a meta-analysis of ifrs adoption effects

TRANSCRIPT

Available online at www.sciencedirect.com

A Meta-analysis of IFRS Adoption Effects

Kamran Ahmeda,⁎, Keryn Chalmersb, Hichem Khlif c

a Department of Accounting, La Trobe University, Melbourne, Victoria 3086, Australiab Department of Accounting and Finance, Monash University, Australia

c University of Economics and Management of Mahdia, University of Monastir, Tunisia

Received 25 September 2012

Abstract

The adoption of IFRS around the globe has stimulated empirical research that investigates thefinancial reporting and capital market effects associated with an accounting regime change. Thesestudies differ in their analysis period, jurisdictional setting, and research design, and they reportvarying findings. We conduct a meta-analysis of IFRS adoption studies investigating financialreporting effects, namely value relevance and earnings transparency in the form of discretionaryaccruals, as well as capital market effects, specifically the quality of analysts' earnings forecasts. Ourfindings show that the value relevance of book value of equity has not increased post-IFRS adoption,whereas the value relevance of earnings has generally increased when assessed using price models.Our results also suggest that discretionary accruals have not reduced, but analysts' forecast accuracyhas increased significantly post-IFRS adoption. Our findings are not affected materially aftercontrolling for moderating factors including jurisdictional differences such as legal origin, theaccounting and auditing enforcement regime, and differences between domestic GAAP and IFRS.However, these associations are moderated by the model used for empirical investigation of valuerelevance and discretionary accrual effects; they are also moderated by the adoption being voluntaryor mandatory. The findings provide evidence to inform policy assessments and deliberations of thefinancial reporting and capital market effects of adopting IFRS.© 2013 University of Illinois. All rights reserved.

JEL classification: M41Keywords: Discretionary accruals; Economic consequences; Analysts' forecasts; IFRS; Meta-analysis andvalue relevance

The International Journal of Accounting 48 (2013) 173–217

⁎ Corresponding author.E-mail addresses: [email protected] (K. Ahmed), [email protected] (K. Chalmers),

[email protected] (H. Khlif).

0020-7063/$ - see front matter © 2013 University of Illinois. All rights reserved.http://dx.doi.org/10.1016/j.intacc.2013.04.002

174 K. Ahmed et al. / The International Journal of Accounting 48 (2013) 173–217

1. Introduction

High-quality information is paramount for the efficient functioning of equity markets.In particular, accounting regimes and generally accepted accounting principles play a crucialrole in shaping the preparation and presentation of financial information to external userswho rely on this information for decision-making. Financial information is important for theinvestment community, therefore adopting International Financial Reporting Standards(IFRS)1 as the basis for the preparation and presentation of financial reports is a significantpublic policy decision demanding a cost/benefit analysis. To date, the empirical evidenceon the benefits for investors are mixed (Brown, 2011). The aim of this paper is to present ameta-analysis of a large collection of papers that investigate the financial reporting and capitalmarket effects associated with IFRS adoption.2 Specifically, the broad research questionaddressed is: has IFRS adoption increased financial reporting quality and improved analysts'information environment?

An espoused benefit of IFRS adoption for some jurisdictions is that financial reportingbecomesmore transparent because IFRS provides users with additional disclosure requirementsand specifies measurement and recognition rules that directly impact the quality of accountingnumbers (Daske, 2006). For example, Barth, Landsman, and Lang (2008) find that firmsadopting IFRS engage in less earnings management, exhibit more timely loss recognition, andprovide more value relevance of earnings. The authors interpret these findings as evidence ofhigher financial reporting quality. Studies have also shown IFRS can enhance analysts'information environment (Byard, Li, & Yu, 2011; Stecher & Suijs, 2012). It is also noted thatjurisdictional differences influence IFRS implementation, hence the quality of accountingnumbers and the information available to markets (e.g., Ball, 2006; Liao, Sellhorn, & Skaife,2012; Stecher & Suijs, 2012).

Empirical studies have investigated the value relevance and discretionary accrual effects ofvoluntary adoption of IFRS (e.g., Ashbaugh & Pincus, 2001; Harris &Muller, 1999; Hung &Subramanyam, 2007; Jermakowicz, Prather-Kinsey, & Wulf, 2007; Van Tendeloo &Vanstraelen, 2005). The regulation passed by the European Parliament and the EuropeanCouncil of Ministers requiring the adoption of IFRS by all European listed entities, as well assimilar developments in other jurisdictions, spawned further value relevance and discretionaryaccrual studies in a mandatory IFRS adoption setting (e.g., Byard et al., 2011; Chalmers,Clinch, & Godfrey, 2008; Cheong, Kim, & Zurbruegg, 2010; Clarkson, Hanna, Richardson,& Thompson, 2011; Devalle, Onali, & Magarini, 2010; Goodwin, Ahmed, & Heaney, 2008;Iatridis, 2010; Zéghal, Chtourou, & Sellami, 2011) as well as the impact on analysts'information environment (e.g., Chalmers, Clinch, Godfrey, & Wei, 2012; Horton, Serafeim,& Serafeim, 2012; Jönsson, Jansson, & van Koch, 2012). Voluntary and mandatory IFRS

1 The predecessors to IFRS were International Accounting Standards (IAS). In our study, IFRS referencingincludes IAS.2 Brüggemann et al. (2012) classify empirical studies of IFRS adoption as financial reporting effect studies

(compliance and accounting choice studies, accounting property studies and value relevance studies), capital marketeffect studies (direct and indirect evidence on economic consequences in capital markets) and macroeconomic effectstudies. Consistent with this classification, we explore the financial reporting effects by meta-analyzing valuerelevance and discretionary accrual studies, and a capital market effect by meta-analyzing analysts' earnings forecastaccuracy studies.

Table 1Sample selection criteria.

Number of papers Independent samples

Initial sample 88Criteria leading to the exclusion of studies

Papers with narrative and descriptive analysis and insufficientdata to compute the size effect for meta-analysis

11

Papers not investigating value relevance, discretionary accrualsor analysts' earnings forecast accuracy IFRS adoption effects

20

Final sample 57Value relevance studies 30 47Discretionary accrual studies 13 29Analysts' earnings forecast accuracy studies 14 20

Total 57 96

175K. Ahmed et al. / The International Journal of Accounting 48 (2013) 173–217

adoption effect studies have been conducted in jurisdictions with varying cultural, institutional,and legislative regimes. These studies have differed in the measurement and modeling of thefinancial reporting effect constructs being investigated. The empirical evidence on the financialreporting and capital market effects is inconsistent and our study synthesizes and reconcilesthese findings.

Studies on the economic consequences of IFRS adoption are highly relevant given thatIFRS are increasingly globally accepted. The motivation of our paper is to reconcile theinconsistent research findings and draw stronger inferences on IFRS adoption effects.Specifically, we are interested in studies that investigate the association between IFRS adoptionand (1) the value relevance of reported book value of equity and earnings, (2) discretionaryaccruals, and (3) analysts' earnings forecast accuracy.3 Identifying the relevant empiricalstudies, we use the approach developed by Rosenthal (1991), Hunter, Schmidt, and Jackson(1982), and Hunter and Schmidt (2000) and we offer a meta-analysis of these three bodiesof literature to integrate the results, detect the causes of the variability of results across studies,and draw conclusions to better understand the IFRS adoption effects.

Meta-analysis is a statistical technique allowing researchers to overcome the shortcomingsof the narrative aspects of empirical reviews. It accumulates the statistical findings of relatedresearch in an attempt to make quantitative generalizations and reduce the limited statisticalpower of studies with small sample sizes. Further, a properly executedmeta-analysis canmakesignificant contributions to practice and policy as well as to general knowledge by developinga robust framework of the whole body of research on a given topic (Lipsey &Wilson, 2001).Despite its popularity in disciplines such as medical research, meta-analysis has not beenextensively used in the accounting literature (Pomeroy & Thornton, 2008) 4 although its use isincreasing. The accounting-related studies applying this methodology meta-analyze selectedpositive accounting theory variables (Christie, 1990), the determinants of disclosure level

3 To assess meta-analytically IFRS adoption effects, it is necessary to have a sufficiently large number of studiesthat have empirically addressed a particular research question. Our choice of discretionary accrual and valuerelevance studies to meta-analyze the financial reporting effects of IFRS adoption, and analysts forecast accuracystudies to meta-analyze a capital market effect, is influenced by this criterion.4 See Pomeroy and Thornton (2008) for an overview of meta-analysis contributions to various disciplines.

176 K. Ahmed et al. / The International Journal of Accounting 48 (2013) 173–217

(Ahmed& Courtis, 1999; Khlif & Souissi, 2010), the effect of corporate governance attributeson earnings management (García-Meca & Sánchez-Ballesta, 2009; Lin & Hwang, 2010),board independence, ownership concentration and voluntary disclosure (García-Meca &Sánchez-Ballesta, 2010), auditors' internal control judgment (Trotman &Wood, 1991), auditfees and firm specific variables (Hay, Knechel, &Wong, 2006), audit committee independenceand financial reporting quality (Kinney & Martin, 1994; Lin & Hwang, 2010; Pomeroy &Thornton, 2008), and non-audit fees and financial reporting quality (Habib, 2012). While thereare reviews that summarize and discuss the empirical literature on IFRS adoption consequences(e.g., Brown, 2011; Brüggemann, Hitz, & Sellhorn, 2012; Houqe, van Kesteren, & Clarkson,2012; Pope & McLeay, 2011; Soderstrom & Sun, 2007), to the best of our knowledge ourstudy is the first attempt to summarize, using an accepted statistical methodology, theseconsequences. In performing the analysis, we test for moderating effects including jurisdictionaldifferences, methodological differences,5 and the mode of IFRS adoption (mandatory orvoluntary) that may explain the inconsistent findings in the literature.

The contributions of our study are threefold. First, we contribute to the debate on IFRSadoption effects by offering a quantitative generalization drawn from a sample of empiricalstudies examining effects of the switch to IFRS. Pope and McLeay (2011) note that the IFRSadoption effect results from the European Union (E.U.) are “far from uniform”. Brown (2011)also discusses the mixed evidence and calls for “improved methods to seek them out”. Ourapproach complements the narrative reviews on the consequences of IFRS adoption andresponds to the challenge to better understand the array of evidence. Second, we provideevidence of the factors that are plausible explanations for the divergent results and anomaliesin the extant literature. Our study aggregates the results of prior studies and summarizes thefindings; it thus facilitates theoretical development and provides direction to future empiricalstudies. For example, we show how jurisdictional differences, research design, and constructmeasurement influence results of IFRS adoption effect studies. Third, our study is a furtherdemonstration of the applicability and usefulness of themeta-analytic technique for accountingresearch.

We find that the value relevance of book value of equity has not increased after IFRSadoption, whereas the value relevance of earnings has generally increased when assessedusing price models. Further, we find that IFRS adoption is not associated with discretionaryaccruals, a construct for earnings management. Finally, our results provide strong support forthe improvement of financial analysts' earnings forecasts in an IFRS regime, suggesting thatanalysts' information environment has improved.

Our results are useful to the investment community and accounting standard-setting bodiesand regulators. The decision by various jurisdictions to permit, converge, or adopt IFRS is apublic policy decision that demands an ex post analysis to determine if the perceived benefits arerealized. Our study provides aggregated evidence on the financial reporting and capital marketeffects flowing from such a decision and the factors influencing such effects. This informsdeliberations by jurisdictions, such as the U.S., contemplating permitting financial reporting inaccordance with IFRS for domestic issuers and assists regulators in IFRS adopting jurisdictions

5 For example, the use of price versus return models to assess the value relevance of earnings and the modelused by studies to measure discretionary accruals.

177K. Ahmed et al. / The International Journal of Accounting 48 (2013) 173–217

to appreciate how their jurisdictional environments are influencing IFRS adoption effects.Knowledge of such influences assists policy makers and accounting standard setters tounderstand the impediments to achieving global financial statement comparability.

The remainder of the paper is structured as follows. In the next section, we present anarrative review of the literature relevant to our study. This section also develops thehypotheses to be tested. The IFRS adoption effect studies reviewed, synthesized andassessed in our study are detailed in Section 3. A discussion of the meta-analytic techniqueapplied to these studies follows in Section 4. Section 5 presents and analyses the empiricalresults of the meta-analysis of the effect of IFRS adoption on the value relevance ofaccounting information, discretionary accruals and analysts' earnings forecasts. Section 6offers conclusions and future research directions.

2. Literature review

The espoused benefits and costs of IFRS adoption are documented in the professionaland academic literature. Benefits cited include reducing information asymmetry, enhancingcapital market efficiency, and greater transparency and consistency across jurisdictions. Theimpediments to the realization of such benefits include communication and interpretationbarriers, permissible alternative accounting treatments and preparer incentives, and a desire tomaintain sovereignty of accounting standard setting and differences in institutional and legalregimes that impact IFRS compliance and enforcement. Ball (2006) argues that the pros andcons are conjectural with IFRS being a “veneer of uniformity” that may not enhance financialreporting comparability. This view is supported by the mixed empirical findings summarizedin review papers (e.g., Brown, 2011; Pope &McLeay, 2011). This study meta-analyzes threebodies of empirical literature on IFRS adoption effects — value relevance, discretionaryaccruals and analysts' earnings forecast accuracy studies — and presents a review of thisliterature.

2.1. IFRS adoption and value relevance studies

The empirical assessments of financial reporting effects associated with IFRS adoptioninclude a body of literature that examines changes in the value relevance of earnings andbook value of equity as the financial reporting quality attribute. Such literature offersfruitful insights on the implications for the association between accounting information andshare prices when the basis for the preparation and presentation of accounting informationchanges (Barth, Beaver, & Landsman, 2001). If IFRS recognition, measurement anddisclosure requirements produce information that is more relevant and faithfully representedrelative to domestic GAAP, the value relevance of the accounting information should increasewith its adoption. To test this espoused benefit of IFRS, empirical studies using price andreturn models have been undertaken in different contexts, jurisdictions, and time periods withvarying results.

Value relevance studies of voluntary IFRS adoption report mixed findings. Forexample, studies of the change in value relevance for German firms electing to use IFRS asthe basis for financial reporting rather than German GAAP (e.g., Bartov, Goldberg, & Kim,2005; Hung & Subramanyam, 2007; Jermakowicz et al., 2007) report evidence of

178 K. Ahmed et al. / The International Journal of Accounting 48 (2013) 173–217

declining, increasing, and no change in the relevance of earnings associated with voluntaryIFRS adoption. Using a sample of firms listed on the Helsinki Stock Exchange between1984 and 1992, Kinnunen, Niskanen, and Kasanen (2000) report a significant decrease inthe correlation between accounting information and share price after voluntary adoption. Incontrast, Bartov et al. (2005) test such an association for German firms that voluntarilyadopted IFRS standards between 1998 and 2000. They report no significant improvementin the association between returns and earnings following the adoption. Hung andSubramanyam (2007) using German firms switching from German GAAP to IFRS duringthe period 1998 and 2002 find that the value relevance of book value of equity is notsignificantly different between the two accounting systems, whereas earnings are morevalue relevant under German GAAP. However, Jermakowicz et al. (2007) report anincrease in the explanatory power of earnings and book value of equity after the voluntaryadoption of IFRS for a sample of DAX-30 firms from 1995 to 2004. Using a Norwegiansetting, Gjerde, Knivsflå, and Sættem (2008) find that book value of equity is more valuerelevant under IFRS, whereas earnings are more value relevant under Norwegian GAAP(NGAAP) employing a price model. The authors find no significant change in valuerelevance when a return model is used.

The decision by jurisdictions to mandate IFRS as the basis for financial report preparationand presentation spawned further research, both intra- and inter-national studies. Thejurisdictions mandatorily adopting IFRS or a version thereof 6 include those with varyinginvestor protection regimes. Some have a common law origin (e.g., Australia, U.K.) andothers a civil law origin (e.g., Germany, France). The within-country studies produceinconsistent findings supporting Ball's (2006) view of the difficulty of developing a theory toexplain the pros and cons of standardized accounting rules within a country let alone acrosscountries. For example, Morais and Curto (2008) find that the value relevance of Portuguesefirms' earnings and book value of equity declines in the post-adoption period. In contrast,Oliveira, Rodrigues, and Craig (2010), find IFRS adoption by Portuguese firms has no effecton the value relevance of book value of equity and decreases the value relevance of earnings.Paglietti (2009), undertaking a similar analysis for Italian firms, finds that the book value ofequity (earnings) is more (less) value relevant under IFRS. She considers also the empiricallinkage between earnings and stock returns as a proxy for value relevance and reports asignificant improvement of the relationship between earnings and stock returns in thepost-IFRS adoption period (2005–2006) compared to the pre-IFRS adoption period (2002–2004). An investigation of Turkish firms (Türel, 2009) reports increases in the relevance ofearnings and book value of equity for firms in the post-IFRS period. Iatridis (2010) finds nosignificant change in the value relevance of accounting information post-IFRS adoption forU.K. firms. A study of Greek firms find an increased relevance for both earnings and bookvalue of equity post IFRS adoption (Iatridis & Rouvolis, 2010); however, the findings aresensitive to the choice of a price versus return model. Using a return model, the authors foundno evidence of value relevance enhancement with IFRS adoption.

6 Jurisdictional approaches to adopting IFRS can vary from requiring firms to prepare financial statements usingIFRS as issued by the IASB thereby ensuring full compliance with IFRS or permitting a version of IFRS whichmay contain deviations from IFRS.

179K. Ahmed et al. / The International Journal of Accounting 48 (2013) 173–217

Outside of the European Union, Chalmers, Clinch, and Godfrey (2011) find thatearnings (book value of equity) has become more relevant (no change in relevance) in thepost-IFRS period using a price model. However, using a return model, they report theassociation between stock return and earnings decreases with IFRS adoption. In Malaysia,an emerging market, Ismail, Van Zijl, and Dunstan (2010) report that the value relevanceof earnings (book value of equity) increases (decreases) with IFRS adoption.

There are numerous cross-country studies of how mandatory IFRS adoption impactsthe association between accounting information and equity values. These studies includeDevalle et al. (2010), Clarkson et al. (2011), and Agostino, Drago, and Silipo (2011).Including firms listed in Italy, France, U.K., Germany and Spain, Devalle et al. (2010) findthat the value relevance of both book value of equity and earnings decreases in Italy andSpain whereas the value relevance of earnings (book value of equity) increases (decreases)in France and Germany. In contrast, both book value and earnings under IFRS are morevalue relevant than domestic GAAP for U.K. firms. However, using a returns-earningsregression model, they find no significant association in France, Germany and Spain, asignificant improvement in the value relevance for Italy, and similar results in the UK.

Clarkson et al. (2011) examine the value relevance of book value and earnings beforeand after the adoption of IFRS for 15 countries, including both common law and civil lawcountries. Their results contained no convincing evidence that IFRS improves the valuerelevance of the book value of equity and earnings. Agostino et al. (2011), focusingexclusively on European banks, report that IFRS adoption increases the value relevance ofearnings, whereas it reduces the value relevance of book value.

Using a same year design, studies have also explored the association betweenaccounting information and market values using the reconciliation information or restatedfinancial statements. Jarva and Lantto (in press) find no significant change in the valuerelevance of book value and earnings for Finnish firms with the adoption of IFRS.Goodwin et al. (2008) report that IFRS based earnings and book value are not more valuerelevant than those reported under Australian GAAP. Chalmers et al. (2008) compare thevalue relevance of book value of equity and earnings measured using Australian GAAPand IFRS for the same year (2005). They find that both domestic GAAP and IFRS numberssummarize similar amounts of information that is reflected in sample firms' share priceswith the domestic GAAP and IFRS book value of equity measurement reflecting informationrelevant to investors beyond each other. In contrast, only IFRS earnings have significantexplanatory power.

In summary, the above narrative review of value relevance studies highlights the mixedevidence on the financial reporting IFRS adoption effects. Given that the IASB intendsIFRS to be a single set of high quality accounting standards to promote transparent andcomparable information to inform economic decisions in a globalized financial world, weuse meta-analysis to synthesize the value relevance studies. Specifically, we empirical testthe following hypotheses:

Hypothesis 1(a). IFRS adoption increases the association between reported book value ofequity and market value of equity.

Hypothesis 1(b). IFRS adoption increases the association between reported earnings andmarket value of equity.

180 K. Ahmed et al. / The International Journal of Accounting 48 (2013) 173–217

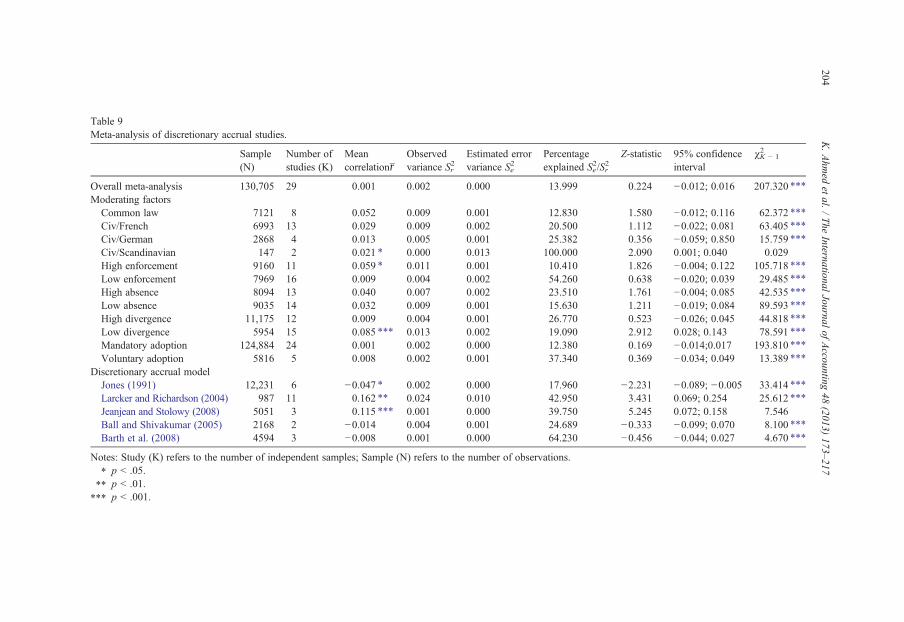

2.2. IFRS adoption and discretionary accruals studies

Studies on the financial reporting effects of IFRS adoption include a focus on theproperties of accounting numbers, particularly properties that proxy for earningsmanagement. Earnings management is viewed as management's intervention in the externalfinancial reporting process with the intent of obtaining private gain via influencing investors'perceptions of the firm's economic performance or influencing the firm's contractualoutcomes (Healy & Wahlen, 1999, Schipper, 1989). The transition to IFRS can reduce thelikelihood of manager's opportunism and earnings management given that the recognitionand disclosure requirements of IFRS relative to some domestic GAAP reduces the scope formanagerial discretion (Leuz, Nanda, &Wysocki, 2003; Ewert &Wagenhofer, 2005; Daske&Gebhardt, 2006). Alternatively, Barth et al. (2008) note that adopting principle-basedaccounting standards, such as IFRS, can increase earnings management given the flexibilityafforded to preparers. The proposition has been empirically tested using discretionaryaccruals as the proxy for earnings management. Comparisons of the level of discretionaryaccruals before and after IFRS adoption, and between countries adopting IFRS and those notadopting, have generated mixed results. For instance, Prather-Kinsey and Shelton (2005)compare South African, U.S. and U.K. firms' discretionary accruals. The sample comprises1583 U.S. firms complying with U.S.-GAAP, 154 South African firms using IFRS and1429 U.K. firms using IFRS from 1999 to 2001. They report that discretionary accruals donot reduce following the adoption of IFRS by South African firms, whereas discretionaryaccruals for U.K. firms applying IFRS are significantly lower than that of the U.S. firmsapplying US-GAAP. Also, using a voluntary adoption setting, Van Tendeloo and Vanstraelen(2005) find that during the period 1999–2001, German firms adopting IFRS have higherdiscretionary accruals relative to German firms reporting under German GAAP.

Callao and Jarne (2010) assess the effect of the transition to IFRS in the E.U. on earningsmanagement practices by comparing discretionary accruals in the periods preceding andimmediately after the mandatory adoption of IFRS. Using a sample of listed firms from 11E.U. countries during 2003 to 2006, they find evidence of an increase in discretionaryaccruals post-IFRS adoption. Contrary findings are reported by Chen, Tang, Jiang, and Lin(2010). Examining discretionary accruals during 2000–2007 for a sample of firms from 15E.U. countries, this study find that discretionary accruals significantly decrease post-IFRSadoption. Houqe, van Zijl, Dunstan, and Karim (2012) using data from 46 countries findthat discretionary accruals have not reduced following mandatory adoption of IFRS.

Within-country studies have also produced inconsistent results. Iatridis (2010) investigateswhether the implementation of IFRS in the U.K. reduces earnings management and findsevidence of such. Iatridis and Rouvolis (2010), who study Greek firms, do not find areduction in earnings management following the adoption of IFRS. Kabir, Laswad, and Islam(2010) focus on the effect of IFRS adoption on earnings management for firms on the NewZealand Stock Exchange. They use a 2000 to 2009 period and find that discretionary accrualsare significantly higher under IFRS than under New Zealand GAAP. In contrast, evidence forFrench companies suggests that mandatory IFRS adoption reduces earnings management(Zéghal et al., 2011).

Similar to the review of value relevance studies, the narrative review of the associationbetween earnings management and IFRS adoption highlights inconsistent findings. Given

181K. Ahmed et al. / The International Journal of Accounting 48 (2013) 173–217

that IFRS is intended to be a single set of high quality accounting standards to promotetransparent and comparable information to inform economic decisions, we propose thefollowing hypothesis for empirical testing using meta-analysis:

Hypothesis 2. IFRS adoption decreases discretionary accruals.

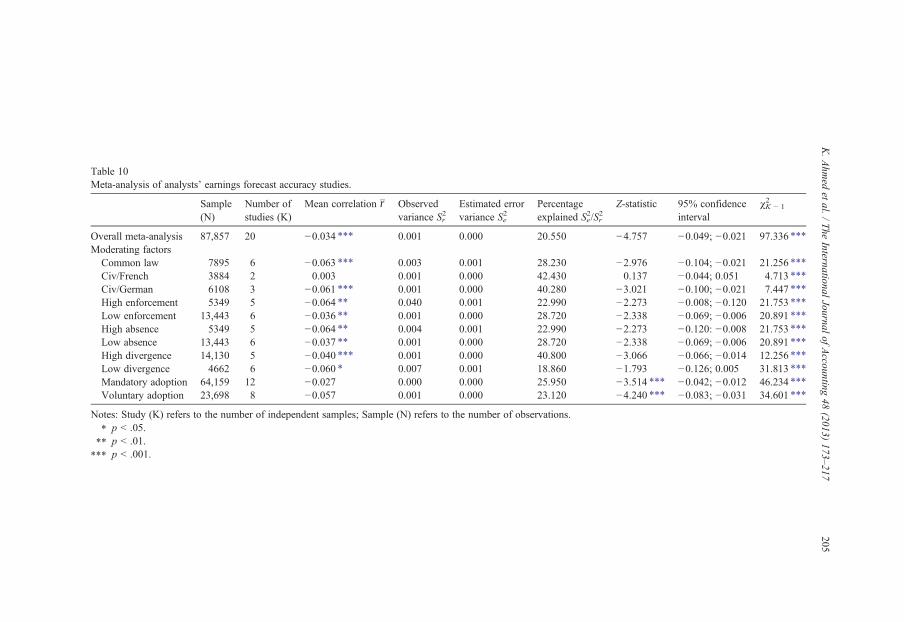

2.3. IFRS adoption and analysts' earnings forecasts

Studies examining analysts' earnings forecasts pre- and post-IFRS adoption arecategorized by Brüggemann et al. (2012) as providing indirect evidence of capital-marketeffects associated with an accounting regime change. Financial analysts are regarded asimportant information intermediaries in capital markets because they provide investors withfuture earnings forecasts (Beaver, 1998). Financial statements represent a fundamental sourceof information used by analysts to make future earnings forecasts. Therefore, financial analystswill have a higher quality information set to inform their predictions if the accounting principlesused to prepare financial statements are transparent and comparable in terms of disclosure andmeasurement rules. This should increase the accuracy of their earnings forecasts, as well.

Relative to some domestic GAAP, IFRS permits or requires more fair value measurementand disclosures.7 These regulations should improve the information environment, the relevanceof accounting information, and predictability. Empirical studies examining the associationbetween IFRS adoption and analysts' earnings forecast accuracy have been conducted overtime and in various jurisdictions (e.g., Ashbaugh & Pincus, 2001; Cuijpers & Buijink, 2005;Hodgdon, Tondkar, Harless, &Adhikari, 2008; Byard et al., 2011; Cheong&AlMasum, 2010;Chalmers et al., 2012; Horton et al., 2012; Jönsson et al., 2012; Kim & Shi, 2012). The resultsgenerally support higher forecast accuracy subsequent to IFRS adoption.

Ashbaugh and Pincus (2001) examine the relationship between the voluntary adoptionof IFRS for a sample of European, Canadian, and Australian firms between 1990 and1993. Their findings show significant improvement in the analysts' forecast accuracy afterthe voluntary adoption of IFRS standards. Hodgdon et al. (2008) also find firms fromcommon and code law countries have better analysts' forecast accuracy followingvoluntary application of IFRS. In contrast, Cuijpers and Buijink (2005) studying E.U.firms report higher uncertainty among analysts (larger forecast errors) for firms using IFRSrelative to firms using domestic GAAP.8 Similarly, Jönsson et al. (2012), studying around2500 firms across five European countries find forecast accuracy is unaffected by IFRS.Byard et al.'s (2011) findings, using a sample of firms from E.U. countries, document thatboth mandatory and voluntary IFRS adoptions are associated with reduced analysts'

7 Standards permitting or requiring fair value include IAS 16 Property, Plant and Equipment, IAS 40 InvestmentProperty, IFRS 5 No-current Assets Held for Sale and Discontinued Operations, IFRS 8 Operating Segments, IAS36 Impairment of Assets, IAS 37 Provisions, Contingent Liabilities and Contingent Assets, IAS 38 IntangibleAssets, and IAS39 Financial Instruments Recognition and Measurement (replaced by IFRS 9 FinancialInstruments).8 The authors note that this may be due to a time lag effect with the benefits of a richer information environment

taking time to permeate through the investment community.

182 K. Ahmed et al. / The International Journal of Accounting 48 (2013) 173–217

forecasts errors although the results differ according to the countries' enforcement regimesand the extent to which IFRS differ from local GAAP. Similar findings have been reportedby Jiao, Koning, Mertens, and Roosenboom (2011) on the impact of mandatory IFRSadoption on analysts' forecasts errors.

Within the Asia-pacific region (Australia, New Zealand and Hong Kong), Cheong et al.(2010) find that IFRS adoption is negatively associated with analysts' earnings errors overa period from 2001 to 2008. Cheong and Masum (2010), Cotter, Tarca, and Wee (2012),and Chalmers et al. (2012) restrict their studies to Australian firms. All three studies findthat IFRS adoption improves analysts' earnings forecast quality.

The narrative review of the association between analysts forecast accuracy and IFRSadoption generally shows less variability in the findings compared to value relevance anddiscretionary accrual studies. Further, most studies report a positive association betweenIFRS adoption and analysts' earnings accuracy. Therefore, we propose the followinghypothesis for empirical testing using meta-analysis:

Hypothesis 3. IFRS adoption improves analysts earnings forecast accuracy.

2.4. Factors moderating the IFRS adoption effects

The preceding literature reviews demonstrates inconsistency in studies' findings of thefinancial reporting effects and, to a lesser extent, capital market effects, of IFRS adoption.There are various factors espoused in the literature that could be contributing to theheterogeneity in the results. Using meta-analysis, it is possible to quantitatively determineif these factors, referred to as moderating factors, influence the IFRS adoption effectsreported. As accounting is the product of its environment, prior research suggests suchdivergence in results are due to jurisdictional differences. For example, Ball (1995) andNobes (1998) contend that accounting systems and the level of market transparency arefunctions of the nature of the legal systems and financing of firms in a country. Theseviews have been broadly assessed in terms of whether a country has a code or common-lawlegal origin. LaPorta, Lopez-de-Silanes, and Shleifer (1998) classify the origin of lawsgoverning investor protection as common law, German civil law, French civil law andScandinavian civil law. They report that investor protection is stronger for common lawjurisdictions, weaker for French civil law jurisdictions with Scandinavian and Germancivil law within this range. The extent of investor protection can influence the benefitsassociated with IFRS adoption and this can be a factor moderating the IFRS adoptioneffects. For example, Barth et al. (2008) find that the value relevance of financial reports islower for countries where: the financial systems are bank oriented (as opposed to marketoriented); private sector bodies are not involved in the accounting standard-setting process;accounting practices follow the Continental model (as opposed to the British–Americanmodel); the tax book conformity is greater; and spending on auditing services is relativelylow. Accordingly, we group the value relevance, discretionary accruals, and analysts'earnings forecast studies by legal origin to statistically test if this is a moderating factor.

In addition to our meta-analysis of studies grouped according to a country's legal origin,we conduct an analysis to assess if a country's level of accounting and auditing enforcement(Enforcement) and differences between a country's domestic accounting standards and

183K. Ahmed et al. / The International Journal of Accounting 48 (2013) 173–217

IFRS (Divergence and Absence) moderate the IFRS adoption effects for value relevance,discretionary accruals, and analysts' earnings forecasts accuracy studies. The financialreporting benefits of IFRS adoption can be impeded by the level of accounting and auditingenforcement in a country (Landsman, Maydew, & Thornock, 2012; Zeff, 2007). Ball (2006)contends that a ‘veneer of uniformity’ conceals differences in IFRS implementation. Using anenforcement proxy constructed by Preiato, Brown, and Tarca (2010) we group studies intohigh and low enforcement groups and meta-analyze these groups.9

Similarly, the benefits of IFRS adoption in isolation of changing other institutionalfactors, such as the capital market development and legal environment, may not enhancefinancial reporting quality (Ding, Hope, Jeanjean, & Stolowy, 2007). Ding et al. (2007)using indices of differences between domestic accounting standards and IFRS, absence anddivergence,10 find that market synchronicity (fraction of stocks that move in the samedirection) varies depending on the level of absence and divergence between domesticGAAP and IFRS. Using Ding et al.'s (2007) absence and divergence indices, we groupstudies into high and low absence and divergence groups and meta-analyze these groups.To partition studies into high and low groups for the enforcement, absence and divergencemoderating factors, we compute the median index value and then we sub-group studieswith respect to these moderator variables. When the score attributed to each study orcountry is inferior (superior) to the median, the group is categorized as having low (high)accounting and auditing enforcement, absence and divergence.

Jeanjean and Stolowy (2008) argue that firms voluntarily adopting IFRS suffer from asample selection bias as only firms seeing an advantage in this accounting change wouldimplement it. This selection bias has the potential to overestimate the expected benefitsof the transition to IFRS, which are inferred solely from studying firms that find it in theirinterest to adopt IFRS before its mandatory application. Further, Platikanova (2009)suggests that investors only partially anticipate IFRS effects for voluntary adopters andDaske, Hail, Leuz, and Verdi (2008) find the capital market effects for voluntary adoptersvaries according to the seriousness of the adoption. Therefore, as voluntary versusmandatory adoption of IFRS may moderate the IFRS effects, we test for this moderatingeffect in our sample of value relevance, discretionary accruals and analysts' earnings forecastaccuracy studies.

Studies investigating the value relevance of earnings pre- and post-IFRS adoptionemploy a price model (stock price regressed on earnings per share) and/or a return model(returns regressed on scaled earnings variables). Kothari and Zimmerman (1995) empiricallyfind that that price models' earnings response coefficients are less biased while return modelshave less serious econometric problems than price models. Van der Meulen, Gaeremynck,

9 Preiato et al. (2010) devise an accounting and auditing enforcement index for 51 countries in 2002, 2005 and2008. The index includes 11 items relating to auditing quality and 7 items relating to a country's enforcementbody. Details on the index are available in Appendix 2, pp.49–50 of their paper.10 Absence measures the extent to which the rules regarding certain accounting issues are missing in domesticaccounting standards but are covered in international accounting standards. Divergence applies in circumstanceswhere the rules regarding the same accounting issue differ in domestic accounting standards and internationalaccounting standards (Ding et al., 2007). The absence and divergence indices for various countries are available inDing et al. (2007) (Table 1, pp. 156 and 157).

184 K. Ahmed et al. / The International Journal of Accounting 48 (2013) 173–217

and Willekens (2007) suggest price earning regressions do not take into account how marketprices react to positive and negative earnings. Consequently, we test if the mixed results forthe IFRS adoption effects on the value relevance of earnings are due to model specification,by meta-analyzing our sample of studies classified according to their use of a price or returnmodel.

Studies of IFRS adoption effects on discretionary accruals employ various models toseparate accruals into their non-discretionary and discretionary components. We classify oursample of discretionary accrual studies according to the model used to measure the constructof interest. The models used are those presented in Jones (1991), Larcker and Richardson(2004), Jeanjean and Stolowy (2008), Kothari, Leone, and Wasley (2005), and Barth et al.(2008). Our tests seeks to determine if the method used to measure discretionary accruals is amoderating factor in the discretionary accruals IFRS adoption effect findings.

In sum, we hypothesize that the association between IFRS adoption and value relevance,discretionary accruals and analysts' forecast accuracy is moderated by differences associatedwith a jurisdiction's legal origin, accounting and auditing enforcement regime and the extentto which domestic GAAP is congruent with IFRS. We also hypothesize that the adoptionincentive — voluntary or mandatory — moderates the associations. Acknowledging thatdesign choices can moderate the empirical findings, the moderating effect of using a price orreturn model is also tested when meta-analyzing value relevance studies. For discretionaryaccrual studies, the moderating effect of the model used to estimate discretionary accruals isinvestigated.

3. Data

Several combinations of keywords are used to obtain relevant studies concerning IFRSadoption effects and 1) value relevance of book value of equity and earnings, 2) discretionaryaccruals, and 3) analysts' earnings forecasts for our analysis.11 Keywords used include ‘IFRS/IAS adoption and value relevance’, ‘IAS/IFRS adoption and earnings management ordiscretionary accruals’ and ‘IAS/IFRS adoption and analysts’ forecasts accuracy/errors indifferent editorial sources including ABI Inform, Blackwell, EBSCO, JSTOR, Emerald,Science Direct, Springer, Taylor and Francis, and SSRN. Further, we also consult numerousaccounting and finance journals that deal with these topics. We also consulted references inthe collected papers to identify other empirical studies relevant to our topic.

Our initial sample consists of 88 papers after ensuring that an earlier version of samestudy had not been included. Eleven papers are eliminated as they only report descriptiveinformation and do not contain sufficient statistical information for further analysis.12

Further, as our meta-analysis is restricted to value relevance, discretionary accruals, andanalysts forecast studies, we eliminated a further 20 empirical papers, reducing the sample

11 It is beyond the scope of this paper to include studies investigating the cost of capital, liquidity and earningspersistence consequences of IFRS adoption or studies examining the effect of IFRS on other consequences such asinformation content (Landsman et al., 2012) and earnings smoothness (Capkun, Collins, & Jeanjean, 2012).12 For example, studies reporting only the coefficients without the exact probability value or associated t-statistic(e.g. Aharony, Barniv, & Falk, 2010) are eliminated.

185K. Ahmed et al. / The International Journal of Accounting 48 (2013) 173–217

to 57 papers yielding 96 independent samples for accumulation and analysis. Table 1summarizes the sample selection process.

It is common for a single primary study to contribute multiple effect sizes. Many studiesestimate regressions using sub-samples of firms and use alternative measures of thedependent and independent variables. Multiple effect sizes can be dealt with by calculatingan average effect size for each study so that each primary study contributes only one effectsize. However, this method underestimates the degree of heterogeneity within studies(Cheung & Chan, 2004). The average effect size is “conceptually ambiguous” whenmoderator variables vary within as well as across studies (Hunter et al., 1982). Therefore,we compute multiple effect sizes for each study and use them as moderating factors forfurther analysis.

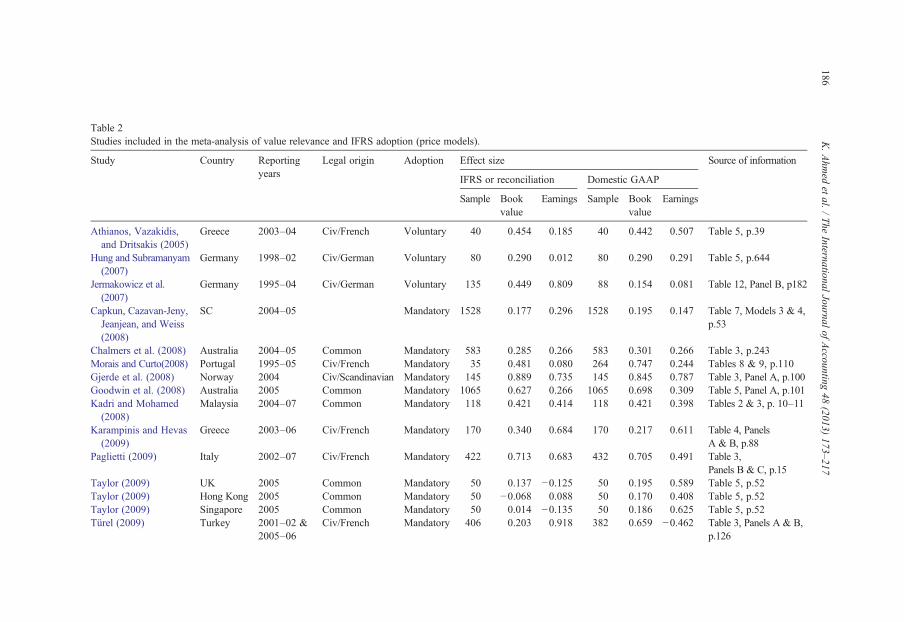

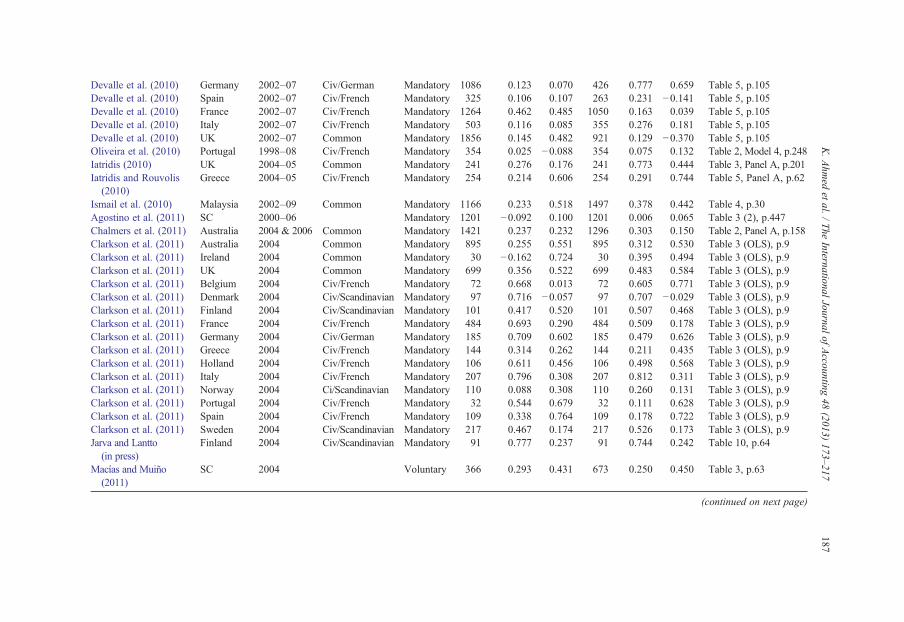

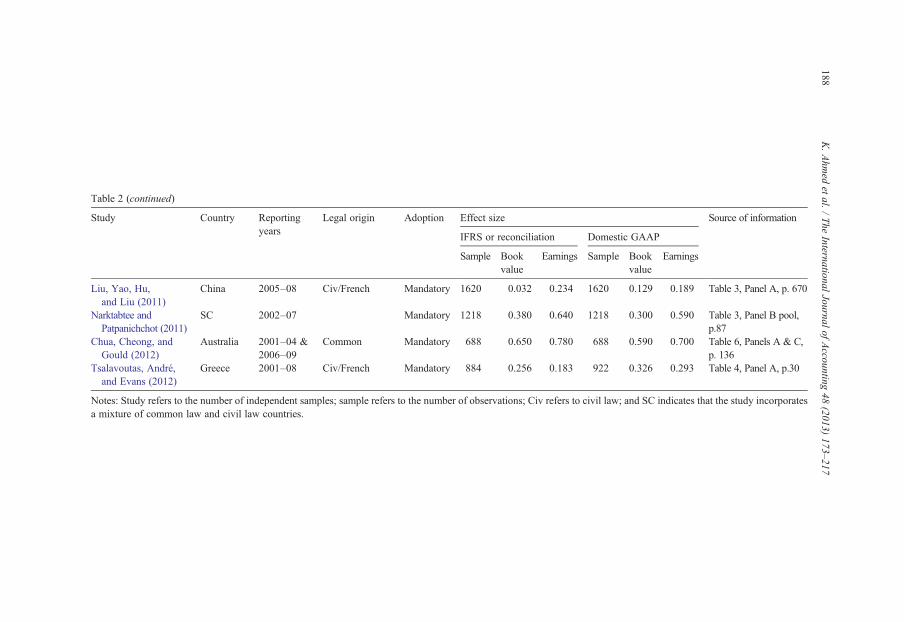

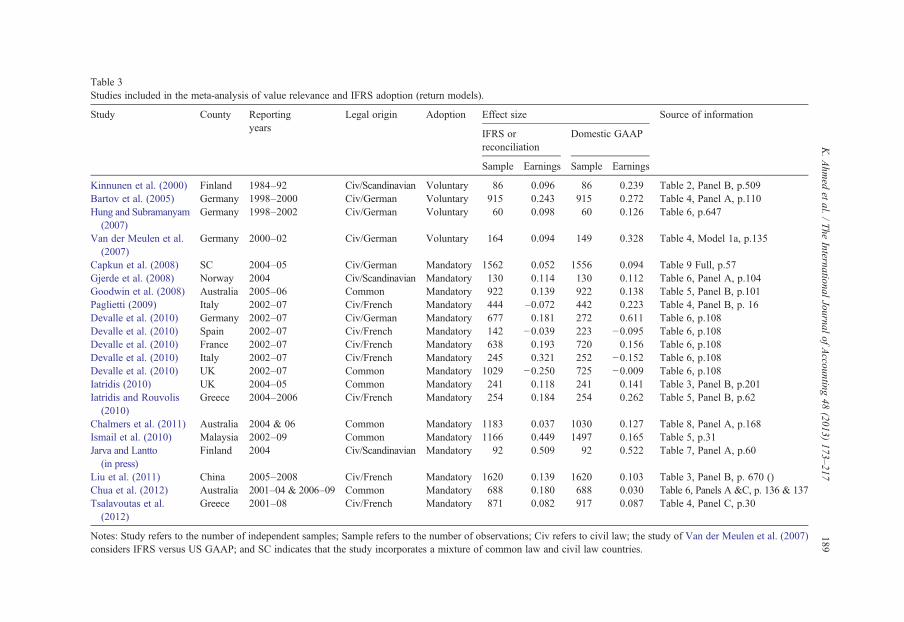

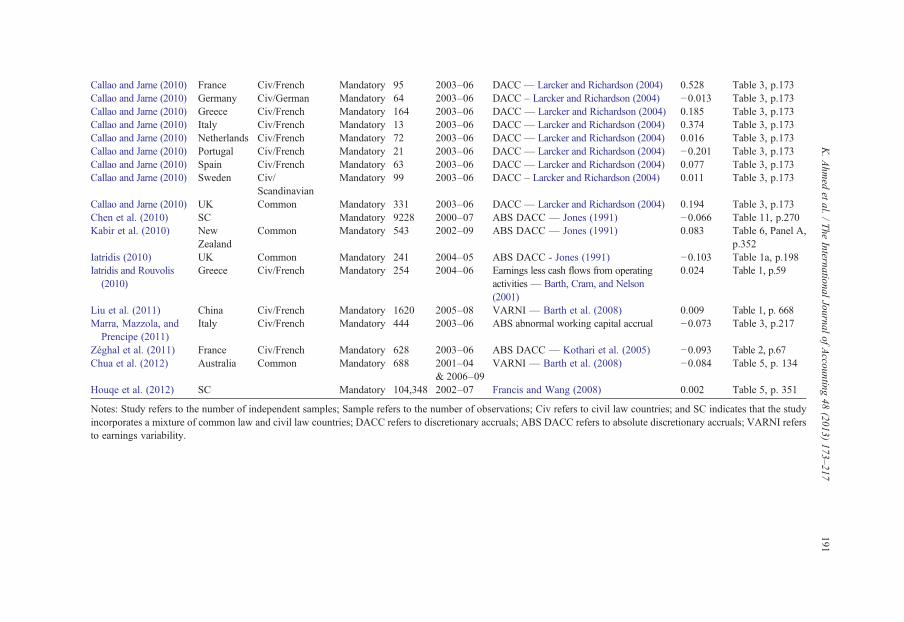

Tables 2–5 present summaries of the studies included in the meta-analysis. Tables 2 and 3detail the price and return model value relevant studies, while Table 4 lists the discretionaryaccruals studies meta-analyzed. Table 5 details the studies investigating analysts' earningsforecast accuracy and IFRS adoption that are included in our meta-analysis.13 For each studylisted, the following attributes are included: year of publication, country focus, whether IFRSadoption is voluntary or mandatory, the number of sample firms, the reporting years examined,and the effect size measure (r) pre- and post-IFRS adoption. Additionally, for discretionaryaccrual studies (Table 4), the model used to measure discretionary accruals is noted.

4. Meta-analysis techniques

Some critics have suggested that narrative reviews suffer because there are notstandardized rules about how to generalize from individual results for a particular researchtopic (e.g., Glass, 1976; Hunter et al., 1982; Rosenthal, 1991). Given these limitations,meta-analysis can be used to overcome the problem of reduced statistical power in studieswith small sample sizes and allows more accurate data analysis relative to narrativereviews. We follow the meta-analysis technique developed by Hunter et al. (1982) andHunter and Schmidt (2000) and Rosenthal (1991) in order to draw logical conclusions frompapers related to IFRS adoption and financial reporting quality. The meta-analysis techniquerequires the computation of the effect size 14 to measure the magnitude of the associationbetween the dependent variables (value relevance, discretionary accruals and analysts'forecast accuracy in our study) and the independent variable (IFRS adoption). For studiesreporting the coefficient of correlation (r), this statistic is used to measure the effect size.

When only t-statistic or z-statistic results are reported, r is computed asffiffiffiffiffiffiffiffiffiffiffiffiffi

t2

t2þdfð Þr

or ZffiffiffiN

p where

df is the residual degrees of freedom computed using the sample size and number ofparameters estimated in a regression. According to Hunter and Schmidt (2000), three steps

13 Most of the value relevance studies assess the value relevance before and after the adoption of IFRS, whilediscretionary and analyst forecasts studies report the association within a single regression model.14 See Rosenthal (1991) for different methods to compute effect size from reported statistics in published papers.

Table 2Studies included in the meta-analysis of value relevance and IFRS adoption (price models).

Study Country Reportingyears

Legal origin Adoption Effect size Source of information

IFRS or reconciliation Domestic GAAP

Sample Bookvalue

Earnings Sample Bookvalue

Earnings

Athianos, Vazakidis,and Dritsakis (2005)

Greece 2003–04 Civ/French Voluntary 40 0.454 0.185 40 0.442 0.507 Table 5, p.39

Hung and Subramanyam(2007)

Germany 1998–02 Civ/German Voluntary 80 0.290 0.012 80 0.290 0.291 Table 5, p.644

Jermakowicz et al.(2007)

Germany 1995–04 Civ/German Voluntary 135 0.449 0.809 88 0.154 0.081 Table 12, Panel B, p182

Capkun, Cazavan-Jeny,Jeanjean, and Weiss(2008)

SC 2004–05 Mandatory 1528 0.177 0.296 1528 0.195 0.147 Table 7, Models 3 & 4,p.53

Chalmers et al. (2008) Australia 2004–05 Common Mandatory 583 0.285 0.266 583 0.301 0.266 Table 3, p.243Morais and Curto(2008) Portugal 1995–05 Civ/French Mandatory 35 0.481 0.080 264 0.747 0.244 Tables 8 & 9, p.110Gjerde et al. (2008) Norway 2004 Civ/Scandinavian Mandatory 145 0.889 0.735 145 0.845 0.787 Table 3, Panel A, p.100Goodwin et al. (2008) Australia 2005 Common Mandatory 1065 0.627 0.266 1065 0.698 0.309 Table 5, Panel A, p.101Kadri and Mohamed(2008)

Malaysia 2004–07 Common Mandatory 118 0.421 0.414 118 0.421 0.398 Tables 2 & 3, p. 10–11

Karampinis and Hevas(2009)

Greece 2003–06 Civ/French Mandatory 170 0.340 0.684 170 0.217 0.611 Table 4, PanelsA & B, p.88

Paglietti (2009) Italy 2002–07 Civ/French Mandatory 422 0.713 0.683 432 0.705 0.491 Table 3,Panels B & C, p.15

Taylor (2009) UK 2005 Common Mandatory 50 0.137 −0.125 50 0.195 0.589 Table 5, p.52Taylor (2009) Hong Kong 2005 Common Mandatory 50 −0.068 0.088 50 0.170 0.408 Table 5, p.52Taylor (2009) Singapore 2005 Common Mandatory 50 0.014 −0.135 50 0.186 0.625 Table 5, p.52Türel (2009) Turkey 2001–02 &

2005–06Civ/French Mandatory 406 0.203 0.918 382 0.659 −0.462 Table 3, Panels A & B,

p.126

186K.Ahm

edet

al./The

InternationalJournal

ofAccounting

48(2013)

173–217

Devalle et al. (2010) Germany 2002–07 Civ/German Mandatory 1086 0.123 0.070 426 0.777 0.659 Table 5, p.105Devalle et al. (2010) Spain 2002–07 Civ/French Mandatory 325 0.106 0.107 263 0.231 −0.141 Table 5, p.105Devalle et al. (2010) France 2002–07 Civ/French Mandatory 1264 0.462 0.485 1050 0.163 0.039 Table 5, p.105Devalle et al. (2010) Italy 2002–07 Civ/French Mandatory 503 0.116 0.085 355 0.276 0.181 Table 5, p.105Devalle et al. (2010) UK 2002–07 Common Mandatory 1856 0.145 0.482 921 0.129 −0.370 Table 5, p.105Oliveira et al. (2010) Portugal 1998–08 Civ/French Mandatory 354 0.025 −0.088 354 0.075 0.132 Table 2, Model 4, p.248Iatridis (2010) UK 2004–05 Common Mandatory 241 0.276 0.176 241 0.773 0.444 Table 3, Panel A, p.201Iatridis and Rouvolis

(2010)Greece 2004–05 Civ/French Mandatory 254 0.214 0.606 254 0.291 0.744 Table 5, Panel A, p.62

Ismail et al. (2010) Malaysia 2002–09 Common Mandatory 1166 0.233 0.518 1497 0.378 0.442 Table 4, p.30Agostino et al. (2011) SC 2000–06 Mandatory 1201 −0.092 0.100 1201 0.006 0.065 Table 3 (2), p.447Chalmers et al. (2011) Australia 2004 & 2006 Common Mandatory 1421 0.237 0.232 1296 0.303 0.150 Table 2, Panel A, p.158Clarkson et al. (2011) Australia 2004 Common Mandatory 895 0.255 0.551 895 0.312 0.530 Table 3 (OLS), p.9Clarkson et al. (2011) Ireland 2004 Common Mandatory 30 −0.162 0.724 30 0.395 0.494 Table 3 (OLS), p.9Clarkson et al. (2011) UK 2004 Common Mandatory 699 0.356 0.522 699 0.483 0.584 Table 3 (OLS), p.9Clarkson et al. (2011) Belgium 2004 Civ/French Mandatory 72 0.668 0.013 72 0.605 0.771 Table 3 (OLS), p.9Clarkson et al. (2011) Denmark 2004 Civ/Scandinavian Mandatory 97 0.716 −0.057 97 0.707 −0.029 Table 3 (OLS), p.9Clarkson et al. (2011) Finland 2004 Civ/Scandinavian Mandatory 101 0.417 0.520 101 0.507 0.468 Table 3 (OLS), p.9Clarkson et al. (2011) France 2004 Civ/French Mandatory 484 0.693 0.290 484 0.509 0.178 Table 3 (OLS), p.9Clarkson et al. (2011) Germany 2004 Civ/German Mandatory 185 0.709 0.602 185 0.479 0.626 Table 3 (OLS), p.9Clarkson et al. (2011) Greece 2004 Civ/French Mandatory 144 0.314 0.262 144 0.211 0.435 Table 3 (OLS), p.9Clarkson et al. (2011) Holland 2004 Civ/French Mandatory 106 0.611 0.456 106 0.498 0.568 Table 3 (OLS), p.9Clarkson et al. (2011) Italy 2004 Civ/French Mandatory 207 0.796 0.308 207 0.812 0.311 Table 3 (OLS), p.9Clarkson et al. (2011) Norway 2004 Ci/Scandinavian Mandatory 110 0.088 0.308 110 0.260 0.131 Table 3 (OLS), p.9Clarkson et al. (2011) Portugal 2004 Civ/French Mandatory 32 0.544 0.679 32 0.111 0.628 Table 3 (OLS), p.9Clarkson et al. (2011) Spain 2004 Civ/French Mandatory 109 0.338 0.764 109 0.178 0.722 Table 3 (OLS), p.9Clarkson et al. (2011) Sweden 2004 Civ/Scandinavian Mandatory 217 0.467 0.174 217 0.526 0.173 Table 3 (OLS), p.9Jarva and Lantto

(in press)Finland 2004 Civ/Scandinavian Mandatory 91 0.777 0.237 91 0.744 0.242 Table 10, p.64

Macías and Muiño(2011)

SC 2004 Voluntary 366 0.293 0.431 673 0.250 0.450 Table 3, p.63

(continued on next page)

187K.Ahm

edet

al./The

InternationalJournal

ofAccounting

48(2013)

173–217

Table 2 (continued)

Study Country Reportingyears

Legal origin Adoption Effect size Source of information

IFRS or reconciliation Domestic GAAP

Sample Bookvalue

Earnings Sample Bookvalue

Earnings

Liu, Yao, Hu,and Liu (2011)

China 2005–08 Civ/French Mandatory 1620 0.032 0.234 1620 0.129 0.189 Table 3, Panel A, p. 670

Narktabtee andPatpanichchot (2011)

SC 2002–07 Mandatory 1218 0.380 0.640 1218 0.300 0.590 Table 3, Panel B pool,p.87

Chua, Cheong, andGould (2012)

Australia 2001–04 &2006–09

Common Mandatory 688 0.650 0.780 688 0.590 0.700 Table 6, Panels A & C,p. 136

Tsalavoutas, André,and Evans (2012)

Greece 2001–08 Civ/French Mandatory 884 0.256 0.183 922 0.326 0.293 Table 4, Panel A, p.30

Notes: Study refers to the number of independent samples; sample refers to the number of observations; Civ refers to civil law; and SC indicates that the study incorporatesa mixture of common law and civil law countries.

188K.Ahm

edet

al./The

InternationalJournal

ofAccounting

48(2013)

173–217

Table 3Studies included in the meta-analysis of value relevance and IFRS adoption (return models).

Study County Reportingyears

Legal origin Adoption Effect size Source of information

IFRS orreconciliation

Domestic GAAP

Sample Earnings Sample Earnings

Kinnunen et al. (2000) Finland 1984–92 Civ/Scandinavian Voluntary 86 0.096 86 0.239 Table 2, Panel B, p.509Bartov et al. (2005) Germany 1998–2000 Civ/German Voluntary 915 0.243 915 0.272 Table 4, Panel A, p.110Hung and Subramanyam(2007)

Germany 1998–2002 Civ/German Voluntary 60 0.098 60 0.126 Table 6, p.647

Van der Meulen et al.(2007)

Germany 2000–02 Civ/German Voluntary 164 0.094 149 0.328 Table 4, Model 1a, p.135

Capkun et al. (2008) SC 2004–05 Civ/German Mandatory 1562 0.052 1556 0.094 Table 9 Full, p.57Gjerde et al. (2008) Norway 2004 Civ/Scandinavian Mandatory 130 0.114 130 0.112 Table 6, Panel A, p.104Goodwin et al. (2008) Australia 2005–06 Common Mandatory 922 0.139 922 0.138 Table 5, Panel B, p.101Paglietti (2009) Italy 2002–07 Civ/French Mandatory 444 –0.072 442 0.223 Table 4, Panel B, p. 16Devalle et al. (2010) Germany 2002–07 Civ/German Mandatory 677 0.181 272 0.611 Table 6, p.108Devalle et al. (2010) Spain 2002–07 Civ/French Mandatory 142 −0.039 223 −0.095 Table 6, p.108Devalle et al. (2010) France 2002–07 Civ/French Mandatory 638 0.193 720 0.156 Table 6, p.108Devalle et al. (2010) Italy 2002–07 Civ/French Mandatory 245 0.321 252 −0.152 Table 6, p.108Devalle et al. (2010) UK 2002–07 Common Mandatory 1029 −0.250 725 −0.009 Table 6, p.108Iatridis (2010) UK 2004–05 Common Mandatory 241 0.118 241 0.141 Table 3, Panel B, p.201Iatridis and Rouvolis(2010)

Greece 2004–2006 Civ/French Mandatory 254 0.184 254 0.262 Table 5, Panel B, p.62

Chalmers et al. (2011) Australia 2004 & 06 Common Mandatory 1183 0.037 1030 0.127 Table 8, Panel A, p.168Ismail et al. (2010) Malaysia 2002–09 Common Mandatory 1166 0.449 1497 0.165 Table 5, p.31Jarva and Lantto(in press)

Finland 2004 Civ/Scandinavian Mandatory 92 0.509 92 0.522 Table 7, Panel A, p.60

Liu et al. (2011) China 2005–2008 Civ/French Mandatory 1620 0.139 1620 0.103 Table 3, Panel B, p. 670 ()Chua et al. (2012) Australia 2001–04 & 2006–09 Common Mandatory 688 0.180 688 0.030 Table 6, Panels A &C, p. 136 & 137Tsalavoutas et al.(2012)

Greece 2001–08 Civ/French Mandatory 871 0.082 917 0.087 Table 4, Panel C, p.30

Notes: Study refers to the number of independent samples; Sample refers to the number of observations; Civ refers to civil law; the study of Van der Meulen et al. (2007)considers IFRS versus US GAAP; and SC indicates that the study incorporates a mixture of common law and civil law countries.

189K.Ahm

edet

al./The

InternationalJournal

ofAccounting

48(2013)

173–217

Table 4Studies included in the meta-analysis of discretionary accrual and IFRS adoption.

Study Country Legal origin Adoption Sample Reportingyears

Accrual proxy Effect size Source ofinformation

IFRSadoption

Prather-Kinsey andShelton (2005)

South Africa Common Voluntary 154 1999–01 ABS DACC — Jones (1991) 0.028 Table 3, p.165

Prather-Kinsey andShelton (2005)

UK Common Voluntary 1429 1999–01 ABS DACC — Jones (1991) −0.055 Table 3, p.165

Van Tendeloo andVanstraelen (2005)

Germany Civ/German Voluntary 636 1999–01 ABS DACC — Jones (1991) 0.110 Table 8, p.172

Jeanjean and Stolowy(2008)

Australia Common Mandatory 1933 2002–06 Income scaled by total assets 0.065 Table 2, p.489

Jeanjean and Stolowy(2008)

France Civ/French Mandatory 1316 2002–06 Income scaled by total assets 0.134 Table 2, p.489

Jeanjean and Stolowy(2008)

UK Common Mandatory 1802 2002–06 Income scaled by total assets 0.150 Table 2, p.489

Guenther, Gegenfurtner,Kaserer, andAchleitner (2009)

Germany Civ/German Voluntary 1311 1998–2004 ABS DACC— Ball and Shivakumar (2005) 0.035 Table 5, Panel B,p.42

Guenther et al. (2009) Germany Civ/German Mandatory 857 2005–08 ABS DACC - Ball and Shivakumar (2005) −0.090 Table 5, Panel C,p.42

Zhou, Xiong, andGanguli. (2009)

China Civ/French Voluntary 2286 1994–00 VARNI – Barth et al. (2008) 0.002 Table 3, p.51

Callao and Jarne (2010) Belgium Civ/French Mandatory 17 2003–06 DACC— Larcker and Richardson (2004) 0.388 Table 3, p.173Callao and Jarne (2010) Finland Civ/

ScandinavianMandatory 48 2003–06 DACC – Larcker and Richardson (2004) 0.041 Table 3, p.173

190K.Ahm

edet

al./The

InternationalJournal

ofAccounting

48(2013)

173–217

Callao and Jarne (2010) France Civ/French Mandatory 95 2003–06 DACC— Larcker and Richardson (2004) 0.528 Table 3, p.173Callao and Jarne (2010) Germany Civ/German Mandatory 64 2003–06 DACC – Larc er and Richardson (2004) −0.013 Table 3, p.173Callao and Jarne (2010) Greece Civ/French Mandatory 164 2003–06 DACC — La ker and Richardson (2004) 0.185 Table 3, p.173Callao and Jarne (2010) Italy Civ/French Mandatory 13 2003–06 DACC— La ker and Richardson (2004) 0.374 Table 3, p.173Callao and Jarne (2010) Netherlands Civ/French Mandatory 72 2003–06 DACC— La ker and Richardson (2004) 0.016 Table 3, p.173Callao and Jarne (2010) Portugal Civ/French Mandatory 21 2003–06 DACC— La ker and Richardson (2004) −0.201 Table 3, p.173Callao and Jarne (2010) Spain Civ/French Mandatory 63 2003–06 DACC— La ker and Richardson (2004) 0.077 Table 3, p.173Callao and Jarne (2010) Sweden Civ/

ScandinavianMandatory 99 2003–06 DACC – Larc er and Richardson (2004) 0.011 Table 3, p.173

Callao and Jarne (2010) UK Common Mandatory 331 2003–06 DACC— La ker and Richardson (2004) 0.194 Table 3, p.173Chen et al. (2010) SC Mandatory 9228 2000–07 ABS DACC Jones (1991) −0.066 Table 11, p.270Kabir et al. (2010) New

ZealandCommon Mandatory 543 2002–09 ABS DACC Jones (1991) 0.083 Table 6, Panel A,

p.352Iatridis (2010) UK Common Mandatory 241 2004–05 ABS DACC ones (1991) −0.103 Table 1a, p.198Iatridis and Rouvolis

(2010)Greece Civ/French Mandatory 254 2004–06 Earnings less c sh flows from operating

activities— B th, Cram, and Nelson(2001)

0.024 Table 1, p.59

Liu et al. (2011) China Civ/French Mandatory 1620 2005–08 VARNI — B th et al. (2008) 0.009 Table 1, p. 668Marra, Mazzola, and

Prencipe (2011)Italy Civ/French Mandatory 444 2003–06 ABS abnorma working capital accrual −0.073 Table 3, p.217

Zéghal et al. (2011) France Civ/French Mandatory 628 2003–06 ABS DACC Kothari et al. (2005) −0.093 Table 2, p.67Chua et al. (2012) Australia Common Mandatory 688 2001–04

& 2006–09VARNI — B th et al. (2008) −0.084 Table 5, p. 134

Houqe et al. (2012) SC Mandatory 104,348 2002–07 Francis and W ng (2008) 0.002 Table 5, p. 351

Notes: Study refers to the number of independent samples; Sample refers to the number of observations; Civ efers to civil law countries; and SC indicates that the studyincorporates a mixture of common law and civil law countries; DACC refers to discretionary accruals; ABS D CC refers to absolute discretionary accruals; VARNI refersto earnings variability.

191K.Ahm

edet

al./The

InternationalJournal

ofAccounting

48(2013)

173–217

krcrcrcrcrck

rc——

- Jaar

arl

—ar

a

rA

Table 5Studies included in the meta-analysis of analysts' earnings forecast accuracy and IFRS adoption.

Study Country Reportingyears

Legal Origin Adoption Sample Forecastaccuracy

Effect size Source of information

IFRS adoption

Ashbaugh and Pincus(2001)

SC 1990–93 Voluntary 136 AFE −0.262 Table 5, Panel B, p.428

Ashbaugh and Pincus(2001)

Canada 1990–93 Common Voluntary 24 AFE −0.057 Table 5, Panel C, p.428

Ernstberger et al.(2008) a

Germany 1998–2004 Civ/German Voluntary 2104 AFE −0.062 Table 9, Model 2 a, p.44

Hodgdon et al. (2008) SC 1999–2000 Voluntary 805 AFE −0.172 Table 5, p.10Cheong and Masum

(2010)Australia 2002–07 Common Mandatory 381 AFE −0.182 Table 3, Eq. (8), p.80

Cheong et al. (2010) Australia, Hong Kongand New Zealand

2001–08 Common Mandatory 456 AFE −0.103 Table 5, Eq. (3), p.137

Cotter et al. (2012) Australia 2003–07 Common Mandatory 512 AFE −0.228 Table 4,Model 1, p.17Glaum, Baetge,

Grothe, andOberdorster (2011)

Germany 1997–2005 Civ/German Voluntary 1908 AFE −0.105 Table 5, p. 20

192K.Ahm

edet

al./The

InternationalJournal

ofAccounting

48(2013)

173–217

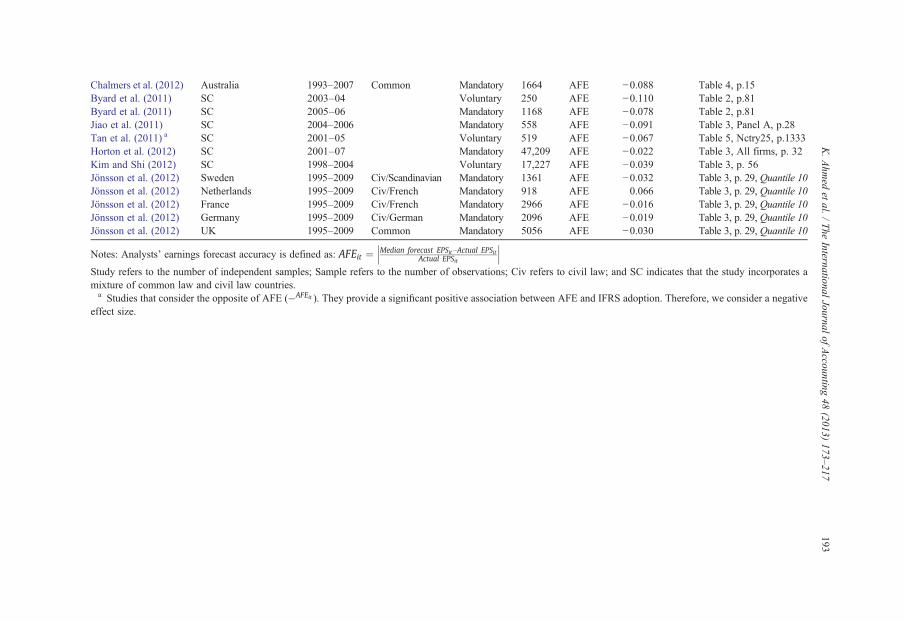

Chalmers et al. (2012) Australia 1993–2007 Common Mandatory 1664 AFE −0.088 Table 4, p.15Byard et al. (2011) SC 2003–04 Voluntary 250 AFE −0.110 Table 2, p.81Byard et al. (2011) SC 2005–06 Mandatory 1168 AFE −0.078 Table 2, p.81Jiao et al. (2011) SC 2004–2006 Mandatory 558 AFE −0.091 Table 3, Panel A, p.28Tan et al. (2011) a SC 2001–05 Voluntary 519 AFE −0.067 Table 5, Nctry25, p.1333Horton et al. (2012) SC 2001–07 Mandatory 47,209 AFE −0.022 Table 3, All firms, p. 32Kim and Shi (2012) SC 1998–2004 Voluntary 17,227 AFE −0.039 Table 3, p. 56Jönsson et al. (2012) Sweden 1995–2009 Civ/Scandinavian Mandatory 1361 AFE −0.032 Table 3, p. 29, Quantile 10Jönsson et al. (2012) Netherlands 1995–2009 Civ/French Mandatory 918 AFE 0.066 Table 3, p. 29, Quantile 10Jönsson et al. (2012) France 1995–2009 Civ/French Mandatory 2966 AFE −0.016 Table 3, p. 29, Quantile 10Jönsson et al. (2012) Germany 1995–2009 Civ/German Mandatory 2096 AFE −0.019 Table 3, p. 29, Quantile 10Jönsson et al. (2012) UK 1995–2009 Common Mandatory 5056 AFE −0.030 Table 3, p. 29, Quantile 10

Notes: Analysts' earnings forecast accuracy is defined as: AFEit ¼ Median forecast EPSit−Actual EPSitActual EPSit

��� ���Study refers to the number of independent samples; Sample refers to the number of observations; Civ refers to civil law; and SC indicates that the study incorporates amixture of common law and civil law countries.a Studies that consider the opposite of AFE (�AFEit ). They provide a significant positive association between AFE and IFRS adoption. Therefore, we consider a negative

effect size.

193K.Ahm

edet

al./The

InternationalJournal

ofAccounting

48(2013)

173–217

194 K. Ahmed et al. / The International Journal of Accounting 48 (2013) 173–217

should be followed to determine the mean correlation rð Þ and the estimate of the populationvariance. The steps are:

Step 1 Compute the mean correlation rð Þ using Eq. (1):

r ¼ ∑ ri:Nið Þ∑Ni

ð1Þ

where:

Ni sample size for study i,ri Pearson correlation coefficient for study i.

Step 2 Calculate the observed variance (Sr2) and the sampling error variance (Se

2) usingEqs. (2) and (3), respectively:

S2r ¼ ∑Ni ri−rð Þ2∑Ni

ð2Þ

S2e ¼ 1−r2� �2

K

∑Nið3Þ

where K is the number of individual studies (effect sizes) included in the meta-analysis. Larger sample sizes are given more weight in order to reduce samplingerror that declines as sample size increases (Hunter & Schmidt, 1990).

Step 3 The variance used to estimate the interval confidence is obtained using Eq. (4).

S2r =K� �

: ð4Þ

Given these two key statistics, the 95% confidence interval is normally constructed toassess the validity of the association of interests as per Eq. (5):

r−ffiffiffiffiffiffiffiffiffiffiffiS2r =K

q� �Z0:975; r þ

ffiffiffiffiffiffiffiffiffiffiffiS2r =K

q� �Z0:975

� ¼ r−

ffiffiffiffiffiffiffiffiffiffiffiS2r =K

q� �1:96ð Þ; r þ

ffiffiffiffiffiffiffiffiffiffiffiS2r =K

q� �1:96ð Þ

� :

ð5Þ

A 95% confidence interval that does not include zero is an indicator that there is a trueassociation between the variables of interest (Dalton, Daily, Johnson, & Ellstrand, 1999). Totest for moderating effects, a chi-square (χ2) statistic test is suggested to determine whetherthe observed variance is trivial or higher than expected (heterogeneous) (Hunter et al., 1982)using Eq. (6):

χ2K−1 ¼ NS2r

1−r2� �2: ð6Þ

195K. Ahmed et al. / The International Journal of Accounting 48 (2013) 173–217

The hypothesis of homogeneity will be rejected in many cases. In order to limit Type Ierror rates, we use a random effects model using Sr

2/k as the standard error in order to createa 95% confidence interval around the mean effect size, and to assess the significance of thenull hypothesis, (H0: r = 0) (Hunter & Schmidt, 2000). The homogeneity test is developedto determine whether the likelihood of variance among effect sizes is due only to samplingerror. Hunter et al. (1982) argue that much of the apparent contradiction in empiricalresearch on a particular topic is the product of statistical artifacts such as range restrictions,measurement unreliability, clerical errors, and differences in factor construct betweenalternative measures of the same construct, in addition to sampling error.

The inability to estimate additional sources of errors provides a conservative estimate ofpopulation correlation and variance that may increase the likelihood of finding potentialmoderators. However, Schmidt, Hunter, Pearlman, and Hirsh (1985) argue that inmeta-analysis, sampling error generally accounts for 75 to 95% of the variability acrossstudies and therefore correlation beyond sampling errors does not have much effect on thevariability. Prior meta-analytic studies in accounting and follow this cut-off (e.g., Ahmed& Courtis, 1999; García-Meca & Sánchez-Ballesta, 2010; Trotman & Wood, 1991). Testsfor the effect of moderating variables involve sub-grouping studies and calculations of rand sr

2 for each of the hypothesized sub-groups. The purpose of sub-grouping is to reduceheterogeneity and to increase explanatory power, and this process continues until theresidual variance is considered to be trivial, or until all identified moderating variables havebeen assessed. Gooding and Wagner (1985) suggest that studies should be classifiedaccording to differences in the measurement of the dependent and the explanatory variableto reduce the level of variance in results.

As discussed, we sub-group studies to examine moderating effects on the associations.Sub-groups are formed according to the jurisdictions' legal origin, accounting and auditingenforcement regime, the congruence between domestic GAAP and IFRS, and the mode ofIFRS adoption. Consistent with LaPorta et al. (1998), we classify legal origin into four groups:1) Common law studies (Common), 2) French civil law studies (Civ/French), 3) Germancivil law studies (Civ/German), and 4) Scandinavian civil law studies (Civ/Scandinavian).The rationale for this classification is based on the assumption that common law and civillaw countries have different properties of accounting information and accounting systemattributes including professionalism and transparency for common law versus statutorycontrol and secrecy for civil law countries. This will influence the IFRS adoption effects.Our classification is based on Stulz and Williamson (2003) (Table 1, p.323–24) and Leuzet al. (2003). For instance, countries in the common law group include the U.K., Canada,Australia, New Zealand, Malaysia, Hong Kong, Singapore, Ireland and South Africa;French civil law countries include Belgium, China, Greece, France, Italy, Netherlands,Portugal, Spain and Turkey; Scandinavian civil law countries include Denmark, Finland,Norway and Sweden; and Germany is the sole country in the German civil law category.

Using the index of jurisdictional accounting and auditing enforcement from Preiato etal. (2010), we sub-group studies into those conducted in jurisdictions with an index higherand lower than the mean (Enforcement high and Enforcement low, respectively). To groupstudies by the differences between a country's domestic GAAP and IFRS, we use Ding etal.'s (2007) indices to construct high and low absence (Absence high and Absence low)and divergence (Divergence high and Divergence low) sub-groups. Given that IFRS

196 K. Ahmed et al. / The International Journal of Accounting 48 (2013) 173–217

adoption may be studied in a voluntary or mandatory setting, sub-group meta-analysis isalso performed on groups of voluntary and mandatory studies, labeled as ‘Voluntaryadoption’ and ‘Mandatory adoption’ respectively. With regard to design issues, wesub-divide value relevance studies into those using price and return models. Further, thediscretionary accrual studies are sub-grouped according to the model used to estimatediscretionary accruals.15

5. Results

Our findings from meta-analyzing value relevance studies are reported in Tables 6 to 8.The meta-analysis of discretionary accruals and analysts' forecast accuracy and theirassociation with IFRS adoption are reported in Tables 9 and 10, respectively. For eachtable, we present the results of the overall meta-analysis and, if the homogeneity test isrejected, the tests for moderating variables including a jurisdiction's legal origin, accountingand auditing enforcement regime, congruence between domestic GAAP and IFRS and modeof IFRS adoption. Further, for the meta-analysis of value relevance (discretionary accruals)studies, we also present the tests for the moderating variable being the model used to estimatevalue relevance (discretionary accruals).

5.1. Meta-analysis of value relevance studies

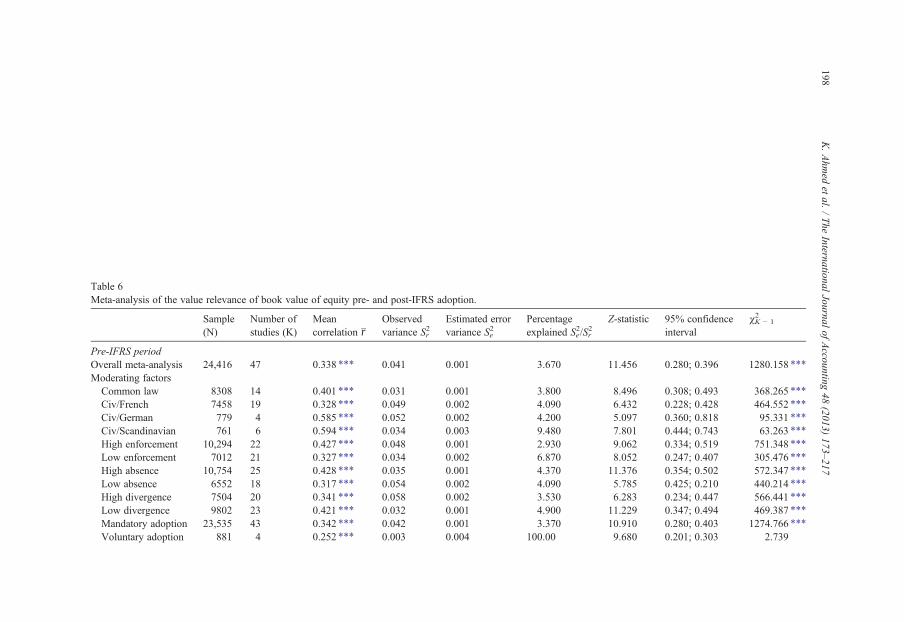

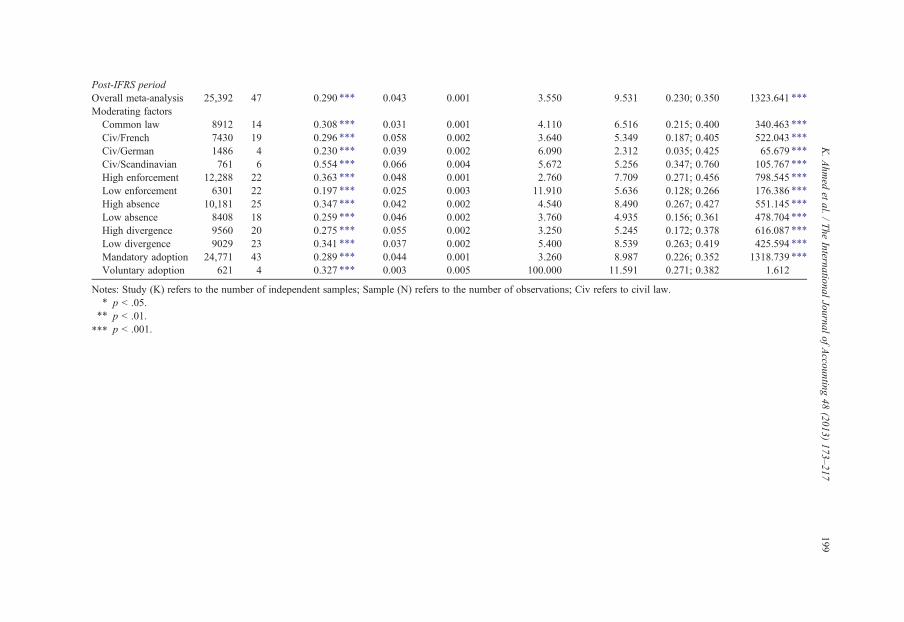

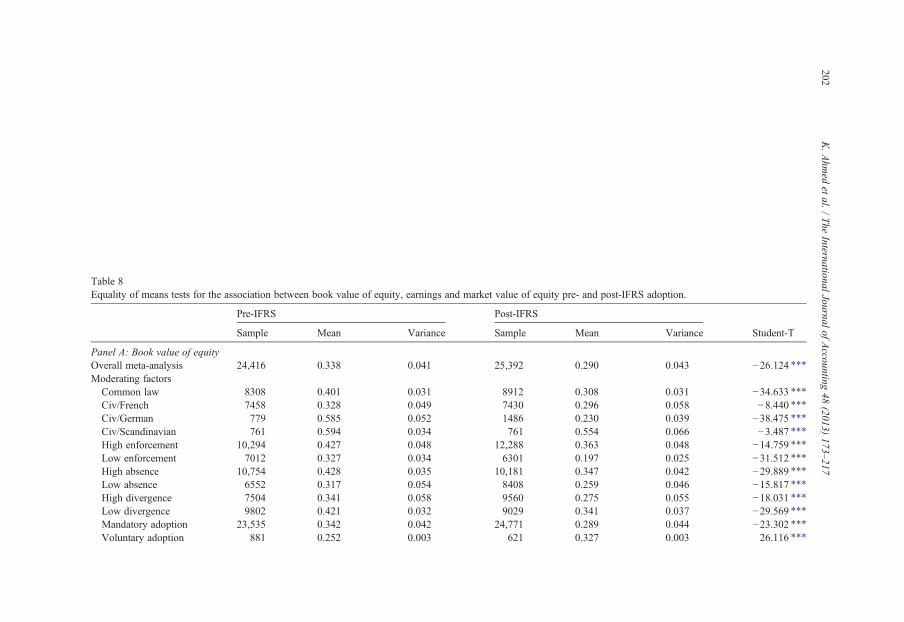

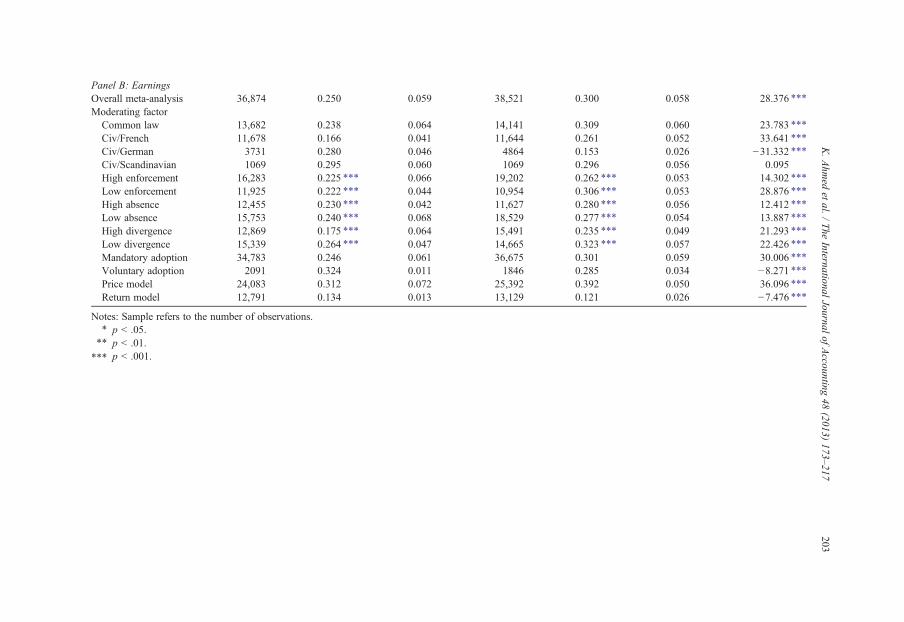

Table 6 reports the value relevance of book value of equity pre- and post-IFRSadoption. The overall meta-analysis provides evidence that the value relevance of equity ishighly significant (p b 0.001) during the pre- and post-IFRS period. However, it decreasesafter the adoption of IFRS as the mean correlation (r) for the pre-IFRS period accounts for0.338 and that for the post-IFRS period accounts for 0.290, with two confidence intervalsthat do not include negative values. Because the homogeneity test is rejected for the twoperiods based on χ2 (p b 0.01), we conduct additional analysis to reduce heterogeneity andtest whether the variability across results is attributed to our moderating factors.

When studies are classified according to a country's legal origin, the value relevanceof book value of equity generally decreases but remains significant. For example, the rofcommon law countries for the pre- IFRS period accounts for 0.401 (z = 8.492) (calculated

as r=ffiffiffiffiffiffiffiffiffiffiffiS2r =K

q) with a confidence interval between 0.308 and 0.493. Under IFRS, ther amounts

to 0.308 (z = 6.516) with a confidence interval between 0.215 and 0.400. Similar results arenoted for Germany. The Scandinavian civil law group shows the r at 0.594 (z = 5.097) and0.554 (z = 2.312) for the pre- and post-IFRS period, respectively. These results suggest that thevalue relevance remains significant, with the lower limit above zero. The French civil lawcountries experience a small decline with the r being 0.328 (z = 6.432) and 0.296 (z = 5.349)for the pre- and post-IFRS period, respectively, with two confidence intervals with lower limitsabove zero. These results suggest that irrespective of a country's legal origin, the association

15 Sub-group meta-analysis is not conducted on analysts' forecast studies error proxies since they are the same inthe studies included in our analysis.

197K. Ahmed et al. / The International Journal of Accounting 48 (2013) 173–217

between book value of equity and market value remains significant in the post-IFRS periodbut its value relevance has declined.

With respect to the moderating effects of the accounting and auditing enforcementregime and congruence between domestic GAAP and IFRS, there is a decrease in thevalue relevance of book value of equity post IFRS adoption for both the high and lowenforcement, absence and divergence groups. For all sub groups, the r is lower in thepost-IFRS period then the pre-IFRS period and the lower limits of the confidence intervalsare all above zero. These results suggest that the decline in the value relevance of the bookvalue of equity occurs irrespective of the accounting and enforcement regime in place orthe differences between IFRS and the previous domestic GAAP.

Classifying the studies into voluntary and mandatory IFRS adoption, the results showthat the value relevance of book value of equity is significant (p b 0.001) for bothmandatory and voluntary adopters. However, the r decreases from 0.342 (z = 10.910) inthe pre-IFRS period to 0.289 (z = 8.987) in the post-IFRS period for the mandatoryadoption group. In contrast, the r for voluntary adoption studies of 0.252 (pre-IFRS) and0.327 post-IFRS suggests that the value relevance of book value of equity for voluntaryadopters increases significantly after adoption.

Overall, the results show that the mean correlation (r), as measured by effect size,between book value of equity and IFRS adoption is significant (p b 0.01) in the pre-IFRSperiod and in the post-IFRS period with the relevance lower in the post IFRS period. Thelow levels of explanatory power (ranging between 3.260% and 11.770%) and high levelsof significant χ2 across the sub-groups indicate that the variation in the degree ofcorrelations between equity and IFRS adoption is not due to sampling error. Among all thesub-groups, the value relevance of equity increases for only the voluntary adoption group.

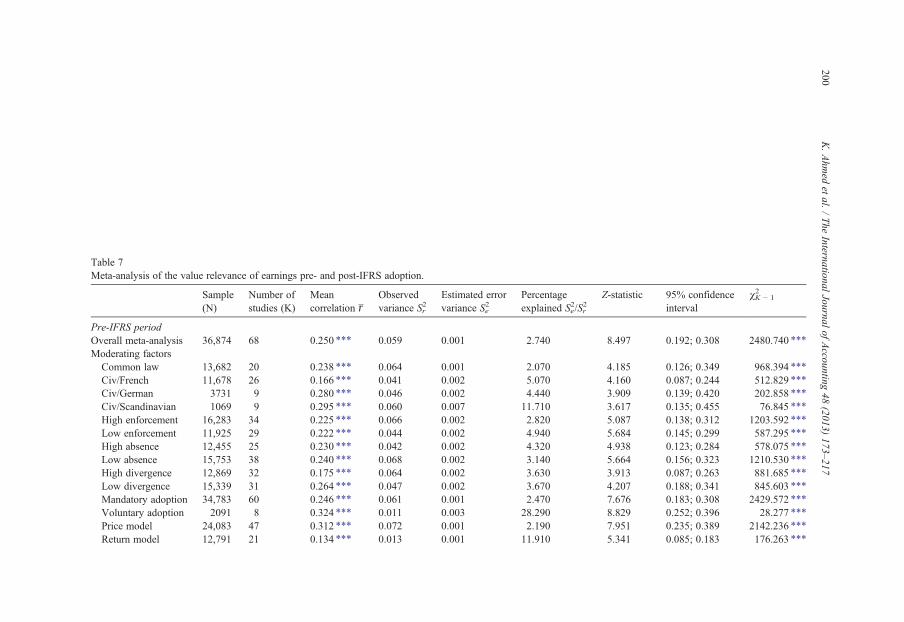

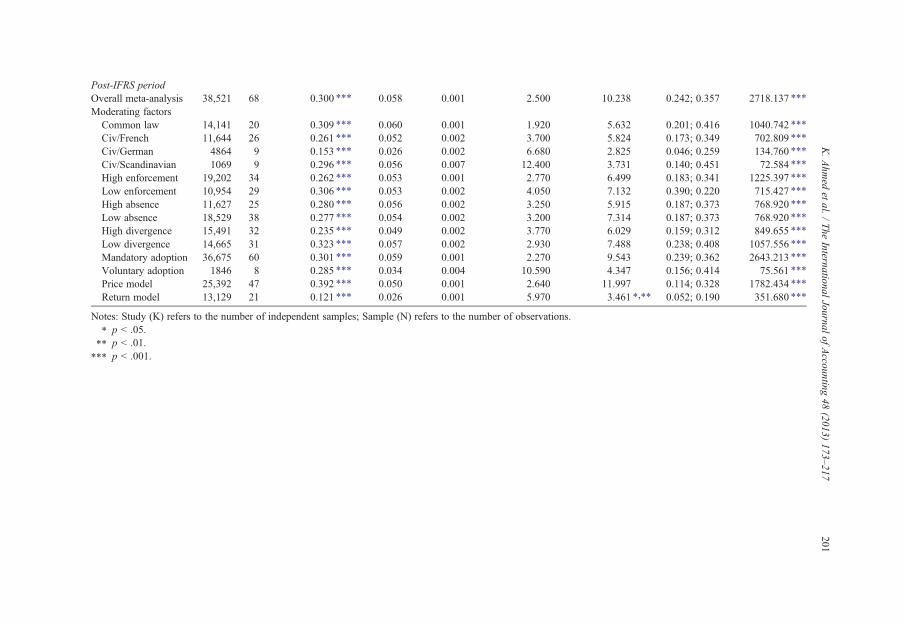

Table 7 reports the meta-analysis results for the value relevance of earnings for theperiod preceding and following IFRS adoption. The analysis provides evidence that thevalue relevance of earnings is highly significant with the significance increasing after IFRSadoption. This is evident in the overall meta-analysis with the r for the pre-IFRS periodbeing 0.250 (z = 8.497) and 0.300 (z = 10.238) post-IFRS.

Testing the moderator effects of the various legal origins shows that for studies withincommon law countries, the r is 0.238 (z = 4.185) and 0.309 (z = 5.632) in the pre- andpost-IFRS period, respectively. For French civil law influenced companies the r is 0.166(z = 4.160) and 0.261 (z = 5.842). For companies in a jurisdiction with a legal origin basedon German civil law, the r is 0.280 (z = 3.909) and 0.153 (z = 2.825); for Scandinaviancivil law firms the r is 0.295 (z = 3.617) and 0.296 (z = 3.731) for the pre-IFRS andpost-IFRS period, respectively, with all associations significant at the 1% level. Theseresults suggest some variability in the IFRS adoption effects on the value relevance ofearnings according to a country's legal origin. The increased value relevance of earningsoccurs in common law and French law countries.

Investigating accounting and auditing enforcement regimes and congruency betweendomestic GAAP and IFRS as moderating factors, we find increasing mean correlations inthe post-relative to the pre-IFRS period, for all sub-groups. Considering accounting andauditing enforcement, the r is 0.225 (high enforcement group) and 0.222 (low enforcementgroup) pre-IFRS and 0.262 (high enforcement) and 0.306 (low enforcement) post-IFRS.With respect to the comparison of domestic GAAP and IFRS, pre-IFRS the r is 0.230,

Table 6Meta-analysis of the value relevance of book value of equity pre- and post-IFRS adoption.

Sample(N)

Number ofstudies (K)

Meancorrelation r

Observedvariance Sr

2Estimated errorvariance Se

2Percentageexplained Se

2/Sr2

Z-statistic 95% confidenceinterval

χK − 12

Pre-IFRS periodOverall meta-analysis 24,416 47 0.338 ⁎⁎⁎ 0.041 0.001 3.670 11.456 0.280; 0.396 1280.158 ⁎⁎⁎

Moderating factorsCommon law 8308 14 0.401 ⁎⁎⁎ 0.031 0.001 3.800 8.496 0.308; 0.493 368.265 ⁎⁎⁎

Civ/French 7458 19 0.328 ⁎⁎⁎ 0.049 0.002 4.090 6.432 0.228; 0.428 464.552 ⁎⁎⁎

Civ/German 779 4 0.585 ⁎⁎⁎ 0.052 0.002 4.200 5.097 0.360; 0.818 95.331 ⁎⁎⁎

Civ/Scandinavian 761 6 0.594 ⁎⁎⁎ 0.034 0.003 9.480 7.801 0.444; 0.743 63.263 ⁎⁎⁎

High enforcement 10,294 22 0.427 ⁎⁎⁎ 0.048 0.001 2.930 9.062 0.334; 0.519 751.348 ⁎⁎⁎

Low enforcement 7012 21 0.327 ⁎⁎⁎ 0.034 0.002 6.870 8.052 0.247; 0.407 305.476 ⁎⁎⁎

High absence 10,754 25 0.428 ⁎⁎⁎ 0.035 0.001 4.370 11.376 0.354; 0.502 572.347 ⁎⁎⁎

Low absence 6552 18 0.317 ⁎⁎⁎ 0.054 0.002 4.090 5.785 0.425; 0.210 440.214 ⁎⁎⁎

High divergence 7504 20 0.341 ⁎⁎⁎ 0.058 0.002 3.530 6.283 0.234; 0.447 566.441 ⁎⁎⁎

Low divergence 9802 23 0.421 ⁎⁎⁎ 0.032 0.001 4.900 11.229 0.347; 0.494 469.387 ⁎⁎⁎

Mandatory adoption 23,535 43 0.342 ⁎⁎⁎ 0.042 0.001 3.370 10.910 0.280; 0.403 1274.766 ⁎⁎⁎

Voluntary adoption 881 4 0.252 ⁎⁎⁎ 0.003 0.004 100.00 9.680 0.201; 0.303 2.739

198K.Ahm

edet

al./The

InternationalJournal

ofAccounting

48(2013)

173–217

Post-IFRS periodOverall meta-analysis 25,392 47 0.290 ⁎⁎⁎ 0.043 0.001 3.550 9.531 0.230; 0.350 1323.641 ⁎⁎⁎

Moderating factorsCommon law 8912 14 0.308 ⁎⁎⁎ 0.031 0.001 4.110 6.516 0.215; 0.400 340.463 ⁎⁎⁎

Civ/French 7430 19 0.296 ⁎⁎⁎ 0.058 0.002 3.640 5.349 0.187; 0.405 522.043 ⁎⁎⁎

Civ/German 1486 4 0.230 ⁎⁎⁎ 0.039 0.002 6.090 2.312 0.035; 0.425 65.679 ⁎⁎⁎

Civ/Scandinavian 761 6 0.554 ⁎⁎⁎ 0.066 0.004 5.672 5.256 0.347; 0.760 105.767 ⁎⁎⁎

High enforcement 12,288 22 0.363 ⁎⁎⁎ 0.048 0.001 2.760 7.709 0.271; 0.456 798.545 ⁎⁎⁎

Low enforcement 6301 22 0.197 ⁎⁎⁎ 0.025 0.003 11.910 5.636 0.128; 0.266 176.386 ⁎⁎⁎

High absence 10,181 25 0.347 ⁎⁎⁎ 0.042 0.002 4.540 8.490 0.267; 0.427 551.145 ⁎⁎⁎

Low absence 8408 18 0.259 ⁎⁎⁎ 0.046 0.002 3.760 4.935 0.156; 0.361 478.704 ⁎⁎⁎

High divergence 9560 20 0.275 ⁎⁎⁎ 0.055 0.002 3.250 5.245 0.172; 0.378 616.087 ⁎⁎⁎

Low divergence 9029 23 0.341 ⁎⁎⁎ 0.037 0.002 5.400 8.539 0.263; 0.419 425.594 ⁎⁎⁎

Mandatory adoption 24,771 43 0.289 ⁎⁎⁎ 0.044 0.001 3.260 8.987 0.226; 0.352 1318.739 ⁎⁎⁎

Voluntary adoption 621 4 0.327 ⁎⁎⁎ 0.003 0.005 100.000 11.591 0.271; 0.382 1.612

Notes: Study (K) refers to the number of independent samples; Sample (N) refers to the number of observations; Civ refers to civil law.⁎ p b .05.⁎⁎ p b .01.⁎⁎⁎ p b .001.

199K.Ahm

edet

al./The

InternationalJournal

ofAccounting

48(2013)

173–217

Table 7Meta-analysis of the value relevance of earnings pre- and post-IFRS adoption.

Sample(N)

Number ofstudies (K)

Meancorrelation r

Observedvariance Sr

2Estimated errorvariance Se

2Percentageexplained Se

2/Sr2

Z-statistic 95% confidenceinterval

χK − 12

Pre-IFRS periodOverall meta-analysis 36,874 68 0.250 ⁎⁎⁎ 0.059 0.001 2.740 8.497 0.192; 0.308 2480.740 ⁎⁎⁎

Moderating factorsCommon law 13,682 20 0.238 ⁎⁎⁎ 0.064 0.001 2.070 4.185 0.126; 0.349 968.394 ⁎⁎⁎