a multi-source, multi-purpose clean fuel for china and the ... · a multi-source, multi-purpose...

TRANSCRIPT

DME A Multi-source, Multi-purpose Clean Fuel

for China and the World

by

Dr. Theo Fleisch

Chairman, International DME Association

Distinguished Advisor, Global Gas Technology, BP

Presented at

DME FORUM 2003

Shanghai Jiao Tong University

SHANGHAI, October 23 – 24, 2003

• Context: GTP -- Gas To Products

CTP – Coal To Products

• The Oxygenate Family

Methanol and DME

• Opportunities for LARGE Markets

• Challenges: Technologies and Economics

• IDA—The International DME Association

• Beyond MeOH/DME: DMM and DMC

• Vision: Gas-, Coal-, and Methanol Refinery

Outline

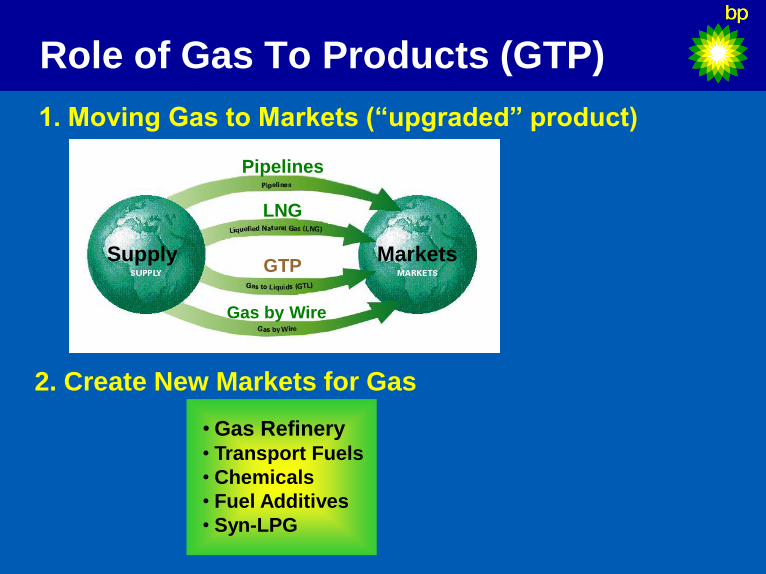

Role of Gas To Products (GTP)

• Gas Refinery • Transport Fuels

• Chemicals

• Fuel Additives

• Syn-LPG

Power Generation

Supply Markets

Pipelines

LNG

GTP

Gas by Wire

1. Moving Gas to Markets (“upgraded” product)

2. Create New Markets for Gas

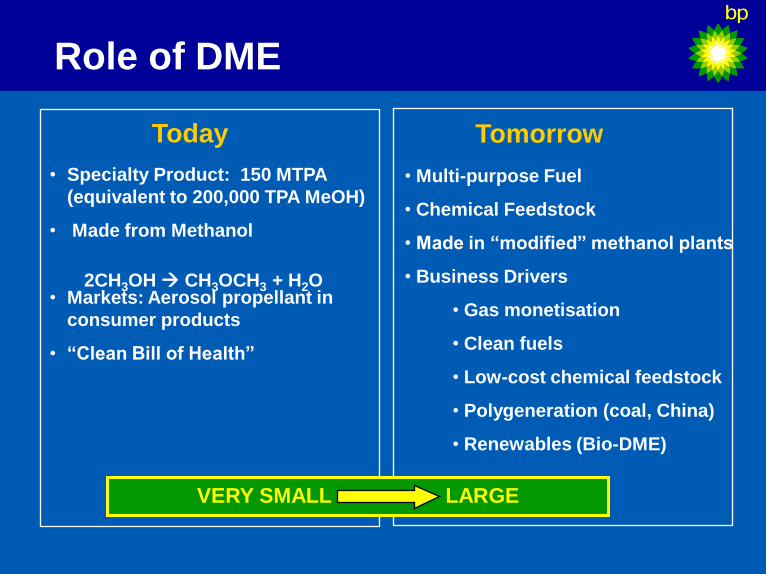

Role of DME

Today

• Specialty Product: 150 MTPA

(equivalent to 200,000 TPA MeOH)

• Made from Methanol

• Markets: Aerosol propellant in

consumer products

• “Clean Bill of Health”

Tomorrow

• Multi-purpose Fuel

• Chemical Feedstock

• Made in “modified” methanol plants

• Business Drivers

• Gas monetisation

• Clean fuels

• Low-cost chemical feedstock

• Polygeneration (coal, China)

• Renewables (Bio-DME)

2CH3OH CH3OCH3 + H2O

VERY SMALL LARGE

CH4

CO + 2 H2

“Synthesis Gas”

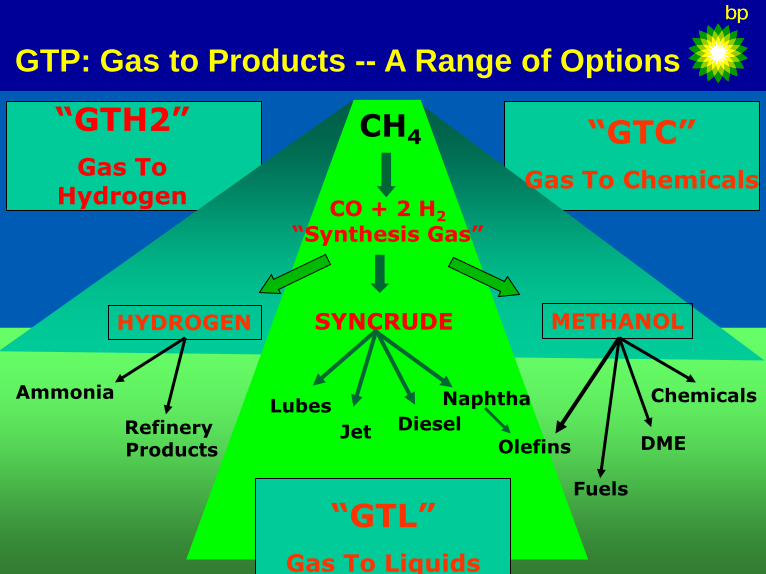

SYNCRUDE METHANOL

Diesel Jet

Naphtha Lubes Chemicals

Olefins Refinery Products

Fuels

Ammonia

DME

GTP: Gas to Products -- A Range of Options

“GTC”

Gas To Chemicals

“GTH2”

Gas To Hydrogen

HYDROGEN

“GTL”

Gas To Liquids

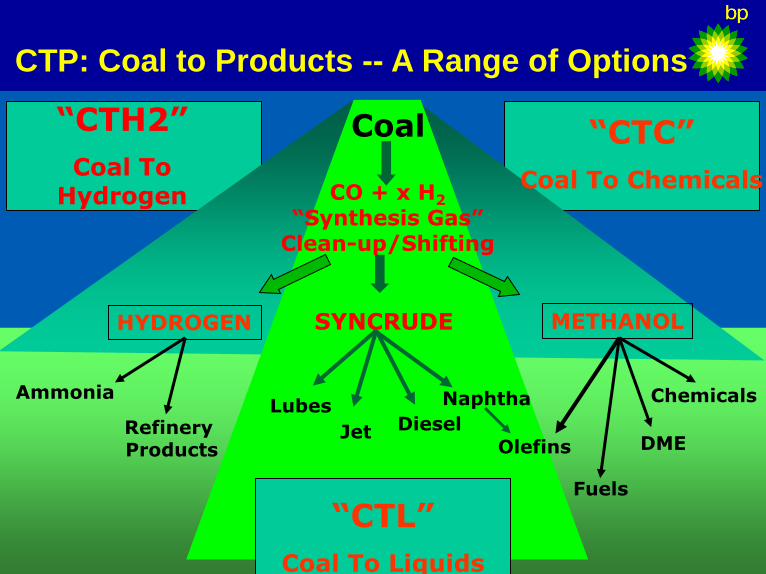

Coal

CO + x H2

“Synthesis Gas” Clean-up/Shifting

SYNCRUDE METHANOL

Diesel Jet

Naphtha Lubes Chemicals

Olefins Refinery Products

Fuels

Ammonia

DME

CTP: Coal to Products -- A Range of Options

“CTC”

Coal To Chemicals

“CTH2”

Coal To Hydrogen

HYDROGEN

“CTL”

Coal To Liquids

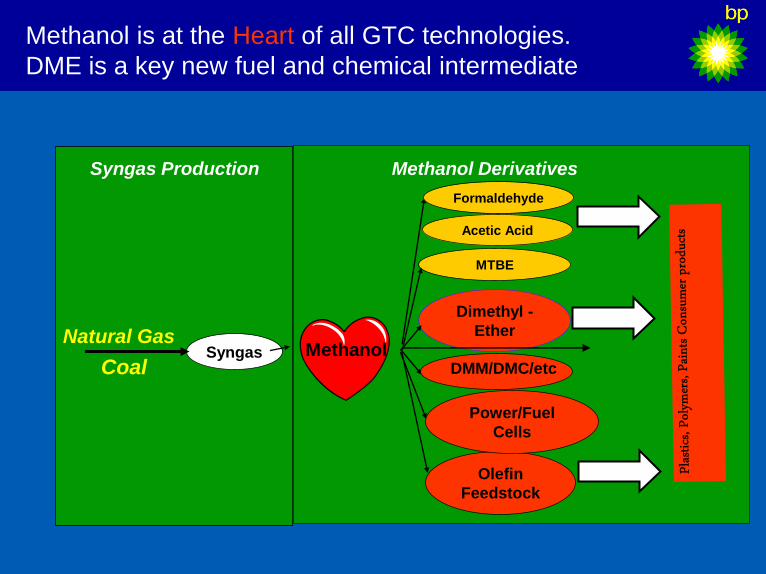

Methanol is at the Heart of all GTC technologies.

DME is a key new fuel and chemical intermediate

Syngas

Acetic Acid

Natural Gas

Syngas Production Methanol Derivatives

MTBE

Dimethyl -

Ether

Olefin

Feedstock

Formaldehyde

Methanol

Power/Fuel

Cells

DMM/DMC/etc Coal

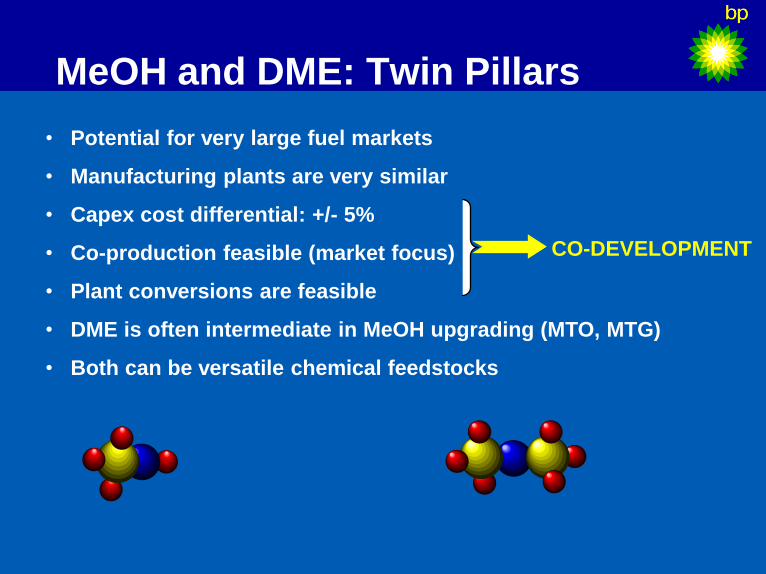

MeOH and DME: Twin Pillars

• Potential for very large fuel markets

• Manufacturing plants are very similar

• Capex cost differential: +/- 5%

• Co-production feasible (market focus)

• Plant conversions are feasible

• DME is often intermediate in MeOH upgrading (MTO, MTG)

• Both can be versatile chemical feedstocks

CO-DEVELOPMENT

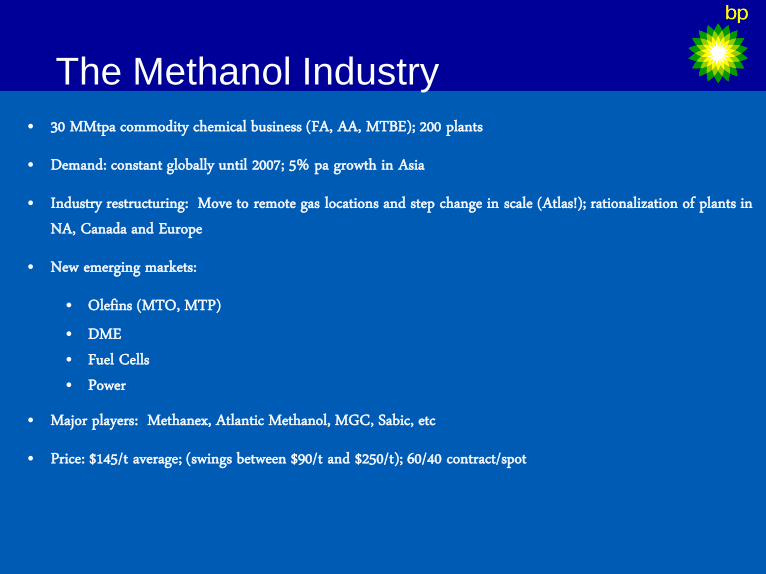

The Methanol Industry

• 30 MMtpa commodity chemical business (FA, AA, MTBE); 200 plants

• Demand: constant globally until 2007; 5% pa growth in Asia

• Industry restructuring: Move to remote gas locations and step change in scale (Atlas!); rationalization of plants in NA, Canada and Europe

• New emerging markets:

• Olefins (MTO, MTP) • DME • Fuel Cells • Power

• Major players: Methanex, Atlantic Methanol, MGC, Sabic, etc

• Price: $145/t average; (swings between $90/t and $250/t); 60/40 contract/spot

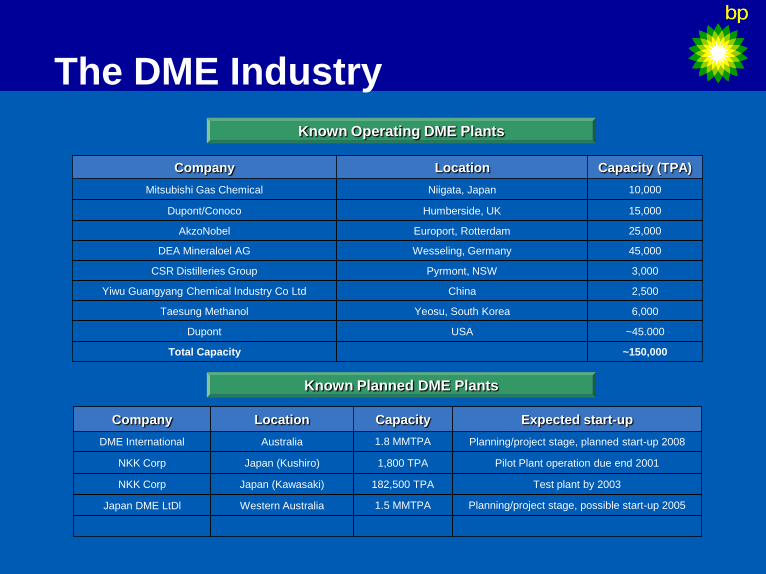

The DME Industry

Mitsubishi Gas Chemical

Dupont/Conoco

AkzoNobel

DEA Mineraloel AG

CSR Distilleries Group

Yiwu Guangyang Chemical Industry Co Ltd

Taesung Methanol

Niigata, Japan

Humberside, UK

Europort, Rotterdam

Wesseling, Germany

Pyrmont, NSW

China

Yeosu, South Korea

10,000

15,000

25,000

45,000

3,000

2,500

6,000

Company Location Capacity (TPA)

Dupont USA ~45.000

Total Capacity ~150,000

DME International

NKK Corp

NKK Corp

Japan DME LtDl

Australia

Japan (Kushiro)

Japan (Kawasaki)

Western Australia

1.8 MMTPA

1,800 TPA

182,500 TPA

1.5 MMTPA

Company Location Capacity

Planning/project stage, planned start-up 2008

Pilot Plant operation due end 2001

Test plant by 2003

Planning/project stage, possible start-up 2005

Expected start-up

Known Operating DME Plants

Known Planned DME Plants

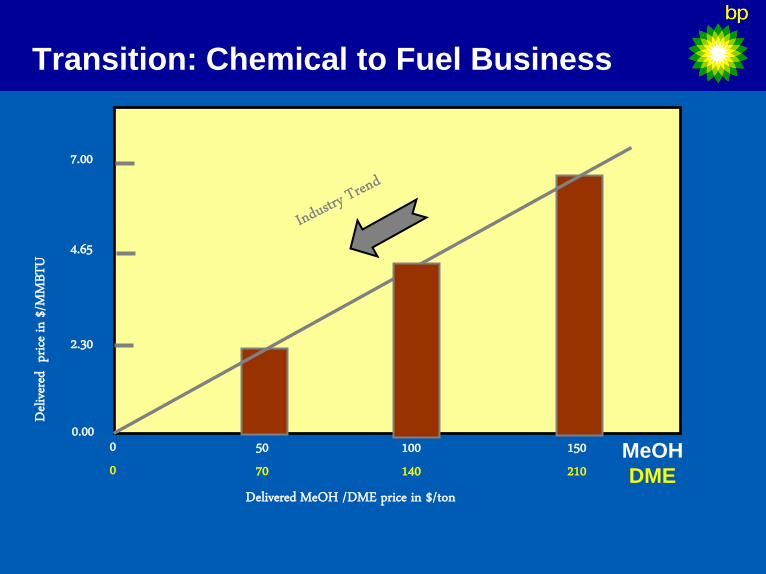

Transition: Chemical to Fuel Business

Delivered MeOH /DME price in $/ton

50 70

100 140

150 210

7.00

4.65

2.30

0.00 0 0

Deliv

ered

price

in $/M

MBTU

MeOH

DME

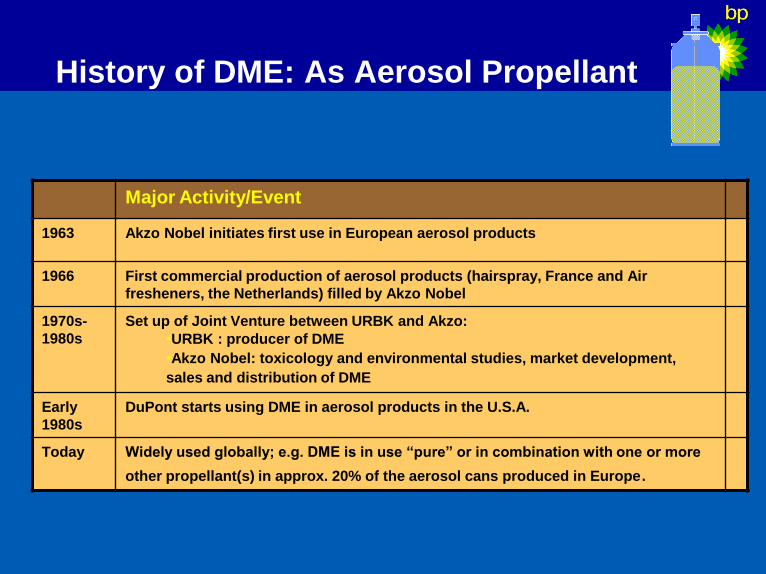

History of DME: As Aerosol Propellant

Major Activity/Event

1963 Akzo Nobel initiates first use in European aerosol products

1966 First commercial production of aerosol products (hairspray, France and Air

fresheners, the Netherlands) filled by Akzo Nobel

1970s-

1980s

Set up of Joint Venture between URBK and Akzo:

•URBK : producer of DME

•Akzo Nobel: toxicology and environmental studies, market development,

sales and distribution of DME

Early

1980s

DuPont starts using DME in aerosol products in the U.S.A.

Today Widely used globally; e.g. DME is in use “pure” or in combination with one or more

other propellant(s) in approx. 20% of the aerosol cans produced in Europe.

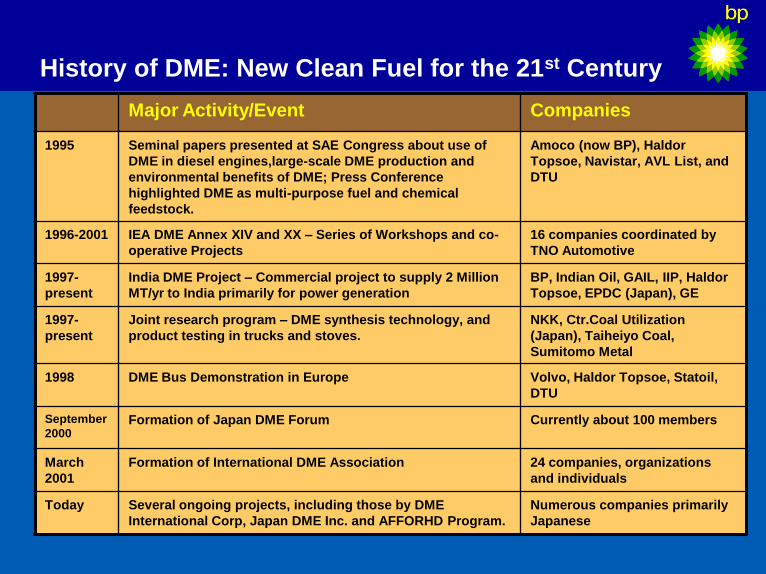

History of DME: New Clean Fuel for the 21st Century

Major Activity/Event Companies

1995 Seminal papers presented at SAE Congress about use of

DME in diesel engines,large-scale DME production and

environmental benefits of DME; Press Conference

highlighted DME as multi-purpose fuel and chemical

feedstock.

Amoco (now BP), Haldor

Topsoe, Navistar, AVL List, and

DTU

1996-2001 IEA DME Annex XIV and XX – Series of Workshops and co-

operative Projects

16 companies coordinated by

TNO Automotive

1997-

present

India DME Project – Commercial project to supply 2 Million

MT/yr to India primarily for power generation

BP, Indian Oil, GAIL, IIP, Haldor

Topsoe, EPDC (Japan), GE

1997-

present

Joint research program – DME synthesis technology, and

product testing in trucks and stoves.

NKK, Ctr.Coal Utilization

(Japan), Taiheiyo Coal,

Sumitomo Metal

1998 DME Bus Demonstration in Europe Volvo, Haldor Topsoe, Statoil,

DTU

September

2000 Formation of Japan DME Forum Currently about 100 members

March

2001

Formation of International DME Association 24 companies, organizations

and individuals

Today Several ongoing projects, including those by DME

International Corp, Japan DME Inc. and AFFORHD Program.

Numerous companies primarily

Japanese

Understanding the potential of DME

• Molecular Structure

• Physical Properties

• Fuel Performance

• Chemistry to other Products

• Environmental, Health and Safety Properties

• Produced in large-scale methanol plants

In order to grasp the potential of DME, one must

understand the following issues:

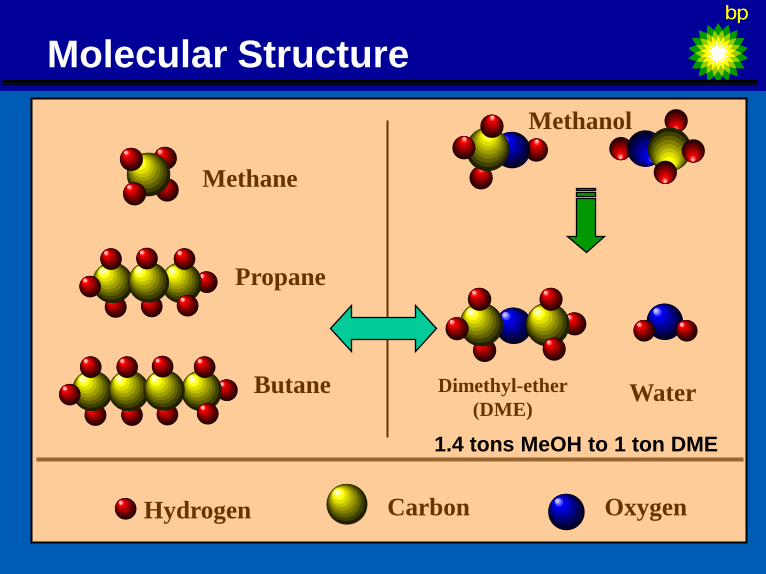

Molecular Structure

Dimethyl-ether

(DME)

Methane

Methanol

Water

Propane

Butane

Hydrogen Carbon Oxygen

1.4 tons MeOH to 1 ton DME

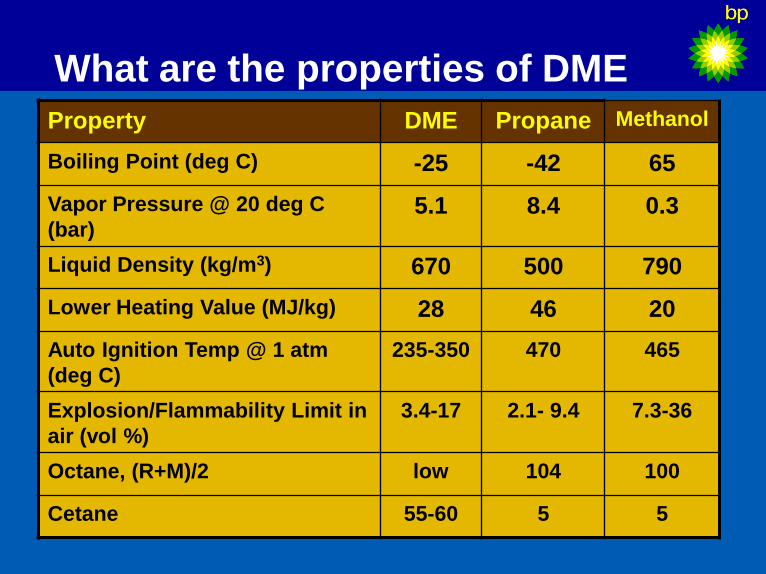

What are the properties of DME

Property DME Propane Methanol

Boiling Point (deg C) -25 -42 65

Vapor Pressure @ 20 deg C

(bar) 5.1 8.4 0.3

Liquid Density (kg/m3) 670 500 790

Lower Heating Value (MJ/kg) 28 46 20

Auto Ignition Temp @ 1 atm

(deg C)

235-350 470 465

Explosion/Flammability Limit in

air (vol %)

3.4-17 2.1- 9.4 7.3-36

Octane, (R+M)/2 low 104 100

Cetane 55-60 5 5

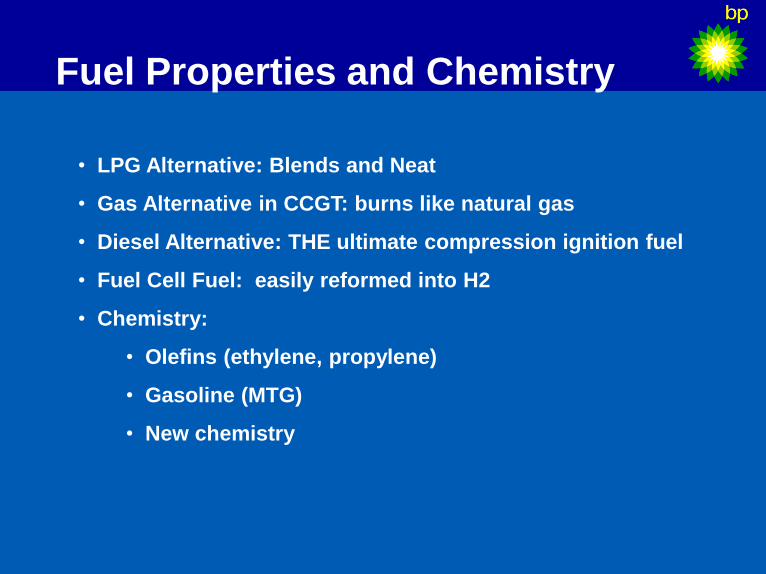

Fuel Properties and Chemistry

• LPG Alternative: Blends and Neat

• Gas Alternative in CCGT: burns like natural gas

• Diesel Alternative: THE ultimate compression ignition fuel

• Fuel Cell Fuel: easily reformed into H2

• Chemistry:

• Olefins (ethylene, propylene)

• Gasoline (MTG)

• New chemistry

Environment, Health, and Safety

• Environmental

• Short half-life in troposphere

• No release into stratosphere

• Quick biodegradation

• Significant end-use emission reductions

• Health

• Virtually Non-toxic

• Not a carcinogen, teratogen or mutagen

• Approved for consumer care products

• Safety

• Like LPG, non-corrosive

• Established codes and standards

• Visible flame

• Context: GTP -- Gas To Products

CTP – Coal To Products

• The Oxygenate Family

Methanol and DME

• Opportunities for LARGE Markets

• Challenges: Technologies and Economics

• IDA—The International DME Association

• Beyond MeOH/DME: DMM and DMC

• Vision: Gas-, Coal-, and Methanol Refinery

Outline

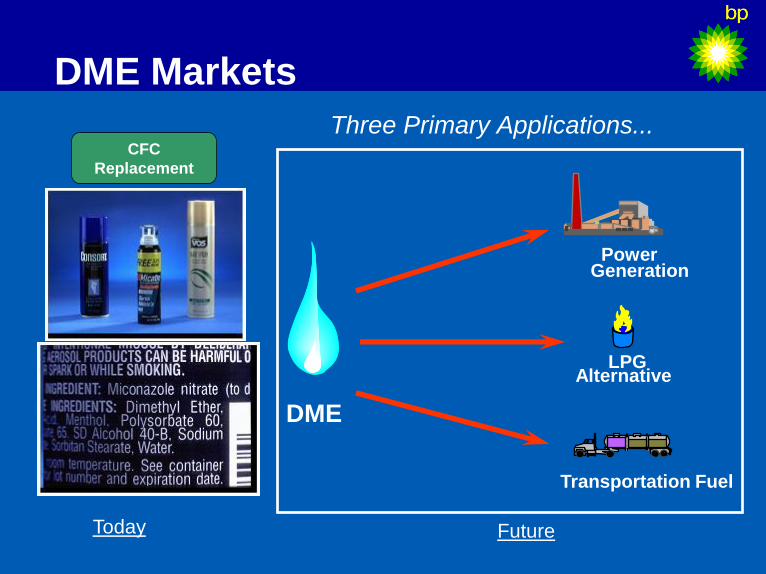

DME Markets

Power Generation

LPG Alternative

Transportation Fuel

DME

Three Primary Applications... CFC

Replacement

Today Future

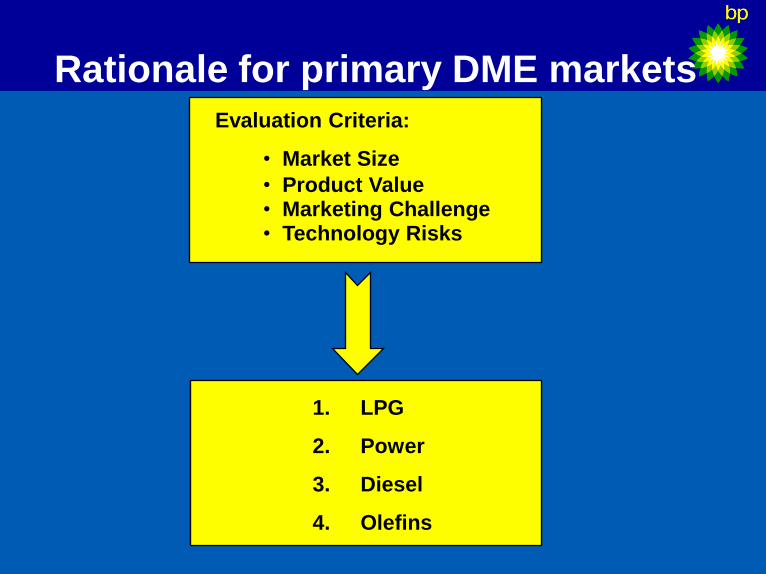

Rationale for primary DME markets Evaluation Criteria:

• Market Size

• Product Value • Marketing Challenge • Technology Risks

1. LPG

2. Power

3. Diesel

4. Olefins

1. DME as an LPG Substitute – Why?

• DME’s physical properties similar to LPG

• LPG is domestic fuel and chemical feedstock

• LPG market is large (180MMTPA in 2000) and

growing fast (5MMTPA through 2015; 9/13MMTPA

DME/methanol equivalent)

• Regional supply/demand imbalances/shortages

• Attractive pricing/economics

• Developing countries (China, India) need portable

(bottled) fuel – even faster demand growth

• Strong quality of life improvement and

environmental driver

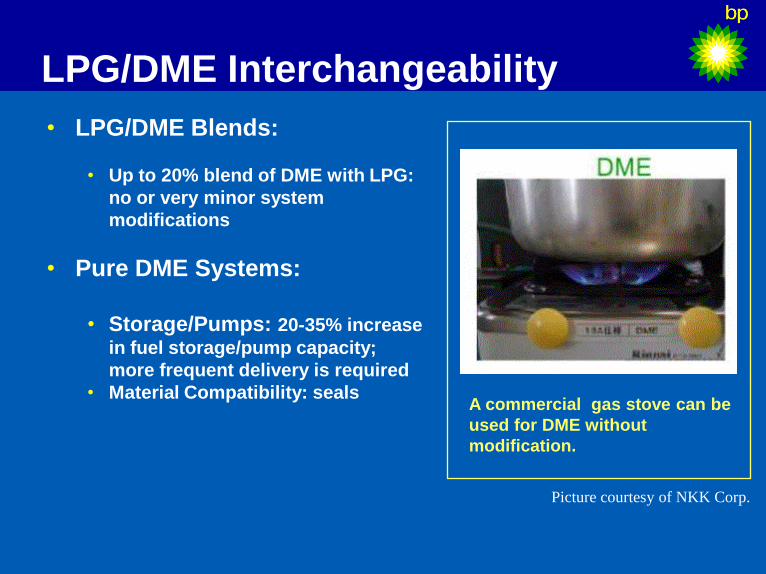

LPG/DME Interchangeability

• LPG/DME Blends:

• Up to 20% blend of DME with LPG:

no or very minor system

modifications

• Pure DME Systems:

• Storage/Pumps: 20-35% increase

in fuel storage/pump capacity;

more frequent delivery is required

• Material Compatibility: seals

Picture courtesy of NKK Corp.

A commercial gas stove can be

used for DME without

modification.

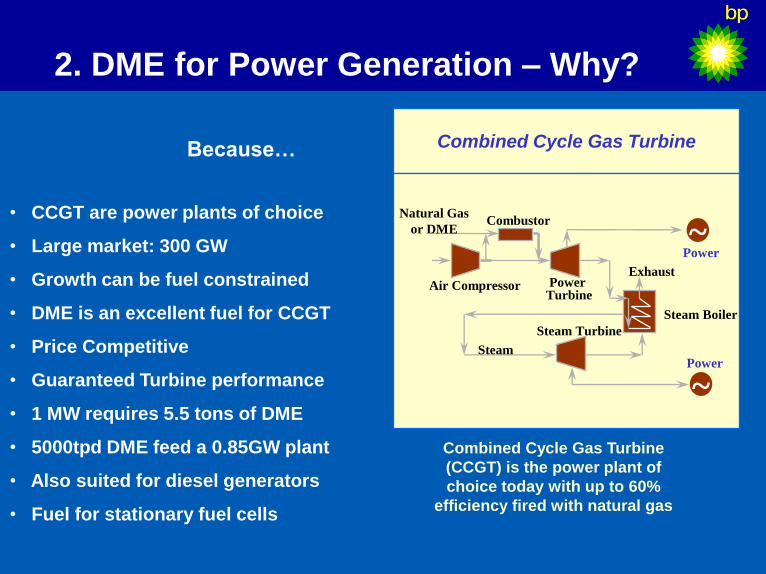

2. DME for Power Generation – Why?

Because… Combined Cycle Gas Turbine

Air Compressor

Combustor

Power Turbine

Steam Boiler

Natural Gas

or DME

Power

Power Steam

Steam Turbine

Exhaust

~

~

Combined Cycle Gas Turbine

(CCGT) is the power plant of

choice today with up to 60%

efficiency fired with natural gas

• CCGT are power plants of choice

• Large market: 300 GW

• Growth can be fuel constrained

• DME is an excellent fuel for CCGT

• Price Competitive

• Guaranteed Turbine performance

• 1 MW requires 5.5 tons of DME

• 5000tpd DME feed a 0.85GW plant

• Also suited for diesel generators

• Fuel for stationary fuel cells

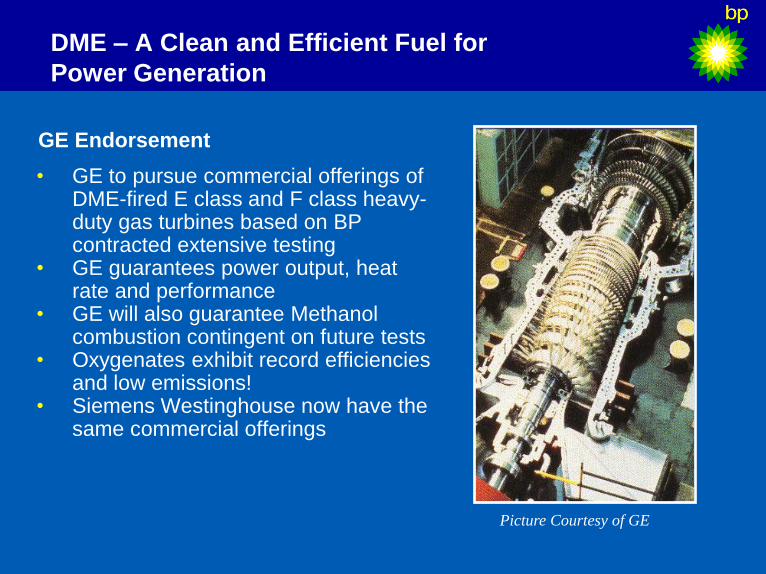

DME – A Clean and Efficient Fuel for

Power Generation

• GE to pursue commercial offerings of DME-fired E class and F class heavy-duty gas turbines based on BP contracted extensive testing

• GE guarantees power output, heat rate and performance

• GE will also guarantee Methanol combustion contingent on future tests

• Oxygenates exhibit record efficiencies and low emissions!

• Siemens Westinghouse now have the same commercial offerings

Picture Courtesy of GE

GE Endorsement

Market Readiness

• Power Producers willing to consider DME and

methanol as fuel

• Gas turbine manufacturers willing to supply new

machines and retrofits

• Energy companies and the methanol industry have

not yet embraced fuel DME/Methanol

Who will create the business?

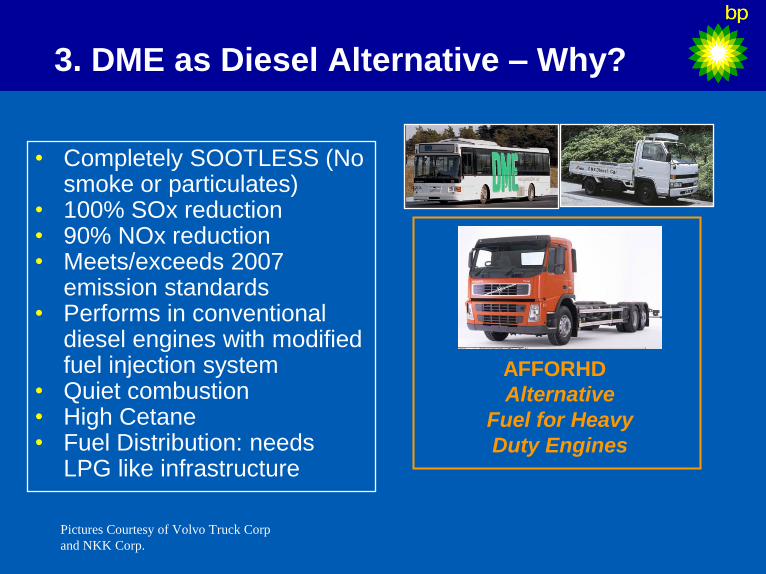

3. DME as Diesel Alternative – Why?

• Completely SOOTLESS (No smoke or particulates)

• 100% SOx reduction • 90% NOx reduction • Meets/exceeds 2007

emission standards • Performs in conventional

diesel engines with modified fuel injection system

• Quiet combustion • High Cetane • Fuel Distribution: needs

LPG like infrastructure

Pictures Courtesy of Volvo Truck Corp

and NKK Corp.

AFFORHD

Alternative

Fuel for Heavy

Duty Engines

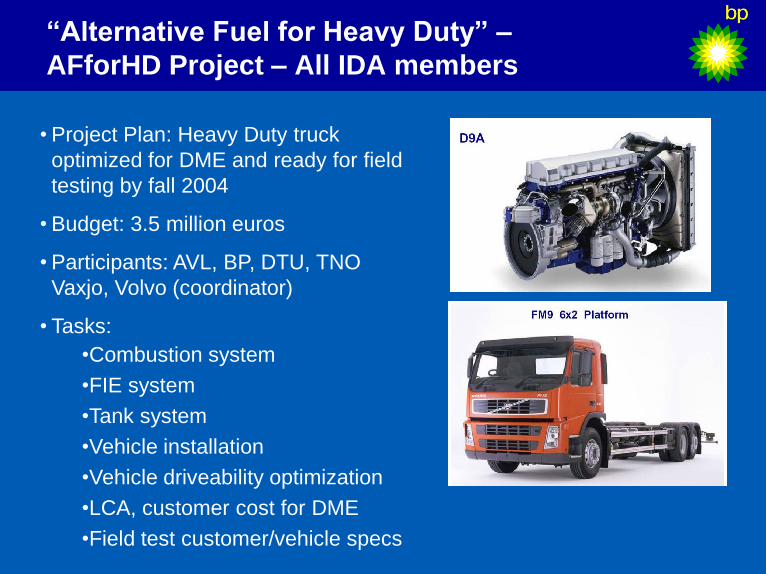

“Alternative Fuel for Heavy Duty” –

AFforHD Project – All IDA members

•Combustion system

•FIE system

•Tank system

•Vehicle installation

•Vehicle driveability optimization

•LCA, customer cost for DME

•Field test customer/vehicle specs

• Project Plan: Heavy Duty truck

optimized for DME and ready for field

testing by fall 2004

• Budget: 3.5 million euros

• Participants: AVL, BP, DTU, TNO

Vaxjo, Volvo (coordinator)

• Tasks:

• Lower cost, more selective feedstocks

• DME is “halfway point” in MTO • Ethylene market currently ~90 MMTPA growing to +160 MMTPA

by 2015 • Propylene market currently ~50 MMTPA growing to +105

MMTPA by 2015 • Combined growth rate of about 10MMTPA • Need about 3 MMTPA of methanol for 1MMTPA propylene world

scale plant

• Economics requires a Methanol price of less than $80/T with Ethylene price at $500/T and Propylene price at $400/T

4. MTO/DTO Technology – Why?

• Technology Developers • MTO

• UOP/Norsk Hydro

• ExxonMobil • MTP

• Lurgi

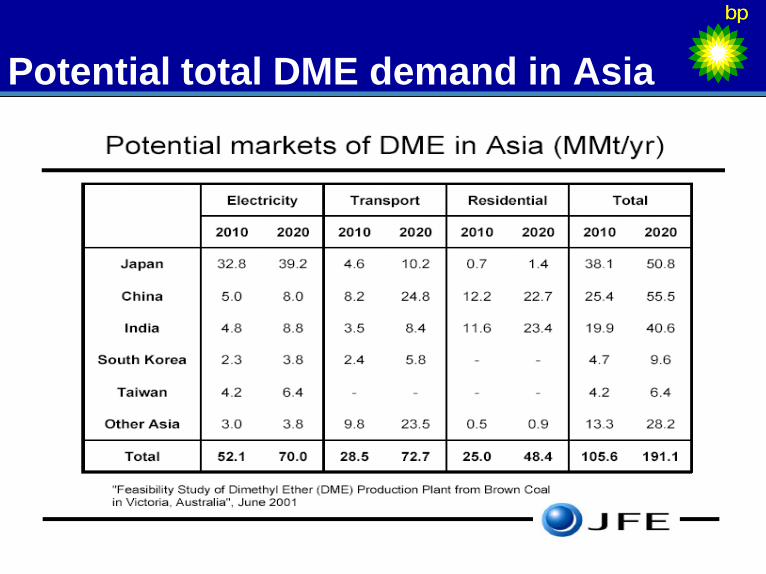

Potential total DME demand in Asia

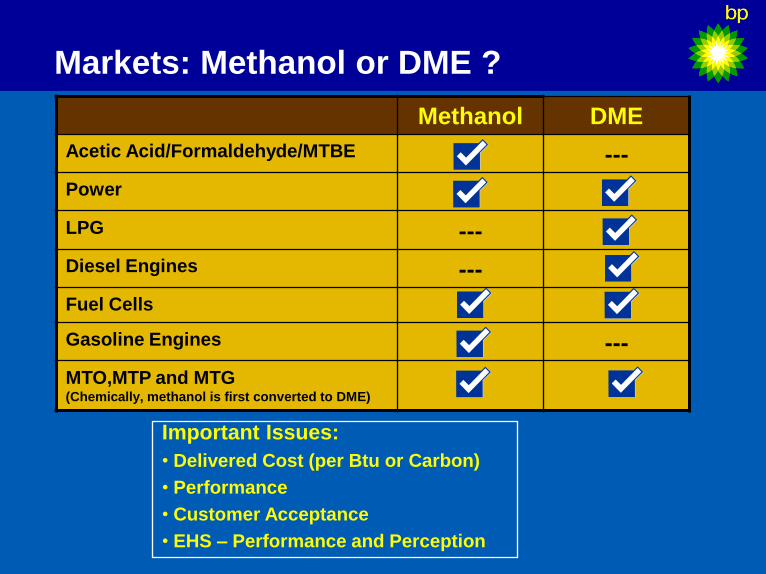

Markets: Methanol or DME ?

Methanol DME

Acetic Acid/Formaldehyde/MTBE ---

Power

LPG ---

Diesel Engines ---

Fuel Cells

Gasoline Engines ---

MTO,MTP and MTG (Chemically, methanol is first converted to DME)

Important Issues:

• Delivered Cost (per Btu or Carbon)

• Performance

• Customer Acceptance

• EHS – Performance and Perception

• Context: GTP -- Gas To Products

CTP – Coal To Products

• The Oxygenate Family

Methanol and DME

• Opportunities for LARGE Markets

• Challenges: Technologies and Economics

• IDA—The International DME Association

• Beyond MeOH/DME: DMM and DMC

• Vision: Gas-, Coal-, and Methanol Refinery

Outline

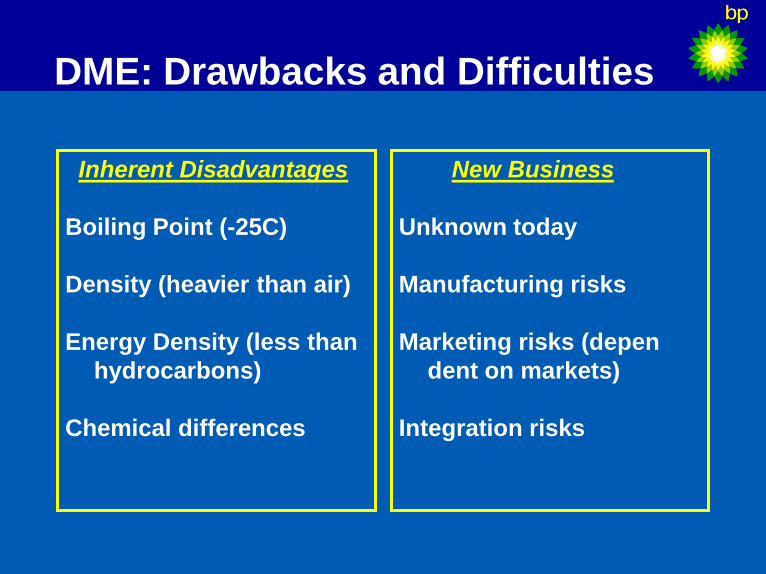

DME: Drawbacks and Difficulties

Inherent Disadvantages

Boiling Point (-25C)

Density (heavier than air)

Energy Density (less than

hydrocarbons)

Chemical differences

New Business

Unknown today

Manufacturing risks

Marketing risks (depen

dent on markets)

Integration risks

Challenges

1. Project Risk and Complexity(Size!)

2. Manufacturing Technologies

3. Integration: Resource to Market;

4. Partnering

5. Financing

6. DME Market Acceptance

7. Global Standards

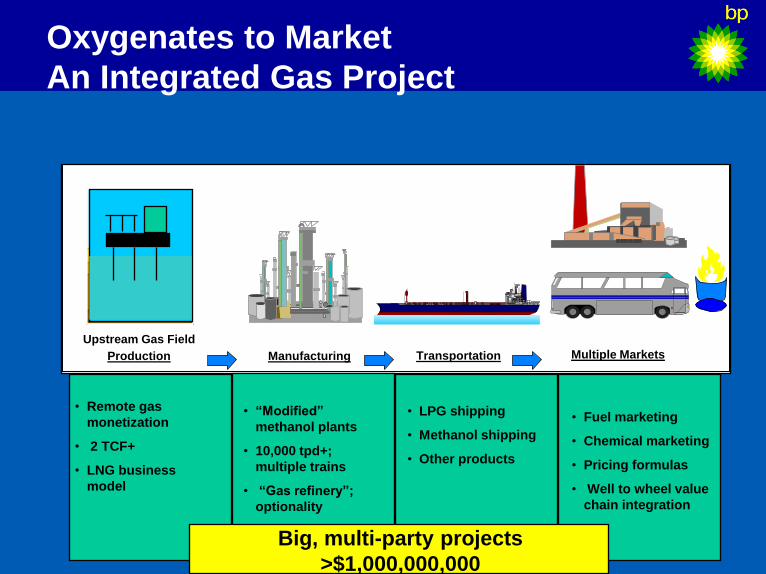

Oxygenates to Market

An Integrated Gas Project

Manufacturing Transportation Multiple Markets

Upstream Gas Field

Production

• Remote gas

monetization

• 2 TCF+

• LNG business

model

• “Modified”

methanol plants

• 10,000 tpd+;

multiple trains

• “Gas refinery”;

optionality

• LPG shipping

• Methanol shipping

• Other products

• Fuel marketing

• Chemical marketing

• Pricing formulas

• Well to wheel value

chain integration

Big, multi-party projects

>$1,000,000,000

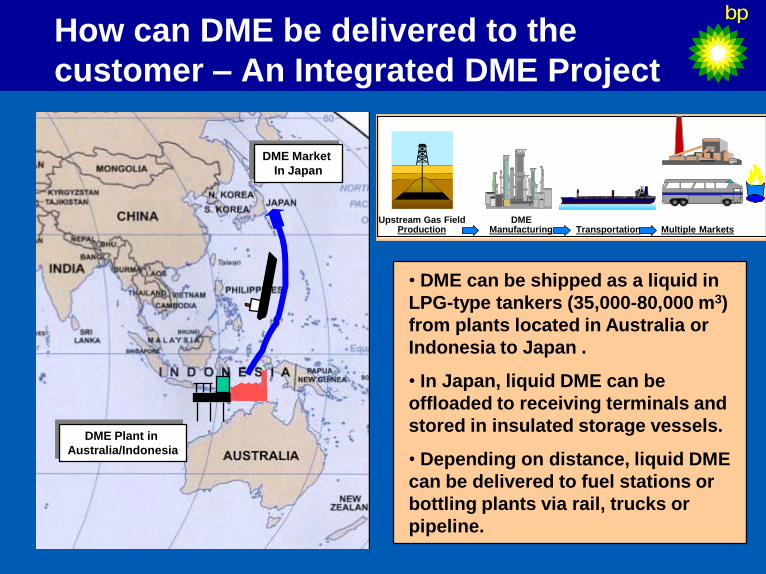

How can DME be delivered to the

customer – An Integrated DME Project

• DME can be shipped as a liquid in

LPG-type tankers (35,000-80,000 m3)

from plants located in Australia or

Indonesia to Japan .

• In Japan, liquid DME can be

offloaded to receiving terminals and

stored in insulated storage vessels.

• Depending on distance, liquid DME

can be delivered to fuel stations or

bottling plants via rail, trucks or

pipeline.

DME Plant in

Australia/Indonesia

DME Manufacturing Transportation Multiple Markets

Upstream Gas Field Production

DME Market

In Japan

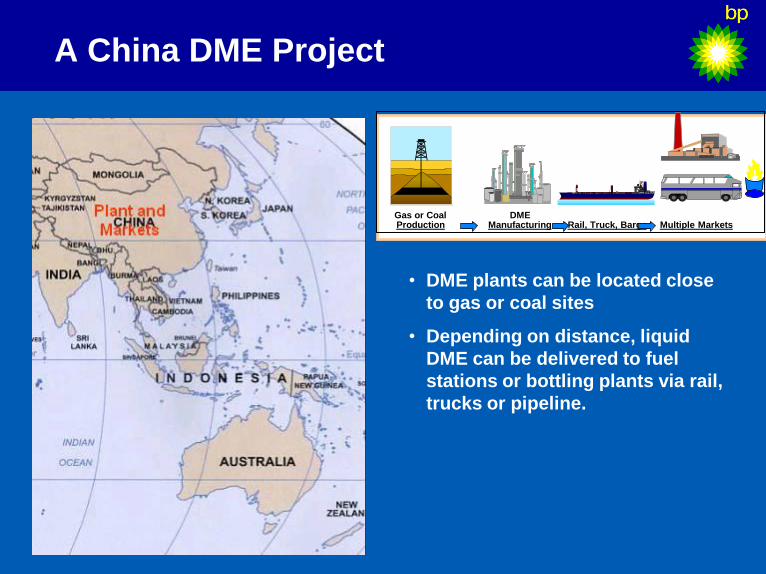

A China DME Project

• DME plants can be located close

to gas or coal sites

• Depending on distance, liquid

DME can be delivered to fuel

stations or bottling plants via rail,

trucks or pipeline.

DME Manufacturing Rail, Truck, Barge Multiple Markets

Gas or Coal Production

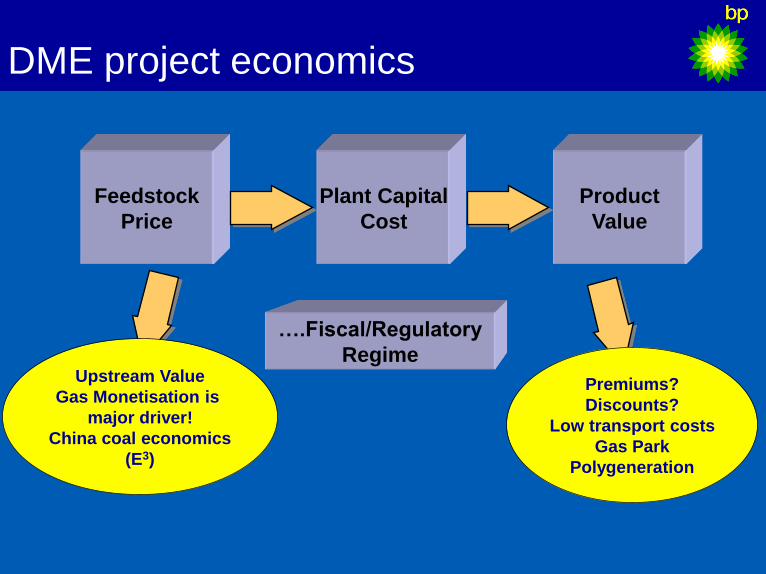

Feedstock

Price

Plant Capital

Cost

Product

Value

….Fiscal/Regulatory

Regime

DME project economics

Premiums?

Discounts?

Low transport costs

Gas Park

Polygeneration

Upstream Value

Gas Monetisation is

major driver!

China coal economics

(E3)

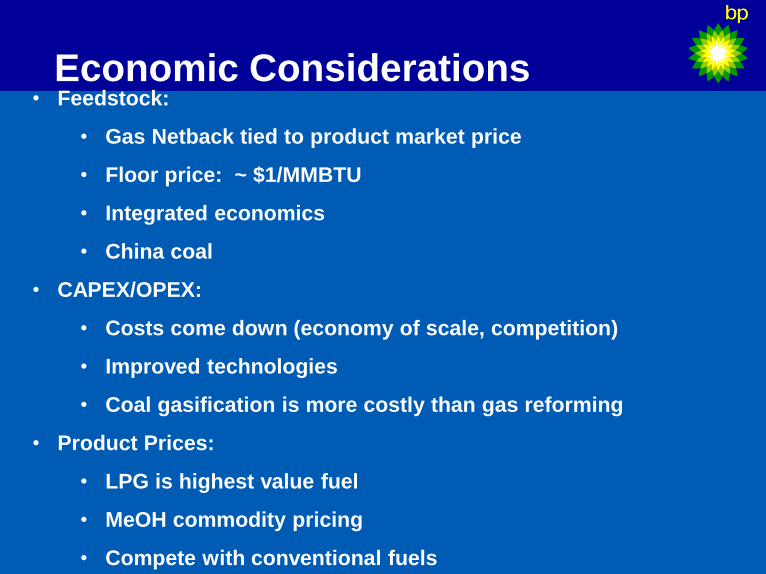

Economic Considerations

• Feedstock:

• Gas Netback tied to product market price

• Floor price: ~ $1/MMBTU

• Integrated economics

• China coal

• CAPEX/OPEX:

• Costs come down (economy of scale, competition)

• Improved technologies

• Coal gasification is more costly than gas reforming

• Product Prices:

• LPG is highest value fuel

• MeOH commodity pricing

• Compete with conventional fuels

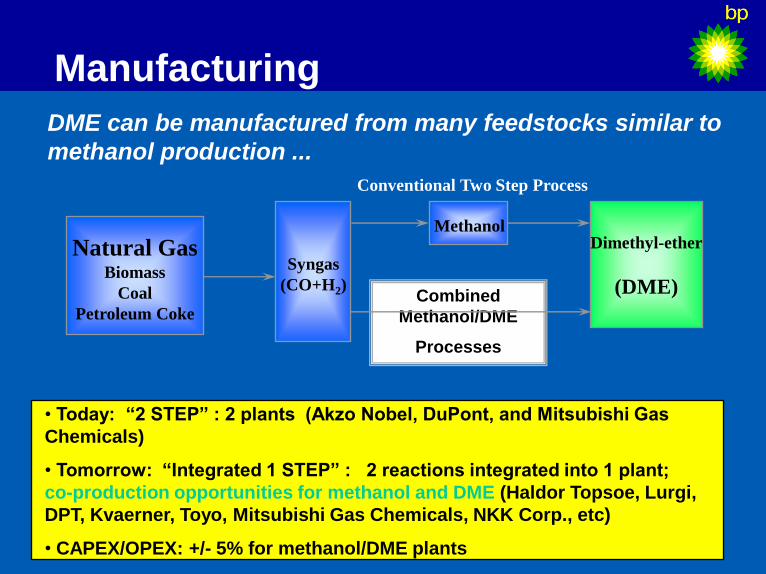

Manufacturing

Combined

Methanol/DME

Processes

Syngas

(CO+H2)

Dimethyl-ether

(DME)

Conventional Two Step Process

Natural Gas Biomass

Coal

Petroleum Coke

Methanol

DME can be manufactured from many feedstocks similar to

methanol production ...

• Today: “2 STEP” : 2 plants (Akzo Nobel, DuPont, and Mitsubishi Gas

Chemicals)

• Tomorrow: “Integrated 1 STEP” : 2 reactions integrated into 1 plant;

co-production opportunities for methanol and DME (Haldor Topsoe, Lurgi,

DPT, Kvaerner, Toyo, Mitsubishi Gas Chemicals, NKK Corp., etc)

• CAPEX/OPEX: +/- 5% for methanol/DME plants

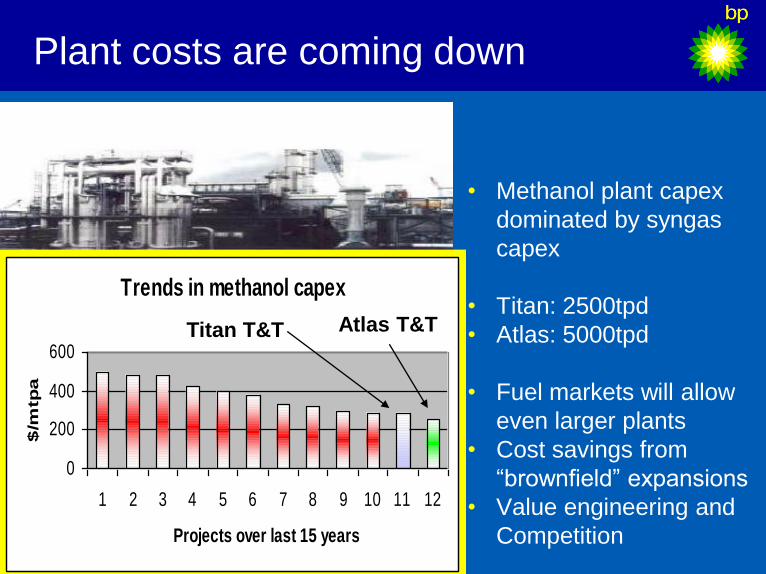

Plant costs are coming down

• Methanol plant capex

dominated by syngas

capex

• Titan: 2500tpd

• Atlas: 5000tpd

• Fuel markets will allow

even larger plants

• Cost savings from

“brownfield” expansions

• Value engineering and

Competition

Titan Trinidad Trends in methanol capex

0

200

400

600

1 2 3 4 5 6 7 8 9 10 11 12

Projects over last 15 years

$/m

tpa

Titan T&T Atlas T&T

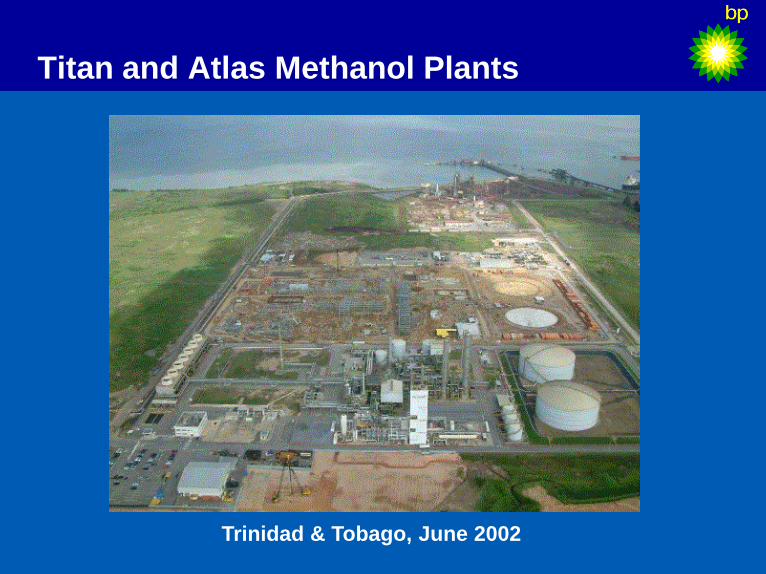

Titan and Atlas Methanol Plants

Trinidad & Tobago, June 2002

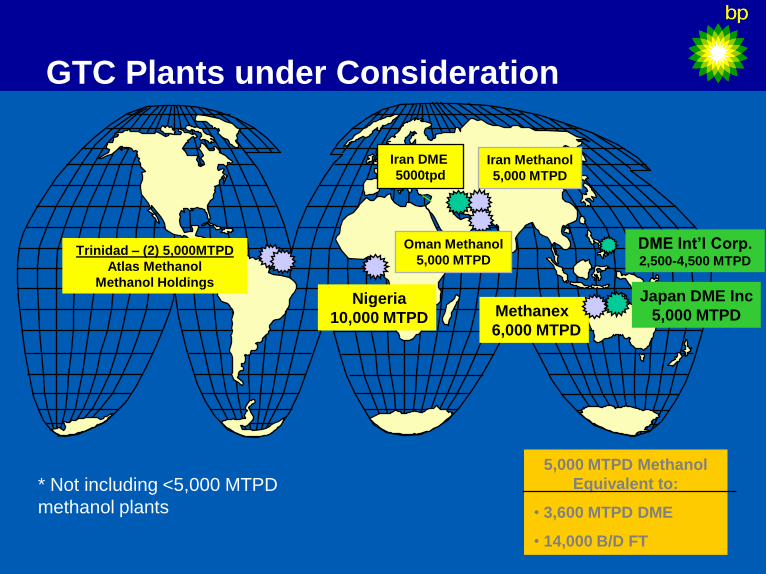

GTC Plants under Consideration

Japan DME Inc

5,000 MTPD Methanex

6,000 MTPD

Iran Methanol

5,000 MTPD

* Not including <5,000 MTPD

methanol plants

5,000 MTPD Methanol

Equivalent to:

• 3,600 MTPD DME

• 14,000 B/D FT

Trinidad – (2) 5,000MTPD

Atlas Methanol

Methanol Holdings

Oman Methanol

5,000 MTPD

DME Int’l Corp. 2,500-4,500 MTPD

Nigeria

10,000 MTPD

Iran DME

5000tpd

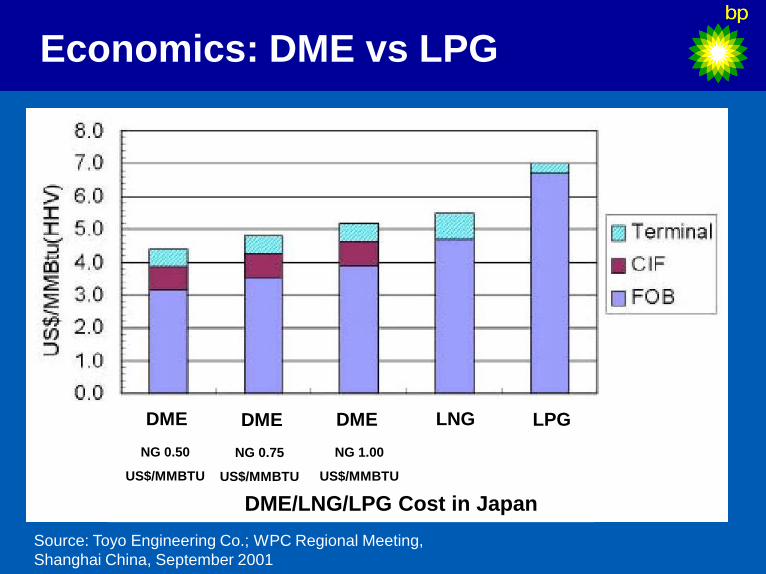

Economics: DME vs LPG

Source: Toyo Engineering Co.; WPC Regional Meeting,

Shanghai China, September 2001

DME/LNG/LPG Cost in Japan

NG 0.50

US$/MMBTU

NG 0.75

US$/MMBTU

NG 1.00

US$/MMBTU

DME DME DME LNG LPG

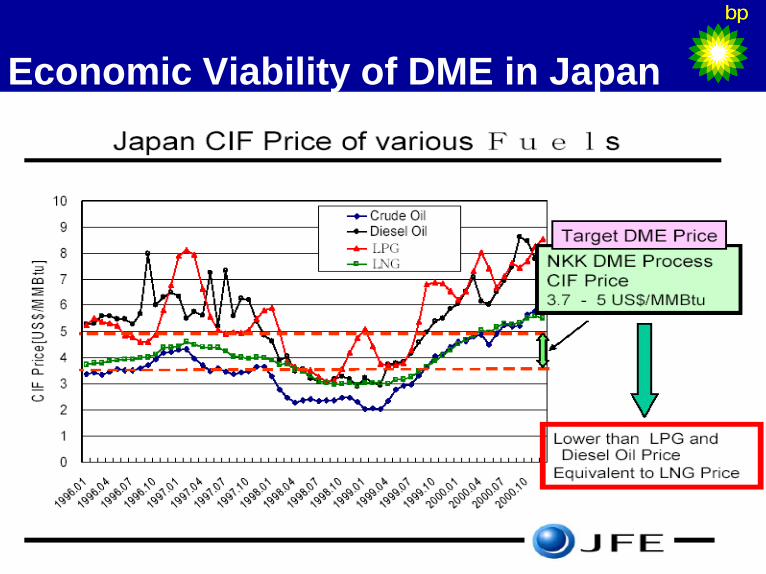

Economic Viability of DME in Japan

• Context: GTP – Gas Monetization

• The Oxygenate Family

• Methanol and DME

• Opportunities for LARGE Markets

• DME Value Chain: Gas to Markets

• Challenges: Technologies and Economics

• IDA—The International DME Association

• DMM and DMC

• Vision: Gas Refinery or Methanol Refinery

Outline

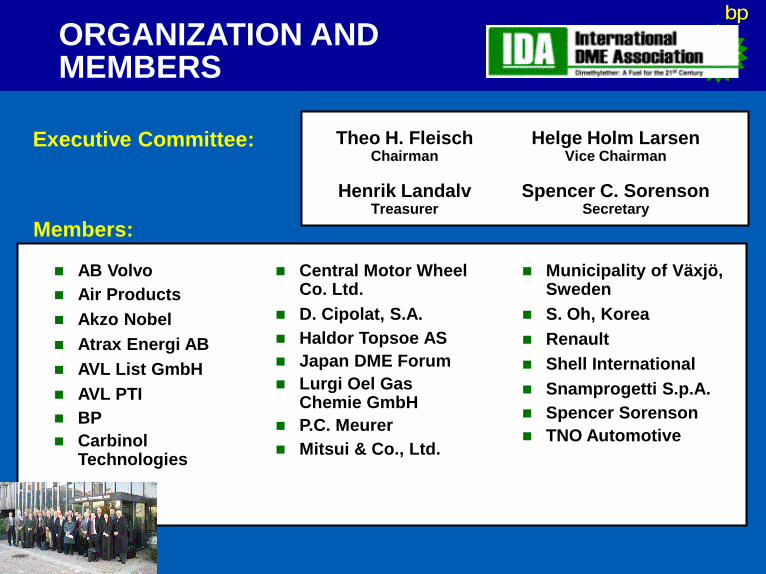

About the IDA

• Formed, in early 2001, as a non-profit organization to promote public awareness of DME and its uses.

• Currently membership includes about 30 companies/organizations/individuals from Europe, North America, Asia and Africa.

• Next Meeting: Phoenix, November 13-14, 2003

• Website for more information: (www.aboutdme.org)

Executive Committee:

Members:

Municipality of Växjö, Sweden

S. Oh, Korea

Renault

Shell International

Snamprogetti S.p.A.

Spencer Sorenson

TNO Automotive

AB Volvo

Air Products

Akzo Nobel

Atrax Energi AB

AVL List GmbH

AVL PTI

BP

Carbinol Technologies

Central Motor Wheel Co. Ltd.

D. Cipolat, S.A.

Haldor Topsoe AS

Japan DME Forum

Lurgi Oel Gas Chemie GmbH

P.C. Meurer

Mitsui & Co., Ltd.

Theo H. Fleisch Chairman

Helge Holm Larsen Vice Chairman

Spencer C. Sorenson Secretary

Henrik Landalv Treasurer

ORGANIZATION AND MEMBERS

• Promotion of Public Awareness of DME

• Source of Information about DME (Environmental, Health, Safety and Economical Aspects)

• Monitoring of DME Relevant Developments (Technical, Legislative, Business and Political Aspects)

• DME Related Literature, Presentations and Workshops

• Platform for International Contacts

• Creation of Business Opportunities

• Non-Profit Organization

OBJECTIVES

International DME Association

Why join IDA?

• Member only workshops (2 per year)

• Access to complete and latest information on DME through website

• Global networking opportunities (members from the whole value chain)

• Shaping future standards and regulations

• Being part in creating new and exciting markets for methanol

• “DME 1” will be hosted in Paris in October 2004 (reduced registration fee)

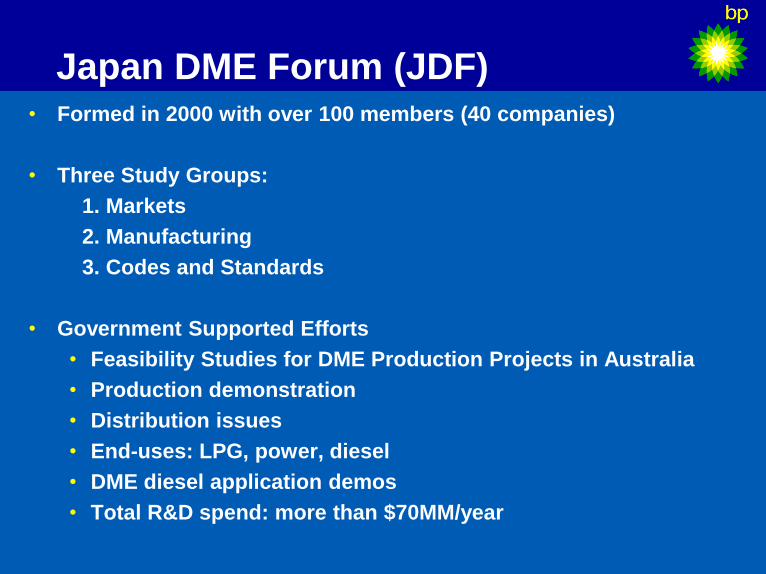

Japan DME Forum (JDF) • Formed in 2000 with over 100 members (40 companies)

• Three Study Groups:

1. Markets

2. Manufacturing

3. Codes and Standards

• Government Supported Efforts

• Feasibility Studies for DME Production Projects in Australia

• Production demonstration

• Distribution issues

• End-uses: LPG, power, diesel

• DME diesel application demos

• Total R&D spend: more than $70MM/year

• Context: GTP – Gas Monetization

• The Oxygenate Family

• Methanol and DME

• Opportunities for LARGE Markets

• DME Value Chain: Gas to Markets

• Challenges: Technologies and Economics

• IDA—The International DME Association

• DMM and DMC

• Vision: Gas Refinery or Methanol Refinery

Outline

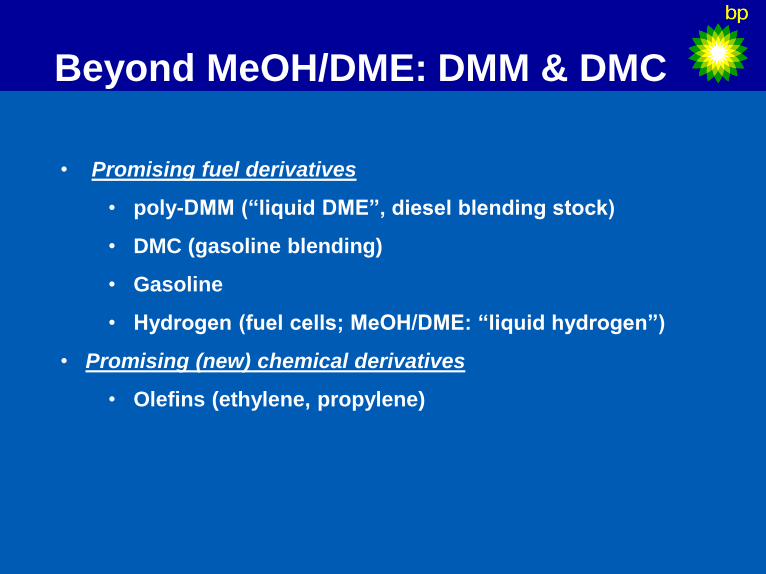

Beyond MeOH/DME: DMM & DMC

• Promising fuel derivatives

• poly-DMM (“liquid DME”, diesel blending stock)

• DMC (gasoline blending)

• Gasoline

• Hydrogen (fuel cells; MeOH/DME: “liquid hydrogen”)

• Promising (new) chemical derivatives

• Olefins (ethylene, propylene)

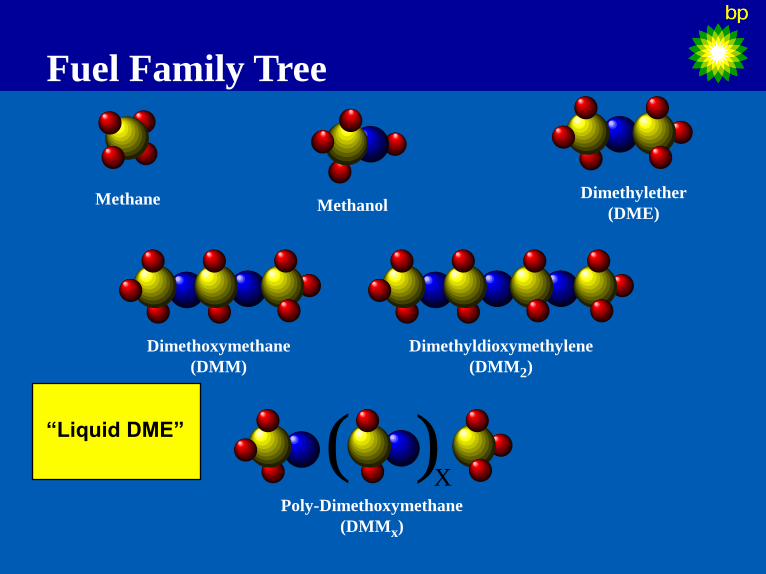

Methane Methanol Dimethylether

(DME)

Dimethoxymethane

(DMM)

Fuel Family Tree

Dimethyldioxymethylene

(DMM2)

Poly-Dimethoxymethane

(DMMx)

( ) X

“Liquid DME”

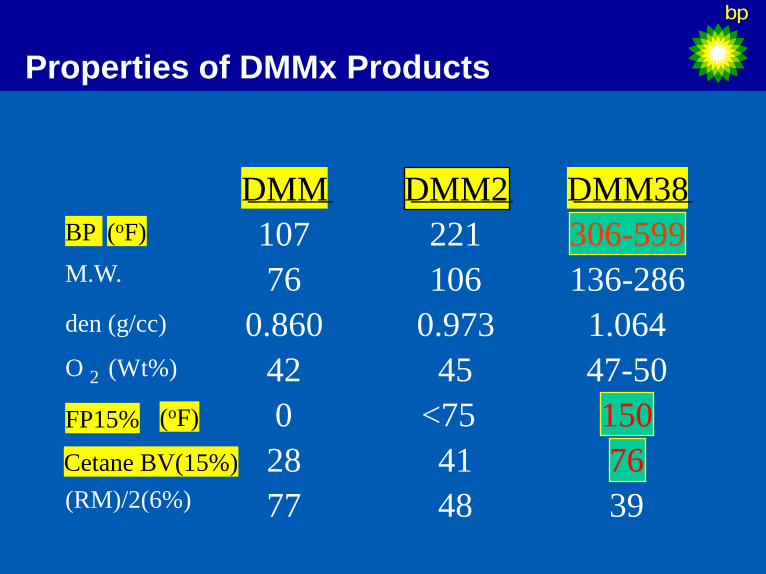

Properties of DMMx Products

DMM DMM2 DMM38

BP (oF) 107 221 306-599 M.W. 76 106 136-286

den (g/cc) 0.860 0.973 1.064

O 2 (Wt%) 42 45 47-50

FP15% (oF) 0 150

Cetane BV(15%) 28 41 76 (RM)/2(6%) 77 48 39

<75

0.4

0.5

0.6

0.7

0.8

0.9

1

0.9 0.92 0.94 0.96 0.98 1 1.02

Normalized NOx

Norm

ali

zed

PM

Carb = California Diesel

LS = Ultra low-sulphur diesel

FT20 = 20% FT diesel 80%

LS

FT100 = Neat FT diesel

B20 = 20% biodiesel in 80% LS

DMM15 = 15% DMM in 85% LS

PM vs Nox Emissions of 7 test fuels (DOE/SWRL)

DMM15

FT100

FT20

B20

LSD

CARB BASE

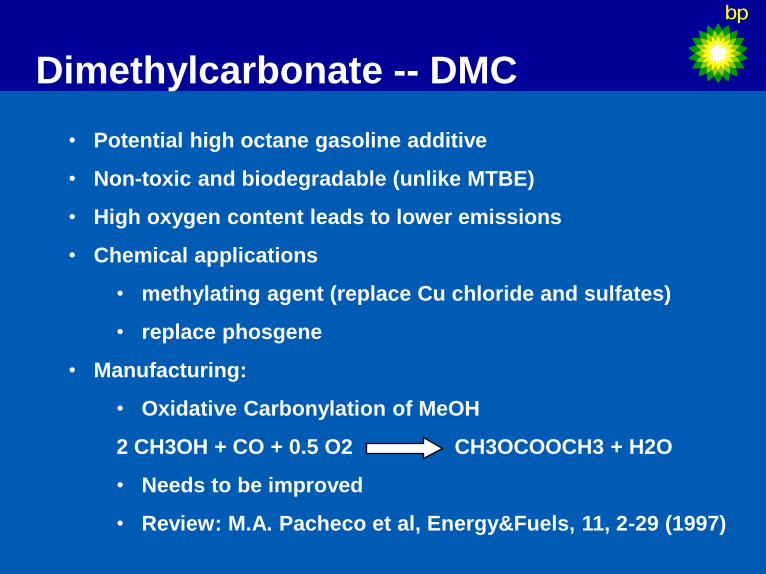

Dimethylcarbonate -- DMC

• Potential high octane gasoline additive

• Non-toxic and biodegradable (unlike MTBE)

• High oxygen content leads to lower emissions

• Chemical applications

• methylating agent (replace Cu chloride and sulfates)

• replace phosgene

• Manufacturing:

• Oxidative Carbonylation of MeOH

2 CH3OH + CO + 0.5 O2 CH3OCOOCH3 + H2O

• Needs to be improved

• Review: M.A. Pacheco et al, Energy&Fuels, 11, 2-29 (1997)

Methanol

DME

Fuel additives

Fuel cells

Chemicals

Olefins

Fuel for Power

LPG substitute

Fuel for Transport

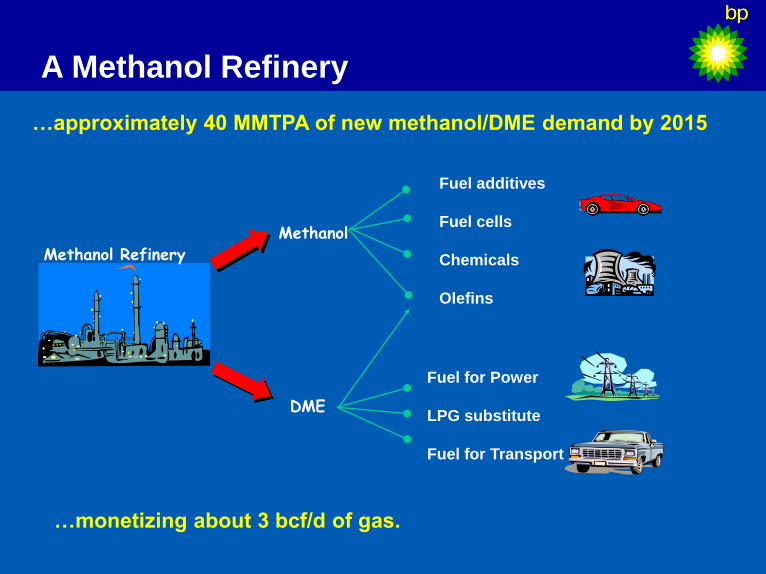

Methanol Refinery

…approximately 40 MMTPA of new methanol/DME demand by 2015

A Methanol Refinery

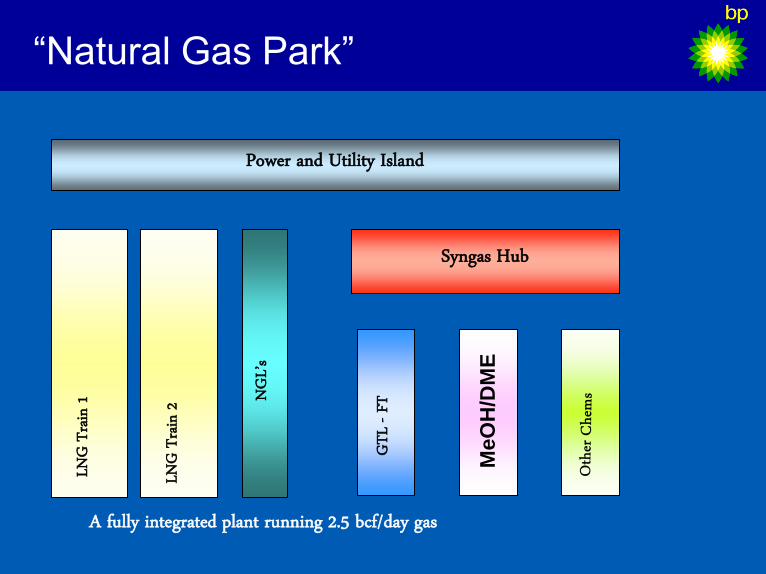

…monetizing about 3 bcf/d of gas.

“Natural Gas Park”

Power and Utility Island

Syngas Hub

LNG

Train

2

LNG

Train

1 NGL’s

GTL -

FT

A fully integrated plant running 2.5 bcf/day gas M

eO

H/D

ME

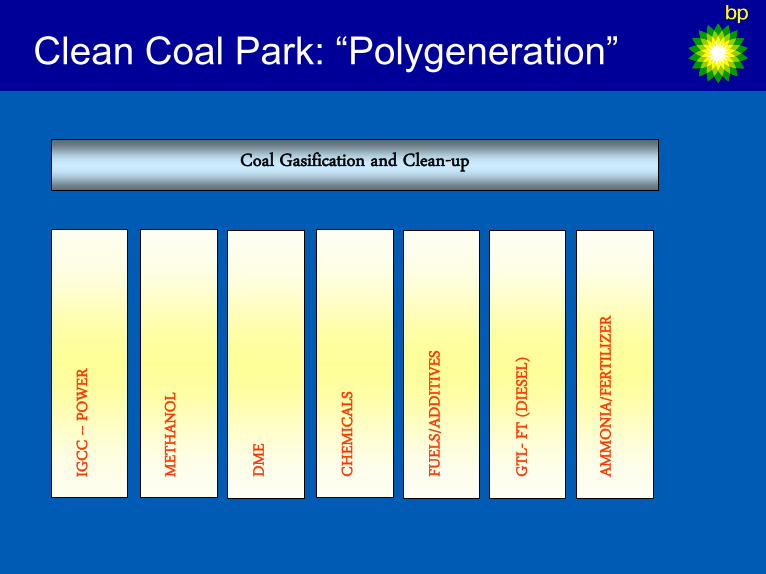

Clean Coal Park: “Polygeneration”

Coal Gasification and Clean-up

IGCC

-- PO

WER

METH

ANOL

DME

CHEM

ICAL

S

FUEL

S/ADD

ITIVE

S

GTL-

FT (D

IESEL

)

AMMO

NIA/

FERT

ILIZE

R

Key Messages -- 1

• Methanol is an important CHEMICAL business today

• The MeOH business is undergoing dramatic changes with

larger plants and low cost gas leading to lower cost MeOH

• Methanol will be the central point in a natural gas park both

as a potential large volume fuel and as feedstock for

numerous other fuels and chemicals

• Future projects are large and complex and require low cost

technologies and new partnerships

• DME is the most promising MeOH derivative

Key Messages -- 2

• DME is a clean, multi-purpose fuel and chemical feedstock

• Domestic Fuel: as synthetic LPG

• Power: as a gas turbine fuel

• Transport: diesel alternative and fuel cell fuel

• Chemicals

• DME can be made from many feedstocks, including biomass

and coal, using available technologies

• DME can be economic today but further cost reductions are

important (technologies, economy of scale)

• Market development is required

• A global DME effort has evolved led by Japan. IDA and JDF

have been formed.

Key Messages -- 3

• There are other interesting fuels in the methanol familiy such

as PDMM for diesel and DMC for gasoline engines

• The MeOH and DME business will be closely intertwined (co-

production of methanol and DME in large scale plants)

• A “Methanol Refinery” can deliver a variety of clean fuels,

chemical feedstocks and finished chemical products

• Methanol Refinery will be part of a “Natural Gas Park” or

“Clean Coal Park”

CREATION OF NEW GLOBAL BUSINESS IS DIFFICULT

GLOBAL COLLABORATION IS REQUIRED