a loose fit: india and the briics ulrich bartsch

TRANSCRIPT

A Loose Fit: India and the BRIICS

Ulrich Bartsch

Themes

• Not an optimal currency area: economic cycles in India and the BRIICS .• Monetary policy through the rear-view mirror.• India’s medium- to long-term prospects: no-one pays the debt.• Work hard to make a living: reforms are needed to tackle structural

barriers to growth.

BRIICS: Divergence in Economic Cycles

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Jan-

07

Apr-

07

Jul-0

7

Oct

-07

Jan-

08

Apr-

08

Jul-0

8

Oct

-08

Jan-

09

Apr-

09

Jul-0

9

Oct

-09

Jan-

10

Apr-

10

Jul-1

0

Oct

-10

Jan-

11

Apr-

11

Jul-1

1

Oct

-11

CPI Inflation

Source: IFS

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

Mar

-98

Oct

-98

May

-99

Dec

-99

Jul-0

0

Feb-

01

Sep-

01

Apr-

02

Nov

-02

Jun-

03

Jan-

04

Aug-

04

Mar

-05

Oct

-05

May

-06

Dec

-06

Jul-0

7

Feb-

08

Sep-

08

Apr-

09

Nov

-09

Jun-

10

Jan-

11

Aug-

11

GDP Growth

Divergence: India’s monetary policy

• Flexible exchange rate as a shock absorber

• Capital controls enhance monetary policy independence

• Foreign reserves to create confidence

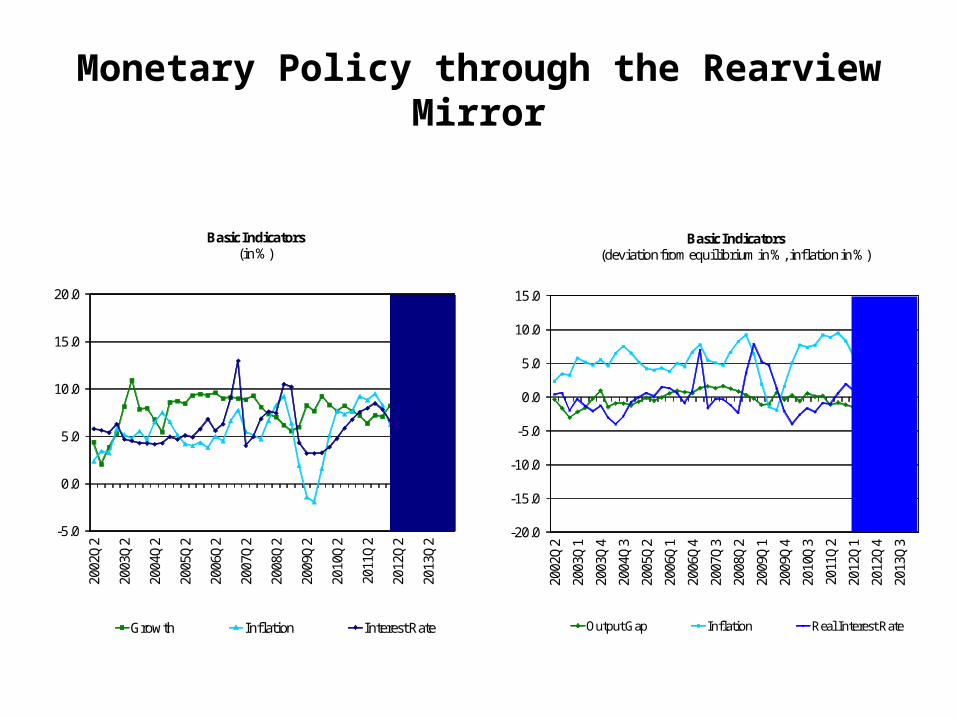

Monetary Policy through the Rearview Mirror

-5.0

0.0

5.0

10.0

15.0

20.0

2002

Q2

2003

Q2

2004

Q2

2005

Q2

2006

Q2

2007

Q2

2008

Q2

2009

Q2

2010

Q2

2011

Q2

2012

Q2

2013

Q2

Basic Indicators(in %)

Growth Inflation Interest Rate

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

2002

Q2

2003

Q1

2003

Q4

2004

Q3

2005

Q2

2006

Q1

2006

Q4

2007

Q3

2008

Q2

2009

Q1

2009

Q4

2010

Q3

2011

Q2

2012

Q1

2012

Q4

2013

Q3

Basic Indicators(deviation from equilibrium in %, inflation in %)

Output Gap Inflation Real Interest Rate

Something for Nothing: India’s Debt Dynamics19

96

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

-12.0

-8.0

-4.0

0.0

4.0

8.0

12.0

-12.0

-8.0

-4.0

0.0

4.0

8.0

12.0r - g Real Int. Rate Real GDP Gr. Rate

Interest Rate and GDP Growth Rate, 1999-2010

Unfavorable Debt Dynamics: Aging Populations in the OECD Countries

Example: GermanyRising welfare costs, falling labor supply, low growth

The Developed Countries are Bankrupt!

Surce: IMF, Fiscal Monitor April 2011, http://www.imf.org/external/pubs/ft/fm/2011/01/pdf/fm1101.pdf

Demographic Transition in India

• The Indian population is among the youngest in the world; only now (2010s) can we see the beginning of the demographic transition to lower dependency ratios.

• The transition comes not only from demographic changes: increasing numbers of women enter the (paid) labor force.

• India will reap the maximum benefit of the transition around 2040 – far later than most other big countries, China included.

• This also means large additions to the labor force: 1 million people per month over the next 20 years.

• Job and skill creation are the biggest challenges.

75000 55000 35000 15000 5000 25000 45000 65000

15-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-7980-8485-8990-9495-99100+

Males Population in Thousands Females

2040

75000 55000 35000 15000 5000 25000 45000 65000

15-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-7980-8485-8990-9495-99100+

Males Population in Thousands Females

2020

75000 55000 35000 15000 5000 25000 45000 65000

15-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-7980-8485-8990-9495-99100+

2000

75000 55000 35000 15000 5000 25000 45000 65000

15-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-7980-8485-8990-9495-99100+

1980

Educational attainment by age group, 1980-2040

No education Primary Secondary Tertiary

Constraints to Growth of Industry

• Land– Archaic rules, eminent domain use leads to discontent (the increase in the value of land from

conversion to industrial, commercial, and residential uses is often not captured by the original owners, who feel cheated), poor land use planning.

• Power– Most surveys of entrepreneurs indicate availability of reliable power as a major constraint. – The constraint is more binding for medium and small firms, as most large firms have captive

generators (which also raises costs).– Large increase in power generation required to sustain high growth – fuel availability constraints.

• Use of natural resources– Hydropower expansion is hampered by conflicts over water and forests.– Conflicts over mining impede exploitation of minerals.

• Environmental regulation– Years of loose enforcement and corruption have created a legacy of destruction, change in

enforcement has stopped projects in late stages of execution, created regulatory uncertainty.

US and Europe Slowing, India and China Catching Up

• From the middle of the last century, Western Europe started diverging from the rest of the world.

• In the 1800s, the US and Western Europe both experienced accelerated per capita GDP growth because of the industrial revolution.

• Growth in India and China continued to be very slow until the 1970s, when it started accelerating in China, and less so in India.

• China and India had the same per capita income in 1973, but then China pulled ahead.

• Since the 1990s, growth in the US and Western Europe is slowing, giving India and China room to catch up.

0 1000 1500 1600 1700 1820 1870 1913 1950 1973 1998 20101

10

100

1000

10000

100000

Per Capita GDP, 0-2010(in constant 1990 U.S. dollars, log scale)

North America Western Europe China India

Source: Angus Maddison, worldeconomy.org.

India and China Regaining their Place in the World Economy?

• Throughout much of recorded history, India and China held a dominant position in world production and income.

• Only in the 1600s, Western Europe started its rise as a global economic force, complemented by the US from the 1800s.

• From 1700s to the turn of the millennium, the global share of China and India fell from 50 to 15 percent.

• Since the 1970s, a turnaround has become visible, and China in particular is increasing its share in the global economy.

0 1000 1500 1600 1700 1820 1870 1913 1950 1973 1998 20100.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

Share in World GDP(in percent)

Total Western Europe United StatesChina India

Final Remarks

• Continued fast growth in India critically depends on removing structural constraints.

• The government is tackling some of them including with new laws and regulation.

• Political leadership required to address politically sensitive issues, such as losses in the electricity sector.

• If structural constraints can be loosened, India could benefit from a strong rise in the economically active population – the demographic dividend – well into the 21st century.

• India could reclaim the place in the world economy it held up to the 17th century, when it accounted for 25% of world GDP.