefExecutiveOfficerofOsloBørstofixthedateofthefirstdayoflisting,whichistobenolaterthan6July2012.

Two market placesOslo Børs offers two market places for listing of shares: Oslo Børs and Oslo Axess. Oslo Børs is the main list, while the junior list Oslo Axess has less stringent listing requirements. Both lists are fully regulated marketplaces.

Oslo Børs is generally the choice for larger, commercial companies which have a track record of 3 years or more and a minimum of 500 relevant shareholders. This market place has a number of different share indices, many of which are tradable and with derivative trading as well.

Oslo Axess is the listing option for smaller and medium sized companies that may not meet the requirements for the main market, such as those in the pre-commercial phase. It should be noted that a company listed on Oslo Axess is subject to almost identical reporting requirements and trade monitoring as for companies listed on the main list, as well as enjoying many of the same advantages of access to equity and bond markets, the same trading platform, analyst coverage and so forth. Since the inception of Oslo Axess in 2007, more than 60 companies have been listed here and many have later moved on to Oslo Børs, when the more stringent listing criteria have been met.

Three routes to listingOslo Børs has three routes to listing, irrespective of whether the listing is aimed at Oslo Børs or Oslo Axess. It should be noted that OsloBørsinternationallyisconsideredtohaveaveryefficientandspeedylistingprocess,andcanprovideaconfidentiallistingprocess just up to a few days before listing.

Standard listing process – minimum eight weeks The standard listing process starts with an introductory report filedbythecompanytoOsloBørs,inlinewithdeadlines set by theExchange.Inthisintroductoryphaseitisconfidentialthatthe company is contemplating a listing. This marks the start of the Oslo Børs’ review process of the company’s eligibility for listing. Concurrent with this initial phase the company will prepare the listing prospectus and to some extent wrap up areaswherethecompanyhasnotyetfulfilledthelistingcriteria. Four weeks after the introductory report, the due diligenceadvisors(legalandfinancial)willpresenttheirresultsandfindingstotheExchange.

Shortly after the due diligence meeting, the company will submit the formal application for listing, and the Exchange will make it public that the company has applied for listing. However, should the market conditions not be suitable, the company can still decide to delay the listing application for a month and keep the potential listing under wraps.

The Board of Oslo Børs will consider the application of listing at its monthly board meeting.

In all, the formal listing process, from introductory meeting to Oslo Børs’ approval for listing, takes eight weeks. Subsequent to the approval for listing, the company has a period of 45 days whereithastofulfillanyoutstandingcriteriaforlisting,includingraisingcapital,gettingsufficientshareholdersetc.Morespecificlisting conditions can also be set by the Exchange.

Oslo Børs has a long history that dates back to 1819.

20 A guide to going public

Flexible track – eight weeks, but listing application submitted just prior to listingThe listing process is still eight weeks and consistent with the ordinary process, but the company can delay the listing application until just a few days prior to the board meeting of Oslo Børs. The company can also agree with Oslo Børs on a specificdatefortheboardmeeting.

Whilethelistingfeeforthisrouteishigherthanthestandardlisting process, it is favoured by many companies as the company canreducetheexposuretothemarketandholdconfidentialthefact that the company is seeking listing to only a few days prior to an Oslo Børs board meeting.

Fast track – four weeks, but demanding and costlyFast track is the option for companies that are well prepared for the IPO process and that aim to get listed in half the time of an ordinary listing. This process involves the same review and due diligence as the standard process, but more resources are spent by Oslo Børs to follow up on the company. All milestones and deadlines are agreed in advance between the Exchange and the company.Aswiththeflexibletrackalternative,thecompanycandelay the listing application up to just a few days prior to the board meeting, meaning that the company can reduce the exposure to the market of the fact that it is applying for listing to justafewdays,justaswiththeflexibletrackoption.

As fast track involves considerable more resources on the part of Oslo Børs, this route is quite expensive.

Foto

: Bår

d G

udim

Executing a successful listing in Oslo 21

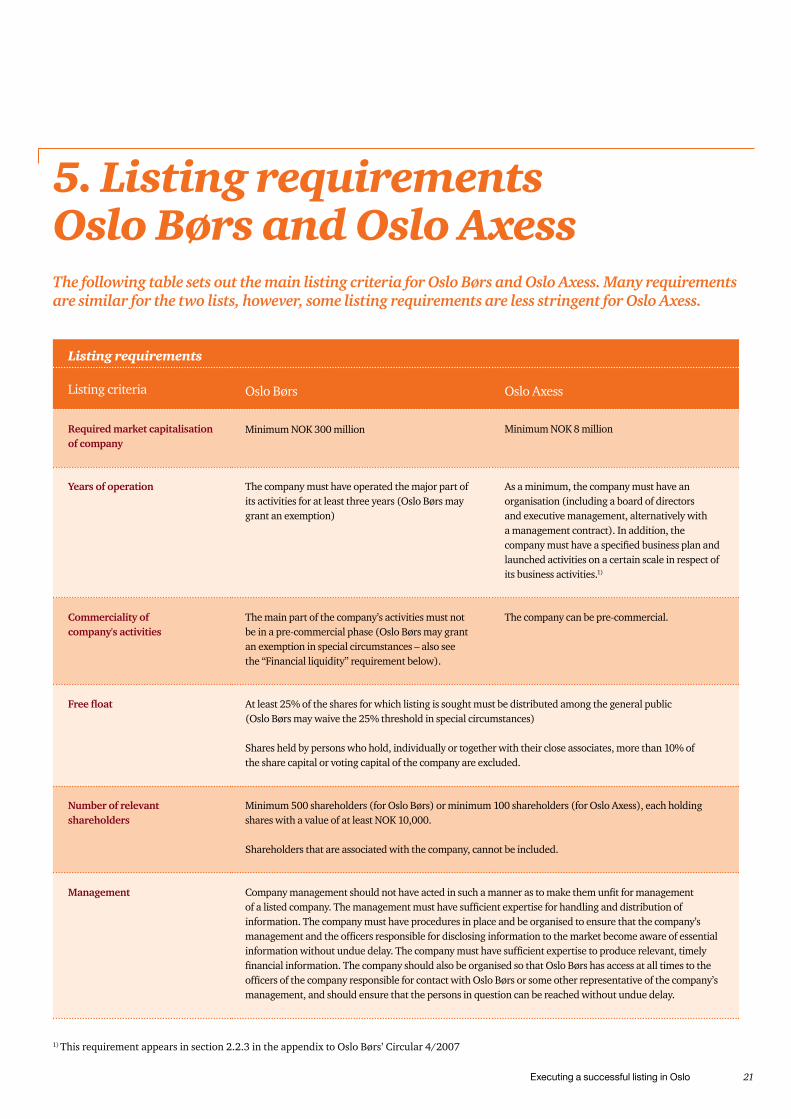

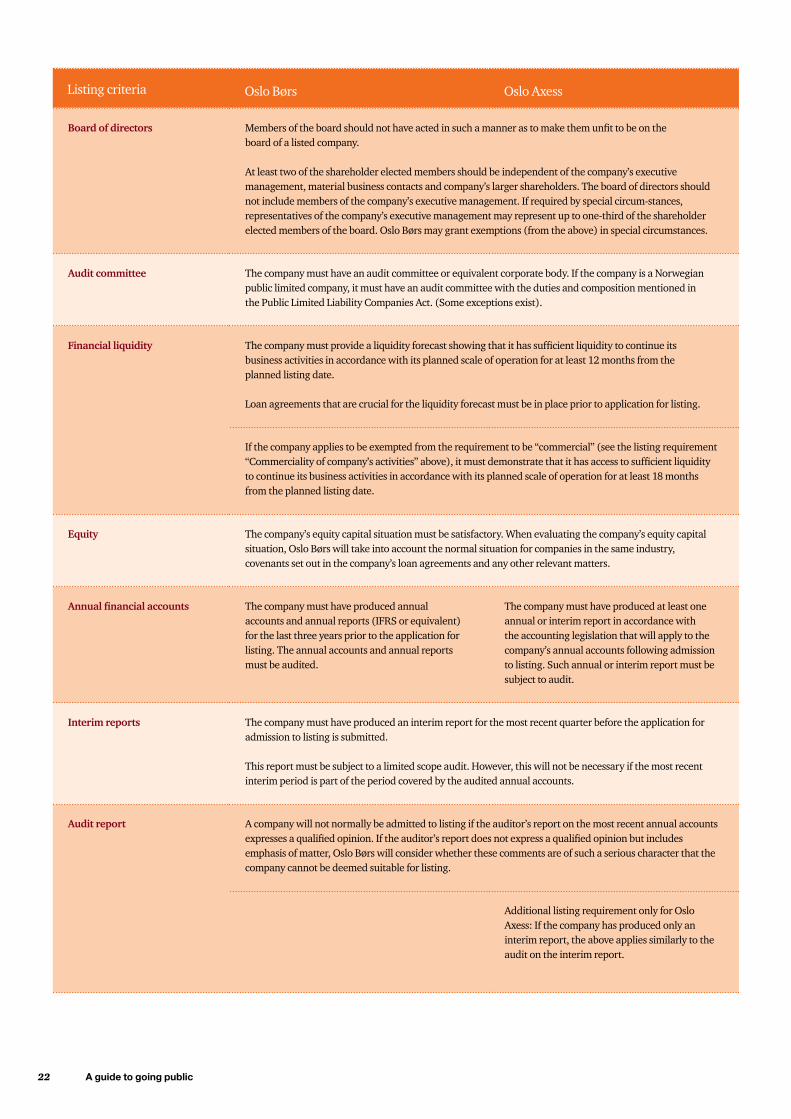

5. Listing requirements Oslo Børs and Oslo AxessThe following table sets out the main listing criteria for Oslo Børs and Oslo Axess. Many requirements are similar for the two lists, however, some listing requirements are less stringent for Oslo Axess.

1) This requirement appears in section 2.2.3 in the appendix to Oslo Børs’ Circular 4/2007

Listing requirements

Listing criteria Oslo Børs Oslo Axess

Required market capitalisation of company

MinimumNOK300million MinimumNOK8million

Years of operation The company must have operated the major part of its activities for at least three years (Oslo Børs may grant an exemption)

As a minimum, the company must have an organisation (including a board of directors and executive management, alternatively with a management contract). In addition, the companymusthaveaspecifiedbusinessplanandlaunched activities on a certain scale in respect of its business activities.1)

Commerciality of company's activities

The main part of the company’s activities must not be in a pre-commercial phase (Oslo Børs may grant anexemptioninspecialcircumstances–alsoseethe “Financial liquidity” requirement below).

The company can be pre-commercial.

Free float At least 25% of the shares for which listing is sought must be distributed among the general public (Oslo Børs may waive the 25% threshold in special circumstances)

Shares held by persons who hold, individually or together with their close associates, more than 10% of the share capital or voting capital of the company are excluded.

Number of relevant shareholders

Minimum 500 shareholders (for Oslo Børs) or minimum 100 shareholders (for Oslo Axess), each holding shareswithavalueofatleastNOK10,000.

Shareholders that are associated with the company, cannot be included.

Management Companymanagementshouldnothaveactedinsuchamannerastomakethemunfitformanagementofalistedcompany.Themanagementmusthavesufficientexpertiseforhandlinganddistributionofinformation. The company must have procedures in place and be organised to ensure that the company’s managementandtheofficersresponsiblefordisclosinginformationtothemarketbecomeawareofessentialinformationwithoutunduedelay.Thecompanymusthavesufficientexpertisetoproducerelevant,timelyfinancialinformation.ThecompanyshouldalsobeorganisedsothatOsloBørshasaccessatalltimestotheofficersofthecompanyresponsibleforcontactwithOsloBørsorsomeotherrepresentativeofthecompany’s management, and should ensure that the persons in question can be reached without undue delay.

22 A guide to going public

Listing requirements

Listing criteria Oslo Børs Oslo Axess

Required market capitalisation of company

MinimumNOK300million MinimumNOK8million

Years of operation The company must have operated the major part of its activities for at least three years (Oslo Børs may grant an exemption)

As a minimum, the company must have an organisation (including a board of directors and executive management, alternatively with a management contract). In addition, the company musthaveaspecifiedbusinessplanandlaunchedactivities on a certain scale in respect of its business activities.1)

Commerciality of company's activities

The main part of the company’s activities must not be in a pre-commercial phase (Oslo Børs may grant anexemptioninspecialcircumstances–alsoseethe “Financial liquidity” requirement below).

The company can be pre-commercial.

Free fl oat At least 25% of the shares for which listing is sought must be distributed among the general public (Oslo Børs may waive the 25% threshold in special circumstances)

Shares held by persons who hold, individually or together with their close associates, more than 10% of the share capital or voting capital of the company are excluded.

Number of relevant shareholders

Minimum 500 shareholders (for Oslo Børs) or minimum 100 shareholders (for Oslo Axess), eachholdingshareswithavalueofatleastNOK10,000.

Shareholders that are associated with the company, cannot be included.

Management Companymanagementshouldnothaveactedinsuchamannerastomakethemunfitformanagementofalistedcompany.Themanagementmusthavesufficientexpertiseforhandlinganddistributionofinformation.The company must have procedures in place and be organised to ensure that the company’s management andtheofficersresponsiblefordisclosinginformationtothemarketbecomeawareofessentialinformationwithoutunduedelay.Thecompanymusthavesufficientexpertisetoproducerelevant,timelyfinancialinformation.ThecompanyshouldalsobeorganisedsothatOsloBørshasaccessatalltimestotheofficersof the company responsible for contact with Oslo Børs or some other representative of the company’s management, and should ensure that the persons in question can be reached without undue delay.

Board of directors Membersoftheboardshouldnothaveactedinsuchamannerastomakethemunfittobeontheboard of a listed company.

At least two of the shareholder elected members should be independent of the company’s executive management, material business contacts and company’s larger shareholders. The board of directors should not include members of the company’s executive management. If required by special circum-stances, representatives of the company’s executive management may represent up to one-third of the shareholder elected members of the board. Oslo Børs may grant exemptions (from the above) in special circumstances.

Audit committee Thecompanymusthaveanauditcommitteeorequivalentcorporatebody.IfthecompanyisaNorwegianpublic limited company, it must have an audit committee with the duties and composition mentioned in the Public Limited Liability Companies Act. (Some exceptions exist).

Financial liquidity Thecompanymustprovidealiquidityforecastshowingthatithassufficientliquiditytocontinueitsbusiness activities in accordance with its planned scale of operation for at least 12 months from the planned listing date.

Loan agreements that are crucial for the liquidity forecast must be in place prior to application for listing.

If the company applies to be exempted from the requirement to be “commercial” (see the listing requirement “Commercialityofcompany’sactivities”above),itmustdemonstratethatithasaccesstosufficientliquiditytocontinue its business activities in accordance with its planned scale of operation for at least 18 months from the planned listing date.

Equity Thecompany’sequitycapitalsituationmustbesatisfactory.Whenevaluatingthecompany’sequitycapitalsituation, Oslo Børs will take into account the normal situation for companies in the same industry, covenants set out in the company’s loan agreements and any other relevant matters.

Annual fi nancial accounts The company must have produced annual accounts and annual reports (IFRS or equivalent) for the last three years prior to the application for listing. The annual accounts and annual reports must be audited.

The company must have produced at least one annual or interim report in accordance with the accounting legislation that will apply to the company’s annual accounts following admission to listing. Such annual or interim report must be subject to audit.

Interim reports The company must have produced an interim report for the most recent quarter before the application for admission to listing is submitted.

This report must be subject to a limited scope audit. However, this will not be necessary if the most recent interim period is part of the period covered by the audited annual accounts.

Audit report A company will not normally be admitted to listing if the auditor’s report on the most recent annual accounts expressesaqualifiedopinion.Iftheauditor’sreportdoesnotexpressaqualifiedopinionbutincludesemphasisof matter, Oslo Børs will consider whether these comments are of such a serious character that the company cannot be deemed suitable for listing.

Additional listing requirement only for Oslo Axess: If the company has produced only an interim report, the above shall apply similarly to the audit report on this interim report.

Due diligence Awrittenfinancialandlegalduediligenceisrequiredfromindependentlegaladvisorsandauditors.

Listing prospectus Alistingprospectus(forcompanieswithNorwayashomestate)hastobeapprovedpriortolistingbytheNorwegianFSA(Finanstilsynet).

Free transferability, share classes, voting rights, minimum value of shares and VPS registration

Stock exchange listed shares should be freely transferable. If the company in any way has been given a discretionary right to bar a share acquisition or to impose other trading restrictions, such right may only be exercisedifthereissufficientcausetobartheacquisitionortoimposeothertradingrestrictions,andsuchimposition does not cause disturbances in the market.

The application for listing must include all shares issued in the same share class. If the company has more than oneclassofshares,thecriteriaforadmissiontolistingmustbesatisfiedforeachclassofsharesforwhichlistingis sought. Oslo Børs may grant an exemption from this provision.

If the company in any way has been given a discretionary right to bar the exercise of voting rights, such discretionaryrightmayonlybeexercisedifthereissufficientcause.

ThesharesmusthaveanexpectedmarketvalueatleastNOK10forlistingonOsloBørsandNOK1forlisting on Oslo Axess

The company’s shares must be registered with a Central Securities Depository authorised pursuant to Section 3-1 of the Securities Register Act.

Reporting on Corporate Governance

CompaniesapplyingforlistingonOsloBørsandAxessmustcomplywiththeNorwegianCodeofPracticeforCorporate Governance or explain any deviation therefrom. Foreign companies can alternatively comply with the equivalent code for the state in which they are registered or the code of practice that applies to the primary market for the shares.

For oil and natural gas companies as well as mining companies

A reserve report is to be prepared prior to application for listing, and to be included in the listing prospectus.

Board of directors Membersoftheboardshouldnothaveactedinsuchamannerastomakethemunfittobeontheboard of a listed company.

At least two of the shareholder elected members should be independent of the company’s executive management, material business contacts and company’s larger shareholders. The board of directors should not include members of the company’s executive management. If required by special circum-stances, representatives of the company’s executive management may represent up to one-third of the shareholder elected members of the board. Oslo Børs may grant exemptions (from the above) in special circumstances.

Audit committee Thecompanymusthaveanauditcommitteeorequivalentcorporatebody.IfthecompanyisaNorwegian public limited company, it must have an audit committee with the duties and composition mentioned in the Public Limited Liability Companies Act. (Some exceptions exist).

Financial liquidity Thecompanymustprovidealiquidityforecastshowingthatithassufficientliquiditytocontinueits business activities in accordance with its planned scale of operation for at least 12 months from the planned listing date.

Loan agreements that are crucial for the liquidity forecast must be in place prior to application for listing.

If the company applies to be exempted from the requirement to be “commercial” (see the listing requirement “Commercialityofcompany’sactivities”above),itmustdemonstratethatithasaccesstosufficientliquidityto continue its business activities in accordance with its planned scale of operation for at least 18 months from the planned listing date.

Equity Thecompany’sequitycapitalsituationmustbesatisfactory.Whenevaluatingthecompany’sequitycapital situation, Oslo Børs will take into account the normal situation for companies in the same industry, covenants set out in the company’s loan agreements and any other relevant matters.

Annual financial accounts The company must have produced annual accounts and annual reports (IFRS or equivalent) for the last three years prior to the application for listing. The annual accounts and annual reports must be audited.

The company must have produced at least one annual or interim report in accordance with the accounting legislation that will apply to the company’s annual accounts following admission to listing. Such annual or interim report must be subject to audit.

Interim reports The company must have produced an interim report for the most recent quarter before the application for admission to listing is submitted.

This report must be subject to a limited scope audit. However, this will not be necessary if the most recent interim period is part of the period covered by the audited annual accounts.

Audit report A company will not normally be admitted to listing if the auditor’s report on the most recent annual accounts expressesaqualifiedopinion.Iftheauditor’sreportdoesnotexpressaqualifiedopinionbutincludesemphasis of matter, Oslo Børs will consider whether these comments are of such a serious character that the company cannot be deemed suitable for listing.

Additional listing requirement only for Oslo Axess: If the company has produced only an interim report, the above applies similarly to the audit on the interim report.

Executing a successful listing in Oslo 23

Thelistabovesetsoutthemainlistingcriteria.Notethatacompanycanapplyforexemptionsfromsomeoftheselistingrequirements. For the full set of listing conditions please see Oslo Børs’ website (http://www.oslobors.no/ob_eng/Oslo-Boers/Listing/Shares-equity-certificates-and-rights-to-shares).

Listing requirements

Listing criteria Oslo Børs Oslo Axess

Required market capitalisation of company

MinimumNOK300million MinimumNOK8million

Years of operation The company must have operated the major part of its activities for at least three years (Oslo Børs may grant an exemption)

As a minimum, the company must have an organisation (including a board of directors and executive management, alternatively with a management contract). In addition, the company musthaveaspecifiedbusinessplanandlaunchedactivities on a certain scale in respect of its business activities.1)

Commerciality of company's activities

The main part of the company’s activities must not be in a pre-commercial phase (Oslo Børs may grant anexemptioninspecialcircumstances–alsoseethe “Financial liquidity” requirement below).

The company can be pre-commercial.

Free fl oat At least 25% of the shares for which listing is sought must be distributed among the general public (Oslo Børs may waive the 25% threshold in special circumstances)

Shares held by persons who hold, individually or together with their close associates, more than 10% of the share capital or voting capital of the company are excluded.

Number of relevant shareholders

Minimum 500 shareholders (for Oslo Børs) or minimum 100 shareholders (for Oslo Axess), eachholdingshareswithavalueofatleastNOK10,000.

Shareholders that are associated with the company, cannot be included.

Management Companymanagementshouldnothaveactedinsuchamannerastomakethemunfitformanagementofalistedcompany.Themanagementmusthavesufficientexpertiseforhandlinganddistributionofinformation.The company must have procedures in place and be organised to ensure that the company’s management andtheofficersresponsiblefordisclosinginformationtothemarketbecomeawareofessentialinformationwithoutunduedelay.Thecompanymusthavesufficientexpertisetoproducerelevant,timelyfinancialinformation.ThecompanyshouldalsobeorganisedsothatOsloBørshasaccessatalltimestotheofficersof the company responsible for contact with Oslo Børs or some other representative of the company’s management, and should ensure that the persons in question can be reached without undue delay.

Board of directors Membersoftheboardshouldnothaveactedinsuchamannerastomakethemunfittobeontheboard of a listed company.

At least two of the shareholder elected members should be independent of the company’s executive management, material business contacts and company’s larger shareholders. The board of directors should not include members of the company’s executive management. If required by special circum-stances, representatives of the company’s executive management may represent up to one-third of the shareholder elected members of the board. Oslo Børs may grant exemptions (from the above) in special circumstances.

Audit committee Thecompanymusthaveanauditcommitteeorequivalentcorporatebody.IfthecompanyisaNorwegianpublic limited company, it must have an audit committee with the duties and composition mentioned in the Public Limited Liability Companies Act. (Some exceptions exist).

Financial liquidity Thecompanymustprovidealiquidityforecastshowingthatithassufficientliquiditytocontinueitsbusiness activities in accordance with its planned scale of operation for at least 12 months from the planned listing date.

Loan agreements that are crucial for the liquidity forecast must be in place prior to application for listing.

If the company applies to be exempted from the requirement to be “commercial” (see the listing requirement “Commercialityofcompany’sactivities”above),itmustdemonstratethatithasaccesstosufficientliquiditytocontinue its business activities in accordance with its planned scale of operation for at least 18 months from the planned listing date.

Equity Thecompany’sequitycapitalsituationmustbesatisfactory.Whenevaluatingthecompany’sequitycapitalsituation, Oslo Børs will take into account the normal situation for companies in the same industry, covenants set out in the company’s loan agreements and any other relevant matters.

Annual fi nancial accounts The company must have produced annual accounts and annual reports (IFRS or equivalent) for the last three years prior to the application for listing. The annual accounts and annual reports must be audited.

The company must have produced at least one annual or interim report in accordance with the accounting legislation that will apply to the company’s annual accounts following admission to listing. Such annual or interim report must be subject to audit.

Interim reports The company must have produced an interim report for the most recent quarter before the application for admission to listing is submitted.

This report must be subject to a limited scope audit. However, this will not be necessary if the most recent interim period is part of the period covered by the audited annual accounts.

Audit report A company will not normally be admitted to listing if the auditor’s report on the most recent annual accounts expressesaqualifiedopinion.Iftheauditor’sreportdoesnotexpressaqualifiedopinionbutincludesemphasisof matter, Oslo Børs will consider whether these comments are of such a serious character that the company cannot be deemed suitable for listing.

Additional listing requirement only for Oslo Axess: If the company has produced only an interim report, the above shall apply similarly to the audit report on this interim report.

Due diligence Awrittenfinancialandlegalduediligenceisrequiredfromindependentlegaladvisorsandauditors.

Listing prospectus Alistingprospectus(forcompanieswithNorwayashomestate)hastobeapprovedpriortolistingbytheNorwegianFSA(Finanstilsynet).

Free transferability, share classes, voting rights, minimum value of shares and VPS registration

Stock exchange listed shares should be freely transferable. If the company in any way has been given a discretionary right to bar a share acquisition or to impose other trading restrictions, such right may only be exercisedifthereissufficientcausetobartheacquisitionortoimposeothertradingrestrictions,andsuchimposition does not cause disturbances in the market.

The application for listing must include all shares issued in the same share class. If the company has more than oneclassofshares,thecriteriaforadmissiontolistingmustbesatisfiedforeachclassofsharesforwhichlistingis sought. Oslo Børs may grant an exemption from this provision.

If the company in any way has been given a discretionary right to bar the exercise of voting rights, such discretionaryrightmayonlybeexercisedifthereissufficientcause.

ThesharesmusthaveanexpectedmarketvalueatleastNOK10forlistingonOsloBørsandNOK1forlisting on Oslo Axess

The company’s shares must be registered with a Central Securities Depository authorised pursuant to Section 3-1 of the Securities Register Act.

Reporting on Corporate Governance

CompaniesapplyingforlistingonOsloBørsandAxessmustcomplywiththeNorwegianCodeofPracticeforCorporate Governance or explain any deviation therefrom. Foreign companies can alternatively comply with the equivalent code for the state in which they are registered or the code of practice that applies to the primary market for the shares.

For oil and natural gas companies as well as mining companies

A reserve report is to be prepared prior to application for listing, and to be included in the listing prospectus.

Due diligence Awrittenfinancialandlegalduediligenceisrequiredfromindependentlegaladvisorsandauditors.

Listing prospectus Alistingprospectus(forcompanieswithNorwayashomestate)hastobeapprovedpriortolistingbytheNorwegianFSA(Finanstilsynet).

Free transferability, share classes, voting rights, minimum value of shares and VPS registration

Stock exchange listed shares should be freely transferable. If the company in any way has been given a discretionary right to bar a share acquisition or to impose other trading restrictions, such right may only be exercisedifthereissufficientcausetobartheacquisitionortoimposeothertradingrestrictions,andsuch imposition does not cause disturbances in the market.

The application for listing must include all shares issued in the same share class. If the company has more thanoneclassofshares,thecriteriaforadmissiontolistingmustbesatisfiedforeachclassofsharesforwhich listing is sought. Oslo Børs may grant an exemption from this provision.

If the company in any way has been given a discretionary right to bar the exercise of voting rights, such discretionaryrightmayonlybeexercisedifthereissufficientcause.

ThesharesmusthaveanexpectedmarketvalueatleastNOK10forlistingonOsloBørsandNOK1for listing on Oslo Axess.

The company’s shares must be registered with a Central Securities Depository authorised pursuant to Section 3-1 of the Securities Register Act.

Reporting on Corporate Governance

CompaniesapplyingforlistingonOsloBørsandAxessmustcomplywiththeNorwegianCodeofPracticefor Corporate Governance or explain any deviation therefrom. Foreign companies can alternatively comply with the equivalent code for the state in which they are registered or the code of practice that applies to the primary market for the shares.

For oil and natural gas companies as well as mining companies

A reserve report is to be prepared prior to application for listing, and to be included in the listing prospectus.

24 A guide to going public

Foreign companies

In general, the listing requirements as set out above, apply equally to primary and secondary listings of foreign companies. However, there are some additional requirements for foreign companies.

Registration of shares with a Central Securities DepositoryThe company’s share capital listed on Oslo Børs will need to be registered with a Central Securities Depository authorised by OsloBørs,usuallytheNorwegianCentralSecuritiesDepository(Verdipapirsentralen–“VPS”).

Accounting standards for financial reportingIFRS, US GAAP2)andJapaneseGAAPareaccountingstandardsaccepted for listing on Oslo Børs and Oslo Axess. The option to reportinlinewithUSGAAPandJapaneseGAAPmight,however, only be possible for third country issuers.

Fornon-EEAissuerswithNorwayashomestatewithfinancialstatements with a closing prior to December 31, 2014 the following GAAPs are also allowed: China, Canada, South- Korea and India.

Social responsibilityDepending on their domestic rules, foreign companies might be required to report on their social responsibility policy.

The report must include a consideration of human rights, employee rights and social conditions, external environment and actions against corruption. The report must, at a minimum, disclose the guidelines, principles, procedures and standards that the company employs in regard to the points mentioned above. In addition, the company shall disclose how they plan to implement these principles, as well as give an assessment of the results achieved as a consequence of the work performed. Companies that don’t have a social responsibility policy must state that fact.

For primary listing in OsloFor foreign companies applying for primary listing the requirements of required market capitalisation, free float and number of relevant shareholders (see listing criteria page21)havetobefulfilledfortheproportionofthesharecapital that is (or will be) registered with the VPS.

For secondary listing in Oslo The requirements for free float and number of relevant shareholders (see listing criteria page 21) apply to the company’s entire share capital. However, a minimum of 100 (for listing on Oslo Axess) or 200 (for listing on Oslo Børs) shareholders holding shares with a value of at least NOK10,000musthavetheirsharesregisteredwiththeVPS.

For secondary listings a limited scope audit of the most recent interim report might not be requested. Depending on the circumstances, Oslo Børs might not require a due diligence of companies applying for secondary listing in Oslo.

2) Generally Accepted Accounting Principles

“On-site” listing meetingsOslo Børs offers “on-site” meetings with companies that intend to list, which means that the pre-listing meeting between the company and Oslo Børs as well as the compulsory introductory course are both held at the company’s premises, against an additional fee.

Executing a successful listing in Oslo 25

6. Life as a public companyThe IPO is not the end result, it is the beginning of a new era for the company.

Thefirstmonthsasapubliccompanyarecritical.Theremaybeuncertainty among investors and analysts because the company is relatively unknown. The newly established public company may also be less familiar with forecasting results and performance. The consequences of not meeting expectations can be severe. An inability to communicate effectively and manage expectations of the analysts and investors can be damaging to shareholder value and compromise credibility.

Asaresult,havingtherightfinancefunction,withtherightcapabilitiestodeliverqualityfinancialreportingattherighttime, is an important factor in a successful IPO. This is typically achievedbyfirstfocusingongettingthemonthlyfinancialcloseprocess in shape to deliver results within an accelerated timeframe, and then preparing the quarterly, half yearly and annualfinancialinformationwiththelevelofdetailandaccuracy that is expected of a public company. A good IPO plan willidentifythecriticalaspectsofthefinancefunctionthatneed to be in place before starting the IPO preparation process -forexample,theCFOandfinancialcontrollerfunctions.Otherfunctions, such as investor relations, can be built up during the IPO preparation process, perhaps initially relying on external resources, and migrating to an internal investor relation function as the IPO launch date approaches. The key is getting the appropriate balance of resources in place at the right time, without overdoing it before the IPO is certain. Once a company is public, considerable effort must be expended tomaintainthemomentumfromthelisting.Aflowofpositivenews to the investors is preferable. If investor enthusiasm for a company is not maintained, trading will decline. If company’s sharesarethinlytraded,manyofthebenefitssoughtfromtheIPO (such as liquidity through a future secondary offering) may not be realized. Effective distribution and support of the stock, aswellascontinuinginterestfromfinancialanalysts,istherefore necessary after the IPO. Company management should continue to meet investors at least quarterly, and follow upwithfinancialanalysts.

Questions to ask after the IPO include:

• Is the company demonstrating a sustained or increasing growth rate that is high enough to attract and satisfy investors?

• Are the company ‘s products or services highly visible and of interest to consumers and investing public? The company should project a positive image to its investors, customers, and community. This is important, since the attitude of the public may sway the share price.

• There is growing interest in corporate social responsibility, including sustainability and climate change issues. Companies should have a strategy to address such concerns.